Embed Size (px)

Citation preview

May 2019

Indian DairyTrends and Dynamics

BOB Capital Markets is a wholly owned subsidiary of Bank of Baroda

Key Players 2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

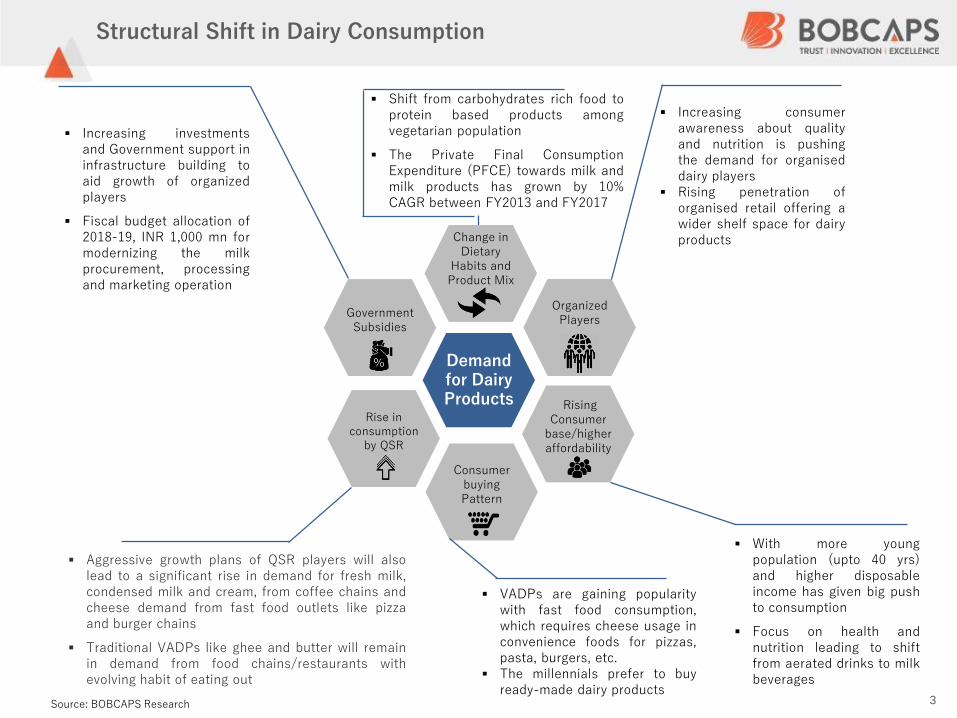

Demand for Dairy Products

Government Subsidies

Rise in consumption

by QSR

Consumer buying Pattern

Rising Consumer

base/higher affordability

Organized Players

Change in Dietary

Habits and Product Mix

▪ Increasing consumerawareness about qualityand nutrition is pushingthe demand for organiseddairy players

▪ Rising penetration oforganised retail offering awider shelf space for dairyproducts

▪ Shift from carbohydrates rich food toprotein based products amongvegetarian population

▪ The Private Final ConsumptionExpenditure (PFCE) towards milk andmilk products has grown by 10%CAGR between FY2013 and FY2017

▪ Increasing investmentsand Government support ininfrastructure building toaid growth of organizedplayers

▪ Fiscal budget allocation of2018-19, INR 1,000 mn formodernizing the milkprocurement, processingand marketing operation

▪ VADPs are gaining popularitywith fast food consumption,which requires cheese usage inconvenience foods for pizzas,pasta, burgers, etc.

▪ The millennials prefer to buyready-made dairy products

▪ With more youngpopulation (upto 40 yrs)and higher disposableincome has given big pushto consumption

▪ Focus on health andnutrition leading to shiftfrom aerated drinks to milkbeverages

▪ Aggressive growth plans of QSR players will alsolead to a significant rise in demand for fresh milk,condensed milk and cream, from coffee chains andcheese demand from fast food outlets like pizzaand burger chains

▪ Traditional VADPs like ghee and butter will remainin demand from food chains/restaurants withevolving habit of eating out

Structural Shift in Dairy Consumption

3Source: BOBCAPS Research

Key Players2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

5

Shift towards VADPs - New Milk Revolution

Raw Milk

Skimmed Milk

Powder

ButtermilkProcessed milk

Khoa

Butter,

Curd

Paneer

Ghee

Yogurt &

Shirkhand

Ice-cream

Cheese

0%

5%

10%

15%

20%

25%

0% 5% 10% 15% 20% 25% 30% 35%

Gro

wth

Ou

tlook

Operating Margin

Operating Margin and Growth Outlook

▪ Milk and traditional value added productshave high penetration both in rural andurban markets but are highly unorganized

▪ Hence growth in these segments will bedriven by the organized players increasingtheir presence

▪ The shift towards VADPs will be thegreatest lever for growth of conventionaldairy players as VADPs have

▪ Huge premium

▪ Longer shelf life

▪ Gross / Operating Margin 2x greaterthan milk

▪ Dairy and milk industry is estimated to growat 12-13% CAGR until 2020-21, driven byrising milk prices, change in product mix,rising share of branded products andincreasing consumption of VADPs

▪ Favorable demographics, high disposableincome, growing urbanization has given abig push to VADPs growth

CommodityProducts

Traditional VADP

Emerging VADP

Products ▪Liquid milk▪Milk Powder

▪Curd & Lassi▪Butter▪Ghee▪Paneer

▪Cheese▪Yogurt▪Flavoured milk▪ Ice-cream

Growth (%) 10-11 12-13 15-20

Penetration

High Med Low

Commodity

Products, 67

Traditional

VADP, 28

Emerging

VADP, 4

Market Share

Category-wise (%)

6

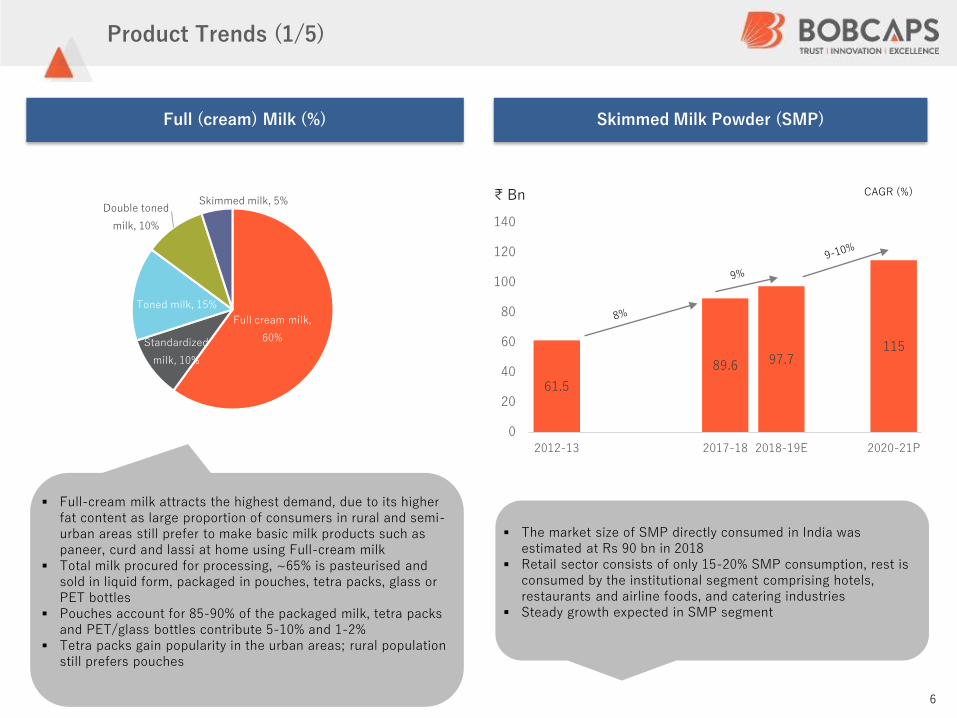

Full (cream) Milk (%)

Product Trends (1/5)

Full cream milk,

60%Standardized

milk, 10%

Toned milk, 15%

Double toned

milk, 10%

Skimmed milk, 5%

Skimmed Milk Powder (SMP)

▪ Full-cream milk attracts the highest demand, due to its higher fat content as large proportion of consumers in rural and semi-urban areas still prefer to make basic milk products such as paneer, curd and lassi at home using Full-cream milk

▪ Total milk procured for processing, ~65% is pasteurised and sold in liquid form, packaged in pouches, tetra packs, glass or PET bottles

▪ Pouches account for 85-90% of the packaged milk, tetra packs and PET/glass bottles contribute 5-10% and 1-2%

▪ Tetra packs gain popularity in the urban areas; rural population still prefers pouches

▪ The market size of SMP directly consumed in India was estimated at Rs 90 bn in 2018

▪ Retail sector consists of only 15-20% SMP consumption, rest is consumed by the institutional segment comprising hotels, restaurants and airline foods, and catering industries

▪ Steady growth expected in SMP segment

61.5

89.6 97.7115

0

20

40

60

80

100

120

140

2012-13 2017-18 2018-19E 2020-21P

₹ Bn CAGR (%)

7

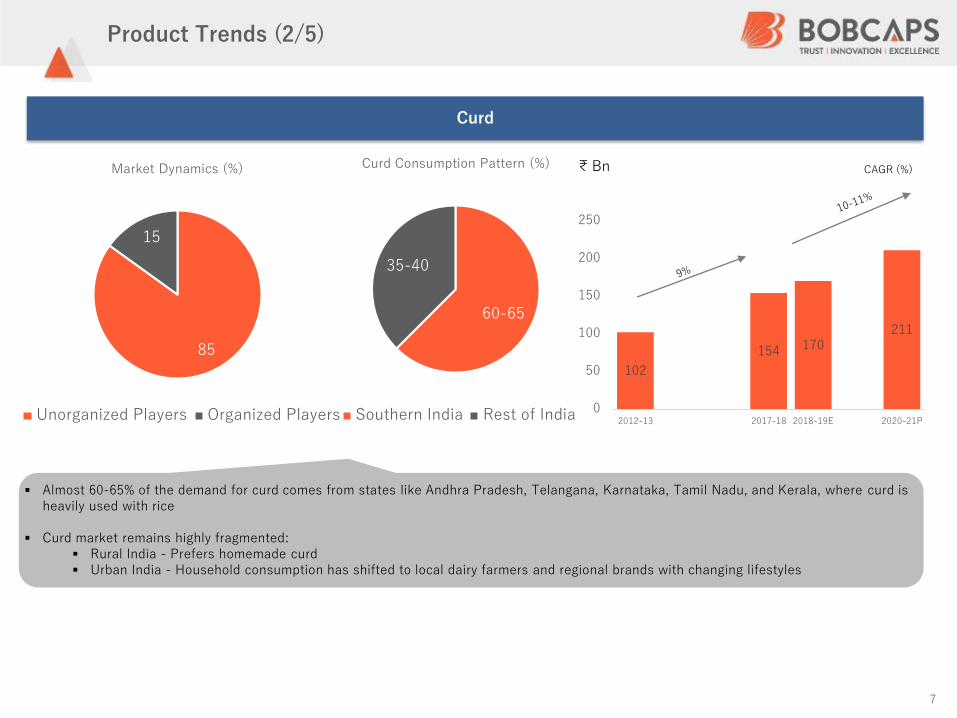

Product Trends (2/5)

Curd

102

154 170211

0

50

100

150

200

250

2012-13 2017-18 2018-19E 2020-21P

₹ Bn

60-65

35-40

Curd Consumption Pattern (%)

Southern India Rest of India

▪ Almost 60-65% of the demand for curd comes from states like Andhra Pradesh, Telangana, Karnataka, Tamil Nadu, and Kerala, where curd is heavily used with rice

▪ Curd market remains highly fragmented: ▪ Rural India - Prefers homemade curd ▪ Urban India - Household consumption has shifted to local dairy farmers and regional brands with changing lifestyles

85

15

Market Dynamics (%)

Unorganized Players Organized Players

CAGR (%)

8

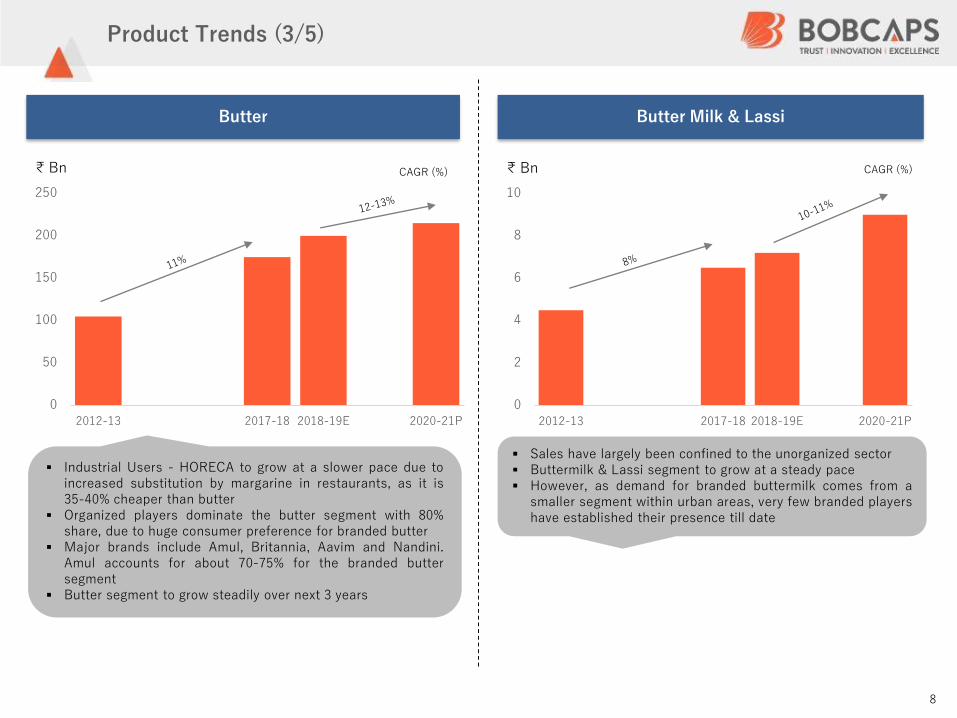

Butter Butter Milk & Lassi

0

50

100

150

200

250

2012-13 2017-18 2018-19E 2020-21P

₹ Bn

0

2

4

6

8

10

2012-13 2017-18 2018-19E 2020-21P

₹ Bn

▪ Industrial Users - HORECA to grow at a slower pace due toincreased substitution by margarine in restaurants, as it is35-40% cheaper than butter

▪ Organized players dominate the butter segment with 80%share, due to huge consumer preference for branded butter

▪ Major brands include Amul, Britannia, Aavim and Nandini.Amul accounts for about 70-75% for the branded buttersegment

▪ Butter segment to grow steadily over next 3 years

▪ Sales have largely been confined to the unorganized sector▪ Buttermilk & Lassi segment to grow at a steady pace▪ However, as demand for branded buttermilk comes from a

smaller segment within urban areas, very few branded playershave established their presence till date

Product Trends (3/5)

CAGR (%)CAGR (%)

9

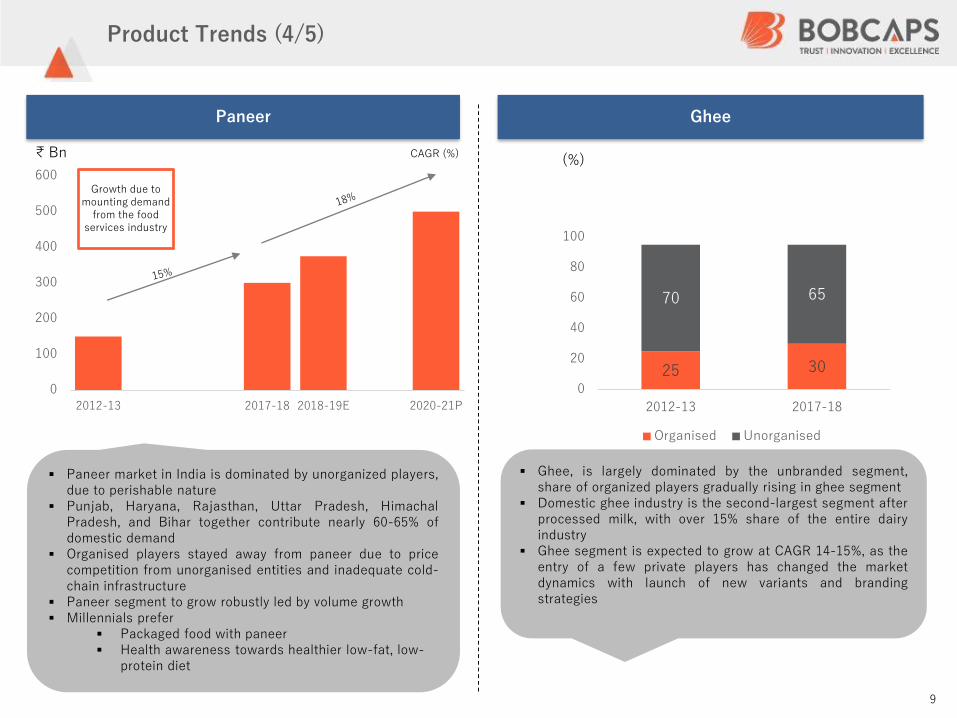

Paneer Ghee

▪ Paneer market in India is dominated by unorganized players,due to perishable nature

▪ Punjab, Haryana, Rajasthan, Uttar Pradesh, HimachalPradesh, and Bihar together contribute nearly 60-65% ofdomestic demand

▪ Organised players stayed away from paneer due to pricecompetition from unorganised entities and inadequate cold-chain infrastructure

▪ Paneer segment to grow robustly led by volume growth▪ Millennials prefer

▪ Packaged food with paneer ▪ Health awareness towards healthier low-fat, low-

protein diet

▪ Ghee, is largely dominated by the unbranded segment,share of organized players gradually rising in ghee segment

▪ Domestic ghee industry is the second-largest segment afterprocessed milk, with over 15% share of the entire dairyindustry

▪ Ghee segment is expected to grow at CAGR 14-15%, as theentry of a few private players has changed the marketdynamics with launch of new variants and brandingstrategies

Growth due to mounting demand

from the food services industry

Product Trends (4/5)

0

100

200

300

400

500

600

2012-13 2017-18 2018-19E 2020-21P

₹ Bn

25 30

70 65

0

20

40

60

80

100

2012-13 2017-18

Organised Unorganised

CAGR (%)(%)

0

10

20

30

40

50

60

70

2012-13 2017-18 2018-19E 2020-21P

₹ Bn

10

Cheese Ice-Cream

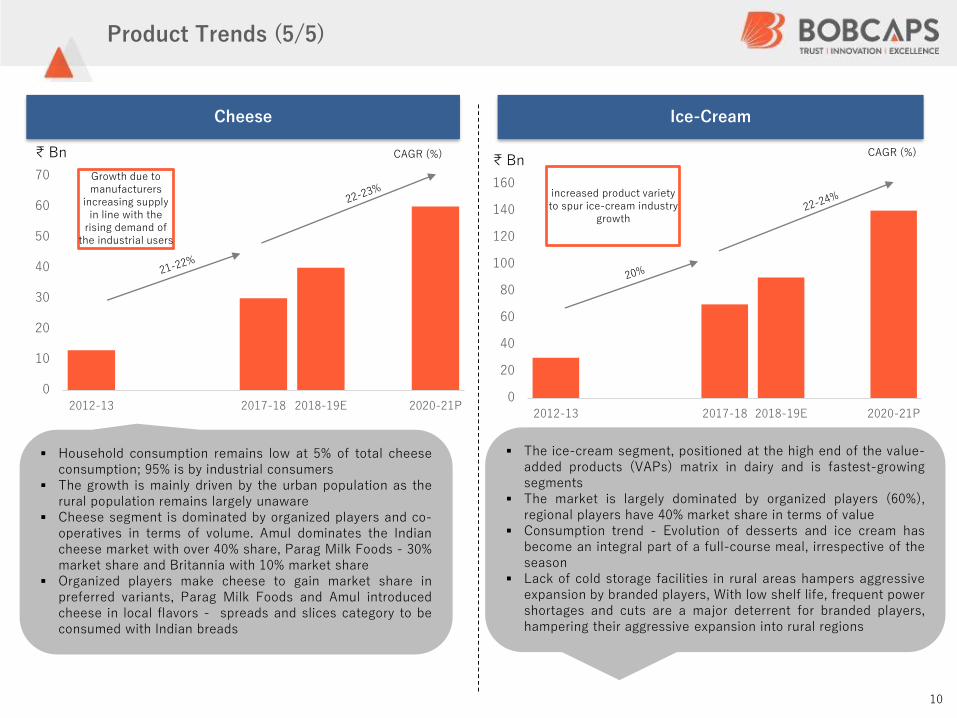

▪ Household consumption remains low at 5% of total cheeseconsumption; 95% is by industrial consumers

▪ The growth is mainly driven by the urban population as therural population remains largely unaware

▪ Cheese segment is dominated by organized players and co-operatives in terms of volume. Amul dominates the Indiancheese market with over 40% share, Parag Milk Foods - 30%market share and Britannia with 10% market share

▪ Organized players make cheese to gain market share inpreferred variants, Parag Milk Foods and Amul introducedcheese in local flavors - spreads and slices category to beconsumed with Indian breads

▪ The ice-cream segment, positioned at the high end of the value-added products (VAPs) matrix in dairy and is fastest-growingsegments

▪ The market is largely dominated by organized players (60%),regional players have 40% market share in terms of value

▪ Consumption trend - Evolution of desserts and ice cream hasbecome an integral part of a full-course meal, irrespective of theseason

▪ Lack of cold storage facilities in rural areas hampers aggressiveexpansion by branded players, With low shelf life, frequent powershortages and cuts are a major deterrent for branded players,hampering their aggressive expansion into rural regions

Growth due to manufacturers

increasing supply in line with the

rising demand of the industrial users

Product Trends (5/5)

0

20

40

60

80

100

120

140

160

2012-13 2017-18 2018-19E 2020-21P

₹ Bn

increased product variety to spur ice-cream industry

growth

CAGR (%)CAGR (%)

Key Players 2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India 3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

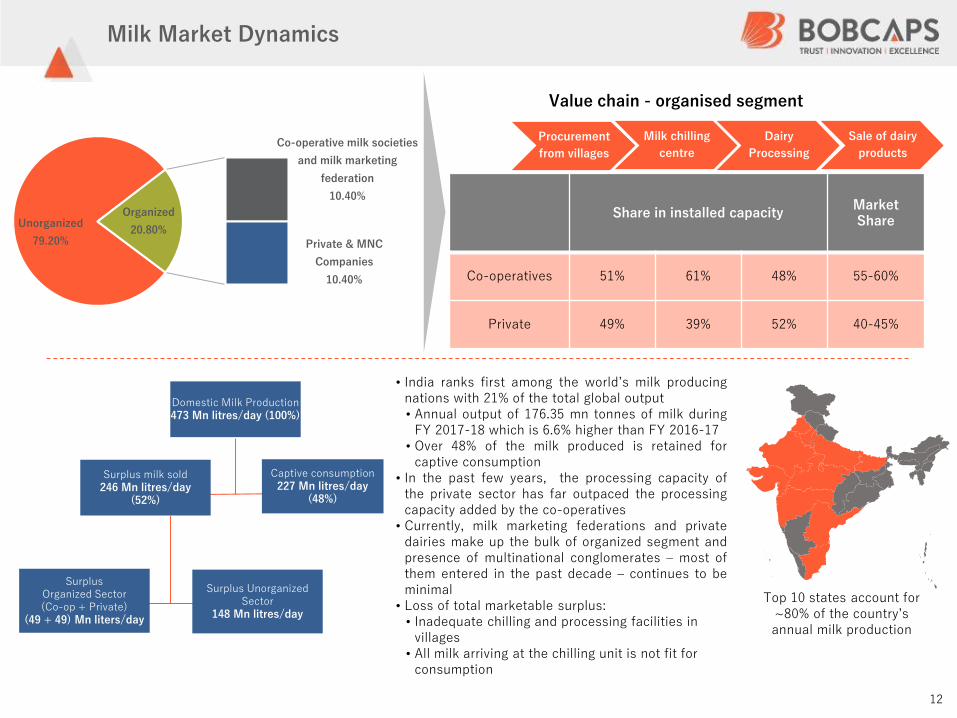

Domestic Milk Production 473 Mn litres/day (100%)

Milk Market Dynamics

• India ranks first among the world’s milk producingnations with 21% of the total global output• Annual output of 176.35 mn tonnes of milk during

FY 2017-18 which is 6.6% higher than FY 2016-17• Over 48% of the milk produced is retained for

captive consumption• In the past few years, the processing capacity of

the private sector has far outpaced the processingcapacity added by the co-operatives

• Currently, milk marketing federations and privatedairies make up the bulk of organized segment andpresence of multinational conglomerates – most ofthem entered in the past decade – continues to beminimal

• Loss of total marketable surplus:• Inadequate chilling and processing facilities in

villages• All milk arriving at the chilling unit is not fit for

consumption

Surplus milk sold 246 Mn litres/day

(52%)

Captive consumption 227 Mn litres/day

(48%)

Surplus Organized Sector (Co-op + Private)

(49 + 49) Mn liters/day

Procurement

from villages

Milk chilling

centre

Dairy

Processing

Sale of dairy

products

Surplus Unorganized Sector

148 Mn litres/day

Share in installed capacity Market Share

Co-operatives 51% 61% 48% 55-60%

Private 49% 39% 52% 40-45%

Value chain - organised segment

Unorganized

79.20%

Co-operative milk societies

and milk marketing

federation

10.40%

Private & MNC

Companies

10.40%

Organized

20.80%

Top 10 states account for ~80% of the country’s annual milk production

12

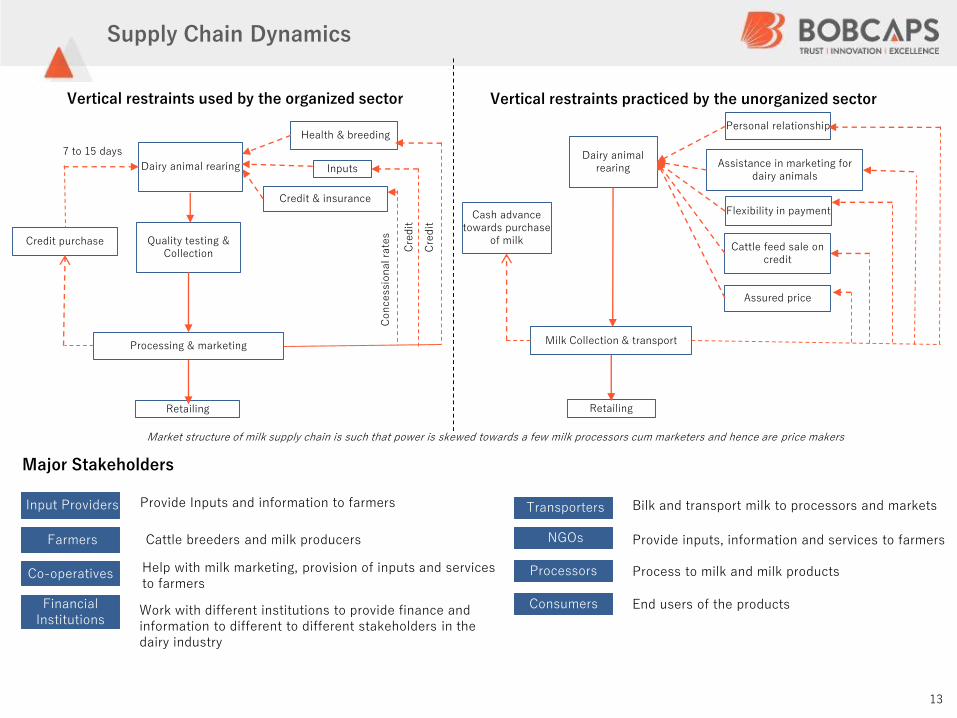

Supply Chain Dynamics

Vertical restraints used by the organized sector

Dairy animal rearing

Milk Collection & transport

Retailing

Personal relationship

Assistance in marketing for dairy animals

Flexibility in payment Cash advance towards purchase

of milk Cattle feed sale on

credit

Assured price

Vertical restraints practiced by the unorganized sector

Market structure of milk supply chain is such that power is skewed towards a few milk processors cum marketers and hence are price makers

Dairy animal rearing

Quality testing & Collection

Processing & marketing

Retailing

Health & breeding

Inputs

Credit & insurance

Credit purchase

7 to 15 days

Con

cessio

nal ra

tes

Cre

dit

Cre

dit

Co-operatives

Financial Institutions

Major Stakeholders

Help with milk marketing, provision of inputs and services to farmers

Work with different institutions to provide finance and information to different to different stakeholders in the dairy industry

Transporters

NGOs Farmers Cattle breeders and milk producers

Input Providers Provide Inputs and information to farmers Bilk and transport milk to processors and markets

Provide inputs, information and services to farmers

Process to milk and milk products Processors

Consumers End users of the products

13

14

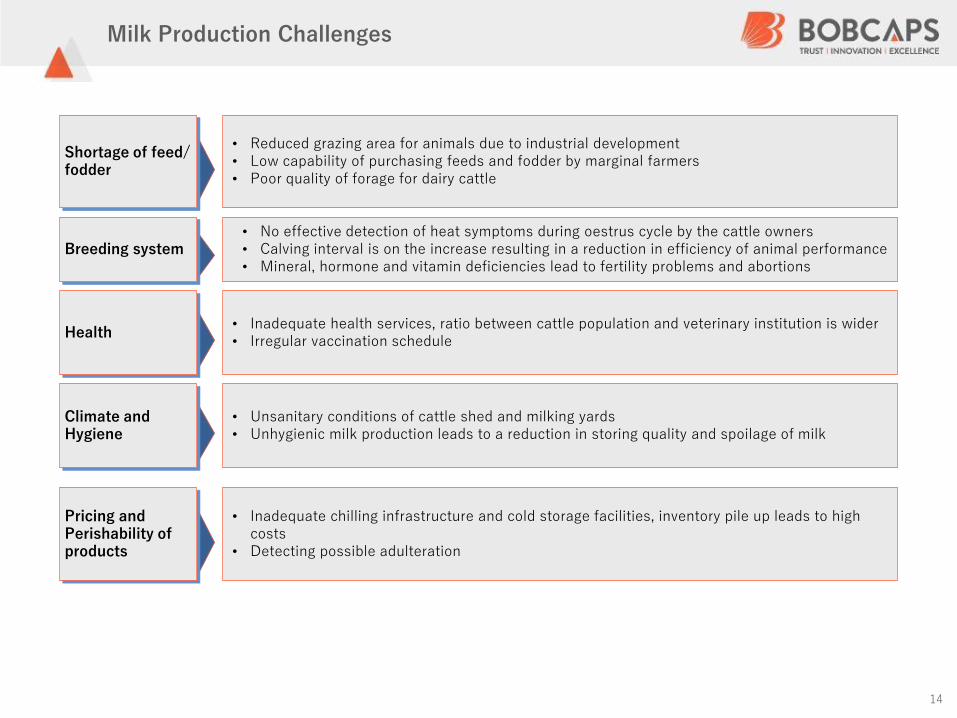

Milk Production Challenges

• Inadequate health services, ratio between cattle population and veterinary institution is wider• Irregular vaccination schedule

Health

• Inadequate chilling infrastructure and cold storage facilities, inventory pile up leads to high costs

• Detecting possible adulteration

Pricing and Perishability of products

• Reduced grazing area for animals due to industrial development • Low capability of purchasing feeds and fodder by marginal farmers• Poor quality of forage for dairy cattle

Shortage of feed/fodder

• No effective detection of heat symptoms during oestrus cycle by the cattle owners • Calving interval is on the increase resulting in a reduction in efficiency of animal performance• Mineral, hormone and vitamin deficiencies lead to fertility problems and abortions

Breeding system

• Unsanitary conditions of cattle shed and milking yards • Unhygienic milk production leads to a reduction in storing quality and spoilage of milk

Climate and Hygiene

15

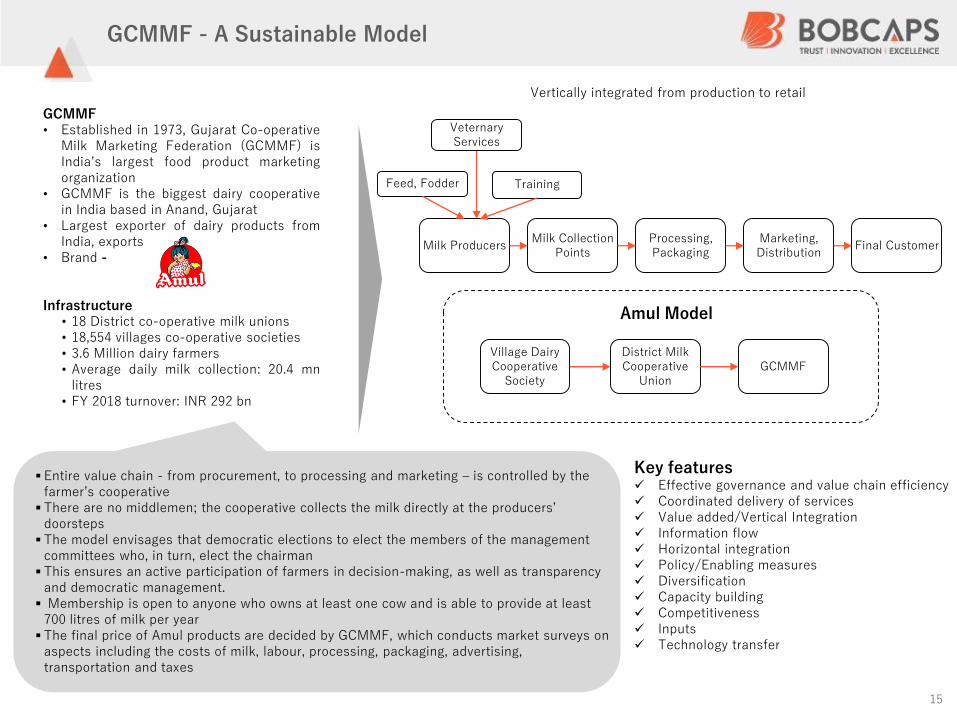

GCMMF• Established in 1973, Gujarat Co-operative

Milk Marketing Federation (GCMMF) isIndia’s largest food product marketingorganization

• GCMMF is the biggest dairy cooperativein India based in Anand, Gujarat

• Largest exporter of dairy products fromIndia, exports

• Brand -

Infrastructure• 18 District co-operative milk unions• 18,554 villages co-operative societies• 3.6 Million dairy farmers• Average daily milk collection: 20.4 mn

litres• FY 2018 turnover: INR 292 bn

Milk Producers Milk Collection

PointsProcessing, Packaging

Marketing, Distribution

Final Customer

Feed, Fodder

VeternaryServices

Training

Village Dairy Cooperative

Society

District Milk Cooperative

UnionGCMMF

Amul Model

▪ Entire value chain - from procurement, to processing and marketing – is controlled by the farmer’s cooperative

▪ There are no middlemen; the cooperative collects the milk directly at the producers’ doorsteps

▪ The model envisages that democratic elections to elect the members of the management committees who, in turn, elect the chairman

▪ This ensures an active participation of farmers in decision-making, as well as transparency and democratic management.

▪ Membership is open to anyone who owns at least one cow and is able to provide at least 700 litres of milk per year

▪ The final price of Amul products are decided by GCMMF, which conducts market surveys on aspects including the costs of milk, labour, processing, packaging, advertising, transportation and taxes

Key features ✓ Effective governance and value chain efficiency ✓ Coordinated delivery of services✓ Value added/Vertical Integration✓ Information flow✓ Horizontal integration✓ Policy/Enabling measures✓ Diversification✓ Capacity building✓ Competitiveness✓ Inputs ✓ Technology transfer

Vertically integrated from production to retail

GCMMF - A Sustainable Model

16

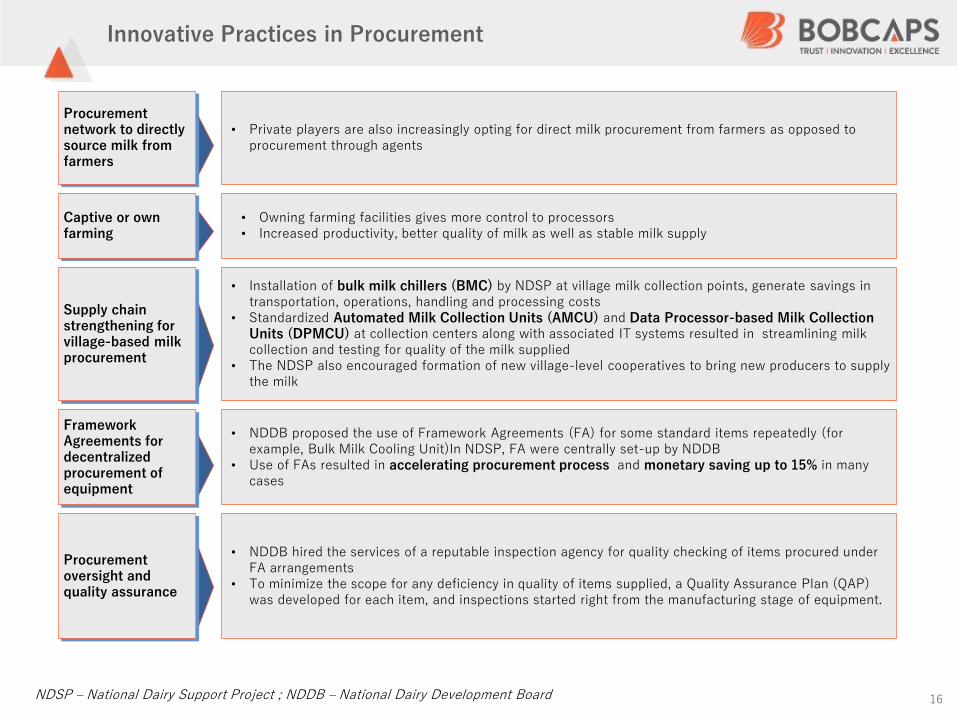

• Installation of bulk milk chillers (BMC) by NDSP at village milk collection points, generate savings in transportation, operations, handling and processing costs

• Standardized Automated Milk Collection Units (AMCU) and Data Processor-based Milk Collection Units (DPMCU) at collection centers along with associated IT systems resulted in streamlining milk collection and testing for quality of the milk supplied

• The NDSP also encouraged formation of new village-level cooperatives to bring new producers to supply the milk

Supply chain strengthening for village-based milk procurement

• NDDB hired the services of a reputable inspection agency for quality checking of items procured under FA arrangements

• To minimize the scope for any deficiency in quality of items supplied, a Quality Assurance Plan (QAP) was developed for each item, and inspections started right from the manufacturing stage of equipment.

Procurement oversight and quality assurance

• Private players are also increasingly opting for direct milk procurement from farmers as opposed to procurement through agents

Procurement network to directly source milk from farmers

• Owning farming facilities gives more control to processors• Increased productivity, better quality of milk as well as stable milk supply

Captive or own farming

Innovative Practices in Procurement

• NDDB proposed the use of Framework Agreements (FA) for some standard items repeatedly (for example, Bulk Milk Cooling Unit)In NDSP, FA were centrally set-up by NDDB

• Use of FAs resulted in accelerating procurement process and monetary saving up to 15% in many cases

Framework Agreements for decentralized procurement of equipment

NDSP – National Dairy Support Project ; NDDB – National Dairy Development Board

Key Players 2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India 3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

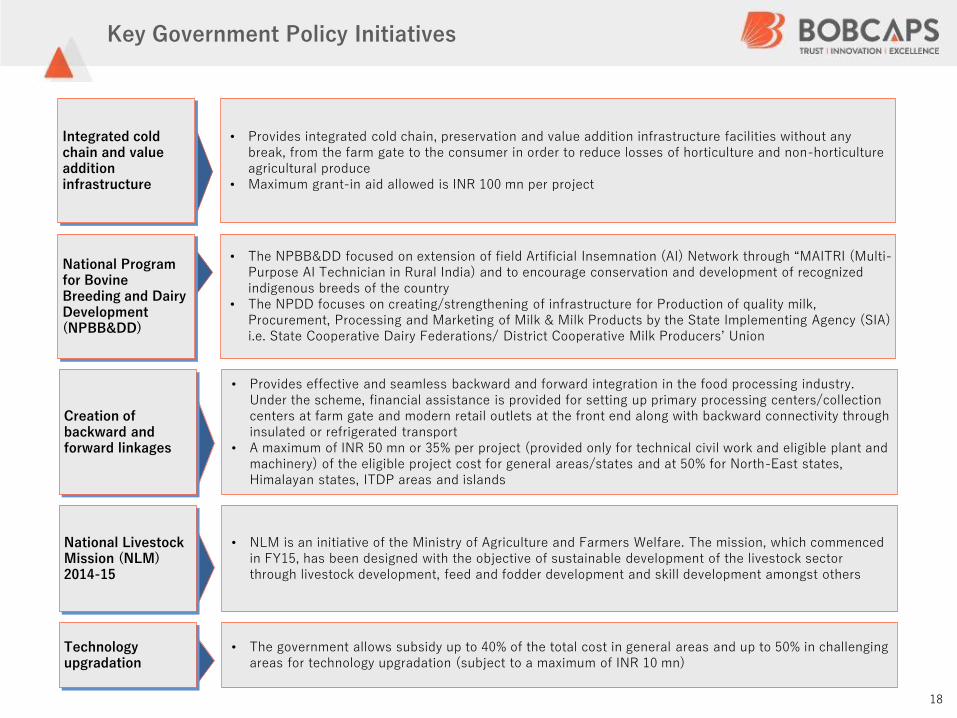

• The government allows subsidy up to 40% of the total cost in general areas and up to 50% in challenging areas for technology upgradation (subject to a maximum of INR 10 mn)

Technology upgradation

• Provides effective and seamless backward and forward integration in the food processing industry. Under the scheme, financial assistance is provided for setting up primary processing centers/collection centers at farm gate and modern retail outlets at the front end along with backward connectivity through insulated or refrigerated transport

• A maximum of INR 50 mn or 35% per project (provided only for technical civil work and eligible plant and machinery) of the eligible project cost for general areas/states and at 50% for North-East states, Himalayan states, ITDP areas and islands

Creation of backward and forward linkages

• Provides integrated cold chain, preservation and value addition infrastructure facilities without any break, from the farm gate to the consumer in order to reduce losses of horticulture and non-horticulture agricultural produce

• Maximum grant-in aid allowed is INR 100 mn per project

Integrated cold chain and value addition infrastructure

• The NPBB&DD focused on extension of field Artificial Insemnation (AI) Network through “MAITRI (Multi-Purpose AI Technician in Rural India) and to encourage conservation and development of recognized indigenous breeds of the country

• The NPDD focuses on creating/strengthening of infrastructure for Production of quality milk, Procurement, Processing and Marketing of Milk & Milk Products by the State Implementing Agency (SIA) i.e. State Cooperative Dairy Federations/ District Cooperative Milk Producers’ Union

National Program for Bovine Breeding and Dairy Development (NPBB&DD)

Key Government Policy Initiatives

• NLM is an initiative of the Ministry of Agriculture and Farmers Welfare. The mission, which commenced in FY15, has been designed with the objective of sustainable development of the livestock sector through livestock development, feed and fodder development and skill development amongst others

National Livestock Mission (NLM) 2014-15

18

Key Players 2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

20

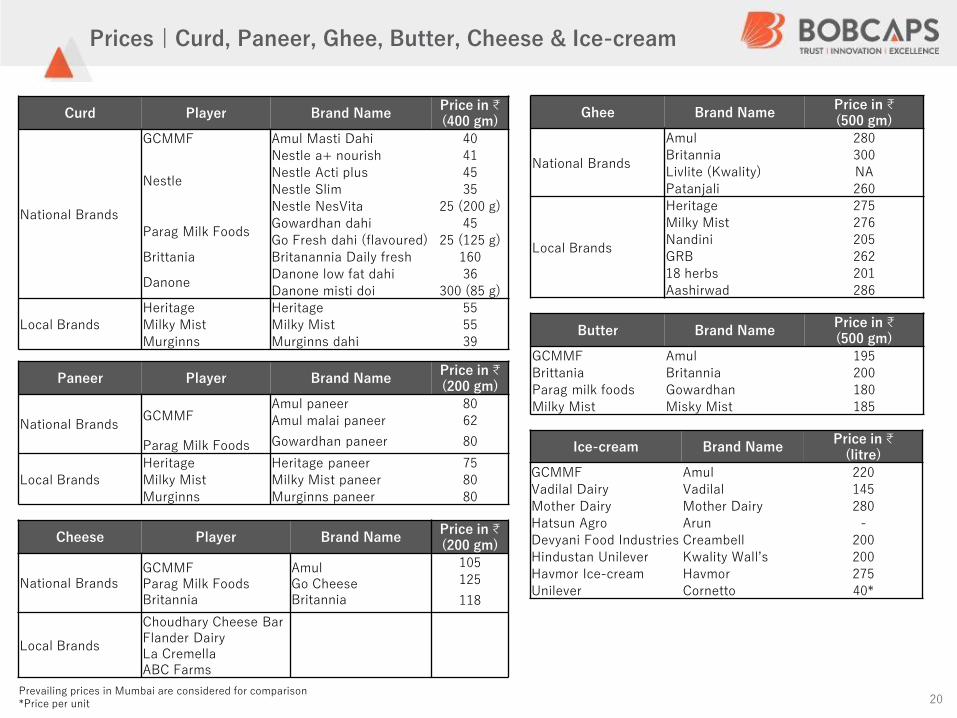

Prices | Curd, Paneer, Ghee, Butter, Cheese & Ice-cream

Ghee Brand NamePrice in ₹(500 gm)

National Brands

Amul 280

Britannia 300

Livlite (Kwality) NA

Patanjali 260

Local Brands

Heritage 275

Milky Mist 276

Nandini 205

GRB 262

18 herbs 201

Aashirwad 286

Butter Brand NamePrice in ₹(500 gm)

GCMMF Amul 195

Brittania Britannia 200

Parag milk foods Gowardhan 180

Milky Mist Misky Mist 185

Curd Player Brand NamePrice in ₹(400 gm)

National Brands

GCMMF Amul Masti Dahi 40

Nestle

Nestle a+ nourish 41

Nestle Acti plus 45

Nestle Slim 35

Nestle NesVita 25 (200 g)

Parag Milk FoodsGowardhan dahi 45

Go Fresh dahi (flavoured) 25 (125 g)

Brittania Britanannia Daily fresh 160

DanoneDanone low fat dahi 36

Danone misti doi 300 (85 g)

Local Brands

Heritage Heritage 55

Milky Mist Milky Mist 55

Murginns Murginns dahi 39

Paneer Player Brand NamePrice in ₹(200 gm)

National BrandsGCMMF

Amul paneer 80

Amul malai paneer 62

Gowardhan paneer 80Parag Milk Foods

Local Brands

Heritage Heritage paneer 75

Milky Mist Milky Mist paneer 80

Murginns Murginns paneer 80

Prevailing prices in Mumbai are considered for comparison*Price per unit

Cheese Player Brand NamePrice in ₹(200 gm)

National BrandsGCMMFParag Milk FoodsBritannia

AmulGo Cheese Britannia

105

125

118

Local Brands

Choudhary Cheese Bar Flander Dairy La CremellaABC Farms

Ice-cream Brand NamePrice in ₹

(litre)

GCMMF Amul 220

Vadilal Dairy Vadilal 145

Mother Dairy Mother Dairy 280

Hatsun Agro Arun -

Devyani Food Industries Creambell 200

Hindustan Unilever Kwality Wall’s 200

Havmor Ice-cream Havmor 275

Unilever Cornetto 40*

21

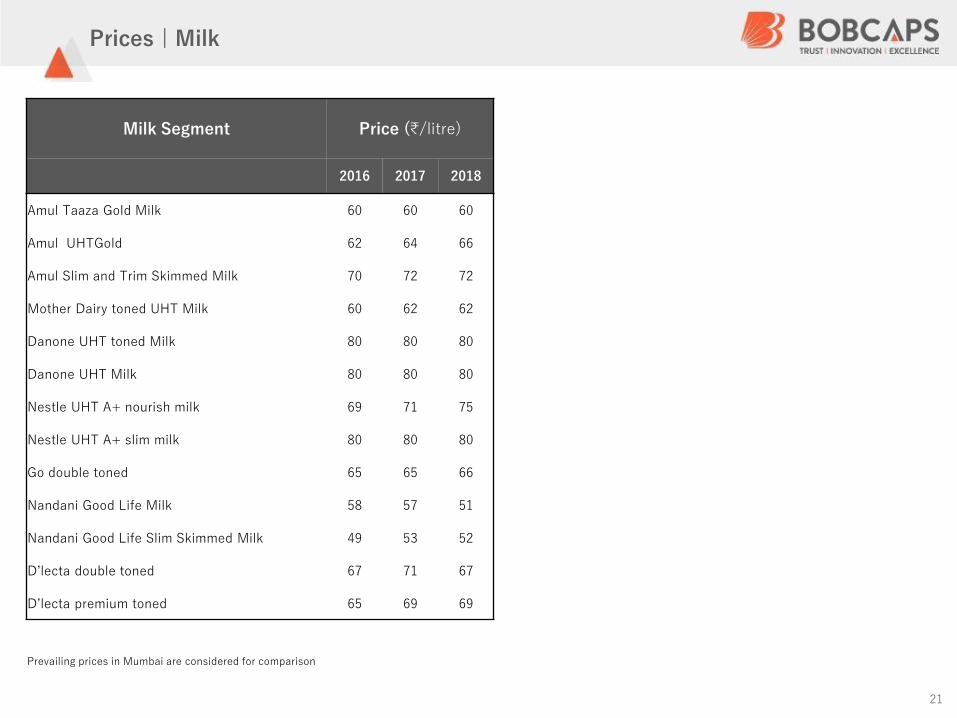

Prices | Milk

Milk Segment Price (₹/litre)

2016 2017 2018

Amul Taaza Gold Milk 60 60 60

Amul UHTGold 62 64 66

Amul Slim and Trim Skimmed Milk 70 72 72

Mother Dairy toned UHT Milk 60 62 62

Danone UHT toned Milk 80 80 80

Danone UHT Milk 80 80 80

Nestle UHT A+ nourish milk 69 71 75

Nestle UHT A+ slim milk 80 80 80

Go double toned 65 65 66

Nandani Good Life Milk 58 57 51

Nandani Good Life Slim Skimmed Milk 49 53 52

D’lecta double toned 67 71 67

D’lecta premium toned 65 69 69

Prevailing prices in Mumbai are considered for comparison

22

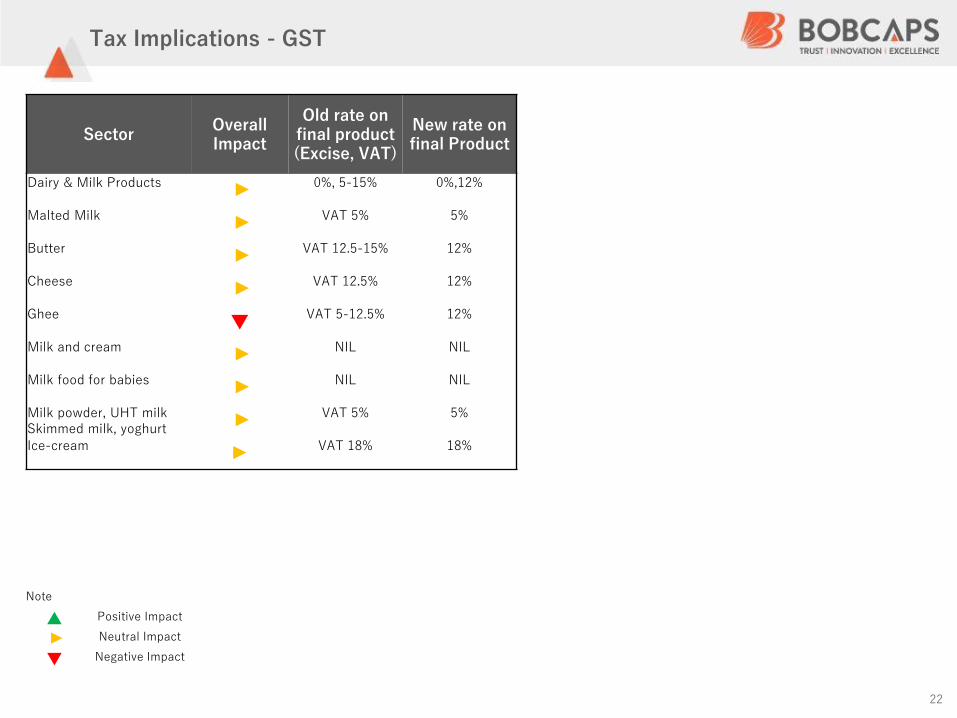

Tax Implications - GST

SectorOverall Impact

Old rate on final product(Excise, VAT)

New rate on final Product

Dairy & Milk Products ► 0%, 5-15% 0%,12%

Malted Milk ► VAT 5% 5%

Butter ► VAT 12.5-15% 12%

Cheese ► VAT 12.5% 12%

Ghee▼

VAT 5-12.5% 12%

Milk and cream ► NIL NIL

Milk food for babies ► NIL NIL

Milk powder, UHT milkSkimmed milk, yoghurt

► VAT 5% 5%

Ice-cream ► VAT 18% 18%

Note

▲ Positive Impact

► Neutral Impact

▼ Negative Impact

Key Players 2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India 3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

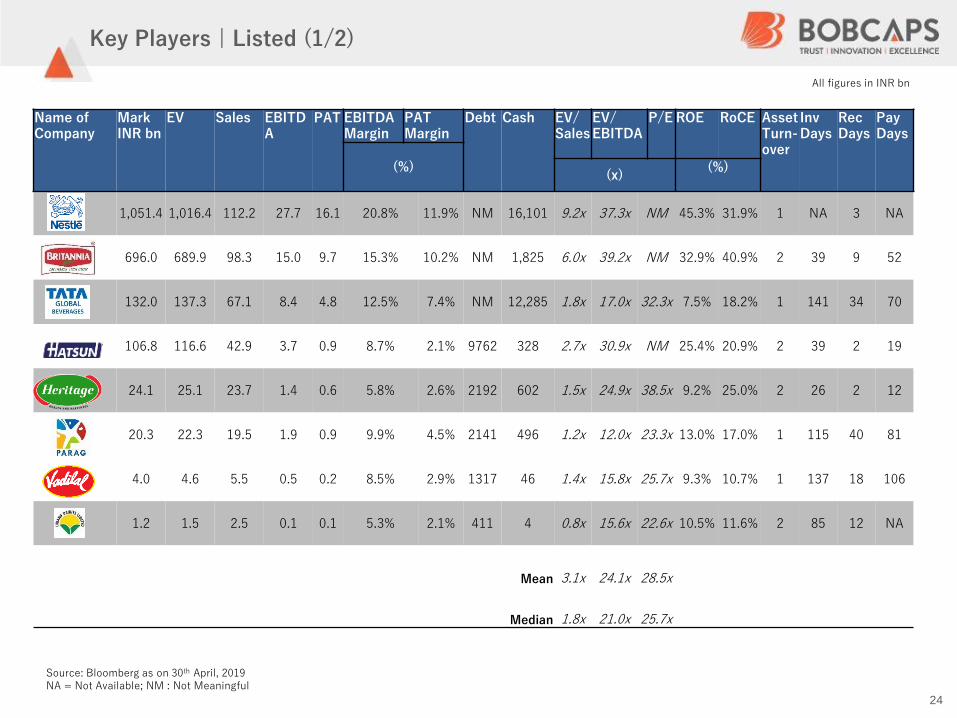

Name of Company

MarkINR bn

EV Sales EBITDA

PAT EBITDAMargin

PAT Margin

Debt Cash EV/Sales

EV/EBITDA

P/E ROE RoCE Asset Turn-over

Inv Days

RecDays

PayDays

(%)(x)

(%)

1,051.4 1,016.4 112.2 27.7 16.1 20.8% 11.9% NM 16,101 9.2x 37.3x NM 45.3% 31.9% 1 NA 3 NA

696.0 689.9 98.3 15.0 9.7 15.3% 10.2% NM 1,825 6.0x 39.2x NM 32.9% 40.9% 2 39 9 52

132.0 137.3 67.1 8.4 4.8 12.5% 7.4% NM 12,285 1.8x 17.0x 32.3x 7.5% 18.2% 1 141 34 70

106.8 116.6 42.9 3.7 0.9 8.7% 2.1% 9762 328 2.7x 30.9x NM 25.4% 20.9% 2 39 2 19

24.1 25.1 23.7 1.4 0.6 5.8% 2.6% 2192 602 1.5x 24.9x 38.5x 9.2% 25.0% 2 26 2 12

20.3 22.3 19.5 1.9 0.9 9.9% 4.5% 2141 496 1.2x 12.0x 23.3x 13.0% 17.0% 1 115 40 81

4.0 4.6 5.5 0.5 0.2 8.5% 2.9% 1317 46 1.4x 15.8x 25.7x 9.3% 10.7% 1 137 18 106

1.2 1.5 2.5 0.1 0.1 5.3% 2.1% 411 4 0.8x 15.6x 22.6x 10.5% 11.6% 2 85 12 NA

Mean 3.1x 24.1x 28.5x

Median 1.8x 21.0x 25.7x

Source: Bloomberg as on 30th April, 2019NA = Not Available; NM : Not Meaningful

24

All figures in INR bn

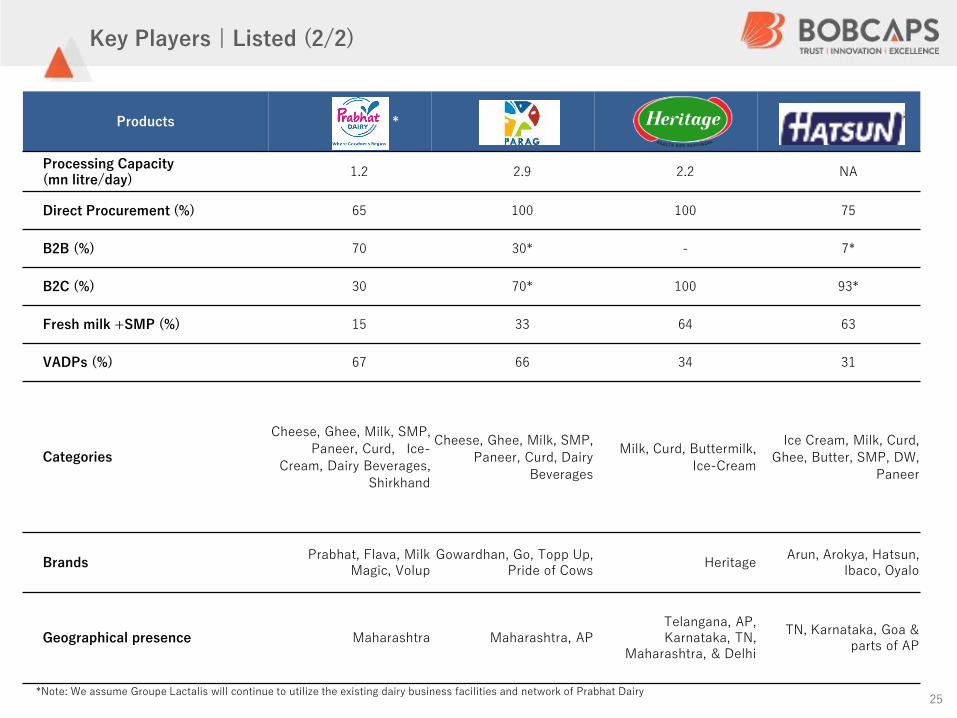

Key Players | Listed (1/2)

25

Products *

Processing Capacity(mn litre/day)

1.2 2.9 2.2 NA

Direct Procurement (%) 65 100 100 75

B2B (%) 70 30* - 7*

B2C (%) 30 70* 100 93*

Fresh milk +SMP (%) 15 33 64 63

VADPs (%) 67 66 34 31

Categories

Cheese, Ghee, Milk, SMP,

Paneer, Curd, Ice-

Cream, Dairy Beverages,

Shirkhand

Cheese, Ghee, Milk, SMP,

Paneer, Curd, Dairy

Beverages

Milk, Curd, Buttermilk,

Ice-Cream

Ice Cream, Milk, Curd,

Ghee, Butter, SMP, DW,

Paneer

BrandsPrabhat, Flava, Milk

Magic, VolupGowardhan, Go, Topp Up,

Pride of CowsHeritage

Arun, Arokya, Hatsun, Ibaco, Oyalo

Geographical presence Maharashtra Maharashtra, APTelangana, AP, Karnataka, TN,

Maharashtra, & Delhi

TN, Karnataka, Goa & parts of AP

*Note: We assume Groupe Lactalis will continue to utilize the existing dairy business facilities and network of Prabhat Dairy

Key Players | Listed (2/2)

Key PlayersSales

INR MnProducts

Geographical Presence

5,101

Milk, Paneer, Ghee,

Butter, Curd, Flavoured

Milk and Ice Cream

4,356 Milk Powder, Butter, Ghee

and Dairy Whitener

3,959

Paneer, Cream, Lassi,

Cheese, Butter, Yogurt,

Ghee, Shrikhand, Khova,

And Fruit Yogurt

3,643

Milk, Lassi, Chaach, Pure

Ghee, Flavoured Milk,

Paneer and Curd

3,133

Ghee, Ice Creams, Instant

Food Mixes, Spice

Masalas and Sweets

3,072 Yogurt, Curd, Buttermilk,

Lassi and Paneer

Key PlayersSales

INR MnProducts

Geographical Presence

11,359

Milk, Flavoured Milk,

Curd, Cream, Buttermilk,

Lassi, Dhood Peda,

Badam Burfi, Milk Cake,

Mysore Pak, Kalakand,

Mistidoi, Ghee, Paneer,

Butter and Yoghurt

11,076

Milk Powders, Milk

Drinks, Bread Spreads

Curd, Lassi, Butter Milk,

Ghee, Paneer, Namkeen,

and Sweets

10,185

Milk, Curd, Butter Milk,

Lassi, Flavored Milk,

Ghee, Butter, Paneer,

Doodhpeda, Basundhi and

Ice Creams

8,738

Milk, Ghee, Dairy Mix,

Curd, Lassi, Buttermilk,

Mishti Dahi, Tea, Coffee,

Milk Shake, Sweets, Ice

Cream, Pudding Paneer

and Milk Powder

5,623

Milk, Butter, Ghee,

Paneer, Shrikhand,

Amrakhand, Curd, Lassi,

Buttermilk, Flavoured Milk

and Milk Powder

26

█ Geographical Presence

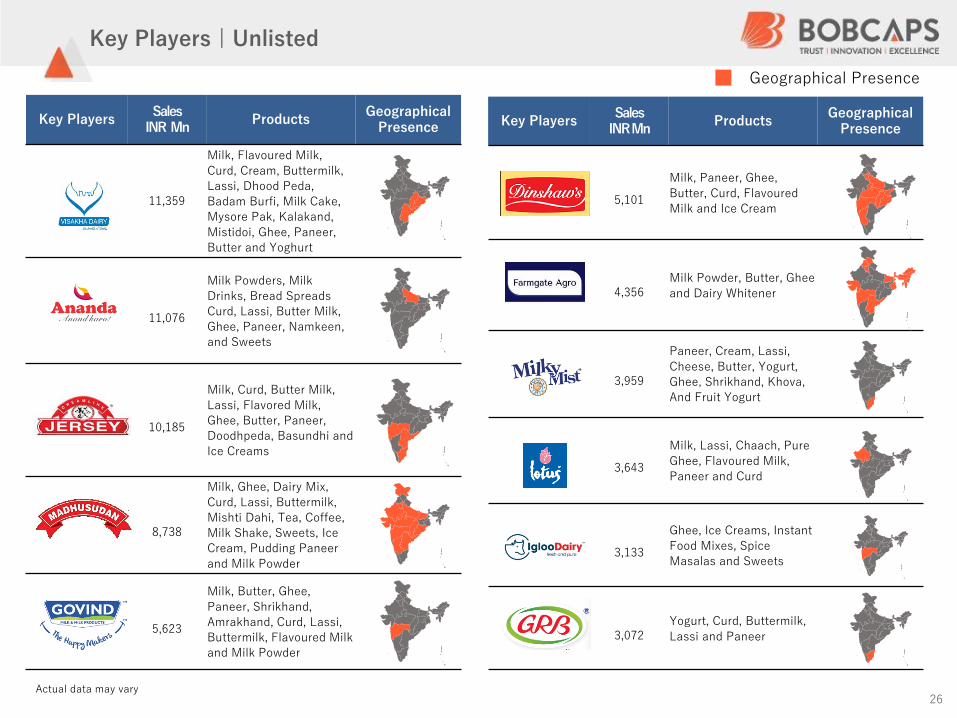

Key Players | Unlisted

Actual data may vary

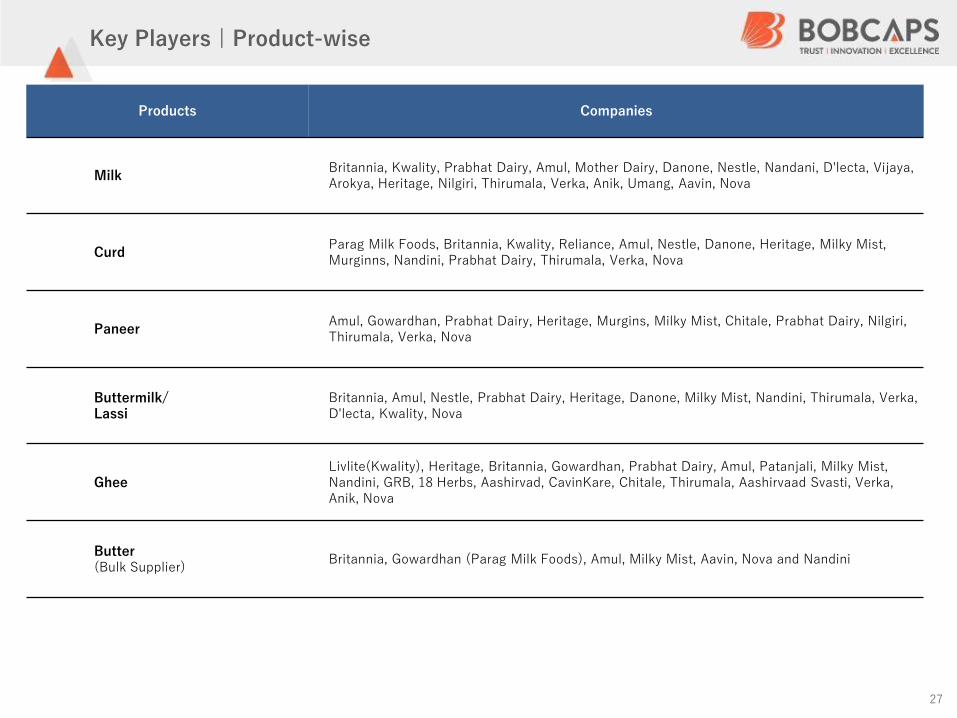

Products Companies

MilkBritannia, Kwality, Prabhat Dairy, Amul, Mother Dairy, Danone, Nestle, Nandani, D'lecta, Vijaya, Arokya, Heritage, Nilgiri, Thirumala, Verka, Anik, Umang, Aavin, Nova

CurdParag Milk Foods, Britannia, Kwality, Reliance, Amul, Nestle, Danone, Heritage, Milky Mist, Murginns, Nandini, Prabhat Dairy, Thirumala, Verka, Nova

PaneerAmul, Gowardhan, Prabhat Dairy, Heritage, Murgins, Milky Mist, Chitale, Prabhat Dairy, Nilgiri, Thirumala, Verka, Nova

Buttermilk/ Lassi

Britannia, Amul, Nestle, Prabhat Dairy, Heritage, Danone, Milky Mist, Nandini, Thirumala, Verka, D'lecta, Kwality, Nova

GheeLivlite(Kwality), Heritage, Britannia, Gowardhan, Prabhat Dairy, Amul, Patanjali, Milky Mist, Nandini, GRB, 18 Herbs, Aashirvad, CavinKare, Chitale, Thirumala, Aashirvaad Svasti, Verka, Anik, Nova

Butter(Bulk Supplier)

Britannia, Gowardhan (Parag Milk Foods), Amul, Milky Mist, Aavin, Nova and Nandini

27

Key Players | Product-wise

Key Players 2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India 3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

29

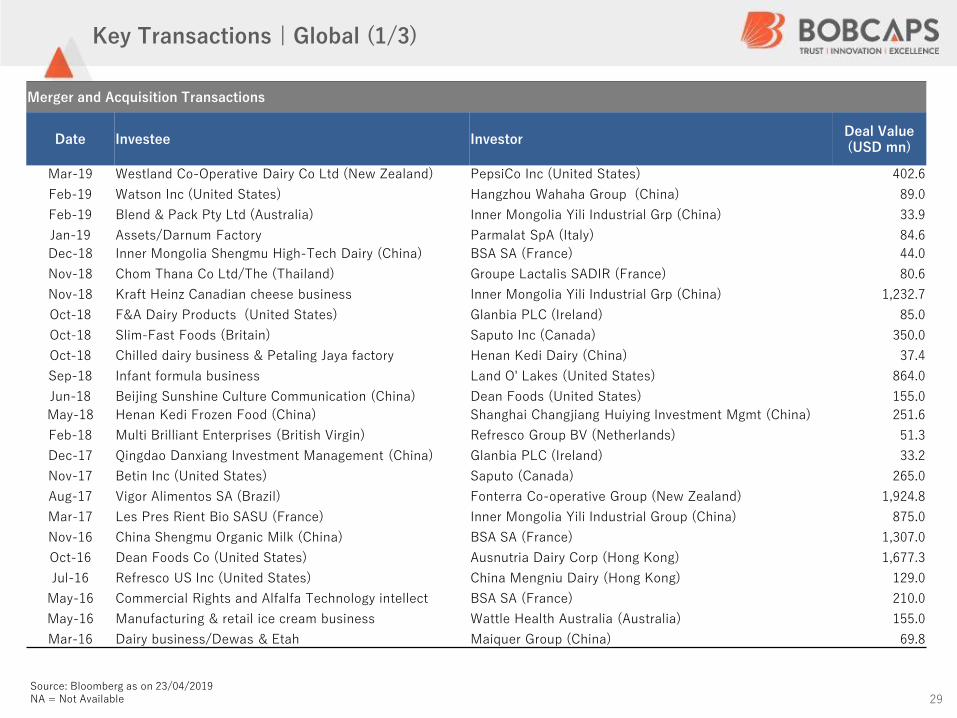

Merger and Acquisition Transactions

Date Investee InvestorDeal Value (USD mn)

Mar-19 Westland Co-Operative Dairy Co Ltd (New Zealand) PepsiCo Inc (United States) 402.6

Feb-19 Watson Inc (United States) Hangzhou Wahaha Group (China) 89.0

Feb-19 Blend & Pack Pty Ltd (Australia) Inner Mongolia Yili Industrial Grp (China) 33.9

Jan-19 Assets/Darnum Factory Parmalat SpA (Italy) 84.6

Dec-18 Inner Mongolia Shengmu High-Tech Dairy (China) BSA SA (France) 44.0

Nov-18 Chom Thana Co Ltd/The (Thailand) Groupe Lactalis SADIR (France) 80.6

Nov-18 Kraft Heinz Canadian cheese business Inner Mongolia Yili Industrial Grp (China) 1,232.7

Oct-18 F&A Dairy Products (United States) Glanbia PLC (Ireland) 85.0

Oct-18 Slim-Fast Foods (Britain) Saputo Inc (Canada) 350.0

Oct-18 Chilled dairy business & Petaling Jaya factory Henan Kedi Dairy (China) 37.4

Sep-18 Infant formula business Land O' Lakes (United States) 864.0

Jun-18 Beijing Sunshine Culture Communication (China) Dean Foods (United States) 155.0

May-18 Henan Kedi Frozen Food (China) Shanghai Changjiang Huiying Investment Mgmt (China) 251.6

Feb-18 Multi Brilliant Enterprises (British Virgin) Refresco Group BV (Netherlands) 51.3

Dec-17 Qingdao Danxiang Investment Management (China) Glanbia PLC (Ireland) 33.2

Nov-17 Betin Inc (United States) Saputo (Canada) 265.0

Aug-17 Vigor Alimentos SA (Brazil) Fonterra Co-operative Group (New Zealand) 1,924.8

Mar-17 Les Pres Rient Bio SASU (France) Inner Mongolia Yili Industrial Group (China) 875.0

Nov-16 China Shengmu Organic Milk (China) BSA SA (France) 1,307.0

Oct-16 Dean Foods Co (United States) Ausnutria Dairy Corp (Hong Kong) 1,677.3

Jul-16 Refresco US Inc (United States) China Mengniu Dairy (Hong Kong) 129.0

May-16 Commercial Rights and Alfalfa Technology intellect BSA SA (France) 210.0

May-16 Manufacturing & retail ice cream business Wattle Health Australia (Australia) 155.0

Mar-16 Dairy business/Dewas & Etah Maiquer Group (China) 69.8

Key Transactions | Global (1/3)

Source: Bloomberg as on 23/04/2019NA = Not Available

30

Private Equity Transactions

Date Investee InvestorDeal Value (USD mn)

Jan-19 United Farmers Holding (Saudi Arabia) Saudi Agricultural & Livestock Investment Co (Saudi Arabia) 28.0

Dec-18 Yashili New Zealand Dairy (France) Danone SA (France) 106.1

Dec-18 Beingmate Baby & Child Food (China) Deyang State-Owned Asset Management (China) 41.3

Oct-18 Kite hill (United States) 301 Inc (United States) 40.0

Oct-18 Shanghai Shoule E-Commerce (China) Maiquer Group (China) 29.4

Aug-18 Synlait Milk (New Zealand) a2 Milk (New Zealand) 109.3

Apr-18 Ausnutria Dairy Corp (China) CITIC Agricultural Industry Fund Management (China) 164.2

Apr-18 Ausnutria Dairy (China) CITIC Agricultural Industry Fund Management (China) 85.8

Nov-17 Vietnam Dairy Products JSC (Singapore) Jardine Cycle & Carriage (Singapore) 616.6

Oct-17 V V Food & Beverage (China) Ningbo Bohonghefeng Investment LP (China) 88.3

May-17 Dodla Dairy (United States) TPG Capital LP/US (United States) 50.0

Mar-17 Synlait Milk (New Zealand) a2 Milk (New Zealand) 33.8

Jan-17 China Modern Dairy Holdings (Hong Kong) China Mengniu Dairy (Hong Kong) 241.5

Dec-16 Parmalat SpA (France) BSA SA (France) 108.2

Oct-16 China Shengmu Organic Milk (China) Inner Mongolia Yili Industrial Group (China) 680.4

Apr-16 Shanghai Milkground Food Tech (China) Jilin Dongxiu Investment (China) 138.0

Jan-16 China Shengmu Organic Milk (China) Nong You (China) 430.4

Jan-16 Albalact SA (France) BSA SA (France) 98.1

Jan-16 Inner Mongolia Youran Animal Husbandry (HK) Yogurt Holding I HK (Hong Kong) 214.7

Source: Bloomberg as on 23/04/2019NA = Not Available

Key Transactions | Global (2/3)

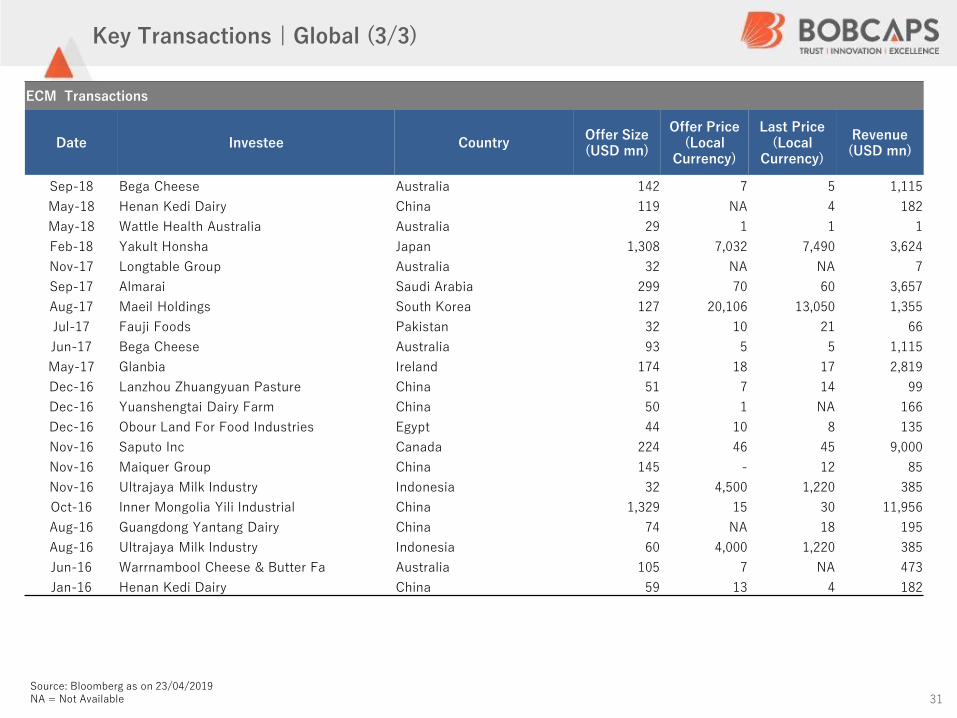

31Source: Bloomberg as on 23/04/2019NA = Not Available

ECM Transactions

Date Investee Country Offer Size(USD mn)

Offer Price(Local

Currency)

Last Price (Local

Currency)

Revenue(USD mn)

Sep-18 Bega Cheese Australia 142 7 5 1,115

May-18 Henan Kedi Dairy China 119 NA 4 182

May-18 Wattle Health Australia Australia 29 1 1 1

Feb-18 Yakult Honsha Japan 1,308 7,032 7,490 3,624

Nov-17 Longtable Group Australia 32 NA NA 7

Sep-17 Almarai Saudi Arabia 299 70 60 3,657

Aug-17 Maeil Holdings South Korea 127 20,106 13,050 1,355

Jul-17 Fauji Foods Pakistan 32 10 21 66

Jun-17 Bega Cheese Australia 93 5 5 1,115

May-17 Glanbia Ireland 174 18 17 2,819

Dec-16 Lanzhou Zhuangyuan Pasture China 51 7 14 99

Dec-16 Yuanshengtai Dairy Farm China 50 1 NA 166

Dec-16 Obour Land For Food Industries Egypt 44 10 8 135

Nov-16 Saputo Inc Canada 224 46 45 9,000

Nov-16 Maiquer Group China 145 - 12 85

Nov-16 Ultrajaya Milk Industry Indonesia 32 4,500 1,220 385

Oct-16 Inner Mongolia Yili Industrial China 1,329 15 30 11,956

Aug-16 Guangdong Yantang Dairy China 74 NA 18 195

Aug-16 Ultrajaya Milk Industry Indonesia 60 4,000 1,220 385

Jun-16 Warrnambool Cheese & Butter Fa Australia 105 7 NA 473

Jan-16 Henan Kedi Dairy China 59 13 4 182

Key Transactions | Global (3/3)

32

Key Transactions | India (1/2)

Source: Deal databasesNA = Not Available

Merger and Acquisition Transactions

Date Investee InvestorDeal Value (INR mn)

% Sought

Jan-19 Sunfresh Agro Industries Tirumala Milk Products 17,000 100

Aug-18 Vijaykant Dairy and Food Products , Adityaa Milk Hindustan Unilever NA 100

Apr-18 Danone Foods and Beverages India, Mfg Facility Parag Milk Foods 300 100

Nov-18 Havmor Ice Cream Lotte Confectionery 9,780 100

Nov-17 Vaman Milk Foods Heritage Foods NA 100

Sep-17 Metro Dairy Keventer Agro NA 47

Oct-16 Reliance Retail , Dairy Business Heritage Foods NA 100

Oct-16 Revera Milk and Foods Anik Industries 1,400 NA

May-16 Teja Dairy, Assets Heritage Foods 6 100

Mar-16 Anik Industries , Dairy Business Lactalis Group 4,500 100

Dec-15 Creamline Dairy Products Godrej Agrovet 1,500 25

Oct-15 AAK Kamani AAK AB 2,600 51

Mar-15 Anik Dairy Lactalis Group NA NA

Sep-14 The Nilgiri Dairy Farm Future Consumer 3,000 98

33

Private Equity Transactions

Investee InvestorDeal Value (INR mn)

% Sought EV/ Revenue EV/ EBITDA

x

Feb-19 Dodla Dairy International Finance Corp. 496 NA NA NA

Dec-18Drums Food International

Danone Manifesto Ventures Inc, DSG Consumer Partner & Individuals

1,820 NA NA NA

May-17 Keventer Agro Mandala Capital 1,700 15.0 1.5 18.0

May-17 Dodla Dairy The Rise 3,210 27.0 0.8 13.0

Jan-17 Milk Mantra Dairy Aavishkaar, Eight Road Ventures - - - -

Dec-16 Gho Agro ASK Pravi 500 NA NA NA

May-16 Parag Milk Foods Abu Dhabi Investment Council 429 2.1 1.5 16.1

Oct-16 HR Food Processing Aavishkaar India, Lok Capital 450 - - -

Apr-16 Sri Krishna Milks Capvent India Advisors 650 NA NA NA

Mar-16 Shreedhar Milk Foods Omrudra International Trading 233 4.4 0.5 13.3

Sep-15 Prabhat Dairy TVS Shriram 850 7.6 1.4 29.1

Apr-14 Hatsun Agro Product Westbridge 361 1.2 1.3 17.8

Nov-12 Neo Milk Products Ambit Pragma 474 100.0 1.1 27.6

Nov-12 Dodla Dairy Proterra Investments 1,100 23.7 0.7 12.7

Sep-12 Prabhat Dairy Proparco SA 1,400 36.8 1.1 24.3

Sep-12 Parag Milk Foods IDFC Private Equity 1,600 32.7 0.8 8.7

Apr-10 Tirumala Milk Products Carlyle Asia 1,000 20.6 1.0 14.0

Mar-10 The Nilgiri Dairy Farm Actis Advisers 231 9.5 1.4 NM

Average 1.1 17.7

Median 1.1 16.1

Key Transactions | India (2/2)

Source: Deal databasesNA = Not Available

ECM Transactions

Date Company Name Deal Type Deal Value

(INR mn)% Sought

DRHP Filed

Aug-18 Dodla Dairy Initial Public Offering 0.0 0.0

Completed

Feb-18 Hatsun Agro Products Rights Issue 5,280 5.88

Sep -15 Parag Milk Foods Initial Public Offering 7,368 40.74

Mar-15 Prabhat Dairy Initial Public Offering 3,650 0.0

Key Players 2

Select Deals | Case Studies

Overview | Indian Dairy Industry1

4

Deal Dynamics | Global and India 3

Products Trends 1A

1B Procurement and Innovative practices

1C Government Schemes

1D Price Analysis

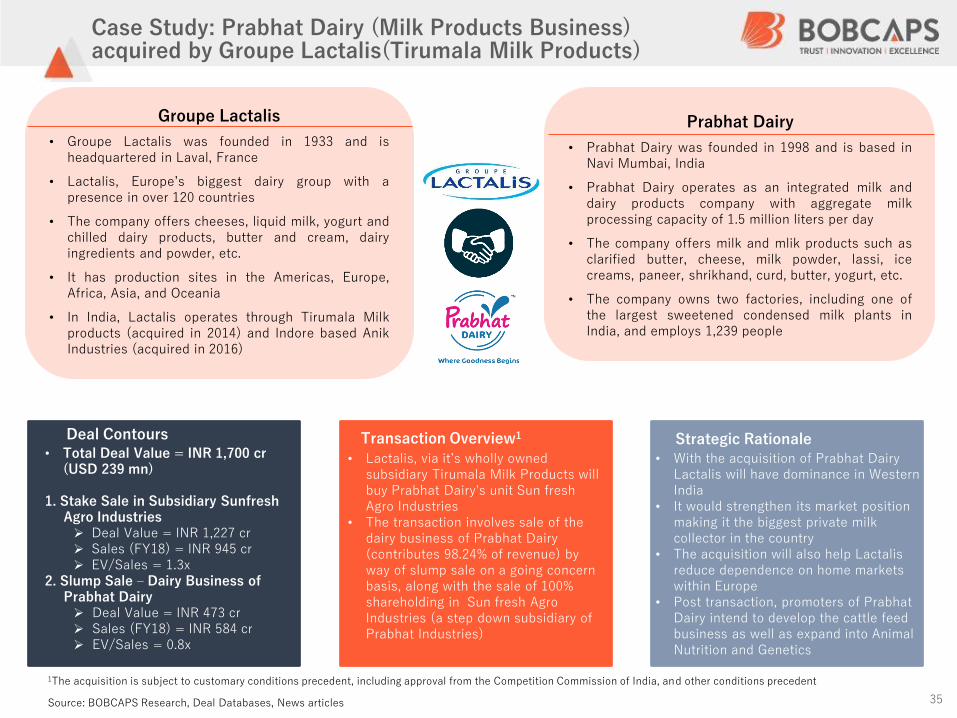

Transaction Overview1 Strategic Rationale • Total Deal Value = INR 1,700 cr

(USD 239 mn)

1. Stake Sale in Subsidiary SunfreshAgro Industries ➢ Deal Value = INR 1,227 cr➢ Sales (FY18) = INR 945 cr➢ EV/Sales = 1.3x

2. Slump Sale – Dairy Business of Prabhat Dairy ➢ Deal Value = INR 473 cr➢ Sales (FY18) = INR 584 cr➢ EV/Sales = 0.8x

• With the acquisition of Prabhat Dairy Lactalis will have dominance in Western India

• It would strengthen its market position making it the biggest private milk collector in the country

• The acquisition will also help Lactalis reduce dependence on home markets within Europe

• Post transaction, promoters of Prabhat Dairy intend to develop the cattle feed business as well as expand into Animal Nutrition and Genetics

Source: BOBCAPS Research, Deal Databases, News articles

Arysta Lifescience

• Arysta Lifescience is a global agricultural company specializing in the development, marketing and distribution of innovative crop protection and life science brands

• 3 large organizations integrated to create Arysta with presence in over 60 countries

• 13 manufacturing facilities with more than 200 active ingredients and 6,850+ registrations

• Arysta LifeScience has a well-integrated biological and chemical portfolio

• Product offering includes BioSolutions, fungicides, herbicides, insecticides and seed treatments

Groupe Lactalis

• Groupe Lactalis was founded in 1933 and isheadquartered in Laval, France

• Lactalis, Europe’s biggest dairy group with apresence in over 120 countries

• The company offers cheeses, liquid milk, yogurt andchilled dairy products, butter and cream, dairyingredients and powder, etc.

• It has production sites in the Americas, Europe,Africa, Asia, and Oceania

• In India, Lactalis operates through Tirumala Milkproducts (acquired in 2014) and Indore based AnikIndustries (acquired in 2016)

35

• Lactalis, via it’s wholly owned subsidiary Tirumala Milk Products will buy Prabhat Dairy's unit Sun fresh Agro Industries

• The transaction involves sale of the dairy business of Prabhat Dairy (contributes 98.24% of revenue) by way of slump sale on a going concern basis, along with the sale of 100% shareholding in Sun fresh AgroIndustries (a step down subsidiary of Prabhat Industries)

Deal Contours

Prabhat Dairy

• Prabhat Dairy was founded in 1998 and is based inNavi Mumbai, India

• Prabhat Dairy operates as an integrated milk anddairy products company with aggregate milkprocessing capacity of 1.5 million liters per day

• The company offers milk and mlik products such asclarified butter, cheese, milk powder, lassi, icecreams, paneer, shrikhand, curd, butter, yogurt, etc.

• The company owns two factories, including one ofthe largest sweetened condensed milk plants inIndia, and employs 1,239 people

Case Study: Prabhat Dairy (Milk Products Business)acquired by Groupe Lactalis(Tirumala Milk Products)

1The acquisition is subject to customary conditions precedent, including approval from the Competition Commission of India, and other conditions precedent

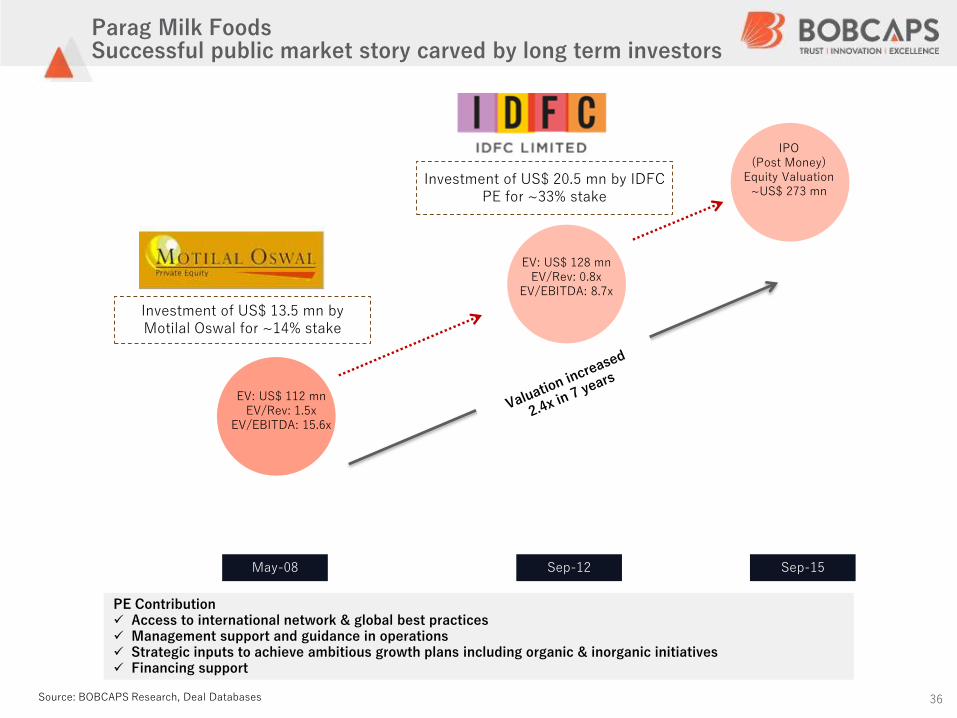

Parag Milk Foods Successful public market story carved by long term investors

Investment of US$ 20.5 mn by IDFC PE for ~33% stake

May-08 Sep-12 Sep-15

EV: US$ 112 mnEV/Rev: 1.5x

EV/EBITDA: 15.6x

IPO(Post Money)

Equity Valuation~US$ 273 mn

Investment of US$ 13.5 mn by Motilal Oswal for ~14% stake

EV: US$ 128 mnEV/Rev: 0.8x

EV/EBITDA: 8.7x

Source: BOBCAPS Research, Deal Databases 36

PE Contribution✓ Access to international network & global best practices✓ Management support and guidance in operations✓ Strategic inputs to achieve ambitious growth plans including organic & inorganic initiatives✓ Financing support

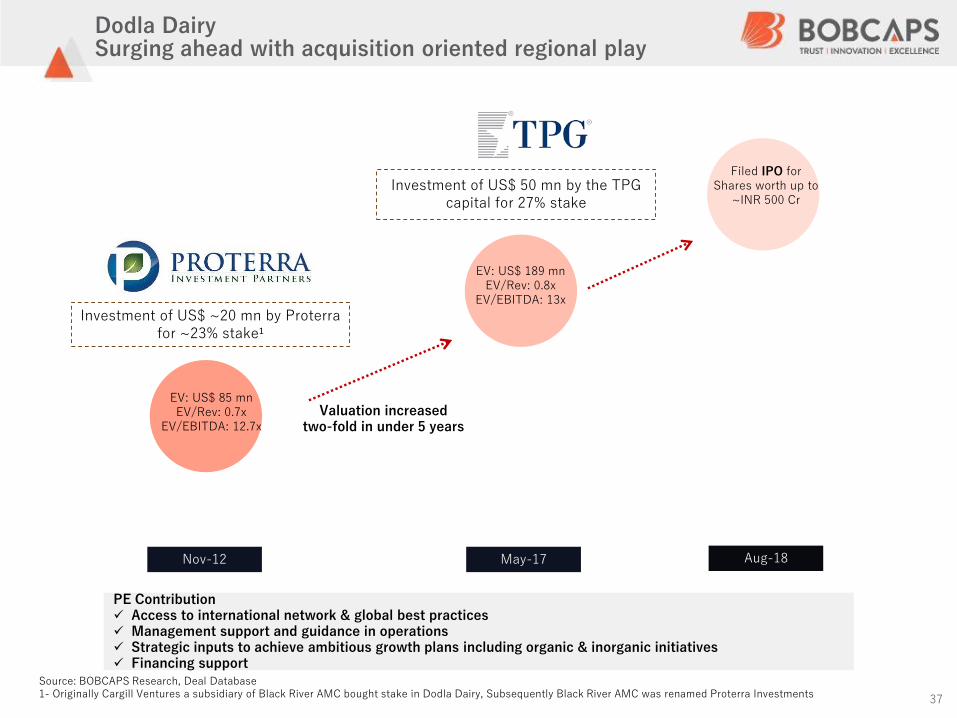

Dodla DairySurging ahead with acquisition oriented regional play

PE Contribution✓ Access to international network & global best practices✓ Management support and guidance in operations✓ Strategic inputs to achieve ambitious growth plans including organic & inorganic initiatives✓ Financing support

Source: BOBCAPS Research, Deal Database1- Originally Cargill Ventures a subsidiary of Black River AMC bought stake in Dodla Dairy, Subsequently Black River AMC was renamed Proterra Investments 37

Investment of US$ 50 mn by the TPG capital for 27% stake

Nov-12 May-17

EV: US$ 85 mnEV/Rev: 0.7x

EV/EBITDA: 12.7x

Investment of US$ ~20 mn by Proterra for ~23% stake1

EV: US$ 189 mnEV/Rev: 0.8x

EV/EBITDA: 13x

Valuation increasedtwo-fold in under 5 years

Filed IPO forShares worth up to

~INR 500 Cr

Aug-18

Twinkle ShahVice President Investment Banking

Dir: +91 22 6138 9342Mob: +91 98202 92630Email:[email protected]

BOB CAPITAL MARKETS LIMITED || Wholly owned subsidiary of Bank of Baroda

1704 - B Wing, Parinee Crescenzo, Plot No. C38/39, G-Block, Bandra Kurla Complex, Bandra (East), Mumbai – 400051

Ph.: +91.22.6138.9300 || Fax: +91.22.6671.8535Web: www.bobcaps.in

Contact Details & Disclaimer

Shradhda SomkuwarAnalystInvestment Banking

Dir: +91 22 6138 9300 (Ext:421)Mob: +91 77095 52510Email:[email protected]

Boddu SanthoshAnalystInvestment Banking

Dir: +91 22 6138 9300 (Ext:418)Mob: +91 81302 21995Email: [email protected]

Avdhoot DeshpandePresidentInvestment Banking

Dir: +91 22 6138 9306Mob: +91 98211 28750Email: [email protected]

Disclaimer

This presentation has been prepared by BOB Capital Markets (“BOBCAPS”) and is considered to be proprietary and strictly confidential.

The industry or any other external information and data contained in this document has not been verified by BOBCAPS representatives. Industry data weresourced from BOBCAPS research, deal databases, industry associations, company websites and leading newsprints. No representation or warranty, expressor implied, is or will be made and no responsibility or liability is or will be accepted by, any member of BOBCAPS, or by any of their respective officers,servants or agents or by their advisers or any other person as to or in relation to the accuracy or completeness of the information or opinions containedherein or supplied herewith or any other written or oral information made available to any interested party or its advisers.

In particular, this document does not constitute or form part of an offer to sell or an invitation to purchase or subscribe for shares or other securities. Itshould be clearly understood that this document does not purport to contain all the information which may be required to evaluate the project and thatrecipients are responsible for making their own decisions as to the completeness, fairness and accuracy of any information or opinion provided.

About BOBCAPS

BOB Capital Markets (BOBCAPS), SEBI registered Category-I Merchant Bank and a wholly owned subsidiary of Bank of Baroda, one of leading India’sleading banking and financial services organization with total assets of US$ 107bn. BOBCAPS is full service Investment Bank and Broking House offeringintegrated solutions with high-quality financial advisory services and financing with team comprising ~80 members across Investment Banking andInstitutional Equities & Broking segment and are rapidly expanding. Our services portfolio is focused across:

• Equity and Debt Capital• IPO• M&A Advisory

• Private Equity Advisory• Institutional Equities• Brokerage Services

• Project Advisory• Stressed Assets Resolutions