Embed Size (px)

Citation preview

WAIPIO (Main Office)94-449 Ukee StreetWaipahu, HI 96797

Mon - Fri: 10:00 a.m. to 6:00 p.m.Sat: 8:00 a.m. to 3:00 p.m.

DIRECT LINE: 73-PHFCU (737-4328)WEBSITE: www.phfcu.com

E-MAIL: [email protected] TOLL-FREE: 1-800-987-5583

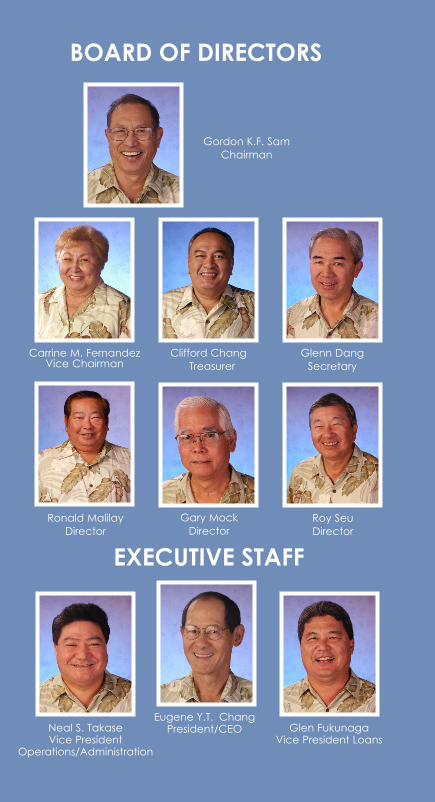

Eugene Y.T. ChangPresident/CEONeal S. Takase

Vice President Operations/Administration

Glen FukunagaVice President Loans

Ronald MalilayDirector

Roy SeuDirector

Glenn DangSecretary

Carrine M. FernandezVice Chairman

Clifford ChangTreasurer

Gary MockDirector

Gordon K.F. SamChairman

Gordon K.F. SamChairman of the

Board of Directors

Eugene Y.T. ChangPresident/CEO

Gordon K.F. SamChairman of the Board

Eugene Y.T. ChangPresident/CEO

Four years after 2008’s “Great Recession,” our state, nation and world economies remain in recovery mode. In order to hasten this recovery process and stimulate the economy, our govern-ment has enacted severe fiscal policies to keep interest rates at historically low levels. This, along with greater regulatory burden, has created a hardship on the financial industry.

Financial institutions make a profit by managing a financial spread between what we collect in terms of loan interest and investment income and payout in the form of dividends. This difference or “spread” is what a financial institution uses to pay its operating costs and cover loan write-offs. Due to an extremely low interest rate environment, this spread declined below historical levels in 2012 and the Credit Union suffered a minor loss. While many financial institutions supplemented their income by charging their members/customers excessive fees, we chose to continue to offer our products and services either free or at a nominal cost.

Despite adversity, the Board of Directors and Management have maintained the Credit Union’s capital reserves. Pearl Harbor Federal Credit Union remains well-capitalized, well positioned un-til our economy fully recovers, and ended 2012 with a Net-Worth Ratio of 9.34%, which is well above the 7% regulatory standard for a “well capitalized” credit union.

Although 2013 is expected to be similar to 2012, we remain confi-dent that Pearl Harbor Federal Credit Union’s substantial strate-gic, financial and organizational strengths have prepared the Credit Union to succeed. We are judiciously investing to improve services and provide value to our members. We are also looking at our existing services and products to find ways to offer future improvements.

Pearl Harbor Federal Credit Union will continue to deliver on our mission to provide members with consistently superior financial value and exceptional service in a friendly, family environment. On behalf of the Board of Directors, management and staff of Pearl Harbor Federal Credit Union, thank you for being part of our credit union family.

BOARD CHAIRMAN & PRESIDENT’S

REPORT

BOARD OF DIRECTORS

EXECUTIVE STAFF

WAIPIO (Main Office)94-449 Ukee StreetWaipahu, HI 96797

Mon - Fri: 10:00 a.m. to 6:00 p.m.Sat: 8:00 a.m. to 3:00 p.m.

DIRECT LINE: 73-PHFCU (737-4328)WEBSITE: www.phfcu.com

E-MAIL: [email protected] TOLL-FREE: 1-800-987-5583

Eugene Y.T. ChangPresident/CEONeal S. Takase

Vice President Operations/Administration

Glen FukunagaVice President Loans

Ronald MalilayDirector

Roy SeuDirector

Glenn DangSecretary

Carrine M. FernandezVice Chairman

Clifford ChangTreasurer

Gary MockDirector

Gordon K.F. SamChairman

Gordon K.F. SamChairman of the

Board of Directors

Eugene Y.T. ChangPresident/CEO

Gordon K.F. SamChairman of the Board

Eugene Y.T. ChangPresident/CEO

Four years after 2008’s “Great Recession,” our state, nation and world economies remain in recovery mode. In order to hasten this recovery process and stimulate the economy, our govern-ment has enacted severe fiscal policies to keep interest rates at historically low levels. This, along with greater regulatory burden, has created a hardship on the financial industry.

Financial institutions make a profit by managing a financial spread between what we collect in terms of loan interest and investment income and payout in the form of dividends. This difference or “spread” is what a financial institution uses to pay its operating costs and cover loan write-offs. Due to an extremely low interest rate environment, this spread declined below historical levels in 2012 and the Credit Union suffered a minor loss. While many financial institutions supplemented their income by charging their members/customers excessive fees, we chose to continue to offer our products and services either free or at a nominal cost.

Despite adversity, the Board of Directors and Management have maintained the Credit Union’s capital reserves. Pearl Harbor Federal Credit Union remains well-capitalized, well positioned un-til our economy fully recovers, and ended 2012 with a Net-Worth Ratio of 9.34%, which is well above the 7% regulatory standard for a “well capitalized” credit union.

Although 2013 is expected to be similar to 2012, we remain confi-dent that Pearl Harbor Federal Credit Union’s substantial strate-gic, financial and organizational strengths have prepared the Credit Union to succeed. We are judiciously investing to improve services and provide value to our members. We are also looking at our existing services and products to find ways to offer future improvements.

Pearl Harbor Federal Credit Union will continue to deliver on our mission to provide members with consistently superior financial value and exceptional service in a friendly, family environment. On behalf of the Board of Directors, management and staff of Pearl Harbor Federal Credit Union, thank you for being part of our credit union family.

BOARD CHAIRMAN & PRESIDENT’S

REPORT

BOARD OF DIRECTORS

EXECUTIVE STAFF

ASSETS Loans to members, less allowance for loan losses Cash and cash equivalents Investments Prepaid and deferred expenses Property and equipment, net Accrued interest on loans Accrued interest on investments NCUSIF depositForeclosed assets Other assets Total assets

LIABILITIES AND MEMBERS’ EQUITY Liabilities: Accounts payable and other liabilities Dividends payable Accrued expenses Total liabilities Commitments and contingent liabilities Members’ equity: Members’ shares: Regular savings Checking Individual Retirement Accounts (IRA’s) Saving Certificates

Members’ equity, substantially restricted Total members’ equity Total liabilities and members’ equity

$ 114,519,73732,520,898

174,748,071 301,003

10,289,921 251,641 405,606

3,048,330 513,000

95,563 336,693,770

390,660 28,968

571,194

990,822

171,644,992 17,246,726 26,384,860 88,994,519

304,271,097

31,431,851

335,702,948

$ 336,693,770

STATEMENTS OF MEMBERS’ EQUITY

Regular ReservesAppropriated Undivided EarningsUndivided Earnings

Total

$ 3,147,179 5,389,33022,895,342

$ 31,431,851

INCOME

Interest income: Loans to members Investments - held-to-maturity and other Total interest income Interest expense: Members’ shares dividends Borrowed funds Total interest expense Net interest income Provision for loan losses Net interest income after provision for loan losses Non-interest income: Gain on investments Loss on disposal of property and equipment Loss on sale of foreclosed assets Fees and charges Other Total non-interest income (loss)

Non-interest expense: Compensation Employee benefits Travel and conference Association dues Office occupancy Office operations Education and promotion Loan servicing Professional and outside services Members’ insurance NCUSIF stabilization Operating fees Other Total non-interest expense Net loss

$ 6,339,489 2,424,415

8,763,904 767,544

—

767,544

7,996,360

8,344,127

—

917,592 493,318

1,397,172

4,337,780 1,892,886 119,818

63,540 652,228

1,418,756 336,125 279,184 111,047

3,412 289,591

77,472 430,317

10,012,156 $

Ryan TsujiChairman of the

Supervisory Commitee

Ryan TsujiChairman of the Supervisory Committee

The Supervisory Committee is comprised of five volun-teers appointed by the Board of Directors from the credit union’s membership to serve as the audit committee for the credit union. Committee members serve as a vol-unteer for a two year term. Jennifer Luke is our newest member of the committee and brings special expertise in the area of auditing. We would also like to congratulate Roy Seu on his appointment as a Director of the Board of Directors. Current members of the committee include Madan Dhakhwa, Joe Lee, Kristen Woo, Jennifer Luke, and myself.

The committee is responsible to ensure that the credit union is managed in the best interest of its membership/owners. The committee meets monthly and conducts internal auditing procedures throughout the year. Its responsibilities include ensuring that the credit union’s policies, procedures and practices are in compliance with sound financial principles and within the laws and regulations that govern federal credit unions. One of the committee’s main responsibilities is to ensure that the credit union’s financial records and reports are accurate. To fulfill this requirement, the committee engaged the firm of Kwock and Company, CPA’s to perform the annual opinion audit.

On behalf of the Supervisory Committee, we thank you the Board of Directors, management and staff for your outstanding work and dedication during this especially difficult economic year. We also thank the membership for allowing us the opportunity to serve our credit union.

2012 SUPERVISORY COMMITTEE REPORT

2012 Statement of Financial Condition 2012 Income Statement

(347,767)

(61)

(270,857)

(13,677)

WAIPIO (Main Office)94-449 Ukee StreetWaipahu, HI 96797

Mon - Fri: 10:00 a.m. to 6:00 p.m.Sat: 8:00 a.m. to 3:00 p.m.

DIRECT LINE: 73-PHFCU (737-4328)WEBSITE: www.phfcu.com

E-MAIL: [email protected] TOLL-FREE: 1-800-987-5583

Eugene Y.T. ChangPresident/CEONeal S. Takase

Vice President Operations/Administration

Glen FukunagaVice President Loans

Ronald MalilayDirector

Roy SeuDirector

Glenn DangSecretary

Carrine M. FernandezVice Chairman

Clifford ChangTreasurer

Gary MockDirector

Gordon K.F. SamChairman

Gordon K.F. SamChairman of the

Board of Directors

Eugene Y.T. ChangPresident/CEO

Gordon K.F. SamChairman of the Board

Eugene Y.T. ChangPresident/CEO

Four years after 2008’s “Great Recession,” our state, nation and world economies remain in recovery mode. In order to hasten this recovery process and stimulate the economy, our govern-ment has enacted severe fiscal policies to keep interest rates at historically low levels. This, along with greater regulatory burden, has created a hardship on the financial industry.

Financial institutions make a profit by managing a financial spread between what we collect in terms of loan interest and investment income and payout in the form of dividends. This difference or “spread” is what a financial institution uses to pay its operating costs and cover loan write-offs. Due to an extremely low interest rate environment, this spread declined below historical levels in 2012 and the Credit Union suffered a minor loss. While many financial institutions supplemented their income by charging their members/customers excessive fees, we chose to continue to offer our products and services either free or at a nominal cost.

Despite adversity, the Board of Directors and Management have maintained the Credit Union’s capital reserves. Pearl Harbor Federal Credit Union remains well-capitalized, well positioned un-til our economy fully recovers, and ended 2012 with a Net-Worth Ratio of 9.34%, which is well above the 7% regulatory standard for a “well capitalized” credit union.

Although 2013 is expected to be similar to 2012, we remain confi-dent that Pearl Harbor Federal Credit Union’s substantial strate-gic, financial and organizational strengths have prepared the Credit Union to succeed. We are judiciously investing to improve services and provide value to our members. We are also looking at our existing services and products to find ways to offer future improvements.

Pearl Harbor Federal Credit Union will continue to deliver on our mission to provide members with consistently superior financial value and exceptional service in a friendly, family environment. On behalf of the Board of Directors, management and staff of Pearl Harbor Federal Credit Union, thank you for being part of our credit union family.

BOARD CHAIRMAN & PRESIDENT’S

REPORT

BOARD OF DIRECTORS

EXECUTIVE STAFF

ASSETS Loans to members, less allowance for loan losses Cash and cash equivalents Investments Prepaid and deferred expenses Property and equipment, net Accrued interest on loans Accrued interest on investments NCUSIF depositForeclosed assets Other assets Total assets

LIABILITIES AND MEMBERS’ EQUITY Liabilities: Accounts payable and other liabilities Dividends payable Accrued expenses Total liabilities Commitments and contingent liabilities Members’ equity: Members’ shares: Regular savings Checking Individual Retirement Accounts (IRA’s) Saving Certificates

Members’ equity, substantially restricted Total members’ equity Total liabilities and members’ equity

$ 114,519,73732,520,898

174,748,071 301,003

10,289,921 251,641 405,606

3,048,330 513,000

95,563 336,693,770

390,660 28,968

571,194

990,822

171,644,992 17,246,726 26,384,860 88,994,519

304,271,097

31,431,851

335,702,948

$ 336,693,770

STATEMENTS OF MEMBERS’ EQUITY

Regular ReservesAppropriated Undivided EarningsUndivided Earnings

Total

$ 3,147,179 5,389,33022,895,342

$ 31,431,851

INCOME

Interest income: Loans to members Investments - held-to-maturity and other Total interest income Interest expense: Members’ shares dividends Borrowed funds Total interest expense Net interest income Provision for loan losses Net interest income after provision for loan losses Non-interest income: Gain on investments Loss on disposal of property and equipment Loss on sale of foreclosed assets Fees and charges Other Total non-interest income (loss)

Non-interest expense: Compensation Employee benefits Travel and conference Association dues Office occupancy Office operations Education and promotion Loan servicing Professional and outside services Members’ insurance NCUSIF stabilization Operating fees Other Total non-interest expense Net loss

$ 6,339,489 2,424,415

8,763,904 767,544

—

767,544

7,996,360

8,344,127

—

917,592 493,318

1,397,172

4,337,780 1,892,886 119,818

63,540 652,228

1,418,756 336,125 279,184 111,047

3,412 289,591

77,472 430,317

10,012,156 $

Ryan TsujiChairman of the

Supervisory Commitee

Ryan TsujiChairman of the Supervisory Committee

The Supervisory Committee is comprised of five volun-teers appointed by the Board of Directors from the credit union’s membership to serve as the audit committee for the credit union. Committee members serve as a vol-unteer for a two year term. Jennifer Luke is our newest member of the committee and brings special expertise in the area of auditing. We would also like to congratulate Roy Seu on his appointment as a Director of the Board of Directors. Current members of the committee include Madan Dhakhwa, Joe Lee, Kristen Woo, Jennifer Luke, and myself.

The committee is responsible to ensure that the credit union is managed in the best interest of its membership/owners. The committee meets monthly and conducts internal auditing procedures throughout the year. Its responsibilities include ensuring that the credit union’s policies, procedures and practices are in compliance with sound financial principles and within the laws and regulations that govern federal credit unions. One of the committee’s main responsibilities is to ensure that the credit union’s financial records and reports are accurate. To fulfill this requirement, the committee engaged the firm of Kwock and Company, CPA’s to perform the annual opinion audit.

On behalf of the Supervisory Committee, we thank you the Board of Directors, management and staff for your outstanding work and dedication during this especially difficult economic year. We also thank the membership for allowing us the opportunity to serve our credit union.

2012 SUPERVISORY COMMITTEE REPORT

2012 Statement of Financial Condition 2012 Income Statement

(347,767)

(61)

(270,857)

(13,677)

ASSETS Loans to members, less allowance for loan losses Cash and cash equivalents Investments Prepaid and deferred expenses Property and equipment, net Accrued interest on loans Accrued interest on investments NCUSIF depositForeclosed assets Other assets Total assets

LIABILITIES AND MEMBERS’ EQUITY Liabilities: Accounts payable and other liabilities Dividends payable Accrued expenses Total liabilities Commitments and contingent liabilities Members’ equity: Members’ shares: Regular savings Checking Individual Retirement Accounts (IRA’s) Saving Certificates

Members’ equity, substantially restricted Total members’ equity Total liabilities and members’ equity

$ 114,519,73732,520,898

174,748,071 301,003

10,289,921 251,641 405,606

3,048,330 513,000

95,563 336,693,770

390,660 28,968

571,194

990,822

171,644,992 17,246,726 26,384,860 88,994,519

304,271,097

31,431,851

335,702,948

$ 336,693,770

STATEMENTS OF MEMBERS’ EQUITY

Regular ReservesAppropriated Undivided EarningsUndivided Earnings

Total

$ 3,147,179 5,389,33022,895,342

$ 31,431,851

INCOME

Interest income: Loans to members Investments - held-to-maturity and other Total interest income Interest expense: Members’ shares dividends Borrowed funds Total interest expense Net interest income Provision for loan losses Net interest income after provision for loan losses Non-interest income: Gain on investments Loss on disposal of property and equipment Loss on sale of foreclosed assets Fees and charges Other Total non-interest income (loss)

Non-interest expense: Compensation Employee benefits Travel and conference Association dues Office occupancy Office operations Education and promotion Loan servicing Professional and outside services Members’ insurance NCUSIF stabilization Operating fees Other Total non-interest expense Net loss

$ 6,339,489 2,424,415

8,763,904 767,544

—

767,544

7,996,360

8,344,127

—

917,592 493,318

1,397,172

4,337,780 1,892,886 119,818

63,540 652,228

1,418,756 336,125 279,184 111,047

3,412 289,591

77,472 430,317

10,012,156 $

Ryan TsujiChairman of the

Supervisory Commitee

Ryan TsujiChairman of the Supervisory Committee

The Supervisory Committee is comprised of five volun-teers appointed by the Board of Directors from the credit union’s membership to serve as the audit committee for the credit union. Committee members serve as a vol-unteer for a two year term. Jennifer Luke is our newest member of the committee and brings special expertise in the area of auditing. We would also like to congratulate Roy Seu on his appointment as a Director of the Board of Directors. Current members of the committee include Madan Dhakhwa, Joe Lee, Kristen Woo, Jennifer Luke, and myself.

The committee is responsible to ensure that the credit union is managed in the best interest of its membership/owners. The committee meets monthly and conducts internal auditing procedures throughout the year. Its responsibilities include ensuring that the credit union’s policies, procedures and practices are in compliance with sound financial principles and within the laws and regulations that govern federal credit unions. One of the committee’s main responsibilities is to ensure that the credit union’s financial records and reports are accurate. To fulfill this requirement, the committee engaged the firm of Kwock and Company, CPA’s to perform the annual opinion audit.

On behalf of the Supervisory Committee, we thank you the Board of Directors, management and staff for your outstanding work and dedication during this especially difficult economic year. We also thank the membership for allowing us the opportunity to serve our credit union.

2012 SUPERVISORY COMMITTEE REPORT

2012 Statement of Financial Condition 2012 Income Statement

(347,767)

(61)

(270,857)

(13,677)