Embed Size (px)

Citation preview

Financial Management For the Non-Financial

Professional

Presented by:The Florida Bar’s

Law Office Management Assistance Service(LOMAS)

850-561-5616

What this course will cover Learning financial management skills

will positively impact your efforts at managing all the other aspects of the business.

Planning Reporting and budgeting Human Resources Facilities and Purchasing Systems and Technology

2LOMAS

What this course will cover Financial Management Basics Strategic Planning Basic financial statements/reports Compensation Budgeting and Reporting Paralegal Utilization Internal Controls and Warning Signals Trust Accounting, Holding Client Property

3LOMAS

How to withstand a slow-down in the economy

Define your marketplace and market niche Learn how to plan. Service businesses:

60% to 80% of your gross revenues are tied up in Occupancy and Personnel costs The most difficult expense categories to change

quickly Cross-train, automate fully, employee leasing Leasing exit strategy, back door. . .

4LOMAS

More on controlling costs

Avoid overtime Bonuses do not increase base wages for overtime

calculations

Part-time staff do not expect group benefits Job sharing

Control purchasing Standard supply inventories

Inventory everything Budget comparisons

5LOMAS

STRATEGIC PLANNING

Two words that scare the heck out of most business owners and managers.

Strategic planning is not marketing. Strategic planning is not about grand

ideas and mission statements. The planning horizon for most service

businesses has changed from “The Five Year Plan” to “The Two Year Plan.”

6LOMAS

What is Strategic Planning?

Key Elements: Top down planning process. Goal with measurable objectives.

e.g., “What should be our optimal market share?” How large should we be for optimal profit margin?

Law Firm with 100 people – 39% profit margin Law Firm with 10 people – 39% profit margin 39% of what?

Analysis of Resources. What do we need to get there? Regular status meetings. Budget, staffing, funding.

7LOMAS

How to learn to plan Being a planner is a learned skill for most people

Forty percent of the public are not planners, it is not in their nature, but everyone can learn how to plan.

Are you a planner? Carl Jung, Myers-Briggs, Kiersey Personality Sorter and more.

No-nonsense books from the ABA. Books from public libraries. Seminars from the American Management

Association, Skillpath.com, Chamber of Commerce. "You've got to be very careful if you don't know

where you're going, because you might not get there." (Yogi Berra).

8LOMAS

Finance Basics

The key is to have a benchmark or expectation to see why your actual figures differ from expectations, and take action based on this.

This is why having a strategic plan and budget are critical.

Use current and past financial statements, and current and past budgets, to create an expectation.

9LOMAS

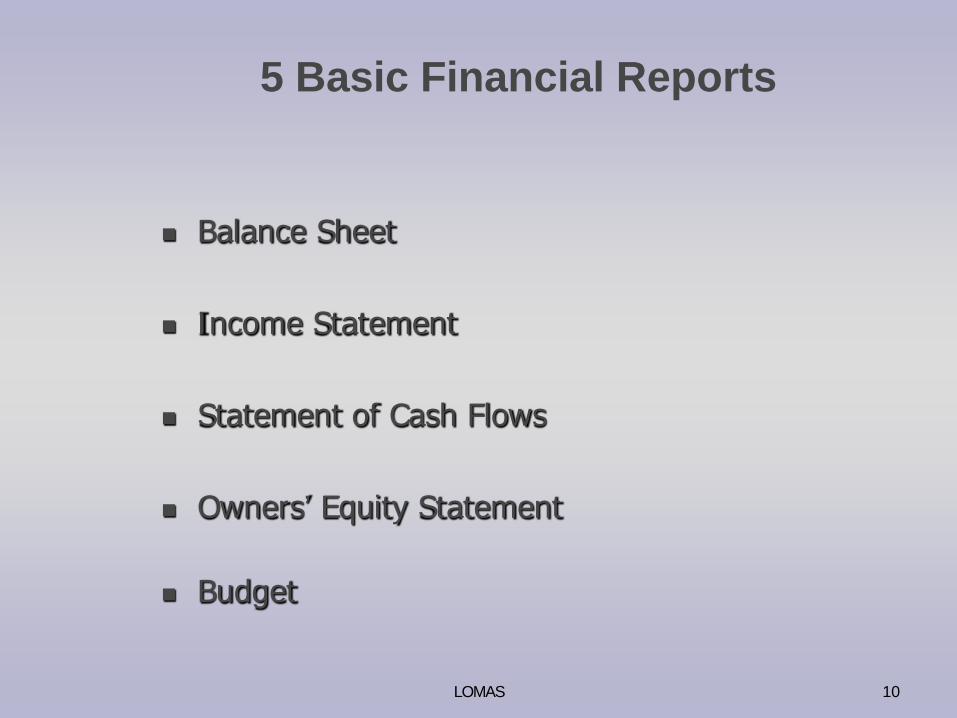

5 Basic Financial Reports

Balance Sheet

Income Statement

Statement of Cash Flows

Owners’ Equity Statement

Budget

10LOMAS

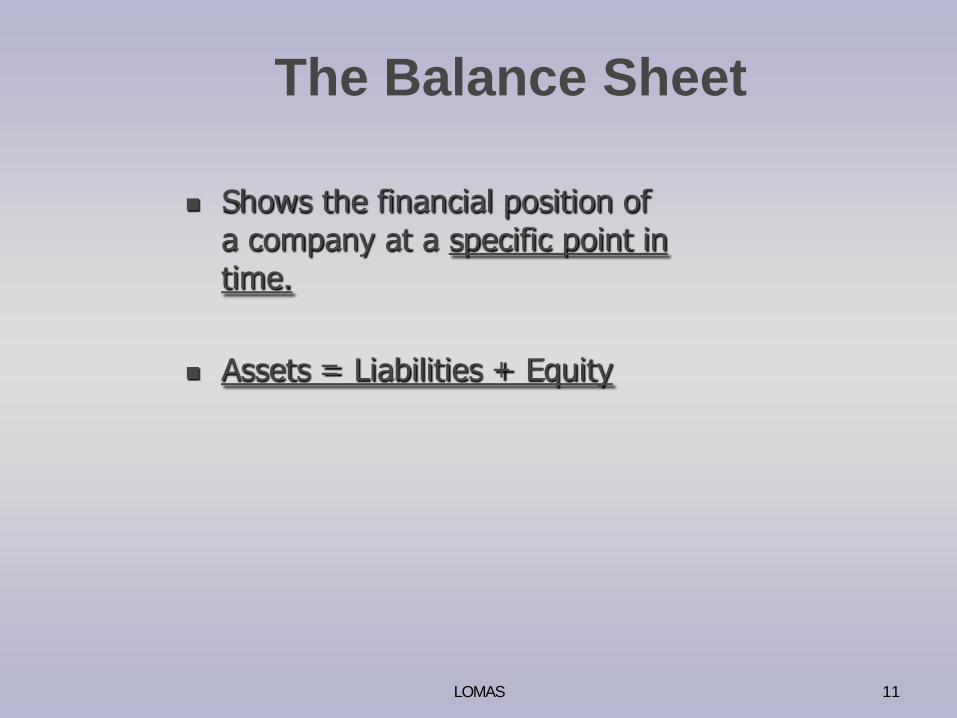

The Balance Sheet

Shows the financial position of a company at a specific point in time.

Assets = Liabilities + Equity

11LOMAS

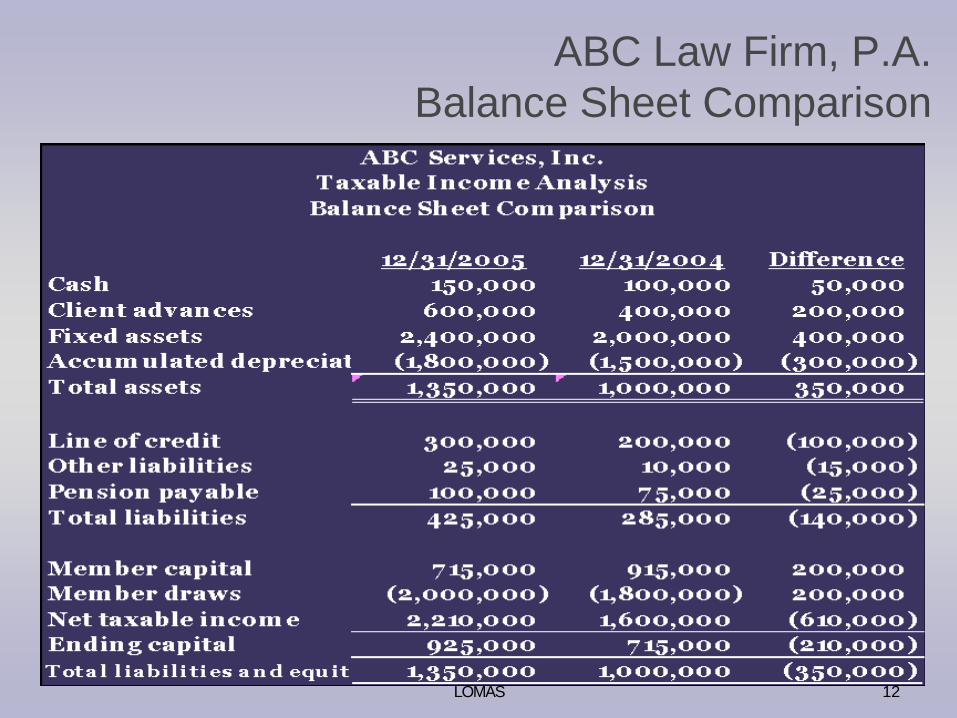

ABC Law Firm, P.A.Balance Sheet Comparison

12LOMAS

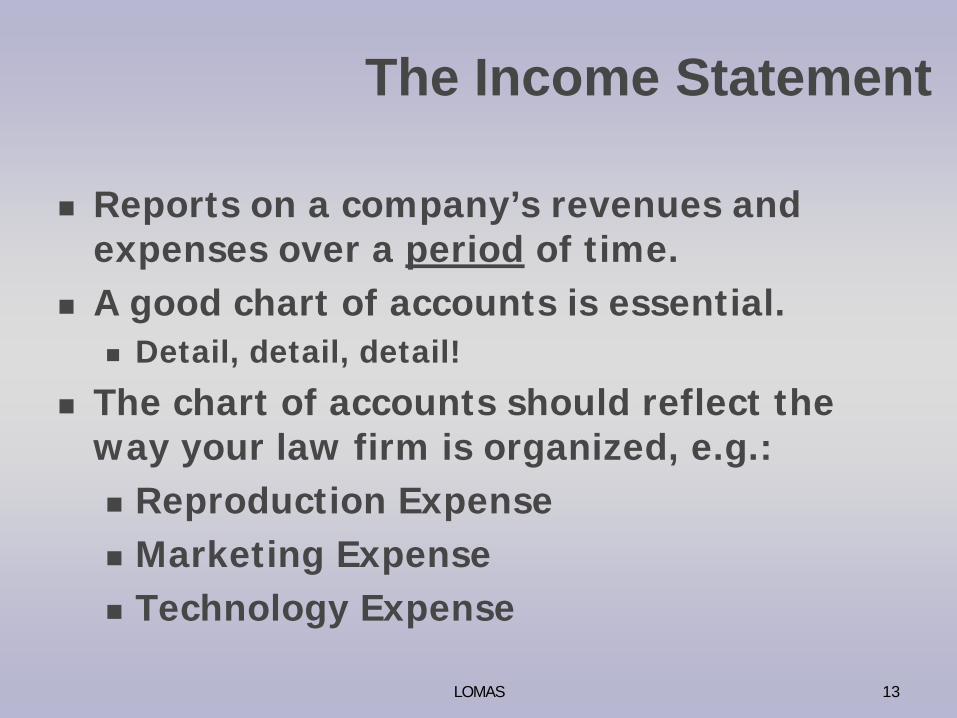

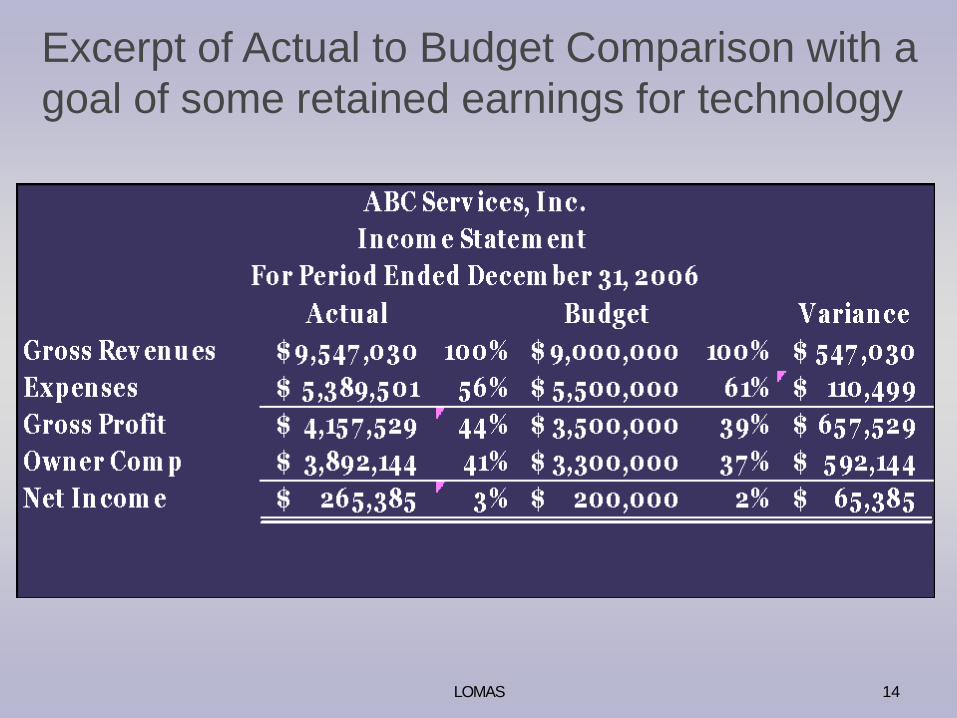

The Income Statement

Reports on a company’s revenues and expenses over a period of time.

A good chart of accounts is essential. Detail, detail, detail!

The chart of accounts should reflect the way your law firm is organized, e.g.: Reproduction Expense Marketing Expense Technology Expense

13LOMAS

Excerpt of Actual to Budget Comparison with a goal of some retained earnings for technology

14LOMAS

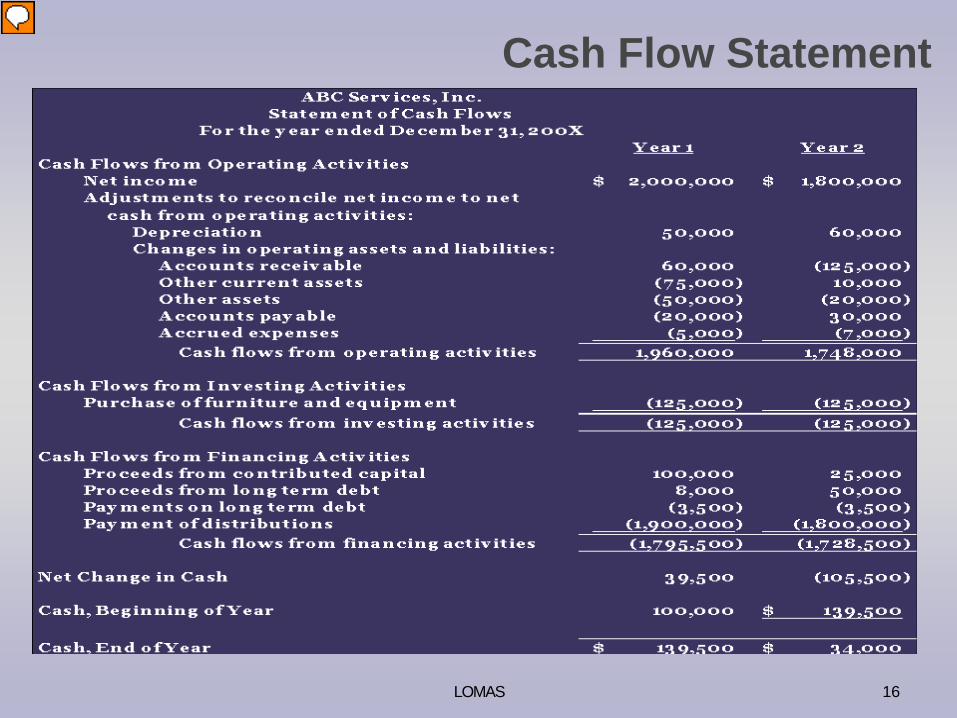

Reconciles net income to the change in cash by showing the sources and uses of cash.

Statement of Cash Flows

15LOMAS

Cash Flow Statement

16LOMAS

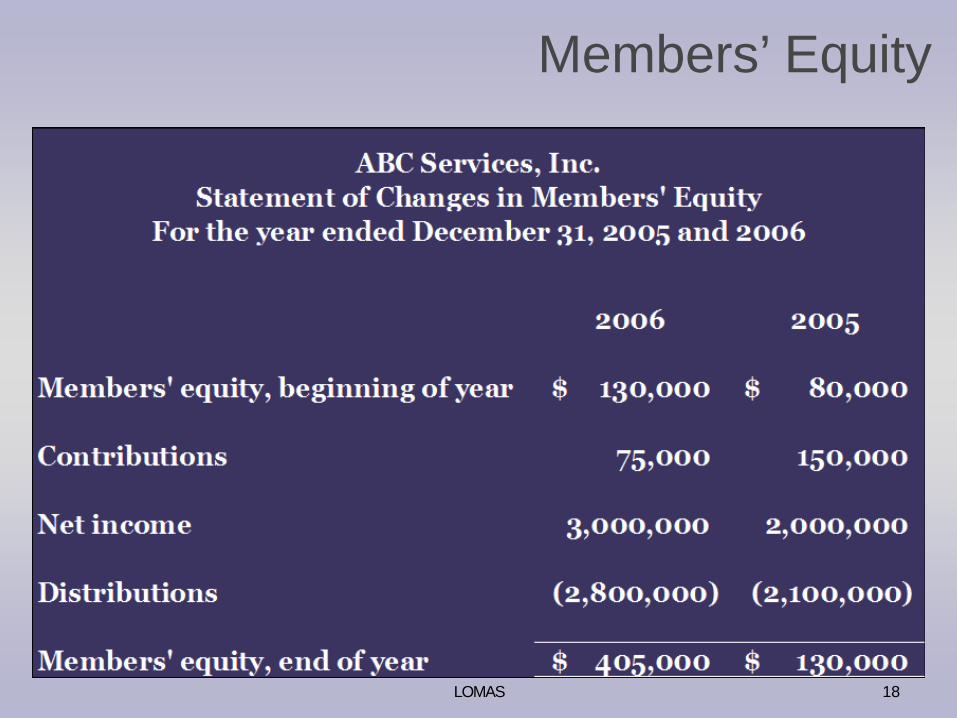

Owner’s Equity Statement

The owners’ equity statement outlines the changes in the owners’ equity accounts during the year.

17LOMAS

Members’ Equity

18LOMAS

Putting It All Together

19LOMAS

How Financial Statements Relate to Each Other

20LOMAS

Capitalization

21LOMAS

Capital required to:

Finance Salaries (secretary,

associate, paralegal)

Overhead (rent, utilities, supplies)

Equipment

Invest in New Markets

Why does a Firm need Capital?

22LOMAS

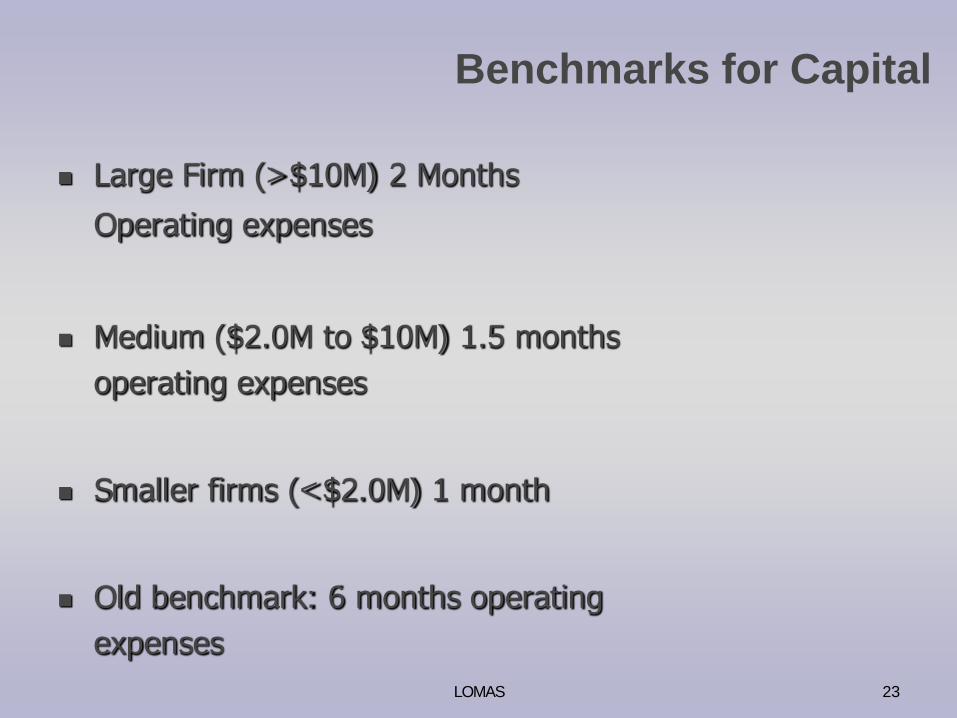

Benchmarks for Capital

Large Firm (>$10M) 2 Months

Operating expenses

Medium ($2.0M to $10M) 1.5 months operating expenses

Smaller firms (<$2.0M) 1 month

Old benchmark: 6 months operating expenses

23LOMAS

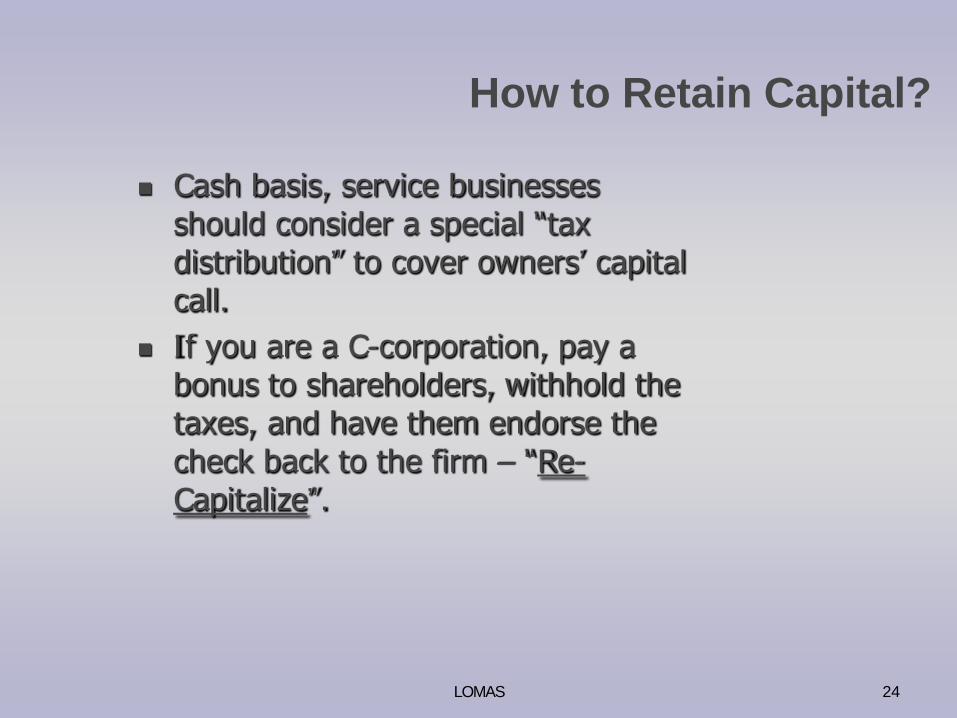

How to Retain Capital?

Cash basis, service businesses should consider a special “tax distribution” to cover owners’ capital call.

If you are a C-corporation, pay a bonus to shareholders, withhold the taxes, and have them endorse the check back to the firm – “Re-Capitalize”.

24LOMAS

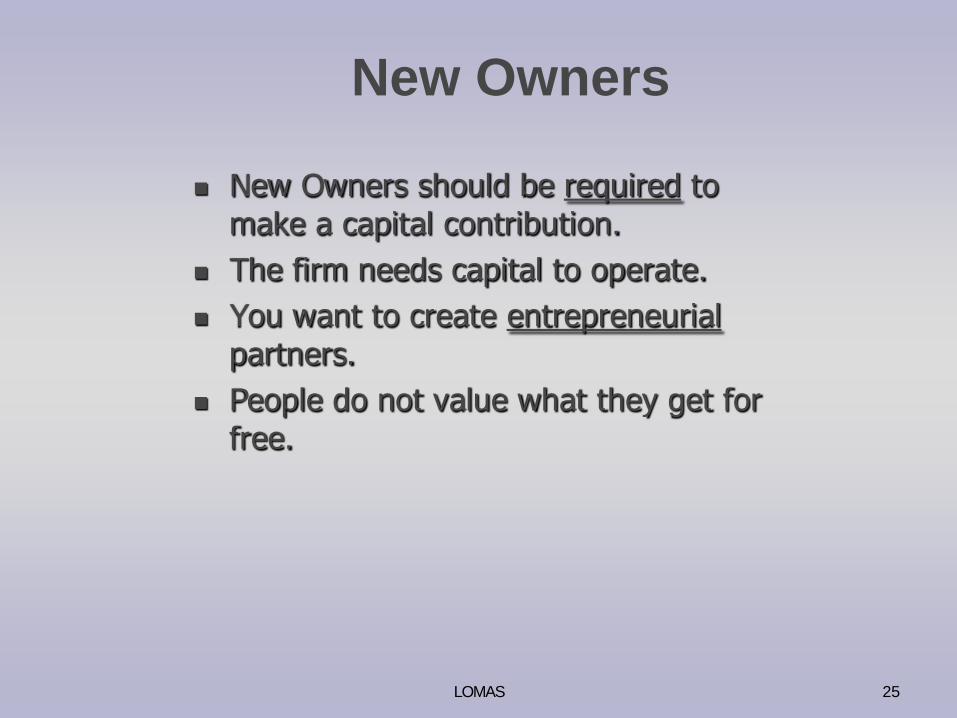

New Owners

New Owners should be required to make a capital contribution.

The firm needs capital to operate. You want to create entrepreneurial

partners. People do not value what they get for

free.

25LOMAS

Compensation

26LOMAS

Compensation

One of the most critical elements in a any business

Drives behavior “You Get What You Reward.”

Must be perceived as fair by the professionals and owners of the business

If key personnel are all mildly dissatisfied with the compensation system, it’s damn near perfect.

27LOMAS

Objective Factors

Origination (Finder)

Manager (Minder)

Producer (Grinder)

Class – Employee Category?

Seniority?

28LOMAS

Subjective Factors

Leadership (or setting a good example) Keeping clients happy Training/Mentoring others Marketing/Community Involvement Technical Skills How do you measure these items?

29LOMAS

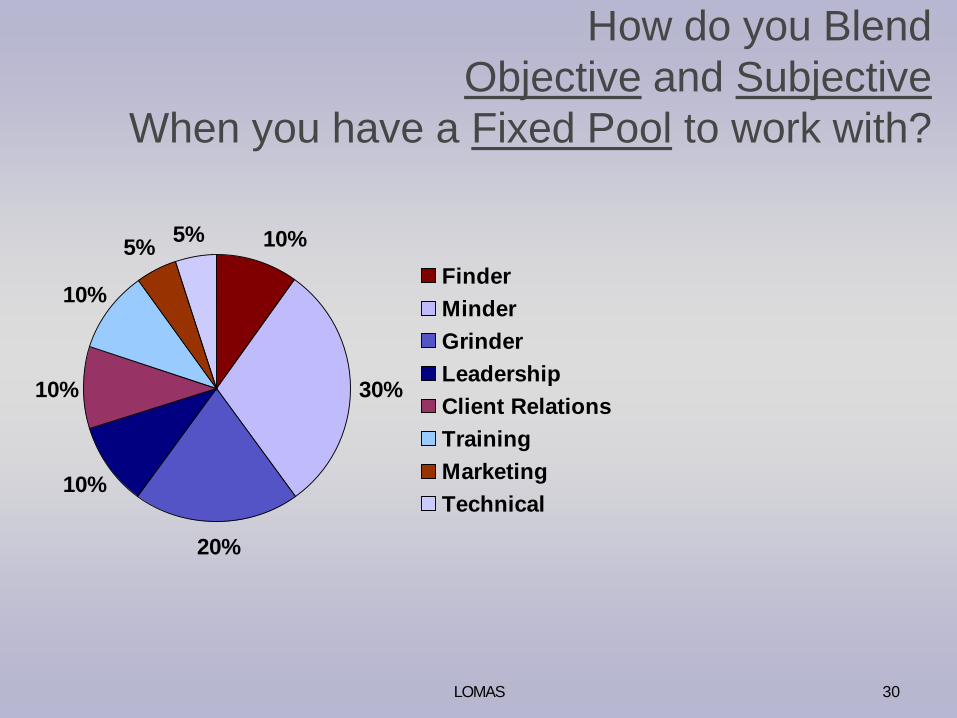

How do you Blend Objective and Subjective

When you have a Fixed Pool to work with?

10%

30%

20%

10%

10%

10%

5% 5%

FinderMinderGrinderLeadershipClient RelationsTrainingMarketingTechnical

30LOMAS

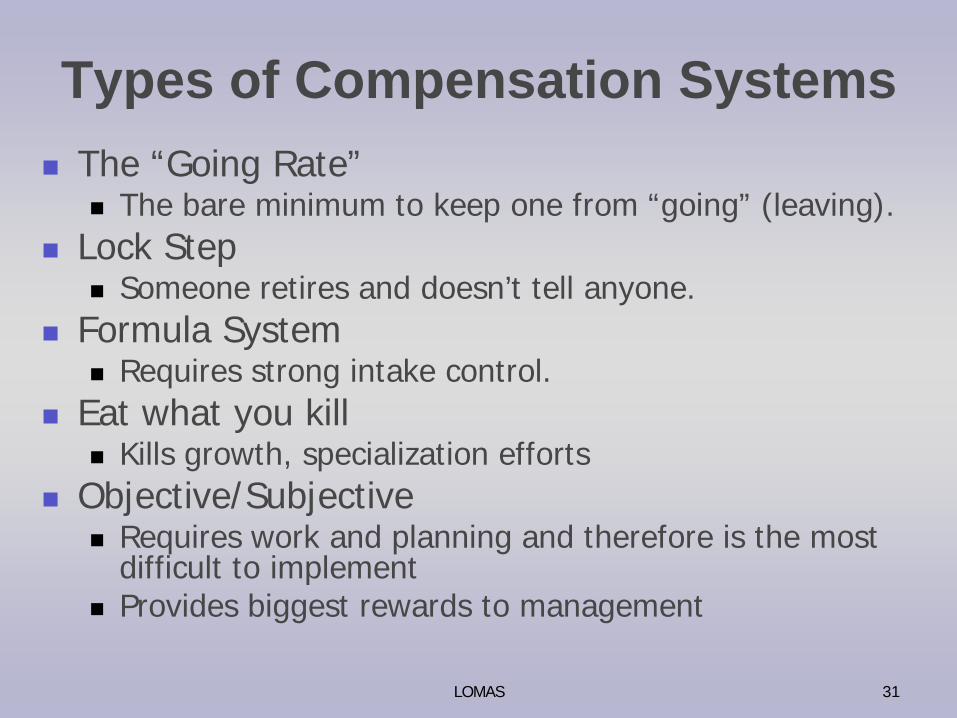

Types of Compensation Systems The “Going Rate”

The bare minimum to keep one from “going” (leaving). Lock Step

Someone retires and doesn’t tell anyone. Formula System

Requires strong intake control. Eat what you kill

Kills growth, specialization efforts Objective/Subjective

Requires work and planning and therefore is the most difficult to implement

Provides biggest rewards to management

31LOMAS

Reporting and Budgeting

32LOMAS

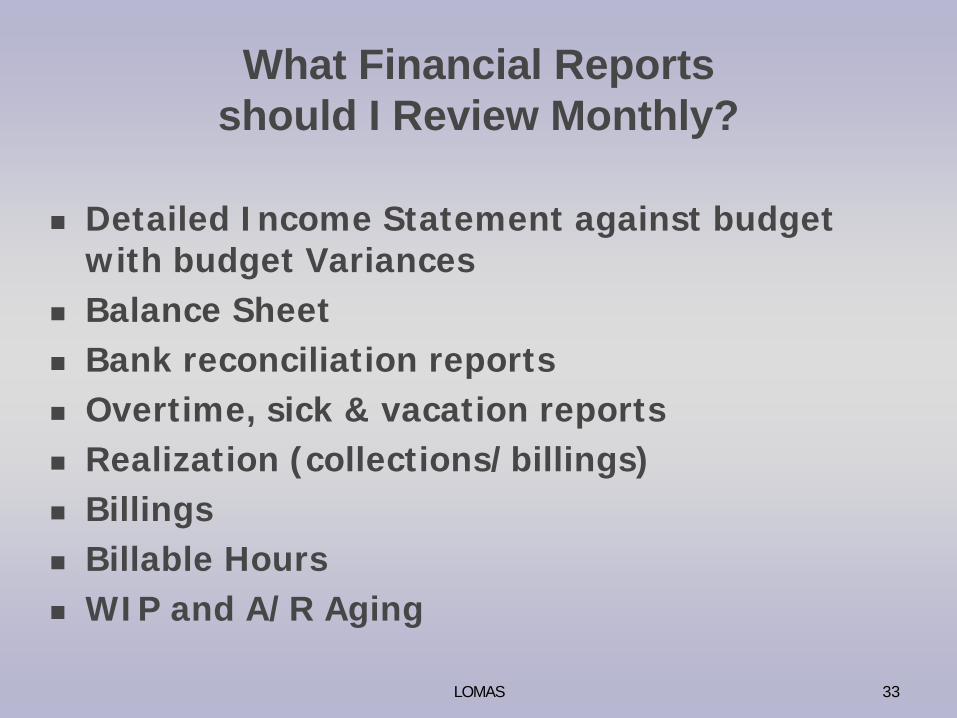

What Financial Reports should I Review Monthly?

Detailed Income Statement against budget with budget Variances

Balance Sheet Bank reconciliation reports Overtime, sick & vacation reports Realization (collections/billings) Billings Billable Hours WIP and A/R Aging

33LOMAS

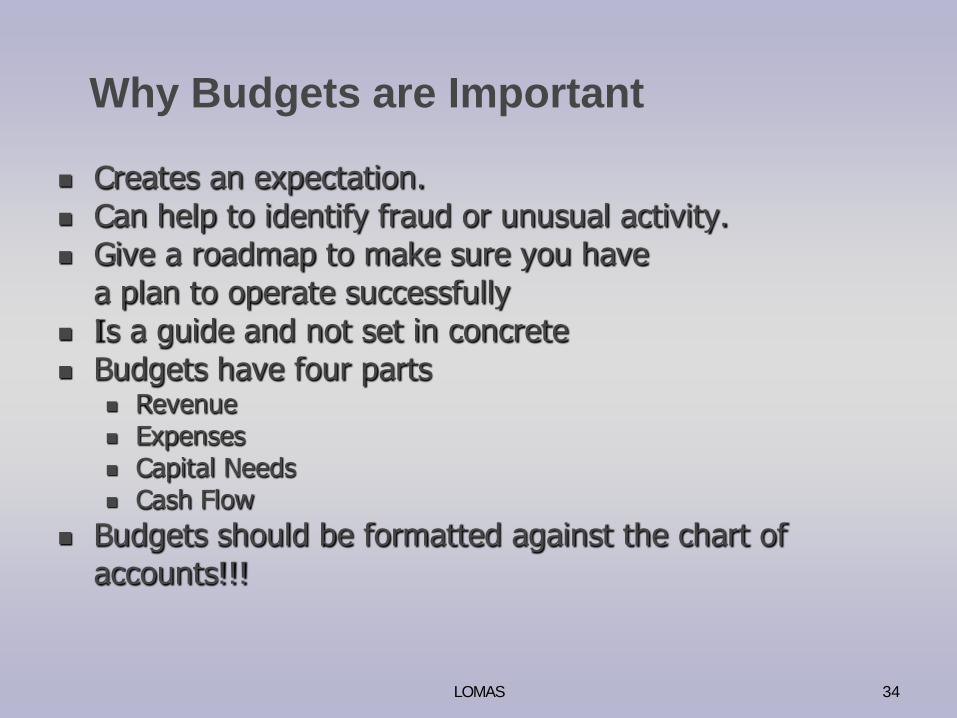

Why Budgets are Important

Creates an expectation. Can help to identify fraud or unusual activity. Give a roadmap to make sure you have

a plan to operate successfully Is a guide and not set in concrete Budgets have four parts

Revenue Expenses Capital Needs Cash Flow

Budgets should be formatted against the chart of accounts!!!

34LOMAS

Income Statement vs. Budget Income statement should be reported with several

columns of information. This may require special programming to your software Actual expense for the month Actual expense YTD Budget allocation YTD Over/under budget for this period: Variance of ‘Actual

Expense YTD’ against ‘Budget Allocation YTD’ (per cash flow budget)

Annual budget allocation Over/under budget: What has not been spent as a

percentage of the total budget

35LOMAS

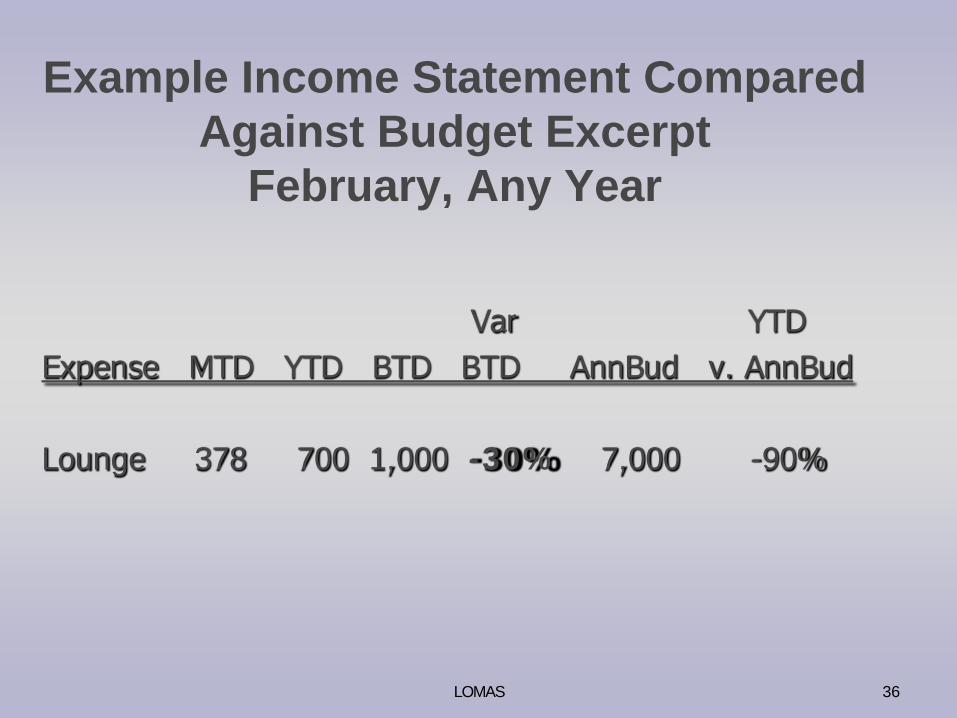

Example Income Statement Compared Against Budget Excerpt

February, Any Year

Var YTDExpense MTD YTD BTD BTD AnnBud v. AnnBud

Lounge 378 700 1,000 -30% 7,000 -90%

36LOMAS

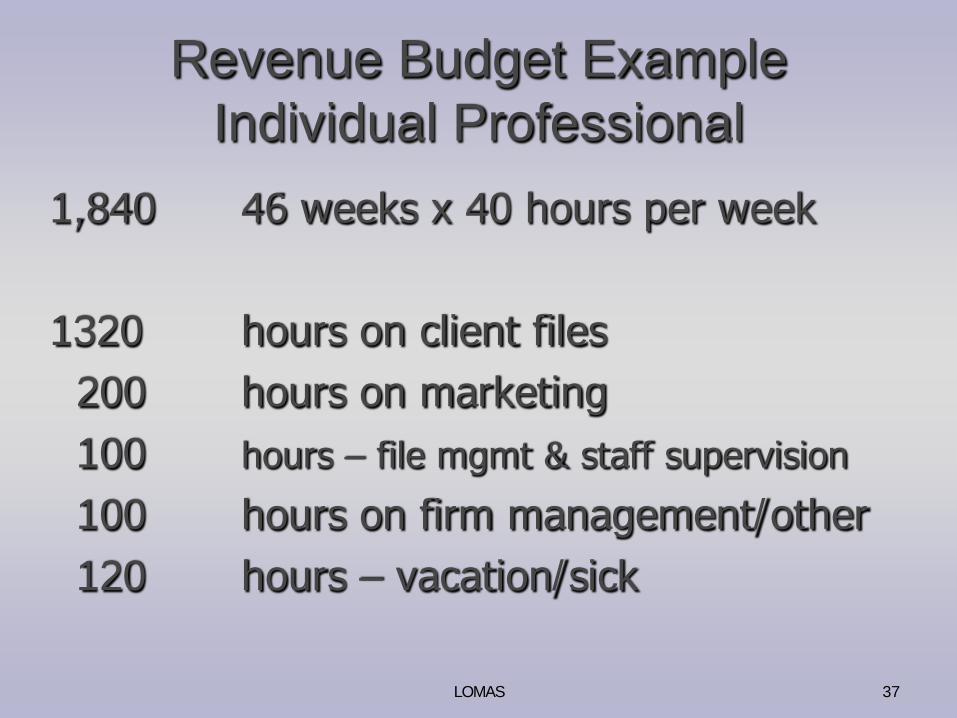

Revenue Budget ExampleIndividual Professional

1,840 46 weeks x 40 hours per week

1320 hours on client files200 hours on marketing100 hours – file mgmt & staff supervision

100 hours on firm management/other120 hours – vacation/sick

37LOMAS

Timekeeping

Why keep time? Productivity Profitability Record of the work

Client relations Risk management

Billing

38LOMAS

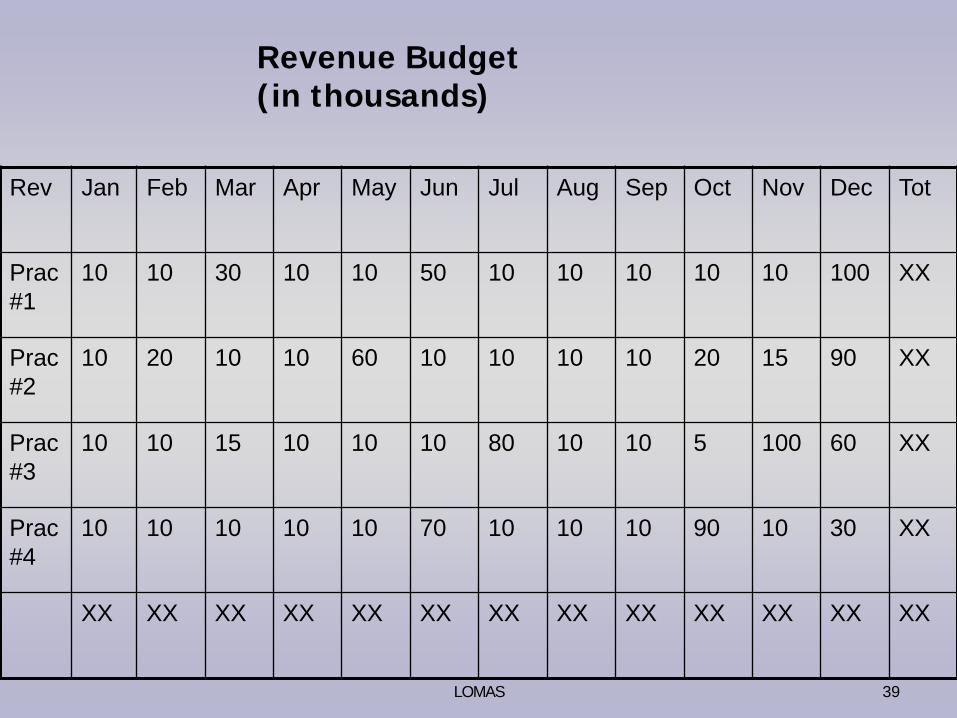

Rev Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Tot

Prac#1

10 10 30 10 10 50 10 10 10 10 10 100 XX

Prac#2

10 20 10 10 60 10 10 10 10 20 15 90 XX

Prac#3

10 10 15 10 10 10 80 10 10 5 100 60 XX

Prac#4

10 10 10 10 10 70 10 10 10 90 10 30 XX

XX XX XX XX XX XX XX XX XX XX XX XX XX

Revenue Budget(in thousands)

39LOMAS

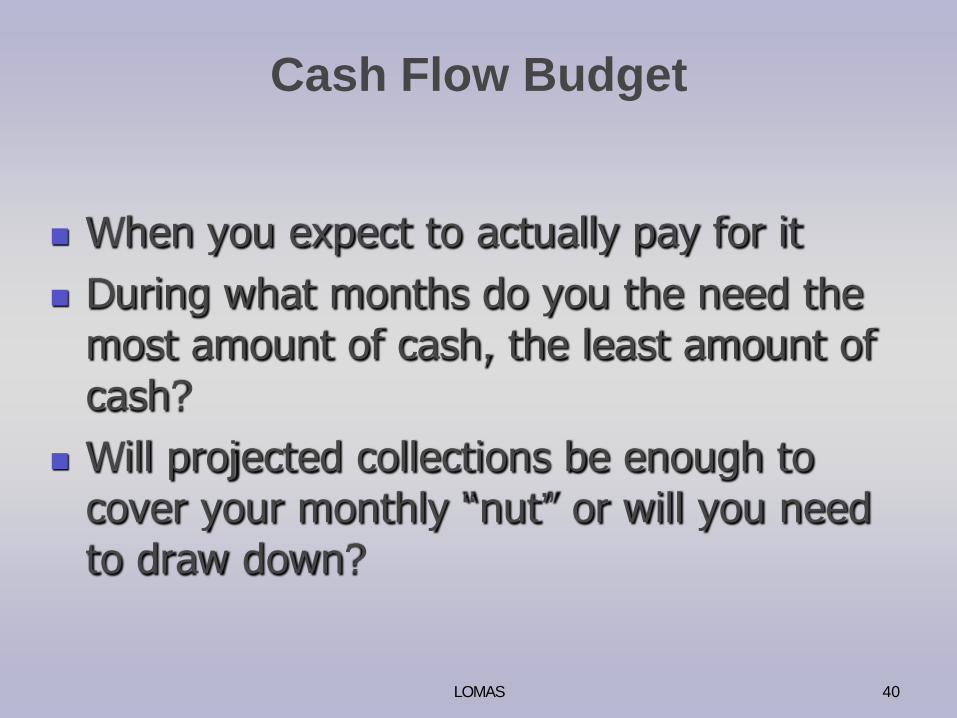

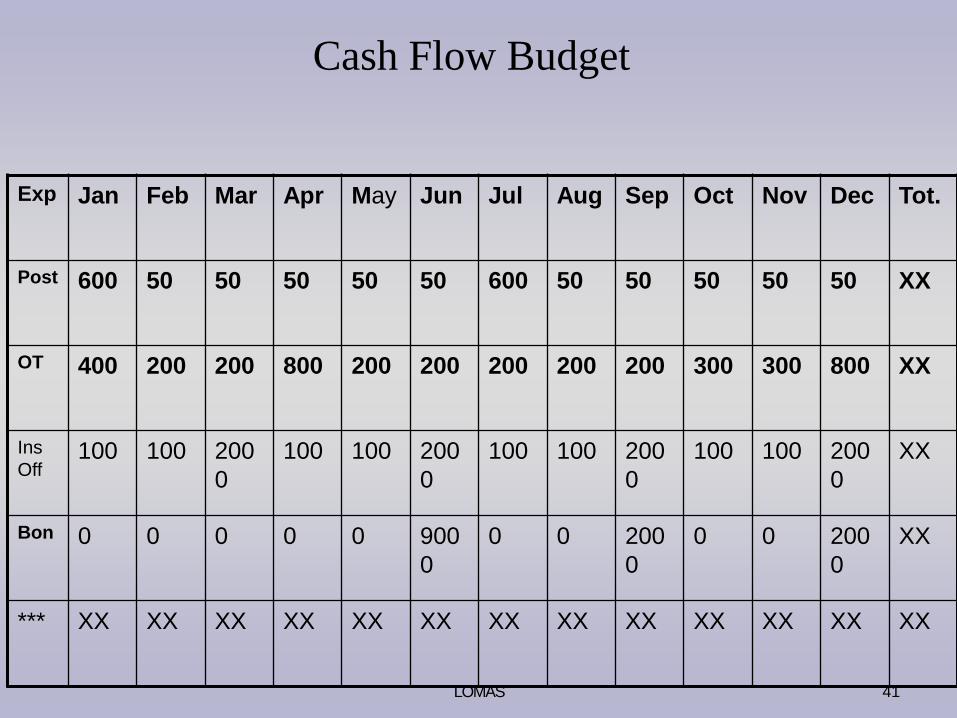

Cash Flow Budget

When you expect to actually pay for it During what months do you the need the

most amount of cash, the least amount of cash?

Will projected collections be enough to cover your monthly “nut” or will you need to draw down?

40LOMAS

Exp Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Tot.

Post 600 50 50 50 50 50 600 50 50 50 50 50 XX

OT 400 200 200 800 200 200 200 200 200 300 300 800 XX

InsOff

100 100 2000

100 100 2000

100 100 2000

100 100 2000

XX

Bon 0 0 0 0 0 9000

0 0 2000

0 0 2000

XX

*** XX XX XX XX XX XX XX XX XX XX XX XX XX

Cash Flow Budget

41LOMAS

Accounts Receivable and Work In ProcessThe Elephant in the Room

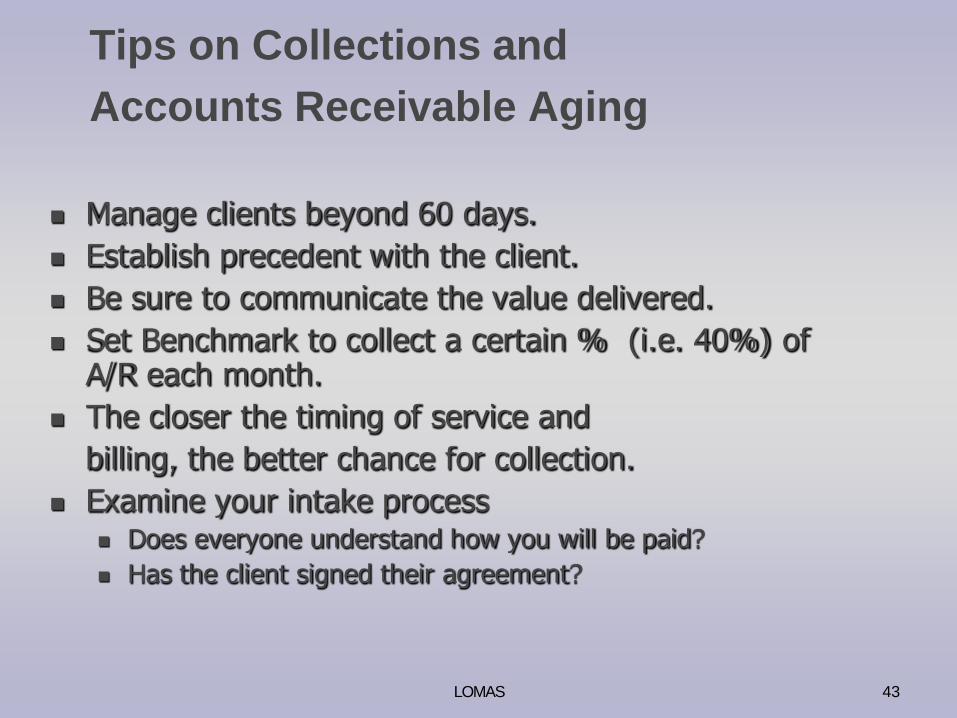

Tips on Collections and Accounts Receivable Aging

Manage clients beyond 60 days. Establish precedent with the client. Be sure to communicate the value delivered. Set Benchmark to collect a certain % (i.e. 40%) of

A/R each month. The closer the timing of service and

billing, the better chance for collection. Examine your intake process

Does everyone understand how you will be paid? Has the client signed their agreement?

43LOMAS

Establish a policy of frequently billing. Money held in WIP is costing the firm money, it has

already paid the salary and supply cost of creating the WIP, but is not enjoying the revenue.

Work to improve your current percentages over 30 days.

Just because it’s WIP does NOT mean it doesn’t have to be reviewed every month Good WIP vs. Bad WIP

Work in Process Aging

44LOMAS

Financial ToolboxOther critical reports

45LOMAS

Reports are Tools

You can have too many tools! Appropriate reports What criteria to include? A large percentage of the population is visual, and

graphs are easier to interpret for them. Not all FM software can do this The Daily/Weekly Report

Critical for start-ups

46LOMAS

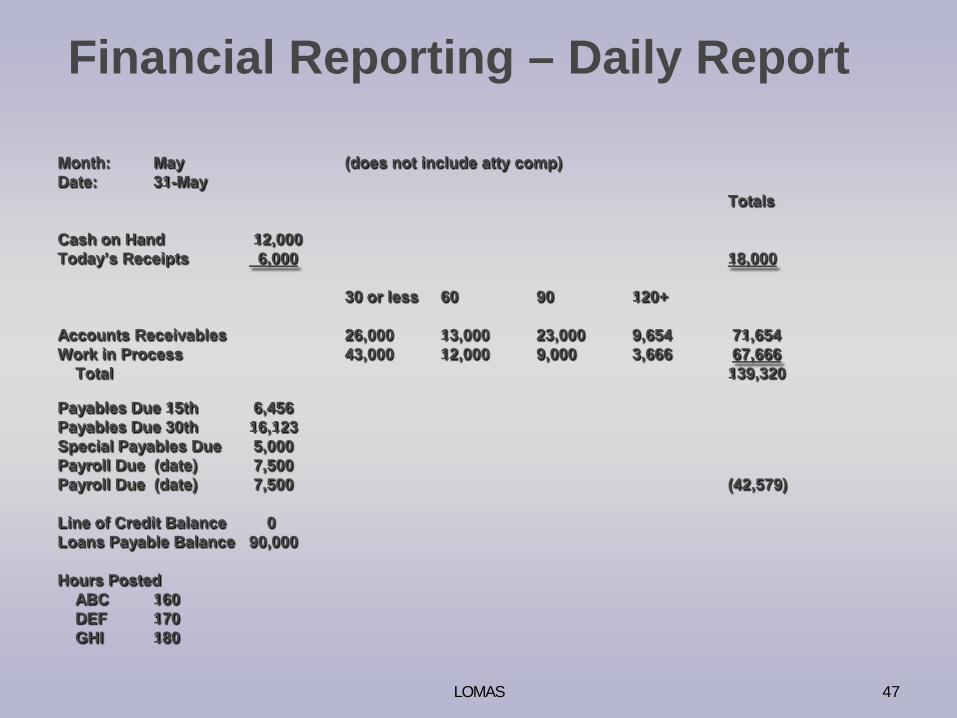

Financial Reporting – Daily Report

Month: May (does not include atty comp)Date: 31-May

Totals

Cash on Hand 12,000Today’s Receipts 6,000 18,000

30 or less 60 90 120+

Accounts Receivables 26,000 13,000 23,000 9,654 71,654Work in Process 43,000 12,000 9,000 3,666 67,666

Total 139,320

Payables Due 15th 6,456Payables Due 30th 16,123Special Payables Due 5,000Payroll Due (date) 7,500Payroll Due (date) 7,500 (42,579)

Line of Credit Balance 0Loans Payable Balance 90,000

Hours PostedABC 160DEF 170GHI 180

47LOMAS

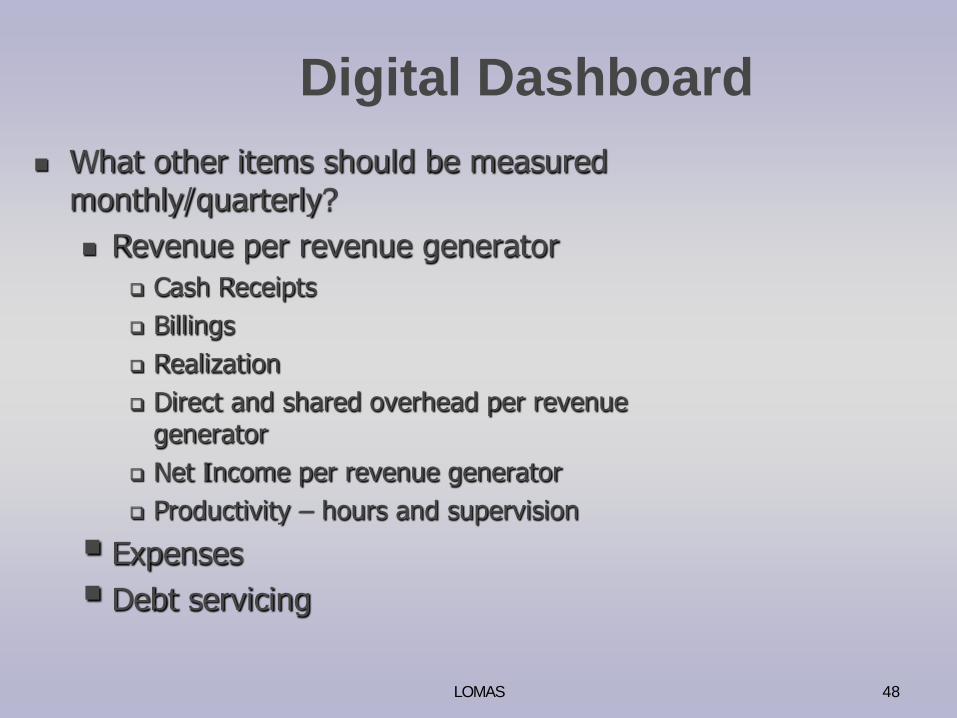

Digital Dashboard What other items should be measured

monthly/quarterly? Revenue per revenue generator

Cash Receipts Billings Realization Direct and shared overhead per revenue

generator Net Income per revenue generator Productivity – hours and supervision

Expenses Debt servicing

48LOMAS

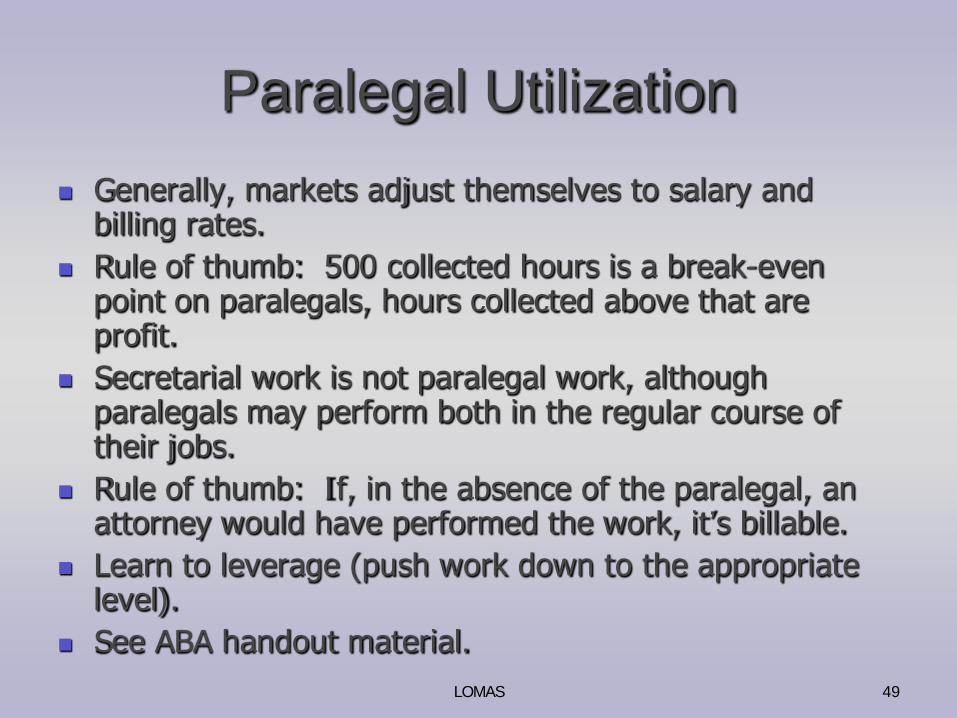

Paralegal Utilization Generally, markets adjust themselves to salary and

billing rates. Rule of thumb: 500 collected hours is a break-even

point on paralegals, hours collected above that are profit.

Secretarial work is not paralegal work, although paralegals may perform both in the regular course of their jobs.

Rule of thumb: If, in the absence of the paralegal, an attorney would have performed the work, it’s billable.

Learn to leverage (push work down to the appropriate level).

See ABA handout material.49LOMAS

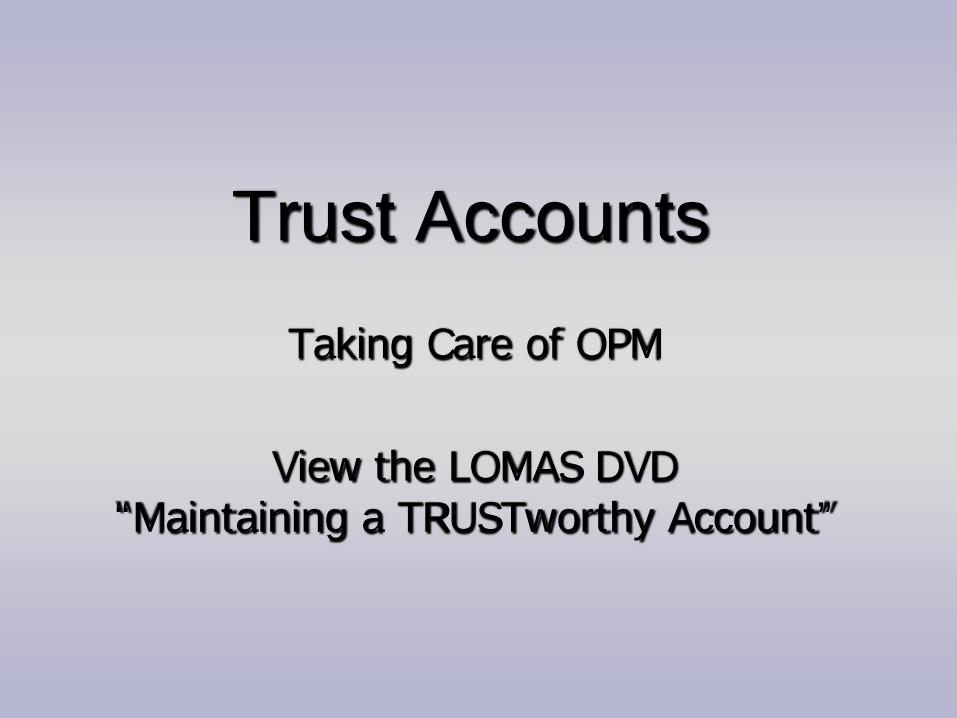

Trust AccountsTaking Care of OPM

View the LOMAS DVD “Maintaining a TRUSTworthy Account”

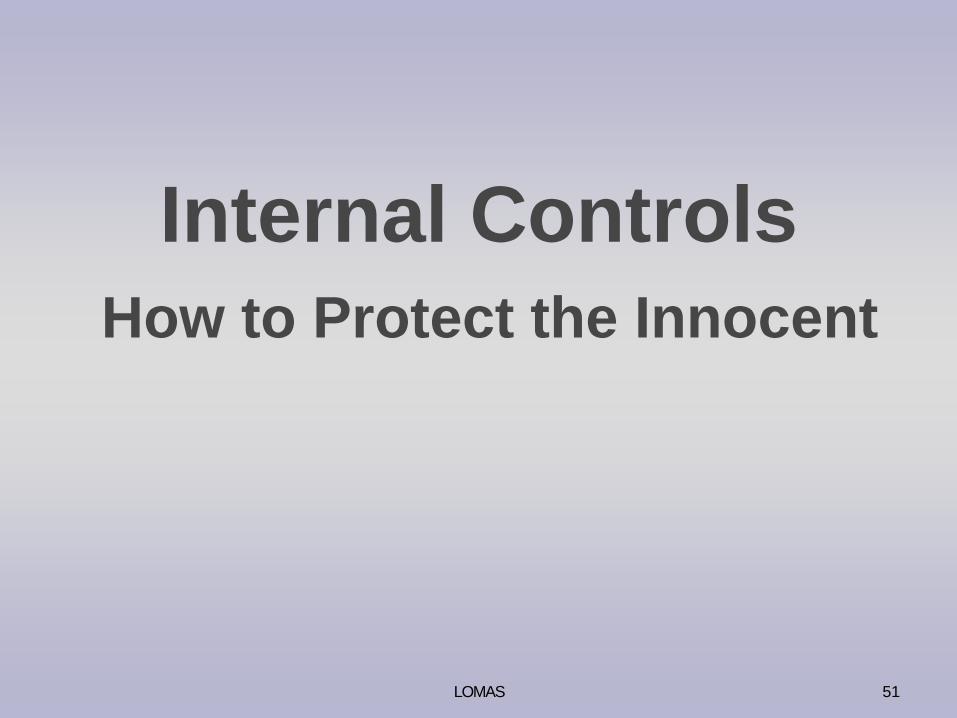

Internal ControlsHow to Protect the Innocent

51LOMAS

Initiation

Authorization

Processing

Recording

A goal of this element of internal control is segregation of duty, including:

Control Policies & Procedures

52LOMAS

Theft of daily deposit

Obtaining computer passwords

Wire transfers

Checks written for personal expenditures

Counterfeit checks

Stolen checks

Staff too chummy with banking personnel

Beware of QuickBooks

Common Fraud Schemes:

Operating & Trust Bank Accounts

53LOMAS

False write downs and write offs

Kickbacks from vendors (client costs advanced)

Unauthorized use of the house charge accounts

Check is written for personal use and posted as something else to the client account

Holding trust money with no documented purpose

Common Fraud Schemes:

Costs Advanced, Accounts Receivable, Fees, and Trust Receipts

54LOMAS

Kickbacks from vendors (operating expenses)

False or inflated vendor invoices

Office purchases on personal credit cards

Excess purchase schemes

Duplicate payment schemes

Common Fraud Schemes:

Accounts Payable, Purchases, & Trust Expenditures

55LOMAS

Ghost Employee

Special projects employee

Overpayment Schemes, overpaying hours

Double payment of Payroll to an Employee

Diverting withholding from payroll checks

Expense report fraud

“Working through lunch”

Common Fraud Schemes:

Payroll & Benefits

56LOMAS

Segregation of Duties

Read General Ledger entries

Budget vs. Actual Comparisons

Watch Fixed Assets and watch for assets that were “expensed.”

Regularly Rotate Duties and Cross-Train

Inventory control

Standard supply inventory and ordering control

Key Control Policies & Procedures

57LOMAS

• Know Your People

• Watch for lack of vacations

• Extravagant Lifestyles

• Open the Bank Statements and review cancelled checks

• Depreciation schedules are NOT inventories

What to Watch For

58LOMAS

Questions?

LOMAS has answers

The Florida Bar’sLaw Office Management Assistance Service

(LOMAS)

www.floridabar.org/lomas

PMA Email:

59LOMAS