Embed Size (px)

Citation preview

Issue 26, December 2015 | Singapore

Board MattersQuarterly

1Year-end mattersfor the auditcommittee

Issues for the auditcommittee to consider

28Malaysia Budget2016

14ACRA’s FinancialReportingSurveillanceProgramme

21ACRA’s AuditQuality IndicatorsDisclosureFramework

24Regulatory updates

EditorialToday’s audit committees play a significant role in corporate governance to maintain stakeholderconfidence. Audit committee members face a range of new challenges as they are tasked with criticaloversight of the complexities of financial reporting, regulatory compliance and risk management.

This issue of Board Matters Quarterly is dedicated to help audit committees identify and prepare for keyfinancial reporting considerations that their companies may face.

We highlight the key findings from the Accounting and Corporate Regulatory Authority’s (ACRA)inaugural report on the key findings on selected financial statements of listed companies with financialyear ended between 1 January 2013 and 31 December 2013 under its Financial Reporting SurveillanceProgramme, and the focus areas for FY2015 financial statements review.

We also take a look at ACRA’s Audit Quality Indicator (AQI) Disclosure Framework, the first of its kind tobe rolled out in this region. The AQI Framework comprises eight comparable quality markers thatcorrelate closely with audit quality based on ACRA’s observations from inspecting auditors over the pastdecade. These include hours spent by senior audit team members involved in the audit, relevantexperience of the senior audit team members and results from internal and external inspections ofauditors. The framework is available for voluntary adoption by audit committees of all listed entities inSingapore from 1 January 2016.

We hope you find Board Matters Quarterly useful, and share it with others. If you have feedback or ideasfor future issues, please contact us at [email protected].

Tan Seng Choon

Assurance Partner and Professional Practice Director

Ernst & Young LLP

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 1

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 2

Year-end matters forthe audit committeeIssues for the audit committee to consider

Audit committees (AC) continue toface significant challenges inoverseeing their companies'compliance with financial reporting,legal and regulatory requirements.

This article is designed to help ACmembers prepare for their upcomingdiscussions with the management andindependent auditors. We also pose aseries of questions for the AC toconsider and provide links to additionalinformation.

Inside:1. Financial reporting

► Fair value measurements► Impairment assessments► Going concern considerations

2. Regulatory developments► Companies (Amendment) Act► ACRA’s FRSP► SGX listing rule changes on poll

voting and disclosure of voteoutcomes

► SGX reviewing companies’compliance with Code CorporateGovernance

► SGX to mandate SustainabilityReporting in 2017

3. Risk management► Fraud risk► Cybersecurity preparedness► Enterprise risk management

4. Audit regulatory initiatives► Enhancing the auditor’s report► ACRA’s AQI Disclosure Framework

5. Tax developments and tax risk► IRAS’s 2015 Singapore Transfer

Pricing Guidelines► Income tax accounting► Managing tax controversies

6. Working with the internal auditor

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 3

1. Financial reporting

Over the last few years, we have seen significant changes anddevelopments on the accounting front with many new financial reportingstandards issued and coming into effect. It was evident based on feedbackgathered, that considerable amount of time and effort were invested onthe implementation of the new standards in 2014.

The AC should be comforted to know that there will be a slight reprieve inFY2015 given that there are very limited new amendments to accountingstandards that will be effective for annual periods beginning on or after 1January 2015. This same “period of calm” will be accorded in 2016 aswell. The next big wave of accounting changes relating to revenuerecognition, financial instruments, and IFRS Convergence come into effectin 2018. These topics will be further explored in upcoming issues of thispublication.

For entities with annual periods beginning on or after 1 July 2014, twoseries of Improvements to Financial Reporting Standards, issued inJanuary and February 2014 and a limited amendment to FRS 19Employment Benefits pertaining to employees’ contributions to definedbenefit plans will be effective. Both Improvements to Financial ReportingStandards contain narrow scope amendments made to a series of FinancialReporting Standards.

While the period of calm does offer a brief respite, we see this as a goodopportunity for the AC to realign its priorities and focus on the other keyareas of emphasis in their organisation. This is especially pertinent in thewake of the challenging economic environment. We highlight three keyareas in the following pages which we believe should be the areas of focusby the AC for the current year-end financial reporting.

The AC needs to understand and assess the quality, not just the acceptability, of critical accounting policies,judgments, and estimates. The AC should also be mindful that the increased focus on transparency in financialreporting as well as disclosures is always present.

The areas of focus for reviews of financial statements issued under the Financial Reporting Practical GuidanceNo. 2 of 2015 by ACRA serve as a good guidance. The Practice Guidance is discussed in more detail in article“ACRA’s Financial Reporting Surveillance Programme” in this issue.

The AC should becomforted to know thatthere will be a slightreprieve in FY2015 giventhat there are verylimited new amendmentsto accounting standardsthat will be effective forannual periods beginningon or after 1 January2015.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 4

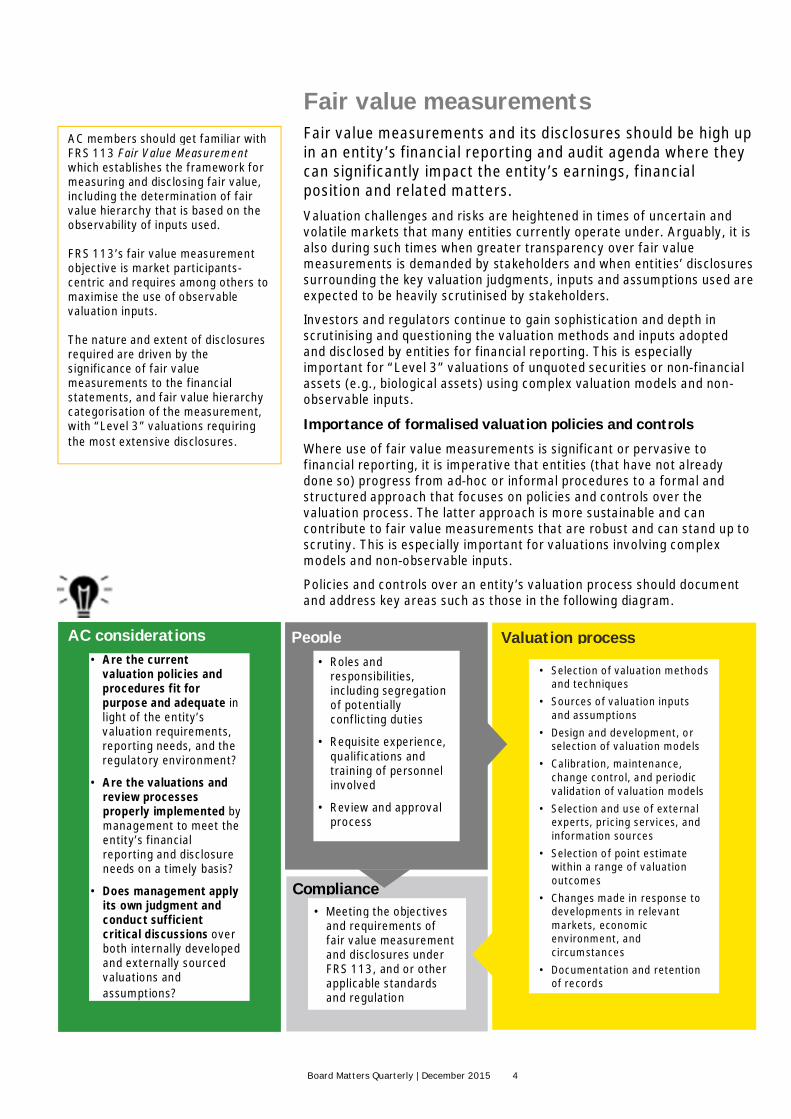

Fair value measurementsFair value measurements and its disclosures should be high upin an entity’s financial reporting and audit agenda where theycan significantly impact the entity’s earnings, financialposition and related matters.).Valuation challenges and risks are heightened in times of uncertain andvolatile markets that many entities currently operate under. Arguably, it isalso during such times when greater transparency over fair valuemeasurements is demanded by stakeholders and when entities’ disclosuressurrounding the key valuation judgments, inputs and assumptions used areexpected to be heavily scrutinised by stakeholders.

Investors and regulators continue to gain sophistication and depth inscrutinising and questioning the valuation methods and inputs adoptedand disclosed by entities for financial reporting. This is especiallyimportant for “Level 3” valuations of unquoted securities or non-financialassets (e.g., biological assets) using complex valuation models and non-observable inputs.

Importance of formalised valuation policies and controls

Where use of fair value measurements is significant or pervasive tofinancial reporting, it is imperative that entities (that have not alreadydone so) progress from ad-hoc or informal procedures to a formal andstructured approach that focuses on policies and controls over thevaluation process. The latter approach is more sustainable and cancontribute to fair value measurements that are robust and can stand up toscrutiny. This is especially important for valuations involving complexmodels and non-observable inputs.

Policies and controls over an entity’s valuation process should documentand address key areas such as those in the following diagram.

AC members should get familiar withFRS 113 Fair Value Measurementwhich establishes the framework formeasuring and disclosing fair value,including the determination of fairvalue hierarchy that is based on theobservability of inputs used.

FRS 113’s fair value measurementobjective is market participants-centric and requires among others tomaximise the use of observablevaluation inputs.

The nature and extent of disclosuresrequired are driven by thesignificance of fair valuemeasurements to the financialstatements, and fair value hierarchycategorisation of the measurement,with “Level 3” valuations requiringthe most extensive disclosures.

• Roles andresponsibilities,including segregationof potentiallyconflicting duties

• Requisite experience,qualifications andtraining of personnelinvolved

• Review and approvalprocess

Valuation processPeople

Compliance• Meeting the objectives

and requirements offair value measurementand disclosures underFRS 113, and or otherapplicable standardsand regulation

• Selection of valuation methodsand techniques

• Sources of valuation inputsand assumptions

• Design and development, orselection of valuation models

• Calibration, maintenance,change control, and periodicvalidation of valuation models

• Selection and use of externalexperts, pricing services, andinformation sources

• Selection of point estimatewithin a range of valuationoutcomes

• Changes made in response todevelopments in relevantmarkets, economicenvironment, andcircumstances

• Documentation and retentionof records

• Are the currentvaluation policies andprocedures fit forpurpose and adequate inlight of the entity’svaluation requirements,reporting needs, and theregulatory environment?

• Are the valuations andreview processesproperly implemented bymanagement to meet theentity’s financialreporting and disclosureneeds on a timely basis?

• Does management applyits own judgment andconduct sufficientcritical discussions overboth internally developedand externally sourcedvaluations andassumptions?

AC considerations

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 5

Impairment assessmentsAs part of financial close, all assets on an entity’s balance sheet that arenot measured at fair value through earnings such as goodwill, intangibles,fixed assets, receivables, and available-for-sale equity investments, needto be assessed for any possible impairment that would require therecognition of losses. Entities are also required to assess whether priorimpairment write-downs of assets other than goodwill have reversed in thecurrent period and should be written back.

Depending on the applicable accounting standards and presence ofimpairment indicators or evidence, a variety of quantitative assessmentsthat rely on the management’s judgments and estimates regarding theassets’ future recoverability may be required.

The impairment assessment of long-lived assets such as goodwill andintangibles using discounted cash flows has often been cited by themanagement as challenging areas of financial reporting. Furthermore,consideration of whether decline in fair value of available-for-sale equityinvestments such as quoted shares is “significant or prolonged”, whichwould require recognition of impairment loss has traditionally been a veryjudgmental and contentious area of financial reporting.

Significant impairment write-downs of long-term capital assets often carryramifications to stakeholders’ confidence on the entity. To buildconfidence with investors, analysts, lenders and regulators, entities needto put in place a robust and integrated impairment assessment andcommunication process.

The AC should consider whether the entity’s current impairmentassessment and communication process already incorporates leadingpractices summarised in the following page.

Going concern considerationsGoing concern considerations may continue to be an issue forsome entities, and AC should maintain close scrutiny of thesituation.Liquidity is a key consideration in assessing an entity’s ability to continueas a going concern. The factors that the AC may consider in its assessmentinclude cash flow forecasts, capital management requirements, debtrepayment, regulatory or contractual restrictions on cash funding. The ACshould also robustly challenge the reasonableness of the assumptions usedby the management in the cash flow forecast, and revalidating the entity’sability to meet debt servicing requirements and debt covenants.

FRS 1 Presentation of Financial Statements requires disclosure of materialuncertainties relating to events or conditions that may cast doubts on theentity’s ability to continue as a going concern. The AC should endeavour todevote more attention on the disclosures should there be materialuncertainties. Even if the management concludes that there is no concernon the going concern assumption, FRS 1 still requires the disclosure of thesignificant judgement made in concluding that there remain no materialuncertainties.

Corporate regulators regardimpairment analyses and disclosureson non-financial assets as one oftheir priority focus areas in theirsurveillance of corporate financialreporting.

The sluggish global economies andfragile business confidence areexpected to draw spotlight on theassessment of impairment for non-financial assets in this coming year-end.

Entities’ accounting responses to theimpact of the current volatilemarkets, which include properreflection of current marketconditions in the assessment of assetimpairments, should be key focusareas of AC members.

Significant impairmentwrite-downs of long-termcapital assets often carryramifications tostakeholders’ confidenceon the entity.

AC considerations

► Where models were used toestimate the value of assetswhich must be tested forimpairment, is the AC satisfied bythe procedures adopted toestimate cash flows, and theappropriate adjustments made forrisks?

► Is the AC satisfied thatappropriate sensitivity analysishas been conducted to flexassumptions to identify howrobust the model outputs are inpractice, and that theassumptions are free from bias?

► Has the management consideredappropriately the potential impactof reasonably possible events?For instance, have relationshipswith third parties been reviewed?Has the potential of third-partydefaults been taken into account?

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 6

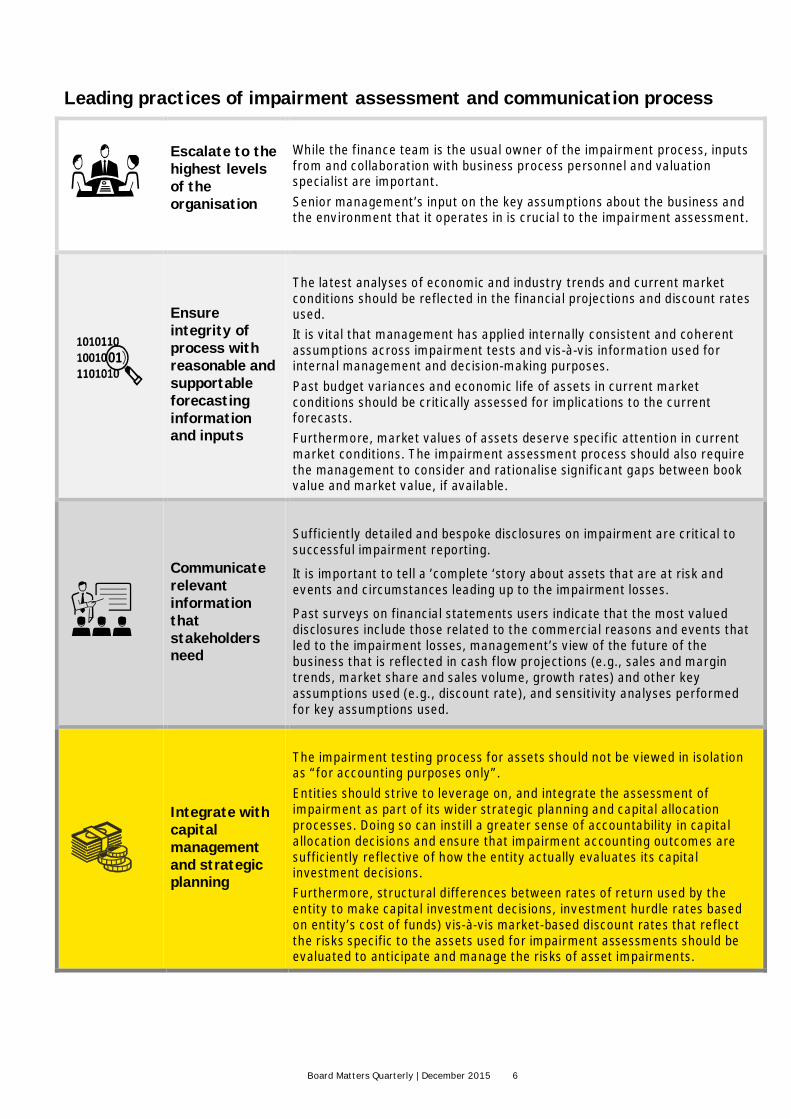

Leading practices of impairment assessment and communication process

Escalate to thehighest levelsof theorganisation

While the finance team is the usual owner of the impairment process, inputsfrom and collaboration with business process personnel and valuationspecialist are important.Senior management’s input on the key assumptions about the business andthe environment that it operates in is crucial to the impairment assessment.

Ensureintegrity ofprocess withreasonable andsupportableforecastinginformationand inputs

The latest analyses of economic and industry trends and current marketconditions should be reflected in the financial projections and discount ratesused.It is vital that management has applied internally consistent and coherentassumptions across impairment tests and vis-à-vis information used forinternal management and decision-making purposes.Past budget variances and economic life of assets in current marketconditions should be critically assessed for implications to the currentforecasts.Furthermore, market values of assets deserve specific attention in currentmarket conditions. The impairment assessment process should also requirethe management to consider and rationalise significant gaps between bookvalue and market value, if available.

Communicaterelevantinformationthatstakeholdersneed

Sufficiently detailed and bespoke disclosures on impairment are critical tosuccessful impairment reporting.

It is important to tell a ’complete ‘story about assets that are at risk andevents and circumstances leading up to the impairment losses.

Past surveys on financial statements users indicate that the most valueddisclosures include those related to the commercial reasons and events thatled to the impairment losses, management’s view of the future of thebusiness that is reflected in cash flow projections (e.g., sales and margintrends, market share and sales volume, growth rates) and other keyassumptions used (e.g., discount rate), and sensitivity analyses performedfor key assumptions used.

Integrate withcapitalmanagementand strategicplanning

The impairment testing process for assets should not be viewed in isolationas “for accounting purposes only”.Entities should strive to leverage on, and integrate the assessment ofimpairment as part of its wider strategic planning and capital allocationprocesses. Doing so can instill a greater sense of accountability in capitalallocation decisions and ensure that impairment accounting outcomes aresufficiently reflective of how the entity actually evaluates its capitalinvestment decisions.Furthermore, structural differences between rates of return used by theentity to make capital investment decisions, investment hurdle rates basedon entity’s cost of funds) vis-à-vis market-based discount rates that reflectthe risks specific to the assets used for impairment assessments should beevaluated to anticipate and manage the risks of asset impairments.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 7

2. Regulatory developments

The key regulatory developments during the year are:► Companies (Amendment) Act► ACRA’s Financial Reporting Surveillance Programme (FRSP)► Singapore Exchange’s (SGX) listing rule changes on poll voting and

disclosure of vote outcomes► SGX review of companies’ compliance with the Code of Corporate

Governance► SGX to mandate sustainability reporting in 2017Companies (Amendment) ActACRA announced in April that the legislative changes to the Companies(Amendment) Act will be effected in two phases. About 40% of the over 200legislative amendments in the first phase took effect on 1 July 2015. Thesecond phase encompassing the rest of the legislative amendments is effectiveon 3 January 2016.

ACRA’s FRSP

On financial reporting front, ACRA issued its inaugural report on keyfindings on FY2013 financial statements of listed companies under itsFRSP in September 2015. The report revealed that there is still room forimprovement as a number of instances of non-compliance with theaccounting standards were identified. In December 2015, ACRA alsopublished the FRSP areas of review focus for the FY2015 FinancialStatements whereby it is bringing tougher corporate governance rules andpossible enforcement action against directors for violations under theCompanies Act. Details of which are covered in “ACRA’s FinancialReporting Surveillance Programme” in this issue.

We summarise the recent regulatory changes that will have an effect on anentity’s operation, financial reporting and disclosures in the following page.

Poll voting and disclosure of vote outcomes

Effective 1 August 2015, listed companies and trusts will be required toconduct voting by poll where shareholders are accorded rightsproportionate to their shareholding and all votes are counted.

Compliance with Code of Corporate Governance

The SGX is reviewing compliance with the Code of Corporate Governance (CGCode) of mainboard-listed companies. The review will cover annual reports ofover 550 mainboard companies released in the 12 months to 30 June 2015.The SGX intends to make public the findings of the review and engage therelevant companies to ensure that shortcomings identified are addressed.

Sustainability reporting in 2017

To increase the transparency of governance of listed entities, the SGXannounced in May 2015 its plans to mandate sustainability reporting on a“comply or explain” basis and target implementation for financial year2017. The SGX is inviting inputs from all stakeholders.

AC considerations► As changes to laws and

regulations are proposed andimplemented, is the managementanalysing the possible effect onthe company?

► Has the management consideredthe impact the regulatorydevelopments may have on itsinternal corporate complianceprogram? What actions should betaken to lessen the impact on theexisting internal corporatecompliance program?

► Considering the significant focusthe regulators are placing oncorporate governance, whatsteps are being taken to ensurethe company’s compliance in thisarea? How effective is themanagement’s process formonitoring compliance withregulatory developments? Hasthe management engaged anyadvisers to assist in itscompliance?

Reference libraryBoard Matters Quarterly,Singapore edition

► March and September 2015editions: Regulatory matters

► September 2015 edition:ACRA’s inaugural report onkey findings under FRSP

► June 2015 edition: Two-phase implementation ofCompanies (Amendment) Act2014

Heightened regulatory activity continues to require the attention of boards including the AC. New regulatorymandates are resulting in an expansion of the AC’s oversight agenda, which requires more time andcommitment.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 8

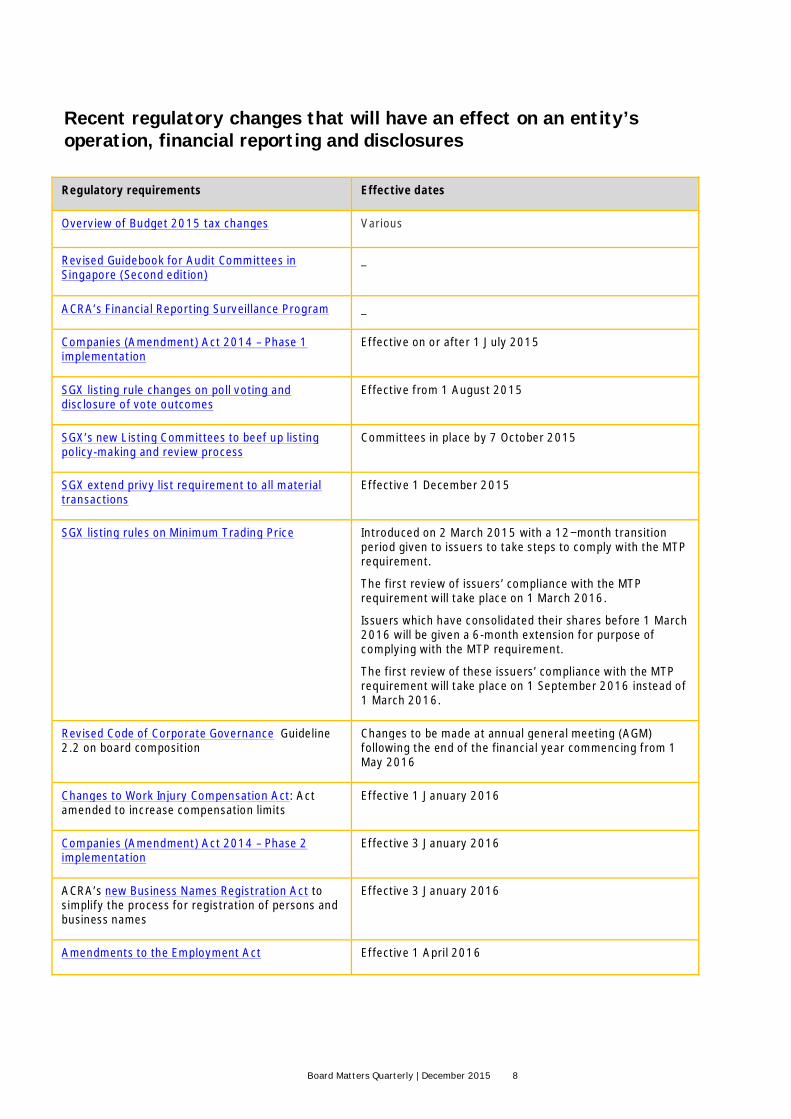

Recent regulatory changes that will have an effect on an entity’soperation, financial reporting and disclosures

Regulatory requirements Effective dates

Overview of Budget 2015 tax changes Various

Revised Guidebook for Audit Committees inSingapore (Second edition)

_

ACRA’s Financial Reporting Surveillance Program _

Companies (Amendment) Act 2014 – Phase 1implementation

Effective on or after 1 July 2015

SGX listing rule changes on poll voting anddisclosure of vote outcomes

Effective from 1 August 2015

SGX’s new Listing Committees to beef up listingpolicy-making and review process

Committees in place by 7 October 2015

SGX extend privy list requirement to all materialtransactions

Effective 1 December 2015

SGX listing rules on Minimum Trading Price Introduced on 2 March 2015 with a 12−month transitionperiod given to issuers to take steps to comply with the MTPrequirement.

The first review of issuers’ compliance with the MTPrequirement will take place on 1 March 2016.

Issuers which have consolidated their shares before 1 March2016 will be given a 6-month extension for purpose ofcomplying with the MTP requirement.

The first review of these issuers’ compliance with the MTPrequirement will take place on 1 September 2016 instead of1 March 2016.

Revised Code of Corporate Governance Guideline2.2 on board composition

Changes to be made at annual general meeting (AGM)following the end of the financial year commencing from 1May 2016

Changes to Work Injury Compensation Act: Actamended to increase compensation limits

Effective 1 January 2016

Companies (Amendment) Act 2014 – Phase 2implementation

Effective 3 January 2016

ACRA’s new Business Names Registration Act tosimplify the process for registration of persons andbusiness names

Effective 3 January 2016

Amendments to the Employment Act Effective 1 April 2016

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 9

3. Risk management

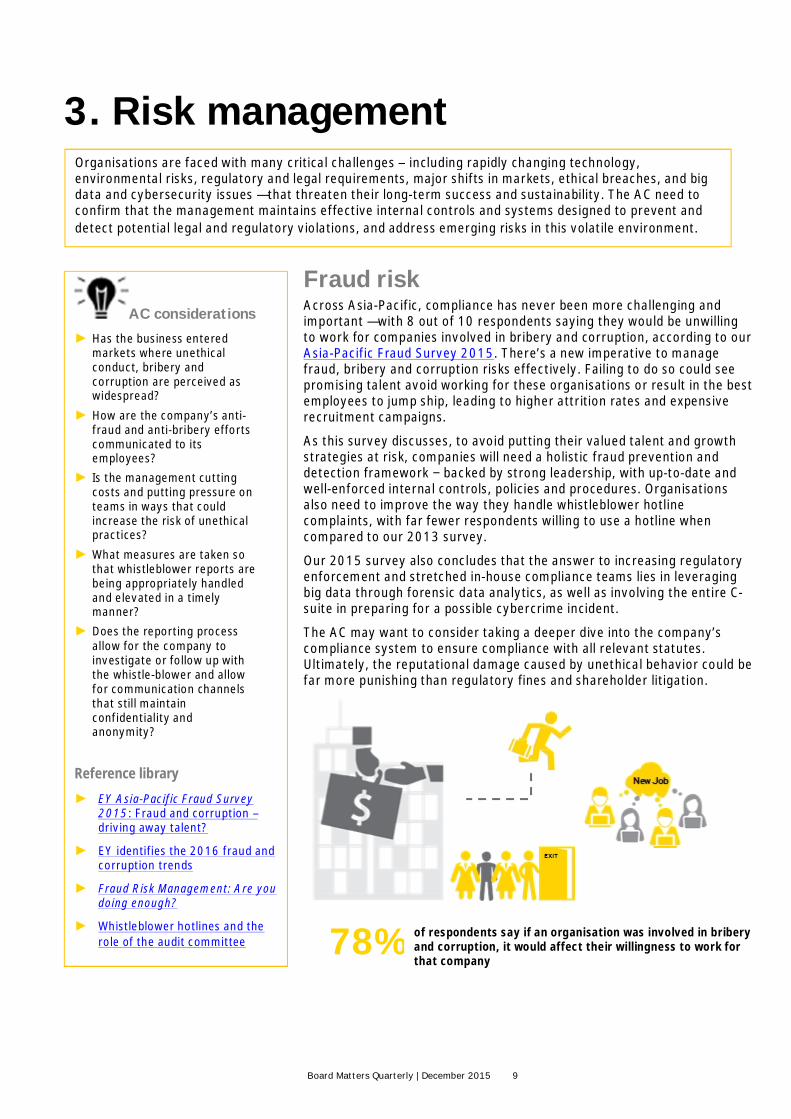

Fraud riskAcross Asia-Pacific, compliance has never been more challenging andimportant — with 8 out of 10 respondents saying they would be unwillingto work for companies involved in bribery and corruption, according to ourAsia-Pacific Fraud Survey 2015. There’s a new imperative to managefraud, bribery and corruption risks effectively. Failing to do so could seepromising talent avoid working for these organisations or result in the bestemployees to jump ship, leading to higher attrition rates and expensiverecruitment campaigns.

As this survey discusses, to avoid putting their valued talent and growthstrategies at risk, companies will need a holistic fraud prevention anddetection framework − backed by strong leadership, with up-to-date andwell-enforced internal controls, policies and procedures. Organisationsalso need to improve the way they handle whistleblower hotlinecomplaints, with far fewer respondents willing to use a hotline whencompared to our 2013 survey.

Our 2015 survey also concludes that the answer to increasing regulatoryenforcement and stretched in-house compliance teams lies in leveragingbig data through forensic data analytics, as well as involving the entire C-suite in preparing for a possible cybercrime incident.

The AC may want to consider taking a deeper dive into the company’scompliance system to ensure compliance with all relevant statutes.Ultimately, the reputational damage caused by unethical behavior could befar more punishing than regulatory fines and shareholder litigation.

wit

h

8

Organisations are faced with many critical challenges — including rapidly changing technology,environmental risks, regulatory and legal requirements, major shifts in markets, ethical breaches, and bigdata and cybersecurity issues — that threaten their long-term success and sustainability. The AC need toconfirm that the management maintains effective internal controls and systems designed to prevent anddetect potential legal and regulatory violations, and address emerging risks in this volatile environment.

AC considerations► Has the business entered

markets where unethicalconduct, bribery andcorruption are perceived aswidespread?

► How are the company’s anti-fraud and anti-bribery effortscommunicated to itsemployees?

► Is the management cuttingcosts and putting pressure onteams in ways that couldincrease the risk of unethicalpractices?

► What measures are taken sothat whistleblower reports arebeing appropriately handledand elevated in a timelymanner?

► Does the reporting processallow for the company toinvestigate or follow up withthe whistle-blower and allowfor communication channelsthat still maintainconfidentiality andanonymity?

Reference library

► EY Asia-Pacific Fraud Survey2015: Fraud and corruption –driving away talent?

► EY identifies the 2016 fraud andcorruption trends

► Fraud Risk Management: Are youdoing enough?

► Whistleblower hotlines and therole of the audit committee 78% of respondents say if an organisation was involved in bribery

and corruption, it would affect their willingness to work forthat company

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 10

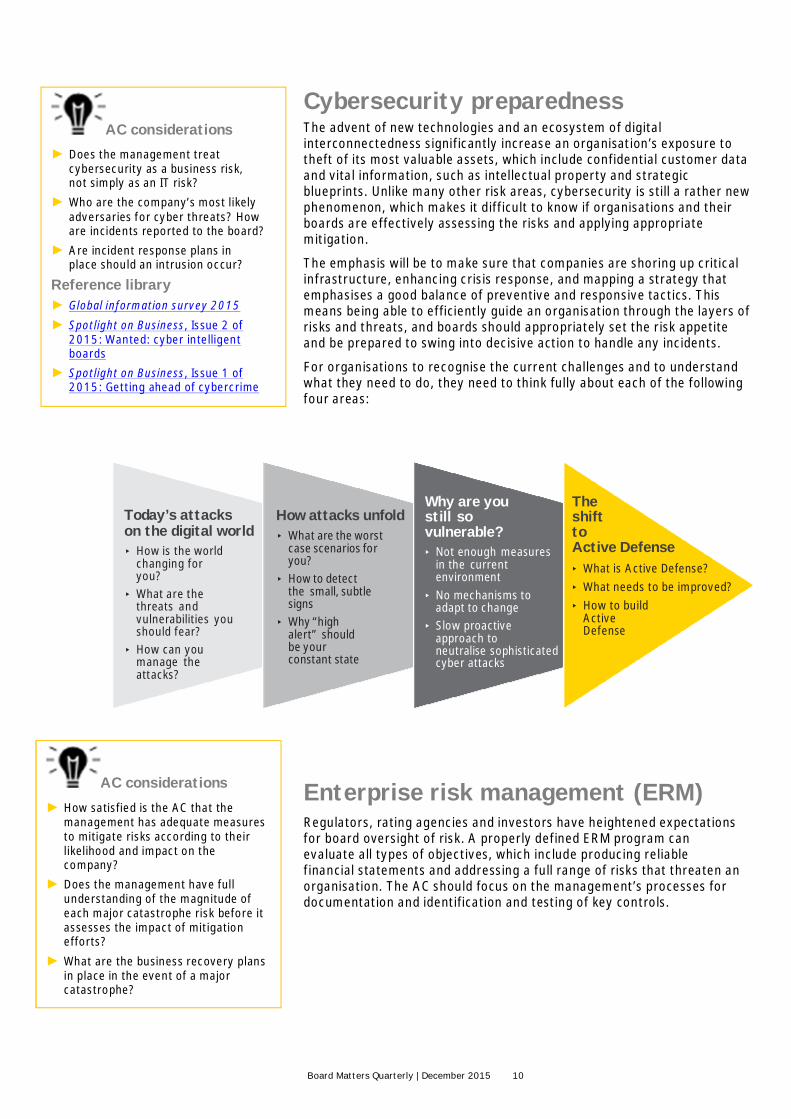

Cybersecurity preparednessThe advent of new technologies and an ecosystem of digitalinterconnectedness significantly increase an organisation’s exposure totheft of its most valuable assets, which include confidential customer dataand vital information, such as intellectual property and strategicblueprints. Unlike many other risk areas, cybersecurity is still a rather newphenomenon, which makes it difficult to know if organisations and theirboards are effectively assessing the risks and applying appropriatemitigation.

The emphasis will be to make sure that companies are shoring up criticalinfrastructure, enhancing crisis response, and mapping a strategy thatemphasises a good balance of preventive and responsive tactics. Thismeans being able to efficiently guide an organisation through the layers ofrisks and threats, and boards should appropriately set the risk appetiteand be prepared to swing into decisive action to handle any incidents.

For organisations to recognise the current challenges and to understandwhat they need to do, they need to think fully about each of the followingfour areas:

Enterprise risk management (ERM)Regulators, rating agencies and investors have heightened expectationsfor board oversight of risk. A properly defined ERM program canevaluate all types of objectives, which include producing reliablefinancial statements and addressing a full range of risks that threaten anorganisation. The AC should focus on the management’s processes fordocumentation and identification and testing of key controls.

Today’s attackson the digital world

How is the worldchanging foryou?What are thethreats andvulnerabilities youshould fear?How can youmanage theattacks?

How attacks unfoldWhat are the worstcase scenarios foryou?How to detectthe small, subtlesignsWhy “highalert” shouldbe yourconstant state

Why are youstill sovulnerable?

Not enough measuresin the currentenvironmentNo mechanisms toadapt to changeSlow proactiveapproach toneutralise sophisticatedcyber attacks

TheshifttoActive Defense

What is Active Defense?What needs to be improved?How to buildActiveDefense

AC considerations► Does the management treat

cybersecurity as a business risk,not simply as an IT risk?

► Who are the company’s most likelyadversaries for cyber threats? Howare incidents reported to the board?

► Are incident response plans inplace should an intrusion occur?

Reference library► Global information survey 2015

► Spotlight on Business, Issue 2 of2015: Wanted: cyber intelligentboards

► Spotlight on Business, Issue 1 of2015: Getting ahead of cybercrime

AC considerations

► How satisfied is the AC that themanagement has adequate measuresto mitigate risks according to theirlikelihood and impact on thecompany?

► Does the management have fullunderstanding of the magnitude ofeach major catastrophe risk before itassesses the impact of mitigationefforts?

► What are the business recovery plansin place in the event of a majorcatastrophe?

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 11

4. Audit regulatory initiatives

Enhancing the auditor’s reportOn 30 July 2015, the Institute of Singapore Chartered Accountantsreleased the new and revised auditor reporting standards. Thesestandards are effective for audits of financial statements for periodsending on or after 15 December 2016.

The most notable enhancement is the new requirement for auditors oflisted entities’ to communicate key audit matters (KAM) in the auditor’sreport − those matters that the auditor views as most significant, with anexplanation of how they were addressed in the audit and references to therelevant note disclosures in the financial statements.

The KAM reporting in the auditor’s report will not only increase therelevance of the financial statements audit, but raise the shareholders’engagement at the AGM.

More work is required in advance to reach an agreement about the keyareas of risk to manage user and analyst interpretations of KAM that couldraise questions among the stakeholders.

As such, timely communication is the key to avoid surprises.

All parties - AC, directors, management, and auditors - should share acommon goal of improving communications so as to ensure smoothimplementation in 2016 calendar-year audits. It is important to use thetransition period from now to 2016 to become familiar and understand thenature of the changes to plan ahead for its implementation.

ACRA’s AQI Disclosure FrameworkThe AC select their auditors based on multiple factors. One importantfactor would be the auditors’ ability to deliver quality audits. Research hasshown that a number of input, process and output factors can collectivelyindicate an auditor’s ability and commitment to deliver high quality audits.These factors are commonly termed as AQI. Globally, there has beengrowing interest in developing indicators on audit quality. In recent years,audit regulators and audit firms in Europe and the US, as well asinternational organisations such as the International Auditing andAssurance Standards Board, have embarked on various projects to explorethe use of AQI.

In October 2015, ACRA has introduced its AQI Disclosure Framework toenable AC of listed companies to better evaluate and select the rightauditor. ACRA’s goal is to equip AC with relevant and timely informationabout recent inspection findings, audit trends and risks, and otherimportant audit quality topics. The AC will be able to utilise the AQIFramework from 1 January 2016. The AQI Disclosure Framework isdiscussed in more details in article “ACRA’s Audit Quality IndicatorsDisclosure Framework” in this issue.

This past year has been marked by significant activities around key issues, such as the extended auditor'sreport, and ACRA’s Audit Quality Indicators (AQI) Disclosure Framework that enable the AC of listedcompanies to better evaluate and select the right auditor.

AC considerations

► What message does the KAMsend to the shareholders?

► How do auditors determine KAM?

► In determining the KAM, what isthe involvement of themanagement and directors?

► How does this impact thecommunication between theauditors, the management, anddirectors?

► Will users of the financialstatements place greaterspotlight on topics highlighted asKAM?

► Will this impact the timing ofthe issuance of annualreports?

► Do the AC and managementunderstand the emergingregulatory requirements, andare they prepared to take thesteps necessary to meet therequired deadlines?

► What steps has the AC taken toincrease transparency aroundits oversight of the auditrelationship?

► What discussion has the AChad with its independentauditor regarding audit qualitymatters?

Reference library► Board Matters Quarterly,

September 2015 edition: Are youready for the new audit reportingregime?

► Board Matters Quarterly, March2015 edition: Imminent changeto the global auditor reporting

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 12

5. Tax developments and tax risk

IRAS’s 2015 Singapore TransferPricing GuidelinesTransfer pricing has been criticised as aiding multinationals in shiftingprofits between jurisdictions. Amid the intensifying focus on the baseerosion and profit shifting (BEPS) Action Plan and transfer pricing auditactivity internationally, the Inland Revenue Authority of Singapore (IRAS)published its revised transfer pricing guidelines in January 2015.A significant highlight of the 2015 Guidelines is the requirement forcontemporaneous transfer pricing, defined as transfer pricingdocumentation prepared no later than the date of filing of the tax returnfor the relevant financial year. This sends a clear message that Singaporetaxpayers should no longer think of transfer pricing documentation as a“nice to have”, but rather a “must have”. This requirement may havearose from IRAS’ observation that as high as 73% of Transfer PricingConsultations (TPC) had inadequate transfer pricing documentation.How do we expect transfer pricing in Singapore to develop in the nearfuture? With transfer pricing still very much in the international limelight,we foresee that IRAS’ focus on transfer pricing will continue to intensify.Already, we have observed more TPC commencing since the issuance ofthe 2015 Guidelines, and an increase in transfer pricing queries in theannual tax return reviews. Finally, transfer pricing dispute resolution willbecome an even more important consideration in the future as Singaporeand other tax authorities build up their transfer pricing resources andcompetencies.

Income tax accountingThis continues to be a leading cause of financial statement restatementand internal control material weaknesses for companies. The AC need tohave a sound understanding of how the company allocates resources totax matters, and whether those resources commensurate with the scopeof tax risk and are consistent with the complexities of the company’s taxstructures and overall demands on the tax function.

Managing tax controversiesTax authorities continue to be more assertive in examining cross-borderactivities, and the volume of tax information exchange agreements hasincreased substantially. In addition, tax audits have become more frequentand aggressive, placing companies under unprecedented scrutiny.Managing tax risk and controversies is expected to become moreimportant for companies. Discussing the potential ramifications of specifictax disputes with management, including the risk of serious penalties andreputational damage, can help the AC understand the process that themanagement uses to identify measure and manage a company’s tax risks.

Companies are increasingly being asked to explain and justify their tax transactions to lawmakers, taxadministrators, stakeholders, customers and the public. Board members need to understand all of thenecessary information to help the company prepare, adapt and respond to a rapidly changing taxenvironment.

AC considerations

► What is the process that themanagement uses to identify,measure and oversee variouscategories of tax risks andtransfer pricing risks and whetherthe related reserves areadequate?

► Has the management conducted astrategic review of theimplications of potential cross-border tax changes for thecompany’s business models andstructures? Has the managementshared this evaluation with theboard?

► Is the company prepared for theexpected substantial increase inglobal reporting requirements andthe commensurate increase incompliance costs?

► Is the company ready forheightened scrutiny and tax auditrisk, which can place increasedpressure on cash tax andeffective tax rate positions?

► Who in the management isresponsible for making tax andtax accounting decisions? Is thisparty empowered to do so, anddoes the party have the requisiteexperience and knowledge?

Reference library► You and the Taxman series

► EY tax news alert

► Transfer Pricing Alert

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 13

6. Working with the internal auditorAn effective internal audit (IA) function can be a powerful safeguard againstdefects in financial controls or financial statements. For example, in the case ofWorldCom, the whistle-blower was a member of WorldCom’s internal auditdepartment.A strong, well-performing internal audit function may also help facilitate the independent auditor’s audit in certainareas. Regular interaction between the AC and the IA is critical to the effective functioning of the IA group. The ACshould take care to determine that appropriate collaboration and communication occur.

The AC should meet regularly and privately with the IA and make sure that the IA has direct access to the AC. TheAC should be comfortable that the IA staff has the appropriate training and supervision to stay professionallycurrent.

AC considerations

► Does the IA director have direct access, and report regularly, to the AC?

► Has the department made any significant recommendations to management about improving internal controls?Does the management have an appropriate and timely response to significant the recommendations andcomments? What follow-up and monitoring procedures are performed by internal audit?

► How do the internal auditors view the quality of the company’s control environment?

► Are the internal auditors aware of any known or suspected instances of employee fraud, questionable or illegalpayments, or violations of laws and regulations?

► How involved is internal audit in investigating matters raised by whistle-blowers?

Reference library

► Boards and internal audit: working together

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 14

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 15

ACRA’s FinancialReportingSurveillanceProgrammeThe key findings from its inaugural report and the focusareas for FY2015 financial statements review.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 16

A. Key findings from ACRA’s review ofFY2013 financial statements

In October 2015, ACRA issued its inaugural report arising from itsreview of selected financial statements of listed companies withfinancial year ended between 1 January 2013 and 31 December 2013(FY2013 financial statements) under its FRSP.

Scope of reviewThe scope of the FRSP’s review for the FY2013 financial statementswas expanded to include reviews of financial statements of listedcompanies with ‘clean’ audit reports, and no longer merely focused onthose with accounting issues highlighted in modified audit reports.

Approach of reviewIn the review of FY2013 financial statements, ACRA deep-dived intoaccounting issues and raised many enquiries in the areas of recognitionand measurement, particularly in relation to complex or unusualtransactions. When the accounting issues are identified, ACRArequested for detailed explanations and where necessary, documentaryevidence to support the accounting position.

Review outcomeThe review outcome revealed that the state of financial reporting bySingapore-incorporated listed companies is generally healthy.However, there is still room for improvement as a number of instancesof non-compliance with the accounting standards were identified.Out of a total of 49 sets of financial statements reviewed, only twocompanies went through the review with no enquiries raised. In fact,directors of four companies received warning letters from ACRA,arising from instances of severe non-compliance.

Causes of non-complianceACRA’s findings revealed that the fundamental cause for the instances ofnon-compliance appeared to stem from a lack of ownership by thedirectors of companies in the financial reporting process. Three main rootcauses of non-compliance were identified as follows:► Insufficient scrutiny by directors when the reported financials did

not accord with their understanding of the business► Over-reliance on accounting team who may lack competence or

diligence► Independent directors did not adequately challenge management’s

judgementThe findings also showed that most of the instances of non-compliancecould have been avoided if the directors, even without the benefit ofdetailed accounting knowledge or professional support, review thefinancial statements carefully and with rigour. The report alsohighlights several case studies aimed at educating directors andcompanies on issues that arise.

The scope of the FRSP’sreview was expanded toinclude reviews offinancial statements with‘clean’ audit reports.

ACRA deep-dived intoaccounting issues andraised many enquiries inthe areas of recognitionand measurement.

ACRA’s findings on thereview of FY2013financial statementsrevealed that:

► the fundamental causefor non-complianceappeared to stem from alack of ownership by thecompanies in thefinancial reportingprocess, and

► most of the instances ofnon-compliance couldhave been avoided if thedirectors review thefinancial statementscarefully and withrigour.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 17

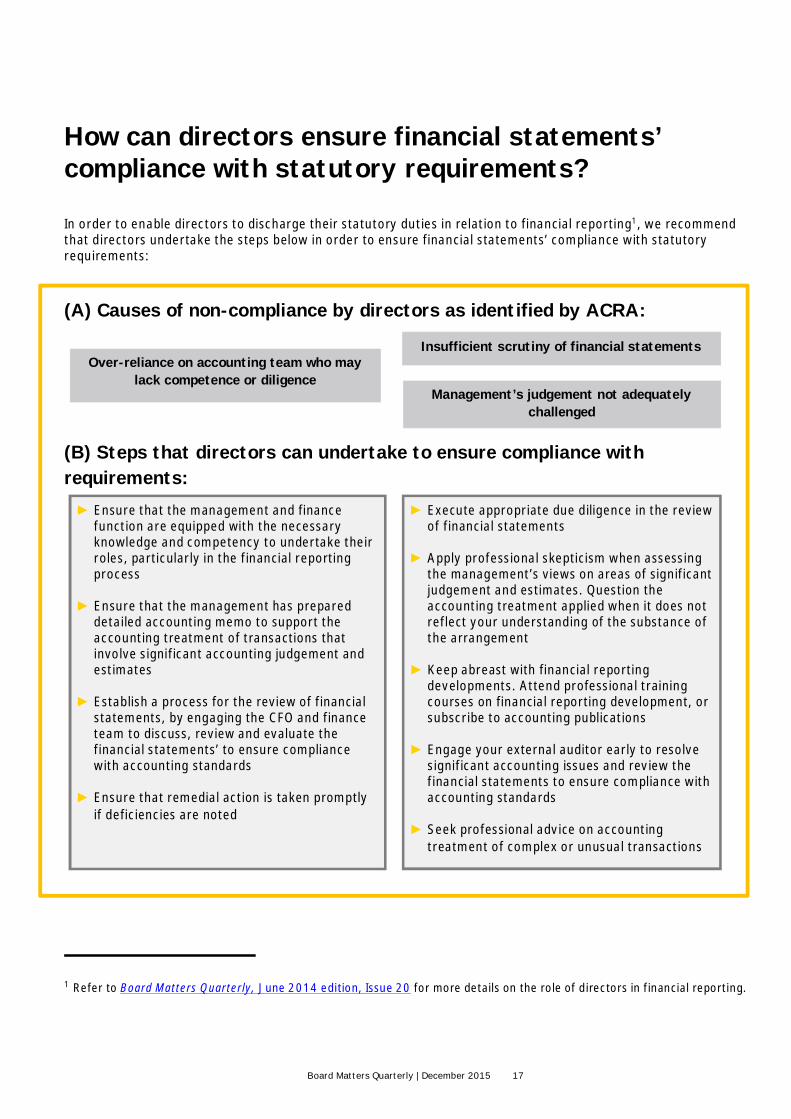

How can directors ensure financial statements’compliance with statutory requirements?

In order to enable directors to discharge their statutory duties in relation to financial reporting1, we recommendthat directors undertake the steps below in order to ensure financial statements’ compliance with statutoryrequirements:

(A) Causes of non-compliance by directors as identified by ACRA:

(B) Steps that directors can undertake to ensure compliance withrequirements:

1 Refer to Board Matters Quarterly, June 2014 edition, Issue 20 for more details on the role of directors in financial reporting.

Insufficient scrutiny of financial statementsOver-reliance on accounting team who may

lack competence or diligenceManagement’s judgement not adequately

challenged

► Execute appropriate due diligence in the reviewof financial statements

► Apply professional skepticism when assessingthe management’s views on areas of significantjudgement and estimates. Question theaccounting treatment applied when it does notreflect your understanding of the substance ofthe arrangement

► Keep abreast with financial reportingdevelopments. Attend professional trainingcourses on financial reporting development, orsubscribe to accounting publications

► Engage your external auditor early to resolvesignificant accounting issues and review thefinancial statements to ensure compliance withaccounting standards

► Seek professional advice on accountingtreatment of complex or unusual transactions

► Ensure that the management and financefunction are equipped with the necessaryknowledge and competency to undertake theirroles, particularly in the financial reportingprocess

► Ensure that the management has prepareddetailed accounting memo to support theaccounting treatment of transactions thatinvolve significant accounting judgement andestimates

► Establish a process for the review of financialstatements, by engaging the CFO and financeteam to discuss, review and evaluate thefinancial statements’ to ensure compliancewith accounting standards

► Ensure that remedial action is taken promptlyif deficiencies are noted

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 18

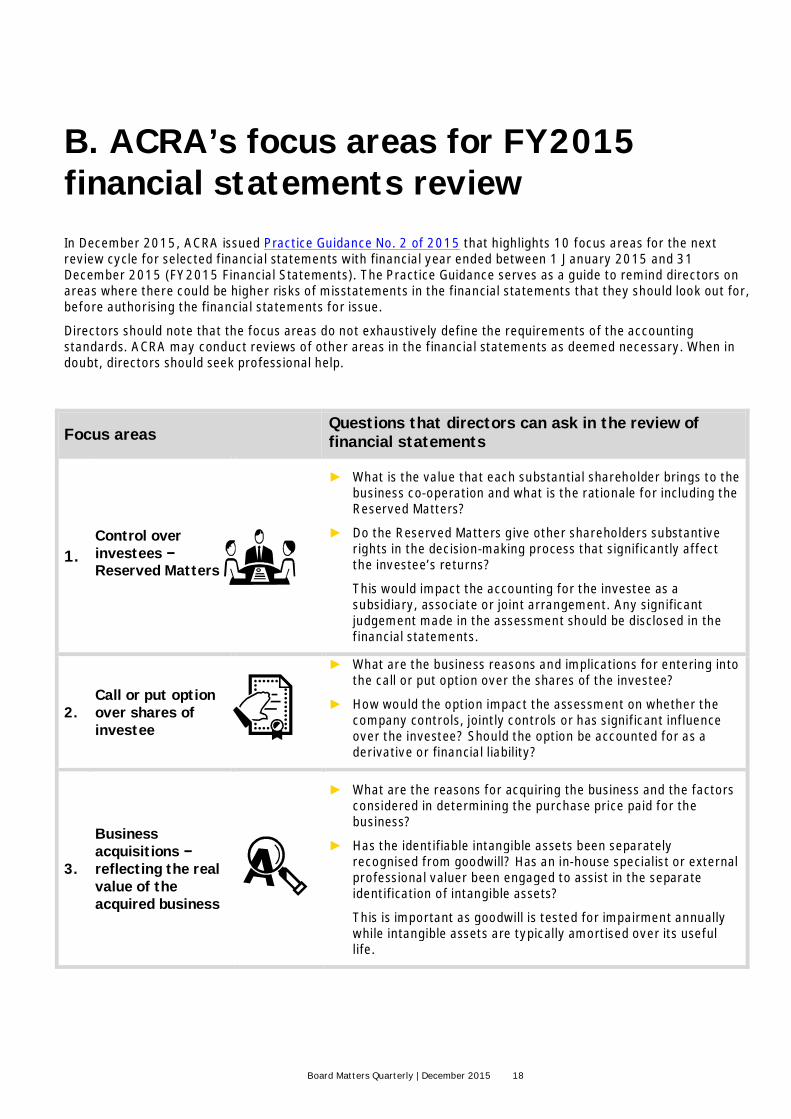

B. ACRA’s focus areas for FY2015financial statements reviewIn December 2015, ACRA issued Practice Guidance No. 2 of 2015 that highlights 10 focus areas for the nextreview cycle for selected financial statements with financial year ended between 1 January 2015 and 31December 2015 (FY2015 Financial Statements). The Practice Guidance serves as a guide to remind directors onareas where there could be higher risks of misstatements in the financial statements that they should look out for,before authorising the financial statements for issue.

Directors should note that the focus areas do not exhaustively define the requirements of the accountingstandards. ACRA may conduct reviews of other areas in the financial statements as deemed necessary. When indoubt, directors should seek professional help.

Focus areasQuestions that directors can ask in the review offinancial statements

1.Control overinvestees −Reserved Matters

► What is the value that each substantial shareholder brings to thebusiness co-operation and what is the rationale for including theReserved Matters?

► Do the Reserved Matters give other shareholders substantiverights in the decision-making process that significantly affectthe investee’s returns?

This would impact the accounting for the investee as asubsidiary, associate or joint arrangement. Any significantjudgement made in the assessment should be disclosed in thefinancial statements.

2.Call or put optionover shares ofinvestee

► What are the business reasons and implications for entering intothe call or put option over the shares of the investee?

► How would the option impact the assessment on whether thecompany controls, jointly controls or has significant influenceover the investee? Should the option be accounted for as aderivative or financial liability?

3.

Businessacquisitions −reflecting the realvalue of theacquired business

► What are the reasons for acquiring the business and the factorsconsidered in determining the purchase price paid for thebusiness?

► Has the identifiable intangible assets been separatelyrecognised from goodwill? Has an in-house specialist or externalprofessional valuer been engaged to assist in the separateidentification of intangible assets?

This is important as goodwill is tested for impairment annuallywhile intangible assets are typically amortised over its usefullife.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 19

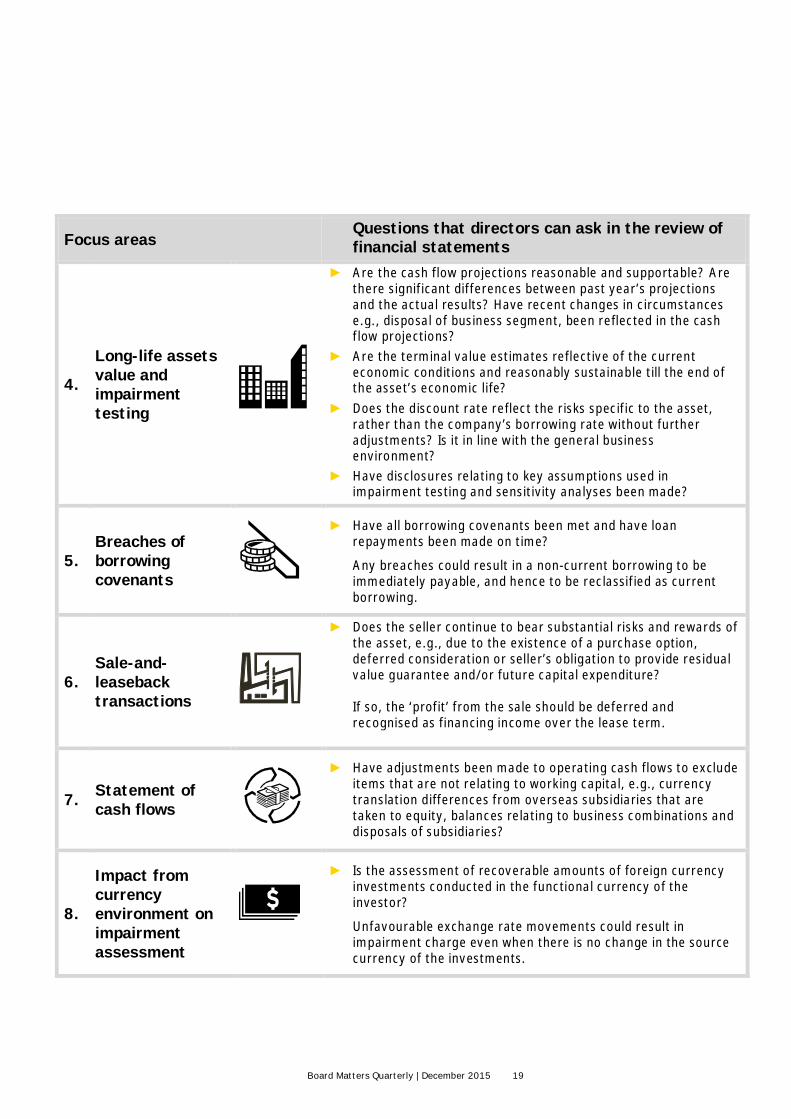

Focus areasQuestions that directors can ask in the review offinancial statements

4.

Long-life assetsvalue andimpairmenttesting

► Are the cash flow projections reasonable and supportable? Arethere significant differences between past year’s projectionsand the actual results? Have recent changes in circumstancese.g., disposal of business segment, been reflected in the cashflow projections?

► Are the terminal value estimates reflective of the currenteconomic conditions and reasonably sustainable till the end ofthe asset’s economic life?

► Does the discount rate reflect the risks specific to the asset,rather than the company’s borrowing rate without furtheradjustments? Is it in line with the general businessenvironment?

► Have disclosures relating to key assumptions used inimpairment testing and sensitivity analyses been made?

5.Breaches ofborrowingcovenants

► Have all borrowing covenants been met and have loanrepayments been made on time?

Any breaches could result in a non-current borrowing to beimmediately payable, and hence to be reclassified as currentborrowing.

6.Sale-and-leasebacktransactions

► Does the seller continue to bear substantial risks and rewards ofthe asset, e.g., due to the existence of a purchase option,deferred consideration or seller’s obligation to provide residualvalue guarantee and/or future capital expenditure?

If so, the ‘profit’ from the sale should be deferred andrecognised as financing income over the lease term.

7. Statement ofcash flows

► Have adjustments been made to operating cash flows to excludeitems that are not relating to working capital, e.g., currencytranslation differences from overseas subsidiaries that aretaken to equity, balances relating to business combinations anddisposals of subsidiaries?

8.

Impact fromcurrencyenvironment onimpairmentassessment

► Is the assessment of recoverable amounts of foreign currencyinvestments conducted in the functional currency of theinvestor?

Unfavourable exchange rate movements could result inimpairment charge even when there is no change in the sourcecurrency of the investments.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 20

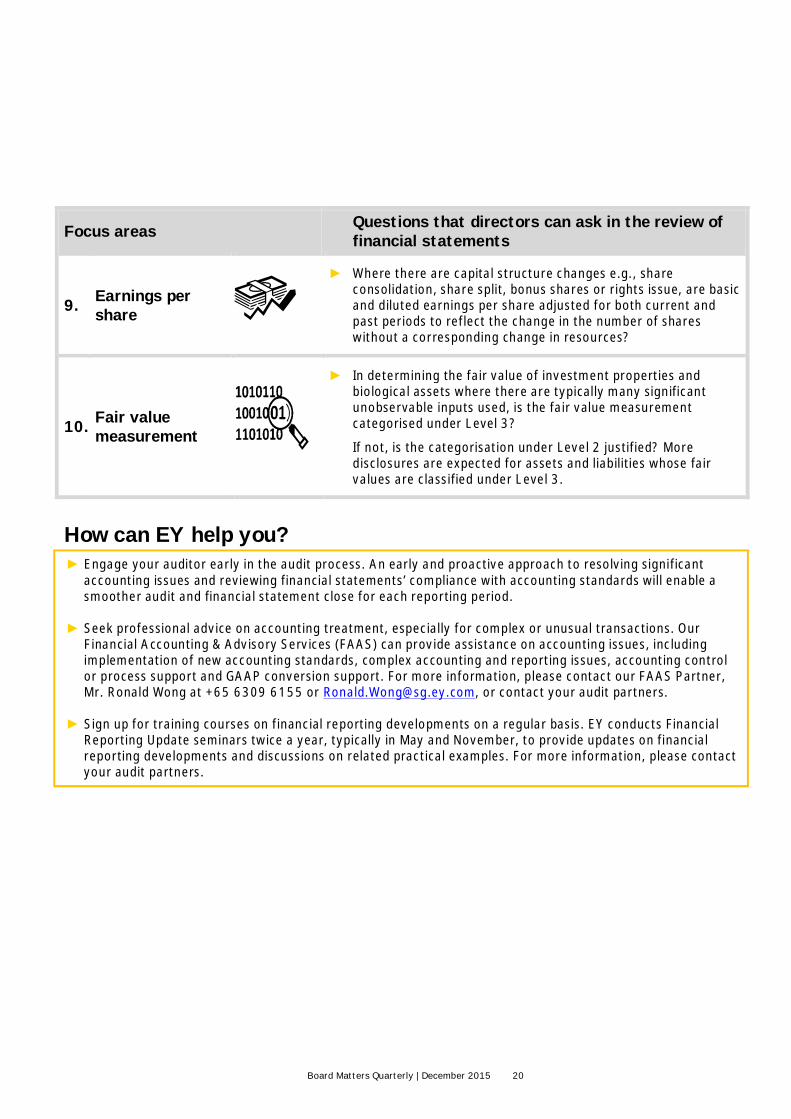

Focus areas Questions that directors can ask in the review offinancial statements

9. Earnings pershare

► Where there are capital structure changes e.g., shareconsolidation, share split, bonus shares or rights issue, are basicand diluted earnings per share adjusted for both current andpast periods to reflect the change in the number of shareswithout a corresponding change in resources?

10. Fair valuemeasurement

► In determining the fair value of investment properties andbiological assets where there are typically many significantunobservable inputs used, is the fair value measurementcategorised under Level 3?

If not, is the categorisation under Level 2 justified? Moredisclosures are expected for assets and liabilities whose fairvalues are classified under Level 3.

How can EY help you?► Engage your auditor early in the audit process. An early and proactive approach to resolving significant

accounting issues and reviewing financial statements’ compliance with accounting standards will enable asmoother audit and financial statement close for each reporting period.

► Seek professional advice on accounting treatment, especially for complex or unusual transactions. OurFinancial Accounting & Advisory Services (FAAS) can provide assistance on accounting issues, includingimplementation of new accounting standards, complex accounting and reporting issues, accounting controlor process support and GAAP conversion support. For more information, please contact our FAAS Partner,Mr. Ronald Wong at +65 6309 6155 or [email protected], or contact your audit partners.

► Sign up for training courses on financial reporting developments on a regular basis. EY conducts FinancialReporting Update seminars twice a year, typically in May and November, to provide updates on financialreporting developments and discussions on related practical examples. For more information, please contactyour audit partners.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 21

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 22

ACRA’s Audit QualityIndicators DisclosureFrameworkFramework to help companies select auditors

In October 2015, ACRA introduced the Audit Quality IndicatorsDisclosure Framework (Framework). The Framework is the first of itskind in the region. Globally, efforts to identify such indicators havepicked up momentum in the past several years with audit regulators inthe US and Europe, as well as international organisations such as theIAASB, had embarked on various projects to explore the use of AQI.

AQI objectiveThe aim of the Framework is to further raise the quality of audits onfinancial statements in Singapore by enhancing discussions betweenAC and audit firms on factors that may be important to the quality ofthe audit during the selection and reappointment of auditors. Forexample, the AQI could help improve the AC’s understanding of afirm’s policies, procedures and processes related to its system ofquality control; provide insights into a particular audit team’sperformance; and clarify risks to audit quality that may exist.

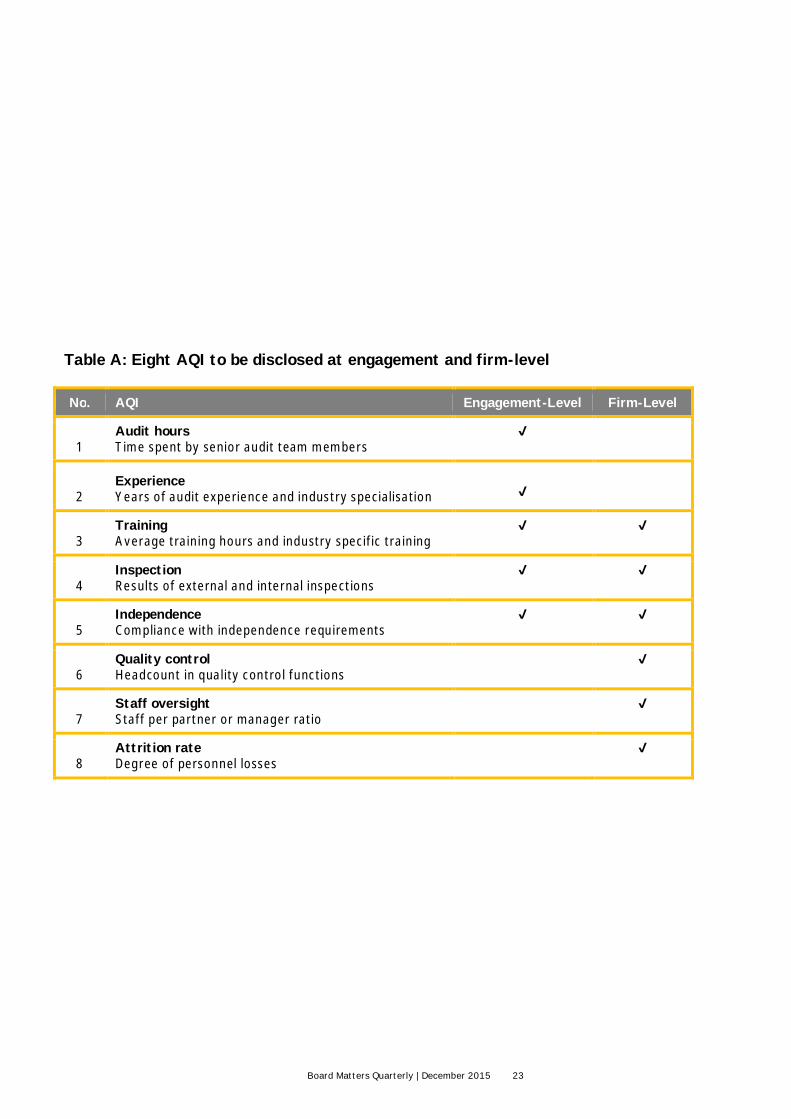

The FrameworkTable A sets out the eight AQI to be disclosed at the engagement andfirm-level.

ACRA believes the Framework will equip the AC with information thatallows them to exercise their professional judgements on elementsthat contribute to, or are indicative of audit quality. ACRA ChiefExecutive Mr. Kenneth Yap said in his keynote speech announcing theAQI Framework that: “The AQI alone are not a silver bullet thatguarantees high quality audits. They do, however provide AC with acomparable basis on which to conduct a conversation on the effort,experience and resources that an audit firm will bring to bear on aparticular audit”. Mr. Yap further added: “I am confident that AC thatutilises the AQI will see audit quality improves over time. This bodeswell for Singapore’s reputation as a transparent and trusted businesshub”.

AC will be able to utilise the AQI Framework from 1 January 2016.The big-four accounting firms have confirmed support for theFramework.

How we see this:EY shares ACRA’sobjective of promotingaudit quality. AQI can helpto improve the AC’sunderstanding of a firm’spolicies, procedures andprocesses related to itssystem of quality control;provide insights into aparticular audit team’sperformance; and clarifyrisks to audit quality thatmay exist.

We believe that identifyingkey factors that impactaudit quality can facilitatea more commonunderstanding of elementsof the audit process andafford useful information toAC and other stakeholders.

We will be communicatingour AQI informationdirectly to AC each yearduring the process of re-appointment orappointment of a newauditor.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 23

Table A: Eight AQI to be disclosed at engagement and firm-level

No. AQI Engagement-Level Firm-Level

1Audit hoursTime spent by senior audit team members

√

2ExperienceYears of audit experience and industry specialisation √

3TrainingAverage training hours and industry specific training

√ √

4InspectionResults of external and internal inspections

√ √

5IndependenceCompliance with independence requirements

√ √

6Quality controlHeadcount in quality control functions

√

7Staff oversightStaff per partner or manager ratio

√

8Attrition rateDegree of personnel losses

√

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 24

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 25

Regulatory updates1. ACRA announcedimplementation date for Phase 2of Companies (Amendments) Act

On 5 November 2015, ACRA announced that thesecond phase of legislative amendments to theCompanies Act will be implemented on 3January 2016. Details are available at ACRAwebsite.

The first phase of implementation, which sawabout 40% of the over 200 amendments comeinto effect, took place on 1 July 2015. The list ofamendments to the Act to be effected from 1July 2015 can be found here.

The selected key legislative amendments to beimplemented in each phase are highlighted in ourJune 2015 edition.

2. SGX reviewing companies’compliance with CorporateGovernance CodeThe SGX is carrying out a review of how listedcompanies abide by the “comply or explain”requirement for principles and guidelines of theSingapore CG Code.

The review is part of SGX’s drive to raisegovernance standards of listed companies andfollows the introduction of a Disclosure Guidancedocument in January 2015 to help companiescomply with key aspects of governance. Thereview is expected to take four months tocomplete.

Listed companies are required under SGX ListingRules to comply with the CG Code, or explaindeviations in their annual reports. Investors canthen evaluate the adequacy of companies’disclosures and whether explanations for anydeviations are meaningful.

The review will cover annual reports of over 550Mainboard-lised companies released in the 12months to 30 June 2015. The SGX intends tomake findings of the review public and engage

with relevant companies to ensure short-comingsidentified are addressed.

The review will capture all aspects of the CG Codeand focus on the areas specified in the SGXDisclosure Guidance document. Examples of keyCG Code principles covered in the review includeboard composition, risk management and internalcontrols and disclosure on remuneration.

Details are available at SGX website.

3. SGX “Trade with Caution”alerts to be more detailed andtargetedSGX will detail in “Trade with Caution (TWC) alertsconcerns about unusual trading activities in acompany’s stock. The alerts will be more targetedas they will be issued on a case-by-case basisinstead of being automatically triggered by acompany’s “not aware” reply to a public queryfrom SGX. The alerts may also contain detailsgathered from SGX’s review of trading activities.

Effective immediately, the new TWC approach isaimed at delivering higher-value information toinvestors. The changes follow feedback frominvestors, market participants and otherstakeholders about the current high volume of theTWC announcements with little new information.In the financial year ended 30 June 2015, 85public queries were issued followed by 47 TWCannouncements.

Currently, TWC alerts are automaticallygenerated. When trading activity of a share isdeemed unusual, which means it cannot beexplained by any publicly-known factor, SGXissues a public query to the company. If thecompany in its reply to SGX says it is not aware ofreasons for the trading activities, SGX issues theTWC alert.

Details are available at SGX website.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 26

Regulatory updates4. SGX gives 6-month extensionto companies consolidating sharesto comply with MTPSGX is giving affected companies carrying out ashare consolidation to comply with the MinimumTrading Price (MTP) requirement, a 6-monthextension before they are reviewed forcompliance with the MTP requirement.

The 6-month volume-weighted average price(VWAP) of the shares of these companies will thusbe assessed only on 1 September 2016 instead of1 March 2016. The extension will only apply tocompanies which have consolidated their sharesbefore 1 March 2016.

Other affected issuers will still have their shares’6-month VWAP reviewed for MTP compliance on 1March 2016. Affected issuers that have not actedto comply with MTP will be placed on the watch listif the VWAP of their shares for the 6−monthperiod from 1 September 2015 is below S$0.20.Once on the watch list, they have three years tomeet the requirement or be delisted.

On 2 March 2015, SGX introduced an MTP forshares of Mainboard-listed companies to improvethe quality of the market and reduce the risk ofexcessive speculation following the extremevolatility of low-capitalisation stocks in October2013. The requirement takes effect from 1 March2016 after a 1-year transition period. As at theend of October 2015, 94 of the 167 companieslikely to be affected by MTP have either acted orannounced plans to comply. Among the 94companies, 86 have decided on a shareconsolidation of which 65 have completed thiscorporate action.

Details are available at SGX website.

5. SGX extended privy listrequirement to all materialtransactionsFollowing public consultation, the SGX has decidedto widen the practice of listed companiesmaintaining a privy list to all materialtransactions, from only certain significanttransactions currently.

Respondents to the consultation were generallysupportive of the practice of keeping the list whichcontains details of parties privy to the transaction.They recognised the privy list as a usefulregulatory tool when SGX conducts aninvestigation into, for instance, insider trading.Currently, the SGX requires the privy list to bemaintained only for certain significanttransactions i.e., takeovers, reverse takeovers orvery substantial acquisitions.

Due to concerns about the privacy of personaldata, companies will be given the flexibility ofdeciding what information the privy list willcontain. More personal data can be provided at alater stage when SGX asks for the privy list.

The consultation also considered the proposedcodification of a practice for listed companiesand/or controlling shareholders to privately notifythe exchange of significant transactions. The SGXhas decided not to proceed with the codificationand will stop requiring the notifications. Thenotifications are made privately to SGX thus notrequiring them should not impact investorinterest.

Nevertheless, companies remain obliged toexercise vigilance and monitor the trading of theirshares when sensitive confidential discussions areon-going, and to make the necessary disclosuresas soon as possible where there is any suggestionof unusual trading.

The changes to the privy list requirement and theremoval of the private notification on significanttransactions are effective 1 December 2015.

Details are available at SGX website.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 27

6. SGX launched compliancebulletin to spell out privatedisciplinary actionsThe SGX has launched a new online listingcompliance bulletin as part of moves to increasetransparency on disciplinary actions.

The bulletin will shed light on non-publicregulatory actions the SGX has taken in responseto listing rule breaches. In addition to publicdisciplinary actions, the SGX takes privateenforcement actions against listed issuers, theirexecutive officers, directors and marketprofessionals.

The bulletin contains case studies of non-publicregulatory decisions that highlight commonpitfalls, areas of concern and circumstances thatwould lead to a breach of the listing rules.

The list does not name firms or individuals butspells out what rules were broken, pinpoints thecommon pitfalls, and how the breaches occurredand what actions were taken. Private disciplinaryactions taken by the SGX include issuingreminders and letters of warning. Some examplesof steps taken by affected issuers to improve theirinternal controls are also mentioned.

The SGX hopes these case studies will provideinsight to market participants on the keyconsiderations the SGX deliberated on whendeciding on regulatory actions.

Also contained in the bulletin is a listingcompliance toolkit, which contains template formsfor corporate actions. The SGX hopes the toolkitwill make regulatory compliance more structured,efficient and simpler to understand.

Details are available at SGX website.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 28

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 29

Malaysia Budget2016Malaysia’s Prime Minister and Finance Minister, YABDato’ Sri Mohd Najib bin Tun Abdul Razak, deliveredhis 2016 Budget Speech on 23 October 2015.

We summarise the key items in the Budget.

Taxability of businessincome in respect ofservices to includeadvance and deferredincomeThe interpretation of whenservice income from abusiness is taxed (i.e., whethersuch income should be taxedwhen it is received orreceivable or only when theservices are actually rendered)has been a contentious issueand has been the subject of arecent court case. With effectfrom YA 2016, it is proposedthat to make it clear thatwhere a debt arises in a basisperiod in respect of servicesrendered or “to be rendered”,the amount of the debt is to betreated as gross income forthat basis period. In otherwords, as long as a debt has

arisen in respect of services(even if such services are notyet rendered), the amount ofthe debt shall be treated asgross business income.

In addition, where any sum isreceived in the course of thecarrying on of a business inrespect of rendering servicesor the use or enjoyment ofproperty, the sum receivedshall be treated as grossbusiness income even if thedebt has not yet arisen. Thiseffectively means thatadvance receipts from suchbusiness activities will bebrought to tax when received.However, if the advance sumsreceived are subsequentlyrefunded by the taxpayer, thetaxpayer can claim a taxdeduction on the refundedamounts in the basis periodwhen the refund is made.

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 30

Interest deductionsubject to DGIR beingnotified in writing whenthe interest is due to bepaidWith effect from YA 2014, anew Section 33(4) providesthat a taxpayer is only eligibleto claim a deduction inrespect of interest onb o rro win gs when suchinterest is “due to be paid”.However, the deduction wouldbe related back to the yearthe interest is payable. Witheffect from YA 2016,taxpayers may only claim thededuction if they notify theDirector General of thededuction in writing not laterthan 12 months from the endof the YA in which the interestexpense becomes “due to bepaid”.

IBA claim no longeravailable on certainbuildings that are letoutWith effect from YA 2016,certain buildings that aredeemed as industrialbuildings will not qualify forindustrial building allowance(IBA) if the building or evenpart of the building is let out.These industrial buildings areas follows: licensed privatehospitals, maternity homes,nursing homes, buildingsused for research,warehouses, buildings used

for approved servicesprojects, hotels, airports,motor racing circuits,buildings used as livingaccommodation of employeesof persons carrying on amanufacturing, hotel ortourism business or anapproved services project;and approved schools oreducational institutions.

This disallowance applies evenif the taxpayer is in thebusiness of letting outproperties. This proposalreflects clearly theGovernment’s policy torestrict the IBA claims only totaxpayers that own thebuilding and use the buildingas an industrial building fortheir own business.

Deemed disposal onreplacement of part ofan asset if the part isdepreciated separatelyunder generallyaccepted accountingprinciplesIt is proposed that where anypart of an asset is replacedwith a new part which isdepreciated separately inaccordance with generallyaccepted accountingprinciples, such part isdeemed to have beendisposed of in that basisperiod for that YA. Thequalifying expenditure of thepart shall be determined in

accordance with the generallyaccepted accountingprinciples and the residualexpenditure shall be reducedby the initial allowance andannual allowance made priorto the deemed disposal. Thisproposal takes effect from YA2016.

Special allowance onsmall value assets onlyavailable to Malaysian-incorporated small andmedium-enterprises(SME)Presently, Paragraph 19A ofSchedule 3 of the ITA allows a100% capital allowance in theyear of purchase for qualifyingassets costing not more thanRM1,300 each. The total valueon which the 100% capitalallowance can be claimed foreach YA is capped atRM13,000.

This cap, however, does notapply to a company resident inMalaysia that has a paid-upcapital in respect of ordinaryshares of RM2.5 million at thebeginning of the basis periodfor a YA. With effect from YA2016, it is proposed that suchSME must also be incorporatedin Malaysia. This proposal willtake effect from YA 2016.

Details are available at here.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | December 2015 31

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction andadvisory services. The insights and quality services wedeliver help build trust and confidence in the capitalmarkets and in economies the world over. We developoutstanding leaders who team to deliver on ourpromises to all of our stakeholders. In so doing, we playa critical role in building a better working world for ourpeople, for our clients and for our communities.

EY refers to the global organisation, and may refer to oneor more, of the member firms of Ernst & Young GlobalLimited, each of which is a separate legal entity.Ernst & Young Global Limited, a UK company limitedby guarantee, does not provide services to clients.For more information about our organisation,please visit ey.com.

© 2015 Ernst & Young LLP.

All Rights Reserved.

APAC no. 12000653

ED None

Ernst & Young LLP (UEN T08LL0859H) is a limited liability partnershipregistered in Singapore under the Limited Liability Partnerships Act (Chapter 163A).

This material has been prepared for general informational purposes onlyand is not intended to be relied upon as accounting, tax, or otherprofessional advice. Please refer to your advisors for specific advice.

www.ey.com