Embed Size (px)

Citation preview

BMO Guaranteed Investment Funds

CLIENT G

UIDE

BMO Insurance offers an extensive portfolio of innovative

individual life, accident and health insurance and annuity

products, plus a solid history of strength and unparalleled

expertise in meeting client needs. Now with BMO Guaranteed

Investment Funds to complement our income annuity

options, you can choose from an even broader range of wealth

management solutions.

BMO Insurance shares the same values that have made

our parent, BMO Financial Group, one of the most recognized and respected financial services

organizations in Canada. Our values, our culture and our vision have been vital factors in the success

that we’ve enjoyed – and that we are confident will continue for years to come.

BMO Financial Group – Who We Are

Established in 1817, BMO Financial Group is a highly diversified financial services provider based in

North America. With total assets of $633 billion and over 47,000 employees, BMO provides a broad

range of retail banking, wealth management and investment banking products and services to more

than 12 million customers.

Insurer FinancialStrength Rating

A.M. Best Company

BMO Life Assurance CompanyA (Excellent)

BMO Insurance Building on Our Strength

1

2

3

Are you…

• Concerned about reaching your retirement savings goal?

• Looking for protection of your hard-earned dollars?

• Tired of low GIC returns?

• Interested in an investment that provides more stable returns to help manage market volatility?

• Confused about what’s the right time to buy or sell investments?

If you answered YES to some or all of these questions, we encourage you to read on about BMO Guaranteed Investment Funds and talk to your advisor.

4

BMO Guaranteed Investment Funds (GIF)

With today’s low interest rates, many Canadians

like you may be concerned about how to meet

your retirement objectives without taking on more

investment risk to get higher potential returns.

Market volatility is the new reality and this presents

risk to your hard-earned savings dollars. You want

investment growth but not at the expense of capital

preservation.

With these concerns in mind, BMO Insurance has

drawn on the strength and expertise of the broader

BMO Financial Group to create a unique investment

opportunity that can be customized for you.

BMO Guaranteed Investment Funds offer:

• A full suite of non-registered and registered savings

and retirement income plans, including TFSA

• Guarantees that protect up to 100%* of your

investment

• Automatic monthly locking-in of market gains to

potentially increase the guaranteed amount you

would receive at a defined “maturity date”†

• Optional automatic locking-in of market gains

every 3 years to potentially increase the guaranteed

amount your beneficiary would receive in the event

of your death‡

• Range of fund choices available based on your

personal need, and designed by one of Canada’s

leading investment managers

• The strength and stability of BMO Financial Group,

one of Canada’s premiere financial institutions

Maximizing your retirement funds doesn’t mean having

to take higher risk. BMO Guaranteed Investment Funds

enable you to take advantage of rising markets, while

enjoying a safety net during market downturns. Sleep-

better-at-night, month, after month, knowing that your

retirement savings are protected, while automatically

locking-in market gains on a regular basis.

We can help you get to your retirement destination.

* At Maturity: 100% on deposits made at least 15 years and 75% on deposits made less than 15 years from the Maturity Date, less a proportionate amount for withdrawals; At Death: 100% on deposits made before the Annuitant is age 75 and 75% on deposits made on or after age 75, less a proportionate amount for withdrawals.

† Automatic monthly resets of the Maturity Guarantee Amount occur up to and including 10 years from the Maturity Date.‡ Automatic resets of the Death Guarantee Amount every 3rd policy anniversary up to and including the last policy anniversary before the Annuitant’s 75th birthday. Additional fee applies.

Protecting Your Retirement Savings

Selecting a Maturity Date

When you purchase a BMO GIF policy, you first select

the date at which you want your policy to mature. We

call this the Maturity Date. The term to the Maturity

Date must be between 15 and 25 years.

At your selected Maturity Date, perhaps coinciding

with your desired retirement age, guarantees are put

in place to help protect the value of your investments.

At your selected Maturity Date, you are guaranteed to

get back at least 100%* of the deposits that you make

15 years or more before the Maturity Date. Deposits

made during the last 15 years to your Maturity Date

are guaranteed at 75%*. We call the minimum

amount you’ll receive at the Maturity Date the

Maturity Guarantee Amount.

For example, if you purchase a BMO GIF policy at age

45, and choose a Maturity Date when you would be 70

(a 25 year term), deposits you make from ages 45 to 55

would be guaranteed at 100%, and deposits you make

from ages 55 to 70 would be guaranteed at 75%.

At the Maturity Date, you would receive the greater of

the Maturity Guarantee Amount or the Market Value of

your policy. This is your Maturity Benefit.

0 5 10 15 20 25

0 10 20 30 40 50 60

0 5 10 15 200 10 20 30 40 50

AGE 45

Deposits guaranteed at 100% Deposits guaranteed at 75%

AGE 70

5a

AGE 55

AGE 45

Deposits guaranteed at 100% Deposits guaranteed at 75%

AGE 100

5b

AGE 75

Oct. 15, 2013AGE 50

Automatic monthly resets

$10,000 deposit

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Policy PurchaseAGE 75

Deposits guaranteed at 100%

Initial deposit

Contract Maturity DateAGE 100

16

Automatic monthly resets No resets9

Oct. 15, 2013AGE 50

Automatic monthly resets

Resets @75%$10,000 deposit

$7,500 depositNov. 15, 2019

No resets

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Dec. 31, 2018AGE 55

Oct. 15, 2013AGE 50

Automatic monthly resets

Resets @75%$10,000 deposit

$7,500 depositNov. 15, 2019

No resets

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Dec. 31, 2018AGE 55

EvelynOct. 15, 2013AGE 65

Dec. 31, 2033AGE 85

Oct. 15, 2020AGE 72

$50,000 Initial Deposit guaranteed at 100%*

$40,000 Subsequent Deposit guaranteed at 100%*

EvelynOct. 15, 2013AGE 65

Automatic monthly resets

Deposits guaranteed at 100%* Deposits guaranteed at 75%*

No resets

Dec. 31, 2033AGE 85AGE 71 AGE 75

$50,000 Initial Deposit guaranteed at 100%*

$40,000 Subsequent Deposit guaranteed at 75%*

AmelieJan. 15, 2014AGE 50

Dec. 31, 2039AGE 75

Dec. 31, 2029AGE 65

* Any withdrawals you make from your policy will reduce your Maturity Guarantee Amount proportionately.

5

Deposit Date Age at Deposit

Deposit Amount

Death Guarantee Amount Percentage

Policy Death Guarantee Amount

December 15, 2014 64 $50,000 100%** $50,000

October 15, 2021 71 $40,000 100%** $90,000

* Any withdrawals you make from your policy will reduce your Death Guarantee Amount proportionately.**Since deposits were made before age 75.

If You Should Pass Away

Continuing with the previous example, if you were

to pass away before your selected Maturity Date,

your beneficiary would receive at least 100%* of the

deposits you make before age 75, and at least 75%*

of the deposits you make at age 75 or older.

The minimum amount your beneficiary will receive

is the Death Guarantee Amount. Your beneficiary

would receive the greater of the Death Guarantee

Amount or the Market Value of your policy. This is

your Death Benefit.

Example of the Death Guarantee Amount and Death Benefit

Evelyn, age 64, purchases a BMO GIF policy and

deposits $50,000 on December 15, 2014. She chooses

a Maturity Date of December 31, 2034 (Evelyn would

be 84). Evelyn makes another Deposit of $40,000 on

October 15, 2021 (Evelyn is 71).

Evelyn passes away at age 81. The Death Guarantee

Amount and Death Benefit are shown in the

example below.

0 5 10 15 20 25

0 10 20 30 40 50 60

0 5 10 15 200 10 20 30 40 50

AGE 45

Deposits guaranteed at 100% Deposits guaranteed at 75%

AGE 70

5a

AGE 55

AGE 45

Deposits guaranteed at 100% Deposits guaranteed at 75%

AGE 100

5b

AGE 75

Oct. 15, 2013AGE 50

Automatic monthly resets

$10,000 deposit

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Policy PurchaseAGE 75

Deposits guaranteed at 100%

Initial deposit

Contract Maturity DateAGE 100

16

Automatic monthly resets No resets9

Oct. 15, 2013AGE 50

Automatic monthly resets

Resets @75%$10,000 deposit

$7,500 depositNov. 15, 2019

No resets

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Dec. 31, 2018AGE 55

Oct. 15, 2013AGE 50

Automatic monthly resets

Resets @75%$10,000 deposit

$7,500 depositNov. 15, 2019

No resets

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Dec. 31, 2018AGE 55

EvelynOct. 15, 2013AGE 65

Dec. 31, 2033AGE 85

Oct. 15, 2020AGE 72

$50,000 Initial Deposit guaranteed at 100%*

$40,000 Subsequent Deposit guaranteed at 100%*

EvelynOct. 15, 2013AGE 65

Automatic monthly resets

Deposits guaranteed at 100%* Deposits guaranteed at 75%*

No resets

Dec. 31, 2033AGE 85AGE 71 AGE 75

$50,000 Initial Deposit guaranteed at 100%*

$40,000 Subsequent Deposit guaranteed at 75%*

AmelieJan. 15, 2014AGE 50

Dec. 31, 2039AGE 75

Dec. 31, 2029AGE 65

6

7

$25K

$50K

$75K

$100K

$125K

$150K

AGE 64 AGE 75 AGE 84

25

DGA = 100% of Deposits DGA = 75% of Deposits

AGE 81

Subsequent deposit of $40,000

Annuitant dies at age 81 with a Market Value of $95,000 and Death Guarantee Amount of $90,000

= Death Benefit of $95,000

AGE 71

Policy Market ValueDeath Guarantee Amount (DGA)

Example of the Death Benefit

64 year old with selected Maturity Date at age 84 and initial deposit of $50,000 with subsequent

deposit of $40,000

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

AGE 40 AGE 50 AGE 55 AGE 65

10

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Market Value of $75,000 with aMaturity Guarantee Amount of $140,000

= Maturity Benefit of $140,000

Highest monthlyreset at $140,000

Policy Market ValueMaturity Guarantee Amount

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

AGE 40 AGE 50 AGE 55 AGE 65

10

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Market Value of $75,000 with aMaturity Guarantee Amount of $140,000

= Maturity Benefit of $140,000

Highest monthlyreset at $140,000

Policy Market ValueMaturity Guarantee Amount

Note: For an additional fee, a Death Guarantee Reset Option is also available. Selected at issue, it

provides automatic Death Guarantee Amount resets every third policy anniversary up to and including

the last policy anniversary before your 75th birthday. Refer to the example in Scenario 3 on pages 14-16

in this Guide for further details.

At the time of Evelyn’s death, the Market Value is $95,000. Since the Death Guarantee Amount at $90,000

is less than the Market value of $95,000, there would be no top-up payment and a Death Benefit of $95,000

would be payable to Evelyn’s beneficiary.

8

Securing Market Gains During a Rising Market

Market activity is unpredictable. A powerful feature

of BMO GIFs is the ability to lock-in market gains

by increasing your Maturity Guarantee Amount

(the minimum amount you’ll receive at the Maturity

Date, less withdrawals). If the Market Value of your

investments is greater than the current Maturity

Guarantee Amount, the Maturity Guarantee Amount

is increased to the Market Value. This is referred to

as a Maturity Guarantee Reset.

Some other segregated fund products allow you to

“reset” only once or twice a year. BMO makes it easy

for you by resetting your Maturity Guarantee Amount

automatically every month. Automatic monthly

resets are done at the end of each month (“Maturity

Reset Date”) up to and including 10 years before your

selected Maturity Date.

BMO GIF automatic monthly resets will help you get

more out of market upswings. No action is required

by you or your advisor… it’s that easy! No second-

guessing whether you’ve picked the right time to

lock-in market gains.

Let’s Look at an Example:

Amelie, age 50, purchases a BMO GIF on January 15,

2015 and deposits $10,000. She selects a Maturity

Date of December 31, 2040 (a 25 year term to Amelie’s

age 75). Amelie makes no further deposits and no

withdrawals. The Maturity Guarantee Amount is

initially set to $10,000 (100% of her initial deposit).

For the first six months, the reset calculations are as

shown in the table below:

Maturity Reset Date(Year 2015)

Maturity Guarantee

Amount before

Maturity Reset Date

Market Value

of Deposits on

Maturity Reset Date

Maturity Guarantee

Amount after

Maturity Reset Date

Jan 31 $10,000 $10,100 $10,100

Feb 28 $10,100 $10,100 $10,100*

Mar 31 $10,100 $9,900 $10,100*

Apr 30 $10,100 $10,300 $10,300

May 31 $10,300 $10,200 $10,300*

Jun 30 $10,300 $10,500 $10,500

*No reset is exercised as the Market Value is lower than or equal to the Maturity Guarantee Amount. The Maturity Guarantee Amount before the reset is maintained.

After the first six months, the minimum amount

Amelie is guaranteed to receive at her selected

Maturity Date (Maturity Guarantee Amount) is

$10,500. This amount could increase as automatic

monthly resets will continue until December 31, 2030

(10 years before Amelie’s selected Maturity Date):

Maturity Guarantee Resets are done separately for

deposits guaranteed at 100% and deposits guaranteed

at 75% and a Maturity Guarantee Amount is determined

for each. The policy Maturity Guarantee Amount is

then the sum total of the two.

Helping You Get to Your Retirement Destination

Your goal may be to maximize your savings while

protecting your investments until you’re ready to

use your savings for retirement income. When you

reach your selected Maturity Date, you will receive

the greater of the Maturity Guarantee Amount (the

minimum amount we guarantee you will receive, less

withdrawals) or the Market Value of your policy. This

is your Maturity Benefit.

During the term your BMO GIF policy will help protect

you during down markets, while allowing you to take

advantage of rising markets.

9

0 5 10 15 20 25

0 10 20 30 40 50 60

0 5 10 15 200 10 20 30 40 50

AGE 45

Deposits guaranteed at 100% Deposits guaranteed at 75%

AGE 70

5a

AGE 55

AGE 45

Deposits guaranteed at 100% Deposits guaranteed at 75%

AGE 100

5b

AGE 75

Oct. 15, 2013AGE 50

Automatic monthly resets

$10,000 deposit

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Policy PurchaseAGE 75

Deposits guaranteed at 100%

Initial deposit

Contract Maturity DateAGE 100

16

Automatic monthly resets No resets9

Oct. 15, 2013AGE 50

Automatic monthly resets

Resets @75%$10,000 deposit

$7,500 depositNov. 15, 2019

No resets

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Dec. 31, 2018AGE 55

Oct. 15, 2013AGE 50

Automatic monthly resets

Resets @75%$10,000 deposit

$7,500 depositNov. 15, 2019

No resets

No resets

Dec. 31, 2023AGE 60

Dec. 31, 2033AGE 70

18

Dec. 31, 2018AGE 55

EvelynOct. 15, 2013AGE 65

Dec. 31, 2033AGE 85

Oct. 15, 2020AGE 72

$50,000 Initial Deposit guaranteed at 100%*

$40,000 Subsequent Deposit guaranteed at 100%*

EvelynOct. 15, 2013AGE 65

Automatic monthly resets

Deposits guaranteed at 100%* Deposits guaranteed at 75%*

No resets

Dec. 31, 2033AGE 85AGE 71 AGE 75

$50,000 Initial Deposit guaranteed at 100%*

$40,000 Subsequent Deposit guaranteed at 75%*

AmelieJan. 15, 2015AGE 50

Dec. 31, 2040AGE 75

Dec. 31, 2030AGE 65

10

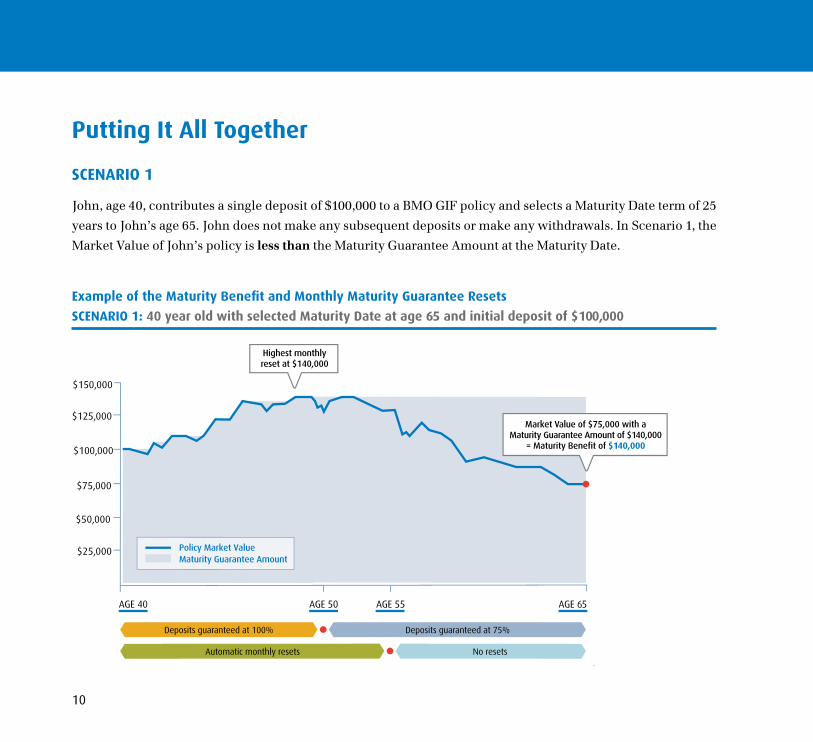

Putting It All Together

SCENARIO 1

John, age 40, contributes a single deposit of $100,000 to a BMO GIF policy and selects a Maturity Date term of 25

years to John’s age 65. John does not make any subsequent deposits or make any withdrawals. In Scenario 1, the

Market Value of John’s policy is less than the Maturity Guarantee Amount at the Maturity Date.

Example of the Maturity Benefit and Monthly Maturity Guarantee Resets

SCENARIO 1: 40 year old with selected Maturity Date at age 65 and initial deposit of $100,000

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

AGE 40 AGE 50 AGE 55 AGE 65

10

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Market Value of $75,000 with aMaturity Guarantee Amount of $140,000

= Maturity Benefit of $140,000

Highest monthlyreset at $140,000

Policy Market ValueMaturity Guarantee Amount

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

AGE 40 AGE 50 AGE 55 AGE 65

10

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Market Value of $75,000 with aMaturity Guarantee Amount of $140,000

= Maturity Benefit of $140,000

Highest monthlyreset at $140,000

Policy Market ValueMaturity Guarantee Amount

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

AGE 40 AGE 50 AGE 55 AGE 65

10

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Market Value of $75,000 with aMaturity Guarantee Amount of $140,000

= Maturity Benefit of $140,000

Highest monthlyreset at $140,000

Policy Market ValueMaturity Guarantee Amount

• Regardless of the Market Value of his investments,

John is assured of receiving at least $100,000 at

the Maturity Date. John’s beneficiary is assured of

receiving at least $100,000 if he were to die before

the Maturity Date.

• Resets of the Maturity Guarantee Amount are

automatically performed at the end of each month

until 10 years before the Maturity Date. Since the

term of the Maturity Date selected was 25 years,

monthly resets are performed for the first 15 years

(to John’s age 55). The highest monthly reset

increased the Maturity Guarantee Amount to

$140,000, effectively locking-in these market gains

at the Maturity Date.

• At the Maturity Date, the Market Value at $75,000

is less than the Maturity Guarantee Amount of

$140,000, so John would receive a top-up payment

of $65,000 making the Maturity Benefit equal

$140,000.

• At age 65, John decides to renew his BMO GIF

policy and selects a subsequent term of 20 years

to John’s age 85. The renewal deposit is $140,000

(the previous term’s Maturity Benefit). Since the

new term selected is at least 15 years, the new

Maturity Guarantee Amount is $140,000 (100%

of the renewal deposit). Since at renewal John is

also under age 75, the Death Guarantee Amount

is reset to $140,000 (since the renewal deposit is

higher than the original Death Guarantee Amount

of $100,000). If, however, John was age 75 or

older at time of renewal, there would be no Death

Guarantee Amount reset and the previous Death

Guarantee Amount of $100,000 would be carried

over to the new term.

11

12

Putting It All Together

SCENARIO 2

In Scenario 2 John also makes a subsequent deposit of $100,000 at age 57, where the Market Value of John’s policy is

again less than the Maturity Guarantee Amount at the Maturity Date.

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

AGE 40 AGE 50 AGE 55 AGE 65

12

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Maturity Guarantee Amount on 2nd deposit

= 75% of $100,000 deposit = $75,000

Maturity Guarantee Amount on 1st deposit

= Highest monthly reset at $140,000

Market Value of $200,000 with a Maturity Guarantee Amount of

$140,000 + $75,000 = $215,000 = Maturity Benefit of $215,000

Policy Market ValueMaturity Guarantee Amount

Example of the Maturity Benefit and Monthly Maturity Guarantee Resets

SCENARIO 2: 40 year old with selected Maturity Date at age 65 and initial deposit of $100,000 with

subsequent deposit of $100,000 at age 57

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

AGE 40 AGE 50 AGE 55 AGE 65

10

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Market Value of $75,000 with aMaturity Guarantee Amount of $140,000

= Maturity Benefit of $140,000

Highest monthlyreset at $140,000

Policy Market ValueMaturity Guarantee Amount

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

AGE 40 AGE 50 AGE 55 AGE 65

10

Deposits guaranteed at 100% Deposits guaranteed at 75%

Automatic monthly resets No resets

Market Value of $75,000 with aMaturity Guarantee Amount of $140,000

= Maturity Benefit of $140,000

Highest monthlyreset at $140,000

Policy Market ValueMaturity Guarantee Amount

• Regardless of the Market Value of his investments,

John will receive at least $175,000 at the Maturity

Date (100% of the initial deposit plus 75% of the

subsequent deposit since it was made less than 15

years to the Maturity Date).

• John’s beneficiary will receive at least $100,000 if

he were to die before the Maturity Date and before

John makes the subsequent deposit of $100,000.

If John was to die before the Maturity Date and

after making the subsequent deposit of $100,000,

his beneficiary would receive at least $200,000

(since John was under age 75 when he made the

subsequent deposit of $100,000, it increased the

Death Guarantee Amount by 100% of the deposit).

• In Scenario 2, the highest monthly reset increased

the Maturity Guarantee Amount to $140,000,

effectively locking-in these market gains in value at

the Maturity Date.

• Since the subsequent deposit of $100,000 was made

within 15 years to the Maturity Date, the maturity

guarantee for this deposit is at 75%, or $75,000.

• At the Maturity Date, the Market Value at $200,000

is less than the Maturity Guarantee Amount of

$215,000, so the Maturity Benefit would equal

$215,000 (a $15,000 top-up payment would be made).

• At age 65, John decides to renew his BMO GIF

policy and selects a subsequent term of 20 years

to John’s age 85. The renewal deposit is $215,000

(the previous term’s Maturity Benefit). Since the

new term selected is at least 15 years, the new

Maturity Guarantee Amount is $215,000 (100% of

the renewal deposit). Since at renewal John is also

under age 75, the Death Guarantee Amount is reset

to $215,000 (since the renewal deposit is higher

than the previous term’s Death Guarantee Amount

of $200,000).

13

Introducing the Death Guarantee Reset OptionBy selecting the Death Guarantee Reset Option†, there is the opportunity to increase the Death Guarantee Amount

by providing automatic Death Guarantee Resets every 3rd policy anniversary up to and including the last policy

anniversary before your 75th birthday. This optional benefit essentially locks-in market gains for the benefit of your

beneficiaries in the event of your death before the Maturity Date.

Let’s look again at the earlier example of the Death Benefit, but this time with the Death Guarantee Reset Option

having been selected.

Putting It All Together

SCENARIO 3

Evelyn, age 64, establishes a Contract selecting the Death Guarantee Reset Option with an Initial Deposit of

$50,000 on October 15, 2014. She chooses a Maturity Date of December 31, 2034 (when Evelyn would be age 84).

Evelyn makes a Subsequent Deposit of $40,000 on October 15, 2021 (when Evelyn is age 71). Evelyn dies at age 81.

15

• Intially, Evelyn’s beneficiary is assured of receiving at least $50,000 if Evelyn were to die before her selected

Maturity Date (Death Guarantee Amount is 100% of the Initial Deposit since it was made before age 75).

Example of the Death Benefit (with Death Guarantee Reset Option selected)

SCENARIO 3: 64 year old with selected Maturity Date at age 84 and initial deposit of $50,000 with

subsequent deposit of $40,000

$25K

$50K

$75K

$100K

$125K

$150K

AGE 64 AGE 84

25

DGA = 100% of Deposits DGA = 75% of Deposits

AGE 81

Subsequent deposit

of $40,000

Market Value of $95,000 and Death Guarantee Amount of $125,000

= Death Benefit of $125,000

DGA reset to $75,000

DGA reset to $125,000

DGA reset to $120,000

70 71 74 75 73AGE 67

Policy Market ValueDeath Guarantee Amount (DGA)

Death Reset Date

continued >>

† Additional fee applies.

• On Evelyn’s 3rd policy anniversary at age 67, the

Market Value of her Contract at $75,000 is greater

than the current Death Guarantee Amount of

$50,000; her Death Guarantee Amount is reset

to $75,000.

• On Evelyn’s 6th policy anniversary at age 70, the

Market Value of her Contract at $65,000 is less than

the current Death Guarantee Amount of $75,000;

the Death Guarantee Amount of $75,000

is maintained.

• The Subsequent Deposit made at Evelyn’s age 71

increased the Death Guarantee Amount by $40,000

to $115,000 (since the Subsequent Deposit was

made before age 75 it is guaranteed at 100%).

• At Evelyn’s 9th policy anniversary at age 73, the

Market Value of her Contract at $120,000 is greater

than the current Death Guarantee Amount of

$115,000; her Death Guarantee Amount is reset

to $120,000.

• Evelyn’s 10th policy anniversary at age 74 is the last

policy anniversary before Evelyn’s 75th birthday

and a final Death Guarantee Reset is performed.

The Market Value of her Contract at $125,000 is

greater than the current Death Guarantee Amount

of $120,000, so her Death Guarantee Amount is

reset to $125,000.

At the time of Evelyn’s death (age 81), her policy

Market Value is $95,000. Since the policy Death

Guarantee Amount at $125,000 is greater than the

Market Value of $95,000, we would make a top-up

payment of $30,000 so that the Death Benefit payable

to Evelyn’s beneficiary would be $125,000.

A summary of the Death Guarantee Resets is shown in the following table:

Death Reset Date (Annuitant’s Age)

Death Guarantee Amount before Death Reset Date

Market Value of Deposits on Death Reset Date

Death Guarantee Amount after Death Reset Date

67 $50,000 $75,000 $75,000

70 $75,000 $65,000 $75,000*

73 $115,000 $120,000 $120,000

74 $120,000 $125,000 $125,000**

* No Death Guarantee Reset is exercised as the Market Value is lower than or equal to the Death Guarantee Amount. The Death Guarantee Amount before the reset is maintained. ** This is the last policy anniversary before the Annuitant’s 75th birthday. A final Death Guarantee Reset is performed even though the policy anniversary does not fall on the normal 3 year cycle.16

Other benefits of BMO Guaranteed Investment Funds

Creditor Protection

BMO GIF policies may be protected from seizure by

creditors as long as an eligible family-class member

or an irrevocable beneficiary is designated.*

Protecting your legacy

By naming a beneficiary, a BMO GIF policy on your

death allows your estate to bypass probate. This

means you can avoid not only probate fees, but

other associated fees such as executor, legal and

accounting.

Avoiding probate† saves time and money, allowing for

a smoother transfer of assets to your inheritors. This

also protects the privacy of your bequests. Combined

with death benefit guarantees and creditor protection,

a BMO GIF policy can be an integral part of a wealth

transfer strategy.

Assuris Protection

Assuris is a not-for-profit organization that protects

Canadian policyholders if their life insurance

company should fail. Assuris will protect your

policy’s guarantee against loss for up to $60,000 or

85% of the value of your guarantee, whichever is

higher. Visit www.assuris.ca for more information.

* Creditor Protection rules depend on legislation and vary by province. It cannot be guaranteed. Please consult a legal advisor for your specific situation.

† Probate fees may not apply in Quebec.

Fund Options and Portfolio Management

Working closely with our portfolio manager, BMO Asset Management Inc., BMO Insurance offers four

distinctive BMO Guaranteed Investment Funds with exposure to North American equity and domestic fixed

income exchange traded funds (ETFs), as well as a money market fund. The balanced fund mandates of

the BMO Guaranteed Investment Funds offer investors a choice of broad exposure to Canadian or North

American based companies or a focus on income generating securities.

Refer to the Fund Profiles for full and current details of each Fund found at www.bmoinsurance.com/GIF

About BMO Asset Management

BMO Asset Management Inc. is part of BMO Global Asset Management, one of the world’s largest 50 asset

managers with over $300 billion in combined assets under management (April 2015).

BMO Asset Management is one of Canada’s leading and fastest growing issuers of ETFs with over $21 billion* in ETF managed assets.* April 2015

19

20

Your Options When You Reach the End of Your Investment Term

When you reach your selected Maturity Date, you can:

• Request the payment of the Maturity Benefit in a

lump sum; or

• Renew your policy by selecting a new Maturity Date

Not ready to take retirement income

If you do not need income at this time, you can choose

to renew your policy by selecting a new Maturity Date

(you can continue to do so until age 100).

There are many benefits to renewing your policy for

another term. You continue to benefit from the same

maturity guarantees and automatic monthly resets

provided the minimum terms for the Maturity Date

are met as described earlier. Plus, if you are under

age 75, there is the opportunity to increase your

Death Guarantee Amount (the minimum amount paid

to your beneficiary on death). If the Maturity Benefit at

renewal is greater than the previous Death Guarantee

Amount, your Death Guarantee Amount would be

increased to equal the Maturity Benefit.

Ready to take retirement income

If you need access to retirement income, you could

renew your policy with the continuation of benefits

as noted earlier. You can easily move funds from a

Registered Retirement Savings Plan (RRSP) policy to

a Registered Retirement Income Fund (RRIF) policy.

Your guarantees would stay intact. BMO Guaranteed

Investment Funds also offer a full suite of locked-in

registered retirement income plans. Minimum

required annual payments under a RRIF or other

locked-in retirement income plan will be made under

a Scheduled Withdrawal Plan (SWP). SWPs are also

available for non-registered plans. Talk to your advisor

for more information.

Alternatively, you could request at renewal to receive

the Maturity Benefit in a lump sum and use these

proceeds to purchase an income annuity. An income

annuity will guarantee an income for as long as you

live, or a term you select. You choose:

• Frequency of income payments (e.g. monthly)

• Number of income payments guaranteed to your

beneficiary in the event of your death

• If you would like your income payments to be indexed

to help protect against inflation

We recommend you speak to your advisor about what

Maturity Date may be suitable for your lifestyle needs

and to ensure you understand all your options when

you reach a Maturity Date.

Note: Any withdrawals, including RRIF withdrawals,

will reduce both the Maturity Guarantee Amount and

the Death Guarantee Amount proportionately.

21

22

Processing of Transactions

BMO Guaranteed Investment Funds offer you

various market-leading benefits that are currently

not available on the market, although they could

be viewed as more important with today’s volatile

markets. However, the processing of certain

transactions (deposits, switches) in BMO GIFs are

made once a month on a specified date. Withdrawals

from any fund and switches to the money market fund

can be made at any time on a daily basis.

Transactions processed monthly include lump

sum deposits and switches (other than to money

market), Pre-authorized Debit Plans (PADs) and

Scheduled Withdrawal Plans (SWPs). They are

processed once a month on the 20th (the transaction

date) if the requirements to complete the transaction

are submitted to us inside the required timeframe

(typically 2 to 5 days before the 20th). If we do not

receive the requirements within the required

timeframe, the transaction will be processed on the

20th of the following month.

Impact of Monthly Processing of Transactions

Some key points to consider with monthly processing:

Deposits

(i) Lump sum deposits (other than to money

market) are first made to a Money Market

Fund designated for holding purposes and

then, switched to the fund you selected on the

20th (the transaction date).

(ii) The number of units of the fund you selected to

be allocated to your contract will depend on the

value of the fund on the transaction date on the

20th, and is not based on the value of the fund

when the deposit was first made.

(iii) The number of units could be higher or lower

than had the transaction been processed on

the date you made the deposit. Therefore, if

the value of the fund on the transaction date is

higher than on the date of the deposit, you will

receive fewer units. Conversely, if the value of

the fund on the transaction date is lower, you

will receive a greater number of units.

For example, you make a deposit of $10,000 in Fund A

on January 28, 2014 when the value of the fund is

$20 per unit. The deposit will first be made to the

Holding Money Market Fund and switched to Fund A

23

on February 20, 2014. Had the deposit been processed

on January 28, 2014 (deposit date), you would have

received 500 units ($10,000 ÷ $20). Assuming that

the value of the Holding Money Market Fund did not

change and on February 20, 2014 Fund A is $25 a unit,

you will receive 400 units ($10,000 ÷ $25). The price of

the fund on January 28, 2014 is not relevant.

If circumstances have changed that a selected fund

may no longer be appropriate, you have the right to

cancel a deposit purchase order. The cancellation

must be submitted in writing before the transaction

is processed by 4:00 p.m. EST on the 15th of the month.

Switches

(i) To process a switch, the units of the initial

fund will be sold and the proceeds used

to purchase units of the new fund. Both

transactions will occur on the same day; in the

case of BMO GIFs, both transactions will be

made on the 20th (the transaction date).

(ii) The number of units of the fund you select to

be switched on the monthly transaction date

could be higher or lower than had the switch

been processed on the same day of the request.

This could be the result of market fluctuations

in the value of the fund being switched into or

the value of the fund being switched out of.

For example, on January 21, 2014 you request a

switch of 50 units out of Fund A to Fund B. On that

day, Fund A is $25 a unit and had the units been sold

then, you would have received $1,250 ($25 x 50).

On February 20, 2014, when the switch is processed,

Fund A is at $23 a unit. The amount to purchase units

of Fund B is $1,150 ($23 x 50).

If your circumstances have changed and the fund

previously selected may no longer be appropriate,

you have the right to cancel a switch order. The

cancellation must be submitted in writing before

the transaction is processed by 4:00 p.m. EST on the

15th of the month.

Please consult with your advisor to fully understand

your options.

You can withdraw your funds at any time on a daily

basis. You also have the option to switch to the money

market fund at any time on a daily basis should

market conditions or personal circumstances dictate

a more conservative investment.

Please review the transaction dates, requirements

and timelines for transactions carefully with

your advisor.

Glossary of Key Terms

Annuitant means the person on whose

life the Maturity Benefit and Death

Benefit are determined.

Beneficiary means the person or entity

entitled to receive the Death Benefit.

Death Benefit is the amount we will

pay your Beneficiary on death. It is the

greater of:

i) the Death Guarantee Amount; and

ii) the Market Value of the Contract.

Death Guarantee Amount is the

minimum amount that will be paid

to your designated Beneficiary

on your death. Withdrawals will

reduce the Death Guarantee Amount

proportionately.

Death Guarantee Reset means if at a

Death Reset Date, the Market Value of

your Deposits (guaranteed at 100%)

is greater than the Death Guarantee

Amount, the Death Guarantee Amount

will be increased to the Market Value.

Death Reset Date means every 3rd policy

anniversary up to and including the

last policy anniversary before your

75th birthday.

Fund(s) means the segregated funds

offered under the Contract.

Market Value means the basis under

which the value of the Contract, a

transaction or a Fund is calculated.

Maturity Benefit is the amount that you

will receive at your selected Maturity

Date. It is the greater of:

i) the Maturity Guarantee Amount or

ii) the Market Value of the Contract.

Maturity Date is the date that you select

when your policy will mature.

Maturity Guarantee Amount is the

minimum amount that will be paid

to you at your chosen Maturity Date.

Withdrawals will reduce the Maturity

Guarantee Amount proportionately.

Maturity Guarantee Reset means

if at a Reset Date the proportionate

Market Value of your Deposits at their

respective guarantee level is greater

than the Maturity Guarantee Amount,

the Maturity Guarantee Amount will

be increased to the proportionate

Market Value.

Maturity Reset Date means the end of

each month up until 10 years before

your selected Maturity Date.

24

Any amount that is allocated to a segregated fund is invested at the risk of the policyowner

and may increase or decrease in value.

Market values and rates of return used in the examples are for illustration purposes only to

show how certain product features work in different situations. They are not indicative of

future performance. BMO Life Assurance Company is the issuer of the BMO GIF individual

variable insurance contract referred to in the Information Folder and the guarantor of any

guarantee provisions therein. This document provides an overview of the product features

and benefits of BMO GIF. The BMO GIF Information Folder and Policy Provisions provide full

details and govern in all cases.

Insurer: BMO Life Assurance Company®Registered trade-mark of Bank of Montreal, used under licence.

For More Information, Talk to Your Advisor Today.

07/1

5-13

91

595E (2015/09/01)

bmoinsurance.com/GIF