Embed Size (px)

Citation preview

1

BMO Nesbitt BurnsFebruary 2005

2

About Implats About Implats ……. the premier . the premier platinum investmentplatinum investment

2

3

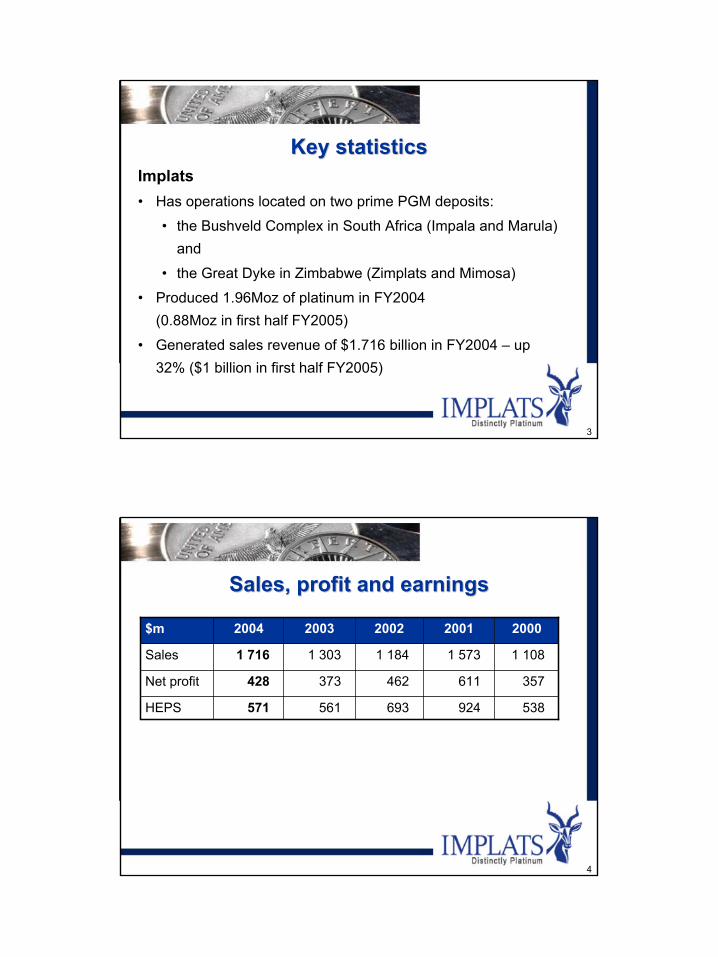

Key statisticsKey statisticsImplats• Has operations located on two prime PGM deposits:

• the Bushveld Complex in South Africa (Impala and Marula) and

• the Great Dyke in Zimbabwe (Zimplats and Mimosa)

• Produced 1.96Moz of platinum in FY2004 (0.88Moz in first half FY2005)

• Generated sales revenue of $1.716 billion in FY2004 – up 32% ($1 billion in first half FY2005)

4

Sales, profit and earnings Sales, profit and earnings

1 1081 5731 1841 3031 716Sales

538924693561571HEPS

357611462373428Net profit

20002001200220032004$m

3

5

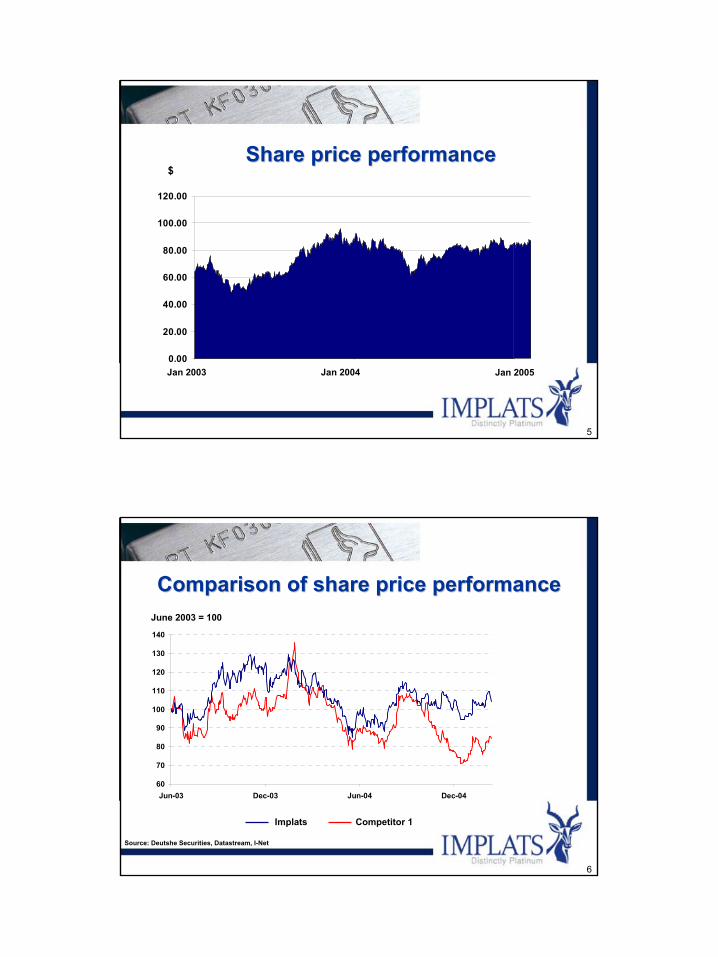

Share price performanceShare price performance

0.00

20.00

40.00

60.00

80.00

100.00

120.00

2003/01/02 2004/01/02 2005/01/02

$

Jan 2004Jan 2003 Jan 2005

6

Comparison of share price performanceComparison of share price performance

60

70

80

90

100

110

120

130

140

Jun-03 Dec-03 Jun-04 Dec-04

June 2003 = 100

Source: Deutshe Securities, Datastream, I-Net

Implats Competitor 1

4

7

Current shareholdingCurrent shareholding

South Africa 60%

UK 12%

USA/Canada 18%

Europe (other) 6%

Unclassified 4%

8

We believe in platinumWe believe in platinum

5

9

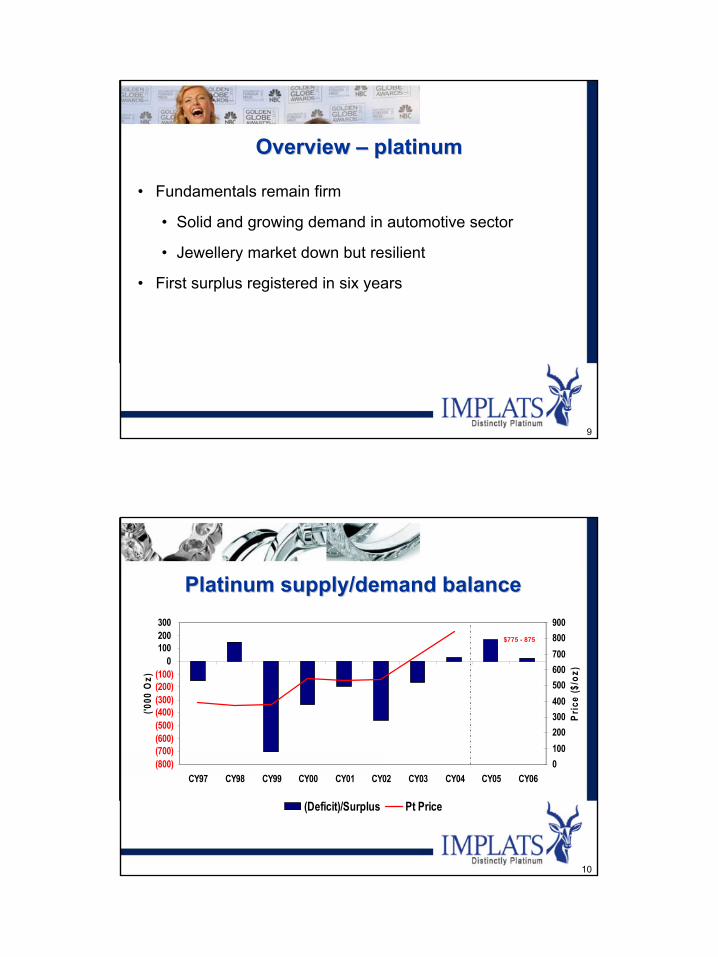

Overview Overview –– platinumplatinum

• Fundamentals remain firm

• Solid and growing demand in automotive sector

• Jewellery market down but resilient

• First surplus registered in six years

10

Platinum supply/demand balancePlatinum supply/demand balance

(800)(700)(600)(500)(400)(300)(200)(100)

0100200300

CY97 CY98 CY99 CY00 CY01 CY02 CY03 CY04 CY05 CY06

('000

Oz)

0100200300400500600700800900

Pric

e ($

/oz)

(Deficit)/Surplus Pt Price

$775 - 875

6

11

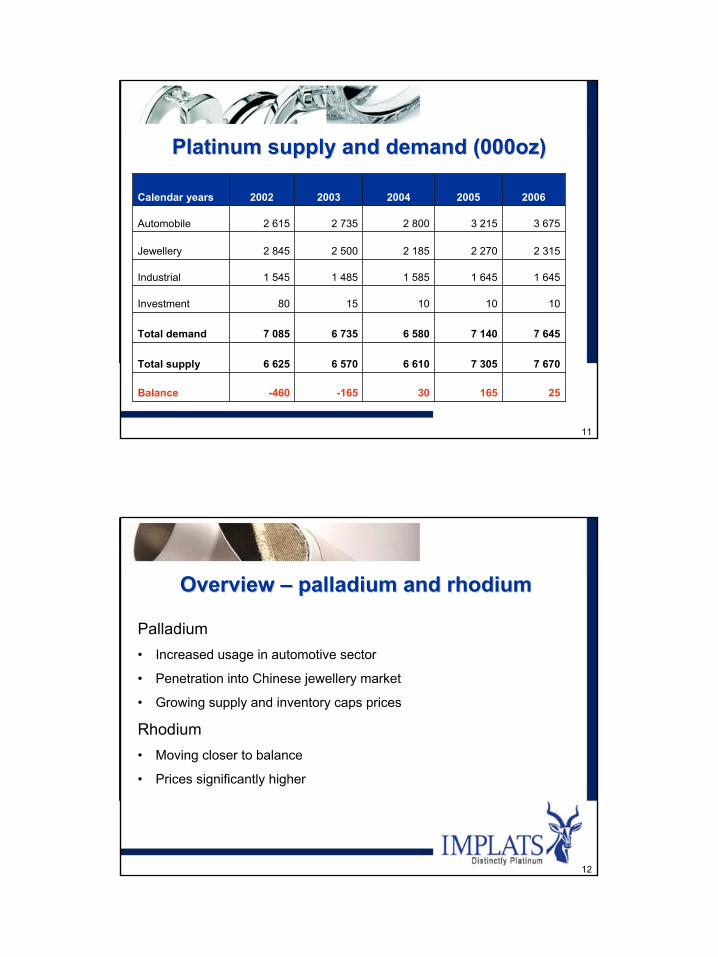

Platinum supply and demand (000oz)Platinum supply and demand (000oz)

2516530-165-460Balance

7 6707 3056 6106 570 6 625Total supply

7 6457 1406 5806 7357 085Total demand

1010101580Investment

1 6451 6451 5851 4851 545Industrial

2 3152 2702 1852 5002 845Jewellery

3 6753 2152 8002 7352 615Automobile

20062005200420032002Calendar years

12

Overview Overview –– palladium and rhodiumpalladium and rhodium

Palladium• Increased usage in automotive sector

• Penetration into Chinese jewellery market

• Growing supply and inventory caps prices

Rhodium• Moving closer to balance

• Prices significantly higher

7

13

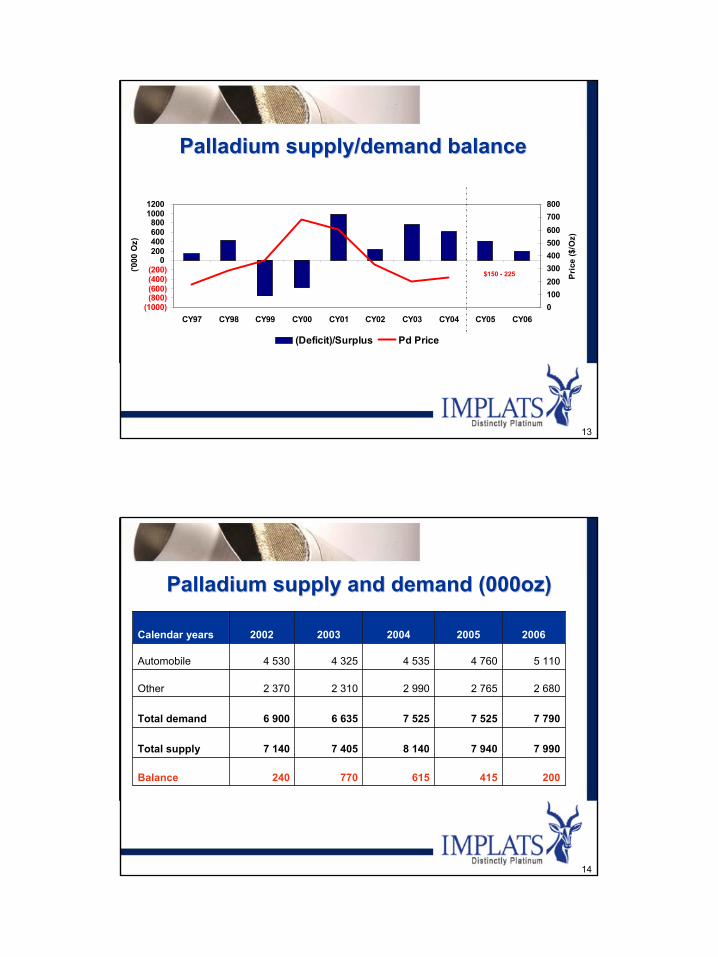

Palladium supply/demand balancePalladium supply/demand balance

(1000)(800)(600)(400)(200)

0200400600800

10001200

CY97 CY98 CY99 CY00 CY01 CY02 CY03 CY04 CY05 CY06

('000

Oz)

0100200300400500600700800

Pric

e ($

/Oz)

(Deficit)/Surplus Pd Price

$150 - 225

14

Palladium supply and demand (000oz)Palladium supply and demand (000oz)

200415615770240Balance

7 9907 9408 1407 405 7 140Total supply

7 7907 5257 5256 6356 900Total demand

2 6802 7652 9902 3102 370Other

5 1104 7604 5354 3254 530Automobile

20062005200420032002Calendar years

8

15

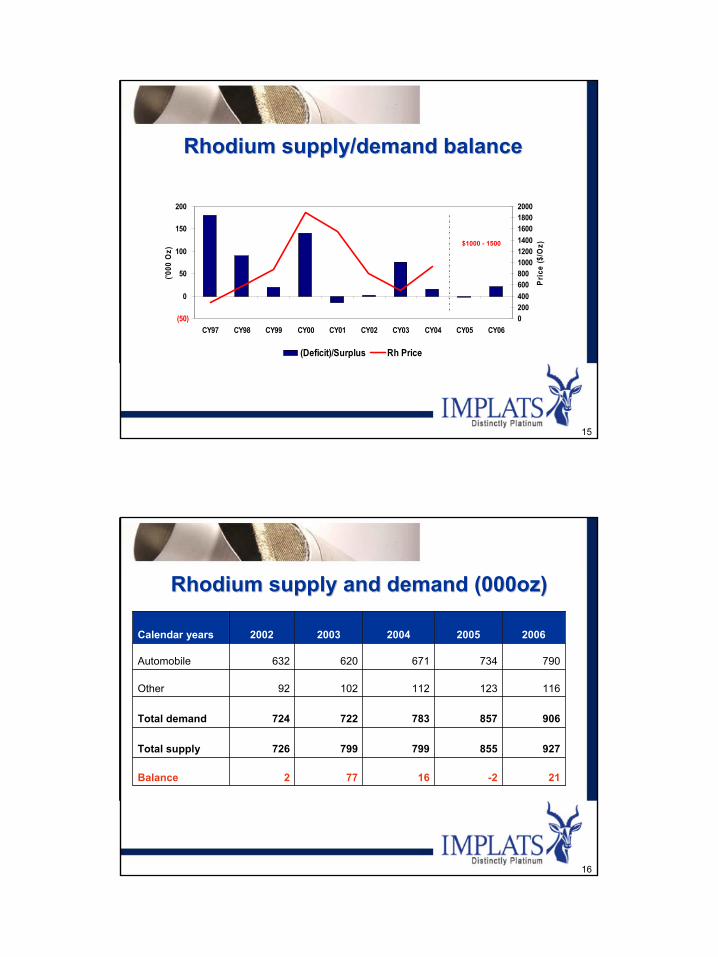

Rhodium supply/demand balanceRhodium supply/demand balance

(50)

0

50

100

150

200

CY97 CY98 CY99 CY00 CY01 CY02 CY03 CY04 CY05 CY06

('000

Oz)

0200400600800100012001400160018002000

Pric

e ($

/Oz)

(Deficit)/Surplus Rh Price

$1000 - 1500

16

Rhodium supply and demand (000oz)Rhodium supply and demand (000oz)

21-216772Balance

927855799799 726Total supply

906857783722724Total demand

11612311210292Other

790734671620632Automobile

20062005200420032002Calendar years

9

17

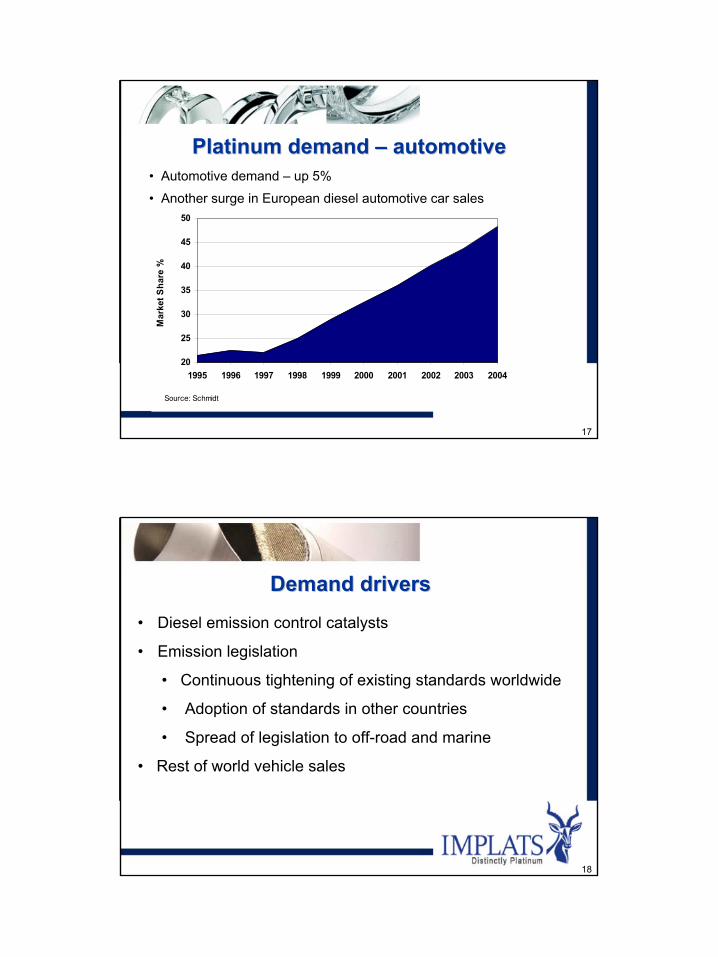

Source: Schmidt

20

25

30

35

40

45

50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Mar

ket S

hare

%Platinum demand Platinum demand –– automotiveautomotive

• Automotive demand – up 5%

• Another surge in European diesel automotive car sales

18

• Diesel emission control catalysts

• Emission legislation

• Continuous tightening of existing standards worldwide

• Adoption of standards in other countries

• Spread of legislation to off-road and marine

• Rest of world vehicle sales

Demand driversDemand drivers

10

19

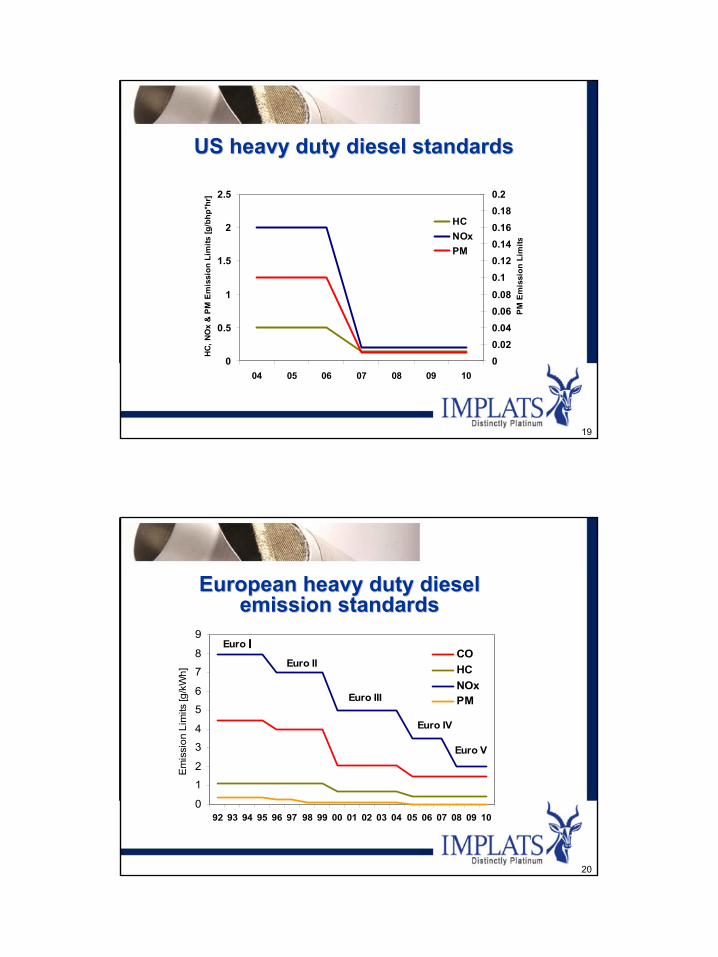

0

0.5

1

1.5

2

2.5

04 05 06 07 08 09 10

HC,

NO

x &

PM E

mis

sion

Lim

its [g

/bhp

*hr]

00.020.040.060.08

0.10.120.140.160.180.2

PM

Em

issi

on L

imits

HCNOxPM

US heavy duty diesel standardsUS heavy duty diesel standards

20

0

1

2

3

4

5

6

7

8

9

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Em

issi

on L

imits

[g/k

Wh]

COHCNOxPM

Euro IEuro II

Euro III

Euro IV

Euro V

European heavy duty diesel European heavy duty diesel emission standardsemission standards

11

21

• Require use of oxidation catalyst to convert hydrocarbonsand carbon monoxide

• Optional use of diesel particulate filters (DPF) to eliminatesoot

• Removes hydrocarbons, carbon monoxide andcomponents of particulate matter

Current diesel emission control catalystsCurrent diesel emission control catalysts

Oxidation catalyst

22

Diesel emission control catalystsDiesel emission control catalysts

• Particulate matter

• NOX emissions

12

23

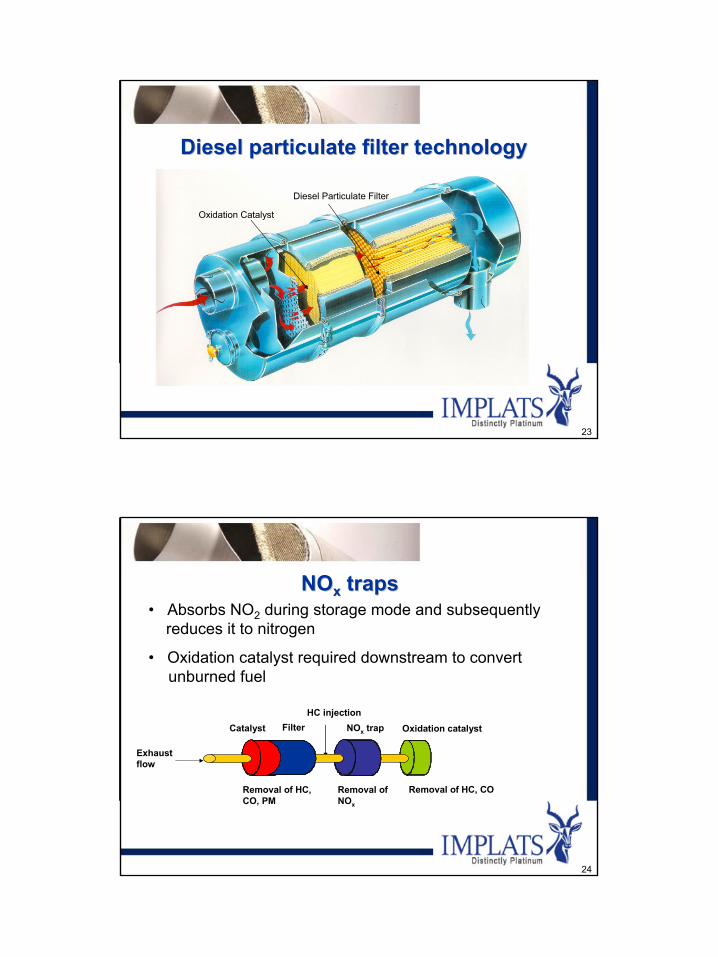

Diesel particulate filter technologyDiesel particulate filter technology

Oxidation Catalyst

Diesel Particulate Filter

24

• Absorbs NO2 during storage mode and subsequently reduces it to nitrogen

• Oxidation catalyst required downstream to convert unburned fuel

NONOxx trapstraps

Removal of HC, CO

Catalyst NOx trap Oxidation catalyst

Removal of NOx

Removal of HC, CO, PM

HC injectionFilter

Exhaust flow

13

25

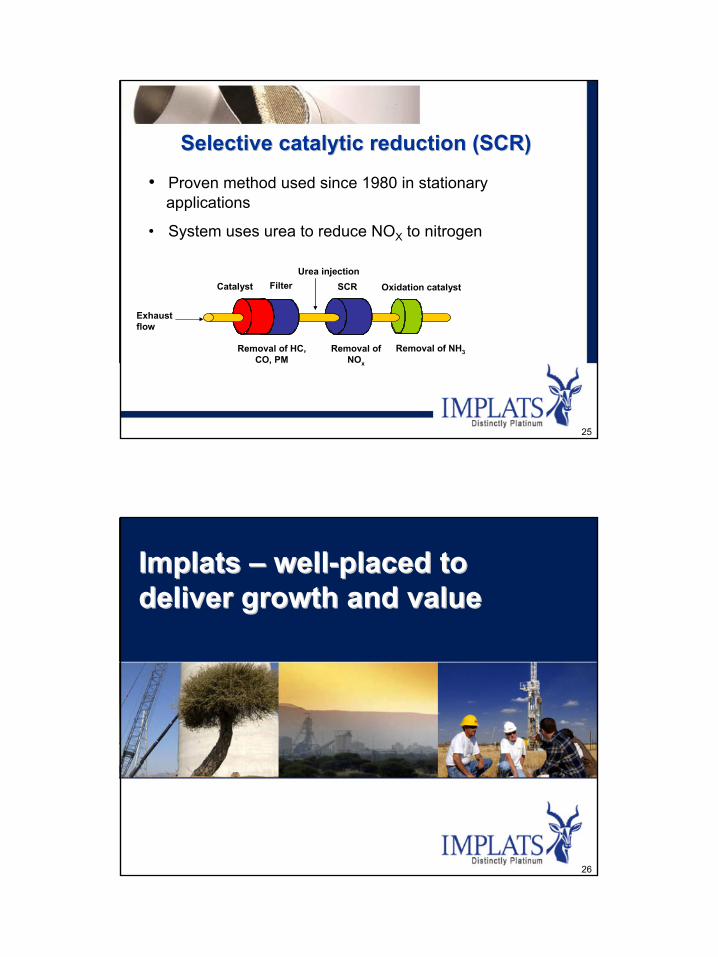

• Proven method used since 1980 in stationaryapplications

• System uses urea to reduce NOX to nitrogen

Removal of NH3

Catalyst SCR Oxidation catalyst

Removal of NOx

Removal of HC, CO, PM

Urea injection

Selective catalytic reduction (SCR)Selective catalytic reduction (SCR)

Filter

Exhaust flow

26

Implats Implats –– wellwell--placed to placed to deliver growth and valuedeliver growth and value

14

27

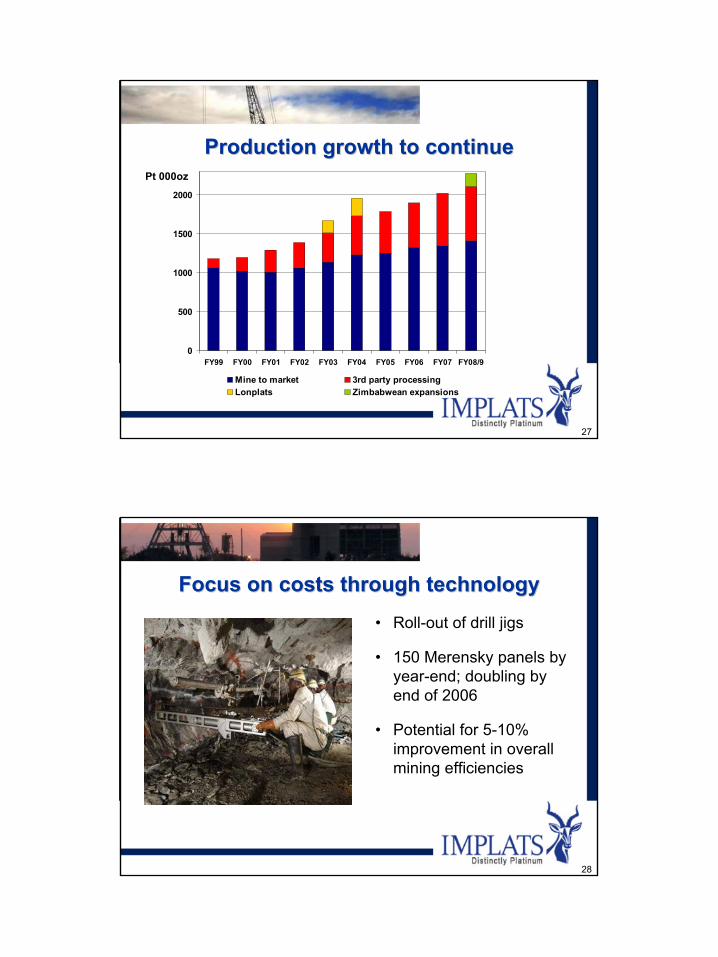

Production growth to continueProduction growth to continuePt 000oz

0

500

1000

1500

2000

FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08/9

Mine to market 3rd party processingLonplats Zimbabwean expansions

28

Focus on costs through technologyFocus on costs through technology• Roll-out of drill jigs

• 150 Merensky panels by year-end; doubling by end of 2006

• Potential for 5-10% improvement in overall mining efficiencies

15

29

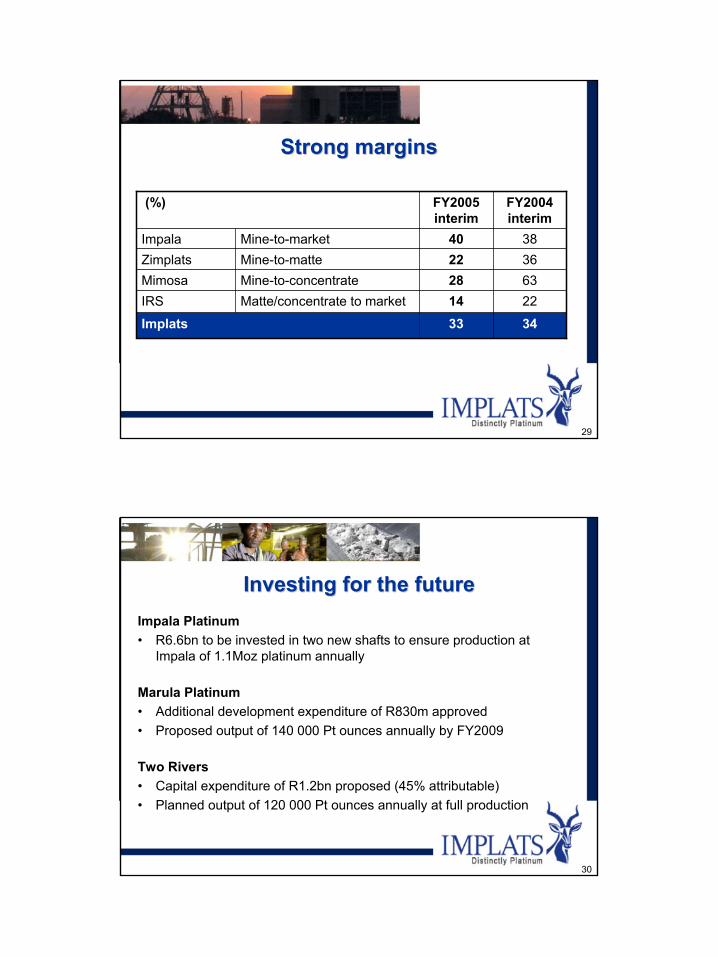

Strong marginsStrong margins

3433Implats2214Matte/concentrate to marketIRS6328Mine-to-concentrateMimosa3622Mine-to-matteZimplats3840Mine-to-marketImpala

FY2004interim

FY2005interim

(%)

30

Investing for the futureInvesting for the futureImpala Platinum• R6.6bn to be invested in two new shafts to ensure production at

Impala of 1.1Moz platinum annually

Marula Platinum• Additional development expenditure of R830m approved• Proposed output of 140 000 Pt ounces annually by FY2009

Two Rivers• Capital expenditure of R1.2bn proposed (45% attributable)• Planned output of 120 000 Pt ounces annually at full production

16

31

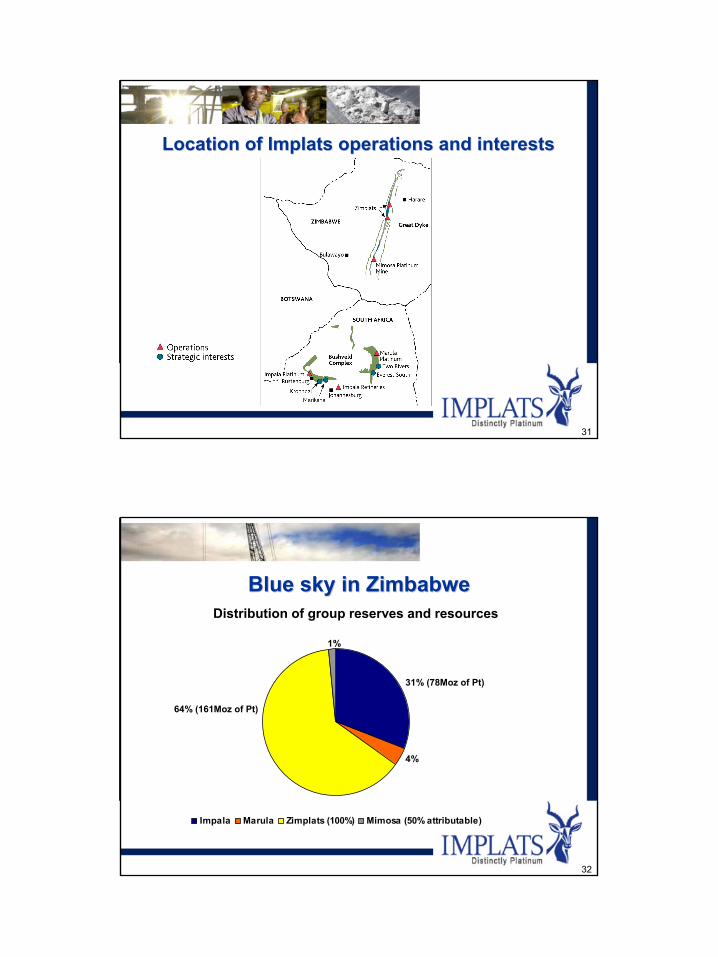

Location of Implats operations and interestsLocation of Implats operations and interests

32

Impala Marula Zimplats (100%) Mimosa (50% attributable)

Blue sky in ZimbabweBlue sky in Zimbabwe

31% (78Moz of Pt)

64% (161Moz of Pt)

Distribution of group reserves and resources

1%

4%

17

33

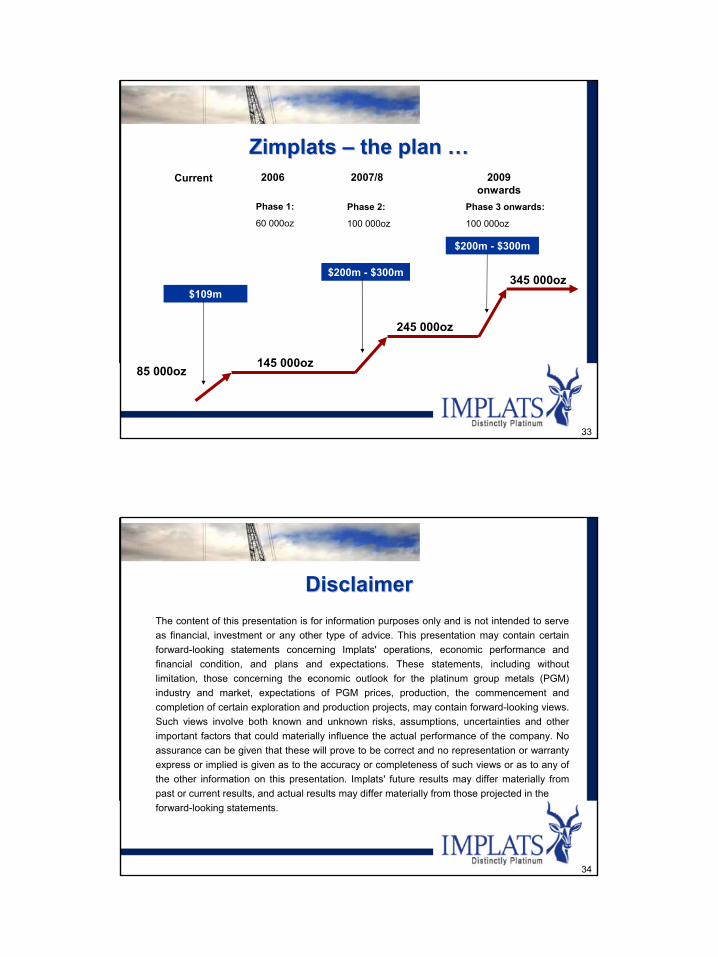

Zimplats Zimplats –– the plan the plan ……

85 000oz145 000oz

245 000oz

345 000oz

Current 2006 2007/8 2009onwards

Phase 1:

60 000oz

Phase 2:

100 000oz

Phase 3 onwards:

100 000oz

$109m

$200m - $300m

$200m - $300m

34

DisclaimerDisclaimerThe content of this presentation is for information purposes only and is not intended to serve as financial, investment or any other type of advice. This presentation may contain certain forward-looking statements concerning Implats' operations, economic performance and financial condition, and plans and expectations. These statements, including without limitation, those concerning the economic outlook for the platinum group metals (PGM) industry and market, expectations of PGM prices, production, the commencement and completion of certain exploration and production projects, may contain forward-looking views. Such views involve both known and unknown risks, assumptions, uncertainties and other important factors that could materially influence the actual performance of the company. No assurance can be given that these will prove to be correct and no representation or warranty express or implied is given as to the accuracy or completeness of such views or as to any of the other information on this presentation. Implats' future results may differ materially from past or current results, and actual results may differ materially from those projected in theforward-looking statements.

18