Embed Size (px)

DESCRIPTION

Gazprom Export Global Newsletter

Citation preview

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 1

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

Page 5

Page 14

© Gazprom Export

www.gazpromexport.com | [email protected] +7 (499) 503-61-61 | [email protected]

Page 10

Gazprom Export Global Newsletter

Elena Burmistrova, Gazprom Export Director General –

2014: Turning Challenges into Opportunities

Small Scale LNG in Perspective – Developments and Potential in Asia

Gazprom Pushes the Boundaries of Global LNG Trading

Page 4

Safeguarding Europe’s Heating Season

2

BLUE FUELGazprom Export Global Newsletter

Publishers Contact Info:www.gazpromexport.com | [email protected] +7 (499) 503-61-61 | [email protected]

To Our Readers: Safeguarding Europe’s Heating Season ...............4

Elena Burmistrova, Gazprom Export Director General – 2014: Turning Challenges into Opportunities ................................5

Blue Corridor NGV Rally 2014: Successes and Challenges .............7

Gazprom Export Volumes of Active Gas in European UGSs Exceed 5 bcm .....................................................9

GM&T France at MGIMO 2nd International Alumni Forum. ............9

Gazprom Pushes the Boundaries of Global LNG Trading ..............10

GM&T Completes First Ship-to-Ship LNG Transfer at Sea ..........12

Did You Know ..................................................................................13

Small Scale LNG in Perspective – Developments and Potential in Asia ...............................................14

Gazprom Germania Supports Russian Language Competition .....19

Gazprom Germania Brings Mariinsky Orchestra to Berlin .............20

Gazprom Goes Twitter ....................................................................21

In this issueDecember 2014/ Vol. 7/ Issue 6

4

In the complicated case of the non-fulfillment of contractual obligations by Ukraine, which had resulted in the accumulation of an outstanding debt of $5.3bn for gas that was delivered and consumed but not paid for, Gazprom, as the major purveyor of energy to Europe and Turkey, has acted responsibly and in good faith.

The trilateral negotiations involving Russia, Ukraine and the European Union culminated in an interim agreement signed on 31 October in Brussels, which was widely viewed as a sensible compromise guaranteeing at least temporary relief. The agreement stipulates that until 31 March 2015, Ukraine will pay the arrears and will also purchase 4 bcm of Gazprom’s gas.

We at Gazprom Export remain fully and firmly committed to the principle pacta sunt servanda, and expect all our counterparts to honor their obligations that have been written, signed and sealed.

As such, we note with satisfaction that as of 9 December 2014 supplies of Russian gas to Ukraine have resumed following the pre-payment of $378.22m from Naftogaz Ukrainy for the supply of 1 bcm in the month of December.

The agreed supplies for Ukraine will mitigate the risk of illegal off-take of Russian gas this winter which unfortunately had happened previously, as publicly admitted by one of the former Ukrainian presidents. However, it has been duly noted that Ukraine’s underground gas storages (UGS) which are used to sustain transit supplies to Europe during peak demand were not sufficiently filled. No less worrisome were reports of occasional off-take from the UGS facilities for Ukrainian domestic consumption.

In view of these persisting uncertainties, Gazprom Export took extra precautions to ensure uninterrupted deliveries to our

European clients. In November, Gazprom Export’s volumes of active gas in European UGSs exceeded 5 bcm. This is 1.5 times more than the level reached in the middle of November 2013. The maximum daily output from the European UGSs used by Gazprom Export will total 80 mcm in the coming winter. With an off-take of 80 mcm, our reserves in European UGSs would last for around 70-75 days, should any unforeseen transit disruptions occur.

On top of that, Gazprom has filled up its UGSs in Russia. Although gas molecules extracted in Russia’s Northern regions would have to travel a larger distance to meet additional demand by European consumers, these extra reserves could still serve as a valuable back-up.

Underground gas storages provide a sustainable operational mode and serve as a balancing mechanism for the European energy system in periods of peak demand. These activities demonstrate once again that Gazprom Group is fully committed to enhancing energy security in Europe, one of the company’s key priorities.

Despite the natural drive for diversifying its customer base, Gazprom Export is fully committed to its long-standing and trustworthy European partners with whom we share a history of efficient and beneficial cooperation for more than 40 years. Gazprom Export continues to pursue a diversification strategy that not only increases our market reach, multiplies export gas destinations and business clientele, but also further enhances existing relationships with our customers in Europe.

We are cautiously optimistic that in spring 2015 Gazprom Export and the entire Gazprom Group will continue to be able to follow their fundamental business interests and contribute to European energy security as reliably as in the past decades.

To Our Readers: Safeguarding Europe’s Heating Season

Sergei Komlev, Head of Contract Structuring and Price Formation Department, Gazprom Export

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 5

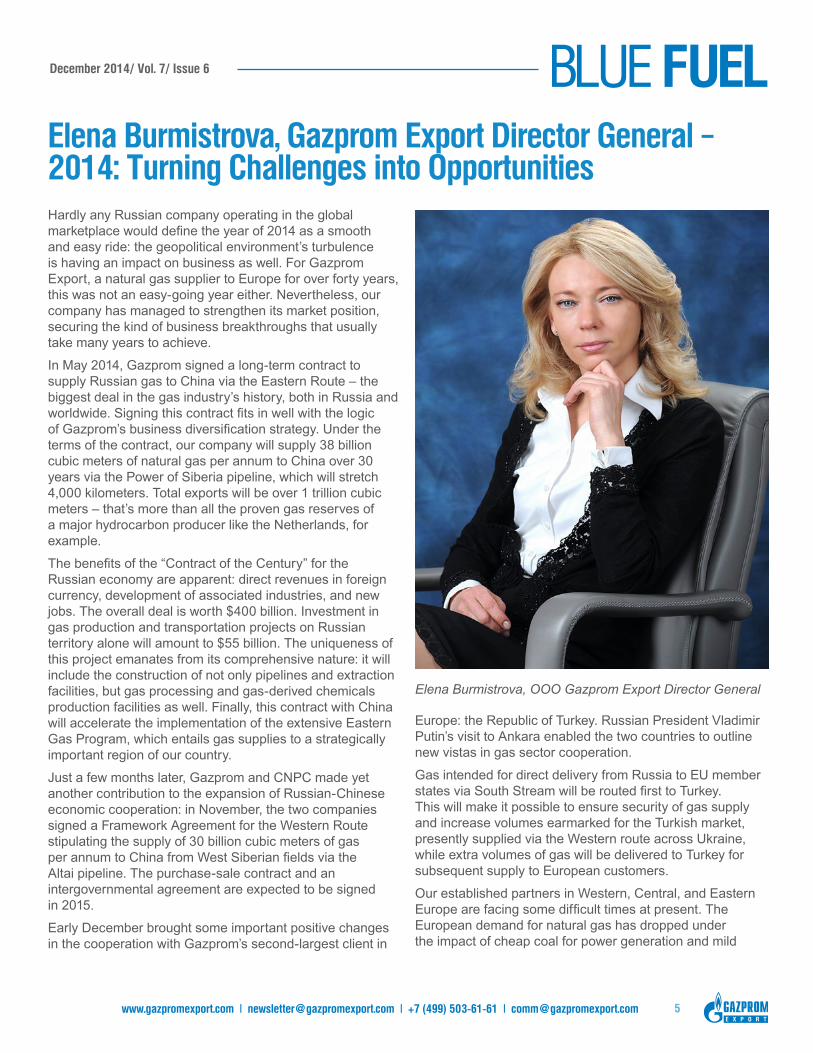

Elena Burmistrova, Gazprom Export Director General – 2014: Turning Challenges into Opportunities Hardly any Russian company operating in the global marketplace would define the year of 2014 as a smooth and easy ride: the geopolitical environment’s turbulence is having an impact on business as well. For Gazprom Export, a natural gas supplier to Europe for over forty years, this was not an easy-going year either. Nevertheless, our company has managed to strengthen its market position, securing the kind of business breakthroughs that usually take many years to achieve.

In May 2014, Gazprom signed a long-term contract to supply Russian gas to China via the Eastern Route – the biggest deal in the gas industry’s history, both in Russia and worldwide. Signing this contract fits in well with the logic of Gazprom’s business diversification strategy. Under the terms of the contract, our company will supply 38 billion cubic meters of natural gas per annum to China over 30 years via the Power of Siberia pipeline, which will stretch 4,000 kilometers. Total exports will be over 1 trillion cubic meters – that’s more than all the proven gas reserves of a major hydrocarbon producer like the Netherlands, for example.

The benefits of the “Contract of the Century” for the Russian economy are apparent: direct revenues in foreign currency, development of associated industries, and new jobs. The overall deal is worth $400 billion. Investment in gas production and transportation projects on Russian territory alone will amount to $55 billion. The uniqueness of this project emanates from its comprehensive nature: it will include the construction of not only pipelines and extraction facilities, but gas processing and gas-derived chemicals production facilities as well. Finally, this contract with China will accelerate the implementation of the extensive Eastern Gas Program, which entails gas supplies to a strategically important region of our country.

Just a few months later, Gazprom and CNPC made yet another contribution to the expansion of Russian-Chinese economic cooperation: in November, the two companies signed a Framework Agreement for the Western Route stipulating the supply of 30 billion cubic meters of gas per annum to China from West Siberian fields via the Altai pipeline. The purchase-sale contract and an intergovernmental agreement are expected to be signed in 2015.

Early December brought some important positive changes in the cooperation with Gazprom’s second-largest client in

Europe: the Republic of Turkey. Russian President Vladimir Putin’s visit to Ankara enabled the two countries to outline new vistas in gas sector cooperation.

Gas intended for direct delivery from Russia to EU member states via South Stream will be routed first to Turkey. This will make it possible to ensure security of gas supply and increase volumes earmarked for the Turkish market, presently supplied via the Western route across Ukraine, while extra volumes of gas will be delivered to Turkey for subsequent supply to European customers.

Our established partners in Western, Central, and Eastern Europe are facing some difficult times at present. The European demand for natural gas has dropped under the impact of cheap coal for power generation and mild

Elena Burmistrova, OOO Gazprom Export Director General

6

weather conditions. Moreover, demand for gas is also falling in the industrial sectors, which are still struggling to recover from the economic crisis. Transit via Ukraine is an additional risk factor for our export supplies.

Of course, all this has had an impact on Russian gas exports in 2014. All the same, Gazprom remains Europe’s leading gas supplier, strictly and conscientiously fulfilling its contractual obligations. We are confident that despite some temporary problems, natural gas is destined to play a key role in the continent’s fuel mix. It remains one of the most environmentally friendly, economical, and readily-available energy sources. We believe in the future of natural gas, the applications for which are expanding along with technological development.

We believe in the future of natural gas, the applications for which are expanding along with technological development.

For instance, the past year has been extremely successful for promoting natural gas as a motor fuel. Methane has established itself as an affordable green alternative fuel for automotive and marine transport. In 2014, Gazprom Export teamed up with Germany’s E.ON and other European companies to organize the eighth annual Blue Corridor Rally for natural gas vehicles (NGVs). In 24 days, the NGV convoy drove 6,600 kilometers (4,100 miles) along European roads. Twelve cities hosted roundtable discussions at which European politicians, analysts, and executives discussed the outlook for

developing the use of gas-motor fuel and the obstacles in its way. The European market has already green-lighted natural gas as a transportation fuel, and if the Europeans continue to pursue their climate goals, Gazprom could contribute even more toward creating the infrastructure required for using eco-friendly and economical natural gas as a motor fuel.

In 2014, Gazprom has set itself fundamentally new objectives for the years ahead. We are facing a great deal of work: over the next few years, we will be busy putting the agreement with China into practice. We will also design some new pipelines: to China via the Western Route and to Turkey across the Black Sea. We will also maintain an active presence in our traditional European market, in the hope that common sense and the need for environmental improvements will lead European regulators to let market mechanisms start working again. Natural gas, unlike renewable energy sources, needs no subsidies; what it does need though is competition on equal terms, a level playing field. In the 21st Century, it is deplorable to watch the coal-fired power industry experience a revival in Europe thanks to counterproductive regulation, blocking the path of power plants fueled by natural gas – the most eco-friendly fossil fuel. Business and common sense needs this distortion to be rectified.

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 7

31 October 2014 saw the successful conclusion of the eighth annual Blue Corridor Rally for natural gas vehicles (NGVs). The teams and their cars have returned to their home cities of Moscow, St. Petersburg, Naberezhnye Chelny, Ljubljana, and beyond.

In 24 days, the compressed natural gas (CNG) powered cars drove over 6,600 kilometers (4,100 miles) across 17 European countries: Russia, Estonia, Latvia, Lithuania, Poland, Czech Republic, Germany, Austria, Liechtenstein, Switzerland, Italy, Slovenia, Croatia, Serbia, Hungary, Slovakia, and Belarus. The Blue Corridor Rally and its associated vehicles involved a total of 28 cars (22 models) from Europe’s leading automakers. Eleven cities along the route hosted roundtable discussions and conferences attended by representatives of national and regional governments, public transit authorities, the automotive industry, equipment suppliers, and the media. Rally participants were invited to the openings of two natural gas fueling stations in the cities of Bamberg, Germany (following reconstruction) and Most, Czech Republic (a new CNG filling station).

As in previous years, the Blue Corridor NGV Rally 2014 was organized by Gazprom Export and Germany’s E.ON. This year they were joined by a young Russian company, Gazprom Gazomotornoye Toplivo. As well as the organizers, Blue Corridor participants and event sponsors included the following companies (listed alphabetically): BRC, Cavagna Group, the CNG Auto portal, Comita, Eesti Gaas, Gazprom Germania, Gazprom Transgaz Belarus, NGV Italy, NGVRUS, NIS, Nordeka, Panrusgas, Promgas, Raritek, SG Dujos Auto, Titan North-West, and VEMEX.

The Blue Corridor NGV Rally’s main aim was to demonstrate the environmental and economic advantages of natural gas compared to conventional oil-based motor fuels. While the organizers displayed a variety of the latest natural gas-fueled cars, rally participants were also interested in seeing firsthand how Europe’s NGV market is developing, taking a look at the latest trends, and learning more about the current barriers for further growth of the sector.

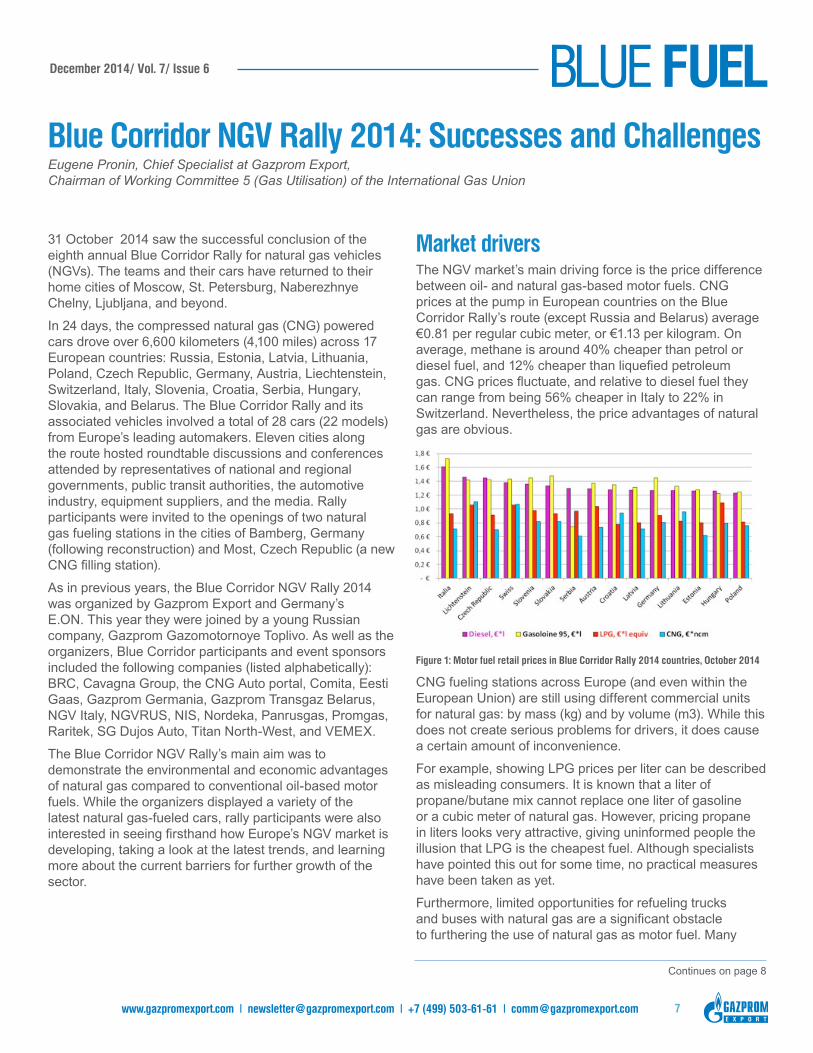

Market driversThe NGV market’s main driving force is the price difference between oil- and natural gas-based motor fuels. CNG prices at the pump in European countries on the Blue Corridor Rally’s route (except Russia and Belarus) average €0.81 per regular cubic meter, or €1.13 per kilogram. On average, methane is around 40% cheaper than petrol or diesel fuel, and 12% cheaper than liquefied petroleum gas. CNG prices fluctuate, and relative to diesel fuel they can range from being 56% cheaper in Italy to 22% in Switzerland. Nevertheless, the price advantages of natural gas are obvious.

Figure 1: Motor fuel retail prices in Blue Corridor Rally 2014 countries, October 2014

CNG fueling stations across Europe (and even within the European Union) are still using different commercial units for natural gas: by mass (kg) and by volume (m3). While this does not create serious problems for drivers, it does cause a certain amount of inconvenience.

For example, showing LPG prices per liter can be described as misleading consumers. It is known that a liter of propane/butane mix cannot replace one liter of gasoline or a cubic meter of natural gas. However, pricing propane in liters looks very attractive, giving uninformed people the illusion that LPG is the cheapest fuel. Although specialists have pointed this out for some time, no practical measures have been taken as yet.

Furthermore, limited opportunities for refueling trucks and buses with natural gas are a significant obstacle to furthering the use of natural gas as motor fuel. Many

Blue Corridor NGV Rally 2014: Successes and ChallengesEugene Pronin, Chief Specialist at Gazprom Export, Chairman of Working Committee 5 (Gas Utilisation) of the International Gas Union

Continues on page 8

8

Continued from page 5

Blue Corridor NGV Rally 2014: Successes and Challenges

stations lack NGV2 fuel nozzles. By no means all stations have NGV1-NGV2 standard adaptors either.

Some stations have dispensers with both kinds of nozzles - but heavy-duty vehicles can be refueled only by prior agreement, since the station is not a licensed retailer (refueler) for buses and trucks.

Refueling for light vehicles isn’t problem-free either. It is often the case that a dispenser with two NGV1 nozzles can only refuel cars from one side at a time.

Developing gas refueling infrastructure and regulationReducing the harmful environmental impact of emissions from transportation remains one of the European Union’s key priorities. As such, natural gas is the only commercially attractive, technologically developed, and plentiful alternative to gasoline or diesel fuel.

Much has been done in recent years to promote the large-scale adoption of CNG and liquefied natural gas (LNG). Yet, the Blue Corridor Rally 2014 showed that opportunities to drive all the way across Europe on natural gas alone remain limited. Gas refueling infrastructure has been well developed in Bulgaria, Germany, Italy, Russia, Czech Republic, Switzerland, and Sweden. However, even these countries have some dead zones without any CNG fueling stations.

The only European country with a developed national gas refueling network is the Principality of Liechtenstein. With its total 380 kilometers of roads (as of November 2011), Liechtenstein has three CNG fueling stations - giving it a network density of 1:127. That’s the best indicator in Europe!

It would be premature to say that commercial NGVs can move freely throughout Europe. The European market for natural gas as a transportation fuel is entering a new phase of development: the investment phase. The past decades have been spent on gradually building support among automakers, transport companies, and politicians. Now it’s time for the key players to come to the fore: investors. In the immediate future, it is necessary to establish comfortable conditions for large-scale, long-term investment in developing gas refueling infrastructure in Europe.

The key role of refueling infrastructure has been recognized at the EU level; new rules adopted on 1 October 2014 oblige the governments of EU member states to take concrete measures to ensure guaranteed access to fueling stations. Most importantly, the EU will participate in co-funding infrastructure.

Ideally, CNG fueling stations should be built every 150 kilometers along Trans-European Transport Network (TEN-T) roads, with LNG stations every 400 kilometers. In cities and suburbs, CNG stations should be no more than 15 km apart by 2025.

Based on these EU recommendations, the number of CNG fueling stations in Europe

Continues on page 9

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 9

Gazprom Export Volumes of Active Gas in European UGSs Exceed 5 bcm

GM&T France at MGIMO 2nd International Alumni Forum: “Demand Security Is a Prerequisite to Supply Security”

In November, Gazprom Export’s volumes of active gas in European underground gas storages (UGS) have exceeded 5 bcm. This is 1.5 times more than the level reached in the middle of November 2013. Gas injections continue in anticipation of the coming winter season.

The maximum daily output of UGSs used by Gazprom Export will exceed 80 mcm in the coming winter.

Enhancing energy security in Europe is one of the key priorities of Gazprom Group – and storing gas in UGSs is one of the key elements in achieving this goal. Underground gas storages provide a sustainable operational mode and serve as a balancing mechanism for the European energy system in periods of peak demand.

The President of Gazprom Marketing & Trading France Iouri Virobian joined the 2nd International Alumni Forum of the prestigious Moscow State Institute of International Relations (MGIMO), where he graduated with Honours before starting his career in the energy business, to participate in a debate dedicated to Europe’s energy security.

The Forum, which coincided with the celebration of the institution’s 70th anniversary in the presence of Russian President Vladimir Putin and Minister for Foreign Affairs Sergey Lavrov, gathered hundreds of researchers, former and current students to discuss latest global economic and social developments.

Speaking alongside economists and representatives from various energy companies, Iouri Virobian agreed with his

fellow panellists on the issue of security of demand being linked to the overall problematic of security of supply as far as Europe is concerned, and on the importance of signals being sent to private investors.

Iouri Virobian highlighted that mid-term uncertainties loom over Europe’s future natural gas consumption in spite of the economic and environmental benefits of this energy source. Natural gas could indeed be a perfect match for the energy transition undertaken in some European countries such as France and Germany. Those transitions - all part of the European Union’s ambitious goals on GHG emission cuts - aim at a thorough rethink of what constitutes a sustainable energy mix, notably through the development of renewable energy sources.

(that is, from the Atlantic to the Urals) should be increased at least ten-fold. At present, there are only 4,200 stations in this area. To ensure good infrastructure coverage the required number of LNG fueling stations can be estimated at 18,000. Construction of this scale would require investments totaling around €20 billion.

And there is another very important condition to boost the NGV sector: national rules for the design, construction, and use of natural gas, hydrogen, and electricity refueling/recharging stations and dispensers should be harmonized within the EU by the end of 2016, and then throughout Europe.

Continued from page 8

Blue Corridor NGV Rally 2014: Successes and Challenges

Continues on page 10

10

However, the energy output of renewable energy is prone to short-term fluctuations that require to be balanced by sophisticated technology in order to ensure energy security and stability. As a clean, flexible and abundant energy source, natural gas has a key role to play, Iouri Virobian stressed. Natural gas is already widely used within the European Union, where it represents 24% of primary energy sources, and could efficiently complement any energy mix shifts that are to be implemented.

Iouri Virobian added that natural gas should not only be a transition “facilitator”, but a key fuel in a new, widely decarbonised energy mix. Natural gas used in maritime or road transportation – sectors largely contributing to GHG emissions – has already demonstrated its environmental value and represents another way to improve energy security in the future.

Yet, natural gas demand in Europe is stagnating, Iouri Virobian recalled, stressing that more worrying than the economic reasons behind the situation was the lack of political reaction to this trend. Current political signals sent to investors, or consumers, are not favouring any increase in natural gas demand in the short-term. Such a prospect is, however, a prerequisite to ensure the needed involvement and investment on the business side, Iouri Virobian insisted.

Securing future energy demand is therefore pivotal to setting the conditions for tomorrow’s supply security, Iouri Virobian concluded, agreeing on its importance with other panellists.

Over the past decade, the growth of short-term LNG trading has been nothing short of remarkable. From less than 15% of total delivered volumes in 2005, the share of spot trades has doubled to almost 30% today according to GIIGNL (International Group of Liquefied Natural Gas Importers). In absolute terms, the figures are even more astounding – from 20mtpa (million tonnes per annum) in 2005 to more than 60mtpa today.

However, it’s been a bumpy ride - the spot Asian delivered prices rose from below $4/

MMBtu in 2009 to over $20/MMBtu in the peak of 2014. The nature of the market has also changed: there’s no longer a simple ‘floating pipeline’ from major producing regions to traditional demand centres. Instead, new supply and demand points have created a highly seasonal LNG spot market, with strong summer/winter spreads and opportunities for cross-basin arbitrage.

The oil-rich Gulf states have demonstrated a strong appetite for importing gas in the form of LNG. Even taking into account the

Continued from page 9

GM&T France at MGIMO 2nd International Alumni Forum: “Demand Security Is a Prerequisite to Supply Security”

Gazprom Pushes the Boundaries of Global LNG Trading

Continues on page 11

Frédéric Barnaud, Executive Director of LNG, Shipping & Logistics, Clean Energy

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 11

Continued from page 10

Gazprom Pushes the Boundaries of Global LNG Trading

recent easing-off in the markets, geopolitical instability had kept oil prices at high levels with plenty of volatility. This makes gas a cleaner and more cost-effective energy source for the traditional hydrocarbon exporters. LNG imports are now an essential source of fuel for the power generation sector to meet peak summer demand, when the desert sun keeps temperatures at above 40 degrees for months on end, and air conditioning is a necessity rather than a luxury.

In South America – especially Argentina – a whole new demand centre for LNG has developed extremely quickly, attracting flows back into the Atlantic basin. Although a highly attractive market, it is not without its problems. Lack of available storage capacity, unpredictable demand and economic instability make it a risky proposition for committing term supplies, but there are opportunities for those who are willing to take on the challenge.

In the next few years, significant new US and Australian LNG projects will come online. More countries will start importing LNG, and the shipping market will be transformed with the introduction of a large number of new, larger, more efficient vessels. All this will involve change and increased uncertainty, but will also bring more liquidity into the markets and create exciting new trading opportunities.

Since 2005, Gazprom – through its dedicated subsidiaries within the Gazprom Marketing & Trading (GM&T) Group– has been at the forefront of these changes. From modest beginnings, Gazprom has become one of the most recognised and successful trading companies in the LNG business. Delivering Russian LNG supplies from Gazprom’s 50%-owned Sakhalin II project in the Far East, GM&T has also built up a wide range of non-Russian LNG supplies for its global portfolio. To date, GM&T has traded gas from most liquefaction projects in the world and delivered to almost every country that imports LNG. GM&T also operates the world’s largest fleet of Ice-Class LNG carriers, some of them custom-built to Gazprom specifications, designed to operate in the harshest conditions of the Arctic north, including the Northern Sea Route.

GM&T’s primary goal is to bring Russian LNG to the market: from the existing Sakhalin II plant and all projects currently under development – including Vladivostok LNG, Baltic LNG, Sakhalin II Train 3 expansion, as well as cooperating with Yamal LNG. Moreover, strong portfolio diversification is the key to growth and profitability; Gazprom traders

therefore strive to achieve a diversity of purchases and sales that capture the highest possible margins.

To this end, GM&T has recently taken full advantage of the oversupply situation in Europe – mainly in Spain and Portugal – by re-exporting LNG back to the global markets. This has the additional effect of diverting non-Russian gas flows away from Europe, thus keeping Gazprom’s pipeline supplies balanced. Most of these cargoes have been placed in the premium Argentine market. This has been a challenging exercise, but Gazprom has now firmly established a significant market share in this important region.

The changes in the LNG environment are not purely physical. Although still in its infancy, a ‘paper’ market of LNG derivative instruments is emerging, with contracts such as ‘JKM Swaps’ being actively traded, with others soon to follow. Gazprom has been active in this new and exciting development from the start, and will continue to participate as the market matures and expands.

Through its commitment to growth, flexibility and operational excellence, Gazprom has become a dynamic and genuinely global player in the LNG trading market. There are challenges ahead, but these will be turned into opportunities, advancing our goal of becoming the leading global energy company.

Frédéric Barnaud

12

Gazprom Marketing & Trading Completes First Ship-to-Ship LNG Transfer at Sea

Gazprom Marketing & Trading (GM&T) has completed the company’s first ship-to-ship (STS) transfer of LNG cargo at sea. The transfer operation occurred between two GM&T-chartered LNG ships – delivering vessel ‘Pskov’ and receiving vessel ‘Yenisei River’. The cargo had been loaded on board ‘Pskov’ in Spain after which a STS operation with ‘Yenisei River’ was chosen for optimising the company’s commercial and shipping portfolio.

The LNG transfer operation took place at sea off Linggi, Malaysia and was successfully completed on 6 December 2014. GM&T was supported by SPT, a specialist STS cargo transfer operator.

Consistent with GM&T Shipping’s commitment to maritime safety, meticulous planning and thorough vetting of processes were completed before the operation. Several GM&T representatives were on board both vessels throughout the operation.

Mr Nikolai Grigoriev, Managing Director, Shipping, GM&T said: “The successful completion of our first ever LNG transfer operation at sea is a testament to GM&T’s expanding shipping capability and flexibility. We are extremely grateful to the Masters and crews of the ‘Pskov’ and ‘Yenisei River’, to the owners of the vessels, Sovcomflot and Dynagas, and to SPT for the safely and efficiently executed operation.”

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 13

Gazprom Marketing & Trading Completes First Ship-to-Ship LNG Transfer at Sea

Did You Know…That You Can both Heat and Refrigerate with Natural Gas?Reprint from Gaswinner, the WINGAS magazine

The Chinese were the first. They knew what natural gas could do, and used it the same way that engineers and zoo directors do today, one thousand years later.

Natural gas for 1,700 yearsThe southern Chinese province of Sichuan plays an important role in the history of salt in China. Reports can be found from as early as the third century concerning the use of natural gas for boiling brine. Natural gas was fed through bamboo canes and then ignited. The brine was heated in large pots and the water evaporated. Salt crystals were what remained.

Odorous thermolampsIn 1799 Philippe Lebon registered a patent for a heater that used natural gas obtained from wood. He called his invention the “thermolamp” because it gave off light as well as heat. The public were able to experience it in action at a Parisian hotel in 1801. Unfortunately, the technology flopped because the distillation furnace and the attached burner gave off such a horrible smell.

Gas keeps the ball rollingFootball matches canceled due to ice and snow are a thing of the past. These days, pitch heaters keep the grass ready for play even in sub-zero temperatures. In some modern football stadiums, natural gas provides the warmth for large underfloor heating systems. At the stadium in Freiburg, Germany, Stirling engines powered by natural gas bring water in the heating pipes up to the right temperature. These powerful systems also supply the heating for the stadium’s restaurant, offices, and fan building.

Gas keeps food fresh Some refrigerators are powered by natural gas instead of electricity. They work using the absorption principle by which a liquid cooling agent is made to evaporate, drawing heat away from the refrigeration compartment. The steam is then absorbed by water. A gas burner heats this solution, causing the cooling agent to evaporate again. The cooling agent is then returned to a liquid state in a condenser. Low-noise gas refrigerators are now standard in mobile homes and other mobile kitchens.

Co-generation unit at the zooAnimals from hot climates need the heat. Zoos with exotic wildlife therefore have an enormous energy demand for heating purposes. Osnabrück Zoo demonstrates how this can be done in a climate-friendly manner. Here, a natural gas-fired CHP unit was installed to heat the tropical house, the South American area, and the monkey house. It also produces one-third of the electricity needed to run the zoo.

14

Small Scale LNG in Perspective – Developments and Potential in AsiaTony Regan, Principal Consultant, Tri-Zen International Pte Ltd

A major new market for liquefied natural gas (LNG) is emerging – the use of LNG as a transportation fuel. Up until recently oil dominated this sector with natural gas having only a 2% market share. Natural gas has been used as a vehicle fuel since the 1930’s and although there are over 16 million natural gas vehicles in use today the bulk of them are in just a handful of countries. The largest markets for natural gas vehicles are Pakistan and Iran followed by Argentina, Brazil, India and China and the fuel is usually compressed natural gas (CNG). We are beginning to see LNG being used as a transportation fuel and the emergence of a compelling case for far greater utilization of LNG. The main drivers are:

Unconventional gas

Over the last five years we have become aware of just how large global unconventional gas resources are. The IEA, World Energy Outlook 2011 suggested that unconventional gas resources could be over 900 Tcm and that ultimately recoverable resources could be as much as 406 Tcm. Thus, almost overnight, gas resources doubled. This, and similar reports from the EIA in the USA, completely changed attitudes to gas and gas supply. The combined resources were equal to 250 years of current production and each region in the world had at least 75 years of potential supply based on current rates of consumption. The shale gas forecasts completely changed attitudes towards gas supply and triggered substantial investment in both gas supply and the development of new gas markets. We have seen more gas going into the power and industrial market and it is now starting to penetrate the huge transportation fuel market.

The environmental driverEmission limits are being introduced by legislation such as the US Cross State Air Pollution Rule and, in particular, fuel sulphur limits are being introduced by the International Maritime Organisation (IMO) on marine fuels. The IMO’s MARPOL Annex VI regulations will lower the permitted sulphur level in marine fuel from 1% to 0.1% in 2015 in order to reduce emissions of Nitrous Oxides (NOx), Sulphur Oxides (SOx), Particulate Matter (PM) and other greenhouse gases, such as Carbon Dioxide (CO2). The lower limit will apply in what are known as Emission Control Areas (ECA) and these are currently Northern Europe and North America. Elsewhere the fuel sulphur limit will go to 0.5% in 2020. The new limits mean that it will no longer be possible to burn fuel oil within an ECA and therefore ship-owners will have to switch to the substantially more expensive ultra low sulphur diesel or to LNG.

Continues on page 15

Source: IEA, World Energy Outlook 2011

0

20

40

60

80

100

120

140

160

180

Europe and Eurasia

North America

La:n America

Asia Middle East Africa

Gas resources by region Tcm

Conven:onal Tight Gas Shale Gas CBM

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 15

Continued from page 14

Small Scale LNG in Perspective – Developments and Potential in Asia

The economic driver

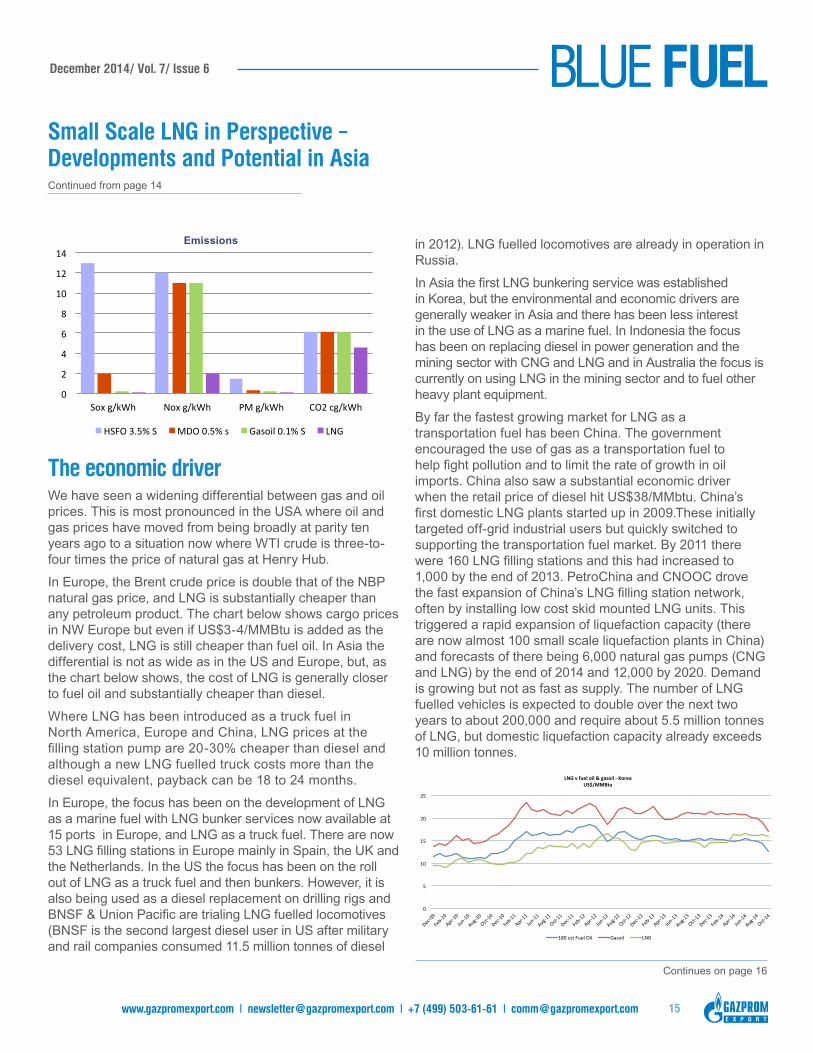

We have seen a widening differential between gas and oil prices. This is most pronounced in the USA where oil and gas prices have moved from being broadly at parity ten years ago to a situation now where WTI crude is three-to-four times the price of natural gas at Henry Hub.

In Europe, the Brent crude price is double that of the NBP natural gas price, and LNG is substantially cheaper than any petroleum product. The chart below shows cargo prices in NW Europe but even if US$3-4/MMBtu is added as the delivery cost, LNG is still cheaper than fuel oil. In Asia the differential is not as wide as in the US and Europe, but, as the chart below shows, the cost of LNG is generally closer to fuel oil and substantially cheaper than diesel.

Where LNG has been introduced as a truck fuel in North America, Europe and China, LNG prices at the filling station pump are 20-30% cheaper than diesel and although a new LNG fuelled truck costs more than the diesel equivalent, payback can be 18 to 24 months.

In Europe, the focus has been on the development of LNG as a marine fuel with LNG bunker services now available at 15 ports in Europe, and LNG as a truck fuel. There are now 53 LNG filling stations in Europe mainly in Spain, the UK and the Netherlands. In the US the focus has been on the roll out of LNG as a truck fuel and then bunkers. However, it is also being used as a diesel replacement on drilling rigs and BNSF & Union Pacific are trialing LNG fuelled locomotives (BNSF is the second largest diesel user in US after military and rail companies consumed 11.5 million tonnes of diesel

in 2012). LNG fuelled locomotives are already in operation in Russia.

In Asia the first LNG bunkering service was established in Korea, but the environmental and economic drivers are generally weaker in Asia and there has been less interest in the use of LNG as a marine fuel. In Indonesia the focus has been on replacing diesel in power generation and the mining sector with CNG and LNG and in Australia the focus is currently on using LNG in the mining sector and to fuel other heavy plant equipment.

By far the fastest growing market for LNG as a transportation fuel has been China. The government encouraged the use of gas as a transportation fuel to help fight pollution and to limit the rate of growth in oil imports. China also saw a substantial economic driver when the retail price of diesel hit US$38/MMbtu. China’s first domestic LNG plants started up in 2009.These initially targeted off-grid industrial users but quickly switched to supporting the transportation fuel market. By 2011 there were 160 LNG filling stations and this had increased to 1,000 by the end of 2013. PetroChina and CNOOC drove the fast expansion of China’s LNG filling station network, often by installing low cost skid mounted LNG units. This triggered a rapid expansion of liquefaction capacity (there are now almost 100 small scale liquefaction plants in China) and forecasts of there being 6,000 natural gas pumps (CNG and LNG) by the end of 2014 and 12,000 by 2020. Demand is growing but not as fast as supply. The number of LNG fuelled vehicles is expected to double over the next two years to about 200,000 and require about 5.5 million tonnes of LNG, but domestic liquefaction capacity already exceeds 10 million tonnes.

Continues on page 16

0

2

4

6

8

10

12

14

Sox g/kWh Nox g/kWh PM g/kWh CO2 cg/kWh

HSFO 3.5% S MDO 0.5% s Gasoil 0.1% S LNG

Emissions

0

5

10

15

20

25

Dec-‐09

Feb-‐10

Apr-‐10

Jun-‐10

Aug-‐10

Oct-‐10

Dec-‐10

Feb-‐11

Apr-‐11

Jun-‐11

Aug-‐11

Oct-‐11

Dec-‐11

Feb-‐12

Apr-‐12

Jun-‐12

Aug-‐12

Oct-‐12

Dec-‐12

Feb-‐13

Apr-‐13

Jun-‐13

Aug-‐13

Oct-‐13

Dec-‐13

Feb-‐14

Apr-‐14

Jun-‐14

Aug-‐14

Oct-‐14

LNG v fuel oil & gasoil -‐ Korea US$/MMBtu

180 cst Fuel Oil Gasoil LNG

16

Continued from page 13

Small Scale LNG in Perspective – Developments and Potential in Asia

This has resulted in PetroChina having to mothball two new liquefaction plants and for many of them to be running at less than half their design capacity. Margins have also been squeezed. The costs of the feedgas into the liquefaction plants increased by 15% last July and again by 18% in September. It can take many months for that increase to work through to retail prices and then it might not be a full pass through. The government has pledged to achieve “market pricing” for natural gas by the end of 2015, but at the moment the liquefaction plants are paying “market price” for their gas whilst retail prices are only slowly catching up. Has the bubble burst? Yes, the boom times are over, there is no longer a $10/MMBtu margin to go after and there is now concern that falling oil prices will close the differential between diesel and LNG. Infrastructure (liquefaction plants and filling stations) has run ahead of the market and there is likely to be a pause in further investment until the market has caught up. Have the fundamentals changed? No, the drivers are still strong and the order books for new LNG fuelled trucks and buses remain strong. 700,000 LNG fuelled trucks are expected to be in circulation by 2020, up from just over 50,000 in 2012, and the government has indicated that it is willing to provide fiscal support, if necessary, to ensure that LNG can continue to be sold at the pump at a 25% discount to diesel.

The uptake of LNG as a marine fuel has been very slow in China as there has been no economic benefit to convert from fuel oil to LNG. There have been a number of trials and there are now some LNG fuelled vessels in operation. The environmental drivers are substantial and the government is now paying more attention to the development of this market. The transport ministry aims to have 2,000 vessels, 2%

of its inland fleet, using LNG by 2015 and 10,000 by 2020.

One thing that has become clear is that there are no technology bottlenecks constraining the development of the market in China. We have seen a rapid increase in technology vendors able to supply all of the required components whether they are liquefaction plants or fuel dispensers, storage tanks or cryogenic valves and metres. All of the Chinese truck manufacturers now offer an LNG fuelled option.

The IMO legislation focused attention on the potential of using LNG as a marine fuel and the economic benefits stimulated the use of LNG as a truck fuel in North America. However, it is becoming increasingly apparent that the markets are not just the marine and road transport sector, but almost the entire diesel market, with the gas utilized being either CNG or LNG. CNG is the appropriate fuel for light duty vehicles such as light trucks and taxis and LNG for heavy vehicles such as large trucks, locomotives and heavy mining plant equipment. For medium duty vehicles such as buses and garbage trucks it can be both, with CNG perhaps the most appropriate for vehicles traveling less than about 250 miles a day.

The development of this market will lead to significant changes to the LNG business model. Currently LNG is delivered to large import terminals where it is regasified before being dispatched as natural gas to its final markets. In these new markets the gas will remain liquefied throughout the supply chain until it is vaporized immediately before being injected into the vehicle engine. Ships will not call into an LNG liquefaction plant or LNG terminal when they want to be fuelled instead they will probably call at satellite terminals or floating storage.

Continues on page 17

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 17

Continued from page 16

Small Scale LNG in Perspective – Developments and Potential in Asia

Continues on page 18

The main means of LNG transportation within these markets will no longer be large LNG carriers but small LNG vessels, trucks, barges and containers. Instead of it being stored in large 180,000 m3 storage tanks it will be stored is smaller 400 or 800m3 bullet tanks. In some cases an end-user may not need any storage tanks as they may utilize the container in which the LNG was delivered. The biggest change will probably relate to the LNG supply. As these markets have started to develop in North America, Australia and China the source of the LNG has been a small scale local liquefaction plant rather than the traditional large scale overseas liquefaction plant.

Some of these are being fed by pipeline gas rather than field production. In Europe these new downstream markets will probably continue to be supplied mainly by imported LNG, but elsewhere we are likely to see local production becoming the norm. These liquefaction plants can range from micro (10 tonnes a day) to small (100-500 tonnes a day) or medium (2,000-3,000 tonnes a day). In some cases they may just supply one customer (for instance a small peak shaving power plant or a bunkering business). All of the main liquefaction train vendors now offer a range of train sizes for these mini, small and medium size liquefaction plants.

18

Continued from page 17

Small Scale LNG in Perspective – Developments and Potential in Asia

The supply chain for these new markets will look very similar to the petroleum supply chain. From its point of production the LNG is likely to be transported by ship, barge, truck or train to intermediate storage and then delivered to storage tanks at the end users site by truck, train or barge. Semi trailer trucks can carry about 30,000 m3 of LNG, rail tank cars about 60,000 m3 and barges/small carriers from 1,000 to 30,000 m3. An attractive proposition, particularly for smaller consumers could be containerised LNG. The containers can be filled at the point of production and then transported by truck/rail/boat directly to the end users site. There they can be used as storage removing the need for the customer to build and maintain their own storage tanks. The standard 20 ft container can hold 8 tonnes of LNG, and 40 ft containers, 16 tonnes. Some containers are also classed as IMO Type C tanks and these can be used onboard vessels as LNG fuel tanks

It is still early days in the development of the downstream LNG markets. There are no significant technology gaps although there are still only a limited range of natural gas engines available for the very heavy duty and high horsepower applications and there are insufficient refueling facilities for the marine market. It will take time for fleet operators to convert vehicles to natural gas or work through their purchase cycle just as it is takes time for truck manufacturers to introduce a full range of natural gas fuelled vehicles. Vessels operating within the ECA’s have been early adopters of LNG whilst many ocean going vessel operators have been reluctant to consider LNG in the absence of an ECA in Asia. Will we see Asian ECA’s? Possibly not, but we are likely to see legislation introduced by individual cities and countries that has a similar effect. China will adopt “China V standards”

(Euro V) in 2017 which will reduce the sulphur level in transportation fuel to less than 0.10 ppm/lt.

How big could this market be? It is too early to say, but some visionaries see most heavy trucks, heavy plant and vessels using LNG in 20 years time. The majority of natural gas vehicles to date has been “aftermarket” conversions, but by the end of 2014 about 4% of new trucks (Class 7&8) in the USA will be fuelled by natural gas and this is expected to increase rapidly with forecasts suggesting between 12% and 35% penetration by 2020. There are already over 100,000 vehicles fueled by LNG in China. CEDIGAZ recently issued a forecast that worldwide demand by heavy trucks could be 45 mtpa in 2025 rising to 96 mtpa by 2035, with China representing almost half the global market. They expect demand from the marine sector is expected to be 35 mtpa in 2025 and 77 mtpa by 2035, but these and other forecasts do not seem to appreciate the size of the potential demand from other sectors such as rail, heavy plant and small scale power. The environmental drivers are expected to remain strong and increase, but the key issue influencing growth will be the difference in price between LNG and diesel. In many countries in Asia diesel prices are over $30/MMBtu and LNG prices between $15 and $20/MMBtu. With that differential we are likely to see the rapid adoption of LNG as a diesel replacement.

Will the recent fall in oil prices reduce the economic attractiveness of LNG as a transportation fuel? Unlikely, the differential between oil and gas remains wide in North America and in Asia, term LNG prices will fall in line with crude prices albeit with a two to three month delay. Thus the economic drivers are likely to remain broadly similar to those in 2014.

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 19

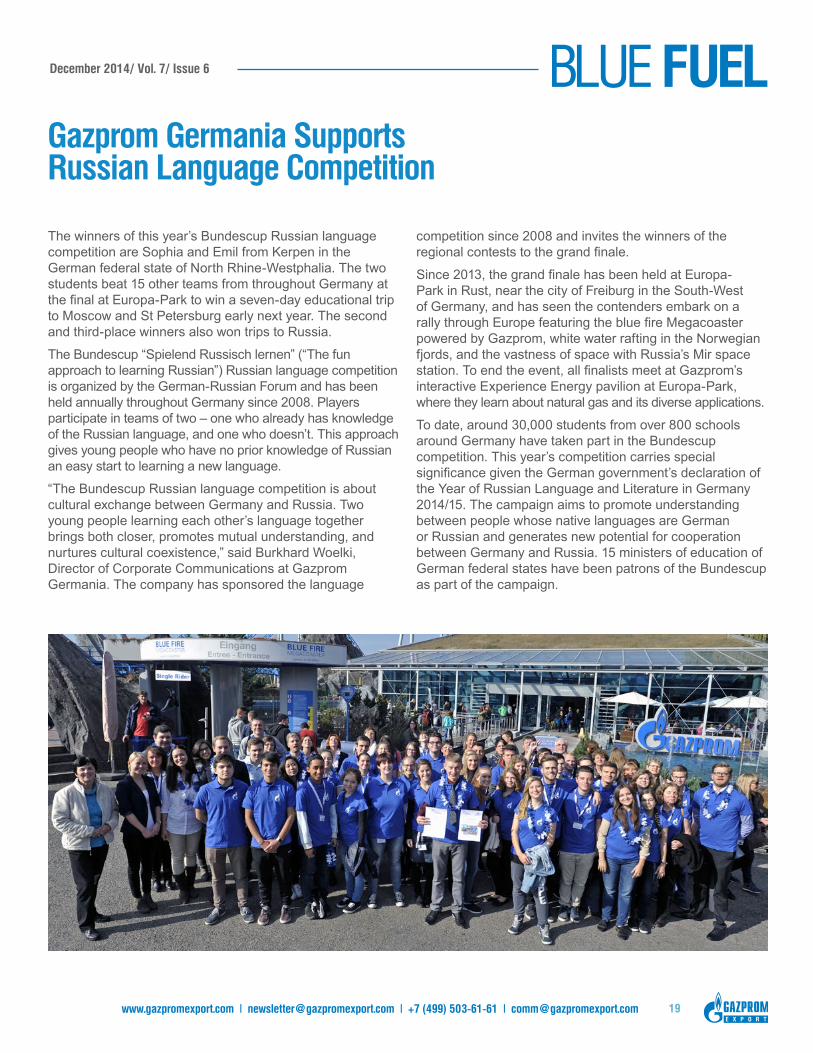

The winners of this year’s Bundescup Russian language competition are Sophia and Emil from Kerpen in the German federal state of North Rhine-Westphalia. The two students beat 15 other teams from throughout Germany at the final at Europa-Park to win a seven-day educational trip to Moscow and St Petersburg early next year. The second and third-place winners also won trips to Russia.

The Bundescup “Spielend Russisch lernen” (“The fun approach to learning Russian”) Russian language competition is organized by the German-Russian Forum and has been held annually throughout Germany since 2008. Players participate in teams of two – one who already has knowledge of the Russian language, and one who doesn’t. This approach gives young people who have no prior knowledge of Russian an easy start to learning a new language.

“The Bundescup Russian language competition is about cultural exchange between Germany and Russia. Two young people learning each other’s language together brings both closer, promotes mutual understanding, and nurtures cultural coexistence,” said Burkhard Woelki, Director of Corporate Communications at Gazprom Germania. The company has sponsored the language

competition since 2008 and invites the winners of the regional contests to the grand finale.

Since 2013, the grand finale has been held at Europa-Park in Rust, near the city of Freiburg in the South-West of Germany, and has seen the contenders embark on a rally through Europe featuring the blue fire Megacoaster powered by Gazprom, white water rafting in the Norwegian fjords, and the vastness of space with Russia’s Mir space station. To end the event, all finalists meet at Gazprom’s interactive Experience Energy pavilion at Europa-Park, where they learn about natural gas and its diverse applications.

To date, around 30,000 students from over 800 schools around Germany have taken part in the Bundescup competition. This year’s competition carries special significance given the German government’s declaration of the Year of Russian Language and Literature in Germany 2014/15. The campaign aims to promote understanding between people whose native languages are German or Russian and generates new potential for cooperation between Germany and Russia. 15 ministers of education of German federal states have been patrons of the Bundescup as part of the campaign.

Gazprom Germania Supports Russian Language Competition

20

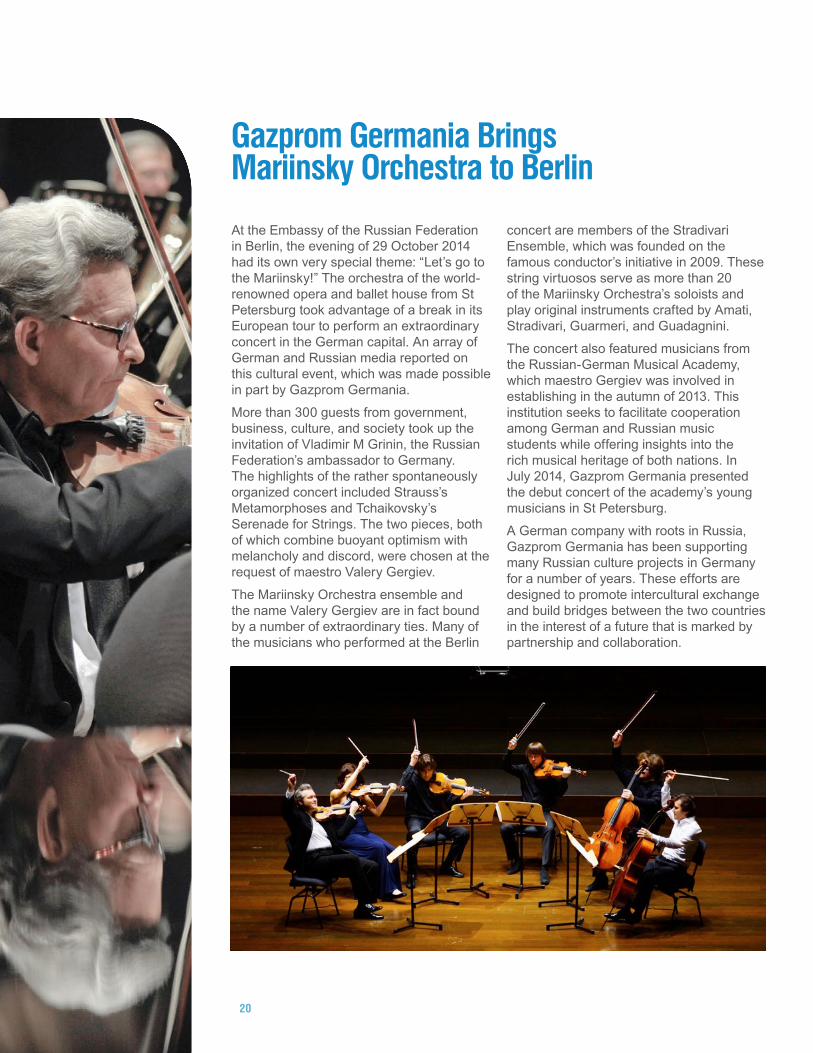

At the Embassy of the Russian Federation in Berlin, the evening of 29 October 2014 had its own very special theme: “Let’s go to the Mariinsky!” The orchestra of the world-renowned opera and ballet house from St Petersburg took advantage of a break in its European tour to perform an extraordinary concert in the German capital. An array of German and Russian media reported on this cultural event, which was made possible in part by Gazprom Germania.

More than 300 guests from government, business, culture, and society took up the invitation of Vladimir M Grinin, the Russian Federation’s ambassador to Germany. The highlights of the rather spontaneously organized concert included Strauss’s Metamorphoses and Tchaikovsky’s Serenade for Strings. The two pieces, both of which combine buoyant optimism with melancholy and discord, were chosen at the request of maestro Valery Gergiev.

The Mariinsky Orchestra ensemble and the name Valery Gergiev are in fact bound by a number of extraordinary ties. Many of the musicians who performed at the Berlin

concert are members of the Stradivari Ensemble, which was founded on the famous conductor’s initiative in 2009. These string virtuosos serve as more than 20 of the Mariinsky Orchestra’s soloists and play original instruments crafted by Amati, Stradivari, Guarmeri, and Guadagnini.

The concert also featured musicians from the Russian-German Musical Academy, which maestro Gergiev was involved in establishing in the autumn of 2013. This institution seeks to facilitate cooperation among German and Russian music students while offering insights into the rich musical heritage of both nations. In July 2014, Gazprom Germania presented the debut concert of the academy’s young musicians in St Petersburg.

A German company with roots in Russia, Gazprom Germania has been supporting many Russian culture projects in Germany for a number of years. These efforts are designed to promote intercultural exchange and build bridges between the two countries in the interest of a future that is marked by partnership and collaboration.

Gazprom Germania Brings Mariinsky Orchestra to Berlin

BLUE FUELDecember 2014/ Vol. 7/ Issue 6

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 21

The European Commission and the Russian Ministry of Energy use it. The New York Times and Russia Today use it as well. And so do most entities and governments. Twitter! With over 600 million users and more than half a million Tweets per day, Twitter has turned into one of the biggest social media platforms of our time. Through Twitter topics can be discussed fast and easy around the world, giving people the chance to express their thoughts and exchange a variety of information in real time. Whereas Facebook became a platform for social interaction with nearly everybody, Twitter offers a more professional background: It attracts a multiplicity of journalists, bloggers, politicians and decision makers.

Gazprom, one of the world’s leading energy companies, is a daily topic on Twitter. People around the world discuss news, thoughts and questions about Gazprom. By creating its own Twitter channels, Gazprom was able to actively join the discussion and directly inform a large audience about the company’s stance toward issues such as Russian gas deliveries in the context of security of supply.

More specifically, 2014 was the year that Gazprom Group entered the corporate Twitter world. Inspired by the success of the Gazprom Football’s online channels, Gazprom Group runs three verified corporate channels. Currently, Gazprom is tweeting every day in Russian, English and German, reaching directly over 28,000 followers and many more interested users. Our analyses have shown that in this short

period of time we were able to become the leader regarding Gazprom and Russian gas supply topics in the Russian, English and German Twitter world.

Yet, this is just the beginning: Every day we try to further enhance our Twitter channels with a variety of actions. In this regard we launched campaigns in 22 different languages in 26 countries. This enables Twitter users that are interested in energy topics all around the world to learn about our channels.

What is the focus of Gazprom’s activity on Twitter? On a daily basis we supply our followers with breaking news, inside information, graphics, short movies and statistics. But that’s not all: Twitter gives us the chance to recognize rising topics right when they emerge and actively engage in discussions with our followers. This enables us to inform a larger audience worldwide about Gazprom and its business conduct.

Gazprom Goes Twitter

You can follow Gazprom on Twitter on: @GazpromNews

@GazpromNewsEN

@GazpromNewsDE

You can find Gazprom Football’s Twitter channel, including the famous ticket lottery #Ticketmania at @GazpromFootball