Embed Size (px)

Citation preview

Blockchain Unlock the business VALUE

Ravi ChamriaCo-Founder - Sofocle Technologies

What is Blockchain? In one sentence……

A blockchain is a list of transactions shared between multiple parties where the new transactions are added at the end, never deleted, and neverchanged.

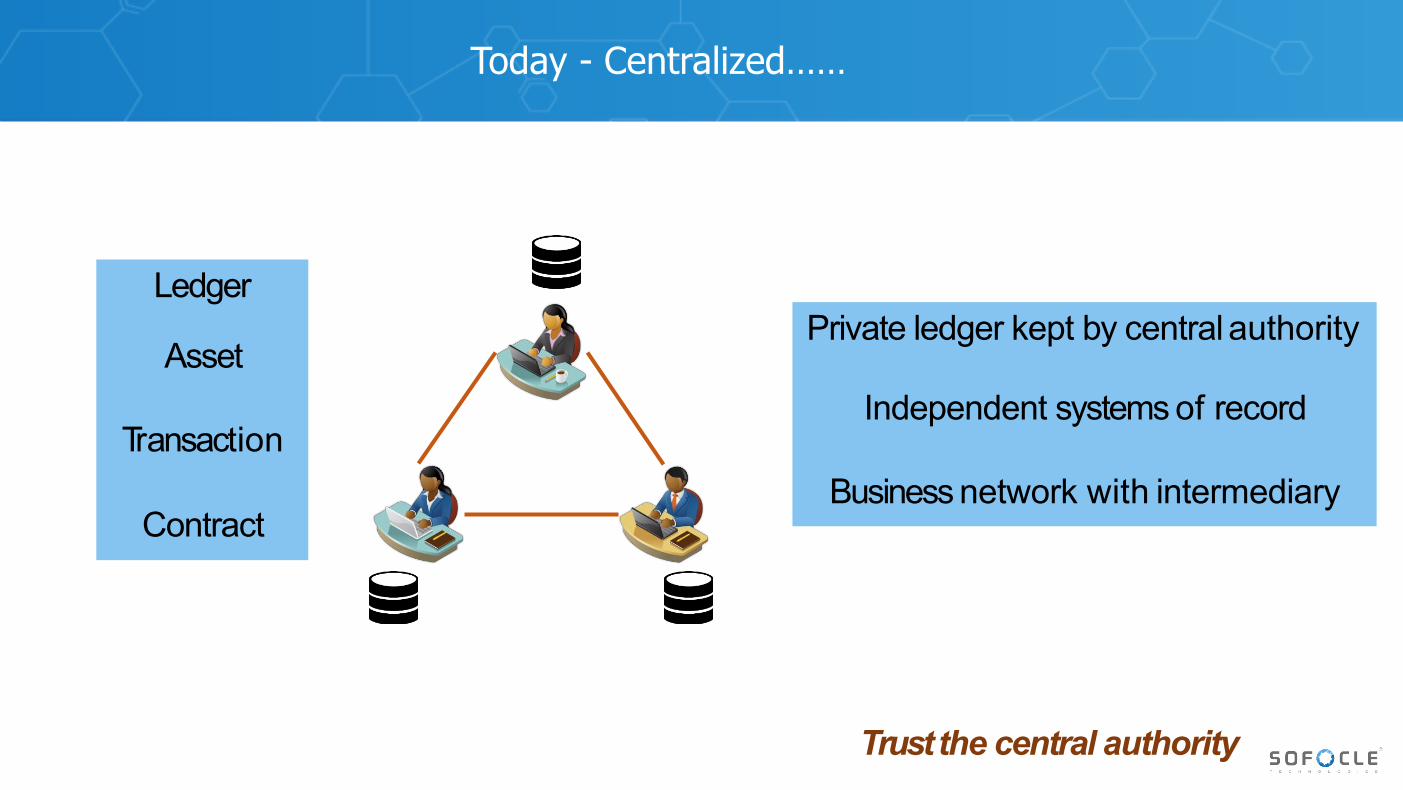

Private ledger kept by central authority

Independent systems of record

Business network with intermediary

Ledger

Asset

Transaction

Contract

Trust the central authority

Today - Centralized……

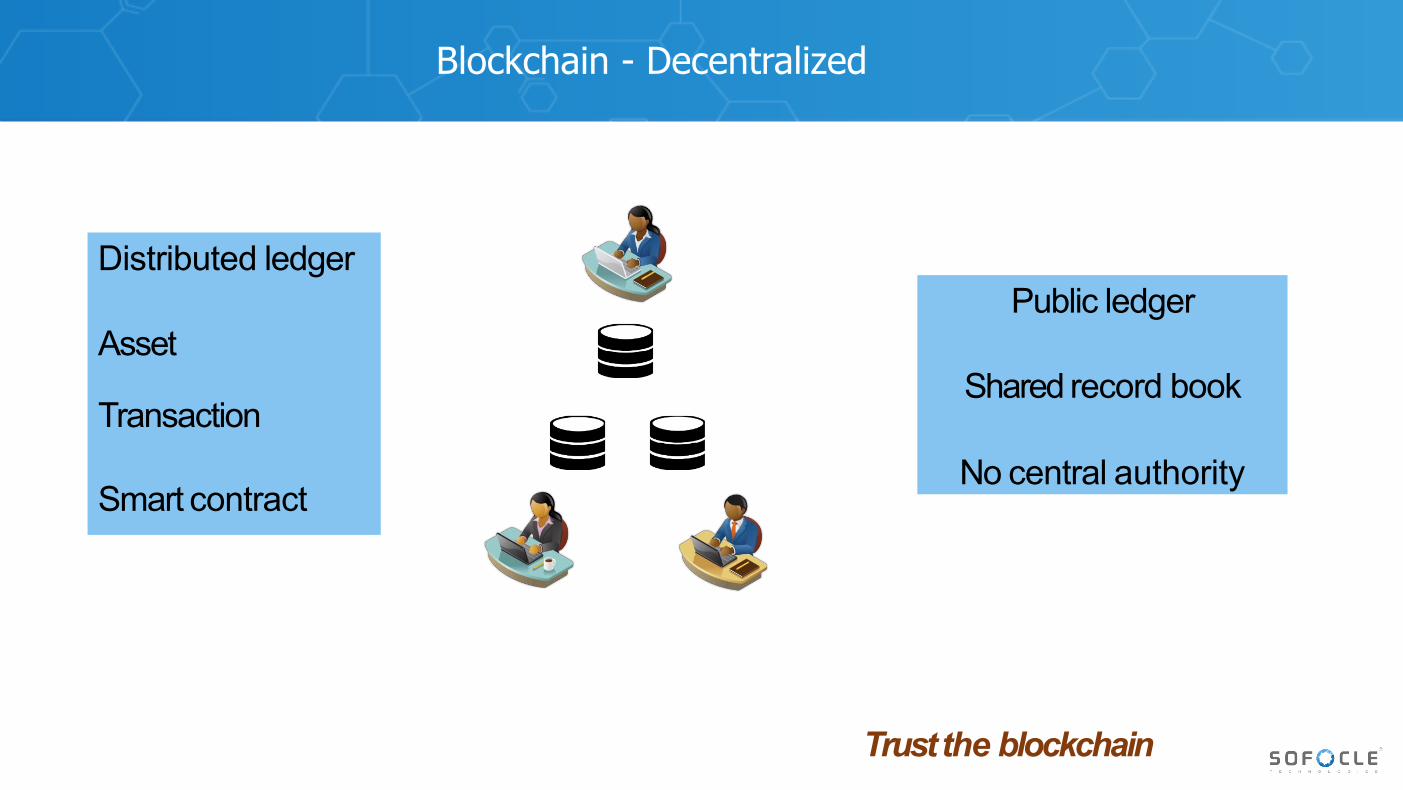

Public ledger

Shared record book

No central authority

Distributed ledger

Asset

Transaction

Smart contract

Trust the blockchain

Blockchain - Decentralized

TransactionTransactionTransaction Transaction

TransactionTransaction

. . .Starting block

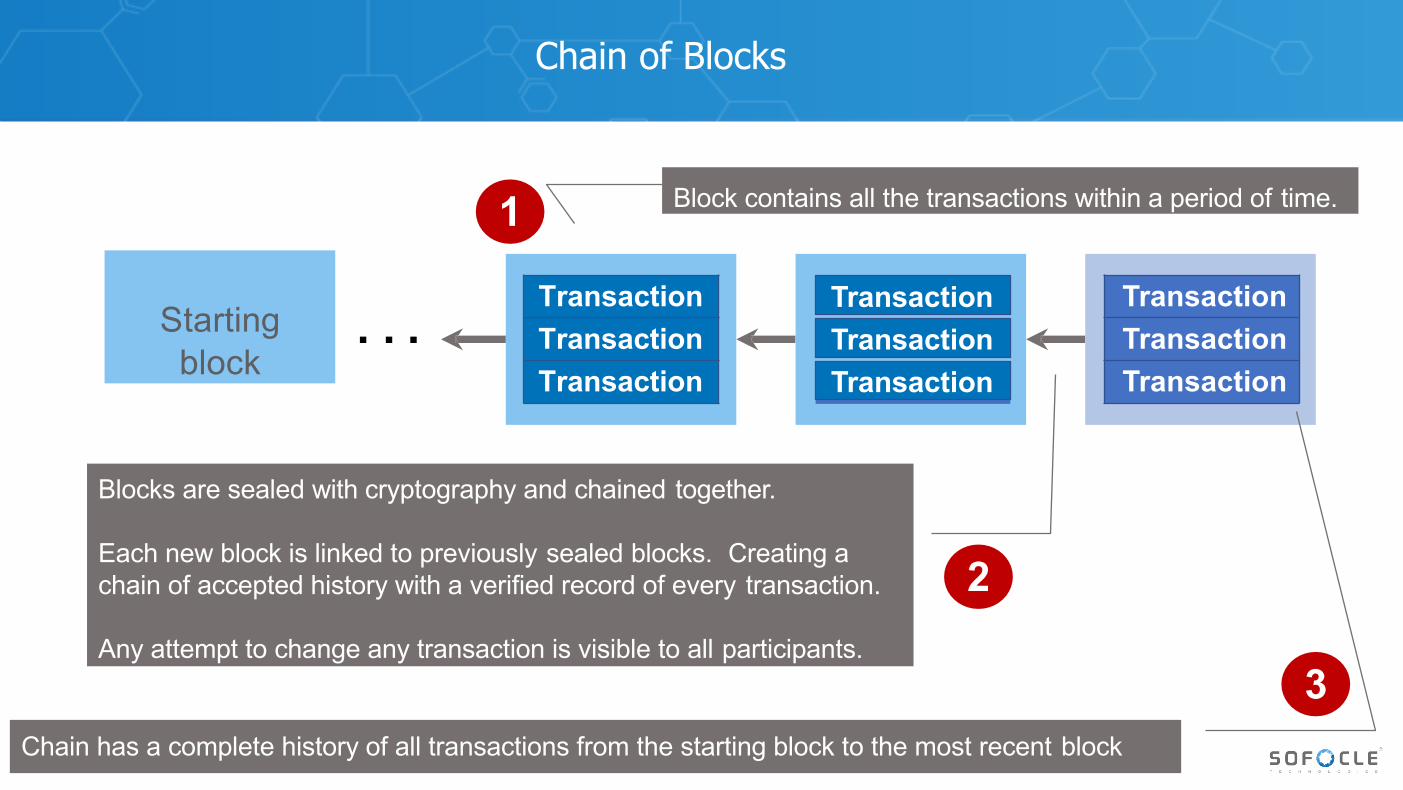

Block contains all the transactions within a period of time.

TransactionTransactionTransaction

Chain has a complete history of all transactions from the starting block to the most recent block

Blocks are sealed with cryptography and chained together.

Each new block is linked to previously sealed blocks. Creating a chain of accepted history with a verified record of every transaction.

Any attempt to change any transaction is visible to all participants.

1

2

3

Chain of Blocks

TransactionTransactionTransaction

TransactionTransactionTransaction

Transaction

. . .Starting block

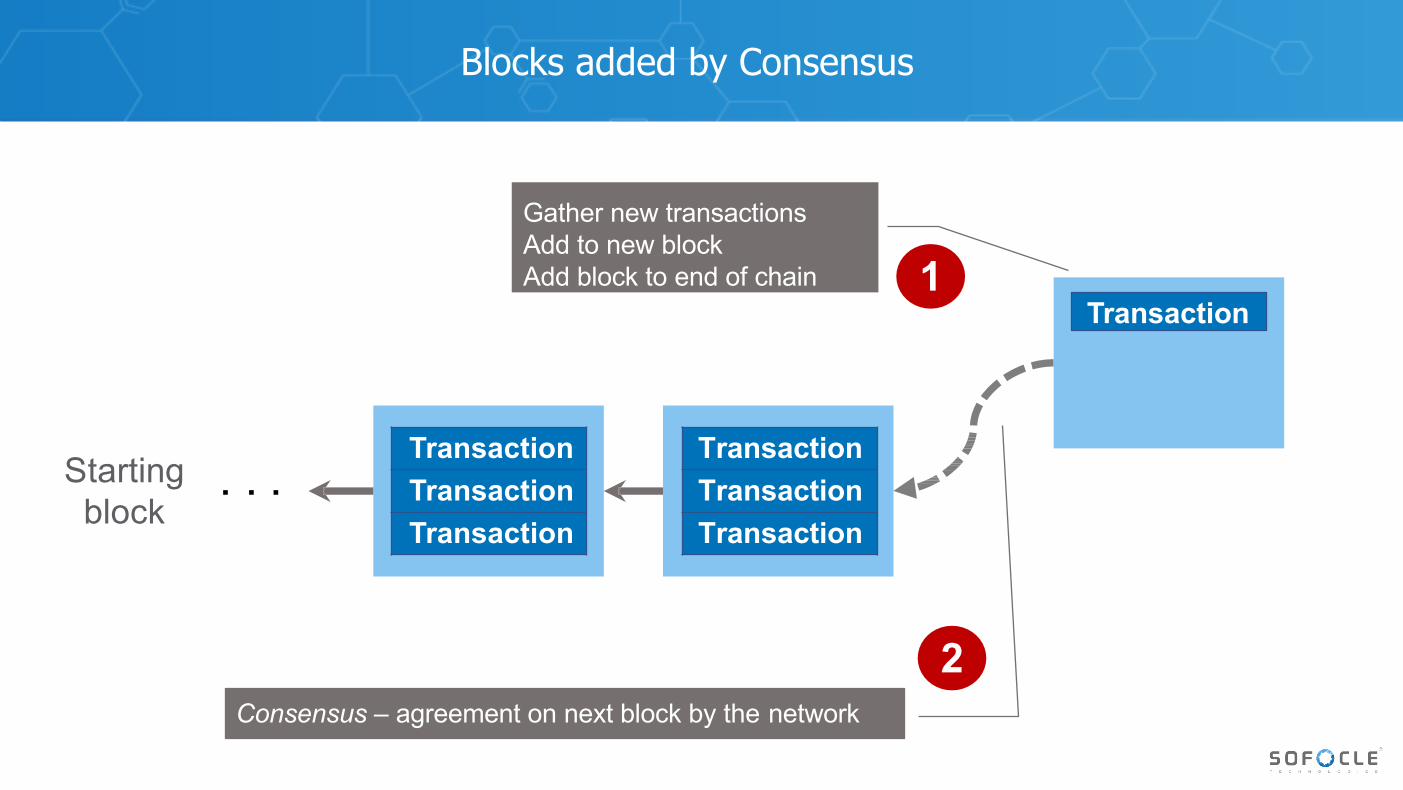

Gather new transactions Add to new blockAdd block to end of chain

Consensus – agreement on next block by the network

1

2

Blocks added by Consensus

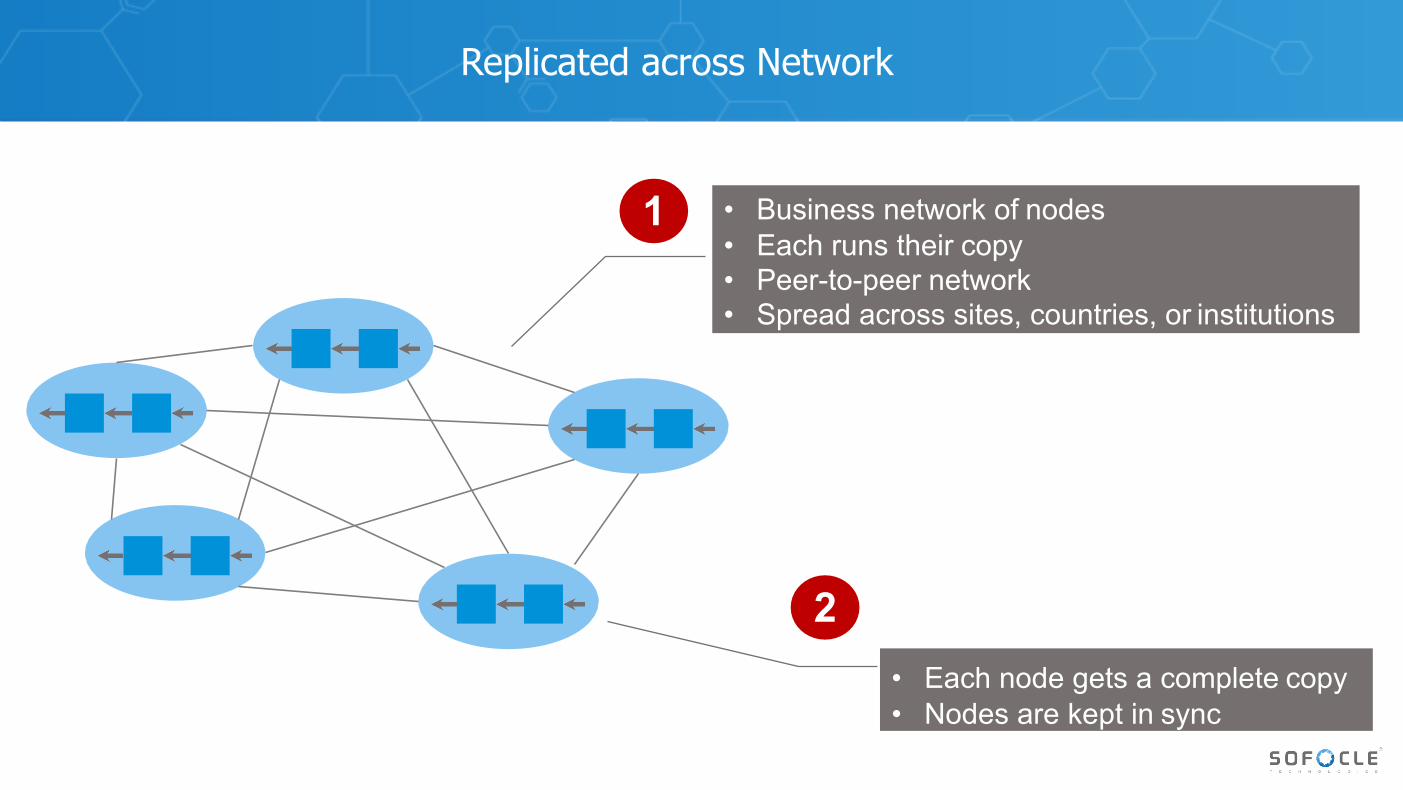

• Business network of nodes• Each runs their copy• Peer-to-peer network• Spread across sites, countries, or institutions

1

• Each node gets a complete copy• Nodes are kept in sync

2

Replicated across Network

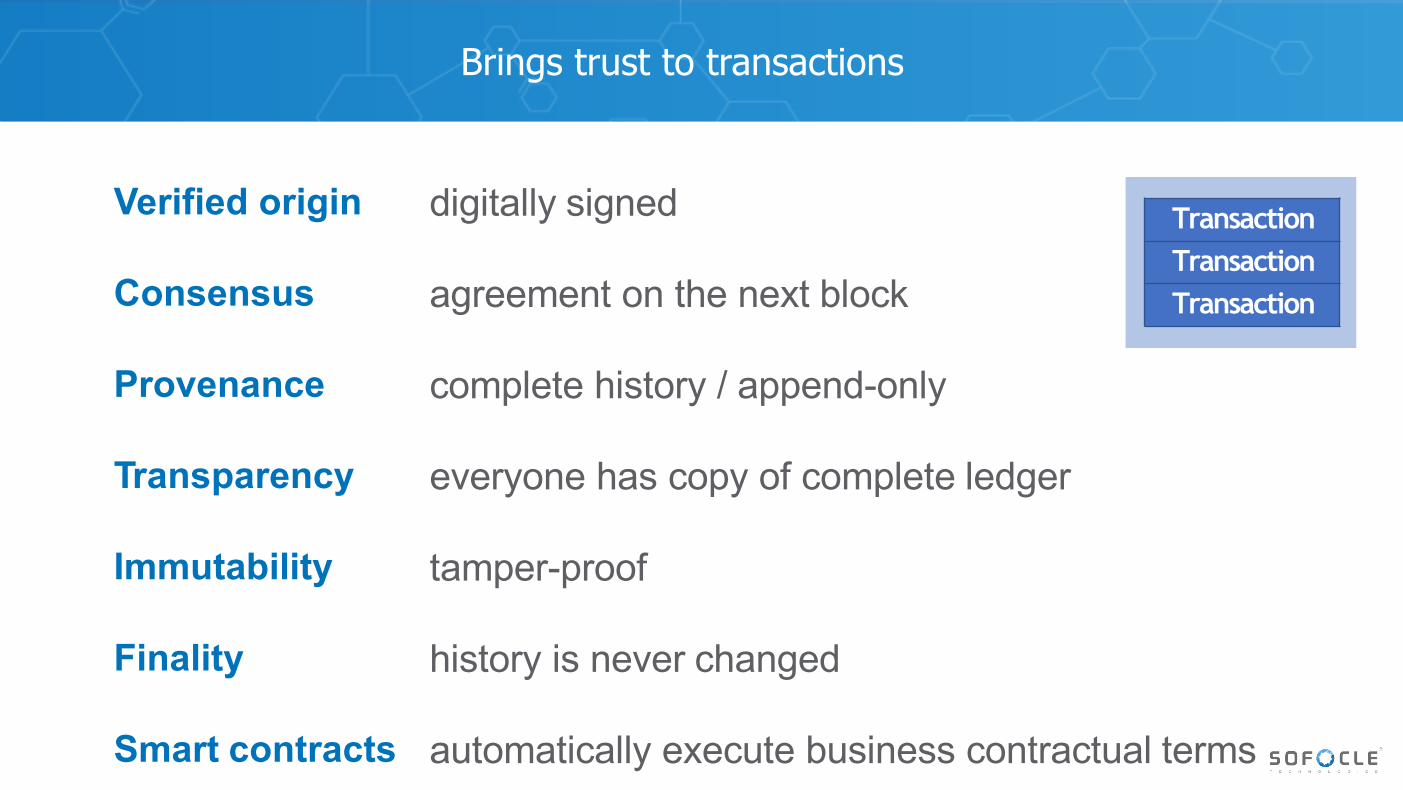

Verified origin digitally signed

Consensus agreement on the next block

Provenance complete history / append-only

Transparency everyone has copy of complete ledger

Immutability tamper-proof

Finality history is never changed

Smart contracts automatically execute business contractual terms

TransactionTransactionTransaction

Brings trust to transactions

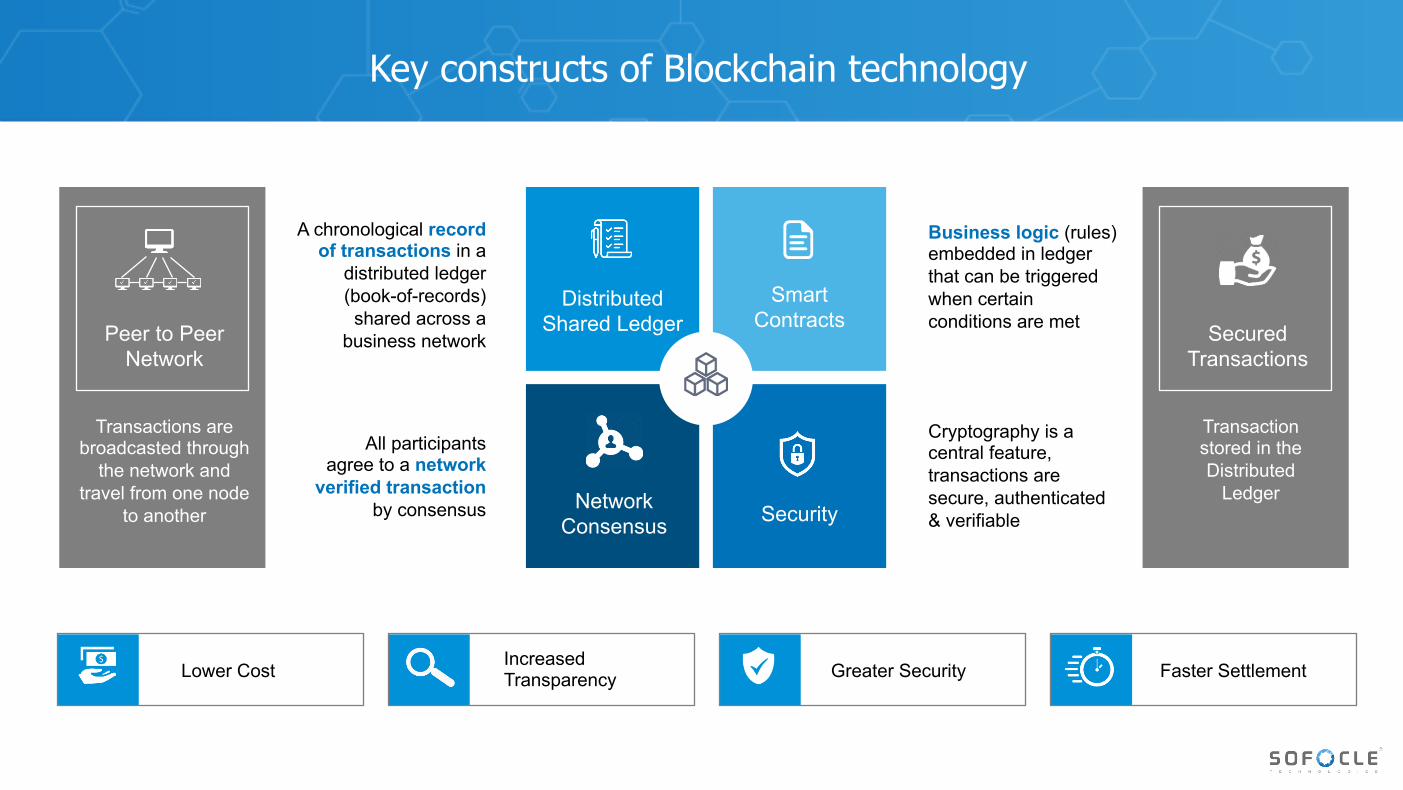

Distributed Shared Ledger

Smart Contracts

Network Consensus Security

A chronological record of transactions in a

distributed ledger (book-of-records) shared across a

business network

All participants agree to a network

verified transaction by consensus

Business logic (rules) embedded in ledger that can be triggered when certain conditions are met

Cryptography is a central feature, transactions are secure, authenticated & verifiable

Peer to Peer Network

Transactions are broadcasted through

the network and travel from one node

to another

Secured Transactions

Transaction stored in the Distributed

Ledger

Lower Cost Increased Transparency Greater Security Faster Settlement

Key constructs of Blockchain technology

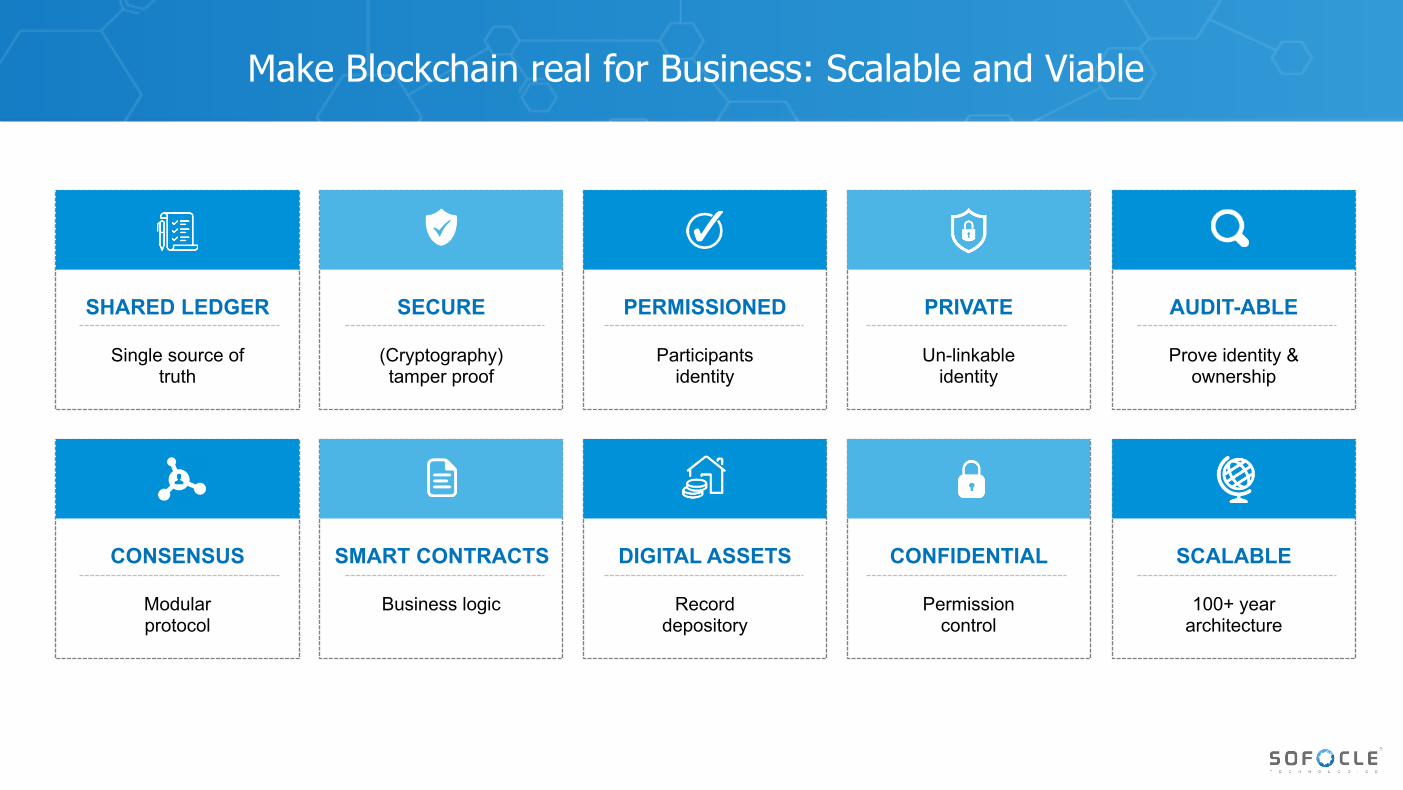

SHARED LEDGER

Single source of truth

SECURE

(Cryptography) tamper proof

PERMISSIONED

Participants identity

PRIVATE

Un-linkable identity

AUDIT-ABLE

Prove identity & ownership

CONSENSUS

Modular protocol

SMART CONTRACTS

Business logic

DIGITAL ASSETS

Record depository

CONFIDENTIAL

Permission control

SCALABLE

100+ year architecture

Make Blockchain real for Business: Scalable and Viable

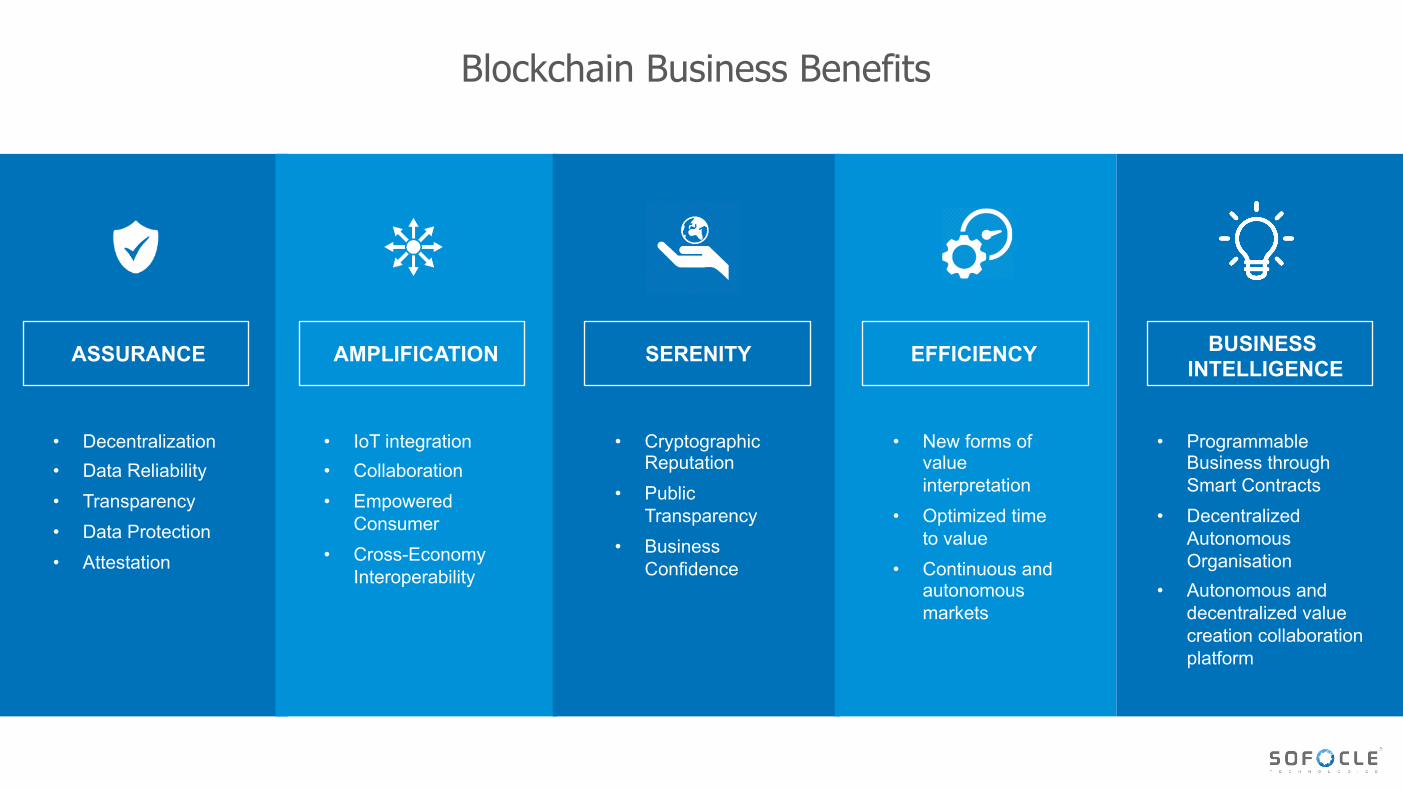

Blockchain Business Benefits

ASSURANCE AMPLIFICATION SERENITY EFFICIENCY BUSINESS INTELLIGENCE

• Decentralization• Data Reliability• Transparency• Data Protection• Attestation

• IoT integration• Collaboration• Empowered

Consumer• Cross-Economy

Interoperability

• Cryptographic Reputation

• Public Transparency

• Business Confidence

• New forms of value interpretation

• Optimized time to value

• Continuous and autonomous markets

• Programmable Business through Smart Contracts

• Decentralized Autonomous Organisation

• Autonomous and decentralized value creation collaboration platform

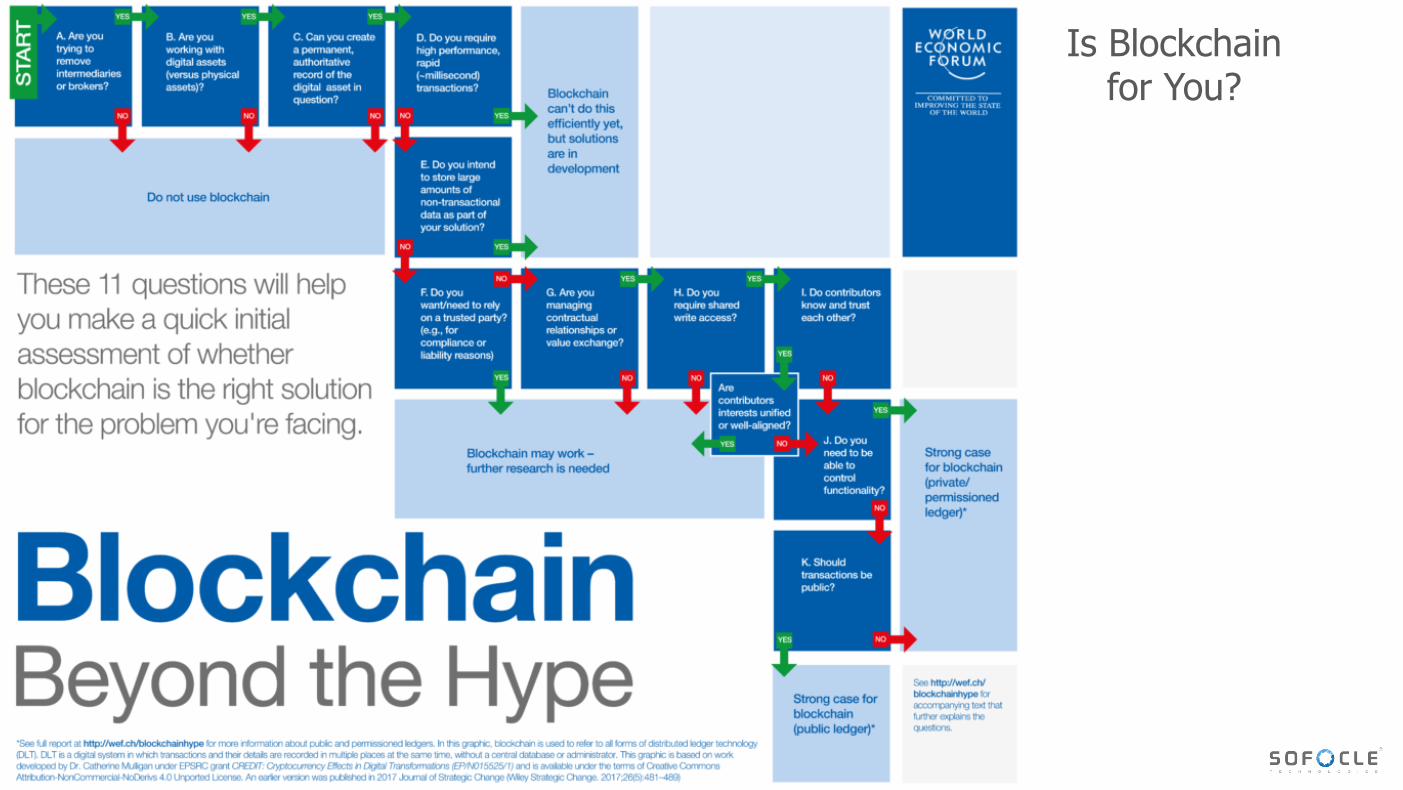

Is Blockchain for You?

A Blockchain-based solution that helps banks/lenders

and enterprises to ease complexities of Supply Chain

Financing and reduce cost by eliminating manual

processes

Invoice Discounting

Sofocle’s supply chain finance solution, with its Blockchain based product ‘sofoCap’ at the centre, give organizations a powerful way to streamline processes and collaborate various stakeholders in a supply chains.

sofoCapInvoices Submission

and Approval

Corporations SMBs

Large companies and SMBs

OnboardingKYC Credit Assessment

Organized Lenders Corporate treasury Insurance firms Pension funds Other capital market participant

BUYERS SUPPLIER

FUNDER

sofoCap Blockchain SCF Solution

These processes of submitting and approving invoices occur on a secure and unalterable platform based on Blockchain

Our Blockchain based and cloud-enabled platform optimizes cash flow by helping buyers/lenders to quickly on-board suppliers.

Simultaneously, we provide the option for suppliers to sell their invoices to funders for early payment at competitive finance rates.

SofoCap dramatically reduces time delays, costs and human errors. It helps suppliers and banks in the lending process by:

By utilizing “Trade Finance” instruments such as Factoring, PO Financing and Vendor Managed Inventory Financing

Our solutions significantly increase transparency for all stake holders by providing real-time and reliable view of every transaction happening in the ecosystem

Against well-known trade instruments such as PO’s, Invoices, Inventory Assets and Payment Obligations

Builds Trustworthy Supply Chain Ecosystem

Facilitates Lending by Financiers

Enhances Liquidity of the Collateralized Assets

By utilizing the underlying Smart Contracts based on pre-defined data triggers such as “due date for loan repayment.”

Automates Execution of Contracts

1

2

3

4

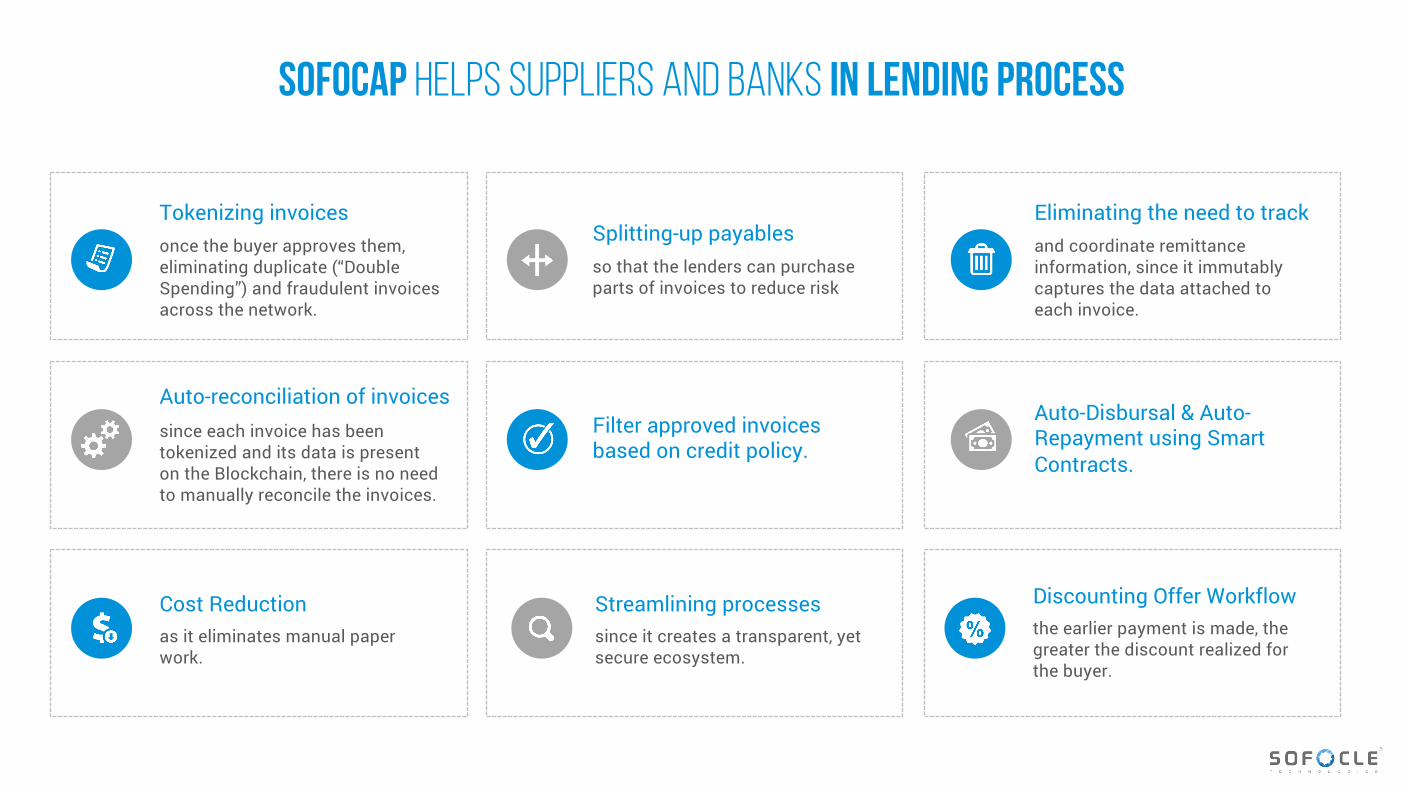

SOFOCAP HELPS SUPPLIERS AND BANKS IN LENDING PROCESS

once the buyer approves them, eliminating duplicate (“Double Spending”) and fraudulent invoices across the network.

so that the lenders can purchase parts of invoices to reduce risk

and coordinate remittance information, since it immutably captures the data attached to each invoice.

since each invoice has been tokenized and its data is present on the Blockchain, there is no need to manually reconcile the invoices.

Filter approved invoices based on credit policy.

Auto-Disbursal & Auto-Repayment using Smart Contracts.

as it eliminates manual paper work.

since it creates a transparent, yet secure ecosystem.

the earlier payment is made, the greater the discount realized for the buyer.

Tokenizing invoices Splitting-up payables

Eliminating the need to track

Auto-reconciliation of invoices

Cost Reduction Streamlining processes Discounting Offer Workflow

Product Supply Chain Tracking Solution Blockchain, mobile and open data to verify information

sofoChain

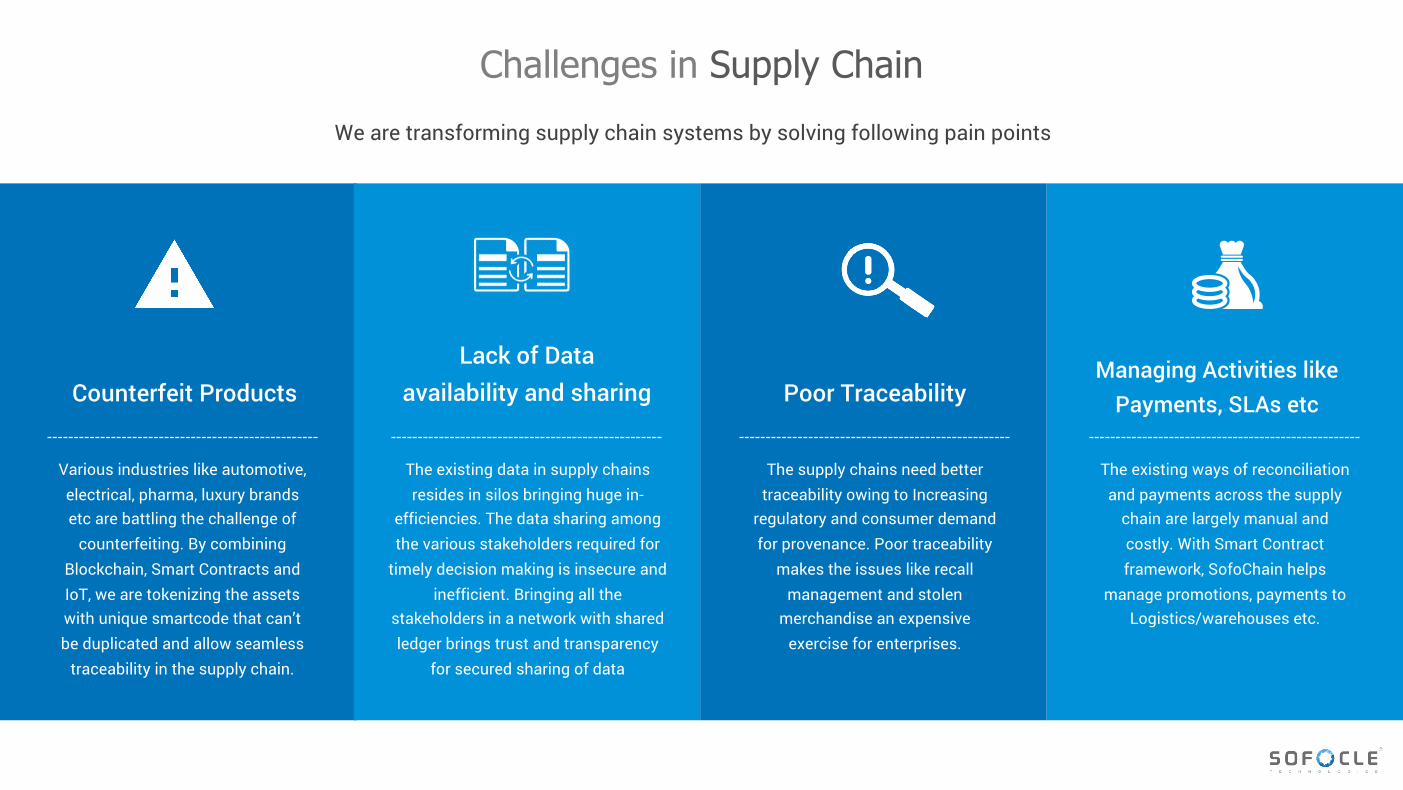

Various industries like automotive, electrical, pharma, luxury brands etc are battling the challenge of

counterfeiting. By combining Blockchain, Smart Contracts and IoT, we are tokenizing the assets with unique smartcode that can’t be duplicated and allow seamless

traceability in the supply chain.

The existing data in supply chains resides in silos bringing huge in-

efficiencies. The data sharing among the various stakeholders required for

timely decision making is insecure and inefficient. Bringing all the

stakeholders in a network with shared ledger brings trust and transparency

for secured sharing of data

The supply chains need better traceability owing to Increasing

regulatory and consumer demand for provenance. Poor traceability

makes the issues like recall management and stolen

merchandise an expensive exercise for enterprises.

The existing ways of reconciliation and payments across the supply

chain are largely manual and costly. With Smart Contract framework, SofoChain helps

manage promotions, payments to Logistics/warehouses etc.

Counterfeit ProductsLack of Data

availability and sharing Poor TraceabilityManaging Activities like

Payments, SLAs etc

Challenges in Supply ChainWe are transforming supply chain systems by solving following pain points

for the quantity and transfer of assets as they move between supply chain nodes, thus avoiding any fake or counterfeit products and verifying the chain of custody.

like serial numbers, bar codes, color, quality, etc.

Since these properties are all linked to the Digital Passport and are not just mere stamps or images, they assist in the chain of verification.

So that the poor products can be traced back to various stages of the supply chain through which it has passed.

sofoChain enables tracking and verification of good and eliminates fake or counterfeit goods/invoices in the supply chain by following means:

By tracking purchase orders, change orders, receipts, shipment notifications and other trade-related documents.

Sofochain

Blockchain based supply chain solution

Create Digital Passport of Physical Assets:

Link & Assign Properties:

Verification:

Track & Trace:

Eliminate Double Spending

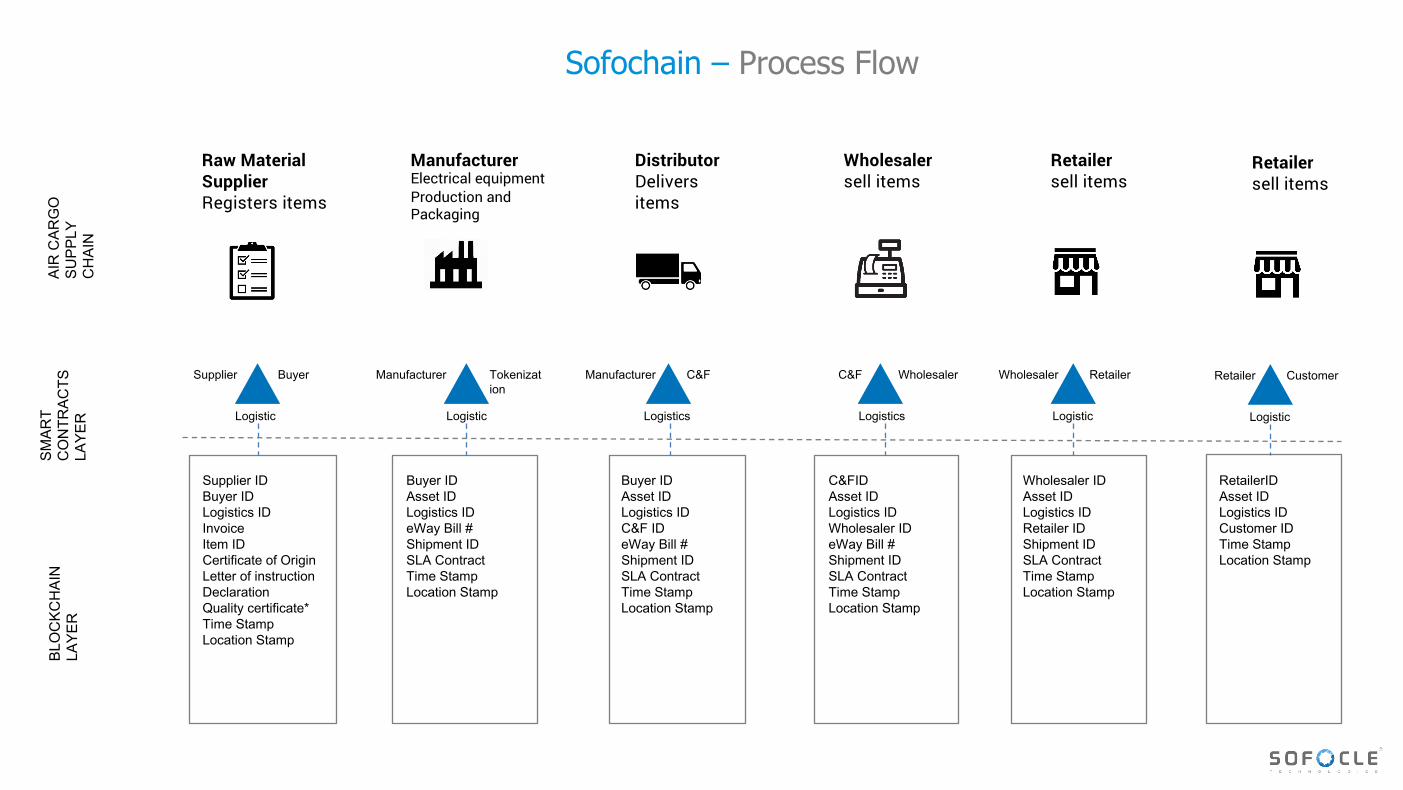

Sofochain – Process Flow

Supplier IDBuyer IDLogistics IDInvoiceItem IDCertificate of OriginLetter of instructionDeclarationQuality certificate*Time StampLocation Stamp

Buyer IDAsset IDLogistics IDeWay Bill #Shipment IDSLA ContractTime StampLocation Stamp

Buyer IDAsset IDLogistics IDC&F IDeWay Bill # Shipment IDSLA ContractTime StampLocation Stamp

C&FIDAsset IDLogistics IDWholesaler IDeWay Bill # Shipment IDSLA ContractTime StampLocation Stamp

Wholesaler IDAsset IDLogistics IDRetailer IDShipment IDSLA ContractTime StampLocation Stamp

C&F Wholesaler

Logistics

Wholesaler Retailer

LogisticLogistics

Manufacturer C&FTokenization

Logistic

ManufacturerBuyer

Logistic

Supplier

SMAR

T C

ON

TRAC

TS

LAYE

R

BLO

CKC

HAI

N

LAYE

RAI

R C

ARG

O

SUPP

LY

CH

AIN

Raw Material SupplierRegisters items

ManufacturerElectrical equipment Production and Packaging

DistributorDelivers items

Wholesalersell items

Retailersell items

Retailersell items

RetailerIDAsset IDLogistics IDCustomer IDTime StampLocation Stamp

Retailer Customer

Logistic

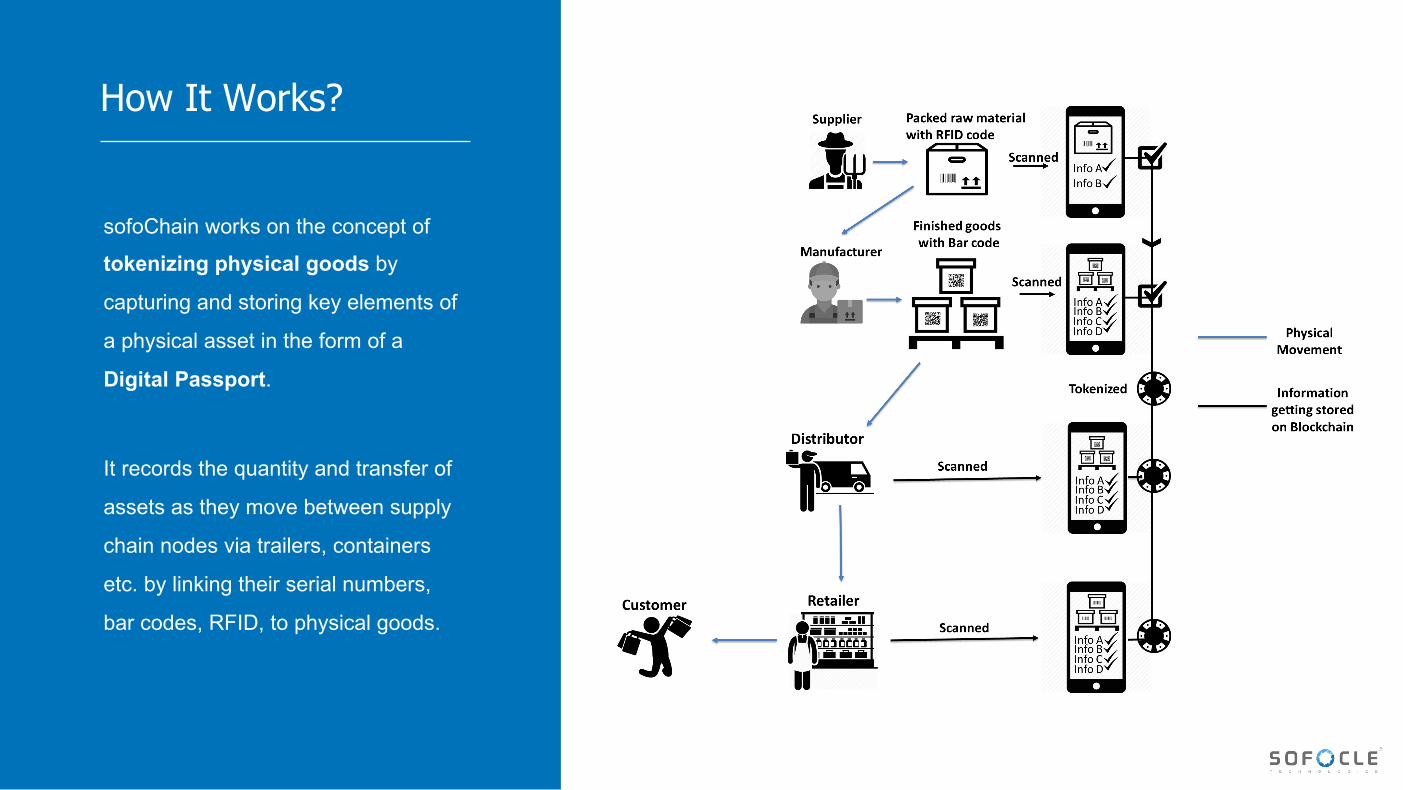

sofoChain works on the concept of

tokenizing physical goods by

capturing and storing key elements of

a physical asset in the form of a

Digital Passport.

It records the quantity and transfer of

assets as they move between supply

chain nodes via trailers, containers

etc. by linking their serial numbers,

bar codes, RFID, to physical goods.

How It Works?

Since the information of the product gets recorded on the

Blockchain and gets tokenized.

Identify & Eliminate Counterfeit Products

Trace Stolen Merchandise

Easy Data availability and sharing

Pinpoint Diverted Good

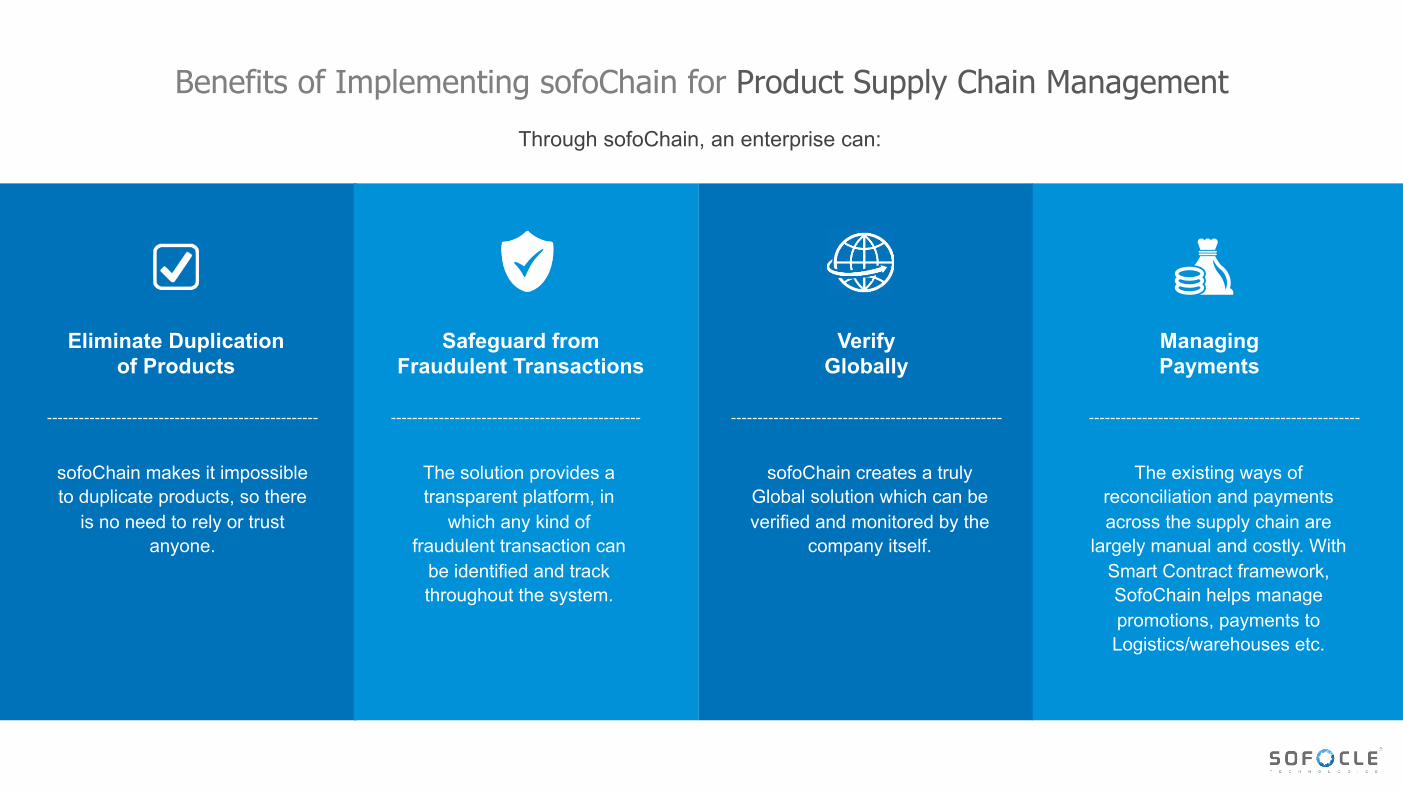

Benefits of Implementing sofoChain for Product Supply Chain ManagementThrough sofoChain, an enterprise can:

The system can easily trace and locate stolen

merchandise.

The existing data in supply chains resides in silos bringing huge in-

efficiencies. The data sharing among the various stakeholders

required for timely decision making is insecure and inefficient. Bringing all the stakeholders in a network with shared ledger brings

trust and transparency for secured sharing of data.

The solution can identify if a product was diverted from its

original destination.

sofoChain makes it impossible to duplicate products, so there

is no need to rely or trust anyone.

Eliminate Duplication of Products

Safeguard from Fraudulent Transactions

Verify Globally

Managing Payments

The solution provides a transparent platform, in

which any kind of fraudulent transaction can

be identified and track throughout the system.

sofoChain creates a truly Global solution which can be verified and monitored by the

company itself.

The existing ways of reconciliation and payments across the supply chain are

largely manual and costly. With Smart Contract framework, SofoChain helps manage promotions, payments to Logistics/warehouses etc.

Benefits of Implementing sofoChain for Product Supply Chain ManagementThrough sofoChain, an enterprise can:

Payments : Global Payments

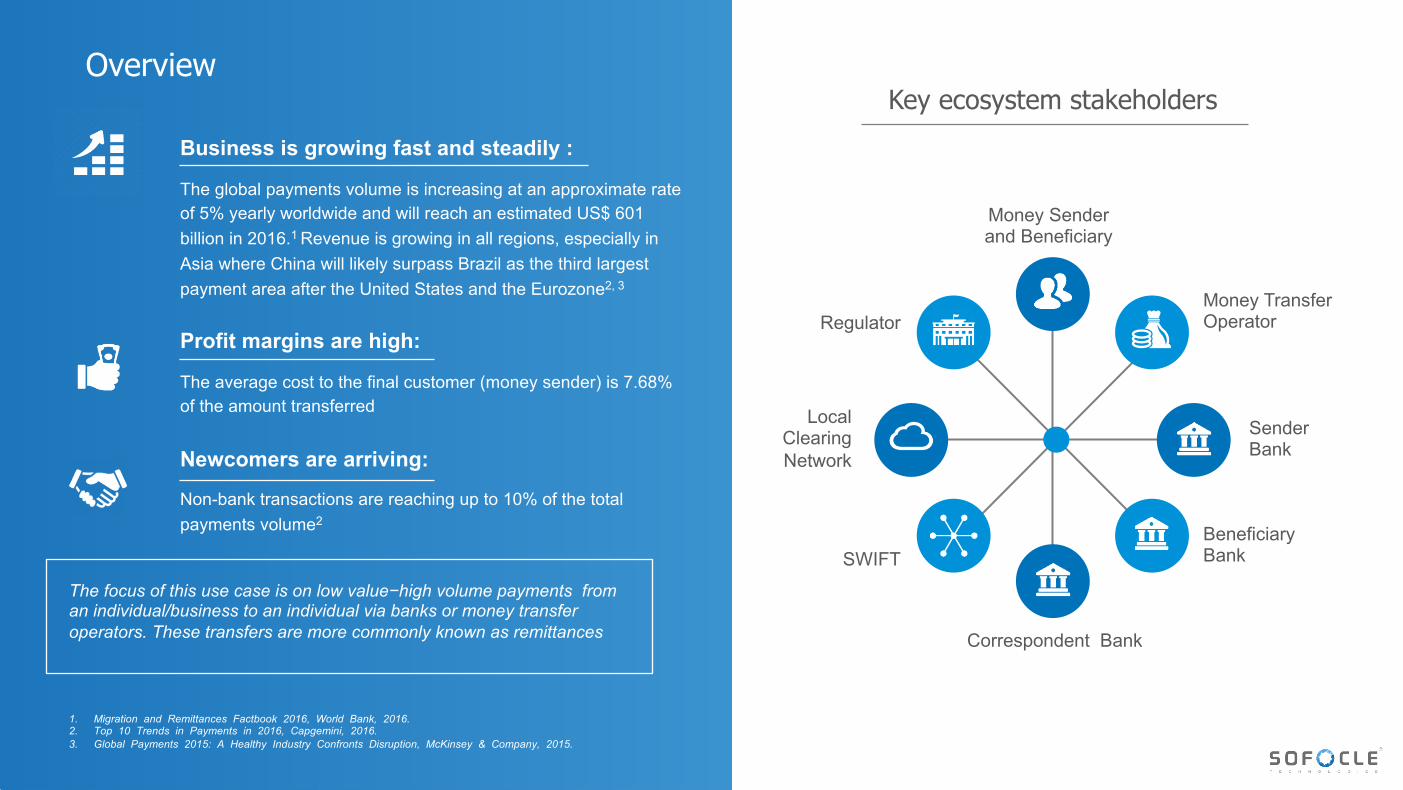

Overview

Business is growing fast and steadily :

The global payments volume is increasing at an approximate rate of 5% yearly worldwide and will reach an estimated US$ 601 billion in 2016.1 Revenue is growing in all regions, especially in Asia where China will likely surpass Brazil as the third largest payment area after the United States and the Eurozone2, 3

Profit margins are high:

The average cost to the final customer (money sender) is 7.68% of the amount transferred

Newcomers are arriving:

Non-bank transactions are reaching up to 10% of the total payments volume2

The focus of this use case is on low value−high volume payments from an individual/business to an individual via banks or money transfer operators. These transfers are more commonly known as remittances

1. Migration and Remittances Factbook 2016, World Bank, 2016.2. Top 10 Trends in Payments in 2016, Capgemini, 2016.3. Global Payments 2015: A Healthy Industry Confronts Disruption, McKinsey & Company, 2015.

Key ecosystem stakeholders

Money Sender and Beneficiary

Regulator

Local Clearing Network

SWIFT

Correspondent Bank

Beneficiary Bank

Sender Bank

Money Transfer Operator

Key market participants

Money Sender and Beneficiary

Regulator

Local Clearing Network

SWIFT

Correspondent Bank

Beneficiary Bank

Sender Bank

Money Transfer Operator

Core

Core

Core

Core

Supporting

Supporting

Supporting

Supporting

An individual or business wishing to transfer money (sender) to another individual or business (beneficiary) internationally

Non-bank companies specialized in international money transfer through a global network of agents

A sender’s preferred bank that offers international money transfer

A bank used by the beneficiary to receive funds

A bank that has access to foreign exchange (FX) corridors and facilitates the transfer (via nostro accounts and SWIFT)

The global member-owned cooperative provider of secure financial messaging and settlement services

The national interbank network that allow financial messaging/settlement (e.g. ACH, SPB and Zengin)

Central banks and monetary authorities that determine and monitor adherence to KYC and AML standards

Market participant Role Description

Sender

Regulator

Local Clearing Network

SWIFT

Correspondent Bank

Sender Bank

Money Transfer Operator

Local Clearing Network

Beneficiary Bank

Money Transfer Operator

Beneficiary

All Banks

Money Transfer Operator

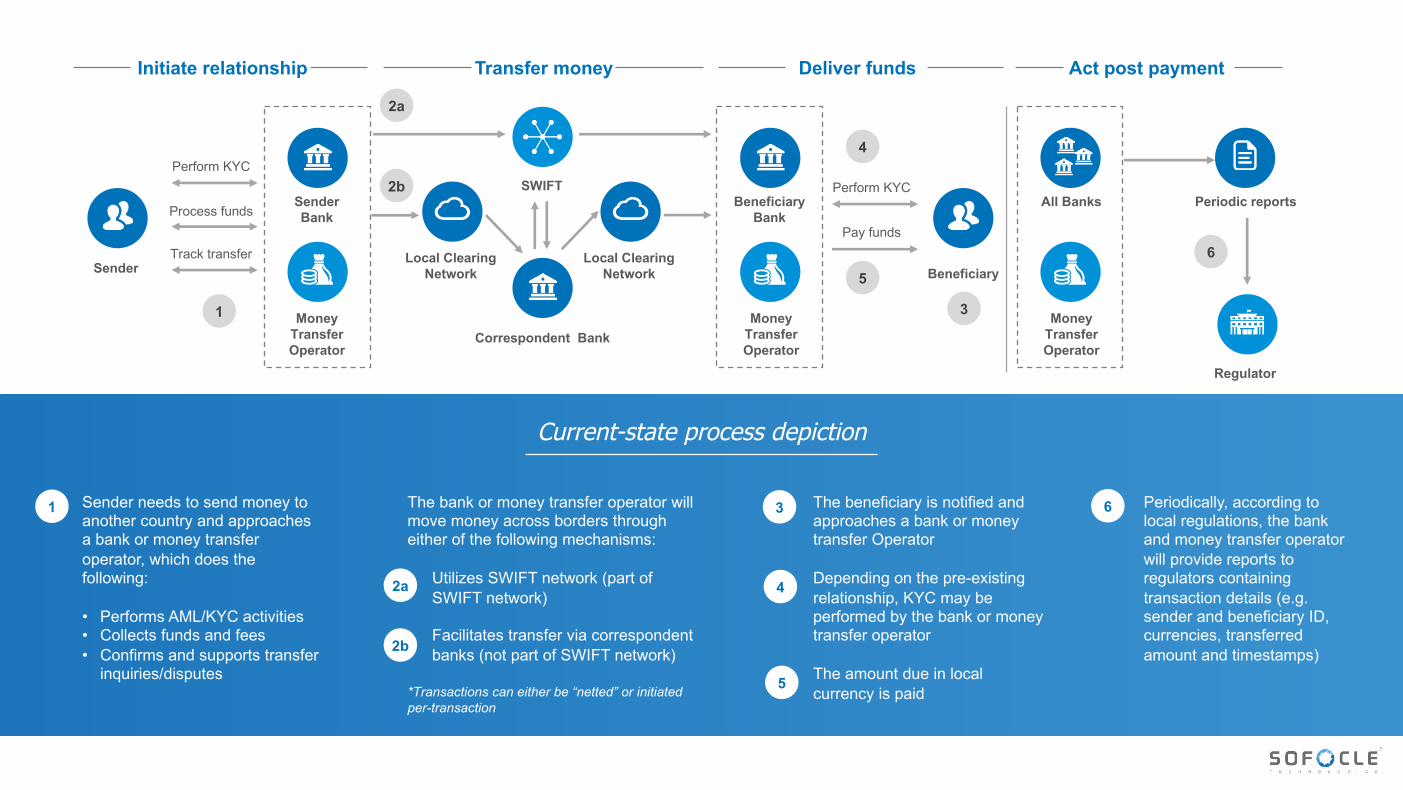

Perform KYC

Process funds

Track transfer

1

2a

2b Perform KYC

Pay funds

3

4

5

Periodic reports

6

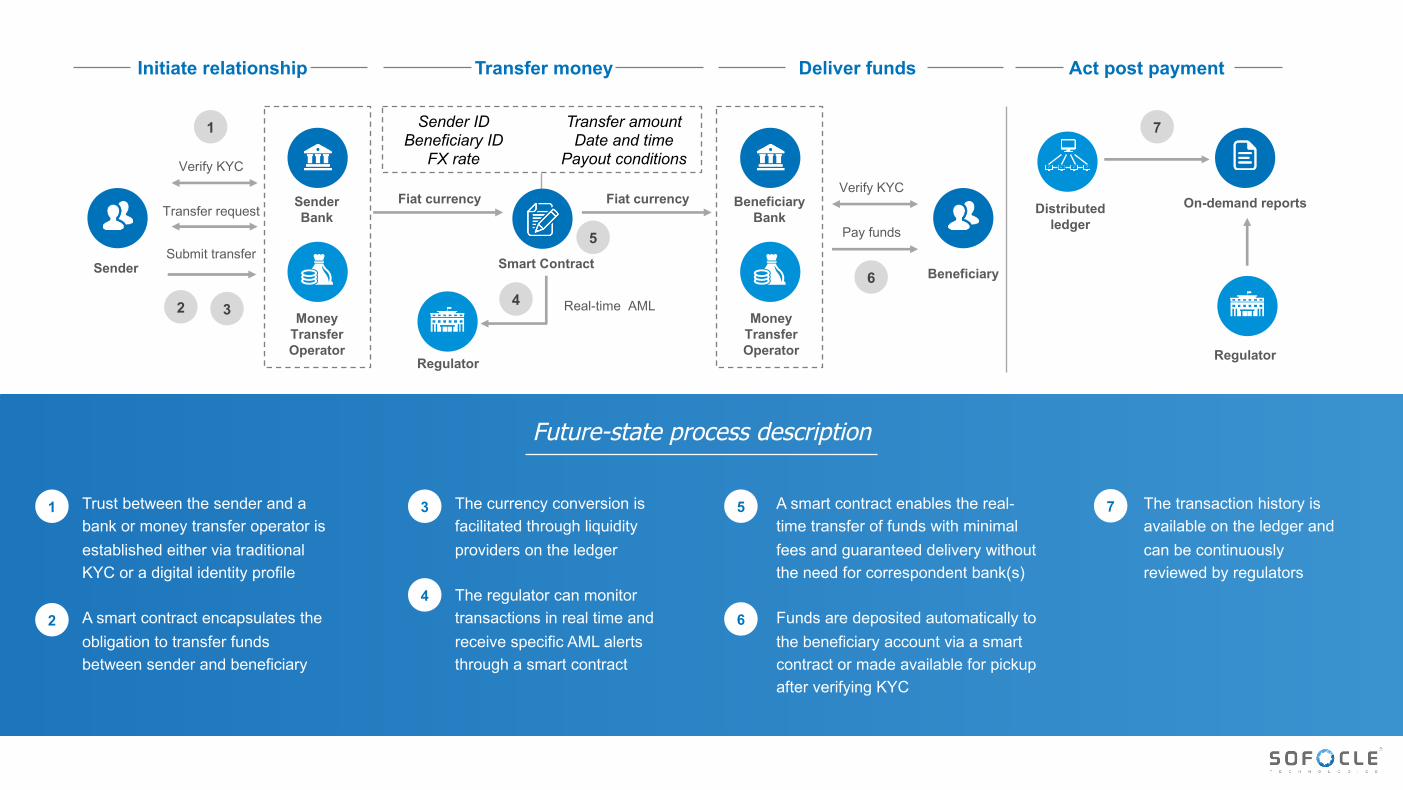

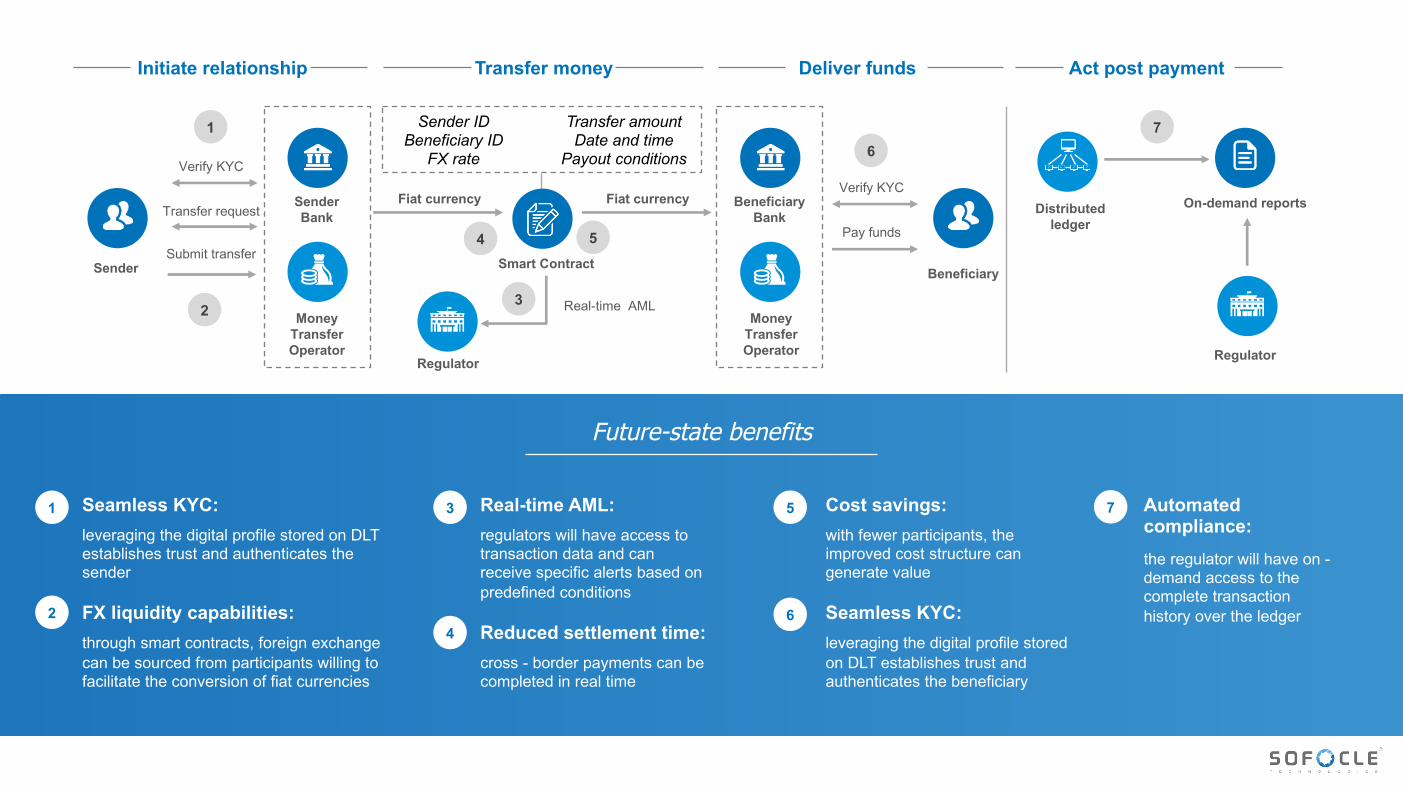

Initiate relationship Transfer money Deliver funds Act post payment

Current-state process depiction

Sender needs to send money to another country and approaches a bank or money transfer operator, which does the following:

• Performs AML/KYC activities• Collects funds and fees• Confirms and supports transfer

inquiries/disputes

The bank or money transfer operator will move money across borders through either of the following mechanisms:

Utilizes SWIFT network (part of SWIFT network)

Facilitates transfer via correspondent banks (not part of SWIFT network)

*Transactions can either be “netted” or initiated per-transaction

The beneficiary is notified and approaches a bank or money transfer Operator

Depending on the pre-existing relationship, KYC may be performed by the bank or money transfer operator

The amount due in local currency is paid

Periodically, according to local regulations, the bank and money transfer operator will provide reports to regulators containing transaction details (e.g. sender and beneficiary ID, currencies, transferred amount and timestamps)

1

2a

2b

3

4

5

6

Sender

Regulator

Local Clearing Network

SWIFT

Correspondent Bank

Sender Bank

Money Transfer Operator

Local Clearing Network

Beneficiary Bank

Money Transfer Operator

Beneficiary

All Banks

Money Transfer Operator

Perform KYC

Process funds

Track transfer

1

Perform KYC

Pay funds

3

4 5

Periodic reports

6

Initiate relationship Transfer money Deliver funds Act post payment

Current-state pain points

Inefficient onboarding: Information about the sender and beneficiary is collected via manual and repetitive business processes

Vulnerable KYC: Limited control exists over the veracity of information and supporting documentation, with various maturity levels across institutions

Cost and delay:

Payments are costly and time consuming depending on route

Error prone:

Information is validated per bank/transaction, resulting in high rejection rate

Liquidity requirement:banks must hold funds in nostroaccounts, resulting in opportunity and hedging costs

Vulnerable KYC: similar to #2, limited control exists over the veracity of information and supporting documentation, with various maturity levels across institutions

Demanding regulatory compliance: due to various data sources and channels or origination,regulatory reports can require costly technology capabilities in addition to complex business processes (often supported by multiple operation teams)

1 5 7

2

7

2

3

4 6

Sender

Regulator

Fiat currency Sender Bank

Money Transfer Operator

Beneficiary Bank

Money Transfer Operator

Beneficiary

Distributedledger

Verify KYC

Transfer request

Submit transfer

1

Verify KYC

Pay funds

3 4

5

On-demand reports

6

Initiate relationship Transfer money Deliver funds Act post payment

Future-state process description

Trust between the sender and a bank or money transfer operator is established either via traditional KYC or a digital identity profile

A smart contract encapsulates the obligation to transfer funds between sender and beneficiary

The currency conversion is facilitated through liquidity providers on the ledger

The regulator can monitor transactions in real time and receive specific AML alerts through a smart contract

A smart contract enables the real-time transfer of funds with minimal fees and guaranteed delivery without the need for correspondent bank(s)

Funds are deposited automatically to the beneficiary account via a smart contract or made available for pickup after verifying KYC

The transaction history is available on the ledger and can be continuously reviewed by regulators

1 5 7

2

7

2

3

46

Fiat currency

Smart Contract

Regulator

Real-time AML

Sender IDBeneficiary ID

FX rate

Transfer amountDate and time

Payout conditions

Sender

Regulator

Fiat currency Sender Bank

Money Transfer Operator

Beneficiary Bank

Money Transfer Operator

Beneficiary

Distributedledger

Verify KYC

Transfer request

Submit transfer

1

Verify KYC

Pay funds

3

4 5

On-demand reports

6

Initiate relationship Transfer money Deliver funds Act post payment

Future-state benefits

2

7

Fiat currency

Smart Contract

Regulator

Real-time AML

Sender IDBeneficiary ID

FX rate

Transfer amountDate and time

Payout conditions

Seamless KYC: leveraging the digital profile stored on DLT establishes trust and authenticates the sender

FX liquidity capabilities: through smart contracts, foreign exchange can be sourced from participants willing to facilitate the conversion of fiat currencies

Real-time AML:regulators will have access to transaction data and can receive specific alerts based on predefined conditions

Reduced settlement time:cross - border payments can be completed in real time

Cost savings:with fewer participants, the improved cost structure can generate value

Seamless KYC: leveraging the digital profile stored on DLT establishes trust and authenticates the beneficiary

Automated compliance: the regulator will have on -demand access to the complete transaction history over the ledger

1 5 7

2

3

46

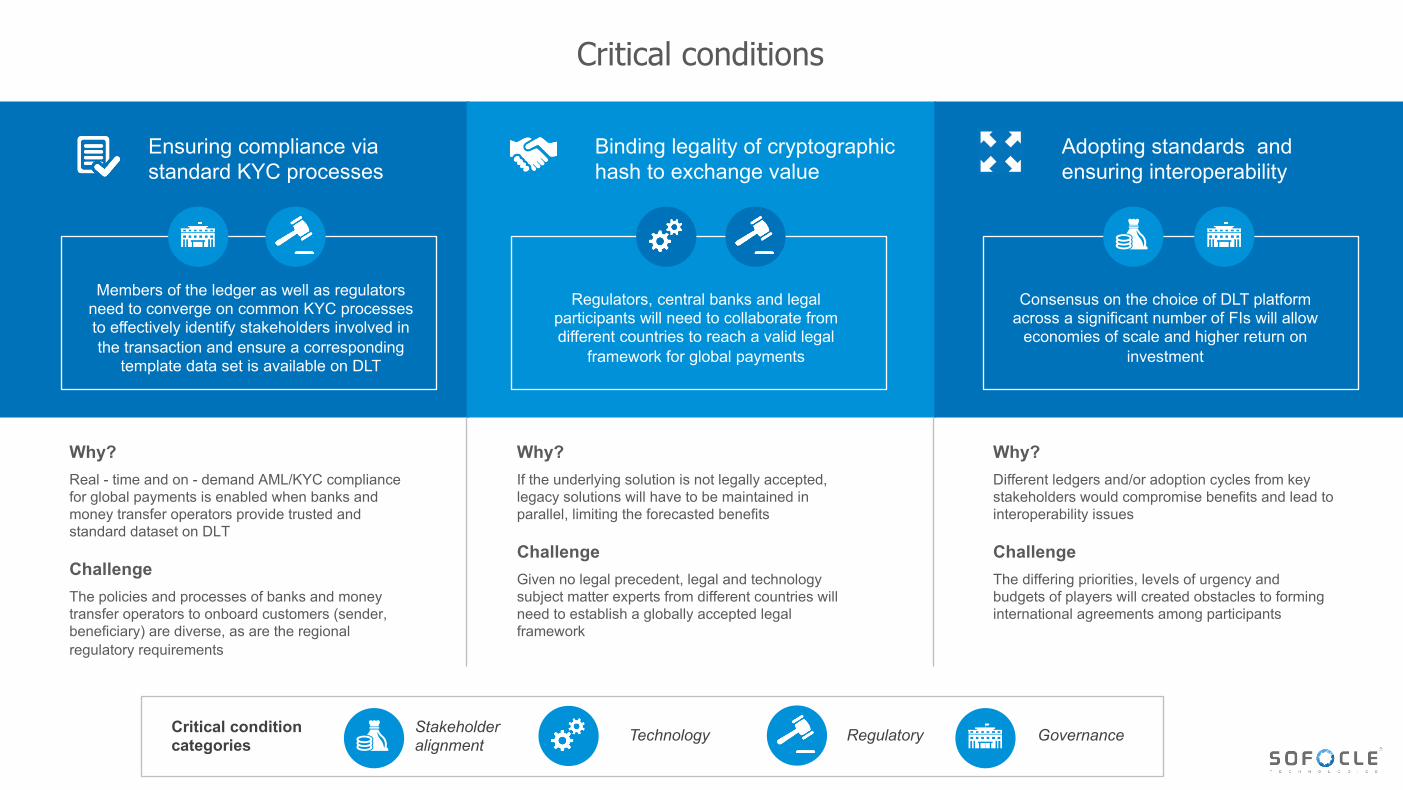

Critical conditions

Ensuring compliance via standard KYC processes

Binding legality of cryptographic hash to exchange value

Adopting standards and ensuring interoperability

Members of the ledger as well as regulators need to converge on common KYC processes to effectively identify stakeholders involved in the transaction and ensure a corresponding

template data set is available on DLT

Regulators, central banks and legal participants will need to collaborate from different countries to reach a valid legal

framework for global payments

Consensus on the choice of DLT platform across a significant number of FIs will allow

economies of scale and higher return on investment

Why?Real - time and on - demand AML/KYC compliance for global payments is enabled when banks and money transfer operators provide trusted and standard dataset on DLT

ChallengeThe policies and processes of banks and money transfer operators to onboard customers (sender, beneficiary) are diverse, as are the regional regulatory requirements

Why?If the underlying solution is not legally accepted, legacy solutions will have to be maintained in parallel, limiting the forecasted benefits

ChallengeGiven no legal precedent, legal and technology subject matter experts from different countries will need to establish a globally accepted legal framework

Why?Different ledgers and/or adoption cycles from key stakeholders would compromise benefits and lead to interoperability issues

ChallengeThe differing priorities, levels of urgency and budgets of players will created obstacles to forming international agreements among participants

Stakeholder alignment Technology Regulatory GovernanceCritical condition

categories

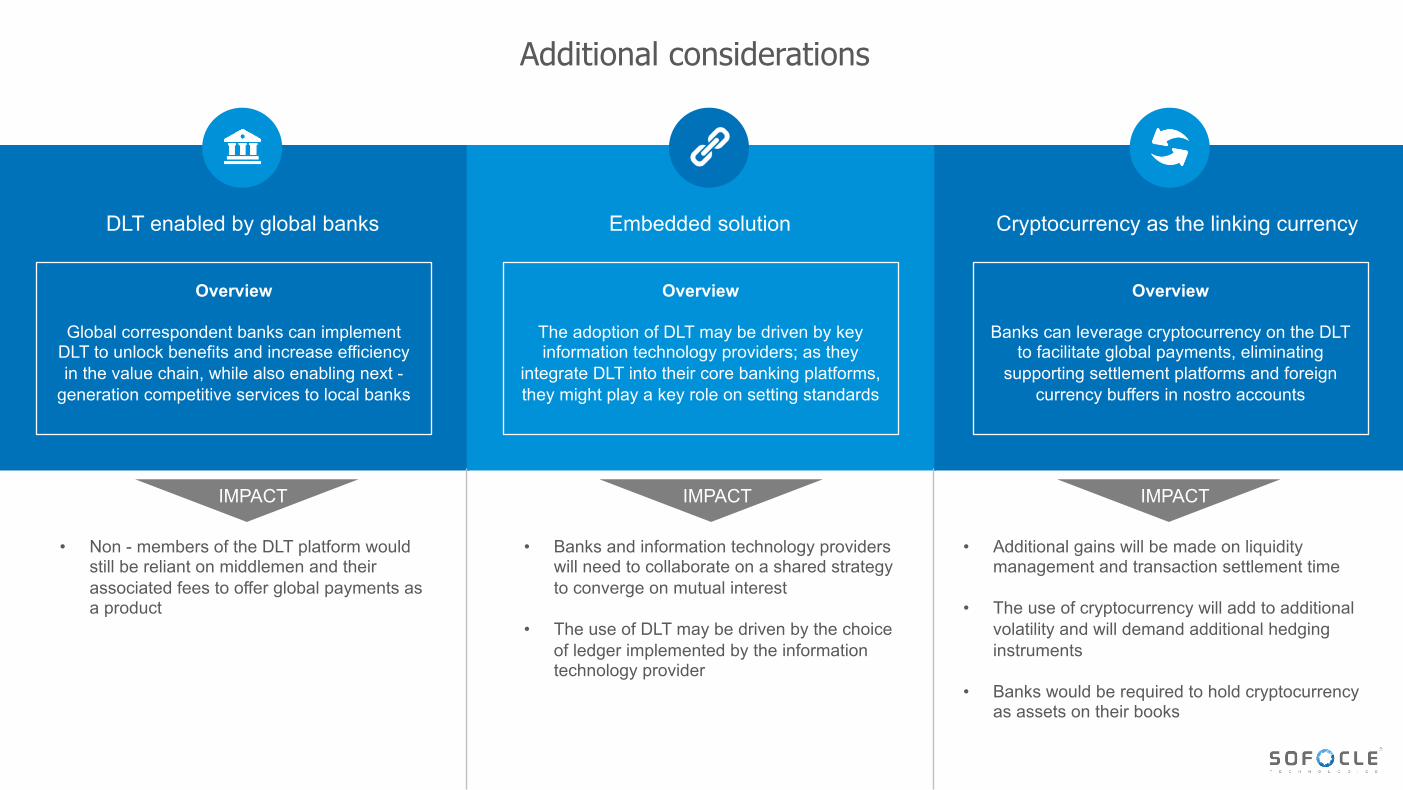

Additional considerations

DLT enabled by global banks Embedded solution Cryptocurrency as the linking currency

• Additional gains will be made on liquidity management and transaction settlement time

• The use of cryptocurrency will add to additional volatility and will demand additional hedging instruments

• Banks would be required to hold cryptocurrency as assets on their books

Overview

Global correspondent banks can implement DLT to unlock benefits and increase efficiency in the value chain, while also enabling next -

generation competitive services to local banks

Overview

The adoption of DLT may be driven by key information technology providers; as they

integrate DLT into their core banking platforms, they might play a key role on setting standards

Overview

Banks can leverage cryptocurrency on the DLT to facilitate global payments, eliminating

supporting settlement platforms and foreign currency buffers in nostro accounts

IMPACT

• Banks and information technology providers will need to collaborate on a shared strategy to converge on mutual interest

• The use of DLT may be driven by the choice of ledger implemented by the information technology provider

IMPACT

• Non - members of the DLT platform would still be reliant on middlemen and their associated fees to offer global payments as a product

IMPACT

Conclusion

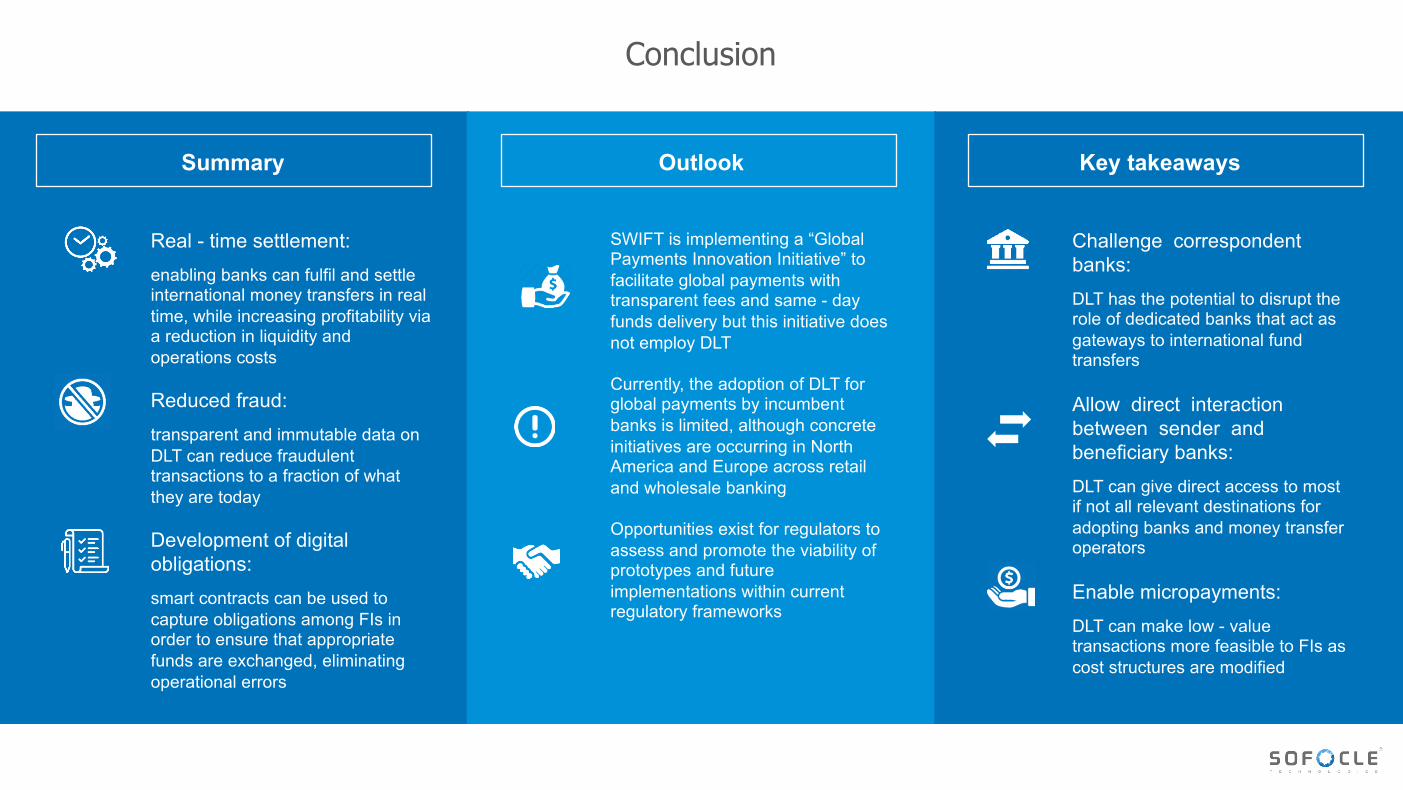

Summary

Real - time settlement:enabling banks can fulfil and settle international money transfers in real time, while increasing profitability via a reduction in liquidity and operations costs

Reduced fraud: transparent and immutable data on DLT can reduce fraudulent transactions to a fraction of what they are today

Development of digital obligations:smart contracts can be used to capture obligations among FIs in order to ensure that appropriate funds are exchanged, eliminating operational errors

Outlook Key takeaways

SWIFT is implementing a “Global Payments Innovation Initiative” to facilitate global payments with transparent fees and same - day funds delivery but this initiative does not employ DLT

Currently, the adoption of DLT for global payments by incumbent banks is limited, although concrete initiatives are occurring in North America and Europe across retail and wholesale banking

Opportunities exist for regulators to assess and promote the viability of prototypes and future implementations within current regulatory frameworks

Challenge correspondent banks:DLT has the potential to disrupt the role of dedicated banks that act as gateways to international fund transfers

Allow direct interaction between sender and beneficiary banks: DLT can give direct access to most if not all relevant destinations for adopting banks and money transfer operators

Enable micropayments:DLT can make low - value transactions more feasible to FIs as cost structures are modified

References

• BlockchainPoweredFinancialInclusion- PresentedbyPani Baruri – Cognizant• FutureOfFinancialInfrastructure– WorldEconomicForum2016

http://www.sofocle.comhttp://www.sofocle.ae

Sofocle Technologies LLC2001, Regal Tower, Business Bay,Dubai, UAE

Address

Mobile: +919821769996 Office: +91 120 6517460 Email: [email protected]

Contact

Sofocle Technologies Pvt. Ltd. A-83, First Floor, Sector-2, Noida - 201301, INDIA

NewDelhi|Dubai|Singapore