Embed Size (px)

Citation preview

Beth Israel Deaconess Medical Center:

How Patient Cost Estimates Will

Improve Patient Satisfaction and

Reduce Hospital Costs

June 17, 2013

• About Beth Israel Deaconess Medical Center

• Healthcare Industry Challenges

• Goals - Getting to the Ideal State

• Our Journey

• Workflows

• Best Practices and Lessons Learned

• Questions and Answers

Today’s Discussion

2

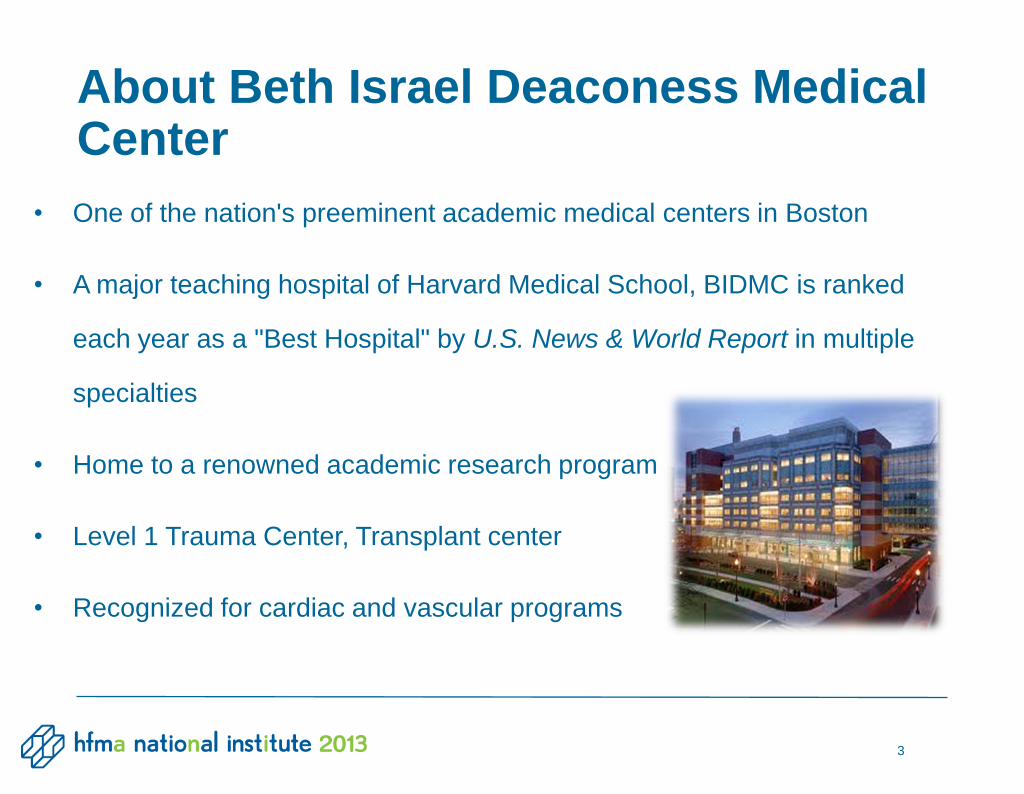

About Beth Israel Deaconess Medical Center

• One of the nation's preeminent academic medical centers in Boston

• A major teaching hospital of Harvard Medical School, BIDMC is ranked

each year as a "Best Hospital" by U.S. News & World Report in multiple

specialties

• Home to a renowned academic research program

• Level 1 Trauma Center, Transplant center

• Recognized for cardiac and vascular programs

l

3

• One of 15 hospitals in the Boston area

• 649 licensed beds: 440 of which are medical/surgical, 77

critical care and 60 OB/GYN beds

• 1,250 physicians, 8,000 employees

• Wide network of growing partnerships and affiliations

– Comprised of multiple community hospitals, physician groups

and community based practices and health centers

– Well over 25 different divisions, each with multiple

departments and clinics including satellites

The Complexity of BIDMC

4

Employers Shift More of the Healthcare Cost to Employees

• Backlash to providers

• Emergence of healthcare consumerism

• Driven by increased costs

Goal: Provide pricing transparency

Healthcare Industry

5

Managed Care Contracting

• Payer contracts require accepting all plans including:

– Tiered contracts

– High deductible plans

– Increased patient responsibility

Goal: Educate on payer benefits and requirements

Healthcare Industry

6

Patient Satisfaction

• Economic environment

• Payment responsibility shift to the consumer

• Uninformed public

• Sticker shock

• Patients taking responsibility for own health

• Increase in self-pay population and bad debt

Goal: Provide accurate estimates prior to service

Healthcare Industry

7

8

Healthcare Industry

Trends in High-Deductible Health Plans

• Upfront deductibles apply to everything except routine

• Patient cost sharing for both hospital and professional

services

• Payer counter strategy for no patient cost for routine

services

Goal: Reduce patient dissatisfaction directed at provider

9

Providing a Holistic View of Out-of-Pocket Services

• No means of accurately determining payer allowances

prior to treatment

• Payers are very careful about how they communicate what

is and is not covered

• Best-guess estimates provided upon patient request

• No collection of co-insurance and deductibles at time of

service

Goal: Increase self pay collections

Healthcare Industry

10

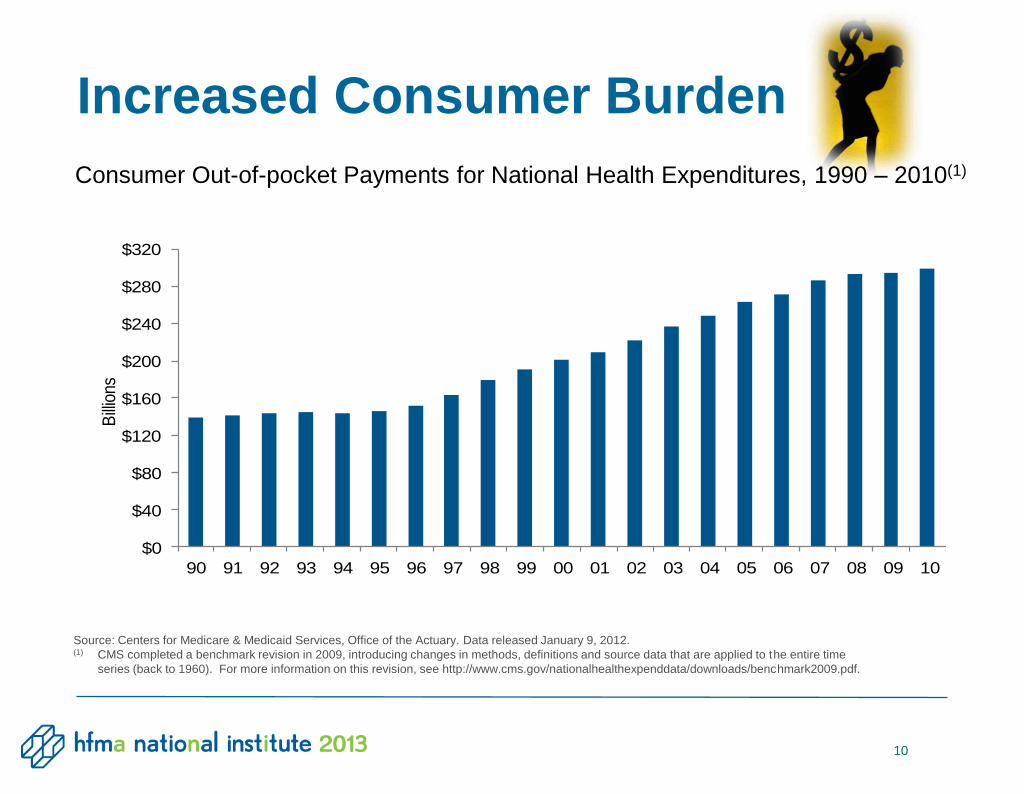

Consumer Out-of-pocket Payments for National Health Expenditures, 1990 – 2010(1)

$0

$40

$80

$120

$160

$200

$240

$280

$320

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Bill

ions

Source: Centers for Medicare & Medicaid Services, Office of the Actuary. Data released January 9, 2012. (1) CMS completed a benchmark revision in 2009, introducing changes in methods, definitions and source data that are applied to the entire time

series (back to 1960). For more information on this revision, see http://www.cms.gov/nationalhealthexpenddata/downloads/benchmark2009.pdf.

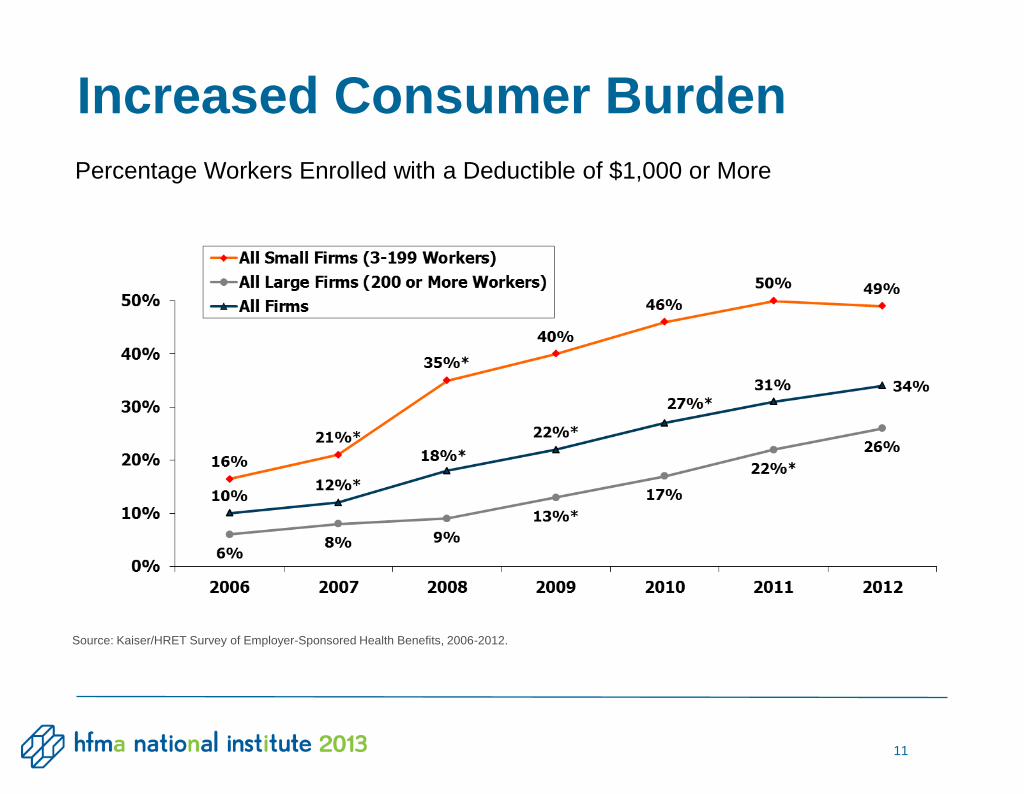

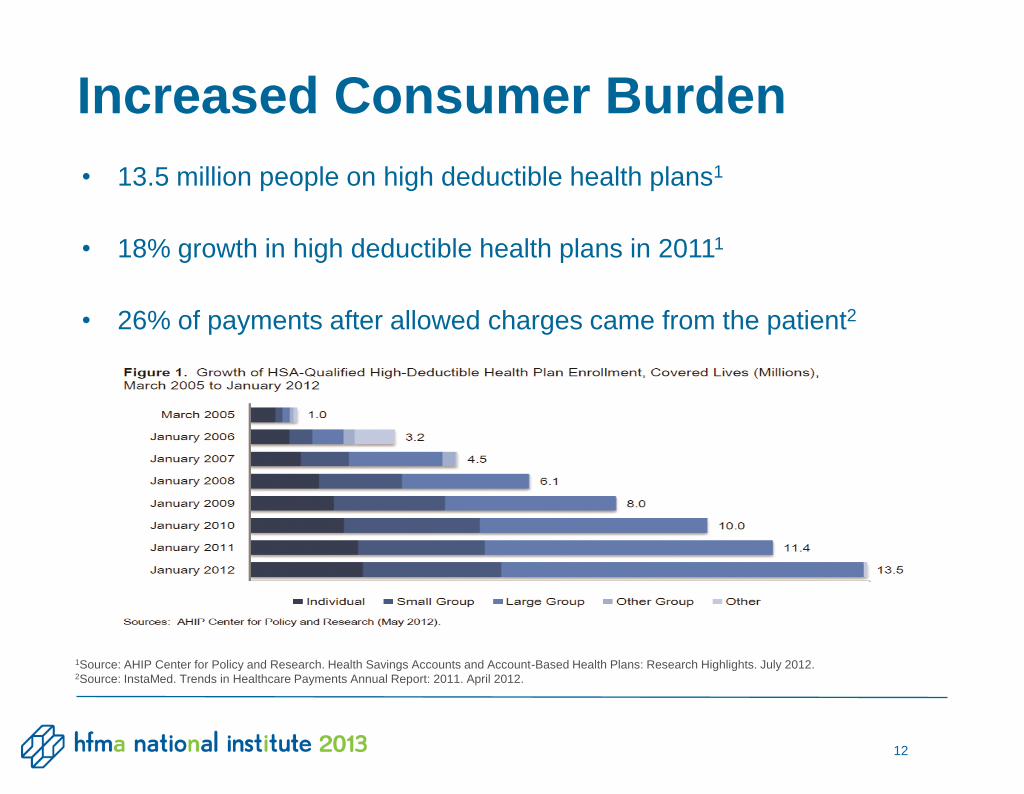

Increased Consumer Burden

11

Percentage Workers Enrolled with a Deductible of $1,000 or More

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2006-2012.

Increased Consumer Burden

12

• 13.5 million people on high deductible health plans1

• 18% growth in high deductible health plans in 20111

• 26% of payments after allowed charges came from the patient2

1Source: AHIP Center for Policy and Research. Health Savings Accounts and Account-Based Health Plans: Research Highlights. July 2012. 2Source: InstaMed. Trends in Healthcare Payments Annual Report: 2011. April 2012.

Increased Consumer Burden

Getting To An Ideal State

• Provide pricing transparency

• Educate on payer requirements and benefits

• Provide estimates prior to service

• Reduce patient dissatisfaction directed at provider

• Increase self pay collections and decrease bad debt

Goals

13

Initial Steps

• Gain strategic support at top levels of the organization

– Champion/s, Physicians

• Engage

– Department / practice liaisons, other billing companies

• Create

– Infrastructure to support project

– Project team

Getting Started

14

Decide on the Direction

• Create an Estimate Tool or Purchase?

– Internal discussion to create a tool

– Review and compare available tools

• Enterprise or Phase In?

– Determine the scope of both

• Communicate and or Collect?

– Identify the value and the impact of each

First Decisions

15

Purchase a Solution

• Why?

– Time to build and price

– Lack of in-house resources

– Packaged solution came with necessary features

Specialty Areas First

• Why?

– Enterprise too large and complex in scope

– Limited resources

Our Decisions

16

Communicate Estimates Initially

• Why?

– Time to obtain and review impact

– Gather and improve from feedback

– Time to prepare for collection roll out

Our Decisions

17

Identify and Select “Best” Practices/Departments to Start

• Some key considerations:

– Highest out of pocket expenses

– Who has the most predictable service?

– Lead time to time of service

– Who is interested in doing estimates

First Adopters

18

Introduce the Project to the Key Departments

• Review the need

• Explain the benefits

• Provide an overview of product and features

• Engage the physicians

Attract Interest

19

Analyze User Workflow

• Which services?

• Who will produce estimates?

• Who has the skills?

• How will estimates be delivered?

Identify Payers for Estimates

• Initially single payers only (no secondary insurers)

• Exclude Medicare, Masshealth (Medicaid)

Customization

20

Communication Strategy

• Collaborate with practice physicians

– Prepare patient

– Provide an introductory letter

– Not a collection notice

Customization

21

Setting Up the Tool

• Charge masters

• Payer contracts

• Matching the tool with the practice

• Provider procedure sets

• DRG or by charges

Set Up

22

Conduct Extensive Testing

• Verify against payments

• Verify against contracts

Provide Training

• On the estimator tool

• Additional necessary training

Milestones

23

Go Live

• Provide support

• Conduct QA

• Provide feedback

Milestones

24

25 25 25 25 25

Obstetrics Selected to Pilot the Tool

• 1st to roll out in May 2013

• Provides the most lead time to the service

• Most predictable service

Pilot Department

Two Estimates

• 1st at the time of scheduling

– Performed by Fiscal Clearance

– Sent with informational package to patient

• 2nd estimate sent at 32 weeks

– Authorization unit re-verifies eligibility, generates new

estimate and mails

– 1st deliveries in June

Workflow

26

Results

• 80 patient estimates sent out the first week

– Estimates produced for the entire month of

August

• Project 40 obstetric estimates weekly going

forward

Workflow

27

• Detail of proposed service

• Financial obligations

• Easy to follow numeric system

• English or Spanish

• Patient Portion Explanation

– Total due and why

– Verbiage - it is an estimate only

Patient Friendly Care Estimate

28

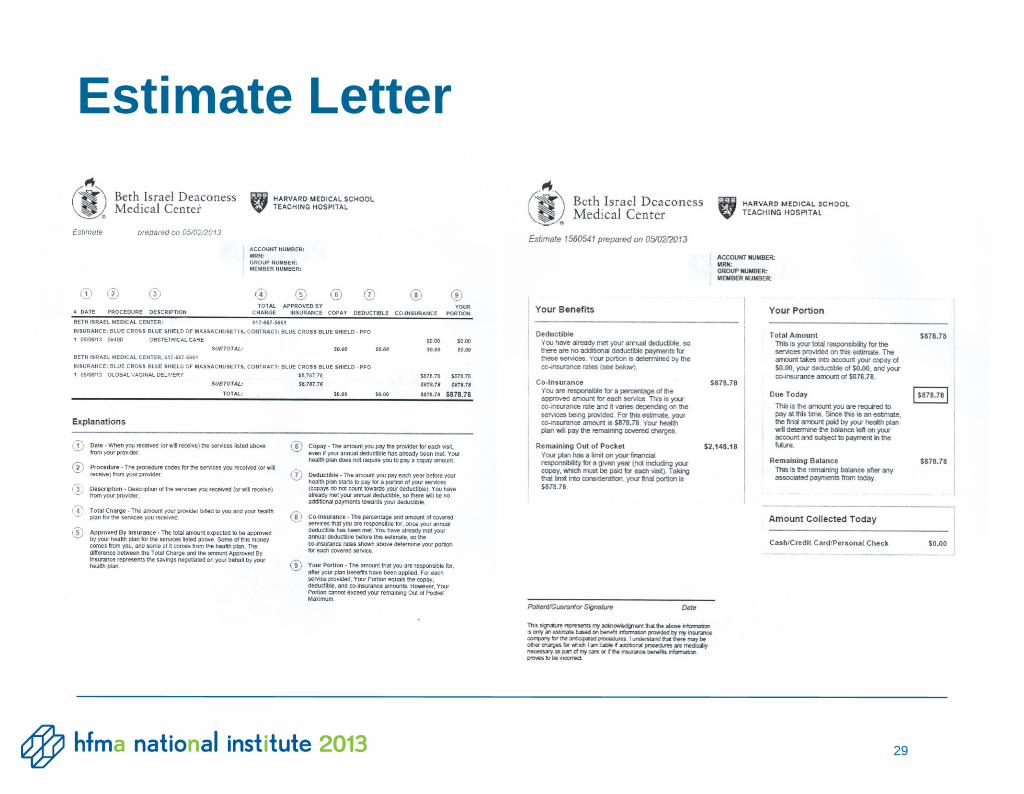

Estimate Letter

29

• Feedback to date from department, patients and

physicians

• Confirm estimate to actual

• Enhance training

• Continuous engagement with department

Continuous Improvement

30

31 31 31 31 31

Radiology

• Two areas

– Diagnostic Breast Imaging

– Mobile Radiology

• Roll out - work in progress

On Deck

Diagnostic Breast Imaging

• Requested by department head because of patient

complaints

• Quick turnaround after routine showed findings

• Estimate to be sent electronically to be delivered in

advance

• Patient responsibility is in stark contrast to routine

• No resource to produce estimates

Workflows

32

Mobile Radiology

• Lower volume

• Scheduled in advance (generally 5 days)

• MR staff have the most flexibility with workload to perform

estimates

Workflows

33

Expand to Other Areas

• Orthopedics, Surgery, Clinics

• Create estimates for additional procedures and payers

Improve the Product

• Identify issues and continue to enhance the product

• Provide training on new features, as necessary

Set Goals

• Identify, measure and monitor results

• Set strategy for collection

Next Steps

34

35 35 35 35

Foster Organizational Commitment

• Get leadership buy in – especially physicians

• Promote patient satisfaction and revenue cycle

optimization

Engage Departments throughout Healthcare System

• Start small with a predictable service

• Support the department to find where it fits in their

workflow

• Provide training

Best Practices and Lessons Learned

Provide Real Time Support to Departments

• On site for start up

• Remote support on-going

• Accuracy counts – spend time to QA

Prepare Patients & Staff for What is Coming and Why

• Publicize the new policy and when it will start

• Post notifications in office and facility

• Include notification in billing statements

Best Practices and Lessons Learned

36

Set Intermediate and Long Term Goals

• Consider education and communication as first step

• Consider partial collections if 100% is too big a step

• Internally celebrate progress

• Solicit and incorporate patient feedback

• Measure success

Best Practices and Lessons Learned

37

Questions?

Thank you!

39

Charles Messinger

Training and QA Director

www.bidmc.org

Beth O’Toole

Senior Director, Revenue Cycle

www.bidmc.org