Embed Size (px)

Citation preview

Bermuda Monetary Authority 1

Business Plan 2012

The Bermuda Monetary Authority (BMA) is the integrated regulator of the financial services

sector in Bermuda.

Established under the Bermuda Monetary Authority Act 1969, the BMA supervises,

regulates and inspects financial institutions operating in or from within the jurisdiction.

It also issues Bermuda’s national currency; manages exchange control transactions;

assists other authorities in Bermuda with the detection and prevention of financial

crime; and advises the Government and public bodies on banking and other financial

and monetary matters.

The Authority develops risk-based financial regulations that it applies to the supervision

of Bermuda’s banks, trust companies, investment businesses, investment funds, fund

administrators, money service businesses and insurance companies.

It also regulates the Bermuda Stock Exchange (BSX).

The Authority has regulatory responsibility for a market that comprises an investment

funds sector with an aggregate Net Asset Value of $178 billion; a banking sector with total

assets of $23 billion; the BSX with total market capitalisation of over $319 billion; as well

as over 1,200 companies in Bermuda’s insurance market with total assets in excess of

$496 billion, a market that wrote $120 billion in gross premiums.

See www.bma.bm for more information about the BMA and the Bermuda market.

Bermuda Monetary Authority 1

Section One Introduction 02

Section Two Commitment to Delivering Quality Supervision 04

Section Three International Developments 14

Section Four Focus on Operational and Cost Efficiencies 15

Business Plan 20122 Section One

Introduction

I am pleased to present the Authority’s

2012 Business Plan, my third as Chief

Executive Officer. Though several

elements of the plan will be familiar as

a result of work streams commenced in

prior years, I should point out that the

strategic intent of this latest edition has

changed significantly.

The 2012 Business Plan signals a

departure from previous plans in that

it heralds a new phase of supervision,

one that marks a shift from policy

development to implementation. This

ranges from enhanced insurance

supervision, to the completion of major

initiatives in the banking sector and a

proposed regime for corporate

service providers.

On the insurance side, attention will

be focused on the framework for group

supervision, which will be applied

to Class 4 and Class 3B companies

during 2012, ahead of the groups

regime becoming effective on 1st

of January 2013. This follows the

completion in 2011 of enabling legal

and infrastructural measures for group

supervision, along with pilot reviews,

trial runs and the identification of over

20 insurance groups for which the

Authority will be Group Wide Supervisor.

In tandem with this work, the Authority

will provide guidance to the market

regarding how it plans to lead and

participate in supervisory colleges,

which will become an increasingly

important forum for our interaction with

other international regulators in the

months ahead.

Indeed, the importance of such

interaction to the success of group

supervision cannot be over-emphasised.

Given the number of meetings that

have already taken place between

the Authority’s supervisors and their

European counterparts, I believe solid

foundations have been laid that will

help underpin the working relationships

considered by many to be a pre-requisite

to effective group supervision.

Among other developments planned

for the insurance sector in 2012 are

proposed changes in captive reporting

requirements as well as an extension

of GAAP reporting requirements to

include Class C and Class D Long-Term

Bermuda Monetary Authority 3

companies for year-end 2012 filings. The

Authority also aims to finalise its plans for

group supervision of the Long-Term sector

during 2012.

In the banking sector, the Authority

will continue to work towards the

development of specific proposals for

the application of Basel III in Bermuda.

Additionally, banking intervention powers

will also be advanced during 2012,

with provision of the required statutory

measures enabling Bermuda’s authorities

to intervene promptly to deal with

problem banks and to protect depositors.

The Corporate Service Provider Business

Act, a new regime for the prudential

regulation and oversight of corporate

service providers, was proposed by the

Authority in 2011 and will be the subject

of market consultation during the

coming year.

In terms of the Authority’s capabilities,

the Business Plan makes clear that we

will continue to focus on operational and

cost efficiencies while providing an IT

infrastructure that enables us to deliver

quality supervision.

Quality supervision will remain a critical

objective in 2012. While the challenge

of change is evident on every page of

the Business Plan, the Authority has

no intention of changing its focus on

providing the kind of quality supervision

that works for Bermuda. In this regard,

the Authority is particularly pleased

with preliminary guidance indicating

that the unique characteristics of

Bermuda’s insurance industry are likely

to be recognised and accommodated

under Europe’s Solvency II Directive.

This is an important aspect of our quest

for Solvency II equivalence. While we

are committed to ensuring we achieve

consistency with international standards,

we do not intend to simply duplicate

them and apply them here. Instead, our

policy is always to adapt such standards

appropriately to take account of the

nature of the business conducted in

our jurisdiction.

As with any exercise concerning future

developments, the Authority’s Business

Plan is premised on certain assumptions.

Not the least of these is the assumption

that we will continue to attract and retain

the talent that will enable us to deliver

the supervisory product expected of us.

While competition for talent remains one

of our toughest challenges, I am confident

that with our existing high level of human

capital and the support of the markets

we supervise, we will continue to provide

the high level of superior service that is

only ever possible from a committed and

motivated professional workforce such

as ours. I am honoured to be able to call

them colleagues and privileged to be

allowed to lead them and the Authority in

the execution of our 2012 Business Plan.

Jeremy CoxChief Executive Officer

Business Plan 20124 Section Two

Commitment to Delivering Quality Supervision

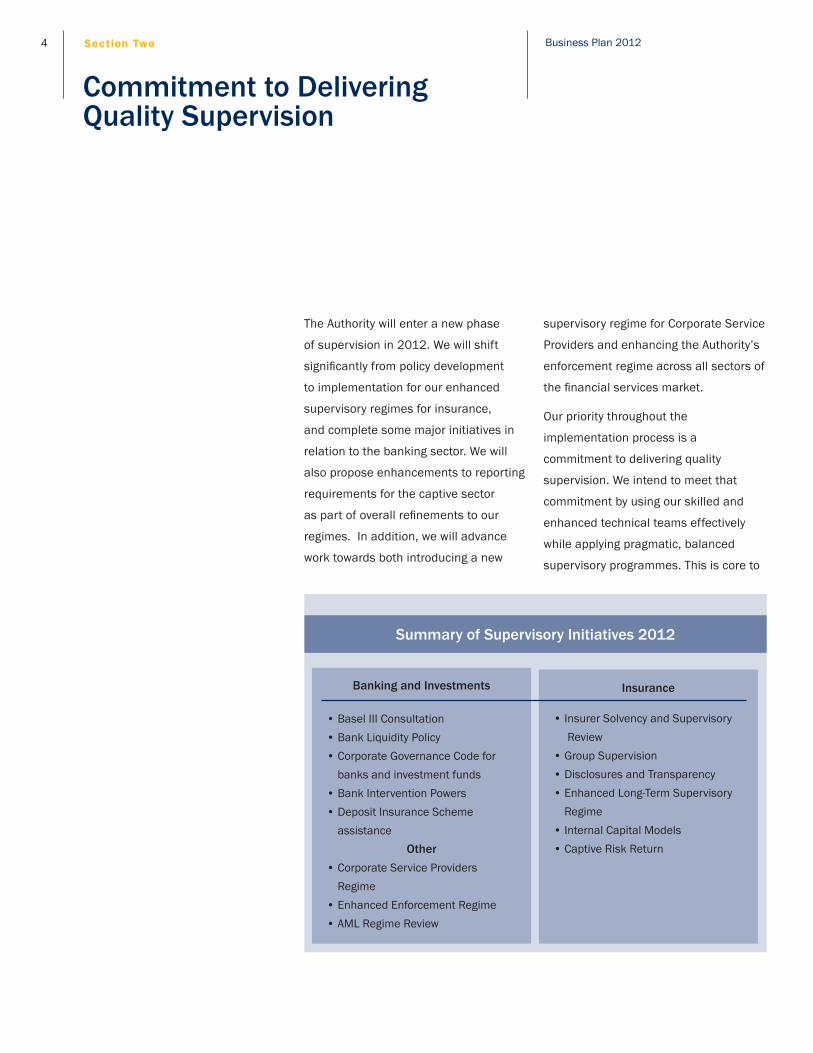

The Authority will enter a new phase

of supervision in 2012. We will shift

significantly from policy development

to implementation for our enhanced

supervisory regimes for insurance,

and complete some major initiatives in

relation to the banking sector. We will

also propose enhancements to reporting

requirements for the captive sector

as part of overall refinements to our

regimes. In addition, we will advance

work towards both introducing a new

supervisory regime for Corporate Service

Providers and enhancing the Authority’s

enforcement regime across all sectors of

the financial services market.

Our priority throughout the

implementation process is a

commitment to delivering quality

supervision. We intend to meet that

commitment by using our skilled and

enhanced technical teams effectively

while applying pragmatic, balanced

supervisory programmes. This is core to

Summary of Supervisory Initiatives 2012

Banking and Investments

• Basel III Consultation • Bank Liquidity Policy• Corporate Governance Code for

banks and investment funds• Bank Intervention Powers• Deposit Insurance Scheme

assistanceOther

• Corporate Service Providers Regime

• Enhanced Enforcement Regime• AML Regime Review

Insurance

• I nsurer Solvency and Supervisory Review

• Group Supervision• Disclosures and Transparency• Enhanced Long-Term Supervisory

Regime• Internal Capital Models• Captive Risk Return

Bermuda Monetary Authority 5

our responsibilities as the regulator of

Bermuda’s financial markets. We will

also ensure that Bermuda’s regulations

balance prudential considerations and

alignment with international standards

with business efficiency.

Insurance Supervision – Moving Forward with Regime ImplementationThrough 2012, work will continue to

implement the policies developed in

2011 to ensure the Authority remains

an effective, risk-based regulator for

the insurance sector. Highlights of our

next phase of enhancements for the

commercial insurance sector’s supervisory

toolkit, i.e. Class 4, Class 3B, Class 3A and

Classes E, D and C Long-Term firms, follow.

Insurer Solvency

Our work on enhancing Bermuda’s

solvency regulations for the insurance

sector has been the cornerstone of policy

and supervisory regime development over

the past three years. Having introduced our

enhanced standard capital model – the

Bermuda Solvency Capital Requirement

(BSCR) - initially for application to Class

Highlights of Insurance Capital Adequacy Framework Changes

Bermuda Solvency Capital Requirement (BSCR) – standard capital model

Economic Balance Sheet

Commercial Insurers Solvency Self-Assessment (CISSA) - Bermuda-specific ORSA process

Quarterly Financial Return

Eligible Capital

• Full implementation for Class 3B insurers as well as Class 4 firms

• Continued phased implementation of refined model for Class 3A and Class E firms for year-end 2011 filings; and to Class C and Class D for 2012 year-end

• Trial run for Class C and D insurers in Q2

• Group BSCR filing for Class 4 and Class 3B groups; trial runs for Class 3A and Class E

• Consultation Paper to be issued by Q2 with proposals for implementation with respect to Long-Term and General Business

• The Authority will begin to review CISSAs in 2012 for year-end 2011 filings from Class 4, 3B, 3A and Class E firms

• The Quarterly Financial Return will be a new filing for May, August and November 2012. It will comprise unaudited financial statements, intragroup transactions and risk concentrations. This requirement will apply to Class 4 and Class 3B insurers.

• Revised Rules effective 1st January 2013 for most classes of insurers.

Component Developments for 2012

Business Plan 20126

4 firms, and subsequently to Class 3B

insurers, we will continue phased roll out

to the rest of the commercial market. This

will also apply to other elements of the

enhanced solvency framework.

Group Supervision

Work during 2011 focused on putting

final elements of the policy and

legislative infrastructure in place for

group supervision. A key element of this

work included issuing the Insurance

(Group Supervision) Rules 2011 as

well as the Insurance (Prudential

Standards) (Insurance Groups Solvency

Requirement) Rules 2011. The Authority

also identified over 20 insurance groups

for which the BMA will be the Group Wide

Supervisor (GWS). We also piloted a trial

run of the Groups BSCR with Class 4 and

Class 3B insurers.

In 2012, the focus will be on preparing

for full implementation of the supervisory

review process for Bermuda’s insurance

groups beginning 1st January 2013.

The platform is set for moving forward in

this regard: group solvency and financial

reporting requirements are in place; we

have established group-specific on-site

processes; and we will apply the framework

fully to Class 4 and Class 3B groups

incorporating insights gained from the trial

run and group on-site pilot reviews.

Holding supervisory colleges with fellow

regulators will remain an important

element of our work. We will use such

colleges to review and assess insurance

groups. This will cover financial soundness

and capital adequacy; group corporate

governance; risk exposures and

concentration; intra-group transfers; and

risk management and internal controls.

We are establishing formal governance

processes for supervisory colleges that the

Authority will host, to ensure clarity for all

participants. These governance processes

will include the use of memoranda

of understanding and confidentiality

agreements, as well as rules of

engagement for decision-making, dispute

resolution and supervisory coordination.

Our work during 2012 will also include a

phased trial run of the Groups’ BSCR with

insurance groups that include large Long-

Term (Class E) insurers, and Class 3A firms

that meet the Authority’s criteria for a group

as outlined in Section 27B of the Insurance

Act 1978. We will also communicate to the

market in the first half of the year regarding

how the Authority will lead and participate

in supervisory colleges.

Insurance group reporting requirements

will take effect for the 2011 year-end;

however, transitional arrangements will

be in place for firms to reach compliance

with other aspects of the group supervision

regime by the time they become effective

on 1st January 2013.

Additional Framework Enhancements

Consistent with the Authority’s overall

commitment to ensure Bermuda’s

framework remains aligned with relevant

international standards, and based on the

European Insurance and Occupational

Pensions Authority’s (EIOPA) recent

Solvency II assessment, we are proposing

specific additional enhancements to our

commercial insurance framework.

We are currently in consultation with the

commercial market on these additional

proposals, which focus on:

• the independence of the internal audit function;

• removing the ability to co-mingle Long-Term and General Business activities

Bermuda Monetary Authority 7

written on a direct basis; • the segregation within an entity of

insurance and non-insurance business;• new licensing requirements;• minimum solvency measures; • solvency reporting and disclosure; and • new material change notifications.

Post-consultation, we will develop

supporting legislative changes. We plan

for these proposals to be effective as of

January 2013.

Insurance Company Disclosures

and Transparency

Effective year ended 31st December

2011, Class 3A and Class E Long-Term

insurers will be required to produce publicly

available GAAP financial statements. This

follows on from similar requirements

for Class 3B and Class 4 insurers that

became effective for year-end 2010 filings.

We plan to extend this requirement to Class

C and Class D Long-Term firms for year-end

2012 filings.

This work completes Phase 1 of our

disclosures and transparency initiative.

Phase 2 (reporting periods 2012 to 2014)

and Phase 3 (reporting periods 2015

and beyond) will be primarily dedicated

to requiring public disclosures that are

consistent with both prevailing international

standards and market conditions. As we

enter Phase 2 in 2012, we will review the

effectiveness of our public disclosures and

propose appropriate enhancements.

BSCR Impact Assessments

The Authority will also seek voluntary

participation from firms for capital

requirement impact assessments

in 2012. This work will assist with

determining how best to transition from

statutory accounting to a GAAP basis

for regulatory capital purposes within

Bermuda’s framework, and how to

appropriately incorporate an economic

balance sheet requirement. It will also be

helpful in enhancing the existing risk-

sensitivity built into the BSCR model.

Enhanced Long-Term

Supervisory Regime

The Authority completed the process to

reclassify Bermuda’s Long-Term insurance

sector into Classes from A through to E

in 2011. This reclassification process

was designed to ensure such firms are

appropriately supervised within the

Authority’s enhanced risk-based framework.

We also conducted a trial run in 2011

of BSCR filings for Class E insurers, as

a precursor to phased implementation

overall for the Long-Term sector. Phased

application of the BSCR for Class E insurers

will take place in 2012, along with trial runs

for Class C and Class D firms. The trial run

will also cover CISSA, eligible capital and

disclosure requirements.

As part of the trial run, the Authority issued

a Group Supervisor Questionnaire to gather

information to determine the Long-Term

firms for which the Authority may assume

responsibility as GWS. We will complete

assessing the market’s responses to this

survey in 2012 to assist with finalising our

plans for group supervision of the Long-

Term sector.

Internal Capital Models

The Authority recognises the complexities

involved in the development of internal

capital models (ICMs), and the significant

time and resources required to ensure

that the review and evaluation of such

models is effective for both the regulator

and the market. In 2011, the Authority

made further progress in the development

and implementation of its framework

Business Plan 20128

through issuing revised Guidance Notes,

conducting a pilot review of a Long-Term

insurer and holding discussions with

individual insurers interested in applying

to use an ICM for regulatory

capital purposes.

In 2012, the Authority will continue

towards full implementation of the

framework by providing further guidance

to the Long-Term sector, enhancing the

ICM Review Process and developing

additional resources to conduct

reviews. The Authority will also engage

in discussions and seek to coordinate

activities with other regulatory agencies in

preparation for Group ICM reviews.

Captive Risk Return

While we have focused our framework

enhancements on the commercial market

in recent years, the Authority is now

proposing refinements to our captive

sector regime to ensure it remains

effective and appropriately consistent

with international standards.

We are proposing enhancements to

reporting requirements for captives, i.e.

General Business Classes 1, 2, 3 and

Classes A and B Long-Term firms through

a new Risk Return. The Risk Return

will include an own risk and solvency

assessment - appropriately modified to

reflect the limited purpose and lower risk

profile of captives.

Internal Capital Models Developments

• Pilot reviews with General Business and Long-Term insurers

• Enhanced ICM qualification process, including development of ICM information requests and internal scoring mechanisms

• Expanded pre-application process

• Revised ICM Guidance Notes to include enhancements to review process and extension of scope to Class 3B and Class 3A firms

• ICM analysis and assessment internal training programme

• ICM review business model finalised

• Review of ICM Guidance Notes to extend scope to Long-Term insurers

• Work with insurers interested in ICM application, including potential pilot review activity for various risk modules

• Internal planning and resource development

• Coordination with other regulatory agencies in preparation for Group ICM reviews

• Finalisation and communication of full implementation timeframe

2012 InitiativesCompleted To Date

Bermuda Monetary Authority 9

This Risk Return will be combined with

existing submissions in one consolidated

annual filing with the Authority,

enhancing the efficiency of the annual

reporting process.

The enhanced reporting will ensure

that captive firms remain appropriately

classified and supervised within our risk-

based framework.

Market consultation on this proposal is in

progress and the Authority will consider

feedback received and the results of a

trial run in finalising the enhancements in

2012. The Authority intends to make these

refinements in a proportionate manner that

ensures that Bermuda’s captive regime

remains fit for purpose, practical and

appropriate.

Banking Supervision – Basel III and BeyondPreparing for Basel III

Basel III is the name given to the revised

set of bank capital standards adopted by

the international banking regulators that

are members of the Basel Committee

on Banking Supervision. In 2012, the

Authority will consider the scope of Basel III

implementation in the Bermuda market.

We have already begun discussions with

the market in this regard, setting out

initial proposals in a Discussion Paper

entitled ‘Implementation of Basel III in

Bermuda’ at the end of 2011. Market

consultation will continue into 2012,

along with our on going monitoring of

international developments on Basel III as

we work towards establishing more specific

proposals for its application in Bermuda.

Bank Liquidity Policy

Our review of the Authority’s existing

liquidity policy for banks began in 2010

and included the release of “Principles

for Sound Liquidity Risk Management

and Supervision” in December 2010.

During 2011 the Authority collected data

on banks’ liquidity risk management

practices through an industry self-

assessment process and assessed

banks’ compliance with the liquidity risk

management principles.

In 2012 we will continue our reviews to

ensure that banks have specific action

plans in place to achieve compliance. We

will continue to review our standards in

light of market consultation and the latest

guidance from the Basel Committee on

liquidity risk management.

Bank Intervention Powers

During 2011, the Authority published

a Consultation Paper on ‘Banking

Intervention Powers’. In 2012, the Authority

will work with industry to finalise the

legislative framework for this initiative,

specifically, development of the Banking

(Special Resolution Regime) Act. The

Act will provide the required statutory

provisions to enable Bermuda authorities

to intervene promptly in order to deal with

problem banks and protect depositors. It

is envisaged that this legislation will be

presented to Parliament in 2012.

Deposit Insurance Scheme (DIS)

In 2011, the Bermuda Government

enacted the Deposit Insurance Act 2011

to prepare the way for implementing this

important consumer protection initiative.

The primary objectives of the deposit

insurance scheme (DIS) are to protect

small depositors and support continued

stability in Bermuda’s financial system

and economy.

Business Plan 201210

As a starting point for establishing the

DIS, the maximum coverage amount

per depositor, per institution will be

$25,000. The Scheme will be funded by

mandatory contributions (premiums) from

all of Bermuda’s banks, as compulsory

participation is an internationally-adopted

practice for such schemes and promotes

comprehensive protection for depositors.

In 2012, the Authority will continue

to assist the Ministry of Finance with

establishing the Deposit Insurance

Corporation (DIC). The DIC will be the

independent statutory body that will

administer the DIS in Bermuda.

Corporate Governance Code

Market consultation is in progress on

the Authority’s proposals to introduce

a Corporate Governance Code for

Bermuda’s banks.

We issued a Consultation Paper at the

end of 2011 proposing 13 principles

and related guidance that reinforce key

elements of corporate governance that are

already generally accepted and established

by banks in Bermuda. The issuance of a

Code will reinforce these sound practices

and provide banks with detailed guidance

on risk management and corporate

governance practices and compliance

with minimum licensing criteria. After

completing consultation with the market,

the Authority will assess feedback received

in order to issue the final Code by end

2012. We intend to consult on extending

the principles established in the Corporate

Governance Code to other financial

services sectors as part of our policy work

in 2012.

Asset Management DevelopmentsWe will also continue to provide input to

market deliberations during the year on

further development of Bermuda’s asset

management sector. Our participation

is to ensure that information from the

regulatory perspective remains a key

part of such developments.

This work is also designed to ensure

that all parties involved, from the

Authority to industry to the Bermuda

Government, take into account both

potential framework enhancements

within Bermuda as well as the impact of

international developments, e.g. Europe’s

Alternative Investment Fund Managers

Directive, and global regulatory measures

being promulgated by the G20 and the

Financial Stability Board.

In 2011 we released a Consultation Paper proposing the prudential regulation and oversight of corporate service providers (CSPs). Establishing such a regime for CSPs would support appropriate supervisory monitoring of this business in Bermuda, while also accommodating the market’s ability and desire to provide such services within the jurisdiction.

We have subsequently issued, for market consultation, draft legislation to facilitate this regulatory oversight - the Corporate Service Provider Business Act 2011. This legislation reflects the long-standing regulatory powers and includes, among other provisions, proposed licensing criteria and reporting requirements for CSPs.

Corporate Service Provider Regime

11Bermuda Monetary Authority

A successful outreach campaign, which continued throughout 2011, has resulted in improved awareness among industry regarding requirements and obligations under Bermuda’s AML/ATF regime. Extension of the on-site programme to support AML supervision during the year also contributed to this higher awareness. The Authority conducted 21 on-site visits in 2011– covering firms in the trust, investment, banking, money service business, and fund administration sectors. In addition, the Unit’s development and maintenance of the non-licensed persons register continues with some 453 institutions currently registered.

The next International Monetary Fund (IMF) review of Bermuda’s AML regime is currently scheduled for early 2014. In 2011, as a part of preparations for the IMF visit, the Authority commissioned an effectiveness review of the regime and compliance levels among Bermuda’s AML-regulated financial institutions in relation to the Financial Action Task Force (FATF) 40+9 recommendations for AML regulation. The report from this initiative is due early in 2012 and its recommendations will assist with applying further refinements to the AML regime during the year as deemed necessary.

The Authority will enter a new phase of AML supervision in 2012. We will conduct industry-specific desk-based reviews during the year. The desk-based reviews will require examination using a risk-based approach of the

AML/ATF policies and procedures of companies in the trust, fund and fund administration, and NLP sectors. This will enable us to direct an element of the resources in our AML/ATF Unit to provide additional technical support to the supervisory teams within the Authority, and ensure training sessions are provided as required. There will also be a greater role for this Unit with respect to supporting general enforcement within the Authority, including refinement of the enforcement process. The Unit will also provide research and direction from the AML perspective, as required, to the supervisory teams who may be considering passing deficiencies they identify within firms to the Enforcement Committee for possible action.

Work has begun to finalise market-specific guidance around AML/ATF, most recently for the trust, investment business and funds sectors. This will be part of a general review we plan to conduct during 2012 of current AML/ATF legislation and guidance notes with a view to updating these framework components as necessary by year-end.

Following the success of the series conducted in 2011, the Authority will also continue to conduct industry outreach seminars during 2012. Areas of focus will include themes arising from the desk-based reviews and the implications of anticipated amendments to the FATF global AML standards. With respect to the sanctions regime, the Authority will document the

oversight framework and communicate our findings to industry. It is also important to note that in addition to our supervisory efforts, this work includes continuing long-standing and effective collaboration with our colleagues in the Bermuda Government - specifically, at the Ministry of Finance, the Ministry of Justice, the Financial Intelligence Agency and the National Anti-Money Laundering Committee.

EnforcementThe Authority continues to make progress with plans to enhance our enforcement framework, to ensure Bermuda remains appropriately aligned with international standards. We completed market consultation on proposals to extend the scope of our enforcement powers to all sectors within Bermuda’s financial services industry in 2011. Following a review of the comments received from this consultation, in 2012 we intend to publish a Statement of Principles and to amend the primary legislation for the insurance, banking, investment, and trust sectors to ensure a uniform set of enforcement powers are available to the Authority across all sectors.

Anti - Money Laundering/Anti - Terrorism Financing Supervision and Enforcement

12 Business Plan 2012

Econ

omic

Bal

ance

She

et

Iss

ue E

cono

mic

Bal

ance

She

et C

onsu

ltatio

n Pa

per -

Gen

eral

Bus

ines

s E

cono

mic

Val

ue D

iscl

osur

es (P

hase

d to

Q4

2012

) P

hase

d Im

plem

enta

tion:

Cla

ss 4

, Cla

ss 3

B, C

lass

3A,

Lon

g-Te

rm

Elig

ible

Cap

ital/

Ow

n Fu

nds

Im

plem

enta

tion:

Cla

ss 3

A P

hase

d Im

plem

enta

tion

Clas

s C

and

Clas

s D

Berm

uda

Solv

ency

Cap

ital R

equi

rem

ent M

odel

(BSC

R)

Tria

l Run

Cla

ss C

and

Cla

ss D

Pha

sed

Impl

emen

tatio

n: C

lass

3A

BSC

R Im

pact

Ass

essm

ents

Inte

rnal

Mod

els

(ICM

)

Sta

ndar

ds &

App

licat

ions

Fra

mew

ork

- Gui

danc

e N

otes

: -

Lon

g-Te

rm S

ecto

r

CISS

A (O

RSA

)

Tria

l Run

: Cla

ss C

and

Cla

ss D

Dis

clos

ures

and

Tra

nspa

renc

y

Pha

sed

Impl

emen

tatio

n: C

lass

3A,

Cla

ss E

; tria

l run

Cla

ss C

and

Cla

ss D

Gro

ups

Pha

sed

Tria

l Run

Gro

ups

BSCR

Cla

ss 3

A an

d Cl

ass

E T

rans

ition

al Im

plem

enta

tion:

Gro

up s

uper

visio

n Cl

ass

4, C

lass

3B

Long

-Ter

m B

usin

ess

Fram

ewor

k

Im

plem

enta

tion:

Lon

g-Te

rm re

clas

sific

atio

n I

ssue

Eco

nom

ic B

alan

ce S

heet

Dis

cuss

ion

Pape

r

INS

UR

AN

CE

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2012

20

13

Bermuda Monetary Authority 13

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2012

20

13

Capt

ives

Ris

k R

etur

n

Iss

ue C

onsu

ltatio

n Pa

per

Ris

k Re

turn

Tria

l Run

BA

NK

ING

& IN

VES

TMEN

TS

Dep

osit

Insu

ranc

e Sc

hem

e

Dep

osit

Insu

ranc

e Co

rpor

atio

n as

sist

ance

com

plet

ed

Bank

ing

Inte

rven

tion

Pow

ers

Iss

ue d

raft

Bank

ing

(Spe

cial

Res

olut

ions

Reg

ime)

Act

Bank

Liq

uidi

ty a

nd C

apita

l

Ass

ess

Impl

emen

tatio

n of

revi

sed

bank

liqu

idity

sta

ndar

ds

Corp

orat

e G

over

nanc

e Co

de fo

r Ber

mud

a Li

cens

ed B

anks

Im

plem

enta

tion:

Issu

e Co

de

E-fil

ing

- Enh

ance

d Re

port

ing

Proc

ess

Ext

end

syst

em to

insu

ranc

e St

atut

ory

Fina

ncia

l Ret

urns

Ext

end

syst

em to

all

licen

sees

(ban

king

, tru

st a

nd in

vest

men

t)

BA

NK

ING

& IN

VES

TMEN

TS

OTH

ER

Corp

orat

e Se

rvic

e Pr

ovid

er R

egim

e

Com

plet

e co

nsul

tatio

n on

dra

ft le

gisl

atio

n

Curr

ency

Act

iviti

es

Dem

onet

isat

ion

of L

egac

y ba

nkno

te s

erie

s

Enfo

rcem

ent

Ena

ctm

ent o

f Enh

ance

d En

forc

emen

t Mea

sure

s Le

gisl

atio

n

Business Plan 201214

International Developments

Section Four

International regulatory initiatives continue to reshape the global regulatory landscape across sectors. These initiatives impact regulators on the jurisdictional level who must balance maintaining regimes that are in line with evolving international standards and also appropriate for local markets.

The Authority will continue to contribute to this on going change process in a substantive way. Along with being keenly aware of the continuing debates on regulatory reform, we remain involved in the work of international standard setters across all financial sectors, in particular with the International Association of Insurance Supervisors (IAIS), through our committee membership. Our appointment in November 2011 to the Chairman position of the IAIS’s Macroprudential Policy and Surveillance Working Group is the most recent example of our contribution to the insurance standard setter’s work. Within the funds

and banking sectors we remain active members of the International Organisation of Securities Commissioners and the Offshore Group of Banking Supervisors, attending regular meetings to discuss and act upon issues relevant to these sectors. This activity will continue in 2012.

As regards supervisory cooperation, we continue to view establishing relationships with our peer regulators as key to fostering high standards in regulation. As such we will consider how best to engage in and maintain such relationships, e.g. possibly building on the number of MOUs that we have signed, which was a total of 18 as of 2011. This includes our most recently signed Multilateral MOU (MMOU) with the Caribbean Regional Regulatory Authorities in May 2011. We will also continue to participate as a member of the IAIS MMOU Signatories Working Group, the group that evaluates countries’ applications to be part of the IAIS MMOU.

Also during 2012 we will continue our international advocacy work, which is focused on effectively communicating the near- and long-term vision of regulation and supervision in Bermuda to relevant external stakeholders. This will include maintaining dialogue with EU and US supervisors and key decision-making bodies. These groups include EIOPA (the European Insurance and Occupational Pensions Authority), the body that conducted our third-country Solvency II equivalence assessment in 2011.

Our varied involvement in the international arena is a key part of our regulatory strategy and supports our goal to be recognised as a leading risk-based financial services regulator. It also allows us to create awareness of the efforts Bermuda is undertaking to develop a first class regulatory framework that can be deemed equivalent by major jurisdictions.

Highlights - Initiatives for International Developments 2012

International Cooperation

Advocacy

Supervisory Cooperation

• Assume Chairmanship of IAIS Macroprudential Policy and Surveillance Working Group, with a focus on global standards for stress testing

• Represent Bermuda at the Financial Stability Board Regional Consultative Group for the Americas

• Continue to provide the Authority’s expertise for training supervisors overseas, to assist with raising the standard of supervision globally

• Continue outreach and awareness-raising programme to key stakeholders overseas to support Bermuda’s standing as a leading financial jurisdiction

• Maintain engagement with relevant European authorities, to support Solvency II equivalence programme, and regulatory bodies in the United States in relation to initiatives relevant to Bermuda

• Continue hosting and participation in supervisory colleges for banking and insurance sectors; in particular, launch colleges as Group-wide Supervisor for identified insurance groups

Bermuda Monetary Authority 15Section Four

Focus on Operational andCost Efficiencies

Resources

During 2012, the Authority’s priorities in regard to augmenting resources in a cost-effective manner will be to:

• continue to resource the Authority with quality staff;

• embed a robust technical competencies regime to ensure learning and development programmes continue to provide quality supervisors; and

• continue to control expenses and achieve further efficiencies in both our internal and external processes.

In 2010 our resourcing strategy included an aggressive recruitment drive to attract key, senior-level individuals to join our policy, risk analytics and supervisory areas, with most of the successful candidates being in place by early 2011. This targeted growth in resources continues and is supporting the development and implementation of our enhanced regulatory policy and supervisory programmes. We accomplished this against the backdrop of a competitive recruitment environment within the global regulatory arena that has regulators seeking to acquire employees with experience relevant to

new regulatory rules, such as Solvency II, from a limited talent pool.

Moving forward, the next phase of our strategy involves maximising efficiencies in our processes as well as leveraging skill-sets and deepening the technical abilities of our team. This work will involve employing hybrid resourcing models, such as co-sourcing arrangements. Co-sourcing is an approach being adopted by most international regulators to meet ever increasing demands for specialised resources. Such arrangements, which typically use external resources for defined periods of time, will allow the Authority to meet immediate resource needs in a cost-efficient manner. We will deploy this arrangement, for example, for our internal model reviews and during peak supervisory periods such as with the review of Statutory Financial Returns. In addition, the Authority remains committed to developing our human capital. During 2012 we will expand and strengthen our leadership development framework by introducing executive coaching. We will also implement the next phase of our technical competencies framework that was introduced in 2011 for our

supervisory units. The framework supports supervisory excellence by ensuring that our teams of supervisors have the appropriate skills, knowledge and expertise to perform their roles effectively. Our work in 2012 will include embedding the framework across our supervisory functions, including learning and development, recruitment and performance management. In this way the Authority is building its technical resources to ensure we have the right people with the right skill-sets to perform our duties as Bermuda’s financial services regulator to the highest standard.

Information Technology

The Authority recognises the important role technology plays in supporting effective supervision, particularly in today’s environment where reporting and regulatory oversight requirements are becoming more complex. With this in mind, implementation of our IT strategy continues. This strategy is designed to ensure that a robust IT infrastructure supports our work to deliver quality supervision. We are ensuring that this infrastructure aligns with the sophisticated nature of the markets we regulate, and provides us

Business Plan 201216

with the ability to adjust to supervisory needs, now and into the future.

During 2011, we met major milestones within our IT plan, particularly with respect to the Authority’s e-filing capabilities. Our focus in 2012 will be to continue developing and deploying our supporting system for e-filing – ERICA (Electronic Regulatory Information Compliance Application). ERICA is a secure web portal that receives, tracks, and processes regulatory filings, material changes and other types of submissions regulated firms make to the Authority. Using the programming language XBRL (extensible Business Reporting Language), ERICA will streamline the reporting, collection and analysis of data for regulatory purposes. This will result in significant efficiencies internally, within our supervisory processes, while making it easier for external firms to be in compliance with the enhanced reporting requirements.

In 2011, we applied our e-filing capabilities to the investment funds sector. In 2012, we will expand these capabilities across the banking and insurance sectors for all compliance

submissions including Prudential Information Returns and Statutory Financial Returns respectively. In addition, we will extend the electronic submissions related to the Bermuda Solvency Capital Requirement, which the Authority introduced in 2010 for Class 4 firms and 2011 for Class 3B insurers, to firms in the remaining applicable insurance classes, including insurance groups. This will bring greater efficiencies in solvency assessments of firms.

The Authority is committed to being at the forefront of technological advancement to enhance regulation and supervision. The effective management of information is a common challenge regulators face worldwide due to the rapid changes occurring within financial regulation in response to the financial crisis. Therefore, during 2012 we will enhance our information management framework using the capabilities afforded through ERICA. These efforts support our commitment to effective supervisory cooperation which is a critical factor in strengthening regulation globally.

Currency Activities

Having successfully introduced a redesigned, award-winning banknote series with enhanced security features two years ago, the Authority will begin the process of demonetising Bermuda’s legacy banknote series in 2012.

Demonetisation is essentially the process whereby the Authority begins ‘calling-in’ currency that will eventually become outdated. As with our previous demonetisation initiatives, once the process for the current legacy note series officially begins, the Authority will no longer release such banknotes for public consumption. The legacy currency will cease to be legal tender after the process is complete. The Authority will announce the details and timeline for this demonetisation process early in 2012. For the general public, this will mean that from 2012 onwards a declining number of legacy banknotes will be in circulation.

Meeting Service Standards The Authority remains committed to transparency in the work we do and to

Bermuda Monetary Authority 17

Transaction

Corporate Registrations:

• Company incorporations • Listed (stock exchange) company

incorporations • Permit companies • Partnerships • Issues and transfer of shares

Investment Fund Applications:

Insurance Licensing and Authorisations1:

• 2010 Class 4 company Statutory Financial Returns

• 2010 Class 3B and Domestic2 Insurance Company Statutory Financial Returns

• 2010 Class 3, 3A and Long-Term company Statutory Financial Returns

• 2010 Class 1 and 2 company Statutory Financial Returns

•Registrations

•Certificate of Compliance

Service Standard

90% of applications within:

24 hours1 hour

2 days2 days2 days

Process and approve 90% of applications for new funds or material changes within 6 business days

100% to be completed by June 1st 2011

100% to be completed by July 1st 2011

100% to be completed by December 31st 2011

100% of companies in risk-based sample to be completed by December 31st 2011

90% to be completed in 3 business days

90% to be completed in 2 business days

2011 Performance

Met

Met: 96%

Met

Met

Met

Met

Met: 96%

Met: 96%

TABLE 1: BMA Performance against 2011 Service Standards

1These service standards were set for year-end 2010 filings of Statutory Financial Returns (SFRs). Companies submit SFRs on a staggered basis throughout the year following the financial year-end. The initial submission deadline for 2010 SFRs was April 2011. In keeping with the BMA’s risk-based approach, SFRs for Class 4 companies were reviewed first. An SFR review involves receiving the Return and conducting a financial analysis of its contents, as well as an assessment of the accuracy, completeness and fairness of each submission. Based on this review firms are subsequently contacted to confirm either that the Authority is satisfied with the SFR or that more information or action in relation to a submission is required, which could include meetings with company management.

2Separate service standards are set for Class 3B and domestic insurance companies in keeping with their risk profile.

Business Plan 201218

Transaction

Corporate Registrations:

• Company incorporations • Listed (stock exchange) company

incorporations • Permit companies • Partnerships • Issues and transfer of shares

Investment Fund Applications:

Insurance Licensing and Authorisations3:

• 2011 Class 4 company Statutory Financial Returns

• 2011 Class 3B and domestic

insurance company Statutory Financial Returns

• 2011 Class 3, 3A and Long-Term company Statutory Financial Returns

• 2011 Class 1 and 2 company Statutory Financial Returns

• Registrations

• Certificates of Compliance

Service Standard

90% of applications within:

24 hours1 hour

2 days2 days2 days

Process and approve 90% of ap-plications for new funds or material changes within 6 business days

100% to be completed by June 1st 2012

100% to be completed by July 1st 2012

100% to be completed by December 31st 2012

100% of companies in risk-based sample to be completed by Decem-ber 31st 2012

90% to be completed in 3 business days

90% to be completed in 2 business days.

Table 2: BMA Service Standards Targets 2012being accountable for the level of service we provide to the Bermuda market. For the third consecutive year, we set service standards for regulatory transactions that various departments conduct with the wide range of entities and financial institutions under our remit. Table 1 shows that the Authority has met all of the targets set for our service standards over the past year. For 2012, we have set such targets as outlined in Table 2.

3 These service standards are set for year-end 2011 filings of Statutory Financial Returns (SFRs). Companies submit on a staggered basis throughout the year following the financial year-end. The initial submission deadline for 2011 SFRs is April 2012.

Bermuda Monetary Authority 19

BMA Management Team – January 2012

Jeremy Cox Chief Executive Officer Bradley Erickson Chief Operating Officer

Banking Trust & Investment (BTI) Marcia Woolridge-Allwood Director Tamara Anfossi Assistant Director, BTI Financial Institutions & Investment Funds Courtney Christie-Veitch Assistant Director, BTI Financial Groups

Corporate Finance Terry Pitcher Head of Finance

Corporate Governance and Communications Pat Phillip-Bassett Deputy Director, Corporate Governance & Communications

Human Resources Mesheiah Crockwell Head Of Human Resources Verna Hollis Smith Assistant Director, Organisation Management

Insurance Licensing & Authorisation Shelby Weldon Director Leslie Robinson Assistant Director, Licensing

Insurance Supervision, Complex Institutions Shanna Lespere Director Niall Farrell Deputy Director, Run-off & Monitoring Diana Nedvidek Deputy Director, Insurance Supervision, Complex Institution s Laila Burke Assistant Director, Insurance Supervision, Complex Institutions Gerald Gakundi Assistant Director, Insurance Supervision, Complex Institutions Susan Molineux Assistant Director, Insurance Supervision, Complex Institutions Sonja Nauta Assistant Director, Insurance Supervision, Complex Institutions Suzanne Williams Assistant Director, Insurance Supervision, Complex Institutions

Legal Services & Enforcement Shauna MacKenzie Director Thomas Galloway Senior Legal Counsel Dina Wilson Assistant Director, Legal Services & Enforcement

Management Services John Dill Director Howard Ho Assistant Director, IT Austin Culmer-Smith Assistant Director, Corporate Operations

Policy, Research & International Affairs Mary Frances Monroe Director Marcelo Ramella Deputy Director, Research & International Affairs Arhat Virdi Assistant Director, Policy

Risk Analytics Craig Swan Director David Theaker Deputy Director, Actuarial Services Andreas Jobst Assistant Director, Chief Economist David Kaniaru Assistant Director, Analytics, Insurance Brant Kizer Assistant Director, Actuarial Services, Property & Casualty Richard May Assistant Director, Actuarial Services, Long-Term Gina Smith Assistant Director, Actuarial Services, Property and Casualty Gary Thomas Assistant Director, Actuarial Services, Long-Term Navid Zarinejad Assistant Director, Actuarial Services, Property and Casualty

Senior Advisors Graeme Dargie Senior Advisor - BTI Roger Scotton Senior Advisor - International Affairs William Kattan Senior Advisor - Legal Services & Enforcement

Notes

Bermuda Monetary Authority 21

BMA House • 43 Victoria Street • Hamilton HM 12 BermudaP.O. Box 2447 • Hamilton HM JX Bermudatel: (441) 295 5278 • fax: (441) 292 7471email: [email protected] • website: www.bma.bm