Embed Size (px)

Citation preview

Ernst & Young Ltd.

AUDITED FINANCIAL STA TEMEN TS DaVinc i Reinsurance Ltd. December 31, 2012 and 2011

Audited Financial Statements

DaVinci Reinsurance Ltd.

December 31, 2012 and 2011

Ernst & Young Ltd. #3 Bermudiana Road Hamilton HM 08, Bermuda P.O. Box 463, Hamilton, HM BX, Bermuda Direct: +1 441 295 7000 Direct Fax: +1 441 295 5193 www.ey.com/bermuda

REPORT OF INDEPENDENT AUDITORS TO THE BOARD OF DIRECTORS AND SHAREHOLDERS OF DAVINCI REINSURANCE LTD. We have audited the accompanying financial statements of DaVinci Reinsurance Ltd., which comprise the balance sheets as of December 31, 2012 and 2011, and the related statements of operations, comprehensive income, changes in shareholders' equity and cash flows for the years then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in conformity with U.S. generally accepted accounting principles; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free of material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of DaVinci Reinsurance Ltd. at December 31, 2012 and 2011, and the results of their operations and their cash flows for the years then ended in conformity with U.S. generally accepted accounting principles.

Hamilton, Bermuda April 15, 2013

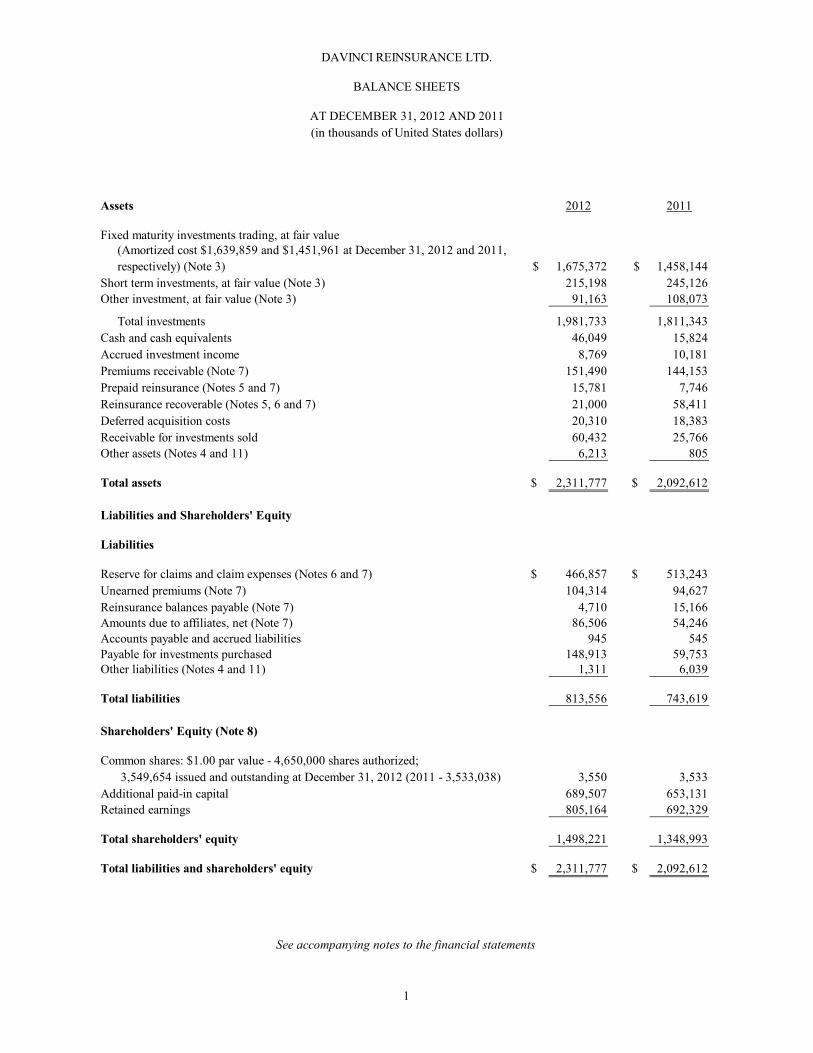

Assets 2012 2011

Fixed maturity investments trading, at fair value

$ 1,675,372 $ 1,458,144 Short term investments, at fair value (Note 3) 215,198 245,126 Other investment, at fair value (Note 3) 91,163 108,073

Total investments 1,981,733 1,811,343 Cash and cash equivalents 46,049 15,824 Accrued investment income 8,769 10,181 Premiums receivable (Note 7) 151,490 144,153 Prepaid reinsurance (Notes 5 and 7) 15,781 7,746 Reinsurance recoverable (Notes 5, 6 and 7) 21,000 58,411 Deferred acquisition costs 20,310 18,383 Receivable for investments sold 60,432 25,766 Other assets (Notes 4 and 11) 6,213 805

Total assets $ 2,311,777 $ 2,092,612

Liabilities and Shareholders' Equity

Liabilities

Reserve for claims and claim expenses (Notes 6 and 7) $ 466,857 $ 513,243 Unearned premiums (Note 7) 104,314 94,627 Reinsurance balances payable (Note 7) 4,710 15,166 Amounts due to affiliates, net (Note 7) 86,506 54,246 Accounts payable and accrued liabilities 945 545 Payable for investments purchased 148,913 59,753 Other liabilities (Notes 4 and 11) 1,311 6,039

Total liabilities 813,556 743,619

Shareholders' Equity (Note 8)

Common shares: $1.00 par value - 4,650,000 shares authorized; 3,549,654 issued and outstanding at December 31, 2012 (2011 - 3,533,038) 3,550 3,533

Additional paid-in capital 689,507 653,131 Retained earnings 805,164 692,329

Total shareholders' equity 1,498,221 1,348,993

Total liabilities and shareholders' equity $ 2,311,777 $ 2,092,612

See accompanying notes to the financial statements

DAVINCI REINSURANCE LTD.

BALANCE SHEETS

AT DECEMBER 31, 2012 AND 2011(in thousands of United States dollars)

(Amortized cost $1,639,859 and $1,451,961 at December 31, 2012 and 2011, respectively) (Note 3)

1

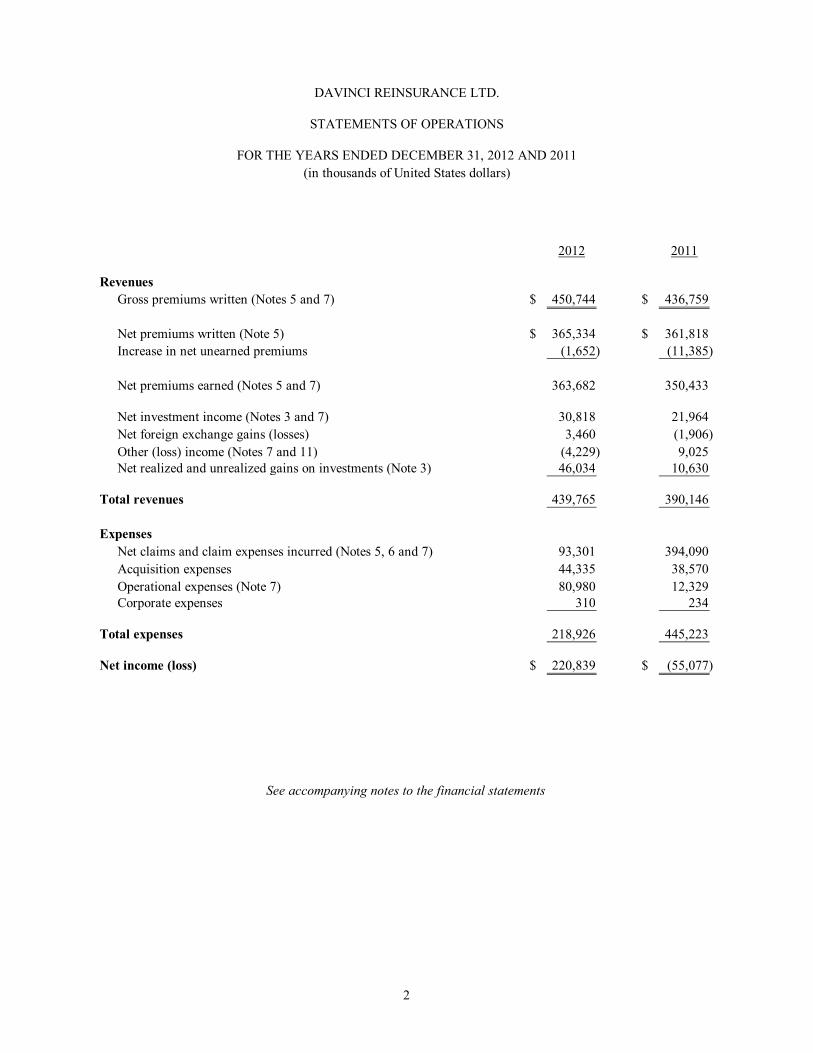

2012 2011

RevenuesGross premiums written (Notes 5 and 7) $ 450,744 $ 436,759

Net premiums written (Note 5) $ 365,334 $ 361,818 Increase in net unearned premiums (1,652) (11,385)

Net premiums earned (Notes 5 and 7) 363,682 350,433

Net investment income (Notes 3 and 7) 30,818 21,964 Net foreign exchange gains (losses) 3,460 (1,906) Other (loss) income (Notes 7 and 11) (4,229) 9,025 Net realized and unrealized gains on investments (Note 3) 46,034 10,630

Total revenues 439,765 390,146

ExpensesNet claims and claim expenses incurred (Notes 5, 6 and 7) 93,301 394,090 Acquisition expenses 44,335 38,570 Operational expenses (Note 7) 80,980 12,329 Corporate expenses 310 234

Total expenses 218,926 445,223

Net income (loss) $ 220,839 $ (55,077)

(in thousands of United States dollars)

See accompanying notes to the financial statements

DAVINCI REINSURANCE LTD.

STATEMENTS OF OPERATIONS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

2

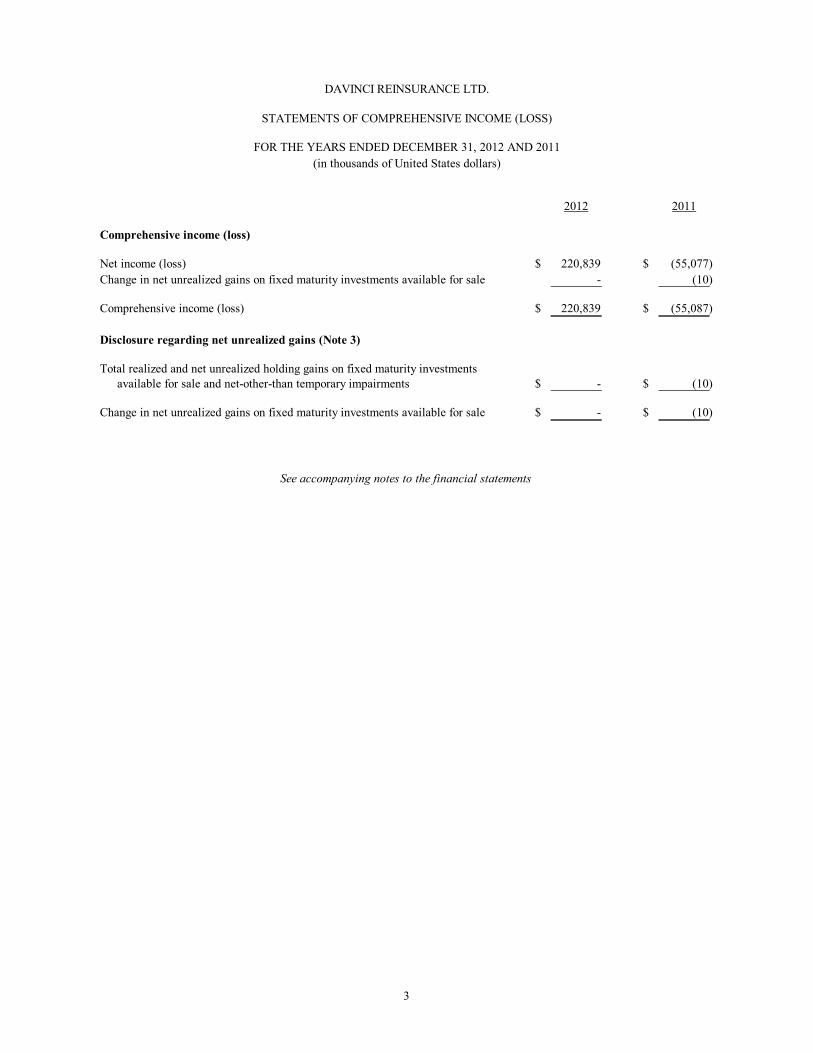

2012 2011

Comprehensive income (loss)

Net income (loss) $ 220,839 $ (55,077) Change in net unrealized gains on fixed maturity investments available for sale - (10)

Comprehensive income (loss) $ 220,839 $ (55,087)

Disclosure regarding net unrealized gains (Note 3)

Total realized and net unrealized holding gains on fixed maturity investmentsavailable for sale and net-other-than temporary impairments $ - $ (10)

Change in net unrealized gains on fixed maturity investments available for sale $ - $ (10)

See accompanying notes to the financial statements

DAVINCI REINSURANCE LTD.

STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011(in thousands of United States dollars)

3

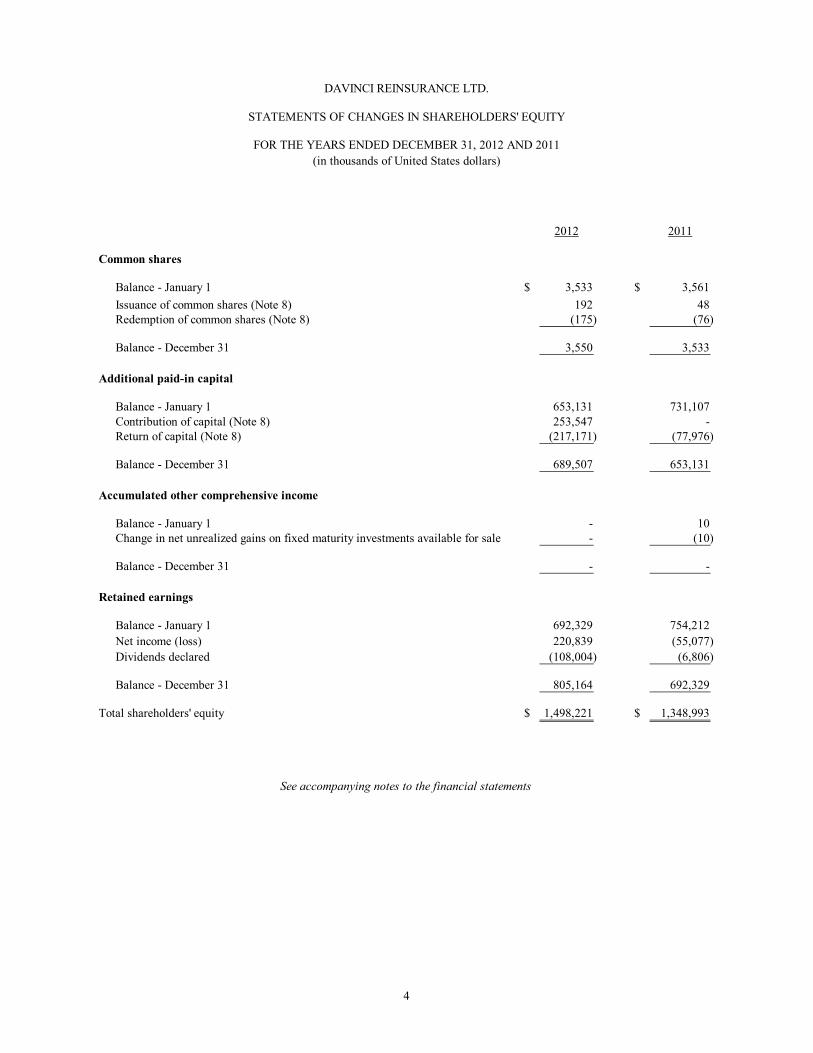

2012 2011

Common shares

Balance - January 1 $ 3,533 $ 3,561 Issuance of common shares (Note 8) 192 48 Redemption of common shares (Note 8) (175) (76)

Balance - December 31 3,550 3,533

Additional paid-in capital

Balance - January 1 653,131 731,107 Contribution of capital (Note 8) 253,547 - Return of capital (Note 8) (217,171) (77,976)

Balance - December 31 689,507 653,131

Accumulated other comprehensive income

Balance - January 1 - 10 Change in net unrealized gains on fixed maturity investments available for sale - (10)

Balance - December 31 - -

Retained earnings

Balance - January 1 692,329 754,212 Net income (loss) 220,839 (55,077) Dividends declared (108,004) (6,806)

Balance - December 31 805,164 692,329

Total shareholders' equity $ 1,498,221 $ 1,348,993

See accompanying notes to the financial statements

DAVINCI REINSURANCE LTD.

STATEMENTS OF CHANGES IN SHAREHOLDERS' EQUITY

(in thousands of United States dollars)FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

4

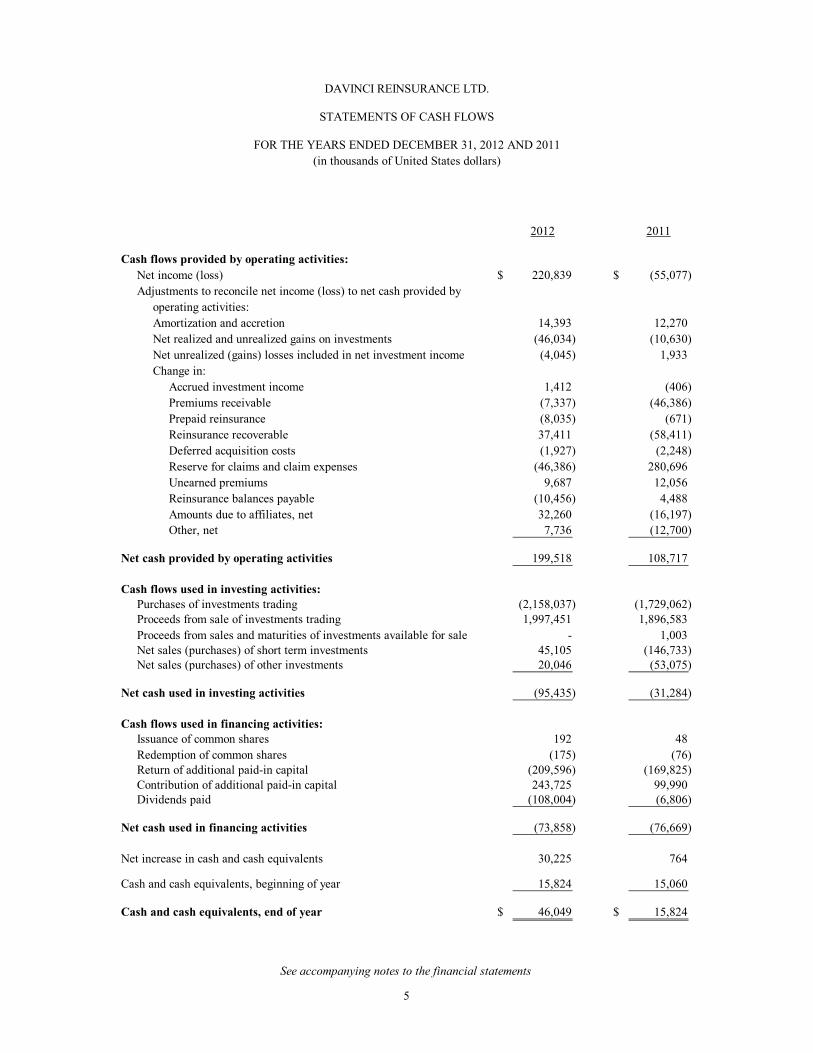

2012 2011

Cash flows provided by operating activities:Net income (loss) $ 220,839 $ (55,077) Adjustments to reconcile net income (loss) to net cash provided by

operating activities:Amortization and accretion 14,393 12,270 Net realized and unrealized gains on investments (46,034) (10,630) Net unrealized (gains) losses included in net investment income (4,045) 1,933 Change in:

Accrued investment income 1,412 (406) Premiums receivable (7,337) (46,386) Prepaid reinsurance (8,035) (671) Reinsurance recoverable 37,411 (58,411) Deferred acquisition costs (1,927) (2,248) Reserve for claims and claim expenses (46,386) 280,696 Unearned premiums 9,687 12,056 Reinsurance balances payable (10,456) 4,488 Amounts due to affiliates, net 32,260 (16,197) Other, net 7,736 (12,700)

Net cash provided by operating activities 199,518 108,717

Cash flows used in investing activities: Purchases of investments trading (2,158,037) (1,729,062) Proceeds from sale of investments trading 1,997,451 1,896,583

Proceeds from sales and maturities of investments available for sale - 1,003 Net sales (purchases) of short term investments 45,105 (146,733) Net sales (purchases) of other investments 20,046 (53,075)

Net cash used in investing activities (95,435) (31,284)

Cash flows used in financing activities:Issuance of common shares 192 48 Redemption of common shares (175) (76) Return of additional paid-in capital (209,596) (169,825) Contribution of additional paid-in capital 243,725 99,990 Dividends paid (108,004) (6,806)

Net cash used in financing activities (73,858) (76,669)

Net increase in cash and cash equivalents 30,225 764

Cash and cash equivalents, beginning of year 15,824 15,060

Cash and cash equivalents, end of year $ 46,049 $ 15,824

See accompanying notes to the financial statements

DAVINCI REINSURANCE LTD.

STATEMENTS OF CASH FLOWS

(in thousands of United States dollars)FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

5

6

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

NOTE 1. ORGANIZATION DaVinci Reinsurance Ltd. (the “Company”) was incorporated under the laws of Bermuda in October 2001 and provides property catastrophe and specialty reinsurance coverages to insurers and reinsurers on a worldwide basis. The Company is a majority-owned subsidiary of DaVinciRe Holdings Ltd. (“DaVinciRe”), a Bermuda company. DaVinciRe is a minority-owned subsidiary of Renaissance Other Investments Holdings Ltd. (“ROIHL”), a Bermuda company, which is a wholly-owned subsidiary of RenaissanceRe Holdings Ltd. (“RenaissanceRe”), also a Bermuda company. NOTE 2. SIGNIFICANT ACCOUNTING POLICIES Basis of Presentation The financial statements have been prepared on the basis of accounting principles generally accepted in the United States (“GAAP”). Use of Estimates in Financial Statements The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported and disclosed amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ materially from those estimates. The major estimates reflected in the Company’s financial statements include, but are not limited to, the reserve for claims and claim expenses, reinsurance recoverables, estimates of written and earned premiums and fair value, including the fair value of investments, financial instruments and derivatives and impairment charges. Premiums and Related Expenses Premiums are recognized as income, net of any applicable retrocessional coverage purchased, over the terms of the related contracts and policies. Premiums written are based on contract and policy terms and include estimates based on information received from both insureds and ceding companies. Subsequent differences arising on such estimates are recorded in the period in which they are determined. Unearned premiums represent the portion of premiums written that relate to the unexpired terms of contracts and policies in force. Amounts are computed by pro-rata methods based on statistical data or reports received from ceding companies. Reinstatement premiums are estimated after the occurrence of a significant loss and are recorded in accordance with the contract terms based upon paid losses and case reserves. Reinstatement premiums are earned when written. Acquisition costs, consisting principally of commissions, brokerage and premium tax expenses incurred at the time a contract or policy is issued, are deferred and amortized over the period in which the related premiums are earned. Deferred policy acquisition costs are limited to their estimated realizable value based on the related unearned premiums. Anticipated claims and claim expenses, based on historical and current experience, and anticipated investment income related to those premiums are considered in determining the recoverability of deferred acquisition costs.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

7

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES, cont’d. Claims and Claim Expenses The reserve for claims and claim expenses includes estimates for unpaid claims and claim expenses on reported losses as well as an estimate of losses incurred but not reported ("IBNR"). The reserve is based on individual claims, case reserves and other reserve estimates reported by insureds and ceding companies as well as management estimates of ultimate losses. Inherent in the estimates of ultimate losses are expected trends in claim severity and frequency and other factors which could vary significantly as claims are settled. The Company does not have the benefit of a significant amount of its own historical experience with its specialty reinsurance line. Accordingly, the setting and reserving for incurred losses in this line of business could be subject to greater variability. Ultimate losses may vary materially from the amounts provided in the financial statements. These estimates are reviewed regularly and, as experience develops and new information becomes known, the reserves are adjusted as necessary. Such adjustments, if any, are reflected in the statements of operations in the period in which they become known and are accounted for as changes in estimates. Reinsurance Amounts recoverable from reinsurers are estimated in a manner consistent with the claim liability associated with the reinsured policies. If the Company determines that adjustments to earlier estimates are appropriate, such adjustments are recorded in the period in which they are determined. Reinsurance recoverables on dual trigger reinsurance contracts require the Company to estimate its ultimate losses applicable to these contracts as well as estimate the ultimate amount of insured industry losses that will be reported by the applicable statistical reporting agency, as per the contract terms. Amounts recoverable from reinsurers are recorded net of a valuation for estimated uncollectible recoveries. Assumed and ceded reinsurance contracts that lack a significant transfer of risk are treated as deposits. Investments, Cash and Cash Equivalents Fixed Maturity Investments Investments in fixed maturities are classified as trading and are reported at fair value. Investment transactions are recorded on the trade date with balances pending settlement reflected in the balance sheet as a receivable for investments sold or a payable for investments purchased. Net investment income includes interest and dividend income together with amortization of market premiums and discounts and is net of investment management and custody fees. The amortization of premium and accretion of discount for fixed maturity securities is computed using the effective yield method. For mortgage-backed securities and other holdings for which there is prepayment risk, prepayment assumptions are evaluated quarterly and revised as necessary. Any adjustments required due to the change in effective yields and maturities are recognized on a prospective basis through yield adjustments. Fair values of fixed maturity investments are based on quoted market prices, or when such prices are not available, by reference to broker or underwriter bid indications and/or internal pricing valuation techniques.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

8

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES, cont’d. The net unrealized appreciation or depreciation on fixed maturity investments trading is included in net realized and unrealized gains on fixed maturity investments in the statements of operations. Realized gains or losses on the sale of fixed maturity investments are determined on the basis of the first in first out cost method. Short Term Investments and Cash and Cash Equivalents Short term investments, which are managed as part of the Company’s investment portfolio and have a maturity of one year or less when purchased, are carried at amortized cost, which approximates fair value. In certain cases, fair value is determined in a manner similar to the Company’s fixed maturity investments noted above, and accordingly, the net unrealized appreciation or depreciation on these short term investments is included in net realized and unrealized gains on investments in the statements of operations. Cash equivalents include money market instruments with a maturity of ninety days or less when purchased. Other Investment The Company accounts for its other investment at fair value in accordance with Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") Topic Financial Instruments, with interest, dividend income, income distributions and realized and unrealized gains and losses included in net investment income. The fair value of the Company’s investment in a senior secured bank loan fund is recorded on its balance sheet in other investment and is established on the basis of the net valuation criteria established by the manager of the investment. The net valuation criteria established by the manager of the investment is established in accordance with the governing documents of the investment. The typical reporting lag experienced by the Company to receive a final net asset value report is one month for senior secured bank loan funds. In certain cases, management’s judgment may also be required to estimate fair value. Actual final valuations may differ, perhaps materially so, from the Company’s estimates and these differences are recorded in the Company’s statement of operations in the period they are reported to the Company as a change in estimate. Derivatives The Company enters into derivative instruments such as futures, options, swaps, forward contracts and other derivative contracts in order to manage its foreign currency exposure, obtain exposure to a particular financial market, for yield enhancement, or for trading and speculation. The Company accounts for its derivatives in accordance with FASB ASC Topic Derivatives and Hedging, which requires all derivatives to be recorded at fair value on the Company’s balance sheet as either assets or liabilities, depending on their rights or obligations, with changes in fair value reflected in current earnings. The Company does not currently apply hedge accounting. The fair value of the Company’s derivatives are estimated by reference to quoted prices or broker quotes, where available, or in the absence of quoted prices or broker quotes, the use of industry or internal valuation models. Fair Value The Company accounts for certain of its assets and liabilities at fair value in accordance with FASB ASC Topic Fair Value Measurements and Disclosures. The Company recognizes the change in unrealized gains and losses arising from changes in fair value in its statements of operations.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

9

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES, cont’d. Foreign Exchange The Company’s functional currency is the United States ("U.S.") dollar. Revenues and expenses denominated in foreign currencies are translated at the prevailing exchange rate at the transaction date. Monetary assets and liabilities denominated in foreign currencies are translated at exchange rates in effect at the balance sheet date, which may result in the recognition of exchange gains or losses which are included in the determination of net income (loss). Recently Adopted Accounting Pronouncements Accounting for Costs Associated with Acquiring or Renewing Insurance Contracts In October 2010, the FASB issued Accounting Standards Update ("ASU") No. 2010-26, Accounting for Costs Associated with Acquiring or Renewing Insurance Contracts ("ASU 2010-26"), which amends FASB ASC Topic Financial Services - Insurance. ASU 2010-26 modifies the definition of the types of costs that can be capitalized in relation to the acquisition of new and renewal insurance contracts. The amended guidance requires costs to be incremental and directly related to the successful acquisition of new or renewal contracts in order to be capitalized as a deferred acquisition cost. Capitalized costs would include incremental direct costs, such as commissions paid to brokers. Additionally, the portion of employee salaries and benefits directly related to time spent for acquired contracts would be capitalized. Costs that fall outside the revised definition must be expensed when incurred. ASU 2010-26 became effective for fiscal periods beginning on or after December 15, 2011, and as a result, the Company adopted ASU 2010-26 effective January 1, 2012. The adoption of ASU 2010-26 did not have a material impact on the Company's statements of operations and financial condition. Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs In May 2011, the FASB issued ASU No. 2011-04, Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs ("ASU 2011-04"), which amends FASB ASC Topic Fair Value Measurement. ASU 2011-04 was issued to provide largely identical guidance about fair value measurement and disclosure requirements with the International Accounting Standards Board's new International Financial Reporting Standards ("IFRS") 13, Fair Value Measurement. ASU 2011-04 does not extend the use of fair value but, rather, provides guidance about how fair value should be applied where it is already required or permitted under GAAP and requires enhanced disclosures covering all transfers between Levels 1 and 2 of the fair value hierarchy. Additional disclosures covering Level 3 assets are also required. ASU 2011-04 became effective for fiscal years, and interim periods within those years, beginning after December 15, 2011 and as a result, the Company adopted ASU 2011-04 effective January 1, 2012. The adoption of ASU 2011-04 did not have a material impact on the Company's statements of operations and financial condition. The additional disclosures required by ASU 2011-04 have been provided in "Note 4. Fair Value Measurements".

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

10

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES, cont’d. Presentation of Comprehensive Income In June 2011, the FASB issued ASU No. 2011-05, Presentation of Comprehensive Income ("ASU 2011-05"), which amends FASB ASC Topic Comprehensive Income. ASU 2011-05 increases the prominence of items reported in other comprehensive income and eliminates the option to present components of other comprehensive income as part of the statement of changes in shareholders' equity. ASU 2011-05 requires that all non-owner changes in shareholders' equity be presented either in a single continuous statement of comprehensive income or in two separate but consecutive statements. ASU 2011-05 became effective for fiscal years, and interim periods within those years, beginning after December 15, 2011, with retroactive application required. The Company adopted ASU 2010-26 effective January 1, 2012 and it did not have a material impact on the Company's statements of operations and financial condition. Recently Issued Accounting Pronouncements Not Yet Adopted Disclosures About Offsetting Assets and Liabilities In December 2011, the FASB issued ASU No. 2011-11, Disclosures about Offsetting Assets and Liabilities ("ASU 2011-11"). The objective of ASU 2011-11 is to enhance disclosures by requiring improved information about financial instruments and derivative instruments in relation to netting arrangements. ASU 2011-11 is effective for interim and annual periods beginning on or after January 1, 2013, with retrospective presentation of the new disclosure required. In January 2013, the FASB issued a related scope clarification, limiting the applicability of the requirements to derivatives, repurchase agreements and reverse repurchase agreements, and securities borrowing/lending transactions. The Company is currently evaluating the impact of this guidance; however, since this update affects disclosures only, it is not expected to have a material impact on the Company's financial statements. Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income In February 2013, the FASB issued ASU No. 2013-02, Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income ("ASU 2013-02"). The objective of ASU 2013-02 is to improve the reporting of classifications out of accumulated other comprehensive income by requiring an entity to report the effect of significant reclassifications out of accumulated other comprehensive income on the respective line items in net income if the amount being reclassified is required under GAAP to be reclassified in its entirety. For other amounts that are not required under GAAP to be reclassified in their entirety to net income in the same reporting period, an entity is required to cross-reference other disclosures required under GAAP that provide additional details about those amounts. ASU 2013-02 is effective for interim and annual reporting periods beginning after December 15, 2012. The Company is currently evaluating the impact of this guidance; however, since this update affects disclosures only, it is not expected to have a material impact on the Company's financial statements.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

11

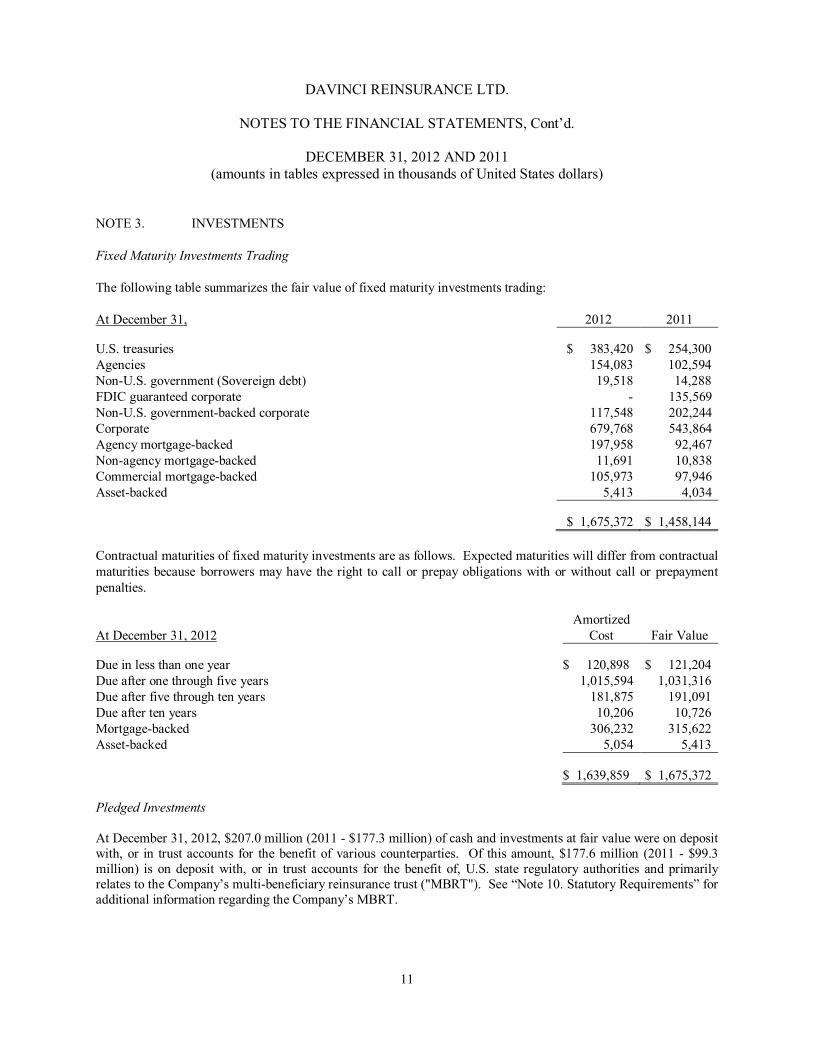

NOTE 3. INVESTMENTS Fixed Maturity Investments Trading The following table summarizes the fair value of fixed maturity investments trading: At December 31, 2012 2011

U.S. treasuries $ 383,420 $ 254,300 Agencies 154,083 102,594 Non-U.S. government (Sovereign debt) 19,518 14,288 FDIC guaranteed corporate - 135,569 Non-U.S. government-backed corporate 117,548 202,244 Corporate 679,768 543,864 Agency mortgage-backed 197,958 92,467 Non-agency mortgage-backed 11,691 10,838 Commercial mortgage-backed 105,973 97,946 Asset-backed 5,413 4,034

$ 1,675,372 $ 1,458,144 Contractual maturities of fixed maturity investments are as follows. Expected maturities will differ from contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties.

At December 31, 2012 Amortized

Cost Fair Value

Due in less than one year $ 120,898 $ 121,204 Due after one through five years 1,015,594 1,031,316 Due after five through ten years 181,875 191,091 Due after ten years 10,206 10,726 Mortgage-backed 306,232 315,622 Asset-backed 5,054 5,413

$ 1,639,859 $ 1,675,372

Pledged Investments At December 31, 2012, $207.0 million (2011 - $177.3 million) of cash and investments at fair value were on deposit with, or in trust accounts for the benefit of various counterparties. Of this amount, $177.6 million (2011 - $99.3 million) is on deposit with, or in trust accounts for the benefit of, U.S. state regulatory authorities and primarily relates to the Company’s multi-beneficiary reinsurance trust ("MBRT"). See “Note 10. Statutory Requirements” for additional information regarding the Company’s MBRT.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

12

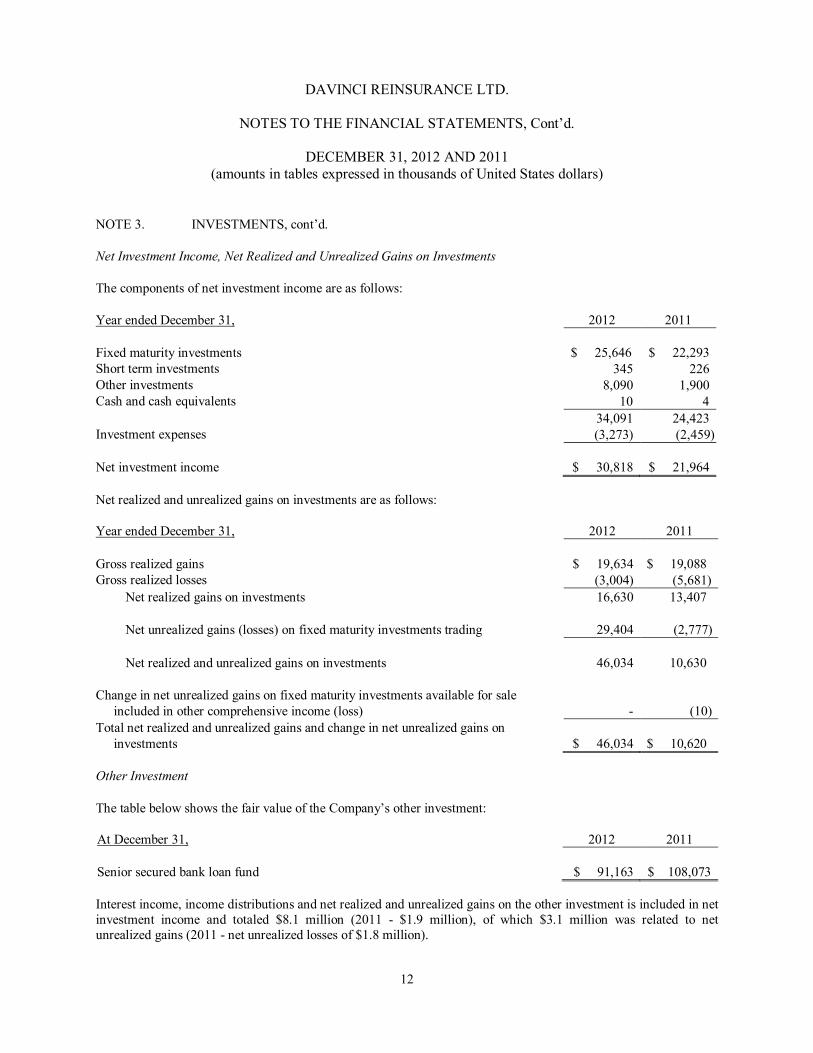

NOTE 3. INVESTMENTS, cont’d. Net Investment Income, Net Realized and Unrealized Gains on Investments The components of net investment income are as follows: Year ended December 31, 2012 2011 Fixed maturity investments

$ 25,646 $ 22,293

Short term investments 345 226 Other investments 8,090 1,900 Cash and cash equivalents 10 4 34,091 24,423 Investment expenses (3,273) (2,459) Net investment income

$ 30,818 $ 21,964

Net realized and unrealized gains on investments are as follows: Year ended December 31, 2012 2011 Gross realized gains $ 19,634 $ 19,088 Gross realized losses (3,004) (5,681)

Net realized gains on investments 16,630 13,407 Net unrealized gains (losses) on fixed maturity investments trading 29,404 (2,777) Net realized and unrealized gains on investments 46,034 10,630

Change in net unrealized gains on fixed maturity investments available for sale

included in other comprehensive income (loss) - (10) Total net realized and unrealized gains and change in net unrealized gains on

investments $ 46,034 $ 10,620 Other Investment The table below shows the fair value of the Company’s other investment: At December 31, 2012 2011 Senior secured bank loan fund

$ 91,163

$ 108,073

Interest income, income distributions and net realized and unrealized gains on the other investment is included in net investment income and totaled $8.1 million (2011 - $1.9 million), of which $3.1 million was related to net unrealized gains (2011 - net unrealized losses of $1.8 million).

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

13

NOTE 4. FAIR VALUE MEASUREMENTS The use of fair value to measure certain assets and liabilities with resulting unrealized gains or losses is pervasive within the Company’s financial statements. Fair value is defined under accounting guidance currently applicable to the Company to be the price that would be received upon the sale of an asset or paid to transfer a liability in an orderly transaction between open market participants at the measurement date. The Company recognizes the change in unrealized gains and losses arising from changes in fair value in its statements of operations. FASB ASC Topic Fair Value Measurements and Disclosures prescribes a fair value hierarchy that prioritizes the inputs to the respective valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1) and the lowest priority to valuation techniques that use at least one significant input that is unobservable (Level 3). The three levels of the fair value hierarchy are described below:

• Fair values determined by Level 1 inputs utilize unadjusted quoted prices obtained from active markets for identical assets or liabilities for which the Company has access. The fair value is determined by multiplying the quoted price by the quantity held by the Company;

• Fair values determined by Level 2 inputs utilize inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. Level 2 inputs include quoted prices for similar assets and liabilities in active markets, and inputs other than quoted prices that are observable for the asset or liability, such as interest rates and yield curves that are observable at commonly quoted intervals, broker quotes and certain pricing indices; and

• Level 3 inputs are based all or in part on significant unobservable inputs for the asset or liability, and include situations where there is little, if any, market activity for the asset or liability. In these cases, significant management assumptions can be used to establish management’s best estimate of the assumptions used by other market participants in determining the fair value of the asset or liability.

In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls has been determined based on the lowest level input that is significant to the fair value measurement of the asset or liability. The Company’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and the Company considers factors specific to the asset or liability.

In order to determine if a market is active or inactive for a security, the Company considers a number of factors, including, but not limited to, the spread between what a seller is asking for a security and what a buyer is bidding for the same security, the volume of trading activity for the security in question, the price of the security compared to its par value (for fixed maturity investments), and other factors that may be indicative of market activity. There have been no material changes in the Company’s valuation techniques, nor have there been any transfers between Level 1 and Level 2, and Level 2 and Level 3, respectively, during the period represented by these financial statements.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

14

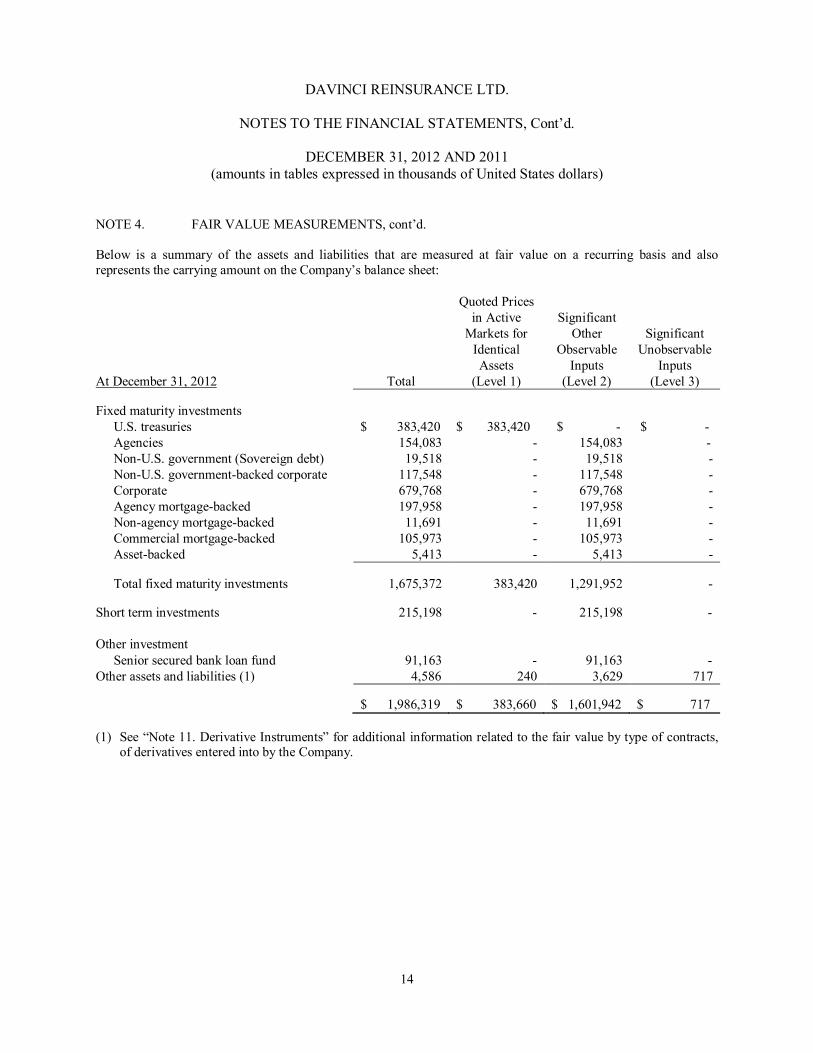

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d. Below is a summary of the assets and liabilities that are measured at fair value on a recurring basis and also represents the carrying amount on the Company’s balance sheet:

At December 31, 2012 Total

Quoted Prices in Active

Markets for Identical Assets

(Level 1)

Significant Other

Observable Inputs

(Level 2)

Significant Unobservable

Inputs (Level 3)

Fixed maturity investments U.S. treasuries $ 383,420 $ 383,420 $ - $ - Agencies 154,083 - 154,083 - Non-U.S. government (Sovereign debt) 19,518 - 19,518 - Non-U.S. government-backed corporate 117,548 - 117,548 - Corporate 679,768 - 679,768 - Agency mortgage-backed 197,958 - 197,958 - Non-agency mortgage-backed 11,691 - 11,691 - Commercial mortgage-backed 105,973 - 105,973 - Asset-backed 5,413 - 5,413 -

Total fixed maturity investments 1,675,372 383,420 1,291,952 -

Short term investments 215,198 - 215,198 -

Other investment Senior secured bank loan fund 91,163 - 91,163 -

Other assets and liabilities (1) 4,586 240 3,629 717

$ 1,986,319 $ 383,660 $ 1,601,942 $ 717

(1) See “Note 11. Derivative Instruments” for additional information related to the fair value by type of contracts, of derivatives entered into by the Company.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

15

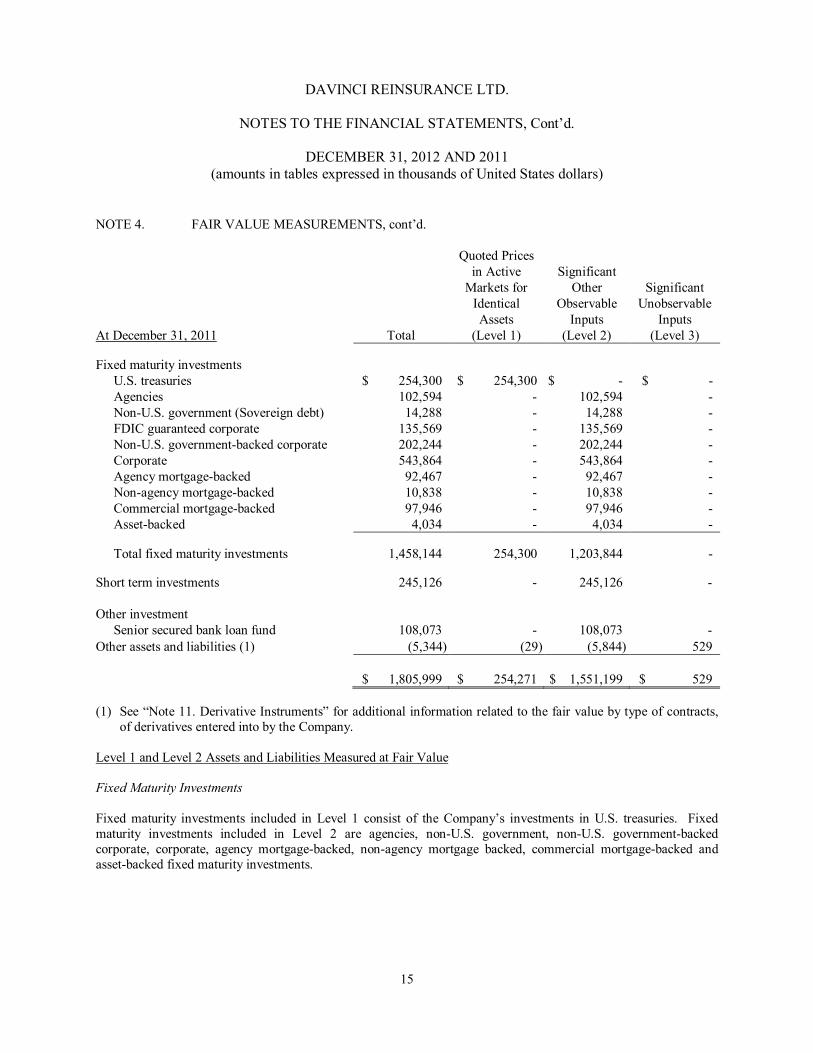

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d.

At December 31, 2011 Total

Quoted Prices in Active

Markets for Identical Assets

(Level 1)

Significant Other

Observable Inputs

(Level 2)

Significant Unobservable

Inputs (Level 3)

Fixed maturity investments

U.S. treasuries $ 254,300 $ 254,300 $ - $ - Agencies 102,594 - 102,594 - Non-U.S. government (Sovereign debt) 14,288 - 14,288 - FDIC guaranteed corporate 135,569 - 135,569 - Non-U.S. government-backed corporate 202,244 - 202,244 - Corporate 543,864 - 543,864 - Agency mortgage-backed 92,467 - 92,467 - Non-agency mortgage-backed 10,838 - 10,838 - Commercial mortgage-backed 97,946 - 97,946 - Asset-backed 4,034 - 4,034 -

Total fixed maturity investments 1,458,144 254,300 1,203,844 -

Short term investments 245,126 - 245,126 -

Other investment Senior secured bank loan fund 108,073 - 108,073 -

Other assets and liabilities (1) (5,344) (29) (5,844) 529

$ 1,805,999

$ 254,271

$ 1,551,199

$ 529

(1) See “Note 11. Derivative Instruments” for additional information related to the fair value by type of contracts, of derivatives entered into by the Company.

Level 1 and Level 2 Assets and Liabilities Measured at Fair Value Fixed Maturity Investments Fixed maturity investments included in Level 1 consist of the Company’s investments in U.S. treasuries. Fixed maturity investments included in Level 2 are agencies, non-U.S. government, non-U.S. government-backed corporate, corporate, agency mortgage-backed, non-agency mortgage backed, commercial mortgage-backed and asset-backed fixed maturity investments.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

16

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d. The Company’s fixed maturity investment portfolios are primarily priced using pricing services, such as index providers and pricing vendors, as well as broker quotations. In general, the pricing vendors provide pricing for a high volume of liquid securities that are actively traded. For securities that do not trade on an exchange, the pricing services generally utilize market data and other observable inputs in matrix pricing models to determine month end prices. Observable inputs include benchmark yields, reported trades, broker-dealer quotes, issuer spreads, bids, offers, reference data and industry and economic events. Index pricing generally relies on market traders as the primary source for pricing, however models are also utilized to provide prices for all index eligible securities. The models use a variety of observable inputs such as benchmark yields, transactional data, dealer runs, broker-dealer quotes and corporate actions. Prices are generally verified using third party data. Securities which are priced by an index provider, are generally included in the index. In general, broker-dealers value securities through their trading desks based on observable inputs. The methodologies include mapping securities based on trade data, bids or offers, observed spreads, and performance on newly issued securities. Broker-dealers also determine valuations by observing secondary trading of similar securities. Prices obtained from broker quotations are considered non-binding, however they are based on observable inputs and by observing secondary trading of similar securities obtained from active, non-distressed markets. The Company considers these Level 2 inputs as they are corroborated with other market observable inputs. The techniques generally used to determine the fair value of the Company’s fixed maturity investments are detailed below by asset class. U.S. treasuries Level 1 - At December 31, 2012, the Company’s U.S. treasuries fixed maturity investments are primarily priced by pricing services and had a weighted average effective yield of 0.4%, a weighted average credit quality of AA (2011 - 0.3% and AA, respectively). When pricing these securities, the pricing services utilize daily data from many real time market sources, including active broker dealers. Certain data sources are regularly reviewed for accuracy to attempt to ensure the most reliable price source is used for each issue and maturity date. Agencies Level 2 - At December 31, 2012, the Company’s agency fixed maturity investments had a weighted average effective yield of 0.6% and a weighted average credit quality of AA (2011 - 0.3% and AA, respectively). The issuers of the Company’s agency fixed maturity investments primarily consist of the Federal National Mortgage Association, the Federal Home Loan Mortgage Corporation and other agencies. Fixed maturity investments included in agencies, are primarily priced by pricing services. When evaluating these securities, the pricing services gather information from market sources and integrate other observations from markets and sector news. Evaluations are updated by obtaining broker dealer quotes and other market information including actual trade volumes, when available. The fair value of each security is individually computed using analytical models which incorporate option adjusted spreads and other daily interest rate data.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

17

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d. Non-U.S. government (Sovereign debt) Level 2 - Non-U.S. government fixed maturity investments held by the Company at December 31, 2012, had a weighted average effective yield of 0.8% and a weighted average credit quality of AA (2011 - 2.0% and AA, respectively). The issuers of securities in this sector are non-U.S. governments and their respective agencies as well as supranational organizations. Securities held in these sectors, are primarily priced by pricing services who employ proprietary discounted cash flow models to value the securities. Key quantitative inputs for these models are daily observed benchmark curves for treasury, swap and high issuance credits. The pricing services may then apply a credit spread for each security which is developed by in-depth and real time market analysis. For securities in which trade volume is low, the pricing services utilize data from more frequently traded securities with similar attributes. These models may also be supplemented by daily market and credit research for international markets. Non-U.S. government-backed corporate Level 2 - Non-U.S. government-backed corporate fixed maturity investments had a weighted effective yield of 0.8% and a weighted average credit quality of AAA at December 31, 2012 (2011 - 1.3% and AAA, respectively). Non-U.S. government-backed fixed maturity investments are primarily priced by pricing services that employ proprietary discounted cash flow models to value the securities. Key quantitative inputs for these models are daily observed benchmark curves for treasury, swap and high issuance credits. The pricing services then apply a credit spread to the respective curve for each security which is developed by in-depth and real time market analysis. For securities in which trade volume is low, the pricing services utilize data from more frequently traded securities with similar attributes. These models may also be supplemented by daily market and credit research for international markets. Corporate Level 2 - At December 31, 2012, the Company’s corporate fixed maturity investments principally consist of U.S. and international corporations and had a weighted average effective yield of 1.6% and a weighted average credit quality of A (2011 - 3.4% and A, respectively). The Company’s corporate fixed maturity investments are primarily priced by pricing services. When evaluating these securities, the pricing services gather information from market sources regarding the issuer of the security and obtain credit data, as well as other observations from markets and sector news. Evaluations are updated by obtaining broker dealer quotes and other market information including actual trade volumes, when available. The pricing services also consider the specific terms and conditions of the securities, including any specific features which may influence risk. In certain instances, securities are individually evaluated using a spread which is added to the U.S. treasury curve or specific swap curve as appropriate. Agency mortgage-backed Level 2 - At December 31, 2012, the Company’s agency mortgage-backed fixed maturity investments included agency residential mortgage-backed securities with a weighted average effective yield of 1.2%, a weighted average credit quality of AA and a weighted average life of 3.3 years (2011 - 1.5%, AA and 2.4 years, respectively). The Company’s agency mortgage-backed fixed maturity investments are primarily priced by pricing services using a mortgage pool specific model which utilizes daily inputs from the active to be announced ("TBA") market which is very liquid, as well as the U.S. treasury market. The model also utilizes additional information, such as the weighted average maturity, weighted average coupon and other available pool level data which is provided by the sponsoring agency. Valuations are also corroborated with daily active market quotes.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

18

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d. Non-agency mortgage-backed Level 2 - The Company’s non-agency mortgage-backed fixed maturity investments include non-agency prime residential mortgage-backed fixed maturity investments. The Company has no fixed maturity investments classified as sub-prime held in its fixed maturity investments portfolio. At December 31, 2012, the Company’s non-agency prime residential mortgage-backed fixed maturity investments have a weighted average effective yield of 0.8%, a weighted average credit quality of AAA, and a weighted average life of 1.8 years (2011 - 2.3%, AAA and 1.1 years, respectively). Securities held in this sector are primarily priced by pricing services using an option adjusted spread ("OAS") model or other relevant models, which principally utilize inputs including benchmark yields, available trade information or broker quotes, and issuer spreads. The pricing services also review collateral prepayment speeds, loss severity and delinquencies among other collateral performance indicators for the securities valuation, when applicable. Commercial mortgage-backed Level 2 - The Company’s commercial mortgage-backed fixed maturity investments held at December 31, 2012 have a weighted average effective yield of 1.6%, a weighted average credit quality of AA, and a weighted average life of 5.6 years (2011 - 3.1%, AA and 6.2 years, respectively). Securities held in this sector are primarily priced by pricing services. The pricing services apply dealer quotes and other available trade information such as bids and offers, prepayment speeds which may be adjusted for the underlying collateral or current price data, the U.S. treasury curve and swap curve as well as cash settlement. The pricing services discount the expected cash flows for each security held in this sector using a spread adjusted benchmark yield based on the characteristics of the security. Asset-backed Level 2 - At December 31, 2012, the Company’s asset-backed fixed maturity investments had a weighted average effective yield of 1.6 %, a weighted average credit quality of AAA and a weighted average life of 5.5 years (2011 - 1.9%, AAA and 6.3 years, respectively). The underlying collateral for the Company’s asset-backed fixed maturity investments primarily consists of student loans and credit card receivables. Securities held in these sectors are primarily priced by pricing services. The pricing services apply dealer quotes and other available trade information such as bids and offers, prepayment speeds which may be adjusted for the underlying collateral or current price data, the U.S. treasury curve and swap curve as well as cash settlement. The pricing services determine the expected cash flows for each security held in this sector using historical prepayment and default projections for the underlying collateral and current market data. In addition, a spread is applied to the relevant benchmark and used to discount the cash flows noted above to determine the fair value of the securities held in this sector. Short Term Investments Level 2 - The fair value of the Company’s portfolio of short term investments are generally determined using amortized cost which approximates fair value and, in certain cases, in a manner similar to the Company’s fixed maturity investments noted above.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

19

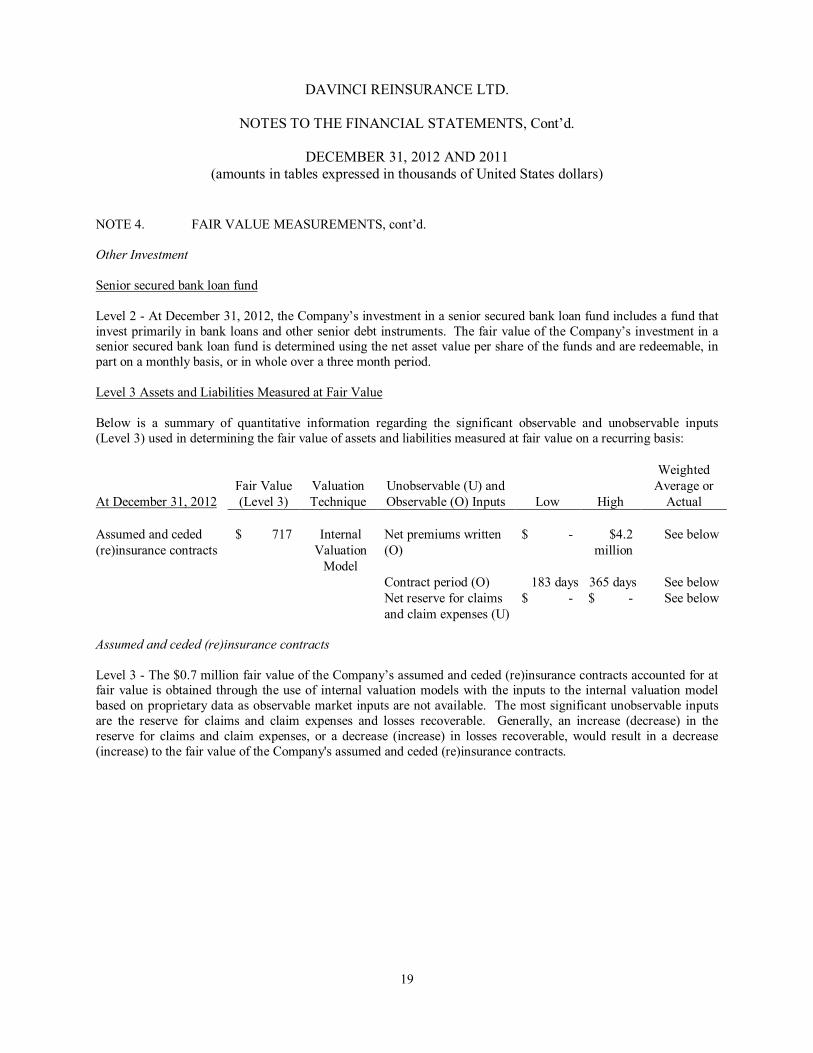

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d. Other Investment Senior secured bank loan fund Level 2 - At December 31, 2012, the Company’s investment in a senior secured bank loan fund includes a fund that invest primarily in bank loans and other senior debt instruments. The fair value of the Company’s investment in a senior secured bank loan fund is determined using the net asset value per share of the funds and are redeemable, in part on a monthly basis, or in whole over a three month period. Level 3 Assets and Liabilities Measured at Fair Value Below is a summary of quantitative information regarding the significant observable and unobservable inputs (Level 3) used in determining the fair value of assets and liabilities measured at fair value on a recurring basis:

At December 31, 2012 Fair Value (Level 3)

Valuation Technique

Unobservable (U) and Observable (O) Inputs Low High

Weighted Average or

Actual Assumed and ceded (re)insurance contracts

$ 717 Internal Valuation

Model

Net premiums written (O)

$ - $4.2 million

See below

Contract period (O) 183 days 365 days See below Net reserve for claims

and claim expenses (U) $ - $ - See below

Assumed and ceded (re)insurance contracts Level 3 - The $0.7 million fair value of the Company’s assumed and ceded (re)insurance contracts accounted for at fair value is obtained through the use of internal valuation models with the inputs to the internal valuation model based on proprietary data as observable market inputs are not available. The most significant unobservable inputs are the reserve for claims and claim expenses and losses recoverable. Generally, an increase (decrease) in the reserve for claims and claim expenses, or a decrease (increase) in losses recoverable, would result in a decrease (increase) to the fair value of the Company's assumed and ceded (re)insurance contracts.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

20

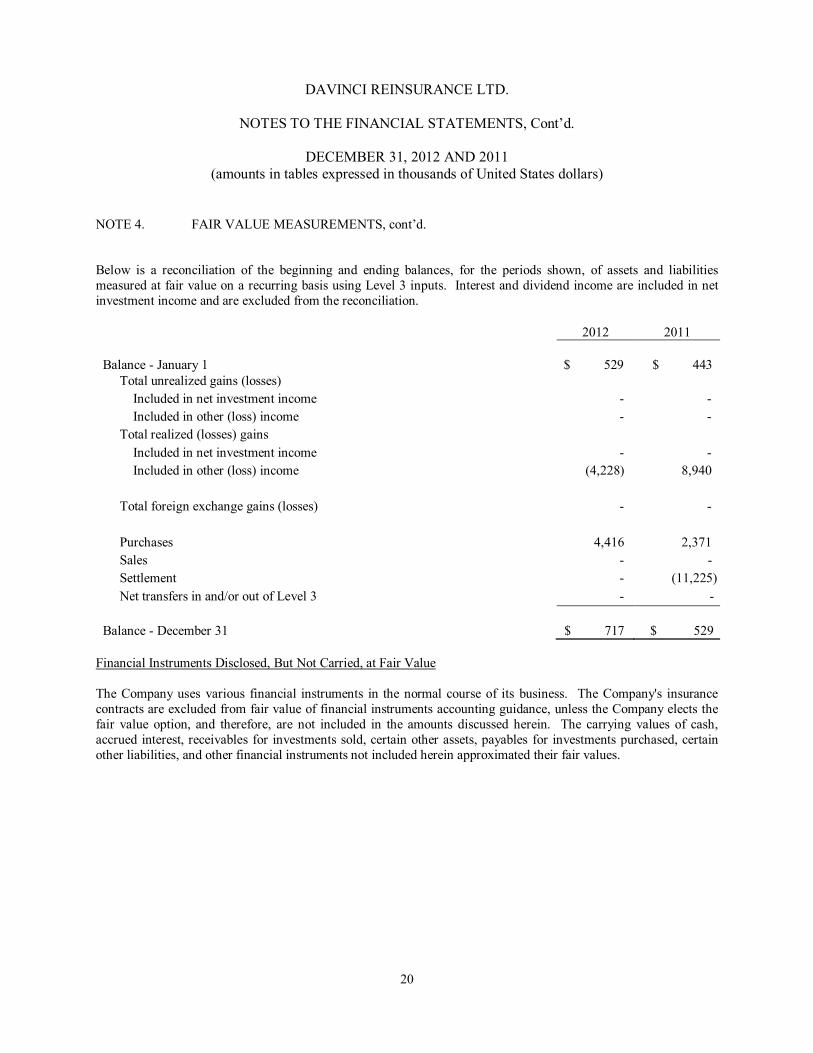

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d. Below is a reconciliation of the beginning and ending balances, for the periods shown, of assets and liabilities measured at fair value on a recurring basis using Level 3 inputs. Interest and dividend income are included in net investment income and are excluded from the reconciliation.

2012 2011 Balance - January 1

$ 529

$ 443

Total unrealized gains (losses) Included in net investment income - - Included in other (loss) income - - Total realized (losses) gains Included in net investment income - - Included in other (loss) income (4,228) 8,940 Total foreign exchange gains (losses) - - Purchases 4,416 2,371 Sales - - Settlement - (11,225) Net transfers in and/or out of Level 3 - - Balance - December 31

$ 717

$ 529

Financial Instruments Disclosed, But Not Carried, at Fair Value The Company uses various financial instruments in the normal course of its business. The Company's insurance contracts are excluded from fair value of financial instruments accounting guidance, unless the Company elects the fair value option, and therefore, are not included in the amounts discussed herein. The carrying values of cash, accrued interest, receivables for investments sold, certain other assets, payables for investments purchased, certain other liabilities, and other financial instruments not included herein approximated their fair values.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

21

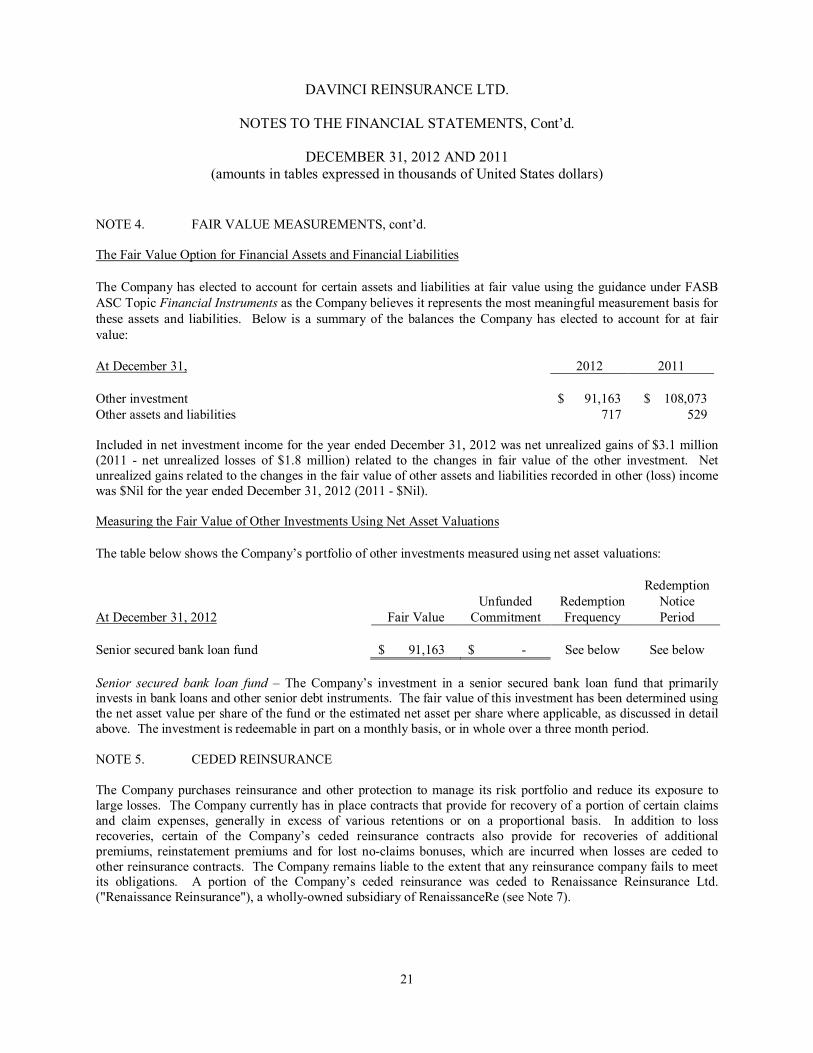

NOTE 4. FAIR VALUE MEASUREMENTS, cont’d. The Fair Value Option for Financial Assets and Financial Liabilities

The Company has elected to account for certain assets and liabilities at fair value using the guidance under FASB ASC Topic Financial Instruments as the Company believes it represents the most meaningful measurement basis for these assets and liabilities. Below is a summary of the balances the Company has elected to account for at fair value: At December 31, 2012 2011 Other investment

$ 91,163

$ 108,073

Other assets and liabilities 717 529 Included in net investment income for the year ended December 31, 2012 was net unrealized gains of $3.1 million (2011 - net unrealized losses of $1.8 million) related to the changes in fair value of the other investment. Net unrealized gains related to the changes in the fair value of other assets and liabilities recorded in other (loss) income was $Nil for the year ended December 31, 2012 (2011 - $Nil). Measuring the Fair Value of Other Investments Using Net Asset Valuations The table below shows the Company’s portfolio of other investments measured using net asset valuations:

At December 31, 2012

Fair Value Unfunded

Commitment Redemption Frequency

Redemption Notice Period

Senior secured bank loan fund

$ 91,163

$ -

See below

See below

Senior secured bank loan fund – The Company’s investment in a senior secured bank loan fund that primarily invests in bank loans and other senior debt instruments. The fair value of this investment has been determined using the net asset value per share of the fund or the estimated net asset per share where applicable, as discussed in detail above. The investment is redeemable in part on a monthly basis, or in whole over a three month period. NOTE 5. CEDED REINSURANCE The Company purchases reinsurance and other protection to manage its risk portfolio and reduce its exposure to large losses. The Company currently has in place contracts that provide for recovery of a portion of certain claims and claim expenses, generally in excess of various retentions or on a proportional basis. In addition to loss recoveries, certain of the Company’s ceded reinsurance contracts also provide for recoveries of additional premiums, reinstatement premiums and for lost no-claims bonuses, which are incurred when losses are ceded to other reinsurance contracts. The Company remains liable to the extent that any reinsurance company fails to meet its obligations. A portion of the Company’s ceded reinsurance was ceded to Renaissance Reinsurance Ltd. ("Renaissance Reinsurance"), a wholly-owned subsidiary of RenaissanceRe (see Note 7).

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

22

NOTE 5. CEDED REINSURANCE, cont’d. The following table sets forth the effect of reinsurance and retrocessional activity on premiums written and earned and on net claims and claim expenses incurred: At December 31, 2012 2011 Premiums written

Assumed $ 450,744 $ 436,759 Ceded (85,410) (74,941)

Net premiums written

$ 365,334 $ 361,818

Premiums earned Assumed $ 441,057 $ 424,703 Ceded (77,375) (74,270)

Net premiums earned

$ 363,682 $ 350,433

Claims and claim expenses Gross claims and claim expenses incurred $ 98,977 $ 452,501 Claims and claim expenses recovered (5,676) (58,411)

Net claims and claim expenses incurred

$ 93,301 $ 394,090

The reinsurers with the three largest balances accounted for 43.4%, 14.3% and 11.7% respectively, of the Company’s reinsurance recoverable balance at December 31, 2012 (2011 - 34.2%, 27.4% and 21.4%, respectively). At December 31, 2012, the Company had a $0.6 million valuation allowance against reinsurance recoverable. The three company-specific components of the valuation allowance represented 24.3%, 17.7% and 8.1%, respectively, of the Company’s total valuation allowance at December 31, 2012 (2011 - three largest company-specific components 50.9%, 30.6% and 15.6%, respectively). NOTE 6. RESERVE FOR CLAIMS AND CLAIM EXPENSES The Company uses statistical and actuarial methods to estimate ultimate expected claims and claim expenses. The period of time from the reporting of a claim to the Company and the settlement of the Company’s liability may be many years. During this period, additional facts and trends will be revealed. As these factors become apparent, case reserves will be adjusted, sometimes requiring an increase or decrease in the overall reserve for claims and claim expenses of the Company, and at other times requiring a reallocation of IBNR reserves to specific case reserves or additional case reserves. These estimates are reviewed regularly, and such adjustments, if any, are reflected in the results of operations in the period in which they become known and are accounted for as changes in estimates. Adjustments to the Company’s reserve for claims and claim expenses can impact current year net income (loss) by increasing net income or decreasing net loss if the estimates of prior year claims and claim expense reserves prove to be overstated or by decreasing net income or increasing net loss if the estimates of prior year claims and claim expense reserves prove to be insufficient.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

23

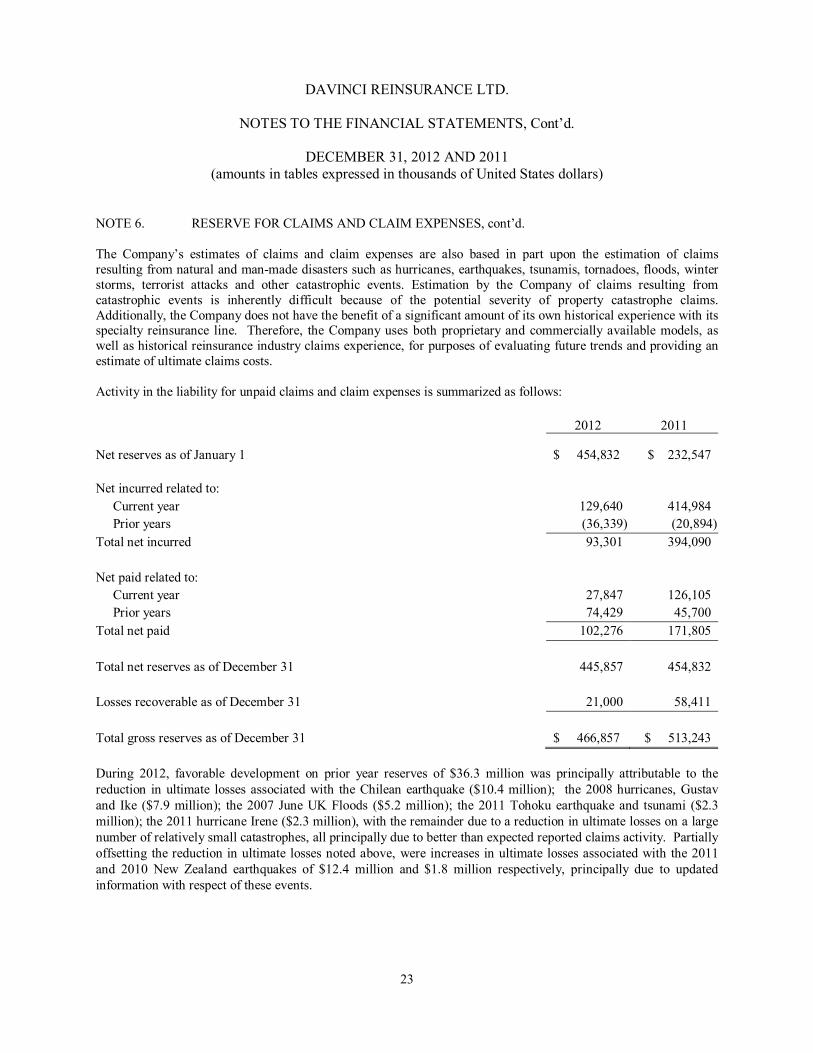

NOTE 6. RESERVE FOR CLAIMS AND CLAIM EXPENSES, cont’d. The Company’s estimates of claims and claim expenses are also based in part upon the estimation of claims resulting from natural and man-made disasters such as hurricanes, earthquakes, tsunamis, tornadoes, floods, winter storms, terrorist attacks and other catastrophic events. Estimation by the Company of claims resulting from catastrophic events is inherently difficult because of the potential severity of property catastrophe claims. Additionally, the Company does not have the benefit of a significant amount of its own historical experience with its specialty reinsurance line. Therefore, the Company uses both proprietary and commercially available models, as well as historical reinsurance industry claims experience, for purposes of evaluating future trends and providing an estimate of ultimate claims costs. Activity in the liability for unpaid claims and claim expenses is summarized as follows:

2012 2011

Net reserves as of January 1

$ 454,832 $ 232,547 Net incurred related to:

Current year 129,640 414,984 Prior years (36,339) (20,894)

Total net incurred 93,301 394,090

Net paid related to: Current year 27,847 126,105 Prior years 74,429 45,700

Total net paid 102,276 171,805

Total net reserves as of December 31 445,857 454,832 Losses recoverable as of December 31 21,000 58,411 Total gross reserves as of December 31 $ 466,857 $ 513,243 During 2012, favorable development on prior year reserves of $36.3 million was principally attributable to the reduction in ultimate losses associated with the Chilean earthquake ($10.4 million); the 2008 hurricanes, Gustav and Ike ($7.9 million); the 2007 June UK Floods ($5.2 million); the 2011 Tohoku earthquake and tsunami ($2.3 million); the 2011 hurricane Irene ($2.3 million), with the remainder due to a reduction in ultimate losses on a large number of relatively small catastrophes, all principally due to better than expected reported claims activity. Partially offsetting the reduction in ultimate losses noted above, were increases in ultimate losses associated with the 2011 and 2010 New Zealand earthquakes of $12.4 million and $1.8 million respectively, principally due to updated information with respect of these events.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

24

NOTE 6. RESERVE FOR CLAIMS AND CLAIM EXPENSES, cont’d. During 2011, favorable development on prior year reserves of $20.9 million was principally attributable to the reduction in ultimate losses associated with tropical cyclone Tasha ($4.5 million); the Chilean earthquake ($4.9 million); the 2005 hurricanes, Katrina, Rita and Wilma ($2.5 million), with the remainder due to a reduction in ultimate losses on a large number of relatively small catastrophes, all principally due to better than expected reported claims activity. Partially offsetting the reduction in ultimate losses noted above, were increases in ultimate losses associated with the September 2010 New Zealand earthquake ($7.9 million), principally due to updated information with respect of the event. NOTE 7. RELATED PARTY TRANSACTIONS AND MAJOR CUSTOMERS The Company entered into reinsurance agreements with Renaissance Reinsurance in each year from 2002 to 2012 and also entered into reinsurance agreements with RenaissanceRe Specialty Risks Ltd., formerly known as Glencoe Insurance Ltd. ("RenaissanceRe Specialty Risks"), a wholly-owned subsidiary of RenaissanceRe, to assume a portion of RenaissanceRe Specialty Risks’ property business in each year from 2002 to 2007. During 2012, net premiums earned assumed from Renaissance Reinsurance were $17.5 million (2011 - $13.3 million). At December 31, 2012, unearned premiums were $4.9 million (2011 - $3.6 million) and premiums receivable were $11.2 million (2011 - $5.7 million). In addition, during 2012, net claims and claim expenses incurred under these agreements with Renaissance Reinsurance and RenaissanceRe Specialty Risks were $9 thousand (2011 - negative $0.3 million) and outstanding reserves for claims and claim expenses assumed under these agreements with Renaissance Reinsurance and RenaissanceRe Specialty Risks at December 31, 2012 were $1.9 million (2011 - $1.9 million). The Company entered into reinsurance agreements to cede a portion of its property catastrophe business to Renaissance Reinsurance in various years from 2002 to 2011. During 2012 net earned premiums ceded under these agreements were $Nil (2011 - $2.6 million) and net claims and claim expenses recovered were $0.3 million (2011 - $11.9 million). At December 31, 2012, reinsurance recoverables under these agreements were $6.1 million (2011 - $11.9 million), prepaid reinsurance for these agreements were $Nil (2011 - $Nil) and reinsurance balances payable were $0.1 million (2011 - $16 thousand). During 2012, the Company entered in to a retrocessional reinsurance agreement with Timicuan Reinsurance III Ltd. (“Tim Re III”), a related party, to cede a portion of the premium and related exposure from a defined selection of the Company’s Florida property catastrophe reinstatement premium protection business incepting on June 1, 2012. During 2012, net earned premiums ceded under these agreements were $10.1 million and net claims and claim expenses recovered were $Nil. At December 31, 2012, losses recoverable under these agreements were $Nil, unearned premium reserves ceded for these agreements were $7.1 million and reinsurance balances payable were $6.4 million. A subsidiary of the Company’s ultimate parent has entered into the following non-insurance transactions with Tower Hill Holdings Inc. ("Tower Hill") and certain of its subsidiaries: a $5.0 million promissory note to Tower Hill Insurance Group, LLC (“THIG”), under common ultimate ownership with Tower Hill; and a $50.0 million, $10.0 million and $0.5 million equity investment in THIG, Tower Hill and Tower Hill Signature Insurance Holdings, Inc. (collectively, the "Tower Hill Companies"), which are accounted for under the equity method of accounting.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

25

NOTE 7. RELATED PARTY TRANSACTIONS AND MAJOR CUSTOMERS, cont’d. The Company has entered into reinsurance agreements with certain subsidiaries and affiliates of Tower Hill and has also entered into reinsurance agreements with respect to business produced by the Tower Hill Companies. For the year ended December 31, 2012, the Company recorded $20.1 million (2011 - $11.6 million) of gross premium written assumed from Tower Hill and its subsidiaries and affiliates. Gross premiums earned totaled $16.3 million (2011 - $11.7 million) and expenses incurred were $1.8 million (2011 - $1.3 million) for the year ended December 31, 2012 related to these contracts. The Company had a net related outstanding receivable balance of $9.0 million as of December 31, 2012 (2011 - $4.9 million). During 2012, the Company recovered net claims and claim expenses of $1 thousand (2011 - $19 thousand) and, as of December 31, 2012, had a net reserve for claims and claim expenses of $23 thousand (2011 - $26 thousand). Under the terms of a management agreement, Renaissance Underwriting Managers, Ltd. ("RUM"), a wholly-owned subsidiary of RenaissanceRe, has contracted to provide all of the Company’s management, underwriting, investment management and administrative functions, for which it is paid a fee that is a percentage of premium and a profit commission. Operational expenses for the year ended December 31, 2012 includes $79.0 million (2011 - $10.4 million) and amounts due to affiliates at December 31, 2012 includes $39.5 million (2011 - $24.6 million) related to the services noted above. Amounts due to affiliates are non-interest-bearing and payable in accordance with the terms of the management agreement. As per the management agreement, $27.3 million (2011 - $13.8 million) of the amounts due to affiliates represents deferred profit commission which is not currently due but will be accrued to offset future underwriting year deficits, should they occur, subject to a maximum dollar amount. Additionally, the Company is required to reimburse RUM for other directly identifiable costs. For the years ended December 31, 2012 and 2011, no such directly identifiable costs were allocated to the Company. See “Note 8. Shareholders’ Equity” for additional information related to transactions with existing and former shareholders. During the year ended December 31, 2012, the Company received 77.3% (2011 - 87.6%) of its gross premiums written from three reinsurance brokers. Subsidiaries and affiliates of AON Benfield, Marsh Inc. and the Willis Group accounted for approximately 51.3%, 19.8%, and 6.2% respectively, of the Company’s gross premiums written in 2012 (2011 - 58.6%, 20.8%, and 8.2%).

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

26

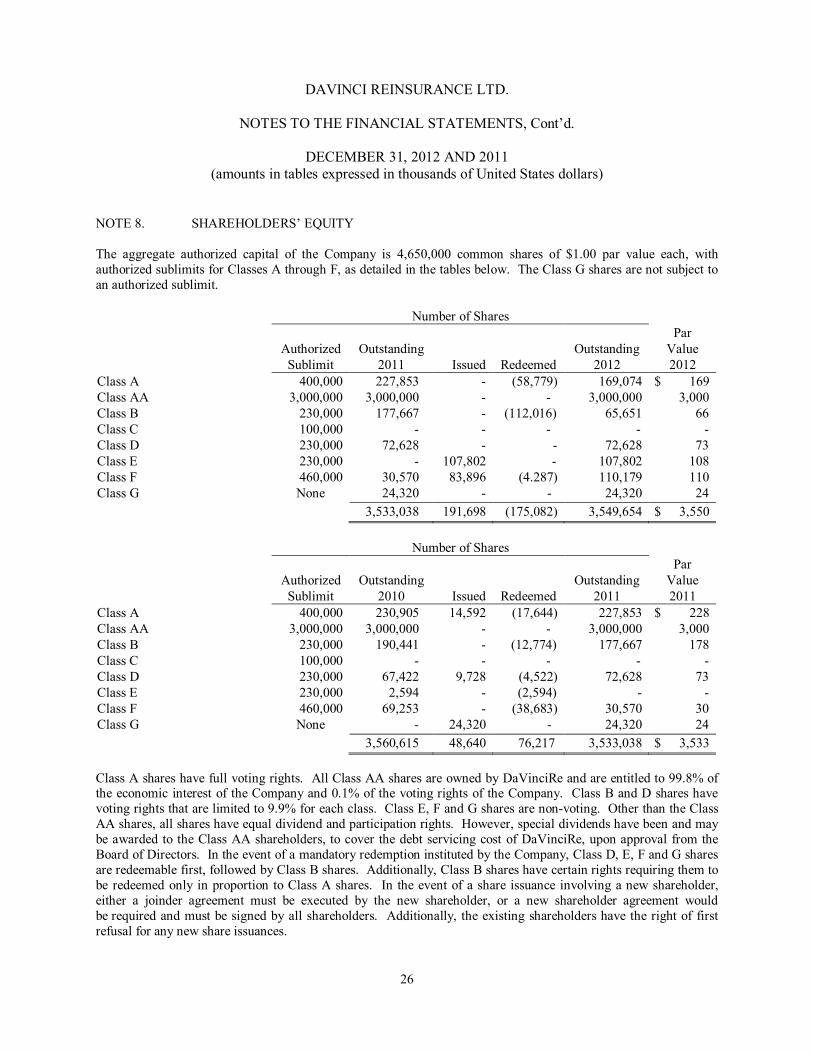

NOTE 8. SHAREHOLDERS’ EQUITY The aggregate authorized capital of the Company is 4,650,000 common shares of $1.00 par value each, with authorized sublimits for Classes A through F, as detailed in the tables below. The Class G shares are not subject to an authorized sublimit. Number of Shares

Authorized Sublimit

Outstanding 2011 Issued Redeemed

Outstanding 2012

Par Value 2012

Class A 400,000 227,853 - (58,779) 169,074 $ 169 Class AA 3,000,000 3,000,000 - - 3,000,000 3,000 Class B 230,000 177,667 - (112,016) 65,651 66 Class C 100,000 - - - - - Class D 230,000 72,628 - - 72,628 73 Class E 230,000 - 107,802 - 107,802 108 Class F 460,000 30,570 83,896 (4.287) 110,179 110 Class G None 24,320 - - 24,320 24 3,533,038 191,698 (175,082) 3,549,654 $ 3,550 Number of Shares

Authorized Sublimit

Outstanding 2010 Issued Redeemed

Outstanding 2011

Par Value 2011

Class A 400,000 230,905 14,592 (17,644) 227,853 $ 228 Class AA 3,000,000 3,000,000 - - 3,000,000 3,000 Class B 230,000 190,441 - (12,774) 177,667 178 Class C 100,000 - - - - - Class D 230,000 67,422 9,728 (4,522) 72,628 73 Class E 230,000 2,594 - (2,594) - - Class F 460,000 69,253 - (38,683) 30,570 30 Class G None - 24,320 - 24,320 24 3,560,615 48,640 76,217 3,533,038 $ 3,533 Class A shares have full voting rights. All Class AA shares are owned by DaVinciRe and are entitled to 99.8% of the economic interest of the Company and 0.1% of the voting rights of the Company. Class B and D shares have voting rights that are limited to 9.9% for each class. Class E, F and G shares are non-voting. Other than the Class AA shares, all shares have equal dividend and participation rights. However, special dividends have been and may be awarded to the Class AA shareholders, to cover the debt servicing cost of DaVinciRe, upon approval from the Board of Directors. In the event of a mandatory redemption instituted by the Company, Class D, E, F and G shares are redeemable first, followed by Class B shares. Additionally, Class B shares have certain rights requiring them to be redeemed only in proportion to Class A shares. In the event of a share issuance involving a new shareholder, either a joinder agreement must be executed by the new shareholder, or a new shareholder agreement would be required and must be signed by all shareholders. Additionally, the existing shareholders have the right of first refusal for any new share issuances.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

27

NOTE 8. SHAREHOLDERS’ EQUITY, cont’d. The Company and its shareholders are party to a shareholders’ agreement (the "Shareholders Agreement") which, among other things, provides the Company’s shareholders, excluding ROIHL, with certain redemption rights that enable each shareholder to notify the Company of such shareholder’s desire for the Company to repurchase up to half of such shareholder’s aggregate number of shares held, subject to certain limitations, such as limiting the aggregate of all share repurchase requests to 25% of the Company’s capital in any given year and satisfying all applicable regulatory requirements. If total shareholder requests exceed 25% of the Company’s capital, the number of shares repurchased will be reduced among the requesting shareholders pro-rata, based on the amounts desired to be repurchased. Shareholders desiring to have the Company repurchase their shares must notify the Company before March 1 of each year. The repurchase price will be based on GAAP book value as of the end of the year in which the shareholder notice is given, and the repurchase will be effective as of such date. Payment will be made by April 1 of the following year, following delivery of the audited financial statements for the year in which the repurchase was effective. The repurchase price is paid net of a holdback for development on outstanding loss reserves after settlement of all claims relating to the applicable years. In advance of the March 1, 2011 redemption notice date, certain third party shareholders of the Company submitted repurchase notes, in accordance with the Shareholders Agreement, for shares of the Company with a GAAP book value of $9.2 million at December 31, 2012. Effective January 1, 2012, the Company redeemed the shares for $9.2 million, less a $1.8 million reserve holdback. On June 1, 2011, the Company completed an equity raise of $100.0 million from new and existing shareholders, including $30.0 million contributed by ROIHL. Effective January 1, 2012, an existing third party shareholder sold a portion of its shares in the Company to a new third party shareholder. In connection with the sale by the existing third party shareholder, the Company retained a $4.9 million holdback. In addition, effective January 1, 2012, ROIHL sold a portion of its shares of DaVinciRe to a separate new third party shareholder and the Company retained a $10.0 million reserve holdback. In connection with these transactions, the Company repurchased Class A and B shares, and issued an equivalent amount of Class E shares. Certain third party shareholders of the Company submitted repurchase notices on or before the required annual redemption notice date of March 1, 2012, in accordance with the Shareholders Agreement, for shares of the Company with a GAAP book value of $53.2 million at December 31, 2012. On June 1, 2012, the Company completed an equity raise of $49.3 million from a new third party investor. In addition, ROIHL and an existing third party investor each sold $24.7 million in common shares of the Company to another existing third party investor, for a total of $49.4 million. In connection with the sale by ROIHL and the existing third party investor, the Company retained a $5.0 million holdback. On October 1, 2012, ROIHL sold a portion of its shares of the Company to a new third party shareholder for $9.8 million. During 2012, the Company declared and paid aggregate cash dividends of $108.0 million (2011 - $6.8 million), of which, $100.0 million was subsequently paid from DaVinciRe to RenaissanceRe to partially settle an existing loan agreement between DaVinciRe and RenaissanceRe. See "Note 13. Subsequent Events" for additional information related to DaVinciRe shareholder transactions which occurred during January 2013.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

28

NOTE 9. TAXATION Under current Bermuda law, the Company is not subject to any income or capital gains taxes. In the event that such taxes are imposed, the Company would be exempted from any such tax until March 2035 pursuant to the Bermuda Exempted Undertakings Tax Protection Act of 1966, and Amended Acts of 1987 and 2011, respectively. NOTE 10. STATUTORY REQUIREMENTS Bermuda Statutory Requirements Under the Insurance Act 1978, amendments thereto and Related Regulations of Bermuda (the "Insurance Act"), the Company is required to prepare statutory financial statements and to file in Bermuda a statutory financial return. The Insurance Act also requires the Company to maintain certain measures of solvency and liquidity. At December 31, 2012, the statutory capital and surplus of the Company was $1.5 billion (2011 - $1.3 billion) and the minimum amount required to be maintained under Bermuda law, the Minimum Solvency Margin, was $182.7 million (2011 - $180.9 million). In addition, a minimum liquidity ratio must be maintained whereby relevant assets, as defined by the Act, must exceed 75% of relevant liabilities. At December 31, 2012 and 2011, the liquidity ratio was met. Under the Insurance Act, the Company is classified as a Class 4 insurer, and therefore must maintain capital at a level equal to its enhanced capital requirement ("ECR") which is established by reference to the Bermuda Solvency Capital Requirement ("BSCR") model. The BSCR is a standard mathematical model designed to give the Bermuda Monetary Authority ("BMA") more advanced methods for determining an insurer's capital adequacy. Underlying the BSCR is the belief that all insurers should operate on an ongoing basis with a view to maintaining their capital at a prudent level in excess of the minimum solvency margin otherwise prescribed under the Insurance Act. Alternatively, under the Insurance Act, insurers may, subject to the terms of the Insurance Act and to the BMA's oversight, elect to utilize an approved internal capital model to determine regulatory capital. In either case, the ECR shall at all times equal or exceed the Class 4 insurer's Minimum Solvency Margin and may be adjusted in circumstances where the BMA concludes that the insurer's risk profile deviates significantly from the assumptions underlying its ECR or the insurer's assessment of its risk management policies and practices used to calculate the ECR applicable to it. While not specifically referred to in the Insurance Act, the BMA has also established a target capital level ("TCL") for each Class 4 insurer equal to 120% of its respective ECR. While a Class 4 insurer is not currently required to maintain its statutory capital and surplus at this level, the TCL serves as an early warning tool for the BMA and failure to maintain statutory capital at least equal to the TCL will likely result in increased BMA regulatory oversight.

DAVINCI REINSURANCE LTD.

NOTES TO THE FINANCIAL STATEMENTS, Cont’d.

DECEMBER 31, 2012 AND 2011 (amounts in tables expressed in thousands of United States dollars)

29