Embed Size (px)

Citation preview

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 1/43

Acquisition of Information in Loan Markets and Bank Market Power

- An Empirical Investigation

Karl-Hermann Fischer

Department of Finance

Johann Wolfgang Goethe University Frankfurt

e-mail:[email protected]

Do commercial banks invest less in information gathering activity when they compete more

aggressively with each other? Does intensifying competitive pressure in bank loan markets affect the

quality of informational ties that bind borrowers and lending banks? Using survey data from German

manufacturing firms, we are able to directly measure information flows from loan applicants to banks.

We find that firms located in more concentrated banking markets have to transfer more project-

specific information to their lending banks. Furthermore we find that banks that systematically acquire

more information about their loan customers are able to provide liquidity without inducing additionalcostly transfer of information. Third, we find credit to be more readily available in more concentrated

banking markets. This latter result confirms recent US findings. However, our analysis of banks’

information acquisition offers first empirical evidence in favour an alternative explanation of why

credit availability systematically varies with bank market structure.

Key Words: Relationship Lending, Bank Market Power, Information Acquisition

JEL Classification: G21, L13

---------------------------------------------------------------------------------------------------------------------------------------

I would like to thank the staff of the Ifo-Institute for Economic Research, Munich, for their help and hospitality.

I am especially indebted to Claudia Plötscher for not only providing access to the data base used in this study but

also for extremely helpful comments and suggestions. I also thank Jean Dermine, Reint Gropp, Craig McKinlay,Steven Ongena, Ulrich Rendtel and Erik Theissen for helpful suggestions and encouragement. Seminar

participants at INSEAD and Goethe University as well as participants of the EFA 2000 meeting in London also

provided helpful comments. All errors and inaccuracies remain the sole responsibility of the author.

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 2/43

2

Acquisition of Information in Loan Markets and Bank Market

Power - An Empirical Investigation

Abstract:

Do commercial banks invest less in information gathering activity when they compete more

aggressively with each other? Does intensifying competitive pressure in bank loan markets

affect the quality of informational ties that bind borrowers and lending banks? Using survey

data from German manufacturing firms, we are able to directly measure information flows

from loan applicants to banks. We find that firms located in more concentrated banking

markets have to transfer more project-specific information to their lending banks.

Furthermore we find that banks that systematically acquire more information about their loan

customers are able to provide liquidity without inducing additional costly transfer of

information. Third, we find credit to be more readily available in more concentrated banking

markets. This confirms recent US findings. However, our analysis of banks’ information

acquisition offers first empirical evidence in favour an alternative explanation of why credit

availability systematically varies with bank market structure.

JEL Classification: G21, L13

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 3/43

3

Do commercial banks invest less in information gathering activity when they compete

more aggressively with each other? There is now considerable interest in whether intensifying

competitive pressure in bank loan markets will affect the quality of informational ties that

bind borrowers and lending banks1. The idea of the transmission of project-specific private

information from a borrowing firm to a lending bank goes back at least to Fama’s (1985)

conjecture that banks provide inside financing as opposed to what was subsequently called

arm’s-length financing provided by capital markets. This notion could be seen as a major

building block of the modern theory of the commercial bank 2

and empirical research has

provided numerous pieces of evidence in favour of it. Although this view is now widely

accepted in general, what determines the intensity of a bank’s information acquisition is still

poorly understood. We do not yet know much about whether some banks acquire more

information and systematically build stronger ties to their customers than others3. What

determines banks’ information gathering activity cross-sectionally, or through time?

Furthermore, are there other related functions that banks perform – for example that of

providing liquidity services to their loan customers – that are affected by banks’ information

acquisition activity?

In this paper we analyse whether local bank market structure – proxying for bank

market power – affects banks’ information acquisition activity. To the best of our knowledge

this is the first empirical study that directly addresses information transmission within bank-

customer relationships. Using survey data from small and medium-sized German

manufacturing firms, we are able to directly measure information flows from firms to banks

within a loan application situation. We find that local bank market concentration has a

positive and significant impact on banks’ information gathering activity. Similarly to

Petersen/Rajan (1995), we take standard measures of the concentration of a local market as an

approximation for bank market power.4

In a second step the data set allows us to consider

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 4/43

4

what could be termed a natural experiment on the hypothesised market structure/information

relationship: For example: if it is true that banks in more concentrated markets systematically

acquire more information in the normal course of a business relationship, these banks should

be able to provide liquidity at short notice without inducing additional costly transfer of

information and vice versa. As a consequence of this, the aforementioned relationship

between market structure and information transmission should be reversed for a subsample of

firms that have experienced a liquidity shock and, as a consequence, demand short-term

liquidity. Our results indicate that in such a situation informational requirements are

significantly lower for firms located in more concentrated banking markets as well as for

firms that already have a long-term relationship with the bank they approach.

In the last step of our analysis we assess whether the informational intensity within

lending relationships addressed in the first part of the study has consequences in terms of

firms’ financing patterns. Here we use information on the degree of discounts for early

payment which are taken by each firm as an approximation of credit availability. This last

step is thus a reappraisal of Petersen/Rajan’s (1995) study, using German data. The results are

similar to the US findings although the first two steps of the study offer an explanation for a

relationship between credit availability and bank market power that differs from

Petersen/Rajan’s as it is more directly related to information acquisition activity. The paper

proceeds as follows: In section I we briefly review the relevant theoretical literature and

derive testable hypotheses. Section II outlines the design of the study and presents our results.

Section III sums up and concludes.

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 5/43

5

I Bank Market Power and Information Acquisition in Loan Markets

There is now intense academic interest in the welfare implications of increasing

competitive pressure in bank loan markets. Standard economic thought predicts positive

welfare effects that arise primarily from lower loan rates and larger loan volume.5

In banking

markets, however, this might not be the whole story as several bank products are

characterised by asymmetry of information between banks and their customers as well as

implicit risk sharing arrangements within multi-period contractual relationships. This seems

to be especially important for bank loan products such as lines of credit, loan commitments or

longer-term bank loans negotiated in spot markets. It is now widely accepted that long-term

relationships between banks and loan customers observable in real-world loan markets

provide a framework within which the solution of information problems is more efficiently

accomplished. It is also widely believed that bank uniqueness rests mainly on a bank’s ability

to acquire and evaluate borrower-specific private information. However, exactly how the

transmission of information within lending relationships takes place has remained largely

unexplored. For example, is learning-by-lending all that is needed to provide banks with

superior information? A learning-by-lending technology is assumed in most of the theory of

relationship lending.6

This notion is also implicit in most empirical studies that try to measure

informational intensities by using the duration of the bank-borrower relationship as a proxy.7

In contrast to this strand of the literature, in what follows we assume that information does not

only accumulate over time but information acquisition is a costly activity and a choice

variable of the bank. Thus the information problem becomes endogenous in the bank’s

incentives to invest in borrower-specific information, which might – among other things – be

influenced by competitive pressure in bank loan markets.

This raises the question of whether taking account of these characteristic features of

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 6/43

6

bank loans in models of bank competition leads to results that go beyond the standard

industrial economics result. The theoretical literature offers at least three explanations of why

bank market power might affect banks’ information gathering activity. We review them

briefly here.

Mayer (1988) claimed that competitive financial markets might be detrimental to

economic welfare in that they make long-term relationships between financiers and

entrepreneurs harder to sustain. This notion was formalised in Petersen/Rajan (1995) who also

provided empirical evidence indicating that small and medium-sized US firms based in more

concentrated banking markets (i) take early payment discounts more often, (ii) show a

stronger reliance on debt financing by financial institutions and (iii) pay lower loan rates

when young, and higher loan rates when old compared to similar firms based in more

competitive markets. In the theoretical part of their paper, Petersen/Rajan focus on a bank’s

ability to share in the future borrower project surplus whenever it exercises market power

over the borrowing firm.

In their theoretical two-period model the bank becomes fully informed after the first

period because of a simple and costless learning-by-lending technology. In what follows we

will argue that costly information acquisition provides another mechanism that makes bank

market power a meaningful determinant of credit availability, although we do not address the

pricing dimension in our empirical study. From our perspective, assuming that information

acquisition activity eats up part of a bank’s resources is crucial but does not seem to be

unrealistic. Casual empiricism tells us instead that commercial banks devote considerable

resources to acquiring and processing borrower specific information. Obviously loan

availability as well as loan pricing should be affected by the accuracy and timeliness of the

information a lending bank has about a borrower’s prospects and credit risk.

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 7/43

7

One reason why increasing bank competition might be detrimental to a lender’s

incentives to undertake costly screening/monitoring is that once a lender has granted a loan to

a firm, other potential lenders might be able to observe this at low cost. Given that the bank

has borne a non-trivial cost in screening the applicant, competitor banks can offer better terms

of lending as they free ride on the first bank’s screening effort. Thus, as a consequence of free

riding behaviour, underprovision of screening prevails in equilibrium in competitive credit

markets.8

Whether information spillover, competitor banks’ free riding, and switching behaviour

on the part of borrowing firms are empirically important, and whether they are related to

market structure in banking markets, are questions that remain to be analysed. There are,

however, several pieces of evidence that would seem to point in this direction. Petersen/Rajan

(1995) find that firms located in the most competitive banking markets are solicited

significantly more often by competitor banks than firms in the least competitive markets. The

difference seems to be especially pronounced for older firms where their mere survival as

well as a sequence of credit granting decisions by banks in the past has already disclosed

signals of project quality to competitor banks. Evidence of another type comes from so-called

bank uniqueness studies: It is now widely believed that announcements of bank loan

agreements systematically lead to re-evaluations of the borrowers by capital market

participants.9

What is often overlooked in interpreting these findings is that measured capital

market reactions are evidence of information spillover effects that take place in financial

markets10

.

A second fundamental hypothesis about the relationship between bank market power

and bank monitoring effort takes entrepreneurial incentive problems more directly into

account. In monitoring an entrepreneur acting under limited liability who – for well known

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 8/43

8

reasons – is willing to shift to inefficient investment projects, a bank normally cannot commit

to a certain level of monitoring. As banks’ monitoring effort serves to deter entrepreneurs

from choosing an inefficient project, whenever a bank exercises market power it is able to

extract part of the incremental surplus created by monitoring (through more efficient

investment decisions). Market power thus acts like an implicit equity stake and serves to

reduce the bank’s own moral hazard problem – that of underproviding costly monitoring

effort ex post. From this perspective a monopolist bank has first-best monitoring incentives as

it is able to appropriate the full project surplus. This idea is formalised in Caminal/Matutes

(2000). There is a trade-off to be taken into account in that increasing bank market power

leads to increasing bank monitoring and thus more efficient allocation of credit and higher

credit availability. On the other hand, bank market power increases loan rates and makes the

incentive problems more severe, forcing the bank to ration credit in order to deal with

borrower moral hazard. As a result of these countervailing forces, the effect of bank market

power on social welfare crucially depends on the severity of the informational asymmetry

between banks and borrowers. However, bank market power is expected to increase

monitoring incentives when information acquisition is costly and the bank cannot commit to a

certain level of monitoring.11

The literature considered so far predicts that there is a positive correlation between

bank market power and banks’ costly information acquisition activity. What makes our

empirical contribution interesting is that other papers contradict this widely held view in that

they predict increasing informational intensity when banking markets become more

competitive.

The paper by Boot/Thakor (2000) adds a new perspective by analysing a bank’s

choice between different informational intensities in the loan products they offer within a

model of imperfect bank competition. The model is basically one of technology choice within

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 9/43

9

a framework of product differentiation. Boot/Thakor then show that increasing interbank

competition could make information-intensive lending practices more attractive and for

certain levels of bank competitiveness even dominate pure transactional lending over the full

range of borrower types. This result rests mainly on the idea that, given increasing

competition from other banks, relationship lending allows heterogeneous banks to partly

insulate themselves against this pressure by offering a more differentiated product.12

After discussing the theoretical work that forms the basis for our empirical study,

several remarks are in order here: Firstly, our study is interested in bank behaviour given bank

market power – of which we believe information acquisition is a central aspect. Thus, this

paper regards bank market power as being exogenous. The question of how the qualitative

aspects of bank-borrower relationships that we address here feed back into banking market

structures obviously goes beyond the scope of our study.13

We will come back to this point in

section 3.7 below.

Secondly, the equilibrium bank behaviour in which this paper is interested should not

be confused with more explicit forms of bank-borrower relationships. It seems important to

make this point clear: The influence that bank market power might have on banks’

information acquisition does not preclude the possibility that some firms might voluntarily

offer banks a type of information monopoly precisely in order to overcome perceived credit

availability problems.14

Given our theoretical discussion above, one external determinant of

these problems (i.e. one that lies outside a firm’s own characteristics) could be bank market

power or a lack thereof.15

Thus, whenever firms can feasibly commit to a long-term

relationship with a bank to overcome credit availability problems caused by bank market

power, our tests would be biased against finding any effect of bank market power on

information gathering, whatever the direction of that relationship might be.16

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 10/43

10

Given the theoretical literature surveyed above, another point deserves to be

mentioned: In Boot/Thakor (2000) a distinction is made between competition from banks and

competition from the capital markets, e.g. from investment banks acting as underwriters in the

corporate bond or commercial paper markets. For the design of our study we can safely say

that, for the sample of small and medium-sized German firms in our analysis, capital market

sources of finance during the sample period were hardly a viable alternative to bank loans. In

Germany, for example, only large firms had access to the commercial paper market or the

market for longer-term bonds and the German market for corporate bonds was thin by any

measure. Descriptive statistics from our sample firms confirm this prior as more than 85% of

all firms that wanted to raise debt financing turned to banks to apply for a loan17

. As the

empirical study relies on the cross-sectional variability of local bank market structures in

Germany it is primarily aimed at measuring the effects of interbank competition on banks’

incentives to invest in relationship-specific information and thus to form strong ties to their

borrowers.

II The empirical study

A Design of the study

Using survey data from small and medium-sized manufacturing firms, this study is in

a unique position to directly measure information flows from firms to banks within a loan

application situation. The study derives two measures to capture the amount and structure of

the information transmitted. We then endeavour to explain this flow of information within a

regression framework and control for firm characteristics, loan variables and standard

relationship variables. We are primarily interested in the relationship between local bank

market structure on the one hand and the information flow on the other. The German banking

market seems to be an excellent terrain for investigating the relationship between information

acquisition and bank market structure. Firstly, the German financial system is often referred to

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 11/43

11

as a classical example of a so called bank-based system, where universal banks play a

dominant role in nearly every segment of the financial market and have built strong ties to the

corporate sector. Secondly, the German banking system, like other continental European

banking markets, was often said to be characterised by collusive behaviour and regulatory

capture, but is now expected to become more competitive as the deregulation and integration

of European financial markets progresses.18

Thirdly, the German banking system is regionally

segmented into many small local markets and thus offers a wide variety of local market

structures which seem to be the relevant market at least for the medium and small sized

segment of the corporate loan market. This latter point is widely recognised as being

applicable to the US banking market, as indicated by the use of local market structure

variables in empirical banking studies.19

It is however neglected in most empirical studies of

European banking markets.

The first step of our analysis, as described above, is to seek to ascertain the

determinants of banks’ information acquisition within the normal course of a business

relationship. As a second step, the data set allows us to consider what could be termed a

natural experiment on the hypothesised market structure/information relationship. For

example, if it is true that banks in more concentrated markets systematically acquire more

information in the normal course of a business relationship, these banks should be able to

provide liquidity at short notice without inducing additional costly transfer of information and

vice versa. As a consequence, the aforementioned correlation between market structure and

information transmission should be reversed in sign for a subsample of firms that have

experienced a liquidity shock and as a consequence demand short-term liquidity. This effect

might be especially important because information transmission from a borrowing firm to a

lending bank within a distress situation might be seriously prone to cheating behaviour on the

part of the firm. Information collected in the past might thus prove to be an extremely helpful

and reliable input into the bank’s decision making when confronted with a borrowing firm’s

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 12/43

12

short-term liquidity needs. Whenever a borrowing firm demands liquidity at short notice, the

bank needs to distinguish between at least two likely explanations for the firm’s current

financial position. On the one hand, the firm might have experienced a drain of liquidity that

has relatively little effect on its prospects and thus its ability to make interest and principal

payments in the future. On the other hand, the liquidity shortage that the firm is currently

experiencing might simply be an indication that the firm is low quality and doomed to fail

anyway. The bank’s position here is that of being exposed to the risk of throwing good money

after bad . Obviously a bank that has acquired more borrower-specific information in the past

should be better able to see through the veil of the firm’s current financial position and assess

its prospects more accurately. As a consequence, less additional information is needed in a

situation where information transmission is especially costly and extremely prone to cheating

behaviour on the part of the firm. Furthermore the timeliness of a bank’s decision might be

crucial in such a scenario and the aspect of the costs to be borne by the firm should not be

neglected, especially if it is a small one and managerial capabilities are a scarce resource.

Note here that the design of the empirical study critically hinges on the distinction

between, on the one hand, information transmission during normal lending business and on

the other, informational requirements that allow banks to provide liquidity services to their

loan customers under exceptional circumstances in which qualitative aspects of the bank-

borrower relationship that have been built up in the past come to bear. Note further that recent

assessments of the functions that commercial banks perform emphasise their funding of

opaque, complex positions based on acquiring borrower-specific information on the one hand

and the provision of liquidity services to their customer on the other.20

Obviously these two

functions are deeply interrelated in that it is the information acquired that make banks a

unique low-cost source of liquidity.

In the third step of our empirical analysis we assess whether the informational

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 13/43

13

intensity within lending relationships addressed in the first part of the analysis has

consequences in terms of firms’ financing patterns. We therefore use information on the

degree to which firms take advantage of early payment discounts as an approximation of the

availability of credit. This last step is a reappraisal of Petersen/Rajan’s (1995) study, using

German data, insofar as we too measure the impact of bank market structure as a determinant

of credit availability. The results that we obtain in this third step of our analysis are similar to

the US findings, but the first two steps of the study offer an explanation for a relationship

between credit availability and bank market power that directly focuses on banks’ information

acqusition.

B The data set

The data set used in this study is from the IfO Institute for Economic Research in

Munich, a leading economic research institution in Germany. In addition to its regular

Investment Survey, IfO conducted a Survey on Corporate Finance in 1997. A questionnaire

was sent to 4,833 manufacturing and construction firms spread all over Germany. As the aim

of the questionnaire was to assess the circumstances and motives of firms’ external financing

decisions, the first part of the survey dealt with equity financing whereas the second part

asked for the firm’s last attempt to raise debt financing. Note that the sample was limited to

firms in the manufacturing or construction sectors only, and is thus quite homogenous. We are

primarily interested in those firms that approached a bank to apply for a bank loan.

Among the 1,531 units that remained after elimination of all firms with incomplete data, we

identified 403 that applied for a bank loan in 1996.

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 14/43

14

C. Information flow variables

Among other things, firms were asked for a list of information items that they had to

submit to the lending bank. Several items – among them cash flow projections, short term

financial statements, feasibility studies or long-term strategies – were offered as a pre-

specified category. Firms could also indicate other items, if any additional information was

transmitted. The firms’ answers to this question serve as a basis for our measure of

information flow to the bank. Our first variable, called INFOCOUNT, is designed simply to

count the information items reported. The assumption here is that a bank’s information

acquisition is a latent unobservable variable and mapped onto an ordinal scale represented by

INFOCOUNT. Obviously this measure is not without its problems. For example, the actual

informational content of the items considered here might overlap.

Our second measure therefore tries to capture the qualitative aspects as well as the cost

aspects that form the basis of the theoretical underpinnings of the empirical study. Here we

draw a distinction between what we refer to as “hard” information and “soft” information

items. Roughly speaking, hard information is defined as information that comes in numbers,

that could be processed automatically, benchmarked against industry averages or comparable

firms. Furthermore this type of information could generally be fed into analytical models, like

discriminant analysis, that are widely used by German banks. In contrast, soft information

could in general not even be reported in standardised fashion as it requires a firm’s managers

to report on their products, customers, investment projects and strategies.

We believe that this distinction is directly related to the cost aspects that drive the

theoretical models discussed above, in which information acquisition was modelled as a sunk

cost investment in bank-customer relationships. The assumption here is that soft information

is more costly to evaluate. We therefore define a second alternative information flow variable

that – as an ordered category – takes the value of 1 when only hard information items are

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 15/43

15

transmitted and the value of 2 whenever, in addition, soft information items are transmitted.

Interestingly, in only 17% of all cases does a bank acquire only soft information, without

acquiring hard items at the same time. This observation might be an indication that the

ordering we have in mind is indeed real. For those observations where only soft information

items are transmitted one could assign INFOSTRUCTURE a value of either 1 or of 2. The

results reported below were achieved when we assigned a value of 1, but using the alternative

method does not change any of our results. We take as a base group those firms which

transmitted balance sheet information only. This is a statutory requirement for all loans larger

than DM 100,000 and is also stipulated in nearly every bank’s internal credit standards,

irrespective of loan volume, so that it does not provide us with any incremental information.

For this base group the variable INFOSTRUCTURE takes a value of 0. We believe that

INFOSTRUCTURE enables us to capture qualitative differences in rating styles among banks

as well as the cost implications of those styles, which are of theoretical interest.

D. Descriptive statistics

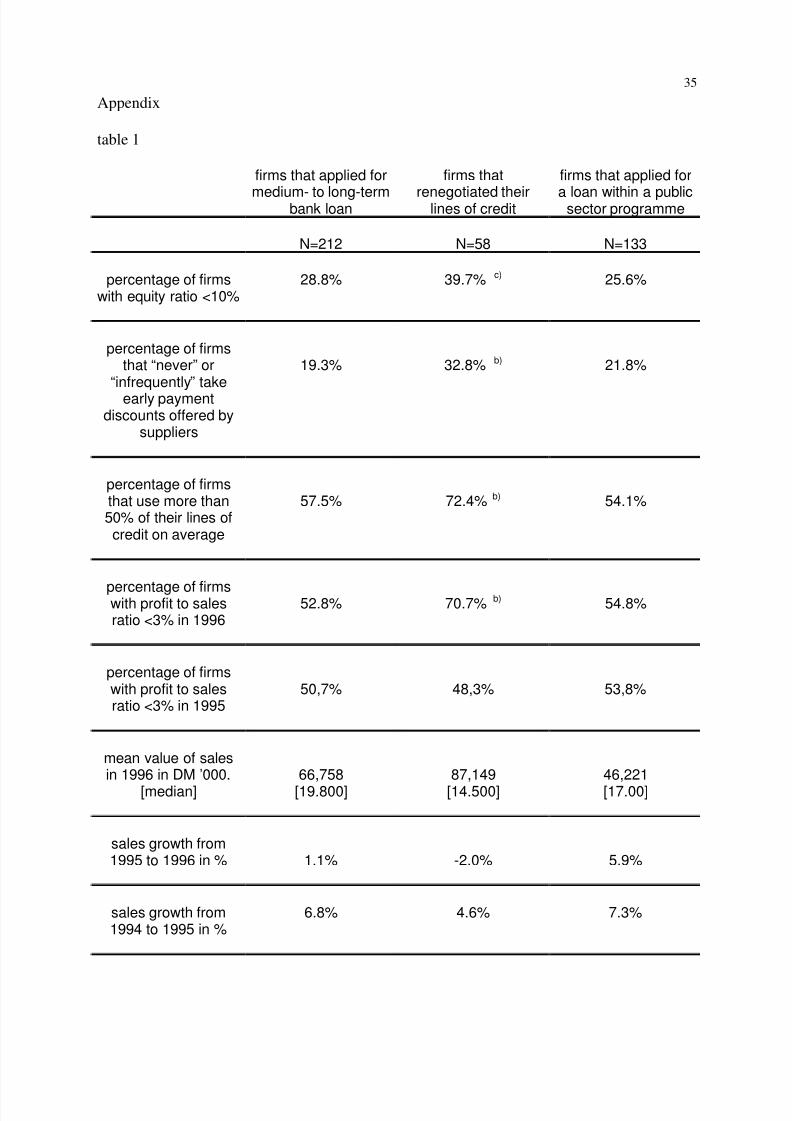

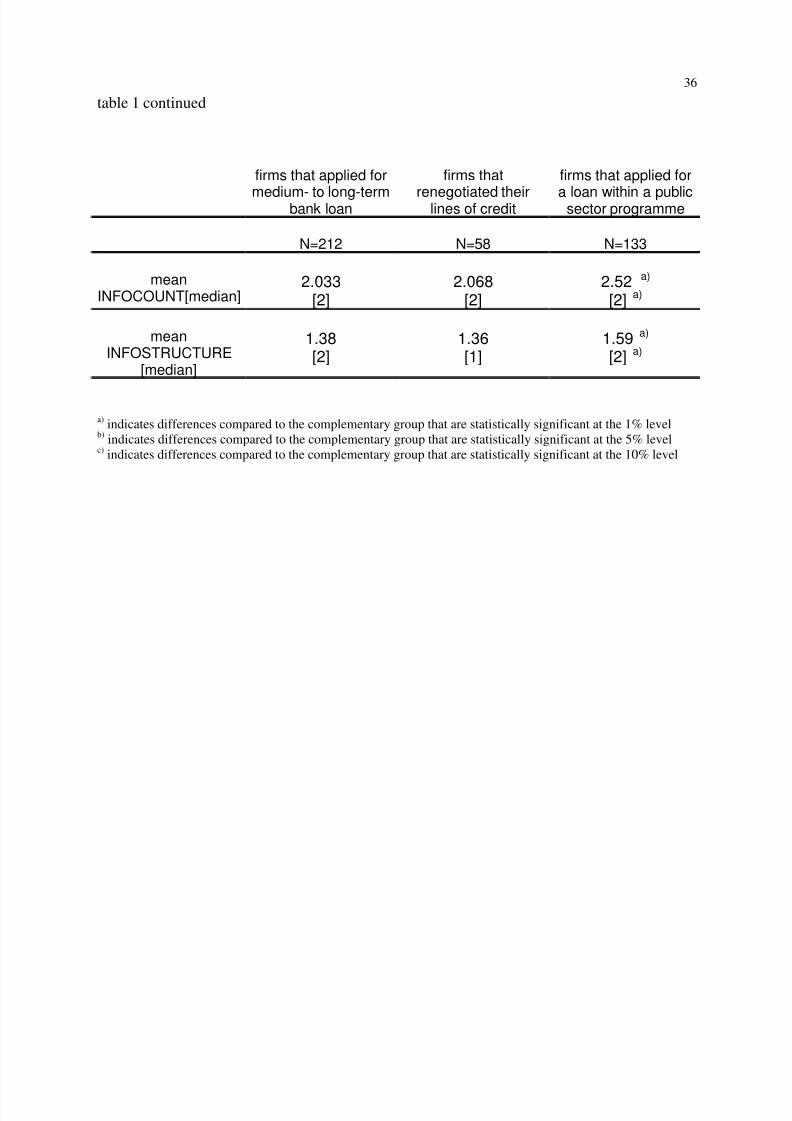

In table 1 we present descriptive statistics for three subsamples that were differentiated

according to the type of loan the firm applied for. 212 firms applied for a medium- to long-

term bank loan, 58 firms renegotiated their lines of credit and 133 firms applied for a loan

under a public sector loan programme, the most prominent of which is the ERP programme, a

successor to the former Marshall Aid Fund. It is important to note here that a line of credit in

Germany takes the form of a transaction account with an overdraft facility. A line of credit

thus is a classical bank product that provvides a loan customer with liquidity services21

.

[table 1 around here]

Firstly it shows that firms that renegotiated their lines of credit are in a poorer

financial position than firms in the other two groups. Differences in terms of early payment

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 16/43

16

discounts taken are statistically significant for that group as compared to the other groups.22

The same holds true for the degree to which firms use their lines of credit on an annual

average basis. Furthermore the sales growth figures point to the causes of these differences in

liquidity position. Firms that renegotiated their lines of credit in 1996 experienced negative

sales growth from 1995 to 1996 on average. This stands in sharp contrast to both other groups

but is not statistically significant (p-value: 0.1518). If one looks at the sales growth figures

lagged one year, no such significant difference can be found. The same time pattern can be

observed if one looks at the percentage of firms that have a profit-to-sales ratio below 3%.

The percentage of firms with low profit-to-sales ratios is significantly higher in 1996 (p-value:

0.0153) among those that renegotiated their lines of credit although this difference does not

show up in the 1995 data. The evidence presented in table 1, together with our general notion

and priors about firms’ motives to renegotiate their lines of credit, leads us to conclude that

firms in that group have on average experienced a liquidity shortage and turn to their banks in

order to demand liquidity at short notice23

. We have already drawn attention to the importance

of this assumption for the design of our study (see above). Banks are assumed to perform a

distinct function in these cases as they provide liquidity services to their loan customers.

Another important result emerges from table 1. In our regression analysis below we

disregard those firms that applied for a bank loan provided under a public sector loan

programme (results for that group are displayed in the fourth column of table 1). In these

public sector programmes, banks merely pass on loans originated by a state-owned bank such

as KfW,24

a federally owned bank that originates loans under the so called ERP programme.25

In some of these cases the bank approached by the borrower does not even bear the full credit

risk inherent in the loan. Furthermore, and even more importantly for our purposes here, one

has to take into account that the informational requirements of loan applications in such a

programme are determined outside the bank-borrower relationship, e.g. in the loan

programme’s guidelines.26

As a consequence of these two fundamental weaknesses, we

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 17/43

17

exclude these 133 firms from our sample. Table 1 shows that in terms of information items

transmitted the subsample is significantly different from the other two groups.

Wilcoxon/Mann-Whitney tests for two subgroups strongly reject the null when firms in this

group are compared to all other firms (p-value: 0.0019). Significant differences are also

displayed in terms of mean values for INFOCOUNT and INFOSTRUCTURE in table 1. It is

thus obvious that information flows within that subsample are quite different, confirming our

priors that other mechanisms are at work here.

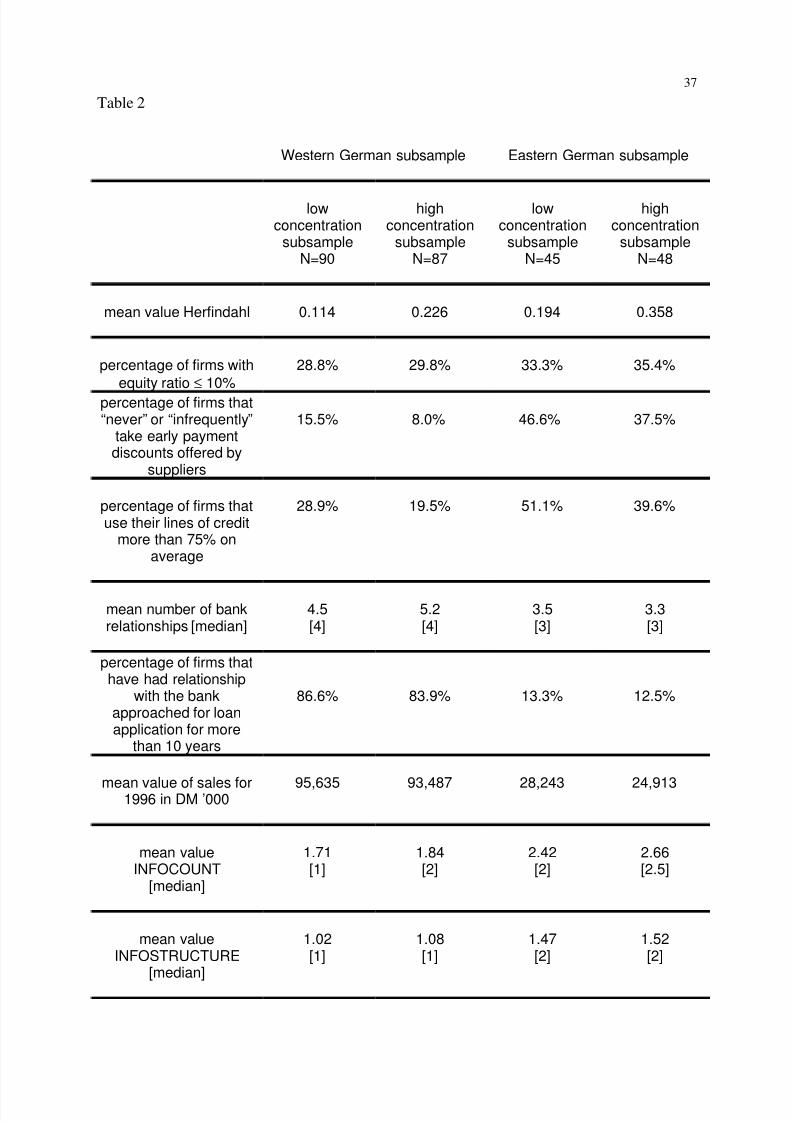

Our next step is to assess whether firms located in more concentrated banking markets

are different from firms in highly competitive bank market areas. As bank market

concentration serves as a key variable in our study, this is an extremely important question to

ask. Table 2 therefore provides descriptive statistics and allows us to analyse whether marked

differences exist between firms from the more concentrated markets and their counterparts

located in more competitive markets. In addition to a sample split by market concentration we

found it important to look for differences between firms located in eastern and western

Germany. Besides likely differences in age, size, industry and financial position this

distinction is also recommended for our purposes, because banking markets in eastern

Germany are significantly more concentrated than local banking markets in western Germany.

Note that to obtain the results displayed in table 2, all observations with public sector loans

had already been eliminated; they will not be considered in what follows.

The general structural difference in terms of market concentration is mirrored in our

sample (the mean value of the Herfindahl is 0.169 for western Germany and 0.279 for eastern

Germany). Thus in order not to bias the interpretation of the descriptive statistics in table 2 we

decided to split the sample into eastern and western German subsamples.27

In most cases,

there are statistically significant differences between the eastern and western German

subsamples in terms of the firms’ characteristics given in table 2 (except for equity ratios).

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 18/43

18

Within these subsamples, however, the differences between firms located in high

concentration banking markets and those in low concentration banking markets are never

statistically significant at conventional levels. Nevertheless an interesting result applies to

those variables that are often interpreted as indicators of firms facing liquidity constraints.

Nearly twice as many firms in low concentration markets reported that they “never” or

“infrequently” take early payment discounts offered by their suppliers. Remember that

Petersen/Rajan (1994, 1995) used early payment discounts taken by their sample firms as an

indicator of credit availability. Given our small sample sizes, the difference based on high and

low concentration subsamples turns out not to be significant at conventional levels for

western German firms (p-value 0.124) and a similar conclusion can be drawn for eastern

German firms. With respect to early payment discounts it is important to note that our sample

is composed entirely of firms from the manufacturing and construction sector and all sample

firms are regularly offered early payment discounts by their suppliers.28

Moreover, the use of credit lines follows a similar pattern to the use of early payment

discounts: Here 28.9% of the firms located in the more competitive markets subsample

reported that on average over the year lines of credit are drawn by more than 75%, whereas

only 19.5% reported comparable use of their lines of credit in the more concentrated markets

(p-value 0.1488). For both variables, the figures for eastern Germany show the same pattern

(fewer firms are liquidity-constrained in the high concentration subsample), although again

the differences are not statistically significant at conventional levels. We will, however, return

to these differences in the third step of our empirical study, where we do not restrict the

analysis to those firms that applied for bank loans in 1996 but use the full sample of firms

within a multivariate framework. For the moment we are interested in the determinants of

bank information acquisition activity, which we are attempting to measure by INFOCOUNT

and INFOSTRUCTURE. As indicated by the last two rows of table 2, there seem to be

marked differences between eastern and western Germany in terms of information acquisition

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 19/43

19

by banks. Again, differences based on market structure split within these subsamples seem to

be of no statistical significance although they are always higher in the high concentration

subsamples.

[table 2 around here]

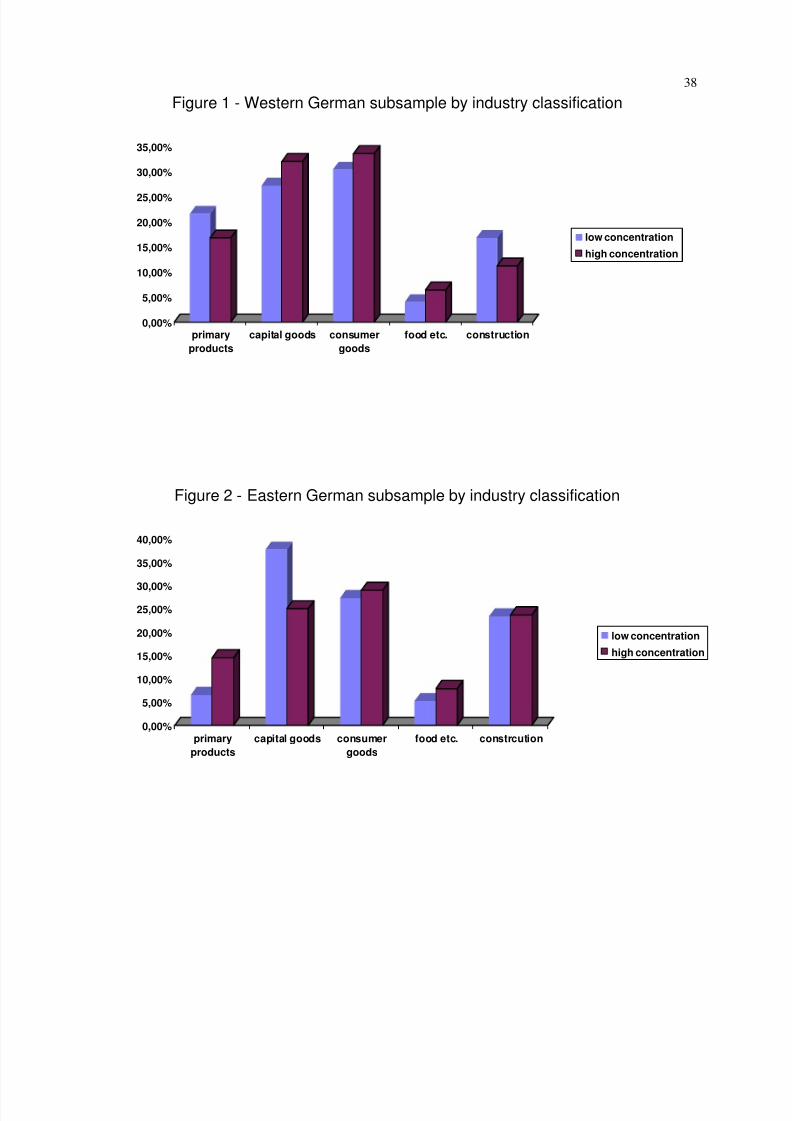

Like Petersen/Rajan (1995) we also checked for the industry composition of our

sample. This might be important because industry is a good proxy for business risk and

tangibility of assets, aspects that are likely to influence a bank’s perception of credit risk.

Figures 1 and 2 show the western German and eastern German subsamples according to the

firms’ industry classification. Here again we do not find marked differences between firms in

low concentration and firms in high concentration markets.

[figures 1 and 2 around here]

E. Regression results

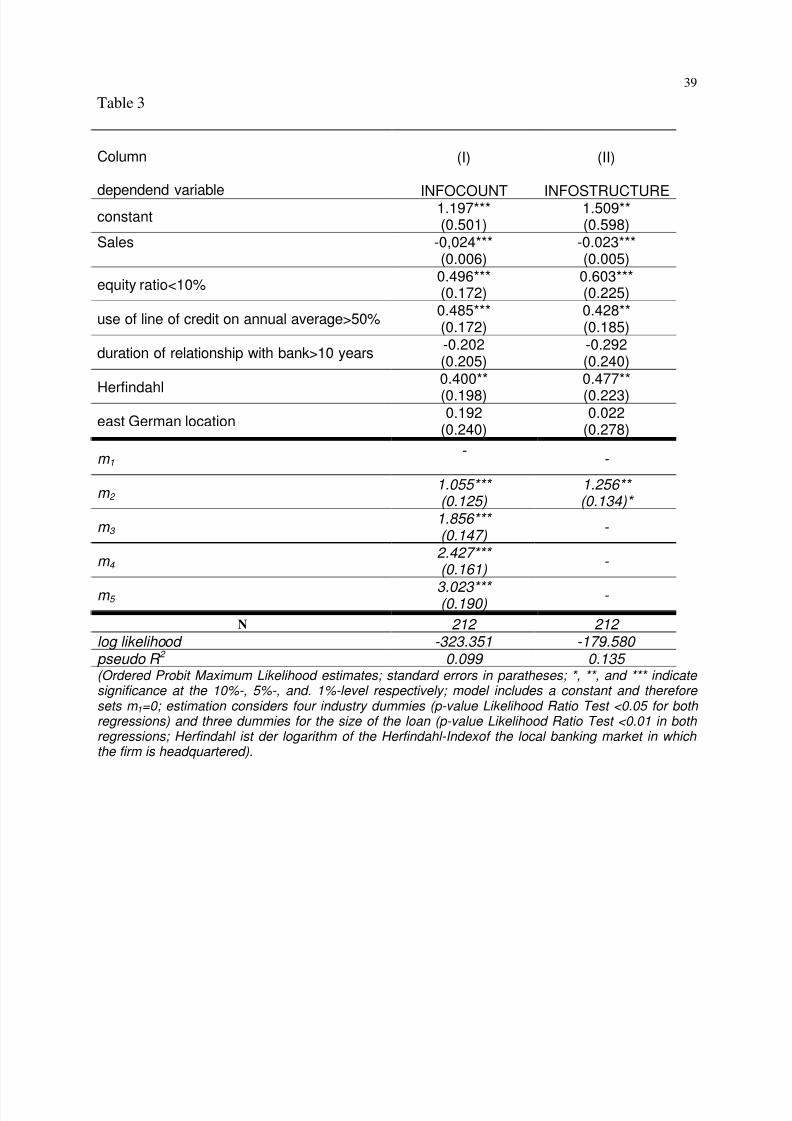

We now study the determinants of the flow of information within a regression

framework. Table 3 displays ordered probit maximum likelihood estimates of the vector of

coefficients for a parsimonious specification for INFOCOUNT and INFOSTRUCTURE as

dependent variables. These specifications serve as our baseline model, and we report an all

extensions and robustness checks below.

A comparison of the results in column I and II of table 3 shows that they are almost

identical for INFOCOUNT and INFOSTRUCTURE as dependent variables. More precisely,

size – as measured by sales – seems to be a major determinant of banks’ information

acquisition activity. Estimated coefficients are negative and highly significant in all

regressions. From a theoretical perspective this is not very surprising, as size is often

interpreted as a proxy for informational problems in that smaller firms face more serious

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 20/43

20

information problems when contracting with their financiers. As banks are seen as specialists

in bridging that informational gap by costly information gathering activity, one should not be

too surprised to see banks producing more information when granting loans to small firms.

Note, however, that we controlled for loan size by introducing three dummy variables. If the

loan size variables actually measured firm size effects, sales should not show up as being

significant. Accounting for loan size seems to be important, as indicated by the results of

Likelihood Ratio tests, but the relevance of size carries over to those specifications where loan

size is not controlled for. On the other hand, controlling for loan size in our baseline

regressions is motivated by the fact that most banks’ internal credit standards require more

information acquisition with larger loan volumes.29

As these internal credit standards are rigid

over time and not adjusted on a customer by customer basis, it seems appropriate to control

for this effect.

A firm’s financial position seems to impact bank information gathering activity in the

sense that firms that are in a poor financial position have to disclose more information to their

potential lenders. The coefficient for the dummy variable indicating whether the firm’s equity

ratio is below a 10% threshold is positive and significant in all regressions. The same holds

true for a dummy variable indicating whether the firm uses more than 50% of its line of credit

on an annual average basis. As an alternative to the latter we also used a dummy variable that

was assigned a value of 1 whenever the firm never or rarely took advantage of early payment

discounts offered by its suppliers and zero otherwise. This variable yielded qualitatively

identical results. In the brief literature survey above it was already mentioned that in theory as

well as in empirical studies of bank-borrower relationships the notion of learning-by-lending

plays a prominent role in the modelling of bank information acquisition. The duration of the

bank-borrower relationship is therefore often used as a metric for informational intensity in

relationship lending. Taking account of the duration of the relationship therefore seems to be

extremely important. Specifications reported in table 3 used a dummy variable indicating

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 21/43

21

whether the firm had a relationship with the bank for more than 10 years. Estimated

coefficients have the expected sign but are not statistically significant. As the questionnaire

allowed us to partition the sample into 5 groups according to the duration measure30

we also

used groups of dummy variables in alternative specifications. Joint tests could reject the null

in these cases and, perhaps even more importantly, the signs were always as expected. Overall

we come to the conclusion that the information that a lending bank naturally accumulates over

time has an impact on information acquisition activity. However this paper argues that the

duration of bank-borrower relationships is not a sufficient metric to capture banks’ incentives

to gather borrower-specific information. The important question raised in this paper is

whether bank market structure – proxying for bank market power – is a determinant of banks’

information acquisition activity. We therefore included a measure of local bank market

concentration in our regression equations. As market share information for bank loans and

deposits is generally not available in Germany, we constructed concentration measures based

on branching information. Denote by MSi,j bank i’s market share in local market j. We

approximated MSi,j by the number of branches that bank i operates in j divided by the total

number of bank branches operated in market j. A local market on the other hand is identical to

a specific administrative regional unit. From this market share data we constructed a

Herfindahl index by squaring individual banks’ market shares and totalling them up. Several

alternative concentration measures were also computed and used in the regressions (see 3.6

below). Table 3 shows that local bank market concentration has a statistically significant

impact on information transmission activity.31

Results with respect to bank market structure

are extremely robust and statistically significant at conventional levels. They lead us to the

central empirical finding of this paper, that of a positive market concentration/information

acquisition relationship in bank loan markets.

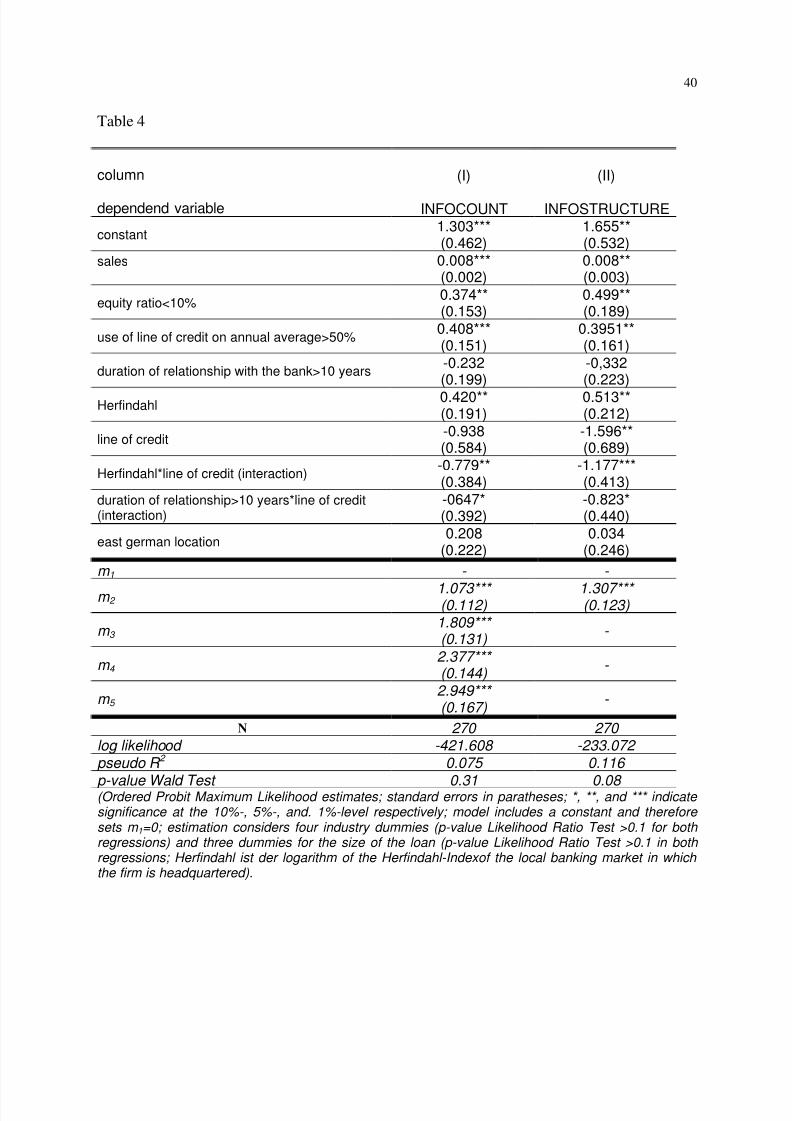

To further investigate this relationship, we conduct something like a natural

experiment . The point here is to explore whether having collected more information in the

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 22/43

22

past enables banks to provide their customers with liquidity at short notice. It is here that

those 58 firms that re-negotiated their lines of credit come into play.32

We therefore re-

estimated the specifications of table 3, simply adding those 58 firms and controlling for

specific effects of that group with respect to INFOCOUNT and INFOSTRUCTURE. The

results are displayed in table 4. To be more precise, we added a dummy variable RLC

indicating whether a firm renegotiated its line of credit. We also added two interaction terms

RLC*Herfindahl and RLC*duration>10. For both terms we expected a negative sign for

reasons set forth above. We introduced RLC*duration>10 into the specification as a check of

plausibility because the natural accumulation of borrower-specific information that occurs

over time might be relevant in situations where borrowers require liquidity, although it

seemed to have no statistically significant impact in normal times. When we interact

Herfindahl with RLC we interpret this as our natural experiment of our first hypothesis of

more information acquisition in more concentrated banking markets; when we interact RLC

with duration>10 we try to provide another check of plausibility as banks that have a longer

relationship with their loan customer should be able to provide liquidity at lower cost. Again

Column I of table 4 displays results obtained for INFOCOUNT as a dependent variable and

column II shows results for INFOSTRUCTURE.

Firstly, all results obtained in our first regressions (table 3) appear also to be valid for

the extended sample. The estimated coefficients for Herfindahl still appear to be positive and

highly significant. Coefficients for both interaction terms have a negative sign and are

themselves highly significant. For INFOCOUNT a Wald-Test cannot reject the null that the

overall effect of market concentration on information acquisition is zero for the RLC group,

although this combined effect has a negative sign. For INFOSTRUCTURE however the null

hypothesis is rejected at conventional levels in all specifications that we estimated. The

coefficient for the RLC dummy is negative, which must be interpreted as follows: Given the

model’s predictions about the effect of equity ratio and liquidity status on the information

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 23/43

23

variable, renegotiations of credit lines are less information-intensive transactions than

applications for long and medium term loans.

F. Robustness/Extensions

Tables 4 and 5 present estimation results for parsimonious specifications. Therefore

considering extensions and checking the robustness of our results seems to be a natural and

important exercise. We performed these extensions for both our first-step regression

(excluding renegotiated lines of credit and interaction terms) as well as for our second-step

regressions (including renegotiated lines of credit and interaction terms). Here we briefly

report on the results obtained:

Eastern German localisation

Given the descriptive statistics in table 2 it seems natural to control for firms headquartered in

the eastern part of Germany as information transmission seemed to be more intensive there.

We did so by introducing a dummy variable into our regression equations. In not a single case

could we reject the null of the estimated coefficient being equal to zero. Estimated

coefficients were highly insignificant so that appropriately accounting for a firm’s financial

position seemed to leave no room for a separate eastern Germany effect. Furthermore, none of

the qualitative results reported in tables 4 and 5 were affected.

Industry classification

We controlled for industry by using a five-group industry classification. We also used more

differentiated industry classifications but that had no effect on the results reported. However,

controlling for industry seemed to be important, as indicated by Likelihood Ratio tests.

Local credit risk

Local banking markets might differ with respect to measures of aggregate credit risk that

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 24/43

24

could not be accounted for by industry classification or the firm’s financial position. One

could think here of a purely local risk measure that is able to capture systematic risk factors

that are relevant only locally. Consider, for example, the possibility that a default by a large

firm might spill over to local suppliers, which might be affected as unsecured creditors of that

firm. We follow Berlin/Mester (1999) in using the local market’s rate of unemployment and

alternatively its one-year lag as a proxy for local credit risk. In no case did the estimated

coefficients show up to be statistically significant nor did any of our results change after

considering local unemployment.

Regional classification

Surprisingly, whether local markets were classified as rural, suburban or urban has no effect

on our measures of market concentration. Mean and median values for Herfindahl or CR3 are

nearly identical if one groups markets according to a regional classification. Nevertheless, we

controlled for regional effects by introducing dummy variables for rural and suburban areas

(taking urban areas as our base group). We find information acquisition to be more intense in

rural areas; estimated coefficients are marginally significant in most specifications. More

limited diversification possibilities in more rural areas could be one explanation for this result.

From this perspective, information acquisition and portfolio diversification might appear to be

alternative mechanisms to control portfolio credit risk. Note here that local banking markets

are dominated by banks that do business only in the specific region where they are

headquartered.33

Because this aspect raises more serious problems for our study we will refer

to it in section 3.7 below.

Firm age, limited liability, industrial group

We also controlled for firm age (using firm age in years as well as the logarithm of firm age in

years) and whether the firm is a corporation acting under limited liability. For the age variable

we censored the observations by restricting the variable to a maximum of 30 years. This was

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 25/43

25

done in order not to bias our results because of some outliers in the sample. Furthermore we

introduced a dummy variable indicating whether the firm belongs to an industrial group. The

liability and group variables might proxy for important aspects of bank’s perceived credit risk.

None of these firm characteristics entered our regressions significantly. Even more important,

considering these variables in our specifications did not alter any of the results reported so far.

Stated purpose

For obvious reasons, it seems to be extremely important not only to control for the firm’s

current financial position, industry and size but also for the incremental investment to be

financed by the loan in question. We have good information on the stated purpose of the

financing. This leads us to introduce a vector of dummy variables indicating whether the loan

will be used for, say, R&D activity, acquisitions, replacement investment, and the like.

Interestingly, results of Likelihood Ratio tests indicated that controlling for purpose is

important in those specifications that use INFOCOUNT as a dependent variable but not for

those using INFOSTRUCTURE. Consistent with our priors with INFOCOUNT as a

dependent variable we find significant effects for acquisitions, growth investments and

rationalisation investments. However none of the results reported in tables 4 and 5 changed by

taking account of stated purposes.

Collateralisation

We have information on whether the bank required collateral to be posted for the loan in

question. Controlling for collateralisation requirements as a binary variable or the type of

collateral to be posted does not have any significant effect on our results. However, our

method of controlling for collateral is incomplete here as we do not have information on the

total degree of collateralisation for all loans taken by the firm, which seems to be much more

important in our case.

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 26/43

26

Number of bank relationships

Given the overall perspective of the analysis it is quite interesting to control for the number of

bank relationships a firm has. On the one hand this is often used a proxy for the intensity of

the bank-borrower relationship – the more exclusive the relationship, the more intense the

relationship is expected to be – on the other hand it could also proxy for inside competition as

opposed to outside competition measured by market concentration. Although the number of

bank relationships never turns out to be statistically significant in our regression, a dummy

variable indicating whether the firm is a one-bank firm (the firm has only one bank

relationship) is robustly negative and highly significant. One should be cautious when

interpreting this finding, because only a few firms (around 5% of all observations) have only

one bank relationship. However a likely interpretation, reminiscent of the “lazy banks” notion

in Manove et al. (1999), is that inside competition might promote information acquisition

whereas outside bank market competition does the opposite.

Alternative measures of bank concentration

As alternatives to the Herfindahl we also considered CR3, the number of banks active in the

market, the ratio of the total number of branches to geographic market size (measured in

square kilometres), and the midpoint between a theoretical upper bound and lower bound for

the Herfindahl given the number of banks in the market.34

The qualitative results were

unaffected by these variations, although significance levels varied slightly but results were

always significant at conventional levels.

G. Caveats: selectivity, endogenous market structure and diversification effects

Several important points deserve mention here. The first has to do with our empirical

methodology: One might argue that results obtained for the chosen group of firms are

seriously biased by an obvious selection problem, namely that the flow of information from

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 27/43

27

firms to banks, which forms the dependent variable in our regression, is only observed for

those firms that applied for a loan in the first place. We will elaborate on this problem shortly.

As the kind of analysis we have in mind simply asks for the probability that the dependent

variable falls into some category of interest, conditional on a vector of covariates, we can only

learn about that probability under the additional condition that a certain event – a loan

application – has taken place.35

Taking that statement seriously means that we could learn

nothing about the probability of interest for those firms that did not apply unless we strongly

assume that the selection that characterises our sample is purely exogenous. As a further

consequence, we could learn nothing about the probability of interest for the whole sample of

firms – unconditional on the event having taken place or not. There are standard methods at

hand that try to account for selectivity by posing strong assumptions about the joint

distribution of the error terms of a selection equation to be estimated and the equation of

interest. We will not report the results obtained with these methods here, although there is a

strong indication that our main qualitative results are indeed unaffected by taking account of a

selection process shaping our data. In particular, we strongly believe that loan application

situations are special in that an intensive exchange of information takes place. By this we

mean that even if one restricted one’s interpretation of our results solely to the group of firms

that actually apply for a loan, one could still learn something about the determinants of banks’

information acquisition activity.

In interpreting the results two other problems arise which we would like to discuss

briefly. Firstly, as already mentioned above, information acquisition might be seen as an

alternative to portfolio diversification as a means of controlling portfolio credit risk. The

information acquisition/market structure relationship that we measure might thus be shaped

by reverse causality in that markets with lower diversification opportunities show higher

concentration. It is important to note here that an overwhelming majority of German banks are

only doing business in a limited regional market, often identical to the market areas that we

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 28/43

28

use in this study to identify local banking markets. This is not only true for all public sector

savings banks but also for mutual banks and a considerable number of private bankers and so-

called regional banks. We tried to control for portfolio effects by inserting a proxy measure

for diversification in our regression equation, very much like a concentration index. This

measure was based on sectoral shares of value added in that specific region. However only

rough sectoral information was available (agriculture, services, manufacturing, trade and

transport). In all our regressions this measure turned out to be highly insignificant. As an

alternative we constructed a probably more sensible measure of the diversification potential

within local banking market. This measure is based on the number of employees in a specific

industry in that particular local banking market. Using a classification scheme with eighteen

industries we measured the concentration of employment across industries which might be

proportional to loan demand across industries. Again this measure did not enter our

regressions in a significant way.

A second interpretation of our results that suggests reverse causality is that

information acquisition and building of strong informational ties with one’s customers is a

means to prevent entry. In a recent contribution, Dell’Ariccia et al. (1999) argue that

informational advantages of incumbent banks might be a deterrent to entry into banking

markets. One could think of a scenario where these informational advantages of incumbents

are not exogenous but endogenously determined to form barriers to entry into local markets.

The low rate of direct penetration of banking markets in Europe – even after implementation

of the single market programme and the common currency – is often interpreted as evidence

of informational entry barriers. The design of our study, however, is incapable of uncovering

this type of relationship.

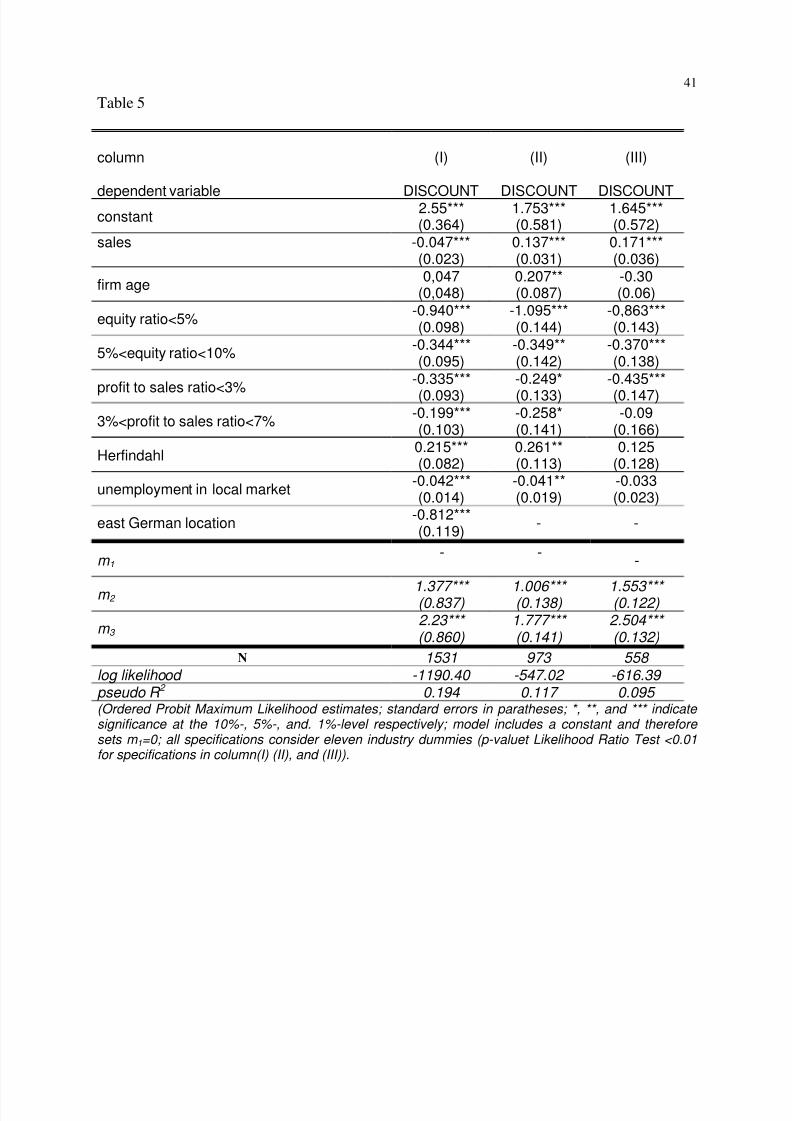

H. Credit availability and early payment discounts

In the last step of our empirical study, we ask whether firms located in more concentrated

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 29/43

29

banking markets are less liquidity-constrained for the reasons discussed above. If in more

concentrated markets banks know systematically more about their clients, there is reason to

believe that they could provide liquidity more easily because incentive problems are better

controlled for. Here we follow Petersen/Rajan (1995) in using information on the share of

early payment discounts taken by the firm as an indicator of credit availability. Within the

questionnaire, firms were asked how often they paid early, thereby taking advantage of

discounts offered by their suppliers. The questionnaire offered 4 categories

(never/rarely/frequently/always) which we take as an ordered category.36

Table 5 shows the

estimation results. Our primary interest here again is in the effect that local banking market

concentration has on the frequency of using early payment discounts offered by suppliers. The

coefficient for the Herfindahl is positive and highly significant in all regressions. Given that

firms’ early payment behaviour is a good indicator of credit availability, these results indicate

that credit is more readily available in more concentrated banking markets. This result is in

line with Petersen and Rajan’s (1995) findings for the local US banking markets. However the

results of the first two steps of our analysis offer a somewhat more focused explanation for

this observation: Petersen and Rajan’s argument points to intertemporal patterns in loan

contracting as a determinant of credit availability. This paper points to another mechanism

that might be important in that it emphasises systematic differences in banks’ accumulation of

borrower-specific information.

Generally, market structure variables seem to be of great importance as shown also by

estimated coefficients for the eastern German dummy, the rate of unemployment and at least

one of the regional dummies. Again the Herfindahl is of primary interest in these regressions.

All other coefficients have the expected sign. Coefficients for firm profitability and equity

ratio as well as sales (again as a size proxy) seem to be significant determinants of credit

availability. We also estimated the specification in table 5 for the western German and eastern

German subsample separately and obtained qualitatively identical results. In both regressions

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 30/43

30

coefficients for the Herfindahl were positive and significant. The overall conclusion from this

last step of the analysis could be summarized as follows: Given that the usage of early

payment discounts by firms is a useful measure of credit availability, credit seems to be more

readily available in more concentrated banking markets. This result is in line with

Petersen/Rajan’s findings for small US firms.37

Unfortunately this study is not able to

distinguish between their explanation for the market power/credit availability correlation and

the one suggested by differences in information acquisition activity.

[table 5 around here]

III. Concluding remarks

In this paper we have argued that information gathering by banks forms the basis for

most of the theory of bank uniqueness. If, however, information acquisition is costly, the

competitive structure of the banking industry might be an important determinant of the

informational intensity of bank-borrower relationships. More recent theoretical assessments of

bank screening/monitoring in loan markets take this into account but offer conflicting

hypotheses about the nature of the impact of bank market structure on information gathering.

Our paper is, to the best of our knowledge, the first attempt to study the market

power/information relationship empirically. We are able to measure information flows from

loan applicants to banks within a loan application situation for a sample of small and medium-

sized German firms. In our study we then try to explain these information flows within a

regression framework. As could be expected, riskier firms and firms that are in a poor

financial position have to disclose more information to their potential lenders when applying

for a loan.

Local banking market structure as approximated by standard measures of market

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 31/43

31

concentration seems to have a considerable influence on banks’ information gathering even if

one controls for loan characteristics as well as for standard relationship variables and market

variables different from concentration. We then ask whether there are situations where cross-

sectional differences in the equilibrium amount of information accumulated in the past might

be of importance in the sense that the transmission of incremental borrower-specific

information might be a substitute for less information acquired in the past. We find banks’

provision of liquidity to their loan customers at short notice to be such a situation. Expressed

the other way around: if a bank has systematically acquired more information in the past, less

additional information is needed to provide liquidity to a borrower that has experienced a

shortage of liquidity. Given the importance that banks’ liquidity provision to borrowing firms

has attracted in recent theories of bank uniqueness, we find this to be a very important aspect

of bank behaviour.

Finally we ask whether, due to superior information acquisition by their lenders, credit

is more readily available to firms in more concentrated markets. Using the share of early

payment discounts taken by the firm as a proxy for credit availability, we find a significantly

positive correlation between bank market concentration and credit availability. This last step

is a reappraisal of Petersen/Rajan’s (1995) study and confirms their findings for US firms.

The first part of our paper, however, offers a somewhat more specific explanation of why this

relationship seems to hold.

To the best of our knowledge, this is the first empirical analysis of a market

power/information acquisition relationship in bank loan markets and a lot more has to be done

in this area to fully understand the implications of recent shifts in the competitive structure of

financial markets. Our results indicate, however, that increasing competitive pressure within

banking markets has a negative impact on banks’ information acquisition and as a

consequence might hamper their function of providing liquidity to borrowers who have

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 32/43

32

experienced a liquidity shock. Taking account of these interrelationships between acquisition

of private information on the one hand and the ability to provide liquidity at short notice on

the other might prove to be extremely important in assessing the welfare implications of

financial intermediary market power.

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 33/43

33

References

Anand, B.N./Galetovic, A. (2000): Information, non-excludability, and financial market structure, in:

Journal of Business Journal of Business 73, S. 357-402

Berger, A.N./Hannan, T.H. (1989): The price concentration relationship in banking, in: Review of

Economics and Statistics, pp. 291-299

Berlin, M./Mester, L. (1999): Deposits and relationship lending, in: Review of Financial Studies

12/3, pp. 579-607

Billet, M.T./Flannery, M.J./Garfinkel, J.A. (1995): The effect of lender identity on a borrowing

firm’s equity return, in: Journal of Finance, vol. L, No. 2, pp. 699-718

Boot, A.W./Thakor, A.V. (2000): Can relationship banking survive competition?, in: Journal of

Finance 55, No 3, pp.679-713.

Caminal, R./Matutes, C. (2000): Can competition in the credit market be excessive?, Working Paper,Center for Economic Policy Research, London

Cetorelli, N. (1997): The role of credit market competition on lending strategies and on capital

accumulation, Working Paper, Federal Reserve Bank of Chicago

Cetorelli, N./Gambera, M. (2000): Bank market structure financial dependence and growth:

International evidence from industry data, Journal of Finance 56, pp. 617-648

Danthine, J-P./Giavazzi, F./Vives, X./von Thadden, E-L. (1999): The future of European banking,

Center for Economic Policy Research, London

Dell’Ariccia, G./Friedman, E./Marquez, R. (1999): Adverse selection as a barrier to entry in the

banking industry, in: RAND Journal of Economics 30, No 3, pp. 515-534

Edwards, J./Fischer, K. (1994): Banks, finance, and investment in Germany, Cambridge University

Press, Cambridge, UK

Elsas, R. (2000): Competition and the determinants of relationship lending, Working Paper,

Department of Finance, University of Frankfurt

Fama, E.F. (1985): What’s different about banks?, in: Journal of Monetary Economics, 15, pp. 29-39.

Fischer, K.H. (2003): Concentration and price in German retail banking - local markets, mergers and

bank interest rates, Working Paper, Department of Finance, University of Frankfurt

Fischer, K.H./Pfeil, C. (2004): Competition and regulation in German banking: An assessment, in:

The German Financial System, J. P. Krahnen and R.H. Schmidt (editors), Oxford University Press,

Oxford/UK.Hannan, T.H. (1991): Bank commercial loan markets and the role of market structure: Evidence from

surveys of commercial lending, in: Journal of Banking and Finance 15, pp. 133-149

Kashyap, A.K./Rajan, R./Stein, J.C. (1999): Banks as liquidity providers: An explanation for the co-

existence of lending and deposit taking, Journal of Finance 57, pp. 33-73

Lummer, S./McConnell, J. (1989): Further evidence on the bank lending process and capital market

responses to bank loan agreements, in: Journal of Financial Economics 25, pp.99-122

Manove, M./Padilla, A.J./Pagano, M. (1998): Collateral vs. project screening: A model of lazy

banks, RAND Journal of Economics 32, pp. 726-744

Manski, C. (1995): Identification problems in the social sciences, Harvard University Press

Mayer, C. (1988): New issues in corporate finance, in: European Economic Review 32, pp. 1167-

1189

Neumark, D./Sharpe, S.A. (1992): Market structure and the nature of price rigidity: Evidence from

the market for consumer deposits, in: Quarterly Journal of Economics, Vol. 107, pp. 657-680

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 34/43

34

Pagano, M. (1993): Financial markets and growth: An overview, in: European Economic Review 37,

pp.613-622.

Petersen, M.A./Rajan, R.G. (1994): The benefits of lending relationships: evidence from small

business data, in: Journal of Finance 49, pp. 3-37.

Petersen, M.A./Rajan, R.G. (1995): The effect of credit market competition on lending

relationships, in: Quarterly Journal of Economics, Vol. 110, pp. 407-443

Rajan, R.G. (1992): Insiders and outsiders: The choice between informed and arms length debt, in:

Journal of Finance 47, pp. 1367-1400.

Rajan, R.G. (1998): Do we still need commercial banks?, in: NBER Reporter Fall 1998, pp. 14-18

Saidenberg, M.R./Strahan, P.E. (1999): Are banks still important for financing large businesses?, in:

Federal Reserve Bank of New York, Current Issues in Economics and Finance

Sharpe, S.A. (1990): Asymmetric information, bank lending and implicit contracts: A stylized model

of customer relationships, in: Journal of Finance 45, pp. 1069-1087.

Vives, X. (1991): Regulatory reform in European banking, in: European Economic Review, Vol 35,

pp. 505-515

Zarutskie, R. (2003): Does bank competition affect how much firms can borrow? New

evidence from the U.S., Working Paper MIT

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 35/43

35

Appendix

table 1

firms that applied for

medium- to long-termbank loan

firms that

renegotiated theirlines of credit

firms that applied for

a loan within a publicsector programme

N=212 N=58 N=133

percentage of firmswith equity ratio <10%

28.8% 39.7% c) 25.6%

percentage of firmsthat “never” or

“infrequently” takeearly payment

discounts offered bysuppliers

19.3% 32.8% b) 21.8%

percentage of firmsthat use more than50% of their lines ofcredit on average

57.5% 72.4% b) 54.1%

percentage of firmswith profit to salesratio <3% in 1996

52.8% 70.7% b) 54.8%

percentage of firmswith profit to salesratio <3% in 1995

50,7% 48,3% 53,8%

mean value of salesin 1996 in DM ’000.

[median]66,758[19.800]

87,149[14.500]

46,221[17.00]

sales growth from1995 to 1996 in % 1.1% -2.0% 5.9%

sales growth from1994 to 1995 in %

6.8% 4.6% 7.3%

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 36/43

36

table 1 continued

firms that applied for

medium- to long-termbank loan

firms that

renegotiated theirlines of credit

firms that applied for

a loan within a publicsector programme

N=212 N=58 N=133

meanINFOCOUNT[median]

2.033[2]

2.068[2]

2.52 a) [2] a)

meanINFOSTRUCTURE

[median]

1.38[2]

1.36[1]

1.59 a) [2] a)

a)indicates differences compared to the complementary group that are statistically significant at the 1% level

b)indicates differences compared to the complementary group that are statistically significant at the 5% level

c) indicates differences compared to the complementary group that are statistically significant at the 10% level

8/8/2019 Ben Me Lech

http://slidepdf.com/reader/full/ben-me-lech 37/43

37

Table 2

Western German subsample Eastern German subsample

lowconcentration

subsampleN=90

highconcentration

subsampleN=87

lowconcentration

subsampleN=45

highconcentration

subsampleN=48

mean value Herfindahl 0.114 0.226 0.194 0.358

percentage of firms with

equity ratio ≤ 10%

28.8% 29.8% 33.3% 35.4%

percentage of firms that“never” or “infrequently”

take early paymentdiscounts offered by

suppliers

15.5% 8.0% 46.6% 37.5%

percentage of firms thatuse their lines of credit

more than 75% onaverage

28.9% 19.5% 51.1% 39.6%

mean number of bankrelationships [median]

4.5[4]

5.2[4]

3.5[3]

3.3[3]

percentage of firms thathave had relationship

with the bankapproached for loanapplication for more

than 10 years