Embed Size (px)

Citation preview

Behavioural Finance and Investment Beliefs

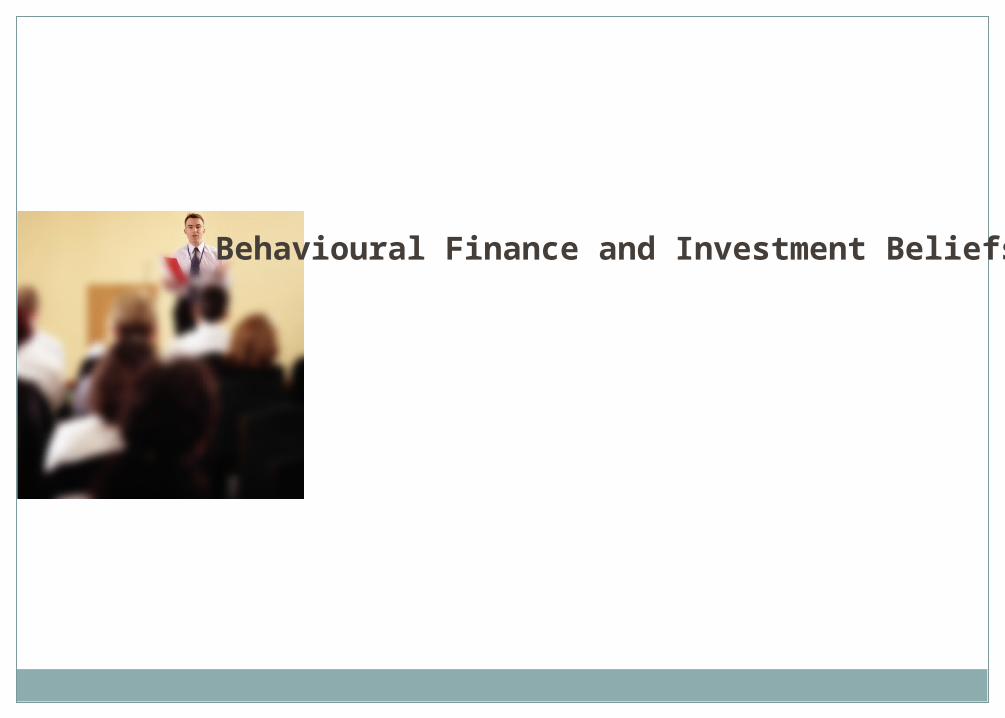

Twin Peaks

1

2

Bubbles

Traditional belief: Financial Markets are efficient, in that they reflect all available information correctly and quickly- Is there an alternative view about the markets?

2

3

Behavioural Finance

Relatively new school of thoughtA marriage of psychology and finance• It says psychology plays a role in financial decision making

Cognitive errors and biases affect investment beliefs, and hence financial choices

Challenges the traditional idea that financial markets are always efficient

3

4

Limits to Arbitrage

Why isn’t mispricing arbitraged away? If there is a significant number of irrational investors, arbitrage is

riskyIf arbitrageurs are risk-averse, their activities will be limited, due

to fundamental risk, implementation costs, and model riskHence, mispricing can exist, particularly in the short term

5

Why Should We Care?

• To better understand our own investment behaviour, and that of others• Set the right incentives for clients, pension plan (DC) design,

financial product design• CIBC Imperial Service: Investor Psychology 101

4

6

Why Should We Care?

To better understand asset management companies that base their investment philosophy on behavioural finance. Examples: The Behavioural Finance group at JPMorgan Asset

Management manages ~ $10 billion “Our behavioural finance funds seek to take advantage of

investor irrationality, capitalising on the anomalies created by investor behaviour to pursue consistent capital growth.”

Value and momentum LSV Asset Management manages ~ $60 billion

Value, long-term contrarian, and short-term momentum

7

Common Behavioural Biases

OverconfidenceLoss aversion

Narrow framingRepresentativeness

Regret avoidanceAmbiguity aversion

Mental accountingAnchoring

6

8

Overconfidence

Better than average

“I am a better than average driver.”

95% of British drivers believe they are better than average (Sutherland 1992)

Illusion of control

“I am unlikely to be involved in a car accident.”

7

9

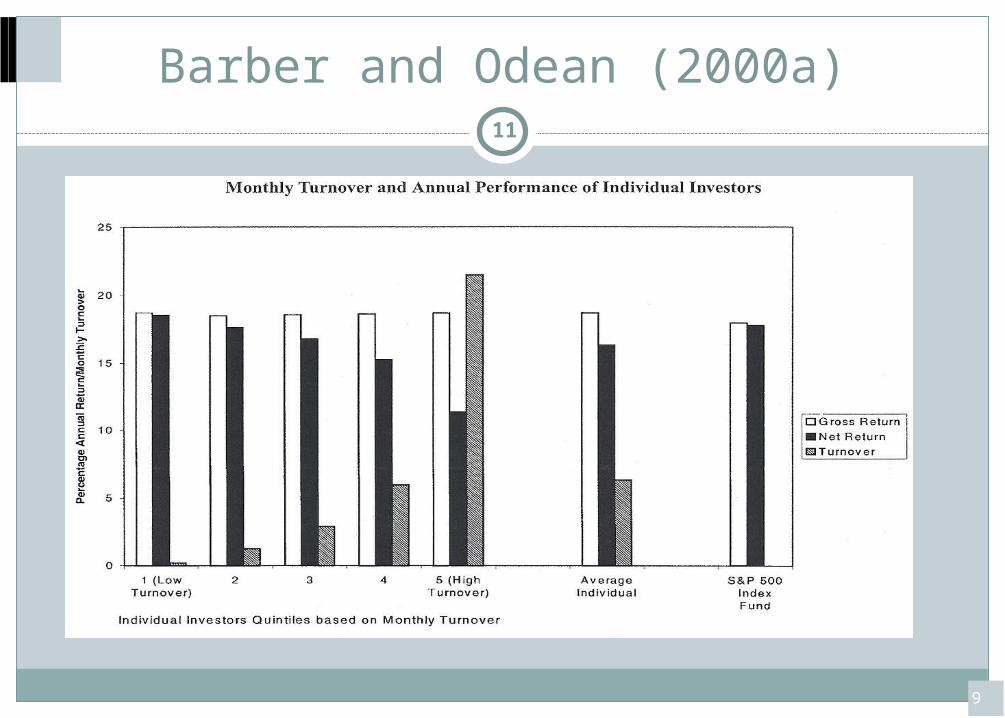

Overconfidence

As applied to investments, overconfidence may lead to excessive trading because these investors believe they possess special knowledge others do not have, such as superior predictive power and information “Trading is hazardous to your wealth” by Barber and Odean

(2000a)

Find that portfolio turnover is a good predictor of poor performance: Investors who traded the most had the lowest returns net of transaction costs

8

10

Barber and Odean (2000a)

9

11

Why Don’t They Learn?

Similar results in other studies: Overconfident traders contribute less to desk profits (Fenton-O’Creevy et al. 2007)

Why don’t overconfident investors learn from their mistakes?

Self-attribution bias

Attribute successes to their own ability

Blame failures on bad luck

10

12

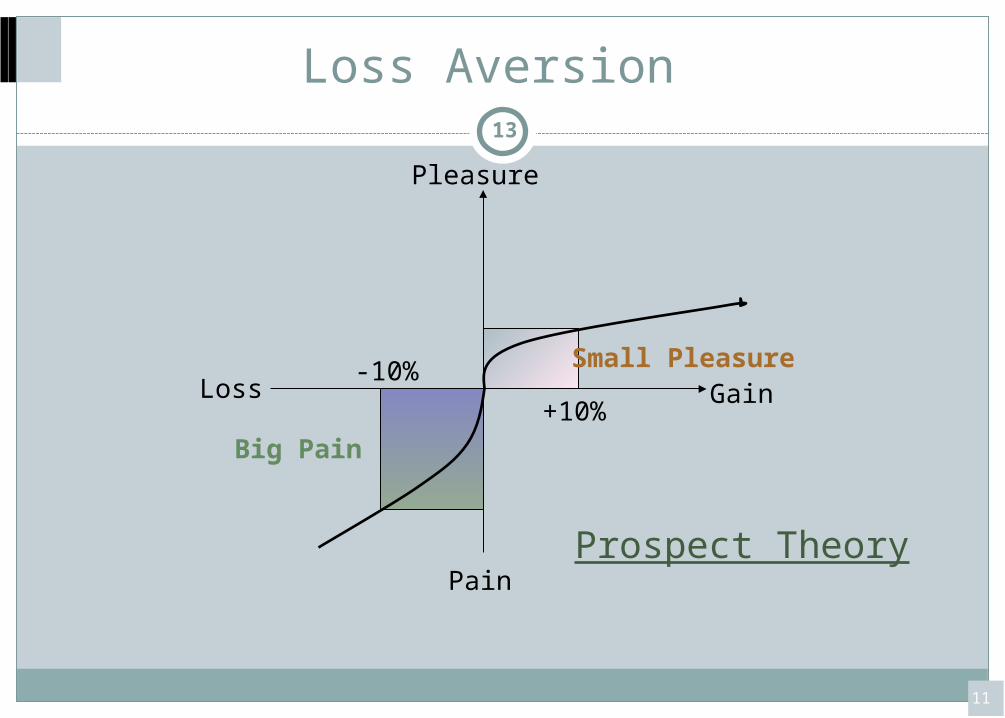

GainLoss

Pleasure

Pain

+10%

-10% Small Pleasure

Big Pain

Loss Aversion

Prospect Theory

11

13

Narrow Framing

Loss aversion may be a consequence of narrow framingNarrow frame of evaluation

Limited set of metrics in evaluating investments

Obsessive about price changes in a particular stock

Myopic behavior even though investment is long-term

Can lead to over-estimation of risk

12

14

Narrow Framing / Loss Aversion

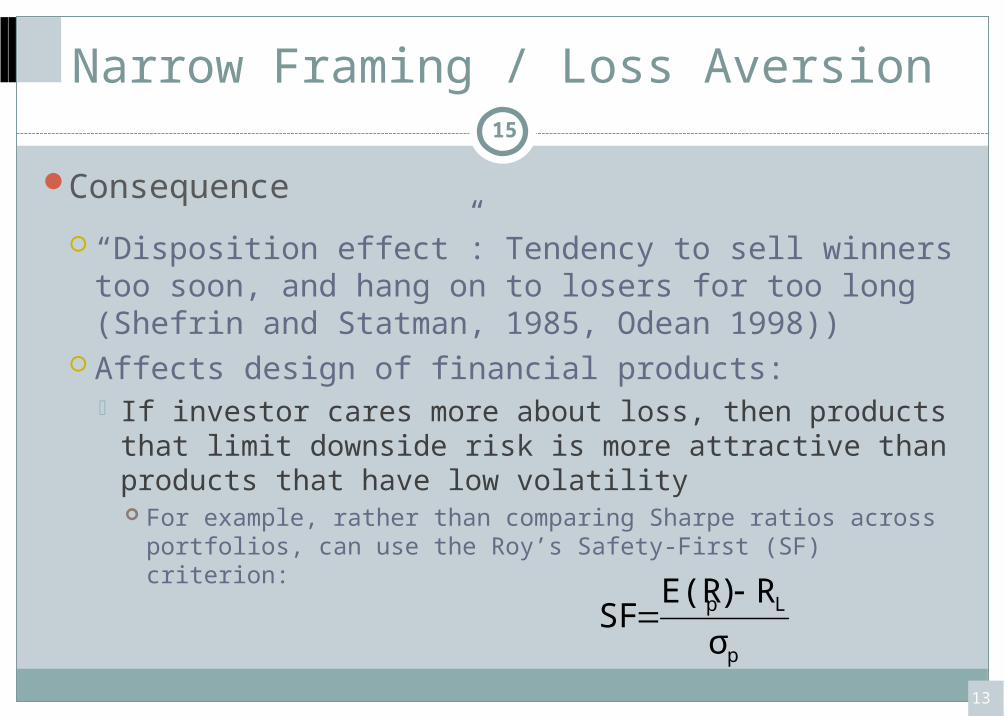

Consequence

“Disposition effect”: Tendency to sell winners too soon, and hang on to losers for too long (Shefrin and Statman, 1985, Odean 1998))

Affects design of financial products: If investor cares more about loss, then products that limit

downside risk is more attractive than products that have low volatility For example, rather than comparing Sharpe ratios across portfolios, can

use the Roy’s Safety-First (SF) criterion:

13

p

Lp

σR)E(R

SF

15

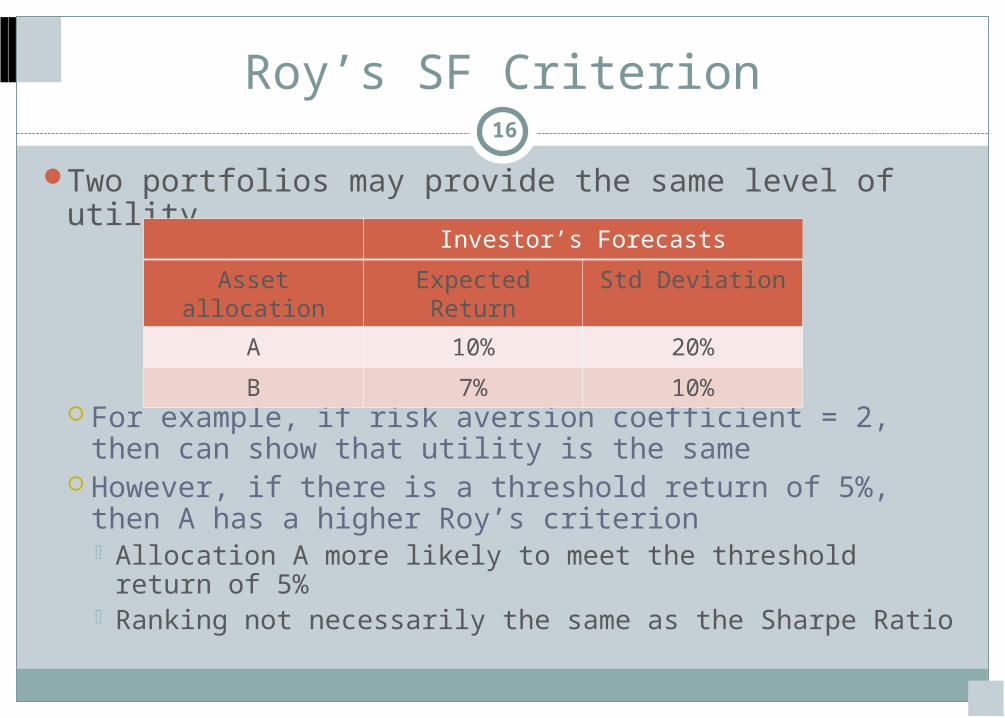

Roy’s SF Criterion

Two portfolios may provide the same level of utility

For example, if risk aversion coefficient = 2, then can show that utility is the same

However, if there is a threshold return of 5%, then A has a higher Roy’s criterion Allocation A more likely to meet the threshold return of 5% Ranking not necessarily the same as the Sharpe Ratio

Investor’s Forecasts

Asset allocation Expected Return Std Deviation

A 10% 20%

B 7% 10%

16

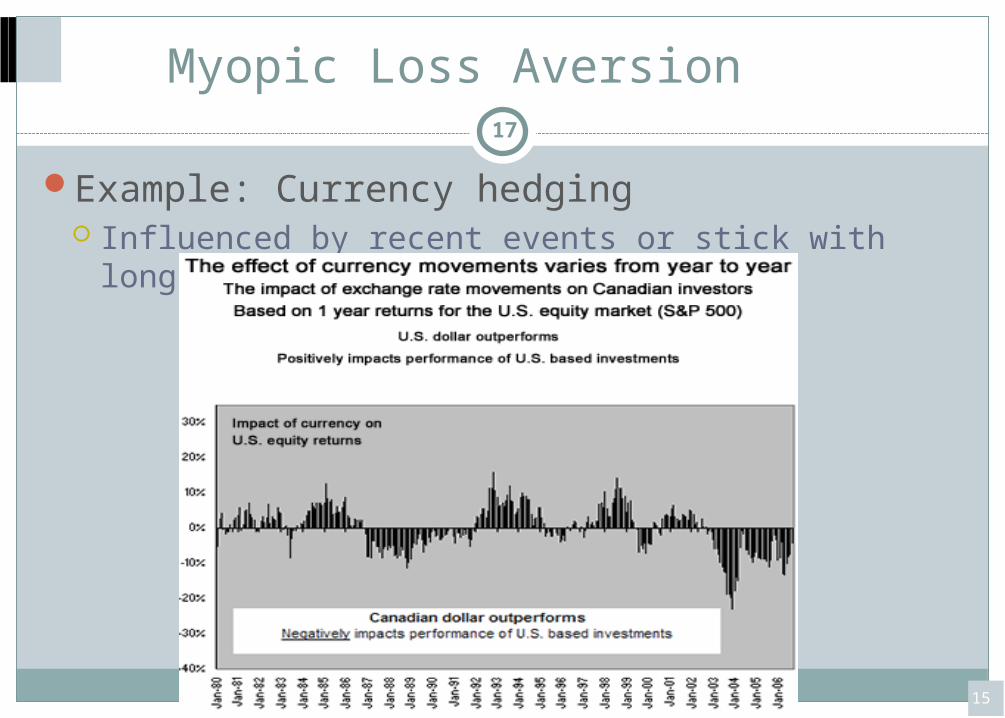

Myopic Loss Aversion

Example: Currency hedging Influenced by recent events or stick with long-term view?

15

17

Representativeness

Making decisions based on recent history, or a small sample size

Believe that it is representative of the future, or the full sample

May lead to “excessive extrapolation”

Erroneously think that recent performance is representative of longer term prospects

16

18

Representativeness

Results: Investors chase past winners

Overreacts to glamour stocks (e.g., technology bubble)

Overreacts to bad news which may be temporary (thus creating “value opportunities”)

Creates short-term momentum, but long-term reversal in returns

What quantitative managers look for

17

19

Regret Avoidance

Leads to procrastination and inertia Status quo bias

Good intentions but poor follow-throughConsequences:

Delayed saving and investment choices led to growth of target date funds

Limit divergence from peers’ average asset allocation, if sensitive to peer comparison herding behaviour of asset managers

Herding behaviour will prolong the bubble (e.g., growth of technology mutual funds in the late 1990s)

18

20

Ambiguity Aversion

Sticking with the familiar

Results in under-diversification

Investors may exhibit home bias, local bias

Bias is more substantial if take into account human capital

From a diversification point of view, DC plans should restrict company share ownership

19

21

Mental Accounting

Tendency to divide total wealth into separate accounts and buckets

Ignores correlation between assets across portfolio May result in tax-inefficient allocations

Naïve diversification in DC pension plans (Benartzi and Thaler 2001) 1/n is found to be the predominant rule Authors find that “the proportion invested in stocks depends

strongly on the proportion of stock funds in the plan” Plan sponsor’s menu of options and choices very important

20

22

Impact on Committee Decision Making

Lack of diversity in membership could pose a problem

Common knowledge syndrome

Less willing to share unique or different information for the sake of social cohesion

It takes 16 similarly-minded committee members to generate the diversity of 4 different-minded members

21

23

Final Thoughts

Some empirical findings are more respected in the profession than others

Stock market returns affected by number of hours of sunshine in NYC…etc.

Point of disagreement More and more asset management companies are using

the “behavioural finance” buzz word (mostly value strategies), as well as investment advisors

22

24

Final Thoughts

Can the two schools of thought co-exist? How I like to think about it: Short-term: markets can be inefficient due to investor

behaviour Long term, markets are on average efficient

25

The Value Premium

Risk-based explanationRelax the assumption in the conventional CAPM that beta

and the market risk premium are constantHML has higher beta when market risk premium is high.

Translation: value stocks do not do well in down markets, and hence are riskier to investors (Petkova and Zhang 2005)

Value firms tend to have greater amounts of tangible assets, and hence less flexibility to adjust capacity during downturns (operating risk)

26