Embed Size (px)

Citation preview

BayWa GroupInterim Report as at 30 June 2010Conference Call, 5 August 2010

> Klaus Josef Lutz, Chief Executive Officer

Market developments in Q2/2010

AgricultureFirmer producer prices (milk and grain) brighten sentiment in the agricultural industry Solid business with subsequent collection and storage of grain; grain selling benefits from strong export b i ( k )

Building Materials

business (weak euro) Strong agricultural resources business despite late start to spring Economic barometer for the agriculture industry in an uptrend

Building MaterialsBusiness climate index (ifo) improved in the building trade Positive stimulus in housing construction (number of building permits on the rise)Seasonal catching-up effects in building materials trading

Volume-related sales of heating oil significantly lower than a year ago

Energy

Development of DIY & Garden Centres hampered by cold, wet weather in May

Volume related sales of heating oil significantly lower than a year agoPrivate household tank filling levels (oil) now below the level customary for the time of the year Economic recovery boosts lubricants businessSolar power business accelerates due to cuts in government-backed promotion of solar energy

2

Development of the Group

3

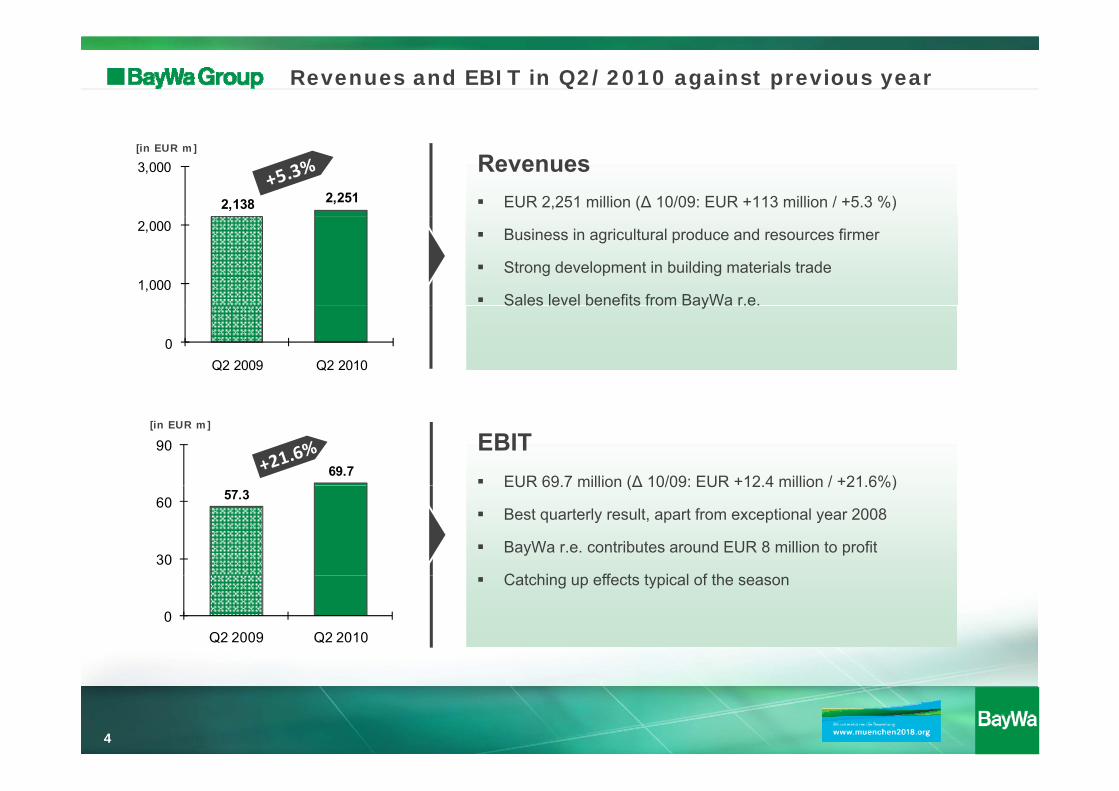

Revenues and EBIT in Q2/2010 against previous year

RevenuesEUR 2,251 million (∆ 10/09: EUR +113 million / +5.3 %) 2,138 2,251

3,000[in EUR m]

Business in agricultural produce and resources firmer

Strong development in building materials trade

Sales level benefits from BayWa r.e.1,000

2,000

y

0Q2 2009 Q2 2010

EBIT EUR 69.7 million (∆ 10/09: EUR +12.4 million / +21.6%)

69.7

90[in EUR m]

EUR 69.7 million (∆ 10/09: EUR 12.4 million / 21.6%)

Best quarterly result, apart from exceptional year 2008

BayWa r.e. contributes around EUR 8 million to profit

C t hi ff t t i l f th

57.3

30

60

Catching up effects typical of the season

0Q2 2009 Q2 2010

4

Year-on-year (Q2) comparison of EBIT

2006 2007 2008 2009 2010

Q2

[EUR m]

80.2

69.770

80

90

[EUR m]

60.1 60.257.3

40

50

60 Ø (Q2; 2006‐2010) = 65.5

10

20

30

0

10

5

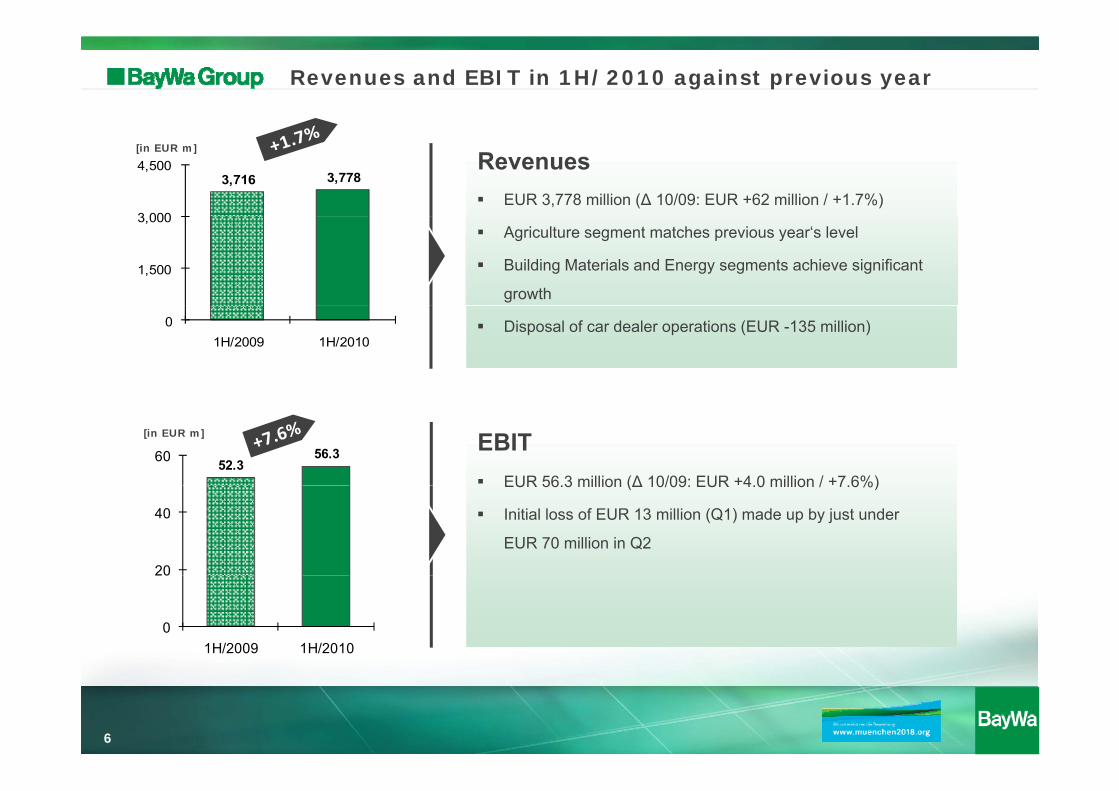

Revenues and EBIT in 1H/2010 against previous year

3,716 3,778

3 000

4,500 RevenuesEUR 3,778 million (∆ 10/09: EUR +62 million / +1.7%)

[in EUR m]

1,500

3,000Agriculture segment matches previous year‘s level

Building Materials and Energy segments achieve significant

growth

01H/2009 1H/2010

Disposal of car dealer operations (EUR -135 million)

EBIT EUR 56.3 million (∆ 10/09: EUR +4.0 million / +7.6%)

52.356.360

[in EUR m]

EUR 56.3 million (∆ 10/09: EUR 4.0 million / 7.6%)

Initial loss of EUR 13 million (Q1) made up by just under

EUR 70 million in Q2

20

40

0

20

1H/2009 1H/2010

6

Year-on-year comparison

in EUR m 1H/2007 1H/2008 1H/2009 1H/2010 ∆10/09 (%)

Revenues 3 414 9 4 381 0 3 716 3 3 777 7 1 7%Revenues 3,414.9 4,381.0 3,716.3 3,777.7 1.7%EBITDA 107.5 152.9 98.9 104.3 5.5%

% of revenues 3.1% 3.5% 2.7% 2.8%EBIT 62.7 107.5 52.3 56.3 7.6%

% of revenues 1.8% 2.5% 1.4% 1.5%EBT 39.2 79.7 30.5 35.9 17.7%

% of revenues 1.1% 1.8% 0.8% 0.9%

Consolidated net income 31.9 62.1 23.5 28.1 19.6%Tax rate 18.6% 22.1% 23.0% 21.7%

Share of minority interest 12.3 15.3 8.3 8.1 -2.4%yas % of net income 38.6% 24.6% 35.3% 28.8%

Share of owners of parent company 19.7 46.8 15.2 20.0 31.6%as % of net income 61.8% 75.4% 64.7% 71.2%

Earnings per share (EPS) in EUR 0.58 1.38 0.45 0.59 31.1%

7

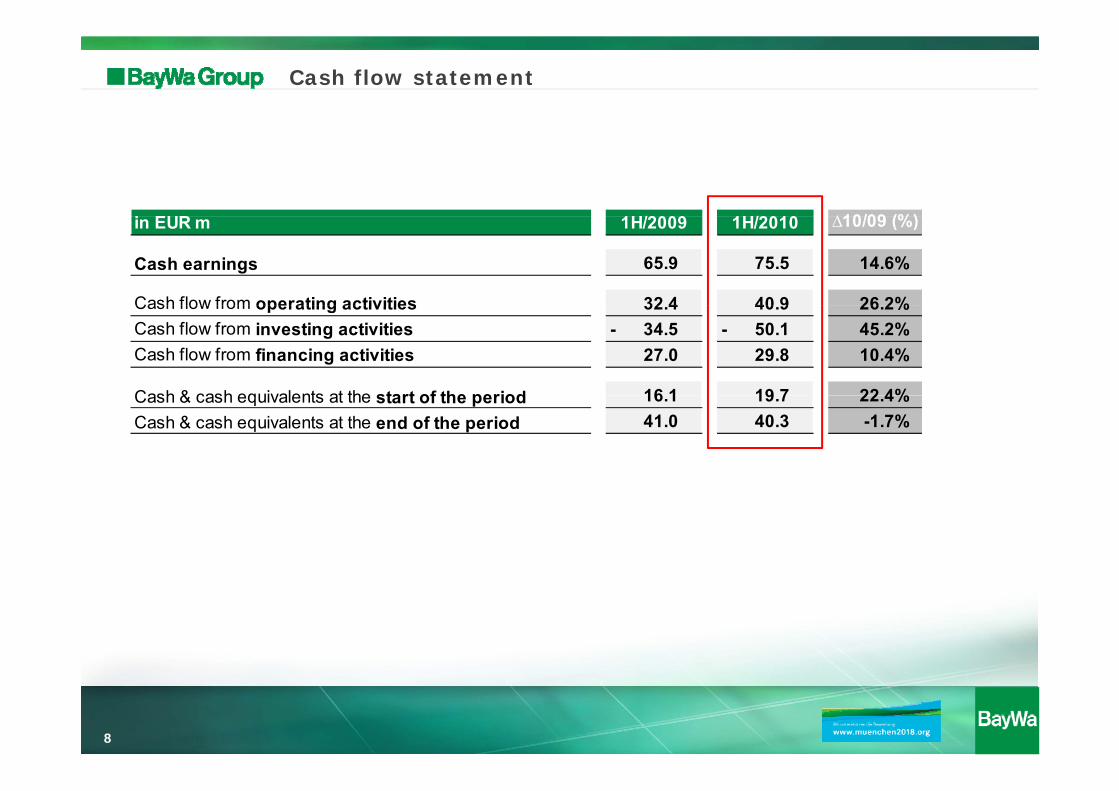

Cash flow statement

i EUR 1H/2009 1H/2010 ∆10/09 (%)in EUR m 1H/2009 1H/2010 ∆10/09 (%)

Cash earnings 65.9 75.5 14.6%

Cash flow from operating activities 32 4 40 9 26 2%Cash flow from operating activities 32.4 40.9 26.2%Cash flow from investing activities 34.5 - 50.1 - 45.2%Cash flow from financing activities 27.0 29.8 10.4%

Cash & cash equivalents at the start of the period 16 1 19 7 22 4%Cash & cash equivalents at the start of the period 16.1 19.7 22.4%Cash & cash equivalents at the end of the period 41.0 40.3 -1.7%

8

Development of the Segments

9

BayWa AgricultureSeeds

lFertilisersCrop protection GrainFeedstuffFeedstuffFruitAgricultural equipment

10

Development in 1H/2010

Development of operating resources

High demand for fertilisers at lower price levels Stable development in demand for seed and crop protection

Development of agricultural produce

From spring onwards, slight uptrend in grain prices Very good grain export business favoured by the weak euro Sound business in subsequent collection/storage of grainGrain speculation increases at the end of Q2 due to dry weather

Development of agricultural equipment

New orders above previous year‘s level (tractors)Above average demand for yard and barn equipment and facilities

11

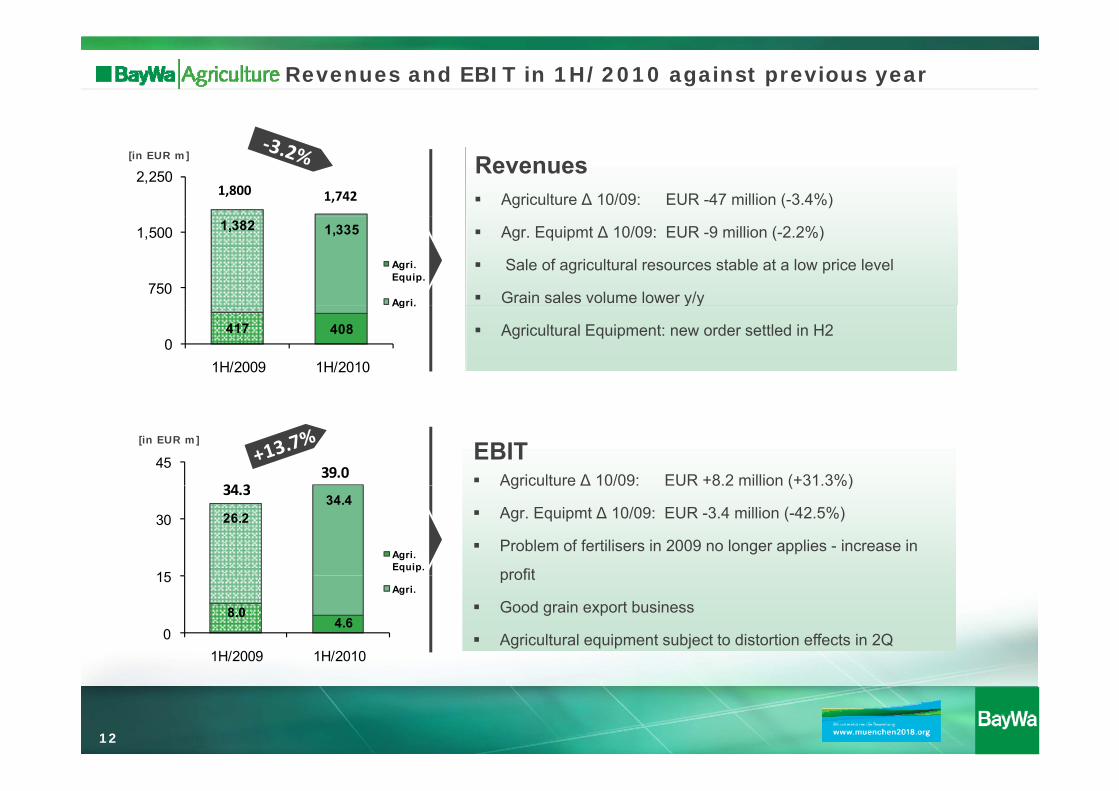

Revenues and EBIT in 1H/2010 against previous year

RevenuesAgriculture ∆ 10/09: EUR -47 million (-3.4%)

2,2501,800 1,742

[in EUR m]

Agr. Equipmt ∆ 10/09: EUR -9 million (-2.2%)

Sale of agricultural resources stable at a low price level

Grain sales volume lower y/y

1,382 1,335

750

1,500

Agri. Equip.

Agri. y y

Agricultural Equipment: new order settled in H2 417 4080

1H/2009 1H/2010

Agri.

EBIT Agriculture ∆ 10/09: EUR +8.2 million (+31.3%)

45

34 339.0

[in EUR m]

Agriculture ∆ 10/09: EUR 8.2 million ( 31.3%)

Agr. Equipmt ∆ 10/09: EUR -3.4 million (-42.5%)

Problem of fertilisers in 2009 no longer applies - increase in

profit

26.234.4

15

30

Agri. Equip.

34.3

profit

Good grain export business

Agricultural equipment subject to distortion effects in 2Q

8.04.6

0

15

1H/2009 1H/2010

Agri.

12

Year-on-year comparison

in EUR m 1H/2007 1H/2008 1H/2009 1H/2010 ∆10/09 (%)

Revenues 1,612.5 2,208.5 1,799.5 1,742.3 -3.2%EBITDA 61 8 103 2 53 5 58 5 9 3%EBITDA 61.8 103.2 53.5 58.5 9.3%

% of revenues 3.8% 4.7% 3.0% 3.4%EBIT 41.7 83.2 34.3 39.0 13.7%

% of revenues 2.6% 3.8% 1.9% 2.2%% of revenues 2.6% 3.8% 1.9% 2.2%EBT 27.5 65.5 19.9 26.3 32.2%

% of revenues 1.7% 3.0% 1.1% 1.5%

13

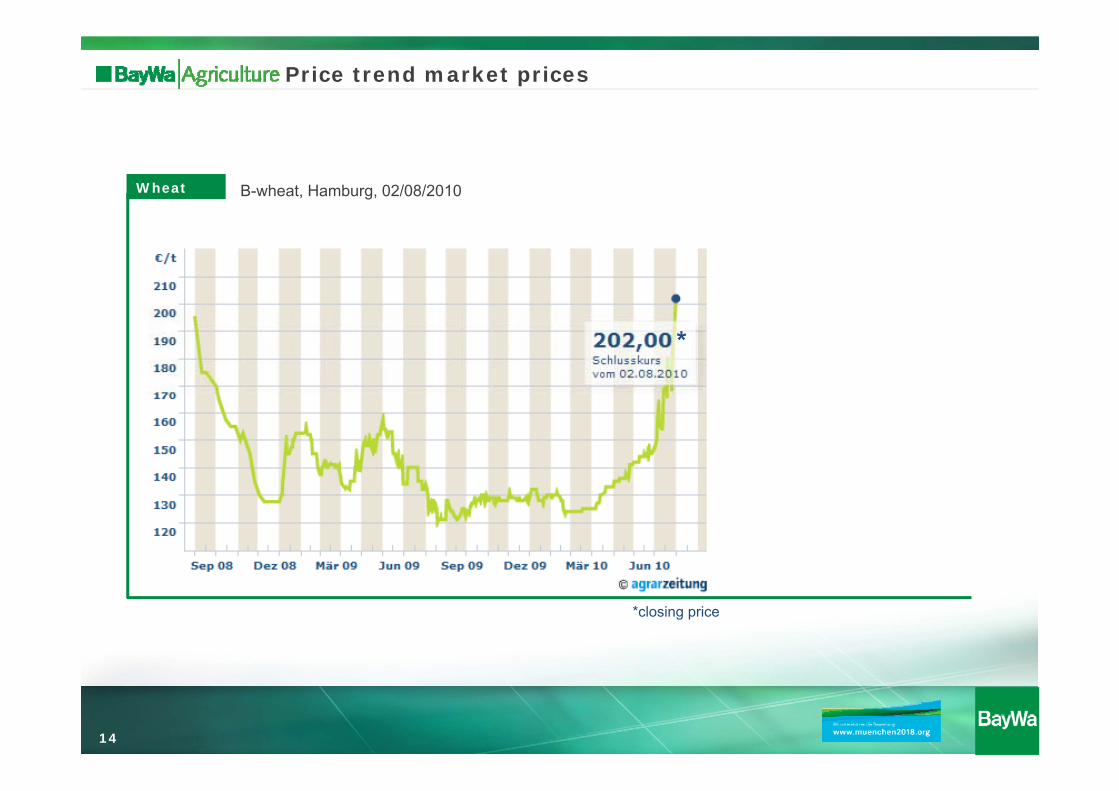

Price trend market prices

Wheat B-wheat, Hamburg, 02/08/2010

*

*

*closing price

14

Grain Balance - World

[in million t, wheat, rice, corn, barley, oat, rye, sorghum]

Szenario 2015/16 *10/11 09/10 08/09 07/08 06/07 05/06 04/05 03/04

P d kti 2 502 2 230 2 222 2 237 2 124 2 002 2 017 2 042 1 862Produktion 2.502 2.230 2.222 2.237 2.124 2.002 2.017 2.042 1.862Anfangsbestand 400 475 448 364 342 389 403 355 429Verfügbar 2.902 2.705 2.670 2.601 2.466 2.391 2.420 2.397 2.291Verbrauch 2.472 2.245 2.195 2.153 2.102 2.049 2.031 1.994 1.936

ProductionLevel at start of periodAvailableConsumption

Endbestand 430 460 475 448 364 342 389 403 355Bestände ./. Verbrauch in % 17 20 22 21 17 17 19 20 18Reichweite Endbestand

64 75 79 76 63 61 70 74 67

pLevel at end of PeriodInventory level ./. consumption in %

Reach at end of period in daysin Tagen 64 75 79 76 63 61 70 74 67Reach at end of period in days

07/2010; *2010/11 prognosis; Values partly estimatedS DRV ACTI S h h DOWJ B W

15

Source: DRV, ACTI Schumacher, DOWJones, BayWa

Price trend market prices

Urea CAN

Calcium ammonium nitrate ex Baltic Sea PortsGranulated urea ex Baltic Sea Ports Calcium ammonium nitrate ex Baltic Sea Ports, 22/07/2010

Granulated urea ex Baltic Sea Ports, 22/07/2010

**

*closing price *closing priceclosing price *closing price

16

BayWa Building Materials

Building Materials dDIY & Garden Centres

17

Development in 1H/2010

Development of Building Materials

Delayed start to the season due to long winter with heavy snowfall Modernisation and refurbishment activities in housing construction gaining momentumDevelopment of logistics services for third parties better than a year ago

Development of DIY and Garden Centres

Product mix having positive effectRenovated markets of Illertissen and Grafenau off to a good startGarden business suffers from cool spring

18

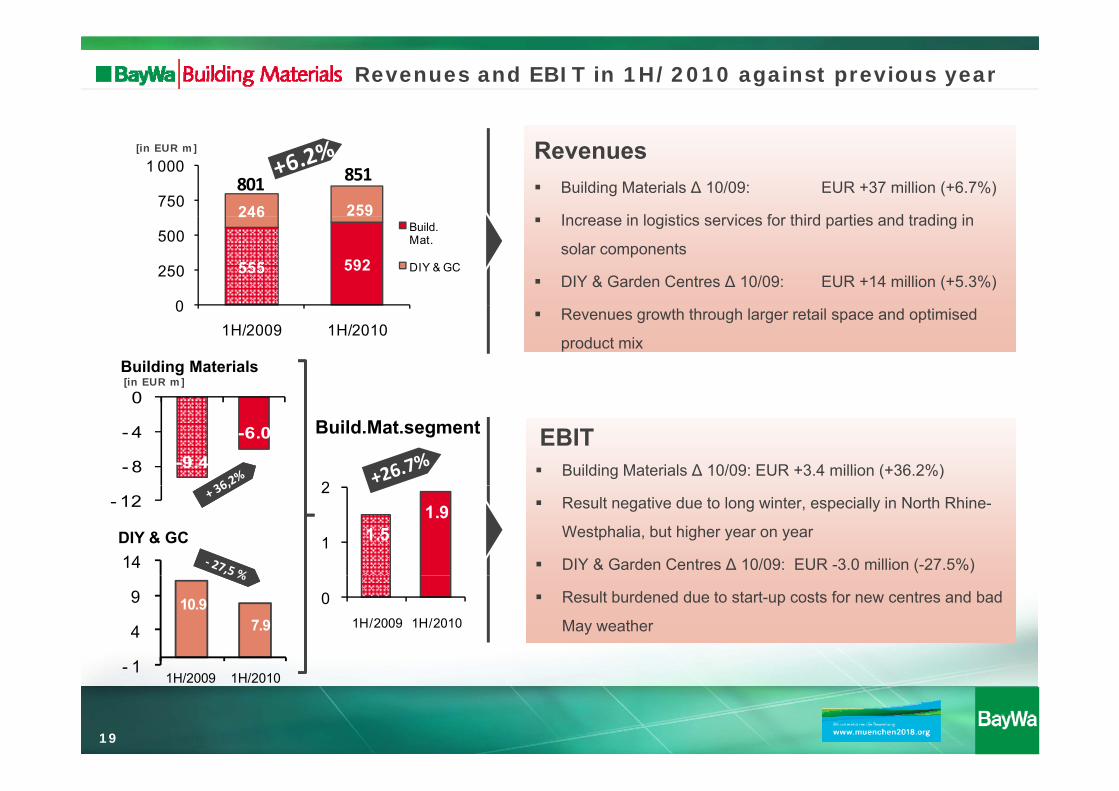

Revenues and EBIT in 1H/2010 against previous year

RevenuesBuilding Materials ∆ 10/09: EUR +37 million (+6.7%)

I i l i ti i f thi d ti d t di i246 259750

1 000 851801

[in EUR m]

Increase in logistics services for third parties and trading in

solar components

DIY & Garden Centres ∆ 10/09: EUR +14 million (+5.3%)555 592

246

0

250

500Build. Mat.

DIY & GC

Revenues growth through larger retail space and optimised

product mix

01H/2009 1H/2010

0

Building Materials[in EUR m]

EBIT Building Materials ∆ 10/09: EUR +3.4 million (+36.2%)-9.4

-6.0

- 8

- 4

0

2

Build.Mat.segment

Result negative due to long winter, especially in North Rhine-

Westphalia, but higher year on year

DIY & Garden Centres ∆ 10/09: EUR -3.0 million (-27.5%)

- 12

141.5

1.9

1

2

DIY & GC

Result burdened due to start-up costs for new centres and bad

May weather 10.9

7.9

1

4

9 01H/2009 1H/2010

19

- 11H/2009 1H/2010

Year-on-year comparison

in EUR m 1H/2007 1H/2008 1H/2009 1H/2010 ∆10/09 (%)

Revenues 806.6 831.2 800.5 851.3 6.3%EBITDA 23 2 24 0 18 4 16 1 -12 5%EBITDA 23.2 24.0 18.4 16.1 -12.5%

% of revenues 2.9% 2.9% 2.3% 1.9%EBIT 8.5 8.7 1.5 1.9 26.7%

% of revenues 1 1% 1 1% 0 2% 0 2%% of revenues 1.1% 1.1% 0.2% 0.2%EBT 1.6 1.7 4.3 - 3.7 - -14.0%

% of revenues 0.2% 0.2% -0.5% -0.4%

20

BayWa EnergyFuel

lHeating oilLubricantsSolid biofuelsBayWa r eBayWa r.e

21

Development in 1H/2010

Development of energy (conventional)Development of energy (conventional)

Fuel: private household tank filling levels now below the average customary for this time of the year Mineral oil: development of margins still stable Development of lubricants business above previous year due to economic influences

Development of BayWa r.e

BayWa r.e’s strategy paying offSolar power business accelerates due to cuts in government-backed promotion of solar energy at mid-year Sale of La Benate Wind Park in FranceSale of La Benate Wind Park in France Tender for Spain‘s largest and most powerful rooftop solar power plant (Barcelona harbour)

22

Revenues and EBIT in 1H/2010 against previous year

Energy (conventional) ∆ 10/09: EUR +58 million (+6.5%)

Price-induced increase in revenues in conventional trading

Revenues

149900

1 200

892

1,099

[in EUR m]

g

BayWa r.e: EUR +149 million

Solar power boom due to lowering of feed in tariffs at mid

892 950

0

300

600

900

renewable Energies

Energy

Solar power boom due to lowering of feed-in tariffs at mid-

year drives BayWa r.e‘s business0

1H/2009 1H/2010

EBIT Energy (conventional) ∆ 10/09: EUR -11.6 million (-84.7%)

14

19

13.7

[in EUR m]

Decline is volume induced; lack of demand for heating oil due

to households covering their requirements in 2009 at low prices 13.7 9.3

4

9

14

renewable Energies

Energy

11.4

BayWa r.e: EUR +9.3 million

MHH Solartechnik‘s contribution to profit approx. EUR 8 million 2.1

‐ 1

4

1H/2009 1H/2010

23

Year-on-year comparison

in EUR m 1H/2007 1H/2008 1H/2009 1H/2010 ∆10/09 (%)

Revenues 795.7 1,075.5 892.4 1,099.0 23.2%EBITDA 4 4 9 4 17 9 17 8 -0 6%EBITDA 4.4 9.4 17.9 17.8 -0.6%

% of revenues 0.6% 0.9% 2.0% 1.6%EBIT 0.7 5.7 13.7 11.4 -16.8%

% of revenues 0 1% 0 5% 1 5% 1 0%% of revenues 0.1% 0.5% 1.5% 1.0%EBT 0.5 5.8 13.3 10.1 -24.1%

% of revenues 0.1% 0.5% 1.5% 0.9%

24

BayWa Other Activities Food production

25

Revenues and EBIT in 1H/2010 against previous year

RevenuesYbbstaler: EUR 51 million224

300[in EUR m]

Frisch & Frost: EUR 34 million

∆ 10/09: EUR -139 million (-62.1%)

Revenues decline owing to disposal of car dealer operations85100

200

Revenues decline owing to disposal of car dealer operations

as from 01/10/200901H/2009 1H/2010

EBIT ∆ 10/09: EUR +1.2 million (+42.9%)

4 0

6[in EUR m]

Slight improvement in profit due to cost reductions2.8

4.0

2

4

01H/2009 1H/2010

26

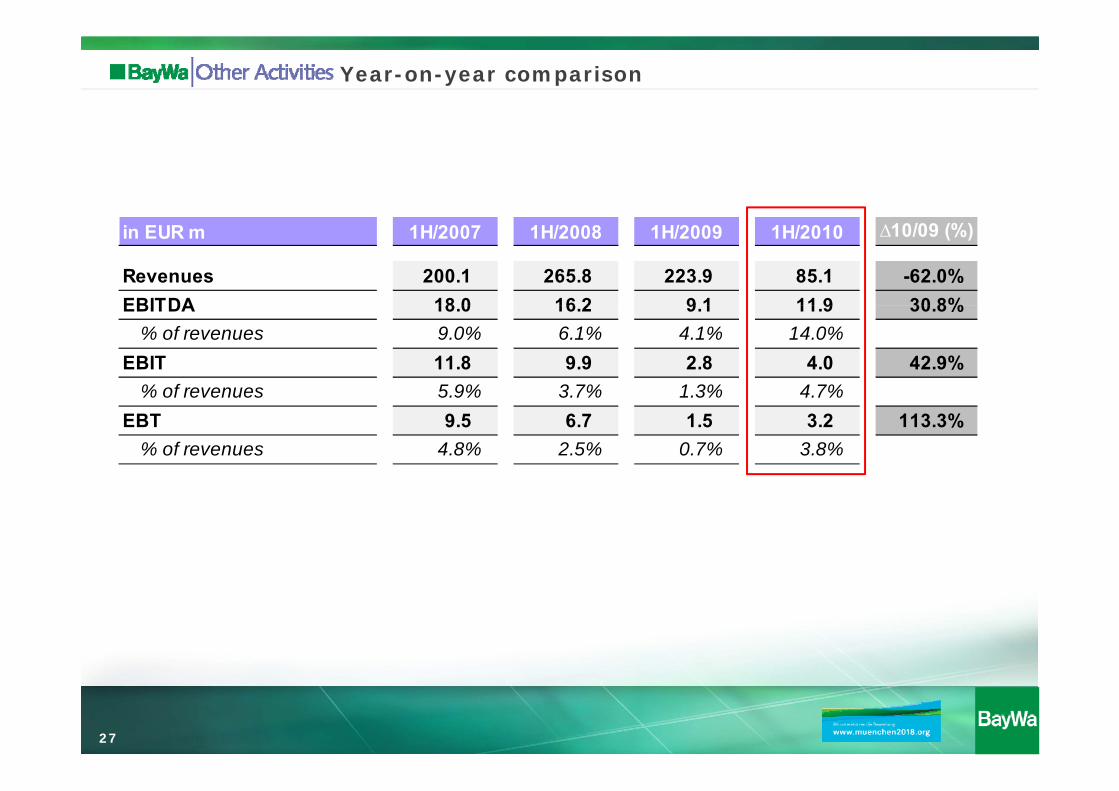

Year-on-year comparison

in EUR m 1H/2007 1H/2008 1H/2009 1H/2010 ∆10/09 (%)

Revenues 200.1 265.8 223.9 85.1 -62.0%EBITDA 18 0 16 2 9 1 11 9 30 8%EBITDA 18.0 16.2 9.1 11.9 30.8%

% of revenues 9.0% 6.1% 4.1% 14.0%EBIT 11.8 9.9 2.8 4.0 42.9%

% of revenues 5 9% 3 7% 1 3% 4 7%% of revenues 5.9% 3.7% 1.3% 4.7%EBT 9.5 6.7 1.5 3.2 113.3%

% of revenues 4.8% 2.5% 0.7% 3.8%

27

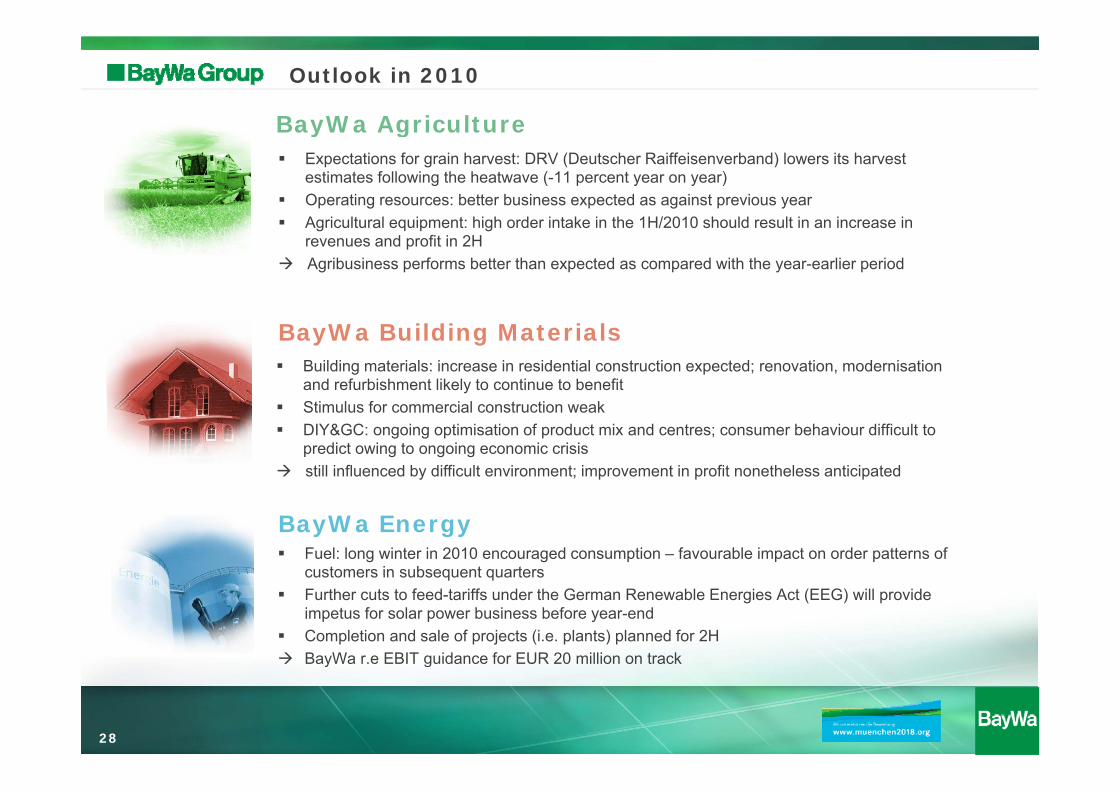

BayWa Agriculture

Outlook in 2010

Expectations for grain harvest: DRV (Deutscher Raiffeisenverband) lowers its harvest estimates following the heatwave (-11 percent year on year) Operating resources: better business expected as against previous year

BayWa Agriculture

Agricultural equipment: high order intake in the 1H/2010 should result in an increase in revenues and profit in 2H Agribusiness performs better than expected as compared with the year-earlier period

BayWa Building MaterialsBuilding materials: increase in residential construction expected; renovation, modernisation and refurbishment likely to continue to benefit Stimulus for commercial construction weak DIY&GC: ongoing optimisation of product mix and centres; consumer behaviour difficult to predict owing to ongoing economic crisis still influenced by difficult environment; improvement in profit nonetheless anticipated

BayWa EnergyFuel: long winter in 2010 encouraged consumption – favourable impact on order patterns of customers in subsequent quarterscustomers in subsequent quarters Further cuts to feed-tariffs under the German Renewable Energies Act (EEG) will provide impetus for solar power business before year-end Completion and sale of projects (i.e. plants) planned for 2H BayWa r.e EBIT guidance for EUR 20 million on track

28

y g

The BayWa ShareThe BayWa Share

29

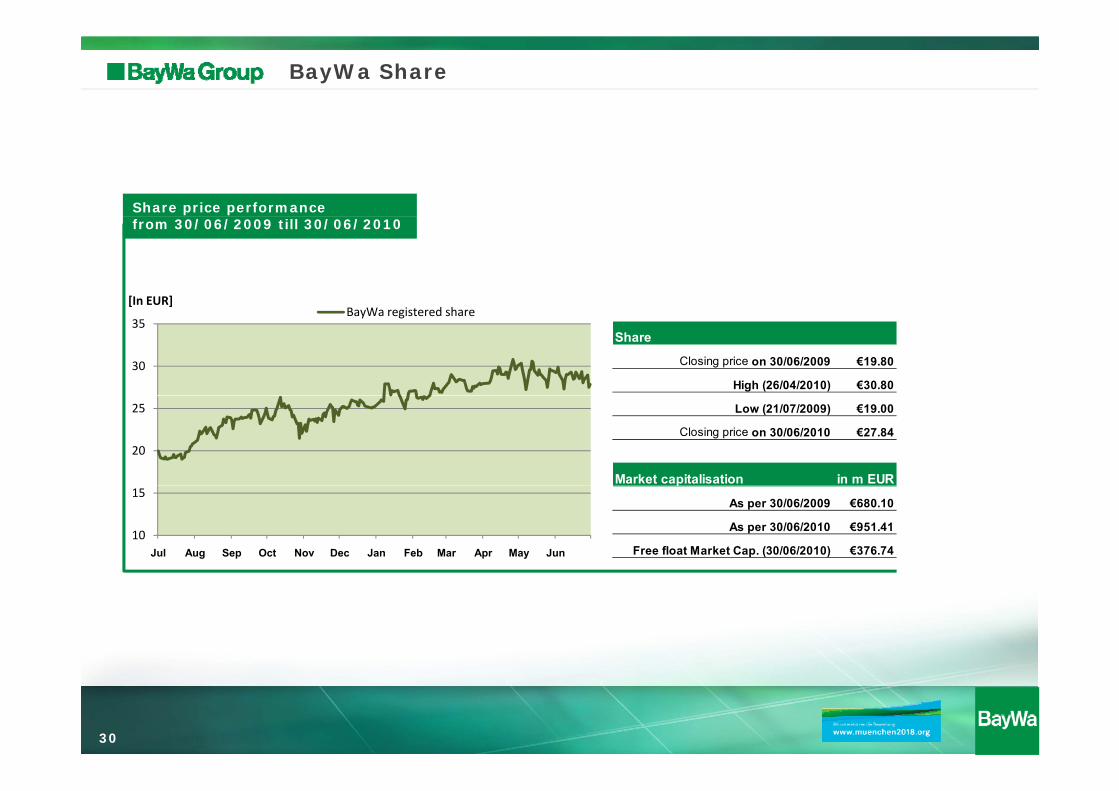

BayWa Share

Share price performance

[In EUR]

from 30/06/2009 till 30/06/2010

[ ]

30

35BayWa registered share

Share

Closing price on 30/06/2009 €19.80

High (26/04/2010) €30.80

20

25 Low (21/07/2009) €19.00

Closing price on 30/06/2010 €27.84

Market capitalisation in m EUR

10

15

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

p

As per 30/06/2009 €680.10

As per 30/06/2010 €951.41

Free float Market Cap. (30/06/2010) €376.74

30

BayWa Share 2010

More information on the BayWa share and share capitalJune 2010

Shareholder structure as per 30/06/2010

Raiffeisen Agrar Invest GmbH

Free float

Stock exchanges Frankfurt, Munich, Xetra

Segment Official Market/Prime Standard

Stock exch. index MDAX (Sec. code no. 519406)

25.12

39.55

Free floatISIN DE0005194062

Share capital EUR 87,307,622.40

Number of shares 34,104,540

Denomination No-par value shares with an arithmetical portion of

35.33

Bayerische

Denomination No par value shares with an arithmetical portion of EUR 2.56 each in the share capital

Securitisation In the form of a global certificate deposited with Clearstream Banking AG. Shareholders participate as co-owners corresponding to the number of shares held (collective custody account)Bayerische

Raiffeisen‐Beteiligungs AG

shares held (collective custody account)

31

Financial Calendar 2010

March 2010

31/03 BayWa AG Annual Results Press Conference

April 2010

01/04 Frankfurt a.M. Analysts‘ Conference

May 2010

06/05 BayWa AG Press Release Q1

07/05 B W AG A l t ‘ C f C ll Q107/05 BayWa AG Analysts‘ Conference Call Q1

June 201018/06 ICM, München Annual General Meeting of Shareholders

August 2010August 201005/08 BayWa AG Press Conference, Half-yearly Results

05/08 BayWa AG Analysts‘ Conference Call

September 2010September 2010

14/09 BayWa AG BayWa Capital Market Day

November 201011/11 BayWa AG Press Conference Q3

11/11 BayWa AG Analysts‘ Conference Call Q3

32

Investor Relations contact

Investor Relations Manager

Josko RadeljicArabellastr. 4D-81925 München

Phone: 0049 / 89 / 92 22 - 38 87Fax: 0049 / 89 / 92 12 - 38 87

E-Mail: [email protected]

33

Disclaimer

The information in this presentation is partly made up of forward-looking statements which are based on assumptions and are subject to unforeseeable risks.In as much as the assumptions on the successful integration of acquisitions and on the internal growth of the company should prove to be inaccurate, or should other unforeseeable risks occur, the possibility of the assets, financial position and results of operations of the Group diverging negatively from the target figures cited in thisoperations of the Group diverging negatively from the target figures cited in this presentation should not be discounted.BayWa AG can therefore undertake no guarantee that the actual development of the net worth, financial position and results of operations of the Group will concur with the target figures described in this presentation

34