Embed Size (px)

DESCRIPTION

Instructions for how to create a cash budget statement.

Citation preview

1

Basic Instructions for a Cash Budget Statement

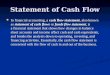

Love Thy Pet Inc.,

Cash Budget For the Year Ending, December 31, 2007

Quarter 1 2 3 4 Beginning cash balance $35,000 $20,000 $20,000 $34,000Add: Cash receipts Cash sales 50,000 60,000 80,000 80,000 Collections from customers 100,000 110,000 130,000 130,000 Receipt of interest 5,000 0 5,000 0 Receipt of dividends from investment 600 0 300 0 Sale of common stock 20,000 20,000 20,000 20,000 Sale of Securities 10,000 5,000 5,000 0 Sale of plant asset 4,000 0 0 0 Total receipts 189,600 165,000 240,300 230,000Total available cash 224,600 205,000 260,300 264,000Less: Cash disbursements Materials (purchases) 56,000 60,000 75,000 75,000 Salaries (direct labor) 32,000 36,000 40,000 40,000 Selling and administrative 95,000 85,000 85,000 85,000 expenses (excluding depreciation Purchase of (title of asset) 10,000 0 0 0 Purchase of investment 6,000 0 0 0 Payment of dividends 12,000 5,000 5,000 5,000 Income tax expense 4,600 4,600 4,600 4,600 Total disbursements 215,600 190,600 209,600 209,600Excess (deficiency) of available 9,000 14,400 50,700 54,400 Cash over disbursements Financing Borrowings 11,000 5,600 0 Repayments—plus $100 interest 16,700 0Ending cash balance $20,000 $20,000 $34,000 $54,400

2

3

Step by Step Instructions

Always start with the name of the company, the title of the statement, and the period for which the statement is being prepared.

Cash receipts section of a Cash Budget Statement

Step 1. Start this section with the schedule of periods of the cash budget statement. This can be broken up into months, quarters, or semiannual periods. Step 2. The next line will be labeled the “Beginning cash balance.” This will be for the first period of the statement in which case that would be the first quarter on this statement. Always finish one quarter or fiscal period before going on to the next. The ending cash balance for one period becomes the beginning cash balance for the next period. Step 3. Next is the title “Add: Cash receipts” no amounts are placed on this line of the statement. Step 4. List cash that is due to be received during the periods for which the statement covers. Only list items that you will be receiving cash from during the period of the statement. You should be giving a list of cash receipts and for what period they are expected to be received during the year.

a. Cash sales b. Collections from customers – this amount comes from the schedule of expected

collections from customers that is created before you start the cash budget. c. Receipt of Interest d. Receipt of dividends from investment(s) e. Sale of common stock f. Sale of Securities g. Sale of plant asset(s)

Step 6. Total all of the cash receipts for each period. The title for this line is “Total receipts.” Step 7. The next line is titled “Total available cash.” You will need to add beginning cash balance to total receipts to get this amount.

4

Step by Step Instructions

Cash disbursements section of a Cash Budget Statement Step 1. Start this section with the title “Less: Cash disbursements.” Again this is just a title line and no amounts are placed on this line. Step 2. Next list any item that you plan on spending money on during the periods covered in this statement. Again list only the items you plan on spending money for during the period of this statement. The list should include any of the following:

a. Materials-(purchases) this amount comes from the schedule of expected payments of purchases that you created before you started this statement.

b. Salaries-(direct labor) this includes benefits and taxes. c. Selling and administrative expenses (excluding depreciation) d. Purchase of (title of asset) e. Purchase of investment f. Payment of dividends g. Income tax expense

Step 3. Total all of the cash disbursements and place that amount on this line. The title for this line will be “Total disbursements.” Step 4. Subtract the total disbursements from the total available cash. Title this line, “Excess (deficiency) of available cash over disbursements.”

Financing section of a Cash Budget Statement Step 1. The first line in this section is titled, “borrowings.” A minimum balance for the bank account should be set for the beginning of each period. If for any reason that amount is not in the account at the end of the prior period than money can be borrowed to bring the account up to that minimum balance. Step 2. The next line in this section is titled, “Repayments—plus $100 interest.” This line is for any repayments of past loans to keep the minimum balance. It should only be used if there is an excess of money over the minimum balance for the end of that period. Notes: Follow all of the steps for the first period before beginning the second and third periods. Before you start a cash budget statement make sure to create (1) a schedule of expected collections from customers and (2) a schedule of expected payments for purchases. As always don’t forget your $ signs and double underlines.