Embed Size (px)

Citation preview

Personal Mortgage Summary

Financial Services & Market Act 2000

As Independent Financial Advisers, we are required to have a due regard for the best interests of clients when giving financial advice. We must do our utmost to ensure that we are aware of your personal and financial circumstances so that our advice is suitable for your needs.

The questions in this Personal Financial Summary have been designed to help your adviser provide advice that meets your needs.

You of course do not have to answer all of the questions but any non-disclosure of vital information could result in the advice you are given, not being appropriate advice. The advice you are given will only be as good as the information provided.

Data Protection Act 1998

The information given in this document will be retained on computer for reference purposes and will be held in accordance with the Data Protection Act 1998. The information may also be used to provide you with details of products suitable to your requirements. For further information please refer to our Terms of Business/Client Agreement.

Terms of Business/Client Agreement

This is an important document that sets out the terms of which any business will take place between PIA Wealth Management and you as a client.

Client Name(s):

Adviser’s Name:

Date:

Mortgage July 2016 1

Mortgage July 2016 2

Why PIA Wealth Management?

Our aim is to build a long-term relationship with you, which is mutually advantageous and an integral part of achieving this is our wholehearted commitment to treating our customers fairly.

Because we are truly independent we can select the most suitable products(s) for your individual needs from the many that are available in the market place.

When making recommendations we will access the entire universe of financial solutions and present the strategy which we believe is best suited to your objectives and priorities, in the most tax-efficient manner.

We strongly recommend that a full financial review is carried out, but appreciate that there may be times when advice is required in specific areas only. For example, at certain times of the year you may wish to focus on one particular area of financial planning that needs to take place before the end of the tax year.

In those circumstances we provide a tailored service known as ‘restricted advice’, where it is specified at the outset that our advice is going to be restricted to one or more areas of financial planning.

We would stress that our recommendation is that a full review is carried out which will enable us to advise you on the key areas of protection and financial investment planning.

Mortgage July 2016 3

BASIC DATA

PERSONAL DETAILS

YOURSELF YOUR PARTNERTitle (Mr / Mrs / Miss / other – please specify

Forename or initials

Surname

Date of birth / / / /

Please tick the appropriate box to indicate your marital status

Single Married Separated Widowed Divorced

Are you co-habiting? Yes/NoIf you are married – are you married to each other?

Yes/No

Address

Postcode

Please tick the appropriate box to indicate your residential status

Homeowner Private Tenant Council Tenant

Lodger Living with parents First Time Buyer

How long at this address (nearest month)

Home telephoneWork telephoneMobile telephoneInternet access Yes/No Yes/No

Email addressHome:

Work:

Home:

Work:

Notes

Mortgage July 2016 4

National Insurance No.Tax Office/Reference NumberFor tax purposes, are you UK domiciled? Yes/No Yes/No

If ‘No’, please state which country you are domiciled inHave you made a will? Yes/No Yes/NoIf no, would you like us to help to arrange this for you?

Yes/No Yes/No

If yes, when was it last updated?Does it still reflect your wishes? Yes/No Yes/No

General Will details, main beneficiaries, etc

Are you likely to be the beneficiary of someone else’s will?

Yes/No Yes/No

Have you established a Lasting Power of Attorney?

Yes/No Yes/No

Date Issued(please provide a copy for our file)

V-TESTED? (Office use only) Yes/No Yes/No

Mortgage July 2016 5

Notes

Smoker status Smoker/Non-Smoker Smoker/Non-SmokerIf you smoked previously, when did you stop smoking? (If applicable)Have you ever suffered any major ill health?(please give details and dates)

Are you subject to regular medication or treatment?(please give details and dates)

Do you have any current health concerns?(please give details and dates)

How would you describe your current state of health?

Excellent ExcellentGood GoodAverage AveragePoor PoorVery Poor Very Poor

Mortgage July 2016 6

Notes

Mortgage July 2016 7

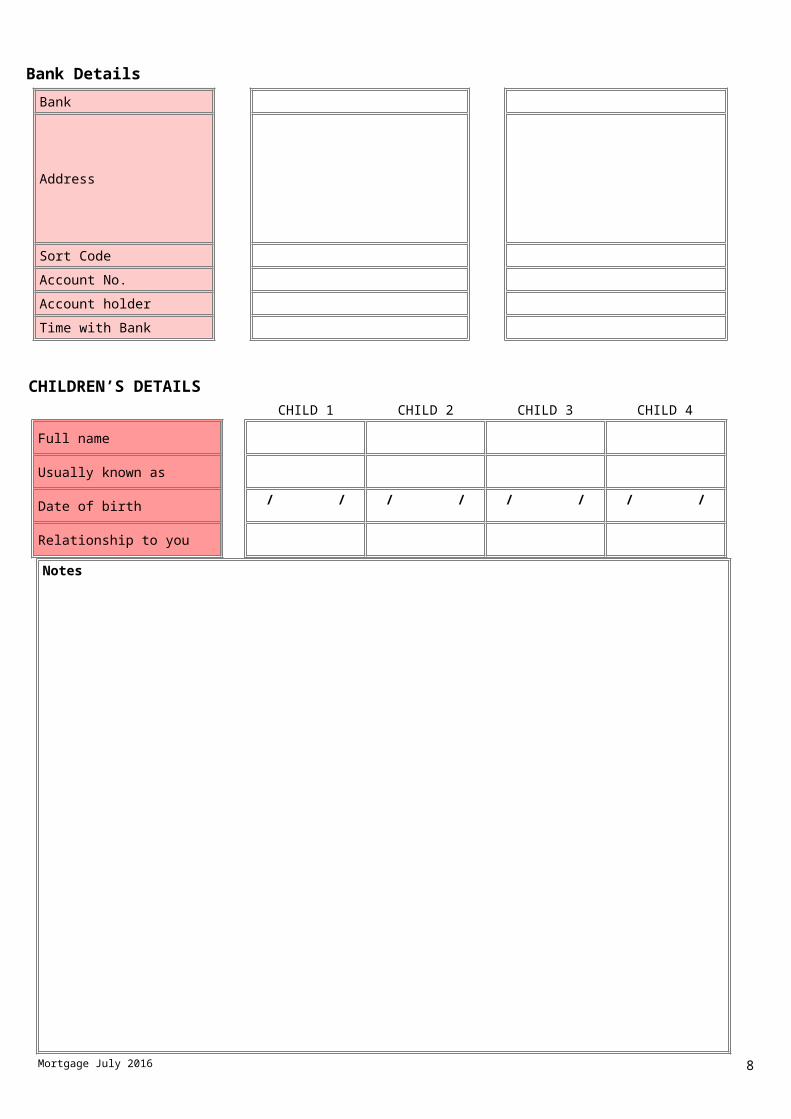

Bank DetailsBank

Address

Sort CodeAccount No.Account holderTime with Bank

CHILDREN’S DETAILSCHILD 1 CHILD 2 CHILD 3 CHILD 4

Full name

Usually known as

Date of birth / / / / / / / /

Relationship to you

Notes

Mortgage July 2016 8

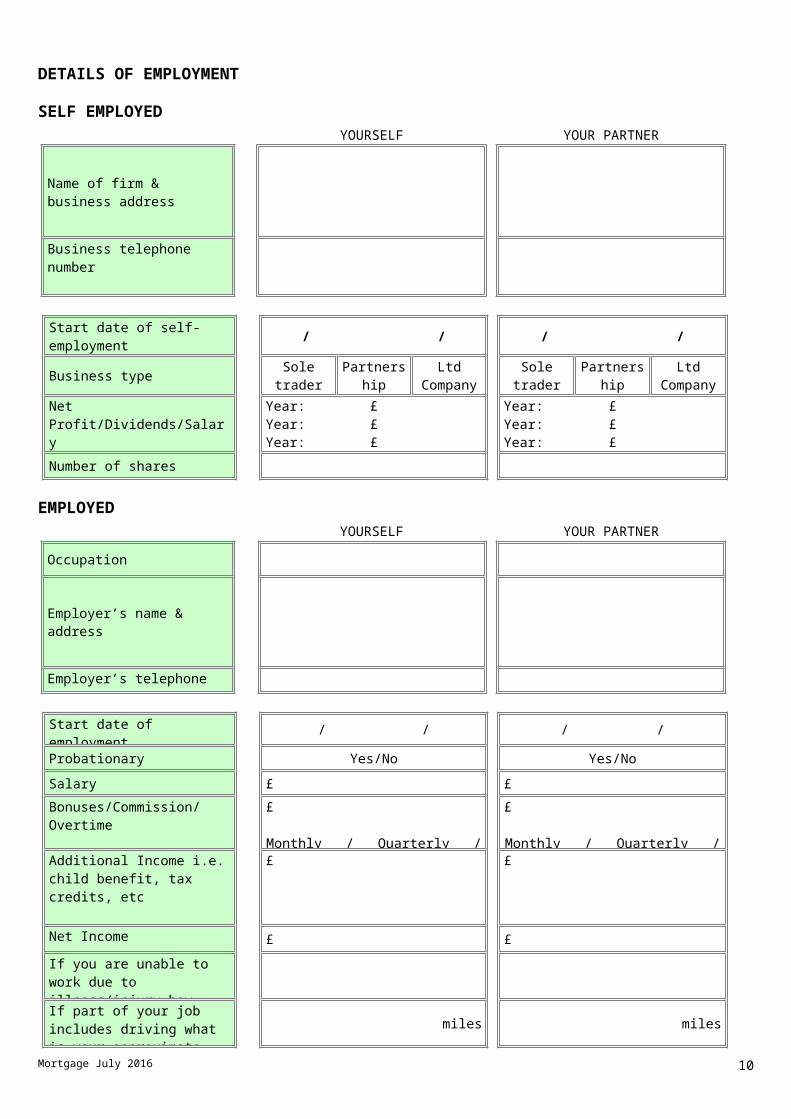

DETAILS OF EMPLOYMENT

SELF EMPLOYEDYOURSELF YOUR PARTNER

Name of firm & business address

Business telephone number

Start date of self-employment / / / /

Business type Sole trader

Partnership

Ltd Company

Sole trader

Partnership

Ltd Company

Net Profit/Dividends/Salary

Year: £Year: £Year: £

Year: £Year: £Year: £

Number of shares

EMPLOYEDYOURSELF YOUR PARTNER

Occupation

Employer’s name & address

Employer’s telephone number

Start date of employment / / / /

Probationary Yes/No Yes/No

Salary £ £Bonuses/Commission/Overtime

Paid

£

Monthly / Quarterly / Annually

£

Monthly / Quarterly / AnnuallyAdditional Income i.e.

child benefit, tax credits, etc

£ £

Net Income £ £If you are unable to work due to illness/injury how long would your employer If part of your job includes driving what is your approximate business

miles miles

Mortgage July 2016 9

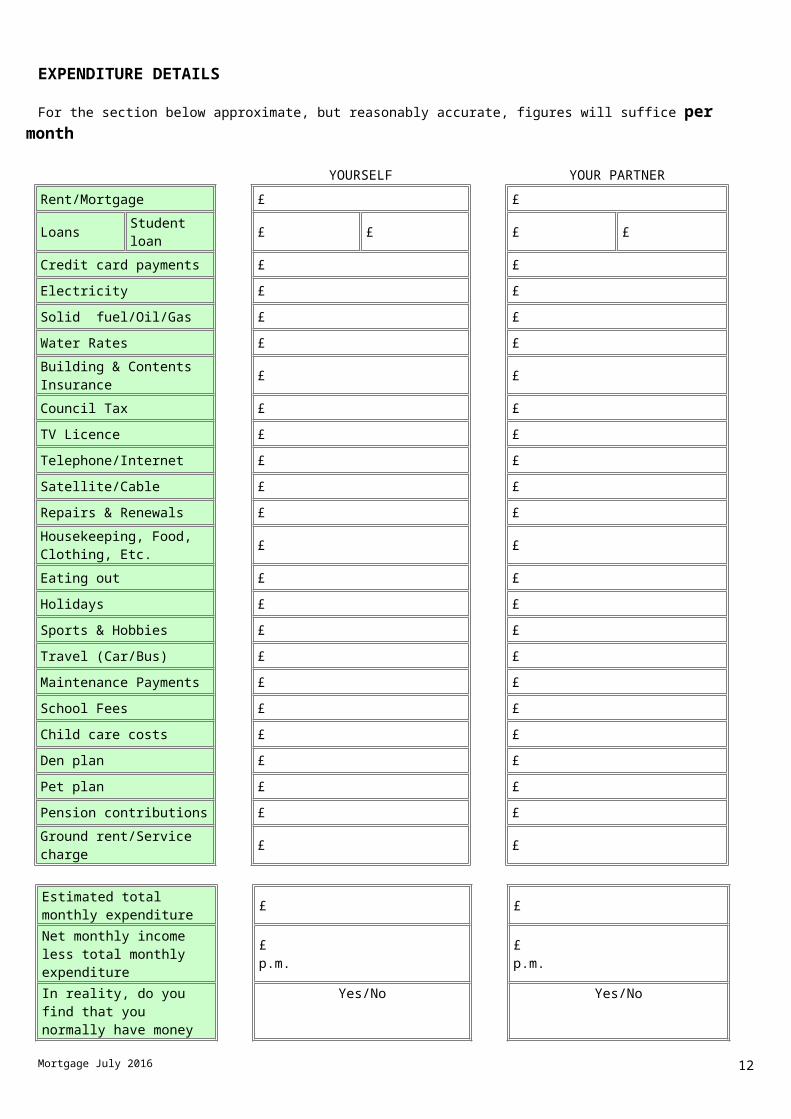

EXPENDITURE DETAILS

For the section below approximate, but reasonably accurate, figures will suffice per month

YOURSELF YOUR PARTNER

Rent/Mortgage £ £

Loans Student loan £ £ £ £

Credit card payments £ £

Electricity £ £

Solid fuel/Oil/Gas £ £

Water Rates £ £Building & Contents Insurance £ £

Council Tax £ £

TV Licence £ £

Telephone/Internet £ £

Satellite/Cable £ £

Repairs & Renewals £ £Housekeeping, Food, Clothing, Etc. £ £

Eating out £ £

Holidays £ £

Sports & Hobbies £ £

Travel (Car/Bus) £ £

Maintenance Payments £ £

School Fees £ £

Child care costs £ £

Den plan £ £

Pet plan £ £

Pension contributions £ £Ground rent/Service charge £ £

Estimated total monthly expenditure £ £

Net monthly income less total monthly expenditure

£ p.m.

£ p.m.

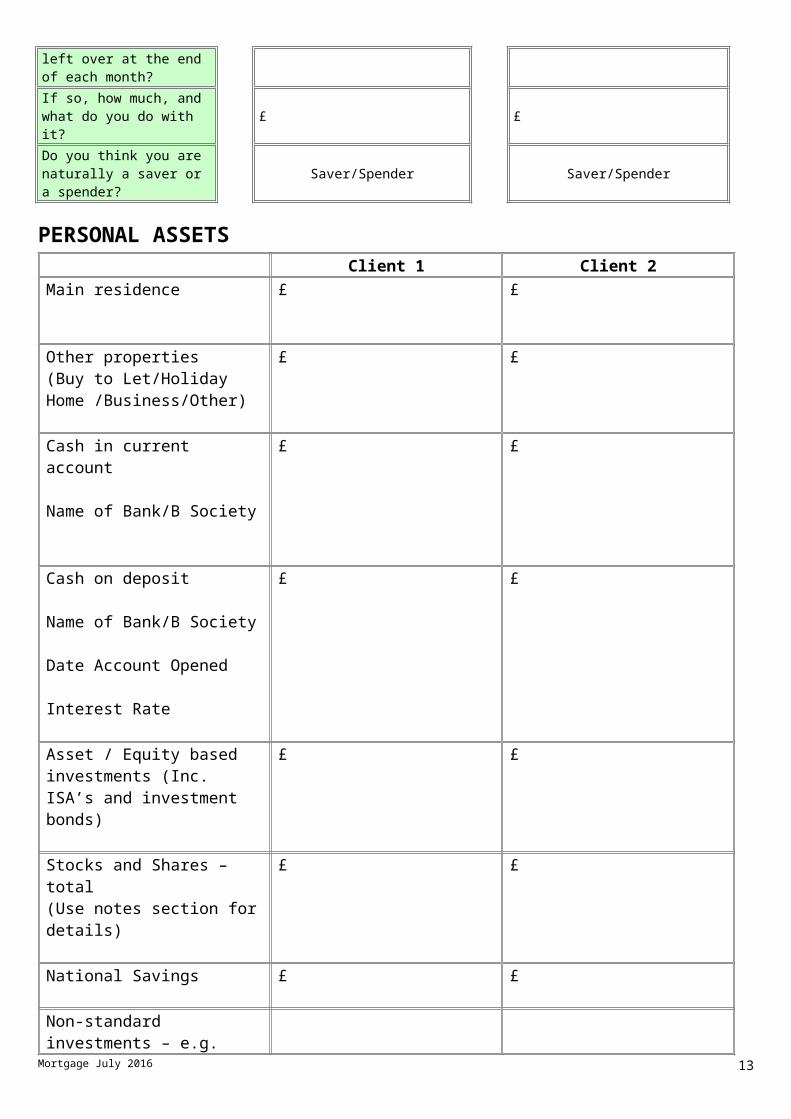

In reality, do you find that you normally have money left over at the end of each month?

Yes/No Yes/No

If so, how much, and what do you do with it? £ £

Do you think you are naturally a saver or a

Saver/Spender Saver/Spender

Mortgage July 2016 10

spender?

PERSONAL ASSETSClient 1 Client 2

Main residence £ £

Other properties(Buy to Let/Holiday Home /Business/Other)

£ £

Cash in current account

Name of Bank/B Society

£ £

Cash on deposit

Name of Bank/B Society

Date Account Opened

Interest Rate

£ £

Asset / Equity based investments (Inc. ISA’s and investment bonds)

£ £

Stocks and Shares – total(Use notes section for details)

£ £

National Savings £ £

Non-standard investments – e.g. gold, art, fine wine etc.

Total Assets £ £

Notes

Mortgage July 2016 11

Mortgage July 2016 12

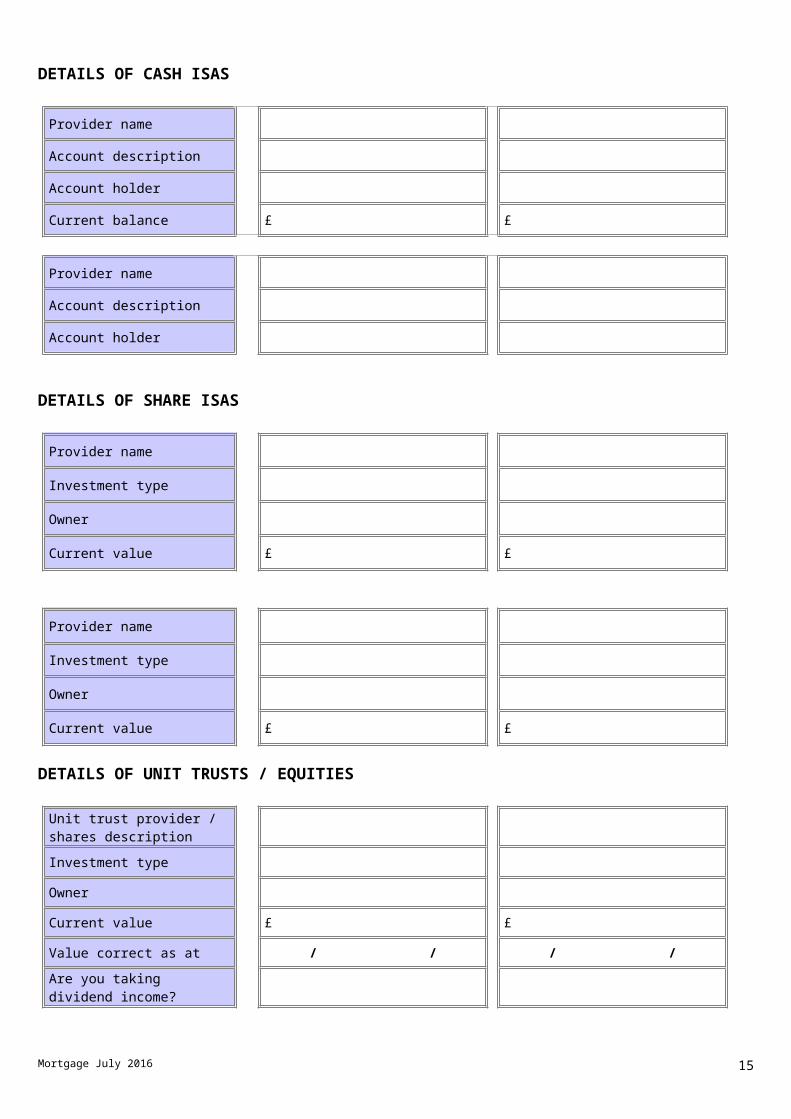

DETAILS OF CASH ISAS

Provider name

Account description

Account holder

Current balance £ £

Provider name

Account description

Account holder

DETAILS OF SHARE ISAS

Provider name

Investment type

Owner

Current value £ £

Provider name

Investment type

Owner

Current value £ £

DETAILS OF UNIT TRUSTS / EQUITIES

Unit trust provider / shares description

Investment type

Owner

Current value £ £

Value correct as at / / / /Are you taking dividend income?

Mortgage July 2016 13

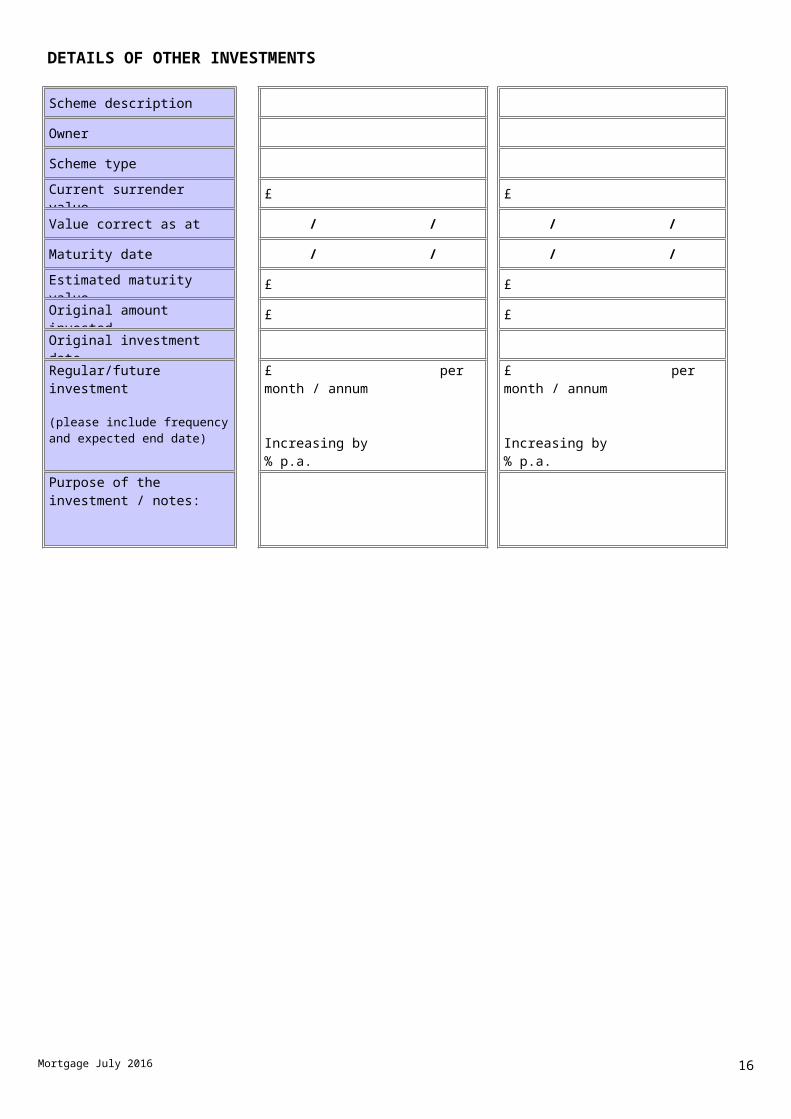

DETAILS OF OTHER INVESTMENTS

Scheme description

Owner

Scheme type

Current surrender value £ £

Value correct as at / / / /

Maturity date / / / /

Estimated maturity value £ £

Original amount invested £ £

Original investment date

Regular/future investment

(please include frequency and expected end date)

£ per month / annum

Increasing by % p.a.

£ per month / annum

Increasing by % p.a.

Purpose of the investment / notes:

Mortgage July 2016 14

DETAILS OF ENDOWMENTS

Provider name

Life Assured

Beneficiary £ £

Current death claim value

Current surrender value % p.a. % p.a.

Estimated maturity value £ £

Maturity date / / / /

Premium £ per month / annum

£ per month / annum

Start date / / / /

Provider name

Life Assured

Beneficiary £ £

Current death claim value

Current surrender value % p.a. % p.a.

Estimated maturity value £ £

Maturity date / / / /

Premium £ per month / annum

£ per month / annum

Start date / / / /

Mortgage July 2016 15

Provider name

Life Assured

Beneficiary £ £

Current death claim value

Current surrender value % p.a. % p.a.

Estimated maturity value £ £

Maturity date / / / /

Premium £ per month / annum

£ per month / annum

Start date / / / /

Provider name

Life Assured

Beneficiary £ £

Current death claim value

Current surrender value % p.a. % p.a.

Estimated maturity value £ £

Maturity date / / / /

Premium £ per month / annum

£ per month / annum

Start date / / / /

Mortgage July 2016 16

DETAILS OF WHOLE OF LIFE / CRITICAL ILLNESS WHOLE OF LIFE POLICIES

Provider name

Grantee

Life Assured

Beneficiary £ £

Critical illness sum assured (if applicable) £ £

Current death claim value

Current surrender value % p.a. % p.a.Premium £ per month /

annum £ per month / annum

Start date / / / /

Provider name

Grantee

Life Assured

Beneficiary £ £

Critical illness sum assured (if applicable) £ £

Current death claim value

Current surrender value % p.a. % p.a.Premium £ per month /

annum £ per month / annum

Start date / / / /

Mortgage July 2016 17

DETAILS OF TERM ASSURANCE / CRITICAL ILLNESS TERM ASSURANCE POLICIES

Provider name

Life Assured

Beneficiary

Critical illness sum assured (if applicable) £ £

Current death claim value £ £

Rate of increase (or decrease) of death claim value

Expiry date / / / /

Premium £ per month / annum

£ per month / annum

Start date / / / /

Provider name

Life Assured

Beneficiary

Critical illness sum assured (if applicable) £ £

Current death claim value £ £

Rate of increase (or decrease) of death claim value

Expiry date / / / /

Premium £ per month / annum

£ per month / annum

Start date / / / /

Mortgage July 2016 18

DETAILS OF PHI POLICIES

Provider name

Insured

Benefit value £ £

Benefit payment frequency

Rate of increase of benefit

Age at which benefit ceases

Deferred period (in weeks)

Premium £ per month / annum

£ per month / annum

Start date / / / /

Premium paid personally or by employer?Accident/ Sickness/ Unemployment Cover Yes/No Yes/No

Details

Mortgage July 2016 19

PERSONAL PENSIONS / STAKEHOLDER PENSIONS / RETIREMENT ANNUITIES

Type of plan (i.e. Stakeholder / PPP / Retirement Annuity)

Underwriter

Pensioner

Current fund value (if known) £ £

Normal Retirement Age

Proposed tax free cash(% of fund) % %

Policy start date / / / /

Gross Premium £ per month / quarter / annum

£ per month / quarter / annum

Premium paid personally or by employer?If the premium increases automatically, please state at what rate. % p.a. % p.a.

Type of plan (i.e. Stakeholder / PPP / Retirement Annuity)

Underwriter

Pensioner

Current fund value (if known) £ £

Normal Retirement Age

Proposed tax free cash(% of fund) % %

Policy start date / / / /

Gross Premium £ per month / quarter / annum

£ per month / quarter / annum

Premium paid personally or by employer?If the premium increases automatically, please state at what rate. % p.a. % p.a.

Mortgage July 2016 20

MONEY PURCHASE OCCUPATIONAL PENSIONS

Type of plan (i.e. Stakeholder / PPP / Retirement Annuity)

Underwriter

Pensioner

Current fund value (if known) £ £

Assumed future fund growth % p.a. % p.a.

Normal Retirement Age

Proposed tax free cash(% of fund) % %Policy start date / / / /

Premium £ per month / quarter / annum

£ per month / quarter / annum

Premium paid personally or by employer?If the premium increases automatically, please state at what rate.

% p.a. % p.a.

FINAL SALARY PENSIONS

Scheme name

Pensioner

Date joined scheme / / / /

Normal Retirement Age

Selected Retirement Age

Scheme basis(e.g. 1/60ths for each year’s service)Do you have an option to take a tax-free lump sum?

Death in Service Benefits?

Death in Retirement Benefits?

Mortgage July 2016 21

DETAILS OF MAIN RESIDENCE

Property description

Owner (if jointly owned please state if Tenancy In Common and percentage owned)

Current value £

DETAILS OF SECOND PROPERTY (Not Buy to Let)

Address

Owner (if jointly owned please state if Tenancy In Common and percentage owned)

Current value £

Mortgage July 2016 22

MORTGAGES AND LOANSMain Residence

Mortgage/Loan Provider

Borrowers

Type of loan(capital repayment / interest only)

Current amount outstanding £

Current interest rate % p.a.

Redemption date / /

Original loan amount £

Start date / /Monthly payment £

Early Repayment Charges Yes/No

Term remaining

Second Home (Other Than Buy to Let)

Mortgage/Loan Provider

Description/Address

Borrowers

Type of loan(capital repayment / interest only)

Current amount outstanding £

Current interest rate % p.a.

Redemption date / /

Original loan amount £

Start date / /

Monthly payment £

Early Repayment Charges Yes/No

Term remaining

Mortgage July 2016 23

Buy to Let property (If applicable)

Mortgage/Loan Provider

Description/Address

Borrowers

Type of loan(capital repayment / interest only)

Current amount outstanding £

Current interest rate % p.a.

Redemption date / /

Original loan amount £

Start date / /

Monthly payment £

Early Repayment Charges Yes/No

Term remaining

Buy to Let property (If applicable)

Mortgage/Loan Provider

Description/Address

Borrowers

Type of loan(capital repayment / interest only)

Current amount outstanding £

Current interest rate % p.a.

Redemption date / /

Original loan amount £

Start date / /

Monthly payment £

Early Repayment Charges Yes/No

Term remaining

Mortgage July 2016 24

Buy to Let property (If applicable)

Mortgage/Loan Provider

Description/Address

Borrowers

Type of loan(capital repayment / interest only)

Current amount outstanding £

Current interest rate % p.a.

Redemption date / /

Original loan amount £

Start date / /

Monthly payment £

Early Repayment Charges Yes/No

Term remaining

Buy to Let property (If applicable)

Mortgage/Loan Provider

Description/Address

Borrowers

Type of loan(capital repayment / interest only)

Current amount outstanding £

Current interest rate % p.a.

Redemption date / /

Original loan amount £

Start date / /

Monthly payment £

Early Repayment Charges Yes/No

Term remaining

Mortgage July 2016 25

CREDIT CARD DETAILS

Description of card/Bank

Cardholder

Current balance £ £

Monthly Payment

To be repaid Yes/No Yes/No

Description of card/Bank

Cardholder

Current balance £ £

Monthly Payment

To be repaid Yes/No Yes/No

Description of card/Bank

Cardholder

Current balance £ £

Monthly Payment

To be repaid Yes/No Yes/No

Description of card/Bank

Cardholder

Current balance £ £

Monthly Payment

To be repaid Yes/No Yes/No

Mortgage July 2016 26

Personal Loans

Lender

Current balance £ £

Monthly Payment £ £

To be cleared Yes/No Yes/No

Lender

Current balance £ £

Monthly Payment £ £

To be cleared Yes/No Yes/No

Lender

Current balance £ £

Monthly Payment £ £

To be cleared Yes/No Yes/No

Lender

Current balance £ £

Monthly Payment £ £

To be cleared Yes/No Yes/No

Mortgage July 2016 27

PROFESSIONAL ADVISERS

Name of adviser

Name of practice

Profession

Address

Telephone number

Name of adviser

Name of practice

Profession

Address

Telephone number

Name of adviser

Name of practice

Profession

Address

Telephone number

Mortgage July 2016 28

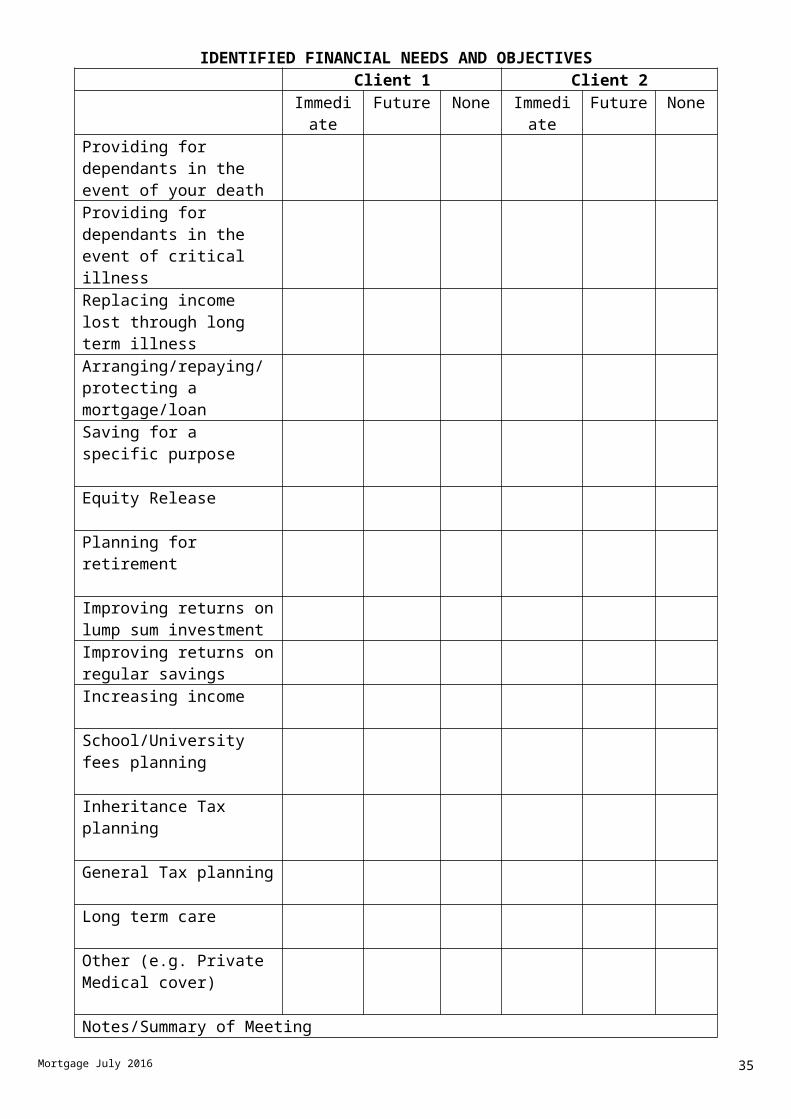

IDENTIFIED FINANCIAL NEEDS AND OBJECTIVESClient 1 Client 2

Immediate

Future None Immediate

Future None

Providing for dependants in the event of your deathProviding for dependants in the event of critical illnessReplacing income lost through long term illnessArranging/repaying/protecting a mortgage/loanSaving for a specific purpose

Equity Release

Planning for retirement

Improving returns on lump sum investmentImproving returns on regular savingsIncreasing income

School/University fees planning

Inheritance Tax planning

General Tax planning

Long term care

Other (e.g. Private Medical cover)

Notes/Summary of Meeting

Mortgage July 2016 29

Mortgage July 2016 30

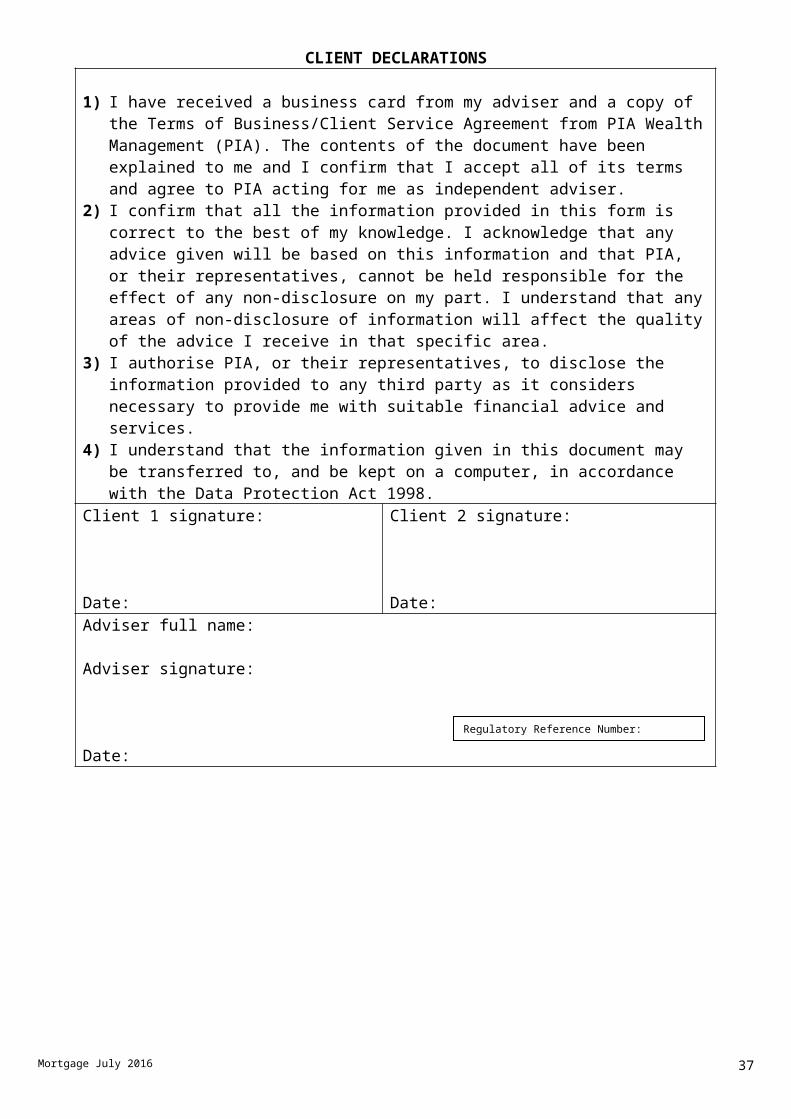

CLIENT DECLARATIONS

1) I have received a business card from my adviser and a copy of the Terms of Business/Client Service Agreement from PIA Wealth Management (PIA). The contents of the document have been explained to me and I confirm that I accept all of its terms and agree to PIA acting for me as independent adviser.

2) I confirm that all the information provided in this form is correct to the best of my knowledge. I acknowledge that any advice given will be based on this information and that PIA, or their representatives, cannot be held responsible for the effect of any non-disclosure on my part. I understand that any areas of non-disclosure of information will affect the quality of the advice I receive in that specific area.

3) I authorise PIA, or their representatives, to disclose the information provided to any third party as it considers necessary to provide me with suitable financial advice and services.

4) I understand that the information given in this document may be transferred to, and be kept on a computer, in accordance with the Data Protection Act 1998.

Client 1 signature:

Date:

Client 2 signature:

Date:Adviser full name:

Adviser signature:

Date:

Mortgage July 2016

Regulatory Reference Number:

31

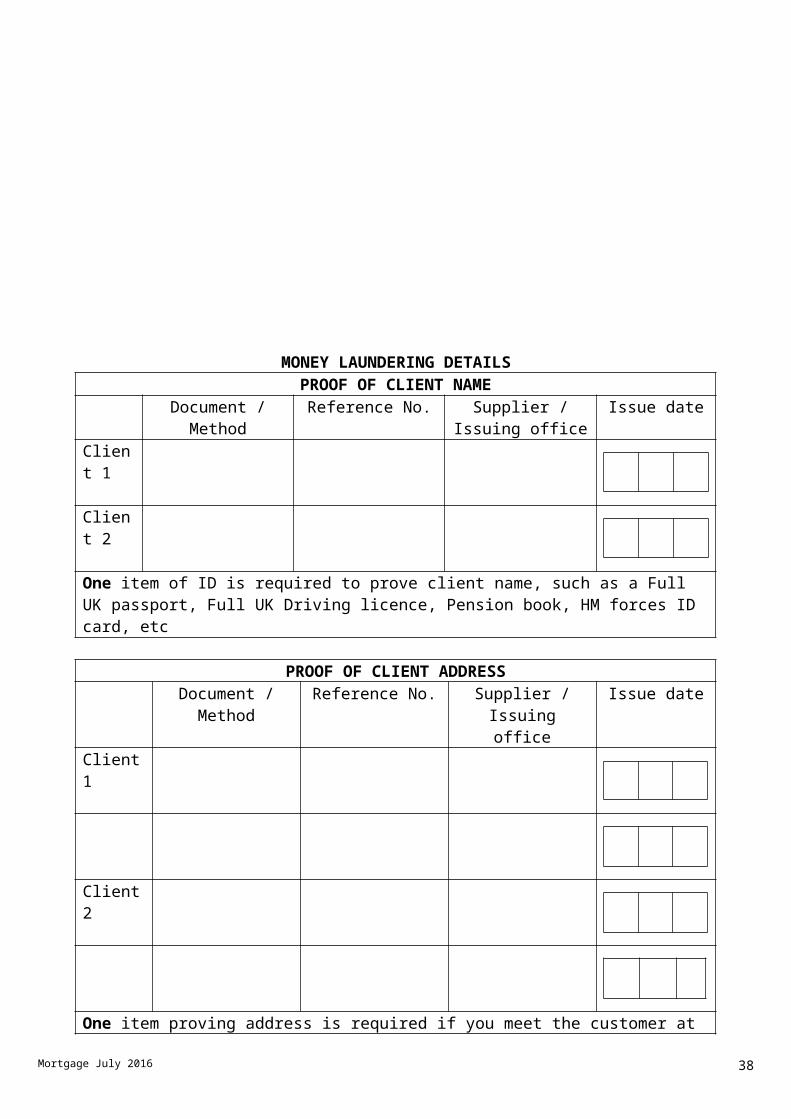

MONEY LAUNDERING DETAILSPROOF OF CLIENT NAME

Document / Method

Reference No. Supplier / Issuing office

Issue date

Client 1

Client 2

One item of ID is required to prove client name, such as a Full UK passport, Full UK Driving licence, Pension book, HM forces ID card, etc

PROOF OF CLIENT ADDRESSDocument /

MethodReference No. Supplier /

Issuing officeIssue date

Client 1

Client 2

One item proving address is required if you meet the customer at that address. (Utility Bill, mortgage statement, credit card bill, etc.). Two items proving address are required if you do not meet the customer at that address. No single document can be used to confirm both name and address.

Mortgage July 2016 32

CLIENT AUTHORITY FORMS

Please fill in with details of existing policies and plans that we do not arrange ourselves in order for us to obtain information on your behalf

Insurance company name and address

Client name, address, DoB and NI number

Policy Number(s)

DoB: / /

NI no:

Please note that I have appointed PIA Wealth Management as my independent financial adviser. Please treat them as my servicing agent in respect of all my policies held with you, release any information that they may request from time to time, and redirect any renewal, trail or fund-based commission to their agency. PIA have confirmed that they will provide a full on-going review service in line with the Retail Distribution Review (From Jan2013) and their Client Servicing Agreement.

Name……………………………………….. Name……………………………………………

Signed………………………………….......... Signed…………………………………………...

Dated……………………………………… Dated……………………………………………

Insurance company name and address

Client name, address, DoB and NI number

Policy Number(s)

DoB: / /

NI no:

Please note that I have appointed PIA Wealth Management as my independent financial adviser. Please treat them as my servicing agent in respect of all my policies held with you, release any information that they may request from time to time, and redirect any renewal, trail or fund-based commission to their agency. PIA have confirmed that they will provide a full

Mortgage July 2016 33

on-going review service in line with the Retail Distribution Review (From Jan2013) and their Client Servicing Agreement.

Name……………………………………….. Name……………………………………………

Signed………………………………….......... Signed…………………………………………...

Dated……………………………………… Dated……………………………………………

Mortgage July 2016 34

Insurance company name and address

Client name, address, DoB and NI number

Policy Number(s)

DoB: / /

NI no:

Please note that I have appointed PIA Wealth Management as my independent financial adviser. Please treat them as my servicing agent in respect of all my policies held with you, release any information that they may request from time to time, and redirect any renewal, trail or fund-based commission to their agency. PIA have confirmed that they will provide a full on-going review service in line with the Retail Distribution Review (From Jan2013) and their Client Servicing Agreement.

Name……………………………………….. Name……………………………………………

Signed………………………………….......... Signed…………………………………………...

Dated……………………………………… Dated……………………………………………

Insurance company name and address

Client name, address, DoB and NI number

Policy Number(s)

Mortgage July 2016 35

DoB: / /

NI no:

Please note that I have appointed PIA Wealth Management as my independent financial adviser. Please treat them as my servicing agent in respect of all my policies held with you, release any information that they may request from time to time, and redirect any renewal, trail or fund-based commission to their agency. PIA have confirmed that they will provide a full on-going review service in line with the Retail Distribution Review (From Jan2013) and their Client Servicing Agreement.

Name……………………………………….. Name……………………………………………

Signed………………………………….......... Signed…………………………………………...

Dated……………………………………… Dated……………………………………………

Mortgage July 2016 36

Mortgage July 2016 37

Date: _____________________________________________

Property Address: _____________________________________________

____________________________Mortgage Type: Re-mortgage / Purchase / Further Advance / Product Transfer / Buy to Let

Supplementary Pages for Mortgages

Financial Services & Market Act 2000Independent Financial Advisers are required to have proper regard for a client’s best interests in any advice given. They must therefore do their utmost to ensure that they are aware of your personal and financial circumstances so that their advice is the most suitable for your needs. The questions here have been specifically designed to help your adviser provide advice that meets your needs. If, for any reason, you decline to answer any or all of the questions or if you fail to provide true and accurate information to the best of your knowledge, the advice given subsequently may not be best advice, as it can only be based on the information provided.

Data Protection Act – Disclosure of InformationThe information given in this document will be retained on computer for reference purposes, and will be held in accordance with the Data protection Act 1998. More information is contained within our Terms of Business letter.

Authorised and Regulated by the Financial Conduct Authority

THE INFORMATION ON THIS FORM IS INSUFFICIENT FOR ADVICE TO BE GIVEN IN ANY AREA WITHOUT THE MAIN FINANCIAL REVIEW HAVING BEEN COMPLETED.

CURRENT MORTGAGE DETAILS

First ApplicantSecond Applicant

a) Lender & Account No

b) Amt of loan o/s £ £c) Term remaining

Years Yearsd) Repayment method Interest only / C & I repayment / Split

I O £____________ C & I £ ____________Interest only / C & I repayment / SplitI O £____________ C & I £ ____________

e) Current rate & amount % £ per month % £ per month

f) Interest rate & type

If 2, 3 or 4 applies, when does rate end?

1/Variable 2/Discount 3/Capped 4/Fixed 5/Offset

________________________________________

1/Variable 2/Discount 3/Capped 4/Fixed 5/Offset

________________________________________g) If selling, what’s price? £ £h) Are there penalties if you trf or repay your existing mortgage now? If yes, how much

Interest Yes / No

Cashback Yes / No

£

Interest Yes / No

Cashback Yes / No

£

i) Are you prepared to pay penalties if you transfer/ repay current mortgage? Yes / No Yes / No

Mortgage July 2016 38

PROPERTY TO BE MORTGAGEDWill this be the only property you own or have a mortgage on?

If ‘No’ please explain

Yes / No Yes / No

Address of property to be mortgaged:

Postcode: Postcode:Price of property being purchased £ Estimated Value £How much do you want to borrow? £ Over what term? YearsDoes this include the addition of fees? Yes / No If ‘yes’ how much is to be added? £Property type: Freehold / Leasehold / Bungalow / Flat / MaisonetteDo you have the funds available to complete this transaction?

Amount of funds available

Source of funds available

Is the vendor/builder paying your deposit?

Yes / No

£_____________________________________________________

______________________________________________________

Yes / NoIf you are purchasing under Right-to-Buy legislation

a) Estimated value

b) Are you borrowing more than the purchase price?

If ‘yes’ please provide approximate cost and brief details

£_____________________________________________________

Yes / No

£_____________________________________________________

______________________________________________________

___________________________________________________________________

Is this a buy-to-let property? If so:-

a) What is the expected rental

Yes / No

£ ____________________________________________________

If you are buying on a Shared Ownership scheme:

a) Percentage of property to be purchased

b) Which Shared Ownership body are you buying from?

c) New Build. Government Equity Scheme

___________ %

______________________________________________________

______________ %

Are any home improvements planned?

If ‘yes’ please provide brief details and approximate costs

Yes / No

______________________________________________________

______________________________________________________

First Applicant Second ApplicantHave you ever had a mortgage or a loan application refused? Yes / No Yes / No

Have you ever had a judgement for a debt of a loan default registered against you?

Yes / No Yes / No

Have you ever been declared bankrupt or made an arrangement with your creditors?

Yes / No Yes / No

Have you ever failed to keep up your payment under any previous or current mortgage, rental or loan agreement?

Yes / No Yes / No

Mortgage July 2016 39

Key Information About the Type of

Mortgage Applicable to You

In order to give you a high standard of service, we need to understand your requirement, attitudes and objectives to help us to provide you with a mortgage fitting your needs and relevant to your circumstances. State a reason where you answer ‘Yes’.

1 Might your income or expenditure change significantly within the foreseeable future?

IncomeApproximate timescale / Amount / Reason _____________________________________________________________________________________________________________

Yes / No

ExpenditureApproximate timescale / Amount / Reason _____________________________________________________________________________________________________________

Yes / No

2 Do you have any plans to pay off some or the entire mortgage in the foreseeable future? Yes / No

Approximate Amount £ _____________________________________________________Approximate timescale / Reason ______________________________________________________________________________________________________________________

3 Are you likely to move home within the mortgage term (other than this transaction)? Yes / No

Larger / SmallerApproximate timescale / Reason ______________________________________________________________________________________________________________________

4 Please indicate the features most important to you:

An upper limit on your mortgage costs for a specific periodReason: _________________________________________________________________

Yes / No

To fix your mortgage costs for a certain period Reason: _________________________________________________________________

Yes / No

Access to an initial cash sum (known as a Cashback) Reason: _________________________________________________________________

Yes / No

A discount on your mortgage repayments in the early years Reason: _________________________________________________________________

Yes / No

No early settlement interest on full or part repayment Reason: _________________________________________________________________

Yes / No

No tie-in after a fixed, discounted or capped interest period Reason: _________________________________________________________________

Yes / No

Use of an offset facilityReason: _________________________________________________________________

Yes / No

Speed of mortgage completion Reason: _________________________________________________________________

Yes / No

Ability to add fees to the loan Reason: _________________________________________________________________

Yes / No

Ability to vary the repayment amount or take repayment holidays Reason: _________________________________________________________________

Yes / No

Mortgage July 2016 40

5 Please indicate whether :-

You are concerned about the possibility of future interest rate movements Reason: _________________________________________________________________

Yes / No

You want the certainty of your mortgage being repaid at the end of the term Reason: _________________________________________________________________

Yes / No

You are comfortable if all or part of your mortgage is repaid from the proceeds of an investment product, i.e. an Endowment, ISA, Pension, Buy to Let? Reason: _________________________________________________________________

Yes / No /All / Part

6 Are you comfortable to have a mortgage outstanding past Normal Retirement Date Yes / No

Means of repayment into retirement ________________________________________

________________________________________________________________________

________________________________________________________________________

7 Changes in personal circumstances, such as loss of income, can lead to you being unable to repay all or part of your mortgage commitments

Do you require payment protection insurance? Yes / No

If ‘Yes’:-

How much repayment cover do you require? Full / Part

Do you want the benefit payment to be in excess of the mortgage repayment? Yes / No

Is the cover to be for joint applicants or a single applicant? Joint / Single

Objectives:

Reason for Recommendation:

Mortgage July 2016 41

Interest Only Mortgage Questionnaire

Client(s) Name

Date

Mortgage repayment breakdown summary

Capital and interest £Investment-backed interest-only £Uncovered interest-only £Total loan £

Part 1: Uncovered interest-only mortgage questionnaire

Will the mortgaged property be used as your main residence?

If not the main residence, please describe below how you intend to use the property:

Please explain below, in as much detail as you can, the reason(s) why you wish to arrange part, or all, of this mortgage on an uncovered interest-only basis:

TICK ONE OR MORE OF THE OPTIONS, THEN GIVE MORE DETAIL IN BOX :PLAN FOR REPAYING UNCOVERED INTEREST-ONLY DEBT risks TickMortgaged property is not main residence, so it can always be sold in absence of any other plan to repay interest-only debt

I / We am / are already retired, and the mortgage debt will be repaid from estate after death

Convert the uncovered interest-only element to repayment when affordable (max timeframe 5 years) 8, 9, 12, 13

Save up regularly, and use money to pay occasional lump sums to the mortgage account over the next few years 2, 3, 4

Use bonuses to pay lump sums to reduce the loan amount. 2, 3, 13Set monthly payment into mortgage account above interest-only level, to gradually reduce debt 2, 4

I / We own one or more additional properties, which will be sold to release money to repay debt on main residence 6, 7

Sell assets (other than property) to release funds to repay the uncovered interest-only debt 7

I / We expect to inherit enough money to cover the uncovered interest-only debt 5

Renovate the mortgaged property and sell it on at a profit within the next three years 11

Sell property and release funds to repay debt by moving to a smaller/cheaper home 10

Sell property and move overseas within the next five years 8

Put off decision about how to repay debt until the next house move (or perhaps the one after that) 1, 8, 9, 12

Use this box to add further detail about the option you’ve ticked, or to explain any other debt repayment plan not included in the table.

Mortgage July 2016 42

RISK FACTORS MOST RELEVANT TO EACH DEBT REPAYMENT PLAN LISTED ON THE PREVIOUS PAGE:SPECIFIC RISK FACTOR(S)

1

Your mortgage will end up costing you more in the long run. If you have borrowed a high percentage of the value of your home, you are relying on house price inflation to clear the current loan, pay for your moving costs, and leave enough equity to buy another property. You may find that your next home is unaffordable, particularly if you are hoping to move up the housing ladder.

2 Many lenders impose early repayment charges on their products – including on regular and lump sum overpayments.

3. If you are counting on putting money into a savings account to use for lump sum repayments, are you sure you’ll be able to afford it and that you’ll have the necessary self-discipline?

4 You should also consider a flexible mortgage, arranged on a repayment basis, that allows you to vary your monthly payments, or even take payment holidays.

5 Unless you are the beneficiary of an estate already going through probate, you cannot guarantee how much you will end up inheriting (if anything), or how long it will be before the money becomes available.

6 It may not be prudent to rely on house price inflation to let you clear any charges on the separate property, PLUS the new mortgage.

7The asset might not be readily sellable, or may fall in value. If it is a property, you need to be confident that there will be sufficient equity available to cover the costs of selling (including clearing any mortgage on it), as well as the sum needed to repay the uncovered debt on your main home.

8If you don’t get round to doing anything to ensure repayment of the debt at the end of the term, you may find that the lender will force the sale of your property to get its money back. If that happened, you would

lose your home and may be forced to rent, or buy somewhere much smaller/cheaper.

9

The longer you wait to switch to a repayment loan (particularly if you want to keep the term the same) the larger the jump in your monthly repayment is likely to be. If the reason you want interest-only to start with is so you can afford the mortgage, affordability may well continue to be a problem. Your salary, and general financial position, might not improve as quickly as you are hoping it will.

10

It may not be safe to assume that downsizing (after moving costs) will repay the whole loan. When it comes to the crunch, you may not want to downsize to clear the debt. Downsizing to release funds to boost your income/lifestyle in retirement is one thing, but being forced to do so just to clear your debts is quite another. This is not considered to be sensible financial planning. If you end up downsizing to help repay your mortgage, it is hard to see what you will have really achieved by borrowing so much, apart from living beyond your means for a few years.

11

Property renovation might not achieve the profits you are hoping for, especially if the work turns out to be more difficult and expensive than expected and/or the property market goes against you. Have you got enough money to cover the renovation costs? Could you afford to switch to repayment later on if your plans go awry?

12

The longer you leave it before you start repaying the debt, the more expensive the loan will end up being, and the bigger the eventual jump in monthly repayments you’ll need to make. You might find that, because you have not made any inroads into your debt during the early years, this limits your ability to move up the property ladder in future.

13Unless you have a written guarantee you are going to receive a bonus and / or salary increase sufficient to make a difference, reliance on this may not be in your interests. How can you be sure the money will become available?

BASIS OF RECOMMENDATIONTICK ONE OF THE OPTIONS BELOW

Adviser recommends that I arrange part/all of the mortgage on an uncovered interest-only basis.

Adviser recommends a different repayment method, (to be described in suitability letter) but I wanted to arrange (part of) the loan on an uncovered interest-only basis.

Mortgage July 2016 43

APPLICANT DECLARATIONS (tick boxes) Self Partner

1 I UNDERSTAND THAT MY HOME IS AT RISK IF I FAIL TO EITHER KEEP UP REPAYMENTS DURING THE TERM OF THE MORTGAGE OR REPAY THE CAPITAL AMOUNT OF THE LOAN AT THE END.

2 I confirm that my plan to repay the uncovered interest-only debt is accurately described in this questionnaire

3 I understand it is my responsibility to put that plan into effect

4The adviser has explained the risk factors that are most relevant in my case (i.e. the risks numbered against my selected “Plan for Repaying uncovered interest-only loan”).

5

I understand that my adviser recommends capital and repayment as the most suitable arrangement for me. However, I wanted part / all of my mortgage on an uncovered interest-only basis and understand that this may be less suitable.

Name (1st Applicant)

SignatureDate

Name (2nd Applicant)

SignatureDate

Additional notes box (e.g, to explain adviser’s recommendation to use interest-only)

Mortgage July 2016 44

Part 2: Investment-backed interest-only mortgage questionnaire(NB: For use only in cases where no investment advice is being provided)

Part 2A: Complete When Customer Using Existing Investment To Repay Part/All Of Loan

The value of investments may go down as well and up and you may not get as much at maturity as you expected to clear the debt.

If the arrangement involves you making specified regular payments, you must ensure you keep making these payments.

WHAT TYPE OF EXISTING INVESTMENT(S) DO YOU INTEND TO USE? (Tick ALL that apply)

Endowment policy

Personal pension

Equity ISA/PEP

Other

- If ‘Other’, please describe

Have you provided details of the existing investment(s) being used?

IF ‘YES’, RECORD DETAILS OF EXISTING INVESTMENT(S) BEING USED TO REPAY THE LOAN

Type of contract

Sum assured or min death

benefit

Lives assured or policyholder

Policy number

Maturity date

Projected value at end term (state assumed % growth

rate)£££

How much of the mortgage do you wish to cover using the existing investments? £

APPLICANT DECLARATIONS (tick boxes) Self Partner

I understand that I have not been provided with investment advice about whether to rely on my existing investments to repay my mortgage debt

I understand that it’s my responsibility to monitor the progress of my investment(s) to make sure they will fully cover the amount of mortgage debt I intend them to repay.

I understand that my home is at risk if I fail to either keep up repayments during the term of the mortgage or repay the capital amount of the loan at the end.

Name (1st Applicant)

SignatureDate

Name (2nd Applicant)

SignatureDate

Mortgage July 2016 45

Part 2B: Complete When Customer Arranging A New Investment To Repay Part / All Of Loan

The value of investments may go down as well and up and you may not get as much at maturity as you expected to clear the debt.

If the arrangement involves you making specified regular payments, you must ensure you keep making these payments.

WHAT TYPE OF INVESTMENT DO YOU INTEND TO ARRANGE? (Tick ALL that apply)

Endowment policy

Personal pension

Equity ISA

Other

- If ‘Other’, please describe

APPLICANT DECLARATIONS (tick boxes) SELF PartnerI understand that it is my responsibility to make sure that I do arrange a

suitable investment to repay my mortgage

I understand that, once it has been set up, I need to monitor it regularly to make sure it remains on track to cover the amount of debt it is intended to

repay

I understand that my home is at risk if I fail to either keep up repayments during the term of the mortgage or repay the capital amount of the loan at the end.

Name (1st Applicant)

SignatureDate

Name (2nd Applicant)

SignatureDate

Adviser to use this box to add any additional notes about the customer’s plans

Mortgage July 2016 46