Embed Size (px)

Citation preview

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 1

BANK OF AMERICA MERRILL LYNCH E&P AND OIL SERVICES CONFERENCE 22 November 2012

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 2

Disclaimer

Important Notice Nothing in this presentation or in any accompanying management discussion of this presentation (the "Presentation") constitutes, nor is it intended to constitute: (i) an invitation or inducement to engage in any investment activity, whether in the United Kingdom or in any other jurisdiction; (ii) any recommendation or advice in respect of the ordinary shares (the "Shares") in Bowleven plc (the "Company"); or (iii) any offer for the sale, purchase or subscription of any Shares. The Shares are not registered under the US Securities Act of 1933 (as amended) (the "Securities Act") and may not be offered, sold or transferred except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and in compliance with any other applicable state securities laws. The Presentation may include statements that are, or may be deemed to be "forward-looking statements". These forward-looking statements can be identified by the use of forward-looking terminology, including the terms "believes", "estimates", "anticipates", "projects", "expects", "intends", "may", "will", "seeks" or "should" or, in each case, their negative or other variations or comparable terminology, or by discussions of strategy, plans, objectives, goals, future events or intentions. These forward-looking statements include all matters that are not historical facts. They include statements regarding the Company's intentions, beliefs or current expectations concerning, amongst other things, the results of operations, financial conditions, liquidity, prospects, growth and strategies of the Company and its direct and indirect subsidiaries (the “Group”) and the industry in which the Group operates. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Forward-looking statements are not guarantees of future performance. The Group’s actual results of operations, financial conditions and liquidity, and the development of the industry in which the Group operates, may differ materially from those suggested by the forward-looking statements contained in the Presentation. In addition, even if the Group’s results of operations, financial conditions and liquidity, and the development of the industry in which the Group operates, are consistent with the forward-looking statements contained in the Presentation, those results or developments may not be indicative of results or developments in subsequent periods. In light of those risks, uncertainties and assumptions, the events described in the forward-looking statements in the Presentation may not occur. Other than in accordance with the Company's obligations under the AIM Rules for Companies, the Company undertakes no obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future events or otherwise. All written and oral forward-looking statements attributable to the Company or to persons acting on the Company's behalf are expressly qualified in their entirety by the cautionary statements referred to above and contained elsewhere in the Presentation.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 3

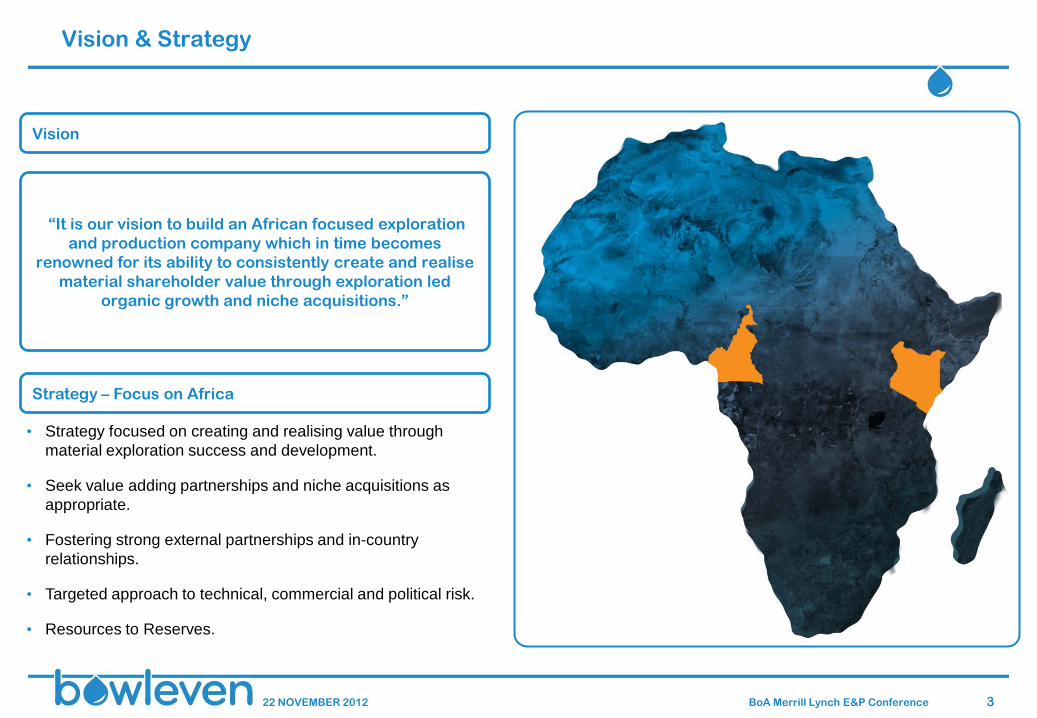

Vision & Strategy

• Strategy focused on creating and realising value through material exploration success and development.

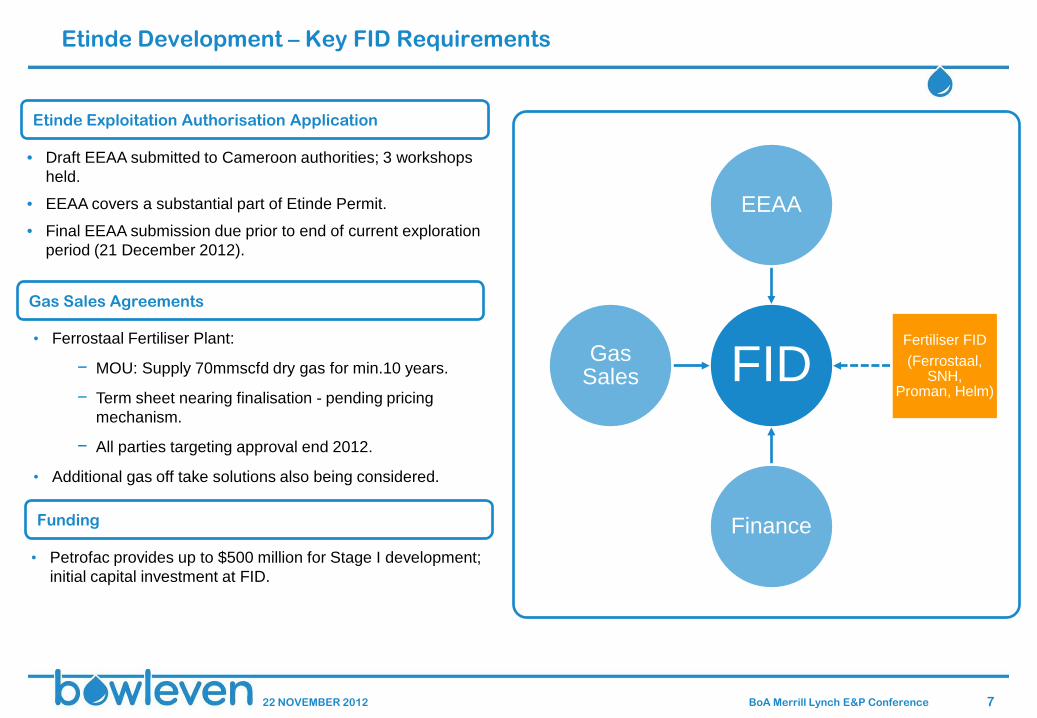

• Seek value adding partnerships and niche acquisitions as appropriate.

• Fostering strong external partnerships and in-country relationships.

• Targeted approach to technical, commercial and political risk.

• Resources to Reserves.

Vision

Strategy – Focus on Africa

“It is our vision to build an African focused exploration and production company which in time becomes

renowned for its ability to consistently create and realise material shareholder value through exploration led

organic growth and niche acquisitions.”

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 4

Company Overview

• 5 blocks in Cameroon covering 4,644km².

• 3 offshore shallow water, 2 onshore; all operated.

• Multiple hydrocarbon discoveries.

• P50 contingent resource base 203 mmboe* (net).

• Phased Hub & Spoke development planned.

• Continued exploration of the Douala Basin.

Cameroon

• Block 11B onshore Kenya covering ~14,000km².

• Early stage exploration; Airborne geophysical survey and 2D seismic acquisition.

• Operated by Adamantine Energy, technical support provided by Bowleven under a TSA.

* Source: Preliminary Results Announcement 6 Nov 2012. Operator’s volumetrics.

Kenya

Kenya

Ethiopia

State back-in rights: Etinde 20%, Bomono 10% (at grant of exploitation licence).

Acreage: 2,316km2

Shallow OffshoreEquity Interest:

75% (Vitol 25%)Operator:

Bowleven Group

Etinde Permit

Acreage: 2,328km2

OnshoreEquity Interest:

100%Operator:

Bowleven Group

Bomono Permit

Nigeria

Cameroon

Acreage: ~14,000km2

OnshoreEquity Interest: 50%

(Adamantine 50%)Operator:

Adamantine

Block 11B

South Sudan

Corporate

• Cash end October 2012 ~$120 million, no debt.

• Petrofac: up to $500 million for Stage I development.

• High equity positions provide farm-out flexibility.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 5

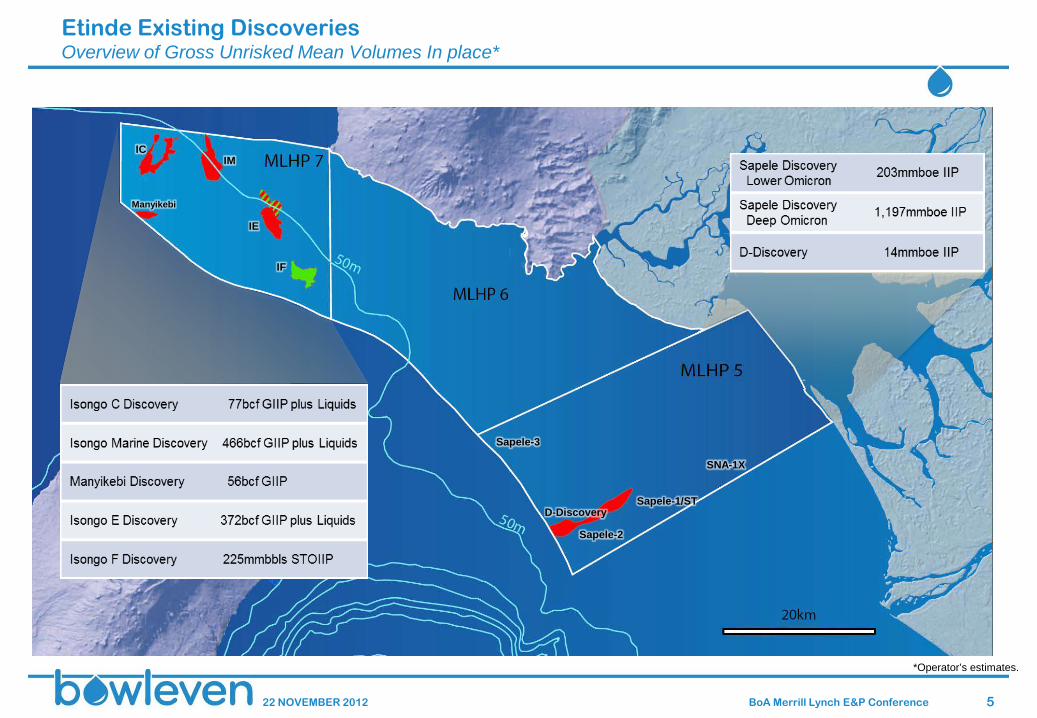

Etinde Existing Discoveries Overview of Gross Unrisked Mean Volumes In place*

Deep Omicron fairway

*Operator’s estimates.

IC

IF

IE

IM

Manyikebi

Sapele-3

Sapele-2

Sapele-1/ST

SNA-1X

D-Discovery

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 6

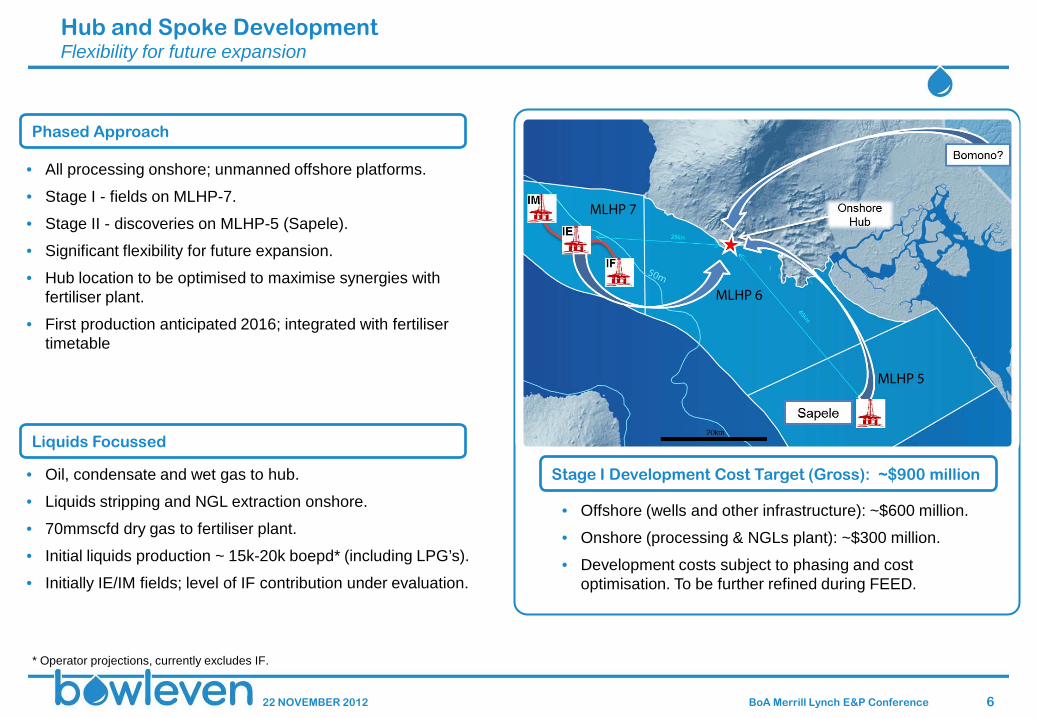

Hub and Spoke Development Flexibility for future expansion

• All processing onshore; unmanned offshore platforms.

• Stage I - fields on MLHP-7.

• Stage II - discoveries on MLHP-5 (Sapele).

• Significant flexibility for future expansion.

• Hub location to be optimised to maximise synergies with fertiliser plant.

• First production anticipated 2016; integrated with fertiliser timetable

• Offshore (wells and other infrastructure): ~$600 million.

• Onshore (processing & NGLs plant): ~$300 million.

• Development costs subject to phasing and cost optimisation. To be further refined during FEED.

Stage I Development Cost Target (Gross): ~$900 million

Phased Approach

• Oil, condensate and wet gas to hub.

• Liquids stripping and NGL extraction onshore.

• 70mmscfd dry gas to fertiliser plant.

• Initial liquids production ~ 15k-20k boepd* (including LPG’s).

• Initially IE/IM fields; level of IF contribution under evaluation.

Liquids Focussed

* Operator projections, currently excludes IF.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 7

Etinde Development – Key FID Requirements

• Petrofac provides up to $500 million for Stage I development; initial capital investment at FID.

Funding

†

• Draft EEAA submitted to Cameroon authorities; 3 workshops held.

• EEAA covers a substantial part of Etinde Permit.

• Final EEAA submission due prior to end of current exploration period (21 December 2012).

Etinde Exploitation Authorisation Application

• Ferrostaal Fertiliser Plant:

− MOU: Supply 70mmscfd dry gas for min.10 years.

− Term sheet nearing finalisation - pending pricing mechanism.

− All parties targeting approval end 2012.

• Additional gas off take solutions also being considered.

Gas Sales Agreements

FID

EEAA

Fertiliser FID (Ferrostaal,

SNH, Proman, Helm)

Finance

Gas Sales

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 8

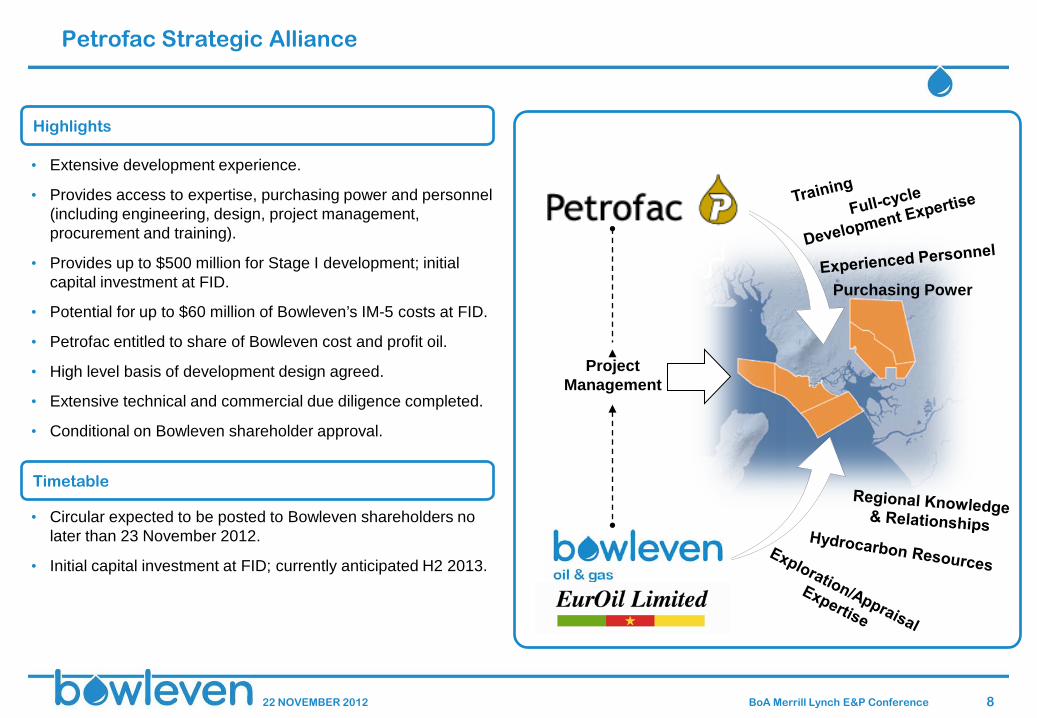

Petrofac Strategic Alliance

• Extensive development experience.

• Provides access to expertise, purchasing power and personnel (including engineering, design, project management, procurement and training).

• Provides up to $500 million for Stage I development; initial capital investment at FID.

• Potential for up to $60 million of Bowleven’s IM-5 costs at FID.

• Petrofac entitled to share of Bowleven cost and profit oil.

• High level basis of development design agreed.

• Extensive technical and commercial due diligence completed.

• Conditional on Bowleven shareholder approval.

Highlights

Timetable

• Circular expected to be posted to Bowleven shareholders no later than 23 November 2012.

• Initial capital investment at FID; currently anticipated H2 2013.

Purchasing Power

Project Management

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 9

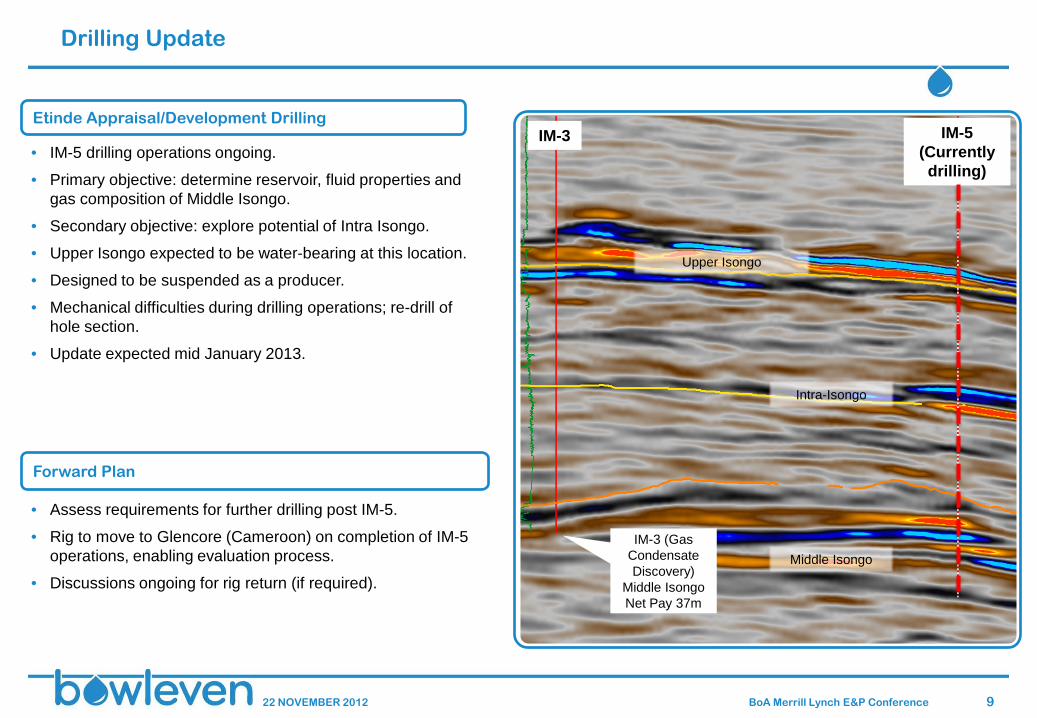

Drilling Update

• IM-5 drilling operations ongoing.

• Primary objective: determine reservoir, fluid properties and gas composition of Middle Isongo.

• Secondary objective: explore potential of Intra Isongo.

• Upper Isongo expected to be water-bearing at this location.

• Designed to be suspended as a producer.

• Mechanical difficulties during drilling operations; re-drill of hole section.

• Update expected mid January 2013.

Etinde Appraisal/Development Drilling

Forward Plan

IM-5 (Currently drilling)

IM-3

Middle Isongo

Intra-Isongo

• Assess requirements for further drilling post IM-5.

• Rig to move to Glencore (Cameroon) on completion of IM-5 operations, enabling evaluation process.

• Discussions ongoing for rig return (if required).

Upper Isongo

IM-3 (Gas Condensate Discovery)

Middle Isongo Net Pay 37m

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 10

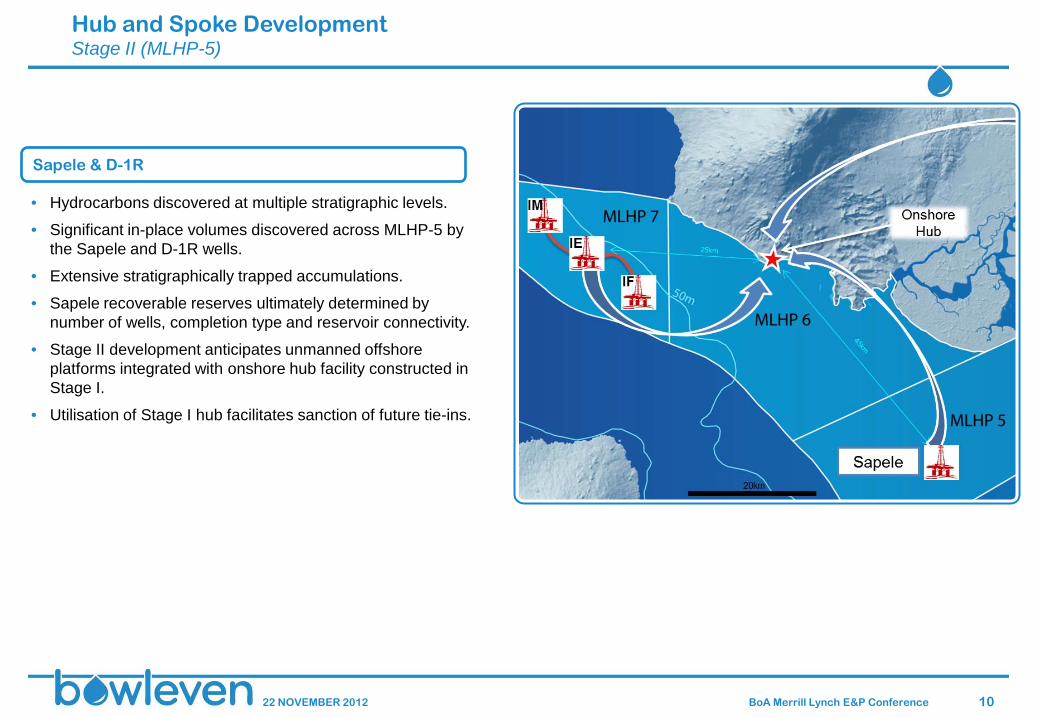

• Hydrocarbons discovered at multiple stratigraphic levels.

• Significant in-place volumes discovered across MLHP-5 by the Sapele and D-1R wells.

• Extensive stratigraphically trapped accumulations.

• Sapele recoverable reserves ultimately determined by number of wells, completion type and reservoir connectivity.

• Stage II development anticipates unmanned offshore platforms integrated with onshore hub facility constructed in Stage I.

• Utilisation of Stage I hub facilitates sanction of future tie-ins.

Sapele & D-1R

Hub and Spoke Development Stage II (MLHP-5)

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 11

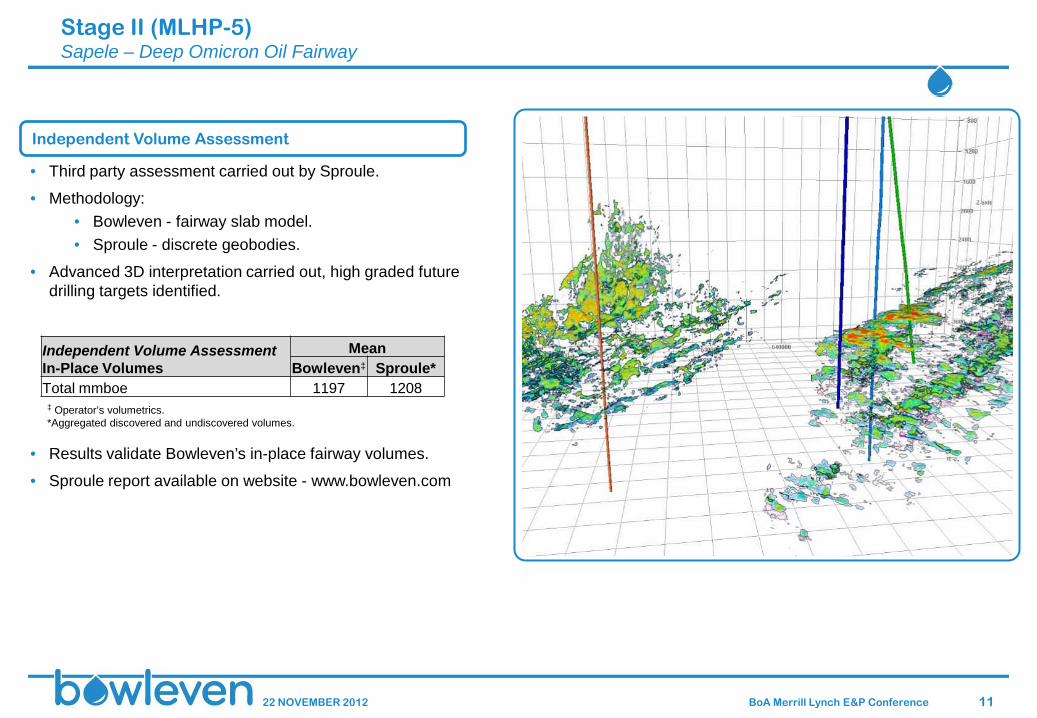

Stage II (MLHP-5) Sapele – Deep Omicron Oil Fairway

Independent Volume Assessment

• Third party assessment carried out by Sproule.

• Methodology: • Bowleven - fairway slab model. • Sproule - discrete geobodies.

• Advanced 3D interpretation carried out, high graded future drilling targets identified.

• Results validate Bowleven’s in-place fairway volumes.

• Sproule report available on website - www.bowleven.com

Independent Volume Assessment In-Place Volumes

Mean Bowleven‡ Sproule*

Total mmboe 1197 1208 ‡ Operator’s volumetrics. *Aggregated discovered and undiscovered volumes.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 12

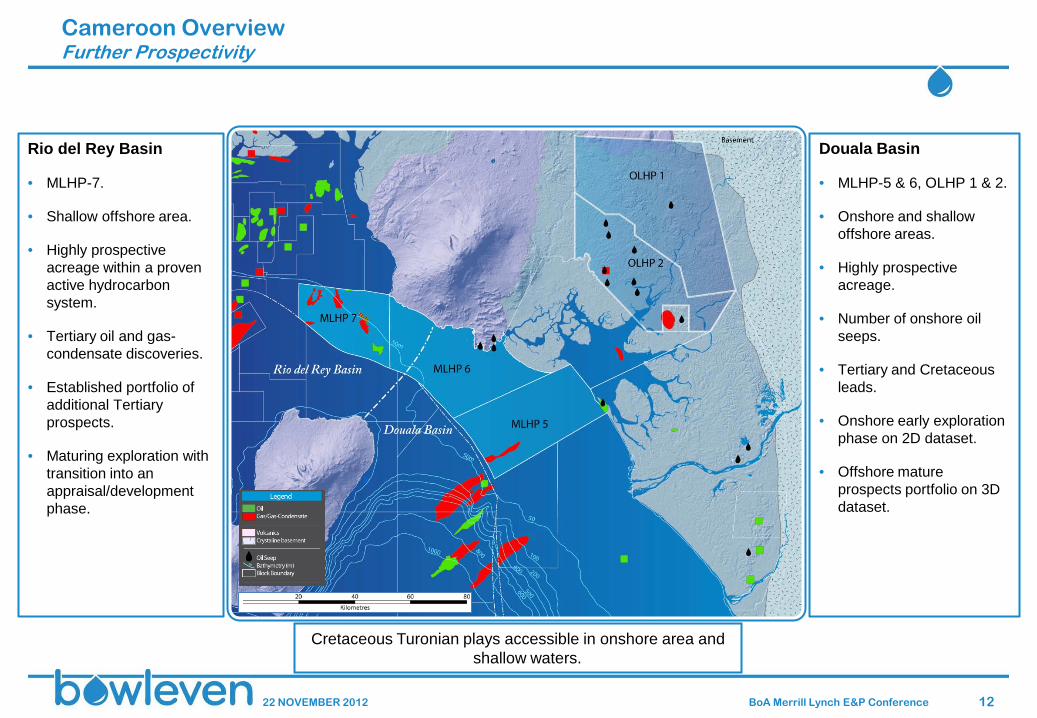

Cameroon Overview Further Prospectivity

Douala Basin

• MLHP-5 & 6, OLHP 1 & 2.

• Onshore and shallow offshore areas.

• Highly prospective acreage.

• Number of onshore oil seeps.

• Tertiary and Cretaceous leads.

• Onshore early exploration phase on 2D dataset.

• Offshore mature prospects portfolio on 3D dataset.

Rio del Rey Basin

• MLHP-7.

• Shallow offshore area.

• Highly prospective acreage within a proven active hydrocarbon system.

• Tertiary oil and gas-condensate discoveries.

• Established portfolio of additional Tertiary prospects.

• Maturing exploration with transition into an appraisal/development phase.

Cretaceous Turonian plays accessible in onshore area and shallow waters.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 13

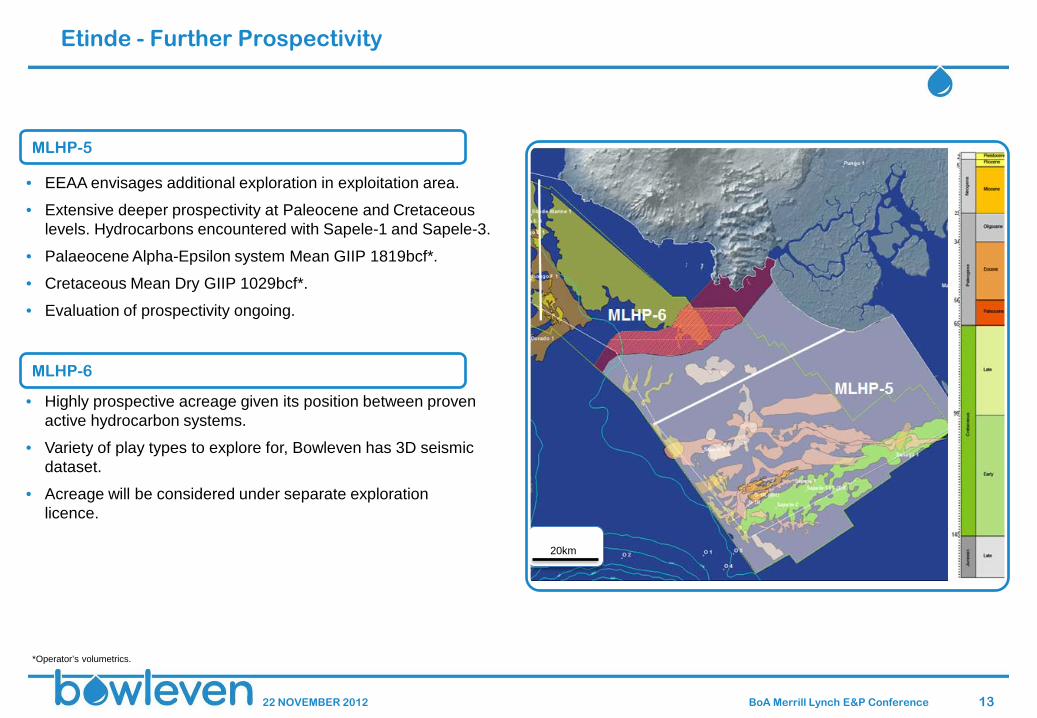

Etinde - Further Prospectivity

MLHP-6

MLHP-5

• EEAA envisages additional exploration in exploitation area.

• Extensive deeper prospectivity at Paleocene and Cretaceous levels. Hydrocarbons encountered with Sapele-1 and Sapele-3.

• Palaeocene Alpha-Epsilon system Mean GIIP 1819bcf*.

• Cretaceous Mean Dry GIIP 1029bcf*.

• Evaluation of prospectivity ongoing.

• Highly prospective acreage given its position between proven active hydrocarbon systems.

• Variety of play types to explore for, Bowleven has 3D seismic dataset.

• Acreage will be considered under separate exploration licence.

*Operator’s volumetrics.

20km

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 14

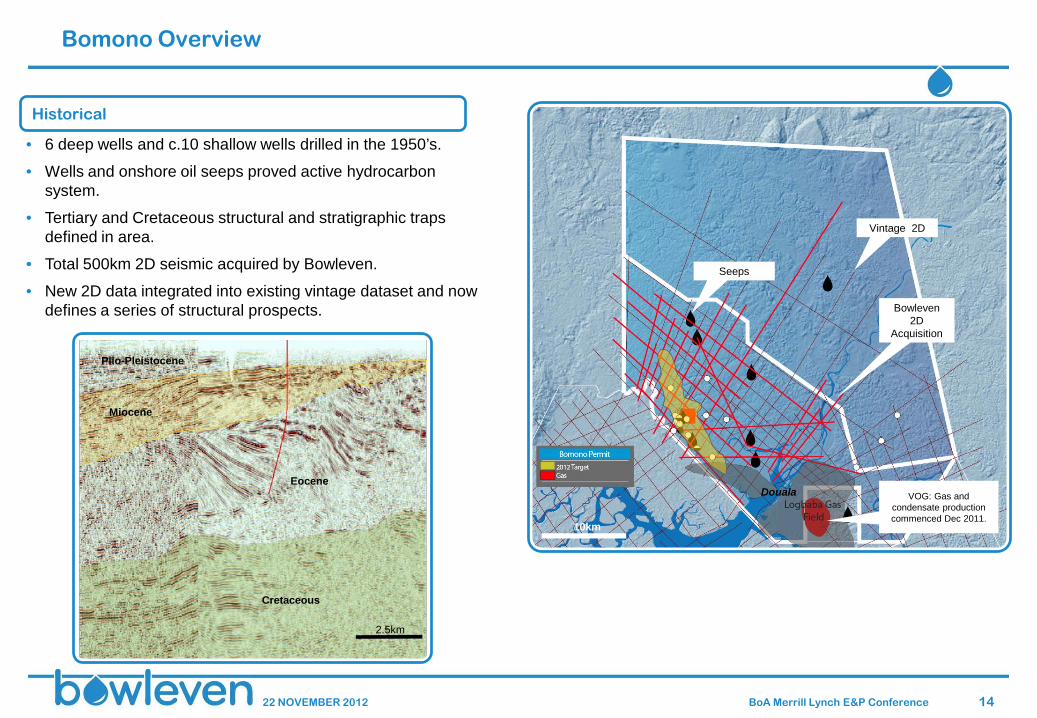

• 6 deep wells and c.10 shallow wells drilled in the 1950’s.

• Wells and onshore oil seeps proved active hydrocarbon system.

• Tertiary and Cretaceous structural and stratigraphic traps defined in area.

• Total 500km 2D seismic acquired by Bowleven.

• New 2D data integrated into existing vintage dataset and now defines a series of structural prospects.

Bomono Overview

Bowleven 2D

Acquisition

Vintage 2D

VOG: Gas and condensate production commenced Dec 2011.

Douala

10km

Seeps

Historical

Plio-Pleistocene

Miocene

Eocene

Cretaceous

2.5km

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 15

Bomono Exploration

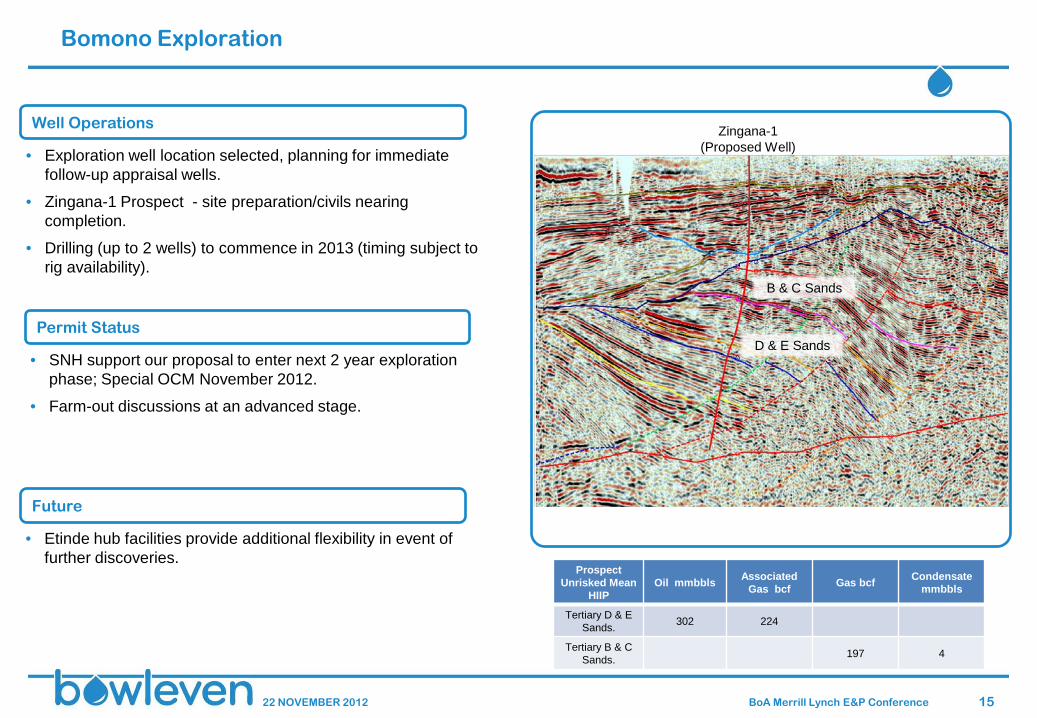

Well Operations

Future

• Exploration well location selected, planning for immediate follow-up appraisal wells.

• Zingana-1 Prospect - site preparation/civils nearing completion.

• Drilling (up to 2 wells) to commence in 2013 (timing subject to rig availability).

• Etinde hub facilities provide additional flexibility in event of further discoveries.

Prospect

Unrisked Mean HIIP

Oil mmbbls Associated Gas bcf Gas bcf Condensate

mmbbls

Tertiary D & E Sands. 302 224

Tertiary B & C Sands. 197 4

Permit Status

• SNH support our proposal to enter next 2 year exploration phase; Special OCM November 2012.

• Farm-out discussions at an advanced stage.

Zingana-1 (Proposed Well)

B & C Sands

D & E Sands

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 16

Kenya

Upcoming Work Programme

• Anticipated 2013 activity:

− Airborne geophysical survey - Q1/Q2.

− Acquisition of 500km 2D seismic - Q2-Q3.

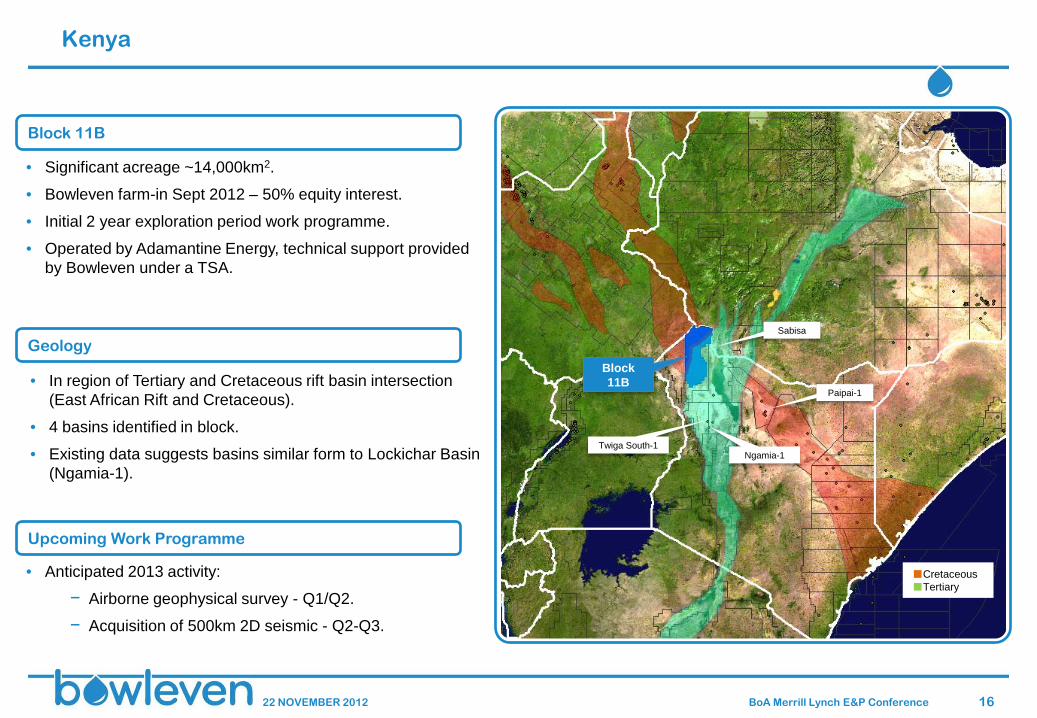

Geology

• In region of Tertiary and Cretaceous rift basin intersection (East African Rift and Cretaceous).

• 4 basins identified in block.

• Existing data suggests basins similar form to Lockichar Basin (Ngamia-1).

• Significant acreage ~14,000km2.

• Bowleven farm-in Sept 2012 – 50% equity interest.

• Initial 2 year exploration period work programme.

• Operated by Adamantine Energy, technical support provided by Bowleven under a TSA.

Block 11B

Block 11B

Ngamia-1 Twiga South-1

Paipai-1

■Cretaceous ■Tertiary

Sabisa

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 17

Kenya Block 11B

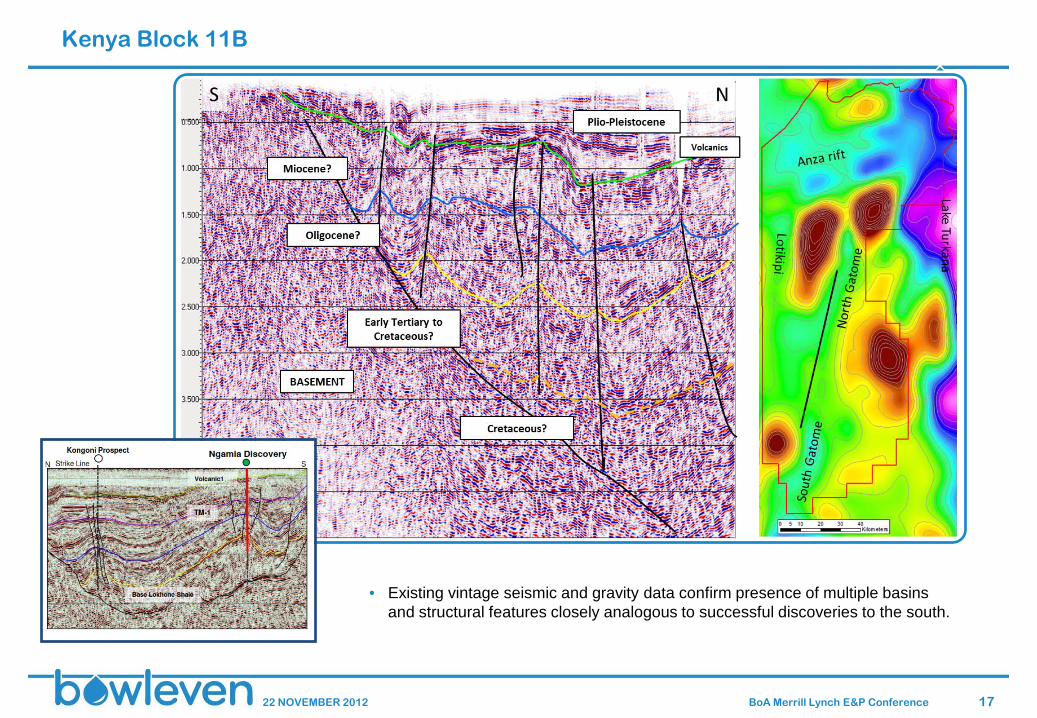

• Existing vintage seismic and gravity data confirm presence of multiple basins and structural features closely analogous to successful discoveries to the south.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 18

Funding Overview

• Cash end October 2012 ~$120 million, no debt.

• Petrofac provides up to $500 million for Stage I development; initial capital investment at FID.

• High equity interest in Etinde & Bomono provides opportunity to introduce additional farm-in partners if appropriate.

• Talks with preferred bidder on Bomono farm-out progressing, expect to cover intended work programme.

• Strategic alliance agreement with Petrofac allows further Etinde farm-down (up to 1/3).

Significant financing flexibility.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 19

Outlook

• Ongoing evaluation of the Douala Basin prospectivity.

• Bomono drilling targeting both Tertiary and Cretaceous prospectivity.

• Commencing exploration activities over new Kenya acreage.

Exploration

†

• Progressing development activities for hub and spoke development, including pre FEED/FEED work.

• Etinde FID targeted for H2 2013 ensuring:

• EEAA approval. • Gas Sales Agreement finalisation. • Access to finance for the development.

• Appraisal/development drilling on MLHP-7.

Resources to Reserves: The Path to Development

oil & gas

Principal Contact: Kerry Crawford Tel: +44 131 524 5678 Kevin Hart Tel: +44 131 524 5678

www.bowleven.com

Bowleven Plc. The Cube 45 Leith Street Edinburgh EH1 3AT United Kingdom

oil & gas

Appendix

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 22

Progress Report

†

Resources to Reserves: The Path to FID*

• Etinde: Ongoing evaluation of Douala Basin prospectivity.

• Bomono: Drilling to commence in 2013 (timing subject to rig availability).

• Bomono: Farm-out discussions at advanced stage.

• Kenya: Work programme commencing.

Exploration Strategy

Resources to Reserves

Exploring the Douala Basin

New Frontiers (Kenya)

* FID: Final Investment Decision ‡MOU: Memorandum of Understanding

Submission of draft Etinde Exploitation Authorisation Application (EEAA).

Agreement of Fertiliser MOU‡.

Gas sales term sheet nearing finalisation - pending pricing mechanism.

Access potential development financing – Petrofac Strategic Alliance.

Drilling programme commenced with appraisal/development drilling ongoing at IM-5.

FID targeted for H2 2013 subject to: • EEAA approval. • Gas Sales Agreement. • Access to development capital secured.

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 23

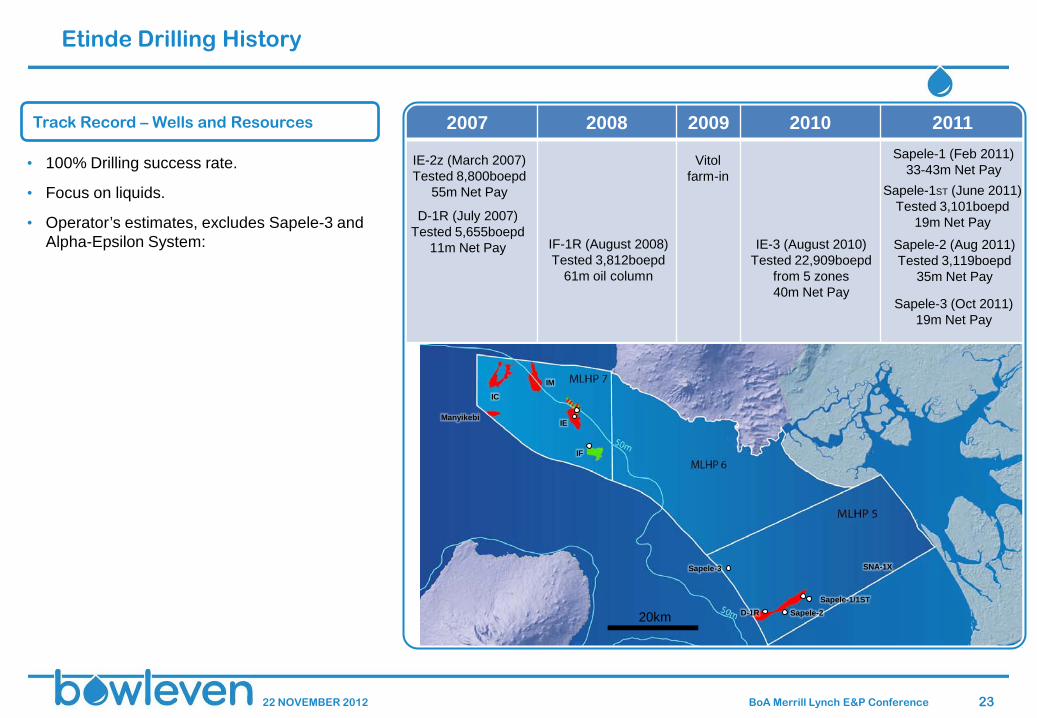

Etinde Drilling History

2007 2008 2009 2010 2011

• 100% Drilling success rate.

• Focus on liquids.

• Operator’s estimates, excludes Sapele-3 and Alpha-Epsilon System:

Track Record – Wells and Resources

IE-3 (August 2010) Tested 22,909boepd

from 5 zones 40m Net Pay

IE-2z (March 2007) Tested 8,800boepd

55m Net Pay

IF-1R (August 2008) Tested 3,812boepd

61m oil column

D-1R (July 2007) Tested 5,655boepd

11m Net Pay

Sapele-1 (Feb 2011) 33-43m Net Pay

Sapele-1ST (June 2011) Tested 3,101boepd

19m Net Pay

Sapele-2 (Aug 2011) Tested 3,119boepd

35m Net Pay

Sapele-3 (Oct 2011) 19m Net Pay

20km

IC

IM

Sapele-3

IE Manyikebi

SNA-1X

Sapele-1/1ST Sapele-2 D-1R

IF

Vitol farm-in

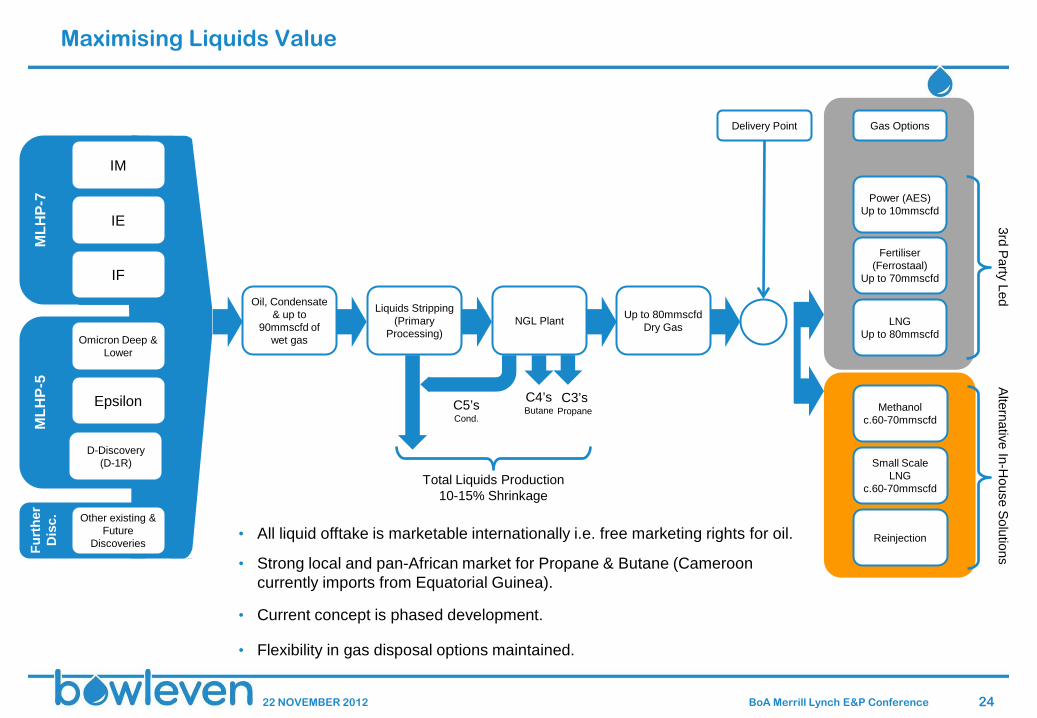

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 24

C5’s Cond.

MLH

P-7

MLH

P-5

Furt

her

Dis

c.

Maximising Liquids Value

• All liquid offtake is marketable internationally i.e. free marketing rights for oil.

• Strong local and pan-African market for Propane & Butane (Cameroon currently imports from Equatorial Guinea).

• Current concept is phased development.

• Flexibility in gas disposal options maintained.

IM

IE

IF

Omicron Deep & Lower

Epsilon

D-Discovery (D-1R)

Other existing & Future

Discoveries

Oil, Condensate & up to

90mmscfd of wet gas

Liquids Stripping (Primary

Processing) NGL Plant Up to 80mmscfd

Dry Gas

Power (AES) Up to 10mmscfd

Fertiliser (Ferrostaal)

Up to 70mmscfd

LNG Up to 80mmscfd

Delivery Point Gas Options

C4’s Butane

C3’s Propane Methanol

c.60-70mmscfd

Small Scale LNG

c.60-70mmscfd

Reinjection

Total Liquids Production 10-15% Shrinkage

3rd Party Led Alternative In-H

ouse Solutions

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 25

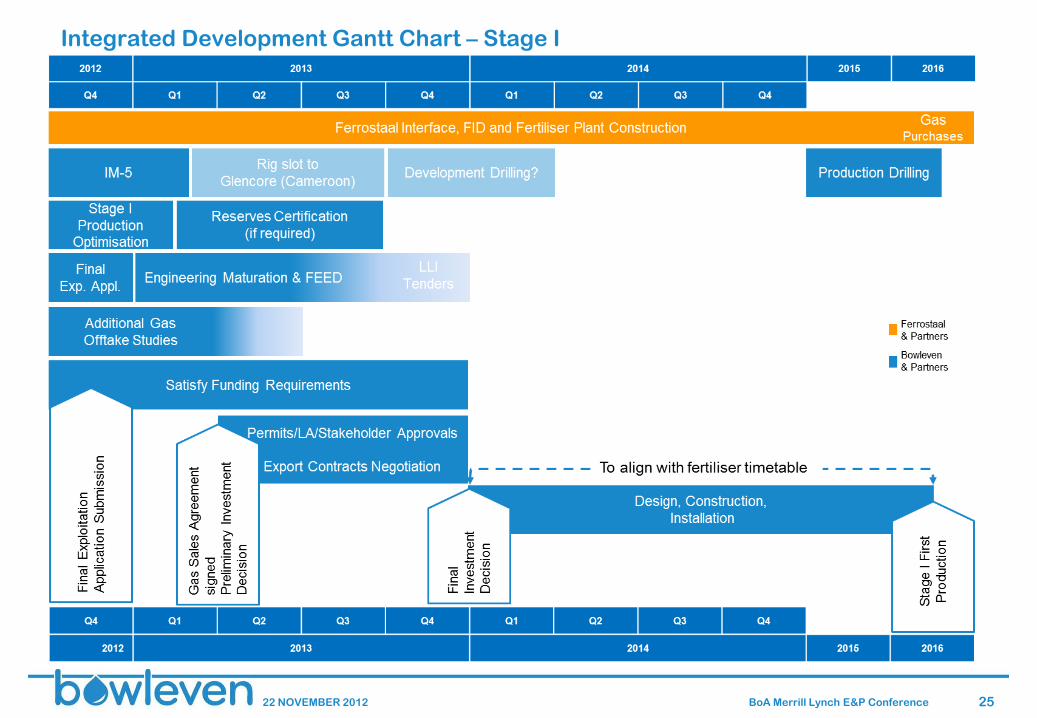

Integrated Development Gantt Chart – Stage I

22 NOVEMBER 2012 BoA Merrill Lynch E&P Conference 26

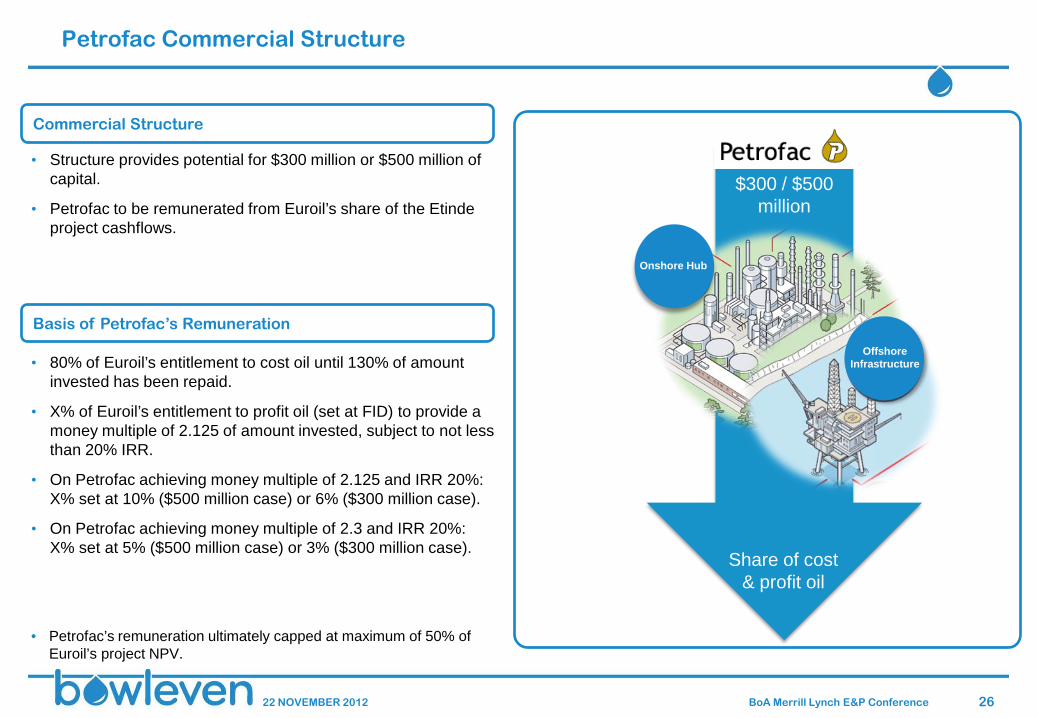

Petrofac Commercial Structure

• 80% of Euroil’s entitlement to cost oil until 130% of amount invested has been repaid.

• X% of Euroil’s entitlement to profit oil (set at FID) to provide a money multiple of 2.125 of amount invested, subject to not less than 20% IRR.

• On Petrofac achieving money multiple of 2.125 and IRR 20%: X% set at 10% ($500 million case) or 6% ($300 million case).

• On Petrofac achieving money multiple of 2.3 and IRR 20%: X% set at 5% ($500 million case) or 3% ($300 million case).

• Petrofac’s remuneration ultimately capped at maximum of 50% of Euroil’s project NPV.

Basis of Petrofac’s Remuneration

Commercial Structure

• Structure provides potential for $300 million or $500 million of capital.

• Petrofac to be remunerated from Euroil’s share of the Etinde project cashflows.

Onshore Hub

Offshore Infrastructure

$300 / $500 million

Share of cost & profit oil