Embed Size (px)

Citation preview

1 1 8 5 I m m o k a l e e Ro a d , N a p l e s , F l o R I da 3 4 1 1 02 3 9 . 2 5 4 . 2 1 0 0 w w w. b a N k o F F l o R I da . c o m

n a s d a q b o f l

Ba

nk

of Flo

rid

a co

rp. a

nn

ua

l r

ep

or

t t

wo

th

ou

san

d se

ve

n

Nasdaq: boFl

B a n k o f F l o r i d a c o r p.a n n u a l r e p o r t

1864_CVR_C2.indd 1 3/15/08 5:22:32 AM

n a s d a q b o f l

M i s s i o n S t a t e m e n t :

To be the “Bank of Choice” for businesses , profess ionals and individuals

with a des ire for re lat ionship-driven financia l so lut ions.

C o m p a n y P r o f i l e :

• Founded in Naples, Florida in September 1998, with first

financial center opening in August 1999

• 4th largest publicly-traded bank holding company headquartered in Florida based on total assets; 5th largest based on market capitalization

• 13 financial centers in 7 distinct and major Florida markets

• Primary focus is lending in the $1 - $15 million range

• Comprehensive suite of products and services specifically designed for business clients and affluent individuals

• Integrated wealth management strategy with our Investment Management Division, Bank of Florida Trust Company

Financial Highlights ................................................ 1Shareholder Letter ................................................... 2 Loans .................................................................... 2 Asset Quality ...................................................... 4 Deposits............................................................... 5 Revenue Growth & Operating Efficiency ..... 6 Bank of Florida Trust Company .................... 7 Market Expansion ............................................. 8 Market Potential ................................................ 8 The Future ........................................................10 Chairman’s Letter ...................................................11Executive Management Team ...............................12Boards of Directors ...............................................12Financial Review (10k) ........................................14

2 0 0 7 a n n u a l r e p o r t

C o r p o r a t e H e a d q u a r t e r s

Bank of Florida Corporation1185 Immokalee RoadNaples, Florida 34110(239) 254-2100Toll Free (866) 226-5352www.bankofflorida.com

M a r k e t M a k e r s

The Michael’s Advisory Group Raymond James & Associates 1301 Riverplace Boulevard, Suite 1900 Jacksonville, FL 32207 (800) 363-9652

R e g i s t r a r a n d Tr a n s f e r A g e n t

Registrar & Transfer10 Commerce DriveCranford, NJ 07016(800) 368-5948www.rtco.com

I n v e s t o r a n d A n a l y s t R e l a t i o n s

Tracy L. KeeganEVP, Chief Financial Officer1185 Immokalee RoadNaples, FL 34110(239) 254-2100

B a n k o f F l o r i d a c o r p.t w o t h o u s a n d s e v e n

A f f i l i a t e C o m p a n i e s

Bank of Florida – SouthwestCollier County 1185 Immokalee Road Naples, Florida 34110

3401 Tamiami Trail North Naples, Florida 34103

2325 Vanderbilt Beach RoadNaples, Florida 34109

Lee County23471 Walden Center Drive Bonita Springs, Florida 34134

6321 Daniels Parkway Fort Myers, Florida 33912

Bank of Florida – SoutheastBroward County200 sw 1st Avenue, Suite 100 Ft. Lauderdale, Florida 33301

5200 North Federal Highway Ft. Lauderdale, Florida 33308

Miami-Dade County19058 Ne 29th Avenue Aventura, Florida 33180

1493 Sunset Drive Coral Gables, Florida 33143

Palm Beach County595 South Federal Highway, Suite 100 Boca Raton, Florida 33432

Bank of Florida – Tampa BayHillsborough County777 S. Harbour Island Boulevard, Suite 125 Tampa, Florida 33602

Pinellas County26417 US Highway 19 North Clearwater, Florida 33761

Bank of Florida Trust CompanyHeadquarters – West Coast1185 Immokalee RoadNaples, Florida 34110

East Coast200 sw 1st Avenue, Suite 1700 Ft. Lauderdale, Florida 33301

1864_CVR_C2.indd 2 3/15/08 5:22:36 AM

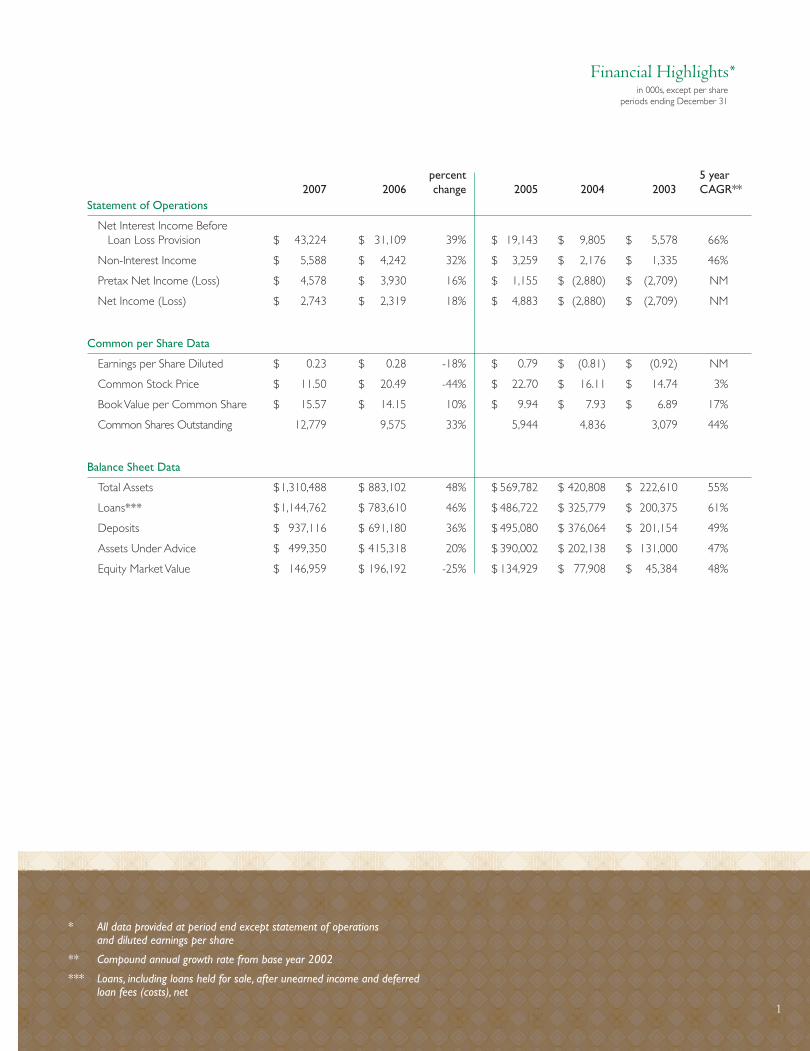

* All data provided at period end except statement of operations and diluted earnings per share

** Compound annual growth rate from base year 2002

*** Loans, including loans held for sale, after unearned income and deferred loan fees (costs), net

Financial Highlights*

percent 5 year 2007 2006 change 2005 2004 2003 CAGR**Statement of Operations

Net Interest Income Before Loan Loss Provision $ 43,224 $ 31,109 39% $ 19,143 $ 9,805 $ 5,578 66%

Non-Interest Income $ 5,588 $ 4,242 32% $ 3,259 $ 2,176 $ 1,335 46%

Pretax Net Income (Loss) $ 4,578 $ 3,930 16% $ 1,155 $ (2,880) $ (2,709) NM

Net Income (Loss) $ 2,743 $ 2,319 18% $ 4,883 $ (2,880) $ (2,709) NM

Common per Share Data

Earnings per Share Diluted $ 0.23 $ 0.28 -18% $ 0.79 $ (0.81) $ (0.92) NM

Common Stock Price $ 11.50 $ 20.49 -44% $ 22.70 $ 16.11 $ 14.74 3%

Book Value per Common Share $ 15.57 $ 14.15 10% $ 9.94 $ 7.93 $ 6.89 17%

Common Shares Outstanding 12,779 9,575 33% 5,944 4,836 3,079 44%

Balance Sheet Data

Total Assets $ 1,310,488 $ 883,102 48% $ 569,782 $ 420,808 $ 222,610 55%

Loans*** $ 1,144,762 $ 783,610 46% $ 486,722 $ 325,779 $ 200,375 61%

Deposits $ 937,116 $ 691,180 36% $ 495,080 $ 376,064 $ 201,154 49%

Assets Under Advice $ 499,350 $ 415,318 20% $ 390,002 $ 202,138 $ 131,000 47%

Equity Market Value $ 146,959 $ 196,192 -25% $ 134,929 $ 77,908 $ 45,384 48%

in 000s, except per shareperiods ending December 31

1

1864_NARC3.indd 11864_NARC3.indd 1 3/15/08 2:05:39 PM3/15/08 2:05:39 PM

M i c h a e l L . M c M u l l a n

President and Chief Executive Offi cerBank of Florida Corporation

T o o u r S h a r e h o l d e r s :

This past year was another marked by double-digit growth,

market expansion and enhancements to our infrastructure.

We reached $.3 billion in assets in 2007, a $427 million or 48%

increase from December 3, 2006, and recorded $2.7 million in

net income, up 8% from 2006.

Included in our 2007 accomplishments are the acquisition of

$276 million asset, Fort Myers-based Old Florida Bank, the

opening of a new financial center in Pinellas County, the

conversion of our core operating systems to one central

processor, and the subsequent service enhancements and

L O A N S

Loans Increased by 22% Organically in 2007, Resulting in Compound Annual Growth of 53% over the

Past Five Years (Excluding Bank Acquisitions).

The loan portfolio increased $361 million or 46% over the past 12 months, totaling $1.1 billion as of December 31, 2007. Excluding the Old Florida Bank acquisition, loan growth was $175 million or 22%. Comparatively, the median increase for our peer group, which includes commercial banks with assets of $470 million to $1.9 billion, was 6%. Over the past fi ve years, loans outstanding have grown at a compound annual rate of 61%, or 53% excluding the Old Florida acquisition and our acquisition of Bristol Bank in Coral Gables, Florida in August 2006.

The profi le of our loan portfolio changed somewhat in 2007 as a result of initiatives to diversify the portfolio in light of market opportunity and risk considerations. With such, permanent commercial real estate (CRE) loans increased by fi ve percentage points to 37% of loans outstanding, largely refl ecting a greater emphasis on offi ce buildings, while residential construction loans decreased by two percentage points to 9% of loans outstanding, and land and development loans were lower by four percentage points to

2

1864_NARC3.indd 21864_NARC3.indd 2 3/15/08 2:05:42 PM3/15/08 2:05:42 PM

of loans outstanding. In total, only $206 million or 18% of our $1.1 billion loan portfolio are residential development or construction in nature. It is also important to note that our portfolio has no subprime loans. The mix of commercial and industrial (C&I) loans rose by nearly one percentage point in the past year to 8% of loans outstanding, and the mix of commercial construction loans increased by one percentage point to 12% of the portfolio. In addition, 45% of our permanent CRE loans and 31% of our commercial construction loans are owner-occupied, which we consider a desirable component of underwriting risk.

Given current market conditions, our overall view for 2008 includes slower than previously anticipated loan growth with a focus primarily on the medical communities in the markets we serve as well as an increased emphasis on C&I lending.

new products resulting from our expanded technology

and resources. The financial statements included with this

Annual Report fully detail our financial achievements for

2007. However, as part of this letter, I want to focus on

some of the key factors driving our performance, and how

favorably we compare to our 9-bank Florida peer group.

3

1864_NARC3.indd 31864_NARC3.indd 3 3/15/08 2:05:50 PM3/15/08 2:05:50 PM

A S S E T Q U A L I T Y

Continued Stringent Focus on Credit Quality. Well-Positioned

Compared to Peers. No Subprime Loans on Books.

Although we were well reserved against our loan portfolio for most of 2007, during a time when many of our peers had experienced declines in credit quality, we did identify certain commercial real estate loans in the fourth quarter that had recently been impacted by market conditions. These loans were primarily located in Lee County within Southwest Florida, where deterioration of real estate values has been among the sharpest in the State. This contraction caused an increase in our nonperforming loans which, along with continued reassessment of loss exposure in the Company’s other markets, resulted in an increase in our provision expense in the fourth quarter. Although our loan loss provision expense in 2007 was 50% higher than in the prior year, the median increase for our peers was over 200%.

Nonperforming loans, as shown in the accompanying pie chart, were $14.2 million at December 31, 2007, virtually all of which were located in the Southwest Florida market. The ratio of nonperforming loans to total loans outstanding at year end was 1.24% better than our peers at 1.42%. The primary factor impacting the Company’s nonperforming loans was overall market value deterioration. It was,

and is, not a result of any relaxation of our underwriting standards or of our evaluation of the credit worthiness of our borrowers.

Our credit review and allowance methodology continue to support and justify our reserve levels, which provide for potential losses inherent in the loan portfolio. At December 31, 2007 our loan loss allowance totaled $14.4 million or 1.26% of loans outstanding, providing coverage for nonperforming loans by 102%, compared to average peer coverage of 93%.

We are confi dent that we will successfully address the pockets of credit concern in the markets we serve, though asset quality challenges are likely to continue through 2008 and perhaps longer. As such, we added a Special Assets Department in 2007 to focus exclusively on problem loans. This department reports to the Company’s Senior Executive Vice President, John James, who has over 40 years experience in Special Asset Management, Risk Management and Credit Administration and has managed through these type cycles before. We believe that the added expense associated with this new team is money well-spent. We also believe that creating a new department specifi cally focused on problem assets will allow the rest of the Company to continue to serve and grow in our markets, which we consider to be among the most distinct markets in Florida.

4

1864_NARC3.indd 41864_NARC3.indd 4 3/15/08 2:05:52 PM3/15/08 2:05:52 PM

5

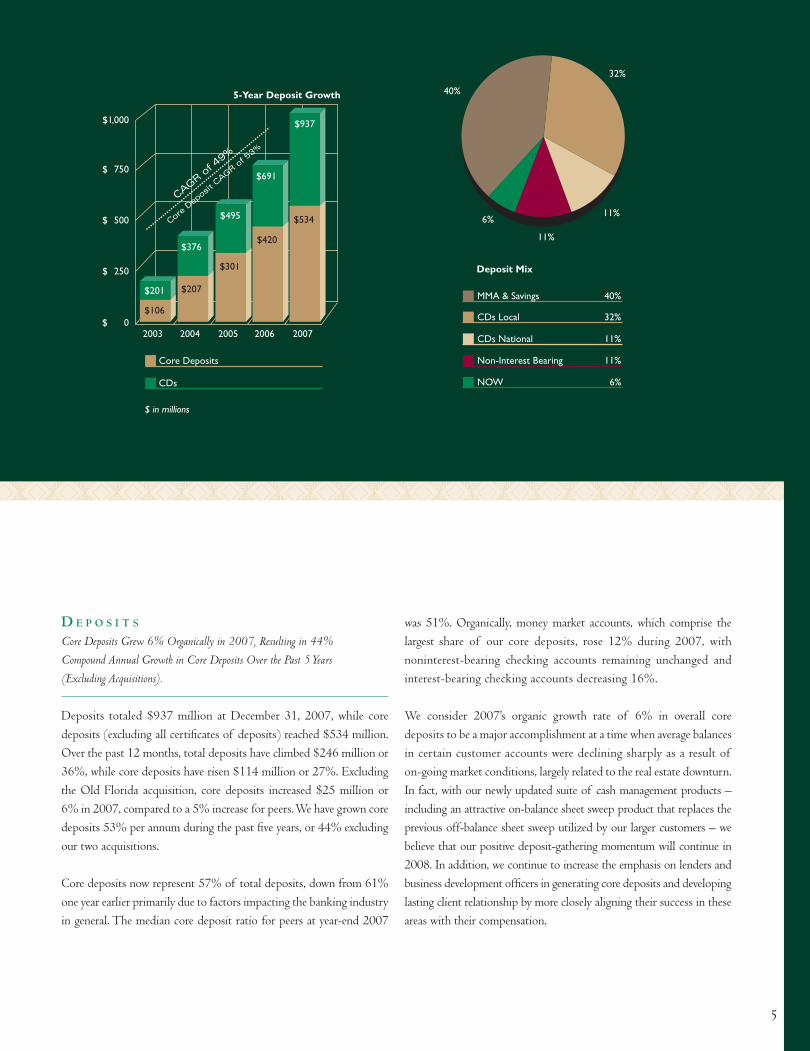

D E P O S I T S

Core Deposits Grew 6% Organically in 2007, Resulting in 44%

Compound Annual Growth in Core Deposits Over the Past 5 Years

(Excluding Acquisitions).

Deposits totaled $937 million at December 31, 2007, while core deposits (excluding all certifi cates of deposits) reached $534 million. Over the past 12 months, total deposits have climbed $246 million or 36%, while core deposits have risen $114 million or 27%. Excluding the Old Florida acquisition, core deposits increased $25 million or 6% in 2007, compared to a 5% increase for peers. We have grown core deposits 53% per annum during the past fi ve years, or 44% excluding our two acquisitions.

Core deposits now represent 57% of total deposits, down from 61% one year earlier primarily due to factors impacting the banking industry in general. The median core deposit ratio for peers at year-end 2007

was 51%. Organically, money market accounts, which comprise the largest share of our core deposits, rose 12% during 2007, with noninterest-bearing checking accounts remaining unchanged and interest-bearing checking accounts decreasing 16%.

We consider 2007’s organic growth rate of 6% in overall core deposits to be a major accomplishment at a time when average balances in certain customer accounts were declining sharply as a result of on-going market conditions, largely related to the real estate downturn. In fact, with our newly updated suite of cash management products – including an attractive on-balance sheet sweep product that replaces the previous off-balance sheet sweep utilized by our larger customers – we believe that our positive deposit-gathering momentum will continue in 2008. In addition, we continue to increase the emphasis on lenders and business development offi cers in generating core deposits and developing lasting client relationship by more closely aligning their success in these areas with their compensation.

5

1864_NARC3.indd 51864_NARC3.indd 5 3/15/08 2:05:54 PM3/15/08 2:05:54 PM

T O P - L I N E R E V E N U E is defi ned by

the Company as net interest income (interest

income on loans and investments, less the cost

of funding those loans and investments and

other assets) plus noninterest income; it excludes

nonrecurring revenue such as securities and other

gains/losses.

6

R E V E N U E G R O W T H & O P E R A T I N G E F F I C I E N C Y

Continued to Expand Top-Line Revenue in 2007 Coupled with Prudent Expense Control,

Once Again Achieving Positive Operating Leverage.

The Company successfully grew top-line revenue by 38% in 2007 resulting in the fi fth full year of recording positive operating leverage, an important measure of improving profi tability.

Net interest income increased by $12.1 million or 39% in 2007 to $43 million, refl ecting growth in average earning assets of 56%, which somewhat offset compression in our net interest margin. Margin compression was characteristic of virtually the entire banking industry, with only three of our nine peers able to offset this impact with earning asset growth. Our 56% increase in earning assets was entirely due to our ability to grow the loan portfolio as discussed above. Without the Old Florida acquisition, net interest income grew $6.2 million or 20% over 2006.

Noninterest income grew 32% in 2007 to $5.6 million, or 14% excluding Old Florida, twice the rate of increase of our peers. Over half of our noninterest income consists of fees earned by Bank of Florida Trust Company, while about one-third consists of deposit account service charges and other fees. The balance of the increase was derived from mortgage banking and gains/losses from securities or other transactions. Increases in noninterest income during 2008 are projected to come from continued growth in trust fees as well as increased service charge income, primarily as a result of providing additional cash management services, revised pricing of depositor services, and the collection of fees that were historically waived.

N e t I n t e r e s t M a r g i n is defi ned as the yield on loans and investments

(earning assets) less underlying deposits and borrowing costs, taken as a percent of earning assets.

1864_NARC3.indd 61864_NARC3.indd 6 3/15/08 2:05:55 PM3/15/08 2:05:55 PM

We expect margin compression to extend into 2008 as competition within our markets continue to hold deposits at very high interest rates, creating an artifi cial fl oor despite the recent cuts by the Federal Reserve Board. How long this competitive situation will persist is unknown. In addition, each Federal Reserve Board rate cut has a short-term negative impact on margin due to the lag in repricing liabilities with scheduled maturities. However, our on-going asset/liability management analysis helps us anticipate this impact and implement strategies to lessen it.

BA N K O F FLO R I DA TRU S T CO M PA N Y

Pretax Profi ts at Bank of Florida Trust Company Grew by 81%. Assets Under

Advice Increased 20% to $499 million.

The Company’s Wealth Management Division, Bank of Florida Trust Company, had another record year in providing investment counseling and advisory services to business owners, executives, professionals, foundations, and other high net worth individuals and families. We continued to capitalize on delivering a nonproprietary/open architecture investment solution that resonates with high net worth individuals who prefer and often demand an advisor without a confl ict of interest. Moreover, the Company expanded its alternative investment offerings to include directional and market neutral hedge funds, commodities, and managed futures for high net worth clients. In addition, the Company’s focus on risk-adjusted returns, diversifi cation, and “best-in-class” manager selection, coupled with high levels of client service and relationship manager accessibility, continued to result strong in referrals from existing clients.

The Trust Company realized a 20% increase in assets under advice during 2007, to $499 million, resulting in a fi ve year compound annual growth rate of 47%. In addition, the median account size increased 11% to over $3.5 million. Revenues increased 21% to $3.1 million in 2007, while pretax net income soared 81% to $945,000, marking the Trust Company’s fourth year of profi tability following its opening in August, 2000.

The success of the Trust Company has afforded us the ability to add highly skilled and experienced professionals that, in turn, should keep us on our high growth trajectory and differentiate us from our competitors. In fact, during the fi rst 30 days of 2008, we have opened and are in the process of funding approximately $30 million in new account relationships. This ramp-up in hiring is expected to result in new account relationships and gross revenues that should be fully evident by fourth quarter 2008, resulting in meaningful net income impact in 2009 and beyond. The Company’s focus on creating genuine client relationships and providing truly objective fi nancial advice and counsel to our clients has resulted in the Trust Company’s clients in Southwest Florida utilizing as many as fi ve banking and wealth management products and services. To further expand both our wealth management and banking businesses, we are implementing a private banking model across the entire banking affi liate footprint. This will allow us to better provide our target clients with a more integrated fi nancial product suite including credit facilities, depository products, and wealth management services, with a dedicated private banking team.

7

1864_NARC3.indd 71864_NARC3.indd 7 3/15/08 2:05:58 PM3/15/08 2:05:58 PM

Escambia

Santa Rosa Okaloosa

Walton

HolmesJackson

Bay

Calhoun

Liberty

Gadsden

Leo

Wakulla

FranklinGulf

Washington

8

High Growth County

Based on Projected Economic Indicator Change ‘05 – ’10*

F L O R I D A ’ S

E C O N O M I C G R O W T H

Medium Growth County

Low Growth County

BOFL currently has financial centers

BOFL expanded in 2007

*Projected Economic Indicator Change measures prospective wealth creation, using changes in population and median household income

BOFL is planning to expand in 2008

M A R K E T E X P A N S I O N

Expanded Market Share in Southwest Florida, Entered Pinellas County, and

Branded Bank of Florida in the Fort Lauderdale Skyline with the Relocation of its

Downtown Affi liate Bank Headquarters.

In addition to adding $276 million in assets to Bank of Florida – Southwest, which nearly doubled its footings to the present $679 million, the Old Florida Bank acquisition expanded our deposit market share in both Collier and Lee Counties to 3.1% and 1.9%, respectively.

Also a result of the Old Florida Bank acquisition, Bank of Florida – Southwest became #3 in market share of Florida-based commercial banks in Collier County and #8 in market share when national, super-regional, and community banks are considered. With the addition of Old Florida’s fi nancial centers, Bank of Florida – Southwest now ranks #12 in deposit market share in Lee County and is among the top fi ve of Florida-based banks and thrifts.

The strategy of extending the presence of Bank of Florida – Tampa Bay into Pinellas County included the opening of a 4,000 square foot fi nancial center in Clearwater with a 16-year banking veteran serving as Market President. In its fi rst six months of operation, the fi nancial center has grown loans to $41 million and deposits to $31 million. As of year-end 2007, total assets of Bank of Florida – Tampa Bay reached $190 million.

Lastly, in mid-November, our $455 million asset Bank of Florida – Southeast, which grew 25% in 2007, announced the relocation of its downtown Fort Lauderdale headquarters to a new 17-story offi ce tower. The Old Chicago-style building, located in the historic arts and entertainment district, has been named the “Bank of Florida Center.” In addition to a full-service banking center on the ground fl oor, nearly 24,000 square feet on the top fl oor houses executive offi ces, commercial lending, wealth management, mortgage lending, and a variety of support functions for the Southeast affi liate. Plans for 2008 include relocating the bank’s Coral Ridge facility to a newly constructed fi nancial center and the opening of a fi nancial center in the fast-growing and affl uent Downtown Coral Gables market. By mid-2008, we will have six locations across Palm Beach, Broward, and Miami-Dade Counties.

M A R K E T P O T E N T I A L

Bank of Florida Markets Continue to be Among the Best in Florida.

With nearly $213 billion in deposits available within the seven counties we serve, there is enormous market potential within which to grow. These markets alone make up 57% of the total deposits in the state of Florida. The accompanying map shows strong growth potential based on population, wealth creation and median household incomes. While Florida is currently undergoing a signifi cant real estate-induced downturn from its historic growth profi le, the state continues to display strong positive economic and demographic characteristics.

1864_NARC3.indd 81864_NARC3.indd 8 3/15/08 2:06:01 PM3/15/08 2:06:01 PM

Leon

Dixie

Levy

Gilchrist Alachua

Marion

Citrus

Taylor

Jefferson MadisonHamilton

Baker

Clay

Duval

St. Johns

Putnam

Flagler

Lake

Volusia

Sumter

Hernando

Pasco

Polk

Hardee

DeSoto

Highlands

Glades

Hendry

Collier

Monroe Miami – Dade

Broward

Palm Beach

Martin

St. Lucie

Okeechobee

Indian River

Osceola

Brevard

Sarasota

Charlotte

Lee

Hillsborough

Pinellas

Manatee

Orange

Seminole

Nassau

Union

BradfordLafayette

Suwannee Columbia Wakulla

FLO R I DA DE P O S I T BA S E

Markets where Bank of Florida has a presence,hold more than half of Florida’s total deposits

Broward $35.4 billionCollier/Lee $22.0 billionHillsborough/Pinellas $41.1 billionMiami-Dade $76.3 billionPalm Beach $37.9 billion

Total Deposits $212.7 billion

Florida’s Total Deposits $373.9 billionSource: FDIC data as of 6/30/07

STRATEGIC ACQUISITION

Old Florida Bankshares, Inc.Completed 2Q 2007(Collier / Lee Counties)

TAMPA BAY EXPANSION

Clearwater Financial Center3Q 2007(Pinellas County)

KEY FINANCIAL

CENTER RELOCATIONS

Downtown Ft. LauderdaleHigh Rise 4Q 2007

Coral Ridge New Facility with Drive-Through1H 2008

PLANNED EXPANSION

Coral Gables at Merrick Way1H 2008

9

1864_NARC3.indd 91864_NARC3.indd 9 3/15/08 2:06:03 PM3/15/08 2:06:03 PM

T H E F U T U R E

Accomplishments and Preparation in 2007 Have Laid the Foundation to

Meet the Challenges of 2008

As discussed earlier in this letter, a critical focus in 2008 will be continued intensive surveillance of our portfolios to proactively detect any future asset quality problems that may occur beyond those that have already surfaced. I am confi dent that our dedicated and experienced special assets team noted earlier will be effective in its charge to resolve problem loans expeditiously while minimizing exposure, and insulate our lenders from distractions that would diminish their new business development efforts.

Another primary focus in 2008 will be tightly managing controllable noninterest expense, holding headcount, especially non-revenue generating personnel, fl at with 2007 year-end levels, which were already reduced late in the fourth quarter by eliminating several non-core and duplicate positions. Also, as previously discussed, we will be investing in our wealth management division with additional personnel and anticipate strong growth in assets under management during 2008. No added occupancy or other infrastructure expense is planned next year, other than that previously discussed.

In 2007, we successfully converted our core operating system to Jack Henry “Silverlake.” This conversion represented a signifi cant upgrade, and for the fi rst time in our history, brought all subsidiaries under a common operating umbrella. The benefi ts of this change reach across all areas of our company including improved fi nancial reporting, an enhanced suite of cash management products and services, and signifi cant operating effi ciencies. We began to reap the benefi ts of this enhancement towards the end of 2007, and look to continue to build on that success in 2008.

Another crucial element to future success is our company’s culture. We have proven that we can differentiate our bank through the tangible spirit of client advocacy. This spirit and culture extend far beyond fulfi lling a banking need. It draws on our internal and external resources to provide clients with unique solutions and

experiences that support them outside of their direct banking needs. We have demonstrated that this approach builds stronger more loyal client relationships and promotes positive awareness of our company and brand.

While 2008 will surely present its share of challenges, we believe that we have an opportunity to selectively increase our presence in the markets we serve. We are learning that our large bank competitors, many of whom have been sharply affected by subprime loans and collateralized securities-related problems that we have avoided, are retrenching from serving long-standing and highly regarded borrowers as part of pull-backs in certain lines of business. In addition, a good number of our community bank peers have also become inwardly focused.

Our short-term asset growth may not be as rapid as in the past and margin compression may reduce the rate of improvement in our earnings over the course of 2008, however, by targeting our loan growth on the products and types of borrowers we know well, incentivizing our new business development efforts in the sale of our improved deposit products and services that will expand our core funding base, and further integrating our wealth management and banking services into a full-featured private banking model, we look forward with enthusiasm to continued achievements in 2008 and successfully coping with any further asset quality issues that may present themselves. As always, I am indebted to our employees, Directors, and shareholders for their support and encouragement, which give us the confi dence to go forward in our mission to continue to build one of the premier banking and wealth management franchises in Florida.

Sincerely,

Michael L. McMullanPresident and Chief Executive Offi cerBank of Florida Corporation

10

1864_NARC3.indd 101864_NARC3.indd 10 3/15/08 2:06:03 PM3/15/08 2:06:03 PM

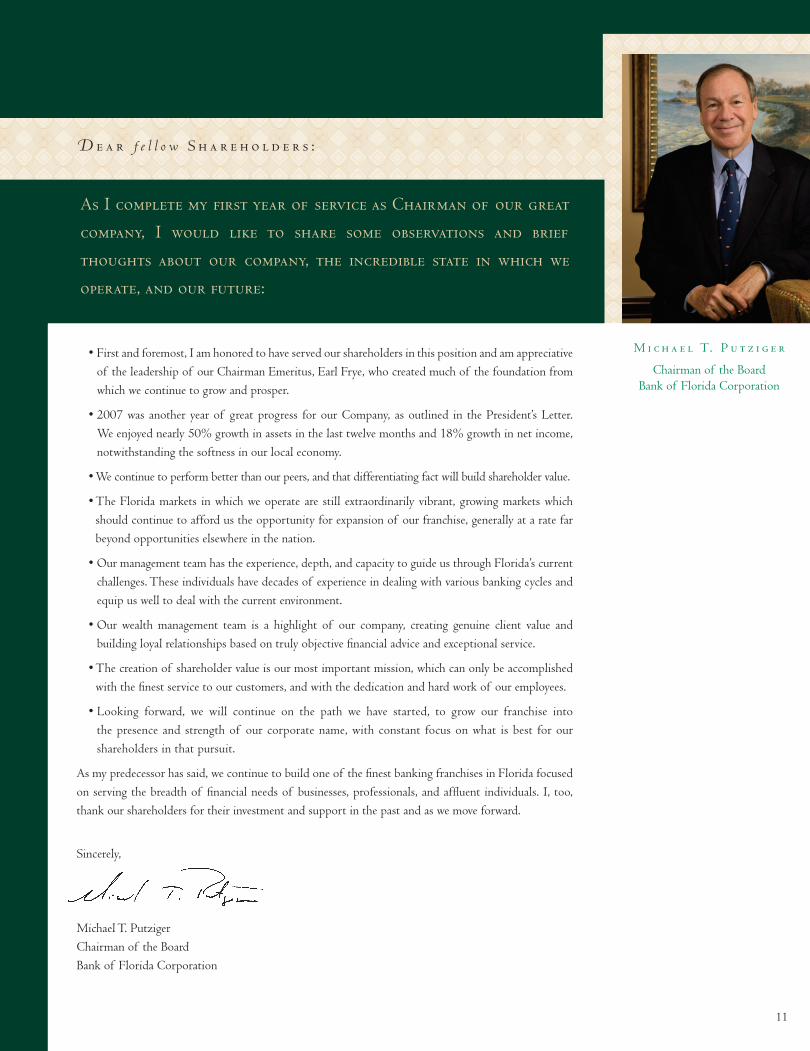

D e a r f e l l o w S h a r e h o l d e r s :

As I complete my first year of service as Chairman of our great

company, I would like to share some observations and brief

thoughts about our company, the incredible state in which we

operate, and our future:

• First and foremost, I am honored to have served our shareholders in this position and am appreciative of the leadership of our Chairman Emeritus, Earl Frye, who created much of the foundation from which we continue to grow and prosper.

• 2007 was another year of great progress for our Company, as outlined in the President’s Letter. We enjoyed nearly 50% growth in assets in the last twelve months and 18% growth in net income, notwithstanding the softness in our local economy.

• We continue to perform better than our peers, and that differentiating fact will build shareholder value.

• The Florida markets in which we operate are still extraordinarily vibrant, growing markets which should continue to afford us the opportunity for expansion of our franchise, generally at a rate far beyond opportunities elsewhere in the nation.

• Our management team has the experience, depth, and capacity to guide us through Florida’s current challenges. These individuals have decades of experience in dealing with various banking cycles and equip us well to deal with the current environment.

• Our wealth management team is a highlight of our company, creating genuine client value and building loyal relationships based on truly objective fi nancial advice and exceptional service.

• The creation of shareholder value is our most important mission, which can only be accomplished with the fi nest service to our customers, and with the dedication and hard work of our employees.

• Looking forward, we will continue on the path we have started, to grow our franchise into the presence and strength of our corporate name, with constant focus on what is best for our shareholders in that pursuit.

As my predecessor has said, we continue to build one of the fi nest banking franchises in Florida focused on serving the breadth of fi nancial needs of businesses, professionals, and affl uent individuals. I, too, thank our shareholders for their investment and support in the past and as we move forward.

Sincerely,

Michael T. Putziger Chairman of the BoardBank of Florida Corporation

M i c h a e l T. P u t z i g e r

Chairman of the BoardBank of Florida Corporation

11

1864_NARC3.indd 111864_NARC3.indd 11 3/15/08 2:06:05 PM3/15/08 2:06:05 PM

B a n k o f F l o r i da C o r p o r at i o n E xe c u t iv e M a n ag e m e n t Te a m

Michael L. McMullanPresident and CEO

John B. JamesSenior Executive Vice President,Chief Administrative Offi cer

Tracy L. KeeganExecutive Vice President,Chief Financial Offi cer

Roy N. HellwegeExecutive Vice President,Director of Banking

Craig D. ShermanExecutive Vice President,Chief Lending Offi cer

John S. ChaperonExecutive Vice President,Director of Corporate Risk Management

Peter SetaroExecutive Vice President,Director of Bank Operations and Technology

Arlette YassaSenior Vice President,Corporate Secretary

B a n k o f F l o r i da C o r p o r at i o n B oa rd o f D i r e c t o r s

Michael T. Putziger, Esq.Chairman of the BoardVice Chairman, WinnCompanies & Counsel to Murtha Cullina, LLP

Joe B. Cox, Esq.Vice Chairman of the BoardAttorney at Law and Partner, Cox & Nici

Donald R. BarberVice Chairman, Boran Craig Barber Engel

H. Wayne Huizenga, Jr.President, Huizenga Holdings, Inc.

John B. JamesSenior Executive Vice President, Chief Administrative Offi cer, Bank of Florida Corporation

LaVonne JohnsonRetired, former Planner and Project Director for Allegheny County, Pennsylvania

Edward KaloustCEO, Medi Weight Loss

Michael L. McMullanPresident and CEO,Bank of Florida Corporation

Harry K. Moon, M.D.President, Himmarshee Surgical Partners

Pierce T. NeeseRetired, former Chairman and CEO of Etowah Bank in Georgia

Ramon A. Rodriguez CPA Executive,Crowe Chizek & Company, LLC

Terry W. StilesChairman and CEO, Stiles Corporation

B a n k o f F l o r i da – S o u t h we s tB oa rd o f D i r e c t o r s

Edward P. MortonChairman of the BoardManaging Director,Wasmer, Schroeder & Company

Donald R. BarberVice Chairman, Boran Craig Barber Engel

Russell A. BuddPresident and CEO,Professional Building Systems

Thomas L. Cook, M.D.Collier Anesthesia, P.A.

Joe B. Cox, Esq.Attorney at Law and Partner, Cox & Nici

Michael J. FryeOwner, RE/MAX Realty Group

Kaleigh GroverAssociate Publisher, Naples Illustrated

James J. Guerra, M.D.Collier Sports Medicine &Orthopaedic Center

Stanley W. HoleRetired, former Chairman ofHole Montes, Inc.

LaVonne JohnsonRetired, former Planner and Project Director for Allegheny County, Pennsylvania

Danny E. Morgan*CEO, Bank of Florida – Southwest

Michael J. RileyChief Strategy Offi cer, NCH Healthcare System

Craig D. ShermanPresident, Bank of Florida – Southwest

Craig D. TimminsPartner, Investment Properties Corporationof Naples

Bernard L. TurnerRetired, Former Chairman andCo-Founder of the Board of the Florida Coastal School of Law

Martin M. WasmerCEO, Wasmer, Schroeder & Company

B a n k o f F l o r i da – S o u t h e a s tB oa rd o f D i r e c t o r s

Harry K. Moon, M.D.Chairman of the BoardPresident, Himmarshee Surgical Partners

Ramon A. RodriguezCPA Executive,Crowe Chizek & Company LLC

John S. ChaperonPresident and CEO, Bank of Florida – Southeast

Jorge H. Garcia, AIA, NCARB CEO, Garcia Stromberg, LLC

Charles K. Cross, Jr.Executive Vice President,Senior Lender, Bank of Florida – Southeast

Steven W. HudsonPresident, Hudson Capital Group

Mark McCormickPresident, Gulfstream Capital Holdings

Kaye PearsonPresident, Poseidon Management, LLC

Christopher F. RodenManaging Director and Founder, Seabridge Capital, LLC

Robert J. YannoManaging Principal, Integrity Capital Corporation

E x e c u t i v e M a n a g e m e n t Te a m &B o a r d s o f D i r e c t o r s

12 *Pending Regulatory Approval

1864_NARC3.indd 121864_NARC3.indd 12 3/15/08 2:06:10 PM3/15/08 2:06:10 PM

B a n k o f F l o r i da – Ta m pa B ayB oa rd o f D i r e c t o r s

Edward KaloustChairman of the BoardCEO, Medi Weight Loss

Robert F. ShuckVice Chairman of the BoardVice Chairman, Raymond JamesFinancial, Inc.

Bradford G. DouglasPrincipal, HuntDouglas Real EstateServices, Inc.

Ignacio A. Ferras III, Ph.D. Managing Partner, Chairman and CEO, Huff, Ferras & Associates, Inc

Honorable Sam M. GibbonsFormer Member of U.S. Congress (Retired)

Roy N. Hellwege Director of Banking, Bank of Florida Corporation

H. Wingfi eld HughesPresident, Forrester-Smith, Inc.,a Division of Geiger

R. Searing MerrillPresident, Boykin Barnett Companies

Mary Anne ReillyCertifi ed Public Accountant, Reilly, Fisher & Solomon, P.A.

Robert E. Schmidt, Jr. CEO, Boulder Venture

L. David Shear, Esq.Attorney at Law and Partner, Ruden, McClosky, Smith, Schuster & Russell, P.A.

Holly TomlinPresident, Tomlin Staffi ng

Chris D. WillmanPresident and CEO, Bank of Florida – Tampa Bay

Edward Zbella, M.D., F.A.C.G., F.A.C.S. President and CEO, Florida Fertility Institute

B a n k o f F l o r i da Tru s t C o m pa n y B oa rd o f D i r e c t o r s

Joe B. Cox, Esq.Chairman of the BoardAttorney at Law and Partner, Cox & Nici

Julie W. HuslerCEO, Bank of Florida Trust Company

John B. JamesSenior Executive Vice President, Chief Administrative Offi cer, Bank of Florida Corporation

Edward KaloustCEO, Medi Weight Loss

Douglas B. Kniskern, Esq.Attorney at Law, Arnstein and Lehr, LLP

Christopher F. RodenManaging Director & Founder, Seabridge Capital, LLC

Harry K. Moon, M.D.President, Himmarshee Surgical Partners

Martin M. WasmerCEO, Wasmer, Schroeder & Company

B a n k o f F l o r i da i nPa l m B e ac h C o u n t yA dv i s o ry B oa rd o f D i r e c t o r s

Jorge H. Garcia, AIA, NCARBChairman of the BoardCEO, Garcia Stromberg, LLC

Howard E. McCall, Jr.Vice Chairman of the BoardPresident, American Equipment Company and President & Managing Director, Mafeks International, LLC

Jan CarlssonAssistant CEO, Lynn Insurance Groupand Principal, LFC Development, LLC

P. Rodney CunninghamPresident, Boca Raton Transportation, Inc.

Timothy R. DevlinPartner, Daszkal Bolton LLP

Charles R. KrauserPresident, Atlantic Development & Management SE, Inc.

Thomas Laird, D.A.President, Laird West, LLC and Laird, LLC

Betty MasiPartner, Genesis Development Group, LLCand Vice President, Seawood Builders

William R. McKay, M.D.Partner, Lighthouse Orthopaedic Associates

B a n k o f F l o r i da i nM i a m i - Da d e C o u n t yA dv i s o ry B oa rd o f D i r e c t o r s

Christopher F. RodenChairman of the BoardManaging Director and Founder, Seabridge Capital, LLC

Carlos Esteban AlbirFounder and President of ABCO Products, Inc.

Ernesto Alvarez President, Coex Coffee International, Inc.

Michael Duchowny, M.D.Senior Staff Attending Physician atMiami Children’s Hospital

Onelio Garcia, Jr., M.D., F.A.C.S.Diplomat, American Board of Plastic Surgery

Rolando Montoya, Ph.D.President of Miami-Dade College,Wolfson Campus

Roberto PelaezMarket President of Miami-Dade Countyfor Bank of Florida

Alfredo PiedraPresident, Breakthru Innovations, LLC

Robert J. YannoManaging Principal, Integrity Capital Corporation

13

1864_NARC3.indd 131864_NARC3.indd 13 3/15/08 2:06:11 PM3/15/08 2:06:11 PM

B A N K o f F L O R I DA C O R P O R AT I O N F i n a n c i a l R e v i e w (0K) T A B L E O F C O N T E N T S

PA RT I

Item 1. Description of Business ................................................................................................................................................................ 1 Background and Prior Operating History ................................................................................................................................ 1 Market Area and Competition .................................................................................................................................................... 2 Distribution of Assets, Liabilities and Stockholders’ Equity: Interest Rates and Interest Differential....................... 3 Return on Equity and Assets ....................................................................................................................................................... 3 Lending Activities .......................................................................................................................................................................... 4 Summary of Loan Loss Experience ........................................................................................................................................... 5 Investment Activities ...................................................................................................................................................................... 6 Sources of Funds ............................................................................................................................................................................ 7 Correspondent Banking ................................................................................................................................................................ 7 Employees ........................................................................................................................................................................................ 8 Recent Accounting Pronouncements ......................................................................................................................................... 8 Monetary Policies ........................................................................................................................................................................... 9 Supervision and Regulation ......................................................................................................................................................... 9Item 1A. Risk Factors ..................................................................................................................................................................................... 14Item 1B. Unresolved Staff Comments ....................................................................................................................................................... 18Item 2. Properties ......................................................................................................................................................................................... 18Item 3. Legal Proceedings ........................................................................................................................................................................... 19Item 4. Submission of Matters to a Vote of Security Holders .......................................................................................................... 19

PA RT I I

Item 5. Market for Common Equity and Related Stockholder Matters .......................................................................................... 19Item 6. Selected Financial Data ................................................................................................................................................................. 21Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation ......................................... 22Item 7a. Quantitative and Qualitative Disclosures about Market Risk .............................................................................................. 33Item 8. Financial Statements and Supplementary Data ....................................................................................................................... 34Item 9. Changes In and Disagreements with Accountants on Accounting and Financial Disclosure ....................................... 35Item 9a. Controls and Procedures............................................................................................................................................................... 35Item 9b. Other information.......................................................................................................................................................................... 36 PA RT I I I

Item 10. Directors and Executive Offi cers of the Registrant ................................................................................................................ 36Item 11. Executive Compensation ............................................................................................................................................................... 36Item 12. Security Ownership of Certain Benefi cial Owners and Management and Related Stockholder Matters .................. 36 Item 13. Certain Relationships and Related Transactions ..................................................................................................................... 36Item 14. Principal Accountant Fees and Services .................................................................................................................................... 36 PA RT I V

Item 15. Exhibits and Financial Statement Schedules ............................................................................................................................ 37 Signatures ......................................................................................................................................................................................... 79

14

1864_NARC3.indd 141864_NARC3.indd 14 3/15/08 2:06:11 PM3/15/08 2:06:11 PM

n a s d a q b o f l

M i s s i o n S t a t e m e n t :

To be the “Bank of Choice” for businesses , profess ionals and individuals

with a des ire for re lat ionship-driven financia l so lut ions.

C o m p a n y P r o f i l e :

• Founded in Naples, Florida in September 1998, with first

financial center opening in August 1999

• 4th largest publicly-traded bank holding company headquartered in Florida based on total assets; 5th largest based on market capitalization

• 13 financial centers in 7 distinct and major Florida markets

• Primary focus is lending in the $1 - $15 million range

• Comprehensive suite of products and services specifically designed for business clients and affluent individuals

• Integrated wealth management strategy with our Investment Management Division, Bank of Florida Trust Company

Financial Highlights ................................................ 1Shareholder Letter ................................................... 2 Loans .................................................................... 2 Asset Quality ...................................................... 4 Deposits............................................................... 5 Revenue Growth & Operating Efficiency ..... 6 Bank of Florida Trust Company .................... 7 Market Expansion ............................................. 8 Market Potential ................................................ 8 The Future ........................................................10 Chairman’s Letter ...................................................11Executive Management Team ...............................12Boards of Directors ...............................................12Financial Review (10k) ........................................14

2 0 0 7 a n n u a l r e p o r t

C o r p o r a t e H e a d q u a r t e r s

Bank of Florida Corporation1185 Immokalee RoadNaples, Florida 34110(239) 254-2100Toll Free (866) 226-5352www.bankofflorida.com

M a r k e t M a k e r s

The Michael’s Advisory Group Raymond James & Associates 1301 Riverplace Boulevard, Suite 1900 Jacksonville, FL 32207 (800) 363-9652

R e g i s t r a r a n d Tr a n s f e r A g e n t

Registrar & Transfer10 Commerce DriveCranford, NJ 07016(800) 368-5948www.rtco.com

I n v e s t o r a n d A n a l y s t R e l a t i o n s

Tracy L. KeeganEVP, Chief Financial Officer1185 Immokalee RoadNaples, FL 34110(239) 254-2100

B a n k o f F l o r i d a c o r p.t w o t h o u s a n d s e v e n

A f f i l i a t e C o m p a n i e s

Bank of Florida – SouthwestCollier County 1185 Immokalee Road Naples, Florida 34110

3401 Tamiami Trail North Naples, Florida 34103

2325 Vanderbilt Beach RoadNaples, Florida 34109

Lee County23471 Walden Center Drive Bonita Springs, Florida 34134

6321 Daniels Parkway Fort Myers, Florida 33912

Bank of Florida – SoutheastBroward County200 sw 1st Avenue, Suite 100 Ft. Lauderdale, Florida 33301

5200 North Federal Highway Ft. Lauderdale, Florida 33308

Miami-Dade County19058 Ne 29th Avenue Aventura, Florida 33180

1493 Sunset Drive Coral Gables, Florida 33143

Palm Beach County595 South Federal Highway, Suite 100 Boca Raton, Florida 33432

Bank of Florida – Tampa BayHillsborough County777 S. Harbour Island Boulevard, Suite 125 Tampa, Florida 33602

Pinellas County26417 US Highway 19 North Clearwater, Florida 33761

Bank of Florida Trust CompanyHeadquarters – West Coast1185 Immokalee RoadNaples, Florida 34110

East Coast200 sw 1st Avenue, Suite 1700 Ft. Lauderdale, Florida 33301

1864_CVR_C2.indd 2 3/15/08 5:22:36 AM

1 1 8 5 I m m o k a l e e Ro a d , N a p l e s , F l o R I da 3 4 1 1 02 3 9 . 2 5 4 . 2 1 0 0 w w w. b a N k o F F l o R I da . c o m

n a s d a q b o f l

Ba

nk

of Flo

rid

a co

rp. a

nn

ua

l r

ep

or

t t

wo

th

ou

san

d se

ve

n

Nasdaq: boFl

B a n k o f F l o r i d a c o r p.a n n u a l r e p o r t

1864_CVR_C2.indd 1 3/15/08 5:22:32 AM