Embed Size (px)

Citation preview

1

Bank Capital Adequacy: Where to Now?

Kevin Davis

Professor of Finance, University of Melbourne

Research Director, Melbourne Centre for Financial Studies

03 9666 1001

2

Outline

• What is bank capital?

• A brief history of bank capital

• Bank capital experiences during the GFC

• Capital lessons from the GFC

• Proposals for bank capital requirements

3

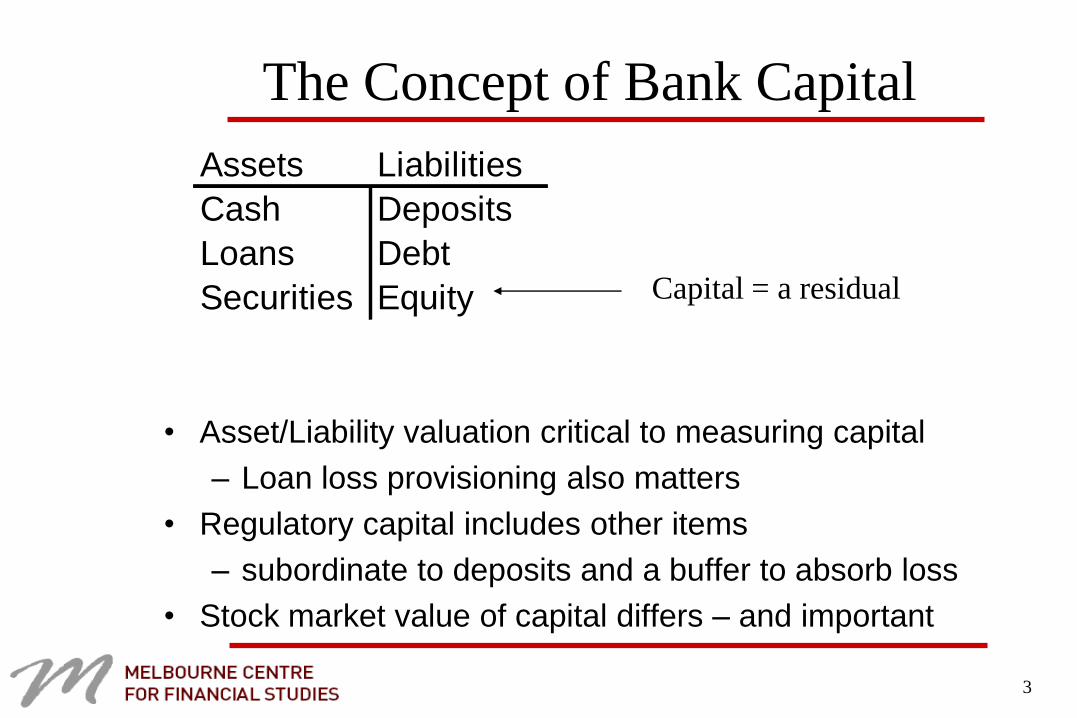

The Concept of Bank Capital

Assets Liabilities

Cash Deposits

Loans Debt

Securities Equity

• Asset/Liability valuation critical to measuring capital

– Loan loss provisioning also matters

• Regulatory capital includes other items

– subordinate to deposits and a buffer to absorb loss

• Stock market value of capital differs – and important

Capital = a residual

4

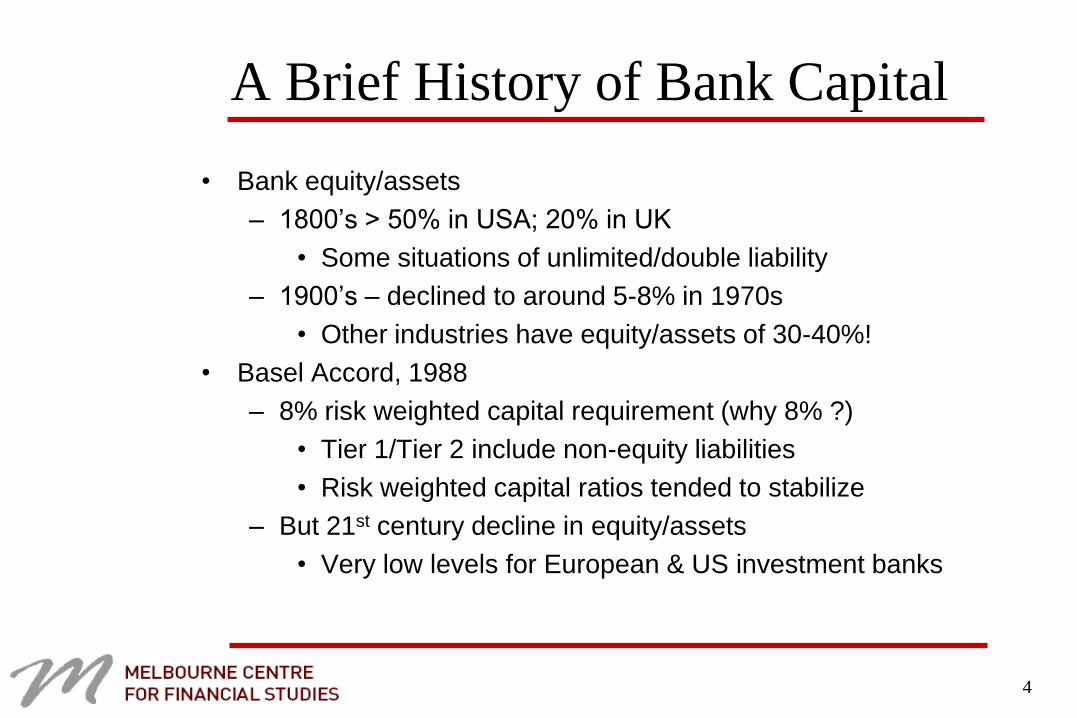

A Brief History of Bank Capital

• Bank equity/assets

– 1800’s > 50% in USA; 20% in UK

• Some situations of unlimited/double liability

– 1900’s – declined to around 5-8% in 1970s

• Other industries have equity/assets of 30-40%!

• Basel Accord, 1988

– 8% risk weighted capital requirement (why 8% ?)

• Tier 1/Tier 2 include non-equity liabilities

• Risk weighted capital ratios tended to stabilize

– But 21st century decline in equity/assets

• Very low levels for European & US investment banks

5

A Brief History of Bank Capital

Source: Bank of Canada

6

A Brief History of Bank Capital

• Basel II Accord – 2006

• Three Pillars: Capital requirements; supervision; disclosure

• Standardized and Internal Ratings Based approach

– Use of ratings agencies and bank credit models

• Changes to the risk weights

• Capital requirement for operational risk

• Provision for capital requirements for interest rate risk in the banking book

• Calibration of overall requirements - no planned change in aggregate capital requirements for the banking sector as a whole.

7

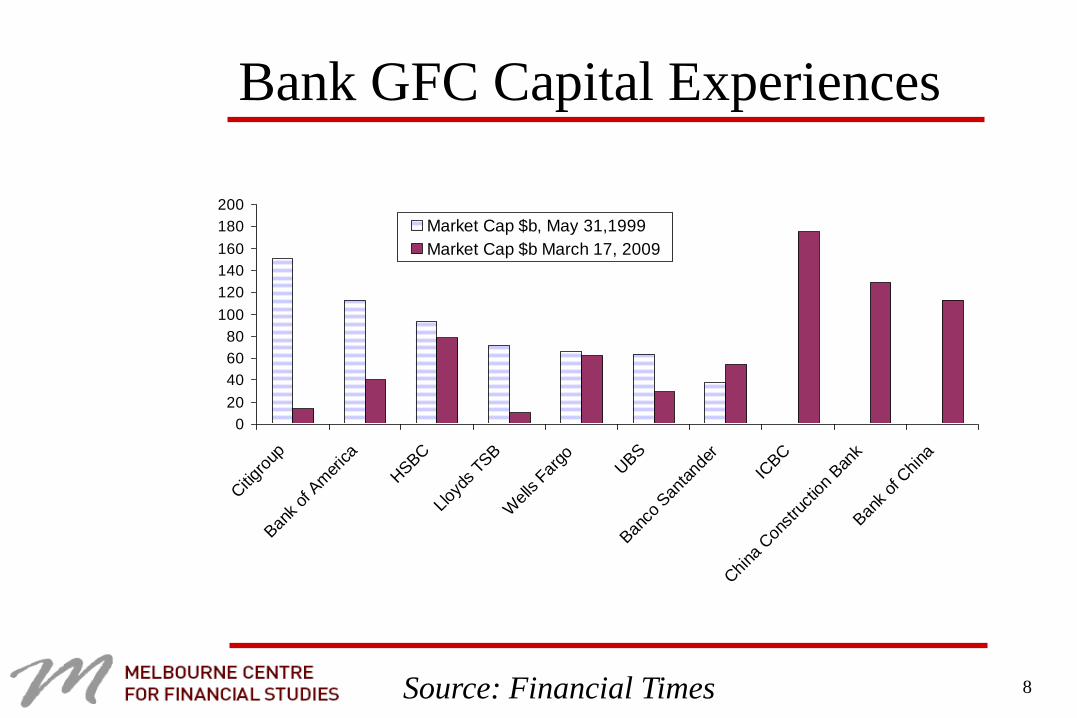

Bank GFC Capital Experiences

Estimated

Holdings

Estimated

Writedowns

Implied

Cumulative

Loss Rate

(percent)

U.S. Banks 12,561 1,025 8.2

U.K. Banks 8,369 604 7.2

Euro Area Banks 22,901 814 3.6

Other Mature Europe Banks 3,970 201 5.1

Asia Banks 7,879 166 2.1

Estimated Global Bank Writedowns: 2007-2010, $US bill

Loans and Securities

Source: IMF

8

Bank GFC Capital Experiences

0

20

40

60

80

100

120

140

160

180

200

Citigr

oup

Ban

k of

Am

erica

HSBC

Lloy

ds T

SB

Wells F

argo

UBS

Ban

co S

anta

nder

ICBC

Chi

na C

onst

ruct

ion

Ban

k

Ban

k of

Chi

na

Market Cap $b, May 31,1999

Market Cap $b March 17, 2009

Source: Financial Times

9

Bank GFC Capital Experiences

0

200

400

600

800

1000

1200

US

UK

Japa

n

Switz

erland

Ger

man

y

Spa

in

Franc

eIta

ly

Net

herla

nds

Aus

tralia

Hon

g Kon

g

Can

ada

Bra

zil

Swed

en

Rus

sia

India

Chi

na

Bank Capitalization $b, 1999

Bank Capitalization $b 2009

Source: Financial Times

10

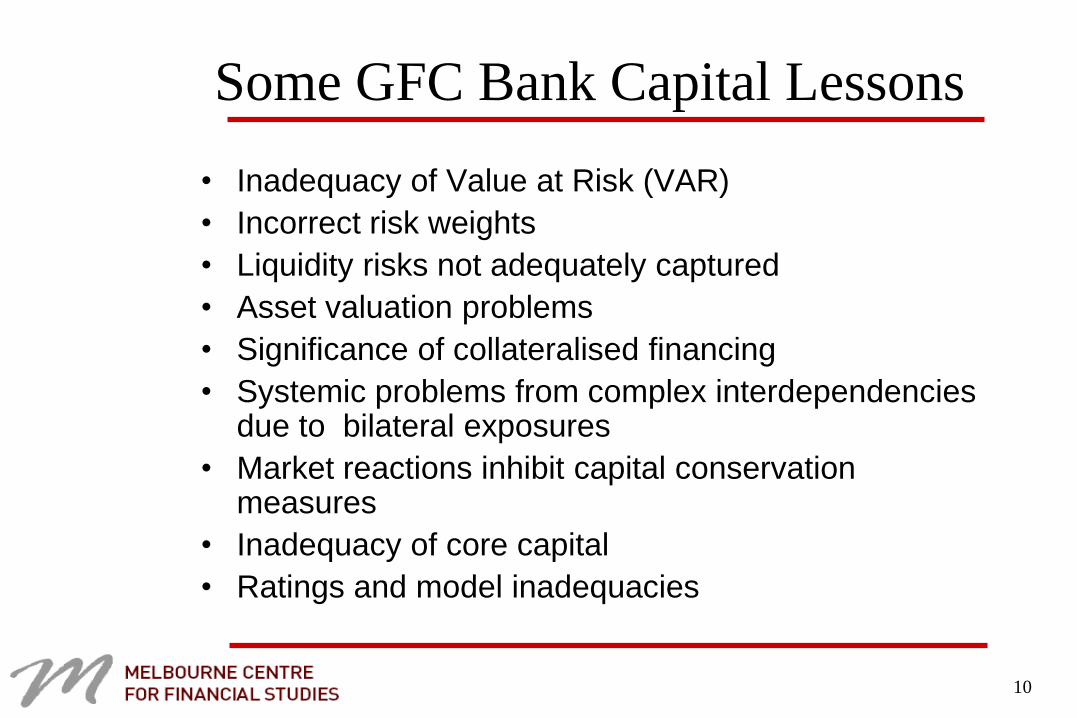

Some GFC Bank Capital Lessons

• Inadequacy of Value at Risk (VAR)

• Incorrect risk weights

• Liquidity risks not adequately captured

• Asset valuation problems

• Significance of collateralised financing

• Systemic problems from complex interdependencies due to bilateral exposures

• Market reactions inhibit capital conservation measures

• Inadequacy of core capital

• Ratings and model inadequacies

11

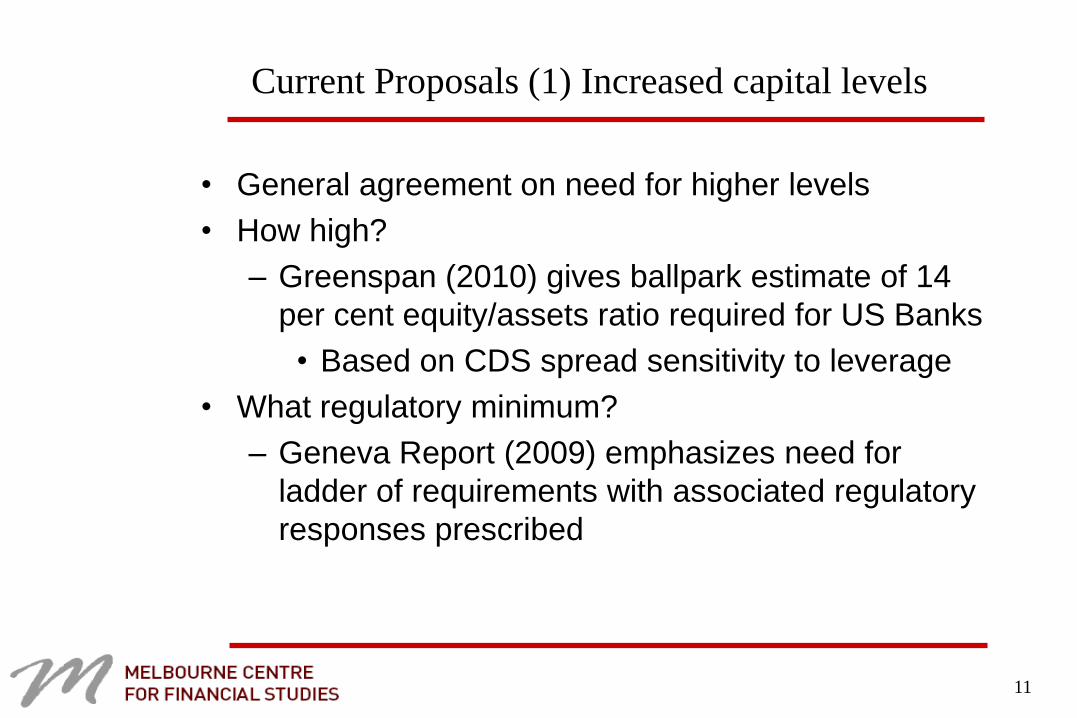

Current Proposals (1) Increased capital levels

• General agreement on need for higher levels

• How high?

– Greenspan (2010) gives ballpark estimate of 14

per cent equity/assets ratio required for US Banks

• Based on CDS spread sensitivity to leverage

• What regulatory minimum?

– Geneva Report (2009) emphasizes need for

ladder of requirements with associated regulatory

responses prescribed

12

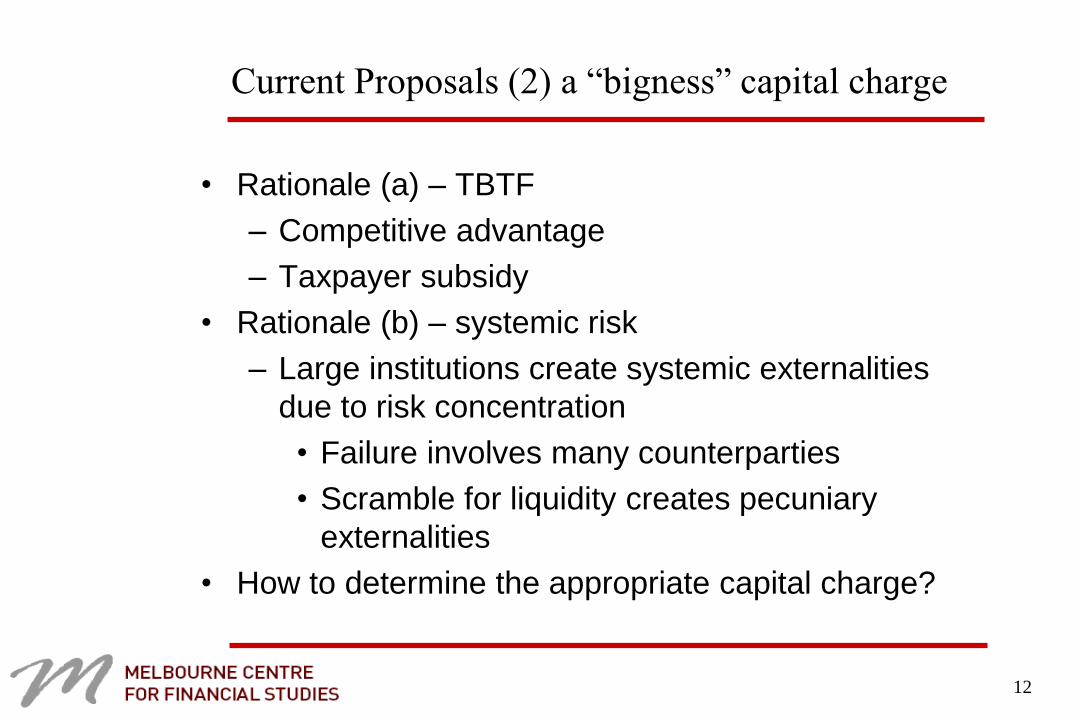

Current Proposals (2) a “bigness” capital charge

• Rationale (a) – TBTF

– Competitive advantage

– Taxpayer subsidy

• Rationale (b) – systemic risk

– Large institutions create systemic externalities

due to risk concentration

• Failure involves many counterparties

• Scramble for liquidity creates pecuniary

externalities

• How to determine the appropriate capital charge?

13

Current Proposals (3) contingent capital

• Requirements for banks to issue hybrid securities

which convert automatically into equity if some

“trigger point” is reached

– Restores core capital

– Market discipline through monitoring by investors

• Reduces likelihood of government injections of

equity in crisis or provision of guarantees (which is

essentially equivalent)

14

Current Proposals (3) contingent capital

• Some examples

– Flannery – reverse convertible debentures (like

converting preference share structure)

– Squam Lake Group – conversion requires both

regulatory declaration of systemic problems and

issuing bank having inadequate capital

– Kashyap, Rajan, and Stein – Catastrophe

insurance

– Hart & Zingales – CDS spreads as trigger for

required new equity issuance

15

Current Proposals (3) contingent capital

• Lloyds Bank (and others) have issued (Nov 09)

CoCo’s

– How will markets react if trigger point is

approached?

• “death spiral convertibles”?

• Would partly-paid shares be an alternative?

– A return to pre limited liability arrangements?

16

Current Proposals (4) Regulatory Risk weight changes

• Basel II (July & Dec 2009)

• Increase in the relative counterparty risk weights for financial

institutions versus corporates

• Increased capital requirements for counterparty risk on

derivatives, repo and securitization transactions.

• Lower relative risk weights for counterparty derivatives

exposures to CCCPs versus bilateral exposures.

• Use of “downturn” PD estimates (and “downturn” LGD)

• “Stressed” VAR in determining capital requirements

• Reduced reliance on ratings agency assessments

• Expected loss provisioning.

17

Current Proposals (5) a leverage ratio

• A complement to risk weighted capital ratio

– Limit to balance sheet expansion

– Offset to model risk, incorrect risk weights

– Used in USA, Canada, Switzerland

• Bank of Canada study suggests it has value

• Problems

– Dealing with off-balance sheet activities

– Downgrades role of risk weighting

• Australian banks and regulators not supporters

– But introduction may change behaviour

18

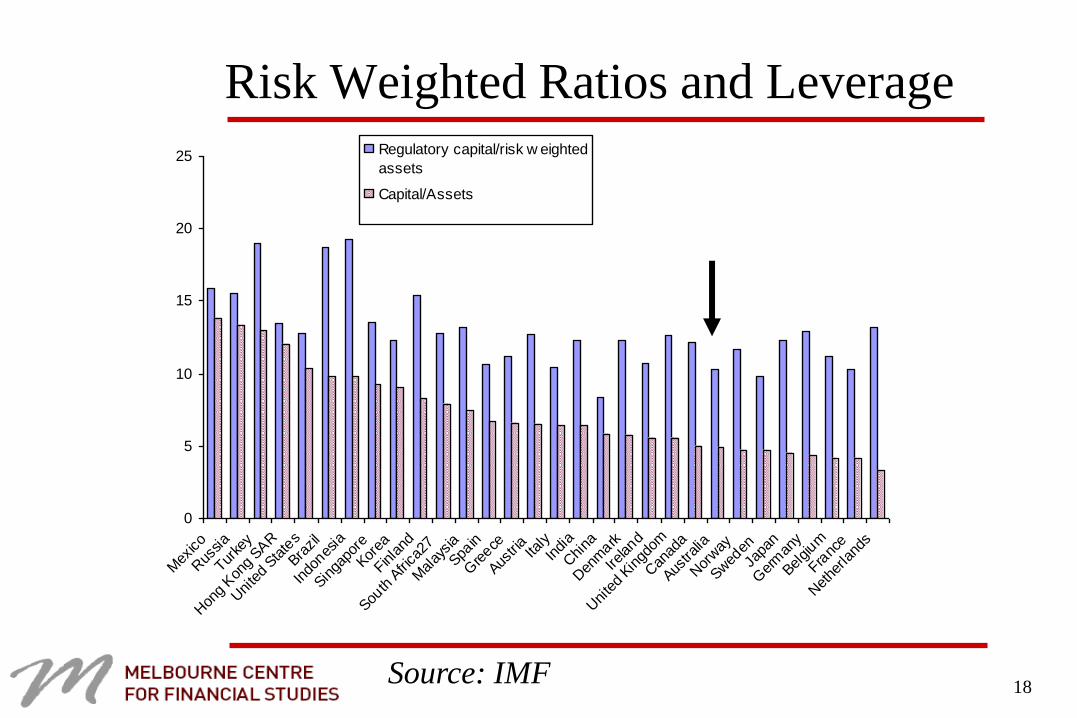

Risk Weighted Ratios and Leverage

0

5

10

15

20

25

Mex

ico

Rus

sia

Turke

y

Hon

g Kon

g SA

R

Uni

ted

State

s

Brazil

Indo

nesia

Singa

pore

Korea

Finla

nd

South

Afri

ca27

Mal

aysia

Spain

Gre

ece

Austri

aIta

lyIn

dia

Chi

na

Den

mark

Ireland

Uni

ted

Kingd

om

Can

ada

Austra

lia

Nor

way

Swed

en

Japa

n

Ger

man

y

Belgium

Franc

e

Net

herla

nds

Regulatory capital/risk w eighted

assets

Capital/Assets

Source: IMF

19

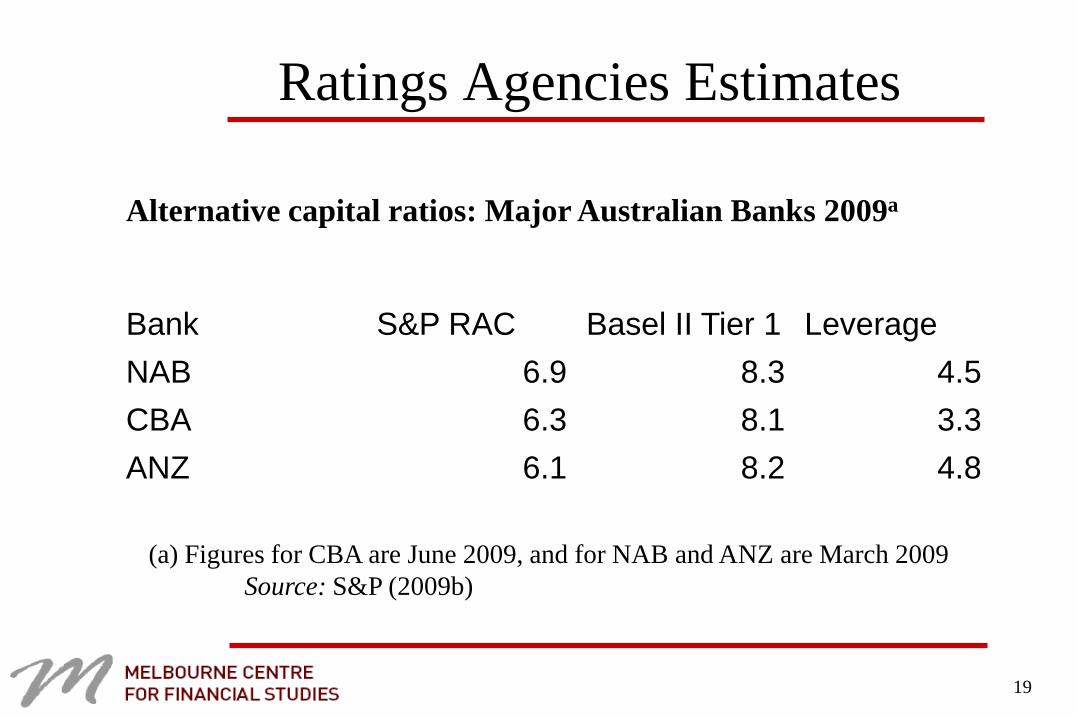

Ratings Agencies Estimates

Alternative capital ratios: Major Australian Banks 2009a

Bank S&P RAC Basel II Tier 1 Leverage

NAB 6.9 8.3 4.5

CBA 6.3 8.1 3.3

ANZ 6.1 8.2 4.8

(a) Figures for CBA are June 2009, and for NAB and ANZ are March 2009

Source: S&P (2009b)

20

Current Proposals (6) improved quality of capital

• Basel Committee

– Larger share of Tier 1 capital to be shareholders

funds (common equity and retained earnings)

– Stricter requirements for hybrids (perpetual,

discretionary non-cumulative dividends/coupons)

– Calibration to occur following an impact

assessment study

• How to incorporate contingent capital?

21

Current Proposals (7) procyclical capital requirements

• Inherent procyclical nature of banking

– In downturn, loan losses reduce capital and

prompt lending restraint

• Higher minimum capital requirements in upswing

and lower in downswing

– In good times build up of capital buffers for use in

poor times

• Rules v Discretion?

22

Conclusions

• Significant changes to bank capital requirements in

progress

• Overall consequences far from obvious

– What proposals will be implemented?

– How will they interact?

• Increase in cost of bank financial intermediation?

– What was the social cost of pre-GFC bank

intermediation?

![Capital Adequacy (E) Task Force - National Association of ... · Capital Adequacy (E) Task Force . RBC Proposal Form [ ] Capital Adequacy (E) Task Force ... LR004 – Mortgages –](https://img.pdfslide.us/doc/110x75/5f0a28317e708231d42a4995/capital-adequacy-e-task-force-national-association-of-capital-adequacy-e.jpg)