Embed Size (px)

DESCRIPTION

Need help with slow payers? Get your bills paid on time and prevent problems with debtors.

Citation preview

LEDGER GUARDwww.ledgerguard.com.au

GOOD PAYERSThe Science of Getting Paid on Time, In Full, Every Time

As a business owner, it’s your right to be paid for the work you do and the goods you supply.

All too often, business owners feel as though they shouldn’t ‘offend’ their clients by implementing debt prevention strategies or following up on unpaid accounts.

The fact is, if you don’t get paid, your business fails. If your business fails, your creditors don’t get paid and so it goes on.

By downloading this eBook, you have made a leap of faith. Even though you may intellectually know what has to be done to ensure you get paid, you may feel as though you don’t have all the tools or you may need that extra prompt to be more proactive and more assertive in your accounts receivable protocols.

In the current business environment, no one is immune to slow payers, bad debt and cash flow problems. We see so many insolvencies listed each and every month. All businesses – large or small – are potentially at risk.

If your business has not experienced problems with non-paying customers to date, you have been very fortunate. However you can’t afford to be complacent. All businesses need to proactively protect their cash flow and profit from any possible fallout from their customers’ cash flow problems.

We’re very pleased to share with you the strategies that we’ve learned over the last twenty years working in the credit management and debt collection industry.

We’ve started with tips for getting out of trouble when you’re faced with seriously slow payers and then moved back to the beginning of a business relationship and focused on tips for preventing problems with debtors in the first place.

You’ll find plenty of practical ideas and strategies you can use immediately to get outstanding accounts paid up to date. You’ll also learn how to better manage your accounts from now on so you never have to wait to get paid. We’ll even show you how to put your invoices ahead of others in the payment queue.

Instead of wasting time chasing up debtors and suffering the frustration that goes with it, wouldn’t you prefer to spend that time growing and developing your business? By investing a little time in reading this eBook, you’ll find the comprehension and motivation you may have needed to take stock of your accounts receivables procedures and evaluate what could be done better.

Ultimately, by implementing our tips and strategies, you’ll find your customers will pay on time, your bank balance will be healthier and your related stresses will be minimised, if not eliminated. We know from experience as we’ve helped hundreds of businesses do just that…

Happy reading and here’s to the end of your debtor woes.

Getting Paid is Not a Privilege, It’s a Right

Debt Prevention Strategies Save You Money & Grief, But What if the Ship Has Sailed? . . . 1

Do You Have a Delinquent Account? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Arranging a Payment Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Continuing Business Safely with Slow Payers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 The Need & the Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 How to Mitigate Your Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-8

Get Paid Faster by Invoicing the Right Way . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

The Art of Invoicing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Don’t Stop Until It’s Paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Start Right for Prompt Payment Every Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

The Basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Upfront Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Post Job Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

The 3 Most Important Front End Strategies for Managing Financial Risk . . . . . . . . . . . . . . 16

This is Where You Need to Start Before You Extend Credit . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Credit Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Terms of Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19-21

Credit Checking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-23

Client Case Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24-25

Client Testimonials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Where to from Here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

About The Authors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

DEBT PREVENTION STRATEGIES SAVE YOU MONEY & GRIEF

But What If The Ship Has Sailed?

How do you get a debtor to pay up if their account is now overdue and you don’t have any debt prevention strategies in place?

1

GET PAID FASTER BY INVOICING THE RIGHT WAY

A Crucial Guide To Avoiding Slow Payers

One of the most effective ways to shore up your business’s cash flow situation is to ensure you get paid faster....

9

CONTINUING BUSINESS SAFELY WITH SLOW PAYERS

Determining Whether To Rescue A Situation Gone Sour

When you have customers whose accounts ‘go bad’, it can be difficult to decide whether or not to continue doing business with them.

4

START RIGHT FOR PROMPT PAYMENT EVERY TIME

Set Yourself Up For Business Sucess

There is no crystal ball that will tell you if you will get paid, in full and on time, but there are steps to reduce or even eliminate the risk. It’s up to you to perform your due diligence.

12

THE 3 MOST IMPORTANT FRONT END STRATEGIES

For Managing Financial Risk

Credit Applications

Terms of Trade

Credit Checks

15

1

4

9

12

16

Contents

DEBT PREVENTION STRATEGIES SAVE YOU MONEY & GRIEF

But What if the Ship Has Sailed?

How do you get a debtor to pay up if their account is now overdue and you don’t have any debt prevention strategies in place?

1

1: ACT NOW!

Waiting patiently — or impatiently, and suffering building frustration — will not get your account paid. Stop hoping for a good outcome. Take action immediately.

2: CALL OR VISIT

Your reminder letter will likely remain unopened or be thrown in the bin. Make those difficult calls. If your calls are not answered, visit your client to discuss the situation.

3: PREPARE YOUR CASE

Before you call or visit your client, gather all the relevant paperwork such as outstanding invoices, statements, credit application and signed contract. Track the case from order number through to proof of delivery and any attempts made to contact for payment. Find out who pays the account so you speak to the correct person.

4: ASK, LISTEN AND COMPREHEND

Ask lots of questions and listen carefully to the answers. Be sure you understand your debtor’s financial situation and how serious their cash flow position is. Never accept that they are waiting to get paid by their customers.

Naturally, at Ledger Guard we’re all about helping our clients to avoid this kind of situation in the first place but let’s face it, business owners are busy people.

Despite best intentions, sometimes busy people procrastinate on putting preventive measures in place … until they are burned.

The good news is that there is still hope for an amiable resolution.

You have extended credit to them based on your terms of payment and they have accepted these terms.

5: REMAIN POLITE AND IN CONTROL

Never attack or abuse your debtor as it will only be counterproductive and will result in the destruction of any ongoing business relationship. Where appropriate, empathise with your debtor. Be fair but be firm about your expected outcome.

6: START AT 100% THEN NEGOTIATE

Always ask for the payment in full first and then consider negotiating on payment terms to accommodate.

7: NEVER ASSUME THEY CAN’T PAY

If your debtor has a cash flow problem, be willing to negotiate a repayment arrangement that they can reasonably afford.

8: RECORD THE CUSTOMER

Keep a record of what is said and promised. Confirm in writing either by email or fax what has been agreed upon.

Do You Have a Delinquent Account?

2

GET PAID UPFRONT FOR FUTURE WORK

If you intend to continue doing business with this debtor, their account could proceed on cash terms until their account is up to date.

Affirmative Action Could Save The Relationship

If your debtor can’t pay the full amount, you need to secure a commitment to pay something immediately, followed by weekly or fortnightly payments as mutually agreed. On a $5,000 outstanding account, $500 a week for ten weeks is better than nothing.

In fact, your debtor will likely feel as though a weight has lifted from his shoulders, knowing he can pay a less overwhelming sum over an agreed period of time.

Ask: “What can you afford to pay me today?”

DRAFTING A PAYMENT AGREEMENT

Draft a Payment Agreement and include terms and conditions covering what is expected from each party, any interest component and/or administration fees and consequences of breaking the agreement. If you need help, Ledger Guard can draft one for you.

GET IT IN WRITING & FOLLOW UP

Once the payment plan has been agreed – and confirmed in writing – it is up to you to rigidly follow up, every time. Monitor the account closely, send payment reminders before each due date and follow up if not paid on the promised date.

Arranging a Payment Plan

WHAT TO DO IF THE PROBLEM PERSISTS

If you continue to get the run-around and your debtor makes no genuine attempt to reach a payment agreement, then your best choice is to hand the account over to a professional debt collection agency like Ledger Guard who is skilled in recovering outstanding accounts while protecting the supplier-client relationship.

3

CONTINUING BUSINESS SAFELY WITH SLOW PAYERS

How to determine the risks vs the rewards and take steps to mitigate your risk.

When you have customers whose accounts are in arrears it can be difficult to decide whether or not to continue doing business with them.

4

On the one hand, you could use the sales but on the other hand, you don’t want to be working for nothing, which is potentially what can happen if you continue to serve problem customers.

Whilst an overdue account could be a once-off situation, there are steps you can take to manage your risk so that you can continue trading with customers whose payment history has not been perfect.

A payment plan is one such step but here are some other valuable suggestions that will help.

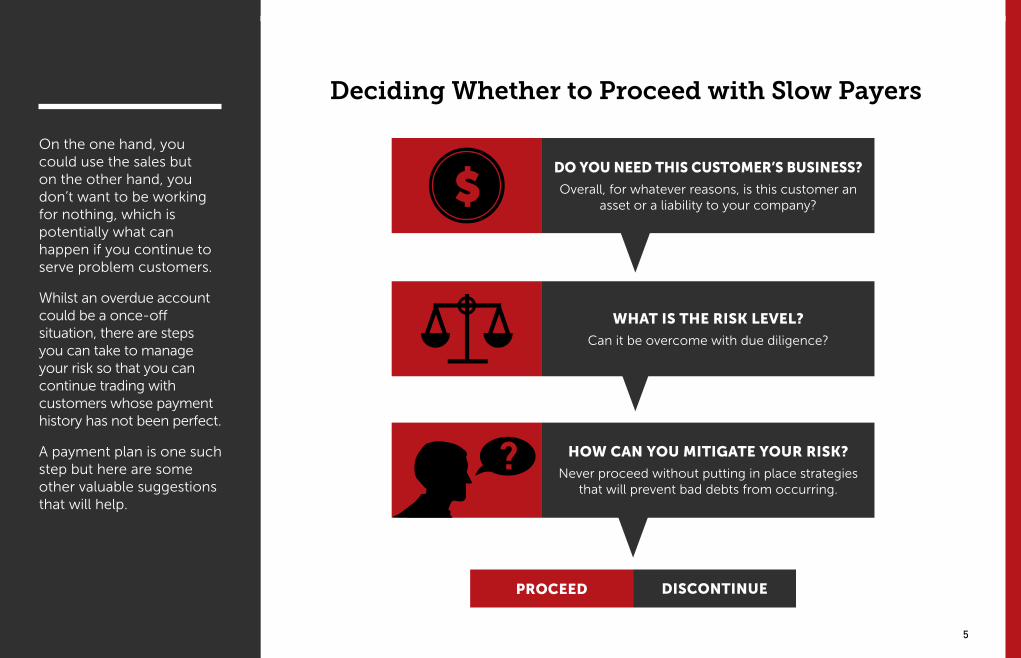

Deciding Whether to Proceed with Slow Payers

DO YOU NEED THIS CUSTOMER’S BUSINESS?

Overall, for whatever reasons, is this customer an asset or a liability to your company?

WHAT IS THE RISK LEVEL?

Can it be overcome with due diligence?

HOW CAN YOU MITIGATE YOUR RISK?

Never proceed without putting in place strategies that will prevent bad debts from occurring.

PROCEED DISCONTINUE

5

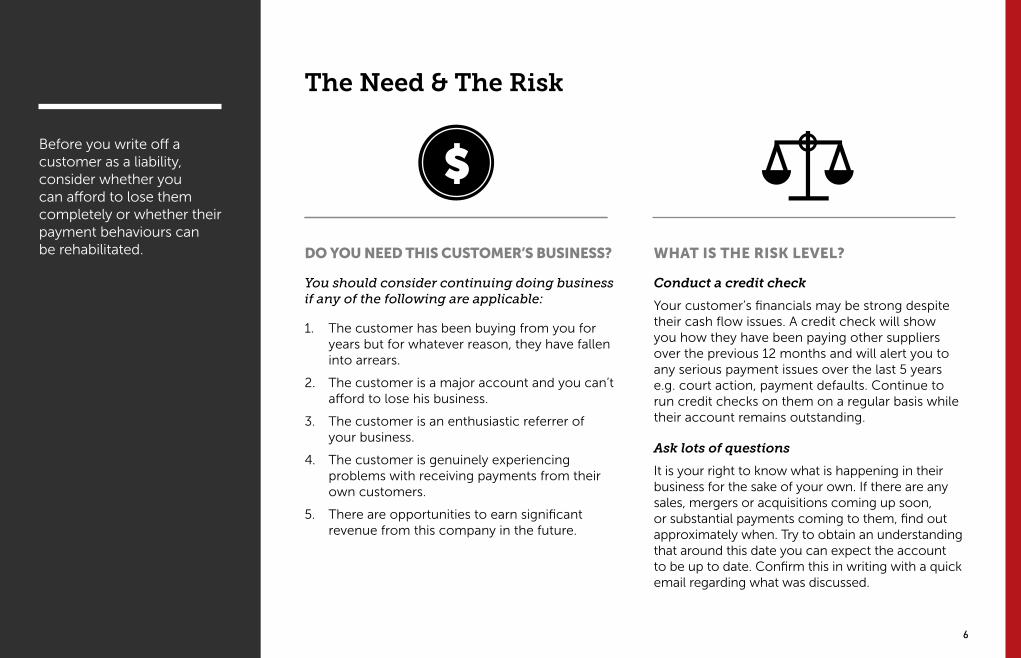

Before you write off a customer as a liability, consider whether you can afford to lose them completely or whether their payment behaviours can be rehabilitated. DO YOU NEED THIS CUSTOMER’S BUSINESS?

You should consider continuing doing business if any of the following are applicable:

1. The customer has been buying from you for years but for whatever reason, they have fallen into arrears.

2. The customer is a major account and you can’t afford to lose his business.

3. The customer is an enthusiastic referrer of your business.

4. The customer is genuinely experiencing problems with receiving payments from their own customers.

5. There are opportunities to earn significant revenue from this company in the future.

WHAT IS THE RISK LEVEL?

Conduct a credit check

Your customer’s financials may be strong despite their cash flow issues. A credit check will show you how they have been paying other suppliers over the previous 12 months and will alert you to any serious payment issues over the last 5 years e.g. court action, payment defaults. Continue to run credit checks on them on a regular basis while their account remains outstanding.

Ask lots of questions

It is your right to know what is happening in their business for the sake of your own. If there are any sales, mergers or acquisitions coming up soon, or substantial payments coming to them, find out approximately when. Try to obtain an understanding that around this date you can expect the account to be up to date. Confirm this in writing with a quick email regarding what was discussed.

The Need & The Risk

6

How To Mitigate Your Risk

Maintain Contact

Keep in touch with the business owner or financial controller so you are foremost in their mind when they are paying accounts. That way you’ll be at the top of their list and the first to know when their cash flow improves and your account can be brought up to date. You also need to be kept in the loop if their situation deteriorates even further.

Keep Accurate Contact Details

It’s vital that you maintain up to date contact information on the business and its owner/s. This is especially important when you have a late payer that must be monitored closely.

Keep a Tight Leash

Treat your debtor with respect, but make sure he knows his account is being watched closely until it is paid.

Reassess Credit Limits and Terms

You may need to adjust these based on the sum outstanding, the information on the credit report and your assessment of your risk. If things still look too risky, then you should supply goods or services on a cash upfront or cash on delivery basis until the account is back on track.

Charge Interest on the Overdue Amount

Doing this will show you are serious about your payment terms and cash flow. Be aware though, that you are only entitled to charge interest if you have an interest clause in the Terms and Conditions agreed to by the customer before your goods/services were supplied.

Secure a Personal Guarantee

If your debtor is a company, seek a personal guarantee from the director. Provided the director has assets e.g. owns a property, this will provide you with some security if the company becomes insolvent before the account has been paid.

Take Out Credit Insurance

For a fee, a credit insurance company like NCI will insure you against bad debt and customer insolvency.

7

How To Mitigate Your Risk

Retaining existing customers is always less costly than attracting new ones, especially if your shared history has been lucrative.

Once you have assessed the risk and implemented the appropriate measures to protect your business, you can afford to be cautiously optimistic that the relationship can continue successfully in the future.

Lodge a Caveat

If you have a Security and Charge clause in your Terms and Conditions, secure the debt by lodging a caveat on property belonging to your debtor.

Implement a Payment Plan

Create one — in writing — that allows your debtor to make regular weekly payments until the account is brought up to date. Make sure you clearly spell out your terms covering the agreement and your debtor signs their acceptance.

Sign Up with a Credit Reporting Company for Email Alerts

Any negative changes to your debtor’s credit file will be emailed to you, and you get to decide what information will trigger the alert. You won’t have to pay unless or until you receive an alert.

Register a Security Interest

The PPSR allows you to register a security interest in your goods. This means that in the event of insolvency, you become a secured creditor.

Factor Your Invoices

Factoring may be a good option if the debtor has a history of not paying on time. Basically, you sell your invoices to a factoring firm – such as Fifo – at up to 80 - 90% of their value and receive the cash upfront as soon as invoices are issued. With Fifo this can even be done with one off invoices. When the factoring company collects the debt they pay you the balance, less their fee. This effectively reduces your profit, but helps maintain your cash flow.

8

GET PAID FASTER BY INVOICING THE RIGHT WAY

A Crucial Guide to Avoiding Slow Payers

Don’t just hope for the best, it’s time to think strategically about getting paid.

9

The Art of Invoicing

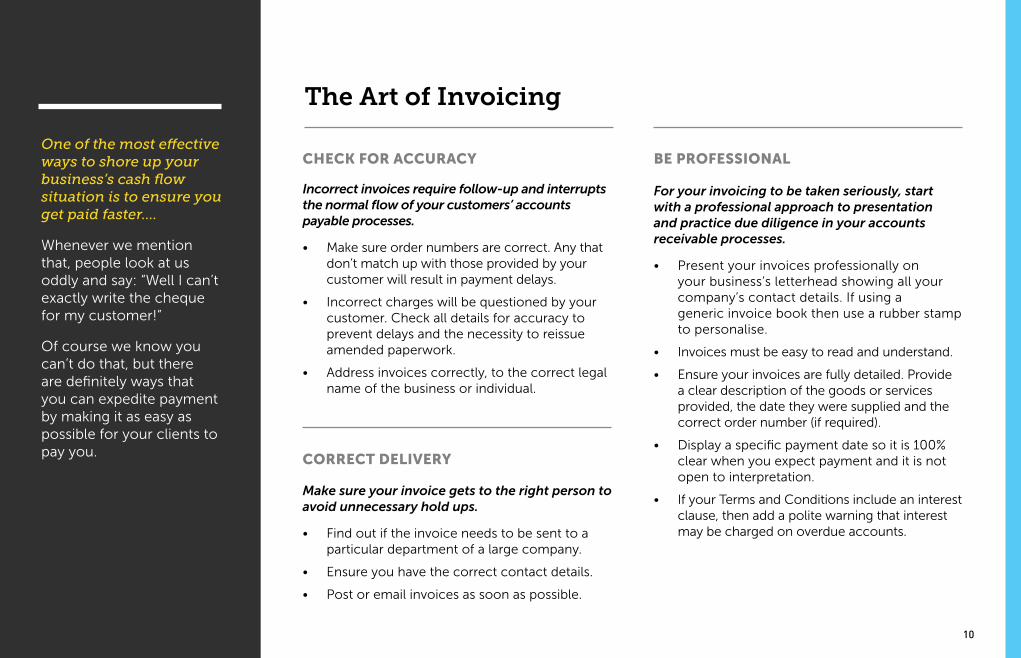

BE PROFESSIONALOne of the most effective ways to shore up your business’s cash flow situation is to ensure you get paid faster....

Whenever we mention that, people look at us oddly and say: “Well I can’t exactly write the cheque for my customer!”

Of course we know you can’t do that, but there are definitely ways that you can expedite payment by making it as easy as possible for your clients to pay you.

For your invoicing to be taken seriously, start with a professional approach to presentation and practice due diligence in your accounts receivable processes.

• Present your invoices professionally on your business’s letterhead showing all your company’s contact details. If using a generic invoice book then use a rubber stamp to personalise.

• Invoices must be easy to read and understand.

• Ensure your invoices are fully detailed. Provide a clear description of the goods or services provided, the date they were supplied and the correct order number (if required).

• Display a specific payment date so it is 100% clear when you expect payment and it is not open to interpretation.

• If your Terms and Conditions include an interest clause, then add a polite warning that interest may be charged on overdue accounts.

Make sure your invoice gets to the right person to avoid unnecessary hold ups.

• Find out if the invoice needs to be sent to a particular department of a large company.

• Ensure you have the correct contact details.

• Post or email invoices as soon as possible.

CORRECT DELIVERY

Incorrect invoices require follow-up and interrupts the normal flow of your customers’ accounts payable processes.

• Make sure order numbers are correct. Any that don’t match up with those provided by your customer will result in payment delays.

• Incorrect charges will be questioned by your customer. Check all details for accuracy to prevent delays and the necessity to reissue amended paperwork.

• Address invoices correctly, to the correct legal name of the business or individual.

CHECK FOR ACCURACY

10

Your invoice must arrive in the hands of the person who is responsible for payment. If it doesn’t, then you can pretty much count on payment delays.

• Find out who pays your invoices and build up a friendly relationship so your account is treated as a priority. This is especially important when cash flow is tight. Email or post invoices directly to that person.

• Know who to contact if a telephone reminder is required.

• Familiarise yourself with your Customers’ accounts staff.

• Include on the invoice the name of the person who placed the order.

THE PERSONAL TOUCH

Everyone is busy. Forgetting to send invoices and forgetting to pay accounts is common, but you can control the timing with these effective measures.

• Invoice immediately. You don’t have to wait until the end of the week or month. It is entirely appropriate to send your invoice on the day your goods are delivered or services completed.

• Send reminder emails the day before your invoice is due. Don’t assume your customer will remember to pay on due date.

TIME CONSIDERATIONS

REWARD PROMPT PAYMENT

Customers who pay on time are like 24-carat gold and should be well looked after.

• Acknowledge customers who pay promptly. A box of chocolates as thanks to a new customer who has paid on time doesn’t cost a lot but is worth a great deal in terms of good will.

• Send a quick email saying “Thank you for your prompt payment. It’s much appreciated. We wish we had more customers like you.”

Don’t Stop Till It’s Paid!

Not all customers are delinquent payers. Some people truly just forget to pay their accounts or invoices can sometimes get lost in the system.

By doing all you can to help your customers pay your invoices on time, you’ll ensure that your cash flow is healthy and that you too can pay your bills on time.

11

START RIGHT FOR PROMPT PAYMENT EVERY TIME

Set Yourself up for Business Success

If you’re not in the habit of anticipating potential credit risk, then it’s time to get on the right track.

12

You’ve heard the expression: “Prevention is better than cure.” Well this rings very true in business.

What you do before you supply your goods and services can spare you a great deal of stress and anxiety, not to mention costs involved in debt collection and the time it takes to chase up bad debts.

There is no crystal ball that will tell you if you will get paid, in full and on time. But there are definite steps you can take to reduce or even eliminate the risk of not getting paid. It’s up to you to perform your due diligence.

The Basics

CREDIT CHECK YOUR CUSTOMERS

Do your homework on your customers — you might find that their accounts payable record is not what it should be. If there is a serious risk of bad debt, then you may be better off leaving the deal on the table and walking away.

Alternatively, if the trade payments information shows they have been paying suppliers outside their payment terms in the last 12 months, then you may opt to request cash on delivery or impose very limited credit terms.

PREVENTATIVE PAPERWORK

Good documentation in place with your customers makes it plain that you intend to be paid for every service you provide and product you sell. The documentation is your insurance policy against bad debts and is also your recourse for debt collection if all your best prevention protocols fail.

CREATE A CREDIT POLICY

You need to write up a set of rules that outline all your credit processes from assessing an applicant for credit, right through to full account payment. You must be completely transparent and upfront with all new customers so that they understand and accept the rules that apply to their credit account including their credit limit, credit period, interest that could be charged if the account is not paid on time and other potential consequences of defaulting on payment.

DOCUMENT YOUR ACCOUNTS PROCESSES

Your accounts processes need to be understood and followed by all relevant accounts and salespeople in your business, and as a team you can then provide your customers with clarity and consistency regarding your management of trade credit.

Being aware of your position is a great way to protect yourself from any otherwise unforeseen issues.

13

USE A CUSTOMER SIGN-OFF FORM

This provides you with written proof that your goods and services were completed to your customer’s satisfaction.

Get Everything in Writing

Verbally agreeing to supply goods and services without first obtaining signed paperwork is a recipe for disaster. All quotes and orders must be confirmed in writing so that you have an efficient paper trail. All variations or changes to Scope of Work must be in writing and signed off by both parties.

Discuss Your Terms

Discuss payment and credit terms upfront so that your customer knows you’re serious about getting paid.

PRACTICE FULL TRANSPARENCY

Showing your customers what you expect from them and what they can expect in return demonstrates good will and encourages a willingness to comply with your terms.

USE A CREDIT ACCOUNT APPLICATION OR SIMPLE INFORMATION FORM

The first function of these forms is to identify the correct person or business entity to invoice. They also provide you with good contact information in the event that you have to chase up a bad debt.

PROVIDE YOUR TERMS AND CONDITIONS TO EVERY CUSTOMER

All customers must receive a copy of your Terms and Conditions before doing business with you so that they know the terms under which you will supply your goods and services. This is a legal document that spells out what is expected of both parties and eliminates the potential for disputes to arise. Your T&Cs also allow you to enforce your contractual rights including the right to claim interest on overdue accounts, and recover the cost of using a third party debt collection firm.

Make your procedures clear to your client and get their agreement in writing to avoid problems down the track.

Upfront Measures

14

One should never assume that payment will be forthcoming, regardless of how large or small the order or invoice. Ultimately, getting paid on time is not just the responsibility of your debtors.

It is a responsibility of yours, as a business owner, to put preventative measures in place that will prevent problem customers from taking advantage of You.

In the event that things do go wrong, you will have adequate measures in place to enable you to pursue debtors yourself or to have a firm such as Ledger Guard follow up for you.

USE TELEPHONE REMINDERS

Phone the person responsible for paying your account a couple of days before the payment due date. A friendly reminder will make sure your invoice hasn’t gone missing and will keep your account foremost in their mind.

The importance of good timing can never be underestimated. Never be too busy to attend to your accounts.

INVOICE PROMPTLY

Don’t delay on invoicing as this sends the wrong message to your customer. Provide an invoice upon delivery of goods or on completion of work or on each agreed stage of work.

Post Job Strategies

15

THE 3 MOST IMPORTANT FRONT END STRATEGIES

For Managing Financial Risk

Credit ApplicationsTerms of TradeCredit Checks

16

This is Where You Need to Start Before You Extend Credit

CREDIT APPLICATIONS

TERMS & CONDITIONS

CREDIT CHECKS

A Credit Application is a document that gathers critical information about your customer that can be used for credit checking.

An Important document that spells out the rules for doing business with you.

Carry out a credit check at the front end to avoid problems in collecting payment at the back end.

17

Know Your Customers

Every customer should fill out a credit application or equivalent that gathers all the important relevant facts about them. This form needs to include a signed agreement to your terms and conditions.

Review the completed application to make sure the information supplied is correct, check out the listed trade references and make sure everything adds up.

Often, the very fact that your customers have signed a Credit Application will make them wary of falling behind on their outstanding debts. And if anyone refuses to complete and sign one, then there is every chance that they are a bad debt risk. Maybe they don’t want you checking up on them and finding out about their poor credit history. In that case, simply explain to them that they can only purchase from your business with payment upfront.

Benefits of Credit Applications

Credit Applications

Free Checklist

Check out our free resources on page 26 to download a comprehensive checklist of the info to request on your Credit Account Application Form.

18

Prepare for The Worst

Expecting clients to instinctively understand the rules of the game will result in difficulties. They are not experts at what you do; you are. So they may not be aware of how the smallest changes to the overall job can cause major blowouts in costs and time.

It’s inevitable then that resentment can arise and a client who engaged you because they love your work can become your most disloyal ex-client. You can protect against this happening by providing them with your Terms of Trade. Spelling out the conditions of working with you can even create raving advocates of your goods and services.

What Terms of Trade Mean

Before you sell goods or services to any customer, it’s important that you provide them with a copy of your terms and conditions. This is a legal document most commonly referred to as Terms of Trade, but also known as Terms of Supply, Terms of Sale, Terms of Engagement and Terms of Hire.

Every business should have Terms of Trade in place before dealing with any and all customers. It protects your business and gives you legal recourse should anything untoward occur.

When to Use Terms of Trade

Once you have your Terms of Trade document created, it should be provided to every customer before any initial transaction is conducted. It should be used for new, unknown contacts as well as old and trusted friends.

Get It in Writing

Verbal agreements can complicate matters when misunderstandings occur and can also lead to your reputation being tarnished. Written legal agreements remove any elements of doubt by spelling out what is expected of each party.

What Terms of Trade Do

Terms of Trade provide a foundation for negotiating and resolving any disputes, and give you the ability to enforce your contractual rights. They also show your customers that you intend to operate fairly and with all terms spelled out before work is undertaken or goods are provided.

In the event that a transaction between your business and your customer goes sour, your Terms of Trade document can give you the right to claim interest on overdue accounts and recover any costs of using a third party to collect the debt.

What Are Terms of Trade

Terms of Trade

Teaching Your Clients How to Treat You

When you do business with clients, the very best thing you can do to set a professional standard, is to demonstrate that you are easy to deal with but, that you are also fair and expect fairness in return.

19

Scope Creep

Who can be Effected by Scope Creep?

Scope creep is common in many industries including web design, graphic design, architecture, construction, accountancy to name a few.

Don’t Just Avoid the Problem

Businesses can sometimes feel as though they have to meet the client’s expectations or lose the client or their referrals. So they give in and comply which leads to resentment and sometimes, cutting corners on the original brief in order to not lose money on the overall job.

The Best Way to Avoid Scope Creep is to Implement Terms of Trade

Terms of Trade should always be:

• Seen as an investment in the success and longevity of your business.

• Written by a professional experienced in the preparation of these documents.

• Written so that they are legal, fair and straightforward.

• Written with the goals of clarity, simplicity and readability in mind.

• Practical and easy to implement.

• Provided to customers before conducting any initial transaction.

• Signed by your customer and returned to you before commencing work or providing goods.

• Reviewed at regular intervals to ensure they continue to serve your business’s needs.

Terms of Trade — The Top 5 Benefits

• They create a solid foundation upon which to base single and ongoing transactions.

• They help to keep your cash flow positive.

• They eliminate the potential for disputes to arise.

• They demonstrate your business’s professionalism.

• They give you peace of mind knowing you and your clients’ legal obligations are spelled out.

Above all else, Terms of Trade are part of good business practice. They enhance your customers’ view of your professionalism and that’s an enormous part of winning new custom from the outset.

Terms of Trade

What is Scope Creep?

When terms and conditions are not spelled out, ‘scope creep’ can occur. This refers to uncontrolled changes in a project’s scope and can lead to unrealistic expectations on the client’s part.

Usually what happens is a client will expect or demand that additions over and above the initial agreement be ‘thrown in’, mostly due to lack of client understanding of what can reasonably be absorbed into a project’s costings.

20

Who Benefits Most from having Terms of Trade?

Unless you are paid upfront in full before you hand over your goods or start your services you are at risk from non- paying customers. Having said that, some businesses face greater risk than others in this category.

To reduce your risk and protect your cash flow you need to use the right documents at the right time in the right way. Even if you can get paid upfront you are still exposed to many potential issues including liability and warranty claims that could cost your business thousands of dollars even if you are insured.

Is Your Business at Risk?

Those whose work or goods are customised for specific clients and cannot easily be sold to another business if the order is canceled or the work disputed, are particularly vulnerable.

Such businesses include steel fabricators, cabinet makers, printers, bespoke tailors and graphic designers. Another susceptible group includes professionals that invest significant human capital upfront such as accountants, architects, engineers and consultants.

Trade industries that purchase specialised products for their customers are also at risk as are businesses of course in the building and construction industry.

Potential Risks That Can be Covered with TOT

• Variations to the original scope of work is a common issue in many industries especially the building and construction industry and the creative industries e.g. web & graphic design.

• Paying suppliers promptly but waiting to get paid by customers. Any business that purchases product from a 3rd party to use in producing goods or services is potentially out of pocket until they are reimbursed by their customer.

• Liability claims when you’re not at fault or could have limited your liability, e.g. a gas fitter or plumber is instructed to dig a channel to lay pipes, hits a fibre optic cable below the ground resulting in a $40,000 repair bill from Telstra.

• Unfair claims for substandard work, injuries or property damage caused by a subcontractor’s negligence, is a common issue for head contractors who operate without a comprehensive agreement in place.

• Canceled orders, after you have started the work and incurred expenses.

• Unfair warranty claims when ultimately, it was user fault , e.g. the remote control for an air conditioner was not used correctly resulting in the unit not working. No repair was needed, but the air conditioning repair business incurred call out costs.

Very few businesses can safely trade without the backup of a well-constructed Terms of Trade (TOT) agreement covering all the potential issues that could cripple the business’s operation.

It always pays to document the agreed terms so that something in writing exists that can be referred to if there is an issue that isn’t your fault or there is a dispute over what was agreed by both parties.

Are You At Risk?

21

Credit Checking Can You Trust Your Customer to Pay You?

Once you have your customer’s completed credit application, you should check out their credit history. You may feel uncomfortable doing so but let us put it this way; if a potential customer said he’d do business with you but only if you worked for him for free, would you take him on? It’s certainly a ludicrous question, but the reality is, plenty of businesses are working for free or delivering free products because they haven’t done the research to find out if their customers can actually pay their invoices.

You deserve to be paid and you deserve peace of mind. Once you’ve run the appropriate checks and found that your new customer has a good credit history and always pays his accounts on time, imagine the sigh of relief you’ll breathe. Not only does it mean you can count on prompt payment but it also means you can be enthusiastic about providing goods and services to this customer. Relationships, even in business, are everything.

Here are three fundamental ways to minimise your exposure to bad debt:

Target Be selective when considering who to supply on credit. Aim to do business only with organisations who have demonstrated the capacity and willingness to pay their invoices.

Investigate It is up to you to reduce your risk of not getting paid. Research the credit history of the company and then make doubly sure by investigating the directors of the business and their other interests.

Review RegularlyNever accept that a healthy credit record will remain so. Monthly, quarterly or half yearly credit check-ups will alert you to any red flags that appear on your client’s records.

How Much Do You Know About Your Client?

Why You Must Credit Check Customers

When you sit down and determine who would be your ideal client, you probably list specifics such as industry, business size and even geographical location. We’re here to tell you that above all else, your prime criteria, before all else should be……

Can Pay, Will Pay?

22

Credit Checking

Automatic Alerts

Ledger Guard can set up – on your behalf – a credit alert on a client’s company so that you can be notified of adverse changes to their credit behaviour, changes in directors and ownership structure and any appointment of an administrator.

This way you won’t be the last one to know what has happened to your client and you will only be charged when a change occurs.

Be Prepared to RefuseSometimes refusal is sadly, the correct strategy when it comes to extending credit. No matter how much you want or even need the business, if there is significant risk that you won’t be paid, you may be working for free. The alternative is to request payment upfront or agree to progress payments by direct debit from a credit account or bank account using an organisation like Ezidebit.

Use Credit Information to Grow, Not Limit, Your Business.

• Credit reporting helps you to identify who is a bad risk, but it also identifies clients with whom you could be doing more business.

• Bad debt has a trickle down effect. Don’t let your business and your good name be infected by clients whose credit situation is in poor health.

• Believing there is good in everyone belongs outside of business. Burying your head in the sand can put YOU out of business.

Credit Reporting Myths

• This company has been my customer for years. I’m sure they’ll always be reliable payers.

In fact 80% of bad debt comes from customers of twelve months or more.

• My customers are huge companies. I’ll always get paid.

In fact big businesses fail too! And their losses can be monumental.

• We can’t afford a credit reporting service.

In fact no business is too small to guard against bad debt. A basic credit check can cost as little as $10 and can spare you hundreds if not thousands of dollars of bad debt.

• I always request 3 trade references from potential customers. That’s good enough.

That is good, but do you really think your potential customer is going to put you in touch with suppliers whom they have failed to pay?

• A credit report won’t guarantee that a business will pay me on time.

Correct. Even the best paying customers may experience changes in their circumstances. An effective credit policy is one that continuously reviews customers and alerts you to such changes.

Benefits of Credit Checking

23

Client Case Studies

Graphic Design Business

This client had a history of slow payers and a few non payers when it came to scope creep.

Ledger Guard drafted robust documentation for them in the form of a Credit Account Application with a Director’s Guarantee section and Terms and Conditions. Not long after introducing their new T&Cs a builder client refused to pay his $46,000 account, citing a third party as being responsible for the debt. Once the graphic designer pointed out that the builder had signed a Director’s Guarantee, he stopped arguing and paid the account in full a week later.

The graphic designer was relieved that for once they had the paperwork right at the front end which made the outcome so positive.

Roofing Contractor

We worked with a very busy successful roofing business – Jones Roofing - back in 2008 to minimise liability and warranty issues and reduce their risk of not getting paid on time. One common issue back then was a customer’s unrealistic expectation of a partial roof repair, blaming our client if the roof leaked again even though it was another part of the roof that now needed attention. The contractors were often called to go back and fix the roof again, which was costing the business each time.

Ledger Guard drafted a number of business documents for Jones Roofing including comprehensive Terms of Trade that addressed their warranty and liability issues and also spelled out their rights and obligations and those of their customer.

We showed Jones Roofing how best to introduce their new documents and what measures they could take to ensure they got paid promptly. We’ve since contacted Lee Francis, the owner of the business to see how his business was faring. He has said they now have good control over their risk and have been paid for all call outs since,

significantly improving profitability.

24

Client Case Studies

Then, to speed things along, when he couldn’t get hold of the Contractor, the Earthmover purchased the materials for the job even though this was not included in his quote. Plus there were many aspects of the job that the Contractor was supposed to organise, but never did, so the Earthmover, wanting to get the job finished, went ahead and did them himself.

All this without any signed paperwork in place, just a perceived understanding. Needless to say, the story didn’t have a happy ending – our client ended up out of pocket by $70,000 when the Contractor became insolvent.

Ledger Guard is currently working with this client to make sure he protects himself first and foremost in every job he takes on and if the risks are too high he walks away.

Earthmoving & Excavation Business

This story highlights the need for due diligence in every circumstance no matter how rushed the job, how well you know your customer or what verbal promises your customer makes.

Our client, we will call him the Earthmover, went out of his way to help a Contractor who had under-quoted a job to the extent that the Earthmover’s fee alone was more than $20,000 over the Contractor’s quoted price. When the Earthmover asked the Contractor what he was going to do about the under-quoting, he was told “Don’t worry, I will make it up on another job”. The Earthmover wasn’t overly worried as he knew the Contractor fairly well and although a slow payer, he always paid up.

However, the risk in the job kept increasing. The Earthmover’s quote was never signed off, he was only given a few drawings – no tender document with terms and conditions, and no deposit received.

25

Client Testimonials

“Being an automotive workshop there are so many rules, regulations and licenses you have to have. One major issue with the automotive servicing industry is Terms and Conditions which we know a lot of other workshops simply do not have.

It gives a clearer understanding to the customer and is also very professional. A meeting with Larry from Ledger Guard was such a pleasure and opened our eyes up to so many different aspects. As well as the Terms and Conditions, Larry and the team at Ledger Guard provided us with Booking Sheets and our Credit Applications.

The most prized document which we believe is priceless is our Terms and Conditions. Larry explained each and every term in detail so we understand it fully. We would recommend Ledger Guard very highly and they have given us peace of mind.

If you are hesitant, don’t be. Ledger Guard is such a friendly company only helping you stay safe in your business.

We haven’t experienced the Debt Collection side of this company (and I hope we never do) but, if we do, we know that Ledger Guard is there to help us.”

Danny & Fiona Johnston, Platinum Automotive SolutionsRepco Authorised Service Centre

“As a practice we’ve just been through a process of reviewing and tightening up our payment and credit Terms and Conditions with an outfit called Ledger Guard. We felt Ledger Guard’s service was extremely professional and their price point offered value for money.”

Brad Peters, Partner, Online Accounting & Taxation Solutions

“Ledger Guard’s service was second to none and their commitment to understanding our business and its requirements was truly outstanding. Dealing with both Geraldine and Larry was extremely easy; they took care of everything and led me through each stage of the process. They were always contactable and happy to answer any questions I had.

Ledger Guard’s documents have provided us a strong framework for our business in terms of dealing with customers and other businesses. Their documentation and advice has provided us peace of mind. All business owners will require Ledger Guard’s services at some stage in their business life-cycle, it is just a matter of whether you are proactive and utilize the service before they are required. I know if I had have used Ledger Guard before, it would have made life a lot easier.”

Michael York, Owner, Flex Removals and All About Removals

“Ledger Guard’s services are an absolute must for any business wanting to limit their exposure to non paying debtors. By utilising their well written Terms and Conditions of Engagement, I feel a lot more confident in the administrative and structural process of taking on jobs and new clients.”

Michelle Jansen, Principal Ecommerce Consultant Cybecom Pty Ltd

“Ledger Guard helped me tighten my Terms of Service document and create a Credit Account Application form for my business. It was done professionally, promptly and at a very reasonable cost.”

Gina Lofaro, the Wordmistress

26

Where to from Here

It can seem overwhelming to have to make changes and create new documents and processes to make sure you get paid what is rightfully yours. After all, you’ve still got customers to serve, sales to make and a million other things business owners have to deal with.

Whilst this eBook has been written as a helpful resource on preventing and controlling debt, Ledger Guard is here to support you. You don’t need to figure it all out yourself. You can trust us to sort it out for you and provide you with exactly what you need.

We can show your accounts team how to best manage the credit processes, so your focus stays firmly on winning new customers that will pay you on time, and providing the best service to those you already have.

Ledger Guard specialises in the following:

• Terms and Conditions and associated forms that will ensure you are in the best possible position to successfully enforce your contractual rights. Ledger Guard offers three packages based on your need and budget.

• Credit reporting to find out if you are likely to get paid. Reports start from just $10.

• Reviewing credit applications to ensure the information you’ve received adds up.

• Assistance with processes for managing your account customers.

• Debt collection if your late payers are too difficult to handle.

Free Resources:

• Book a FREE 15-minute consult to discuss and assess your needs – contact Larry Brownson on 0439 630 722 or 07 3630 2533.

• Ask for a FREE review of your current Terms of Trade to find out if your level of protection is adequate for your business. Contact us on 07 3630 2533 or email your documents to be reviewed to [email protected].

• Download a FREE comprehensive checklist on what information should be requested on a Credit Account Application Form.

• Subscribe to Ledger Guard’s FREE monthly e-newsletter with more practical tips and strategies for managing trade credit.

• Access archived articles and newsletters on Ledger Guard’s website www.ledgerguard.com.au

27

About the Authors

They have written this eBook with all small to medium businesses in mind because without the benefit of in-house solicitors or accountants keeping a watchful eye over the day to day running of a business, there is a far greater risk of debtor problems.

If you would like find out more information on anything you have read in this ebook, feel free to contact Ledger Guard.

Phone: 0439 630 722 or 07 3630 2533

Email: [email protected]

Web: www.ledgerguard.com.au

“Our focus has always been on what should happen before you supply your goods and services. We firmly believe prevention is better than cure in every situation and urge you to introduce the strategies we recommend to reduce your risk and increase the cash coming into your business.”

Larry BrownsonLedger Guard

Larry and Geraldine Brownson established Ledger Guard in 2004 to help business owners in the small to medium business sector avoid debtor problems and manage their cash flow.

After experiencing their own crisis with debtors in a previous business, they took a look at how large businesses protected themselves. What they learned was that they should have had a signed agreement in place outlining their Terms and Conditions in the first instance which would have been extremely effective in avoiding bad debts.

Working in debtor management and debt collection further convinced Larry and Geraldine that every business, no matter how small, should focus on protecting themselves at the front end to avoid costly problems further down the track.

Ledger Guard is a licensed debt collection agency and a member of the Institute of Mercantile Agents.

28

www.ledgerguard.com.au