Embed Size (px)

DESCRIPTION

B121. Chapter 12 Finance. Accounting concepts & principles. Financial statements are prepared at the end of a period. - PowerPoint PPT Presentation

Citation preview

B121

Chapter 12

Finance

Accounting concepts & principles

Financial statements are prepared at the end of a period.

The form and content of such financial statements are often regulated by statute or regulations produced by accounting bodies(e.g. the International Accounting Standards Board).

There is often general requirement that these statement should give a true and fair view of the affairs of the organization.

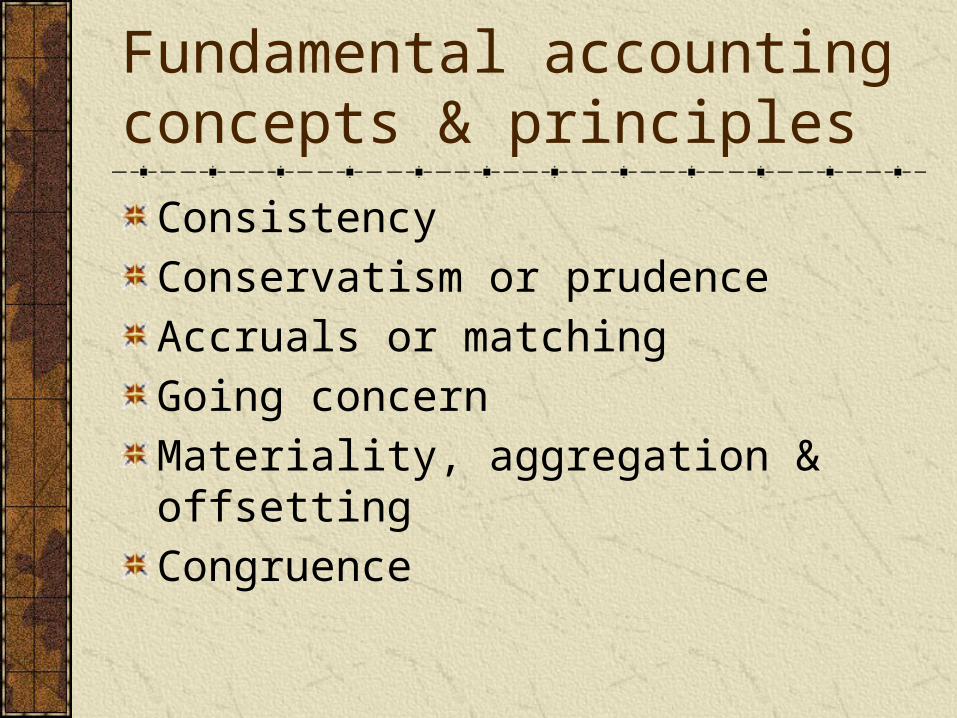

Fundamental accounting concepts & principles

Consistency

Conservatism or prudence

Accruals or matching

Going concern

Materiality, aggregation & offsetting

Congruence

Profit or not-for-profit

Organizations are often differentiated in terms of the sector of the economy to which they belong: pubic or private. They also are classified according to whether or not their primary motive is profit.

Assets & liabilities

Assets - it is something which the organization owns and which has a market value.

Liability – it is a debt that the organization owes to another person or organization.

Net worth – it is the value of the assets less the value of the liabilities as recorded in the books of accounts.

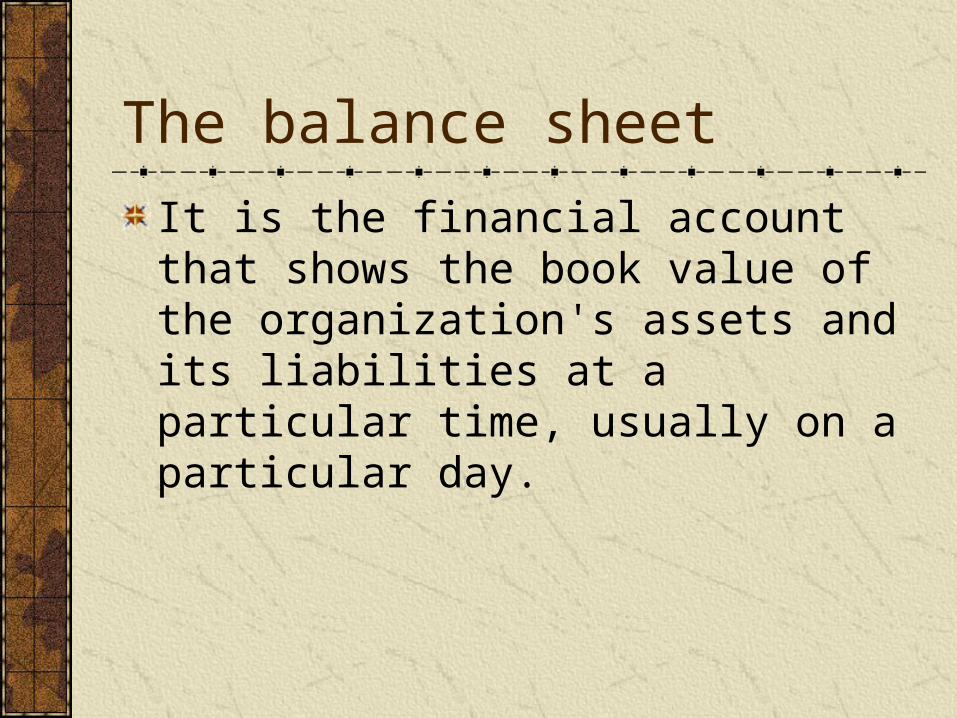

The balance sheet

It is the financial account that shows the book value of the organization's assets and its liabilities at a particular time, usually on a particular day.

Profit statement

It shows the income that the organization has earned from its activities during a particular period and the expenditures it has incurred.

Operating profit – is the difference between the income – the earning – from sales, and the direct cost of those sales.

Cash account

It shows the cash that the organization has received and the cash the organization has paid.

Flow of cash

The stock of cash

Managing the flows

Budgeting A budget is a published forecast of how an organization's resources are to be used in the best possible way to achieve its objectives.

Benefits of budgeting

Provides a framework for planning.

Aids the coordination of activities.

Provides the basis for monitoring progress and control.

Helps managers to justify their use of resources.

Provides a steady pressure to improve performance.

Facilitates control

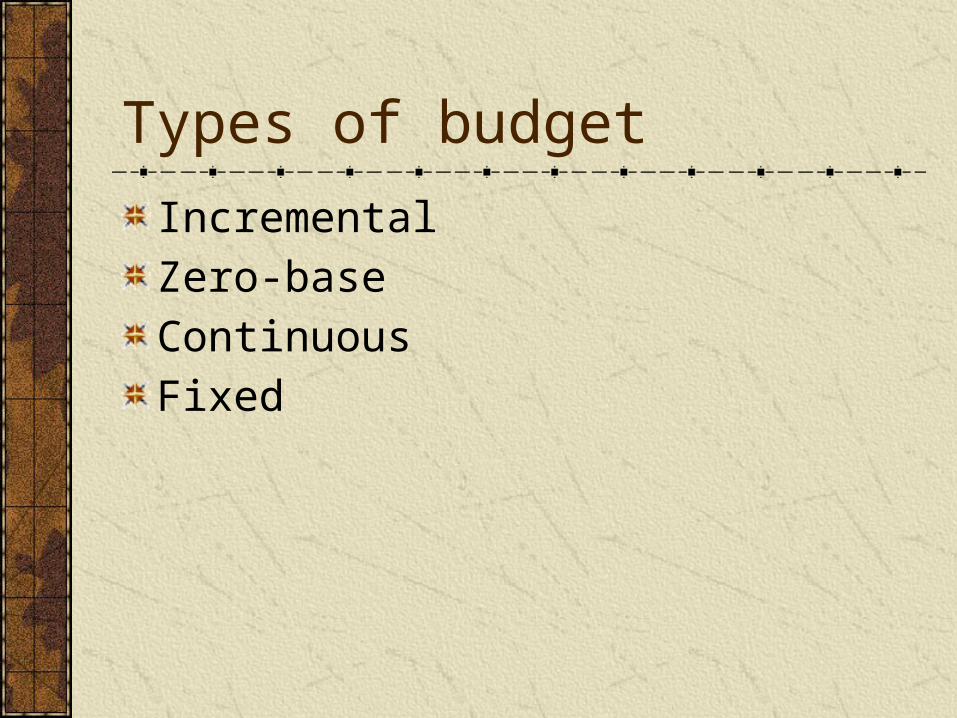

Types of budget

Incremental

Zero-base

Continuous

Fixed

Working capital

It is used to describe how the day-to-day activities of an organization are funded.

It comprises current assets minus current liabilities.

The organization must ensure it has adequate cash to pay its creditors when required.

Depreciation

It is the term used to describe the process of charging, over time, the cost of a long-life asset to a profit or income and expenditure statement.

Methods of depreciation

Cost could be charged in equal amounts each year.

Reducing balance.

Different types of costs

Fixed costs

Variable costs

Direct costs

Indirect costs

Break-even

Break-even (or break even) is the point of balance between making either a profit or a loss.

The accounting method of calculating break-even point does not include cost of working capital.

The financial method of calculating break-even, called value added break-even analysis, is used to assess the feasibility of a project. This method not only accounts for all costs, it also includes the opportunity costs of the capital required to develop a project.

The margin of safety

In Break even analysis (accounting), margin of safety is how much output or sales level can fall before a business reaches its breakeven point.

Margin of Safety = Actual Sales - Breakeven Sales

Marginal analysis

Marginal cost and marginal revenue

The equilibrium of output

Ratio analysis

A tool used by individuals to conduct a quantitative analysis of information in a company's financial statements. Ratios are calculated from current year numbers and are then compared to previous years, other companies, the industry, or even the economy to judge the performance of the company. Ratio analysis is predominately used by proponents of fundamental analysis.

Return on capital employed

ROCE = operating profit / capital employed

(Expressed as a %)

ROCE is used to prove the value the business gains from its assets and liabilities. A business which owns lots of land but has little profit will have a smaller ROCE to a business which owns little land but makes the same profit.

It basically can be used to show how much a business is gaining for its assets, or how much it is losing for its liabilities.

Asset utilization ratio

The asset utilization ratio is calculated by dividing total sales by the net book value of the capital assets. AUR = value of sale/capital employed

The asset utilization ratio measures management's ability to make the best use of its assets to generate revenue. The more effectively that the equipment is used, the more profitable the company will be. Rather than acquiring additional equipment and incurring additional production costs, make better use of existing capacity.

Return on sales

Return on sales = operating profit / value of sales

ROS indicates how much profit an entity makes after paying for variable costs of production such as wages, raw materials, etc. (but before interest and tax). It is the return achieved from standard operations and does not include unique or one off transactions. ROS is usually expressed as a percentage of sales (revenue).

Margins & mark-ups

Margins – it describes the profit earned as a percentage of the sales value.

Mark-up – it describes the amount added on to cost to arrive at the selling price as a percentage of cost.