Embed Size (px)

Citation preview

B P W E A L T H

Wipro

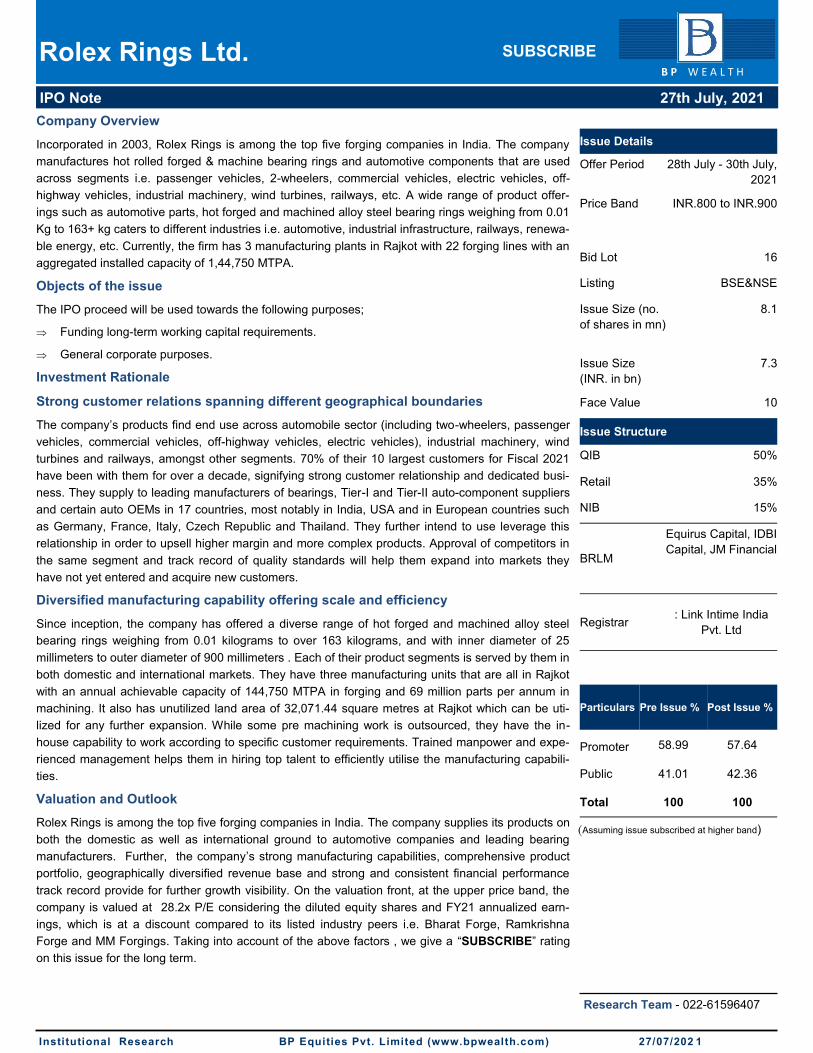

Issue Details

Offer Period 28th July - 30th July,

2021

Price Band INR.800 to INR.900

Bid Lot 16

Listing BSE&NSE

Issue Size (no.

of shares in mn)

8.1

Issue Size

(INR. in bn)

7.3

Face Value 10

Issue Structure

QIB 50%

Retail 35%

NIB 15%

BRLM

Equirus Capital, IDBI

Capital, JM Financial

Registrar : Link Intime India

Pvt. Ltd

Company Overview

Incorporated in 2003, Rolex Rings is among the top five forging companies in India. The company

manufactures hot rolled forged & machine bearing rings and automotive components that are used

across segments i.e. passenger vehicles, 2-wheelers, commercial vehicles, electric vehicles, off-

highway vehicles, industrial machinery, wind turbines, railways, etc. A wide range of product offer-

ings such as automotive parts, hot forged and machined alloy steel bearing rings weighing from 0.01

Kg to 163+ kg caters to different industries i.e. automotive, industrial infrastructure, railways, renewa-

ble energy, etc. Currently, the firm has 3 manufacturing plants in Rajkot with 22 forging lines with an

aggregated installed capacity of 1,44,750 MTPA.

Objects of the issue

The IPO proceed will be used towards the following purposes;

Funding long-term working capital requirements.

General corporate purposes.

Investment Rationale

Strong customer relations spanning different geographical boundaries

The company’s products find end use across automobile sector (including two-wheelers, passenger

vehicles, commercial vehicles, off-highway vehicles, electric vehicles), industrial machinery, wind

turbines and railways, amongst other segments. 70% of their 10 largest customers for Fiscal 2021

have been with them for over a decade, signifying strong customer relationship and dedicated busi-

ness. They supply to leading manufacturers of bearings, Tier-I and Tier-II auto-component suppliers

and certain auto OEMs in 17 countries, most notably in India, USA and in European countries such

as Germany, France, Italy, Czech Republic and Thailand. They further intend to use leverage this

relationship in order to upsell higher margin and more complex products. Approval of competitors in

the same segment and track record of quality standards will help them expand into markets they

have not yet entered and acquire new customers.

Diversified manufacturing capability offering scale and efficiency

Since inception, the company has offered a diverse range of hot forged and machined alloy steel

bearing rings weighing from 0.01 kilograms to over 163 kilograms, and with inner diameter of 25

millimeters to outer diameter of 900 millimeters . Each of their product segments is served by them in

both domestic and international markets. They have three manufacturing units that are all in Rajkot

with an annual achievable capacity of 144,750 MTPA in forging and 69 million parts per annum in

machining. It also has unutilized land area of 32,071.44 square metres at Rajkot which can be uti-

lized for any further expansion. While some pre machining work is outsourced, they have the in-

house capability to work according to specific customer requirements. Trained manpower and expe-

rienced management helps them in hiring top talent to efficiently utilise the manufacturing capabili-

ties.

Valuation and Outlook

Rolex Rings is among the top five forging companies in India. The company supplies its products on

both the domestic as well as international ground to automotive companies and leading bearing

manufacturers. Further, the company’s strong manufacturing capabilities, comprehensive product

portfolio, geographically diversified revenue base and strong and consistent financial performance

track record provide for further growth visibility. On the valuation front, at the upper price band, the

company is valued at 28.2x P/E considering the diluted equity shares and FY21 annualized earn-

ings, which is at a discount compared to its listed industry peers i.e. Bharat Forge, Ramkrishna

Forge and MM Forgings. Taking into account of the above factors , we give a “SUBSCRIBE” rating

on this issue for the long term.

IPO Note 27th July, 2021

Rolex Rings Ltd. B P W E A L T H

Particulars Pre Issue % Post Issue %

Promoter 58.99 57.64

Public 41.01 42.36

Total 100 100

(Assuming issue subscribed at higher band)

Research Team - 022-61596407

SUBSCRIBE

Institutional Research BP Equities Pvt. Limited (www.bpwealth.com) 27/07/202 1

Rolex Rings Ltd. IPO Note

Institutional Research BP Equities Pvt. Limited (www.bpwealth.com) 27/07/202 1 2

B P W E A L T H

Source: RHP, BP Equities Research

Income Statement (In mn)

Cash Flow Statement (In mn)

Particulars FY19 FY20 FY21

Revenue

Revenue From Operations 6,163 6,660 9,043

Total Revenue 6,163 6,660 9,043

Expenses

Raw Material Consumed 3,166 3,137 4,529

Changes in Inventories of Finished Goods and Work-In-Progress

(292) 156 (190)

Employee Benefit Expenses 519 527 608

Other Expenses 1,682 1,626 2,085

Total Operating Expenses 5,075 5,446 7,032

EBITDA 1,088 1,214 2,011

Depreciation and Amortisation Expense 254 265 254

Other Income 34 93 69

EBIT 868 1,042 1,825

Finance Costs 117 322 420

Exceptional Item - - -

Share in Profit/(Loss) of Joint Ventures - - -

PBT 751 721 1,405

Current Tax 130 127 309

Deferred Tax Charge (248) 64 506

Total Tax (118) 191 815

PAT 869 529 590

Diluted EPS 31.9 19.4 21.6

Particulars FY19 FY20 FY21

Cash flow from operating activities 592 1,838 1,938

Cash flow from investing activities (363) (142) (363)

Cash flow from financing activities (195) (1,685) (1,580)

Net increase/(decrease) in cash and cash equivalents 34 11 (6)

Cash and cash equivalents at the beginning of the period 12 1 7

Cash and cash equivalents at the end of the period 46 12 1

Source: RHP, BP Equities Research

Rolex Rings Ltd. IPO Note

Institutional Research BP Equities Pvt. Limited (www.bpwealth.com) 27/07/202 1 3

B P W E A L T H

Key Risks

The company has defaulted in payment of certain loans in the past, and have undergone CDR.

The company is heavily dependent on the performance of the automotive sector in India, Europe, North America, Latin America and

some part of Asia. Any adverse changes in the conditions affecting these markets can adversely impact our business, results of oper-

ations, cash flows and financial condition

The continuing impact of the outbreak of the COVID-19 could have a significant effect their operations, and could negatively impact

their business, revenues, financial condition, cash flows and results of operations.

Balance Sheet (In mn)

Source: RHP, BP Equities Research

Particulars FY19 FY20 FY21

Liabilities

Share Capital 240 240 240

Other Equity 1,914 2,441 3,328

Net Worth 2,154 2,681 3,568

Long Term Borrowings 913 442 323

Deferred Tax Liabilities - - -

Long-Term Provisions 23 31 31

Other Non Current Liabilities 678 750 504

Total Non Current Liabilities 1,614 1,223 858

Trade Payables 913 739 1,176

Current Tax Liability 107 3 75

Borrowings 2,343 1,939 1,836

Other Financial Liabilities 671 261 434

Lease Liabilities

Other Current Liabilities 13 8 15

Short Term Provisions 7 7 7

Total Current Liabilities 4,054 2,957 3,544

Total Equity & Liabilities 7,823 6,862 7,970

Assets

Property, Plant & Equipment 3,808 3,730 3,714

Capital Work in Progress 10 - 12

Right Use Of Assets 1 1 1

Other Intangible Assets 14 12 9

Capital Work In Progress 10 - 12

Financial Assets 158 59 140

Other Tax Assets 20 20 20

Deferred Tax Assets (net)

Other Non-Current Assets 131 111 288

Total Non current assets 4,142 3,933 4,183

Investment 1.23 31 1

Trade Receivables 1,815 1,277 1,708

Cash and Cash Equivalents 1 13 47

Other Current Assets 114 92 194

Bank Balances 45 151 58

Other Financial Assets 102 59 68

Inventories 1,602 1,306 1,711

Total Current Asset 3,680 2,929 3,787

Net Current Assets (374) (28) 243

Total Assets 7,823 6,862 7,970

Research Desk Tel: +91 22 61596406

Disclaimer Appendix

Institutional Sales Desk Tel: +91 22 61596403/04/05

Analyst (s) holding in the Stock : Nil

Analyst (s) Certification:

We analysts and the authors of this report, hereby certify that all of the views expressed in this research report accurately reflect our

personal views about any and all of the subject issuer (s) or securities. We also certify that no part of our compensation was, is, or will

be directly or indirectly related to the specific recommendation (s) or view (s) in this report. Analysts aren't registered as research ana-

lysts by FINRA and might not be an associated person of the BP Equities Pvt. Ltd. (Institutional Equities).

General Disclaimer

This report has been prepared by the research department of BP EQUITIES Pvt. Ltd, is for information purposes only. This report is not

construed as an offer to sell or the solicitation of an offer to buy or sell any security in any jurisdiction where such an offer or solicitation

would be illegal.

BP EQUITIES Pvt. Ltd have exercised due diligence in checking the correctness and authenticity of the information contained herein, so

far as it relates to current and historical information, but do not guarantee its accuracy or completeness. The opinions expressed are our

current opinions as of the date appearing in the material and may be subject to change from time to time. Prospective investors are cau-

tioned that any forward looking statement are not predictions and are subject to change without prior notice.

Recipients of this material should rely on their own investigations and take their own professional advice. BP EQUITIES Pvt. Ltd or any

of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvert-

ent error in the information contained in this report. BP EQUITIES Pvt. Ltd. or any of its affiliates or employees do not provide, at any

time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied

warranties of merchantability, fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own

investigations.

BP EQUITIES Pvt. Ltd and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities men-

tioned in this report. Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to

update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that pre-

vent us from doing so.

This report is not directed to or intended for display, downloading, printing, reproducing or for distribution to or use by any person in any

locality, state and country or other jurisdiction where such distribution, publication or use would be contrary to the law or regulation or

would subject to BP EQUITIES Pvt. Ltd or any of its affiliates to any registration or licensing requirement within such jurisdiction.

B P W E A L T H

Corporate Office:

4th floor,

Rustom Bldg,

29, Veer Nariman Road, Fort,

Mumbai-400001

Phone- +91 22 6159 6464

Fax-+91 22 6159 6160

Website- www.bpwealth.com

Registered Office:

24/26, 1st Floor, Cama Building,

Dalal street, Fort,

Mumbai-400001

BP Wealth Management Pvt. Ltd.

CIN No: U67190MH2005PTC154591

BP Equities Pvt. Ltd.

CIN No: U67120MH1997PTC107392