Embed Size (px)

Citation preview

February 19, 2015

British Columbia Utilities Commission Sixth Floor 900 Howe Street Vancouver, BC V6Z 2N3

building trust. driving confidence.

Attention: Ms. Erica Hamilton, Commission Secretary and Director

Re: ICBC's 2014 Revenue Requirements Application - ICBC's Rebuttal Evidence

Dear Ms. Hamilton:

Pursuant to Commission Order G-155-14, please find attached ICBC's Rebuttal Evidence. This filing contains the follo"".ing:

• Part A, ICBC's Rebuttal Evidence in respect of the evidence of the Canadian Office and Professional Employees Union, Local 378 (Exhibits C3-8, C3-9, and C3-10).

• Part B, ICBC's Rebuttal Evidence in respect of the evidence of Mr. Richard Landale (Exhibits C1-8 and C1-9).

Yours truly,

June Elder Manager, Corporate Regulatory Affairs

Cc: Registered Intervenors Geri Prior, B.Comm, FCA, Chief Financial Officer, ICBC Steve Yendall, Vice President, Insurance and Driver Licensing, ICBC

Attachments

151 West Esplanade I North Vancouver I British Columbia I V7M 3H9 I 604-661-2800 I [email protected]

B-17

PART A

ICBC’S REBUTTAL EVIDENCE IN RESPECT OF EVIDENCE

OF THE CANADIAN OFFICE AND PROFESSIONAL EMPLOYEES UNION, LOCAL 378 (COPE)

Insurance Corporation of British Columbia Rebuttal Evidence February 19, 2015

IN THE MATTER OF

THE UTILITIES COMMISSION ACT

R.S.B.C. 1996, Chapter 473, as amended and the

INSURANCE CORPORATION ACT R.S.B.C. 1996, Chapter 228, as amended

and

AN APPLICATION BY THE INSURANCE CORPORATION OF BRITISH COLUMBIA (“ICBC”) FOR APPROVAL OF

THE REVENUE REQUIREMENTS FOR UNIVERSAL COMPULSORY AUTOMOBILE INSURANCE EFFECTIVE NOVEMBER 1, 2014

REBUTTAL EVIDENCE OF ICBC TO COPE

1. This Rebuttal Evidence responds to the ICBC Call Center Workforce Review Report (the

Report), prepared by Ms. Penny Reynolds and filed on behalf of COPE (Exhibits C3-8, C3-9,

and C3-10).

2. ICBC focuses on the most significant topics of contention regarding the Report; ICBC’s

silence on other topics should not be interpreted as concurrence.

New Claims Initiation (Service Level)

3. The Report assumes that ICBC’s target is 80% of calls answered within 100 seconds

(the Report refers to this as “service level”). For example, pages 11 and 37 of the Report

both state, “While the stated goal of ICBC is to answer 80% of calls in 100 seconds, service

levels declined and remained well below the 80% mark throughout the period in question

from early 2013 to the end of the study period in late 2014.”

4. Much of Ms. Reynolds’ analysis and many of her conclusions are based on this

erroneous assumption. A few examples of this are provided below.

• “The base staff requirement (commonly referred to as “bodies in chairs”) was calculated based on ICBC’s stated speed-of-answer goal of 80% of calls answered in 100 seconds.” (page 26)

Insurance Corporation of British Columbia A-1 Rebuttal Evidence February 19, 2015

• “This analysis provides calculations of appropriate staffing levels for the center based on … ICBC’s established service goals for policyholders ….” (page 23)

• “ICBC met the service level goal in only half the intervals in 2012, and the successive years of 2013 and 2014 got progressively worse.” (page 39)

• “… it is recommended that ICBC … move to immediately staff up to fill the current personnel gaps in order to accomplish stated service goals from a customer perspective and reasonable occupancy goals from an employee view.” (page 50)

ICBC’s response

5. Ms. Reynolds’ analysis is incorrect in its assumption that ICBC’s target is 80% of calls

answered within 100 seconds and therefore many of her conclusions are invalid.

6. Consistent with the Decision on 2013 Revenue Requirements (Order G-63-14), ICBC

no longer reports on the New Claims Initiation1 measure for calls answered within 120 seconds

and 210 seconds, but continues to report on the New Claims Initiation measure for calls

answered within 100 seconds. However, ICBC no longer manages to meet 80% of calls

answered within 100 seconds. Beginning in 2013, steps taken to enhance claims handling

have had some adverse impact on the New Claims Initiation performance measure, but

improve the customer experience and First Call Resolution. Although fewer calls were handled

within 100 seconds in 2013, ICBC’s Claims Services Satisfaction and First Call Resolution

scores remained high. Please also see the responses to information requests 2014.1 RR

BCUC.78.3, 2014.1 RR COPE 6.1-4, and 2014.2 RR COPE.34.5 in this regard.

7. As discussed below, while ICBC is focused primarily on First Call Resolution and does

not staff to ensure that operational metrics are met at all times, ICBC does still track the New

Claims Initiation statistic internally. ICBC’s bodily injury claims calls have generally achieved

the 80% of calls answered in 100 seconds measure, but this is as a consequence of initiatives

primarily designed to improve claims handling at first notice of loss (FNOL).

1 Any instances where ICBC has inadvertently referred in information request responses to “First Call Initiation” should be read as “New Claims Initiation”.

Insurance Corporation of British Columbia A-2 Rebuttal Evidence February 19, 2015

Call Centre Operational Metrics

8. Ms. Reynolds uses data from ICBC’s responses to information requests to provide

additional detail on the operational call centre metrics used in day to day call centre

management. For example, there is considerable discussion about:

• Average handle time, with Ms. Reynolds’ point being: “…call handle times have increased substantially over time. While there have been some decreases in the AHT in recent months, the numbers are still well above 2012 levels and remain above 2013 levels as well.” (page 6 and page 33)

• Call workload, with Ms. Reynolds’ point being: “The Claims Hierarchy project rolled out in April 2013 and there is a corresponding significant jump in workload beginning in May 2013. The next sizable jump in workload occurs November 2013 with the rollout of ClaimCenter. While an increase in calls does occur steadily over time, the major change in workload is due to the increased time required to handle calls.” (page 7 and page 34)

• Call abandons and call abandon rates, with Ms. Reynolds’ point being: “…call volumes have steadily increased over time, and two projects (Claims Hierarchy and ClaimCenter) undertaken in the recent past have caused handle times to increase substantially. These increases in both call volume and call handle times have added a substantial workload burden for the center. However, the management team has elected not to increase by enough staff to correspond to the increased workload.” (page 23)

ICBC’s response

9. ICBC confirms that changes associated with Claims Transformation caused a

temporary deterioration in the Claims Contact Centre operational metrics. While Ms. Reynolds

has graphed the data in a slightly different manner, ICBC had provided similar information in

its information request responses. In the responses to information requests 2014.1 RR

BCUC.50.1-4 and 2014.2 RR BCUC.115.1, ICBC provided graphs which, similar to the graphs

in the Report, show the temporary increases in average handle time, average speed of

answer, and abandon rates related to the rollout of ClaimCenter in Phase 1 (November 2013),

Phase 2 (February 2014), and Phase 3 (late April 2014). The key point, however, is that the

impacts were expected, as was the current trend towards recovery that is evident in both

ICBC’s and Ms. Reynolds’ graphs.

10. In information requests on the Report, COPE was asked for their view on the drop in

call abandonment numbers from July 2014 to October 2014. COPE states that trunk lines

were added in July and speculates that staff returning from holidays was a major contributor

Insurance Corporation of British Columbia A-3 Rebuttal Evidence February 19, 2015

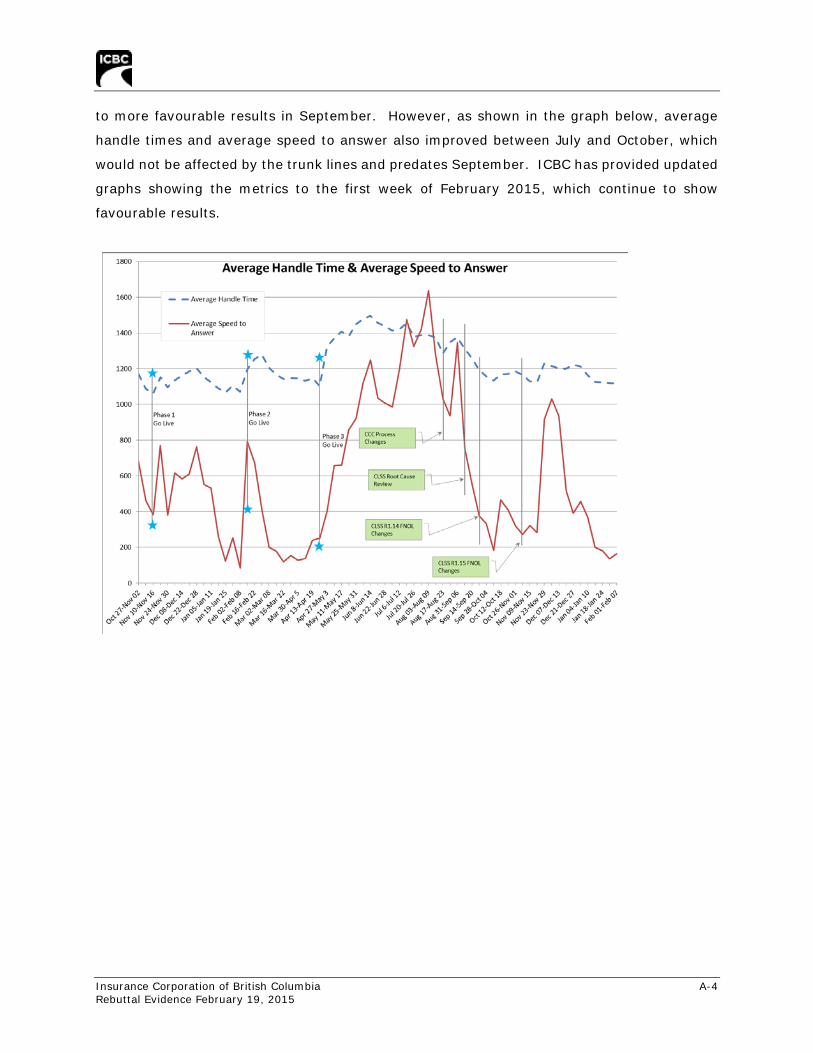

to more favourable results in September. However, as shown in the graph below, average

handle times and average speed to answer also improved between July and October, which

would not be affected by the trunk lines and predates September. ICBC has provided updated

graphs showing the metrics to the first week of February 2015, which continue to show

favourable results.

Insurance Corporation of British Columbia A-4 Rebuttal Evidence February 19, 2015

11. Similarly, COPE was asked about their evidence showing a decline in deflected calls,

but an increase in November 2014. COPE speculates this is call volume seasonality and that

there were not enough trunks available. While seasonality can affect the volume of calls at

the Claims Contact Centre, there are other factors including specific weather, and it may not

be possible to correctly anticipate and staff for every winter storm. In the response to

information request 2014.2 RR BCUC.115.1 ICBC notes increases in average handle times

and average speed to answer coincided with significant winter weather in many areas of the

province.

12. Given the magnitude of systems and business process changes, ICBC had anticipated

a 12 to 18 month period of stabilization after full implementation of ClaimCenter, in which

adjusters would become fully proficient in handling claims and during which efficiencies and

systems fixes would be identified. ICBC management had advised COPE to expect transitional

impacts and in 2012 COPE signed a Memorandum of Understanding (MOU) with ICBC (Exhibit

B-10) acknowledging the stabilization period. The MOU includes the statement that, “Within

24 months of system implementation across the Corporation, the Corporation will commence

a workload benchmarking study for job profiles that have been altered / created by the Claims

Job Hierarchy …”

Insurance Corporation of British Columbia A-5 Rebuttal Evidence February 19, 2015

13. While the Report acknowledges that there has been an improvement in the Claims

Contact Centre operational metrics, it says, “… the numbers are still well above 2012 levels

and remain above 2013 levels as well.” This fact should not be surprising nor should it be

construed as problematic. As referred to above, changes were introduced in April 2013 to

improve the claims experience through better First Call Resolution at FNOL. For injury claims,

addressing all of the immediate needs of the injured party at FNOL includes a more

comprehensive discussion of their entitlements and provides pre-approved access to

treatment. These changes adversely affect the New Claims Initiation performance measure

reported in the Application, Chapter 10, but improve the customer experience. Even though,

overall, fewer calls were handled within 100 seconds in 2013, the customer satisfaction and

experience score remains high.

14. As mentioned above, ICBC does not operate the Claims Contact Centre so as to ensure

operational metrics like New Claims Initiation are met at all times, above all other

considerations, and for all types of claims handled by the Claims Contact Centre. However,

ICBC still tracks and refers to operational metrics. While ICBC no longer has a New Claims

Initiation target of 80% of all calls answered in 100 seconds, it is a useful operational metric

regarding wait time and ICBC continues to track this metric. The 2013 improvements to the

FNOL process discussed above were intended to improve claims handling and included a

dedicated line for bodily injury claims. The results in the graph below show that ICBC’s

average speed of answer on the dedicated bodily injury claims has been at least 80% of calls

answered in 100 seconds in all months except June 2013 when the figure dipped to 73%. In

its responses to the Commission’s information requests, COPE has incorrectly tried to link the

acceleration in the Legal Representation Rate to the New Claims Initiation performance

measure for all types of claims. Since the Legal Representation Rate pertains to bodily injury

claims, COPE’s assertion that longer wait times for bodily injury claimants has led to increased

legal representation is without merit.

Insurance Corporation of British Columbia A-6 Rebuttal Evidence February 19, 2015

15. ICBC’s progress during the transition period continues to track the same typical

“Change Curve” of a large scale claims transformation that was discussed by Accenture in the

response to information request 2014.2 RR COPE.32.3.3-4.

16. In spite of the observation that there has been improvement in the Claims Contact

Centre operational metrics and the existing agreement between ICBC and COPE regarding

the timing of a workload study, Ms. Reynolds still concludes that more staffing is required.

This conclusion is again based on the incorrect assumption that ICBC has a New Claims

Initiation performance measure target of 80% of all calls answered within 100 seconds.

Moreover, even if ICBC were to establish this as a target for all claims, increasing staffing is

not the only way to meet it. For example, ICBC is seeing a significant improvement in average

speed to answer and average handle times in response to enhancements to systems and

processes, and tools and training. While COPE says in its responses to Commission

information requests that, “ICBC should analyze the call handling process to determine if

there are opportunities to reduce AHT”, ICBC has already done so and there has been, as

anticipated, a substantial improvement in average handle time and average speed of answer

in recent months. ICBC believes that it has struck the right balance in terms of staffing.

17. In its Decision on 2013 Revenue Requirements, the Commission recognized the

amount of change being undertaken, and that transformation entails some adverse impact,

Insurance Corporation of British Columbia A-7 Rebuttal Evidence February 19, 2015

stating, “… ICBC is undergoing significant organizational changes especially in the claims area.

The Panel understands that any time change occurs within an organization, especially a major

shift in how a particular area operates, the transitional period can have a consequential impact

on costs, as well as productivity and performance impacts.” The 12 to 18 month estimated

transition period for Claims Transformation, which is typical for changes of this scope, ends

in mid to late 2015. This means the vast majority of Claims Transformation impacts will have

ended before or within a few months of ICBC filing the 2015 Revenue Requirements

Application. The Decision on 2013 Revenue Requirements noted that ICBC will propose

changes to the overall suite of performance measures, after Claims Transformation, as part

of its 2017 Revenue Requirements Application. This remains ICBC’s intention.

18. ICBC will also continue to monitor the call centre metrics as indicators of call centre

proficiency because they provide useful information about internal management of the call

centre. However, customer feedback indicates that the quality of the call is more of a

contributing factor to customer satisfaction than service level (wait time) and the First Call

Resolution call quality measure is now the leading call centre driver in measuring customer

satisfaction. Please see the responses to information requests 2014.1 RR BCUC.47.3 and

2014.1 RR COPE.6.1-4 for further information.

Selection of Data in Evidence

19. Notwithstanding concerns that COPE’s representatives raised in Matters of Interest

(Exhibit C3-2) regarding the selection of data, Ms. Reynolds’ evidence considers and

comments on only parts of the data.

• Page 15 of the Report says Mondays are busy days, but much of the analysis in

the report pertains to a one half-hour time period from Monday, October 27, 2014.

• Page 20 of the Report focuses on corporate employee engagement scores and

postulates that the workload in the Claims Contact Centre is “likely a significant

factor in the decline”.

• Page 39 of the Report includes statistics from the Society of Workforce Planning

Professionals regarding a 2009 self-reporting survey on speed of answer goals.

• Pages 19 and 46 of the Report mention, but Ms. Reynolds does not appear to

include in her analysis, the “stretch breaks” provided for as part of the Collective

Agreement.

Insurance Corporation of British Columbia A-8 Rebuttal Evidence February 19, 2015

ICBC’s response

20. Although Ms. Reynolds acknowledges that results vary from day to day, she selects

from what she describes as “… busy days like Mondays …” for her analysis. She then focuses

on only one half-hour period from that day; i.e., October 27, 2014 at 10:30 a.m., and does

not discuss how results vary within each day. The data in ICBC’s response to information

request 2014.2 COPE.35.2, Attachment A – CCC CSA Call Statistics All Monday Intervals 2013

January to 2014 November, show that, except for overnight periods with a zero service level,

COPE selected the period with the lowest service level and highest number of abandoned calls

for that day. Had COPE selected the next time period; i.e., October 27, 2014 at 11:00 a.m.,

the service level would have been 33% with 7 abandoned calls; or, had they selected the

2:00 p.m. time period on the same day, the service level would have been 100% with no

abandoned calls. Given the very small snapshot of data used, a 30 minute time period is not

valid for generalizing to other time periods.

21. Ms. Reynolds’ discussion on employee engagement also only tells part of the story.

She attempts to draw a link between corporate engagement scores and what Ms. Reynolds

perceives as understaffing in the Claims Contact Centre. The Claims Contact Centre is part

of the Claims Division. As shown on page 47 of the Report, there was a 7 percentage point

improvement in the employee engagement score for Claims Division in 2013 in comparison

to 2012. In other words, while low, Claims Division employee engagement showed some

improvement during a period when one might have expected it to decline.

22. In making her argument regarding service levels, Ms. Reynolds cites information from

the Society of Workforce Planning Professionals. Leaving aside for the moment that ICBC

does not have a New Claims Initiation (service level) target of 80% of calls answered within

100 seconds, the information Ms. Reynolds cites is from a 2009 self-reporting survey which

does not focus on organizations that are implementing significant systems and business

process changes.

23. Notwithstanding Ms. Reynolds’ comments, based on occupancy levels, about a

“breather” in between calls, her critique does not align with the current Collective Agreement.

The Collective Agreement provides for either a rest break or stretch break in every hour.

Please see ICBC’s response to information request 2014.1 RR COPE.10.15.a-b for more

information on stretch breaks and the guidelines.

Insurance Corporation of British Columbia A-9 Rebuttal Evidence February 19, 2015

Customer Satisfaction

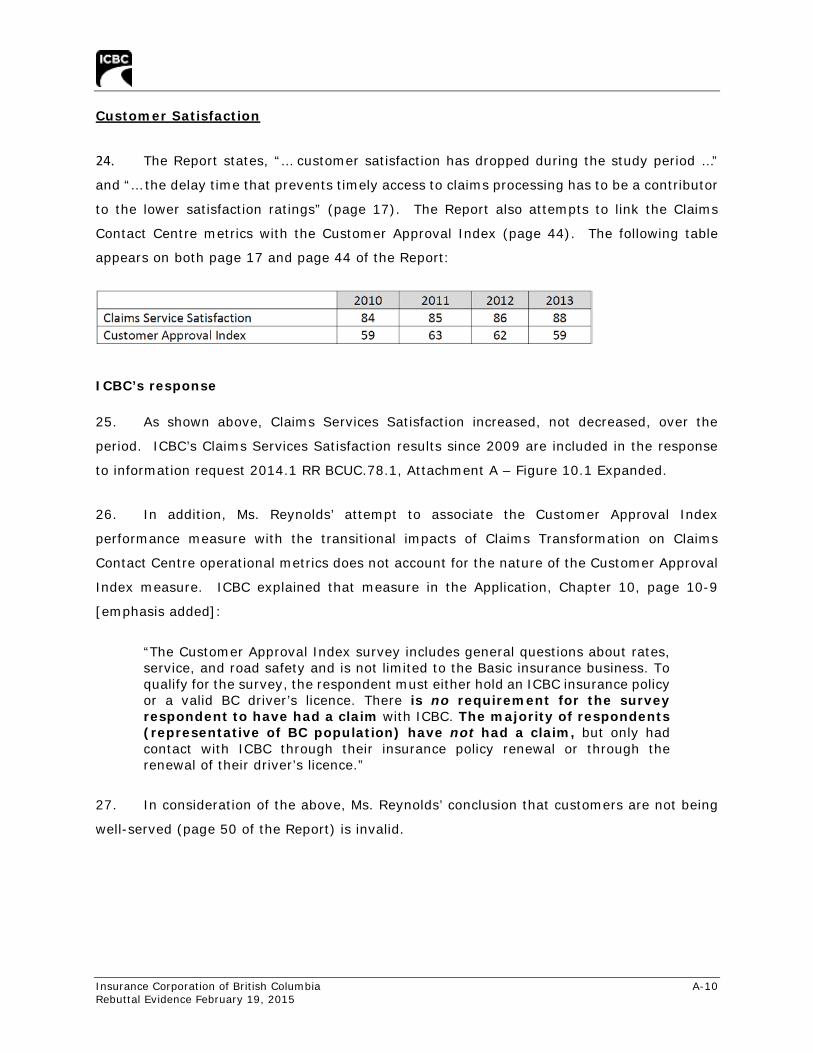

24. The Report states, “… customer satisfaction has dropped during the study period …”

and “… the delay time that prevents timely access to claims processing has to be a contributor

to the lower satisfaction ratings” (page 17). The Report also attempts to link the Claims

Contact Centre metrics with the Customer Approval Index (page 44). The following table

appears on both page 17 and page 44 of the Report:

ICBC’s response

25. As shown above, Claims Services Satisfaction increased, not decreased, over the

period. ICBC’s Claims Services Satisfaction results since 2009 are included in the response

to information request 2014.1 RR BCUC.78.1, Attachment A – Figure 10.1 Expanded.

26. In addition, Ms. Reynolds’ attempt to associate the Customer Approval Index

performance measure with the transitional impacts of Claims Transformation on Claims

Contact Centre operational metrics does not account for the nature of the Customer Approval

Index measure. ICBC explained that measure in the Application, Chapter 10, page 10-9

[emphasis added]:

“The Customer Approval Index survey includes general questions about rates, service, and road safety and is not limited to the Basic insurance business. To qualify for the survey, the respondent must either hold an ICBC insurance policy or a valid BC driver’s licence. There is no requirement for the survey respondent to have had a claim with ICBC. The majority of respondents (representative of BC population) have not had a claim, but only had contact with ICBC through their insurance policy renewal or through the renewal of their driver’s licence.”

27. In consideration of the above, Ms. Reynolds’ conclusion that customers are not being

well-served (page 50 of the Report) is invalid.

Insurance Corporation of British Columbia A-10 Rebuttal Evidence February 19, 2015

First Call Resolution/SQM Group Statistics

28. Ms. Reynolds seems to question the First Call Resolution data.

• “… it is unclear from the data provided here whether ICBC’s actual FCR results are as stellar as noted. The results reported are good, but only represent about one percent of customers’ perspectives. And more importantly, even if the results are excellent and customers are happy with call resolution, it does not mean that it is acceptable to ignore the speed of answer.” (page 20)

• “While it is good that ICBC measures FCR and views this as a primary driver of customer satisfaction, it should be noted that there is actually only a very small percent of customers who are providing feedback related to call resolution. First, it is unclear how a decision is made about which customers to survey in the first place. But the primary problem is the percent of customers actually represented by this FCR survey data. Only about one percent of callers are providing feedback about their view of FCR.” (page 43)

ICBC’s response

29. Ms. Reynolds seems to imply that there may be an issue with the First Call Resolution

surveys; however, there seems to be some confusion between response rate and sample size

in both the Report and in COPE’s responses to information requests. ICBC has already

provided evidence on the high degree of statistical accuracy of the survey (please see the

response to information request 2014.1 RR COPE.8.8).

30. ICBC referred this issue to SQM Group since the matter pertains to sampling methods.

SQM Group provided the following information in overview of the rigour and science behind

their sampling methods.

SQM uses a standard 95% confidence interval when calculating the margin of error of the survey results. A 95% confidence interval means that if the sampling was repeated, then 19 times out of 20, the true proportion for the population of ICBC customers would be in the interval surrounding the sample proportion. SQM assumes an infinite customer base for calculating the margin of error, and as such the true margin of error will be lower based on the size of the population that is being measured. For ICBC, SQM uses a stratified random sampling approach to ensure that we survey for all adjusters who take calls. Each call record we receive from ICBC is stratified by adjuster and then records are randomly selected for each adjuster. This makes sure that the sample is representative of the service that ICBC provides to its customers. By

Insurance Corporation of British Columbia A-11 Rebuttal Evidence February 19, 2015

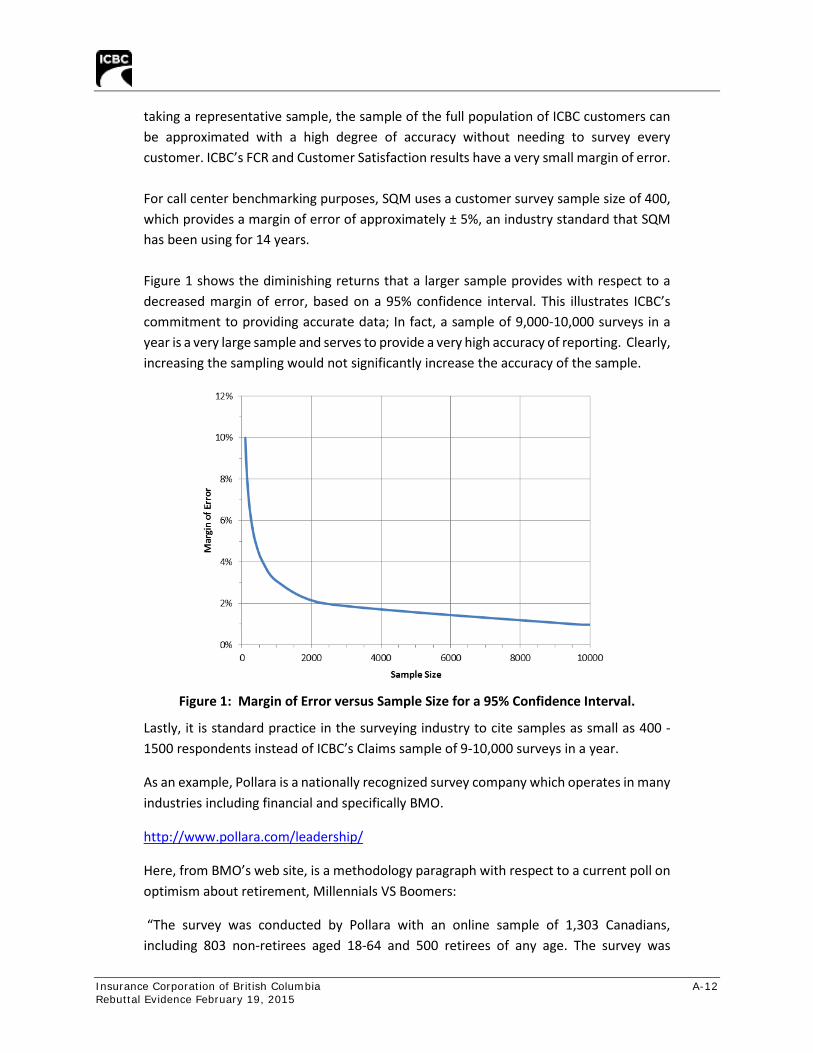

taking a representative sample, the sample of the full population of ICBC customers can be approximated with a high degree of accuracy without needing to survey every customer. ICBC’s FCR and Customer Satisfaction results have a very small margin of error. For call center benchmarking purposes, SQM uses a customer survey sample size of 400, which provides a margin of error of approximately ± 5%, an industry standard that SQM has been using for 14 years. Figure 1 shows the diminishing returns that a larger sample provides with respect to a decreased margin of error, based on a 95% confidence interval. This illustrates ICBC’s commitment to providing accurate data; In fact, a sample of 9,000-10,000 surveys in a year is a very large sample and serves to provide a very high accuracy of reporting. Clearly, increasing the sampling would not significantly increase the accuracy of the sample.

Figure 1: Margin of Error versus Sample Size for a 95% Confidence Interval.

Lastly, it is standard practice in the surveying industry to cite samples as small as 400 - 1500 respondents instead of ICBC’s Claims sample of 9-10,000 surveys in a year.

As an example, Pollara is a nationally recognized survey company which operates in many industries including financial and specifically BMO.

http://www.pollara.com/leadership/

Here, from BMO’s web site, is a methodology paragraph with respect to a current poll on optimism about retirement, Millennials VS Boomers:

“The survey was conducted by Pollara with an online sample of 1,303 Canadians, including 803 non-retirees aged 18-64 and 500 retirees of any age. The survey was

Insurance Corporation of British Columbia A-12 Rebuttal Evidence February 19, 2015

conducted from November 12 to November 17, 2014. A probability sample of 1,303 would yield results accurate to ± 2.7 per cent, while a probability sample of 803 would yield results accurate to ± 3.5 per cent 19 times out of 20. Results have been weighted using the latest census data to be representative of Canadians as a whole.”

http://newsroom.bmo.com/press-releases/bmo-canadian-millennials-are-more-optimistic-abou-tsx-bmo-201501280989374001

31. COPE includes in responses to information requests an opinion, attributed to a Dr. Fred

Van Bennekom, that it is better to take First Call Resolution data from data collection systems.

Other industry experts do not share Dr. Van Bennekom’s view. An excerpt from a book

written by Mr. Mike Desmarais, President and founder of SQM Group and referenced in a white

paper abstract states, “SQM’s research shows that call centers using internal FCR metrics

report their FCR 10% to 20% higher than their VoC FCR performance. In the vast majority of

cases, internal FCR methods overstate the call center’s FCR performance and are difficult to

accurately measure.”2 More information and greater detail on the above statistics can also

be found on SQM’s website, for example:

Our research shows that when FCR is reported by internal methods, the call center industry average is 84%. However, when FCR is reported by external methods, the call center industry average is 68%. It has been SQM’s experience that the internal methods over inflate FCR performance and therefore, when your FCR performance is in the mid-eighties there is no sense of urgency to make improvements. Each method for measuring FCR is useful in helping the call center improve their FCR performance. However, the external method in which the customer determines if their call was resolved on the first call is what matters the most.3

No Other Alternative Service Provider

32. On pages 13 to 14 of the Report, Ms. Reynolds says the call abandon numbers and

percentages are, “… extremely high for an organization like ICBC where there is no other

alternative service-provider available for the caller. While it is more common to see high

abandons for a call center where there are many competitors and alternatives available, ICBC

has a captive audience of customers with no place else to go to discuss a claim.”

2 Mike Desmarais, “First Call Resolution: Defining, Measuring and Improving”, SQM Group, http://www.sqmgroup.com/pdf/first-call-resolution-whitepaper.pdf, accessed February 12, 2015. In the quote, VoC stands for Voice of the Customer. 3 “First Call Resolution (FCR) – The Metric that Matters Most”, SQM Group, http://www.sqmgroup.com/fcr-metric-that-matters-most, accessed February 12, 2015.

Insurance Corporation of British Columbia A-13 Rebuttal Evidence February 19, 2015

ICBC’s response

33. In BC, ICBC is the sole provider of Basic automobile insurance and sells Optional

automobile insurance in a competitive marketplace. Many customers now prefer alternative

methods such as internet, e-mail, and text messaging over telephone conversations. The

option to report by eClaim has become prominent in ICBC’s Interactive Voice Response

messaging when the customer calls to report a claim and is on hold. There is a segment of

the customer base that would choose to report by eClaim regardless of wait times and are

likely to abandon a call for eClaim upon hearing that alternative. Please see the response to

information request 2014.2 RR BCOAPO.20.2.

Longer-Term Impacts

34. Ms. Reynolds hypothesizes that, “The biggest cost to ICBC may be the long-term

damage that can be done to ICBC’s service reputation …” (page 20), and, “… lessened service

and lack of access to process claims effectively might impact the Legal Representation

Rate ….” (page 49)

ICBC’s response

35. As stated above, service levels (New Claims Initiation) for bodily injury claims are at

least 80% of calls answered in 100 seconds and, since the Legal Representation Rate pertains

to bodily injury claims, the assertion of lessened service and lack of access is incorrect. In

the Application, Chapter 6, ICBC describes enhanced access through improved explanation of

benefits, immediate access to medical treatment, and quicker files assignment to the resource

with the skills and experience to best handle the type of claim presented.

36. The Claims Hierarchy was implemented in 2013 and rollout of ClaimCenter began in

late 2013; throughout this period Claims Customer Satisfaction and First Call Resolution

remained high. As previously discussed, call centre operational metrics are also improving in

the latter half of 2014, as anticipated. ICBC expects impacts of Claims Transformation to be

transitional and not long-term.

37. While Ms. Reynolds speculates that the transitional impacts of Claims Transformation

might impact the Legal Representation Rate, she does not point to any data or analysis to

support her supposition. In addition, in its responses to Commission information requests,

Insurance Corporation of British Columbia A-14 Rebuttal Evidence February 19, 2015

COPE appears to misinterpret ICBC’s response to information request 2014.1 RR BCUC.50.5

because that evidence states, “… implementation of the new claims management system in

2013 and 2014 … does not coincide with the acceleration in the rate of legal representation

on mild STI [Soft Tissue Injury] claims first observed in 2011.”

38. The Customer Attitudes Survey, summarized in the Application, Chapter 6, looked at

many factors that could influence a customer’s decision to seek representation. Although

COPE asserts in its responses to Commission information requests that ICBC did not “look

into the proverbial mirror”, the Customer Attitudes Survey did, in fact, consider drivers such

as whether the customer expected: a difficult process; unfair compensation; unfair treatment;

and biased adjusters. The results of the Customer Attitudes Survey found that the leading

influence was the perception of lawyer benefits, with all of the above exerting less influence.

In addition, in the long-term, Claims Transformation puts ICBC in a better position to improve

claims handling, irrespective of the transitional impacts.

Managing Costs and Services

39. Ms. Reynolds also speculates about operating costs associated with the transitional

impacts of Claims Transformation, as well as the impacts on customer and employee

satisfaction (please see for instance, page 49). On page 50 of the Report, she recommends,

“… ICBC re-examine its staffing levels and add requisite staff to correspond to current and

planned workloads.” Also on page 50, she states, “The forecasting and planning process in

place appears to be a sound one. With the upheaval and learning curve of the transformation

project mostly over, it is recommended that ICBC create a solid forecast for 2015 and

2016 ...”

ICBC’s response

40. COPE also received information requests on their evidence regarding operating costs

during the transition period. While COPE was asked for the labour costs associated with the

staffing levels depicted in the Report on page 16 (also on page 27), they instead provided an

estimation of the incremental salary costs of one full-time adjuster in the Claims Contact

Centre, and those salaries as a percentage of the required Basic insurance premium for policy

year 2014. ICBC has not validated COPE’s calculations, although it does note that the wages

for group 8 adjusters and group 5 adjusters appear to have been reversed. ICBC provided

the actual budgeted average compensation cost for a Customer Service Adjuster full-time

Insurance Corporation of British Columbia A-15 Rebuttal Evidence February 19, 2015

equivalent (group 8) in response to information request 2014.2 RR COPE.34.1.1-2. Costs to

temporarily add staff would also include recruiting, training, and eventually attrition costs.

41. While COPE appears to be highlighting that each individual salary is a small part of

required Basic insurance premium, this misses the point. As discussed elsewhere, ICBC is in

a transition period and it makes little sense to hire and train staff to maintain staffing levels

that may not be required as the efficiencies are gained when emerging from transition. As

discussed earlier in this document, ICBC and COPE have already agreed that ICBC will conduct

a workload benchmarking study after a period of stabilization. It is premature to do so at this

time as ICBC is still in the midst of stabilization.

42. ICBC’s budgets and forecasts are always “solid” in that they use the best information

available at the time they are prepared. ICBC’s budgets are prepared in the fall of each year.

Thus, ICBC’s 2015 budget was prepared in fall 2014 using the best, most up-to-date

information about staffing levels and requirements that was available, including information

on the current status of Claims Transformation. Please see the response to information

request 2014.1 RR COPE.10.11 for more information. The factors involved in the assessment

of the business requirements underlying the budget for the Claims Contact Centre are

discussed in the response to information request 2014.1 RR COPE.6.1-4.

Insurance Corporation of British Columbia A-16 Rebuttal Evidence February 19, 2015

PART B

ICBC’S REBUTTAL EVIDENCE IN RESPECT OF EVIDENCE

OF MR. LANDALE

Insurance Corporation of British Columbia Rebuttal Evidence February 19, 2015

IN THE MATTER OF

THE UTILITIES COMMISSION ACT

R.S.B.C. 1996, Chapter 473, as amended and the

INSURANCE CORPORATION ACT R.S.B.C. 1996, Chapter 228, as amended

and

AN APPLICATION BY THE INSURANCE CORPORATION OF BRITISH COLUMBIA (“ICBC”) FOR APPROVAL OF

THE REVENUE REQUIREMENTS FOR UNIVERSAL COMPULSORY AUTOMOBILE INSURANCE EFFECTIVE NOVEMBER 1, 2014

REBUTTAL EVIDENCE OF ICBC TO MR. LANDALE

1. This Rebuttal Evidence responds to Intervenor Evidence filed by Mr. Landale (Exhibits

C1-8 and C1-9). This Rebuttal Evidence focuses only on some key aspects of Mr. Landale’s

position. ICBC’s silence should not be interpreted as agreement with Mr. Landale. ICBC

generally disagrees with much of what Mr. Landale has written.

Actuarial Professional Conduct

2. Mr. Landale makes a number of assertions about how ICBC’s actuaries undertake their

actuarial analysis, in effect suggesting that it is fabricated to achieve a desired result. For

instance, in paragraph 66.6 of his evidence, Mr. Landale states:

• “Intervener evidence submitted herein identifies by way of simplification while using “Bodily Injury – Personal” as an example, how actuarial judgement and preferential selection can predetermine a desired outcome.” (paragraph 66.6)

• “Again by way of my example, any database subjected to a user predisposed input can be manipulated to craft the 5.2% Indicated Rate Change for Basic Insurance Premiums, while following accepted actuarial practice standards and procedures. (paragraph 23)”

3. Mr. Landale’s position is based on “evidence” labelled RTL Evidence #1-1 to #1-4

described as follows in paragraphs 3 and 4:

Insurance Corporation of British Columbia B-1 Rebuttal Evidence February 19, 2015

3. I unreservedly advise that my actuarial model evidence is a total fabrication. It is a construction to make the point that ICBC also constructs their models to justify and support the end, their end for a 5.2% Indicated Rate Change.

4. I am not an actuary, or an accountant, so I make no claim to assert my evidence “RTL Evidence #1-1, #1-2, #1-3, #1-4, #1-51 as fact, but rather as examples of how one can manufacture an outcome, while maintaining ethical and professional standards, albeit while following Special Direction IC2.

ICBC’s response

4. Actuarial analytical work is subject to professional obligations. It would be contrary to

those professional obligations to undertake actuarial analysis in the manner that Mr. Landale

suggests.

5. ICBC notes that Mr. Landale made a similar assertion during the 2013 Revenue

Requirements Proceeding in Exhibit C1-10, in which he stated:

ICBC’s Actuarial modeling is of very selective criteria manifested within ICBC, (there is no apparent “independent” review of the criteria, (ref: page 3-34 & 3-35). This criterion is chosen not to reduce rate increases, but to support rate increases. Model testing is carried out until ICBC finds the desired outcome.

6. ICBC responded as follows in its 2013 Revenue Requirements Application Rebuttal

Evidence (Exhibit B-12 in that proceeding), and these comments are equally applicable today:

ICBC’s actuaries, like all actuaries practicing in Canada, are bound by the Rules of Professional Conduct and the Standards of Practice of the Canadian Institute of Actuaries. ICBC’s actuaries have complied with these Rules and Standards.

The first rule of the Rules of Professional Conduct deals with professional integrity and states “A member shall act honestly, with integrity and competence, and in a manner to fulfil the profession’s responsibility to the public and to uphold the reputation of the actuarial profession.” For an actuary to act as Mr. Landale claims would completely violate the actuary’s ethical responsibilities to the public and would diminish the reputation of the actuarial profession. The spirit and intent that are to govern an actuary’s work is captured by Guiding Principle No. 1 of the Canadian Institute of Actuaries which states: “In carrying on its activities and programs, the Institute holds the duty of the profession to the public above the needs of the profession and its members.”

7. In the context of this Application, ICBC’s actuaries view that their duty to the public is

to perform their work in compliance with Special Direction IC2, which embodies the public

1 Note that RTL Evidence #1-5 is incorrectly identified as part of this “evidence”. As indicated, the table in RTL Evidence #1-5 is copied from ICBC’s response to information request 2014.1 RR BCUC.1.1.

Insurance Corporation of British Columbia B-2 Rebuttal Evidence February 19, 2015

policy as determined by government that the Commission is bound to follow in fixing rates

for Basic insurance. That public policy requires rates be set according to accepted actuarial

practice. Specifically, this requires the actuaries who have prepared and reviewed the

Application to make a best estimate of the claims costs and expenses for Basic insurance and

the premium rates needed to meet those claims costs and expenses. A best estimate is

defined by the Standards of Practice of the Canadian Institute of Actuaries as an estimate

that is without bias, neither conservative nor unconservative.

8. The type of pre-determined rate analysis described by Mr. Landale would not be

considered a best estimate of future costs, and therefore could not be in accordance with

accepted actuarial practice. ICBC’s actuaries have retained their professional integrity

throughout this rate setting process, and neither the Filing Actuary nor the Reviewing Actuary

had any difficulty declaring in writing that the analysis complied with accepted actuarial

practice.

Appropriate Description and Disclosure

9. In a number of instances, Mr. Landale challenges the sufficiency of ICBC’s evidence.

In paragraph 67, Mr. Landale states, for example: “Based on the evidenced [sic] offered

herein for the BCUC Commissioners to examine, I assert the limitations of my evidence is

based on the lack of analysis and discussion by ICBC in their 2014 RRA filing exhibit B-3 and

all succeeding exhibit filings to date.” He makes similar statements in paragraphs 26 and 28.

10. Mr. Landale also makes a number of other statements regarding the sufficiency of the

disclosure in his paragraphs 8 through 16 that relate to the general application of standard

actuarial methods. Among these is an observation in paragraph 13 relating to bodily injury

claims counts which relate to elements directly addressed in the Application and information

requests, which is described further in the section entitled “Bodily Injury Claims Counts”

below.

ICBC’s response

11. ICBC believes that the level of analysis and discussion regarding the rate indication is

appropriate. The Application, Chapter 3 provides both a high level summary as well as the

detailed actuarial analysis. The high level summary is intended to assist the users’

understanding of the key assumptions that influence the actuarial forecasts, including

Insurance Corporation of British Columbia B-3 Rebuttal Evidence February 19, 2015

noteworthy methodology changes which are highlighted in Chapter 3, Section C. The detailed

actuarial analysis includes extensive discussion of the data used, the methods and

assumptions employed, and the results. Formulae and references are provided to enable an

intended user of the rate filing who is knowledgeable in actuarial techniques as they apply to

automobile insurance in BC to follow the application of methods and the calculation of the

rate indication. Thereby the Application documents the actuaries’ analysis and all key

assumptions. ICBC actuaries endeavor to present their analysis in the same manner from

application to application in order to facilitate comparison with prior revenue requirements

applications. Further description and disclosure that may be desired with relation to any of

the actuarial assumptions is then available to the Commission and intervenors through

information requests.

12. Although the discussion in the Application, Chapter 3 and the accompanying actuarial

exhibits include substantial explanatory notes, it is not intended to be a primer on the general

application of standard actuarial methods for the estimation of claims costs. A standard

educational text regarding the application of actuarial methods to estimation of claims costs

can be found at:

http://www.casact.org/library/studynotes/Friedland_estimating.pdf.

13. With reference to accepted actuarial practice in Canada, the appropriate level of

description and disclosure for an actuarial report such as the revenue requirements analysis

is addressed in Section 1820 of the Standards of Practice of the Canadian Institute of

Actuaries. As it is a report prepared for external users, the Application is necessarily both

formal and detailed in the information it provides (addressed in Section 1820.06). In that

context, Section 1820.07 addresses the level of exposure:

Appropriate description and disclosure in a report strike a balance between too little and too much. Too little disclosure deprives the user of needed information. Too much disclosure may exaggerate the importance of minor matters, imply a diminution of the actuary’s responsibility for the work, or make the report hard to read.

14. ICBC believes that the description and disclosure provided in the rate level indication

analysis, including additional information made available through information requests,

strikes an appropriate balance and provides the users with sufficient information to

understand the key assumptions on which the rate indication relies. ICBC’s external

Reviewing Actuary’s opinion confirms that the rate level indication analysis is consistent with

Insurance Corporation of British Columbia B-4 Rebuttal Evidence February 19, 2015

accepted actuarial practice in Canada, which includes the standards for appropriate

description and disclosure in Section 1820.

15. Key users of the actuarial rate indication analysis include the Commission staff and the

independent actuarial consultants engaged by the Commission. During the course of the Oral

Hearing on 2013 Revenue Requirements, the counsel for the Commission2 provided an

additional comment supporting the sufficiency of the documentation of the actuarial rate level

indication analysis, as follows:

MR. MILLER: Q: Good morning, panel. First of all, Staff and the actuarial consultants would like to commend the Insurance Corporation for a well prepared actuarial component of the application. It’s better than they’ve seen in many jurisdictions, so welcome -- I mean thank you.

Independent Review of Revenue Requirements Analysis

16. In paragraph 63 of his evidence, Mr. Landale states: “The BCUC must employ a true

“Independent Actuarial Review” before reaching a decision for this current 2014 RRA.” Also

in paragraph 50, he states:

What should be construed by the Commission and interveners as to the reliability of Miss [sic] Camille Minogue, an employee of ICBC for some 10 years, and Mr. William Weiland, the Principal and Consulting Actuary with Eckler Ltd signatures. (see Appendix D for email copy). Where is the Independent Actuary Review?, meaning non ICBC employees.

ICBC’s response

17. As noted in paragraph 5, Mr. Landale made a similar assertion during the 2013

Revenue Requirements Proceeding in Exhibit C1-10. ICBC responded as follows in its Rebuttal

Evidence Exhibit B-12, and the same response is applicable today.

Finally, Mr. Landale is incorrect in his belief that there is no independent review of the actuarial assumptions. In fact, the revenue requirements application process is an independent review of the rate application by the Commission, which engages independent actuaries to assist in the review process. Also, ICBC engages an external actuary to review its analysis prior to filing the Application.

18. Although Mr. Landale refers to Mr. Weiland in paragraph 50 as an employee of ICBC,

Mr. Landale is well aware that this is not the case. Mr. Landale had sought confirmation of

2 Oral Hearing on 2013 Revenue Requirements, Transcript Volume 4, page 551, line 24 to page 552, line 3.

Insurance Corporation of British Columbia B-5 Rebuttal Evidence February 19, 2015

this fact from ICBC, and was provided with an email explaining that Mr. Weiland is not an

ICBC employee. The email is appended in Attachment B-1, and is quoted below for ease of

reference:

Further to your telephone call today, ICBC confirms that Ms. Minogue is a full time employee of ICBC. Ms. Minogue is ICBC’s Chief Actuary and has held this position for approximately 10 years.

Mr. Weiland is not an employee of ICBC. Mr. Weiland is the Principal and Consulting Actuary with Eckler Ltd. He has held this position since 1992. He has been ICBC’s external actuary since 1996.

19. In Attachment B-2 ICBC provides information on the standing of Ms. Minogue and Mr.

Weiland filed as Exhibit B-9 during the 2013 Revenue Requirements Proceeding, a proceeding

in which Mr. Landale participated. As indicated in Attachment B-2, ICBC had engaged Mr.

Weiland in 2013 to review the actuarial analysis chapter (Chapter 3) of the 2013 Revenue

Requirements Application. Mr. Weiland also fulfilled this function for the current Application.

The content of Chapter 3 is the basis of the actuarial rate indication.

20. The Commission also engages independent actuarial consultants to assist it in the

process of reviewing the revenue requirements application and specifically the actuarial

analysis chapter. There was a significant volume of information requests and associated cross

examination during the Oral Hearing on 2013 Revenue Requirements (Transcript Volume 4,

page 551, line 24 to page 574, line 10 and page 577, line 24 to page 620, line 3) arising from

the Commission’s independent actuarial consultants’ examination of the methods and

assumptions used in the determination of the claims cost estimates. As noted above in

paragraph 15 of this Rebuttal Evidence, during that oral hearing the counsel for the

Commission commended ICBC on behalf of the independent actuarial consultants for “a well

prepared actuarial component … better than they’ve seen in many jurisdictions ...”

Mr. Landale participated in the Oral Hearing and copies of the transcript were available to

him.

21. Similarly the Commission has engaged the same independent actuarial consultants to

assist in their review of the actuarial analysis in the current Application and there was again

a large volume of information requests focusing on the differences between the methodologies

used in the current Application to those used in the 2013 Revenue Requirements Application.

Insurance Corporation of British Columbia B-6 Rebuttal Evidence February 19, 2015

ICBC Responses to Mr. Landale’s Information Requests

22. In paragraph 5 of his evidence, Mr. Landale states:

I would also remind the Commissioners that from the 2011 RRA I have challenged ICBC’s actuarial modeling in various submissions, letters to the Commission and during the 2013 RRA oral hearings. To date ICBC has dismissed me as well as the BCUC in their last two decisions in this regard.

ICBC’s response

23. ICBC understands that intervenors may not always agree with the answers provided,

but disagreeing with the response is different from ICBC not answering the question. ICBC

believes that it has gone above and beyond with Mr. Landale since he began participating in

the process beginning with the Revenue Requirements Proceeding for the 2012 Policy Year.

ICBC has spent significant effort and time in developing responses to Mr. Landale’s

information requests and matters of interest in both the 2013 and 2014 Revenue

Requirements Proceedings. Please see Attachment B-3 for the 2014 listing of Mr. Landale’s

information requests and matters of interest on the topic of the actuarial analysis to which

ICBC has appropriately responded.

24. In addition to responding to questions formally, ICBC has also answered Mr. Landale’s

questions informally outside of the Commission’s process on a number of occasions (an

example of which is the email correspondence attached at Attachment B-1). ICBC’s Corporate

Regulatory Affairs staff and its legal counsel have taken the time during proceedings and

workshops to help Mr. Landale understand the process and the regulatory framework.

Bodily Injury Claims Counts

25. In the section of his evidence entitled “Discussion of Exhibit C.1.0 Summary of Bodily

Injury Selections – Personal”, paragraph 13, Mr. Landale states with reference to the

Application, Chapter 3, Exhibit C.1.2.1:

Understanding the product in column 7, namely “38,491” is critically important because Exhibit C1.1.1 AY 2014 column 1 is the “Selected Incurred Count”. If one were to change the “Count Development Factor” (CDF) column 6 in exhibit C.1.2.1 to the same factor used in ICBC 2013 RRA the “Selected Incurred Count” would be 37,587 x 1.0230 = 38,451 rather than the 2014 RRA “Selected Incurred Count” of 38,491. So why then is the value of 50 Selected Incurred Count differential important, because of the upstream/downstream model utilization in Exhibit C.1.1.1.

Insurance Corporation of British Columbia B-7 Rebuttal Evidence February 19, 2015

ICBC’s response

26. ICBC described in the Application (please see Chapter 3, paragraph 47) that there has

been a shift in the recording pattern of bodily injury claims, where there is now a greater

delay between the date of loss and the first recording of a bodily injury claim. A consequence

of this shift is that higher count development factors are observed in Exhibits C.1.2.1 and

C.1.2.2. Further information regarding this observation was requested by the Commission in

2014.1 RR BCUC.19.1, to which ICBC provided a response. There were no follow up

information requests.

Capital Maintenance

27. Mr. Landale’s discussion regarding capital maintenance suggests that ICBC has been

misleading. In the section “Following the Money to the MCT”, paragraph 32, Mr. Landale

states:

After finding on page 3-34 of the RRA

“D.9 Capital Maintenance 100. Exhibit Set G shows the calculation of capital maintenance, which is the cost of maintaining capital at the target level. Exhibit Set G also shows an allocation of Basic equity that is used to allocate investment income and capital maintenance to the coverage level. An increase in the amount of capital maintenance has an impact of +0.2 percentage points on the PY 2014 indicated rate change.” contrary to Slide #10 [of the Review Working Session presentation Exhibit B-7] [Emphasis added by Mr. Landale]

28. In his response to information request BCUC.2.1 in Exhibit C1-9, Mr. Landale asserts

that the calculation of the capital maintenance in the Application, Chapter 3, Exhibit G.2 is

flawed because it does not correlate with slide 8 of the September 26, 2014 Review Working

Session presentation.

29. In paragraph 45 of Exhibit C1-8, Mr. Landale states:

In Slide #11 ICBC titles the slide “Capital Levels do not make rates higher for customers” The most misleading statement ICBC has made in this current application.

ICBC’s response

30. Mr. Landale is mistaken with respect to slide 10 of the Review Working Session

presentation. Slide 10 does indicate that the increase in the amount of capital maintenance

Insurance Corporation of British Columbia B-8 Rebuttal Evidence February 19, 2015

has an impact of +0.2 percentage points on the policy year 2014 indicated rate change. Slide

10 indicates that the capital maintenance included in the required premium for the 2014 policy

year is $64 million and represents 2.4% of the required premium. The capital maintenance

included in the required premium for the 2013 policy year is $57 million and represents 2.2%

of the then required premium. The difference between these two represents 0.2 percentage

points of the 2014 policy year rate indication. ICBC showed the calculation for this in its

response to Mr. Landale’s Matter of Interest 2014 RR RL.MOI.9.

31. Mr. Landale is correct that the calculation of the capital maintenance in the Application,

Chapter 3, Exhibit G.2 does not correlate with slide 8 of the Review Working Session

presentation. However, Mr. Landale is incorrect that the calculation of the capital

maintenance in The Application, Chapter 3, Exhibit G.2 is flawed. The calculation of the capital

maintenance in Chapter 3, Exhibit G.2 is carried out in compliance with the Commission-

approved Capital Management Plan and in particular the directive: “The Panel accepts the

ICBC proposed 10 year transition period to reach the 145% MCT new Capital Management

Target.” As explained in the response to information request 2014.1 RR RM.3, the 10-year

transition period refers to the period of time over which ICBC will phase-in the full capital

maintenance provision.

32. Slide 8 of the Review Working Session presentation reflects how the capital

maintenance will be calculated once the transition period is complete. Slide 9 of the Review

Working Session presentation explains that the capital maintenance amount in the 2013 rates

is $57 million, representing a shortfall of 1% of the required premium which is being

transitioned into the rate over a period of 10 years. The example calculation in slide 8

provides the amount of capital maintenance that would be included in the required premium

if the 10-year transition were already complete. The calculation of the capital maintenance

shown in slide 8 is provided in Attachment B-4.

33. Mr. Landale has also misinterpreted the content of slide 11 of the Review Working

Session presentation in asserting that ICBC has made misleading statements and

misrepresented material information. Slide 11 of the Review Working Session presentation

refers to the fact that capital maintenance contributes $64 million to the required premium;

but expected investment income to be made on this capital reduces the required premium by

$67 million. There is therefore a net reduction of $3 million in the amount of premium revenue

that is required; hence the statement that capital levels do not make rates higher

Insurance Corporation of British Columbia B-9 Rebuttal Evidence February 19, 2015

for customers. The response to information request 2014.1 RR RL.5.12 provides the detailed

calculation.

Errata on Appendix 11 B of the Application

34. In paragraphs 48, 50 and 51, Mr. Landale states:

48. Reminding the BCUC Commissioners that on September 18th ICBC issued their “Errata to ICBC’s 2014 Revenue Requirements Application BIIS Sept 18, 2014”, to their Appendix 11B – Basic Insurance Information Sharing”. 50. In my response I question among other things why did ICBC actuaries sign off on these exhibits in the original 2014 RRA? … What assurances does ICBC offer that the resubmitted 105 page worksheets are accurate? Why did ICBC not submit along with this errata Miss Minogue re-certification? 51. Lastly, and I admit, what does this mean to the final outcome in the determination of the 5.2% Indicated Rate Change. Respectfully, I rely on the BCUC Chairman to confirm his satisfaction on this matter.

ICBC’s response

35. The errata referred to above relate to information filed in the Application, Appendix 11

B and this information is not used in the determination of the actuarial rate indication.

36. In its response to Mr. Landale’s information request 2014.1 RR RL.8.0, ICBC explained

that:

The Filing Actuary’s Opinion in the Application Chapter 3, Section D.12 and the Reviewing Actuary’s Opinion in Chapter 3, Section D.13 are professional certifications that relate to the data and calculations that comprise the actuarial rate indication analysis. This analysis is the topic of Chapter 3. ICBC notes, as a factual matter, that there have been no errata identified that relate to either the data or calculations in Chapter 3. The process used by ICBC actuaries to prepare the rate indication is subject to strong governance protocols…

37. In addition, “.. ICBC submits that the public should have full confidence that the rate

indication is prepared according to accepted actuarial practice and that the information

provided by ICBC to support the rate request is complete and accurate.”

Insurance Corporation of British Columbia B-10 Rebuttal Evidence February 19, 2015

Canada Pension Plan (CPP) and Consumer Price Index (CPI)

38. In paragraphs 52 and 53, Mr. Landale states:

52. The two subjects CCP [sic] and CPI have been thoroughly discussed during this current 2014 RRA, so I am not going to burden the record with further discussion … 53. Special Direction IC2 requires ICBC to raise rates to cover costs, there is no point arguing this mandate.

ICBC’s response

39. In its response to Mr. Landale’s information request 2014.1 RR RL.4.1, ICBC explained

that:

The CPI is based on a market basket of goods and services which have no meaningful relationship with the “goods” in ICBC’s claims “basket”. Basic insurance rates are determined primarily by the changing loss cost on each of ICBC’s Basic Plate Owner and Manual coverages. ICBC’s claim costs are impacted by inflationary pressures above and beyond the inflation as measured in the Canada all-items CPI. These costs have been accounted for in order to determine rate changes that are in accordance with accepted actuarial practice.

40. ICBC agrees that it has spent significant time and effort in responding to information

requests on the topic of the CPI and ICBC’s claims costs in this and past proceedings. The

Commission can obtain an indication of just how much work has gone into addressing an issue

about which the Commission has no jurisdiction, by referring to Attachment B-3 to see the

number of CPI related responses to information requests and matters of interest from this

2014 Revenue Requirements Proceeding alone (there were 31).

Insurance Corporation of British Columbia B-11 Rebuttal Evidence February 19, 2015

Attachment B-1 – ICBC’s Email to Mr. Landale Regarding Ms. Minogue and Mr. Weiland

Insurance Corporation of British Columbia Rebuttal Evidence February 19, 2015

1

From: RegaffairsSent: Friday, January 09, 2015 1:57 PMTo: [email protected]: Commission Secretary BCUC:EX ([email protected]); Elder, June;

RegaffairsSubject: Response to your query regarding Ms. Minogue and Mr. Weiland

Dear Mr. Landale,

Further to your telephone call today, ICBC confirms that Ms. Minogue is a full time employee of ICBC. Ms. Minogue is ICBC’s Chief Actuary and has held this position for approximately 10 years.

Mr. Weiland is not an employee of ICBC. Mr. Weiland is the Principal and Consulting Actuary with Eckler Ltd. He has held this position since 1992. He has been ICBC’s external actuary since 1996.

Thank you.

Corporate Regulatory Affairs – ICBC [email protected]

Attachment B-2 – Excerpts from ICBC’s 2013 Revenue Requirements Proceeding, Exhibit B-9 Regarding the Standing of Ms. Minogue and Mr. Weiland

Insurance Corporation of British Columbia Rebuttal Evidence February 19, 2015

ICBC Filing re: Revenue Requirements Application for the 2013 Policy Year

Insurance Corporation of British Columbia Page 1 of 2

January 2014

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

DIRECT TESTIMONY OF CAMILLE MINOGUE

Q1. Please state your name and present position.

A. My name is Camille Minogue. I hold the position of Chief Actuary at ICBC.

Q2. How long have you held that position?

A. For approximately nine years.

Q3. What positions did you hold prior to joining ICBC and with whom?

A. I began my actuarial career in 1991 with the Safeco Corporation, and in November

2000 was named Assistant Vice President, at which time I was responsible for rate

making for all casualty lines in SAFECO Commercial Enterprise. I moved to the

Mattei Companies in 2002, and there I held the position of Vice President and Chief

Actuary. In 2004, I joined ICBC as the Chief Actuary. A copy of my curriculum vitae

is attached.

Q4. What are your professional qualifications?

A. I have a PhD in Mathematics from Washington State University (1991). I am a

Fellow of the Casualty Actuarial Society (1996) and an Affiliate member of the

Canadian Institute of Actuaries (2006).

Q5. Have you previously testified before this Commission?

A. Yes.

Q6. What role did you play in the development of the Revenue Requirements Application?

A. I helped to prepare, and have overall responsibility for, the actuarial evidence in the

Application, including Chapter 3 (Actuarial Rate Level Indication Analysis). I vetted

the actuarial analysis undertaken in support of the Application. I was responsible for

ensuring that the actuarial analysis complies with accepted actuarial practice. My

certification of the rate indication in my capacity as ICBC’s Chief Actuary is included

at the end of Chapter 3 of the Application.

ICBC Filing re: Revenue Requirements Application for the 2013 Policy Year

Insurance Corporation of British Columbia Page 2 of 2

January 2014

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

Q7. What sections of the Filing will you be speaking to in the Commission hearing?

A. I will be speaking to the actuarial evidence, including Chapters 3 and 4.

Q8. Does this complete your direct testimony?

A. Yes.

Camille Minogue, FCAS, Ph.D.

151 West Esplanade – L299504

North Vancouver, B.C. V7M 3H9

(604) 982-7289 / [email protected]

Professional Experience

Chief Actuary

Insurance Corporation of British Columbia (“ICBC”)

2004 – Present

Lead all actuarial functions within the corporation and, since 2008, other advanced analytics functions of

the corporation.

Support the regulatory aspects relating to ICBC’s open and transparent public rate application process,

assisting with the preparation of written applications and information request processes, as well as

representing ICBC as expert witness in public hearings.

Responsible for the full spectrum of corporate actuarial services, including rate indication analyses,

quarterly reserve reviews, determining revenue requirements of the corporation, and testing the adequacy

of capital reserves.

Support of high value corporate projects through the provision of advanced analytics services, including

predictive models, program evaluations, customer research and other appropriate and insightful analytics;

examples range from the development of claims predictive models to assist with claims segmentation

objectives to road safety program evaluations in support of initiatives aimed at reducing crashes.

Vice President and Chief Actuary

The Mattei Companies, Seattle WA

2002 – 2004

Directed all actuarial functions of the company; involved in the company’s strategic and tactical planning,

and company marketing.

Assistant Vice President and Actuary

Safeco Property & Casualty Companies, Seattle, WA

1991 – 2002

Upon becoming a fellow of the Casualty Actuarial Society (CAS), was promoted to leadership roles and

made responsible for the pricing of all commercial casualty lines. Later led Commercial Actuarial

Consulting with responsibility for reserving, forecasting and planning, and executive analyses.

Educational Degrees and Professional Designations

Affiliate of the Canadian Institute of Actuaries (CIA), 2005

Fellow of the Casualty Actuarial Society (CAS), 1996

Ph.D., Mathematics, Washington State University, 1991

MS, Mathematics, Washington State University, 1987

Certificate of Competence in German, Universität Bielefeld, Germany, 1986

BS, Mathematics, University of Alaska, Fairbanks, 1984

Selected Professional and Volunteer Activities

Adjunct Professor, Department of Statistics and Actuarial Science at Simon Fraser University,

2013 – 2018

Member of the Program Planning Committee of the CAS, 2007 – 2011

Member of Casualty Actuaries of the Northwest (CANW), 1991 – present

Visiting Instructor in the Department of Statistics and Actuarial Science at Simon Fraser

University, Fall Semesters 2006 and 2008

President of the CANW, 2006 – 2007

Member of the Program Planning Committee of the CANW, 2005 – 2007

Board Member of the State of Washington Midwifery Joint Underwriting Assoc., 1997 – 2002

Member of Insurance Services Office Commercial Casualty Actuarial Panel, 1998 – 2000

ICBC Filing re: Revenue Requirements Application for the 2013 Policy Year

Insurance Corporation of British Columbia Page 1 of 2

January 2014

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

DIRECT TESTIMONY OF WILLIAM T. WEILAND

Q1. Please state your name and present position.

A. My name is William T. Weiland. I hold the position of Principal and Consulting

Actuary with Eckler Ltd.

Q2. How long have you held that position?

A. I have been a Principal and Consulting Actuary at Eckler Ltd. since 1992.

Q3. How long have you been ICBC’s external actuary?

A. Since 1996.

Q4. What other positions have you held and with whom?

A. From 1986 to 1992, I held the position of Consulting Actuary at MLH&A Inc. From

1975 to 1986, I held various positions from Actuarial Analyst to Associate Actuary to

Director of Corporate Planning with Travelers Canada, a large property and casualty

insurer in Canada until its sale in the late 1980’s. A copy of my curriculum vitae is

attached.

Q5. What are your professional qualifications?

A. I am a Fellow of the Canadian Institute of Actuaries (1982) and Fellow of the

Casualty Actuarial Society (1982).

Q6. Have you previously testified before this Commission?

A. Yes.

Q7. What role did you play in the development of this Filing?

A. I was engaged by ICBC as a consulting actuary to provide actuarial consulting

services, which includes reviewing ICBC’s selection of methods and assumptions

underlying this Application. My role was also to assess whether the actuarial rate

indication developed by ICBC’s actuaries accords with accepted actuarial practice. I

reviewed Chapter 3 (Actuarial Rate Level Indication Analysis), inclusive of the

ICBC Filing re: Revenue Requirements Application for the 2013 Policy Year

Insurance Corporation of British Columbia Page 2 of 2

January 2014

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

actuarial Exhibits, for this purpose. My opinion that the indicated changes in average

rate level presented in the Application have been calculated in accordance with

accepted actuarial practice is found at page 3-34 of the Application.

Q8. What sections of the Filing will you be speaking to in the Commission hearing?

A. I will be speaking to those elements of Chapter 3 that relate to the determination of

“Claims Costs”, the “PY 2012 Loss Cost Forecast Variance and Loss Cost Trend to PY

2013”. My role includes speaking to how those elements of the rate indication

accord with accepted actuarial practice in Canada.

Q9. Does this complete your direct testimony?

A. Yes.

William T. Weiland, FCIA, FCAS

110 Sheppard Avenue East, Suite 900

Toronto, Ontario M2N 7A3

(416) 696-3011 / [email protected]

Professional Experience

Principal and Consulting Actuary

Eckler Ltd.

1992 – Present

Consults to insurance companies, associations, governments and self-insured entities in Canada advising

on property casualty insurance matters including the valuation of policy liabilities, the assessment of risks

affecting insurer capital and the pricing of insurance products.

Is the appointed actuary for several insurance companies and foreign branches operating in Canada

including automobile insurers, commercial property insurers, professional liability insurers, title insurers

and marine insurers. Provides expert testimony before provincial rate regulators in defense of rate filings.

Has been consulting to ICBC as an actuarial advisor since 1996 and at present provides the actuarial

opinion in the financial statements of ICBC regarding the amount of the policy liabilities. Provides

actuarial support to ICBC in relation to applications to ICBC’s regulator, the BC Utilities Commission,

which includes providing evidence and witness support in the written and oral rate application processes.

Vice President and Consulting Actuary

MLH+A , Toronto, Ontario

1986 – 1992

Consulted to insurance companies, associations, governments and self-insured entities in Canada advising

on property casualty insurance matters including the valuation of policy liabilities, the assessment of risks

affecting insurer capital and the pricing of insurance products.

Director, Corporate Planning

Travelers Canada, Toronto, Ontario

1984 – 1986

Directed corporate planning activities for a multi-line insurer relating to property casualty, life and group

insurance.

Various Actuarial Positions

Travelers Canada, Toronto, Ontario

1975 - 1984

Held actuarial positions of increasing responsibility from actuarial analyst to Associate Actuary.

Selected Professional Activities

Chair (1990 – 1992), Vice Chair (1989 – 1990) and Member (1986 – 1989) of the Committee on

Property Casualty Insurance Financial Reporting of the Canadian Institute of Actuaries

The Committee developed the CIA Standard of Practice for financial reporting which came into effect

during my term as Chair.

Member of Council (now the Board) of the Canadian Institute of Actuaries, 1993 – 1996

The Council of the Canadian Institute of actuaries is the governing body of the profession in Canada.

Chair (2009 – 2011) and Member (2004 – 2009) of the Committee on Professional Conduct of the

Canadian Institute of Actuaries

The Committee is responsible for all disciplinary matters concerning the CIA’s Members and Associates

and for providing them with counseling and education concerning disciplinary matters.

MCT Advisory Committee

Member of the Joint Industry-OSFI MCT Advisory Committee (“MAC Committee”) from 2010 to

present. The MAC Committee is responsible for advising OSFI and the industry regarding best practices

for developing Economic Capital Models that are used by insurers to measure the amount capital needed

relative to the risks which an insurer is exposed.

Gold Service Award, 2002

Received from the Canadian Institute of Actuaries the Gold service award, which is the highest level of

recognition for volunteer service within the Institute.

Educational Degrees and Professional Designations

Fellow of the Canadian Institute of Actuaries (CIA), 1982

Fellow of the Casualty Actuarial Society (CAS), 1982

Bachelor of Science, University of Toronto, 1975

Attachment B-3 – ICBC’s Responses to Mr. Landale’s Information Requests and Matters of Interest

Insurance Corporation of British Columbia Rebuttal Evidence February 19, 2015

In this Attachment, ICBC’s responses to the Mr. Landale’s information requests and matters of interest for the 2014 Revenue Requirements Proceeding are listed as follows:

1. those related to the CPP and the CPI; and 2. those related to the actuarial analysis.

1. References to CPP/CPI

References Information Provided

2014 RR RL.MOI.2 2014.1 RR RL.4.1 2014.1 RR RL.4.2 2014.1 RR RL.4.3 2014.1 RR RL.4.4 2014.1 RR RL.4.8 2014.1 RR RL.5.14 2014.1 RR RL.11.5 2014.2 RR RL.9.1 2014.2 RR RL.13.2

Comparisons between CPI and loss trend and Basic insurance rate increases. ICBC explains that the Basic insurance rate increases largely track the increasing trend in loss costs. Loss cost inflation exceeds that of the CPI.

2014.1 RR RL.5.1 2014.1 RR RL.5.2 2014.1 RR RL.5.3 2014.1 RR RL.5.4 2014.2 RR RL.11.1 2014.2 RR RL.12.1-2

Loss cost composition, trend and calculation. ICBC describes how the loss cost trend is determined.

2014 RR RL.MOI.1 2014.1 RR RL.5.5-6 2014.1 RR RL.5.7 2014.1 RR RL.13.1 2014.2 RR RL.13.1 2014.2 RR RL.13.3

CPP/CPI and rate change band. ICBC explains that the loss cost trend is more likely to impact future rate increases than the rate change band specified in Special Direction IC2.

2014.1 RR RL.4.6 2014.1 RR RL.4.7 2014.1 RR RL.5.8-9 2014.2 RR RL.9.2

Impact of Basic insurance rate increases on seniors.

2014.1 RR RL.4.5 2014.1 RR RL.8.3 2014.1 RR RL.8.4 2014.1 RR RL.10.1-3 2014.2 RR RL.10.1

CPI source to be used in the Application.

Insurance Corporation of British Columbia 1 Rebuttal Evidence February 19, 2015

2. References to actuarial analysis

References Topics

2014 RR RL.MOI.6