Embed Size (px)

Citation preview

Kate Swann

Managing DirectorArgos

Agenda

• Argos proposition and business model

• Financial performance

• Drivers of growth

• Agenda for growth going forward

• Summary

Proposition and Business Model

0

10

20

30

40

50

60

70

80

Conve

nienc

ePric

e

Range

Quality

Service

/ Adv

ice Other

Habit /

Inertia

Source: Argos market research

Argos: More choice, less hassle, low pricesArgos: More choice, less hassle, low prices

% of consumers

Unique in the retail marketUnique in the retail market

• Pick up own catalogue

• Choose at home

• Use store to collect or order

• Use store as collection point

• OR order at home

• OR use home delivery

Proposition and Business Model

Low cost operatorLow cost operator

• Secondary/non prime locations

• Small shop floor

• Large stockroom

• Catalogue display space

• Catalogue collection

• Daily delivery

• Lower store staff costs

• Very little shrinkage

Proposition and Business Model

0

500

1,000

1,500

2,000

2,500

98 99 00 01 H1 00 H1 01

SalesSales£m

Financial Performance

Excluding Argos Additions and jungle.com

Year to March

+3%+7%

+11%

+14%+17%

0

20

40

60

80

100

120

140

160

180

98 99 00 01

Financial Performance

Operating profitOperating profit£m

Year to March

-4%+14%

+22%

Excluding Argos Additions and jungle.com

0

10

20

30

40

50

60

70

80

98 99 00 01

%

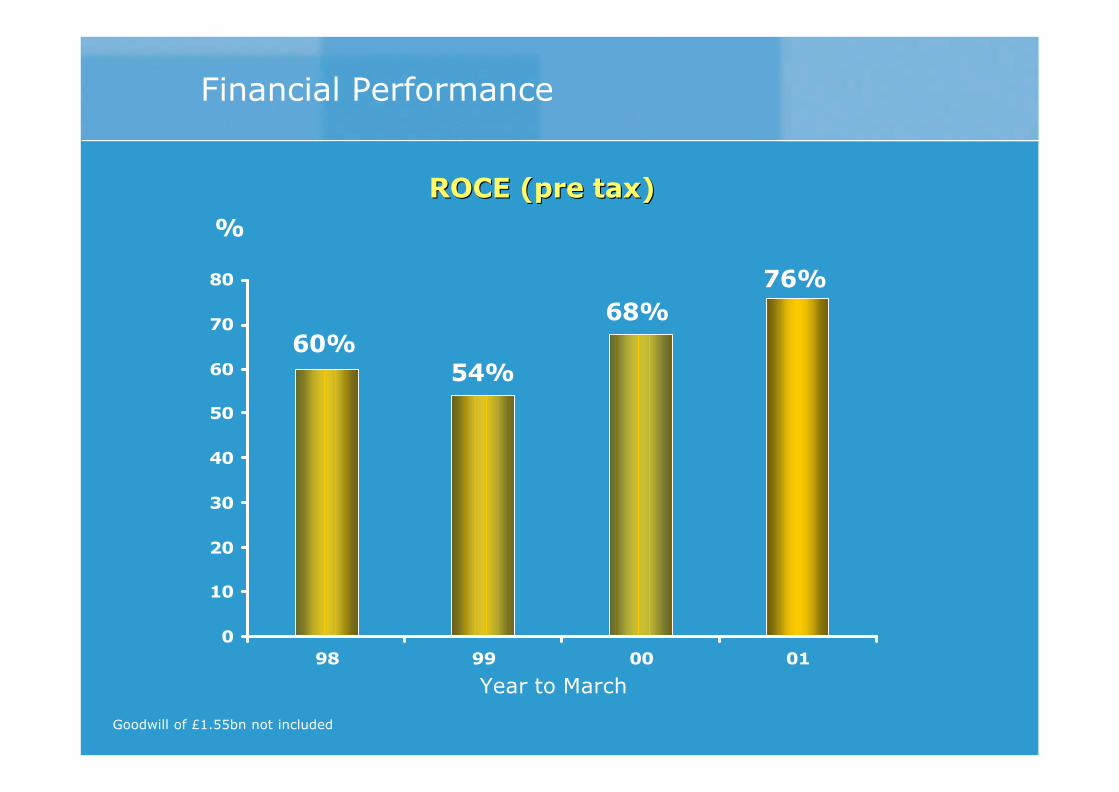

Financial Performance

ROCE (pre tax)ROCE (pre tax)

Year to March

54%60%

68%76%

Goodwill of £1.55bn not included

0

2

4

6

8

10

12

14

16

18

20

Source: British Retail Consortium non-food, non-clothing sales

Financial Performance

Argos sales growth rate Argos sales growth rate continues to be above marketcontinues to be above market

Others (excl. Argos)Argos

Eight week rolling growth

2000 2001

% growth

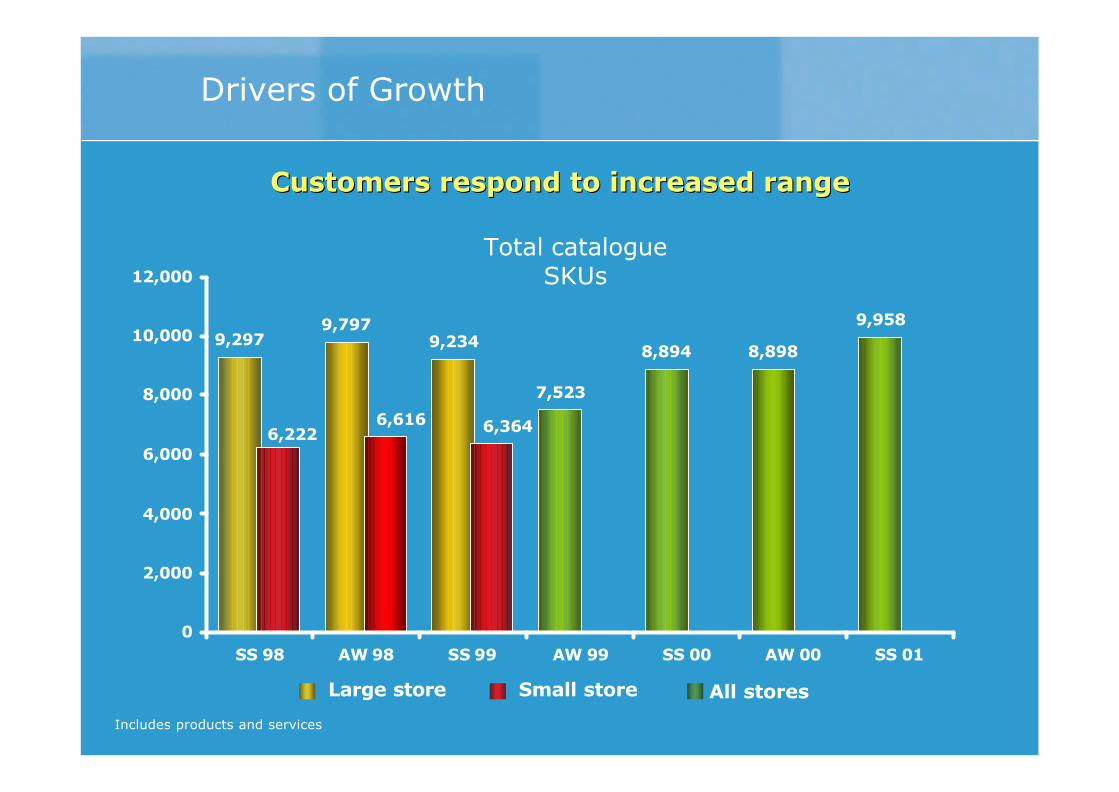

9,2979,797

9,234

7,523

8,894 8,898

9,958

6,3646,6166,222

0

2,000

4,000

6,000

8,000

10,000

12,000

SS 98 AW 98 SS 99 AW 99 SS 00 AW 00 SS 01

Total catalogue SKUs

Customers respond to increased rangeCustomers respond to increased range

Drivers of Growth

Small storeLarge store All stores

Includes products and services

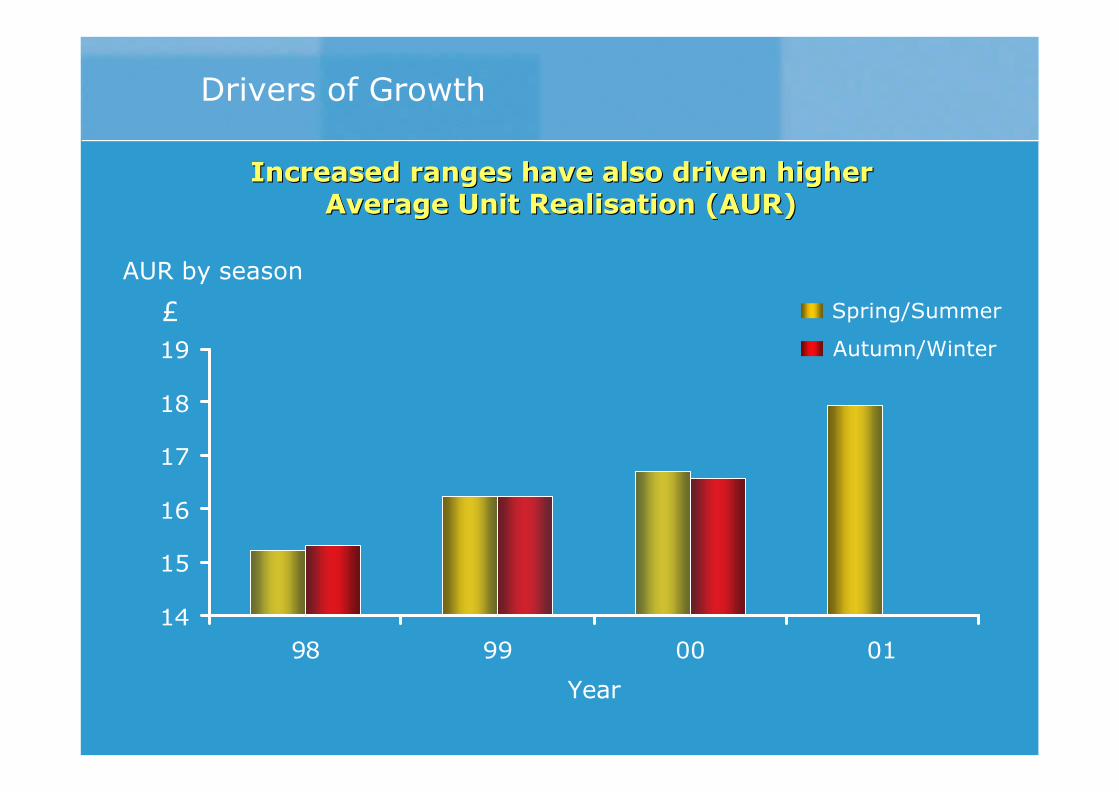

14

15

16

17

18

19

98 99 00 01

AUR by season

Spring/Summer

Autumn/Winter

Increased ranges have also driven higher Increased ranges have also driven higher Average Unit Realisation (AUR)Average Unit Realisation (AUR)

Drivers of Growth

£

Year

Drivers of Growth

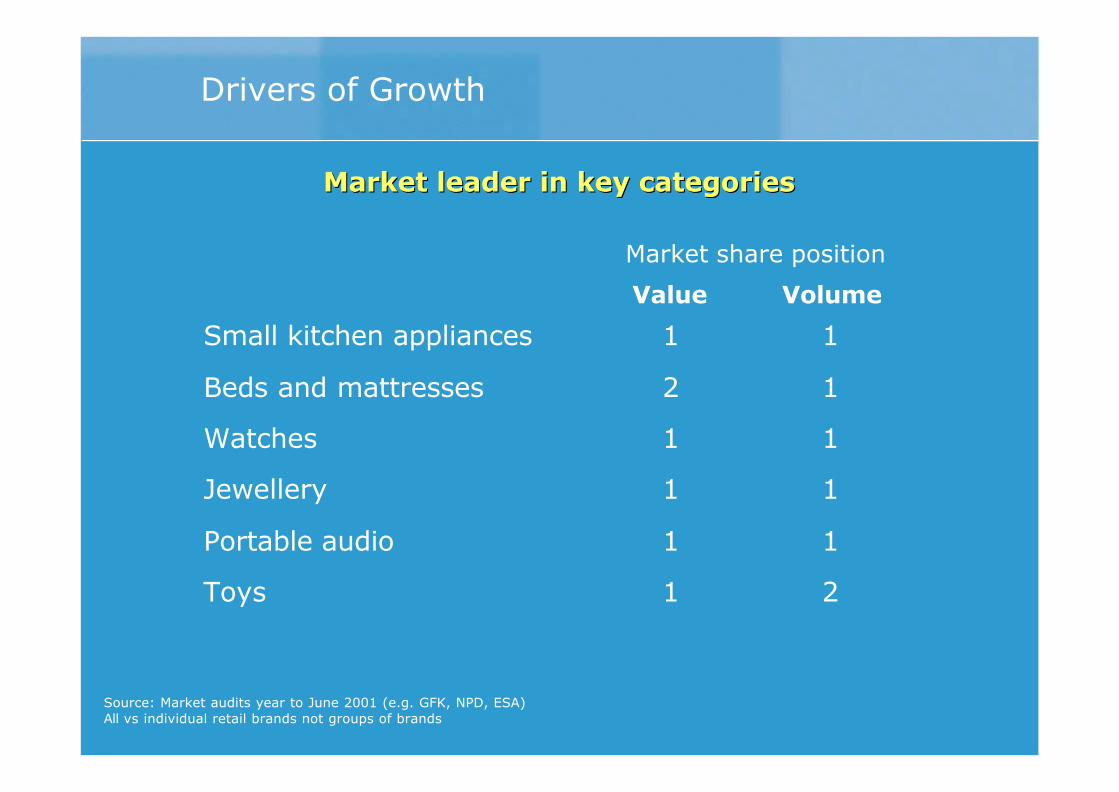

Value Volume

Small kitchen appliances 1 1

Beds and mattresses 2 1

Watches 1 1

Jewellery 1 1

Portable audio 1 1

Toys 1 2

Source: Market audits year to June 2001 (e.g. GFK, NPD, ESA)All vs individual retail brands not groups of brands

Market leader in key categoriesMarket leader in key categories

Market share position

Source: GFK, ONS, NPD, Argos (Year Ending 2000)

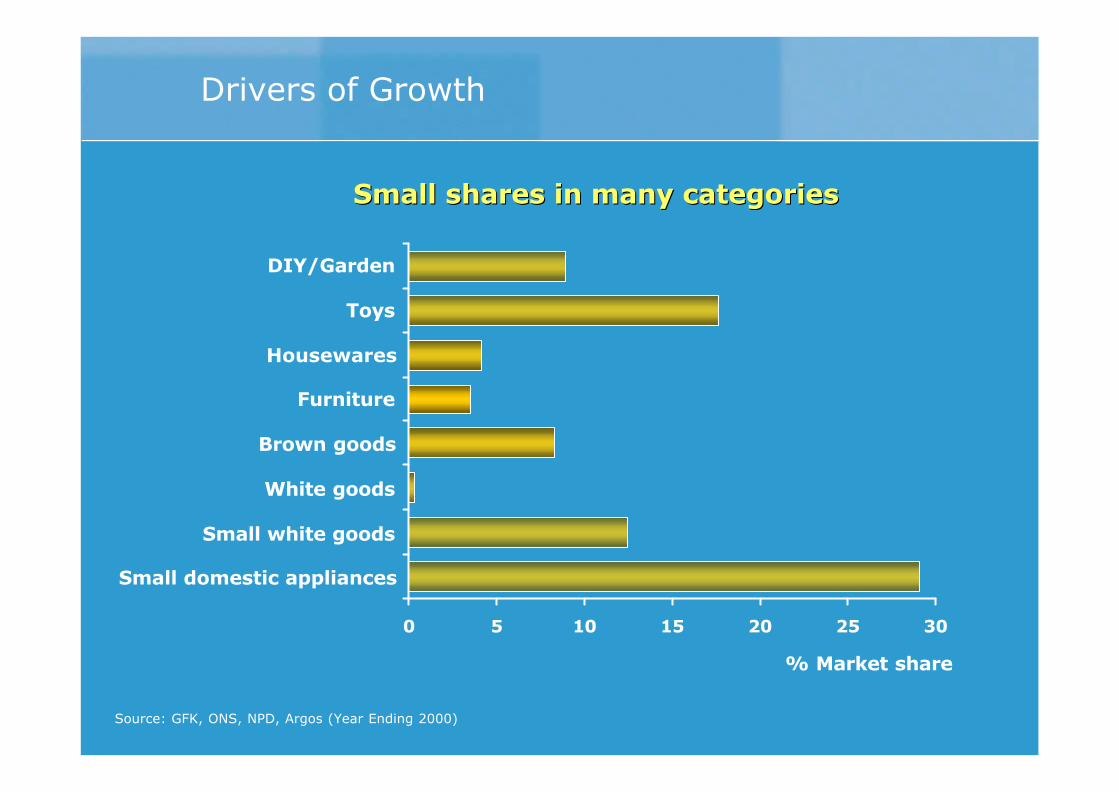

0 5 10 15 20 25 30

% Market share

DIY/Garden

Toys

Housewares

Furniture

Brown goods

White goods

Small white goods

Small domestic appliances

Drivers of Growth

Small shares in many categoriesSmall shares in many categories

Investment to improve the shopping experienceInvestment to improve the shopping experience

Drivers of Growth

July 99 - July 00- +/-June 00 June 01

Modern 77 79 +2

Cares about my needs 52 55 +3

Always has new ideas 50 52 +2

Changing for better 48 51 +3

Exciting 23 24 +1

Dull 15 15 -

Source: Core track October 2001

Drivers of Growth

Argos imagery - total agreement (all respondents)

Improved consumer perceptionImproved consumer perception

Serviceability %

7696 97 98 99 00 01*

78

80

82

84

86

88

90

Drivers of Growth

Serviceability has fallen as demand has risenServiceability has fallen as demand has risen

Serviceability is defined as value of sales as % of total sales demand

Year* Estimate

• 13 stores opened in last 12 months

• Easily exceeding IRR targets of 10% post tax

• Stand alone stores and multistore towns have exceeded

targets

• Fit out costs of these stores have fallen by over 20%

Drivers of Growth

Performance of new stores exceeded expectationsPerformance of new stores exceeded expectations

Argos Stores In Cambridge

0 0.5 1

miles

A1307

A1309

A11

34

A1303

A603

A1307

A11

34

A1303

A14Cambridge Retail ParkCambridge Retail ParkCambridge Retail ParkCambridge Retail ParkCambridge Retail ParkCambridge Retail ParkCambridge Retail ParkCambridge Retail ParkCambridge Retail Park

Cambridge city ctrCambridge city ctrCambridge city ctrCambridge city ctrCambridge city ctrCambridge city ctrCambridge city ctrCambridge city ctrCambridge city ctr

Cambridge Cambridge multistoremultistore towntown

• One mile

apart

• One store

sales = c.£6m

• Two stores

sales = c.£12m

Drivers of Growth

Cambridge city centre

Cambridge retail park

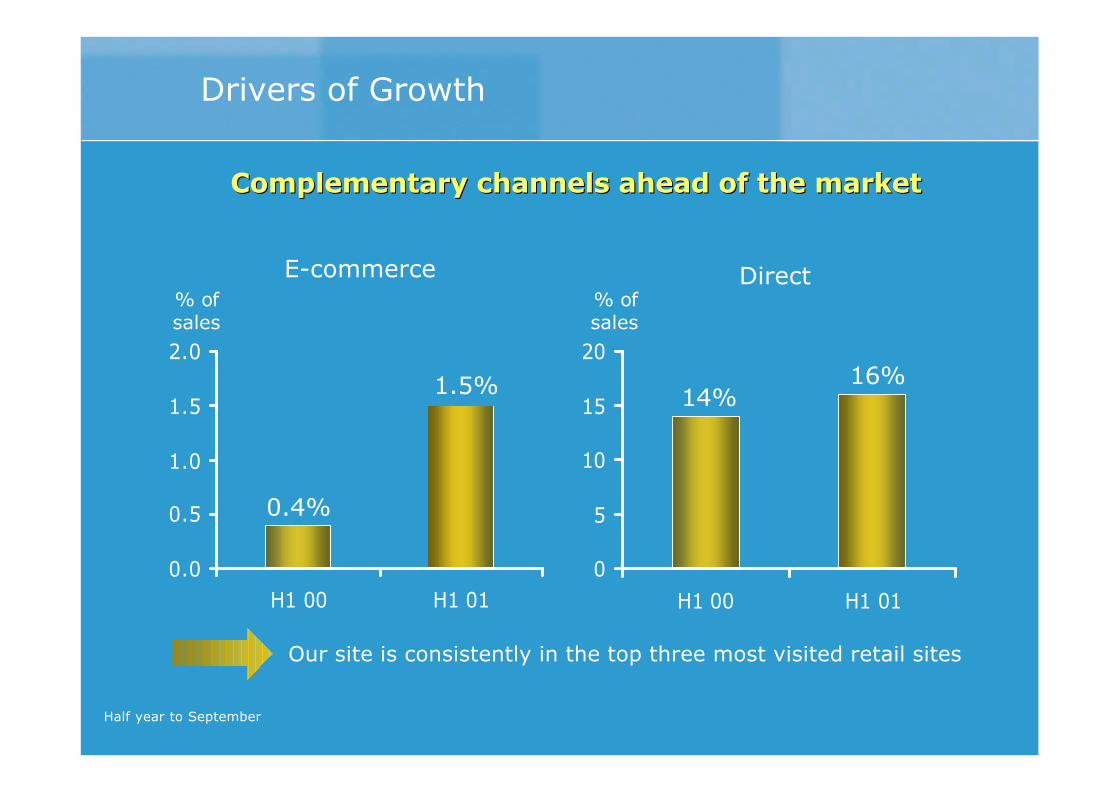

Complementary channels ahead of the marketComplementary channels ahead of the market

Our site is consistently in the top three most visited retail sites

Drivers of Growth

E-commerce Direct

0.0

0.5

1.0

1.5

2.0

H1 00 H1 010

5

10

15

20

H1 00 H1 01

0.4%

1.5% 14%16%

% ofsales

% ofsales

Half year to September

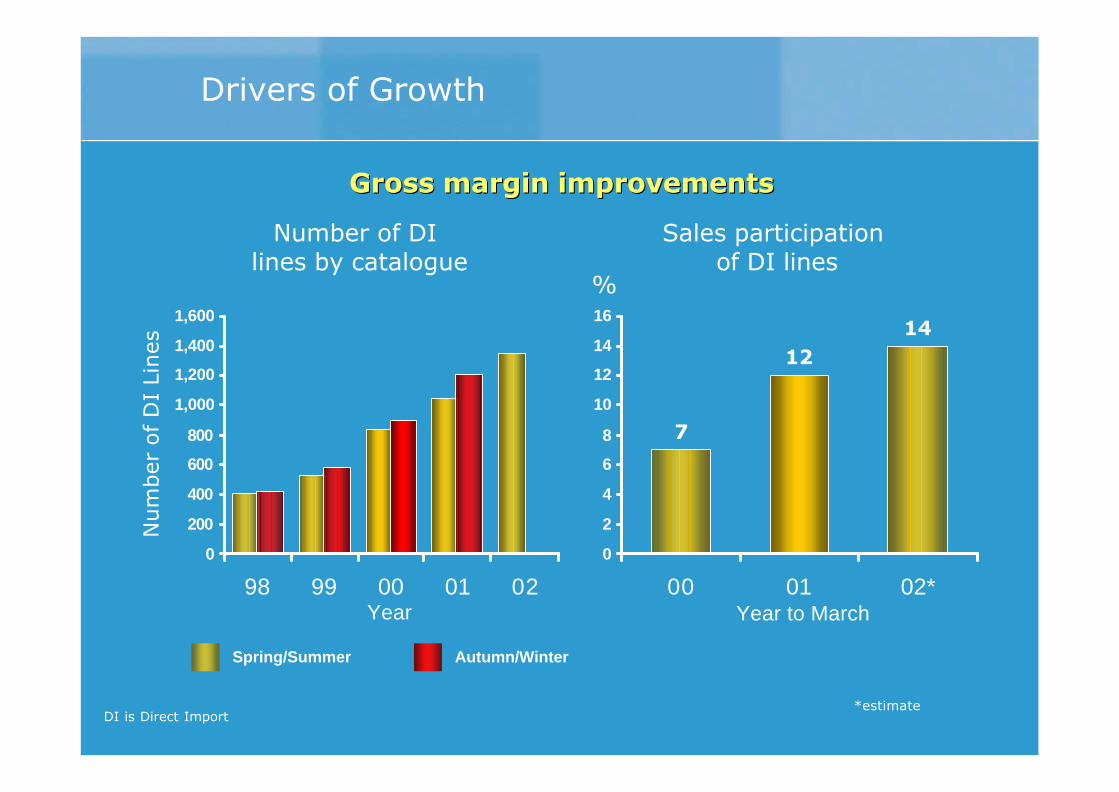

7

1214

0

2

4

6

8

10

12

14

16

00 01 02*

0

200

400

600

800

1,000

1,200

1,400

1,600

98 99 00 01 02Year

Drivers of Growth

Gross margin improvementsGross margin improvements

*estimateDI is Direct Import

Spring/Summer Autumn/Winter

Number of DI lines by catalogue

Num

ber

of D

I Li

nes

Sales participation of DI lines

%

Year to March

Agenda for Growth

Key opportunitiesKey opportunities

• Small shares

• More choice

• Invest in infrastructure

• Improve serviceability

• Broaden our franchise

• Enhance store convenience

• Develop convenience based channels

• Maintain strong value perception

Agenda for Growth

• Stores supply chain

• Argos Direct infrastructure and proposition

• New stores

• Improved in-store experience

• Extra range

Key initiativesKey initiatives