Embed Size (px)

Citation preview

1

Avoiding the Eye of the Storm-Lebanese Experience

Muhammad BaasiriVice-Governor

Banque du Liban

Ninth Annual International Seminar on Policy Challenges for the Financial SectorEmerging from the Crisis – Building a Stronger International Financial

System

Washington D.C., June 3-5, 2009

This presentation presents the sole view of the author

2

What made Lebanon avoid the eye of the storm?I- Introduction

While many banks in most countries of the worldwere significantly affected by the turmoil &governments & central banks were injecting hugeamounts of money to support their banking &financial systems, Lebanon was “bucking thetrend”:– No Cash injection by the central bank in the banking

system– Customers Deposits increased by 16% in 2008– Banks profits recorded a yearly growth of about 25% in

2008

3

What made Lebanon avoid the eye of the storm?II- Overview: Lebanese Banking System

(in bln of USD) (% to TA)

Assets Sep-08 Dec-08 Sep-08 Dec-08

Cash & Central Bank 25.1 27.0 25% 27%

Investment in TBs & Eurobonds 25.5 26.7 26% 26%

Due from Banks 15.1 15.6 15% 15%

Investment in Securities 3.5 2.7 4% 3%

Net Loans 23.7 24.1 24% 24%

Investment in Subsidiaries & Associates 3.1 3.1 3% 3%

Fixed Assets 1.0 1.0 1% 1%

Other Assets 1.5 1.4 2% 1%

Total Assets 98.5 101.6 100% 100%

4

What made Lebanon avoid the eye of the storm?II- Overview: Lebanese Banking System

Liabilities & Shareholders' EquitySep-08 Dec-08 Sep-08 Dec-08

Due to Central Bank 1.1 1.1 1% 1%

Due to Banks 7.5 7.8 8% 8%

Customers' deposits 77.1 80.2 78% 79%

Bonds Issued 0.1 0.1 0% 0%

Other Creditors 3.2 2.9 3% 3%

Subordinated loans 0.3 0.3 0% 0%

Revaluation Reserves 0.5 0.3 0% 0%

Shareholders' Equity 7.9 7.9 8% 8%

Net Income 0.9 1.1 1% 1%

Liabilities & Shareholders' Equity98.5 101.6 100% 100%

5

Funding Structure as of 31/12/2008

Customer deposits,

79%

Equity 8%Other 4% Banks 9%

Banks Customer deposits Equity Other

6

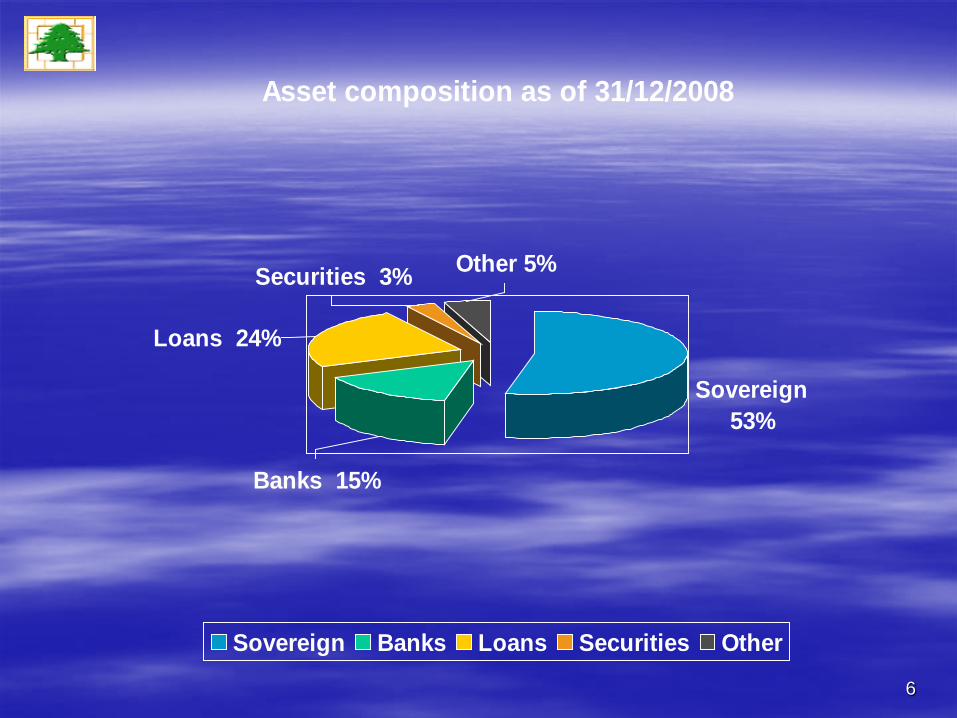

Asset composition as of 31/12/2008

Sovereign 53%

Other 5%

Banks 15%

Loans 24%

Securities 3%

Sovereign Banks Loans Securities Other

7

What made Lebanon avoid the eye of the storm?II- Overview: Lebanese Banking System

Traditional banking:– Stable Funding mainly customer deposits; negligible reliance on interbank

funding– High Sovereign (53% of TA)– Conservative Lending (24% of TA)– Relatively High Liquidity– Low Investment in Securities (3% of TA)

The latter was not a coincidence; It was triggered by the prudentialmeasures set by Banque du Liban (BDL) to ban risks.

Customers deposits > 3 times GDP (one of the highest ratios in theworld) which prompted strict prudential regulations.

8

What made Lebanon avoid the eye of the storm?III- Main reasons

Main Reasons can be divided into 4 categories:

A- Policies & Prudential Measures set by the BDL

B- Effective role of the Supervisory Authority

C- Confidence in the Banking System

D- Other Factors

9

What made Lebanon avoid the eye of the storm?III- reasons

A- Policies & Prudential Measures set by BDLi- Investment in financial instruments

Derivatives not allowed (BDL Circular July 2004)– Banks are prohibited from carrying out for their own accounts operations on

derivatives except for hedging purposes

Limits on investment in non resident debenture bonds (BDL Circular July 2004)– Sovereign: limited to G10 countries– Corporate Bonds: min rating: BBB– Max limit = Total up to 50% of bank equity, including:

Limits on investment in structured products (BDL Circular July 2004)– min rating A– capital guaranteed– Max limit = Total up to 25% of bank equity

Limits on Investment in stocks (Code of Money & Credit CMC Art. 153)– Banks Participations & investment in stocks & fixed assets for their own use in

addition to loans granted to related parties should not exceed bank equity

10

What made Lebanon avoid the eye of the storm?III- reasons

A- Policies & Prudential Measures by BDLii- Direct Investment in Real Estate

Banks are prohibited from investment in real estate except to acquiretheir premises (BDL Circular Nov. 1999)

The latter is also subject to BDL prior approval

Banks (even Islamic Banks which usually can carry out real estateactivities) are prohibited from financing directly or indirectly speculativeoperations in real estate (BDL Circular July 2008)

Real estate acquired in settlement of bad loans should be liquidatedwithin a maximum of 2 years (CMC Art. 154; BDL Circular Dec. 2000)

11

What made Lebanon avoid the eye of the storm?III- reasons

A- Policies & Prudential Measures by BDL

iii- Investment in loans

Loans against financial instruments (BDL CircularOctober 1998)– Limited to 50% of the portfolio– Margin call at 25% decline in the value of portfolio

Real Estate loans (BDL Circular July 2008)– Limited to 60% of real estate value / project value– Prohibited for speculation purposes

12

What made Lebanon avoid the eye of the storm?III- reasons

A- Policies & Prudential Measures by the Central Bank

iv- Issuance Structured Products & Derivatives (BDL Circular Dec. 1999)

Issuance & marketing of Structured Products & Derivatives is subject tothe prior approval of BDL unless it is targeted to be sold to less than 15clients (Other than banks & financial institutions)

Proper disclosure about the risks & returns of such products arereviewed by the regulator for customer protection

Banks’ guarantee of such products is limited to a total maximum of 7%of their equity

13

What made Lebanon avoid the eye of the storm?III- reasons

A- Policies & Prudential Measures by BDL

v- Adoption of Basel II

In April 1st 2006, BDL decided to adopt Basel II(Standardized Approach) effective 1/1/2008

This has boosted banks equity which increased by $1.4 bln(20%) since then

Capital Adequacy Ratio (CAR) Basel II is around 12%today (400 bp above the minimum 8%)

14

What made Lebanon avoid the eye of the storm?III- reasons

B- Effective Role of the Supervisory Authority

Banking Control Commission (BCC) played a very important rolethrough ensuring on an on-going basis banks’ compliance with theabove said policies & regulations

BCC off site supervision carried out on a monthly basis monitoring ofbanks’ financial statements & key indicators, and compliance withmajor laws & regulations

BCC on site supervision extends beyond review & assessment ofbanks internal systems, policies & procedures (including riskmanagement & internal control) to performing transaction tests (handson supervision) & review of a relatively big part of credit files

15

What made Lebanon avoid the eye of the storm?III- reasons

B- Effective Role of the Supervisory Authority

On going communication & meetings withbanks senior management

This ensured:– Better understanding of banks risk profile &

early capture of new risks– Adequate provisioning levels– Proper safe lending & sound investment

16

What made Lebanon avoid the eye of the storm?III- reasons

C- Confidence in the Lebanese Banking System

Experience in dealing with shocks: given its geography, history & frequentpolitical turbulence, Lebanon proved to be resilient to shocks (local & externalshocks) which bolstered the Confidence in the Lebanese banking system

Prudent monetary and banking policies including preventive measures and thestable parity of the exchange rate

Good track record in dealing with troubled banksBDL has been very keen about Systemic Risk, has taken appropriate measures to

avoid it :– Over the last two decades or so, several banks were merged, self liquidated at no

loss to depositors– BDL took over 2 banks & sold them later at a profit– BDL encouraged Mergers & Acquisitions through incentives including soft loans

17

What made Lebanon avoid the eye of the storm?III- reasons

D- Other factors

Limited exposure abroad– Major expansion abroad of Lebanese banks is recent (mainly in the

last 2 years) which limited the risks abroad– Non resident loans are relatively small (16% of total loans)– Loans to a single non resident client or a group of related non

resident clients are capped to a maximum of 10 – 20% of bankequity depending on the rating of the country where the loan isused (BDL Circular Nov. 2006)

Relatively high liquidity levels with stable deposit base(Resident, Lebanese expatriates & regional depositors)

Well capitalized banks (CAR around 12%)

18

What made Lebanon avoid the eye of the storm?IV- Lessons Learned

Strengthening prudential regulation & oversight withless reliance on market discipline that proved to beineffective in constraining risk taking especially outsidethe banking sector.

All-encompassed regulation: Oversight to cover allfinancial aspects including non banks like insurancecompanies, mutual funds…

Enhancement of cross border communication &cooperation .

Always remembering the basics of banking andbanking supervision without being mesmerized bycomplex and sometimes flawed mathematical formulasand models.

19

What made Lebanon avoid the eye of the storm?IV- Lessons Learned

Building capital buffer in good times, where profits arehigh & capital is more easily available, that in bad timescan help to offset procyclical pressures

Introducing capital charges for higher-than-averageliquidity risk

Improving risk management :“If you don’t understand it,don’t invest in it”. Investment in complex products shouldbe assessed very carefully internally avoiding full relianceon Credit Rating Agencies

Compensation schemes should focus on the level of risktaking rather than on only short term returns

20

THANK YOU