Embed Size (px)

Citation preview

Name of chairman

AUTUMN PRESS CONFERENCEOctober 18, 2007

2007 9 months sales conference call – October 2007 Name of chairman2

Disclaimer

This presentation contains forward looking statements which reflect Management’s current views and estimates. The forward looking statements involve certain risks and uncertainties that could cause actual results to differ materially from those contained in the forward looking statements. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

2 Name of chairmanAUTUMN PRESS CONFERENCE 2007

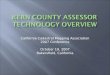

Key Figures

• Sales of CHF 78.7bn, up CHF 6.5bn (+9%)

• Above-target Organic Growth of 7.2%

• Real Internal Growth of 4.5%

• Food and Beverages: 6.8% Organic Growth

3 Name of chairmanAUTUMN PRESS CONFERENCE 2007

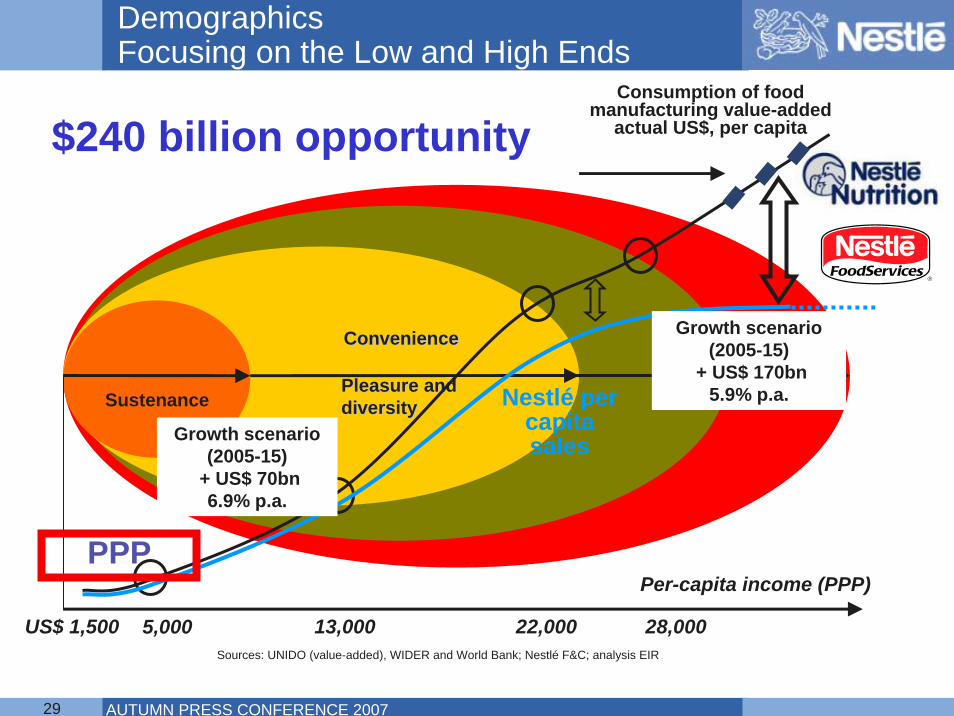

SustenancePleasure andPleasure anddiversitydiversity

ConvenienceConvenience

5,000 13,000 22,000

Per-capita income (PPP)

Consumption of food manufacturing value-added

actual US$, per capita

28,000

Nestlé per capita sales

Sources: UNIDO (value-added), WIDER and World Bank; Nestlé F&C; analysis EIR

Growth scenario (2005-15)

+ US$ 170bn5.9% p.a.

Growth scenario (2005-15)

+ US$ 70bn6.9% p.a.

Demographics Focusing on the Low and High Ends

US$ 1,500

PPP

$240 billion opportunity

4 Name of chairmanAUTUMN PRESS CONFERENCE 2007

P. Polman

5 Name of chairmanAUTUMN PRESS CONFERENCE 2007

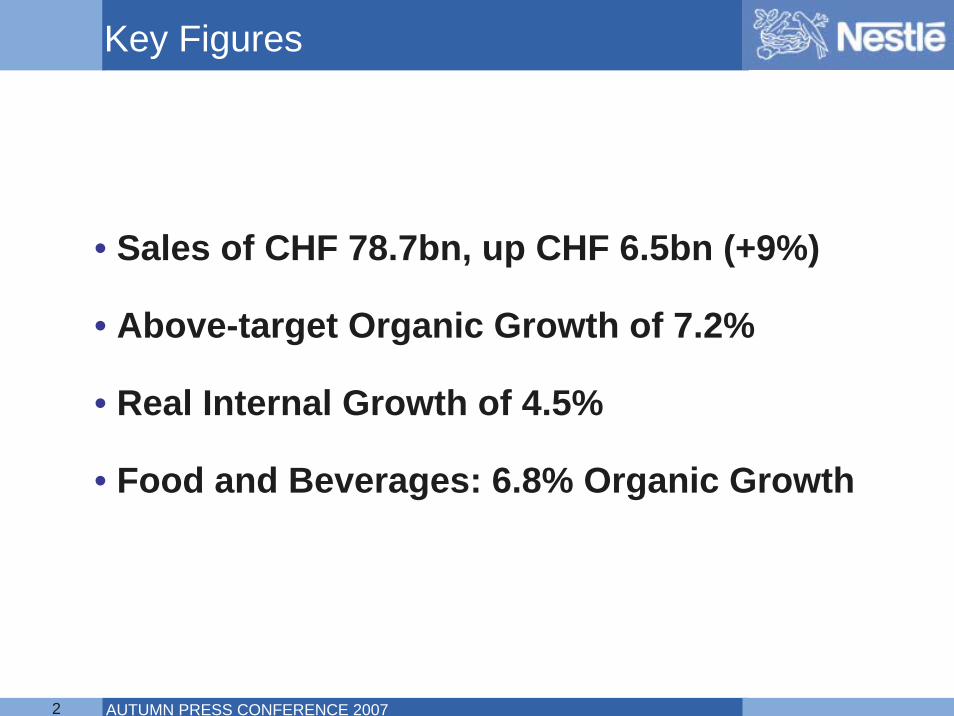

+ 0.9%+ 0.9%

+ 2.7%

+ 4.5%

CHF 78.7 bio

Acq. / Divest.Exchange

Rates

Pricing & others

RIG + 7.2%organicgrowth

+ 9.0%total

evolution

Total Group

+ 1.0%

+ 1.1%

+ 2.6%

+ 4.2%

CHF 73.2 bio

Acq. / Divest.

Pricing & others

RIG + 6.8%organicgrowth

+ 8.9%total

evolution

Food & Beverage

Exchange Rates

9 months sales 2007: Organic growth of 7.2%9 months sales 2007: Organic growth of 7.2%

6 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Strong organic growth - highlights

• Organic growth of 7.2%

• Food and Beverage delivers 6.8% organic growth – strong performances in most areas

• Total sales increase 9% to CHF 78.7 billion

• Raw material costs up sharply, particularly agricultural

• Full Year targets reconfirmed:approaching 7% organic growthimprovement in constant currency EBIT margin

• Creation of Nestlé Professional – a global foodservices business

7 Name of chairmanAUTUMN PRESS CONFERENCE 2007

-5

0

5

10

15

20

25

30

35

40

OG % Jan-Sep 2007

BAB's:

Food & Beverage Billionaire Brands Organic Growth

Average market growth

8 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Organic Growth by product groupPharmaceutical products

PharmaSales : 5.5 CHF bio

RIG : +9.2%OG : +10.3%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

9 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Organic Growth by product groupNestlé Nutrition

Nestlé NutritionSales : 5.7 CHF bio

RIG : +6.6%OG : +9.7%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

Nestlé Nutrition

10 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Organic Growth by product groupNestlé Waters

Nestlé WatersSales : 8.2 CHF bio

RIG : +5.4%OG : +6.9%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

Nestlé Nutrition

Nestlé Waters

11 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Organic Growth by product groupConfectionery

ConfectionerySales : 8.4 CHF bio

RIG : +2.6%OG : +5.4%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

Nestlé Nutrition

Nestlé Waters

Confectionery

12 Name of chairmanAUTUMN PRESS CONFERENCE 2007

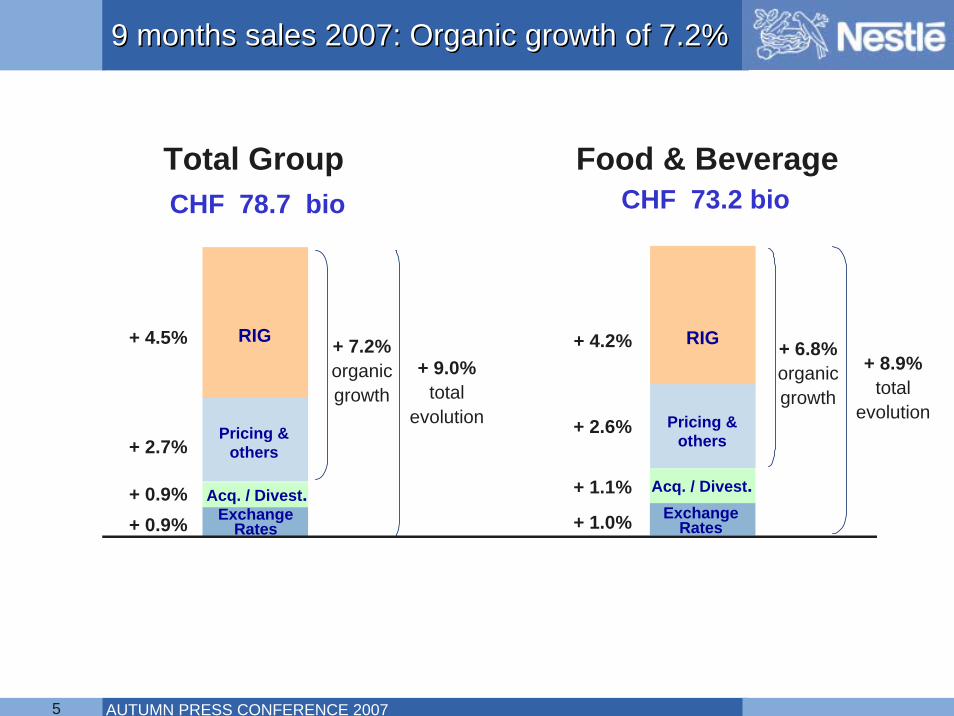

Organic Growth by product groupPetCare

PetCareSales : 9.0 CHF bio

RIG : +4.1%OG : +7.1%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

Nestlé Nutrition

Nestlé Waters

Confectionery

PetCare

13 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Organic Growth by product groupPowdered & Liquid Beverages

Powdered & Liquid BeveragesSales : 12.8 CHF bio

RIG : +7.5%OG : +10.0%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

Nestlé Nutrition

Nestlé Waters

Confectionery

PetCare

Powdered & Liquid Beverages

14 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Leveraging our expertise across lifestages

15 Name of chairmanAUTUMN PRESS CONFERENCE 2007

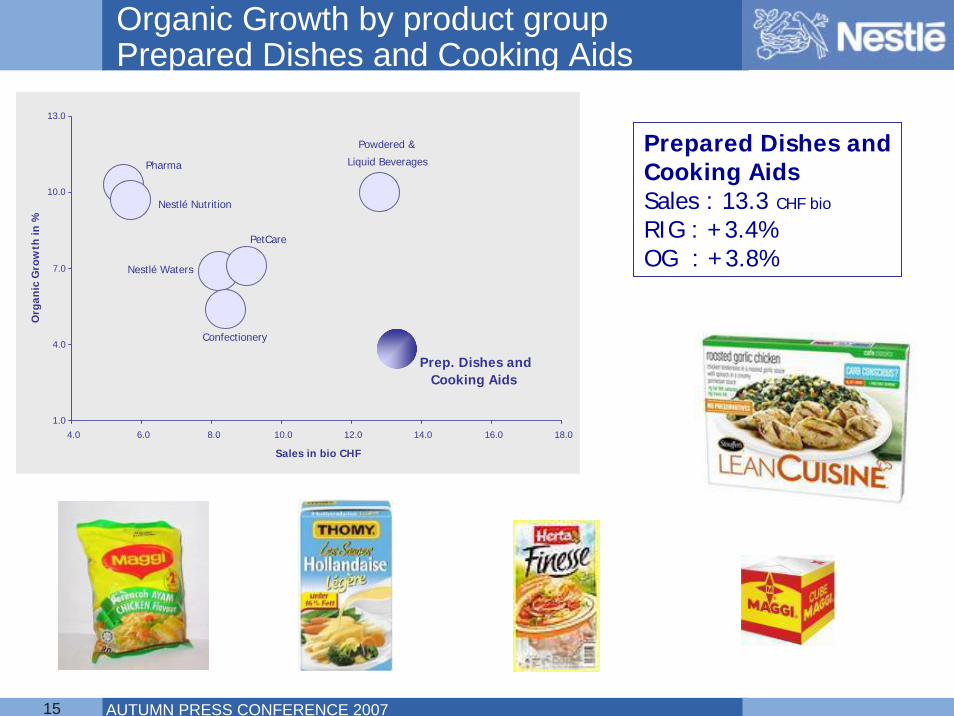

Organic Growth by product groupPrepared Dishes and Cooking Aids

Prepared Dishes andCooking AidsSales : 13.3 CHF bio

RIG : +3.4%OG : +3.8%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

Nestlé Nutrition

Nestlé Waters

Confectionery

PetCare

Powdered &

Liquid Beverages

Prep. Dishes and Cooking Aids

16 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Organic Growth by product groupDairy (incl. Ice Cream)

Dairy (incl. IC)Sales : 15.7 CHF bio

RIG : +1.8%OG : +6.5%

Pharma

1.0

4.0

7.0

10.0

13.0

4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

Sales in bio CHF

Org

anic

Gro

wth

in %

Nestlé Nutrition

Nestlé Waters

Confectionery

PetCare

Powdered &

Liquid Beverages

Prep. Dishes and

Cooking Aids

Dairy

17 Name of chairmanAUTUMN PRESS CONFERENCE 2007

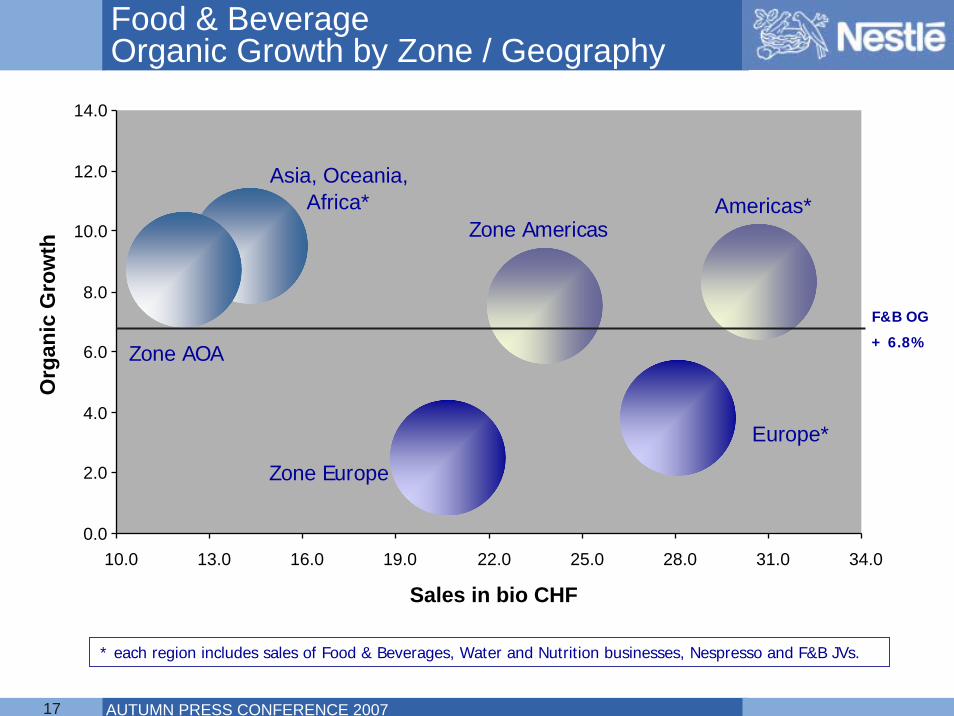

Food & BeverageOrganic Growth by Zone / Geography

* each region includes sales of Food & Beverages, Water and Nutrition businesses, Nespresso and F&B JVs.

F&B OG

+ 6.8%

Europe*

Asia, Oceania, Africa*

Zone Europe

Zone AOA

Americas*Zone Americas

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

10.0 13.0 16.0 19.0 22.0 25.0 28.0 31.0 34.0

Sales in bio CHF

Org

anic

Gro

wth

18 Name of chairmanAUTUMN PRESS CONFERENCE 2007

2005 2006 2007 2008

Nestlé on its way towards Nutrition, Health and Wellness

CHF 5 bio CHF 10 bio

Jenny Craig (Aug) NMN (July)Gerber (Sept)

Proteika (April)Musashi (Nov)

Leverage recent acquisitions and Extend our leadership by becoming the most innovative personalised Nutrition Company

19 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Agricultural commodities prices continue to trend higher

20 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Conclusion The Nestlé Model reconfirmed

• Outlook unchanged from Half Year

• The Nestlé Model reconfirmed for 2007

• Raw material environment tough – as expected

• Organic growth to approach 7%

• Improvement in constant currency EBIT margin

21 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Nutrition, Health & Wellness the driver ofNutrition, Health & Wellness the driver ofgrowth and profitabilitygrowth and profitability

The Nestlé Model

5-6% organic growth Sustainable improvement in EBIT

Improving trend in Return on Invested Capital

22 Name of chairmanAUTUMN PRESS CONFERENCE 2007

23 Name of chairmanAUTUMN PRESS CONFERENCE 2007

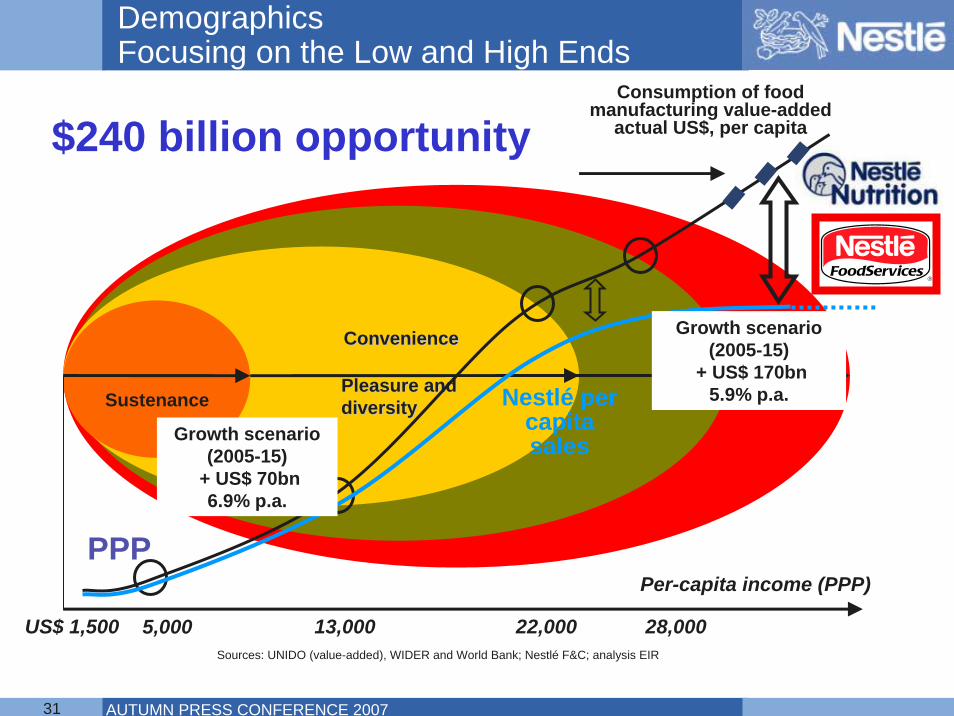

SustenancePleasure andPleasure anddiversitydiversity

ConvenienceConvenience

5,000 13,000 22,000

Per-capita income (PPP)

Consumption of food manufacturing value-added

actual US$, per capita

28,000

Nestlé per capita sales

Sources: UNIDO (value-added), WIDER and World Bank; Nestlé F&C; analysis EIR

Growth scenario (2005-15)

+ US$ 170bn5.9% p.a.

Growth scenario (2005-15)

+ US$ 70bn6.9% p.a.

Demographics Focusing on the Low and High Ends

US$ 1,500

PPP

$240 billion opportunity

24 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Global Presence in HealthCare Nutrition

HealthCare Nutrition – Facts & FiguresSales in billion CHF: 1.7Markets: 30Employees: ~ 2'500

25 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Conditions for Success

• Strong R&D

• Specialized marketing capabilities

• Capacity to distribute through all channels

26 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Delivering Excellence to Babies

• Gerber founded in 1928 with mission to help parents raise happy, healthy babies

• Heritage of product innovation

• Recognized leader in developing cutting-edge science on infant and toddler feeding

Dorothy S. Gerber

27 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Our Consumers

Performance Nutrition

Energy bars, specialty liquids,

proteins and training nutrition

Weight ManagementPersonalized

weight management

programs

HealthCare NutritionEnteral and oral nutrition

for Critical Care, diabesity, cancer,

pediatric and elderly patients

Infant NutritionInfant formulas,

pediatric specialties, infant cereals,

meals and drinks,Baby Care

28 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Our Business

Nestlé NutritionBusiness Units: 4

Employees: 20'000

Office locations: 12

Factories: 30

Technical centres: 5

29 Name of chairmanAUTUMN PRESS CONFERENCE 2007

SustenancePleasure andPleasure anddiversitydiversity

ConvenienceConvenience

5,000 13,000 22,000

Per-capita income (PPP)

Consumption of food manufacturing value-added

actual US$, per capita

28,000

Nestlé per capita sales

Sources: UNIDO (value-added), WIDER and World Bank; Nestlé F&C; analysis EIR

Growth scenario (2005-15)

+ US$ 170bn5.9% p.a.

Growth scenario (2005-15)

+ US$ 70bn6.9% p.a.

Demographics Focusing on the Low and High Ends

US$ 1,500

PPP

$240 billion opportunity

30 Name of chairmanAUTUMN PRESS CONFERENCE 2007

PPP Examples

South Africa

Thailand

31 Name of chairmanAUTUMN PRESS CONFERENCE 2007

SustenancePleasure andPleasure anddiversitydiversity

ConvenienceConvenience

5,000 13,000 22,000

Per-capita income (PPP)

Consumption of food manufacturing value-added

actual US$, per capita

28,000

Nestlé per capita sales

Sources: UNIDO (value-added), WIDER and World Bank; Nestlé F&C; analysis EIR

Growth scenario (2005-15)

+ US$ 170bn5.9% p.a.

Growth scenario (2005-15)

+ US$ 70bn6.9% p.a.

Demographics Focusing on the Low and High Ends

US$ 1,500

PPP

$240 billion opportunity

32 Name of chairmanAUTUMN PRESS CONFERENCE 2007

What is Foodservice?

• We talk of foodservice every time that food or beverage is purchased and consumed away from home

• The consumption is in most cases immediate and on the spot

• Operators: restaurants, cafés, convenience stores, pubs, canteens, hospitals, schools, vending

33 Name of chairmanAUTUMN PRESS CONFERENCE 2007

• Due to shifts in demographics, socio-economic factors and consumer behaviour, foodservice represents an increasingly important consumer option

• Consumption varies from market to market, but consumer demand for convenience, taste and nutrition is driving foodservice growth in all markets

• The OOH spending today accounts for 30-50% of total consumer food and beverage purchases in mature economies

• The trend is a further and long term growth in OOH consumption

A Growing Trend

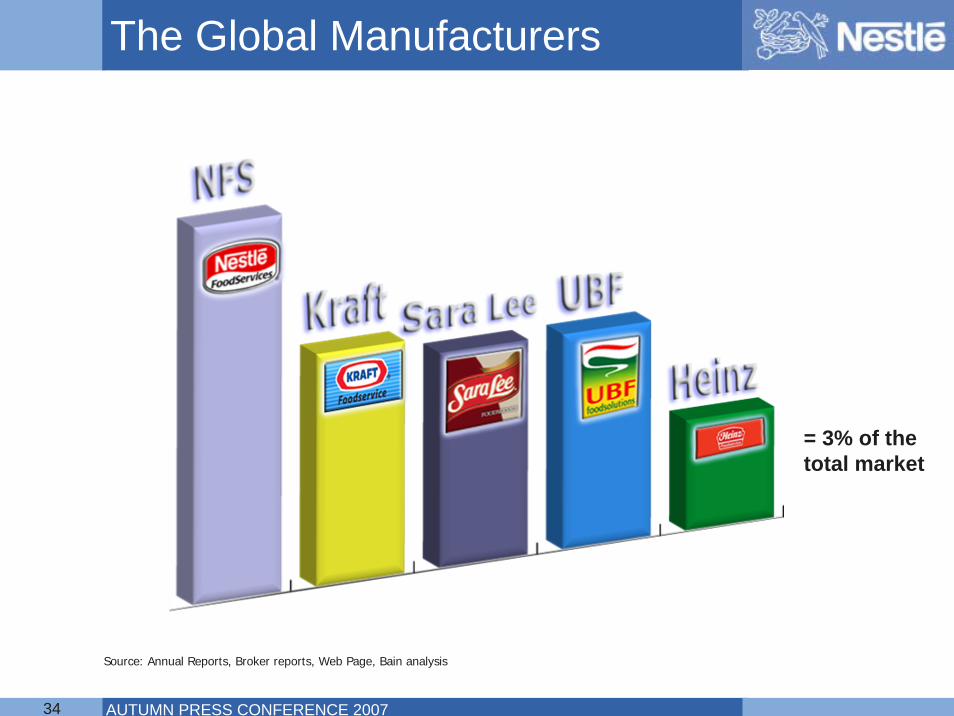

34 Name of chairmanAUTUMN PRESS CONFERENCE 2007

The Global Manufacturers

Source: Annual Reports, Broker reports, Web Page, Bain analysis

= 3% of the total market

35 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Two Key Priorities

"The Global leader in branded hot and cold non-carbonated

Beverage solutions"

"Be the Local and Regionalleader in strategic Food

product solutions"

36 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Nestlé Professional

37 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Nescafé Dolce Gusto

38 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Nescafé Dolce Gusto

39 Name of chairmanAUTUMN PRESS CONFERENCE 2007

0 1 2 3 4 5 6 7 8 9 10

Quick to prepare

Easy to use

Easy to clean

Made by well-known brand

Suitable for everyday use

Attractive design

Great taste/superior quality

Cream/foam

Each person his choice

Wide range

9.6

9.6

9.5

9.4

9.3

9.2

9.1

9.1

8.3

7.3

Consumer Feedback

40 Name of chairmanAUTUMN PRESS CONFERENCE 2007

• France

• Spain

• Italy

• Portugal

• Austria

• Czech-Slovak

• Japan (test 800 -7/11 stores)

Launch Wave 2

41 Name of chairmanAUTUMN PRESS CONFERENCE 2007

2 Welcome Pack Executions

Germany/France/CH/Austria/UK/Czech/Slovakia

Spain/Portugal/Italy

Nescafé Dolce Gusto

42 Name of chairmanAUTUMN PRESS CONFERENCE 2007

1 European Packaging Solution

• 16 capsules per box• 8 languages

Nescafé Dolce Gusto

43 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Same Demo Material

Nescafé Dolce Gusto

44 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Same POS Material

Nescafé Dolce Gusto

45 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Innovation Capsules

46 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Innovation Capsules

47 Name of chairmanAUTUMN PRESS CONFERENCE 2007

48 Name of chairmanAUTUMN PRESS CONFERENCE 2007

Next Media Events

21 February 2008 – Spring Press Conference 10 April 2008 – Annual General Meeting21 April 2008 – First Quarter Sales

7 August 2008 – Half-Year Results23 October 2008 – Autumn Press Conference