Embed Size (px)

Citation preview

Automated Underwriting:Threat or Opportunity?Jason Bowman, Head of Accelerated Underwriting, NA

Dan Drabik, Senior Magnum Consultant

Introduction

Ever feel overwhelmed by the pace of change?

3

The pace of change

1997 High End Desktop 2012 Smartphone DifferentialProcessor 266 MHz 1.5 GHz 10x fasterMemory 32 MB 1.5 GB 48x moreStorage 4.3 GB 32 GB 8x more

Cost $2,800 $600 Fifth of priceWeight 25-30 pounds 5 ounces 1% of weight

iPad adoptionhit 20 milliondevices in just15 months

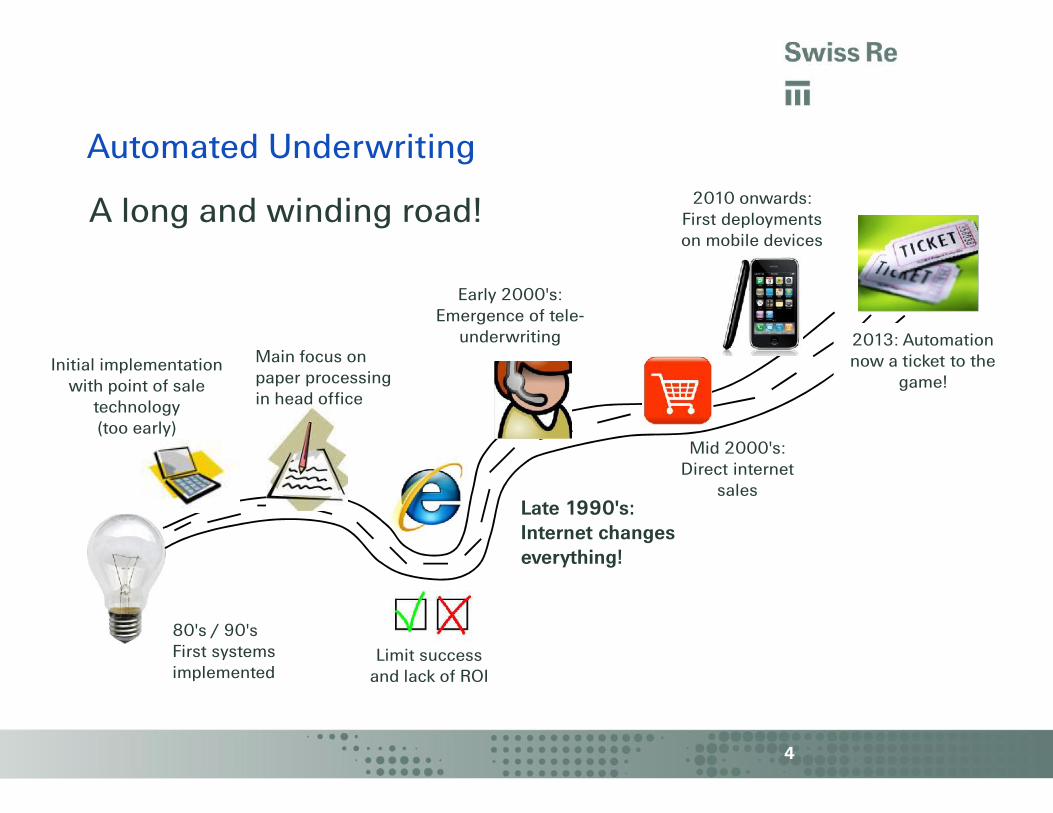

Limit successand lack of ROI

Late 1990's:Internet changeseverything!

4

Automated Underwriting

A long and winding road!

80's / 90'sFirst systemsimplemented

Initial implementationwith point of sale

technology(too early)

Main focus onpaper processingin head office

Early 2000's:Emergence of tele-

underwriting 2013: Automationnow a ticket to the

game!

2010 onwards:First deploymentson mobile devices

Mid 2000's:Direct internet

sales

5

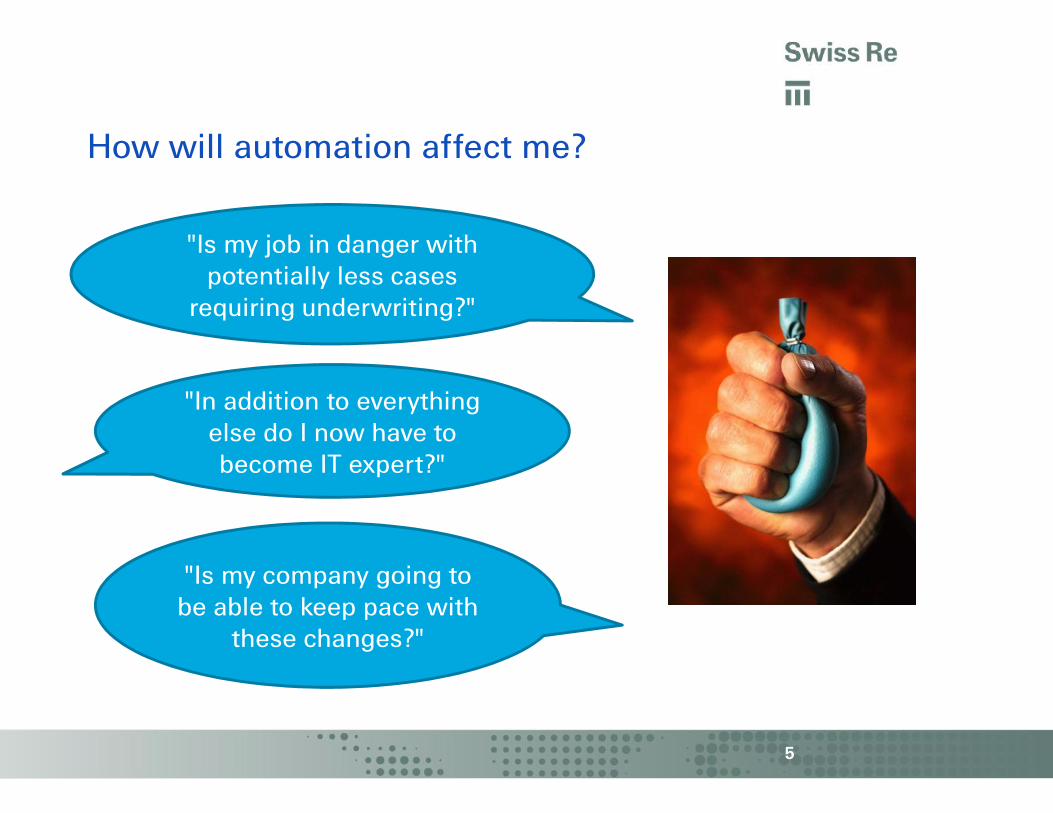

How will automation affect me?

"Is my job in danger withpotentially less cases

requiring underwriting?"

"In addition to everythingelse do I now have tobecome IT expert?"

"Is my company going tobe able to keep pace with

these changes?"

The market perspective

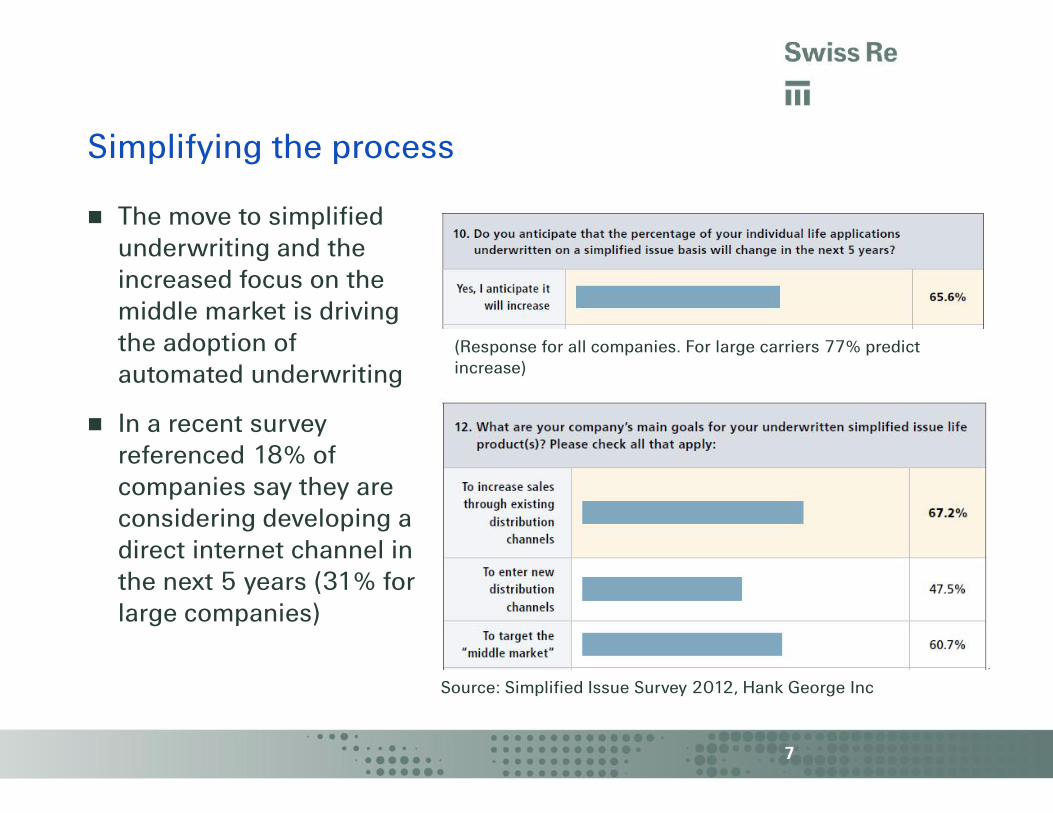

The move to simplifiedunderwriting and theincreased focus on themiddle market is drivingthe adoption ofautomated underwriting

In a recent surveyreferenced 18% ofcompanies say they areconsidering developing adirect internet channel inthe next 5 years (31% forlarge companies)

7

Simplifying the process

Source: Simplified Issue Survey 2012, Hank George Inc

(Response for all companies. For large carriers 77% predictincrease)

8

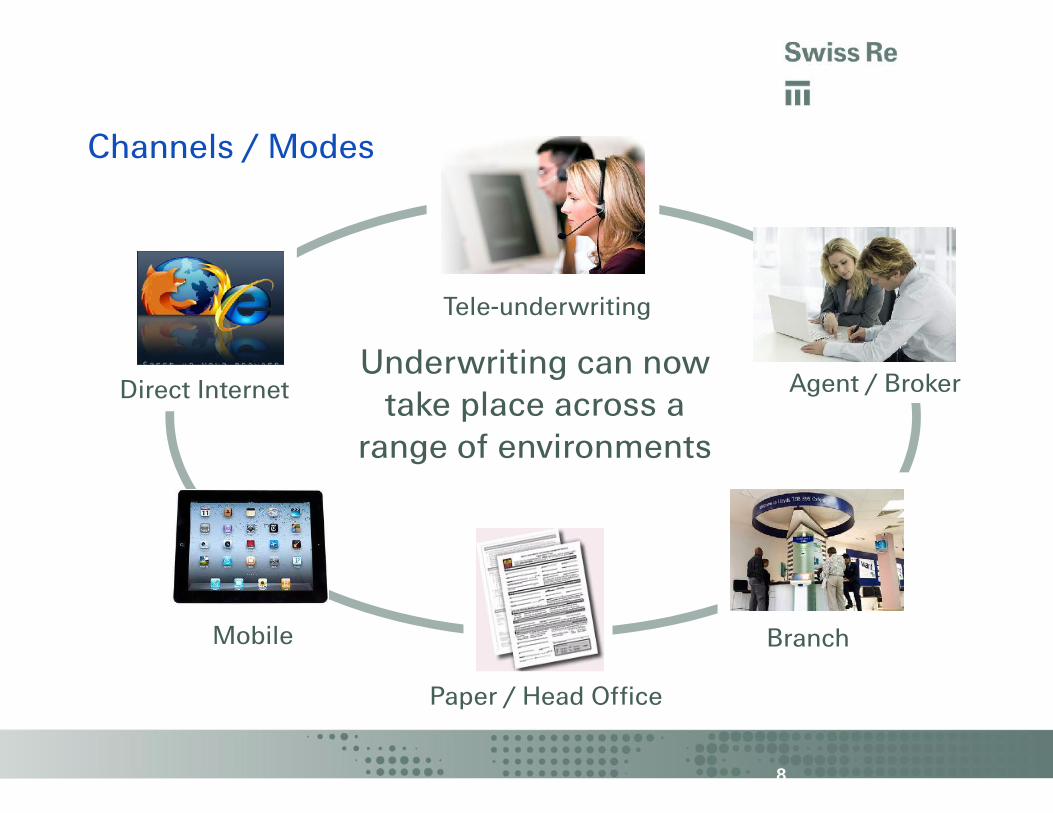

Channels / Modes

Underwriting can nowtake place across a

range of environments

Direct Internet

Paper / Head Office

Branch

Tele-underwriting

Mobile

Agent / Broker

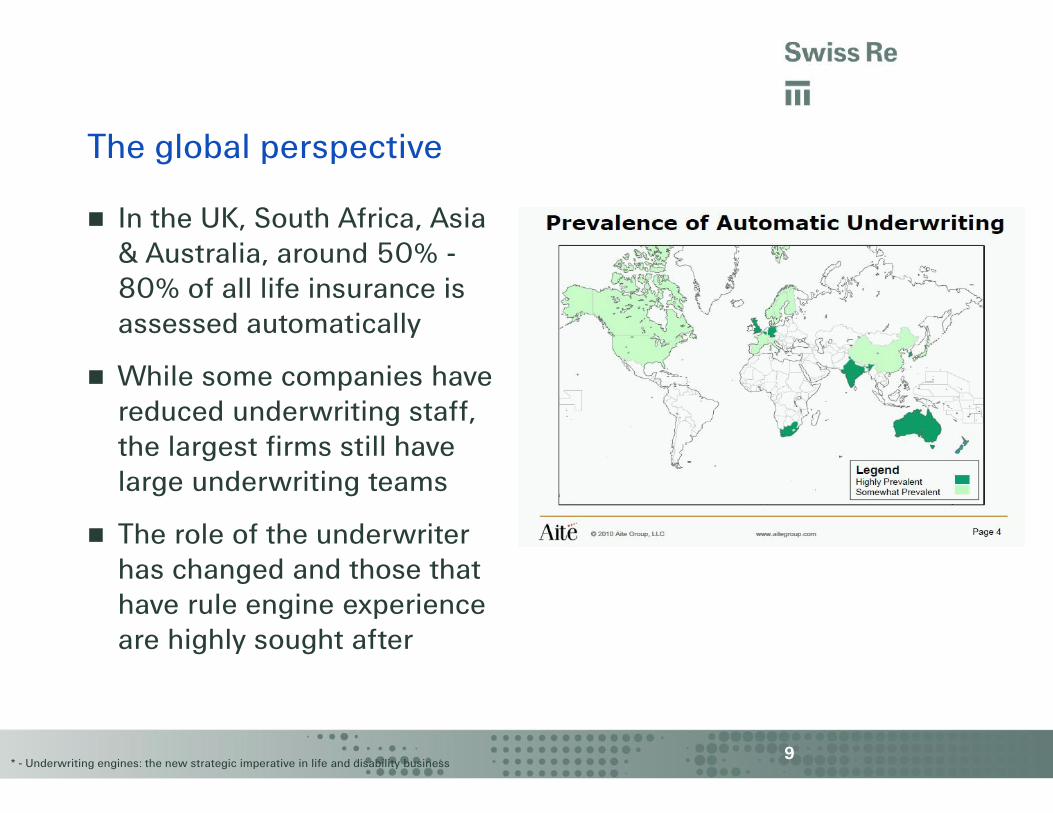

In the UK, South Africa, Asia& Australia, around 50% -80% of all life insurance isassessed automatically

While some companies havereduced underwriting staff,the largest firms still havelarge underwriting teams

The role of the underwriterhas changed and those thathave rule engine experienceare highly sought after

9

The global perspective

* - Underwriting engines: the new strategic imperative in life and disability business

10

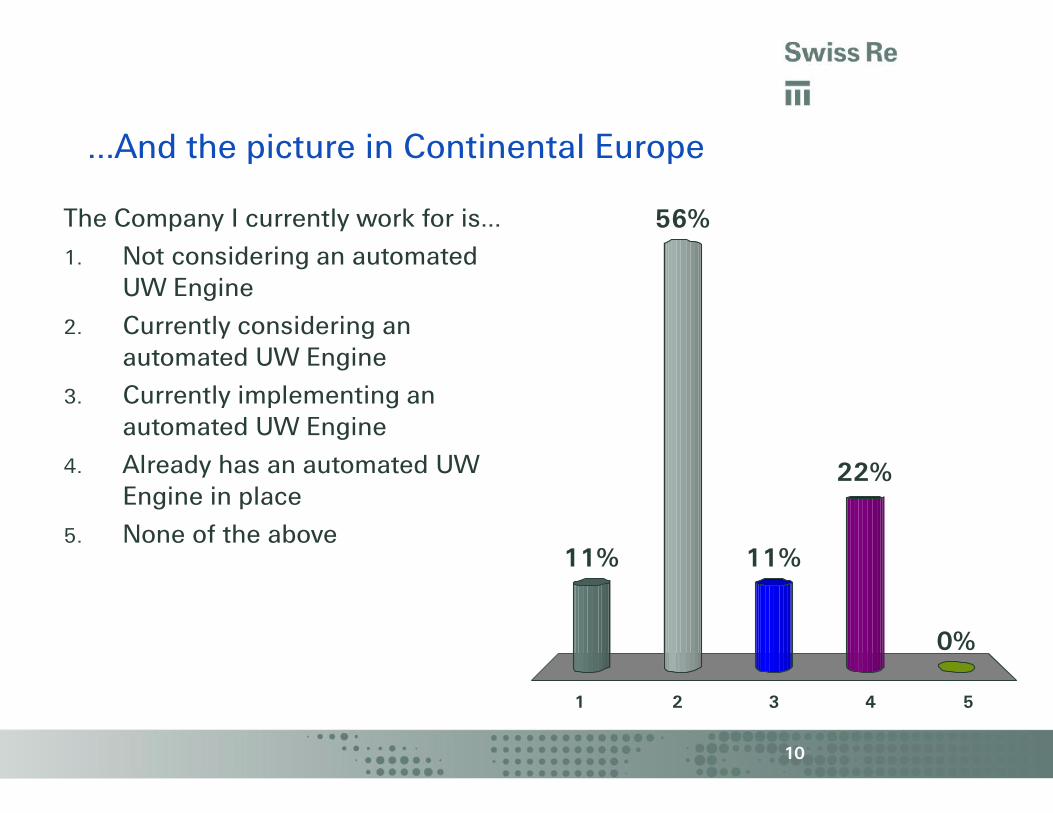

…And the picture in Continental Europe

1 2 3 4 5

11%

56%

0%

22%

11%

The Company I currently work for is…1. Not considering an automated

UW Engine2. Currently considering an

automated UW Engine3. Currently implementing an

automated UW Engine4. Already has an automated UW

Engine in place5. None of the above

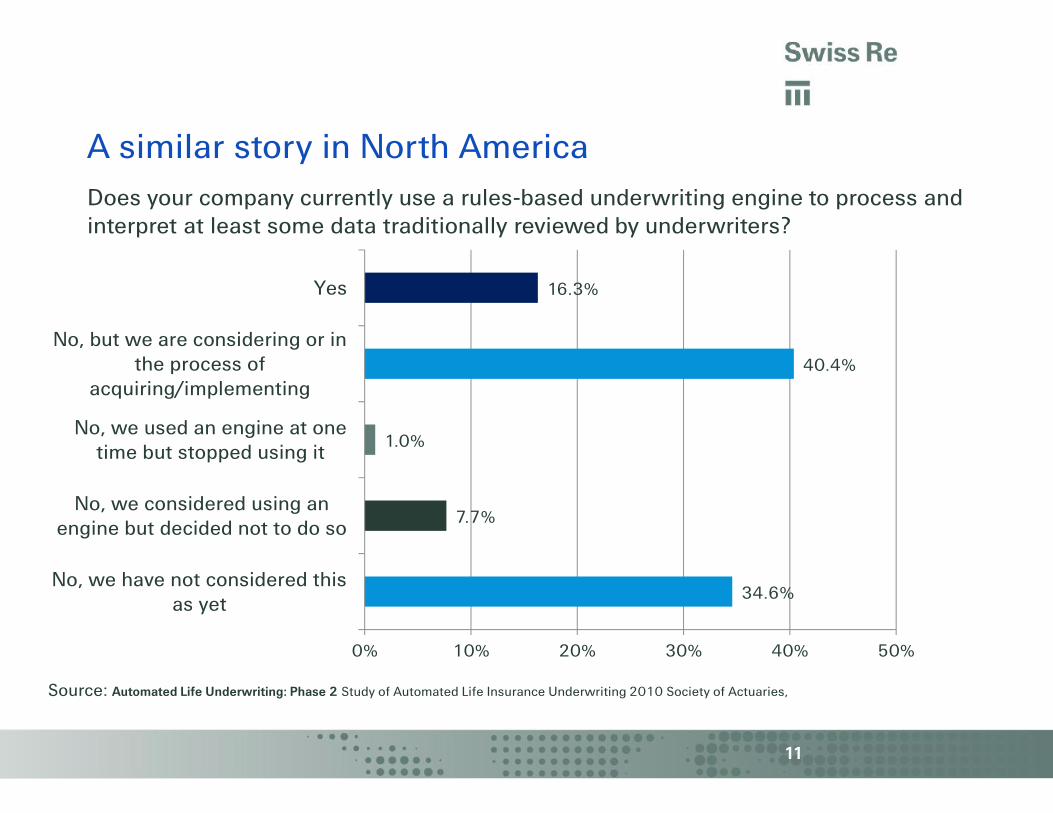

Does your company currently use a rules-based underwriting engine to process andinterpret at least some data traditionally reviewed by underwriters?

11

A similar story in North America

34.6%

7.7%

1.0%

40.4%

16.3%

0% 10% 20% 30% 40% 50%

No, we have not considered thisas yet

No, we considered using anengine but decided not to do so

No, we used an engine at onetime but stopped using it

No, but we are considering or inthe process of

acquiring/implementing

Yes

Source: Automated Life Underwriting: Phase 2 Study of Automated Life Insurance Underwriting 2010 Society of Actuaries,

The "new" underwriter

Some common reasons underwriters have negative perceptionsabout engine-based underwriting

Fear of the impact on job security

Pushback from some advisers

Not being comfortable defending engine decisions

Underwriting is a science and an art (no longer true?)

13

Underwriter objections to automation

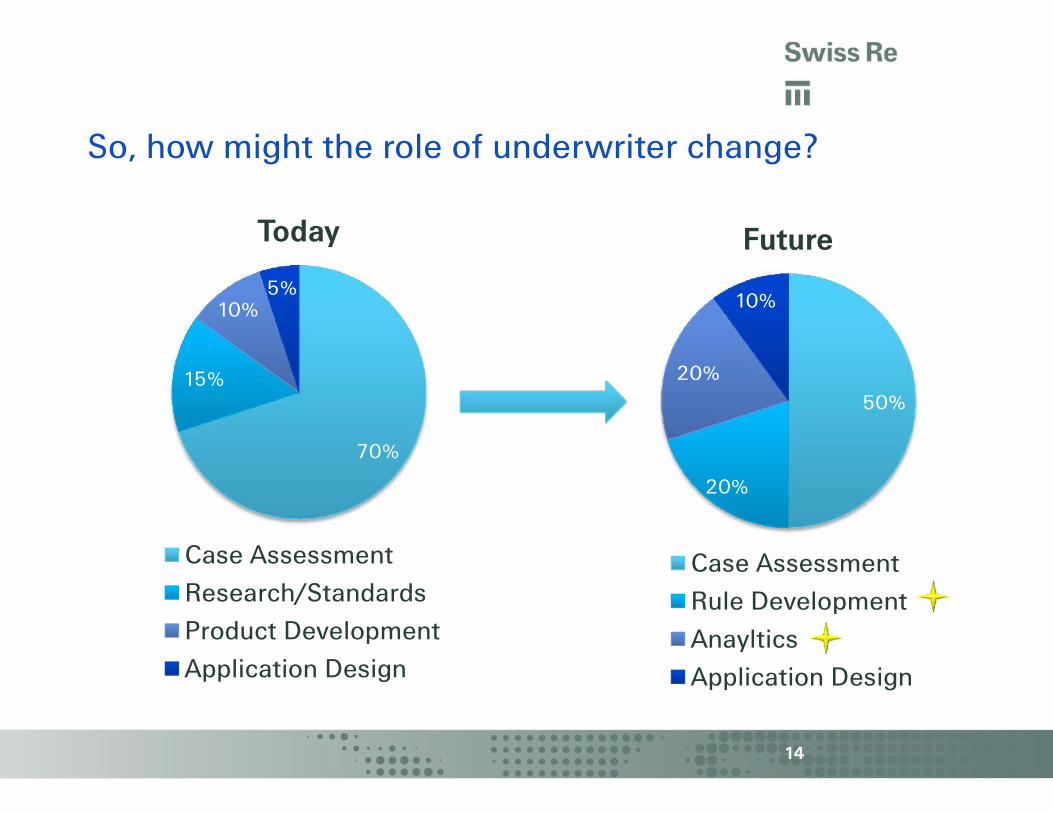

70%

15%

10%5%

Today

Case AssessmentResearch/StandardsProduct DevelopmentApplication Design

14

So, how might the role of underwriter change?

50%

20%

20%

10%

Future

Case AssessmentRule DevelopmentAnaylticsApplication Design

//SMITH1 JOB 1,LEO,MSGCLASS=X // EXEC PGM=IEFBR14 //NEWDS DDDSN=SMITH.LIB.CNTL,DISP=(NEW,CATLG),VOL=SER=WORK02, //UNIT=3390,SPACE=(CYL,(3,1,25) //OLDDS DD D

//ADDPROC1 JOB 1,SMCHUGH,MSGCLASS=X // EXEC PGM=IEBUPDTE//SYSPRINT DD SYSOUT=* //SYSUT1 DD DISP=OLD,DSN=MY.PROCLIB//SYSUT2 DD DISP=OLD,DSN=MY.PROCLIB //SYSIN DD DATA ./ ADDLIST=ALL,NAME=MYJOB1 //STEP1 EXEC=SUZNX1 //PRINT DD SYSOUT=A// (more JCL for MYJOB1) //SYSUDUMP DD SYSOUT=* (last JCL forMYJOB1) ./ REPL LIST=ALL,NAME=LASTJOB //LIST EXEC PGM=SUZNLIST// (more JCL for this procedure) //* LAST JCL STATEMENT FOR LASTJOB ./ENDUP /*SN=SMITH.OLD.DATA,DISP=(OLD,DELETE)

//SMITH2 JOB 1,GEOFF,MSGCLASS=X // EXEC PGM=IEBGENER //SYSINDD DUMMY //SYSPRINT DD SYSOUT=X //SYSUT1 DDDISP=SHR,DSN=SMITH.SEQ.DATA //SYSUT2 DDDISP=(NEW,CATLG),DSN=SMITH.COPY.DATA,UNIT=3390, //VOL=SER=WORK02,SPACE=(TRK,3,3))

15

Rule development – the old way!

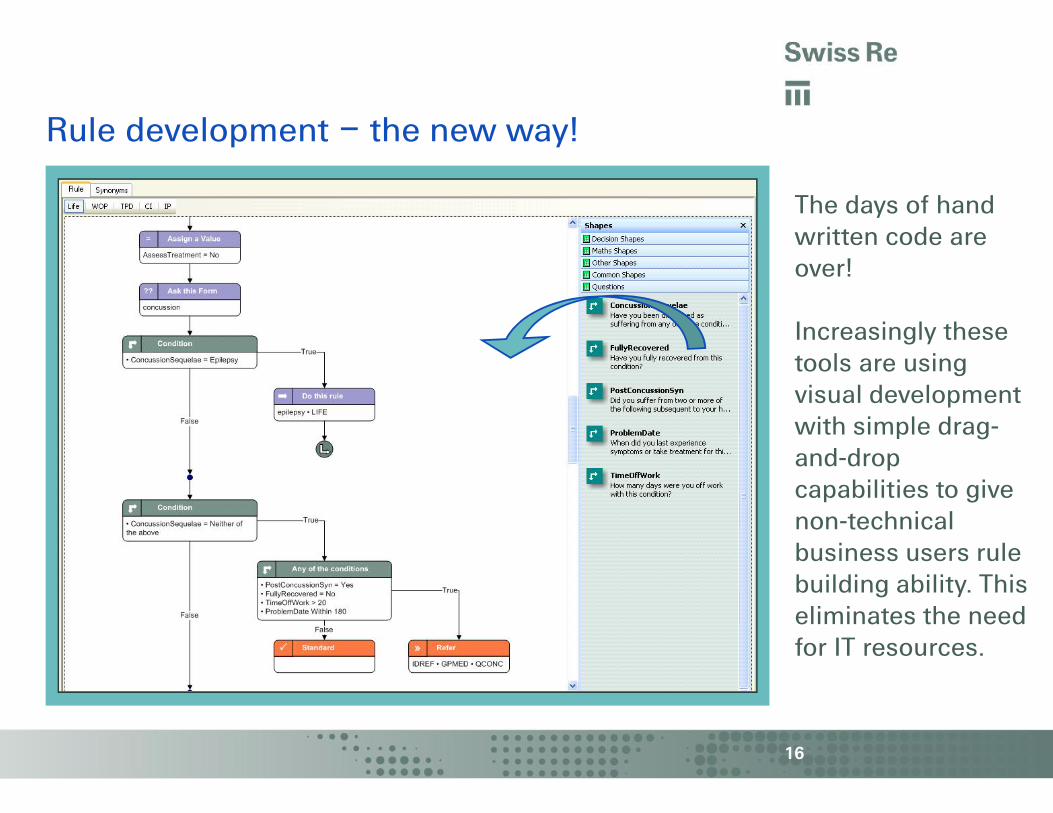

Rule development – the new way!

16

The days of handwritten code areover!

Increasingly thesetools are usingvisual developmentwith simple drag-and-dropcapabilities to givenon-technicalbusiness users rulebuilding ability. Thiseliminates the needfor IT resources.

17

Analytics

How much of our medicalbudget is spent on casesthat never complete?

How do differentunderwriting

approaches compare e.g. tele-uw, direct internet, traditional?

What are thebest questions

on the application form forgathering disclosures. Whichquestions add little value?

How reliable is client disclosedinformation versusmedical evidence forany given impairment?

Which of oursalespeople areencouraging the

clients to non-discloseand submit fraudulentapplications?

18

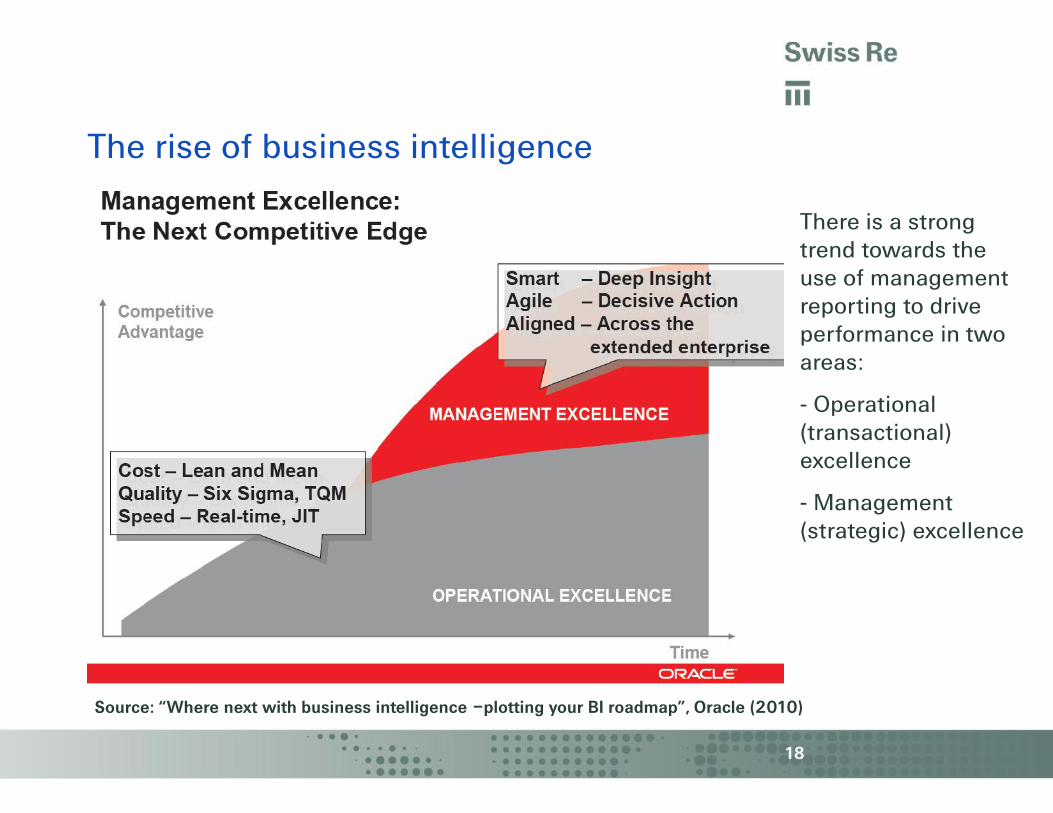

The rise of business intelligence

Source: “Where next with business intelligence –plotting your BI roadmap”, Oracle (2010)

There is a strongtrend towards theuse of managementreporting to driveperformance in twoareas:

- Operational(transactional)excellence

- Management(strategic) excellence

19

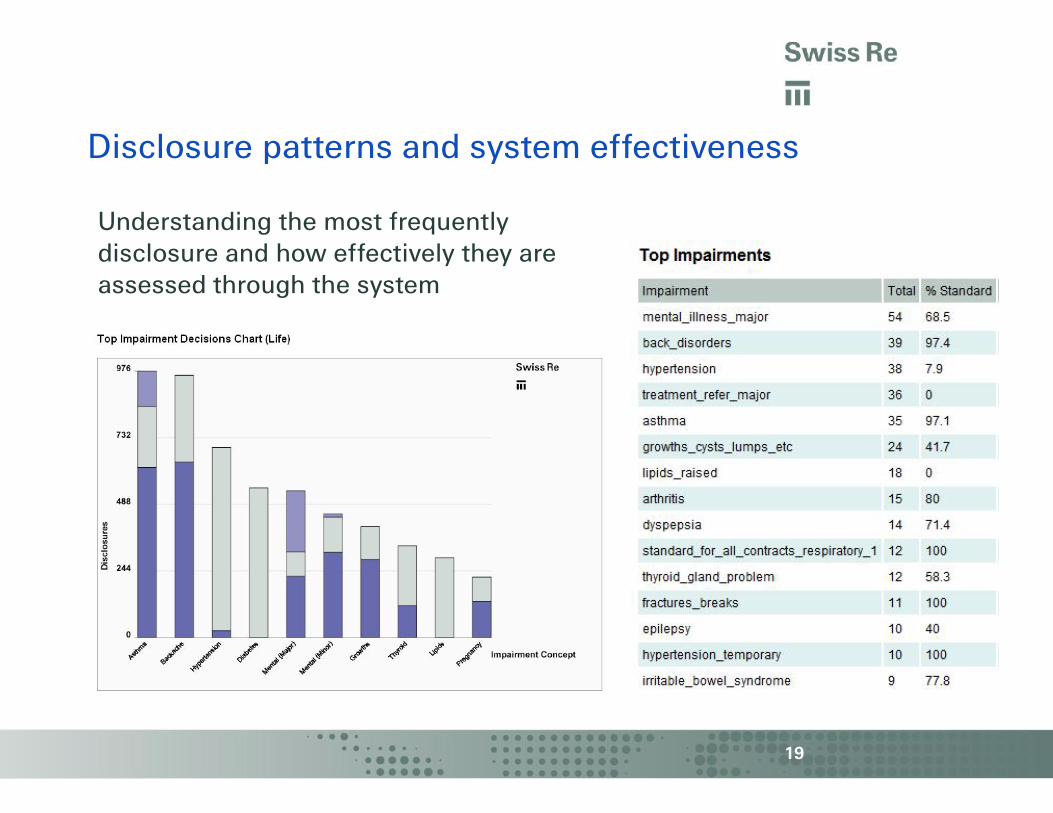

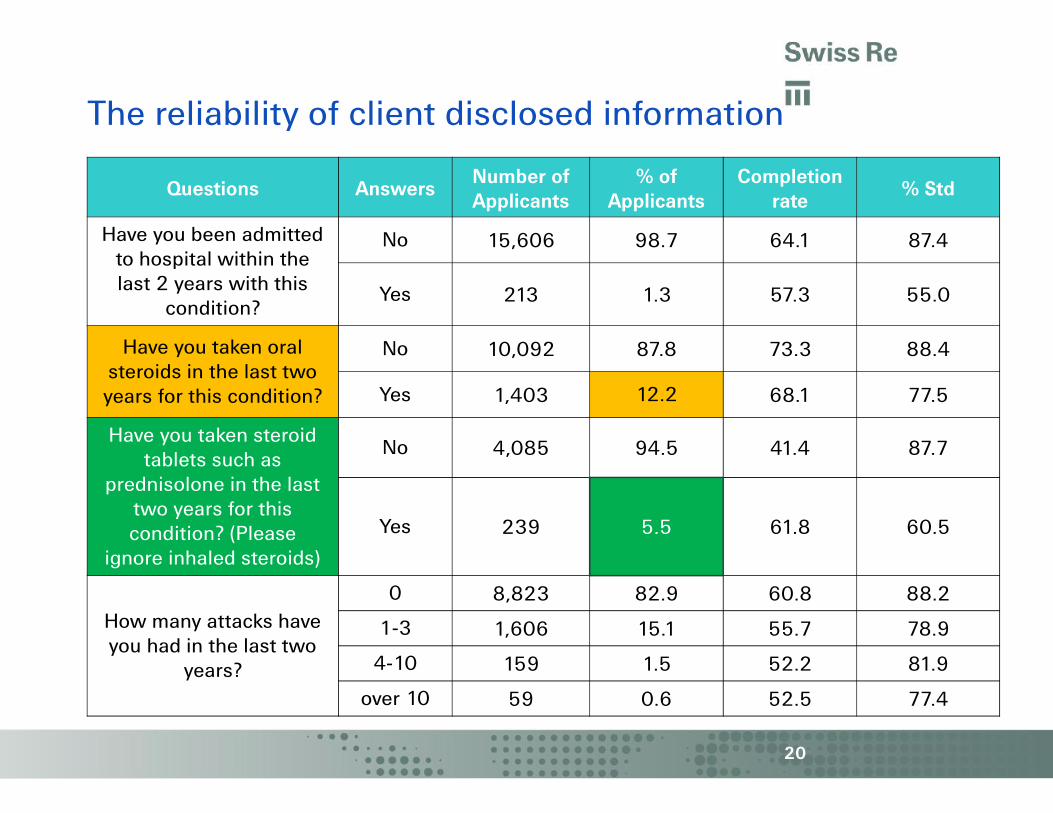

Disclosure patterns and system effectiveness

Understanding the most frequentlydisclosure and how effectively they areassessed through the system

The reliability of client disclosed information

20

Questions AnswersNumber ofApplicants

% ofApplicants

Completionrate

% Std

Have you been admittedto hospital within thelast 2 years with this

condition?

No 15,606 98.7 64.1 87.4

Yes 213 1.3 57.3 55.0

Have you taken oralsteroids in the last twoyears for this condition?

No 10,092 87.8 73.3 88.4

Yes 1,403 12.2 68.1 77.5

Have you taken steroidtablets such as

prednisolone in the lasttwo years for thiscondition? (Please

ignore inhaled steroids)

No 4,085 94.5 41.4 87.7

Yes 239 5.5 61.8 60.5

How many attacks haveyou had in the last two

years?

0 8,823 82.9 60.8 88.2

1-3 1,606 15.1 55.7 78.9

4-10 159 1.5 52.2 81.9

over 10 59 0.6 52.5 77.4

21

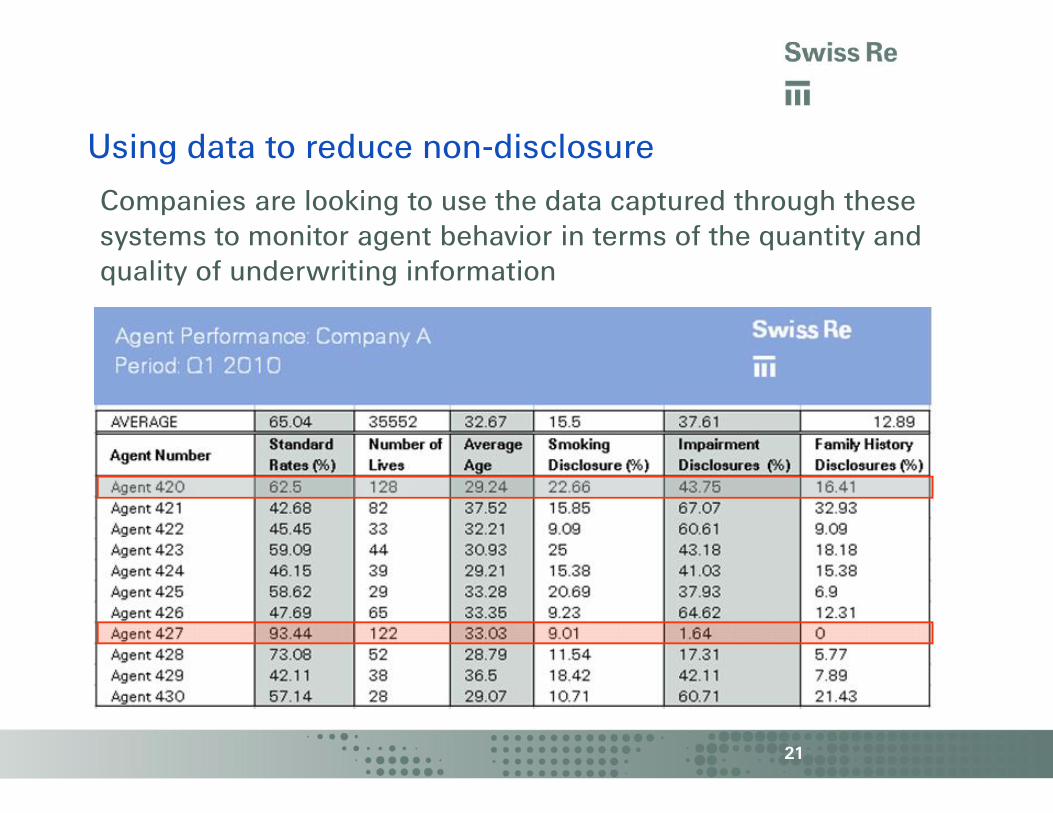

Using data to reduce non-disclosure

Companies are looking to use the data captured through thesesystems to monitor agent behavior in terms of the quantity andquality of underwriting information

22

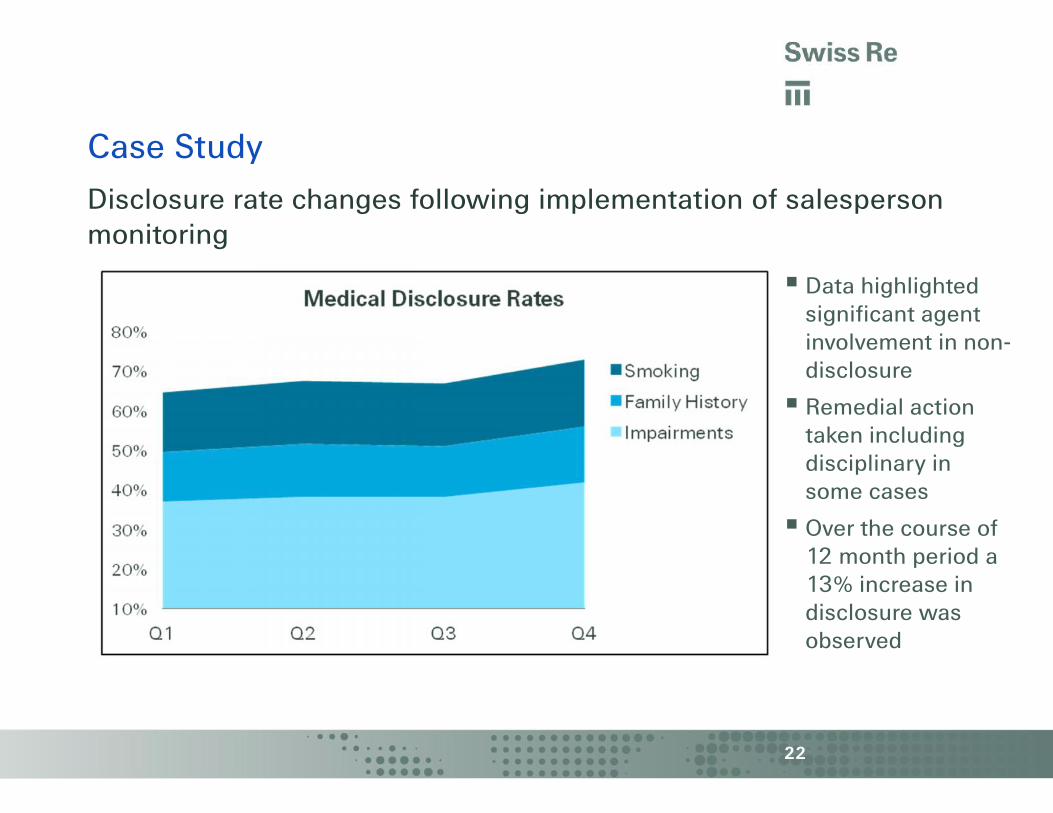

Case StudyDisclosure rate changes following implementation of salespersonmonitoring

Data highlightedsignificant agentinvolvement in non-disclosure

Remedial actiontaken includingdisciplinary insome cases

Over the course of12 month period a13% increase indisclosure wasobserved

23

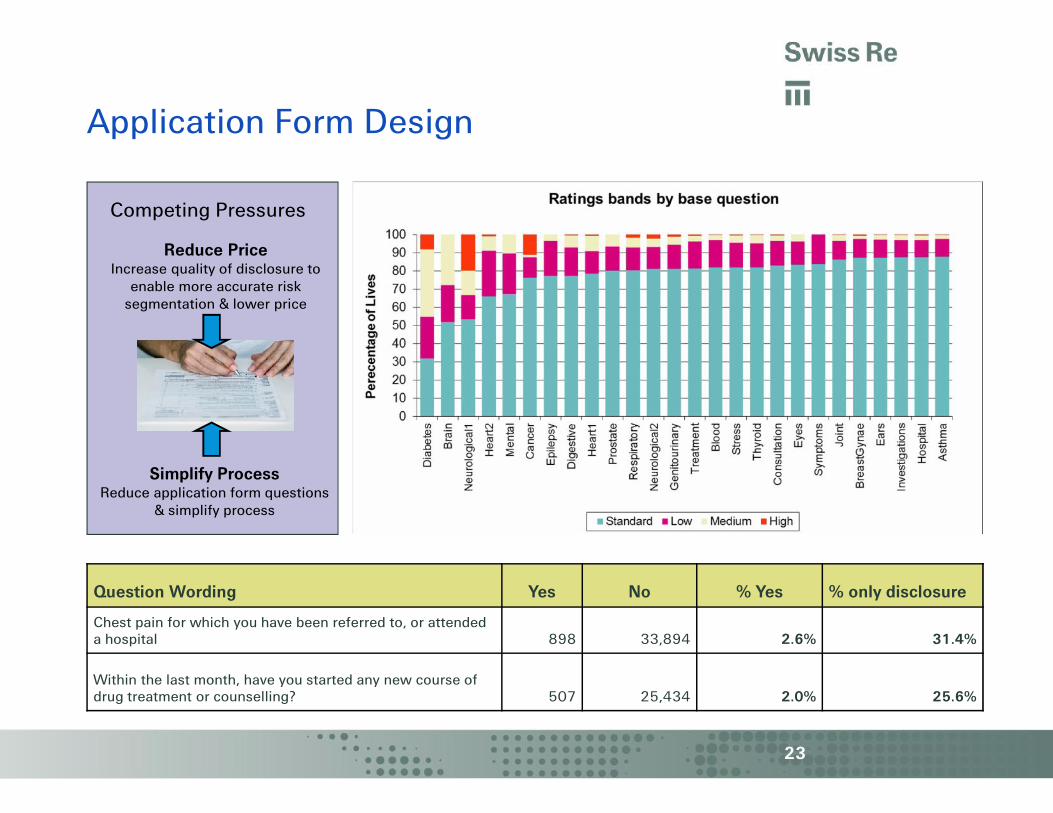

Application Form Design

Simplify ProcessReduce application form questions

& simplify process

Reduce PriceIncrease quality of disclosure to

enable more accurate risksegmentation & lower price

Competing Pressures

Question Wording Yes No % Yes % only disclosure

Chest pain for which you have been referred to, or attendeda hospital 898 33,894 2.6% 31.4%

Within the last month, have you started any new course ofdrug treatment or counselling? 507 25,434 2.0% 25.6%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

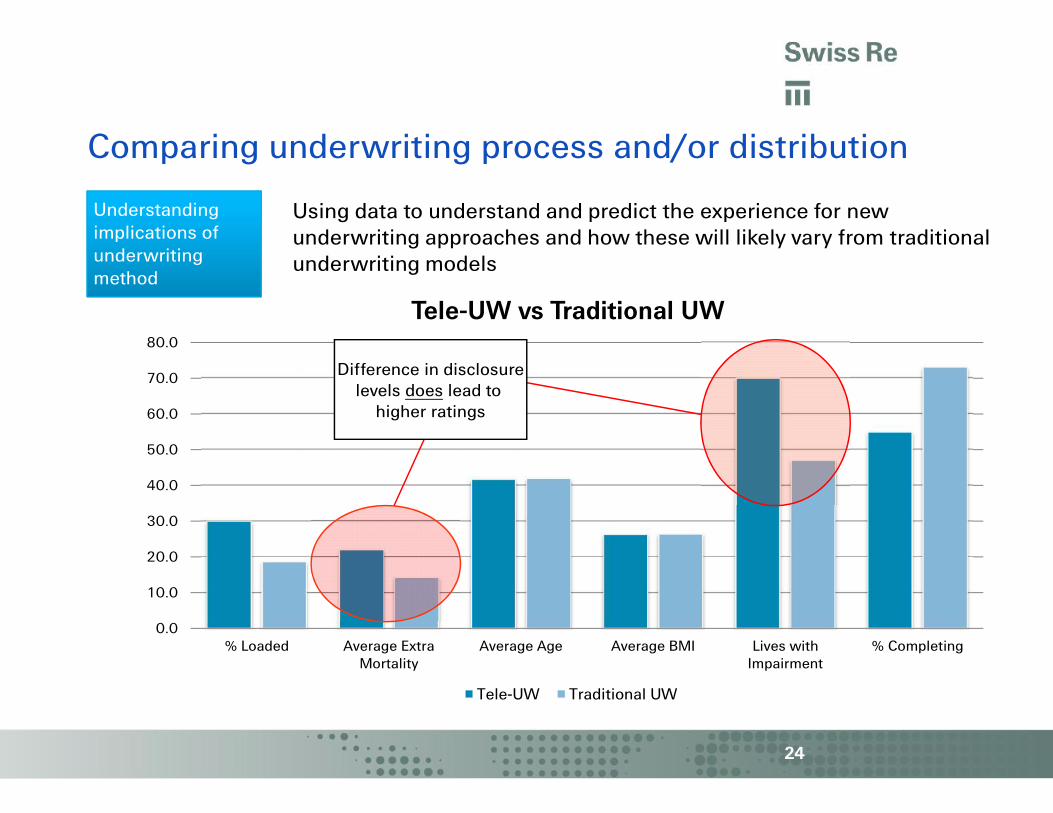

80.0

% Loaded Average ExtraMortality

Average Age Average BMI Lives withImpairment

% Completing

Tele-UW vs Traditional UW

Tele-UW Traditional UW

24

Comparing underwriting process and/or distribution

Understandingimplications ofunderwritingmethod

Understandingimplications ofunderwritingmethod

Using data to understand and predict the experience for newunderwriting approaches and how these will likely vary from traditionalunderwriting models

Difference in disclosurelevels does lead to

higher ratings

Technology advances are having a major impact on theunderwriting process

The pace of change is increasing

The role of the underwriter is vital but will be potentially quitedifferent in the future

Keys to adapting to the future

– Remain open and interested in new developments

– Encourage your company to embrace technology that puts the business(rather than the IT department) in control, and the customer at thecenter

– Get involved & enjoy the journey!

25

Summary

26

Do you have anyquestions?

CONFIDENTIAL | RESTRICTED DISTRIBUTION

26

Thank you

Legal notice

©2013 Swiss Re. All rights reserved. You are not permitted to create anymodifications or derivatives of this presentation or to use it for commercialor other public purposes without the prior written permission of Swiss Re.

Although all the information used was taken from reliable sources, Swiss Redoes not accept any responsibility for the accuracy or comprehensiveness ofthe details given. All liability for the accuracy and completeness thereof orfor any damage resulting from the use of the information contained in thispresentation is expressly excluded. Under no circumstances shall Swiss Reor its Group companies be liable for any financial and/or consequential lossrelating to this presentation.

28