Embed Size (px)

Citation preview

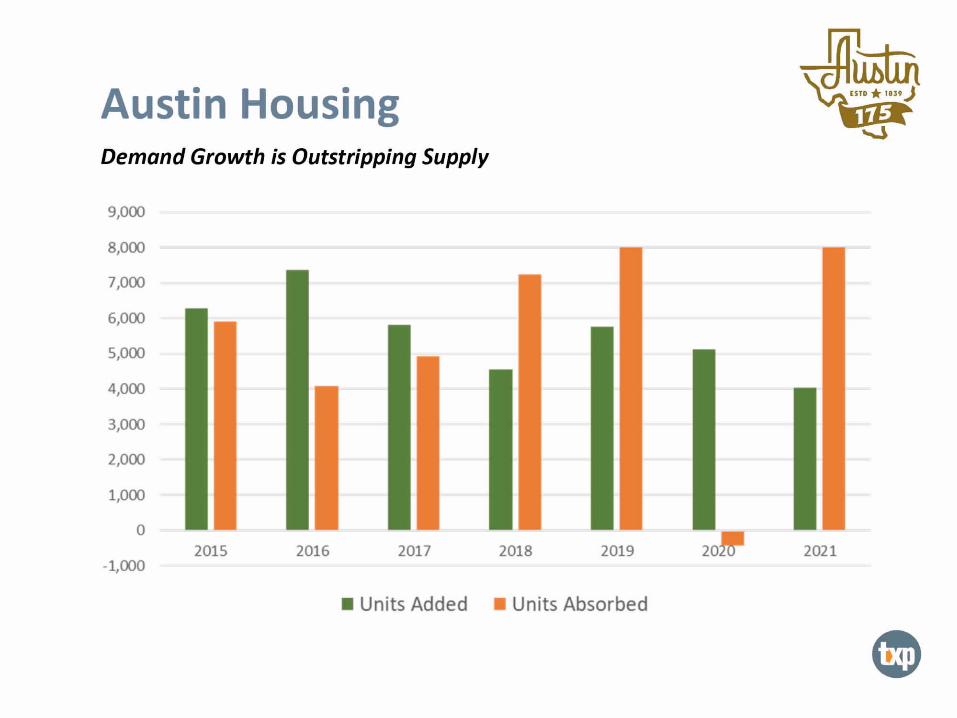

Austin Housing

KAtih??ESTD *1839??

November 30, 2021Jon Hockenyos

Ir-1-ca Ublll.Austin Economy

iiHow Austin MSA Became One of the Least Affordable Regions in America "

The impact of COVID-19 continues to recede in Austin, as most indicators now exceed pre-pandemic levels. Its too soon to know about the impact of Omicron.Overthe past twelve months (through October) the Austin MSA has added 77,100 net new

jobs, a gain of 7.0 percent since October 2020 (and over 40,000 above October 2019). Overall,the Austin area remains among the regional economic sta rs in the United States, with thepandemic only enhancing trends that have been in evidence for some time.At this point, supply/cost issues are the main economic challenges, be it in housing, materials,or labor force. In terms of jobs, all sectors have returned to pre-pandemic levels, with much ofthe fruits of recent expansions/relocations such as Tesla yet to be fully realized.With in-migration expected to continue at a rapid rate, overall growth in the region will remain

strong forthe foreseeable future.The real estate side of the pandemic also has been heated:

Perfect storm forowner-occupied residential, esp. single-family- record levels of localactivity and extraordinary increases in prices/rents. There are some signs that the rate ofgrowth is abating (especially at the high-end) but affordability is a distant memory.Industrial/wa rehouse benefit from heightened "hunkering down1,

Office, small retail, and hospitality are last to recover - some progress. ©

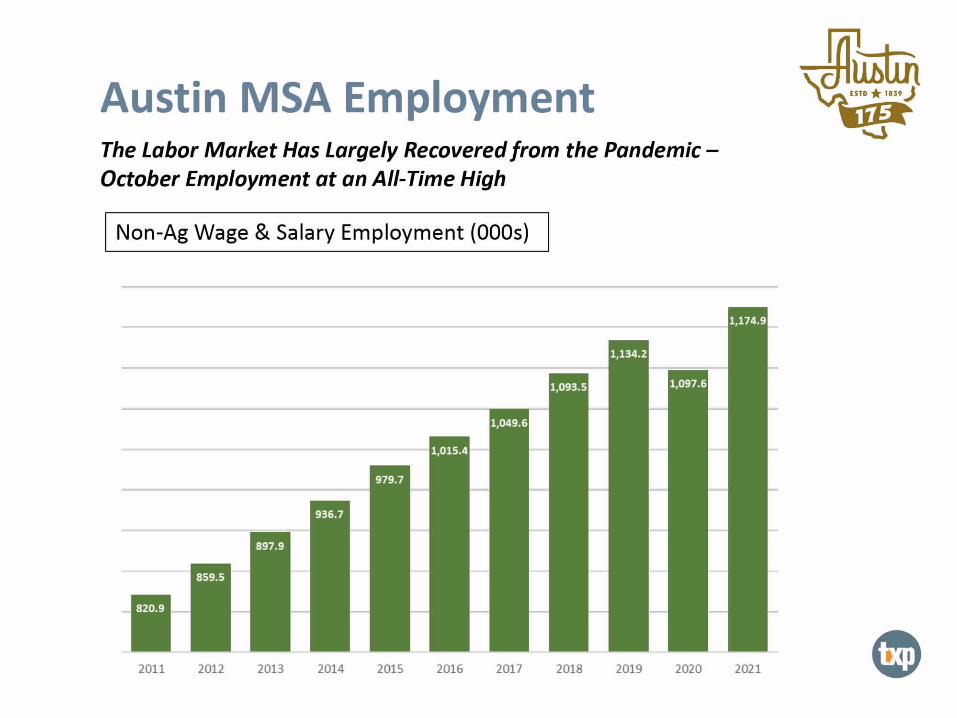

Ir-1-Austin MSA Employment 401 Ubl,UlThe Labor Market Has Largely Recovered from the Pandemic -October Employment at an All-Time High

Non-Ag Wage & Salary Employment (000s)

1,174.9

1,134.2

1,093.5 1,097.6

1,049.6

1,015.4

979.7

936.7

897.9

859.5

820.9

©2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Ir-1-Austin MSA Employment 401 Ubl,UlIn Spite of Four Major Shocks, Austin Has Grown at an ExceptionallyRapid Rate (3.8%) for DecadesOctober Data: 12-Month Percentage Change in Non-Ag W&S

14.096 -

12.056

10.0%

8.0%

6.0%

4.0% -

2.0%

0.0%

-2.056 -S&L Crisis 9.11/.com

-4.0% Great Recession COVID-19-6.056

1981 1985 1989 1993 1997 2001 2005 2009 2013 2017 2021 ©

Ir-1-ca Ublll.Austin Housing ? A ISTD * 1839 J

Demand Growth is Outstripping Supply

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0 112015 2016 2017 2018 2019 20?/ 2021

-1,000

• Units Added • Units Absorbed

©

Ir-1-401 Ubl,UlAustin Housing

City of Austin Resident Jobs vs. Permitted Housing Units

35,000

30,000 Since 2011, there have been 32,666 more

jobs created for Austin residents than25,000 permitted housing units in the city20,000

15,000

10,000

5,000

02011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

-O-Jobs -O-Housing Units ©

Ir-1-401 Ubl,UlABOR Housing

Average and Median Home Price ($000s)$700.0

$650.0 Avg Annual Wage in Travis County is $801<.Assume a double-income household at that

$600.0rate ($16010 and can afford 3X - $70k short of

$550.0 the median, $188k short of the average.

$500.0

$450.0

$400.0 -

$350.0

$300.0

$250.0 - 1 11Oct-15 Oct-16 Oct-17 Oct-18 Oct-19 Oct-20 Oct-21

• Average I Median ©

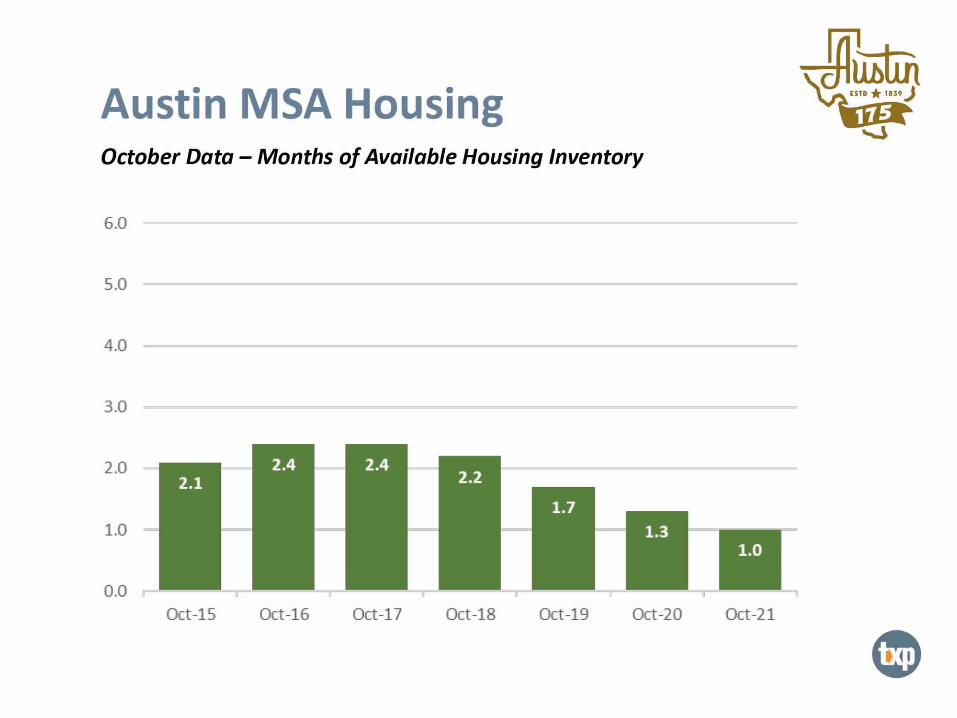

Ir-1-ca Ublll.Austin MSA Housing

October Data - Months ofAvailable Housing Inventory

6.0

5.0

4.0

3.0

2.0 2.4 2.42.1 2.2

1.71.0 1.3

1.0

0.0 11

Oct-15 Oct-16 Oct-17 Oct-18 Oct-19 Oct-20 Oct-21

©

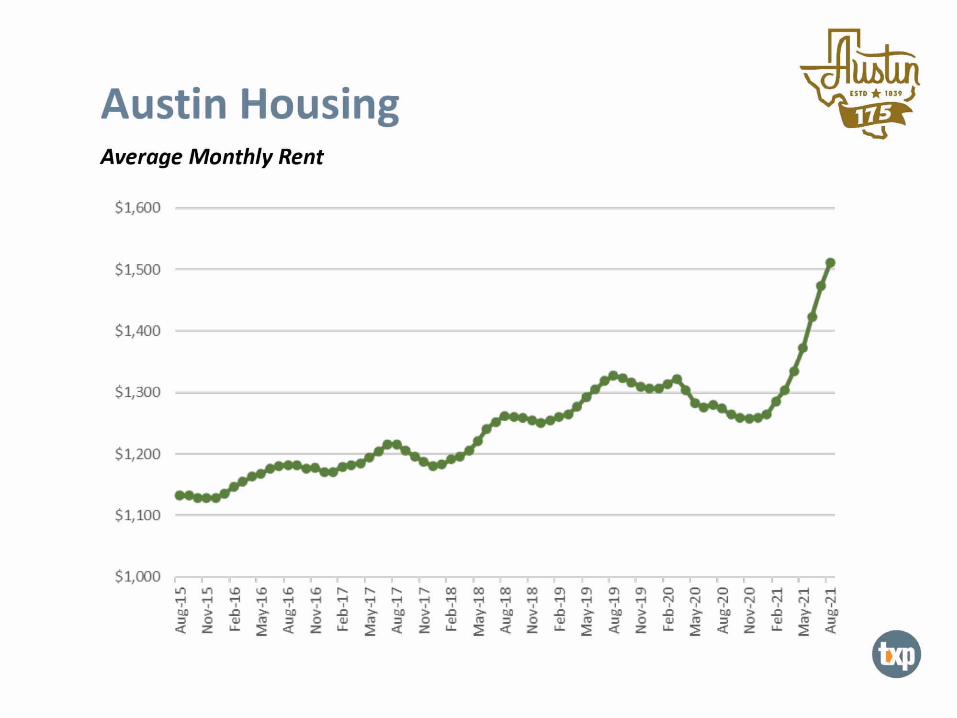

Ir-1-401 Ubl,UlAustin Housing

Average Monthly Rent

$ 1,600

$ 1,500

51,400 -

$ 1,300

$ 1,200

$ 1,100

51,000 ? J

h

ZZ

©

Ir-1-401 Ubl,UlConclusions

This Could be the Roaring 20s - But Supply/Capacity is a Huge Issue

Over the longer-term, Austin and the region are expected to continue to growmore rapidly than either the state or the nation, as the appeal as a relativelycost-effective location for technology and intellectual property-based activityremains a substantial competitive advantage.However, rapidly rising costs (especially for housing), unprecedented levels ofcongestion )and overall concern regional infrastructure capacity), and thestrain on the community's cultural and recreational amenities are all

beginning to take a toll on quality of life.On the housing side:

Demand far outstrips supply, especially for housingthat serves those without highhousehold income and/or substantial capital to invest.

Historic patterns of not meeting demand, both for owner-occupied andrental;

},"Housing as asset bids up prices;Rapid economic growth, historically low interest rates, and in-migration all ?contribute

Conclusions (cont.) Ir-1-401 Ubl,Ul

Affordable housing (in the technical sense) is an important part ofthe equation, which requires significant federal (and often local)subsidy. However, Austin and regional agencies must go beyondsubsidy to meet the challenge of better aligning demand and supply.

Institutional capital is focused on maximizing rates of return - tends tofocus on higher-end product and won't/can't accept reduced ROI in

light of investment parameters.The housing market is somewhat fungible; if those of certain income are

priced out at expected level, they will move down the market toconsume product that might otherwise be available to those with lowerincomes.

Austin must look to increase supply at all levels (with possibleexception of high-end). Tools could include: access to public land forhousing, policies/programs to encourage campus-based employersto build on-site, further streamlining the regulatory process, andremoval/reduction of capacity limits in the land development code.This is arguably the most significant economic development issue ©facing the community today.

![[July '10] Housing Market Analysis for Austin, Texas [by Ankit Patel]](https://img.pdfslide.us/doc/110x75/577d37591a28ab3a6b957741/july-10-housing-market-analysis-for-austin-texas-by-ankit-patel.jpg)