Embed Size (px)

Citation preview

RICHARD G. BRODY, JOHN M. COULTER and ALIREZA DANESHFAR

AUDITOR PROBABILITY JUDGMENTS: DISCOUNTINGUNSPECIFIED POSSIBILITIES

ABSTRACT. Tversky and Koehler’s support theory attempts to explain whyprobability judgments are affected by the manner in which formally similar eventsare described. Support theory suggests that as the explicitness of a descriptionincreases, an event will be judged to be more likely. In the present experiment, ex-perienced decision-makers from large, international accounting firms were givencase-specific information about an audit client and asked to provide a series ofjudgments regarding the perceived likelihood of events. Unpacking a hypothesisinto four formally equivalent hypotheses more than doubled its perceived like-lihood. These results are largely consistent with support theory, extending itsgeneralizability to applied contexts involving business professionals. Further, thepaper finds that task-specific factors, a previously untested area, can also affectsupport theory interpretations.

1. INTRODUCTION

In evaluating multiple hypotheses, decision makers often provideevaluations that deviate from normative probability theory. Understandard probability theory, the judged probability of a given hy-pothesis should not be affected by the description of its extension.However, a considerable amount of research examining the judg-ments of experts performing familiar, professional tasks has shownthat separating a hypothesis into two or more components increasesits overall perceived likelihood, and that the overall probability as-signed to individually presented exclusive and exhaustive eventsoften exceeds 100%. Examples include auto mechanics (Fischhoffet al., 1978), physicians (Redelmeier et al., 1995), and stock optionstraders (Fox et al., 1996).

Tversky and Koehler (1994) have developed a framework calledsupport theory to explain the findings of research on the evaluationof alternative descriptions of the same hypothesis. Support theoryproposes that while each hypothesis refers to a unique event, a givenevent can be described by more than one hypothesis. For example,

Theory and Decision 54: 85–104, 2003.© 2003 Kluwer Academic Publishers. Printed in the Netherlands.

86 R.G. BRODY ET AL.

the hypotheses "death due to traffic accident, drowning, electro-cution, or any other accident" and "death due to an accident" aredifferent descriptions of the same event (Redelmeier et al., 1995).According to support theory, an event will be judged more likely asthe explicitness of its description increases. A more explicit descrip-tion may lead decision makers to recall more evidence in support ofa hypothesis, or make existing evidence more salient. The strongersupport for the hypothesis results in a higher judged probability(Tversky and Koehler, 1994; Ayton, 1997).

This paper examines the descriptive validity of support theoryin an applied professional decision making context. We presentedcase-specific information about an audit client to professional aud-itors in three separate experimental scenarios, obtaining evidenceon the effect of such evidence on auditors’ evaluation of multiplehypotheses. As likelihood assessment and hypothesis evaluation canaffect both the effectiveness and efficiency of an audit (Heiman,1990; Asare and Wright, 1997), these findings are particularly relev-ant to auditors, who make a series of such judgments and decisionsin the process of rendering an opinion on the financial condition ofa company.

We also examined the effect of the riskiness of the client onauditors’ judgments. Previous research did not explicitly manipulatecharacteristics that could potentially affect the evaluation of hypo-theses. Research has shown that client risk affects attention to, andevaluation of, audit evidence (e.g., Phillips, 1999; Guess et al., 2000;Wright and Bedard, 2000). Since support theory is not sufficientlywell developed to support the development of formal hypothesesbased on the effect of client risk, we examine it on an exploratorybasis.

Overall our results show that auditors’ judgments are generallyconsistent with support theory. Unpacking an event into more de-tail increased its perceived likelihood, and we did find evidenceof binary complementarity. However, task-specific factors did af-fect subjects’ judgments. Specifically, client risk affected unpackingjudgments and binary probability judgments. Judgments involvingaccount balance overstatement differed from formally equivalentjudgments involving understatement of the same balance. Decisionsbetween issuing an unqualified audit opinion and a qualified opinion

AUDITOR PROBABILITY JUDGMENTS 87

also did not conform to the predictions of support theory. Taken asa whole, the findings suggest the general applicability of supporttheory in an applied professional setting, but underscore the needto consider carefully the contextual features of the auditing environ-ment in generalizing psychology theories to such settings (see Smithand Kida, 1991, for an overview of this area).

The remainder of this paper is organized as follows. The nextsection reviews relevant background research and develops the hy-potheses of the study. The third section reviews the research meth-odology, and the fourth section presents and discusses the results.The fifth section offers a conclusion, discusses the limitations of thestudy, and offers suggestions for further research.

2. BACKGROUND AND HYPOTHESES

This study incorporates two important considerations regarding thegeneralizability of support theory that have not been considered byprior research. These are the knowledge structure of the profession-als performing the task, and the characteristics of the task itself. Themotivation for their inclusion is discussed below. The major findingsof support theory to date are then referenced in the development ofindividual hypotheses.

2.1. Knowledge Structure

One important element missing from previous research on supporttheory is explicit consideration of the knowledge structure the de-cision maker brings to bear upon the task. Though studies such asRedelmeier et al. (1995) and Fischhoff et al. (1978) do examine thejudgments of experts performing familiar tasks (physicians and automechanics, respectively), the tasks examined are generic in and ofthemselves, perhaps offering domain familiarity but not tapping intoimportant knowledge elements the professionals involved would useto reach a judgment.

Such consideration of knowledge structure is important in anauditing, as research has shown that auditors have difficulty in mak-ing conditional probability judgments where the judgments they arebeing asked to make do not correspond with their knowledge struc-

88 R.G. BRODY ET AL.

tures (Nelson et al., 1995). Thus, the scenarios we presented to sub-jects were consistent with Nelson et al.’s (1995) findings that audit-ors organize their knowledge around audit objectives and not trans-action cycles. Psychology research has also shown that decisionmakers have difficulty in making probability judgments that do notinvolve "natural" sample spaces (Gavanski and Hui, 1992; Shermanet al., 1992).

2.2. Client Risk

Research has found that many facets of audit decisions are affectedby perceptions of the riskiness of the client, including the degree ofattention paid to aggressive financial reporting (Phillips, 1999), theextent of planned substantive testing to be performed (Guess et al.,2000), and on the effectiveness of the audit program itself (Wrightand Bedard, 2000).

Taken as a whole, the results of these and other studies suggestthat client risk is an important variable that should be considered ina study of auditor judgment. Indeed, Wright and Bedard (2000) callfor additional research into the client risk-based contingent natureof auditors’ identification of financial statement errors and auditplanning decisions. Higher perceived client risk should lead to anincreased assessment of the likelihood of financial statement errorsand misstatements, but not in a manner that systematically violatesnormative probability theory.

2.3. Unpacking

Support theory provides a framework for making a series of empiric-ally supportable predictions about the evaluation of hypotheses. Forexample, it holds that the judged probability of an event increases ifits description is unpacked into more explicit alternatives. Tverskyand Koehler (1994) asked subjects to estimate the probability that anindividual’s recent death resulted from unnatural causes. Unpackingthe focal hypothesis “death due to unnatural causes” into seven moreexplicit but formally equivalent alternatives increased the supportfor the hypothesis and its judged probability went from 45 to 83%.

Other research has also found that a unpacking a hypothesis intoalternatives increases its judged probability (e.g., Fischhoff et al.,

AUDITOR PROBABILITY JUDGMENTS 89

1978; Redelmeier et al., 1995). Accordingly, we expected auditors’judgments to follow such a pattern. Our first hypothesis is that:

H1: Auditors’ judged probability of a given hypothesis will in-crease when it is unpacked into more explicit equivalentalternatives.

2.4. Subadditivity

Support theory predicts that a hypothesis is judged as more likelywhen considered in isolation because decision makers underweightthe unspecified alternatives to the hypothesis. Under standard prob-ability theory, the sum of the judged probabilities for a set of mu-tually exclusive and exhaustive hypotheses should be additive. Forexample, if four sports teams remain in a tournament and differentgroups of subjects are each asked to give the probability that onegiven team will win, the mean judgments provided across all fourteams should sum to 100%. However, support theory suggests thatthe implicit alternatives (in this example, the other three teams notbeing explicitly mentioned) to the focal hypothesis will be under-weighted, resulting in aggregate probability judgments of explicitlystated hypotheses that are subaddditive (i.e., that add to more than100%).1 Our second hypothesis is that:

H2: Auditors’ probability judgments of implicit disjunctions ofevents will be subadditive (i.e., sum to more than 100%).

2.5. Binary Complementarity

Support theory argues that in evaluating individual elements of ex-plicit binary disjunctions, decision makers will produce judgmentsthat are additive (i.e., that sum to 100%). Tversky and Koehler(1994) term this binary complementarity.2 For example, if twoteams are known to be playing a game and different groups of sub-jects are each asked to give the probability that a given team willwin, the mean judgments given by both groups should sum to 100%.Research examining such judgments has found evidence consistentwith this prediction (e.g., Wallsten et al., 1992; Tversky and Fox,1995). Thus, our third hypothesis is that:

H3: Auditors’ judgments of explicit disjunctions will be addit-ive (i.e., sum to 100%).

90 R.G. BRODY ET AL.

3. EXPERIMENTAL DESIGN

This section first describes the overall methodology of the study.Information specific to each individual experimental scenario is thenpresented separately.

3.1. Subjects

The subjects (overall n = 141) were auditors at Northeastern U.S.offices of Big 5 international public accounting firms and had anaverage of nearly 4.5 years of professional audit experience (mean= 53.7 months). There were two means of distributing the case ma-terials. The primary method (for approximately 85% of subjects)was that the materials were distributed and controlled directly byone of the researchers who was present at the participating firm’soffice. The second method involved the mailing of materials to afirm’s office. A contact person within the firm distributed them toparticipants who mailed the completed instruments back to one ofthe researchers.

3.2. Experimental Materials

Subjects were given a booklet containing a cover page, introduction,instructions, the experimental tasks to be completed, and a demo-graphic questionnaire. The cover page explained that the subjectswere taking part in a study designed to examine the judgment pro-cesses of auditors. Subjects were informed that the experimentalmaterials would take approximately 35–45 minutes to complete.The group that completed the materials under the direction of theresearchers took this amount of time to complete them, and thereis no reason to believe that the other group took longer than this todo so. The two groups were compared across all measures and therewere no significant differences between them. As a result the groupsare combined for purposes of analysis.

The introduction presented subjects with a description of a hy-pothetical audit client, Reed Electronics. Depending upon experi-mental condition, Reed was portrayed as being either a high risk or alow risk client. After reading this description, subjects were asked tomake a preliminary assessment of the level of overall risk present in

AUDITOR PROBABILITY JUDGMENTS 91

the audit. This assessment was made on a scale from 1 to 9, with en-dpoints representing low and high levels of overall risk, respectively.Results indicate that this manipulation was successful, as high risksubjects found Reed to be riskier than did low risk subjects (meanassessments = 7.33 vs. 3.14, t = 21.24, p < 0.001). Subjects werethen asked to complete each of the experimental tasks (describedbelow), to provide demographic information, and thanked for parti-cipating in the study. The tasks were presented to the subjects in theorder described below.

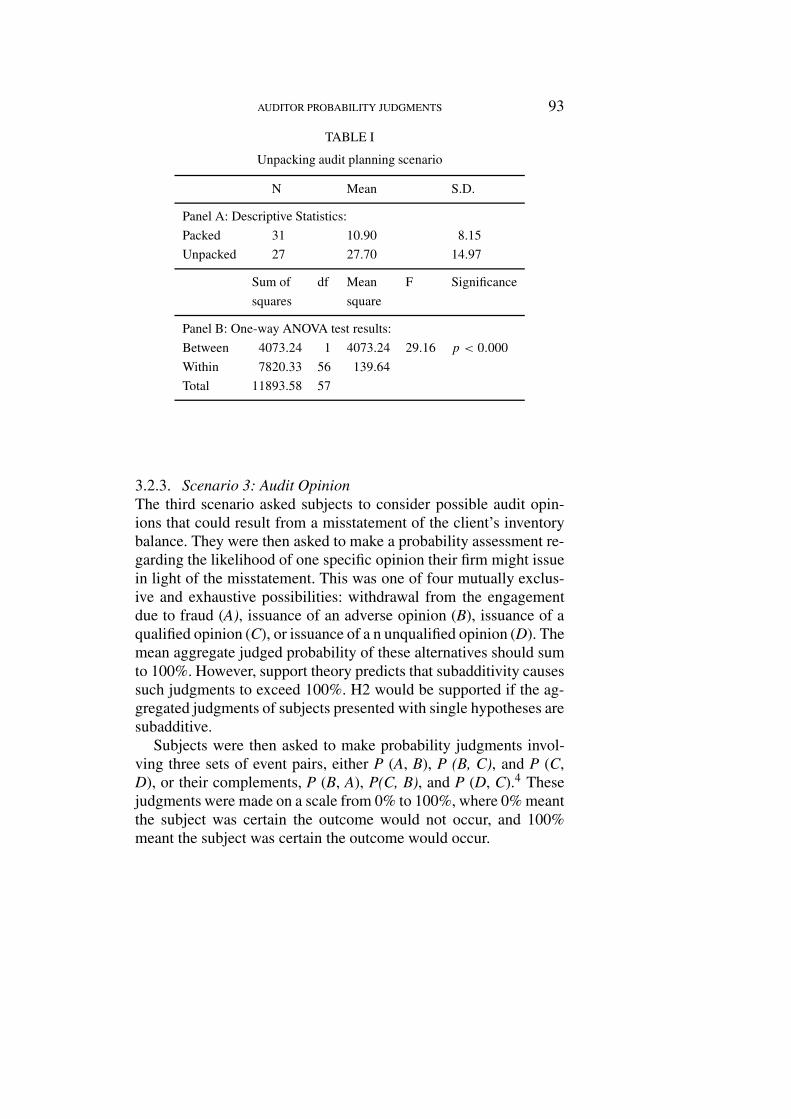

3.2.1. Scenario 1: Audit PlanningThe first scenario presented to subjects asked them to assume that amisstatement violating the audit objective of valuation had occurred.They were then told that this misstatement had occurred in onlyone transaction cycle, and asked to make a probability assessmentregarding the likelihood that the misstatement occurred in a giventransaction cycle.3 These assessments were made numerically on ascale from 0 to 100%, where 0% indicates no probability of the valu-ation misstatement occurring in that transaction cycle, and 100%indicates the subject was certain that the misstatement would occurin that cycle. Since the list of outcomes presented includes all pos-sible cycles, subjects were instructed to make sure their responsestotaled 100%.

In this scenario, auditors were presented with two possible hy-potheses regarding a misstatement involving the valuation objectivein the “Inventory/Purchases” (Hypothesis A) or “Sales and Collec-tion” transaction cycle (Hypothesis B). A residual hypothesis C waspresented in two different forms: to subjects in the packed condition,C was simply “Some other transaction cycle.” In the unpacked con-dition, C was presented as four mutually exclusive and exhaustivealternatives C1, C2, C3 and C4 (“Investing,” “Financing,” “Payroll,”and “Some other” transaction cycle, respectively). Since the eventsportrayed in the two conditions are formally equivalent, the aggreg-ate probability assigned to the 4-fold description of C should bethe same as that assigned to the one-event description. However,since support theory suggests that unpacking an event increases itsperceived likelihood, H1 suggests that the unpacked description ofC will be assigned a higher total probability.

92 R.G. BRODY ET AL.

3.2.2. Scenario 2: Accounts ReceivableIn this scenario, subjects were told that substantive testing had dis-covered a misstatement in a client’s accounts receivable balance.They were then asked to make three probability judgments regardingthis misstatement. Depending upon experimental condition, thesejudgments were the likelihood that the balance was each of

understated (U)materially overstated (MO), andoverstated, but not materially overstated (NMO)

or that it was

overstated (O)materially understated (MU), andunderstated, but not materially understated (NMU).

Ordering of these possibilities was randomized between subjects.In this scenario, evidence supporting H1 would be provided by thesum of probability judgments involving unpacked descriptions (MO+ NMO, or MU + NMU) exceeding the estimates involving packeddescriptions of the formally equivalent outcome (O or U, respect-ively).

Subjects were also asked to make two additional judgments. Halfof the subjects were first told to assume that Reed’s Accounts Re-ceivable balance was, in fact, over (under) stated, and asked to in-dicate the probability that the balance was either: (1) materially over(under) stated, or (2) over (under) stated, but not materially over(under) stated. Then subjects who were initially told to assume theaccount balance was overstated were asked to assume instead that itwas understated (and vice versa), and were again asked to make asimilar judgment concerning the misstatement.

In these cases, where subjects were explicitly asked to considerthe probability of one of two possible outcomes occurring, sup-port theory predicts additivity for the combined probability judg-ments involving the two alternatives. H3 would be supported if suchjudgments added to 100%.

AUDITOR PROBABILITY JUDGMENTS 93

TABLE I

Unpacking audit planning scenario

N Mean S.D.

Panel A: Descriptive Statistics:

Packed 31 10.90 8.15

Unpacked 27 27.70 14.97

Sum of df Mean F Significance

squares square

Panel B: One-way ANOVA test results:

Between 4073.24 1 4073.24 29.16 p < 0.000

Within 7820.33 56 139.64

Total 11893.58 57

3.2.3. Scenario 3: Audit OpinionThe third scenario asked subjects to consider possible audit opin-ions that could result from a misstatement of the client’s inventorybalance. They were then asked to make a probability assessment re-garding the likelihood of one specific opinion their firm might issuein light of the misstatement. This was one of four mutually exclus-ive and exhaustive possibilities: withdrawal from the engagementdue to fraud (A), issuance of an adverse opinion (B), issuance of aqualified opinion (C), or issuance of a n unqualified opinion (D). Themean aggregate judged probability of these alternatives should sumto 100%. However, support theory predicts that subadditivity causessuch judgments to exceed 100%. H2 would be supported if the ag-gregated judgments of subjects presented with single hypotheses aresubadditive.

Subjects were then asked to make probability judgments invol-ving three sets of event pairs, either P (A, B), P (B, C), and P (C,D), or their complements, P (B, A), P(C, B), and P (D, C).4 Thesejudgments were made on a scale from 0% to 100%, where 0% meantthe subject was certain the outcome would not occur, and 100%meant the subject was certain the outcome would occur.

94 R.G. BRODY ET AL.

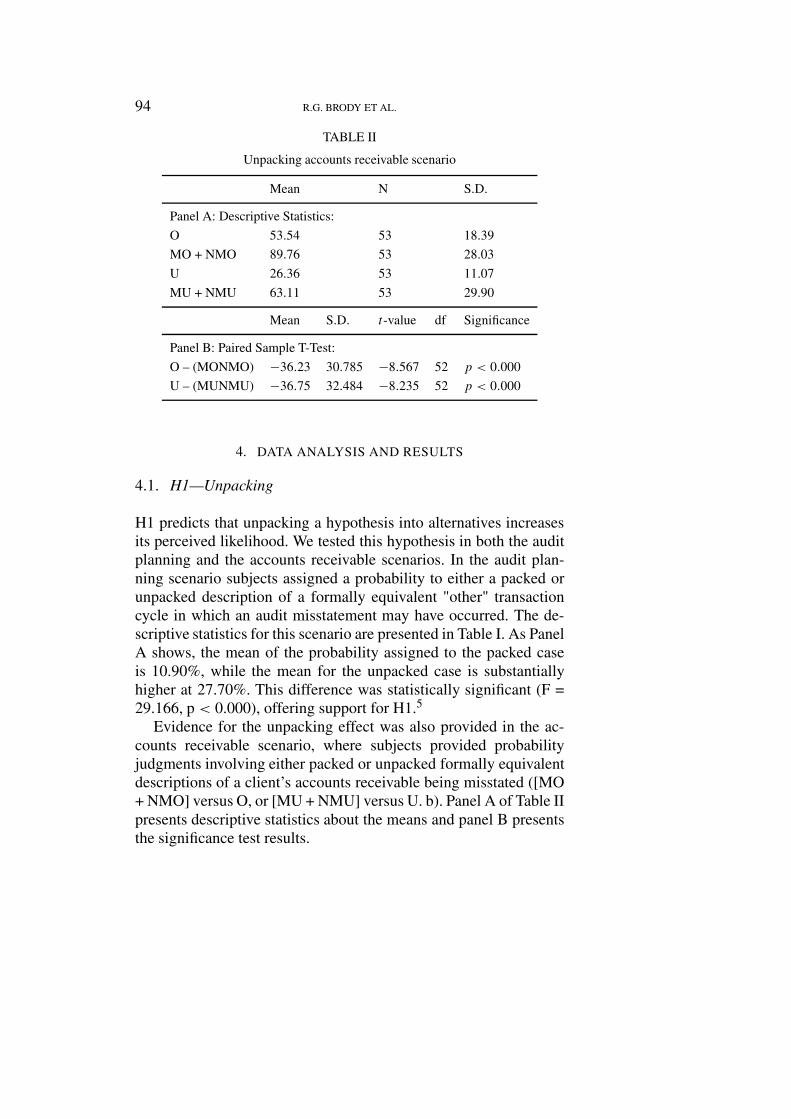

TABLE II

Unpacking accounts receivable scenario

Mean N S.D.

Panel A: Descriptive Statistics:

O 53.54 53 18.39

MO + NMO 89.76 53 28.03

U 26.36 53 11.07

MU + NMU 63.11 53 29.90

Mean S.D. t-value df Significance

Panel B: Paired Sample T-Test:

O – (MONMO) −36.23 30.785 −8.567 52 p < 0.000

U – (MUNMU) −36.75 32.484 −8.235 52 p < 0.000

4. DATA ANALYSIS AND RESULTS

4.1. H1—Unpacking

H1 predicts that unpacking a hypothesis into alternatives increasesits perceived likelihood. We tested this hypothesis in both the auditplanning and the accounts receivable scenarios. In the audit plan-ning scenario subjects assigned a probability to either a packed orunpacked description of a formally equivalent "other" transactioncycle in which an audit misstatement may have occurred. The de-scriptive statistics for this scenario are presented in Table I. As PanelA shows, the mean of the probability assigned to the packed caseis 10.90%, while the mean for the unpacked case is substantiallyhigher at 27.70%. This difference was statistically significant (F =29.166, p < 0.000), offering support for H1.5

Evidence for the unpacking effect was also provided in the ac-counts receivable scenario, where subjects provided probabilityjudgments involving either packed or unpacked formally equivalentdescriptions of a client’s accounts receivable being misstated ([MO+ NMO] versus O, or [MU + NMU] versus U. b). Panel A of Table IIpresents descriptive statistics about the means and panel B presentsthe significance test results.

AUDITOR PROBABILITY JUDGMENTS 95

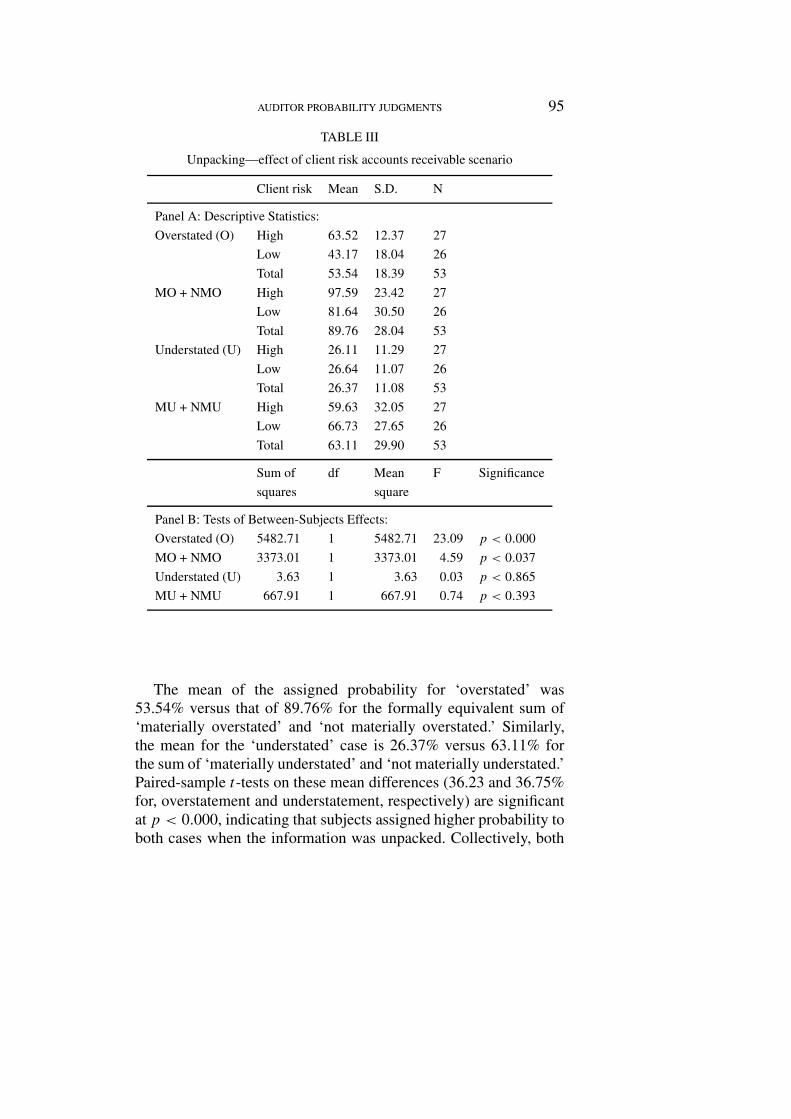

TABLE III

Unpacking—effect of client risk accounts receivable scenario

Client risk Mean S.D. N

Panel A: Descriptive Statistics:

Overstated (O) High 63.52 12.37 27

Low 43.17 18.04 26

Total 53.54 18.39 53

MO + NMO High 97.59 23.42 27

Low 81.64 30.50 26

Total 89.76 28.04 53

Understated (U) High 26.11 11.29 27

Low 26.64 11.07 26

Total 26.37 11.08 53

MU + NMU High 59.63 32.05 27

Low 66.73 27.65 26

Total 63.11 29.90 53

Sum of df Mean F Significance

squares square

Panel B: Tests of Between-Subjects Effects:

Overstated (O) 5482.71 1 5482.71 23.09 p < 0.000

MO + NMO 3373.01 1 3373.01 4.59 p < 0.037

Understated (U) 3.63 1 3.63 0.03 p < 0.865

MU + NMU 667.91 1 667.91 0.74 p < 0.393

The mean of the assigned probability for ‘overstated’ was53.54% versus that of 89.76% for the formally equivalent sum of‘materially overstated’ and ‘not materially overstated.’ Similarly,the mean for the ‘understated’ case is 26.37% versus 63.11% forthe sum of ‘materially understated’ and ‘not materially understated.’Paired-sample t-tests on these mean differences (36.23 and 36.75%for, overstatement and understatement, respectively) are significantat p < 0.000, indicating that subjects assigned higher probability toboth cases when the information was unpacked. Collectively, both

96 R.G. BRODY ET AL.

TABLE IV

Subadditivity

High client risk Low client risk

(aggregate n = 14) (aggregate n = 13)

Fraud 42.14% Fraud 28.46%

Adverse 39.54% Adverse 26.25%

Qualified 49.23% Qualified 28.57%

Clean 42.00% Clean 72.29%

Total 172.91% Total 154.66%

the audit planning and accounts receivable scenarios offer supportfor the unpacking effect.

The client risk manipulation also significantly affected unpack-ing in the accounts receivable scenario, as can be seen from TableIII. An overall MANOVA is significant at F = 6.449, p < 0.000,showing that there are significant differences between the dependentvariables in the scenario. Panel B of Table III reveals significanteffects for client risk when subjects were asked to provide judg-ments regarding either the overstatement of the account balance(significant at 0.000 level), or where separate judgments of mater-ially overstated and not materially overstated cases were elicited(significant at 0.003 level). However, there was no significant effectfor client risk in judgment involving the understatement of accountsreceivable. These results offer a potential extension of support the-ory, suggesting that a task-specific factor such as client risk affectsthe judged probability of uncertain events. Auditors appear to judgeoverstatement of an asset as more likely for high risk clients thanthey do for low risk clients, and no such difference is observed forthe understatement of an asset.

4.2. H2—Subadditivity

In the audit opinion scenario, subjects were asked to provide prob-ability judgments regarding one of the following four possibilitiesregarding a client: issuance of an unqualified opinion (A), a qualified

AUDITOR PROBABILITY JUDGMENTS 97

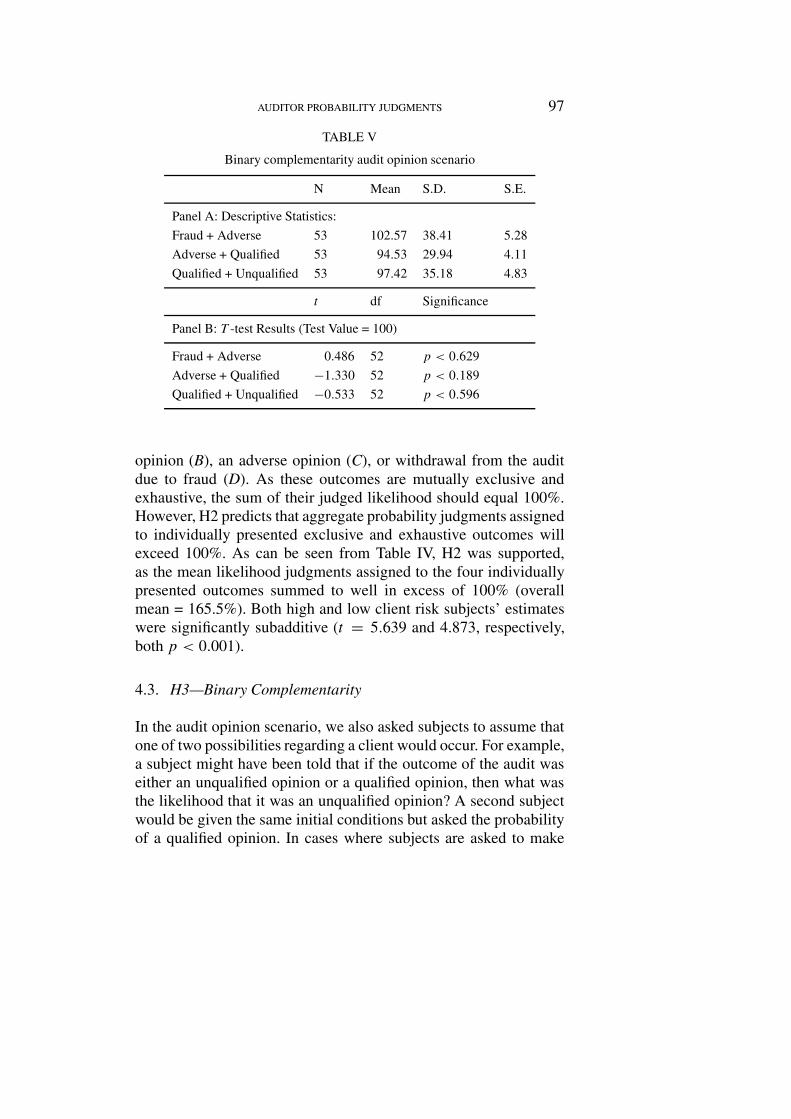

TABLE V

Binary complementarity audit opinion scenario

N Mean S.D. S.E.

Panel A: Descriptive Statistics:

Fraud + Adverse 53 102.57 38.41 5.28

Adverse + Qualified 53 94.53 29.94 4.11

Qualified + Unqualified 53 97.42 35.18 4.83

t df Significance

Panel B: T -test Results (Test Value = 100)

Fraud + Adverse 0.486 52 p < 0.629

Adverse + Qualified −1.330 52 p < 0.189

Qualified + Unqualified −0.533 52 p < 0.596

opinion (B), an adverse opinion (C), or withdrawal from the auditdue to fraud (D). As these outcomes are mutually exclusive andexhaustive, the sum of their judged likelihood should equal 100%.However, H2 predicts that aggregate probability judgments assignedto individually presented exclusive and exhaustive outcomes willexceed 100%. As can be seen from Table IV, H2 was supported,as the mean likelihood judgments assigned to the four individuallypresented outcomes summed to well in excess of 100% (overallmean = 165.5%). Both high and low client risk subjects’ estimateswere significantly subadditive (t = 5.639 and 4.873, respectively,both p < 0.001).

4.3. H3—Binary Complementarity

In the audit opinion scenario, we also asked subjects to assume thatone of two possibilities regarding a client would occur. For example,a subject might have been told that if the outcome of the audit waseither an unqualified opinion or a qualified opinion, then what wasthe likelihood that it was an unqualified opinion? A second subjectwould be given the same initial conditions but asked the probabilityof a qualified opinion. In cases where subjects are asked to make

98 R.G. BRODY ET AL.

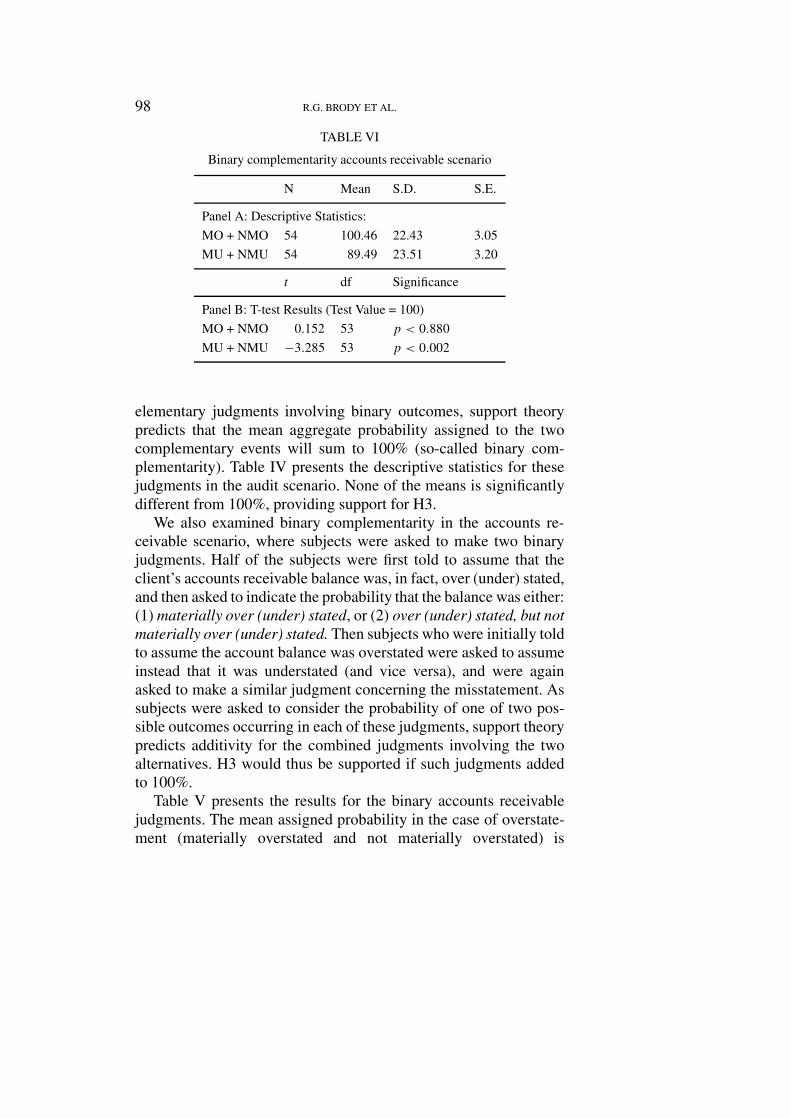

TABLE VI

Binary complementarity accounts receivable scenario

N Mean S.D. S.E.

Panel A: Descriptive Statistics:

MO + NMO 54 100.46 22.43 3.05

MU + NMU 54 89.49 23.51 3.20

t df Significance

Panel B: T-test Results (Test Value = 100)

MO + NMO 0.152 53 p < 0.880

MU + NMU −3.285 53 p < 0.002

elementary judgments involving binary outcomes, support theorypredicts that the mean aggregate probability assigned to the twocomplementary events will sum to 100% (so-called binary com-plementarity). Table IV presents the descriptive statistics for thesejudgments in the audit scenario. None of the means is significantlydifferent from 100%, providing support for H3.

We also examined binary complementarity in the accounts re-ceivable scenario, where subjects were asked to make two binaryjudgments. Half of the subjects were first told to assume that theclient’s accounts receivable balance was, in fact, over (under) stated,and then asked to indicate the probability that the balance was either:(1) materially over (under) stated, or (2) over (under) stated, but notmaterially over (under) stated. Then subjects who were initially toldto assume the account balance was overstated were asked to assumeinstead that it was understated (and vice versa), and were againasked to make a similar judgment concerning the misstatement. Assubjects were asked to consider the probability of one of two pos-sible outcomes occurring in each of these judgments, support theorypredicts additivity for the combined judgments involving the twoalternatives. H3 would thus be supported if such judgments addedto 100%.

Table V presents the results for the binary accounts receivablejudgments. The mean assigned probability in the case of overstate-ment (materially overstated and not materially overstated) is

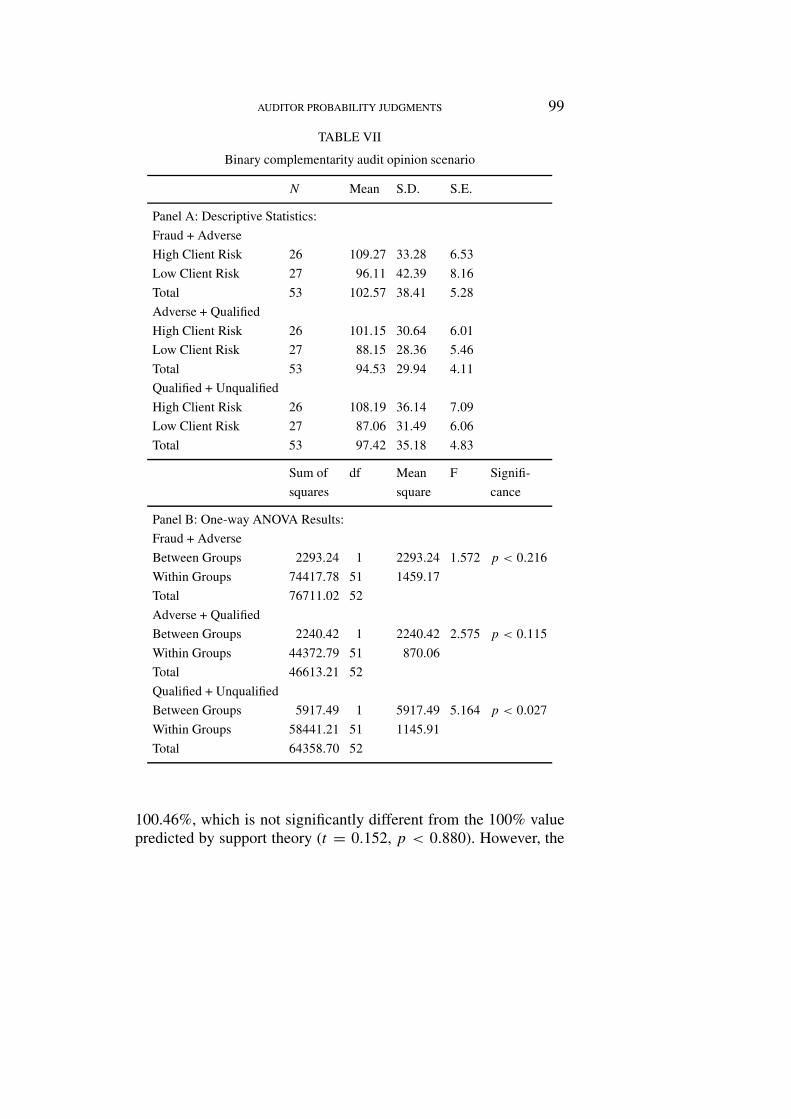

AUDITOR PROBABILITY JUDGMENTS 99

TABLE VII

Binary complementarity audit opinion scenario

N Mean S.D. S.E.

Panel A: Descriptive Statistics:

Fraud + Adverse

High Client Risk 26 109.27 33.28 6.53

Low Client Risk 27 96.11 42.39 8.16

Total 53 102.57 38.41 5.28

Adverse + Qualified

High Client Risk 26 101.15 30.64 6.01

Low Client Risk 27 88.15 28.36 5.46

Total 53 94.53 29.94 4.11

Qualified + Unqualified

High Client Risk 26 108.19 36.14 7.09

Low Client Risk 27 87.06 31.49 6.06

Total 53 97.42 35.18 4.83

Sum of df Mean F Signifi-

squares square cance

Panel B: One-way ANOVA Results:

Fraud + Adverse

Between Groups 2293.24 1 2293.24 1.572 p < 0.216

Within Groups 74417.78 51 1459.17

Total 76711.02 52

Adverse + Qualified

Between Groups 2240.42 1 2240.42 2.575 p < 0.115

Within Groups 44372.79 51 870.06

Total 46613.21 52

Qualified + Unqualified

Between Groups 5917.49 1 5917.49 5.164 p < 0.027

Within Groups 58441.21 51 1145.91

Total 64358.70 52

100.46%, which is not significantly different from the 100% valuepredicted by support theory (t = 0.152, p < 0.880). However, the

100 R.G. BRODY ET AL.

mean for the case of understatement (materially understated andnot materially understated) is significantly lower than 100% (t =−3.285, p < 0.002). Thus, H3 is supported for overstatement judg-ments but not for judgments involving understatement.

Client risk had a significant effect on binary judgments in theaudit opinion and accounts receivable scenarios. The results of anANOVA investigating the effect of client risk in the audit opinionscenario are presented in Table VI. Here, the client risk factor wassignificant only for the qualified vs. unqualified judgment (meanjudgments = 108.19 and 87.06% for high ad low risk, respectively,F = 5.164, p < 0.027), and is insignificant in other two cases(adverse versus qualified and fraud versus adverse). This result in-dicates that subjects are sensitive to client risk in making binaryjudgments between a negative and a positive report, and that they donot consider client risk when they are facing decisions about auditopinions that are both negative in nature.

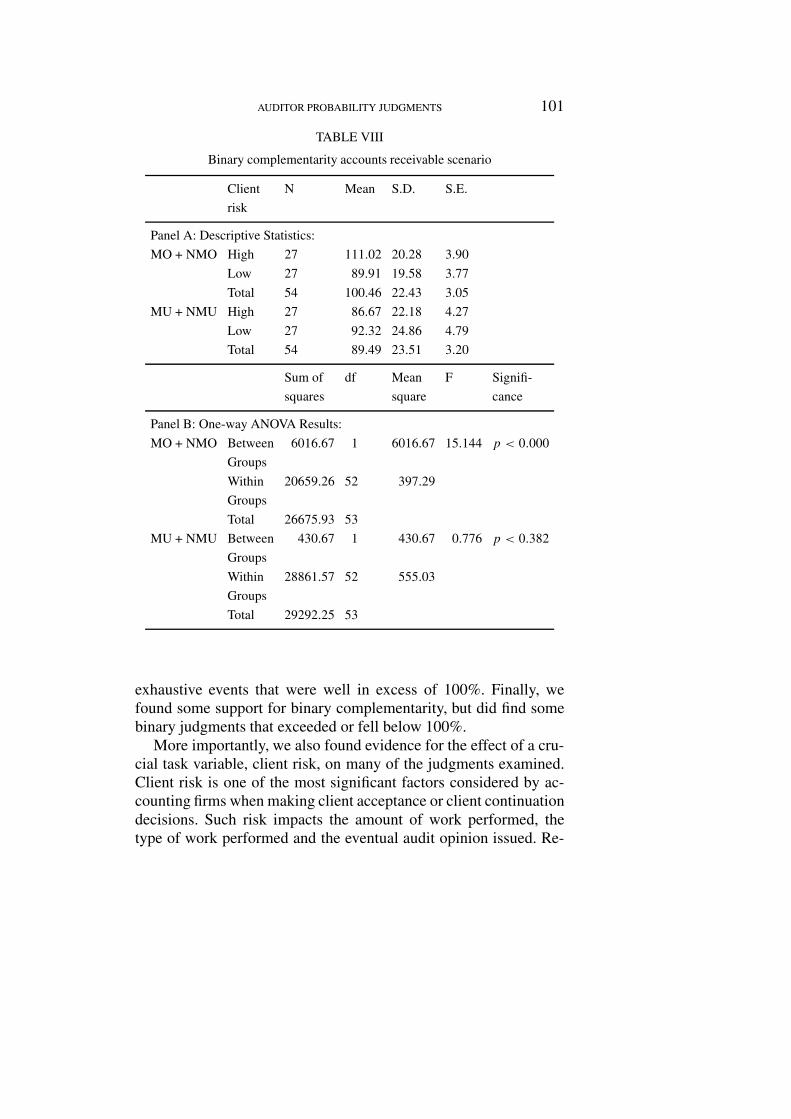

Results for the effect of client risk in the accounts receivablescenario are presented in Table VIII. The probability assigned tothe case of ‘not overstated’ and ‘materially not overstated’ is sig-nificantly higher than 100% (mean is 111.02) for a high risk clientand is lower than 100% (mean = 89.91) for a low risk client (F =15.144, p < 0.000). No such difference is present for judgments in-volving understatement. Thus support theory’s prediction of binarycomplementarity appears to be affected by client risk for situationsinvolving asset overstatement by a high risk client.

5. CONCLUSIONS

5.1. Interpretation of results

The results of this study are the first to offer evidence to supportthe generalizability of Tversky and Koehler’s (1994) support theoryto audit settings. We found that unpacking a hypothesis concerningan inventory misstatement into four formally equivalent hypothesesmore than doubled its perceived likelihood. Similar findings wereobtained regarding the valuation of a client’s accounts receivablebalance. Our hypothesis involving subadditivity was also supported,as subjects provided aggregate judgments of mutually exclusive and

AUDITOR PROBABILITY JUDGMENTS 101

TABLE VIII

Binary complementarity accounts receivable scenario

Client N Mean S.D. S.E.

risk

Panel A: Descriptive Statistics:

MO + NMO High 27 111.02 20.28 3.90

Low 27 89.91 19.58 3.77

Total 54 100.46 22.43 3.05

MU + NMU High 27 86.67 22.18 4.27

Low 27 92.32 24.86 4.79

Total 54 89.49 23.51 3.20

Sum of df Mean F Signifi-

squares square cance

Panel B: One-way ANOVA Results:

MO + NMO Between 6016.67 1 6016.67 15.144 p < 0.000

Groups

Within 20659.26 52 397.29

Groups

Total 26675.93 53

MU + NMU Between 430.67 1 430.67 0.776 p < 0.382

Groups

Within 28861.57 52 555.03

Groups

Total 29292.25 53

exhaustive events that were well in excess of 100%. Finally, wefound some support for binary complementarity, but did find somebinary judgments that exceeded or fell below 100%.

More importantly, we also found evidence for the effect of a cru-cial task variable, client risk, on many of the judgments examined.Client risk is one of the most significant factors considered by ac-counting firms when making client acceptance or client continuationdecisions. Such risk impacts the amount of work performed, thetype of work performed and the eventual audit opinion issued. Re-

102 R.G. BRODY ET AL.

cent high profile company failures (e.g., Enron, Global Crossing)have not only highlighted the significance of audit risk, they havedemonstrated the critical nature of audit judgments.

Thus, while support theory appears to be generalizable to anauditing context, important features of the audit environment ap-pear to affect its descriptive validity. Further research is necessaryto determine what other task-specific features of the auditing envir-onment might also affect the predictions of support theory.

In addition to the theoretical significance of these results, thereis also a great deal of practical significance. Auditing professionalsoperate in a highly litigious environment and any additional know-ledge about their decision making process contributes towards im-provements that can be made in this process. Due to the inherentlimitations in conducting complex behavioral research with audit-ing professionals, it is often difficult to provide additional insightsinto certain areas of audit decision-making. These results provideevidence as to the relevance and continued significance of researchin this area.

5.2. Implications for future research

We examined the effect of client risk on the predictions of supporttheory but did not specify hypotheses involving risk because therewas no theoretical support for doing so. However, it appears that thepossible effect of client risk on binary judgments may be worthyof additional study, given our results. Ayton (1997) notes that theremay be factors that cause binary judgments to be subadditive andsometimes superadditive (i.e., sum to less than 100%), but doesnot offer specific suggestions that could guide audit researchers indeveloping empirically testable hypotheses in this regard. Anotherpossible extension of the study would be to examine probabilityjudgments conditioned on transaction cycles instead of on audit ob-jectives. Subadditivity might be enhanced in this case, as auditorsless able to accurately judge error frequencies in such situations(Nelson et al., 1995). Overall, additional audit research examiningsupport theory appears warranted, as it also remains to be seen ifjudgments that do not conform to standard probability theory causesuboptimal performance in practice.

AUDITOR PROBABILITY JUDGMENTS 103

NOTES

1. This has also been termed supra-additivity (e.g., Asare and Wright, 1995).Since we examine Tversky and Koehler’s support theory, we have chosen touse their terminology.

2. Research has found aggregate judgments of explicit disjunctions in excessof 100% (e.g., Teigen, 1983, 1988; Asare and Wright, 1995). Possible ex-planations include lack of formal statistical training (Teigen, 1983, 1988) ormethodological problems (Asare and Wright, 1995). In the latter study, sub-jects were instructed to treat five possible outcomes as mutually exclusive andexhaustive, when in fact two or more of the outcomes could well have takenplace at the same time.

3. Instructions to assume a single cycle as the cause of the misstatement areconsistent with previous audit research (e.g., Libby, 1985; Bedard and Biggs,1991; Asare and Wright, 1995, 1997).

4. Asking subjects to make a judgment involving P (A, B) means they are toprovide the judged probability of event A occurring, given that one of event Aor B will occur. P (B, A) is the complement of this.

5. A t-test was also computed under the assumption of unequal variances. Res-ults confirmed the one-way ANOVA result that means of the groups (packedand unpacked) are significantly different at p < 0.000.

REFERENCES

Asare, S. and Wright, A. (1995), Normative and substantive expertise in mul-tiple hypotheses evaluation, Organizational Behavior and Human DecisionProcesses 64, 171–184.

Asare, S. and Wright, A. (1997), Evaluation of competing hypotheses in auditing,Auditing, A Journal of Theory and Practice 16, 1–13.

Ayton, P. (1997), How to be incoherent and seductive, Bookmakers’ odds andsupport theory, Organizational Behavior and Human Decision Processes 72,99–115.

Bedard, J. and Biggs, S. (1991), Processes of pattern recognition and hypothesisgeneration in analytical review, The Accounting Review 66, 622–642.

Fischhoff, B., Slovic, P. and Lichtenstein, S. (1978), Fault trees: Sensitivity of es-timated failure probabilities to problem representation, Journal of ExperimentalPsychology: Human Perception and Performance 4, 330-344.

Fox, C. R., Rogers, B. and Tversky, A. (1996), Options traders exhibit subadditivedecision weights, Journal of Risk and Uncertainty 13, 5–17.

Gavanski, I. and Hui, C. (1992), Natural sample spaces and uncertain belief,Journal of Personality and Social Psychology (November), 766–780.

Heiman, V. (1990), Auditors’ assessments of likelihood explanations duringanalytical review. The Accounting Review 65, 875–890.

104 R.G. BRODY ET AL.

Libby, R. (1985), Availability and the generation of hypotheses in analyticalreview, Journal of Accounting Research 23, 648–667.

Nelson, M., Libby, R. and Bonner, S. (1995), Knowledge structures and the es-timation of conditional probabilities in audit planning, The Accounting Review70, 27–47.

Redelmeier, D., Koehler, D. J., Liberman, V. and Tversky, A. (1995), Probabilityjudgment in medicine: Discounting unspecified possibilities, Medical DecisionMaking 15, 227–230.

Sherman, S., McMullen, M. and Gavanski, I. (1992), Natural sample spacesand the inversion of conditional judgments, Journal of Experimental SocialPsychology 28, 401–421.

Smith, J. and Kida, T. (1991), Heuristics and biases: Expertise and task realism inauditing, Psychological Bulletin 109, 472–489.

Teigen, K. (1983), Studies in subjective probability III: The unimportance ofalternatives, Scandinavian Journal of Psychology 24, 97–105.

Teigen, K. (1988), When are low-probability events judged to be ‘probable’?Effects of outcome-set characteristics on verbal probability estimates, ActaPsychologia 68, 157–174.

Tversky, A. and Fox, C. (1995), Weighing risk and uncertainty, PsychologicalReview 102, 269–283.

Tversky, A. and Koehler, D. (1994), Support theory: A nonextensional represent-ation of subjective probability, Psychological Review 101(4), 547–567.

Wallsten, T. S., Budescu, D. A. and Zwick, R. (1992), Comparing the calibrationand coherence of numerical and verbal probability judgments, ManagementScience 39, 176–190.

Windschitl, P. (2000), The binary additivity of subjective probability does notindicate the binary complementarity of perceived certainty, OrganizationalBehavior and Human Decision Processes 81, 195–225.

Address for correspondence: Dr. Richard G. Brody, Department of Accounting,University of New Haven, 300 Orange Avenue, West Haven, CT 06516, USA.Phone: +1-(203)-932-7450; Fax: +1-(203)-931-6092;E-mail: [email protected]