Embed Size (px)

Citation preview

i NSSF Audited Financial Statements for 2021

AUDITED FINANCIALSTATEMENTS 2021For the year ending 30 June 2021

“Delivering a triumphant return amid a pandemic induced new normal – we rose up; sailed through the waves of change to make lives better for all”Workers House, NSSF Headquarters

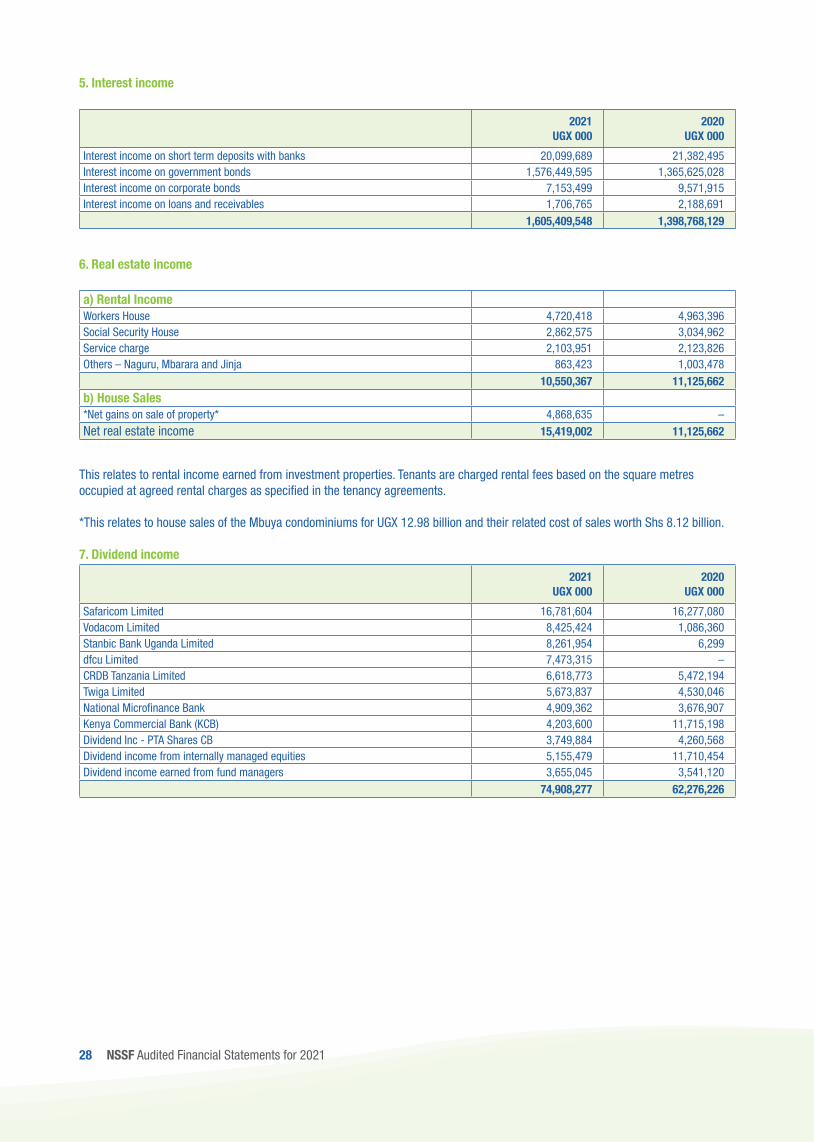

TABLE OF CONTENTS

National Social Security Fund financial statements for theyear ending 30 June 2021

Fund information 1–2Report of the directors 3Statement of directors’ responsibilities 4–5Report of the independent auditor 6–8

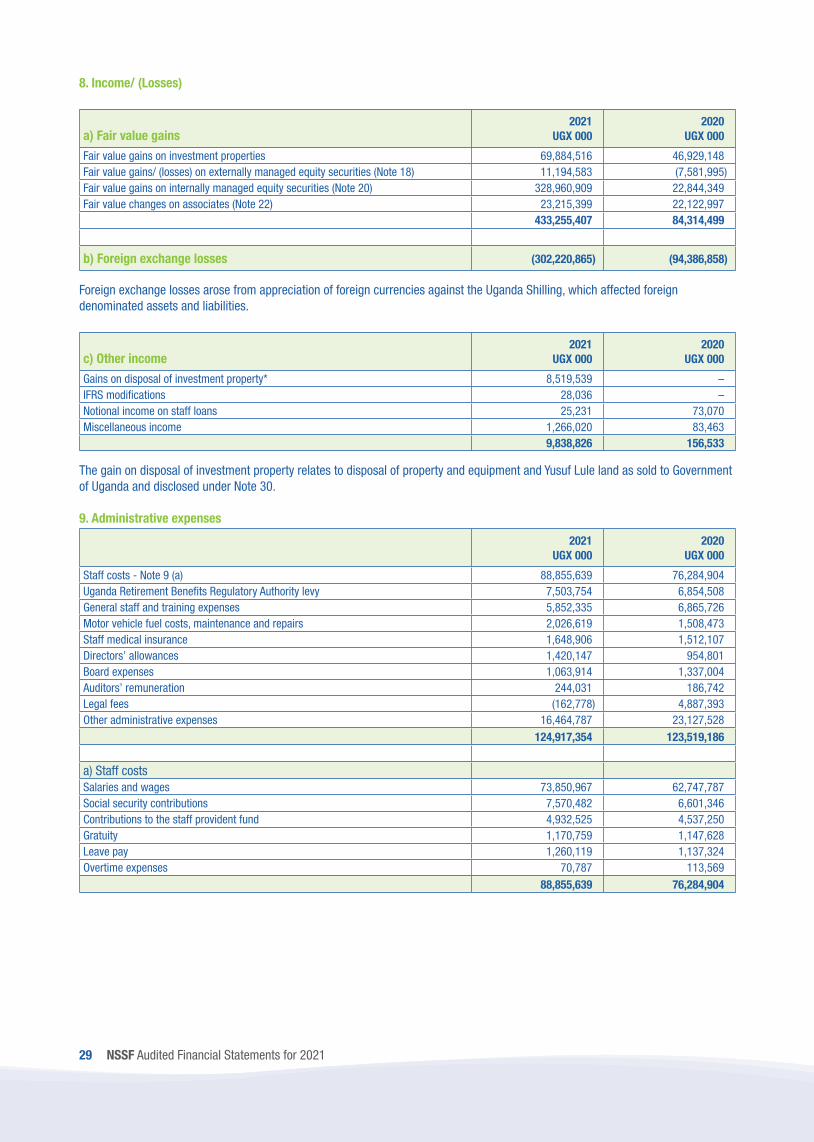

CONTENTS

Statement of changes in net assets available for benefits 9Statement of net assets available for benefits 10Statement of changes in members’ funds and reserves 11Statement of cash flows 12Notes to the financial statements 13

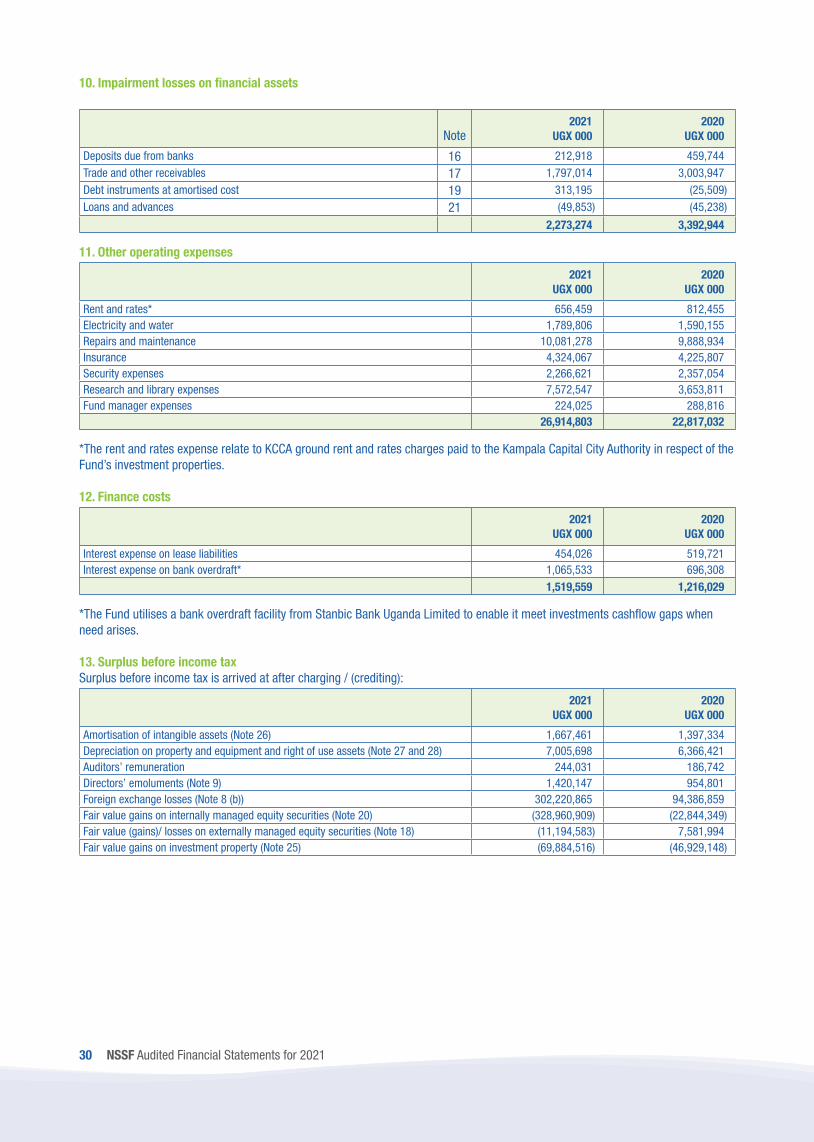

FINANCIAL STATEMENTS

1 NSSF Audited Financial Statements for 2021

FUND INFORMATIONDIRECTORS

Dr. Peter Kimbowa Chairman (Appointed on 1 September 2021)Mr. Richard Byarugaba Managing DirectorMr. Patrick Ocailap MemberMr. Aggrey David Kibenge Member (Appointed 10 November 2020)Ms. Penninah Tukamwesiga MemberDr. Sam Lyomoki Member (Appointed on 1 September 2021)Mr. Bahemuka Julius Member (Appointed on 1 September 2021)Mr. Lwabayi Mudiba Hassan Member (Appointed on 1 September 2021)Mr. Fred K. Bamwesigye MemberDr. Silver Mugisha Member (Appointed on 1 September 2021)Mr. Patrick Byabakama Kaberenge Chairman (Appointment term ended on 31 August 2021)Mr. Peter Christopher Werikhe Member (Appointment term ended on 31 August 2021)Dr. Isaac E.W Magoola Member (Appointment term ended on 31 August 2021)Mr. D. Stephen Mugole Mauku Member (Appointment term ended on 31 August 2021)Mrs. Florence Namatta Mawejje Member (Appointment term ended on 31 August 2021)

REGISTERED OFFICE14th Floor, Workers HousePlot No. 1, Pilkington RoadP. O. Box 7140Kampala

AUDITORThe Auditor GeneralOffice of the Auditor GeneralApollo Kaggwa RoadP. O. Box 7083Kampala

DELEGATED AUDITORPricewaterhouseCoopersCertified Public Accountants10th Floor, Communications House1 Colville StreetP. O. Box 882Kampala, Uganda

Sebalu & Lule AdvocatesS&L ChambersPlot 14, Mackinnon RoadP. O. Box 2255Kampala, Uganda

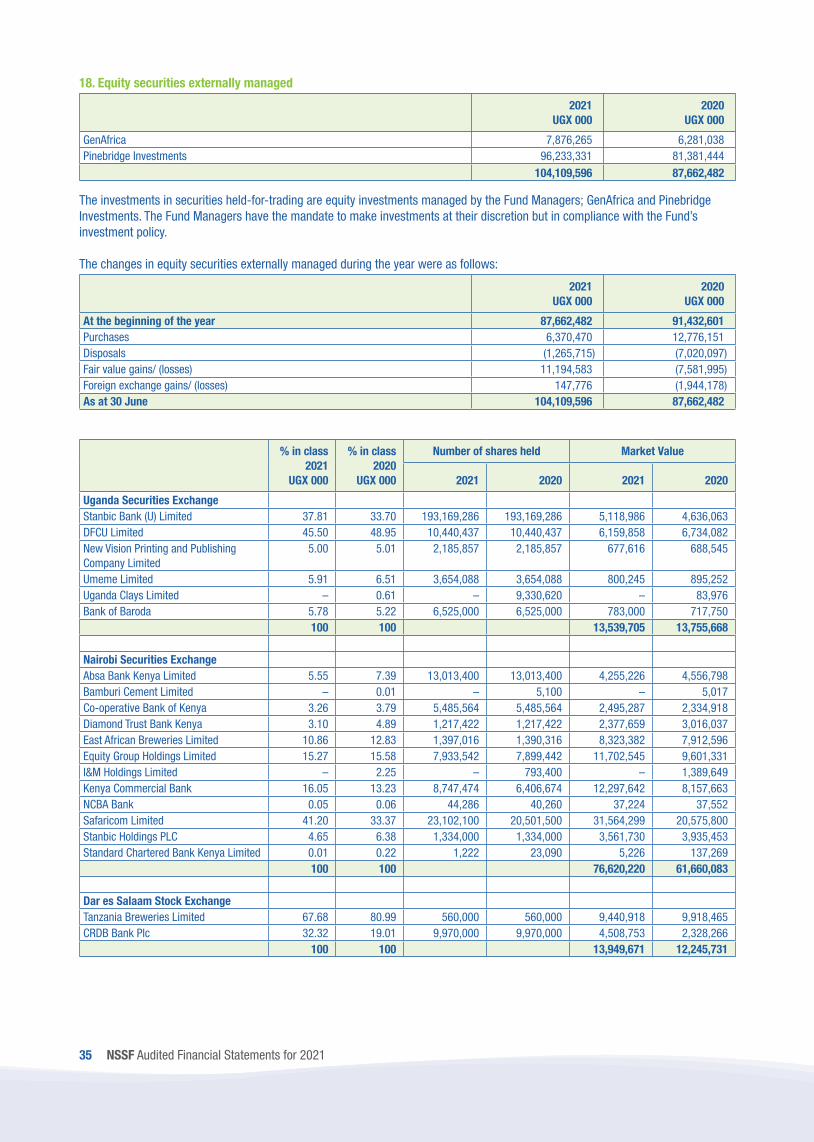

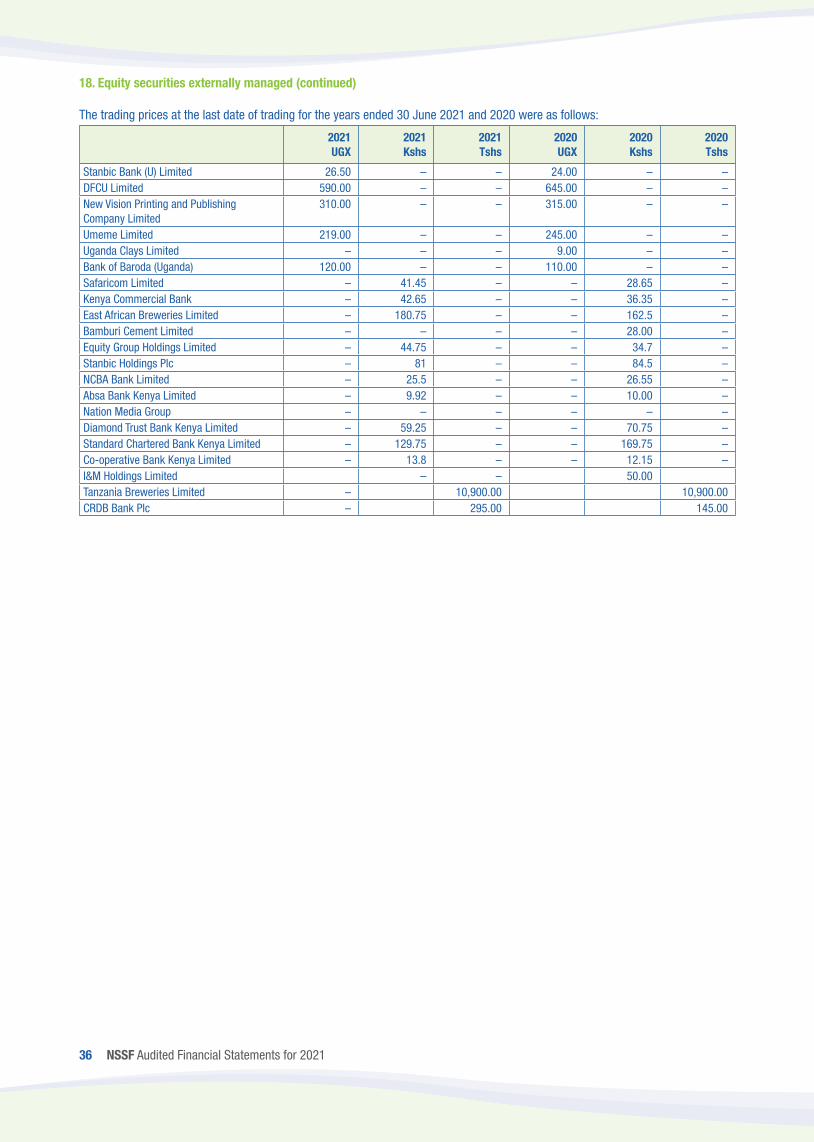

Kampala Associated AdvocatesPlot 14, Nakasero RoadP. O. Box 9566Kampala, Uganda

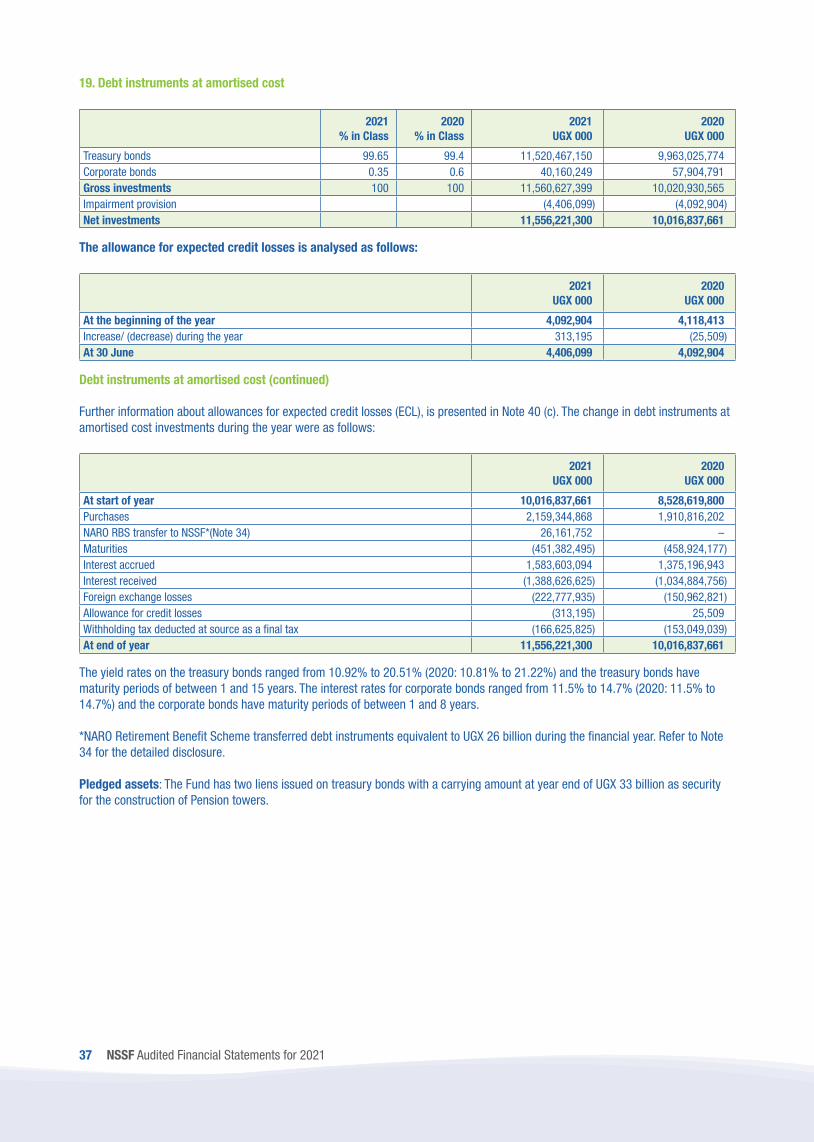

GP Advocates(Formerly Omunyokol & Co. Advocates)Colline House, 3rd FloorPlot 4, Pilkington RoadP. O. Box 6737Kampala, Uganda

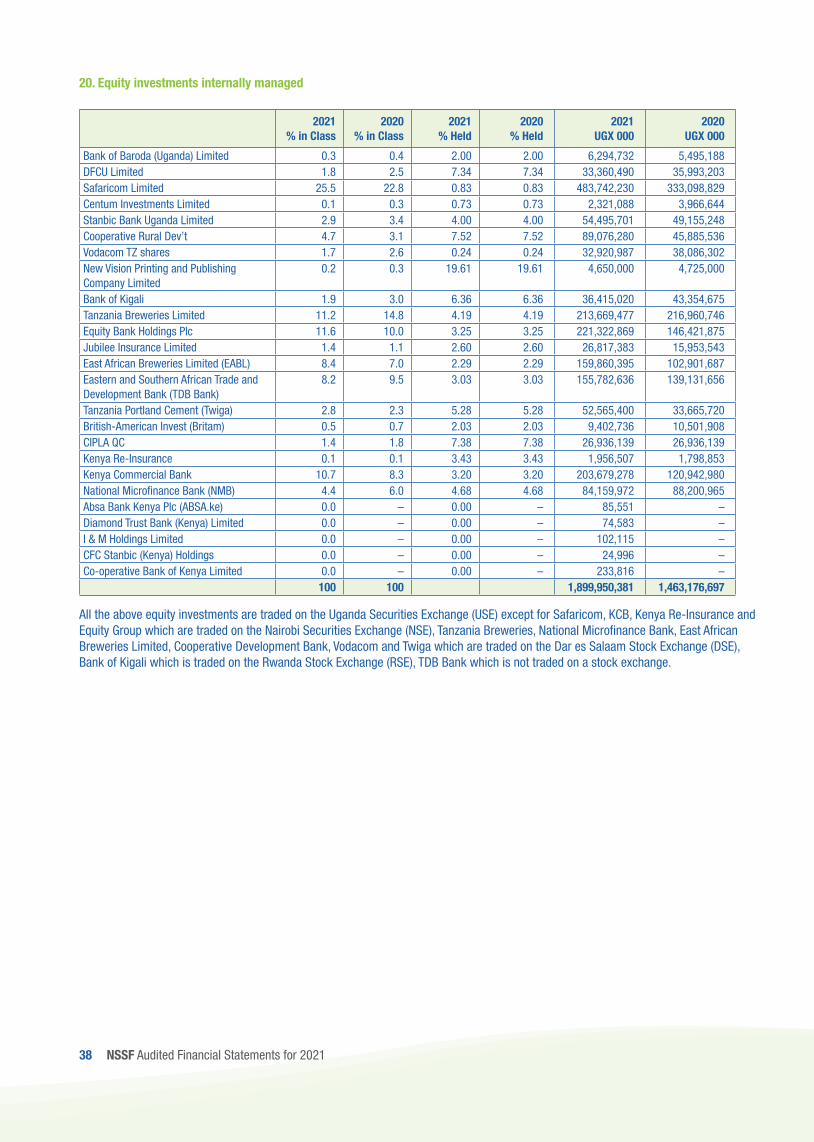

Kiwanuka & Karugire AdvocatesPlot 5A2, Acacia AvenueP. O. Box 6061Kampala, Uganda

Kasirye, Byaruhanga & Co. AdvocatesPlot 33, Clement AvenueP. O. Box 10946Kampala, Uganda

Nangwala Rezida & Co. AdvocatesPlot 9, Yusuf Lule RoadP. O. Box 10304Kampala, Uganda

ADVOCATES

2 NSSF Audited Financial Statements for 2021

Standard Chartered Bank Uganda LimitedSpeke RoadP. O. Box 7111Kampala, Uganda

Stanbic Bank Uganda LimitedPlot 17 Hannington RoadP. O. Box 7131Kampala, Uganda

Housing Finance BankPlot 25 Kampala RoadP. O. Box 1539Kampala, Uganda

Tropical Bank LimitedPlot 27 Kampala RoadP. O. Box 9485Kampala, Uganda

Bank of AfricaPlot 45 Jinja RoadP. O. Box 2750Kampala, Uganda

United Bank for Africa (Uganda) LimitedPlot 2, Jinja RoadP. O. Box 7396Kampala, Uganda

Ecobank Uganda LimitedPlot 4 Parliament AvenueP. O. Box 7368Kampala, Uganda

Finance Trust Bank LimitedPlot 121 & 115, Block 6, KatweP. O. Box 6972Kampala, Uganda

Exim Bank Uganda LimitedPlot 6, Hannington RoadP. O. Box 36206Kampala, Uganda

Orient Bank LimitedOrient Plaza No. 14 Kampala RoadP. O. Box 3072Kampala, Uganda

Post Bank Uganda LimitedPlot 4/6 Nkurumah RoadP. O. Box 7189Kampala, Uganda

Citibank Uganda LimitedPlot 4, Ternan Avenue NakaseroP. O. Box 7505Kampala, Uganda

Bank of Baroda Uganda LimitedPlot 18 Kampala RoadP. O. Box 7197Kampala, Uganda

Absa Bank Uganda LimitedPlot 2A & 4A, Nakasero RoadP. O. Box 7101Kampala, Uganda

dfcu Bank LimitedPlot 26, Kyadondo RoadP. O. Box 70Kampala, Uganda

Centenary Rural Development BankPlot 44-46 Kampala RoadP. O. Box 1892Kampala, Uganda

Diamond Trust Bank Uganda LimitedPlot 17/19, Kampala RoadP. O. Box 7155Kampala, Uganda

Equity Bank Uganda LimitedPlot 390, Muteesa Road KampalaP. O. Box 10184Kampala, Uganda

Guaranty Trust Bank Uganda LimitedPlot 56 Kiira RoadP. O. Box 7323Kampala, Uganda

KCB Bank Uganda LimitedPlot 7 Kampala RoadP.O. Box 7399Kampala, Uganda

NCBA Bank Uganda LimitedRwenzori TowersP. O. Box 28707Kampala, Uganda

BANKERS

3 NSSF Audited Financial Statements for 2021

REPORT OF THE DIRECTORS

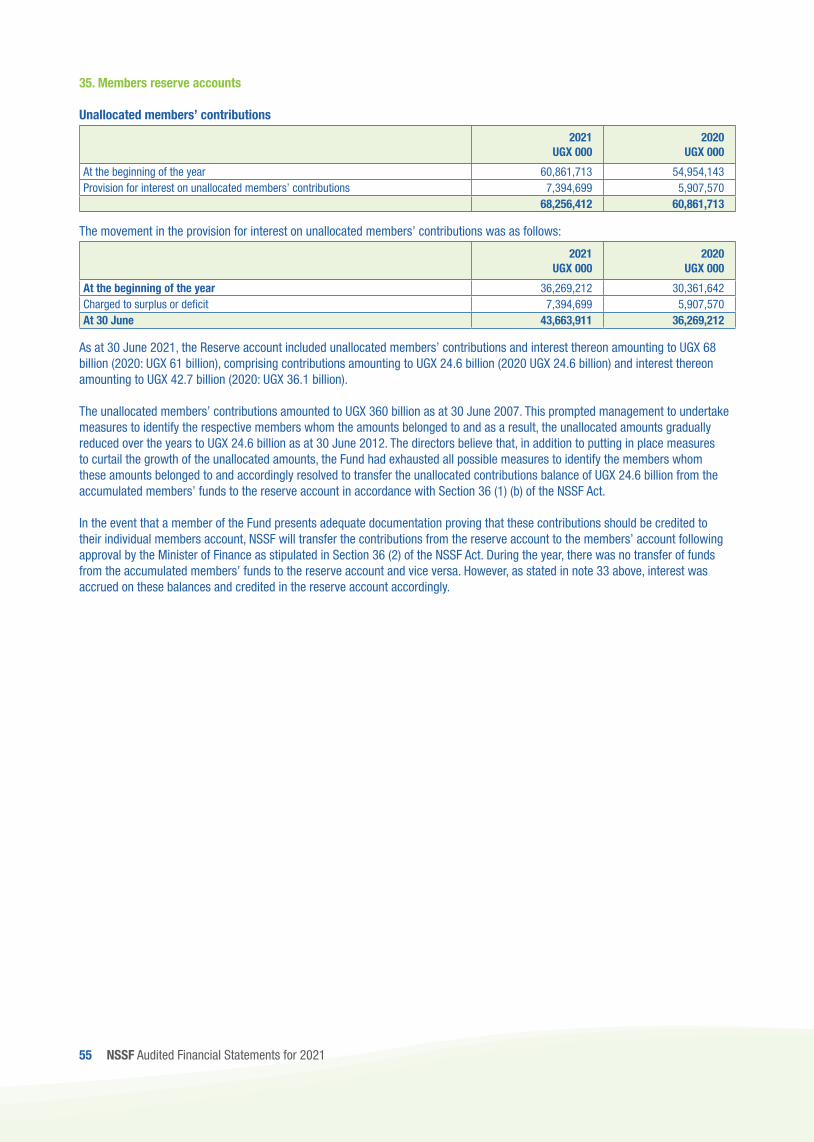

The Directors submit their report together with the audited financial statements for the year ended 30 June 2021 which disclose the state of affairs of the National Social Security Fund (‘the Fund’ or “NSSF”), in accordance with Section 32 (Cap. 222) of the National Social Security Fund Act (‘NSSF Act’).

1. IncorporationThe Fund is a corporate body established by an Act of Parliament and is domiciled in Uganda and licensed as a Retirement Benefit Scheme under the Uganda Retirement Benefits Regulatory Act (2011).

2. Principal activityThe Fund was established by an Act of Parliament to provide for its membership, payment of contributions to, and payment of benefits out of the Fund. NSSF is a provident fund that pays out contributions in lump sum. It is open to all employees in the private sector including Non-Governmental Organizations that are not covered by the Government’s pension scheme. It is a scheme instituted for the protection of employees against the uncertainties of social and economic life. The Fund is financed by employees’ and employers’ contributions. The total contribution is 15% of the employees’ gross salary, of which the employer is entitled to recover 5% from the employee.

3. Results from operationsThe results of the Fund are set out on page 9.

4. Interest to membersInterest is computed based on the opening balances of the members’ funds less benefits paid during the year. The interest rate used to allocate interest for the year the year ended 30 June 2021 was 12.15% (2020: 10.75%).

5. Reserves and accumulated fundsThe reserves of the Fund and the accumulated member funds are set out on Page 11 and Page 53.

6. Unallocated members’ fundsThese are collections received from employers that have not yet been allocated to individual member accounts due to incomplete details of the members. Management has put in place mechanisms to continuously follow up the missing details from the employers to update the individual members’ accounts.

7. DirectorsThe Directors who held office during the year and up to the date of this report are set out on page 1.

8. AuditorsIn accordance with Section 32 (2) of the NSSF Act (Cap 222) Laws of Uganda, the financial statements are required to be audited once every year by the Auditor General of Uganda or an auditor appointed by him to act on his behalf. For the year ended 30 June 2021, PricewaterhouseCoopers Certified Public Accountants was appointed to act on behalf of the Auditor General.

9. Approval of the financial statementsThe financial statements were approved at the meeting of the Directors held on 17th September 2021.

By Order of the Board,

Ms Agnes Tibayeita IsharazaCORPORATION SECRETARY

STATEMENT OF DIRECTORS’ RESPONSIBILITIES

The Uganda Retirement Benefits Regulatory Authority (URBRA) Act 2011 and Regulations require the Directors to make available to the Fund’s members and other parties, audited financial statements for each financial year which show a true and fair view of the state of affairs of the Fund as at the end of the financial year.

It also requires the Directors to ensure that the Fund keeps proper accounting records which disclose with reasonable accuracy the financial position of the Fund and safeguard the assets of the Fund.

The Directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, the URBRA Act and National Social Security Fund (NSSF) Act 1985; and, for such internal controls as directors determine are necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

The Board of Directors confirm that, during the year under review, in the execution of their duties they have complied with the requirements imposed by URBRA Act and the NSSF Act. The Directors also confirm that:

• Adequate accounting records were kept inclusive of proper minutes of all resolutions passed by the Board of Directors;• They took such steps as were reasonably open to them to safeguard the assets of the Fund and to prevent and detect fraud and

other irregularities;• Proper internal control systems were employed by or on behalf of the Fund;• Adequate and appropriate information was communicated to the members including their rights, benefits and duties in terms of

the rules of the Fund;• Reasonable steps to ensure that contributions, where applicable, were paid timely to the Fund;• Expert advice was obtained on matters where they lacked sufficient expertise;• The rules, operation and administration of the Fund complied with the URBRA Act and all applicable legislation; and,• Funds were invested and maintained in accordance with the Fund’s investment policy statement and Investment Regulations

issued by URBRA.

Approval of the annual financial statementsThe Directors accept responsibility for the annual financial statements, which have been prepared using appropriate accounting policies supported by reasonable and prudent judgments and estimates, in conformity with IFRS and the NSSF Act. The Directors are of the opinion that the financial statements give a true and fair view of the financial affairs of the Fund and its operating results.

The Directors ascertain that the auditor was given unrestricted access to all financial information and all representations made to them during their audit were valid and appropriate.

Notwithstanding the above-mentioned information, the Directors wish to draw attention to fact that the Fund did not appoint a fund manager for internally managed investments as required by section 60 (2) of the URBRA Act after undertaking a cost-benefit analysis which indicated that the internal risk controls were sufficient in that regard.

The financial statements for the year ended June 2020 have been restated to modify the presentation in line with the requirements of IAS 26, Accounting and Reporting for Retirement Benefit Plans.

4 NSSF Audited Financial Statements for 2021

5 NSSF Audited Financial Statements for 2021

Dr. Peter KimbowaCHAIRMAN

Mr. Richard ByarugabaMANAGING DIRECTOR

Dr Silver MugishaDIRECTOR

Date: 24 September 2021

STATEMENT OF DIRECTORS’ RESPONSIBILITIES (CONTINUED)

These financial statements:• were approved by the Board of Directors on17th September 2021;• are, to the best of the Directors’ knowledge and belief, confirmed to be complete and correct; and,• fairly represent the net assets of the Fund as at 30 June 2021 as well as the results of its activities for the year then ended in

accordance with IFRS.

In preparing the financial statements, the Directors have assessed the Fund’s ability to continue as a going concern. In performing this assessment, the Directors have considered the results of the Fund’s assessment of the possible impact on its cash flows and operations as a result of the macroeconomic impact of Covid-19 on the local Ugandan market and wider international economy that is disclosed in Note 44 of the financial statements. The Directors hereby report that nothing has come to their attention to indicate that the Fund will not remain a going concern for at least twelve months from the date of this statement.

The Directors confirm that for the year ended 30 June 2021, the National Social Security Fund has submitted all regulatory and other returns and any other information as required by the provision of the URBRA Act.

Nothing has come to the attention of the Directors to indicate that the Fund will not be able to meet its obligations and the requirements of the URBRA Act for the next twelve months from the date of this statement.

The new NSSF Board Chairman, Mr. Peter Kimbowa welcomes the Minister of Finance, Matia Kasaija at the 12th Board of Directors inauguaration.

6 NSSF Audited Financial Statements for 2021

REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF NATIONAL SOCIAL SECURITY FUND FOR THE YEAR ENDED 30 JUNE 2021

The Rt. Hon. Speaker of Parliament

Our opinionI have audited the financial statements of National Social Security Fund (NSSF) which comprise the Statement of Net Assets Available for Benefits as at 30th June 2021 and the Statement of Changes in Net Assets Available for Benefits, Statement of Changes in Members’ Funds and Reserves and Statement of Cash Flows for the year then ended, and notes to the financial statements, includinga summary of significant accounting policies as set out on pages 9 to 72.

In my opinion, the financial statements present a true and fair view of the financial position of the Fund as at 30th June 2021, and of its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards and in the manner required by the Uganda Retirement Benefits Regulatory Authority Act and the NSSF Act.

Basis for opinionI conducted my audit in accordance with International Standards on Auditing (ISAs). My responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of my report. I am independent of the Fund in accordance with the Constitution of the Republic of Uganda, 1995 (as amended), the National Audit Act, 2008, theInternational Ethics Standards Board for Accountants (IESBA) Code of Ethics for Professional Accountants (Parts A and B) and other independence requirements applicable to performing audits of Financial Statements in Uganda. I have fulfilled my other ethical responsibilities in accordance with the IESBA Code, and in accordance with other ethical requirements applicable to performing audits in Uganda. I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis for my opinion.

Key audit matterKey audit matters are those matters that, in my professional judgment, were of most significance in my audit of the financial statements of the current period. This matter was addressed in the context of my audit of the Fund’s financial statements as a whole, and in forming my opinion thereon, and I do not provide a separate opinion on these matters. In addition to the matters described below to be the key audit matters to be communicated in my report. For each matter below, my description of how my audit addressed the matters is provided in that context.

I have fulfilled the responsibilities described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of my report, including in relation to these matters. Accordingly, my audit included performance of procedures designed to respond to my assessment of the risks of material misstatement of the financial statements. The results of my audit procedures, including the procedures performed to address the matters, provide the basis for my audit opinion on the accompanying financial statements.

7 NSSF Audited Financial Statements for 2021

REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF NATIONAL SOCIAL SECURITY FUND FOR THE YEAR ENDED 30 JUNE 2021 (CONTINUED)

Details are outlined below:

Key audit matter How our audit addressed the key audit matter

Valuation of investment propertiesAs disclosed in Note 25 of the financial statements, the Directors used independent registered valuers to determine the fair values of investment properties amounting to Shs 852,506 million at 30 June 2021 (2020: Shs 725,470 million).

I considered this a key audit matter due to significant judgment exercised by the Directors and the complexity involved in the determination of the fair value of investment properties.

Specifically, significant judgement has been exercised in:

• determining the valuation techniques used by the external valuers i.e. discounted cash flow, cost approach and sales comparison method taking into consideration the effects of Corona Virus 2019 (Covid – 19) pandemic; and

• evaluation of the assumptions applied in determination of unobservable inputs such as comparable market prices, based on location of the property, projected future cash flows, future rent escalations, exit values and the discount rates relevant in determination of the fair value of investment properties

My audit procedures are summarised as follows:

I reviewed the Fund’s valuation reports for significant investments.

I evaluated the appropriateness of the valuation methodology applied by the Directors in the determination of fair value for consistency with IAS 40;

I tested the Director’s basis for valuation. On a sample basis, I recomputed the expected fair value of the investment property to form an independent judgement as to whether the valuation was in line with the Fund’s policy taking into consideration the expected impact of Covid-19 on various assumptions;

I tested the accuracy of the data used to derive unobservable inputs such as comparable market prices based on location of the property, projected future cash flows, future rent escalations, exit values and the discount rates and independently recomputed unobservable inputs on a sample basis to determine that they were derived in line with the Fund’s valuation policy;

I assessed the competence, objectivity and integrity of the independent valuers. I also reviewed their experience and professional qualifications and

I assessed the adequacy of the disclosures in the financial statements in accordance with IAS 40.

Based on my audit procedure undertaken above, I noted no significant issues in relation to Accounting for valuation of investment properties.

Other informationThe Directors are responsible for the other information. The other information comprises the information included in the Fund Information, the Director’s Report and the Statement of Directors’ Responsibilities, but does not include the financial statements and my audit report thereon.

My opinion on the financial statements does not cover the other information and I do not express any form of assurance conclusion thereon.

In connection with my audit of the financial statements, my responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the financial statements or my knowledge obtained in the audit, or otherwise appears to be materially misstated.

If, based on the work I have performed, I conclude that there is a material misstatement of the other information, I am required to report that fact. I have nothing to report in this regard.

Responsibilities of the Directors for the financial statementsThe Directors are responsible for the preparation of the financial statements that give a true and fair view in accordance with International Financial Reporting Standards, Uganda Retirement Benefits Regulatory Act, National Social Security Act and, for such internal control as the Directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the Directors are responsible for assessing the Fund’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the Directors either intend to liquidate the Fund or to cease operations, or have no realistic alternative but to do so.

REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF NATIONAL SOCIAL SECURITY FUND FOR THE YEAR ENDED 30 JUNE 2021 (CONTINUED)

The Directors are responsible for overseeing the Fund’s financial reporting process.

Auditor’s responsibilities for the audit of the financial statementsMy responsibility as required by Article 163 of the Constitution of the Republic of Uganda and Sections 13 and 19 of the National Audit Act, 2008 is to audit and express an opinion on these statements based on my audit. My objective is to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the financial statements.

As part of an audit in accordance with ISAs, I exercise professional judgment and maintain professional skepticism throughout the audit. I also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the Directors.

Auditor’s responsibilities for the audit of the financial statements• Conclude on the appropriateness of the Directors’ use of the going concern basis of accounting and, based on the audit evidence

obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Fund’s ability to continue as a going concern. If I conclude that a material uncertainty exists, I am required to draw attention in my report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. My conclusion is based on the audit evidence obtained up to the date of my report. However, future events or conditions may cause the Fund to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

I communicate with the Directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that I identify during my audit.

John F.S MuwangaAUDITOR GENERAL24 September 2021

8 NSSF Audited Financial Statements for 2021

9 NSSF Audited Financial Statements for 2021

Note2021

UGX 000

Restated2020

UGX 000

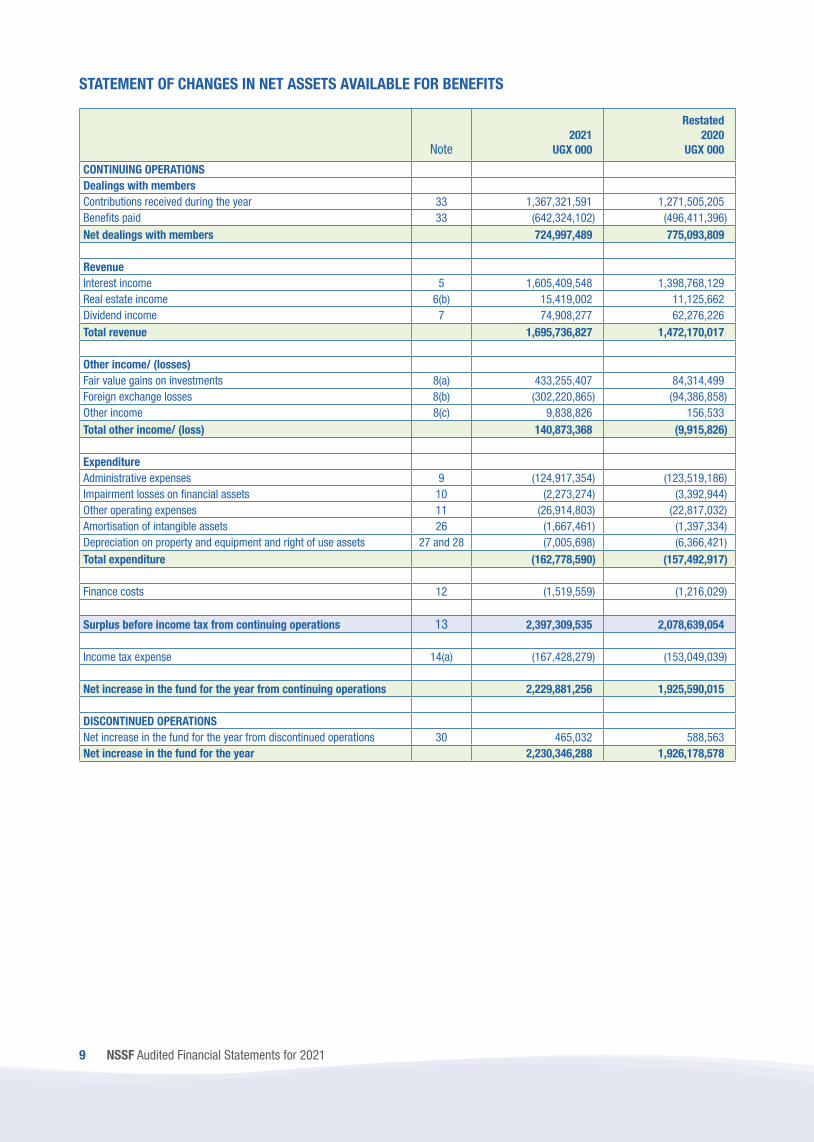

CONTINUING OPERATIONSDealings with membersContributions received during the year 33 1,367,321,591 1,271,505,205Benefits paid 33 (642,324,102) (496,411,396)Net dealings with members 724,997,489 775,093,809

RevenueInterest income 5 1,605,409,548 1,398,768,129Real estate income 6(b) 15,419,002 11,125,662Dividend income 7 74,908,277 62,276,226Total revenue 1,695,736,827 1,472,170,017

Other income/ (losses)Fair value gains on investments 8(a) 433,255,407 84,314,499Foreign exchange losses 8(b) (302,220,865) (94,386,858)Other income 8(c) 9,838,826 156,533Total other income/ (loss) 140,873,368 (9,915,826)

ExpenditureAdministrative expenses 9 (124,917,354) (123,519,186)Impairment losses on financial assets 10 (2,273,274) (3,392,944)Other operating expenses 11 (26,914,803) (22,817,032)Amortisation of intangible assets 26 (1,667,461) (1,397,334)Depreciation on property and equipment and right of use assets 27 and 28 (7,005,698) (6,366,421)Total expenditure (162,778,590) (157,492,917)

Finance costs 12 (1,519,559) (1,216,029)

Surplus before income tax from continuing operations 13 2,397,309,535 2,078,639,054

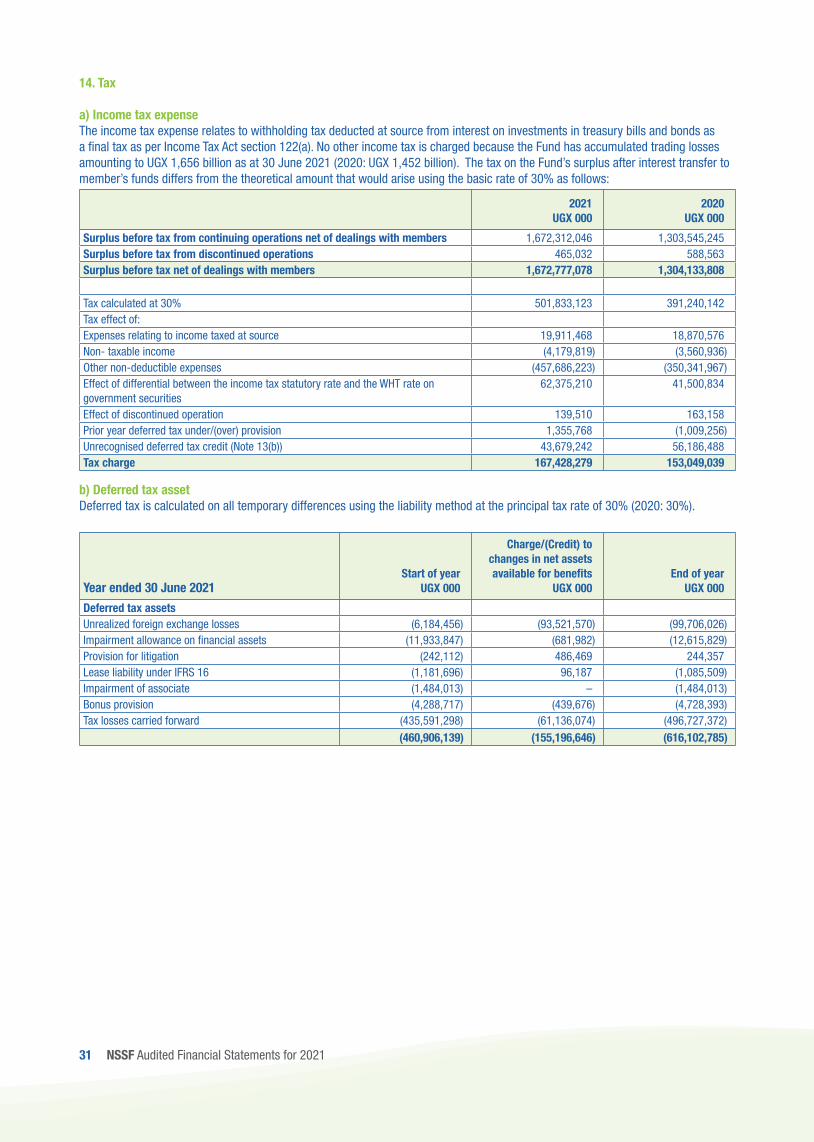

Income tax expense 14(a) (167,428,279) (153,049,039)

Net increase in the fund for the year from continuing operations 2,229,881,256 1,925,590,015

DISCONTINUED OPERATIONSNet increase in the fund for the year from discontinued operations 30 465,032 588,563Net increase in the fund for the year 2,230,346,288 1,926,178,578

STATEMENT OF CHANGES IN NET ASSETS AVAILABLE FOR BENEFITS

10 NSSF Audited Financial Statements for 2021

Note2021

UGX 000

Restated2020

UGX 000

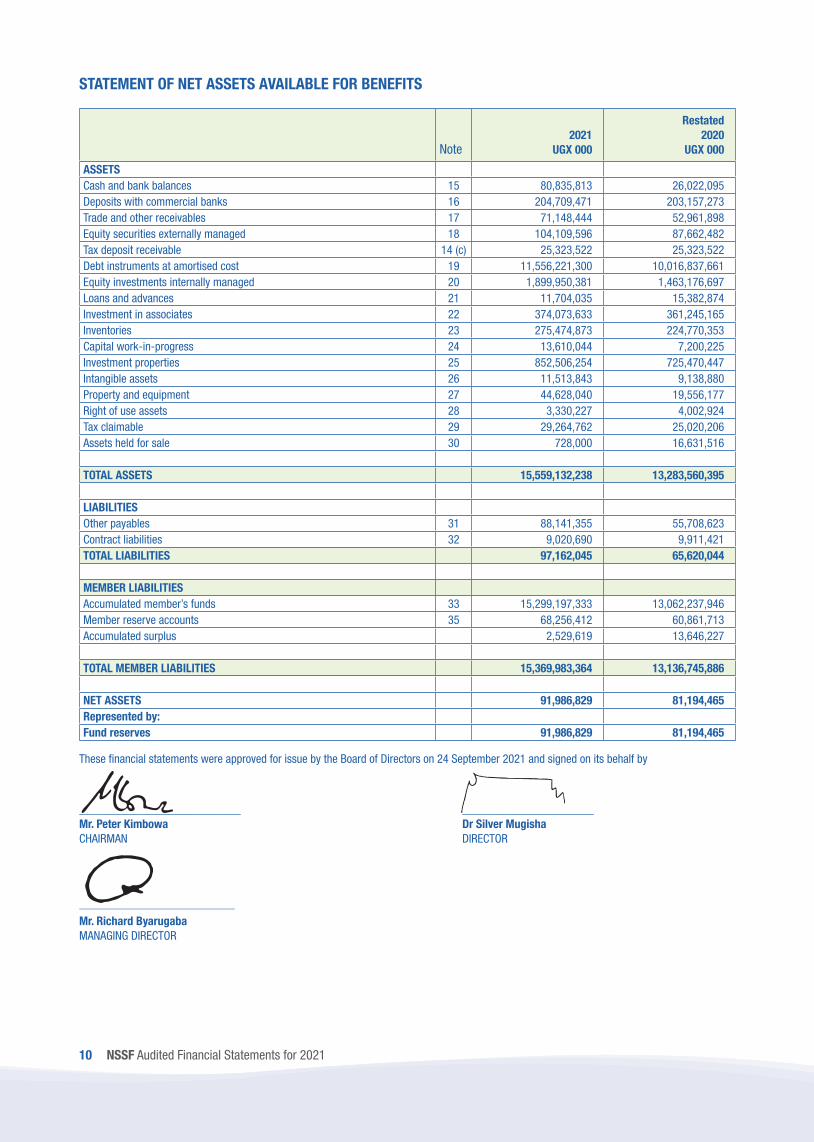

ASSETSCash and bank balances 15 80,835,813 26,022,095Deposits with commercial banks 16 204,709,471 203,157,273Trade and other receivables 17 71,148,444 52,961,898Equity securities externally managed 18 104,109,596 87,662,482Tax deposit receivable 14 (c) 25,323,522 25,323,522Debt instruments at amortised cost 19 11,556,221,300 10,016,837,661Equity investments internally managed 20 1,899,950,381 1,463,176,697Loans and advances 21 11,704,035 15,382,874Investment in associates 22 374,073,633 361,245,165Inventories 23 275,474,873 224,770,353Capital work-in-progress 24 13,610,044 7,200,225Investment properties 25 852,506,254 725,470,447Intangible assets 26 11,513,843 9,138,880Property and equipment 27 44,628,040 19,556,177Right of use assets 28 3,330,227 4,002,924Tax claimable 29 29,264,762 25,020,206Assets held for sale 30 728,000 16,631,516

TOTAL ASSETS 15,559,132,238 13,283,560,395

LIABILITIESOther payables 31 88,141,355 55,708,623Contract liabilities 32 9,020,690 9,911,421TOTAL LIABILITIES 97,162,045 65,620,044

MEMBER LIABILITIESAccumulated member’s funds 33 15,299,197,333 13,062,237,946Member reserve accounts 35 68,256,412 60,861,713Accumulated surplus 2,529,619 13,646,227

TOTAL MEMBER LIABILITIES 15,369,983,364 13,136,745,886

NET ASSETS 91,986,829 81,194,465Represented by:Fund reserves 91,986,829 81,194,465

These financial statements were approved for issue by the Board of Directors on 24 September 2021 and signed on its behalf by

___________________________ ______________________Mr. Peter Kimbowa Dr Silver MugishaCHAIRMAN DIRECTOR

__________________________Mr. Richard ByarugabaMANAGING DIRECTOR

STATEMENT OF NET ASSETS AVAILABLE FOR BENEFITS

11 NSSF Audited Financial Statements for 2021

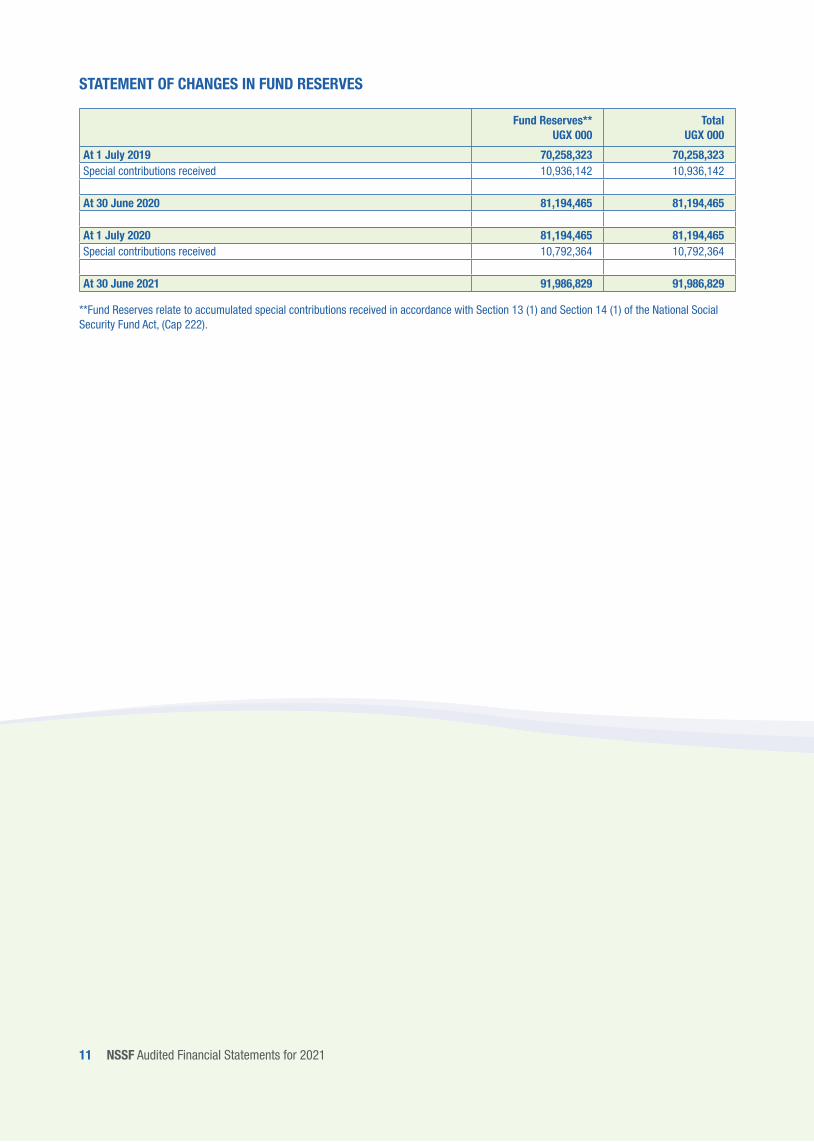

STATEMENT OF CHANGES IN FUND RESERVES

Fund Reserves**UGX 000

TotalUGX 000

At 1 July 2019 70,258,323 70,258,323Special contributions received 10,936,142 10,936,142

At 30 June 2020 81,194,465 81,194,465

At 1 July 2020 81,194,465 81,194,465Special contributions received 10,792,364 10,792,364

At 30 June 2021 91,986,829 91,986,829

**Fund Reserves relate to accumulated special contributions received in accordance with Section 13 (1) and Section 14 (1) of the National Social Security Fund Act, (Cap 222).

12 NSSF Audited Financial Statements for 2021

STATEMENT OF CASH FLOWS

Note2021

UGX 0002020

UGX 000

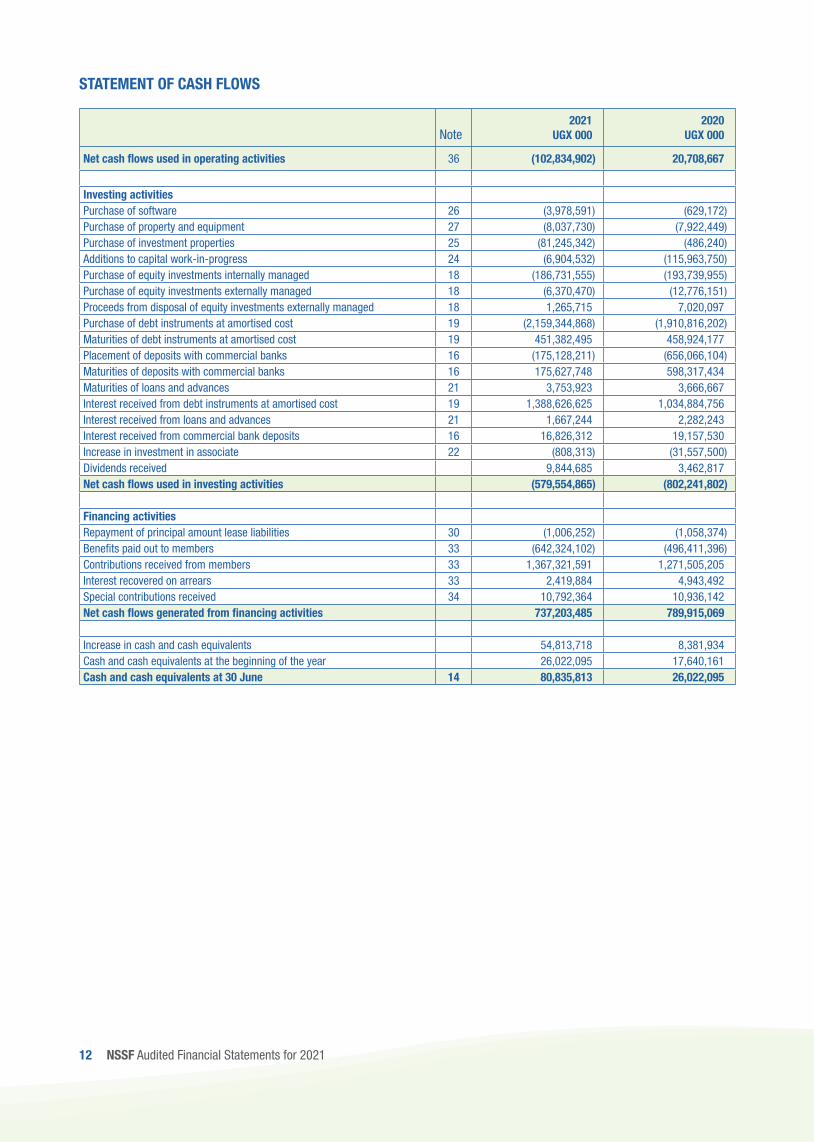

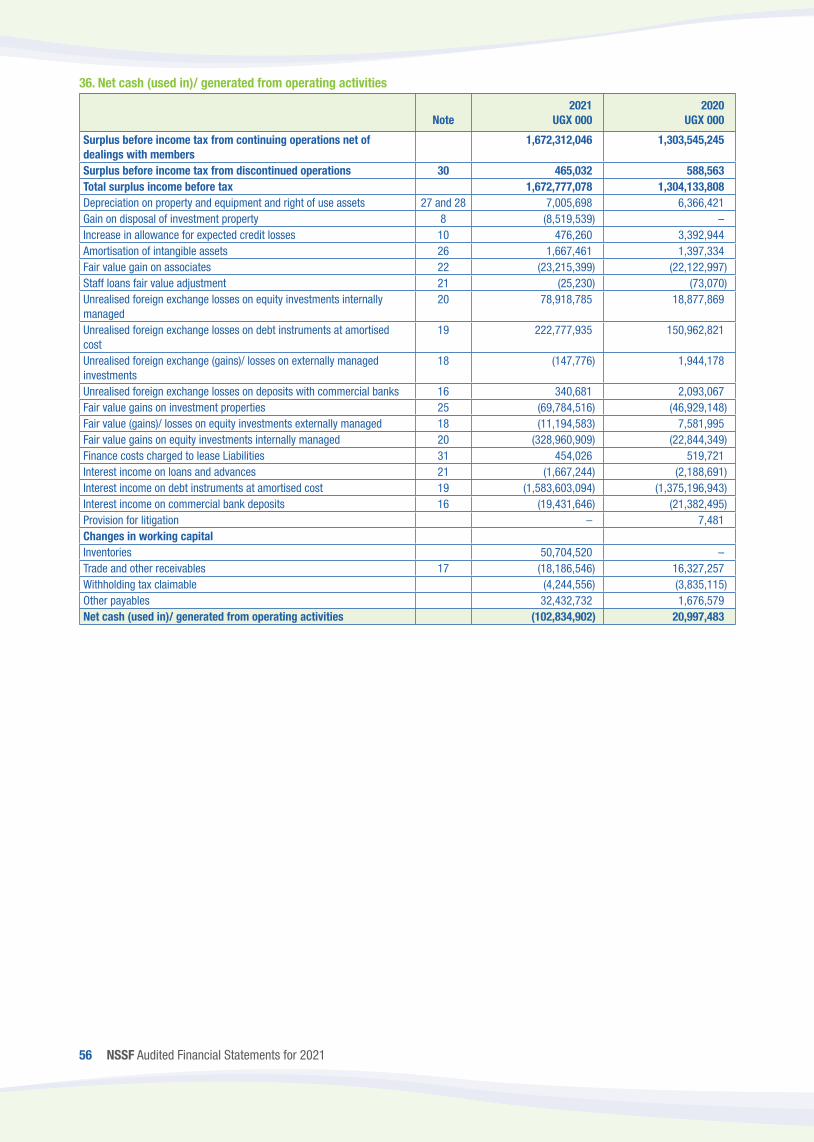

Net cash flows used in operating activities 36 (102,834,902) 20,708,667

Investing activitiesPurchase of software 26 (3,978,591) (629,172)Purchase of property and equipment 27 (8,037,730) (7,922,449)Purchase of investment properties 25 (81,245,342) (486,240)Additions to capital work-in-progress 24 (6,904,532) (115,963,750)Purchase of equity investments internally managed 18 (186,731,555) (193,739,955)Purchase of equity investments externally managed 18 (6,370,470) (12,776,151)Proceeds from disposal of equity investments externally managed 18 1,265,715 7,020,097Purchase of debt instruments at amortised cost 19 (2,159,344,868) (1,910,816,202)Maturities of debt instruments at amortised cost 19 451,382,495 458,924,177Placement of deposits with commercial banks 16 (175,128,211) (656,066,104)Maturities of deposits with commercial banks 16 175,627,748 598,317,434Maturities of loans and advances 21 3,753,923 3,666,667Interest received from debt instruments at amortised cost 19 1,388,626,625 1,034,884,756Interest received from loans and advances 21 1,667,244 2,282,243Interest received from commercial bank deposits 16 16,826,312 19,157,530Increase in investment in associate 22 (808,313) (31,557,500)Dividends received 9,844,685 3,462,817Net cash flows used in investing activities (579,554,865) (802,241,802)

Financing activitiesRepayment of principal amount lease liabilities 30 (1,006,252) (1,058,374)Benefits paid out to members 33 (642,324,102) (496,411,396)Contributions received from members 33 1,367,321,591 1,271,505,205Interest recovered on arrears 33 2,419,884 4,943,492Special contributions received 34 10,792,364 10,936,142Net cash flows generated from financing activities 737,203,485 789,915,069

Increase in cash and cash equivalents 54,813,718 8,381,934Cash and cash equivalents at the beginning of the year 26,022,095 17,640,161Cash and cash equivalents at 30 June 14 80,835,813 26,022,095

13 NSSF Audited Financial Statements for 2021

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2021

1. Fund informationNational Social Security Fund (the “Fund”) is a corporate body domiciled in Uganda. The Fund is primarily involved in collection of contributions and investment of the contributions in a professional manner to earn a good return to meet the benefit obligations to its members as stipulated under the National Social Security Fund Act (Cap 222). The address of the Fund’s registered office is:

14th Floor, Workers HousePlot No. 1, Pilkington RoadP. O. Box 7140Kampala, Uganda.

The Fund is a defined contribution scheme which is open to all employees in the private sector, with a total contribution of 15% of the employees’ gross salary (employer contribution 10%, employee contribution 5%).

During the year ended 30 June 2021, the Fund paid benefits to 29,914 beneficiaries (2020: 21,726 beneficiaries). According to the NSSF Act (Cap. 19), the benefits paid out of the Fund include:

• Age benefits - payable to a member who has reached the retirement age of 55 years;• Withdrawal benefits - payable to a member who has attained the age of 50 years, and is out of regular employment for one year;• Invalidity benefits - payable to a member who because of illness or any occurrence develops incapacity to engage in gainful

employment;• Survivors benefits – payable to the dependant survivor(s) in the unfortunate event of member’s death;• Emigration grants – payable to a member (Ugandan or Expatriate) who is leaving the country for good. Such a member must

have been contributing for a minimum of four financial years; else will have to forfeit the 10% employer contribution; and,• Exempted employment benefits – payable to a contributing member who joins employment categories that are exempted i.e.

have their social protection schemes that are recognised under the existing law and are exempted from contributing to NSSF e.g. the army, police, prison, civil service and government teaching service employees or members of any scheme who have received exemption from the Minister responsible for Social Security in writing.

As part of reforms whose objective is a liberalised and regulated retirement benefits sector. Government of Uganda enacted the Retirement Benefits Regulatory Authority Act in September 2011. The law established the Uganda Retirement Benefits Regulatory Authority (URBRA) whose function is to regulate all retirement schemes including NSSF. The Fund has a valid operating license (Licence No. RBS 0002) issued by URBRA in line with UBRA Act.

In March 2018, Cabinet approved the National Social Security Fund Amendment Bill 2018.This Bill was tabled before Parliament in 2019. The amendment seeks to permit the fund continue as a national scheme and the sole recipient of mandatory contributions for the country’s working population. The amendment also seeks to provide for mid-term access to benefits, and bring on board new products including education, maternity, housing, health and unemployment.

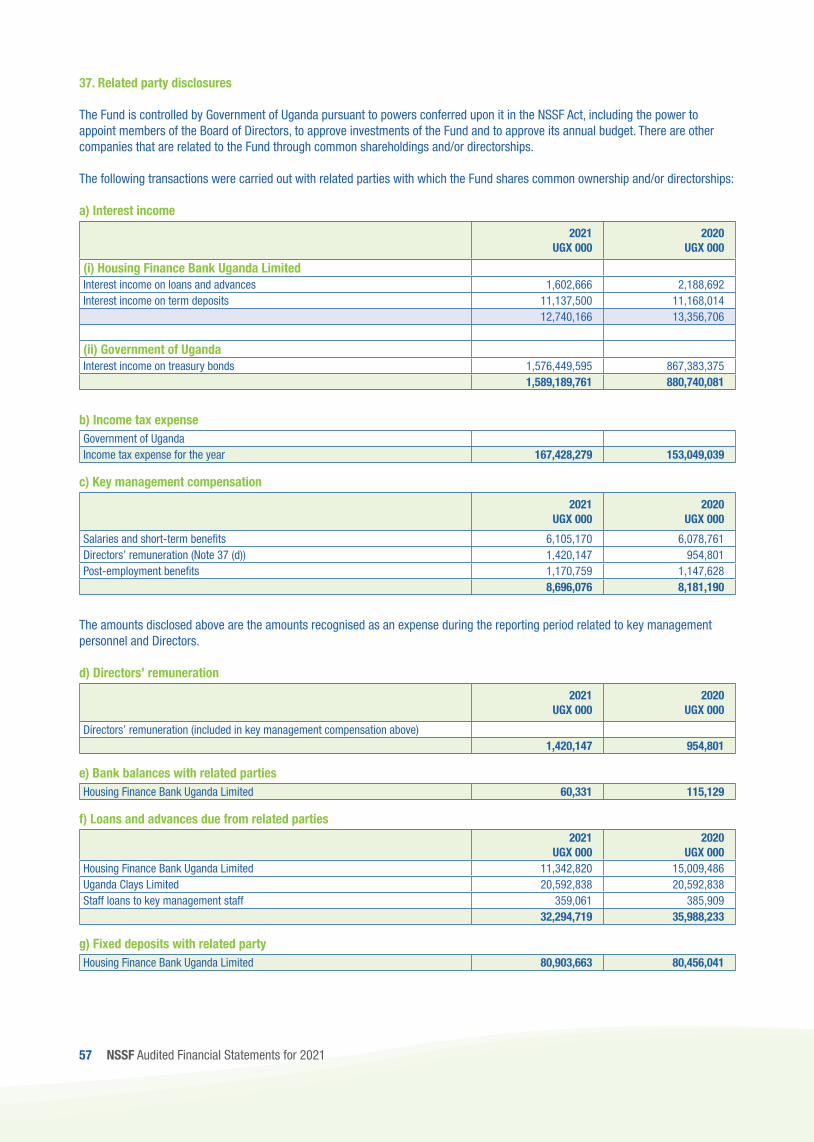

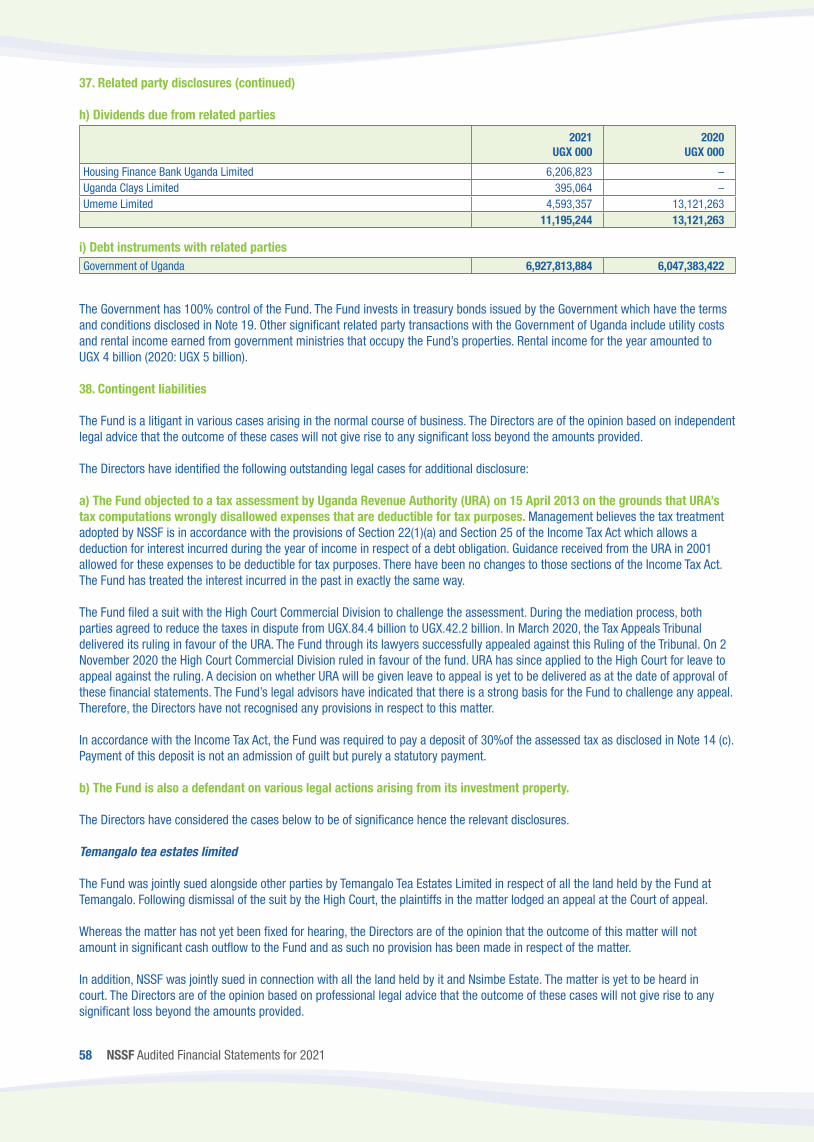

The Fund is also listed in Class 1 of the Public Enterprises Reform and Divestiture Act as an entity in which the Government of Uganda (GoU) shall retain 100% control and/or ownership.

2. Basis of preparationThe financial statements of the Fund have been prepared in accordance and compliance with International Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board (IASB) and fulfilment of the requirements of the NSSF Act.

The financial statements have been prepared on a historical cost basis except as otherwise indicated below. The financial statements are presented in Uganda Shillings (UGX), which is the Fund’s functional currency, and all values are rounded off to the nearest thousand (UGX 000), except where otherwise indicated.

3. Summary of significant accounting policiesThe principal accounting policies set out below have been applied consistently to all periods presented in the financial statements.

14 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)a) Investment in associatesAssociates are all entities over which the Fund has significant influence but not control or joint control. This is generally the case where the Fund holds between 20% and 50% of the voting rights of the underlying entity. Investments in associates are initially recognised at cost and subsequently measured at fair value. Where the measurement of fair value is not possible due to absence of quoted prices in an active market, the Fund applies its share of net assets in the associate as derived using the equity method of accounting as a proxy to fair value. Under the equity method, the carrying amount of the investment is adjusted to recognise changes in the Fund’s share of the net assets of the associate since the acquisition date. Changes in the Fund’s share of net assets are recognised in the statement of changes in net assets available for benefits.

b) Foreign currencies

The Fund’s financial statements are presented in Uganda Shillings, which is also the Fund’s functional currency.

Transactions in foreign currencies during the year are translated into Uganda Shillings at the exchange rate ruling at the date of the transaction.

Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated into Uganda Shillings at the exchange rates ruling at that date. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates at the dates of the initial transactions. Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are translated to Uganda Shillings at the date when the fair value was determined.

Foreign currency gains and losses arising from settlement or translation of monetary items are recognised in the statement of changes in net assets available for benefits.

c) Revenue recognitionRevenue from contracts with customersRevenue is recognised to the extent that it is probable that the economic benefits will flow to the Fund and the revenue can be reliably measured, regardless of when the payment is received. Revenue is measured at the fair value of the consideration received or receivable, excluding discounts, rebates, and other sales taxes or duty.

Sale of propertiesThe Fund develops and sells residential properties. Revenue is recognised at a point in time when legal tittle has passed to the buyer.

The Fund has arrangements for full or partial prepayment of consideration under its standard property sale contracts. A contract liability for the advance payment is recognised at the time of cash receipt. Revenue is recognised when the property sale is concluded as described above.

Contract balances

Contract assets

A contract asset is the right to consideration in exchange for goods or services transferred to the customer. If the Fund performs by transferring properties to a customer before payment is due, a contract asset is recognised for the earned consideration.

(i) Significant financing componentGenerally, the Fund receives accepts advance rent payment from its customers. Using the practical expedient in IFRS 15, the Fund does not adjust the promised amount of consideration for the effects of a significant financing component if it expects, at contract inception, that the period between the transfer of the promised good or service to the customer and when the customer pays for that good or service will be one year or less.

Trade receivables

A receivable represents the Fund’s right to an amount of consideration that is unconditional (i.e., only the passage of time is required before payment of the consideration is due). Refer to accounting policies of financial assets in Note 3 (d) Financial instruments – initial recognition and subsequent measurement.

15 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)c) Revenue recognition (continued)(i) Significant financing component (continued)

Contract liabilities

A contract liability is the obligation to transfer goods or services to a customer for which the Fund has received consideration (or an amount of consideration is due) from the customer. If a customer pays consideration before the Fund transfers goods or services to the customer, a contract liability is recognised when the payment is made, or the payment is due (whichever is earlier). Contract liabilities are recognised as revenue when the Fund performs under the contract.

Interest income/ expense

Interest income and expense on all interest-bearing instruments are recognised using the effective interest method in statement of changes in net assets available for benefits.

The effective interest method is a method of calculating the amortised cost of a financial asset or a financial liability and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts financial instruments estimated future cash payments or receipts through its expected life or, where appropriate, a shorter period to the net carrying amount. When calculating the effective interest rate, the Fund estimates cash flows considering all contractual terms of the financial instrument (for example, prepayment options) but does not consider future credit losses. The calculation includes all fees paid or received between parties to the contract that are an integral part of the effective interest rate, transaction costs and all other premiums or discounts.

The difference from the previous carrying amount is booked as a positive or negative adjustment to the carrying amount of the financial asset or liability on the balance sheet with a corresponding increase or decrease in interest income/ expense calculated using the effective interest method.

Dividends

Dividends on equity investments are recognised as income in the statement of changes in net assets available for benefits when the right of payment has been established, which is generally after declaration of dividends and approval by the shareholders of investee companies.

Rental income

Rental income from investment properties is recognized in the statement of changes in net assets available for benefits on the straight-line basis over the term of the lease.

Other income

Other income relates to fair value gains and losses related to equity instruments and investment in associates. It also includes gains from disposal of the Fund’s assets.

Financial instruments – initial recognition and subsequent measurementA financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity.

16 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)d) Financial instruments(i) Financial assets

Initial recognition and measurement

Financial assets are recognised when the Fund becomes a party to the contractual provisions of the instrument. Regular way purchases and sales of financial assets are recognised on trade-date, being the date on which the Fund commits to purchase or sell the asset.

Initial recognition and measurement

At initial recognition, the Fund measures a financial asset at its fair value plus or minus, in the case of a financial asset not at fair value, transaction costs that are incremental and directly attributable to the acquisition or issue of the financial asset, such as fees and commissions. Transaction costs of financial assets carried at fair value are expensed in statement of changes in net assets available for benefits. After initial recognition subject to increase in credit risk, an expected credit loss allowance (ECL) is recognised for financial assets measured at amortised cost.

For a financial asset to be classified and measured at amortised cost or fair value, it needs to give rise to cash flows that are ‘solely payments of principal and interest (SPPI)’ on the principal amount outstanding. This assessment is referred to as the SPPI test and is performed at an instrument level.

The Fund’s business model for managing financial assets refers to how it manages its financial assets to generate cash flows. The business model determines whether cash flows will result from collecting contractual cash flows, selling the financial assets, or both.

Subsequent measurement

The financial assets are subsequently measured at fair value with the exception of government securities and fixed bank deposits which are subsequently measured at amortised cost This treatment reflects the fact that these instruments are used to match the obligations of the Fund.

The amortised cost is the amount at which the financial asset is measured at initial recognition minus the principal repayments, plus or minus the cumulative amortisation using the effective interest method of any difference between that initial amount and the maturity amount and, for financial assets, adjusted for any loss allowance.

The Fund’s financial assets comprise of the following:

• Cash and cash equivalent (Note 15)• Debt instruments at amortised cost (Note 19)• Equity instruments (Notes 18 and 20)• Loans and advances (Note 21)• Trade and other receivables (Note 17)• Deposits with commercial banks (Note 16)

Derecognition

A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is primarily derecognised when:

• The rights to receive cash flows from the asset have expired; or• The Fund has transferred its rights to receive cash flows from the asset or has assumed an obligation to pay the received cash

flows in full without material delay to a third party under a ‘pass-through’ arrangement; and either (a) the Fund has transferred substantially all the risks and rewards of the asset, or (b) the Fund has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

When the Fund has transferred its rights to receive cash flows from an asset or has entered into a pass-through arrangement, it evaluates if, and to what extent, it has retained the risks and rewards of ownership.

17 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)d) Financial instruments (continued)(i) Financial assets (continued)

Derecognition (continued)

When it has neither transferred nor retained substantially all of the risks and rewards of the asset, nor transferred control of the asset, the Fund continues to recognise the transferred asset to the extent of its continuing involvement. In that case, the Fund also recognises an associated liability. The transferred asset and the associated liability are measured on a basis that reflects the rights and obligations that the Fund has retained.

Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Fund could be required to repay.

Impairment of financial assets

Further disclosures relating to impairment of financial assets are also provided in the following notes:

• Disclosures for significant assumptions (Note 39)• Debt instruments at amortised cost (Note 19)• Loans and advances (Note 21)• Trade and other receivables (Note 17)• Deposits with commercial banks (Note 16)

The Fund recognises an allowance for expected credit losses (ECLs) for all financial assets that are measured at amortised cost. ECLs are based on the difference between the contractual cash flows due in accordance with the contract and all the cash flows that the Fund expects to receive, discounted at an approximation of the original effective interest rate. The expected cash flows will include cash flows from the sale of collateral held or other credit enhancements that are integral to the contractual terms.

ECLs are recognised in two stages. For credit exposures for which there has not been a significant increase in credit risk since initial recognition, ECLs are provided for credit losses that result from default events that are possible within the next 12-months (a 12-month ECL). For those credit exposures for which there has been a significant increase in credit risk since initial recognition, a loss allowance is required for credit losses expected over the remaining life of the exposure, irrespective of the timing of the default (a lifetime ECL).

For trade receivables and contract assets, the Fund applies a simplified approach in calculating ECLs. Therefore, the Fund does not track changes in credit risk, but instead recognises a loss allowance based on lifetime ECLs at each reporting date. The Fund is applying a single loss-rate approach to receivables or groups of receivables as might be appropriate based on its average historical loss rate.

Depending on the data, the Fund applies either of two ways of computing the loss rate per period. A loss rate is computed as the ratio of outstanding invoice beyond the default period and invoices raised at the beginning of each period. Currently invoices raised majorly relate to rental space occupied by the tenants on the Fund’s lettable properties.

In case of payments on the outstanding invoices, the recovery rate is computed as a ratio of payments made on bills raised per time period before the default date. The loss rate is then obtained as 1 – recovery rate. A common approximation is to cap recovery rates at 100% where payments exceed invoice amounts. The single loss rate is adjusted for forward-looking factors specific to the debtors and the economic environment. The single loss rate estimates are applied to each category of gross receivables.

The Fund considers whether ECLs should be estimated individually for any period-end receivables, e.g. because specific information is available about those debtors.

The Fund has applied the single loss rate approach to all other financial assets recognised as other receivables e.g dividends receivable.

For all other financial instruments, the Fund recognises lifetime ECL when there has been a significant increase in credit risk since initial recognition. However, if the credit risk on the financial instrument has not increased significantly since initial recognition, the Company measures the loss allowance for that financial instrument at an amount equal to 12 month ECL.

18 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)d) Financial instruments (continued)(i) Financial assets (continued)

Impairment of financial assets (continued)

Lifetime ECL represents the expected credit losses that will result from all possible default events over the expected life of a financial instrument. In contrast,12 month ECL represents the portion of lifetime ECL that is expected to result from default events on a financial instrument that are possible within12 months after the reporting date.

The Fund considers a financial asset to have low credit risk when the asset has external credit rating of investment grade’ in accordance with the globally understood definition or if an external rating is not available, the asset has an internal rating of ‘performing’. Performing means that the counterparty has a strong financial position and there is no past due amounts.

Financial assets are written off either partially or in their entirety only when the Fund has no reasonable expectation of recovering a financial asset in its entirety or a portion thereof. If the amount to be written off is greater than the accumulated loss allowance, the difference is first treated as an addition to the allowance that is then applied against the gross carrying amount. Any subsequent recoveries are credited to the statement of changes in net assets available for benefits.

(ii) Financial liabilities

Initial recognition and measurement

Financial liabilities are initially measured at fair value. Transaction costs that are directly attributable to the acquisition or issue of financial liabilities (other than financial liabilities at fair value) are added to or deducted from the fair value of the financial liabilities, as appropriate, on initial recognition. Transaction costs directly attributable to the acquisition of financial liabilities at fair value are recognised immediately in the statement of changes in net assets available for benefits.

Subsequent measurement

The Fund’s payables majorly relate to amounts due to contractors for works done on property developments and amounts due to other suppliers of goods and services consumed in day to day operations of the Fund.

Other payables are carried at amortised cost, which approximates the consideration to be paid in the future for goods and services received.

Derecognition

A financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires.When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as the derecognition of the original liability and the recognition of a new liability. The difference in the respective carrying amounts is recognised in the Statement of Changes in Net Assets Available for Benefits.

Offsetting

Financial assets and liabilities are offset and the net amount reported in the statement of net assets available for benefits when there is a currently enforceable legal right to offset the recognised amounts and there is an intention to settle on a net basis, or realise the asset and settle the liability simultaneously.

e) Fair value measurement

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value measurement is based on the presumption that the transaction to sell the asset or transfer the liability takes place either:

• In the principal market for the asset or liability; or• In the absence of a principal market, in the most advantageous market for the asset or liability.

The principal or the most advantageous market is usually accessible by the Fund.

19 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)e) Fair value measurement (continued)

The fair value of an asset or a liability is measured using the assumptions that market participants would use when pricing the asset or liability, assuming that market participants act in their economic best interest.

Where the market price of a financial asset is not observable the Fund applies a valuation model to estimate the fair value at the reporting date.

A fair value measurement of a non-financial asset takes into account a market participant’s ability to generate economic benefits by using the asset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use.

The Fund uses valuation techniques that are appropriate in the circumstances and for which sufficient data are available to measure fair value, maximising the use of relevant observable inputs and minimising the use of unobservable inputs.All assets and liabilities for which fair value is measured or disclosed in the financial statements are categorised within the fair value hierarchy, described as follows, based on the lowest level input that is significant to the fair value measurement as a whole:

• Level 1 – quoted (unadjusted) market prices in active markets for identical assets or liabilities.• Level 2 – valuation techniques for which the lowest level input that is significant to the fair value measurement is directly or

indirectly observable• Level 3 – valuation techniques for which the lowest level input that is significant to the fair value measurement is unobservable.

For assets and liabilities that are recognised in the financial statements at fair value on a recurring basis, the Fund determines whether transfers have occurred between levels in the hierarchy by re-assessing categorisation (based on the lowest level input that is significant to the fair value measurement as a whole) at the end of each reporting period.

The Fund’s management investment committee determines the policies and procedures for recurring fair value measurement of investment properties. The management investment committee delegates the role of selection/ determination of involvement of the external valuers to a valuation committee which is comprised of the real estate manager, finance manager, procurement manager and legal officer.

External valuers are involved for valuation of significant assets, such as investment properties. Selection of external valuers is determined every two years by the valuation committee and after discussion with and approval by the contracts committee and the accounting officer. Selection criteria include market knowledge, reputation, independence and whether professional standards are maintained.

Valuers are normally rotated at each round of valuation with no single valuer performing consecutive valuations. The valuation committee decides, after discussions with the Fund’s external valuers, which valuation techniques and inputs to use for each case.

Fair value related disclosures for financial instruments and non-financial assets that are measured at fair value or where fair values are disclosed, are summarized in the following notes:

• Disclosures for valuation methods, significant estimates and assumptions – Note 4 and 39;• Quantitative disclosures of fair value measurement hierarchy – Note 41;• Financial instruments (including those carried at amortised cost) – Notes 15,16, 17, 18, 20 and 40;• Investment property – Note 25; and• Capital work in progress – Note 24.

f) Property and equipment

Property and equipment is stated at cost, net of accumulated depreciation and/or accumulated impairment losses, if any. Cost includes expenditures that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and direct labour, any other costs directly attributable to bringing the assets to a working condition for their intended use, and the costs of dismantling and removing the items and restoring the site on which they are located. Purchased software that is integral to the functionality of the related equipment is capitalized as part of that equipment.

When parts of an item of property or equipment have different useful lives, they are accounted for as separate items (major components) of property and equipment.

20 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)f) Property and equipment (continued)

Repairs and maintenance are charged to profit or loss during the financial period in which they are incurred. The cost of major renovations is included in the carrying amount of the asset when it is probable that future economic benefits in excess of the most recently assessed standard of performance of the existing asset will flow to the Company and the renovation replaces an identifiable part of the asset. Major renovations are depreciated over the remaining useful life of the related asset.

Changes in the expected useful life are accounted for by changing the depreciation period or methodology, as appropriate, and treated as changes in accounting estimates.

Depreciation is calculated to write off the cost of items of property and equipment less their estimated residual values using the reducing balance method over their estimated useful lives and is generally recognised in surplus or deficit.

The estimated annual depreciation rates for the current and comparative periods are as follows:

Percentage

Machinery 20 %Motor vehicles 20 %Furniture and equipment 12.5 %Computer equipment and other electronic gadgets 25%-33%

Depreciation commences once the asset is capitalized and is ready for use as intended by management and ceases on the day of derecognition.

The residual values, useful lives and methods of depreciation of property, plant and equipment are reviewed at each financial year end and adjusted prospectively, if appropriate.

An item of property and equipment and any significant part initially recognised is derecognised upon disposal, when the fund loses control of the asset or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in other operating income in the statement of changes in net assets available for benefits when the asset is derecognised.

Land and buildings, which represent that portion of mixed-use properties that is owner occupied, are subsequently measured at fair value with changes in fair value recognised in the statement of changes in net assets available for benefits and depreciation measured to write down the post valuation amount over the remaining useful life of the property.

g) Intangible assets

Intangible assets acquired separately are measured on initial recognition at cost. Following initial recognition, intangible assets are carried at cost less any accumulated amortisation and any accumulated impairment losses.

Intangible assets with finite lives are amortised over the useful economic life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortisation period and the amortisation method for an intangible asset with a finite useful life are reviewed at least at each financial year-end. Changes in the expected useful life or the expected pattern of consumption of future economic benefits embodied in the asset are accounted for by changing the amortisation period or method, as appropriate, and are treated as changes in accounting estimates. The amortisation expense on intangible assets with finite lives is recognised in the statement of changes in net assets available for benefits in the expense category consistent with the function of the intangible asset. There are no intangible assets with indefinite useful lives.

Intangible assets are amortised at a rate of 10% p.a.

Gains or losses arising from derecognition of an intangible asset are measured as the difference between the net disposal proceeds and the carrying amount of the asset and are recognised in the statement of changes in net assets available for benefits when the asset is derecognised.

21 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)

h) Investment properties

Investment properties are measured initially at cost, including transaction costs. The carrying amount includes the cost of replacing part of an existing investment property at the time that cost is incurred if the recognition criteria are met and excludes the costs of day-to-day servicing of an investment property.

Subsequent to initial recognition, investment properties are stated at fair value, which reflects market conditions at the reporting date. All of the Fund’s property interests held under operating leases to earn rentals or for capital appreciation purposes are accounted for as investment properties and are measured using the fair value model. Gains or losses arising from changes in the fair values of investment properties are included in surplus or deficit in the period in which they arise, including the corresponding tax effect.

Investment properties are derecognised either when they have been disposed of (i.e., at the date the recipient obtains control) or when they are permanently withdrawn from use and no future economic benefit is expected from their disposal. The difference between the net disposal proceeds and the carrying amount of the asset is recognised in surplus or deficit in the period of derecognition. The amount of consideration to be included in the gain or loss arising from the derecognition of investment property is determined in accordance with the requirements for determining the transaction price in IFRS 15.

Transfers are made to or from investment property only when there is a change in use. For a transfer from investment property to owner-occupied property, the deemed cost for subsequent accounting is the fair value at the date of change in use. When the use of property changes from owner occupied to investment property, the property is re-measured at fair value and reclassified as investment property.

Right-of-use assets that meet the definition of investment property are presented as investment property.

i) Inventories

The Fund’s inventories comprise of completed housing units for sale and housing units for sale that are under development. Inventories are initially recognised at cost and remeasured to fair value at each reporting date.

j) Impairment of non-financial assets

The carrying amounts of the Fund’s non-financial assets other than investment properties, inventories and deferred tax assets are reviewed at each reporting date to determine whether there is any indication of impairment. If such condition exists, the asset’s recoverable amount is estimated and an impairment loss recognised in surplus or deficit whenever the carrying amount of an asset exceeds its recoverable amount.

An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s (CGU) fair value less costs of disposal and its value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets.

In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. In determining fair value less costs of disposal, recent market transactions are taken into account. If no such transactions can be identified, an appropriate valuation model is used.

Impairment losses are recognised in the statement of changes in net assets available for benefits in expense categories consistent with the function of the impaired asset.

An assessment is made at each reporting date to determine whether there is an indication that previously recognised impairment losses no longer exist or have decreased. If such indication exists, the Fund estimates the asset’s or CGU’s recoverable amount. A previously recognised impairment loss is reversed only if there has been a change in the assumptions used to determine the asset’s recoverable amount since the last impairment loss was recognised. The reversal is limited so that the carrying amount of the asset does not exceed its recoverable amount or exceed the carrying amount that would have been determined, net of depreciation or amortisation, had no impairment loss been recognised for the asset in prior years. Such reversal is recognised in the statement of changes in net assets available for benefits.

22 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)

k) Employee benefits(i) GratuityThe Fund’s terms and conditions of employment provide for gratuity to qualifying employees equivalent to 20% of the monthly salary per year of service to the organisation. This employment benefit is accrued on a monthly basis and paid annually in arrears. The provision in the financial statements takes account of service rendered by employees up to the reporting date and is based on the calculated staff benefits payable.

(ii) Staff provident fundThe Fund operates a defined contribution plan for all qualifying employees with contributions being made by the employees and a portion by the fund on behalf of each employee. The contributions payable to the plan are in proportion to the services rendered to the Fund by the employees and are recorded as an expense under ‘staff costs’ in the statement of changes in net assets available for benefits. Unpaid contributions are recorded as a liability.

l) ProvisionsA provision is recognised if, as a result of a past event, the Fund has a present legal or constructive obligation that can be estimated reliably and it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability.

Where the Fund expects a provision to be reimbursed, for example under an insurance contract, the reimbursement is recognised as a separate asset but only when the reimbursement is virtually certain.

m) Income taxIncome tax expense comprises current tax and change in deferred tax. Income tax expense is recognised in surplus or deficit.

Current tax is provided for on the surplus for the year adjusted in accordance with the Ugandan Income Tax Act. Current income tax assets and liabilities for the current and prior periods are measured at the amount expected to be recovered from or paid to the taxation authorities.

Deferred tax is provided for using the liability method, for all temporary differences between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes at the and reporting date. However, if the deferred tax arises from the initial recognition of an asset or liability in a transaction other than a business combination that at the time of the transaction affects neither accounting nor taxable surplus or deficit, it is not accounted for. In respect of temporary differences associated with investments in subsidiaries and associates, deferred tax assets and liabilities are not recognised where the timing of the reversal of the temporary differences can be controlled and it is probable that the temporary differences will not reverse in the foreseeable future.

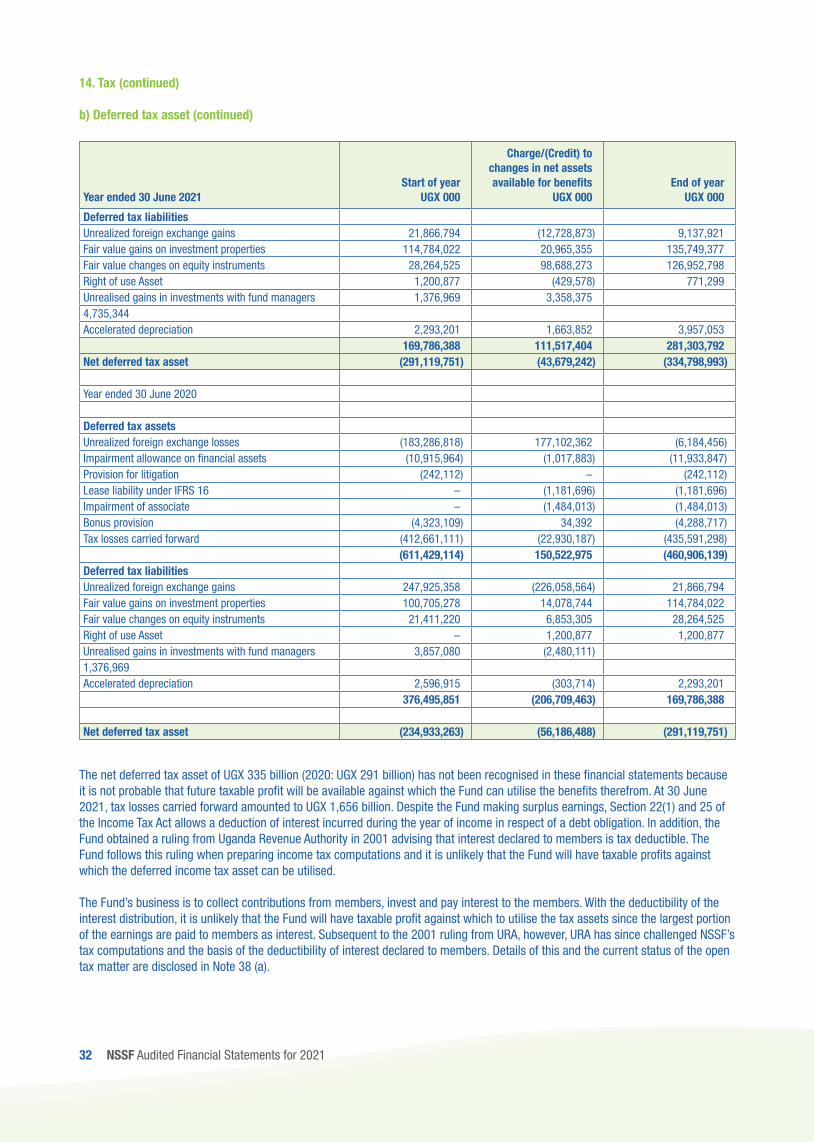

Deferred tax assets are recognised for all deductible temporary differences, the carry forward of unused tax credits and any unused tax losses to the extent that it is probable that taxable surplus will be available against which the deductible temporary differences, and the carry forward of unused tax credits and unused tax losses can be utilised.

The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable surplus will be available to allow all or part of the deferred tax asset to be utilised. Unrecognised deferred tax assets are reassessed at each reporting date and are recognised to the extent that it has become probable that future taxable surplus will allow the deferred tax asset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the year when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the reporting date.

Deferred income tax assets and deferred income tax liabilities are offset if a legally enforceable right exists to set off current tax assets against current income tax liabilities and the deferred income taxes relate to the same taxable entity and the same taxation authority.

The net amount of value added tax recoverable from, or payable to, the taxation authority is included as part of accounts receivable or accounts payable in the statement of net assets available for benefits.

23 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)

n) Cash and cash equivalents

Cash and cash equivalents in the statement of net assets available for benefits comprise cash at banks and on hand and short-term highly liquid deposits with an original maturity of three months or less, that are readily convertible to a known amount of cash and subject to an insignificant risk of changes in value.

For the purposes of the statement of cash flows, cash and cash equivalents comprise cash and bank balances and short-term highly liquid deposits in form of mobile money balances (as disclosed in Note 15 that are available on demand as at the reporting date.

o) Capital work-in-progress

Capital work in progress (CWIP) relates to ongoing capital projects of investment or operational nature. Additions to capital work in progress are initially recognised at cost and subsequently measured at fair value.

p) Members’ funds

The Fund is funded through contributions from members and investment income.

(i) The Fund recognises a liability to pay benefits to members composed of contributions declared on the account of each member and interest accumulated on each account in accordance with the obligations laid out in the NSSF Act.

(ii) Interest is allocated to each members’ account at the rate declared by the Minister for each member in consultation with the Board of Directors each year, and is recognised in the statement of net assets available for benefits.

(iii) Interest payments to members

Interest payable on members’ accumulated contributions is calculated based on the opening accumulated contributions (standard contribution plus interest) less benefits paid during the year. The effective interest rate used to compute interest accrued to members is approved by the Minister of Finance, Planning & Economic Development in accordance with Section 35 (1) and (2) of the National Social Security Fund Act and is treated as an expense.

The recognition of the expense and respective interest provision is based on the requirement under the NSSF Act to recognise member balances as a debt obligation.

(iv) Benefit payments to members

Benefits payments to members are made upon meeting criteria for payment as set out in the NSSF Act. Such payments recognised as a charge in the statement of changes in net assets available for benefits, and as a reduction from members’ funds when paid.

(v) Contributions from members

Member contributions remitted by their employers are recognized in the statement of changes in net assets available for benefits when received. Contributions due but not yet received at the end of the financial year are not accrued but accounted for and recognized in subsequent years when received.

q) Reserve account

The reserve account is credited with special contributions by non-eligible employees and amounts recovered in form of fines and penalties from employers that fail to remit members funds as stipulated in the National Social Security Fund Act. The special contributions are credited directly to the reserve account while the fines and penalties are recognised through the statement of changes in net assets available for benefits and then appropriated from the accumulated surplus/deficit to the reserve account. Transfers from the reserve account require the approval of the Minister of Finance in accordance with the NSSF Act.

24 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)

r) Leases

The Fund assesses at contract inception whether a contract is, or contains, a lease. That is, if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

The Fund as a lessee

The Fund applies a single recognition and measurement approach for all leases, except for short-term leases and leases of low-value assets. The Fund recognises lease liabilities to make lease payments and right-of-use assets representing the right to use the underlying assets.

Right-of-use assets (except those meeting the definition of investment property)

The Fund recognises right-of-use assets at the commencement date of the lease (i.e., the date the underlying asset is available for use). Right-of-use assets are measured at cost, less any accumulated depreciation and impairment losses, and adjusted for any remeasurement of lease liabilities.

The cost of right-of-use assets includes the amount of lease liabilities recognised, initial direct costs incurred, and lease payments made at or before the commencement date less any lease incentives received. Right-of-use assets are depreciated on a straight-line basis over the shorter of the lease term and the estimated useful lives of the assets. The Fund considered tenancy arrangements for its branches with an estimated lease term of 3 to 6 years.

If ownership of the leased asset transfers to the Fund at the end of the lease term or the cost reflects the exercise of a purchase option, depreciation is calculated using the estimated useful life of the asset.

The right-of-use assets are presented within Note 28 and are subject to impairment in line with the Fund’s policy as described in Note 3 (j) Impairment of non-financial assets.

Right-of-use assets (meeting the definition of investment property)

The Fund’s accounting policy for investment properties is disclosed in Note 3 (h).

Lease liabilities

At the commencement date of the lease, the Fund recognises lease liabilities measured at the present value of lease payments to be made over the lease term. The lease payments include fixed payments (less any lease incentives receivable), variable lease payments that depend on an index or a rate, and amounts expected to be paid under residual value guarantees. The lease payments also include the exercise price of a purchase option reasonably certain to be exercised by the Fund and payments of penalties for terminating the lease, if the lease term reflects the Fund exercising the option to terminate. Variable lease payments that do not depend on an index or a rate are recognised as expenses in the period in which the event or condition that triggers the payment occurs.

In calculating the present value of lease payments, the Fund uses its incremental borrowing rate at the lease commencement date because the interest rate implicit in the lease is not readily determinable. After the commencement date, the amount of lease liabilities is increased to reflect the accretion of interest and reduced for the lease payments made. In addition, the carrying amount of lease liabilities is remeasured if there is a modification, a change in the lease term, a change in the lease payments (e.g. changes to future payments resulting from a change in an index or rate used to determine such lease payments) or a change in the assessment of an option to purchase the underlying asset.

The Fund’s lease liabilities are presented within other payables in Note 31.

Short-term leases and leases of low-value assets

The Fund applies the short-term lease recognition exemption to its short-term leases of any rental payments (i.e., those leases that have a lease term of 12 months or less from the commencement date and do not contain a purchase option). It also applies the lease of low-value assets recognition exemption to leases that are considered to be low value. Lease payments on short-term leases and leases of low value assets are recognised as expense on a straight-line basis over the lease term.

25 NSSF Audited Financial Statements for 2021

3. Summary of significant accounting policies (continued)r) Leases (continued)

The Fund as a lessor

Leases in which the Fund does not transfer substantially all the risks and rewards incidental to ownership of an asset are classified as operating leases. Rental income arising is accounted for on a straight-line basis over the lease terms and is included in revenue in the statement of profit or loss due to its operating nature. Initial direct costs incurred in negotiating and arranging an operating lease are added to the carrying amount of the leased asset and recognised over the lease term on the same basis as rental income.

s) Current/non-current distinction

The Fund presents assets and liabilities in decreasing order of liquidity which provides information that is reliable and more relevant than a current/non-current presentation because the Fund does not supply goods or services within a clearly identifiable operating cycle.

The operating cycle of the Fund is the time between the acquisition of assets for processing and their realisation in cash or cash equivalents. When the Fund’s normal operating cycle is not clearly identifiable, it is assumed to be twelve months.