Embed Size (px)

DESCRIPTION

Audited Financial Statements for Shortgrass Library System for the 2011 Fiscal Year

Citation preview

Shortgrass Library System Financial Statements

December 31, 2011

Management's Responsibility

To the Stakeholders of Shortgrass Library System: I

Management is responsible for the preparation and presentation of the accompanying financial statements, including responsibility for

significant accounting judgments and estimates in accordance with Canadian generally accepted accounting principles. This

responsibility includes selecting appropriate accounting principles and methods, and making decisions affecting the measurement of

transactions in which objective judgment is required.

In discharging its responsibilities for the integrity and fairness of the financial statements, management designs and maintains the

necessary accounting systems and related internal controls to provide reasonable assurance that transactions are authorized, assets

are safeguarded and financial records are properly maintained to provide reliable information for the preparation of financial statements.

The Board of Trustees is composed entirely of Directors who are neither management nor employees of the Organization. The Board is

responsible for overseeing management in the performance of its financial reporting responsibilities, and for approving the financial

information. The Board fulfils these responsibilities by reviewing the financial information prepared by management and discussing

relevant matters with management and external auditors. The Board is also responsible for recommending the appointment of the

Organization's external auditors.

MNP LLP. an independent firm of Chartered Accountants, is appointed by the trustees to audit the financial statements and report

directly to them; their report follows. The external auditors have full and free access to, and meet periodically and separately with, both

the Board and management to discuss their audit findings.

April 18, 2012

Ch��

Independent Auditors' Report

To the Members of Shortgrass Library System:

We have audited the accompanying financial statements of Shortgrass Library System, which comprise the statement of financial position as at December 31, 2011 and the statements of operations, changes in net assets and cash flows, including the related schedules, for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian generally accepted accounting principles, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statement.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion.

Opinion In our opinion, except for the effects of failing to capitalize and amortize capital assets as described in the Other Matter Paragraph, these financial statements present fairly, in all material respects the financial position of Shortgrass Library System as at December 31, 2011, and the results of its operations, changes in net assets and its cash flows for the year then ended in accordance with Canadian generally accepted accounting principles.

Other Matter Note 2 describes the Organization's accounting policy with respect to capital assets and indicates that the Organization has not adopted the policy of capitalization and amortization as recommended under Canadian generally accepted accounting principles. The informational requirements of the users of the financial statements are more closely met by the current policy of expensing the cost of capital assets fully in the year of acquisition. The amount of adjustment necessary under Canadian generally accepted accounting principles is not readily determinable at this time.

Medicine Hat, Alberta MN?LLf' April 18, 2012 Chartered Accountants

Box 580, 666- 4tll Street SE, Medicine Hat, Alberta, T1A 7G5, Phone: (403) 527-4441, 1 (877) 500-0786

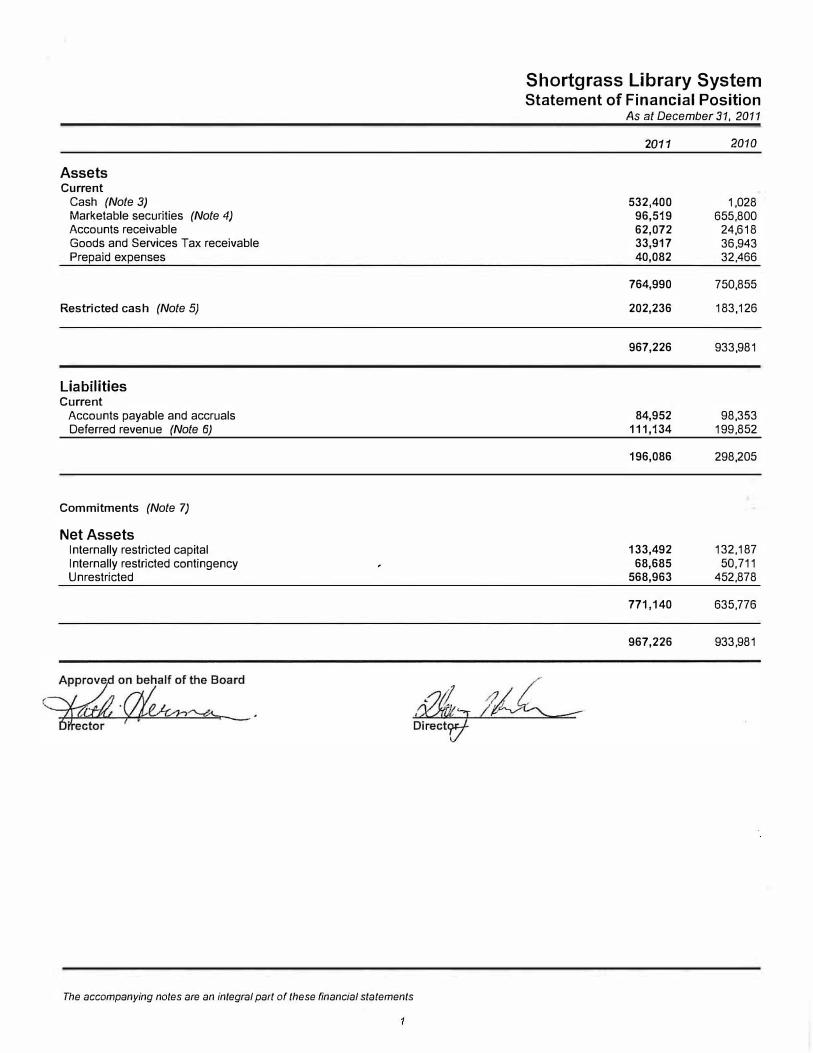

Assets Current

Cash (Note 3) Marketable securities (Note 4) Accounts receivable Goods and Services Tax receivable Prepaid expenses

Restricted cash (Note 5)

Liabilities Current

Accounts payable and accruals Deferred revenue (Note 6)

Commitments (Note 7)

Net Assets Internally restricted capital Internally restricted contingency Unrestricted

The accompanying notes are an integral part of these financial statements

Shortgrass Library System Statement of Financial Position

As at December 31, 2011

2011 2010

532,400 96,519 62,072 33,917 40,082

764,990

202,236

967,226

84,952 111,134

196,086

133,492 68,685

568,963

771 '140

967,226

1,028 655,800

24,618 36,943 32,466

750,855

183,126

933,981

98,353 199,852

298,205

132,187 50, 711

452,878

635,776

933,981

Revenue APLEN CAP grant - libraries APLEN grant- SLSHQ Contract services - MHSD #76 & Prairie Rose Datacom reimbursements Donated monies and staff order reimbursements Establishment grant Integrated library system reimbursements Investment income Member library boards materials (Note 9) Member municipalities operational Miscellaneous Non-resident fees and other Provincial grants Special grants

Expenses APLEN CAP grant expense & capital - libraries APLEN grant expense & capital - SLSHQ Additional resources Advertising and promotions Alberta library Board expenses Building costs - repairs, maintenance and supplies Capital purchases Consultancy and programs Contract work - MHSD #76 Contract work - Prairie Rose Donated monies and staff order purchases Establishment grant expense - capital Insurance - building Library materials Member library managers expense Resource sharing payments Rural services payments Special grants expense & capital SLSHQ Telephone Utilities

The accompanying notes are an integral part of t11ese financial statements

2

Shortgrass Library System Statement of Operations

For the year ended December 31, 201 1

2011 2010

35,566 24,627

108,599 5,595

15,864 20,307 18,278

4,554 488,852 468,748

6,719 60

521,470 72,910

1 ,792,149

34,301 24,627

5,026 13,361

5,382 13,462 25,332

4,107 8,615 5,124

15,896 20,307

6,148 395,076

6,299 14,000 48,200 24,361

484 27,497

697,605

19,443 8,347

107,431 6,080

16,485 16,134 12,180

3,120 476,733 449,041

9,630 540

517,020 147,890

1,790,074

17,425 8,347 5,167

14,996 5,359

13,847 30,248 27,046

4,225 10,122

6,880 16,485 16,134

7,960 353,218

6,850 14,000 48,200 97,719

400 22,205

726,833

Continued on next page

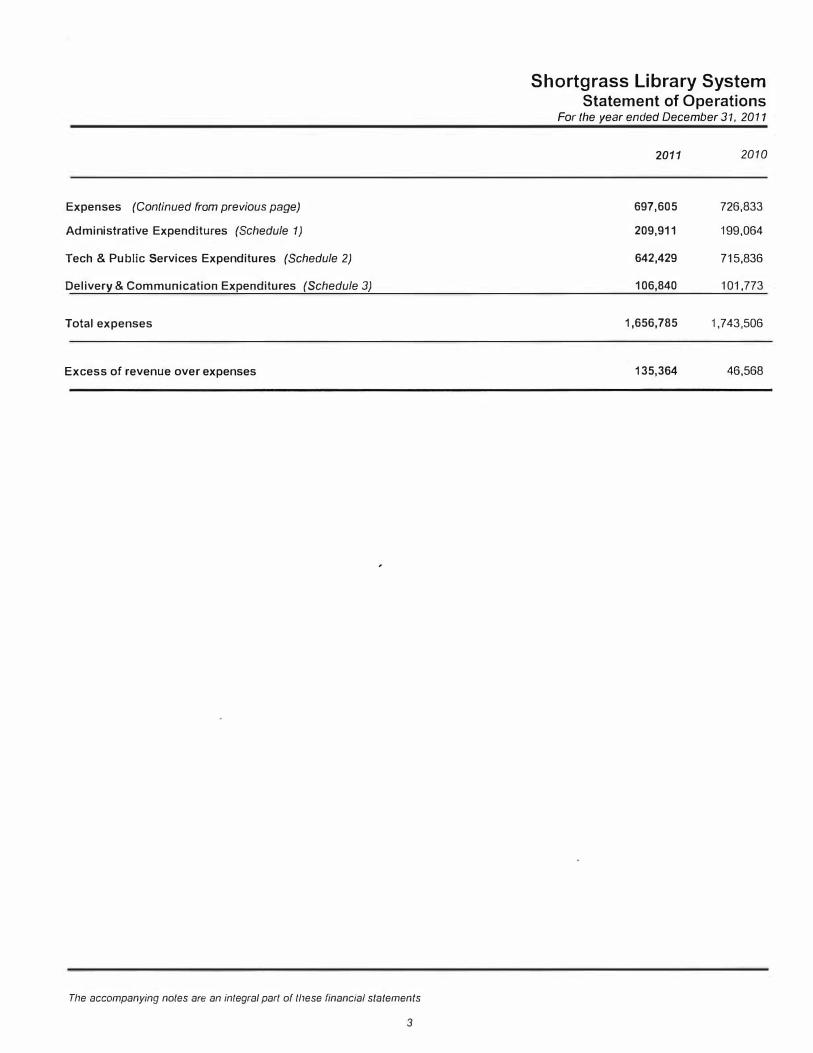

Expenses (Continued from previous page)

Administrative Expenditures (Schedule 1)

Tech & Public Services Expenditures (Schedule 2)

Delivery & Communication Expenditures (Schedule 3)

Total expenses

Excess of revenue over expenses

Tile accompanying notes are an integral part of tllese financial statements

3

Shortgrass Library System Statement of Operations

For the year ended December 31, 2011

2011 2010

697,605 726,833

209,911 199,064

642,429 715,836

106,840 101,773

1,656,785 1,743,506

135,364 46,568

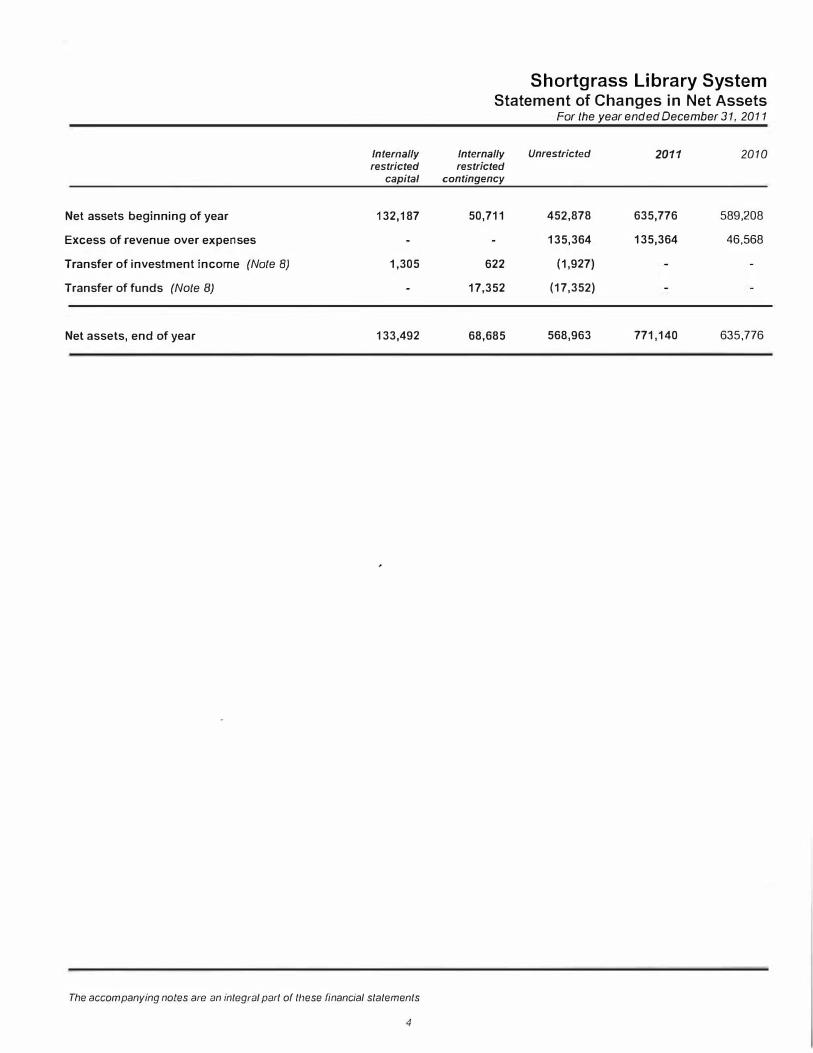

Shortgrass Library System Statement of Changes in Net Assets

For the year ended December 31, 2011

Internally Internally Unrestricted 2011 2010 restricted restricted

capital contingency

Net assets beginning of year 132,187 50,711 452,878 635,776 589,208

Excess of revenue over expenses 135,364 135,364 46,568

Transfer of investment income (Note B) 1,305 622 (1 ,927)

Transfer of funds (Note 8) 17,352 (17,352)

Net assets, end of year 133,492 68,685 568,963 771,140 635,776

The accompanying notes are an integral part of these financial statements

4

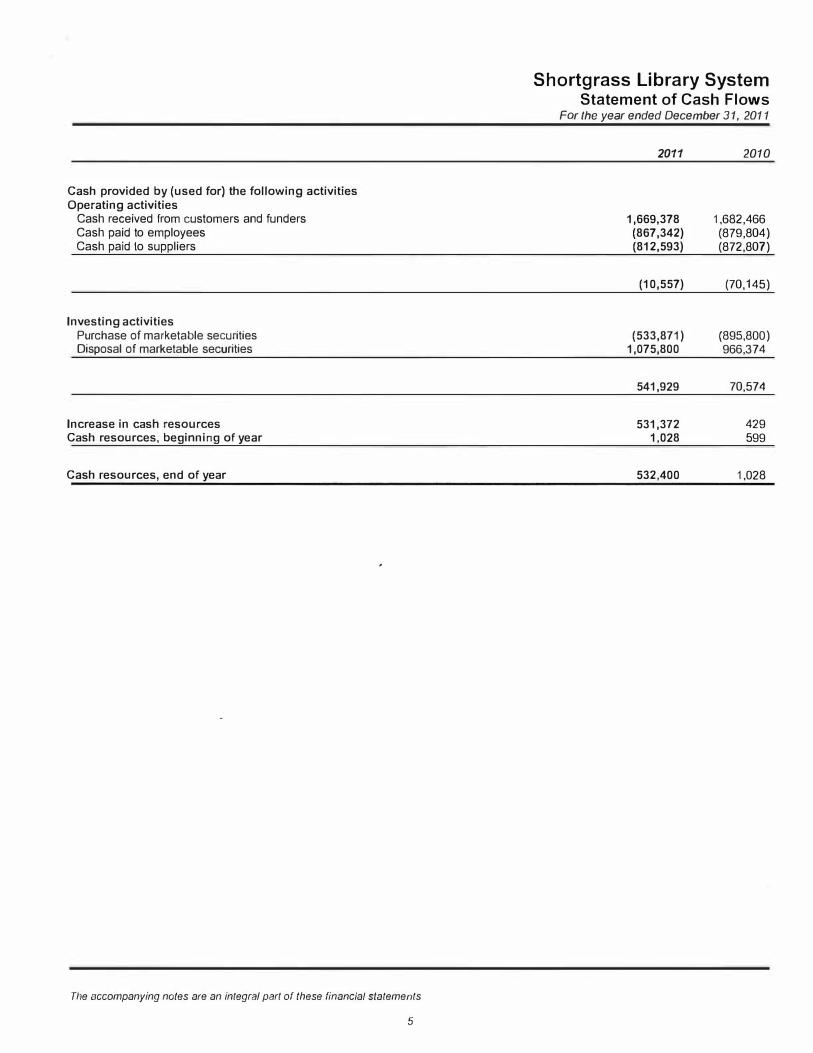

Cash provided by (used for) the following activities Operating activities

Cash received from customers and funders Cash paid to employees Cash paid lo suppliers

Investing activities Purchase of marketable securities Disposal of marketable securities

Increase in cash resources Cash resources, beginning of year

Cash resources, end of year

The accompanying notes are an integral part of these financial statements

5

Shortgrass Library System Statement of Cash Flows

For the year ended December 31, 2011

2011 2010

1,669,378 1,682,466 (867,342) (879,804) (812,593) (872,807)

(1 0,557) (70,145)

(533,871) (895,800) 1,075,800 966,374

541,929 70,574

531,372 429 1,028 599

532,400 1,028

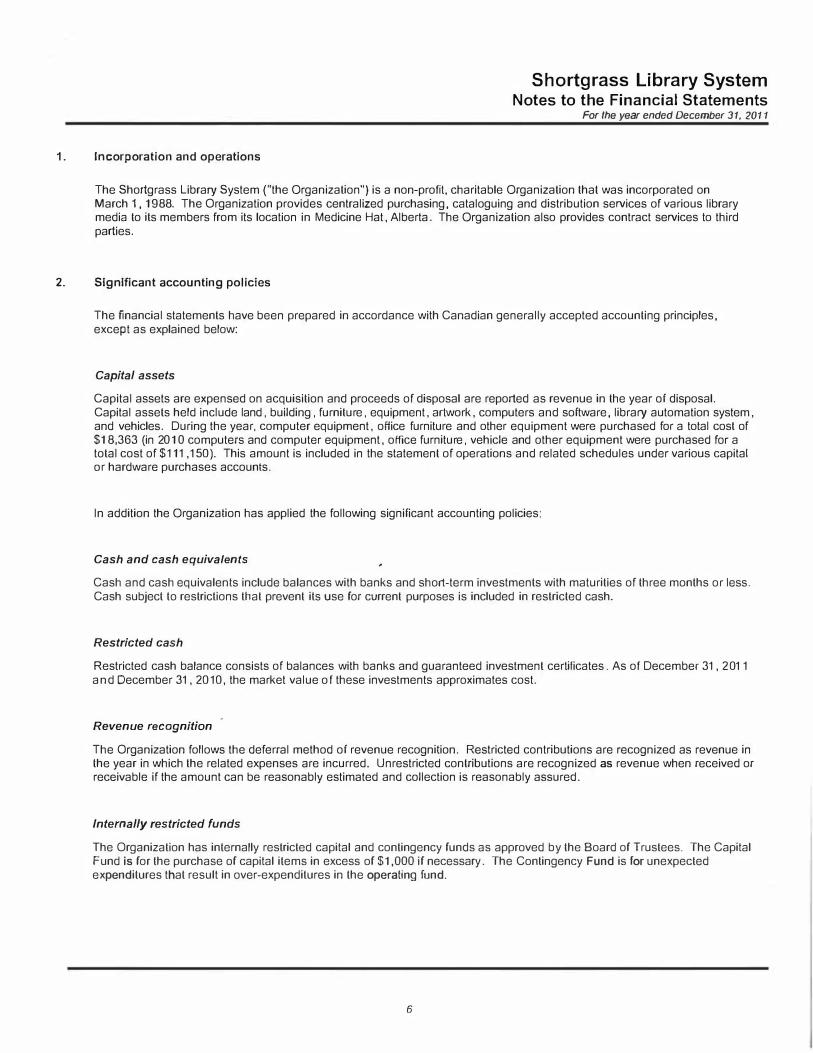

1. Incorporation and operations

Shortgrass Library System Notes to the Financial Statements

For the year ended December 31, 2011

The Shortgrass Library System ("the Organization") is a non-profit, charitable Organization that was incorporated on March 1, 1988. The Organization provides centralized purchasing, cataloguing and distribution services of various library media to its members from its location in Medicine Hat, Alberta. The Organization also provides contract services to third parties.

2. Significant accounting policies

The financial statements have been prepared in accordance with Canadian generally accepted accounting principles, except as explained below:

Capital assets

Capital assets are expensed on acquisition and proceeds of disposal are reported as revenue in the year of disposal. Capital assets held include land, building, furniture, equipment, artwork, computers and software, library automation system, and vehicles. During the year, computer equipment, office furniture and other equipment were purchased for a total cost of $18 ,36 3 (in 2010 computers and computer equipment, office furniture, vehicle and other equipment were purchased for a total cost of $ 111,150 ). This amount is included in the statement of operations and related schedules under various capital or hardware purchases accounts.

In addition the Organization has applied the following significant accounting policies:

Cash and cash equivalents

Cash and cash equivalents include balances with banks and short-term investments with maturities of three months or less. Cash subject to restrictions that prevent its use for current purposes is included in restricted cash.

Restricted cash

Restricted cash balance consists of balances with banks and guaranteed investment certificates. As of December 31, 2011 and December 31, 20 10 , the market value of these investments approximates cost.

Revenue recognition

The Organization follows the deferral method of revenue recognition. Restricted contributions are recognized as revenue in the year in which the related expenses are incurred. Unrestricted contributions are recognized as revenue when received or receivable if the amount can be reasonably estimated and collection is reasonably assured.

Internally restricted funds

The Organization has internally restricted capital and contingency funds as approved by the Board of Trustees. The Capital Fund is for the purchase of capital items in excess of $1,000 if necessary. The Contingency Fund is for unexpected expenditures that result in over-expenditures in the operating fund.

6

2. Significant accounting policies (Continued from previous page)

Income taxes

Shortgrass Library System Notes to the Financial Statements

For the year ended December 31, 2011

The Organization is registered as a charitable organization under the Income Tax Act (the "Act") and as such is exempt from income taxes and is able to issue donation receipts for income tax purposes. In order to maintain its status as a registered charity under the Act, the Organization must meet certain requirements within the Act. In the opinion of management, these requirements have been met.

Measurement uncertainty

The preparation of financial statements in conformity with Canadian generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements. and the reported amounts of revenues and expenses during the reporting period. Accounts receivable are stated after evaluation as to their collectibility and an appropriate allowance for doubtful accounts is provided where considered necessary. These estimates and assumptions are reviewed periodically and, as adjustments become necessary they are reported in earnings in the periods in which they become known.

Contributed materials and services

Contributed materials and services are recognized in the financial statements when their fair value can be reasonably determined and they are used in the normal course of the Organization's operations and would otherwise have been purchased.

Pension expense

The Shortgrass Library System participates in the Local Authorities Pension Plan (LAPP), which is one of the plans covered by the Alberta Public Sector Pension Plans Act. The LAPP serves about 200,000 people and over 400 employers. The LAPP is financed by employer and employee contributions and by investment earnings of the LAPP Fund.

Contributions for current service are recorded as expenditures in the year in which they become due.

The Organization is required to make current service contributions to the LAPP of 9.49% (9.06 % in 201 0 ) of pensionable earnings up to the year's maximum pensionable earnings under the Canadian Pension Plan and 13 .13 % (12 .53 % in 2010 ) on pensionable earnings above this amount. Employees of the Organization are required to mal<e current service contributions of 8 .49% (8 .06 % in 201 0 ) of pensionable salary up to the year's maximum pensionable salary and 12.13 % (11 .53 % in 201 0 ) on pensionable salary above this amount.

Total current service contributions by the Organization to the LAPP in 2011 were $5 9,804 (201 0 - $45,285 ). Total current service contributions by the employees of the Organization to the Local Authorities Pension Plan in 201 1 were $52,94 6 (2010 - $40 ,394).

7

2. Significant accounting policies (Continued from previous page)

Financial instruments

Held for trading:

Shortgrass Library System Notes to the Financial Statements

For the year ended December 31, 201 1

Any financial instrument whose fair value can be reliably measured may be designated as held for trading on initial recognition or adoption of CICA 3855 Financial Instruments- Recognition and Measurement, even if that instrument would not otherwise satisfy the definition of held for trading. The Organization has classified the following financial assets as held for trading: cash and marketable securities (see Note 3 and Note 4 ). The Organization has designated cash and operational GIG's on initial recognition as held for trading in accordance with its risk management strategy, as doing so allows the Organization to eliminate or significantly reduce a measurement or recognition inconsistency; as the instruments are evaluated on a fair value basis in accordance with the Organization's documented risk management strategy and reported to key management personnel on that basis. These instruments are initially recognized at their fair value, determined by published price quotations in an active market.

Fees incurred on an exchange of financial liabilities or a modification of the terms of financial liabilities that is accounted for as an extinguishment are included as part of the gain or loss on extinguishment, while any related other costs incurred are recognized in current year earnings. All fees and costs incurred on the exchange or modification of a financial liability not accounted for as an extinguishment, are recognized in current year earnings.

Held for trading financial instruments are subsequently measured at their fair value. Net gains and losses arising from changes in fair value include interest and dividend income and are recognized immediately in income.

Loans and receivables:

The Organization has classified the following financial-assets as loans and receivables: trade accounts receivable, grant receivable and accrued interest receivable. These assets are initially recognized at their fair value, determined by terms of the agreement entered into. Fair value is approximated by the instrument's initial cost in a transaction between unrelated parties. Transactions to purchase or sell these items are recorded on the trade dale, and transaction costs are immediately recognized in income.

Loans and receivables are subsequently measured at their amortized cost, using the effective interest method. Under this method, estimated future cash receipts are exactly discounted over the asset's expected life, or other appropriate period, to its net carrying value. Amortized cost is the amount at which the financial asset is measured at initial recognition less principal repayments. plus or minus the cumulative amortization using the effective interest method of any difference between that initial amount and the maturity amount. and less any reduction for impairment or uncolleclabilily. Net gains and losses arising from changes in fair value include interest and are recognized in net income upon derecognition or impairment.

8

2. Significant accounting policies (Continued from previous page)

Held to maturity:

Shortgrass Library System Notes to the Financial Statements

For the year ended December 31, 2011

The Organization has classified the following financial assets as held to maturity: restricted cash (see Note 5 ). These assets are initially recognized at their fair value, determined by recent arm's length market transactions for the same instrument. Fair value is approximated by the instrument' s initial cost in a transaction between unrelated parties. Transactions to purchase or sell these items are recorded on the trade date, and transaction costs are immediately recognized in income.

Held to maturity financial assets are subsequently measured at amortized cost using the effective interest method. Under this method, estimated future cash receipts are exactly discounted over the asset's expected life, or other appropriate period, to its net carrying value. Amortized cost is the amount at which the financial asset is measured at initial recognition less principal repayments, plus or minus the cumulative amortization using the effective interest method of any difference between that initial amount and the maturity amount, and less any reduction for impairment or uncollectability. Net gains and losses arising from changes in fair value include interest and are recognized in net income upon derecognition or impairment.

Other financial liabilities:

The Organization has classified the following financial liabilities as other financial liabilities: accounts payable and accruals. These liabilities are initially recognized at their fair value. Fair value is approximated by the instrument's initial cost in a transaction between unrelated parties. Transactions to purchase or sell these items are recorded on the trade date, and transaction costs are immediately recognized in income.

Fees incurred on an exchange of financial liabilities or a modification of the terms of financial liabilities that is accounted for as an extinguishment are included as part of the gain 'or loss on extinguishment, while any related other costs incurred are recognized in current year earnings. Any related other costs incurred are recognized in current year earnings.

Other financial liabilities are subsequently measured at amortized cost using the effective interest method. Under this method, estimated future cash payments are exactly discounted over the liability's expected life, or other appropriate period, to its net carry value. Amortized cost is the amount at which the financial liability is measured at initial recognition less principal repayments, and plus or minus the cumulative amortization using the effective interest method of any difference between that initial amount and the maturity amount. Net gains and losses arising from changes in fair value include interest income and are recognized in net income upon derecognition or impairment.

Recent Accounting Pronouncements

Canadian accounting standards for not-for-profit organizations

In October 2010, the Accounting Standards Board (AcSB) approved the accounting standards for private sector not-forprofit organizations (NFPOs) to be included in Part Ill of the CICA Handbook-Accounting ("Handbook"). Part Ill will comprise:

• The existing "4400 series" of standards dealing with the unique circumstances of NFPOs, currently in Part V of the Handbook; and

• The new accounting standards for private enterprises in Part II of the Handbook, to the extent that they would apply to NFPOs.

Effective for fiscal years beginning on or after January 1, 2 012 , private sector NFPOs will have the option to adopt either Part Ill of the Handbook or International Financial Reporting Standards (I FRS). Earlier adoption is permitted.

9

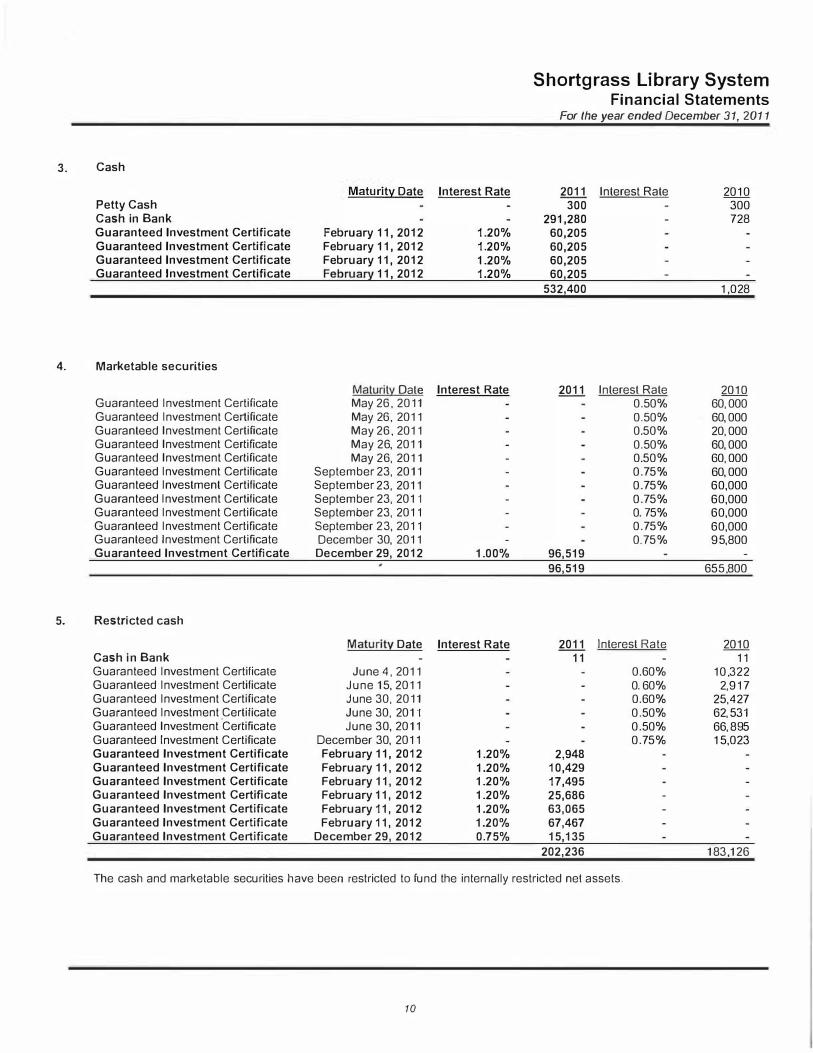

3. Cash

4.

5.

Petty Cash Cash in Bank Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate

Marketable securities

Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate

Restricted cash

Cash in Bank Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment _Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate Guaranteed Investment Certificate

Maturity Date

February 11, 2012 February 11, 2012 February 11, 2012 February 11, 2012

Maturity Date May 26, 2011 May 26, 2011 May 26, 2011 May 26, 2011 May 26, 2011

September 23, 2011 September 23, 2011 September 23, 201·1 September 23, 2011 September 23, 2011 December 30, 2011

December 29, 2012

Maturity Date

June 4, 2011 June15,2011 June 30, 2011 June 30, 201"1 June 30, 2011

December 30, 2011 February 11, 2012 February 11, 2012 February 11, 2012 February 11, 2012 February 11, 2012 February 11, 2012

December 29, 2012

Interest Rate

1.20% 1.20% 1.20% 1.20%

Interest Rate

1.00%

Interest Rate

1.20% 1.20% 1.20% 1.20% 1.20% 1.20% 0.75%

Shortgrass Library System Financial Statements

For the year ended December 31, 2011

2011 Interest Rate 300

291,280 60,205 60,205 60,205 60,205

532,400

2011

96,519 96,519

2011 11

2,948 10,429 17,495 25,686 63,065 67,467 15,135

202,236

Interest Rate 0 .50% 0 .50% 0.50% 0.50% 0.50% 0 .75% 0 .75% 0 .75% 0.75% 0 .75% 0.75%

Interest Rate

0 .60% 0.60% 0.60% 0 .50% 0 .50% 0 .75%

2010 300 728

1,028

2010 60,000 60,000 20,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 95,800

655,800

2010 11

10,322 2,917

25,427 62,531 66,895 15,023

183,126

The cash and marketable securities have been restricted to fund the internally restricted net assets.

10

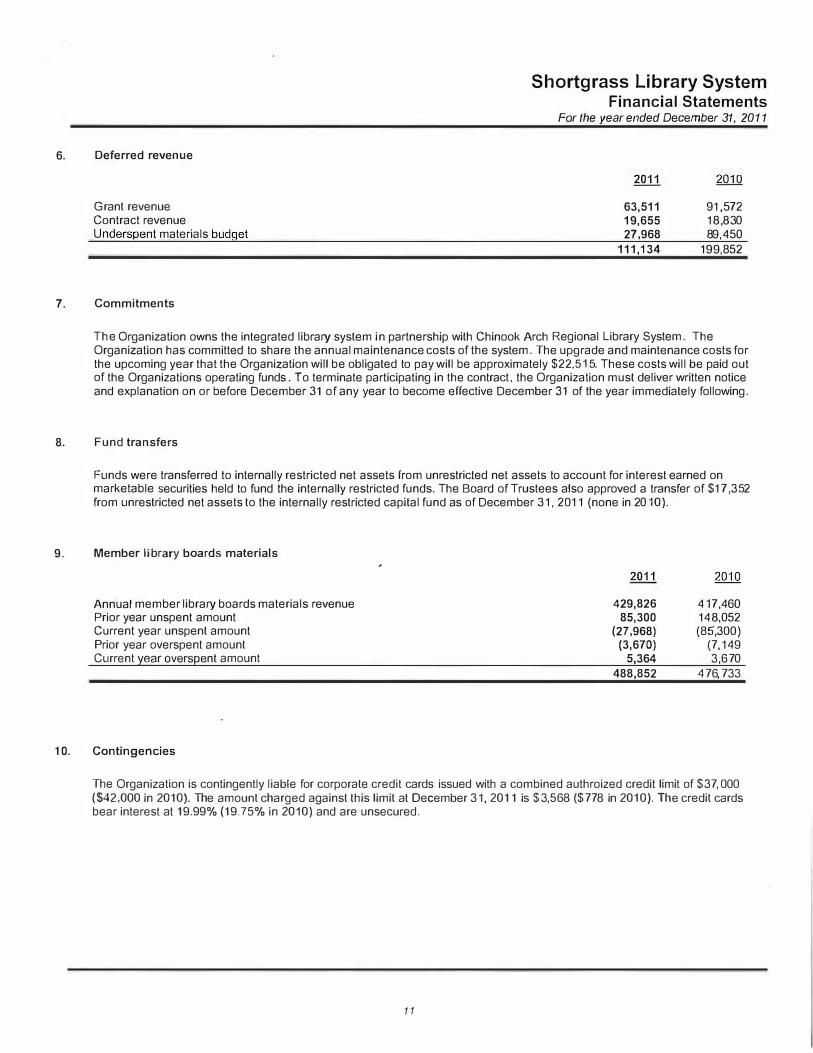

6. Deferred revenue

Grant revenue Contract revenue Underspent materials budget

7. Commitments

Shortgrass Library System Financial Statements

For the year ended December 31, 20 11

63,511 19,655 27,968

111,134

91 ,572 18,830 89,450

199,852

The Organization owns the integrated library system in partnership with Chinook Arch Regional Library System. The Organization has committed to share the annual maintenance costs of the system. The upgrade and maintenance costs for the upcoming year that the Organization will be obligated to pay will be approximately $22,515. These costs will be paid out of the Organizations operating funds. To terminate participating in the contract, the Organization must deliver written notice and explanation on or before December 31 of any year to become effective December 31 of the year immediately following.

8. Fund transfers

Funds were transferred to internally restricted net assets from unrestricted net assets to account for interest earned on marketable securities held to fund the internally restricted funds. The Board of Trustees also approved a transfer of $17,352 from unrestricted net assets to the internally restricted capital fund as of December 31, 2011 (none in 20·1 0).

9. Member library boards materials

Annual member library boards materials revenue Prior year unspent amount Current year unspent amount Prior year overspent amount Current year overspent amount

10. Contingencies

429,826 85,300

(27,968) (3,670)

5,364 488,852

417,460 148,052 (85,300 )

(7,149 3 ,670

476,733

The Organization is contingently liable for corporate credit cards issued with a combined authroized credit limit of $37,000 ($42,000 in 2010). The amount charged against this limit at December 31, 2011 is $3,568 {$778 in 20'10). The credit cards bear interest at 19.99% (19.75% in 2010) and are unsecured.

11

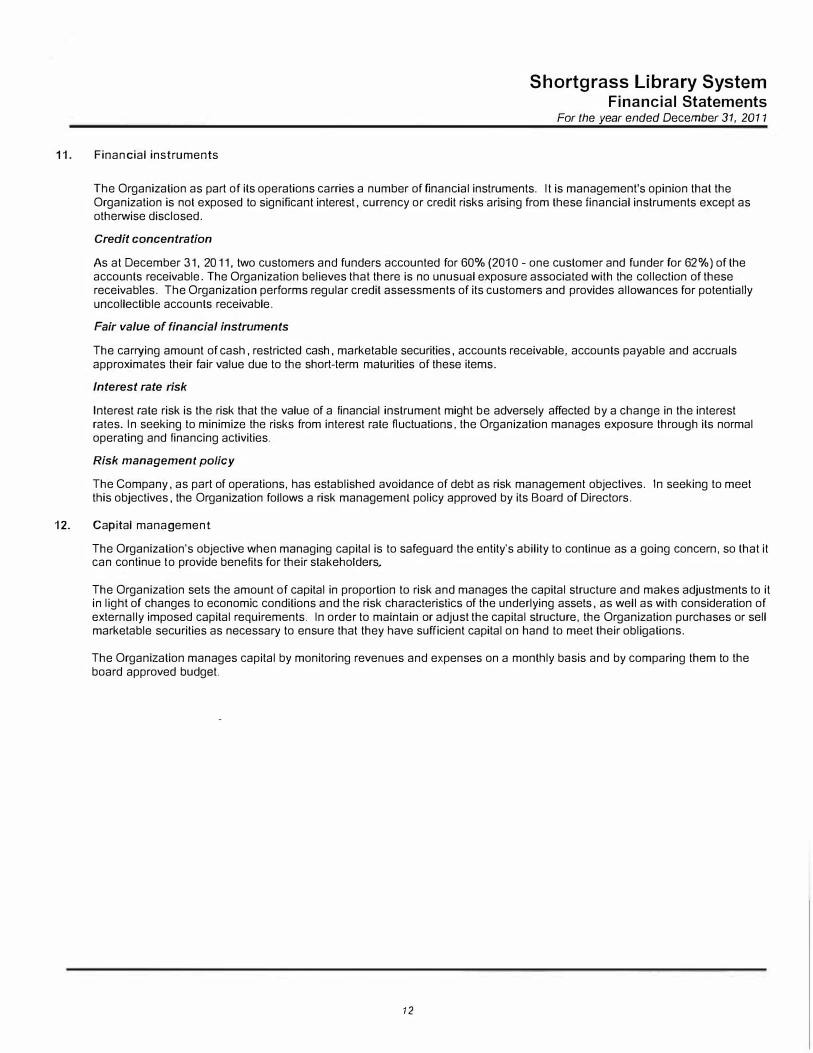

11. Financial instruments

Shortgrass Library System Financial Statements

For the year ended December 31, 2011

The Organization as part of its operations carries a number of financial instruments. It is management's opinion that the Organization is not exposed to significant interest, currency or credit risks arising from these financial instruments except as otherwise disclosed.

Credit concentration

As at December 31, 2011, two customers and funders accounted for 6 0% (2010- one customer and funder for 6 2%) of the accounts receivable. The Organization believes that there is no unusual exposure associated with the collection of these receivables. The Organization performs regular credit assessments of its customers and provides allowances for potentially uncollectible accounts receivable.

Fair value of financial instruments

The carrying amount of cash, restricted cash, marketable securities, accounts receivable, accounts payable and accruals approximates their fair value due to the short-term maturities of these items.

Interest rate risk

Interest rate risk is the risk that the value of a financial instrument might be adversely affected by a change in the interest rates. In seeking to minimize the risks from interest rate nuctuations, the Organization manages exposure through its normal operating and financing activities.

Risk management policy

The Company, as part of operations, has established avoidance of debt as risk management objectives. In seeking to meet this objectives, the Organization follows a risk management policy approved by its Board of Directors.

12. Capital management

The Organization's objective when managing capital is to safeguard the entity's ability to continue as a going concern, so that it can continue to provide benefits for their stakeholders,

The Organization sets the amount of capital in proportion to risk and manages the capital structure and makes adjustments to it in light of changes to economic conditions and the risk characteristics of the underlying assets, as well as with consideration of externally imposed capital requirements. In order to maintain or adjust the capital structure, the Organization purchases or sell marketable securities as necessary to ensure that they have sufficient capital on hand to meet their obligations.

The Organization manages capital by monitoring revenues and expenses on a monthly basis and by comparing them to the board approved budget.

12

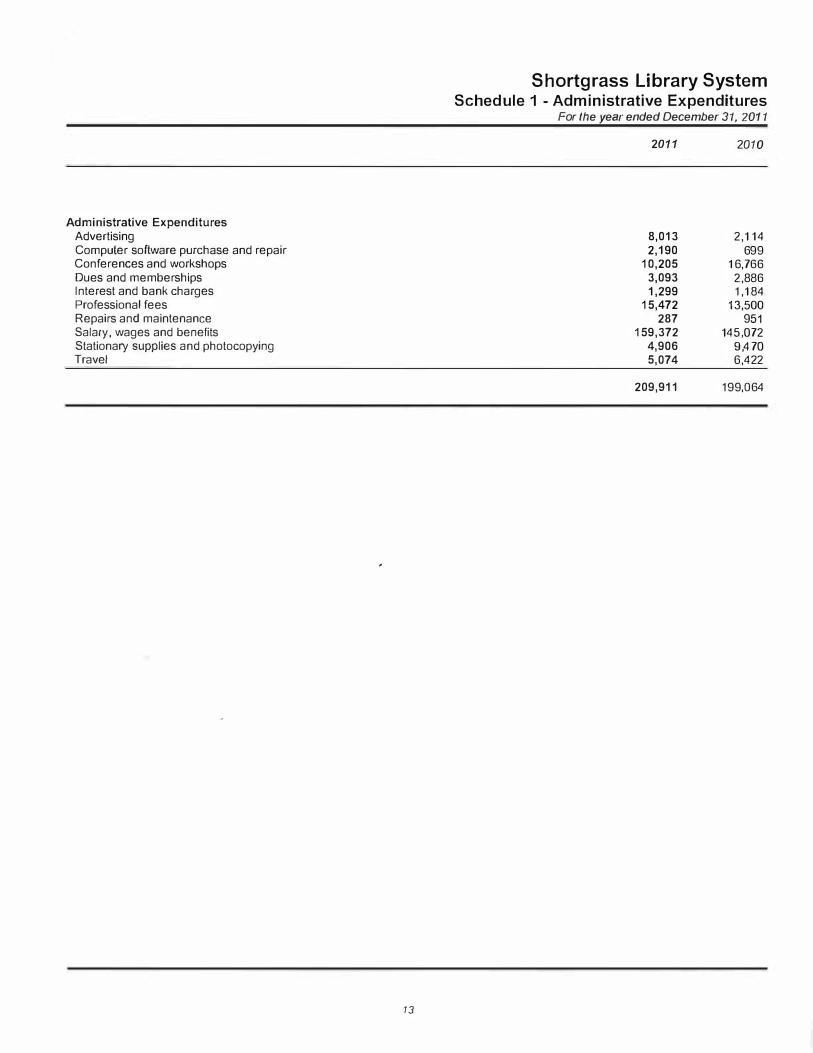

Administrative Expenditures Advertising Computer software purchase and repair Conferences and workshops Dues and memberships Interest and bank charges Professional fees Repairs and maintenance Salary, wages and benefits Stationary supplies and photocopying Travel

13

Shortgrass Library System Schedule 1 - Administrative Expenditures

For the year ended December 31, 2011

2011 2010

8,013 2,190

10,205 3,093 1,299

15,472 287

159,372 4,906 5,074

209,911

2 ,114 699

16,766 2 ,886 1,184

13,500 9 51

145,072 9,470 6,422

199,064

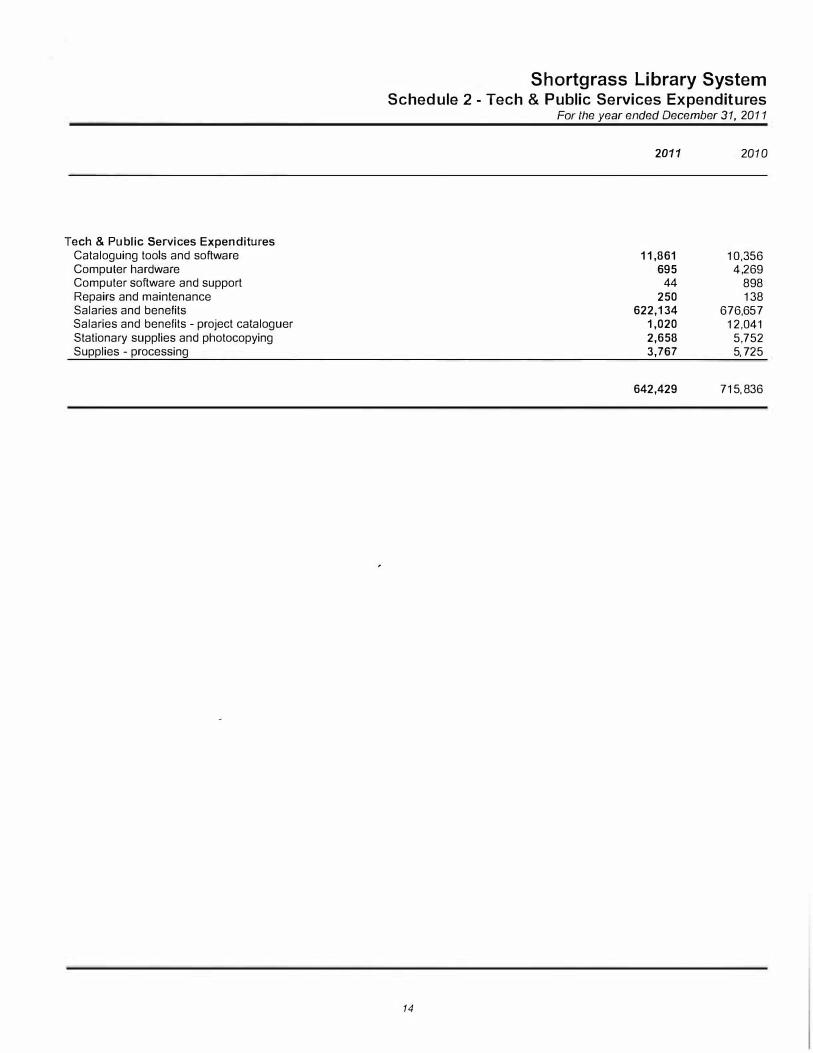

Tech & Public Services Expenditures Cataloguing tools and software Computer hardware Computer software and support Repairs and maintenance Salaries and benefits Salaries and benefits - project cataloguer Stationary supplies and photocopying Supplies - processing

Shortgrass Library System Schedule 2- Tech & Public Services Expenditures

For the year ended December 31, 2011

14

2011 2010

11,861 695 44

250 622,134

1,020 2,658 3,767

642,429

10,356 4,26 9

8 98 138

676,657 12,041

5,752 5,725

715,836

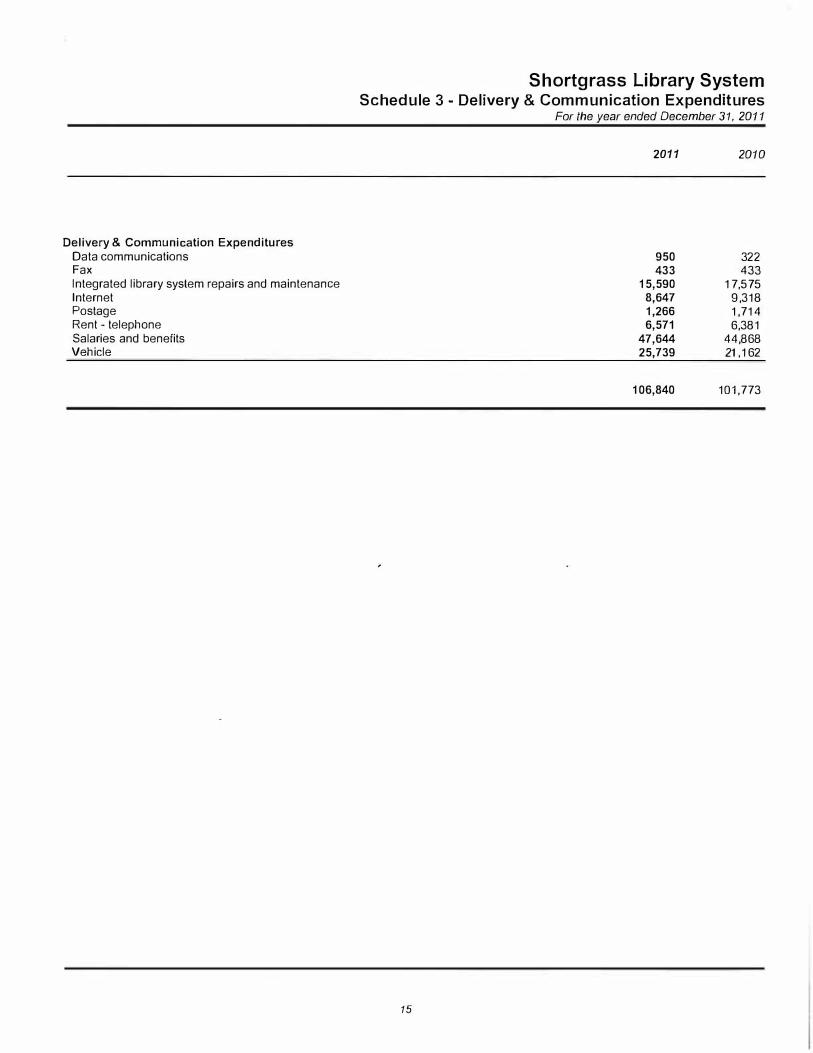

Delivery & Communication Expenditures Data communications Fax Integrated library system repairs and maintenance Internet Postage Rent - telephone Salaries and benefits Vehicle

Shortgrass Library System Schedule 3- Delivery & Communication Expenditures

For the year ended December 31, 2011

15

2011 2010

950 322 433 433

15,590 17,575 8,647 9,318 1,266 1,714 6,571 6,381

47,644 44,868 25,739 21 '162

106,840 101,773