Embed Size (px)

Citation preview

Audit of Cash

Prepared by :-•Nurulain binti Asri•Nur Athirah binti Abd Hadi•Nur Atiqah Syafiqa binti Rosli•Tuan Noorfarahanim binti Tuan Ibrahim

Prepared for :-•Nor Azam bin Yaacob

What are the auditor’s What are the auditor’s primary concernsprimary concerns with regard to with regard to cashcash??

• existence• completeness• physical control• presentation and disclosure

Cash Audit ProceduresCash Audit Procedures

perform analytical proceduresto test the

reasonablenessof cash balances

Cash Audit ProceduresCash Audit Procedures

Enquire of management regarding anycash requirements or restrictions from

debt agreements.

What is What is kitingkiting??

Kiting is an irregularity wherebyan overstatement of cash is

created by a cash transfer betweenbank accounts.

The deposit isrecorded in cash receipts but

the disbursement is not re-corded in cash disbursements.

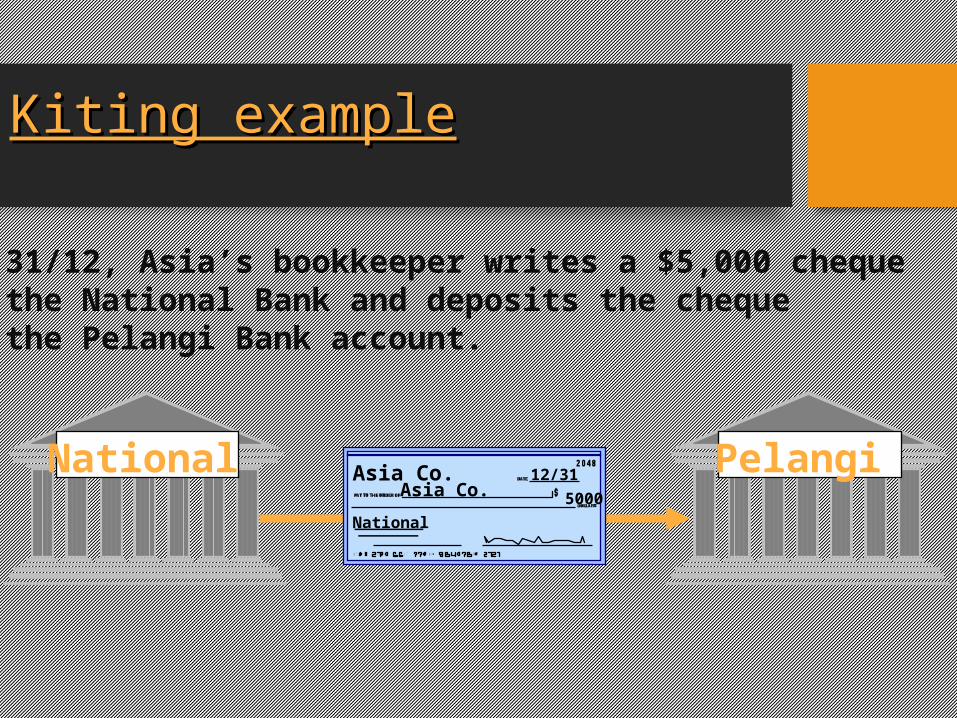

Kiting exampleKiting example

On 31/12, Asia’s bookkeeper writes a $5,000 chequeon the National Bank and deposits the cheque in the Pelangi Bank account.

National Pelangi12/31 Asia Co.Asia Co. 5000

National

cash receipts journaldescription _ $$ _Dec. 31, 2004Misc. revenue 5000

cash payments journaldescription _ $$ _Dec.31, 2004 - no activity -

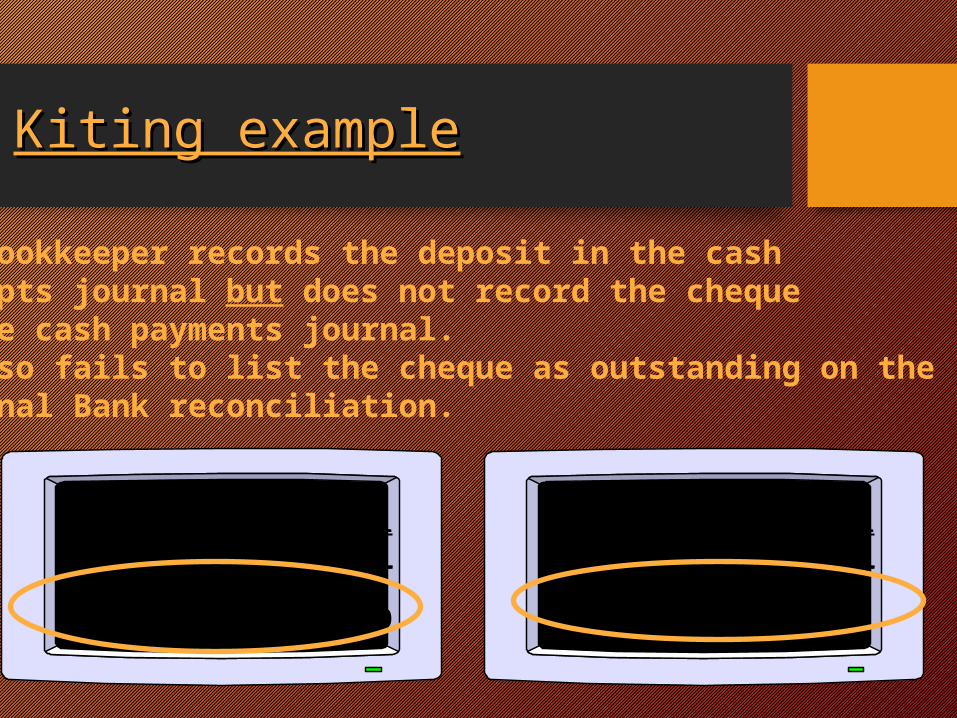

Kiting exampleKiting example

The bookkeeper records the deposit in the cash receipts journal but does not record the chequein the cash payments journal. He also fails to list the cheque as outstanding on the National Bank reconciliation.

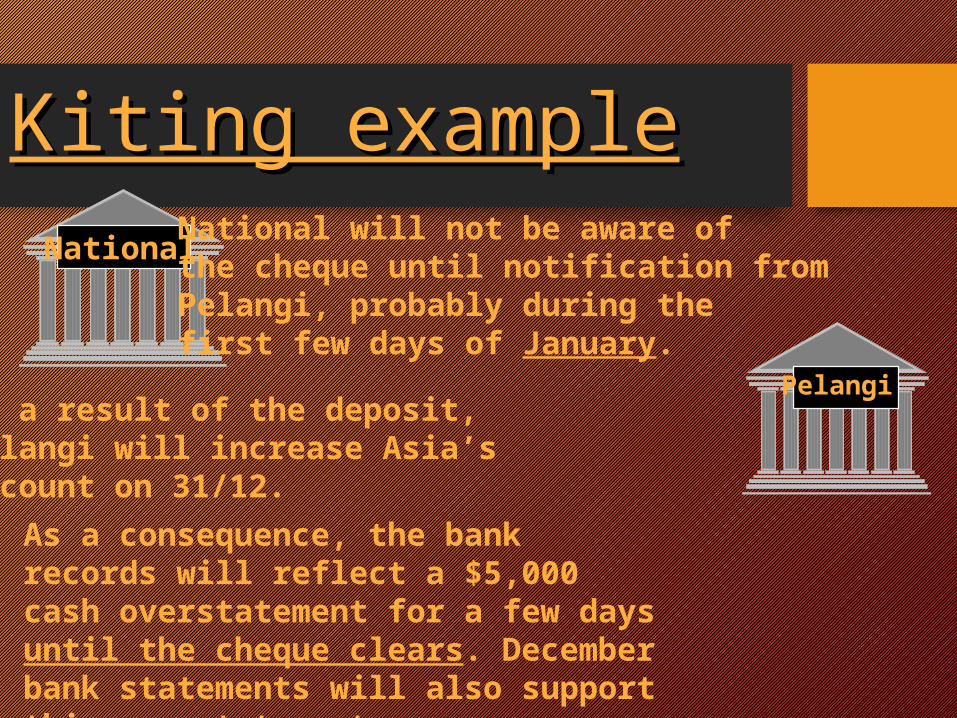

Kiting exampleKiting exampleNational

Pelangi

National will not be aware of the cheque until notification fromPelangi, probably during thefirst few days of January.

As a result of the deposit,Pelangi will increase Asia’s account on 31/12.

As a consequence, the bank records will reflect a $5,000 cash overstatement for a few days until the cheque clears. December bank statements will also support this overstatement.

From an internal control perspective, From an internal control perspective, why does why does kitingkiting occur? occur?

inadequate segregation ofduties between accounting and cash custody

What effect is What effect is changing technologychanging technology having on the likelihood of having on the likelihood of kitingkiting??

Kiting is becomingless likely because the “float” is shrinking; i.e., cheques clear banks faster than in the past.

What What audit proceduresaudit procedures may detect may detect kitingkiting??

tests related tothe cutoff bank statement and schedule of bank transfers

Cash Audit ProceduresCash Audit Procedures

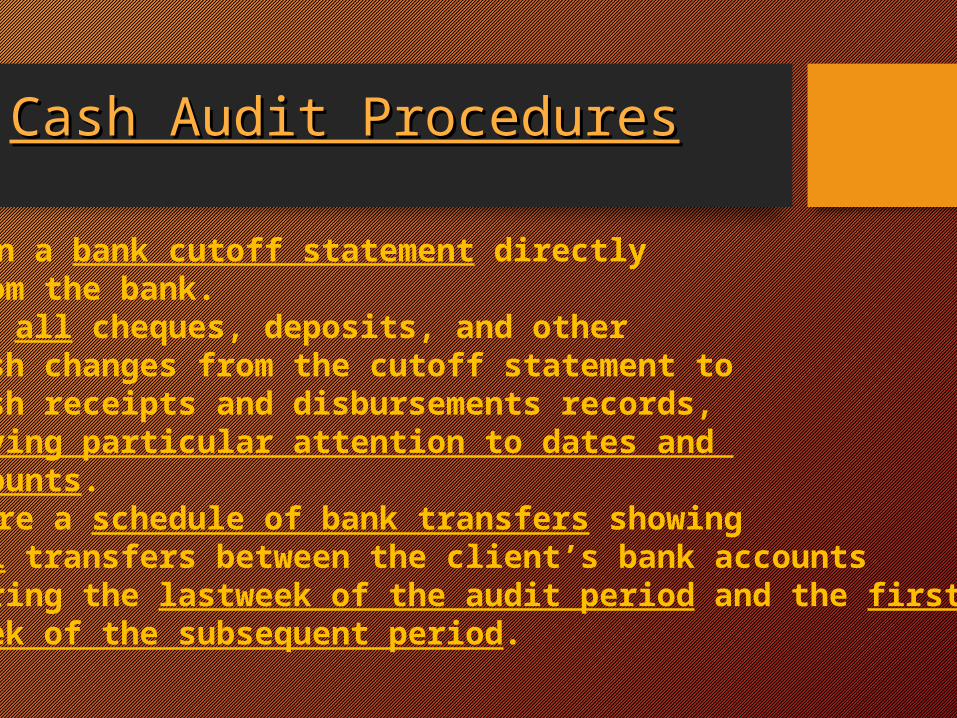

Obtain a bank cutoff statement directlyfrom the bank.

A bank cutoffstatement is prepared

ten business days after thebalance sheet date.

Most items that were outstand-ing at year-end have clearedwhen the cutoff statement

is prepared (cheques, deposits).

Cash Audit ProceduresCash Audit Procedures

• Obtain a bank cutoff statement directly from the bank.• Trace all cheques, deposits, and other cash changes from the cutoff statement to cash receipts and disbursements records, paying particular attention to dates and amounts.• Prepare a schedule of bank transfers showing all transfers between the client’s bank accounts during the lastweek of the audit period and the first week of the subsequent period.

Cash Audit ProceduresCash Audit Procedures

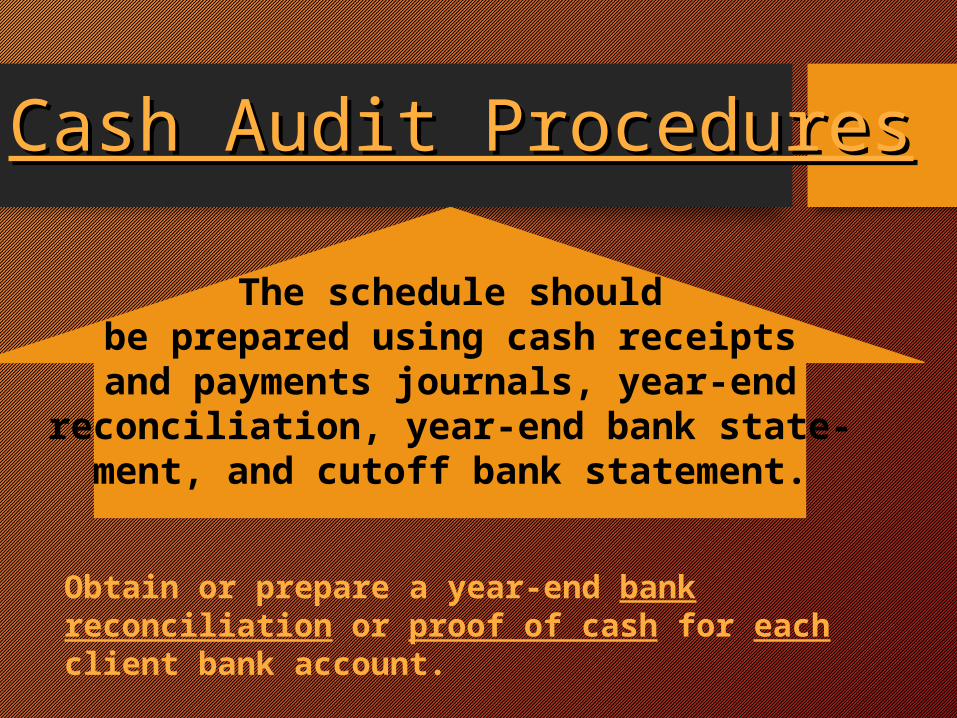

The schedule shouldbe prepared using cash receiptsand payments journals, year-end

reconciliation, year-end bank state-ment, and cutoff bank statement.

Obtain or prepare a year-end bank reconciliation or proof of cash for each client bank account.

Cash Audit ProceduresCash Audit Procedures

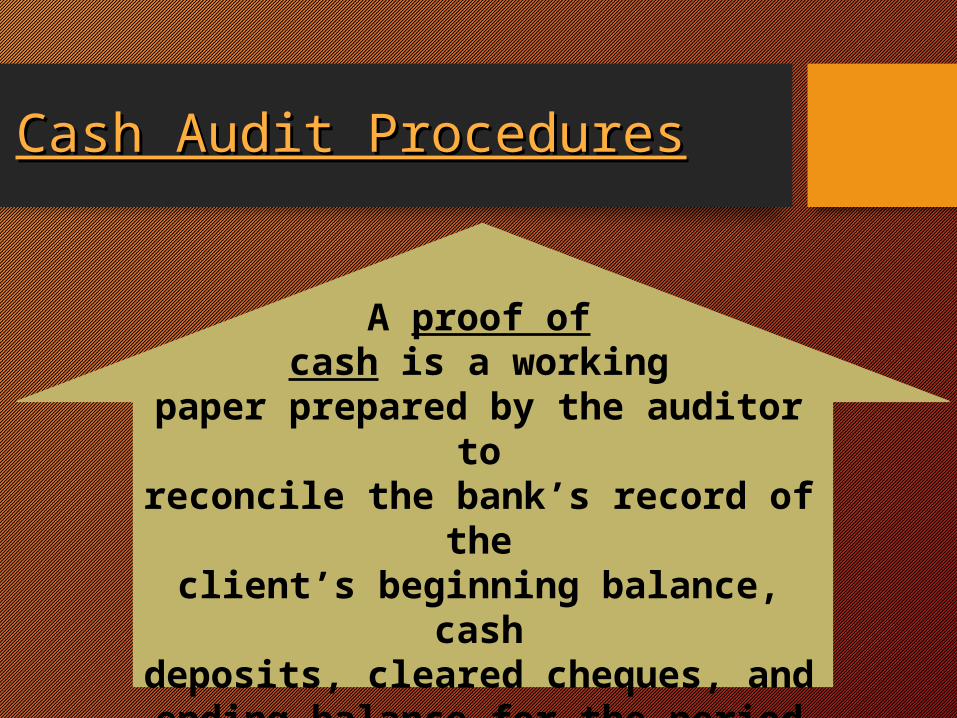

A proof ofcash is a working

paper prepared by the auditor toreconcile the bank’s record of theclient’s beginning balance, cashdeposits, cleared cheques, and

ending balance for the period withthe client’s records.

Cash Audit ProceduresCash Audit Procedures

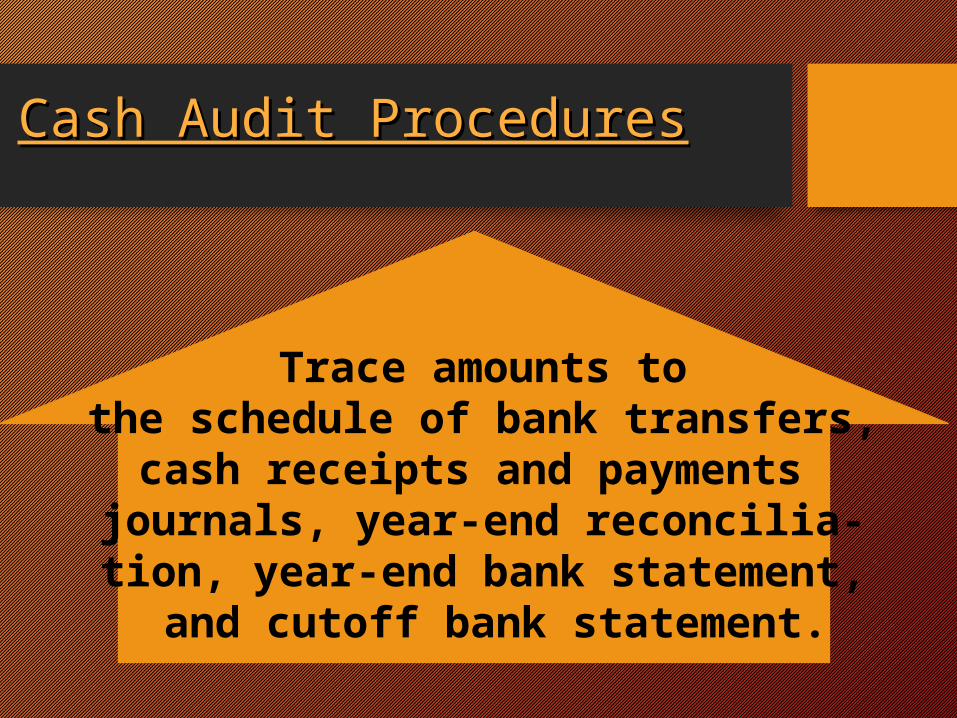

Trace amounts tothe schedule of bank transfers,

cash receipts and payments journals, year-end reconcilia-

tion, year-end bank statement, and cutoff bank statement.

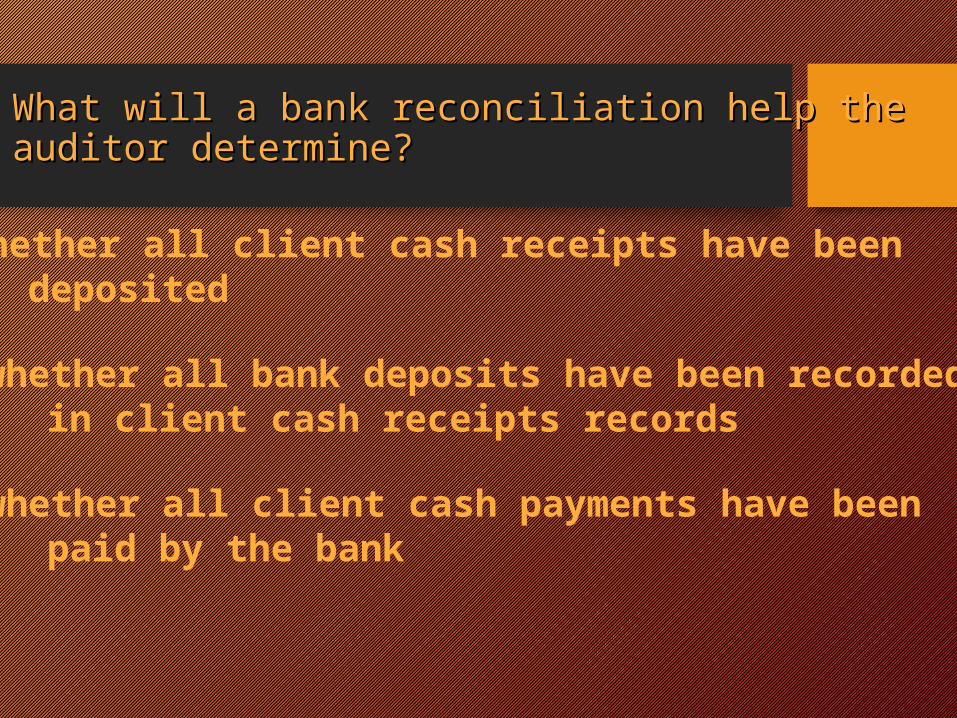

What will a bank reconciliation help the auditor What will a bank reconciliation help the auditor determine?determine?

- whether all client cash receipts have been deposited

- whether all bank deposits have been recorded in client cash receipts records

- whether all client cash payments have been paid by the bank

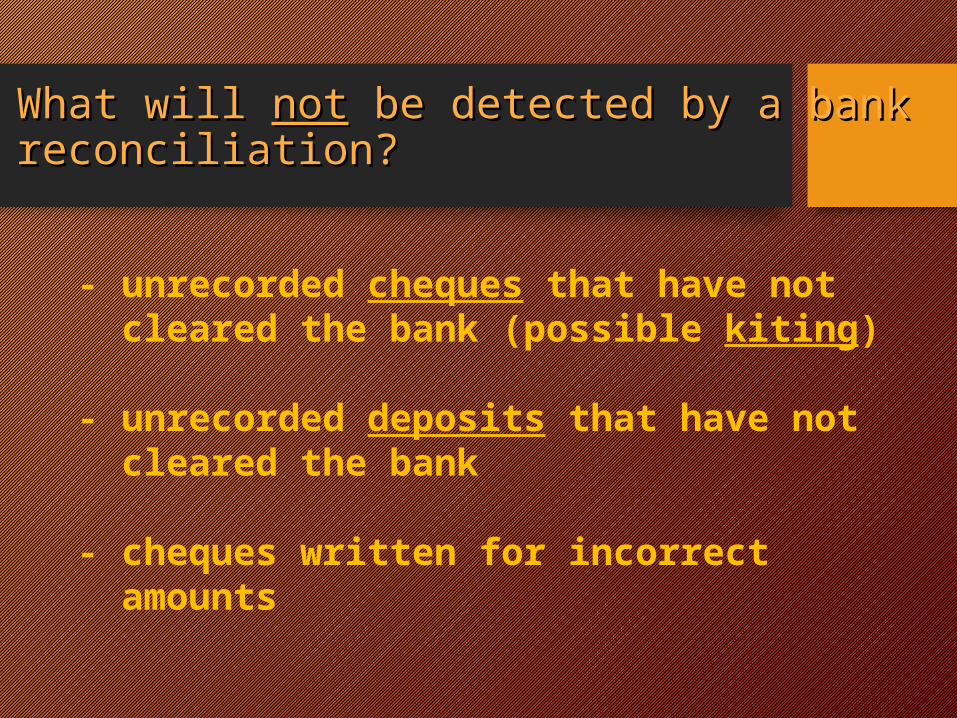

What will What will notnot be detected by a bank be detected by a bank reconciliation?reconciliation?

- unrecorded cheques that have not cleared the bank (possible kiting)

- unrecorded deposits that have not cleared the bank

- cheques written for incorrect amounts

Cash Audit ProceduresCash Audit Procedures

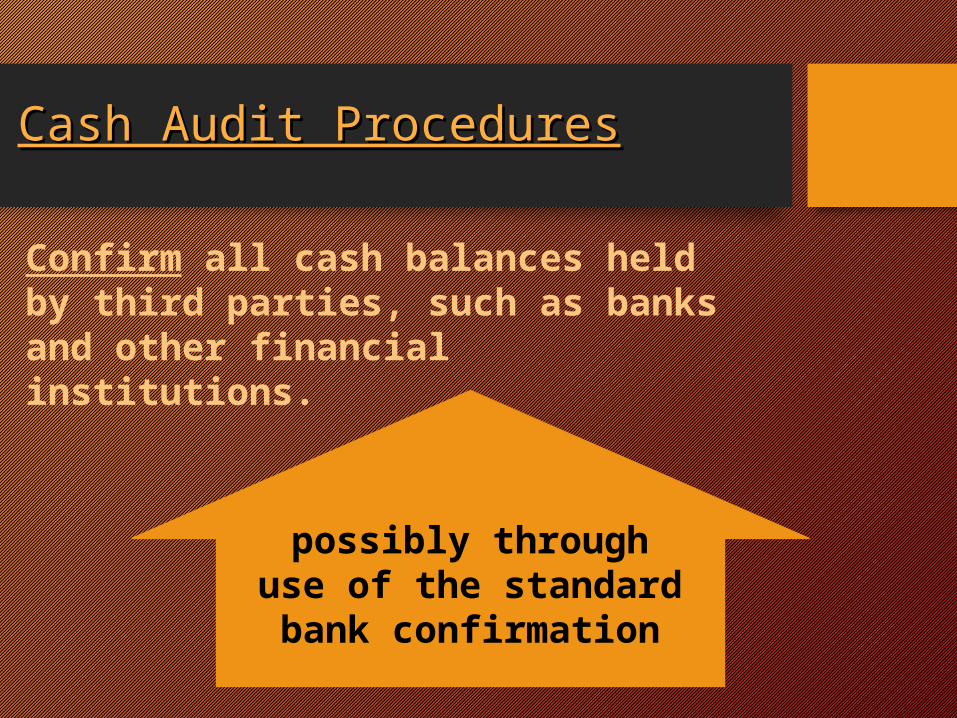

Confirm all cash balances held by third parties, such as banks and other financial institutions.

possibly throughuse of the standardbank confirmation

Cash Audit ProceduresCash Audit Procedures

Count all cash on hand at the client’spremises. If cash is located in multipleplaces, count cash simultaneously toavoid double counting.

Cash Audit ProceduresCash Audit Procedures

Review cutoffof cash receipts

anddisbursements.

Cash Audit ProceduresCash Audit Procedures

Review monthlyclient-prepared

bankreconciliations.

Cash Audit ProceduresCash Audit Procedures

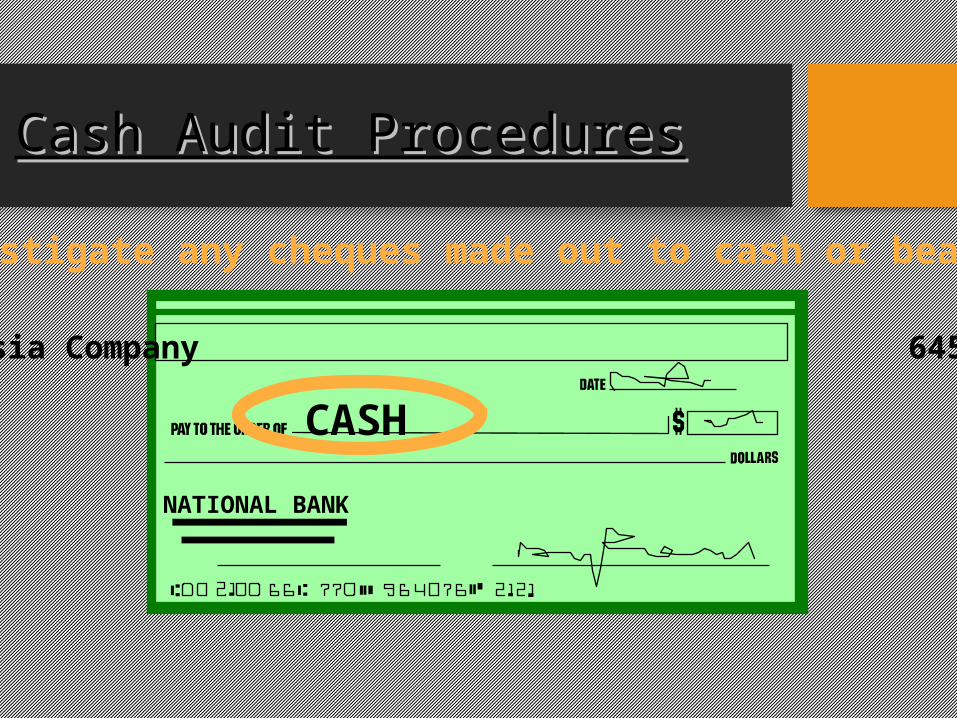

Investigate any cheques made out to cash or bearer.

Asia Company 6458

CASH

NATIONAL BANK

Cash Audit ProceduresCash Audit Procedures

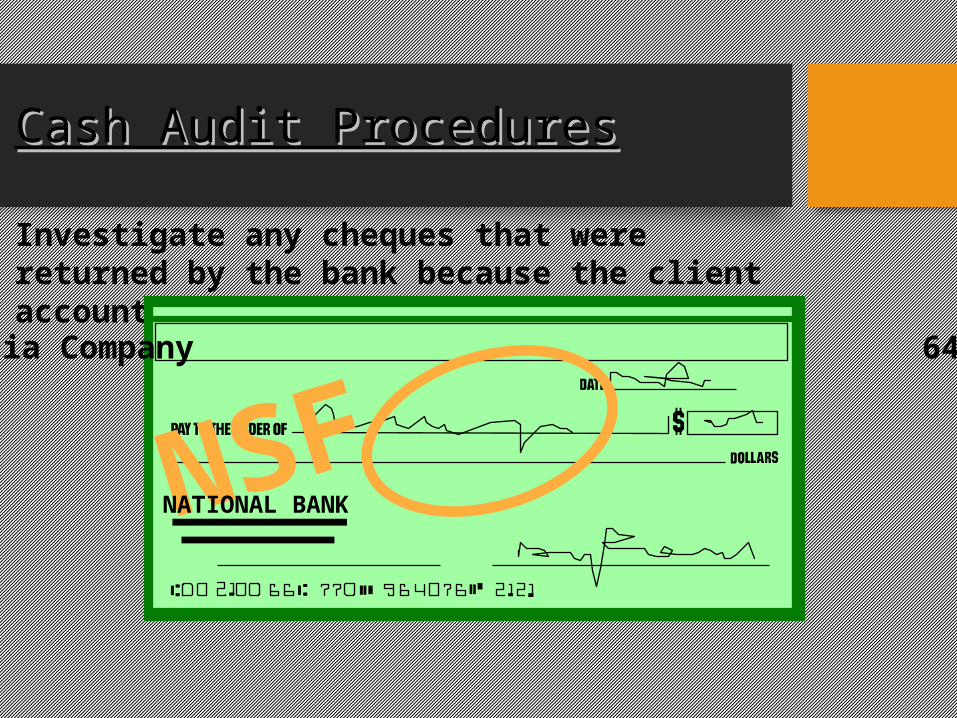

Investigate any cheques that were returned by the bank because the client account had insufficient funds.

Asia Company 6458

NSFNATIONAL BANK

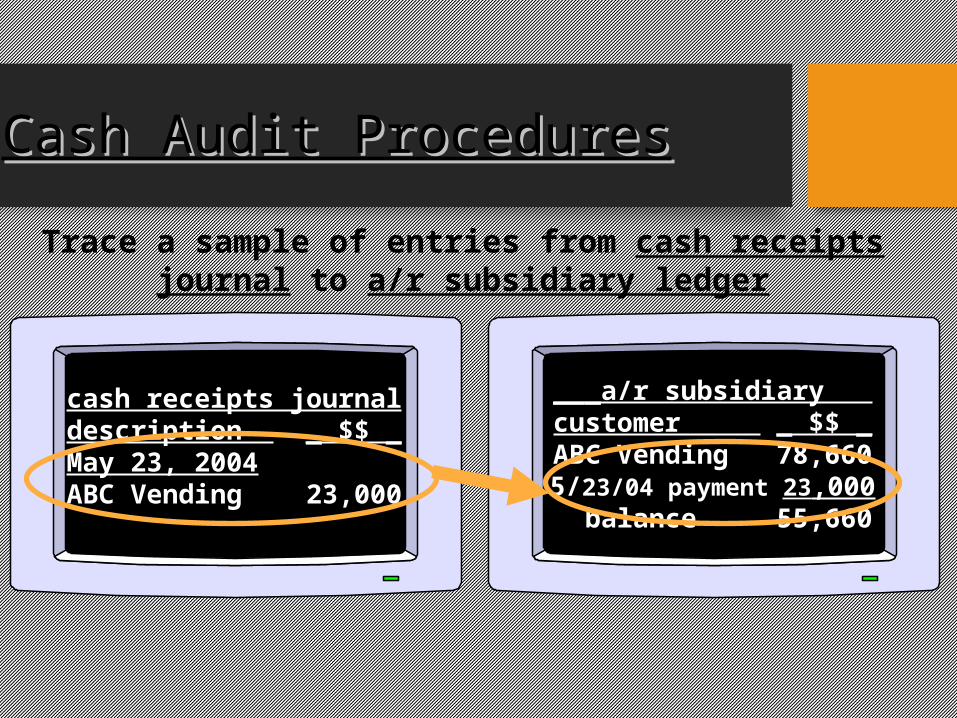

Trace a sample of entries from cash receipts journal to a/r subsidiary ledger

Cash Audit ProceduresCash Audit Procedures

cash receipts journaldescription _ $$ _May 23, 2004ABC Vending 23,000

___a/r subsidiary customer _ $$ _ABC Vending 78,6605/23/04 payment 23,000 balance 55,660

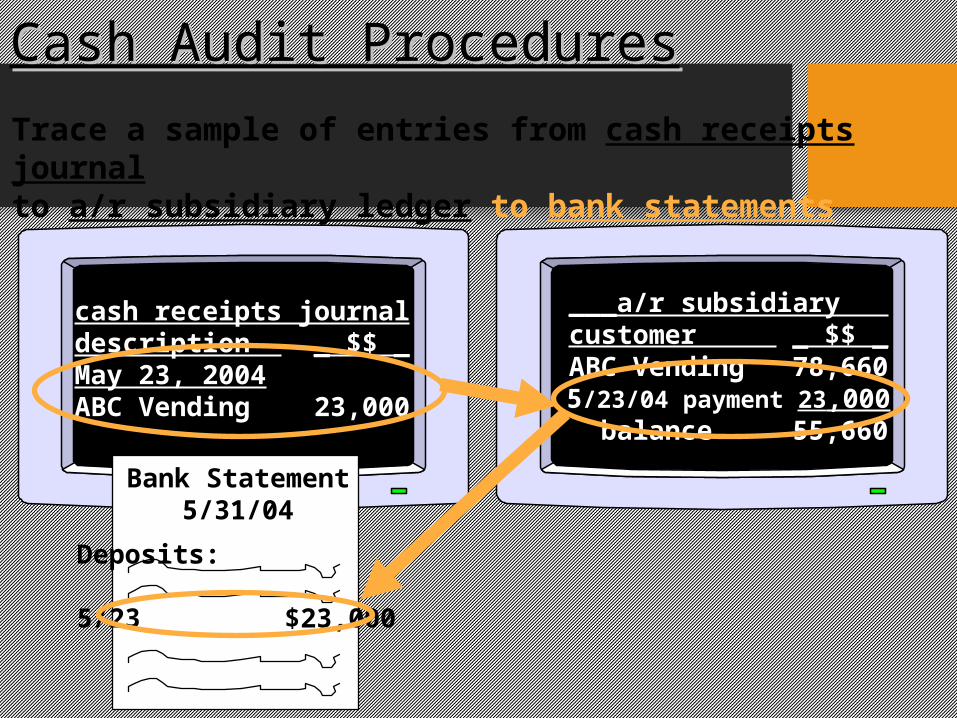

Trace a sample of entries from cash receipts journal to a/r subsidiary ledger to bank statements

cash receipts journaldescription _ $$ _May 23, 2004ABC Vending 23,000

Bank Statement5/31/04

Deposits:

5/23 $23,000

Cash Audit ProceduresCash Audit Procedures

___a/r subsidiary customer _ $$ _ABC Vending 78,6605/23/04 payment 23,000 balance 55,660

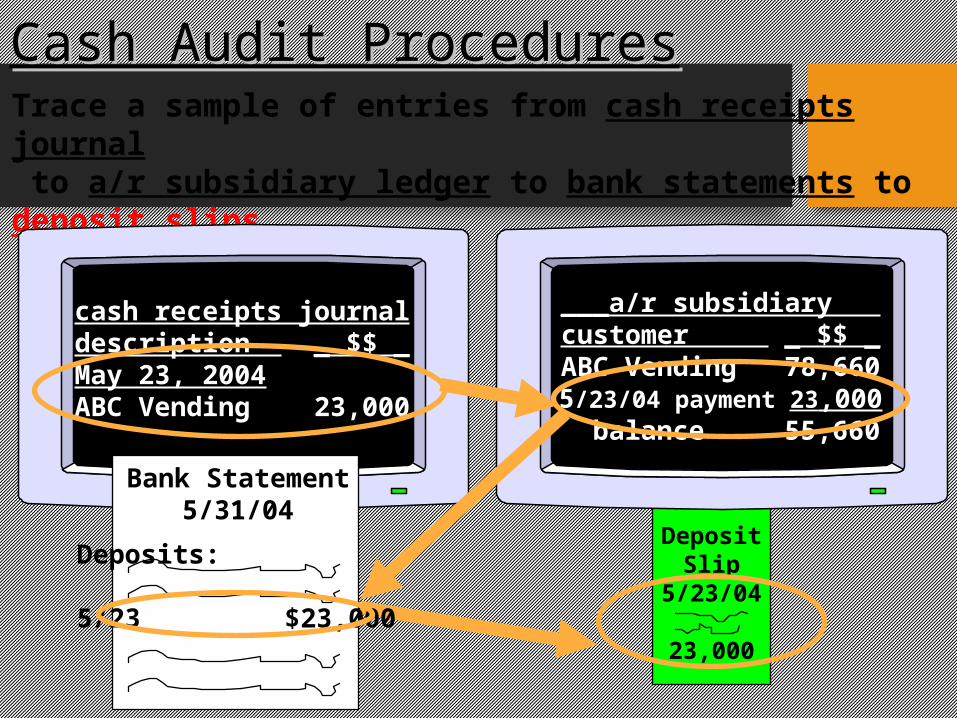

Trace a sample of entries from cash receipts journal to a/r subsidiary ledger to bank statements to deposit slips.

cash receipts journaldescription _ $$ _May 23, 2004ABC Vending 23,000

Bank Statement5/31/04

Deposits:

5/23 $23,000

Cash Audit ProceduresCash Audit Procedures

DepositSlip

5/23/04

23,000

___a/r subsidiary customer _ $$ _ABC Vending 78,6605/23/04 payment 23,000 balance 55,660

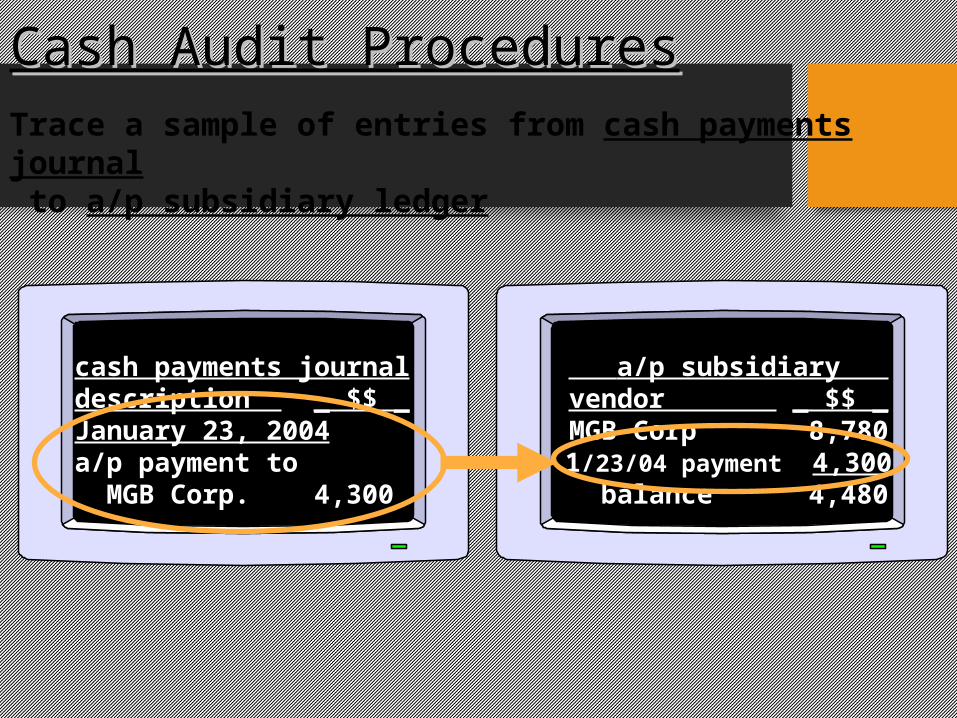

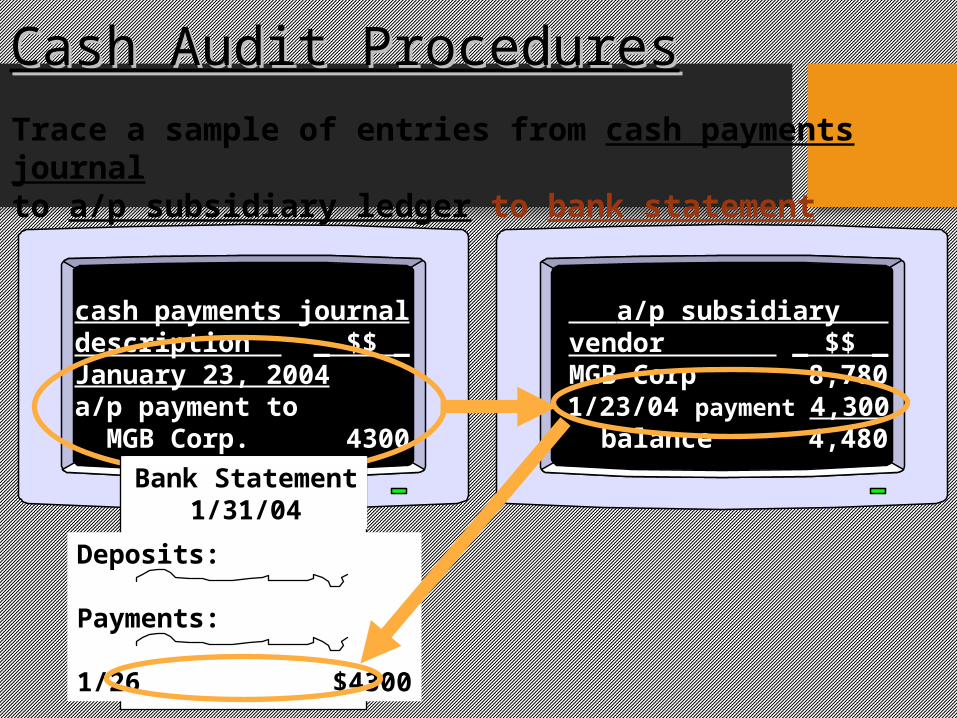

Trace a sample of entries from cash payments journal to a/p subsidiary ledger

Cash Audit ProceduresCash Audit Procedures

cash payments journaldescription _ $$ _January 23, 2004a/p payment to MGB Corp. 4,300

a/p subsidiary vendor _ $$ _MGB Corp 8,7801/23/04 payment 4,300 balance 4,480

Trace a sample of entries from cash payments journal to a/p subsidiary ledger to bank statement

cash payments journaldescription _ $$ _January 23, 2004a/p payment to MGB Corp. 4300

Bank Statement1/31/04

Deposits:

Payments:

1/26 $4300

Cash Audit ProceduresCash Audit Procedures

a/p subsidiary vendor _ $$ _MGB Corp 8,7801/23/04 payment 4,300 balance 4,480

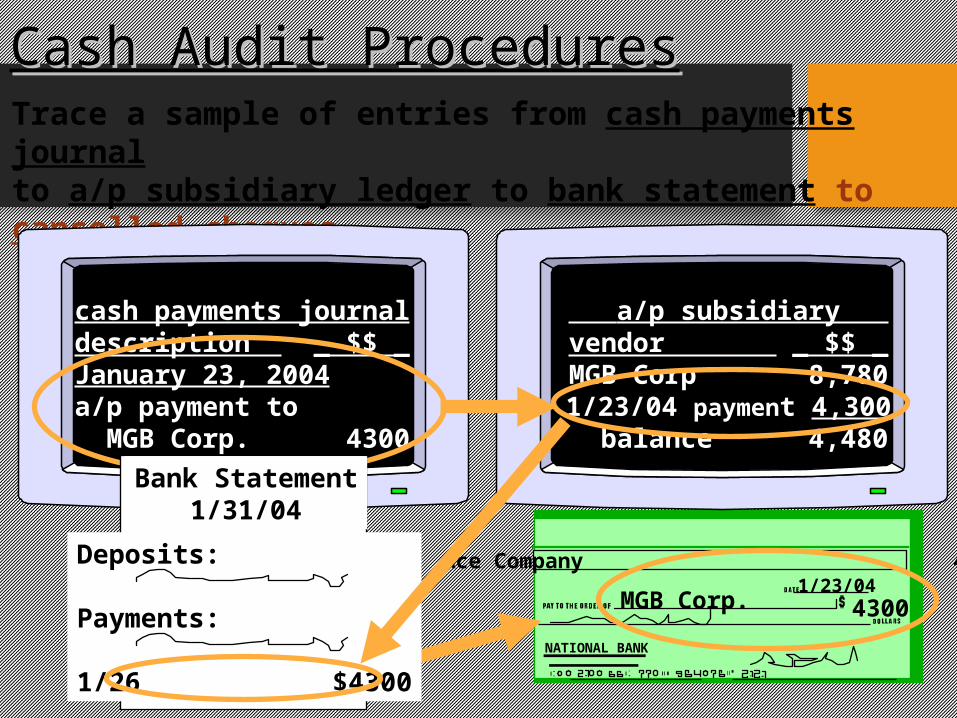

Trace a sample of entries from cash payments journal to a/p subsidiary ledger to bank statement to cancelled cheques.

cash payments journaldescription _ $$ _January 23, 2004a/p payment to MGB Corp. 4300

Bank Statement1/31/04

Deposits:

Payments:

1/26 $4300

Cash Audit ProceduresCash Audit Procedures

Ace Company 4512

MGB Corp.1/23/04

4300

a/p subsidiary vendor _ $$ _MGB Corp 8,7801/23/04 payment 4,300 balance 4,480

NATIONAL BANK

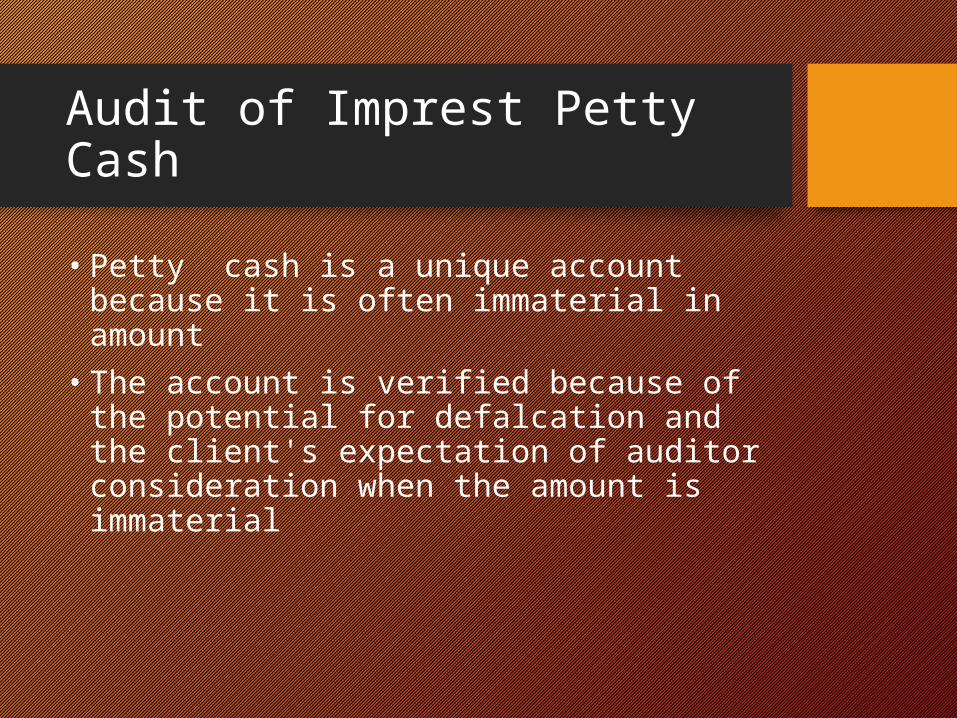

Audit of Imprest Petty Cash

• Petty cash is a unique account because it is often immaterial in amount

• The account is verified because of the potential for defalcation and the client's expectation of auditor consideration when the amount is immaterial

Audit of Imprest Petty Cash

• Internal control over petty cash• Audit tests for petty cash

Internal Control over Petty Cash

• The use of an impress fund that is the responsible of one individual

• Petty cash funds should be kept separate from all other activities

• There should be limits on the amount of any expenditure from petty cash funds

• The type of expenditure that can be made from petty cash transactions should be well defined by company policy

Internal Control over Petty Cash

• When a disbursement is made from petty cash, then require a responsible official's approval on a pre-numbered petty cash form

• The total of the actual cash and checks in the fund plus the total unreimbursed petty cash forms should equal the total amount of the petty cash fund stated in the general ledger

• Periodically, surprise counts and a reconciliation of the petty cash fund should be made by the internal auditor or other responsible official

• When the petty cash balance runs low, a check payable to the petty cash custodian should be written on the general cash account for the reimbursement of petty cash

• The check should be for exact amount of the pre-numbered vouchers that are submitted as evidence of actual expenditures

• These vouchers should be verified by the account payable clerk and cancelled to prevent their reuse

Audit Tests for Petty Cash

• Determine the client's procedures for handling the fund by discussing internal controls with the custodian and examining the documentation of a few transactions

• Obtaining an understanding of internal control, identify internal controls and weaknesses

• It is often desirable use a flowchart and an internal control questionnaire, primarily for documentation in subsequent audits

• The common procedures are to count the petty cash balance and to carry detailed tests of one or two reimbursement transactions

• The primary procedures should include footing the petty cash vouchers supporting the amount of the reimbursement, accounting for a sequence of petty cash vouchers, examining the petty cash vouchers for authorization and cancellation, and examining the attached documentation for reasonableness

• Typical supporting documentation includes cash register tapes, invoices, and receipts

• Petty cash tests can ordinarily be performed at any time during the year

• If the balance in the petty cash fund is considered material, it should be counted at the end of the year

• Unreimbursed expenditures should be examined as a part of the count to determine whether the amount of unrecorded expenses is material