Embed Size (px)

Citation preview

Shaw and Partners

0.94500 0000 000

AMS – Equity Report current as at –30/04/2021–Pg. 1

Atomos Ltd (AMS) Rating: Buy | Risk: High | Price Target: $1.53

Capturing 8K performance at 1080p prices

James Bisinella | Analyst

+61 3 9268 1123 [email protected]

Jonathon Higgins | Analyst

+61 3 9268 1182 [email protected]

Event We initiate on Atomos (ASX: AMS) with a Buy Recommendation and Price Target of $1.53 per share (61.9% upside).

Highlights • Market leading products addressing hypergrowth trends – Atomos designs,

manufactures and distributes market leading monitor-recorders globally. These products RRP from US$299 to US$6,499 with gross margins of ~45%. Atomos gives video professionals a faster, superior quality and more affordable output which is highly sought after in the digital age driven by hypergrowth across streaming (Netflix with >200m subscribers), social media (Instagram and Facebook with 2.8bn and 1.3bn users respectively) and gaming (Twitch with ~10m streamers and growing ~150% MoM).

• Positioned for revenue acceleration in 2H21 – Atomos is entering 2H21 on strong grounds with revenue of $32.8m accelerating MoM in 1H21. A recent company outlook statement pointed to sales momentum continuing into 2H21, which supports our revenue estimate of $39.4m or +20% HoH in 2H21 alongside maiden contributions from software sales, Ninja launches, further ProRes RAW integrations, rising organic website visits (+7.6% MoM in April) and growth in the recently launched Neon range.

• Ninja range extended to 8K and streaming – Yesterday AMS announced the launch of the Ninja V+ (first monitor-recorder with 8K recording), Ninja Stream (livestream across the world without a PC) and H.265 codec for Ninja V (via a US$99 software upgrade from May 2021). These represent high quality and relevant opportunities in growing markets with live product launches slated for May 6th which should shed further light.

• Product expansion opportunities to contribute – Over and above growth in the existing product base, Atomos is planning new product launches over the next 6 - 18 months including new categories (gaming), further ProRes RAW integrations and Series 2 product range releases. Additionally, partnership opportunities with the likes of Disney, Zoom, Netflix, Twitch, Cisco could also provide further upside opportunities.

• Profits to emerge alongside operating leverage – We anticipate material operating leverage as Atomos continues to scale its business after turning EBITDA and cashflow positive in the most recent half. Latest 1H21 results and Shaw estimates include:

▪ Revenue: $32.8m at 1H21, Shaw estimates of $39.4m, $72.2m and $88.5m across 2H21e, FY21e and FY22e respectively. We anticipate strong growth driven by new product launches, core video thematic tailwinds, market leadership and accelerating performance in Entertainment across recently launched Neon products.

▪ Gross profit and margins: $14.7m / 44.9% gross margin at 1H21, Shaw estimates of $17.9m, $32.6m and $40.9m across 2H21e, FY21e and FY22e respectively. We see potential for more favourable GM profile over time including software sales.

▪ EBITDA (post-R&D) and margins: $3.0m at 1H21 at 9.2% EBITDA margin, Shaw estimates of $3.6m, $6.6m and $10.2m across 2H21e, FY21e and FY22e respectively.

• Video the enduring modern communication modality of choice – The importance of video communication emerged pre-Covid and accelerated during the WFH phenomenon. Video has proven more efficacious than traditional print and radio media. Internet-based video is forecast to reach 82% of internet traffic in 2022 (source: Cisco). With users and penetration rising in all Atomos segments (Social, Pro-Video, Entertainment) we see social media, gaming and video streaming continuing to drive adoption.

• Risks – Technological change, competition, supply chain, IP protection, cash burn (net cash ~$23m), international operations and key board/management risk, among others.

Recommendation Atomos offers exposure to a globally relevant, market leader in the monitor-recorder space. With superior design, manufacturing and distribution, we see Atomos continuing to deliver significant revenue growth alongside high gross margins and a scalable business model. Initiate with Buy Recommendation. 299

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 2

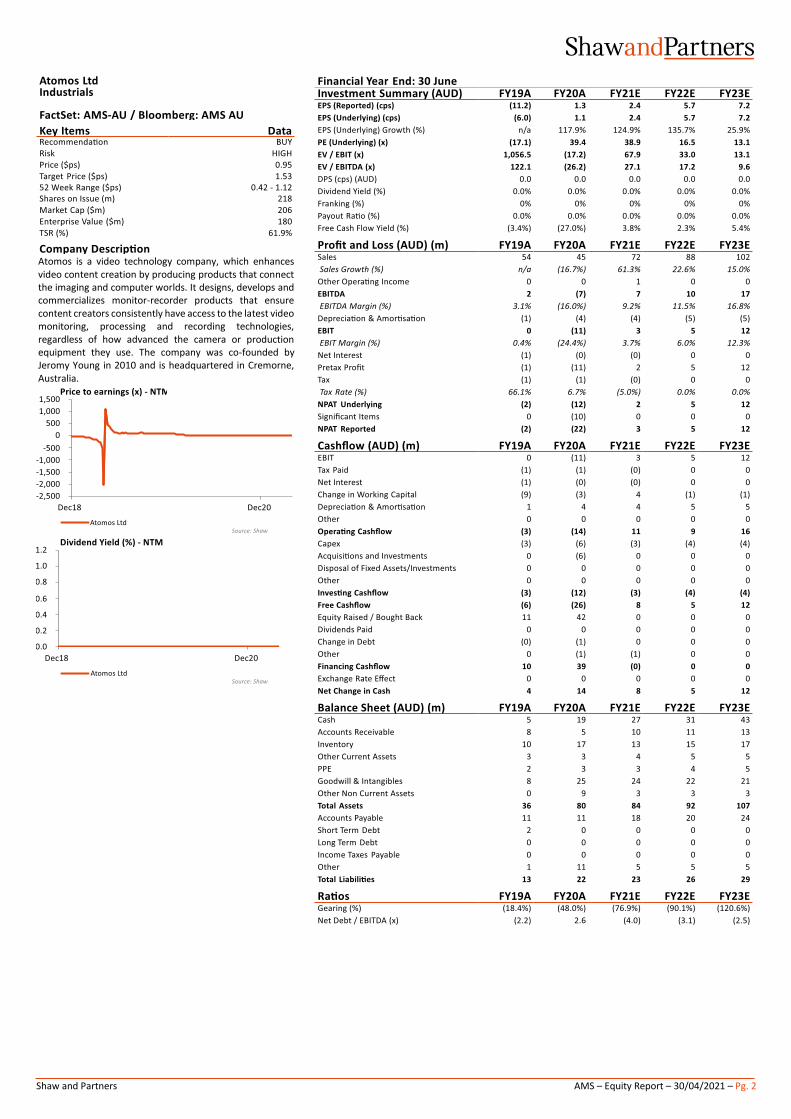

Atomos is a video technology company, which enhances video content creation by producing products that connect the imaging and computer worlds. It designs, develops and commercializes monitor-recorder products that ensure content creators consistently have access to the latest video monitoring, processing and recording technologies, regardless of how advanced the camera or production equipment they use. The company was co-founded by Jeromy Young in 2010 and is headquartered in Cremorne, Australia.

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 3

Contents SECTION 1: BUILDING A GLOBAL VIDEO MOAT ACROSS HARDWARE, SOFTWARE AND NEW PRODUCTS ....4

1.1 Exiting with impressive cadence in month-on-month growth ................................................................. 4

1.2 New product launches, gaming and other adjacencies ............................................................................ 4

1.3 Operating leverage emerging against market leadership......................................................................... 6

1.4 Software potential upside not priced in ................................................................................................... 6

SECTION 2: BUSINESS OVERVIEW .............................................................................................................7

2.1 High level business model and overview .................................................................................................. 7

2.2 Market leading video-monitors ................................................................................................................ 7

2.3 Resellers .................................................................................................................................................. 11

2.4 Website traffic and social media ............................................................................................................. 12

2.5 The Atomos competitive advantage ....................................................................................................... 14

SECTION 3: KEY ASSUMPTIONS AND FINANCIALS ................................................................................... 15

3.1 Revenue segments and regions .............................................................................................................. 16

3.2 Operating performance .......................................................................................................................... 18

3.3 Balance sheet and cashflow .................................................................................................................... 20

SECTION 4: THE BOOMING VIDEO AND CONTENT INDUSTRY .................................................................. 22

4.1 The rise in video content and social media ............................................................................................. 22

4.2 Video game streaming phenomenon ..................................................................................................... 23

SECTION 5: VALUATION ......................................................................................................................... 24

5.1 Target EBITDA multiple (peers’ analysis) ................................................................................................ 24

5.2 Discounted cash flow (DCF) .................................................................................................................... 25

5.3 Valuation conclusion ............................................................................................................................... 26

SECTION 6: SHARE STRUCTURE AND SHAREHOLDERS ............................................................................. 27

SECTION 7: BOARD AND MANAGEMENT ................................................................................................ 28

7.1 Board ....................................................................................................................................................... 28

7.2 Management ........................................................................................................................................... 28

SECTION 8: CORE DRIVERS AND CATALYSTS ............................................................................................ 29

SECTION 9: KEY RISKS ............................................................................................................................ 30

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 4

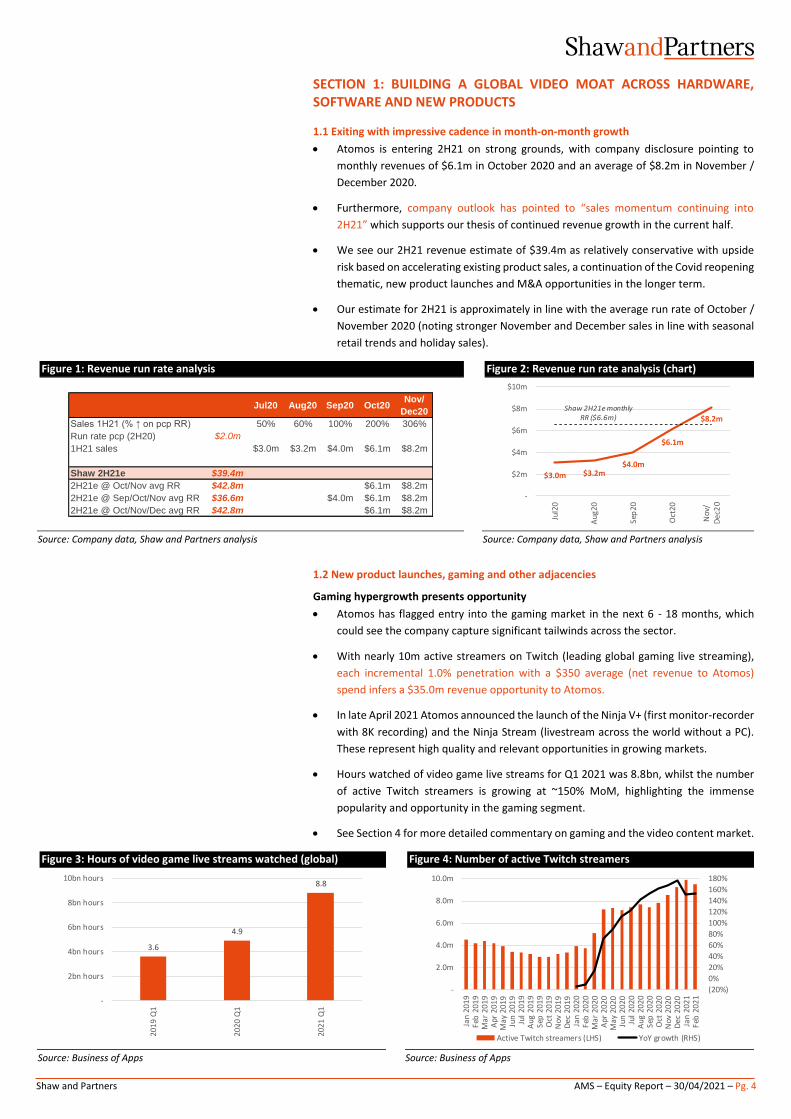

SECTION 1: BUILDING A GLOBAL VIDEO MOAT ACROSS HARDWARE, SOFTWARE AND NEW PRODUCTS

1.1 Exiting with impressive cadence in month-on-month growth

• Atomos is entering 2H21 on strong grounds, with company disclosure pointing to

monthly revenues of $6.1m in October 2020 and an average of $8.2m in November /

December 2020.

• Furthermore, company outlook has pointed to “sales momentum continuing into

2H21” which supports our thesis of continued revenue growth in the current half.

• We see our 2H21 revenue estimate of $39.4m as relatively conservative with upside

risk based on accelerating existing product sales, a continuation of the Covid reopening

thematic, new product launches and M&A opportunities in the longer term.

• Our estimate for 2H21 is approximately in line with the average run rate of October /

November 2020 (noting stronger November and December sales in line with seasonal

retail trends and holiday sales).

Figure 1: Revenue run rate analysis Figure 2: Revenue run rate analysis (chart)

Source: Company data, Shaw and Partners analysis Source: Company data, Shaw and Partners analysis

1.2 New product launches, gaming and other adjacencies

Gaming hypergrowth presents opportunity

• Atomos has flagged entry into the gaming market in the next 6 - 18 months, which

could see the company capture significant tailwinds across the sector.

• With nearly 10m active streamers on Twitch (leading global gaming live streaming),

each incremental 1.0% penetration with a $350 average (net revenue to Atomos)

spend infers a $35.0m revenue opportunity to Atomos.

• In late April 2021 Atomos announced the launch of the Ninja V+ (first monitor-recorder

with 8K recording) and the Ninja Stream (livestream across the world without a PC).

These represent high quality and relevant opportunities in growing markets.

• Hours watched of video game live streams for Q1 2021 was 8.8bn, whilst the number

of active Twitch streamers is growing at ~150% MoM, highlighting the immense

popularity and opportunity in the gaming segment.

• See Section 4 for more detailed commentary on gaming and the video content market.

Figure 3: Hours of video game live streams watched (global) Figure 4: Number of active Twitch streamers

Source: Business of Apps Source: Business of Apps

Jul20 Aug20 Sep20 Oct20Nov/

Dec20

Sales 1H21 (% ↑ on pcp RR) 50% 60% 100% 200% 306%

Run rate pcp (2H20) $2.0m

1H21 sales $3.0m $3.2m $4.0m $6.1m $8.2m

Shaw 2H21e $39.4m

2H21e @ Oct/Nov avg RR $42.8m $6.1m $8.2m

2H21e @ Sep/Oct/Nov avg RR $36.6m $4.0m $6.1m $8.2m

2H21e @ Oct/Nov/Dec avg RR $42.8m $6.1m $8.2m

$3.0m $3.2m$4.0m

$6.1m

$8.2mShaw 2H21e monthly

RR ($6.6m)

-

$2m

$4m

$6m

$8m

$10m

Jul2

0

Au

g20

Sep

20

Oct

20

No

v/D

ec2

0

3.6

4.9

8.8

-

2bn hours

4bn hours

6bn hours

8bn hours

10bn hours

20

19

Q1

20

20

Q1

20

21

Q1

(20%)

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

-

2.0m

4.0m

6.0m

8.0m

10.0m

Jan

20

19

Feb

201

9M

ar 2

01

9A

pr

20

19

May

201

9Ju

n 2

01

9Ju

l 2

01

9A

ug

20

19

Sep

201

9O

ct 2

01

9N

ov

20

19

Dec

201

9Ja

n 2

02

0Fe

b 2

020

Mar

20

20

Ap

r 2

02

0M

ay 2

020

Jun

20

20

Jul

20

20

Au

g 2

02

0Se

p 2

020

Oct

20

20

No

v 2

02

0D

ec 2

020

Jan

20

21

Feb

202

1

Active Twitch streamers (LHS) YoY growth (RHS)

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 5

Apple ProRes RAW integrations

• Apple ProRes RAW refers to a high-performance video capture standard that was first

integrated by Atomos.

• Atomos is integrated with 32 cameras (including Nikon, Canon, Panasonic and several

others) with company guidance pointing to a target of 43 integrations by December

2022.

• Monthly activations have also increased ~450% over the last year, signalling rapid

uptake in popularity and exposure which should continue to see Atomos sales

accelerate in future periods as the activation trajectory continues to rise.

Figure 5: Pro Res RAW integration profile

Source: Company data, Shaw and Partners analysis

Software sales represent a free hit in our view

• As discussed above, the launch of paid software upgrades in February 2021 continues

to present upside risk to revenues and earnings in our view.

• Having launched Ninja V enablement of H.265 video codec via a US$99 software

upgrade at the end of April 2021 and launching May 2021, we expect incremental

revenues to begin contributing from FY22e.

• See Figure 6 for our analysis on potential revenue, noting this is likely being overlooked

by the market in our view and not included in our forecasts.

Neon (Entertainment segment) to contribute

• Atomos soft launched its Neon range in the Entertainment segment in 1H21, which

contributed ~$1.0m of sales for the half across a sector still impacted by Covid.

• Commentary from the company at 1H21 (announced February 2021) suggested that

customer feedback to date has been “very positive” and 2H21 sales are continuing to

underpin acceleration for Neon across the remainder of the half.

• We note that the Neon 17 and Neon 24 are in backorder at digiDirect (Australian

Reseller) and markertek (US Reseller), supporting our thesis of continued strong sales

as flagged by the company.

M&A optionality to contribute

• Having established a market leading business in the monitor-recorder segment,

Atomos has grown predominantly through in-house R&D alongside the acquisition of

Timecode providing access to a patented technology solution.

• In terms of M&A opportunities, the company has flagged that it will consider

acquisitions within the spaces of:

▪ Technology across new and future defining standards.

▪ Complimentary tech.

▪ New complementary markets.

• Having reached positive EBITDA (post-R&D) in 1H21 and Shaw forecasting $10.2m

EBITDA in FY22e, we see the potential for accretive acquisitions in the medium term as

recently flagged by management.

489

833

2,683

-

500

1,000

1,500

2,000

2,500

3,000

1H20 2H20 1H21 2H21e 1H22e 2H22e 1H23e

-

10

20

30

40

50

ProRes Raw enabled cameras (LHS) ProRes Raw mthly activations (RHS)

Mid

po

int

est

ima

te

Mid

po

int

est

ima

te

Co

mp

any

guid

ance

Co

mp

any

guid

ance

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 6

1.3 Operating leverage emerging against market leadership

• Atomos is at an inflection point in which a combination of tailwinds include sales run

rating higher, new product launches imminent, market leadership emerging and new

verticals emerging in hypergrowth segments (i.e. gaming).

• Adjacent to these tailwinds are a well-managed business with prudent management

controlling operating expenses resulting in the emergence of operating leverage.

• Our analysis suggests market leadership for Atomos in the camera-monitor space in a

deep global market which is demonstrating signs of accelerating.

• On this basis, we forecast revenues of $72.2m, $88.5m and $101.7m and EBITDA (post-

R&D) of $6.6m, $10.2m and $17.0m across FY21e - FY23e as operating leverage

emerges.

1.4 Software potential upside not priced in

• In February 2021 Atomos launched the sale of paid software upgrades or plug-in apps,

initially an SDI RAW upgrade for Ninja V, as well H.265 video codec launching May

2021. We expect incremental revenues to begin contributing from FY22e.

• Software sales gives Atomos the ability to generate a new high gross margin earnings

segment, thus providing greater depth to earnings.

• Our view is that this opportunity provides upside potential that isn’t being fully

recognised by the market.

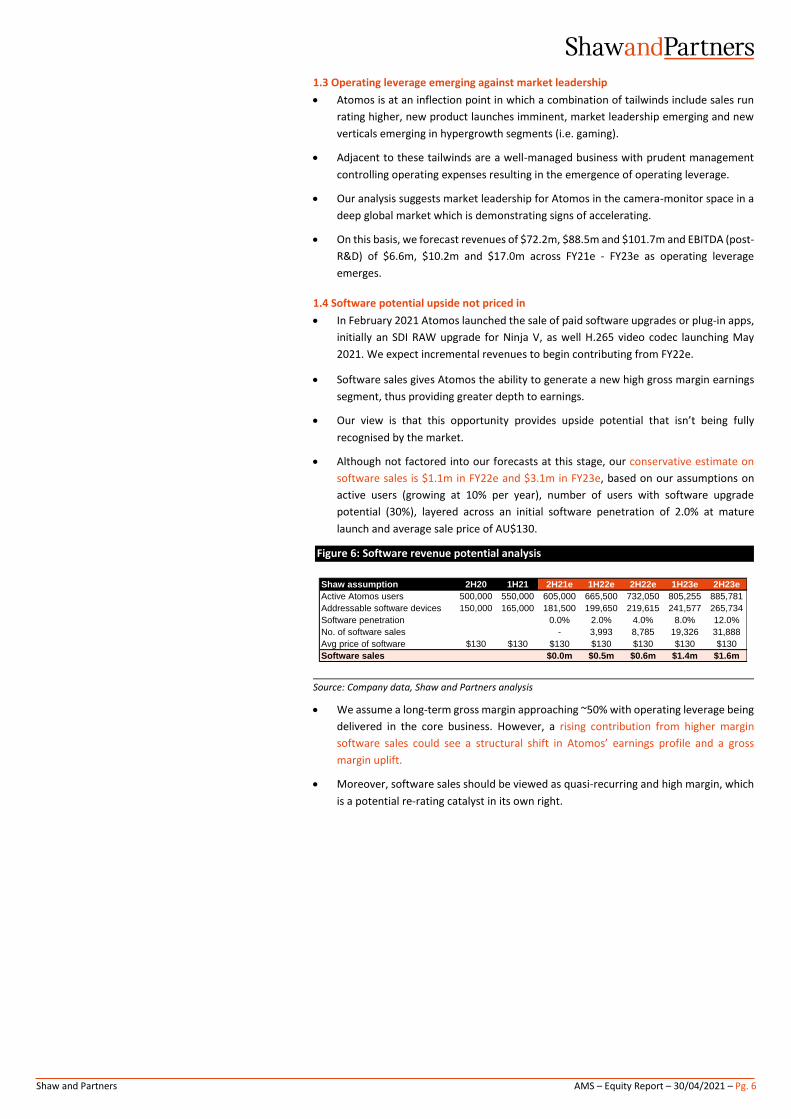

• Although not factored into our forecasts at this stage, our conservative estimate on

software sales is $1.1m in FY22e and $3.1m in FY23e, based on our assumptions on

active users (growing at 10% per year), number of users with software upgrade

potential (30%), layered across an initial software penetration of 2.0% at mature

launch and average sale price of AU$130.

Figure 6: Software revenue potential analysis

Source: Company data, Shaw and Partners analysis

• We assume a long-term gross margin approaching ~50% with operating leverage being

delivered in the core business. However, a rising contribution from higher margin

software sales could see a structural shift in Atomos’ earnings profile and a gross

margin uplift.

• Moreover, software sales should be viewed as quasi-recurring and high margin, which

is a potential re-rating catalyst in its own right.

Shaw assumption 2H20 1H21 2H21e 1H22e 2H22e 1H23e 2H23e

Active Atomos users 500,000 550,000 605,000 665,500 732,050 805,255 885,781

Addressable software devices 150,000 165,000 181,500 199,650 219,615 241,577 265,734

Software penetration 0.0% 2.0% 4.0% 8.0% 12.0%

No. of software sales - 3,993 8,785 19,326 31,888

Avg price of software $130 $130 $130 $130 $130 $130 $130

Software sales $0.0m $0.5m $0.6m $1.4m $1.6m

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 7

SECTION 2: BUSINESS OVERVIEW

2.1 High level business model and overview

• Atomos manufactures and sells market leading video-monitor recorders to enable

creative professionals to easily create and edit high quality content.

• These products give video professionals a faster, higher quality and more affordable

production system through monitors which plug into existing camera units.

• For example, Atomos’ monitor-recorders can potentially result in a $10k camera

producing cinematic quality content usually reserved for ~$100k equipment, for just a

fraction of the cost (i.e. US$6,499 for a Neon 24 in the Entertainment segment).

• Users of Atomos devices include social media, YouTube, TV or cinema content creators.

• Atomos was first to implement the Apple ProRes RAW format and as a result has a

longstanding relationship with Apple.

• Products are distributed via Resellers in 74 countries across all global regions including

Africa, Americas, Asia, Europe and Oceania.

• In 1H21 Atomos delivered record revenue of $32.8m, gross margins of 44.9% and

EBITDA (post R&D) of $3.0m.

• Atomos is based in Melbourne and has 8 offices globally across the USA, Japan, China,

UK and Germany.

2.2 Market leading video-monitors

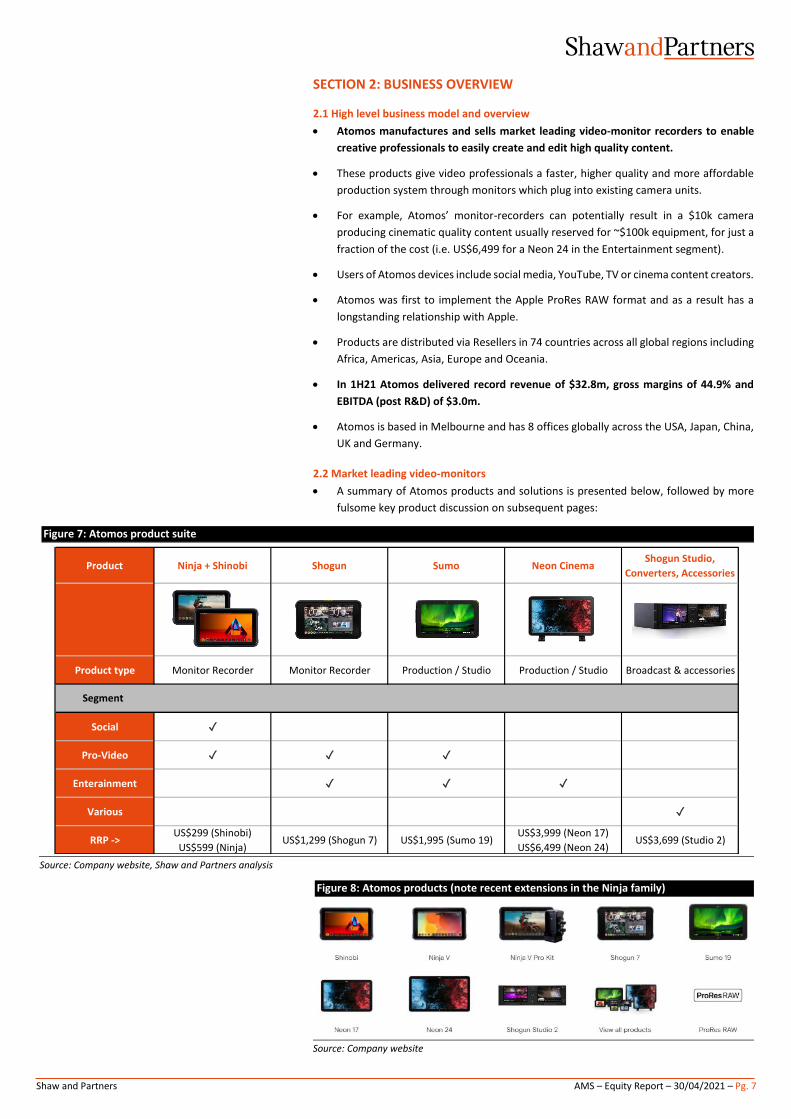

• A summary of Atomos products and solutions is presented below, followed by more

fulsome key product discussion on subsequent pages:

Figure 7: Atomos product suite

Source: Company website, Shaw and Partners analysis

Figure 8: Atomos products (note recent extensions in the Ninja family)

Source: Company website

Product Ninja + Shinobi Shogun Sumo Neon CinemaShogun Studio,

Converters, Accessories

Product type Monitor Recorder Monitor Recorder Production / Studio Production / Studio Broadcast & accessories

Social ✓

Pro-Video ✓ ✓ ✓

Enterainment ✓ ✓ ✓

Various ✓

RRP ->US$299 (Shinobi)

US$599 (Ninja)US$1,299 (Shogun 7) US$1,995 (Sumo 19)

US$3,999 (Neon 17)

US$6,499 (Neon 24)US$3,699 (Studio 2)

Segment

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 8

Ninja V and Shinobi ranges

• Ninja V is a field monitor for content creators looking to capture high quality industry

standard codecs including ProRes RAW.

• The Ninja V allows videos to be uploaded to YouTube, with one use case including for

capturing footage from gaming sessions proving to be increasingly popular.

• Shinobi is Atomos’ first stand-alone small monitor (5”), which features screen

processing technology and professional monitoring tools.

• The Shinobi features a 4K monitor, 1000nit screen and weighs 200g.

• Ninja V / Shinobi price: US$599 / US$299

Figure 9: Ninja V and Shinobi

Source: Company website

Shogun range

• The Shogun takes RAW data directly from a camera’s sensor and preserves the

unprocessed image, giving users freedom to adjust and finesse video in post-

production finishing.

• Applying ProRes compression technology to RAW image data adds an additional layer

of optionality for users as ProRes RAW files are typically smaller than other formats.

This allows users to import, edit and grade faster and more efficiently.

• Shogun 7 price: US$1,299

Figure 10: Shogun 7

Source: Company website

Sumo range

• The Sumo range is a Pro-Video / Entertainment device with a large LCD panel.

• The device processes the output from cameras or games consoles and maps the

footage across a dynamic range in real time. It can be used as a director or client

monitor in the field, or an affordable high-dynamic-range (HDR) studio monitor.

• Sumo 19 price: US$1,995

Figure 11: Sumo 19

Source: Company website

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 9

Neon Cinema range

• The Neon Cinema device is a precision on-set and in-studio 4K HDR production monitor

that is capable of recording and playback.

• The device comes in 17”and 24” sizes, with pricing commensurately increasing with

size.

• Via the Neon Cinema, recordings can be played back and reviewed without needing to

off-load media or take the camera out of record mode.

• Neon 17 / 24 price: US$3,999 / US$6,499

Figure 12: Atomos Neon 17

Source: Company website

Shogun Studio, converters and accessories

• The Shogun Studio is a multi-channel device that enables the use of touch screens for

4K/HD recording, monitoring, editing and playback.

• The Shogun Studio is suitable for high-end production including live events, outside

broadcast vehicles, production galleries, master control rooms or post-production

facilities.

• In addition to core devices, Atomos offers a range of accessories to enhance video

production including syncing multiple devices, extending battery life, improving

visibility, calibration systems and cables to connect Atomos recorders or monitors to

computers.

• Shogun Studio 2 price: US$3,699

Figure 13: Shogun Studio and accessories

Source: Company website

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 10

Apple ProRes RAW

• Apple ProRes RAW is a Codec which more specifically allows users to import and edit

RAW data straight from a camera sensor. A “recording format” or “Codec” refers to

the way in which a video is captured and recorded by a camera device.

• ProRes RAW is a new standard in video capture which gives content creators increased

flexibility when adjusting images for factors such as brightness and shadow detail.

• ProRes RAW is supported by HDMI (high-definition multimedia interface) and serial

digital interface (SDI) cameras.

▪ HDMI is a typically used in consumer or prosumer environment, whilst SDI is a

professional video signal preferred in production environments.

• Footage is compressed and sped up (whilst maintaining quality), whilst being fully

supported in a range of applications including Final Cut Pro, Adobe Premiere Pro and

Avid Media Composer.

Figure 14: ProRes RAW manufacturer ecosystem

Source: Company website

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 11

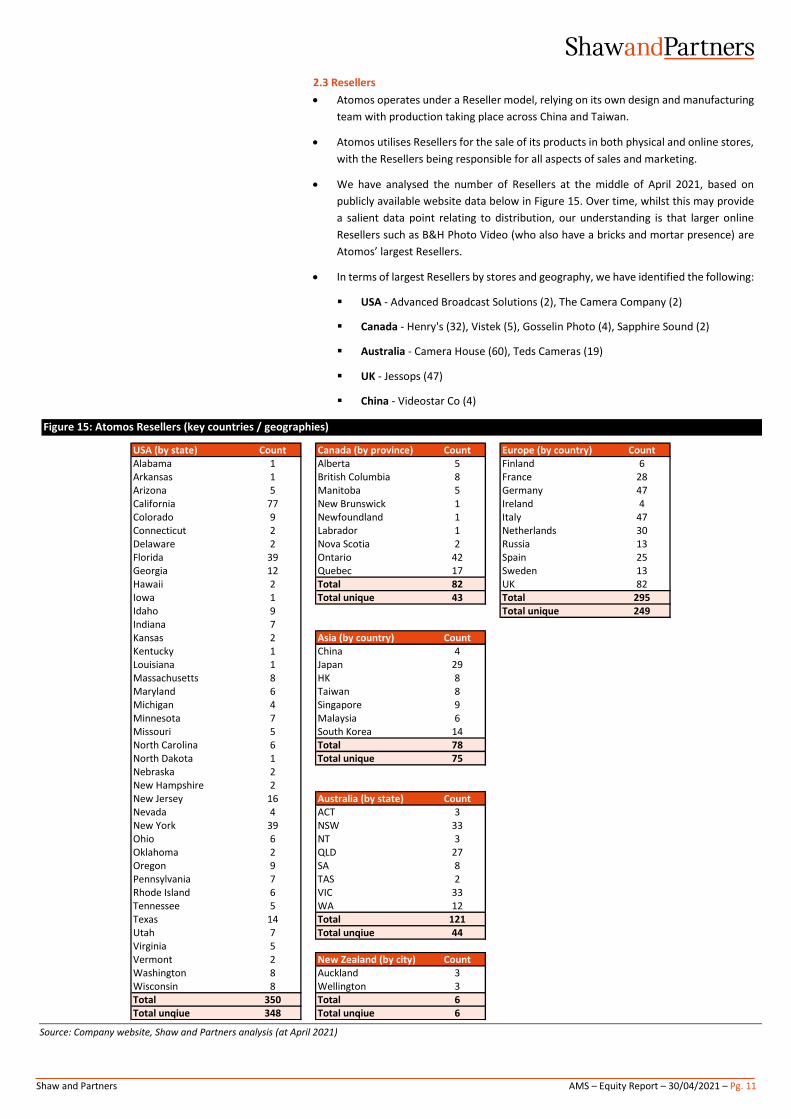

2.3 Resellers

• Atomos operates under a Reseller model, relying on its own design and manufacturing

team with production taking place across China and Taiwan.

• Atomos utilises Resellers for the sale of its products in both physical and online stores,

with the Resellers being responsible for all aspects of sales and marketing.

• We have analysed the number of Resellers at the middle of April 2021, based on

publicly available website data below in Figure 15. Over time, whilst this may provide

a salient data point relating to distribution, our understanding is that larger online

Resellers such as B&H Photo Video (who also have a bricks and mortar presence) are

Atomos’ largest Resellers.

• In terms of largest Resellers by stores and geography, we have identified the following:

▪ USA - Advanced Broadcast Solutions (2), The Camera Company (2)

▪ Canada - Henry's (32), Vistek (5), Gosselin Photo (4), Sapphire Sound (2)

▪ Australia - Camera House (60), Teds Cameras (19)

▪ UK - Jessops (47)

▪ China - Videostar Co (4)

Figure 15: Atomos Resellers (key countries / geographies)

Source: Company website, Shaw and Partners analysis (at April 2021)

USA (by state) Count Canada (by province) Count Europe (by country) CountAlabama 1 Alberta 5 Finland 6Arkansas 1 British Columbia 8 France 28Arizona 5 Manitoba 5 Germany 47California 77 New Brunswick 1 Ireland 4Colorado 9 Newfoundland 1 Italy 47Connecticut 2 Labrador 1 Netherlands 30Delaware 2 Nova Scotia 2 Russia 13Florida 39 Ontario 42 Spain 25Georgia 12 Quebec 17 Sweden 13Hawaii 2 Total 82 UK 82Iowa 1 Total unique 43 Total 295Idaho 9 Total unique 249Indiana 7Kansas 2 Asia (by country) CountKentucky 1 China 4Louisiana 1 Japan 29Massachusetts 8 HK 8Maryland 6 Taiwan 8Michigan 4 Singapore 9Minnesota 7 Malaysia 6Missouri 5 South Korea 14North Carolina 6 Total 78North Dakota 1 Total unique 75Nebraska 2New Hampshire 2New Jersey 16 Australia (by state) CountNevada 4 ACT 3New York 39 NSW 33Ohio 6 NT 3Oklahoma 2 QLD 27Oregon 9 SA 8Pennsylvania 7 TAS 2Rhode Island 6 VIC 33Tennessee 5 WA 12Texas 14 Total 121Utah 7 Total unqiue 44Virginia 5Vermont 2 New Zealand (by city) CountWashington 8 Auckland 3Wisconsin 8 Wellington 3Total 350 Total 6Total unqiue 348 Total unqiue 6

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 12

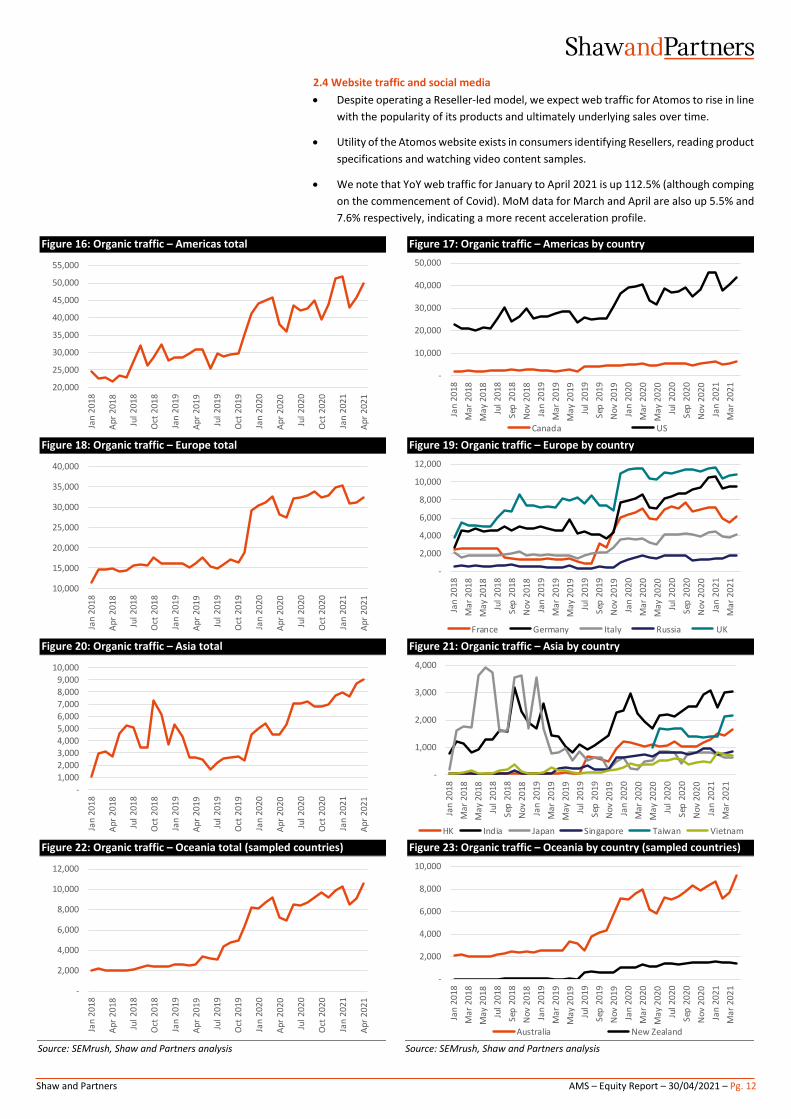

2.4 Website traffic and social media

• Despite operating a Reseller-led model, we expect web traffic for Atomos to rise in line

with the popularity of its products and ultimately underlying sales over time.

• Utility of the Atomos website exists in consumers identifying Resellers, reading product

specifications and watching video content samples.

• We note that YoY web traffic for January to April 2021 is up 112.5% (although comping

on the commencement of Covid). MoM data for March and April are also up 5.5% and

7.6% respectively, indicating a more recent acceleration profile.

Figure 16: Organic traffic – Americas total Figure 17: Organic traffic – Americas by country

Figure 18: Organic traffic – Europe total Figure 19: Organic traffic – Europe by country

Figure 20: Organic traffic – Asia total Figure 21: Organic traffic – Asia by country

Figure 22: Organic traffic – Oceania total (sampled countries) Figure 23: Organic traffic – Oceania by country (sampled countries)

Source: SEMrush, Shaw and Partners analysis Source: SEMrush, Shaw and Partners analysis

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

Jan

20

18

Ap

r 2

01

8

Jul 2

01

8

Oct

20

18

Jan

20

19

Ap

r 2

01

9

Jul 2

01

9

Oct

20

19

Jan

20

20

Ap

r 2

02

0

Jul 2

02

0

Oct

20

20

Jan

20

21

Ap

r 2

02

1

-

10,000

20,000

30,000

40,000

50,000

Jan

20

18

Ma

r 2

01

8

Ma

y 2

01

8

Jul

20

18

Sep

20

18

No

v 2

01

8

Jan

20

19

Ma

r 2

01

9

Ma

y 2

01

9

Jul

20

19

Sep

20

19

No

v 2

01

9

Jan

20

20

Ma

r 2

02

0

Ma

y 2

02

0

Jul

20

20

Sep

20

20

No

v 2

02

0

Jan

20

21

Ma

r 2

02

1

Canada US

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Jan

20

18

Ap

r 2

01

8

Jul 2

01

8

Oct

20

18

Jan

20

19

Ap

r 2

01

9

Jul 2

01

9

Oct

20

19

Jan

20

20

Ap

r 2

02

0

Jul 2

02

0

Oct

20

20

Jan

20

21

Ap

r 2

02

1

-

2,000

4,000

6,000

8,000

10,000

12,000Ja

n 2

01

8

Ma

r 2

01

8

May

20

18

Jul

20

18

Sep

20

18

No

v 2

01

8

Jan

20

19

Ma

r 2

01

9

May

20

19

Jul

20

19

Sep

20

19

No

v 2

01

9

Jan

20

20

Ma

r 2

02

0

Ma

y 2

02

0

Jul

20

20

Sep

20

20

No

v 2

02

0

Jan

20

21

Ma

r 2

02

1

France Germany Italy Russia UK

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Jan

20

18

Ap

r 2

01

8

Jul 2

01

8

Oct

20

18

Jan

20

19

Ap

r 2

01

9

Jul 2

01

9

Oct

20

19

Jan

20

20

Ap

r 2

02

0

Jul 2

02

0

Oct

20

20

Jan

20

21

Ap

r 2

02

1

-

1,000

2,000

3,000

4,000

Jan

20

18

Ma

r 2

01

8

Ma

y 2

01

8

Jul 2

01

8

Sep

20

18

No

v 2

01

8

Jan

20

19

Ma

r 2

01

9

Ma

y 2

01

9

Jul 2

01

9

Sep

20

19

No

v 2

01

9

Jan

20

20

Ma

r 2

02

0

Ma

y 2

02

0

Jul 2

02

0

Sep

20

20

No

v 2

02

0

Jan

20

21

Ma

r 2

02

1

HK India Japan Singapore Taiwan Vietnam

-

2,000

4,000

6,000

8,000

10,000

12,000

Jan

20

18

Ap

r 2

01

8

Jul 2

01

8

Oct

20

18

Jan

20

19

Ap

r 2

01

9

Jul 2

01

9

Oct

20

19

Jan

20

20

Ap

r 2

02

0

Jul 2

02

0

Oct

20

20

Jan

20

21

Ap

r 2

02

1

-

2,000

4,000

6,000

8,000

10,000

Jan

20

18

Ma

r 2

01

8

Ma

y 2

01

8

Jul

20

18

Sep

20

18

No

v 2

01

8

Jan

20

19

Ma

r 2

01

9

Ma

y 2

01

9

Jul

20

19

Sep

20

19

No

v 2

01

9

Jan

20

20

Ma

r 2

02

0

Ma

y 2

02

0

Jul

20

20

Sep

20

20

No

v 2

02

0

Jan

20

21

Ma

r 2

02

1

Australia New Zealand

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 13

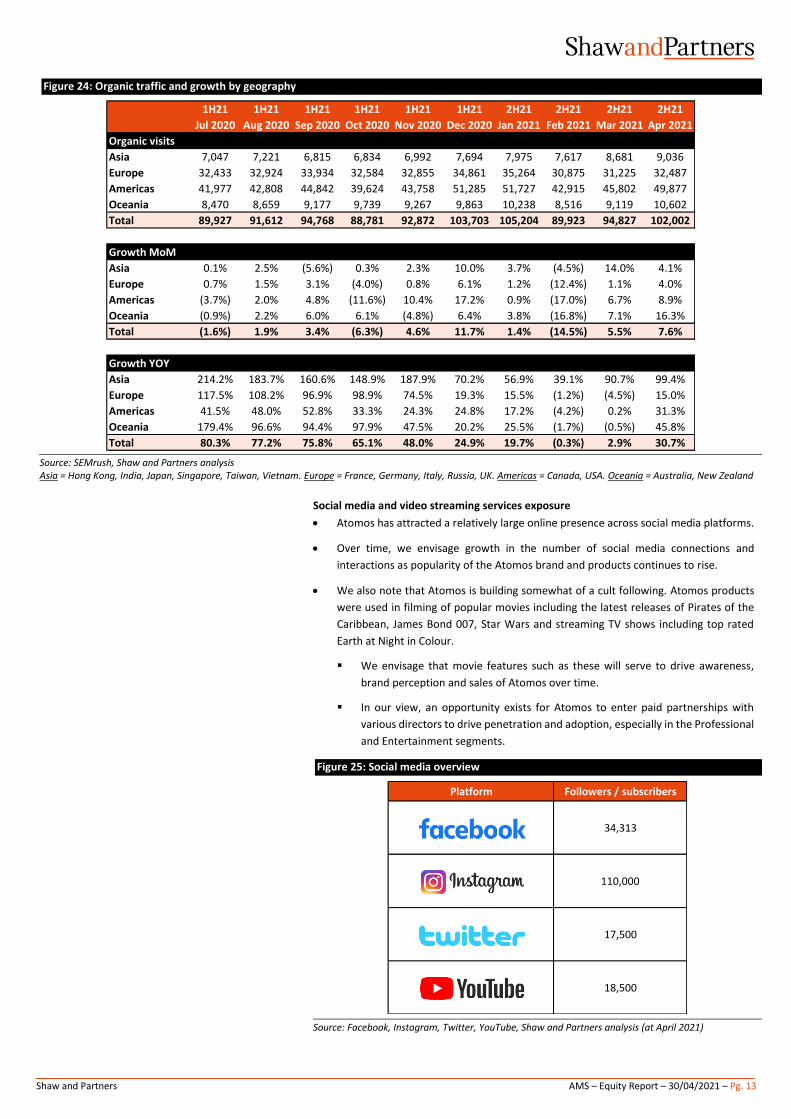

Figure 24: Organic traffic and growth by geography

Source: SEMrush, Shaw and Partners analysis Asia = Hong Kong, India, Japan, Singapore, Taiwan, Vietnam. Europe = France, Germany, Italy, Russia, UK. Americas = Canada, USA. Oceania = Australia, New Zealand

Social media and video streaming services exposure

• Atomos has attracted a relatively large online presence across social media platforms.

• Over time, we envisage growth in the number of social media connections and

interactions as popularity of the Atomos brand and products continues to rise.

• We also note that Atomos is building somewhat of a cult following. Atomos products

were used in filming of popular movies including the latest releases of Pirates of the

Caribbean, James Bond 007, Star Wars and streaming TV shows including top rated

Earth at Night in Colour.

▪ We envisage that movie features such as these will serve to drive awareness,

brand perception and sales of Atomos over time.

▪ In our view, an opportunity exists for Atomos to enter paid partnerships with

various directors to drive penetration and adoption, especially in the Professional

and Entertainment segments.

Figure 25: Social media overview

Source: Facebook, Instagram, Twitter, YouTube, Shaw and Partners analysis (at April 2021)

1H21 1H21 1H21 1H21 1H21 1H21 2H21 2H21 2H21 2H21

Jul 2020 Aug 2020 Sep 2020 Oct 2020 Nov 2020 Dec 2020 Jan 2021 Feb 2021 Mar 2021 Apr 2021

Organic visits

Asia 7,047 7,221 6,815 6,834 6,992 7,694 7,975 7,617 8,681 9,036

Europe 32,433 32,924 33,934 32,584 32,855 34,861 35,264 30,875 31,225 32,487

Americas 41,977 42,808 44,842 39,624 43,758 51,285 51,727 42,915 45,802 49,877

Oceania 8,470 8,659 9,177 9,739 9,267 9,863 10,238 8,516 9,119 10,602

Total 89,927 91,612 94,768 88,781 92,872 103,703 105,204 89,923 94,827 102,002

Growth MoM

Asia 0.1% 2.5% (5.6%) 0.3% 2.3% 10.0% 3.7% (4.5%) 14.0% 4.1%

Europe 0.7% 1.5% 3.1% (4.0%) 0.8% 6.1% 1.2% (12.4%) 1.1% 4.0%

Americas (3.7%) 2.0% 4.8% (11.6%) 10.4% 17.2% 0.9% (17.0%) 6.7% 8.9%

Oceania (0.9%) 2.2% 6.0% 6.1% (4.8%) 6.4% 3.8% (16.8%) 7.1% 16.3%

Total (1.6%) 1.9% 3.4% (6.3%) 4.6% 11.7% 1.4% (14.5%) 5.5% 7.6%

Growth YOY

Asia 214.2% 183.7% 160.6% 148.9% 187.9% 70.2% 56.9% 39.1% 90.7% 99.4%

Europe 117.5% 108.2% 96.9% 98.9% 74.5% 19.3% 15.5% (1.2%) (4.5%) 15.0%

Americas 41.5% 48.0% 52.8% 33.3% 24.3% 24.8% 17.2% (4.2%) 0.2% 31.3%

Oceania 179.4% 96.6% 94.4% 97.9% 47.5% 20.2% 25.5% (1.7%) (0.5%) 45.8%

Total 80.3% 77.2% 75.8% 65.1% 48.0% 24.9% 19.7% (0.3%) 2.9% 30.7%

Platform Followers / subscribers

34,313

110,000

17,500

18,500

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 14

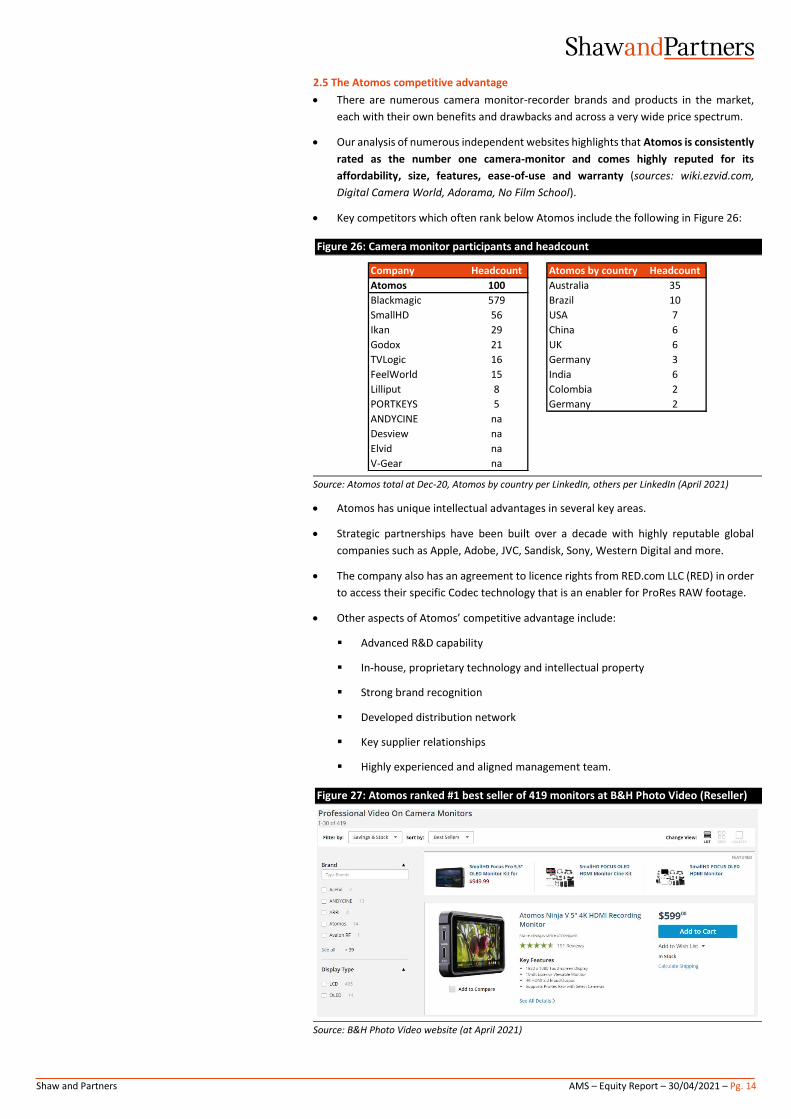

2.5 The Atomos competitive advantage

• There are numerous camera monitor-recorder brands and products in the market,

each with their own benefits and drawbacks and across a very wide price spectrum.

• Our analysis of numerous independent websites highlights that Atomos is consistently

rated as the number one camera-monitor and comes highly reputed for its

affordability, size, features, ease-of-use and warranty (sources: wiki.ezvid.com,

Digital Camera World, Adorama, No Film School).

• Key competitors which often rank below Atomos include the following in Figure 26:

Figure 26: Camera monitor participants and headcount

Source: Atomos total at Dec-20, Atomos by country per LinkedIn, others per LinkedIn (April 2021)

• Atomos has unique intellectual advantages in several key areas.

• Strategic partnerships have been built over a decade with highly reputable global

companies such as Apple, Adobe, JVC, Sandisk, Sony, Western Digital and more.

• The company also has an agreement to licence rights from RED.com LLC (RED) in order

to access their specific Codec technology that is an enabler for ProRes RAW footage.

• Other aspects of Atomos’ competitive advantage include:

▪ Advanced R&D capability

▪ In-house, proprietary technology and intellectual property

▪ Strong brand recognition

▪ Developed distribution network

▪ Key supplier relationships

▪ Highly experienced and aligned management team.

Figure 27: Atomos ranked #1 best seller of 419 monitors at B&H Photo Video (Reseller)

Source: B&H Photo Video website (at April 2021)

Company Headcount Atomos by country Headcount

Atomos 100 Australia 35

Blackmagic 579 Brazil 10

SmallHD 56 USA 7

Ikan 29 China 6

Godox 21 UK 6

TVLogic 16 Germany 3

FeelWorld 15 India 6

Lilliput 8 Colombia 2

PORTKEYS 5 Germany 2

ANDYCINE na

Desview na

Elvid na

V-Gear na

Shaw and Partners AMS – Equity Report – 30/04/2021 – Pg. 15

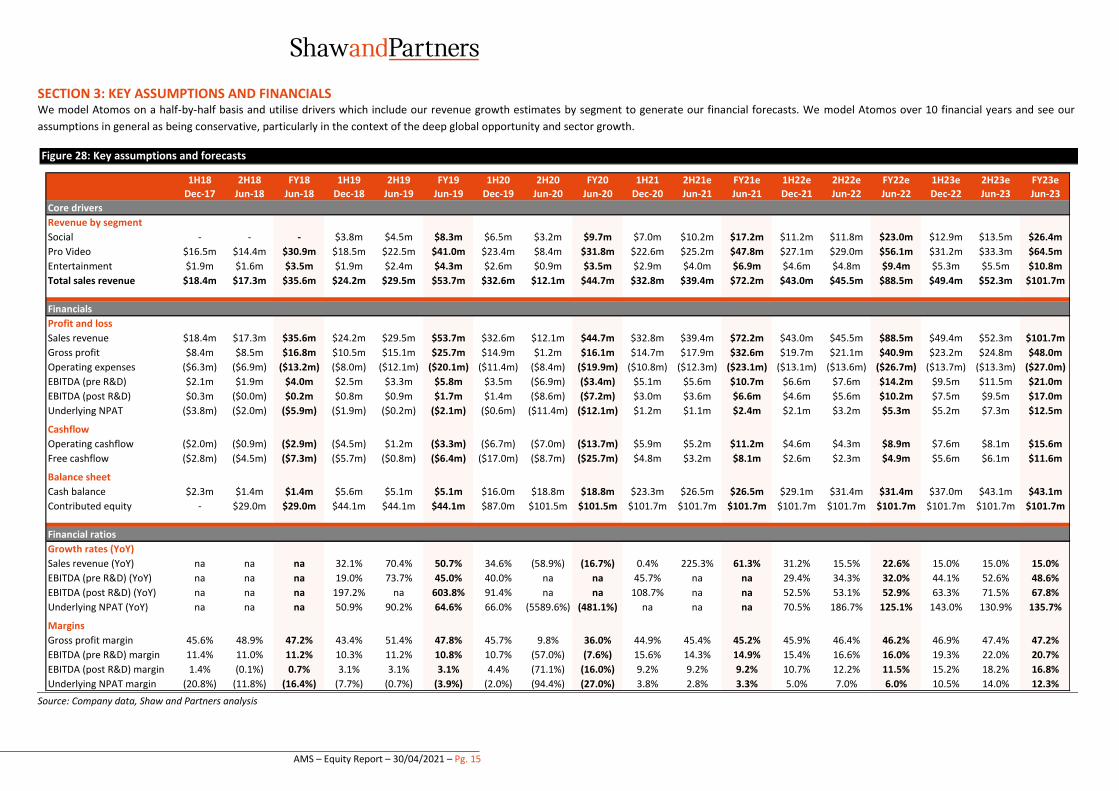

SECTION 3: KEY ASSUMPTIONS AND FINANCIALS We model Atomos on a half-by-half basis and utilise drivers which include our revenue growth estimates by segment to generate our financial forecasts. We model Atomos over 10 financial years and see our

assumptions in general as being conservative, particularly in the context of the deep global opportunity and sector growth.

Figure 28: Key assumptions and forecasts

Source: Company data, Shaw and Partners analysis

1H18 2H18 FY18 1H19 2H19 FY19 1H20 2H20 FY20 1H21 2H21e FY21e 1H22e 2H22e FY22e 1H23e 2H23e FY23e

Dec-17 Jun-18 Jun-18 Dec-18 Jun-19 Jun-19 Dec-19 Jun-20 Jun-20 Dec-20 Jun-21 Jun-21 Dec-21 Jun-22 Jun-22 Dec-22 Jun-23 Jun-23

Core drivers

Revenue by segment

Social - - - $3.8m $4.5m $8.3m $6.5m $3.2m $9.7m $7.0m $10.2m $17.2m $11.2m $11.8m $23.0m $12.9m $13.5m $26.4m

Pro Video $16.5m $14.4m $30.9m $18.5m $22.5m $41.0m $23.4m $8.4m $31.8m $22.6m $25.2m $47.8m $27.1m $29.0m $56.1m $31.2m $33.3m $64.5m

Entertainment $1.9m $1.6m $3.5m $1.9m $2.4m $4.3m $2.6m $0.9m $3.5m $2.9m $4.0m $6.9m $4.6m $4.8m $9.4m $5.3m $5.5m $10.8m

Total sales revenue $18.4m $17.3m $35.6m $24.2m $29.5m $53.7m $32.6m $12.1m $44.7m $32.8m $39.4m $72.2m $43.0m $45.5m $88.5m $49.4m $52.3m $101.7m

Financials

Profit and loss

Sales revenue $18.4m $17.3m $35.6m $24.2m $29.5m $53.7m $32.6m $12.1m $44.7m $32.8m $39.4m $72.2m $43.0m $45.5m $88.5m $49.4m $52.3m $101.7m

Gross profit $8.4m $8.5m $16.8m $10.5m $15.1m $25.7m $14.9m $1.2m $16.1m $14.7m $17.9m $32.6m $19.7m $21.1m $40.9m $23.2m $24.8m $48.0m

Operating expenses ($6.3m) ($6.9m) ($13.2m) ($8.0m) ($12.1m) ($20.1m) ($11.4m) ($8.4m) ($19.9m) ($10.8m) ($12.3m) ($23.1m) ($13.1m) ($13.6m) ($26.7m) ($13.7m) ($13.3m) ($27.0m)

EBITDA (pre R&D) $2.1m $1.9m $4.0m $2.5m $3.3m $5.8m $3.5m ($6.9m) ($3.4m) $5.1m $5.6m $10.7m $6.6m $7.6m $14.2m $9.5m $11.5m $21.0m

EBITDA (post R&D) $0.3m ($0.0m) $0.2m $0.8m $0.9m $1.7m $1.4m ($8.6m) ($7.2m) $3.0m $3.6m $6.6m $4.6m $5.6m $10.2m $7.5m $9.5m $17.0m

Underlying NPAT ($3.8m) ($2.0m) ($5.9m) ($1.9m) ($0.2m) ($2.1m) ($0.6m) ($11.4m) ($12.1m) $1.2m $1.1m $2.4m $2.1m $3.2m $5.3m $5.2m $7.3m $12.5m

Cashflow

Operating cashflow ($2.0m) ($0.9m) ($2.9m) ($4.5m) $1.2m ($3.3m) ($6.7m) ($7.0m) ($13.7m) $5.9m $5.2m $11.2m $4.6m $4.3m $8.9m $7.6m $8.1m $15.6m

Free cashflow ($2.8m) ($4.5m) ($7.3m) ($5.7m) ($0.8m) ($6.4m) ($17.0m) ($8.7m) ($25.7m) $4.8m $3.2m $8.1m $2.6m $2.3m $4.9m $5.6m $6.1m $11.6m

Balance sheet

Cash balance $2.3m $1.4m $1.4m $5.6m $5.1m $5.1m $16.0m $18.8m $18.8m $23.3m $26.5m $26.5m $29.1m $31.4m $31.4m $37.0m $43.1m $43.1m

Contributed equity - $29.0m $29.0m $44.1m $44.1m $44.1m $87.0m $101.5m $101.5m $101.7m $101.7m $101.7m $101.7m $101.7m $101.7m $101.7m $101.7m $101.7m

Financial ratios

Growth rates (YoY)

Sales revenue (YoY) na na na 32.1% 70.4% 50.7% 34.6% (58.9%) (16.7%) 0.4% 225.3% 61.3% 31.2% 15.5% 22.6% 15.0% 15.0% 15.0%

EBITDA (pre R&D) (YoY) na na na 19.0% 73.7% 45.0% 40.0% na na 45.7% na na 29.4% 34.3% 32.0% 44.1% 52.6% 48.6%

EBITDA (post R&D) (YoY) na na na 197.2% na 603.8% 91.4% na na 108.7% na na 52.5% 53.1% 52.9% 63.3% 71.5% 67.8%

Underlying NPAT (YoY) na na na 50.9% 90.2% 64.6% 66.0% (5589.6%) (481.1%) na na na 70.5% 186.7% 125.1% 143.0% 130.9% 135.7%

Margins

Gross profit margin 45.6% 48.9% 47.2% 43.4% 51.4% 47.8% 45.7% 9.8% 36.0% 44.9% 45.4% 45.2% 45.9% 46.4% 46.2% 46.9% 47.4% 47.2%

EBITDA (pre R&D) margin 11.4% 11.0% 11.2% 10.3% 11.2% 10.8% 10.7% (57.0%) (7.6%) 15.6% 14.3% 14.9% 15.4% 16.6% 16.0% 19.3% 22.0% 20.7%

EBITDA (post R&D) margin 1.4% (0.1%) 0.7% 3.1% 3.1% 3.1% 4.4% (71.1%) (16.0%) 9.2% 9.2% 9.2% 10.7% 12.2% 11.5% 15.2% 18.2% 16.8%

Underlying NPAT margin (20.8%) (11.8%) (16.4%) (7.7%) (0.7%) (3.9%) (2.0%) (94.4%) (27.0%) 3.8% 2.8% 3.3% 5.0% 7.0% 6.0% 10.5% 14.0% 12.3%

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 16

3.1 Revenue segments and regions

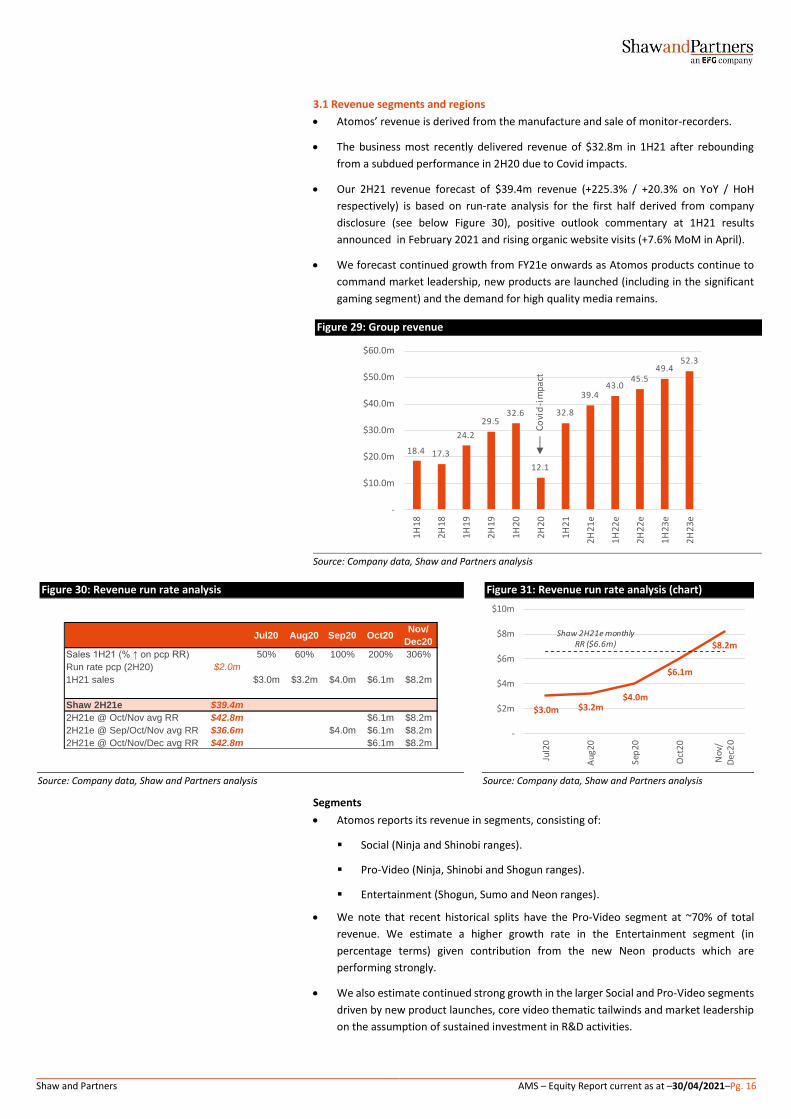

• Atomos’ revenue is derived from the manufacture and sale of monitor-recorders.

• The business most recently delivered revenue of $32.8m in 1H21 after rebounding

from a subdued performance in 2H20 due to Covid impacts.

• Our 2H21 revenue forecast of $39.4m revenue (+225.3% / +20.3% on YoY / HoH

respectively) is based on run-rate analysis for the first half derived from company

disclosure (see below Figure 30), positive outlook commentary at 1H21 results

announced in February 2021 and rising organic website visits (+7.6% MoM in April).

• We forecast continued growth from FY21e onwards as Atomos products continue to

command market leadership, new products are launched (including in the significant

gaming segment) and the demand for high quality media remains.

Figure 29: Group revenue

Source: Company data, Shaw and Partners analysis

Figure 30: Revenue run rate analysis Figure 31: Revenue run rate analysis (chart)

Source: Company data, Shaw and Partners analysis Source: Company data, Shaw and Partners analysis

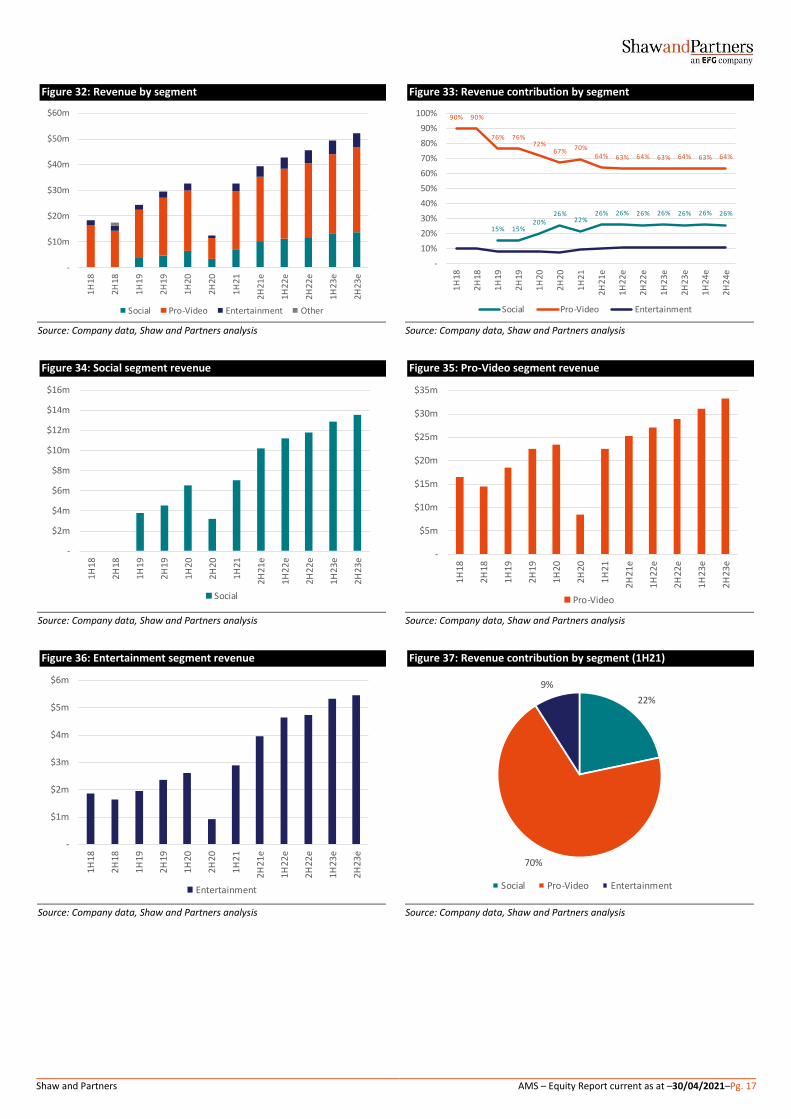

Segments

• Atomos reports its revenue in segments, consisting of:

▪ Social (Ninja and Shinobi ranges).

▪ Pro-Video (Ninja, Shinobi and Shogun ranges).

▪ Entertainment (Shogun, Sumo and Neon ranges).

• We note that recent historical splits have the Pro-Video segment at ~70% of total

revenue. We estimate a higher growth rate in the Entertainment segment (in

percentage terms) given contribution from the new Neon products which are

performing strongly.

• We also estimate continued strong growth in the larger Social and Pro-Video segments

driven by new product launches, core video thematic tailwinds and market leadership

on the assumption of sustained investment in R&D activities.

18.4 17.3

24.2

29.532.6

12.1

32.8

39.443.0

45.549.4

52.3

-

$10.0m

$20.0m

$30.0m

$40.0m

$50.0m

$60.0m

1H18

2H18

1H19

2H19

1H20

2H20

1H21

2H21

e

1H22

e

2H22

e

1H23

e

2H23

e

Covi

d-i

mpa

ct

Jul20 Aug20 Sep20 Oct20Nov/

Dec20

Sales 1H21 (% ↑ on pcp RR) 50% 60% 100% 200% 306%

Run rate pcp (2H20) $2.0m

1H21 sales $3.0m $3.2m $4.0m $6.1m $8.2m

Shaw 2H21e $39.4m

2H21e @ Oct/Nov avg RR $42.8m $6.1m $8.2m

2H21e @ Sep/Oct/Nov avg RR $36.6m $4.0m $6.1m $8.2m

2H21e @ Oct/Nov/Dec avg RR $42.8m $6.1m $8.2m

$3.0m $3.2m$4.0m

$6.1m

$8.2mShaw 2H21e monthly

RR ($6.6m)

-

$2m

$4m

$6m

$8m

$10m

Jul2

0

Au

g20

Sep

20

Oct

20

No

v/D

ec2

0

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 17

Figure 32: Revenue by segment Figure 33: Revenue contribution by segment

Source: Company data, Shaw and Partners analysis Source: Company data, Shaw and Partners analysis

Figure 34: Social segment revenue Figure 35: Pro-Video segment revenue

Source: Company data, Shaw and Partners analysis Source: Company data, Shaw and Partners analysis

Figure 36: Entertainment segment revenue Figure 37: Revenue contribution by segment (1H21)

Source: Company data, Shaw and Partners analysis Source: Company data, Shaw and Partners analysis

-

$10m

$20m

$30m

$40m

$50m

$60m

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Social Pro-Video Entertainment Other

15% 15%20%

26%22%

26% 26% 26% 26% 26% 26% 26%

90% 90%

76% 76%72%

67% 70%64% 63% 64% 63% 64% 63% 64%

-

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

1H

24

e

2H

24

e

Social Pro-Video Entertainment

-

$2m

$4m

$6m

$8m

$10m

$12m

$14m

$16m

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Social

-

$5m

$10m

$15m

$20m

$25m

$30m

$35m

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Pro-Video

-

$1m

$2m

$3m

$4m

$5m

$6m

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Entertainment

22%

70%

9%

Social Pro-Video Entertainment

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 18

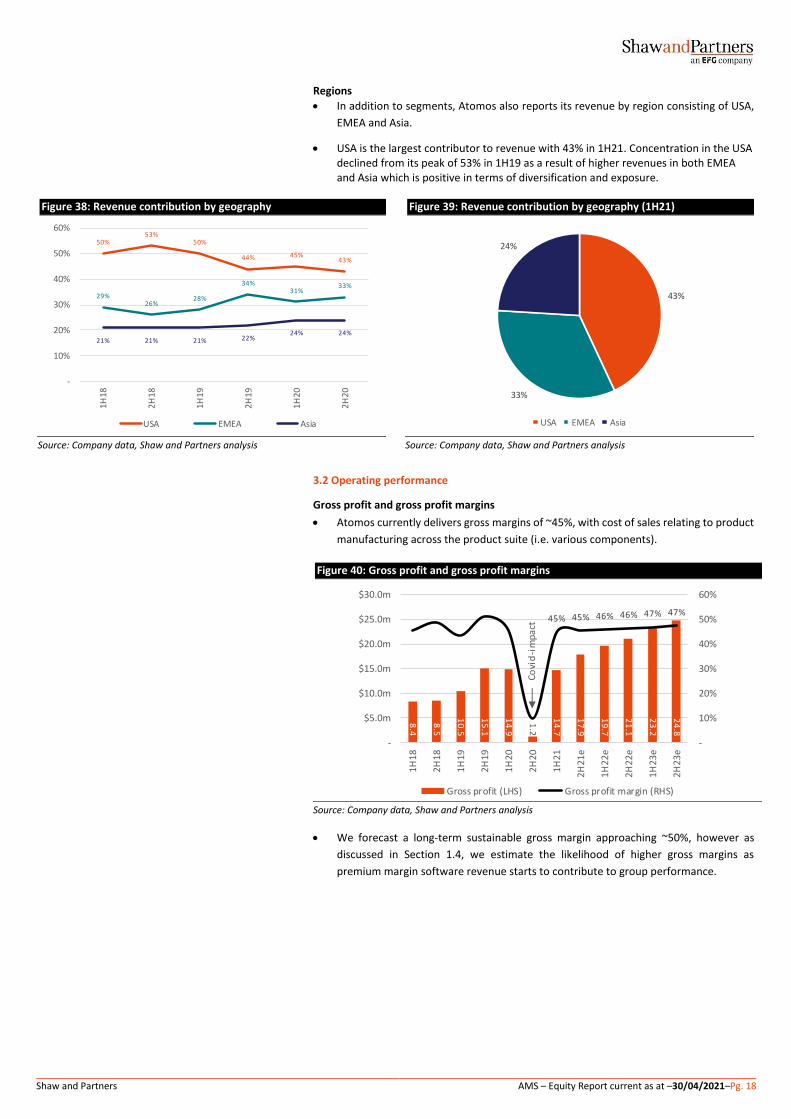

Regions

• In addition to segments, Atomos also reports its revenue by region consisting of USA,

EMEA and Asia.

• USA is the largest contributor to revenue with 43% in 1H21. Concentration in the USA declined from its peak of 53% in 1H19 as a result of higher revenues in both EMEA and Asia which is positive in terms of diversification and exposure.

Figure 38: Revenue contribution by geography Figure 39: Revenue contribution by geography (1H21)

Source: Company data, Shaw and Partners analysis Source: Company data, Shaw and Partners analysis

3.2 Operating performance

Gross profit and gross profit margins

• Atomos currently delivers gross margins of ~45%, with cost of sales relating to product

manufacturing across the product suite (i.e. various components).

Figure 40: Gross profit and gross profit margins

Source: Company data, Shaw and Partners analysis

• We forecast a long-term sustainable gross margin approaching ~50%, however as

discussed in Section 1.4, we estimate the likelihood of higher gross margins as

premium margin software revenue starts to contribute to group performance.

50%53%

50%

44% 45%43%

29%26%

28%

34%31%

33%

21% 21% 21% 22%24% 24%

-

10%

20%

30%

40%

50%

60%

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

USA EMEA Asia

43%

33%

24%

USA EMEA Asia

8.4

8.5

10

.5

15

.1

14

.9

1.2

14

.7

17

.9

19

.7

21

.1

23

.2

24

.8

45% 45% 46% 46% 47% 47%

-

10%

20%

30%

40%

50%

60%

-

$5.0m

$10.0m

$15.0m

$20.0m

$25.0m

$30.0m

1H18

2H18

1H

19

2H19

1H20

2H20

1H21

2H21

e

1H22

e

2H22

e

1H23

e

2H23

e

Gross profit (LHS) Gross profit margin (RHS)

Covi

d-i

mpa

ct

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 19

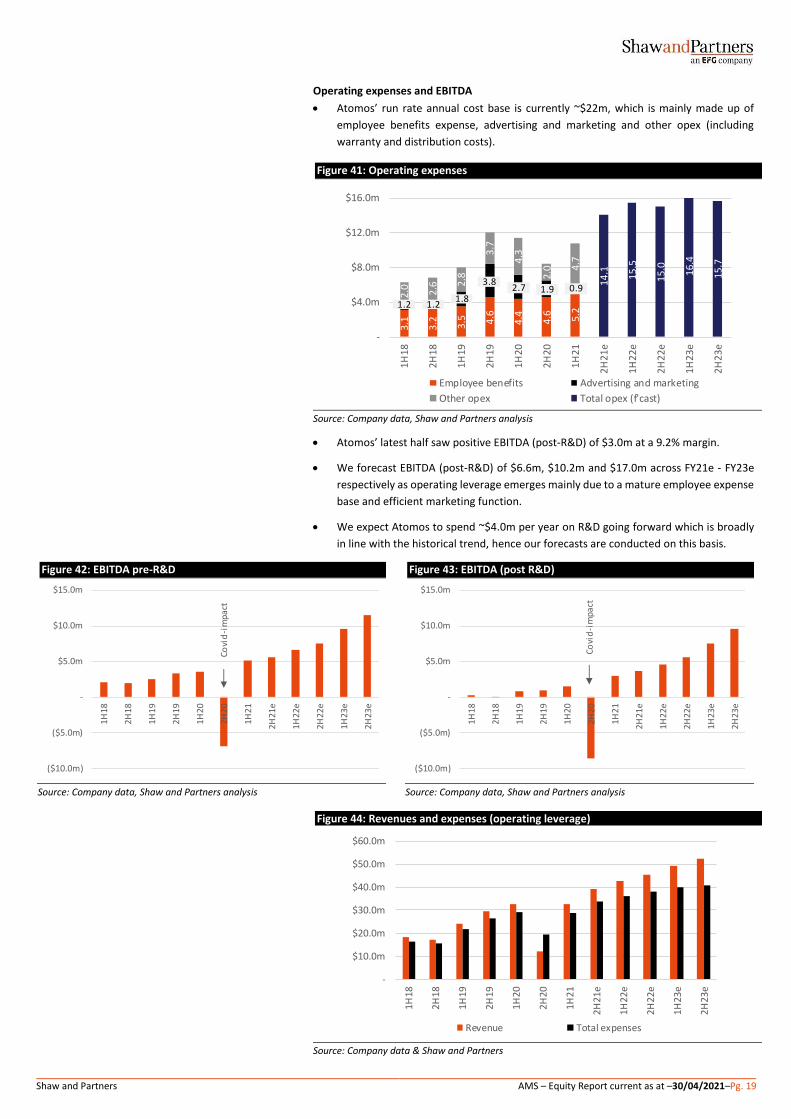

Operating expenses and EBITDA

• Atomos’ run rate annual cost base is currently ~$22m, which is mainly made up of

employee benefits expense, advertising and marketing and other opex (including

warranty and distribution costs).

Figure 41: Operating expenses

Source: Company data, Shaw and Partners analysis

• Atomos’ latest half saw positive EBITDA (post-R&D) of $3.0m at a 9.2% margin.

• We forecast EBITDA (post-R&D) of $6.6m, $10.2m and $17.0m across FY21e - FY23e

respectively as operating leverage emerges mainly due to a mature employee expense

base and efficient marketing function.

• We expect Atomos to spend ~$4.0m per year on R&D going forward which is broadly

in line with the historical trend, hence our forecasts are conducted on this basis.

Figure 42: EBITDA pre-R&D Figure 43: EBITDA (post R&D)

Source: Company data, Shaw and Partners analysis Source: Company data, Shaw and Partners analysis

Figure 44: Revenues and expenses (operating leverage)

Source: Company data & Shaw and Partners

3.1 3.2 3.5 4.6

4.4 4.6 5.2

2.0 2.6 2

.8

3.7

4.3

2.0 4.

7

14

.1 15

.5

15.0 16

.4

15

.7

-

$4.0m

$8.0m

$12.0m

$16.0m

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Employee benefits Advertising and marketing

Other opex Total opex (f'cast)

1.2 1.21.8

3.82.7 1.9 0.9

($10.0m)

($5.0m)

-

$5.0m

$10.0m

$15.0m

1H18

2H18

1H19

2H19

1H20

2H20

1H21

2H21

e

1H22

e

2H22

e

1H23

e

2H23

e

Covi

d-i

mpa

ct

($10.0m)

($5.0m)

-

$5.0m

$10.0m

$15.0m

1H

18

2H18

1H19

2H19

1H20

2H20

1H21

2H21

e

1H22

e

2H22

e

1H23

e

2H

23

e

Co

vid

-im

pa

ct

-

$10.0m

$20.0m

$30.0m

$40.0m

$50.0m

$60.0m

1H18

2H18

1H19

2H19

1H20

2H20

1H21

2H21

e

1H22

e

2H22

e

1H23

e

2H23

e

Revenue Total expenses

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 20

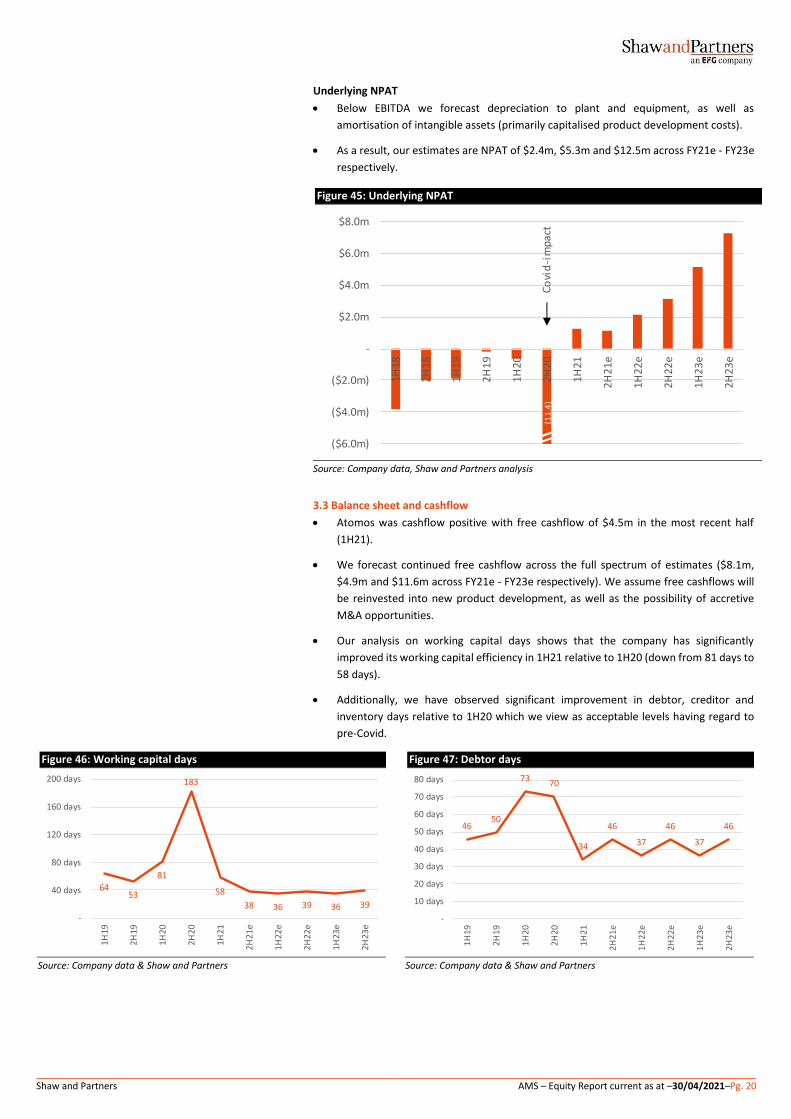

Underlying NPAT

• Below EBITDA we forecast depreciation to plant and equipment, as well as

amortisation of intangible assets (primarily capitalised product development costs).

• As a result, our estimates are NPAT of $2.4m, $5.3m and $12.5m across FY21e - FY23e

respectively.

Figure 45: Underlying NPAT

Source: Company data, Shaw and Partners analysis

3.3 Balance sheet and cashflow

• Atomos was cashflow positive with free cashflow of $4.5m in the most recent half

(1H21).

• We forecast continued free cashflow across the full spectrum of estimates ($8.1m,

$4.9m and $11.6m across FY21e - FY23e respectively). We assume free cashflows will

be reinvested into new product development, as well as the possibility of accretive

M&A opportunities.

• Our analysis on working capital days shows that the company has significantly

improved its working capital efficiency in 1H21 relative to 1H20 (down from 81 days to

58 days).

• Additionally, we have observed significant improvement in debtor, creditor and

inventory days relative to 1H20 which we view as acceptable levels having regard to

pre-Covid.

Figure 46: Working capital days Figure 47: Debtor days

Source: Company data & Shaw and Partners Source: Company data & Shaw and Partners

(11

.4)

($6.0m)

($4.0m)

($2.0m)

-

$2.0m

$4.0m

$6.0m

$8.0m

1H18

2H18

1H19

2H19

1H20

2H20

1H21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Covi

d-i

mpa

ct

6453

81

183

58

38 36 39 36 39

-

40 days

80 days

120 days

160 days

200 days

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

4650

7370

34

46

37

46

37

46

-

10 days

20 days

30 days

40 days

50 days

60 days

70 days

80 days

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 21

Figure 48: Creditor days Figure 49: Inventory days

Source: Company data & Shaw and Partners Source: Company data & Shaw and Partners

• At December 2020, Atomos had $23.3m cash on hand. If the business continues to

operate in line with our expectations, we do not envisage the company requiring any

additional capital.

• We note that if Atomos intends to accelerate growth via inorganic opportunities as

flagged in their latest set of results, we could see the requirement for an additional

capital injection for M&A related costs.

• In terms of M&A opportunities, the company has flagged that it will consider

acquisitions across:

▪ Technology across new and future defining standards.

▪ Complimentary tech

▪ New complementary markets.

Figure 50: Free cashflow Figure 51: Cash balance

Source: Company data & Shaw and Partners Source: Company data & Shaw and Partners

5155

82

4439

53

43

55

45

59

-

20 days

40 days

60 days

80 days

100 days

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

147122

153

281

153

109

154

111

157

113

-

50 days

100 days

150 days

200 days

250 days

300 days

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

(17

.0)

($10.0m)

($8.0m)

($6.0m)

($4.0m)

($2.0m)

-

$2.0m

$4.0m

$6.0m

$8.0m

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

-

$5.0m

$10.0m

$15.0m

$20.0m

$25.0m

$30.0m

$35.0m

$40.0m

$45.0m

1H

18

2H

18

1H

19

2H

19

1H

20

2H

20

1H

21

2H

21

e

1H

22

e

2H

22

e

1H

23

e

2H

23

e

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 22

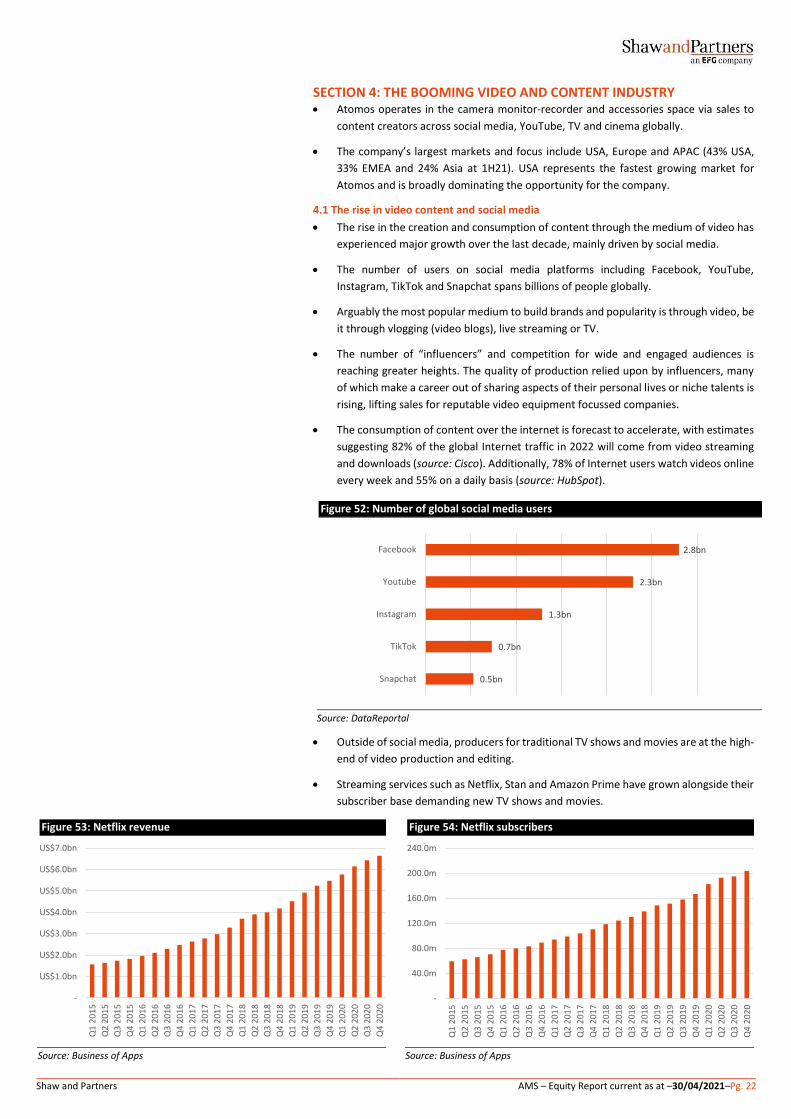

SECTION 4: THE BOOMING VIDEO AND CONTENT INDUSTRY • Atomos operates in the camera monitor-recorder and accessories space via sales to

content creators across social media, YouTube, TV and cinema globally.

• The company’s largest markets and focus include USA, Europe and APAC (43% USA,

33% EMEA and 24% Asia at 1H21). USA represents the fastest growing market for

Atomos and is broadly dominating the opportunity for the company.

4.1 The rise in video content and social media

• The rise in the creation and consumption of content through the medium of video has

experienced major growth over the last decade, mainly driven by social media.

• The number of users on social media platforms including Facebook, YouTube,

Instagram, TikTok and Snapchat spans billions of people globally.

• Arguably the most popular medium to build brands and popularity is through video, be

it through vlogging (video blogs), live streaming or TV.

• The number of “influencers” and competition for wide and engaged audiences is

reaching greater heights. The quality of production relied upon by influencers, many

of which make a career out of sharing aspects of their personal lives or niche talents is

rising, lifting sales for reputable video equipment focussed companies.

• The consumption of content over the internet is forecast to accelerate, with estimates

suggesting 82% of the global Internet traffic in 2022 will come from video streaming

and downloads (source: Cisco). Additionally, 78% of Internet users watch videos online

every week and 55% on a daily basis (source: HubSpot).

Figure 52: Number of global social media users

Source: DataReportal

• Outside of social media, producers for traditional TV shows and movies are at the high-

end of video production and editing.

• Streaming services such as Netflix, Stan and Amazon Prime have grown alongside their

subscriber base demanding new TV shows and movies.

Figure 53: Netflix revenue Figure 54: Netflix subscribers

Source: Business of Apps Source: Business of Apps

2.8bn

2.3bn

1.3bn

0.7bn

0.5bn

Youtube

TikTok

Snapchat

-

US$1.0bn

US$2.0bn

US$3.0bn

US$4.0bn

US$5.0bn

US$6.0bn

US$7.0bn

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

15

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

16

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

17

Q1

20

18

Q2

20

18

Q3

20

18

Q4

20

18

Q1

20

19

Q2

20

19

Q3

20

19

Q4

20

19

Q1

20

20

Q2

20

20

Q3

20

20

Q4

20

20

-

40.0m

80.0m

120.0m

160.0m

200.0m

240.0m

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

15

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

16

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

17

Q1

20

18

Q2

20

18

Q3

20

18

Q4

20

18

Q1

20

19

Q2

20

19

Q3

20

19

Q4

20

19

Q1

20

20

Q2

20

20

Q3

20

20

Q4

20

20

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 23

4.2 Video game streaming phenomenon

• Video game streaming is a new age, interactive platform for audiences to engage with

popular gaming personalities.

• Since launching in 2011, Twitch (leading global gaming live streaming platform), has

seen a rapid user base expansion.

• Hours watched of video game live streams for Q1 2021 reached 8.8bn, whilst the

number of Twitch streamers is nearing 10m and growing ~150% MoM (source: Business

of Apps).

• With 2.69 billion gamers globally, the number of gamers is expected to rise to 3.07

billion by 2023 (source: Statista). A high proportion of gamers enjoy viewing and

following other people playing their favourite games, underpinning growth in the

consumption of video game live streams.

• Similar to social media platforms, the market for efficiently produced, high quality

content has increased as competition for viewership intensifies and streamers look to

offer a differentiated experience to their audiences.

Figure 55: Hours of video game live streams watched (global) Figure 56: Number of active Twitch streamers

Source: Business of Apps Source: Business of Apps

3.6

4.9

8.8

-

2bn hours

4bn hours

6bn hours

8bn hours

10bn hours

20

19

Q1

20

20

Q1

20

21

Q1

(20%)

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

-

2.0m

4.0m

6.0m

8.0m

10.0m

Jan

20

19

Feb

201

9M

ar 2

01

9A

pr

20

19

May

201

9Ju

n 2

01

9Ju

l 2

01

9A

ug

20

19

Sep

201

9O

ct 2

01

9N

ov

20

19

Dec

201

9Ja

n 2

02

0Fe

b 2

020

Mar

20

20

Ap

r 2

02

0M

ay 2

020

Jun

20

20

Jul

20

20

Au

g 2

02

0Se

p 2

020

Oct

20

20

No

v 2

02

0D

ec 2

020

Jan

20

21

Feb

202

1

Active Twitch streamers (LHS) YoY growth (RHS)

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 24

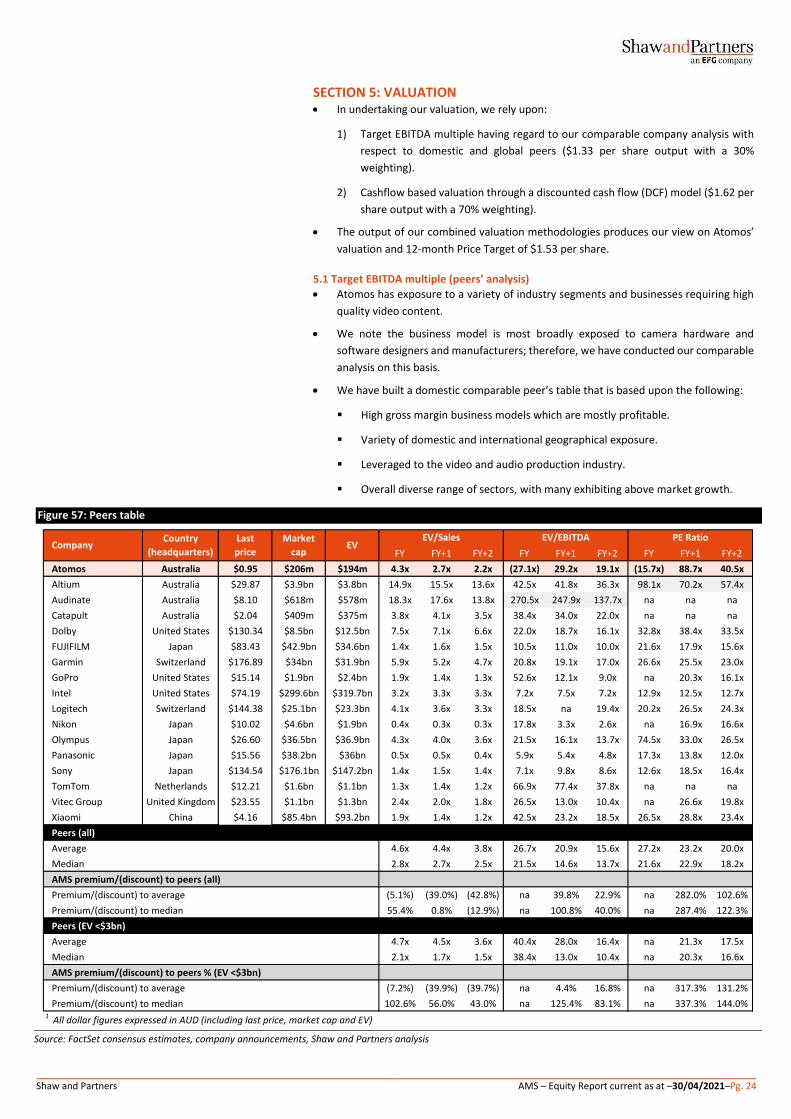

SECTION 5: VALUATION • In undertaking our valuation, we rely upon:

1) Target EBITDA multiple having regard to our comparable company analysis with

respect to domestic and global peers ($1.33 per share output with a 30%

weighting).

2) Cashflow based valuation through a discounted cash flow (DCF) model ($1.62 per

share output with a 70% weighting).

• The output of our combined valuation methodologies produces our view on Atomos’

valuation and 12-month Price Target of $1.53 per share.

5.1 Target EBITDA multiple (peers’ analysis)

• Atomos has exposure to a variety of industry segments and businesses requiring high

quality video content.

• We note the business model is most broadly exposed to camera hardware and

software designers and manufacturers; therefore, we have conducted our comparable

analysis on this basis.

• We have built a domestic comparable peer’s table that is based upon the following:

▪ High gross margin business models which are mostly profitable.

▪ Variety of domestic and international geographical exposure.

▪ Leveraged to the video and audio production industry.

▪ Overall diverse range of sectors, with many exhibiting above market growth.

Figure 57: Peers table

Source: FactSet consensus estimates, company announcements, Shaw and Partners analysis

FY FY+1 FY+2 FY FY+1 FY+2 FY FY+1 FY+2

Atomos Australia $0.95 $206m $194m 4.3x 2.7x 2.2x (27.1x) 29.2x 19.1x (15.7x) 88.7x 40.5x

Altium Australia $29.87 $3.9bn $3.8bn 14.9x 15.5x 13.6x 42.5x 41.8x 36.3x 98.1x 70.2x 57.4x

Audinate Australia $8.10 $618m $578m 18.3x 17.6x 13.8x 270.5x 247.9x 137.7x na na na

Catapult Australia $2.04 $409m $375m 3.8x 4.1x 3.5x 38.4x 34.0x 22.0x na na na

Dolby United States $130.34 $8.5bn $12.5bn 7.5x 7.1x 6.6x 22.0x 18.7x 16.1x 32.8x 38.4x 33.5x

FUJIFILM Japan $83.43 $42.9bn $34.6bn 1.4x 1.6x 1.5x 10.5x 11.0x 10.0x 21.6x 17.9x 15.6x

Garmin Switzerland $176.89 $34bn $31.9bn 5.9x 5.2x 4.7x 20.8x 19.1x 17.0x 26.6x 25.5x 23.0x

GoPro United States $15.14 $1.9bn $2.4bn 1.9x 1.4x 1.3x 52.6x 12.1x 9.0x na 20.3x 16.1x

Intel United States $74.19 $299.6bn $319.7bn 3.2x 3.3x 3.3x 7.2x 7.5x 7.2x 12.9x 12.5x 12.7x

Logitech Switzerland $144.38 $25.1bn $23.3bn 4.1x 3.6x 3.3x 18.5x na 19.4x 20.2x 26.5x 24.3x

Nikon Japan $10.02 $4.6bn $1.9bn 0.4x 0.3x 0.3x 17.8x 3.3x 2.6x na 16.9x 16.6x

Olympus Japan $26.60 $36.5bn $36.9bn 4.3x 4.0x 3.6x 21.5x 16.1x 13.7x 74.5x 33.0x 26.5x

Panasonic Japan $15.56 $38.2bn $36bn 0.5x 0.5x 0.4x 5.9x 5.4x 4.8x 17.3x 13.8x 12.0x

Sony Japan $134.54 $176.1bn $147.2bn 1.4x 1.5x 1.4x 7.1x 9.8x 8.6x 12.6x 18.5x 16.4x

TomTom Netherlands $12.21 $1.6bn $1.1bn 1.3x 1.4x 1.2x 66.9x 77.4x 37.8x na na na

Vitec Group United Kingdom $23.55 $1.1bn $1.3bn 2.4x 2.0x 1.8x 26.5x 13.0x 10.4x na 26.6x 19.8x

Xiaomi China $4.16 $85.4bn $93.2bn 1.9x 1.4x 1.2x 42.5x 23.2x 18.5x 26.5x 28.8x 23.4x

Peers (all)

Average 4.6x 4.4x 3.8x 26.7x 20.9x 15.6x 27.2x 23.2x 20.0x

Median 2.8x 2.7x 2.5x 21.5x 14.6x 13.7x 21.6x 22.9x 18.2x

AMS premium/(discount) to peers (all)

Premium/(discount) to average (5.1%) (39.0%) (42.8%) na 39.8% 22.9% na 282.0% 102.6%

Premium/(discount) to median 55.4% 0.8% (12.9%) na 100.8% 40.0% na 287.4% 122.3%

Peers (EV <$3bn)

Average 4.7x 4.5x 3.6x 40.4x 28.0x 16.4x na 21.3x 17.5x

Median 2.1x 1.7x 1.5x 38.4x 13.0x 10.4x na 20.3x 16.6x

AMS premium/(discount) to peers % (EV <$3bn)

Premium/(discount) to average (7.2%) (39.9%) (39.7%) na 4.4% 16.8% na 317.3% 131.2%

Premium/(discount) to median 102.6% 56.0% 43.0% na 125.4% 83.1% na 337.3% 144.0%1 All dollar figures expressed in AUD (including last price, market cap and EV)

EVPE RatioEV/Sales EV/EBITDA

CompanyCountry

(headquarters)

Last

price

Market

cap

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 25

• In general, we note the following:

▪ Atomos trades at a historical EV/sales multiple of 4.3x, which represents a 5.1%

discount to the peer group’s latest average historical EV/sales multiple of 4.6x.

▪ Atomos trades at a forward EV/sales (2022) multiple of 2.2x, which represents a

42.8% discount to the peer group’s latest average forward EV/sales multiple of

3.8x.

▪ Although slightly loss making at EBITDA in FY20, Atomos trades at a forward

EV/EBITDA (2022) multiple of 19.1x, which represents a 22.9% premium to the

peer group’s latest average forward EV/EBITDA multiple of 15.6x.

• We see Atomos as having an above average organic revenue and earnings growth

profile over our forecast horizon relative to domestic and global listed peers.

• In order to derive the output for Atomos’ valuation of $1.33 per share on a target

EBITDA multiple basis, we applied a conservative EBITDA multiple of 20.0x on FY23e

EBITDA of $21.0m (pre-R&D), discounted at our WACC of 11.0%.

• We note that our forward EBITDA multiple assumption of 20.0x represents a significant

discount to the historical trading multiple of the peer set of 26.7x and a discount to the

average forward (2021) multiple of 20.9x.

Figure 58: Target EBITDA assumptions and output

Source: Shaw and Partners analysis

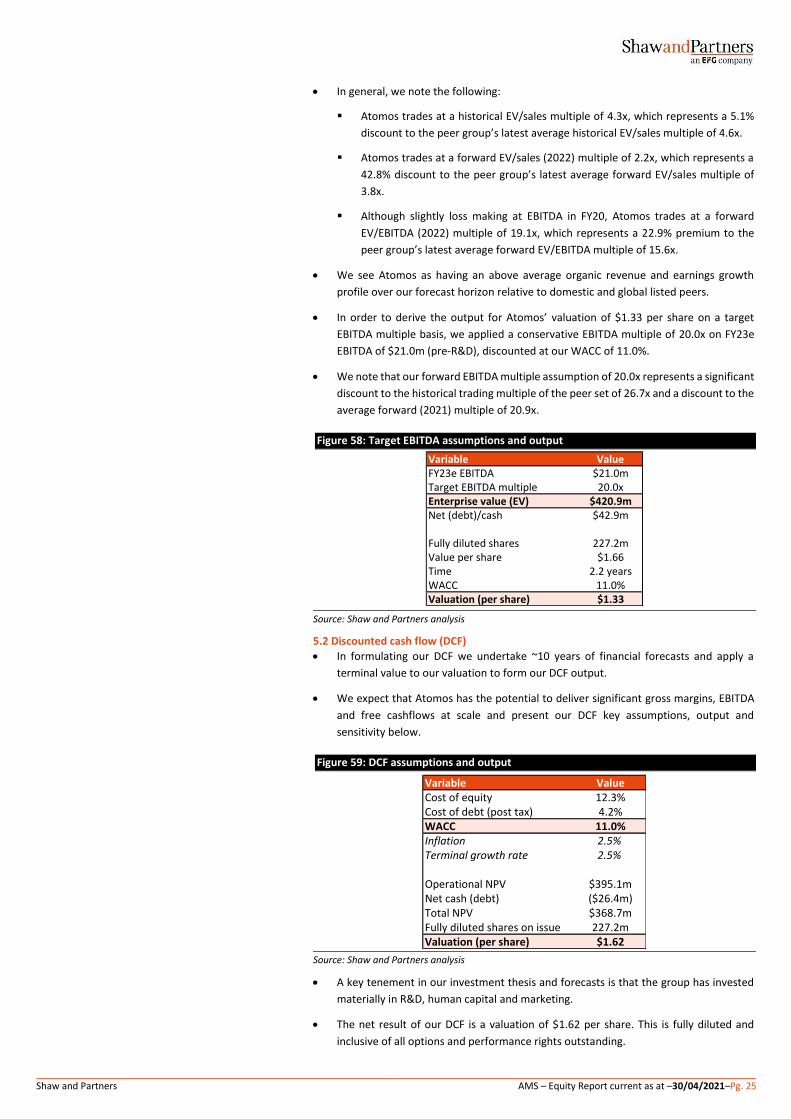

5.2 Discounted cash flow (DCF)

• In formulating our DCF we undertake ~10 years of financial forecasts and apply a

terminal value to our valuation to form our DCF output.

• We expect that Atomos has the potential to deliver significant gross margins, EBITDA

and free cashflows at scale and present our DCF key assumptions, output and

sensitivity below.

Figure 59: DCF assumptions and output

Source: Shaw and Partners analysis

• A key tenement in our investment thesis and forecasts is that the group has invested

materially in R&D, human capital and marketing.

• The net result of our DCF is a valuation of $1.62 per share. This is fully diluted and

inclusive of all options and performance rights outstanding.

Variable ValueFY23e EBITDA $21.0mTarget EBITDA multiple 20.0xEnterprise value (EV) $420.9mNet (debt)/cash $42.9m

Fully diluted shares 227.2mValue per share $1.66Time 2.2 yearsWACC 11.0%Valuation (per share) $1.33

Variable ValueCost of equity 12.3%Cost of debt (post tax) 4.2%WACC 11.0%Inflation 2.5%Terminal growth rate 2.5%

Operational NPV $395.1mNet cash (debt) ($26.4m)Total NPV $368.7mFully diluted shares on issue 227.2mValuation (per share) $1.62

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 26

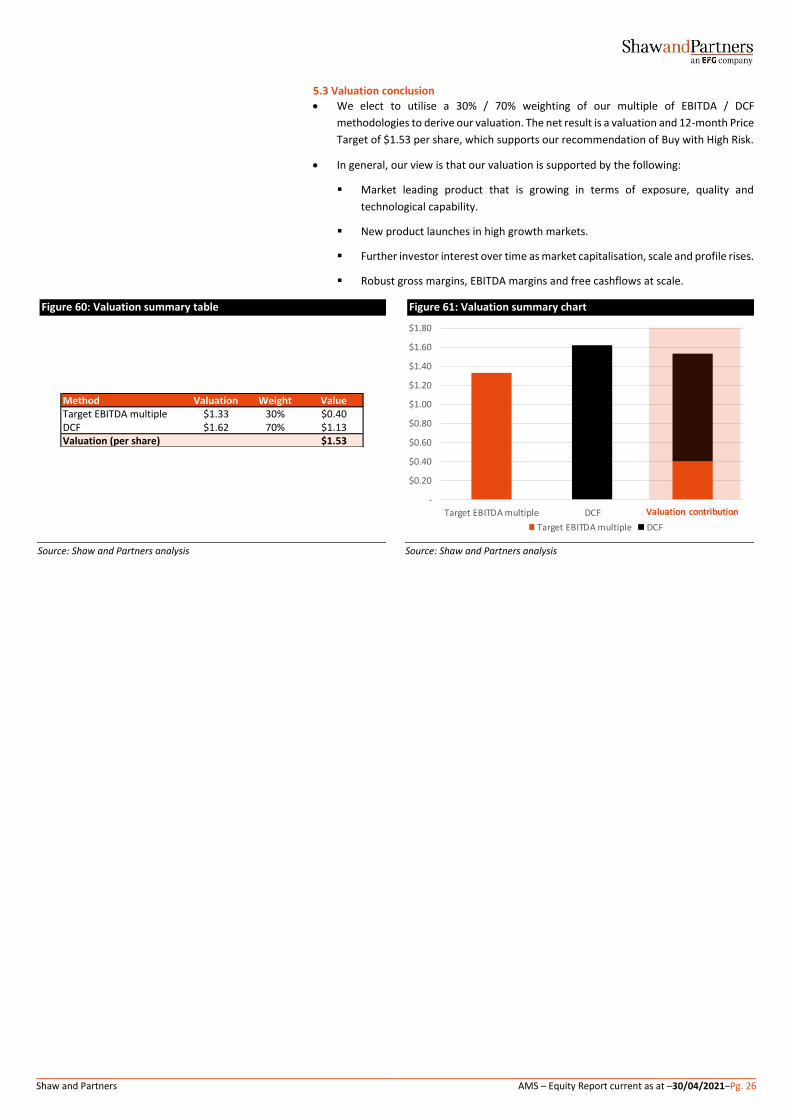

5.3 Valuation conclusion

• We elect to utilise a 30% / 70% weighting of our multiple of EBITDA / DCF

methodologies to derive our valuation. The net result is a valuation and 12-month Price

Target of $1.53 per share, which supports our recommendation of Buy with High Risk.

• In general, our view is that our valuation is supported by the following:

▪ Market leading product that is growing in terms of exposure, quality and

technological capability.

▪ New product launches in high growth markets.

▪ Further investor interest over time as market capitalisation, scale and profile rises.

▪ Robust gross margins, EBITDA margins and free cashflows at scale.

Figure 60: Valuation summary table Figure 61: Valuation summary chart

Source: Shaw and Partners analysis

Source: Shaw and Partners analysis

Method Valuation Weight Value Target EBITDA multiple $1.33 30% $0.40DCF $1.62 70% $1.13Valuation (per share) $1.53

-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

Target EBITDA multiple DCF Valuation contribution

Target EBITDA multiple DCF

Valuation contribution

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 27

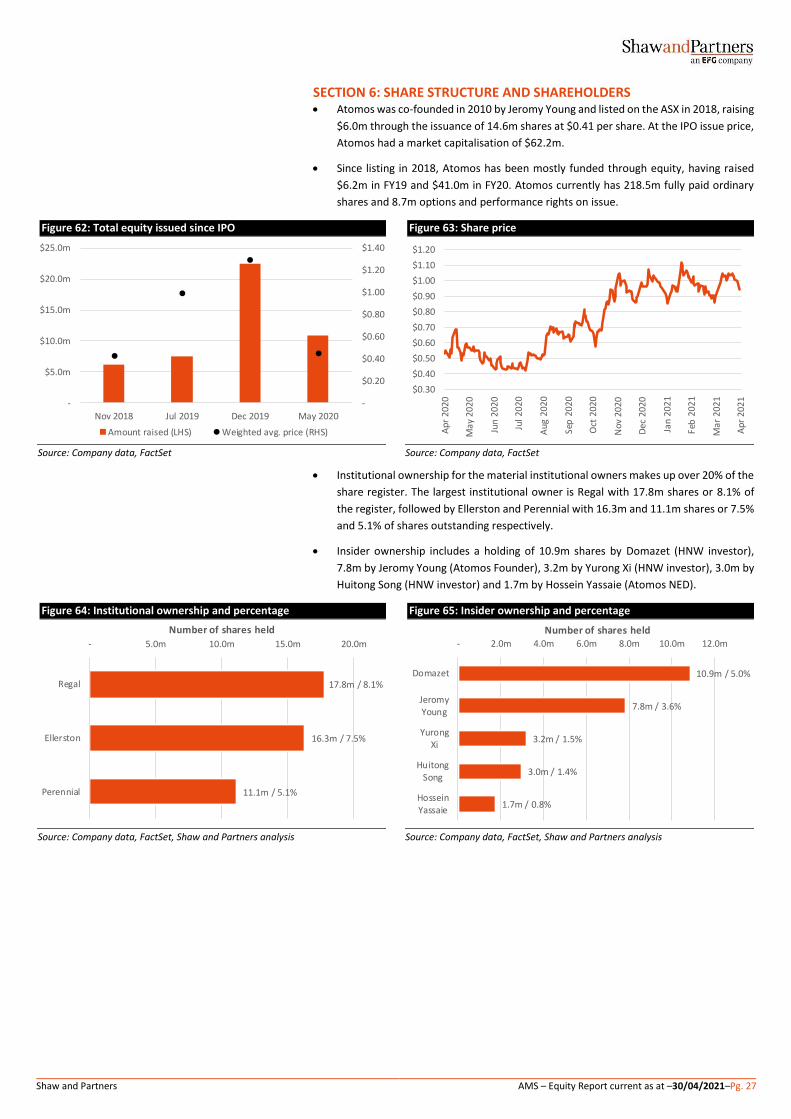

SECTION 6: SHARE STRUCTURE AND SHAREHOLDERS • Atomos was co-founded in 2010 by Jeromy Young and listed on the ASX in 2018, raising

$6.0m through the issuance of 14.6m shares at $0.41 per share. At the IPO issue price,

Atomos had a market capitalisation of $62.2m.

• Since listing in 2018, Atomos has been mostly funded through equity, having raised

$6.2m in FY19 and $41.0m in FY20. Atomos currently has 218.5m fully paid ordinary

shares and 8.7m options and performance rights on issue.

Figure 62: Total equity issued since IPO Figure 63: Share price

Source: Company data, FactSet Source: Company data, FactSet

• Institutional ownership for the material institutional owners makes up over 20% of the

share register. The largest institutional owner is Regal with 17.8m shares or 8.1% of

the register, followed by Ellerston and Perennial with 16.3m and 11.1m shares or 7.5%

and 5.1% of shares outstanding respectively.

• Insider ownership includes a holding of 10.9m shares by Domazet (HNW investor),

7.8m by Jeromy Young (Atomos Founder), 3.2m by Yurong Xi (HNW investor), 3.0m by

Huitong Song (HNW investor) and 1.7m by Hossein Yassaie (Atomos NED).

Figure 64: Institutional ownership and percentage Figure 65: Insider ownership and percentage

Source: Company data, FactSet, Shaw and Partners analysis Source: Company data, FactSet, Shaw and Partners analysis

-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

-

$5.0m

$10.0m

$15.0m

$20.0m

$25.0m

Nov 2018 Jul 2019 Dec 2019 May 2020

Amount raised (LHS) Weighted avg. price (RHS)

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

Ap

r 2

02

0

Ma

y 2

02

0

Jun

20

20

Jul 2

020

Au

g 2

02

0

Sep

202

0

Oct

20

20

Nov

202

0

Dec

202

0

Jan

20

21

Feb

202

1

Mar

20

21

Ap

r 2

02

1

17.8m / 8.1%

16.3m / 7.5%

11.1m / 5.1%

Regal

Ellerston

Perennial

- 5.0m 10.0m 15.0m 20.0m

Number of shares held

10.9m / 5.0%

7.8m / 3.6%

3.2m / 1.5%

3.0m / 1.4%

1.7m / 0.8%

Domazet

JeromyYoung

YurongXi

HuitongSong

HosseinYassaie

- 2.0m 4.0m 6.0m 8.0m 10.0m 12.0m

Number of shares held

Shaw and Partners AMS – Equity Report current as at –30/04/2021–Pg. 28

SECTION 7: BOARD AND MANAGEMENT

7.1 Board

Chris Tait, Executive Chairman Chris has over 25 years of experience advising private and public companies on general strategic advice, M&A and raising capital. He has also held senior executive roles in a major public company, WHSmith where he was initially Director of Strategy and Acquisitions and then CFO of the Asia Pacific operations. Co-Founder and Managing Director of Henslow, an independent advisory firm and Corporate Adviser to Atomos.

Sir Hossein Yassaie, Non-Executive Director Sir Hossein has over 35 years of experience in specialised research and development and semiconductors and was Founder of Imagination Technologies and held the position of CEO for 18 years. Hossein received a knighthood in 2013 in recognition of his services to technology and innovation in the United Kingdom.

Stephen Stanley, Non-Executive Director Stephen has over 25 years’ experience in the Logistics sector in Australia, Asia, Europe and North America. Stephen was previously Director for Corporate Development for Toll Holdings from 1999 until 2012 and Non-Executive Director for Cabcharge Australia. Stephen is also currently Chairman for Ventura Motors.

7.2 Management