Embed Size (px)

Citation preview

ATM – Mobile Integration Guide:Strategies for Successful Omnichannel Banking

DEVELOPED AND PUBLISHED BY:

SPONSORED BY:

GUIDE

© 2014 NETWORLD MEDIA GROUP 2

CONTENTSPage 3 Contributing organizations

Page 4 Introduction ATM-mobile integration survey Lack of integration Future plans Innovators ATM growth ATM models Mobile growth Channel architecture

Page 10 Chapter 1 ATM-mobile integration survey results

Page 19 Chapter 2 Key trends in cross-channel integration Cardless withdrawals through mobile pre-staging QR codes Mobile wallets Omnichannel Branch transformation ATM models Beyond silo channels architecture Fundamental change WWS

Page 26 Chapter 3 Case Studies of ATM and branch innovators Bank of America Branches BBVA BBVA Compass ABIL Nationwide Building Society Royal Bank of Scotland Customer recommendations Mobile ATM St. George Bank Wells Fargo

Page 35 Chapter 4 Interviews with innovative banks Alfa Bank Banco Sabadell Bank of Ireland BBVA BBVA Compass CaixaBank Low added value transactions Chase Co-op Financial Services Commerzbank CU24 Erste Group Bank/Ceska Sporitelna HSBC Bank USA Intesa Sanpaolo Bank Poste Italiane/BancoPosta SunTrust Bank UBS Branch of the future

Page 53 References

Published by Networld Media Group © 2014 Networld Media Group Written by Robin Arnfield, contributing writer, ATMmarketplace.com Tom Harper, president and CEO Kathy Doyle, executive vice president and publisherSuzanne Cluckey, editorGreg Sharpless, editorial directorTiffany Smith, custom content editor

© 2014 NETWORLD MEDIA GROUP 3

CONTRIBUTING ORGANIZATIONSAuriga (Italy)

Andrew Martin, Retail Banking Consulting Group (U.K.)

ATMIA

Bank of Ireland

Banco Sabadell (Spain)

Bank of America (U.S.)

BBVA (Spain)

BBVA Compass (U.S.)

David Cavell, international retail banking consultant (U.K.)

CaixaBank (Spain)

Chase (U.S.)

Commerzbank (Germany)

Co-op Financial Services (U.S.)

CU24 (U.S.)

Ed O’Brien, Director, Banking Channels Advisory Service, Mercator Advisory Group (U.S.)

Erste Group (Austria)/Ceska Sporitelna (Czech Republic)

Barry Forbes, independent payments consultant (U.K./South Africa)

Karen Epper Hoffman, Writer/Analyst, Lafferty Group

HSBC Bank USA

Intesa Sanpaolo Bank (Italy)

Nationwide Building Society (U.K.)

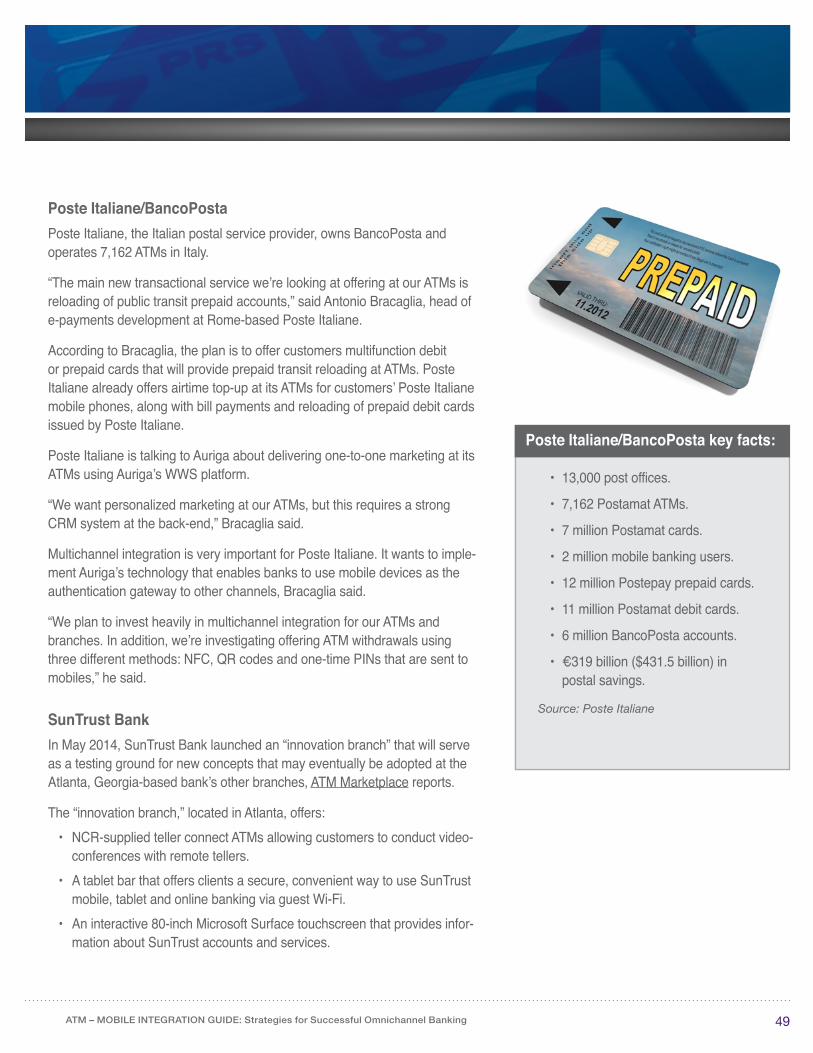

Poste Italiane/BancoPosta (Italy)

Royal Bank of Scotland (U.K.)

SunTrust Bank (U.S.)

UBS

UniCredit (Italy)

Wells Fargo (U.S.)

© 2014 NETWORLD MEDIA GROUP 4

ATM Marketplace surveyed financial institutions worldwide and conducted detailed interviews with leading European and U.S. banks to compile its 2014 ATM-Mobile Integration Guide, illustrating trends in multichannel banking around the world.

The Guide examines how banks are developing cross-channel strategies linking their ATMs with their mobile channels, their branches and Internet banking. It also identifies how the role of the ATM will evolve in the future omnichannel banking environment.

ATM Marketplace thanks Auriga for allowing us to bring this publication to you at no cost. We also thank all the participants in our survey.

ATM-mobile integration surveyIn July 2014, ATM Marketplace conducted an international survey of banks’ multichannel banking services and strategies, including their deployment of ATM-mobile integration technology.

The survey received responses from 169 banks, credit unions and other types of financial institutions (FIs) from around the world.

Respondents were asked “How many ATMs do you have?” One-third (33 percent) have more than 2,000 ATMs, while 28 percent have 1–100 ATMs, 20 percent have 101–500 ATMs and 19 percent have 501–2,000 ATMs.

For 44 percent of respondents to a question about investment priorities, investing in multichannel integration is a top priority, while 41 percent said investing in integration is important, but other technology investments have greater priority.

Just over half (54 percent) of respondents have a branch transformation program, but only 38 percent have a branch of the future where they test new self-service applications.

Lack of integrationThe survey found that many banks have yet to integrate their ATM and mo-bile channels. Three-quarters (76 percent) of those that responded to the question “Do you currently offer mobile integration services at your ATMs?” said they do not.

Robin ArnfieldATMMarketplace.com

Robin Arnfield has been a technology journalist since 1983. His work has been published in ATM Marketplace, Mobile Payments Today, ATM & Debit News, ISO & Agent, CardLine, Bank Technology News, Cards International and Electronic Payments International. He has covered the United Kingdom, European, North American and Latin American payments markets.

INTRODUCTION

5ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

Mobile ATM transactions involving one-time codes are the most popular mobile cash access method, while ATM location services are the most prevalent mobile integration service offered, the survey found.

Of the responses to the question, “Which mobile integration services do you offer?”, 75 percent offer ATM location via mobile devices and 56 percent offer cardless ATM transactions using a one-time authentication code.

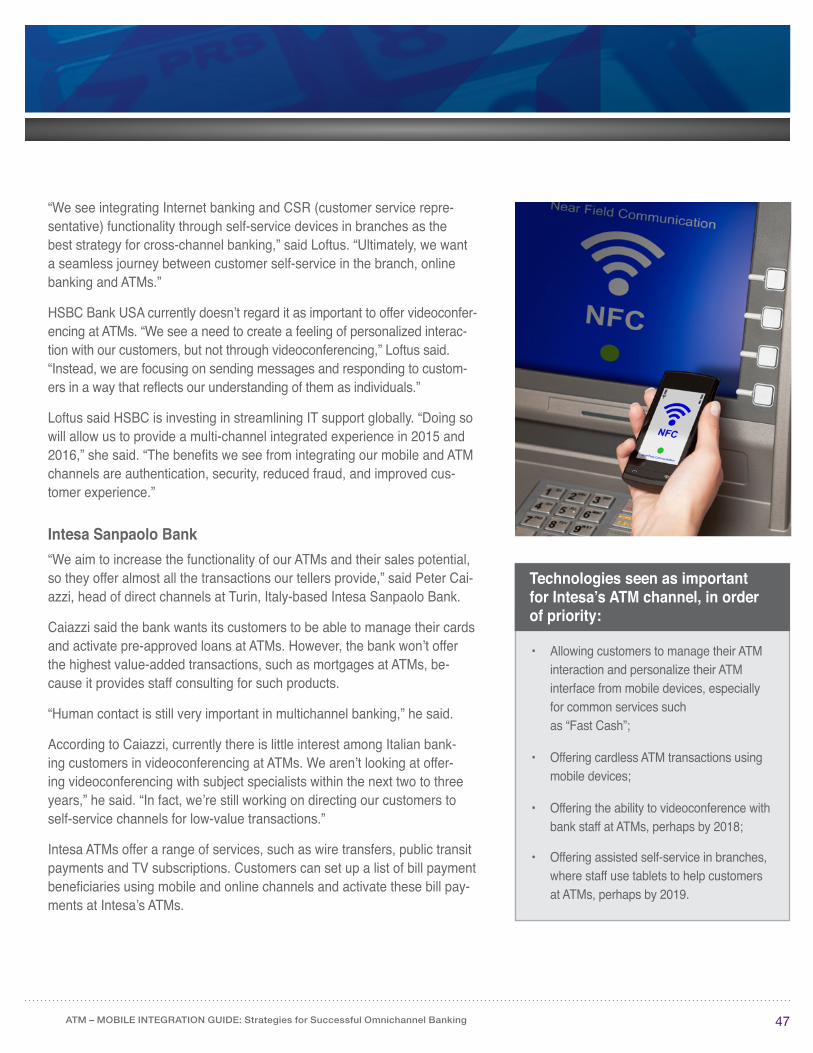

One-fifth (22 percent) offer cardless transactions from mobile wallets using QR codes, while 19 percent offer a real-time view on the user’s mobile de-vice of services available at a selected ATM, and 19 percent offer cardless transactions using near field communications-enabled mobile devices.

The survey found a low level of adoption of technology allowing transac-tions to be pre-staged on one channel for completion on another. Only 24 percent of respondents when asked about transaction pre-staging allow customers to pre-stage a transaction on one channel, such as the web or mobile banking, and complete it on another, such as an ATM.

Auriga’s WinWebServer (WWS) multichannel and cross-channel platform, offering what the banking industry refers to as “omnichannel” capabilities, allows customers to pre-stage ATM withdrawals on their mobile devices. “Users can configure their preferred withdrawal details in our app and simply select these predefined preferences at the ATM,” said David Smith, Auriga’s business development director. “The net effect is greater consumer convenience, security and transaction speed.”

Future plansOf the responses to the question, “Which mobile integration services do you plan to offer at your ATMs within the next two to three years?”, 54 percent plan to offer ATM location via mobile devices.

Nearly half (45 percent) plan to offer cardless transactions from NFC-enabled mobile devices and 37 percent plan to allow customers to manage their ATM or debit card accounts from mobile devices.

Only 30 percent of respondents when asked about personalization allow their customers to personalize the user interface and customer experience at their ATMs and other self-service devices such as smartphones. How-ever, 39 percent plan to offer their customers this option in the next two to three years.

6ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

Nearly half (46 percent) of responses to a question about self-service bank-ing terminals offer assisted self-service where staff equipped with tablets are able to help customers perform transactions at the terminals.

However, 56 percent of respondents plan to offer assisted self-service within the next two to three years.

The survey also found a low level of adoption in remote video teller technol-ogy. The majority (85 percent) of respondents when asked about video-conferencing don’t offer videoconferences with customer service staff or product experts at their ATMs or self-service banking terminals.

However, 64 percent of respondents aim to offer videoconferencing at their ATMs or self-service banking terminals within the next two to three years.

InnovatorsFor the Guide, ATM Marketplace conducted in-depth interviews with innova-tive banks in Europe and the U.S., including Spain’s BBVA and CaixaBank, Chase, HSBC Bank USA, Italy’s Intesa Sanpaolo Bank and UniCredit, and Russia’s Alfa Bank. The interviews revealed a strong interest in mobile-ATM integration and in offering user interface personalization at ATMs.

“We’re currently developing our cross-channel strategy so that any transac-tion can be prepared and/or launched using any channel and completed in any other,” a CaixaBank spokesperson said.

Mobile is central to CaixaBank’s multichannel strategy. “We’re promoting mobile not just as the authentication method for accessing home banking but also for interacting with our ATMs through cardless NFC technology,” the CaixaBank spokesperson said.

For CaixaBank, it is important to allow customers to manage their ATM interaction and personalize their ATM interface from mobile devices, the spokesperson said.

“Consumers are embracing mobile technology very rapidly and expect it to be integrated into banking and payments channels,” said Terry Pierce, senior product manager at U.S. credit union ATM network operator Co-op Financial Services.

For Manuel Crespo, BBVA’s head of physical channels technology, multi-channel integration is a very high priority.

“Consumers are embracing mobile technology very

rapidly and expect it to be integrated into banking and

payments channels.” — Terry Pierce, senior product manager

Co-op Financial Services

7ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

“It’s very important to enable all transactions initiated on mobile devices to be seamlessly completed on another channel,” he said. “Since mobile devices play such an important role in our lives, they should be considered as the main method for authenticating payments and customer service requests.”

Peter Caiazzi, head of direct channels at Intesa Sanpaolo Bank, said Intesa plans to increase the functionality of its ATMs and their sales potential, so that the ATMs offer almost all the transactions the tellers provide.

“For example, we want our customers to be able to manage their cards and activate pre-approved loans at our ATMs. However, we won’t offer the high-est value-added transactions, such as mortgages, as we provide consulting with our staff for these products. Human contact is still very important in multichannel banking,” he said.

ATM growthAccording to U.K.-based consultancy Retail Banking Research, the global installed base of ATMs rose by 8 percent to 2.6 million in 2012.

8ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

ATM modelsInternational retail banking consultant David Cavell says banks are begin-ning to deploy two different types of ATM:

• Advanced multifunction ATMs;

• Tablet-based ATMs where the screen is mounted like a portrait tablet instead of integrated inside a fascia.

Cavell noted that everything that can be done on a high-function ATM or self-service kiosk can now be done on a tablet. In this scenario, the ATM would be reduced to a physically-secure cash storage box, which would be controlled by a tablet belonging to the customer or supplied by the bank.

Mobile growthAccording to Forrester Research, the number of European mobile phone banking users will rise from 42 million users in 2013 to 99 million in 2018, while European tablet banking users will rise from 19 million users in 2013 to 115 million in 2018.

In January 2014, the European ATM Security Team released the results of a poll of users of its website on attitudes toward contactless ATM access. According to EAST, 74 percent of respondents indicated that they would be happy to use contactless card or smartphone technology to make an ATM withdrawal; only slightly more than one-quarter said they wouldn’t want to use the technology

A U.S. consumer survey by Mercator Advisory Group in November 2013 found that banking via mobile device is fast becoming a preferred way for consumers to conduct banking activities and manage financial information on-the-go.

“Mobile and tablet banking use is rising rapidly and becoming a preferred banking method as consumers take advantage of multiple channels for their banking activities,” said Karen Augustine, manager of Primary Data Services at Mercator.

Channel architecture“Instead of saying that they have independent service silos and channels, each with their own functionality, and trying to integrate these channels at

“Mobile and tablet banking use is rising rapidly and becoming

a preferred banking method as consumers take advantage

of multiple channels for their banking activities.”

— Karen Augustine, manager of Primary Data Services, Mercator

9ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

the back-end, banks need to step right out of the banking environment and look at their channels from the customer perspective,” said Auriga’s Smith.

However, this process involves a fundamental change in a bank’s channel architecture. According to Smith, Auriga sees the mobile phone, not the ATM, as the center of the omnichannel banking environment, because the mobile phone goes everywhere with the customer.

Instead of investing in technology that perpetuates a fragmented services approach, banks should deploy systems that facilitate the customer experi-ence by sharing the same data and business rules across multiple chan-nels, Smith said.

“ATMs must be able to provide customers with all the functions available on other channels,” said Carmine Evangelista, Auriga’s chief technology of-ficer. “When banks implement a truly multichannel architecture, their ATMs will be able to provide customers with all the functions available on other channels, without duplicating development costs.”

© 2014 NETWORLD MEDIA GROUP 10

CHAPTER 1ATM-mobile integration survey results

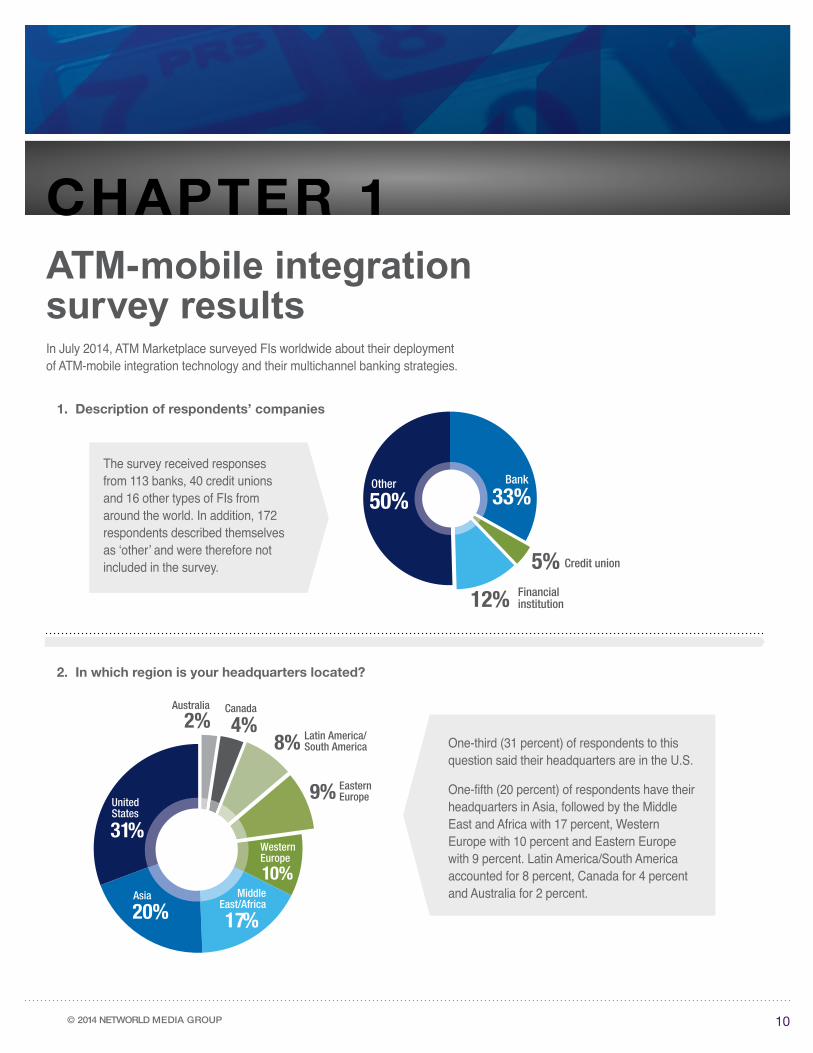

1. Description of respondents’ companies

2. In which region is your headquarters located?

The survey received responses from 113 banks, 40 credit unions and 16 other types of FIs from around the world. In addition, 172 respondents described themselves as ‘other’ and were therefore not included in the survey.

One-third (31 percent) of respondents to this question said their headquarters are in the U.S.

One-fifth (20 percent) of respondents have their headquarters in Asia, followed by the Middle East and Africa with 17 percent, Western Europe with 10 percent and Eastern Europe with 9 percent. Latin America/South America accounted for 8 percent, Canada for 4 percent and Australia for 2 percent.

In July 2014, ATM Marketplace surveyed FIs worldwide about their deployment of ATM-mobile integration technology and their multichannel banking strategies.

Bank

33%

Credit union 5% Financial institution 12%

Other

50%

Australia

2%

Canada

4%

Latin America/South America 8%

Eastern Europe 9%

WesternEurope

10% Middle

East/Africa

17% Asia

20%

United States

31%

11ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

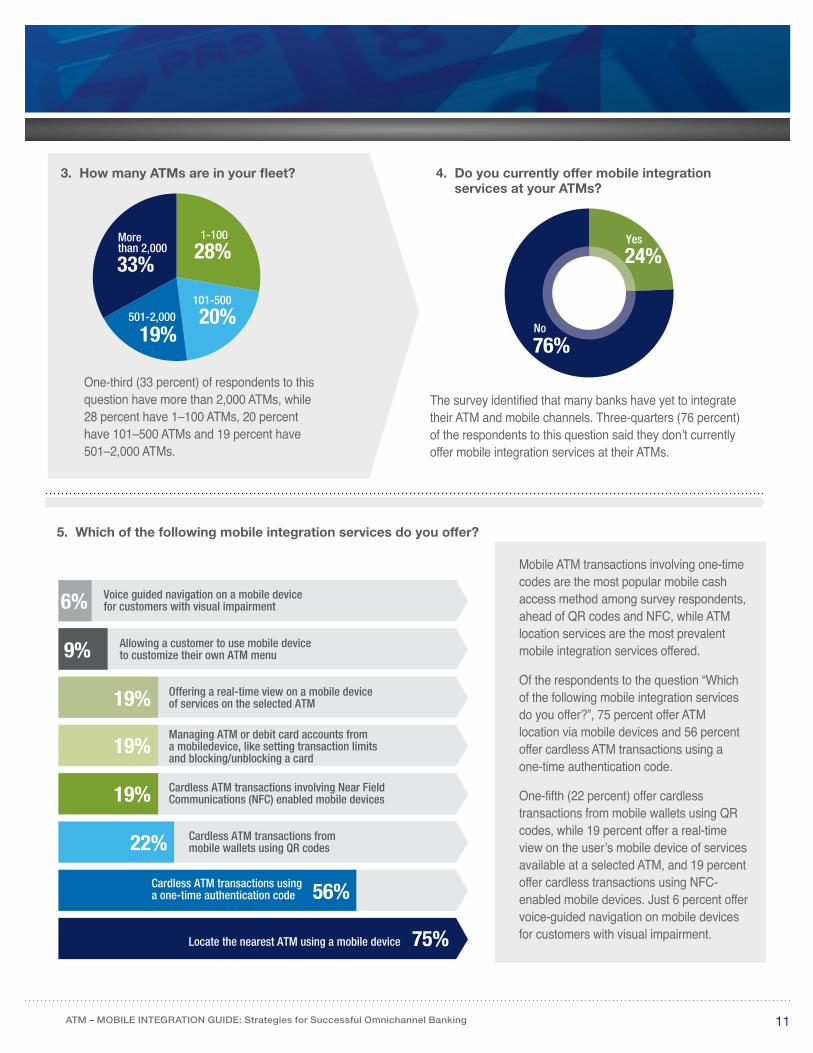

3. How many ATMs are in your fleet?

5. Which of the following mobile integration services do you offer?

4. Do you currently offer mobile integration services at your ATMs?

Mobile ATM transactions involving one-time codes are the most popular mobile cash access method among survey respondents, ahead of QR codes and NFC, while ATM location services are the most prevalent mobile integration services offered.

Of the respondents to the question “Which of the following mobile integration services do you offer?”, 75 percent offer ATM location via mobile devices and 56 percent offer cardless ATM transactions using a one-time authentication code.

One-fifth (22 percent) offer cardless transactions from mobile wallets using QR codes, while 19 percent offer a real-time view on the user’s mobile device of services available at a selected ATM, and 19 percent offer cardless transactions using NFC-enabled mobile devices. Just 6 percent offer voice-guided navigation on mobile devices for customers with visual impairment.

One-third (33 percent) of respondents to this question have more than 2,000 ATMs, while 28 percent have 1–100 ATMs, 20 percent have 101–500 ATMs and 19 percent have 501–2,000 ATMs.

1-100

28%

101-500

20% 501-2,000

19%

More than 2,000

33%

The survey identified that many banks have yet to integrate their ATM and mobile channels. Three-quarters (76 percent) of the respondents to this question said they don’t currently offer mobile integration services at their ATMs.

Yes

24%

No

76%

75%Locate the nearest ATM using a mobile device

56%Cardless ATM transactions using a one-time authentication code

22% Cardless ATM transactions from mobile wallets using QR codes

19% Cardless ATM transactions involving Near FieldCommunications (NFC) enabled mobile devices

19%Managing ATM or debit card accounts froma mobiledevice, like setting transaction limits and blocking/unblocking a card

19% Offering a real-time view on a mobile device of services on the selected ATM

9% Allowing a customer to use mobile device to customize their own ATM menu

6% Voice guided navigation on a mobile device for customers with visual impairment

12ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

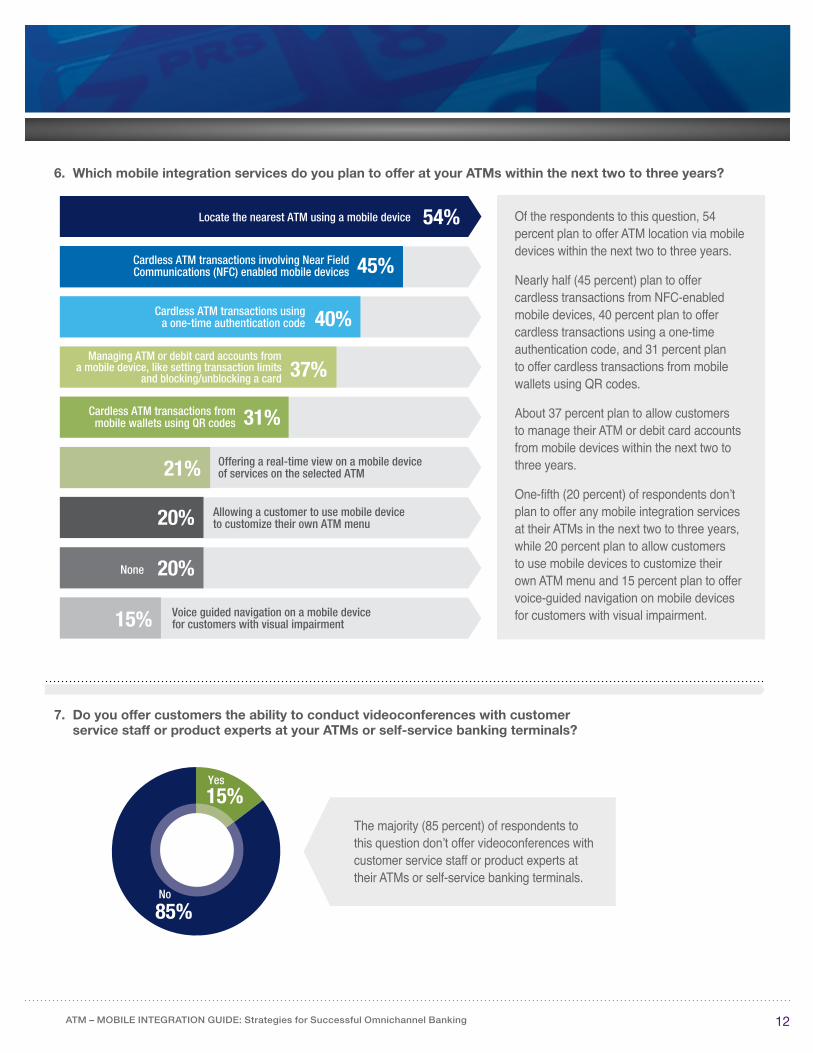

6. Which mobile integration services do you plan to offer at your ATMs within the next two to three years?

7. Do you offer customers the ability to conduct videoconferences with customer service staff or product experts at your ATMs or self-service banking terminals?

The majority (85 percent) of respondents to this question don’t offer videoconferences with customer service staff or product experts at their ATMs or self-service banking terminals.

Of the respondents to this question, 54 percent plan to offer ATM location via mobile devices within the next two to three years.

Nearly half (45 percent) plan to offer cardless transactions from NFC-enabled mobile devices, 40 percent plan to offer cardless transactions using a one-time authentication code, and 31 percent plan to offer cardless transactions from mobile wallets using QR codes.

About 37 percent plan to allow customers to manage their ATM or debit card accounts from mobile devices within the next two to three years.

One-fifth (20 percent) of respondents don’t plan to offer any mobile integration services at their ATMs in the next two to three years, while 20 percent plan to allow customers to use mobile devices to customize their own ATM menu and 15 percent plan to offer voice-guided navigation on mobile devices for customers with visual impairment.

45%Cardless ATM transactions involving Near FieldCommunications (NFC) enabled mobile devices

31%Cardless ATM transactions frommobile wallets using QR codes

40%Cardless ATM transactions usinga one-time authentication code

37%Managing ATM or debit card accounts from

a mobile device, like setting transaction limitsand blocking/unblocking a card

20% Allowing a customer to use mobile device to customize their own ATM menu

54%Locate the nearest ATM using a mobile device

21% Offering a real-time view on a mobile device of services on the selected ATM

15% Voice guided navigation on a mobile device for customers with visual impairment

20%None

Yes

15%

No

85%

13ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

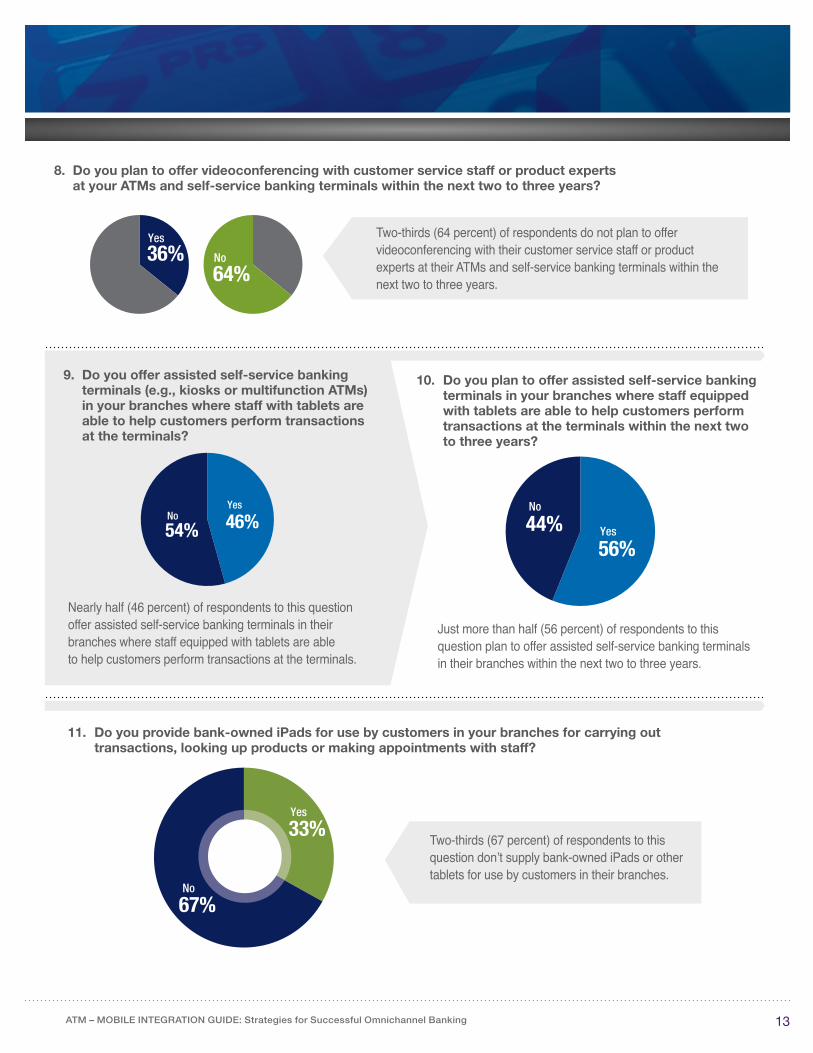

8. Do you plan to offer videoconferencing with customer service staff or product experts at your ATMs and self-service banking terminals within the next two to three years?

9. Do you offer assisted self-service banking terminals (e.g., kiosks or multifunction ATMs) in your branches where staff with tablets are able to help customers perform transactions at the terminals?

10. Do you plan to offer assisted self-service banking terminals in your branches where staff equipped with tablets are able to help customers perform transactions at the terminals within the next two to three years?

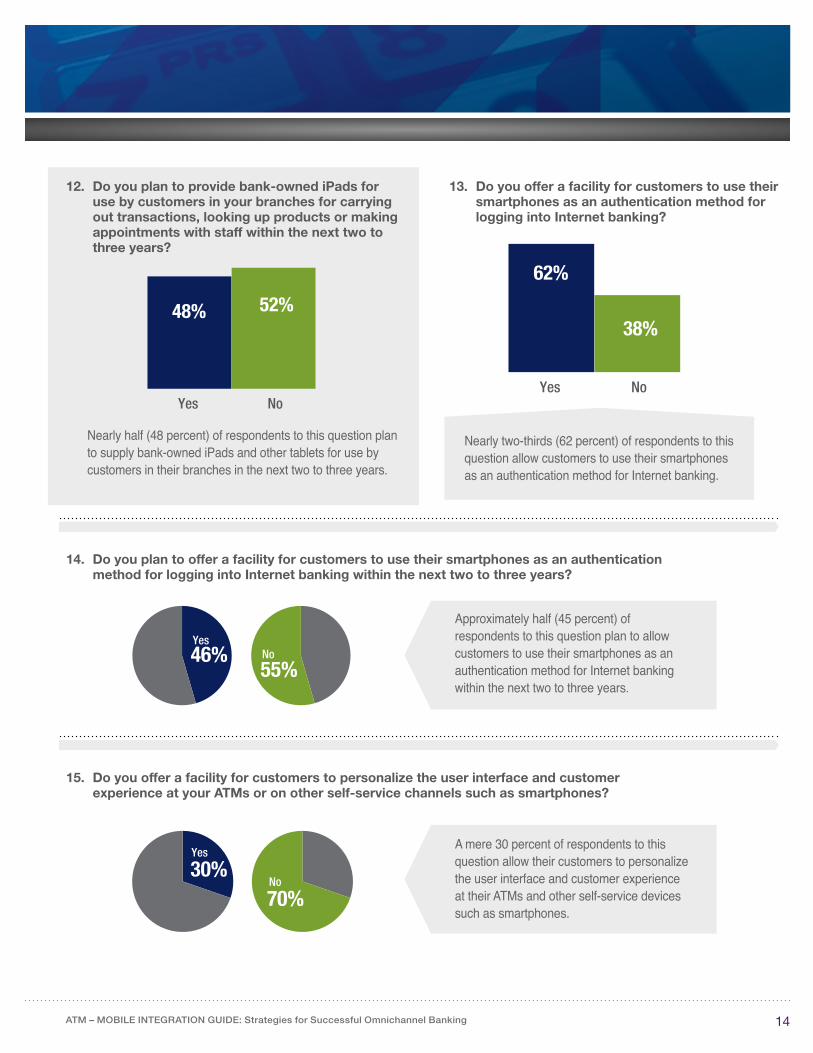

11. Do you provide bank-owned iPads for use by customers in your branches for carrying out transactions, looking up products or making appointments with staff?

Two-thirds (64 percent) of respondents do not plan to offer videoconferencing with their customer service staff or product experts at their ATMs and self-service banking terminals within the next two to three years.

Nearly half (46 percent) of respondents to this question offer assisted self-service banking terminals in their branches where staff equipped with tablets are able to help customers perform transactions at the terminals.

Yes

46%

No

54%

Just more than half (56 percent) of respondents to this question plan to offer assisted self-service banking terminals in their branches within the next two to three years.

Yes

56%

No

44%

Two-thirds (67 percent) of respondents to this question don’t supply bank-owned iPads or other tablets for use by customers in their branches.

Yes

33%

No

67%

No

64% 36% Yes

14ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

12. Do you plan to provide bank-owned iPads for use by customers in your branches for carrying out transactions, looking up products or making appointments with staff within the next two to three years?

14. Do you plan to offer a facility for customers to use their smartphones as an authentication method for logging into Internet banking within the next two to three years?

15. Do you offer a facility for customers to personalize the user interface and customer experience at your ATMs or on other self-service channels such as smartphones?

13. Do you offer a facility for customers to use their smartphones as an authentication method for logging into Internet banking?

Approximately half (45 percent) of respondents to this question plan to allow customers to use their smartphones as an authentication method for Internet banking within the next two to three years.

A mere 30 percent of respondents to this question allow their customers to personalize the user interface and customer experience at their ATMs and other self-service devices such as smartphones.

Nearly half (48 percent) of respondents to this question plan to supply bank-owned iPads and other tablets for use by customers in their branches in the next two to three years.

48% 52%

Yes No

Nearly two-thirds (62 percent) of respondents to this question allow customers to use their smartphones as an authentication method for Internet banking.

62%

38%

Yes No

Yes 46% No

55%

Yes

30% No

70%

15ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

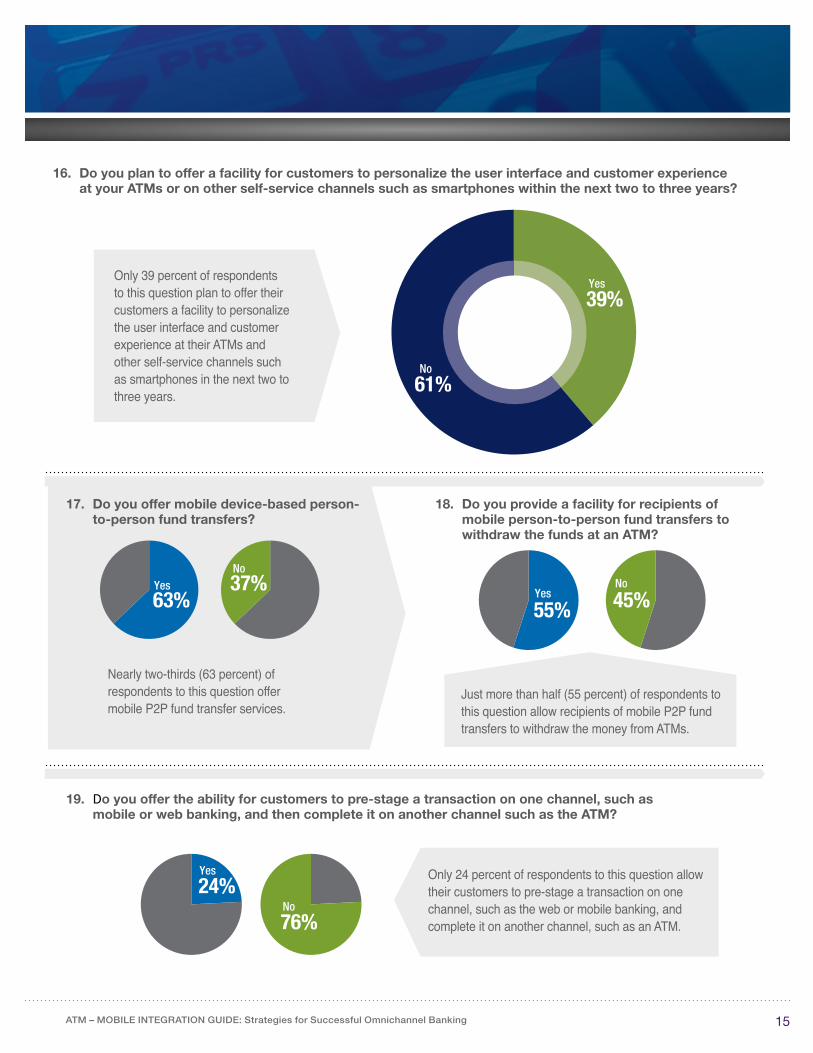

16. Do you plan to offer a facility for customers to personalize the user interface and customer experience at your ATMs or on other self-service channels such as smartphones within the next two to three years?

17. Do you offer mobile device-based person- to-person fund transfers?

19. Do you offer the ability for customers to pre-stage a transaction on one channel, such as mobile or web banking, and then complete it on another channel such as the ATM?

18. Do you provide a facility for recipients of mobile person-to-person fund transfers to withdraw the funds at an ATM?

Nearly two-thirds (63 percent) of respondents to this question offer mobile P2P fund transfer services.

Only 39 percent of respondents to this question plan to offer their customers a facility to personalize the user interface and customer experience at their ATMs and other self-service channels such as smartphones in the next two to three years.

Yes

39%

No

61%

No

37% Yes

63%

Just more than half (55 percent) of respondents to this question allow recipients of mobile P2P fund transfers to withdraw the money from ATMs.

Yes

55% No

45%

Only 24 percent of respondents to this question allow their customers to pre-stage a transaction on one channel, such as the web or mobile banking, and complete it on another channel, such as an ATM.

No

76%

Yes

24%

16ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

20. Do you have a branch of the future where you test new self-service applications?

21. How do you see the role of the ATM within your branches evolving over the next few years?

About 38 percent of respondents to this question have a branch of the future where they test new self-service applications.

38% 62%

Yes No

• Acting as a 24-hour branch.

• A very crucial touch point through which banks can reach customers beyond transactional banking.

• Adding additional functionality at ATMs such as remote video teller services.

• Alignment with teller transactions, e.g. 100 percent cash deposit availability.

• ATMs will become purely cash dispensers and won’t need a personal deposit functionality as mobile deposit and P2P transfers continue to grow.

• ATMs will continue to be an important channel for servicing clients over the next few years.

• ATMs will provide another channel for offering relevant product or services to customers using CRM. Customers will be able to customize their ATM menu.

• ATMs will be used to cross-sell more of our bank’s products, and will perform more cashless transactions.

• ATMs will become the primary service channel, replacing tellers.

• ATMs will become 100 percent cardless, and fully integrated with internet-based mobile browser applications.

• ATMs will be a main point of contact for our customers to do account deposits. We will move teller transactions to our deposit-accepting ATMs along with adding interactive kiosk functionality.

• Biometric authentication offered at ATMs.

• CRM role with more sales-oriented applications.

• Availability of e-receipts and QR codes.

• Increased footfall with the addition of transactions including domestic remittances for unbanked customers.

• Interfacing with other channels to form a robust platform.

• ATMs will become the channel of choice to fulfill transactions initiated from mobile devices; we envisage ATMs fulfilling 80 percent of teller counter transactions, freeing up our teller counters to perform other higher-value transactions.

• Moving toward all envelope-free ATMs and looking into multifunction ATMs.

• Pushing more self-service transactions to our cash-handling ATMs by training end users in branches.

Answers to this question include:

17ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

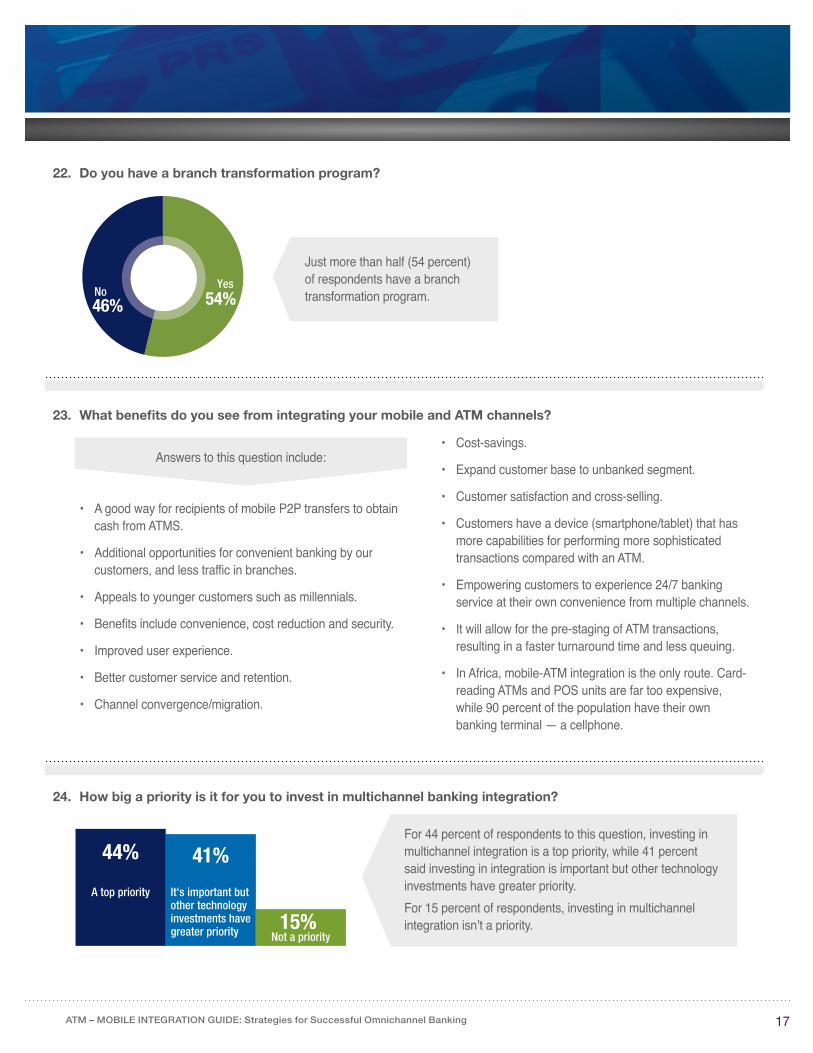

22. Do you have a branch transformation program?

23. What benefits do you see from integrating your mobile and ATM channels?

24. How big a priority is it for you to invest in multichannel banking integration?

Just more than half (54 percent) of respondents have a branch transformation program.

Yes 54% No

46%

• A good way for recipients of mobile P2P transfers to obtain cash from ATMS.

• Additional opportunities for convenient banking by our customers, and less traffic in branches.

• Appeals to younger customers such as millennials.

• Benefits include convenience, cost reduction and security.

• Improved user experience.

• Better customer service and retention.

• Channel convergence/migration.

• Cost-savings.

• Expand customer base to unbanked segment.

• Customer satisfaction and cross-selling.

• Customers have a device (smartphone/tablet) that has more capabilities for performing more sophisticated transactions compared with an ATM.

• Empowering customers to experience 24/7 banking service at their own convenience from multiple channels.

• It will allow for the pre-staging of ATM transactions, resulting in a faster turnaround time and less queuing.

• In Africa, mobile-ATM integration is the only route. Card-reading ATMs and POS units are far too expensive, while 90 percent of the population have their own banking terminal — a cellphone.

Answers to this question include:

44% 41%

A top priority

15% Not a priority

It's important but other technology investments have greater priority

For 44 percent of respondents to this question, investing in multichannel integration is a top priority, while 41 percent said investing in integration is important but other technology investments have greater priority.For 15 percent of respondents, investing in multichannel integration isn’t a priority.

18ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

25. What response have you seen from your customers to your mobile-ATM integration initiatives?

26. What personalization features do you offer at your ATMs and other self-service channels?

More than one-third (38 percent) of respondents to this question provide personalized product advertising and offers at their ATMs, while 28 percent offer customizable menus and 28 percent offer the ability to set up alerts based on specific rules. Just 19 percent offer the ability to produce specific reports.

Significantly, 44 percent of respondents don’t offer customizable menus; personalized product advertising and offers; the ability to set up alerts based on specific rules or the ability to produce specific reports.

• A good response from customers.

• Appreciation coupled with high expectation.

• Better response from our younger users and worse from older customers.

• Enthusiastic acceptance and adoption.

• Faster adoption of new functionality.

• Favorable.

• Great response — they love it.

• Adoption is growing sharply.

• Increased revenue, repeat customers, very positive feedback from customers and employees.

Answers to this question include:

28% Customizablemenus

38% Personalizedproduct advertisingand offers

28% The ability to set up alerts based on specific rules

19% The ability toproduce specificreports

44% None of the above

© 2014 NETWORLD MEDIA GROUP 19

Key trends in cross-channel integrationDue to the rapid rise in smartphone and tablet usage, the mobile channel is becoming increasingly central to consumers’ banking experience.

Forrester Research predicts that the number of European mobile phone banking users will rise from 42 million users in 2013 to 99 million in 2018, while European tablet banking users will rise from 19 million users in 2013 to 115 million in 2018. Growing tablet ownership, the increased availability of tablet banking apps, and fewer security fears among tablet users versus mobile users are among the key drivers behind the tablet banking growth predicted by Forrester.

“As customers start using their tablets and smartphones to do their bank-ing, some will stop using their desktop and laptop PCs,” said Forrester analyst Stephen Walker.

A November 2013 U.S. consumer survey carried out by Mercator Advisory Group found that banking via mobile device is fast becoming the preferred method for consumers to conduct banking activities and manage financial information on the go. Mercator found that nearly half of U.S. consumers perform banking activities on mobile phones or tablets, up from around one-third in 2012.

Karen Augustine, Mercator’s manager of Primary Data Services, said that mobile and tablet banking use is rising rapidly and becoming a preferred banking method as U.S. consumers take advantage of multiple channels for their banking activities.

“Mobile banking users are most likely to re-evaluate their financial institu-tions and open new accounts,” she said. “Financial institutions need to con-tinue to improve the usability and functionality for mobile and tablet banking or consumers will take their business elsewhere.”

CHAPTER 2

“The number of European mobile phone banking users is set to grow from 42 million users in

2013 to 99 million in 2018, while European tablet banking users

will rise from 19 million users in 2013 to 115 million in 2018.”

— Source: Forrester Research

20ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

Cardless withdrawals through mobile pre-staging“Our survey found that there is a strong interest among U.S. consumers in being able to pre-stage ATM transactions on mobile devices,” said Ed O’Brien, director of Mercator’s Banking Channels Advisory Service. “They like the idea of the greater security and time-saving offered by cardless transactions compared to card-based ATM transactions.”

Barry Forbes, a South Africa-based independent payments consultant, said he believes it’s important to appreciate that pre-staging is really a mobile banking application and is very complex to implement in a non- on-us environment.

O’Brien estimates that U.S. banks will move from pilots of ATM-mobile inte-gration services to implementation within the next six to 18 months.

“QR codes are increasingly being used for mobile cash access at ATMs because they don’t require hardware upgrades at ATMs,” he said. “I think QR codes could be a bridge strategy to NFC-based cardless withdrawals over the next few years.”

QR codesA QR code-based ATM transaction involves cash being withdrawn from a mobile wallet linked to a bank account.

Customers pre-stage a QR code-based cash withdrawal on their smart-phone using their mobile banking app. After they have initiated the transac-tion, a QR code may be texted to their smartphone and then scanned at the ATM in order to authenticate the withdrawal. Alternatively, the ATM may display a QR code which the user scans on their smartphone.

According to “Cardless ATMs, Are Mobile Transactions the Future of the ATM Industry?”, a white paper sponsored by the ATMIA (ATM Industry As-sociation) and Kahuna ATM Solutions, the security advantage of QR codes is that they typically work like one-time tokens, as they are unique codes that can only be used once.

Examples of banks deploying QR codes for ATM transactions include Tur-key’s Türk Ekonomi Bankasi and IsBank, and U.S.-based WinTrust Finan-cial Trust, Diebold Federal Credit Union and City National Bank.

Mobile walletsTwenty percent of mobile phones will have mobile wallet capability by 2018, according to U.K.-based Juniper Research. This compares to less than 10 percent at the end of 2013.

21ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

According to Juniper Research, two wallet models will drive growth:

• In emerging/developing markets, stored-value accounts are enabling first-time financial access for unbanked individuals. Juniper Research anticipates a surge in deployments across sub-Saharan Africa, devel-oping Asia and Latin America.

• Across North America and Western Europe, wallets are expected to feature contactless payment functionality, such as host card emulation-based (HCE) NFC services.

With both HCE- and QR code wallet-based payment schemes, mobile pay-ments take place using payment credentials stored in the cloud instead of on a smartphone’s secure element, the traditional model for NFC payments.

OmnichannelO’Brien said he thinks banks need to move from a multichannel to an omnichannel approach, stating that, “True omnichannel includes not just integration but also collaboration between the different channels so banks can have a 360 degree real-time view of customers’ needs and behaviors, and customers can start a transaction on one channel and complete it on another and obtain real-time information.”

Auriga was ahead of the curve, because it developed a complete solution which is both multichannel and cross-channel before the market started speaking about omnichannel.

O’Brien said multichannel banking systems typically use inefficient point-to-point channel integration technology that has to be patched on each channel with every new operating system or application update. To achieve omnichannel integration, banks should use integration hubs.

By using an integration hub, banks are able to adjust their software once at one level for all their channels, he said. Another benefit is that an integra-tion hub provides bank customers with near real-time capability. By con-trast, multichannel systems don’t offer real-time integration, as they rely on batch processing to update balances on different channels.

“The concept of omnichannel is growing in importance in retail banking, with the need for customer convenience taking precedence,” wrote Ron Mazur-sky, director of Mercator’s Debit Advisory Services, in Payments Journal. “Consumers want the comfort of using the easiest method to reach their bank and transact in the way that’s easiest for them at a given time. This could include starting a transaction on mobile, moving to online when they reach the office, and ending the transaction with a call to their bank officer.”

“The concept of omnichannel is growing in importance in

retail banking, with the need for customer convenience

taking precedence.”

—wrote Ron Mazursky, director of Mercator’s Debit Advisory Services, in Payments Journal

22ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

A key driver for investing in omnichannel integration is to improve the cus-tomer experience.

“C-level bank executives realize the importance of offering good customer experience if their bank is to remain a primary financial institution for their customers,” O’Brien said. “Banks are moving to omnichannel so they can compete more effectively against the direct banks and the new innovative payment companies as well as against other incumbent banks.”

O’Brien said banks need to be able to deploy analytical CRM technology so they can predict the types of products their customers will want to purchase.

“This will result in customers feeling that their bank appreciates and understands them, and enable the bank to increase its share of their wallet,” he said.

Branch transformationLarge U.S. banks are moving to a hub-and-spoke branch infrastructure involving a small number of full-size branches and a larger number of mini-branches offering self-service machines as well as assisted self-service.

Assisted self-service involves bank staff using tablets to help customers with their self-service transactions and advise them on products of potential interest to them.

“When a customer puts their card into an ATM or self-service kiosk, a mes-sage goes to an employee’s tablet to say the customer is at that machine,” said David Smith, Auriga’s business development director.

The agent can see on their tablet what the customer is doing at that ma-chine, as well as the transaction history and account status for the cus-tomer and what marketing promotions have been sent to them. One benefit is that, if the customer needs to withdraw $2,000 to buy a car, for example, and their daily limit is $1,000, the agent can override this block and let the customer withdraw the $2,000, Smith said.

“Mobile is changing the branch from the transactional hub which it used to be, to a sales center,” said Karen Epper Hoffman, a writer/analyst with U.K.-based Lafferty Group. “I’m seeing a lot more bank branches that look like Apple stores, with staff carrying iPads and tablets.”

Epper observed that tellers are using mobile technology to interact more ef-fectively with customers. And banks are also starting to locate their product specialists in central offices and allow customers to interact with them via video links at in-branch self-service kiosks.

23ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

ATM models

According to U.K.-based international retail banking consultant David Cavell, two different ATM models are beginning to be deployed:

• Advanced multifunction ATMs such as those installed by BBVA and CaixaBank.

• Tablet-based ATMs where the screen is mounted like a portrait tablet instead of being integrated within a fascia. One example is Chase’s tablet-based Express Banking Kiosk ATMs.

“Ultimately, a bank could remove the tablet from the ATM, reducing the ATM to a physically secure storage box which is controlled by a customer-owned or bank-supplied mobile device,” Cavell said. The ATM’s role would be restricted to accepting and dispensing money.

“Everything that you can do on a high-function ATM or self-service kiosk can now be done on a tablet,” Cavell said. “You need to think what your branches will be like in five years’ time, and what devices you will be offering in your branches. Then you need to develop a strategy for these devices.”

In October 2013, the Ukraine’s PrivatBank announced the Topless ATM, a “black box” without a screen which it described as the world’s first con-tactless Android-based ATM. Because the Topless ATM is controlled by a customer’s smartphone and has no unnecessary components such as a keypad or card reader, it costs half of the price of a conventional ATM, PrivatBank says.

“In the branch of the future, employees’ role will change

from being providers of services with low added

value to consultants advising customers about the bank’s

products. Greeters will assist customers with their self-

service transactions.”— Carmine Evangelista,

Auriga’s chief technology officer

24ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

“We developed the Topless ATM by ruthlessly cutting off the completely unnecessary upper part of a typical ATM,” said Alexander Vityaz, vice chair-man of PrivatBank’s Board. “Now every customer has their own personal display, card reader and keyboard – a smartphone.”

Beyond silo channels architectureAccording to Auriga’s Smith, instead of saying that they have independent service silos and channels, each with their own functionality, and trying to integrate these channels at the back-end, banks need to step right out of the banking environment and look at their channels from the cus-tomer perspective.

“Banks need to ask themselves how customers want to interact with their bank, for example through smartphones and tablets, and what banking tasks they want to do,” Smith said. “Our WinWebServer (WWS) solution al-ready supports the omnichannel requirement to access any service through any channel, a feature that has been well proven by our customers and greatly appreciated by consumers.”

Fundamental changeThe process of moving to an omnichannel environment requires a funda-mental change in a bank’s channel architecture.

“Rather than investing in technology that perpetuates a fragmented ser-vices approach, banks should implement systems that facilitate their customers’ experience by sharing the same data and business rules across multiple channels and touch points,” Smith said.

“I’m seeing a number of banks accept that their existing IT infrastructure can’t adapt to the omnichannel world and seek partners with the ability to provide cross-channel solutions,” said Andrew Martin, CEO of U.K.-based Retail Banking Consulting Group.

Smith stressed the importance of banks educating staff and customers about the new self-service capabilities that they deploy in their branches and on their mobile channels.

“We’re seeing the first pilots of the new mobile-centric architecture,” said Smith. “Banks which are sitting on the sidelines and don’t get their new architecture in place will be left several years behind the leaders.”

25ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

WWSIn Auriga’s WWS omnichannel platform, the mobile is the front-end gateway to all other channels such as ATMs and Internet banking. Using the mobile device as the authentication method for Internet banking has a significant effect on reducing fraud.

“WWS converts every channel into a web environment,” Smith said. “It also allows customers to use their mobile device to personalize the options menu at their bank’s ATMs so they only see the transactions they are inter-ested in. They can also set up third-party ATM withdrawals from their bank accounts from their mobile device through WWS. This means that a parent can send their son or daughter a one-time authentication code enabling them to withdraw cash from the parent’s account without needing a card.”

“Banks need to have common imagery and navigation tools

across all their customer-activated devices along

with a high degree of user customization.”

— David Cavell, international retail banking consultant

© 2014 NETWORLD MEDIA GROUP 26

Case Studies of ATM and Branch InnovatorsThis chapter profiles leading innovators in ATM, digital banking and branch transformation in Europe, the U.K. and the U.S.

Bank of AmericaBank of America launched its teller assisted ATMs, which combine ATM self-service features with the human touch of a teller, in April 2013. The bank is installing these advanced ATMs in banking centers, drive-up and remote locations, offering video links to remote BofA call center staff during extended hours.

Bank of America launched its teller assisted ATMs, which combine ATM self-service features with the human touch of a teller, in April 2013. The bank is installing these advanced ATMs in banking centers, drive-up and remote locations, offering video links to remote BofA call center staff during extended hours.

Services offered by teller assist ATMs include:• Receive cash withdrawals in various denominations ($1, $5, $20 and $100).• Cash checks and receive exact change.• Deposit checks with cash back.• Make loan or credit card payments.• Access with a U.S. government-issued photo ID if ATM/debit card isn’t available.• Receive available balances for BofA accounts.• Print mini or full statements for checking and savings accounts.

As of July 2014, Teller Assist ATMs had been installed in eight markets, including Atlanta, Boston, Charlotte and Metro New York/New Jersey. In Q3 2014, BofA will roll out Teller Assist ATMs to six new markets including Los Angeles, Philadelphia and San Francisco.

CHAPTER 3

“ATM deployers failing to migrate to Windows XP after April 8, 2014,

run the risk of serious fines for non-PCI compliance” — Aravinda Korala, CEO of KAL

27ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

BranchesBofA opened the first of its new Express Banking Centers in Manhattan in August 2013. These centers offer a more flexible schedule than a full-service branch, while integrating self-service technology including Teller Assist ATMs and providing on-site associates to help customers with their financial needs.

A full-service BofA banking center is available generally within three miles from Express Banking centers.

“Associates at Express Banking centers aren’t behind teller stations,” BofA said. “They’re in the lobby, working with customers to answer questions and demonstrate how to use all the banking options Bank of America offers.”

Associates can demonstrate specific high-tech features on handheld tab-lets. They can also tell customers how to download the mobile banking app, and use a simulator to walk them through how to use new banking options, such as depositing checks via mobile phone. If customers have additional questions or need a problem resolved, they can meet with an associate in a private office.

By the end of 2013, five additional Express Banking Center locations had opened in Boston, Charlotte and the Metro New York City area. BofA plans to open a few additional locations in the second half of 2014, which are scheduled to be in both existing markets and new markets.

In January 2014, Finextra quoted BofA’s CFO Bruce Thompson as saying its branch banking network could drop below 5,000 by the end of 2014 as its mobile channels continue to take market share. According to Finextra, BofA’s branches fell to 5,151 in Q4 2013 from 5,478 a year earlier.

As at June 2014, BofA had 15 million active mobile banking users who ac-cess their accounts on a mobile device 165 million times per month.

In May 2014, BofA said it would roll out videoconferencing to 500 branches across the U.S. using Cisco Telepresence technology to enable customers to talk to bank product specialists. The rollout follows a two-year trial in 85 branches that saw 10,000 interactions take place over Cisco’s videoconfer-encing equipment.

BBVA

In March 2014, Spain’s BBVA created a dedicated division to manage the group’s digital banking services. The Digital Banking division’s priority is to accelerate the digital transformation of all BBVA’s businesses across all the

28ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

group’s geographical regions, and develop new digital businesses.

“BBVA is reinventing itself, converting an efficient and profitable analog bank of the 20th century into a digital house of the 21st century based on knowledge,” Francisco González, BBVA’s chairman, said. “If they want to compete with the digital companies disrupting financial business such as Google, Facebook and Amazon, banks can no longer hide behind regula-tory barriers.”

Banks must change rapidly if they don’t want to be ousted by new digital players, and use their main competitive advantage: information. Banking is a knowledge-based industry and therein lays its tremendous growth poten-tial, González said.

Because of its central role in BBVA’s digital transformation, Digital Banking is in charge of all the group’s commercial offerings, its multichannel strategy, its distribution model, and the design of commercial and operational processes.

Digital Banking is responsible for BBVA’s internal operations, such as Wizzo, as well as its startup investments through its financial technology venture capital arm BBVA Ventures, and acquisitions such as U.S. Internet- and mobile-only bank Simple, which BBVA bought in February 2014.

Wizzo is a Web mobile app for iOS and Android that allows customers to send money to each other by using their Wizzo username, email or mobile phone number. Customers can also use Wizzo to withdraw cash from ATMs without using cards by entering a code sent to their mobile phone.

BBVA CompassIn May 2014, BBVA Compass named Jeff Dennes as head of the new Digital Banking division at the Birmingham, Alabama-based subsidiary of BBVA. Dennes previously led digital innovation efforts at SunTrust Bank and Huntington Bank.

Since January 2014, BBVA Compass has been testing videoconferencing-based drive-through banking at three Houston locations, where customers can summon remote tellers via devices with high-definition screens that double as full-service ATMs.

Customers at the three locations can opt for full-service assistance from a teller; operate the units in self-service mode like an ATM or select an as-sisted mode, where the tellers can guide them through their transactions.

The remote tellers, based in the bank’s call center, are available during

“BBVA is reinventing itself, converting an efficient and

profitable analog bank of the 20th century into a digital house of the 21st century

based on knowledge.” — Francisco González, BBVA’s chairman

29ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

business hours and can be summoned at the touch of a button. The tellers also can identify customers as account holders without the use of ATM or debit cards by verifying the customer’s information.

BBVA is developing a high-tech prototype branch in San Antonio, Texas, which incorporates touchscreens, self-service kiosks, video links to remote bankers and futuristic “pods” for meetings with clients.

ABILIn Spain, BBVA has been rolling out multifunction ABIL ATMs that it de-signed with Wincor Nixdorf based on observations of how people behaved at ATMs in BBVA branches in Spain, Mexico and the U.S.

By the end of 2013, 100 ABIL ATMs had been installed in Spain. The ATMs offer several new functions compared with traditional ATMs, including:

• Account access using electronic IDs and passwords from bbva.es.• Ability to complete NFC transactions with contactless cards.• Account statements printed in DIN A4 format.

In addition, ABIL ATMs feature a large touchscreen and an intuitive user interface. BBVA intends to gradually establish this new self-service terminal as its standard ATM.

Nationwide Building SocietyThe U.K.’s Nationwide Building Society is rolling out in-branch video links that let customers talk to off-site mortgage consultants. By April 2014, the Nationwide Now project had reached around 60 branches, with more to come, Finextra reports.

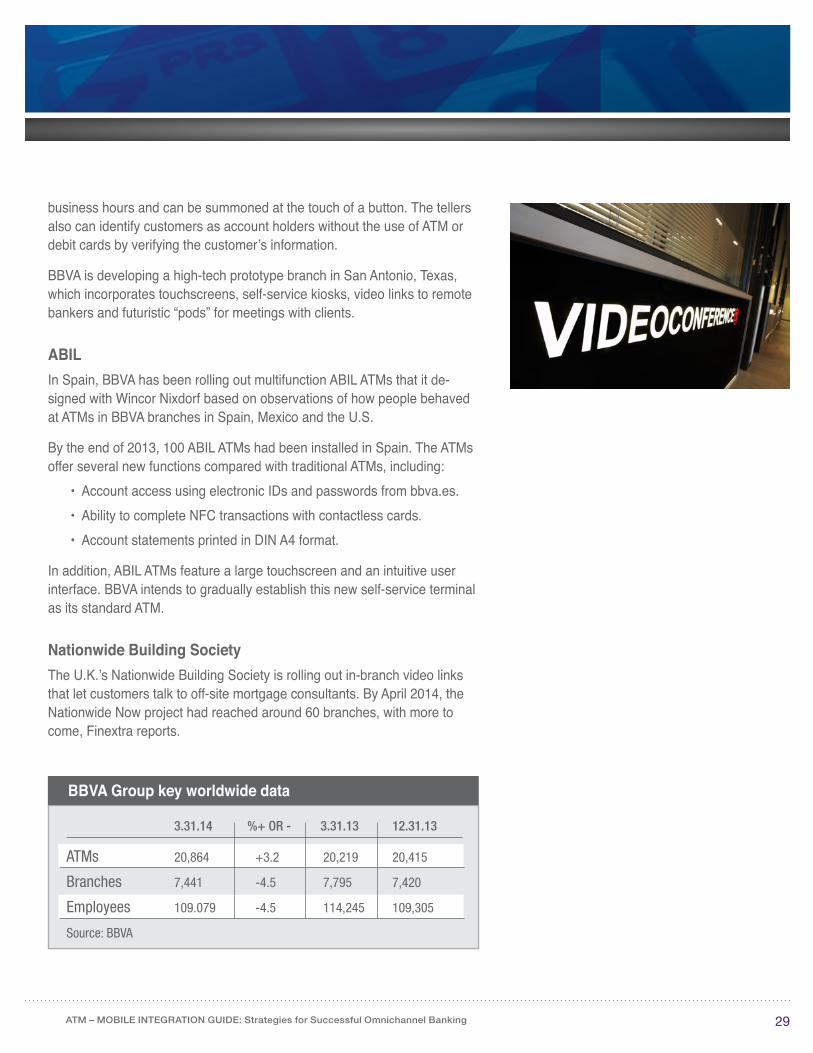

3.31.14 %+ OR - 3.31.13 12.31.13

ATMs 20,864 +3.2 20,219 20,415

Branches 7,441 -4.5 7,795 7,420

Employees 109.079 -4.5 114,245 109,305

Source: BBVA

BBVA Group key worldwide data

30ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

Instead of killing off traditional branches, digital technology could breathe new life into them, Nationwide’s chief executive Graham Beale told Finextra.

Beale expects that in the future customers will use Nationwide’s video service from their own homes via tablets and laptops. But meanwhile, the technology is helping to keep branches alive, as videoconferencing is more economically viable for remote branches with low customer numbers than deploying full-time mortgage consultants, he told Finextra.

“As part of its commitment to innovate and give customers a variety of ways to access their money, Nationwide has invested heavily in its ATM net-work,” Dean Spencer, program leader at Nationwide, told ATM Marketplace. “We’ve introduced a popular ‘favorites’ tool which enables customers to ac-cess their most common ATM transactions quicker and faster. Also, nearly 1,000 new ATMs have been deployed in our network, all of which have state-of-the-art touchscreen and security technology.”

Nationwide is looking at several ways to continue to innovate in its ATM net-work, including videoconferencing, cardless payments and mobile interac-tions, Spencer said.

In March 2014, Nationwide launched @asknationwide, becoming the first U.K. branch-based FI to offer its customers 24/7 Twitter coverage. @askna-tionwide answers customers’ questions, as well as providing them with customer service information and support, any time of day or night.

Royal Bank of ScotlandIn June 2014, Royal Bank of Scotland and its National Westminster Bank subsidiary announced plans to spend £1 billion ($1.71 billion) over three years to rebuild their consumer and small business banking operations, with investment in digital channels as the main focus.

Customer service improvements planned by the RBS Group include:

• Mobile banking that allows customers to view and amend regular pay-ments on mobile devices as well as online.

• Online banking that is more intuitive and allows content to be tailored to the individual.

• Improvements to more than 400 branches, including the addition of iPads for online banking access by customers and Wi-Fi that lets them use their own devices in-branch.

31ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

• Almost 100 new ATM locations across the U.K. to increase cash ac-cess, and almost 600 more cash and deposit machines (CDMs) in branches to accept checks, cash and coins.

• Improved systems will allow staff to see all the interactions a customer has with RBS, to better know and advise them.

The investment is driven by a dramatic change in customer behavior, RBS said, which includes a 200 percent increase in customer use of online and mobile technology.

Les Mattheson, RBS’s CEO of Personal and Business Banking, said in an investor presentation that 40 percent of the bank’s transactions now go through its mobile channel.

“In our branch network, the number of transactions fell by 30 percent be-tween 2010 and 2013, and we expect that trend to continue,” he said.

Customer recommendations“We’re working hard to ensure we offer informed product recommendations to customers,” Mattheson said. “What that means is using the data that we hold across the range of products and relationships we have with custom-ers to understand what it is they really need and when they might need it.”

Mattheson gave the example that, if a customer contacts the bank, whether it’s through a branch, a landline call or a mobile phone, representatives will be able to talk to them about a particular service need or a product need based on the data collected about the customer’s habits and behaviors.

“Collecting customer data tells us we should be talking to them about. We’ve been making investments in this area over the last four years and have a large customer database that helps us know and understand what it is customers need, sometimes before they do,” he said.

Mobile ATMRBS and NatWest’s Get Cash cardless ATM withdrawal service uses a smartphone app to generate a one-time six-digit PIN that is sent to the customer’s phone. The customer enters this code into one of the banking group’s ATMs and CDMs to withdraw cash.

According to RBS, more than 120,000 Get Cash transactions occur each month in the U.K.

32ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

“Get Cash is intended as an emergency cash withdrawal service for people who have left home without their cards, and has proved very successful,” said Retail Banking Consulting Group’s Martin.

RBS offers a service that allows customers to upload their ID documents such as drivers’ licenses for checking account opening by smartphone. More than 1,300 IDs uploaded via smartphone are verified by RBS each month for account-opening purposes.

St. George BankIn May 2014, Australia’s St. George Bank launched a trial of iBeacon technology in its branches, sending personalized information to customers’ iPhones when they enter a branch.

“Our customers’ needs are rapidly changing. They want

to bank day-to-day in the most convenient ways available.

We must respond to their needs and continue to improve on

the service we offer both online and on mobile.”

— Les Matheson, CEO of Personal and Business Banking at Royal Bank of Scotland

RBS and NatWest have:

• 6 million active online customers.• 3 million active mobile customers. • 280 million digital transactions processed per annum.• 3,700 ATMs.• 850 cash and deposit machines.• £25 billion ($42.86 billion) cash withdrawals from

ATMs/CDMs in 2013.• 10 personal banking call centers.• 3,300 U.K.-based personal banking call center staff,

excluding Web chat.• 30 million assisted, telephone transactions per annum,

excluding IVR.• 2,000 branches.• 16,300 personal and business banking staff.• £62 billion ($106.29 billion) cash and coin transactions in

branches per annum, including deposits and withdrawals over the counter, through CDMs and Business Quick Deposit cash deposits.

Source: Royal Bank of Scotland. These figures are for RBS and Nat-West’s mainland U.K. business and exclude Ulster Bank.

33ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

iBeacons use Bluetooth low energy-based proximity sensing to communi-cate with Apple iOS-based devices.

St. George has installed iBeacons in three branches in Sydney, enabling bank-owned iPads to send welcome messages and tailored information di-rectly to customers’ iPhones. Recipients can reply to the message or cancel the interaction.

St. George said the trial aims to obtain customer feedback to ensure iBea-con technology “genuinely meets their needs” and improves their banking experience. Once the trial is completed, St. George will plan how to roll out iBeacons across its branch network.

George Frazis, St. George Banking Group’s CEO, said the launch of the new technology forms part of an increased focus on delivering an innova-tive and customer-centric in-branch experience.

“The future of business will be in the ability to anticipate customers’ needs, understand what matters to them and act on that knowledge to surprise and delight them,” he said.

Frazis said the investment in iBeacon will help the bank achieve that — and it has the potential to dramatically change the service experience in Australian banking. The iBeacon trial forms part of a broader investment in St. George’s retail branches that will see more digital technology and increased staff ex-pertise to make banking simpler, easier and faster for customers, he said.

Wells FargoIn April 2013, Wells Fargo announced a new branch concept, the neighbor-hood bank format.

“The concept is designed to deliver the on-site banking experience Wells Fargo customers expect, but in a smaller format allowing the company to offer store locations with personalized service, in settings not suitable for its larger stores,” the bank said.

The new store format is 1,000 square feet and offers paperless, secure workflow as well as wireless technology that helps staff provide faster service, and new large-screen ATMs. The first store using the new design opened in Washington D.C.’s NoMa neighborhood in April 2013. A tradi-tional Wells Fargo branch’s size is 3,000–4,000 square feet.

34ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

“With this new store concept, we’ll be able to offer person-to-person sales and service along with leading banking technology in settings that previous-ly would have discouraged us from building a store,” said Jonathan Velline, head of ATM banking and store strategy at Wells Fargo. “Stores are central to our strategy of providing excellent service and meeting our customers’ financial needs.”

Velline said that, in designing the new store format, Wells Fargo paid atten-tion to creating areas within the smaller layout where team members and customers can conduct business and have important financial conversa-tions, including private meetings.

The new store design offers technology found in traditional Wells Far-go stores, such as ATM software that anticipates a customer’s preferred transactions, image deposits, instant issue debit cards and email and text receipts. It also features wireless tablets that team members use to serve customers and sell products to them.

Each neighborhood store provides a free wireless hotspot for customers to use. After hours, the store transitions into a smaller lobby format, providing customers with 24/7 access to several ATMs that dispense $1, $5 and $100 bills in addition to the $20 bills a typical ATM offers.

In February 2013, Wells Fargo started rolling out an ATM interface that offers personalization features. Highlights include “favorites” that appear in the color green based on the customer’s ATM usage, as well as customized screens based on the customer’s preferences. A “Balance Dashboard” features bal-ances at-a-glance, if the customer chooses, for their most used accounts.

ATM Cash Tracker, a tool to help customers manage their finances, now automatically appears on the main Wells Fargo ATM screen. This feature allows customers to visually track their monthly Wells Fargo ATM withdraw-als. Customers can also set a monthly withdrawal target and can view details about how much they withdrew the prior month and their average over the past 12 months.

© 2014 NETWORLD MEDIA GROUP 35

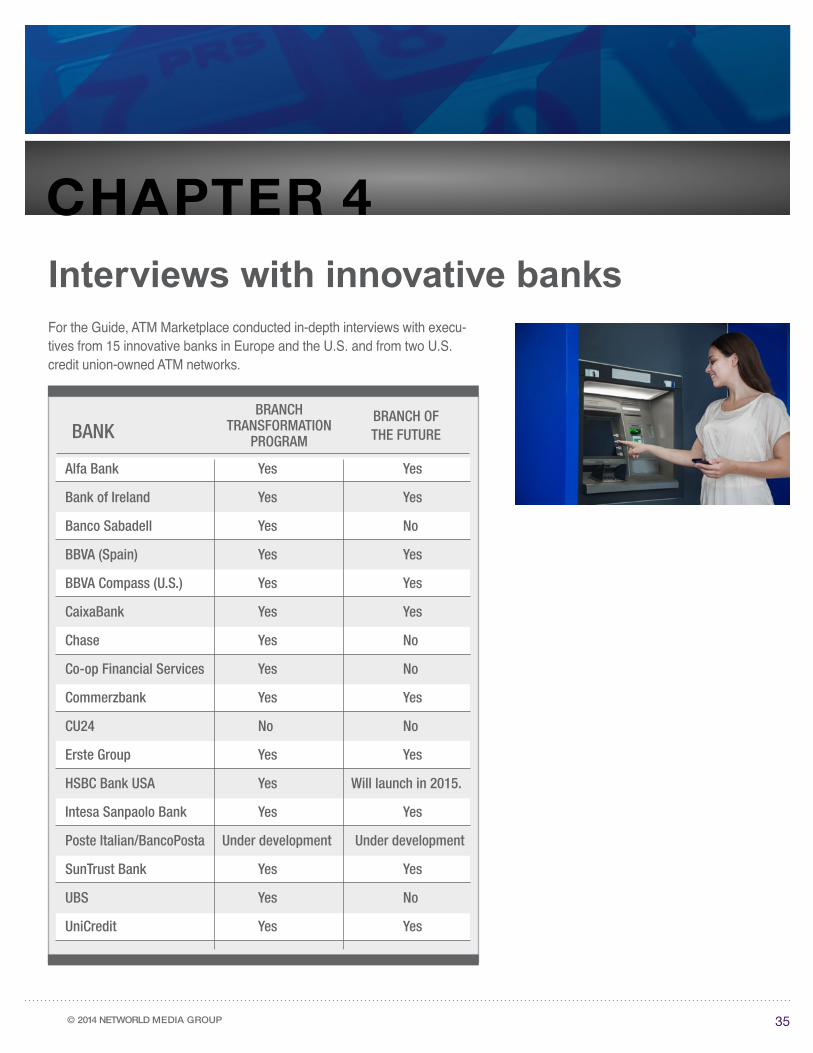

For the Guide, ATM Marketplace conducted in-depth interviews with execu-tives from 15 innovative banks in Europe and the U.S. and from two U.S. credit union-owned ATM networks.

Interviews with innovative banks

CHAPTER 4

BANKBRANCH

TRANSFORMATION PROGRAM

BRANCH OF THE FUTURE

Alfa Bank Yes Yes

Bank of Ireland Yes Yes

Banco Sabadell Yes No

BBVA (Spain) Yes Yes

BBVA Compass (U.S.) Yes Yes

CaixaBank Yes Yes

Chase Yes No

Co-op Financial Services Yes No

Commerzbank Yes Yes

CU24 No No

Erste Group Yes Yes

HSBC Bank USA Yes Will launch in 2015.

Intesa Sanpaolo Bank Yes Yes

Poste Italian/BancoPosta Under development Under development

SunTrust Bank Yes Yes

UBS Yes No

UniCredit Yes Yes

36ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

The majority of the banks interviewed have a branch transformation program and a branch of the future.transactions and apply for products.

Alfa BankMoscow-based Alfa Bank’s ATM network includes 3,100 ATMs that it owns and 12,000 ATMs owned by its partner banks.

“The role of ATMs in our branches will become more important in the next few years because of the opportunity to add new functions and focus on cost effectiveness,” said Maxim Dareshin, head of Alfa Bank’s self-service systems development department.

For Dareshin, it is important for banks to offer the ability to videoconference with bank customer service staff or subject experts at ATMs and to offer card-less ATM transactions using mobile devices.

“The benefit of ATM-mobile integration will be faster transaction times and new user interface opportunities,” Dareshin said. “But integrating ATMs with smartphones will be very challenging.”

ATM-mobile integration services currently offered by Alfa Bank comprise:• Managing ATM or debit card accounts from mobile devices.• Locating ATMs using mobile devices.• Offering a real-time view on a mobile device of services

on the selected ATM.

In addition, Alfa Bank customers can use their smartphones as an authen-tication method for logging into Internet banking. Although Alfa Bank offers mobile P2P transfer services, it doesn’t allow recipients of mobile transfers to withdraw cash from ATMs.

Within the next two to three years, Alfa Bank plans to offer cardless ATM transactions involving NFC-enabled mobile devices and cardless transac-tions using one-time authentication codes.

Dareshin said that personal contact is still important between bank staff and customers who use self-service technology.

“Many people still need to be helped while using self-service devices, or they have additional questions,” he said. “For example, a customer knows how to repay his loan, but he’s forgotten the amount he needs to pay. We plan to offer videoconferencing with customer service staff or product experts at our

“The benefit of ATM-mobile integration will be faster

transaction times and new user interface opportunities.”

— Maxim Dareshin, head of Alfa Bank’s self-service systems development department

37ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

ATMs and self-service banking terminals in the next two to three years.”

Alfa Bank provides bank-owned iPads for use by customers in its branches for carrying out transactions, looking up products or making appointments with staff.

Banco Sabadell“We see in-branch ATMs evolving to new models that enable customers to carry out self-service transactions that are currently performed by branch staff,” said Christian Raset, director of management and design of Sabadell, Spain-based Banco Sabadell’s digital platforms. “We also think ATMs must become integrated with mobile services, such as cardless NFC transactions and pre-staging ATM withdrawals from cellphones.”

Raset said the mobile channel will be the most important channel for expand-ing Sabadell’s relationship with its clients over the next few years. “Mobile will also be key to increasing the services offered by our ATMs,” he said.

For Sabadell, multichannel integration is a priority.

“Our plan for the next three years has a clear focus on the digital transforma-tion of the bank and of the services we offer our clients,” Raset said. “En-abling our clients to carry out transactions on multiple channels will lead to greater customer satisfaction and a closer relationship with Sabadell.”

In 2012, Sabadell launched its Instant Money cardless cash withdrawal service, which allows customers to withdraw cash from its ATMs using a one-time PIN sent to their mobile phones.

“Spanish banks are among the most advanced in Europe in terms of the services they offer at their ATMs,” said Retail Banking Consulting Group’s Martin. “Sabadell has seen huge adoption of its Instant Money Service.”

Raset said that in the next few years Sabadell will carry out several pilots integrating its different channels such as mobile and ATMs.

“We plan to offer NFC cardless ATM withdrawals and QR code-based mobile ATM withdrawals, and will offer customers a real-time view on their cell-phones of services offered on our ATMs,” he said. “We are currently carrying out pilots of remote customer service applications such as videoconferenc-ing, and we plan to provide branch staff with tablets so they can present product offers to clients.”

“Enabling our clients to carry out transactions

on multiple channels will lead to greater customer satisfaction and a closer

relationship with Sabadell.” — Christian Raset, director of management

and design of Sabadell

38ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

Bank of Ireland

“Over the next few years, we see our branches evolving from a staff-assisted service model to customer self-service, particularly for cash and deposit services,” said Garvan Callan, head of Direct Channel Banking at Dublin, Ireland-based Bank of Ireland. “We also want to reduce the cost of cash han-dling in our branch network through local cash recycling. Our plan is to train our staff to direct and guide customers through self-service options at ATMs, and we will also be deploying enhanced product offers and product cross-selling opportunities through ATMs.”

Videoconferencing at ATMs, ATM user-interface personalization and cardless ATM transactions are among the enhanced customer service options that BoI is evaluating.

“We see mobile devices as being core to our omnichannel strategy,” Callan said. “Integrating our mobile and ATM channels will enable us to offer a con-sistent user experience and integrated product promotion across all channels and touch points, contributing to our strategic objective to increase product sales through our digital channels.”

BBVA“ATMs will have two important roles in the future,” said Manuel Crespo, Madrid, Spain-based BBVA’s head of physical channels technology. “Firstly, they will absorb the majority of low-value transactions, allowing staff to per-form higher-value tasks for customers. Secondly, ATMs will serve as the link between digital and physical banking channels.”

Crespo believes it will be important to offer videoconferencing at ATMs, per-sonalization of ATM interfaces from mobile devices, cardless ATM transac-tions, cash recycling at ATMs and ATM access via biometrics.

“Biometrics will provide an alternative to card and PIN-based transactions, allowing non-card customers to access the ATM network,” he said.

For Crespo, the best cross-channel strategy is to offer the same user experience across all channels. Processes must be designed and imple-mented in the same way, as opposed to having different processes for each channel. This will allow customers to jump seamlessly from one channel to another, and initiate transactions on a mobile device which they complete on another channel.

“Biometrics will provide an alternative to card and

PIN-based transactions, allowing non-card

customers to access the ATM network.”

— Manuel Crespo, BBVA’s head of physical channels technology

39ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

“Since mobile devices play such an important role in our lives, they should be considered as the main method for authenticating payments and customer service requests,” he said.

BBVA’s ATMs offer the following facilities:• Customizable menus.• Personalized product advertising and offers.• The ability to set up alerts based on specific rules.

Currently, BBVA offers the following mobile integration services at its ATMs:• Cardless ATM transactions involving NFC-enabled mobile devices.• Cardless ATM transactions using a one-time authentication code.• Locating the nearest ATM using mobile devices.• Withdrawals of cash received via mobile P2P fund transfers.

BBVA plans to roll out cardless ATM transactions from mobile wallets using QR codes by the end of 2014, and it is developing the following services:

• Allowing a customer to use their mobile device to customize their own ATM menu.

• Offering a real-time view on a mobile device of services on the selected ATM.

Based on its U.S. subsidiary BBVA Compass’ drive-thru ATM videoconferenc-ing services, BBVA is working on a proof of concept for videoconferencing at its Spanish ATMs, Crespo said.

Following the 2013 launch of assisted self-service banking terminals at its flagship branch of the future in Spain, BBVA plans to roll out assisted self-service technology in its other branches.

BBVA Compass“Offering videoconferencing technology is essential for connecting ATM users with tellers when assistance is needed,” said Jill Hunt, director of channel operations and customer advocacy at BBVA Compass. “Doing so will also allow bank teams to answer product questions and potentially generate new accounts.”

ATM-mobile integration can help strengthen customer experiences, said Hunt. “For example, customers who’ve forgotten their ATM/debit cards could

40ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

potentially use a mobile device to initiate a transaction to be completed at an ATM,” she said. “On-the-go customers can also use a mobile app to locate nearby BBVA Compass ATMs.”

Within the next two to three years, BBVA Compass plans to offer:• Cardless ATM transactions from mobile wallets using QR codes.• Cardless ATM transactions using a one-time authentication code.• Managing ATM/debit card accounts from mobile devices.

Multichannel integration is a major priority for BBVA Compass as customers expect to have seamless experiences, regardless of the channel they use, Hunt said. In addition, multichannel integration opens the door to new ways of banking.

CaixaBankBarcelona, Spain-based CaixaBank has deployed more than 1,000 Punt Groc (i.e., yellow point) advanced multifunction ATMs. Its total ATM fleet consists of 10,000 ATMs.

Punt Groc ATMs offer cash withdrawals via contactless cards and have a double screen design enabling products and services to be advertised on one screen while the other is used for transactions. More than 200 differ-ent transaction types are available at Punt Groc ATMs, including pre-agreed loans, virtual cards and withdrawing funds received via mobile P2P transfers.

CaixaBank customers can personalize the Punt Groc ATM initial services menu and view personalized product offers. The “frequent operations” option showing a customer’s most-used transactions can be configured via ATMs or through CaixaBank’s online banking channel.

Low added value transactions“ATMs must become the basis for cash management in branches,” said a CaixaBank spokesperson. “Incorporating a cash recycling function in our ATMs during 2014 is a step in this direction. In addition, ATMs need to take over most of the low added-value transactions that are still carried out at branches, while also offering the sale of simple financial products.”

Mobile is a central part of CaixaBank’s multichannel strategy due to the ubiq-uity of mobile devices among its customers.

41ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

For CaixaBank, it is important to offer the following technologies at ATMs:• Allowing customers to manage their ATM interaction and personalize

their ATM interface from mobile devices.• Offering cardless ATM transactions using mobile devices.• Biometric authentication.

CaixaBank currently offers the following ATM-mobile integration services:• Cardless ATM transactions involving NFC-enabled mobile devices.• Cardless ATM transactions using a one-time authentication code.• Managing ATM/debit card accounts from mobile devices.• Locating the nearest ATM using mobile devices.• Offering a real-time view on a mobile device of services on the

selected ATM.

“We’re currently developing our cross-channel integration strategy so that any transaction can be prepared and/or launched through any channel and completed in any other,” the spokesperson said. “However, we don’t view the ATM as the most convenient channel for videoconferencing.”

In November 2013, CaixaBank opened a branch of the future in Barcelona that is designed to resemble an Apple store and offers advanced ATMs and tablets. The branch, called A Diagonal, has a 1,000 square metre surface area, with no physical barriers between customers and employees.

ChaseChase, the U.S. retail banking arm of JPMorgan Chase, is re-envisioning its branch model along the lines of the Apple stores.

Chase says its new branches are designed to meet the needs of today’s customer:

• More self-service technology up front. • Employees moving around — often with a tablet in hand — to greet

customers, help with a quick need or bring a customer to a high-top table with a computer for further assistance.

• Fewer teller booths with shorter lines for those who still need the assis-tance of a teller.

“While our customers are rapidly adopting our

self-service technologies, branches are still a critical

part of their banking experience.”

— Michael Fusco, Chase spokesperson

42ATM – MOBILE INTEGRATION GUIDE: Strategies for Successful Omnichannel Banking

• Significantly more private offices for customers needing a specialist in small business, mortgage or retirement planning.