Embed Size (px)

Citation preview

Asset Prices and the Demand for Asset ValuesAuthor(s): M. C. UrquhartSource: The Canadian Journal of Economics / Revue canadienne d'Economique, Vol. 2, No. 4(Nov., 1969), pp. 477-491Published by: Wiley on behalf of the Canadian Economics AssociationStable URL: http://www.jstor.org/stable/133837 .

Accessed: 17/06/2014 16:20

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Wiley and Canadian Economics Association are collaborating with JSTOR to digitize, preserve and extendaccess to The Canadian Journal of Economics / Revue canadienne d'Economique.

http://www.jstor.org

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

ASSET PRICES AND THE DEMAND FOR ASSET VALUES*

M. C. URQUHART Queen's University

Les prix et la demande d'actifs. Les questions traitees ici concernent la demande globale d'actifs reels dans le secteur prive d'une economie et le r6le de leurs prix dans le meca- nisme d'equilibre general. On postule le plein-emploi, un etat stationnaire et l'absence d'incertitude.

Le modele initial comporte les caracteristiques suivantes : l'absence d'6pargne nette, un seul produit dont il est impossible de faire l'entreposage, deux inputs, et un niveau donne de production. Les deux inputs sont le travail et le sol. Le sol est le seul actif. II est detenu par les individus pour leur permettre d'obtenir un flux de consommation different de leur flux de revenu. Le critere de choix en consommation est la maximation du bien-etre de toute l'existence. Pour toute periode, on observe une distribution de la population entre les diffe- rentes etapes de l'existence. Les facteurs d6terminants de la consommation, et done de l'epargne nette, sont alors les suivants : le revenu courant, les revenus attendus dans les periodes subsequentes, la valeur des actifs detenus, le taux d'interet et les gouts. Le prix de I'actif est une donnee pour les individus. Mais il est determine par le mecanisme d'equilibre general. C'est un element central de ce mecanisme.

Dans ce monde stationnaire caracterise par l'absence d'incertitude, les taux d'interet reel ne sont relies qu'aux prix des actifs. L'incidence sur la consommation courante du niveau du taux d'interet, en lui-meme, met en cause le resultat net des effets de revenu et de substitution. On sait en effet qu'ils agissent en sens contraires sur la consommation. Par opposition aux taux d'interet bas, les taux d'interet eleves ont un effet de substitution qui conduit a une diminution de la consommation courante. II s'additionne a un effet semblable rattache a la chute de la valeur des actifs causee par la hausse des taux d'interet. L'effet de revenu est en sens contraire des deux precedents.

Une situation ou L'effet de substitution est plus important que l'effet de revenu concourt a la stabilit6 du systeme. La situation inverse conduit a son instabilite.

L'auteur fait un certain nombre de developpements et d'applications a partir de ce modele.

In my presidential address I should have liked to continue the pattern set by my immediate predecessors. The last two presidential addresses of our parent organization, the old Canadian Political Science Association, and the first address of the new Canadian Economics Association were respectively anal- yses, in a quantitative setting, of the state of the social sciences in Canada and of Canada's economic policies toward the less-developed countries. Since these addresses were given, major reappraisals of "science" policy (including the social sciences) have been launched, by official or semi-official bodies, and our programme of foreign aid is being reconsidered actively. For these reappraisals, the work of the foregoing authors both in their presidential addresses and in other ways has been most timely. I am pleased to have the opportunity to pay tribute to the work of those three persons who were, in effect, the founders of our Association. And I am greatly honoured that one of them, the first Presi- dent of the Canadian Economics Association, is chairman tonight.

A heavy commitment to another project, which has lasted longer than I had originally anticipated, has made impossible any great amount of quantitative work on my part for this occasion. My address therefore is in different vein. *Presidential address to the Meetings of the Canadian Economics Association, June 1969.

Canadian Journal of Economics/Revue canadienne d'Economique, II, no. 4 November/novembre 1969. Printed in Canada/Imprime au Canada.

I I ? -- '' IltlCIIC 113 r Ir I r I - '

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

I examine, from a somewhat different viewpoint than that which is usually taken, the determinants, in the private sector of the economy, of the aggregate demand for assets and of the prices of assets and their bearing on interest rate determination in a full employment economy. I shall define the term "assets" more fully later but, for the time being, I mean by an asset some physical property or some net claim against the state that has a net value as measured in terms of consumer goods.

The asset values, asset prices, and factor service prices with which I deal are measured in consumer goods and the interest rates are real rates. Interest rates are related to asset prices since the real rate of interest, in its objective manifestation, is a ratio between the net value of the productive services or other periodic income yielded by an asset and the price of the asset itself.

My paper falls into two parts. First I develop, through use of a simple example, an illustration of the elements that affect the demand for asset values. In this part the main emphasis is on the equilibrating roles of the real price of assets and of real asset values in the determination of the equilibrium of the

economy. This approach permits one to point up certain historical develop- ments and certain features of the economy that raise policy problems. The second part of the paper deals with a few examples of the latter.

Until recently, relatively little attention has been given to the aggregate demand for assets, and for a very simple reason. Typically, neo-classical econo- mics, in explaining the working of a private enterprise economy and, among other things, the rate of interest, worked with an analytical system in which there were essentially five major sets of markets. They were: (i) the market for consumer goods; (ii) the market for newly-produced capital goods; (iii) the market for services of the factors of production; (iv) the market for one special asset, money; (v) the market for other assets.

In an explanation of the levels of production and disposition of commodities, of the allocation of factor services in production, of the prices both of com- modities and of factor services, and of the general level of prices, the condi- tions that led to equilibrium in the first four markets were developed. By Walras's law, if the first four markets were in equilibrium the fifth market, the market for non-monetary assets, must also be in overall equilibrium. Conse- quently little was said (or written) about the conditions of overall demand and supply in the fifth or asset market, though a good deal was written about some sub-markets such as, for example, the market for bonds.

Some aspects of the asset market were introduced into the above system, however, in an explanation of the determination of interest rates. The versions of determination of the latter varied but one commonly accepted (non- monetary) version was that the interest rate was determined in the market for newly-produced capital goods and was the main equilibrating force in that market. The prices of the services of newly-produced (and already existing) capital goods were determined in the factor markets. The prices of the capital goods themselves were determined by costs of production of newly produced capital goods at the margin of their production. Investment was carried to the point at which (full-employment) saving equalled investment. In the Fisher version, saving was determined by the desire of individuals or households to spread consumption through time in order to maximize utility over time. The

478 M. C. URQUHART

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

Asset Prices and Values

existing stock of capital, measured in some real sense, let us say as a number of machines, was an explanatory variable in the equations of the investment market since its quantity helped determine the prices of the services of capital goods through its effects on the marginal efficiency of investment. The prices of already existing assets were equal to the capitalized values of their annual services at rates of interest determined in the equilibrium of the market for

saving and investment (lending and borrowing). Money rates of interest in the shortrun were affected by monetary forces, but not in the long-term full-employment static equilibrium.

In the foregoing, the nature of the aggregate real demand for assets, implied (or assumed) from the equilibrium of the other markets, was such as to take all existing assets off the market plus the additions to capital goods at prices that would clear the investment market. Indeed, of course, the fact that there had been net saving in prior periods implied that previously produced capital goods had been purchased at their production costs in these prior periods, since the only way that net saving for a whole economy could occur was by the channelling of the net saving into net acquisition of capital goods. Pre-

sumably, if net saving continued, the members of the economy wished still to hold the old capital goods and such other net assets as had been inherited from the past, as well as to add those that were newly produced. But the full

implications of the equilibrium of the first four markets for that of the fifth, the asset market, were not worked out.

Then came Keynes with his postulation of a long term underemployment equilibrium, which was a consequence of the nature of marginal propensities to consume out of income, of interest-inelastic marginal efficiency of invest- ment schedules, of a critical role for money in affecting interest rates, and of a minimum boundary on interest rates (some would add, though not Keynes himself, I believe, rigid prices). To deal with the Keynesian dilemma, econo- mists then introduced the total real value of assets (or a part of assets) as an

explanatory variable in the equations of the market for consumer goods. For if a Keynesian unemployment equilibrium existed, it could be eliminated by a fall in money prices which increased the real value of money and fixed

money-sum securities (bonds) and thus caused a rise in real consumption relative to a given real income. When the value of assets measured in terms of consumer goods was introduced into the consumption equation, the implica- tion for the demand for assets which followed from the equilibrium of the other markets became more apparent than hitherto. A considerable amount of work has been done now, on the nature of the demand for assets by Marschak and Makower, Metzler, Tobin, Turvey, and Chase to mention only a few

examples. And there are strong implications for the demand for assets in the work of Friedman, Modigliani and Brumberg and others on the nature of

consumption functions. It is to an explicit examination of the nature of the

aggregate demand for all assets in terms of consumer goods in the private sector of the economy, which I shall call henceforth the demand for asset values, and its implications for asset prices and the rate of interest that I now turn.1

lIt is redundant perhaps to speak of asset values but usage has it now that the term "asset" sometimes implies a physical property.

479

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

M. C. URQUHART

I now should define "assets" more specifically. The assets of which I speak are privately-held properties on which the economic system has created an

exchangeable value for consumer goods. The asset values are net values in that, for most of our deliberations, they net out gross private asset values

against gross private debt. Since they are net assets they include only items such as: natural resources (farm land, sites for buildings and for other uses, mineral resources and the like) and the net stock of real capital or equities in the foregoing; the net public debt held in the private sector; that part of the

privately-held money stock which is a liability of the public sector of the

economy; and net international claims. These properties have been accepted by individuals as assets because they yield either a tangible income or a

utility. I shall follow usage in calling properties against which there are no debts for the private sector as a whole "outside" assets and properties against which there are debts for the private sector as a whole "inside" assets.

My general assumptions within which the remainder of the paper is done follow. First, I deal mainly with static systems and a world of certainty. Second, my attention is focused on individual behaviour and the general equilibrium in the private sector of the economy, with only limited reference to certain features of the public sector, which are taken as data. Third, I assume that liabilities of the public sector in the form of its public debt or of the money it has issued are not regarded by individuals or households as their own private liabilities in their role as members of the state. Fourth, I assume a full employment economy and leave aside the much more difficult question of an economy with unemployment, the type of economy with which Turvey and Tobin have worked.

Since I should like to proceed by building on the foundations of individual or household behaviour I wish to develop an example of a very simple economy which will illustrate these foundations without it being necessary to go into their formal derivation. It is easiest to proceed, in the first instance, by abstraction from the production (and consumption) of capital goods and from the role of money. Therefore, to illustrate the role of asset values and asset prices, in the general equilibrium, in my initial example, I have delib- erately used what I call land as my sole asset. It is an outside asset.

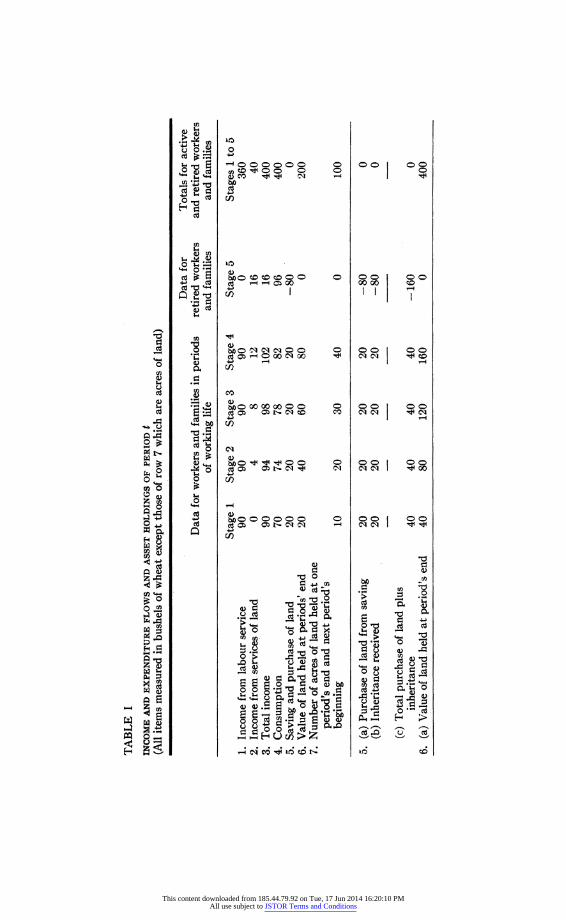

I postulate then a very simple economy, exemplified by Table I, in which: (1) there is produced only one simple non-storable consumer product, let us

say soft wheat measured in bushels; (2) there are two inputs, a fixed amount of labour which does not need to be further specified, and land of which there is 100 acres. Both land and labour are fully employed; (3) with full employment the total amount of wheat produced is 400 bushels; (4) of this product, 360 bushels, determined by a Cobb-Douglas production function under competitive conditions, is received by labour and 40 bushels is received by the owners of the land; (5) in any particular period of time t, the inhabi- tants of the economy are dispersed through five stages of life of which the first four are working stages and the fifth is the stage of retirement. For con- venience, let us assume that each stage of life is equal in length to the time- period t and that there is a stationary state balance in the numbers in each stage of life; (6) there is no money, the prices of the services of labour and

480

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

TABLE I

INCOME AND EXPENDITURE FLOWS AND ASSET HOLDINGS OF PERIOD t (All items measured in bushels of wheat except those of row 7 which are acres of land)

Data for Totals for active Data for workers and families in periods retired workers and retired workers

of working life and families and families

Stage 1 Stage 2 Stage 3 Stage 4 Stage 5 Stages 1 to 5 1. Income from labour service 90 90 90 90 0 360 2. Income from services of land 0 4 8 12 16 40 3. Total income 90 94 98 102 16 400 4. Consumption 70 74 78 82 96 400 5. Saving and purchase of land 20 20 20 20 -80 0 6. Value of land held at periods' end 20 40 60 80 0 200 7. Number of acres of land held at one

period's end and next period's beginning 10 20 30 40 0 100

5. (a) Purchase of land from saving 20 20 20 20 -80 0 (b) Inheritance received 20 20 20 20 -80 0

(c) Total purchase of land plus inheritance 40 40 40 40 -160 0

6. (a) Value of land held at period's end 40 80 120 160 0 400

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

M. C. URQUHART

land and the outright purchase price of land itself are measured in bushels of wheat; (7) the labour income is earned in equal amounts by each group in the first four stages of life; (8) the only way in which savings can be held for use in retirement is through purchase of land during one's working life for sale to obtain consumer goods in retirement; (9) those who hold land receive the income of that land which they owned at the beginning of the particular stage in which they live.

I assume that the individuals within the economy try to distribute their

expenditure on consumer commodities through the different stages of their life to maximize their satisfaction over their lifetime; in so doing they will

satisfy the usual marginal conditions for maximization. In this case, the maxi- mization means saving and buying assets in the working stages of life and

selling assets and dissaving in the stage of retirement.2 The determination of asset values (land prices) and of the rate of interest

in the above situation, where all of production is currently consumed, is illus- trated by the data of the first seven lines of Table I, which reflect the circum- stances of a particular (let us say, representative) period of time t. In period t, each person or household belongs in one of the five stages of a lifetime. Thus, the data of each of the stages of life in Table I present a cross section of the circumstances of each group in the time-period t; the last column reflects the circumstances of those in all stages of life in time-period t. In the table all the quantities except those of row 7 are in bushels of wheat. I should add that the contours of the entries for the five stages of life are most important. Behind them lie the individual or family behaviour that provides the basis of the remainder of the paper.

In this economy, labour income (line 1) is equally divided among those in the four working stages of life; the retired have no such income. Income from the services of land is distributed as in line 2 in a manner described below. Total income (line 3) is merely the sum of labour and land income.

The consumption decisions, in period t, of those in each stage of life are

dependent on their current income, their expected future income, the consumer

goods (wheat) value of the assets they have acquired already and the rate of interest. Given these elements, consumers plan to spread consumption through the remainder of their lifetime in a way to maximize lifetime satisfaction. Whilst the data for the table, for those in each stage of life, reflect the posi- tions, in time-period t, of those who fall within each stage, let us also assume that the data for any stage reflect the expectations, for the remaining periods of their lives, of those in that stage or in an earlier stage. Consumption (line 4) and its counterpart, saving (line 5), represent the results of the summation

2The maximizing behaviour is of the usual kind. The decision-making unit acts to maximize U = U(Cl, C2 ... Cn)

subject to the constraint n n

Ao + E y./(l +- r)8 = E c,/(l - r)*, (s 1... n) s=lr s=l

where U is lifetime utility, c8 is planned consumption in stage s of life, Ao is initial asset values, Ya is labour income in stage s of life, and r is the rate of interest; Cn+ maybe added for asset values to be passed on to heirs. Then cl = f ( Y ... Yn A0, r). Current consumption is a function of initial asset values, present and expected future income and the rate of interest.

482

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

Asset Prices and Values

of decisions on the part of individuals or households. Those in the working stages of life save some part of their income which is entirely consumed during retirement.

Since land is the only asset available as a repository for savings, the amounts saved in each of the working stages of life are used to purchase land which can be sold in retirement to permit consumption by the retired. The value of the net purchases of land by the active workers (savers) in period t is thus

equal to their saving and the value of net sales of land by the retired (dis- savers) is equal to dissaving. Eighty bushels worth of land is bought by the savers from the dissavers. A wheat price becomes established on land which

equates the saving and purchases of land by the active workers with the dis-

saving and sale of land by the retired; the price of land is the equilibrating element in the system.

The land purchased in each stage of working life will have accumulated as shown in lines 6 and 7 which give, respectively, the value of land measured in wheat and the number of acres of land held by those in each stage of life at the end of that stage. In passing, we note that it is this distribution of hold-

ings of land among those in various stages of life which determines the distri- bution of income from the services of land amongst those in the various stages (line 2). The aggregate demand for the stock of land values is determined by the desire to hold a certain value of land at the end of each stage of life. The

price of land that makes net saving and net purchases of land by active workers in time-period t equal to net dissaving and sales of land by the retired, also makes the aggregate demand for all land equal to the aggregate supply which, of course, exemplifies Walras's law.

Since there are 100 acres of land and the equilibrium total value of land is 200 bushels, the price (capital value) of an acre of land is two bushels. The value of the services of land per period is 40 bushels in total or two-fifths of a bushel per acre. Accordingly, the rate of interest is 20 per cent. It is assumed, in the above example, that the maximizing pattern of consumption and saving is consistent with this 20 per cent of interest.

It is clear from the above that the real values placed on assets in any period affect the consumption of that period directly quite apart from their effects on the rate of interest. In our example, the consumption of the retired depends almost entirely on asset values. The consumption of others in later stages of

working life also will be affected by the values of the assets they have accumu- lated to those stages.

It is not clear what effect the level of thie interest rate will have on the desired contour of consumer expenditure through stages of life. The interest rate is a datum for individuals of course. High as compared to low interest rates have two effects which will work in opposite directions in their influence on current consumption. On the one hand, a high interest rate makes present relative to future consumption expensive. The substitution effect of a high as

compared to a low interest rate is to reduce current consumption relative to

planned future consumption; in other words it increases current saving. On the other hand, for net savers (and we are here dealing with an economy of net asset holders) the income effect of such high interest rates is to increase

483

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

M. C. URQUHART

both current and planned future consumiption; it decreases current saving. If the planning horizon is long, both effects can be powerful. But which dominates depends on the contours of the indifference maps representing the valuations of present and future consumption.

If the income and substitution effects of interest rate levels cancel among stages of life so that the profiles of consumer expenditure are not affected by the interest rate, there will not be a feedback from the interest rate determined

by the price of land to the price of land itself. If the substitution effect of the interest rate level dominates the income effect, as is often assumed, consump- tion in earlier stages of life will be lower and saving higher with high interest rates than with low rates - the contour of consumer expenditures will be

changed to lower present consumption in favour of future consumption. Consequently, by itself, a high interest rate will mean that larger asset values will be accumulated and total asset values will be higher than with a low interest rate. From the viewpoint of the stability conditions of the system, if asset prices should fall below their equilibrium level both the asset value effect and the dominant substitution effect of the concomitant higher interest rate will cause an excess demand for assets. Thus if the substitution effect dominates, the equilibrating effects of asset prices and the concomitant inter- est rates which, of course, are uniquely related, reinforce one another. If the income effect should dominate, the asset price and interest rate effects iun counter to one another.3

The results of the above may be illustrated by the use of a very simple linear model.4 The variables I use are: y = income in real terms (bushels of wheat); c = consumption in real terms; A = tlhe value of assets measured in bushels of wheat; k = the stock of land measured in acres; X = the price of a unit

(acre) of land measured in bushels of wheat; r = the rate of interest; q the total payment for the services of land measured in wheat. An approxima- tion of the consumption function is given by the following equation. Real

consumption is a function of real income, the real value of assets and interest rates. The parameters a1 and a2 will themselves be functions of the distribu- tion of assets and income among those in the various stages of life.5

c = aiy + a2A + a3y/r.

In equilibrium with full employment (y = y), all the land being held by some- one (k k= ), and the payment for land services being determined by the production function (q = q) we have the equilibrium equation to clear the goods market, which follows from the condition that in equilibrium c = y.

(1) Y = aly + a2A + aay/r. 3It should be noted that a variation of the interest rate, let us say an increase, caused by a variation of the prices of the services of assets, total income being given, has its own effect on equilibrium asset values the nature of which will depend on whether the income effect or the substitution effect of interest rates dominates. In this case, a dominant substitution effect, by itself, means higher aggregate asset values; a dominant income effect means, by itself, lower aggregate asset values. 4I wish to emphasize that this linear model is illustrative only. It may help a bit in showing how the general equilibrium works. iThere is always a problem of aggregation in an aggregate consumption function. This

one is no exception.

484

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

Asset Prices and Values

We also have from the asset market

(2) A Xk (k = k);

(3) r q/(Xk) (q = q and k = k).

The term q/k is the wheat price of the services of an acre of land. The interest rate is the ratio of the price of services of land to the price of land itself.

By substituting equations 2 and 3 in equation I and solving for the price of land, we get:

X = y/k[(l - a)/(02 + ay/q)];

A = y (1 - a)/(a2 + a3y/q);

r = q/y[(a2)/l( - ai)] + as/(l - al).

If the income and substitution effects of changes in interest rates cancel, then a3 will be zero.

I dwell briefly on three variations of the above model which will elaborate its characteristics. First, it will be readily apparent that if a change in tastes, which lowered the attractiveness of consumption during retirement, causes equilibrium saving to fall to 10 bushels of wheat in each of the working stages of life and hence dissaving in retirement to fall to 40 bushels, then in the new equilibrium, accumulated asset values at the end of each stage of life and hence the total value of all assets will be half of what they were before. As a result of the fall in the demand for the stock of asset values, if the interest rate effect can be neglected, the price of land will be one bushel per acre and the interest rate will be forty per cent.

Second, reverting to our initial equilibrium, let us suppose that it becomes the aim of those within each stage of life to accumulate as assets to pass on, at the end of their retirement, 80 bushels worth of land to those still living. The demand for aggregate asset values rises. I illustrate the new equilibrium by substituting lines 5 (a), (b) and (c), and 6 (a) for lines 5 and 6 in Table I. Wlhat has happened is that the price of land has doubled to four bushels per acre. Saving by those in each stage of life remains as before, but those in each working stage of life add to their asset values 40 bushels worth of wheat of which 20 bushels comes from saving and 20 bushels from inheritance of land; the retired sell 80 bushels worth of land to finance retirement consumption and leave, as bequests, 80 bushels worth of land to those in the working stages of life. With the doubling of land prices the rate of interest has fallen to 10 per cent since the price of land services is unchanged. The distribution among stages of life of income, consumption, saving, and land holdings are as they were initially. All that has happened is that asset values have doubled because people want to hold more assets for purposes other than supporting consump- tion in retirement. I have abstracted from the possible effects of the change in interest rates on the desired time-pattern of consumption.

Third, let us again begin with the initial equilibrium but suppose that a Hicks-neutral technological change doubles real output and income. Such a change would double the real values of each of the services of a physical unit of land and a physical unit of labour. If the pattern of tastes is such that, aside

485

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

M. C. URQUHART

from the effect of any change in interest rates, individuals wish to maintain the same shapes of consumption and saving contours throughout their lives as before, then in the working stages of life, they would have twice the income and would wish to both consume and save twice as much as before; they would also wish to hold twice the asset values they held before. Those in retirement would wish to begin retirement with twice as much wealth in land as before in order that they could support twice as much consumption during retirement by disposing of this wealth. Both the total value of assets and the

price of land would be doubled. The prices of the productive services of land would also have doubled owing to the increased output. Interest rates would then remain as before. A major point of interest here is that the increase of income has increased the demand for assets, in this case, in proportion to the increase in income, but that there has been no change in interest rates. The retired will have benefitted along with those in working stages of life since their asset values are increased with the rise in the price of assets.

Before proceeding to examine some of the interesting implications of the nature of the demand for assets I should like to summarize what we have seen thus far.

First, the demand for assets, measured in terms of consumer goods (wheat), is a function of the profiles of expected receipts of income and desired patterns of consumer expenditure. The greater the desire to consume in the future, though still within one's lifetime, the larger is the demand for assets measured in consumer goods, the higher are asset prices and the lower are interest rates.

Second, the greater the desire to hold asset values to pass on to one's bene- ficiaries the greater will be the demand for asset values, the higher will be asset prices and the lower the interest rate.

Third, the higher the level of income, the larger is y, the greater will be the demand for asset values.

Fourth, we cannot say with certainty what the effects of interest rate levels will be on the contours of consumer expenditures through stages of life. If the substitution effect dominates, a high interest rate, by itself, tends to lower desired consumption in earlier stages of life, to lead to a greater demand for assets and higher aggregate asset values; if the income effect dominates, the tendencies are in the other direction.

I should like to devote the remainder of the paper to examining what light the foregoing way of looking at the demand for asset values may throw on the demand for real assets and hence indirectly on the incentives to accumulate

capital goods. The common explanation of the level of investment in a full-

employment economy is that it is determined by the interaction of marginal efficiency of investment schedules with saving schedules, interest rates being determined in the process and being one of the main equilibrating prices.6 One may alternatively take the approach of comparing the asset prices of capital goods as determined by the aggregate net demand for asset values with the costs of producing capital goods. Now capital goods will be produced and added to the supply of assets to the point at which the price of assets just equals their cost of production. I propose to go at the matter this way. My 6As noted above, interest rate adjustment is not, by itself, equilibrating if income effects dominate substitution effects.

486

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

Asset Prices and Values

attention will be almost wholly devoted to a discussion of the demand for assets and particularly to the demand for those assets whose services are inputs in the production process. I bring in the role of real assets in production only to the extent that their prices and the prices of their services affect the interest rates and hence the demand for assets themselves; I do not deal with the fac- tors that affect the costs of producing new real assets.

Now there are more net assets than just land and capital goods in the supply of assets to the private sector of the economy; in particular there are govern- ment bonds and money. Since the real quantity of these latter assets in the market will meet part of the total demand for asset values they will affect the real demand for the land (and capital goods) and consequently their prices. I should like first to see what the presence of government bonds and money means for the price of real assets.

A question that arises immediately is whether the existence of new types of assets such as, for example, bonds will from their differentiated nature increase the aggregate demand for all asset values in our full-employment economy. This result could occur if the insertion of the new assets increased real income

by increasing the efficiency with which production and exchange can be carried on. If such occurs, the increased real income would increase the demand for assets as we noted above. We should keep in mind, however, that in fact, the private sector of the economy can throw up properties of many different types that are assets to particular individuals even though many of these private gross assets may have offsetting private liabilities. The point is

that, for those who wish them, the private sector provides a great variety of

gross assets such as commercial paper, bonds and equities, and money created

through the private banking system, besides the physical assets. Hence, the

private sector can have a mixture of gross assets within itself that permits efficient organization of production; accordingly, I would argue that the inser- tion of new assets from outside the private economy does not, in itself, increase real income and the demand for asset values. If they are to have an effect on the aggregate demand for asset values it must come through their effect on the interest rate.

The first step toward realism is to compare the effect, on total asset values and real asset prices in the private sector of the economy, of money provided from without the private sector (outside money) with the effect of money provided from within the private sector (inside money).

For individuals who hold money it is an asset, like any other asset, except that it yields no tangible return. In our world of certainty it will be held be- cause it reduces the costs of transactions. That the quantity of money affects the general level of money prices need not concern us at this time. The matter of concern is that individuals do wish to hold a quantity of money measured in real terms that bears a relationship to the real volume of transactions. Money is an asset to them. And what we are doing is comparing the effects of outside

money with those of inside money.7 If money is provided from without the private sector as a liability of the

7I do not deal with the fact that the desired real volume of money will be affected by the existence of near-moneys. The presence of the latter does not affect the general tenor of the argument.

487

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

488 M. C. URQUHART

public sector or if it is a commodity such as gold it will be a net part of the total of all asset values, measured in consumer commodities, of the private sector. The asset values of other assets will be accordingly reduced, their prices in consumer goods will be lower and interest rates higher.

If, on the other hand, the money is inside money, created through a banking system of the private economy, the consumer goods asset value of the money to the non-banking part of the economy is matched by an equivalent of other

private asset values held by the banks themselves. In this case, money is not a net asset to the private sector, the prices of real assets will be higher than if there were outside money and interest rates will be lower.8 Other things being equal, the higher asset prices of a system with inside money will provide a greater inducement to the production of capital goods than one with outside

money. If there are government bonds in the private sector that have been issued in

the past to pay for a non-recurrent government expenditure, asset prices of

productive assets will be affected. Since the coupons on the bonds are paid from an equivalent amount of taxes, there is a transfer of income within the

private sector of the economy which, along with the tax transfer effects them- selves, we ignore. There is no change in real income. If the bonds are per- petuals and have a total coupon value yield in wheat of one-half the yield on land, it will be almost as if we had increased the quantity of land and its yield by fifty per cent.9 If the interest rate effect on saving is zero, the desired con- tours of consumption expenditures through stages of life will be as before, the

price of land will have fallen to two-thirds its original level if there are no other assets than the land and the bonds and the rate of interest will be increased by one half.

If the bonds have a principal sum with a definite maturity, the results may be changed quantitatively, though not qualitatively; the principal sum plays some part in determining the bond value as well as the coupon rate. And, of course, as the maturity shortens, the more important the principal sum be- comes in determining the asset value of the bond.

If the interest rate effect is such that the substitution effect dominates, the fall in land prices will be moderated and total asset values will be higher than otherwise, owing to people saving more in working stages of life to consume more in retirement. The wheat prices of physical assets will nevertheless have fallen. Since these real assets could just as well have been an existing stock of real capital goods as land, the fall in their prices will lower the inducements to the production of new capital goods.

Government bonds are typically issued in monetary rather than in real terms. Hence a monetary inflation lowers consumer goods value of government bonds. The asset values of other assets, including our land, and the real price of assets are accordingly raised and interest rates lowered.

Let us now introduce capital goods that may be produced themselves into

8To the extent that the banks of the private sector must hold a reserve commodity, that part of their assets is an outside asset. 9There has been no addition to income in this case since the coupons on the bonds are paid from taxes.

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

Asset Prices and Values

our system. I propose to make additional land itself, homogeneous in quality with the old land, the producible capital good. Thus we continue to have the same factors and products as before, but have an additional production func- tion for the production of land. The ramifications of the latter are important but I carry on without going into them now.

New land can be produced only if the production of wheat and accordingly current consumption is less than total production. The smaller consumption must be induced, in part, from lower real value of existing assets and hence a lower real price of land. If the interest rate effect on consumption contours is zero, the lower aggregate asset values must account entirely for the reduced

consumption. The lower asset values would result from newly produced assets

being sold to those who are net savers at lower prices than hitherto existed.10 The old asset values would be reduced because the retired cannot sell their assets at the old prices and others in the later stages of life will also have the asset values of their old assets reduced. Indeed the elasticity of demand for the physical quantity of assets with respect to price must be less than

unity so that absolute asset values fall."l It may be noted in passing that the new assets will produce new income in the future, an effect which will be

anticipated, but this makes no qualitative change to our results. If the interest rate effect is not zero but if the substitution effect dominates,

the rise in interest rates will, by itself, lead to a desire for increased net saving among those in working stages of life, will, by itself, lead to some increase in demand for asset values, and will accordingly diminish the fall in asset prices and the rise in the interest rate itself.

If the addition of capital goods is accompanied by, let us say, a Hicks- neutral technical change, the result becomes different. The technological change raises the whole contour of present and expected future incomes. Accordingly, maximizing behaviour will lead to both current consumption and current saving of all those in working stages of life being increased. The technological change tends to raise the level of desired asset values and asset prices. If the retired have been wise and invested in equities they also will benefit from the technological change from the rise in the prices of physical assets.

We can go further on this matter of technical change in the above circum- stances. Given plausible conditions similar to those of Milton Friedman, A Theory of the Consumption Function (Princeton, N.J., 1957) in which he argues that permanent consumption may be expected to be a constant propor- tion of permanent income, if real income rises in proportion to the physical capital stock, whether it be caused by neutral technological change or a growth of population concomitant with the increase of physical capital, the desired aggregate asset values will maintain the same ratio to the physical capital stock as before, and hence real asset prices and, given our production function, 10Here we take a step toward process analysis. The proportions of the acreage of land held in earlier stages of life rise. "This result follows because, while the reduction of consumption of the retired will be equal to the full fall in the asset values they hold, the reduction of consumption of those in later stages of life on account of the fall in values of their old assets will be less than this fall, if maximizing behaviour is followed.

489

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

M. C. URQUHART

interest rates will be unchanged. The plausible conditions are that indifference surfaces of present and future consumption that correspond to different levels of lifetime (permanent) income are homogeneous, that the contours of popula- tion and income distribution among different stages of life along with taste fac- tors remain unchanged and that the ratio of total investment in human capital relative to that in physical capital remains unchanged. In this case, maximizing behaviour will lead to desired asset values being a constant proportion of income. If real income then grows in proportion to the capital stock so will real desired asset values, and asset prices will be unchanged. There would be, in these particular circumstances, a constant ratio of asset values to physical capital.

The causes of the change in income (or output) will have a bearing on interest rates. For example, suppose the growth of output has been caused by a capital "saving" technical change. In that case, the price of the services of a

physical unit of capital will be lower than otherwise and interest rates will be lower. If interest rates affect the contour of desired consumption then total real asset values and asset prices will be affected.

Mention was made above of investment in human capital. If investment in one's children's education is a way of passing asset values on to future genera- tions, it may replace the holding of tangible asset values for this purpose and lead to a lowering of the level of desired tangible asset values, even though the sum of tangible and intangible asset values are unaltered. Tangible asset

prices may accordingly be lower. I should like to refer to one institutional arrangement that may have an

important bearing on asset prices. If in-payments into retirement funds are invested in an economy's assets for disbursement on retirement, it is as if individuals had accumulated asset values for themselves. If, however, a pen- sion plan is arranged so that those in working stages of life pay taxes that support the retired directly, an important demand for asset values is re- moved. Each working individual feels that he is accumulating asset values if he can in turn depend on the next generation to pay his retirement benefit. It is as if an outside asset, the pledge of the state to pay pensions, has been added.

Finally, one can point to important historical episodes which can be illumin- ated by applying the above tools. Hoarded gold in many countries has pro- vided outside asset values that have lowered the real prices of other assets and led to high interest rates. On the other hand, the development of frac- tional-reserve private banking has economized on the use of outside assets in monetary systems. The existence of the extended family system, wherein fami- lies in working generations support retired relatives, removes a source of demand for asset values. Conversely, the entail, ensuring that estates must be passed intact from one generation to the next, must have increased asset values and asset prices.

One must be careful about the inferences drawn from the above. For example, it is all very well to say that the presence of government bonds in an economy lowers real asset values and raises interest rates. Yet the original benefits of the public expenditure, which the bonds financed when issued, may

490

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions

Asset Prices and Values 491

more than justify their existence as an asset of an economy. Similarly, less-

developed countries may issue outside money as a means of financing develop- ment programmes. Further, we need much more knowledge of the parameters of our asset system before drawing hasty conclusions. Nevertheless, this way of looking at things can contribute substantially, I believe, to the handling of a number of problems, including possibly those of stabilization and growth, that have not yielded readily to treatment by more conventional means.

This content downloaded from 185.44.79.92 on Tue, 17 Jun 2014 16:20:10 PMAll use subject to JSTOR Terms and Conditions