Embed Size (px)

Citation preview

Asset Development and Financial Literacy

1

Asset Development and Financial Literacy

For Individuals with Disabilities, their Families and Support Network

(Use “Notes View” to view instructor narrative.)

Asset Development and Financial Literacy

2

“Few people have ever spent their way out of poverty. Those who escape do so through saving and investing for the long-term.”

Michael SherradenCenter for Social Development

Sherraden, M. (2005). Inclusion in Asset Building.

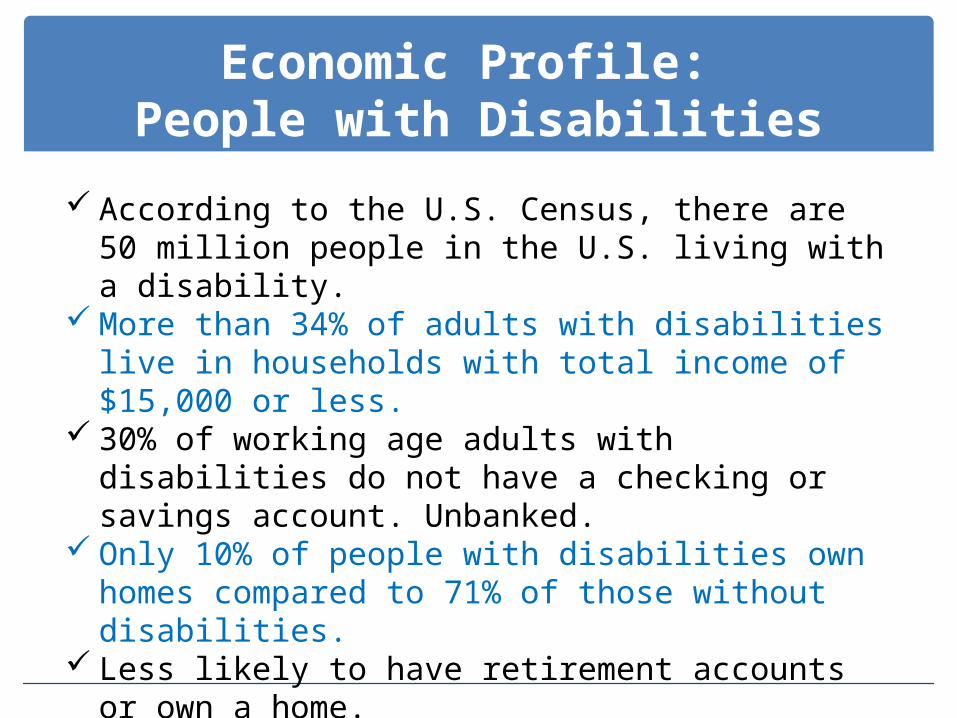

Economic Profile: People with Disabilities

According to the U.S. Census, there are 50 million people in the U.S. living with a disability.

More than 34% of adults with disabilities live in households with total income of $15,000 or less.

30% of working age adults with disabilities do not have a checking or savings account. Unbanked.

Only 10% of people with disabilities own homes compared to 71% of those without disabilities.

Less likely to have retirement accounts or own a home. More likely to be asset poor.

Sources: The White House, Executive Summary: Fulfilling America's Promise to Americans with Disabilities. (http://www.whitehouse.gov/news/freedominitiative/freedominitiative.html.) April 2001 and National Disability Institute

Asset Development and Financial Literacy

4

If you support individuals who are working and are beginning to develop goals such as:

Buying a home, Starting a business, Taking educational or vocational courses,

Then you are working with someone who will benefit from Asset Development and Financial Literacy. Information on who to contact will be provided later in the presentation.

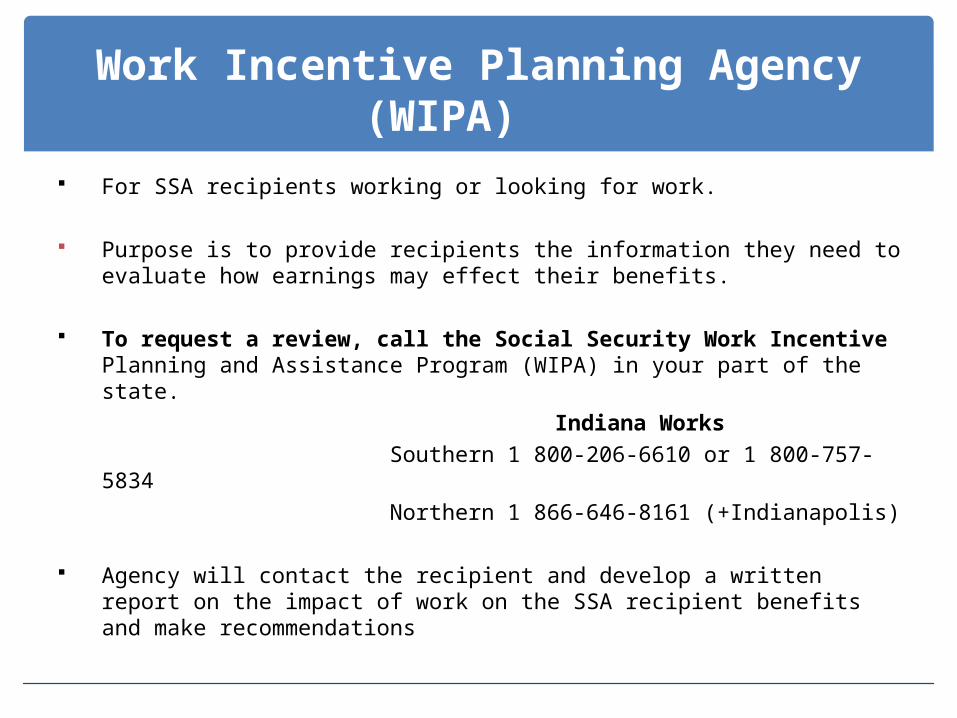

Work Incentive Planning Agency(WIPA)

For SSA recipients working or looking for work.

Purpose is to provide recipients the information they need to evaluate how earnings may effect their benefits.

To request a review, call the Social Security Work Incentive Planning and Assistance Program (WIPA) in your part of the state.

Indiana Works

Southern 1 800-206-6610 or 1 800-757-5834

Northern 1 866-646-8161 (+Indianapolis)

Agency will contact the recipient and develop a written report on the impact of work on the SSA recipient benefits and make recommendations

Federal and State Benefit Programs

There are several federal and state benefit programsto considered when someone is working.

• Social Security Disability Insurance (Title II)• Supplemental Security Income (Title XVI)• Medicaid• Medicare• HUD• Food Stamps• TANF

Asset Development and Financial Literacy

7

What is Financial Literacy?

Financial Literacy

8http://www.youtube.com/watch?v=23zghpS9034

What is Financial Literacy?

Financial Literacy is defined as:

“having the knowledge, skills and confidence to make responsible financial decisions”. (Task Force on Financial Literacy, 2010)

9

http://en.wikipedia.org/wiki/Financial_literacy

Benefits Management-BIN-SSDI, SSI-Medicaid , MedicareHUDTANF, Food StampsEtc…

Guardianship & Representative payee statusWorkin

g & Earning

Savings, IDA’s, HUD, Trusts, IRA, etc…

Financial Literacy is a broad field that includes:

Asset Development-Home-Business-Voc/Ed

Community integration

Self -direction

10

Freedom, choice

Stability

Opportunity to work & participate

Mentoring, coaching

Asset Development and Financial Literacy

11

What is an Asset?

Asset Development and Financial Literacy

12

What is Asset Development?

What is Asset Development?

Asset development is:

“Saving money and making investments that increase in value over time”.

“As individuals develop assets,

they and their families will be more able to move out of poverty and remain out of poverty”.

Task Force on Financial Literacy, 2010

http://www.disability.gov/community_life/independent_living/asset_development

13

Difference: Assets vs Income

Assets are the accumulation of value or aggregation of wealth.

The focus is on longer term stability.

Income is the flow of money to an individual household that meet daily living expenses.

The focus is on short term needs.

14

What is Asset Development?

Asset Development is buying a home, investing in a business, learning a new skill or putting aside money in a savings account for emergencies.

Assets provide long term benefits.

Assets are usually economic resources: Assets are anything that can be turned into cash(minus the debt owed).

Assets can also be human resources: Skills or education can be considered assets.

Asset Development and Financial Literacy

Financial Literacy is a large body of information about finances. One of the parts is Asset Development.

16

Asset Development

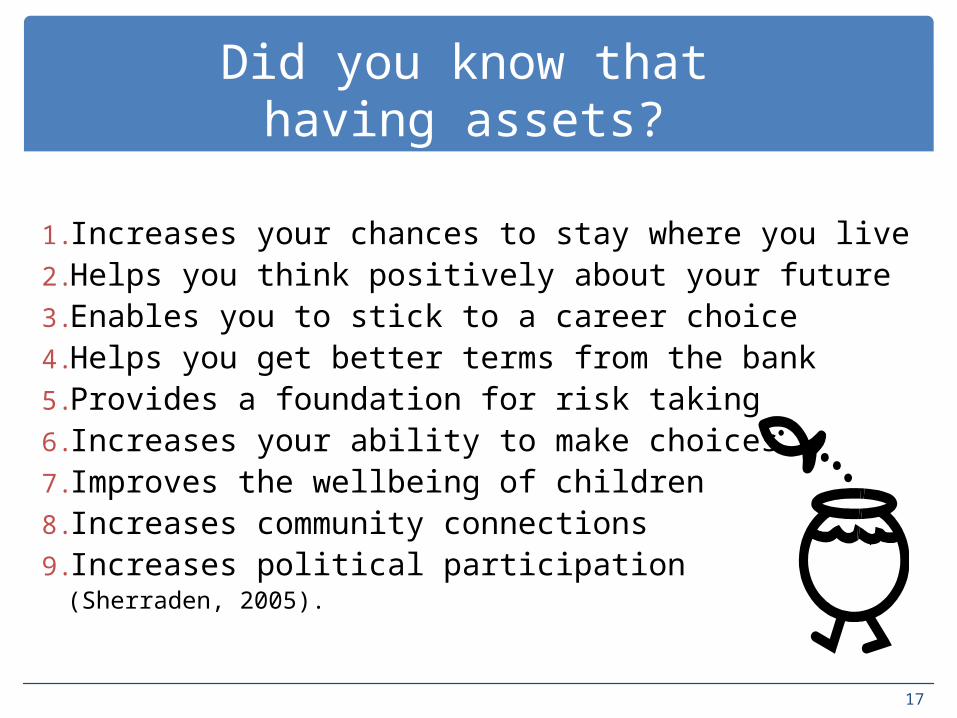

Did you know that having assets?

1. Increases your chances to stay where you live 2.Helps you think positively about your future 3.Enables you to stick to a career choice 4.Helps you get better terms from the bank 5.Provides a foundation for risk taking 6. Increases your ability to make choices7. Improves the wellbeing of children 8. Increases community connections 9. Increases political participation

(Sherraden, 2005).

17

Programs to Help Develop Assets

1. Social Security Social Security Work IncentivesPlans for Achieve in Self-Support (PASS)Property Essential to Self-Support (PESS)

2. Internal Revenue ServiceEITC (Earned Income Tax Credits)VITA (Volunteers in Tax Assistance)

3. Indiana Housing and Community Development AuthorityIndividual Development Accounts (IDA’s)

4. Trust funds Private TrustsARC Master Trust

18

Historical programs that have helped people with assets

Homestead Acts (not good for everyone)G.I. BillsHome interest mortgage deductionTax shelters for retirement savingsIndividual Tax deductions Business Tax deductions Trusts

Asset Development and Financial Literacy Thinking Differently

Asset Development and Financial Literacy helps by:• Linking individuals with financial literacy resources• Linking with asset development programs• Integrate asset development and financial literacy in

person centered planning meetings for greater self sufficiency and financial independence

You can help by: • Thinking beyond employment goals• Talking about Asset Development and Financial

Literacy concepts to other friends and families • Providing different kinds of supports

20

Asset Development and Financial Literacy

“Never believe that a few caring people

can't change the world.”

Margaret Mead

21

Information Websites

• Indiana Institute on Disability and Community-Benefits Management http://www.iidc.indiana.edu/index.php?pageId=18

• National Disability Institutehttp://www.realeconomicimpact.org/

• Virginia Commonwealth Universityhttp://www.vcu-ntc.org/resources/cwicmanual.cfm

• Social Security http://www.ssa.gov/disabilityresearch/wi/detailedinfo.htm

• Southern Indiana WIPAhttp://www.iidc.indiana.edu/disabilitybenefitsandwork/workincentivescoordinators.htm

Who to contact about Asset Development and

Financial Literacy Trainings

Contact your local Indiana United Way

(317) 923-2377Contact your local Community Action Program (CAP)

(317) 638.4232 or 1.800.382.9895 Contact the local Purdue Extension office

(765) 494-8491Contact the Indiana Housing and Community

Development Authority

(800) 872-0371

23

ResourcesFederal and State Asset Development Programs

Social Security Administration

Assets For Independencehttp://www.acf.hhs.gov/programs/ocs/afi/assets.html

Individual Development Accounts (IDA’s)

Indiana Housing and Community Development Authority

http://www.in.gov/ihcda/

Self Sufficiency ProgramsHousing and Urban Development (HUD) local offices

Development

http://www.hud.gov/local/index.cfm?topic=offices&state=in

References

Assets. (2010). In Merriam-Webster Online Dictionary. Retrieved March 17, 2010, from http://www.merriam-webster.com/dictionary/assets

Sherraden, M. (2005). Inclusion in Asset Building. Testimony for Hearing on ”Building Assets for Low- Income Families” Subcommittee on Social Security and Family Policy Senate Finance Committee and Social Security, testimony, President’s Commission to Strengthen Social Security, April 28, 2005.

Disability Studies Quarterly, Vol. 26, No 1 Winter” Copyright 2006 by the Society for Disability Studies

Making your Money Work, Purdue Extension Services. Purdue: West Lafayette, Indiana

Task Force on Financial Literacy

http://www.financialliteracyincanada.com/eng/about-financial-literacy/definition.php

25