Embed Size (px)

Citation preview

The opinions expressed in this presentation are those of the speaker. The International Foundationdisclaims responsibility for views expressed and statements made by the program speakers.

Asset Allocation in Health and Pension Plans—Your Key Decision

Ian W. JonesDirector and Senior ConsultantThe Bogdahn GroupBuffalo, New York

I02-1

Asset Allocation in Health and Pension Plans—

Your Key Decision• Understanding your demographics and fund projections• Estimating future asset class returns and risk

expectations• ls there an optimal asset allocation model?• What are the different and dominant types of risk

associated with various asset allocation models?• Trade-off of risk and return

I02-2

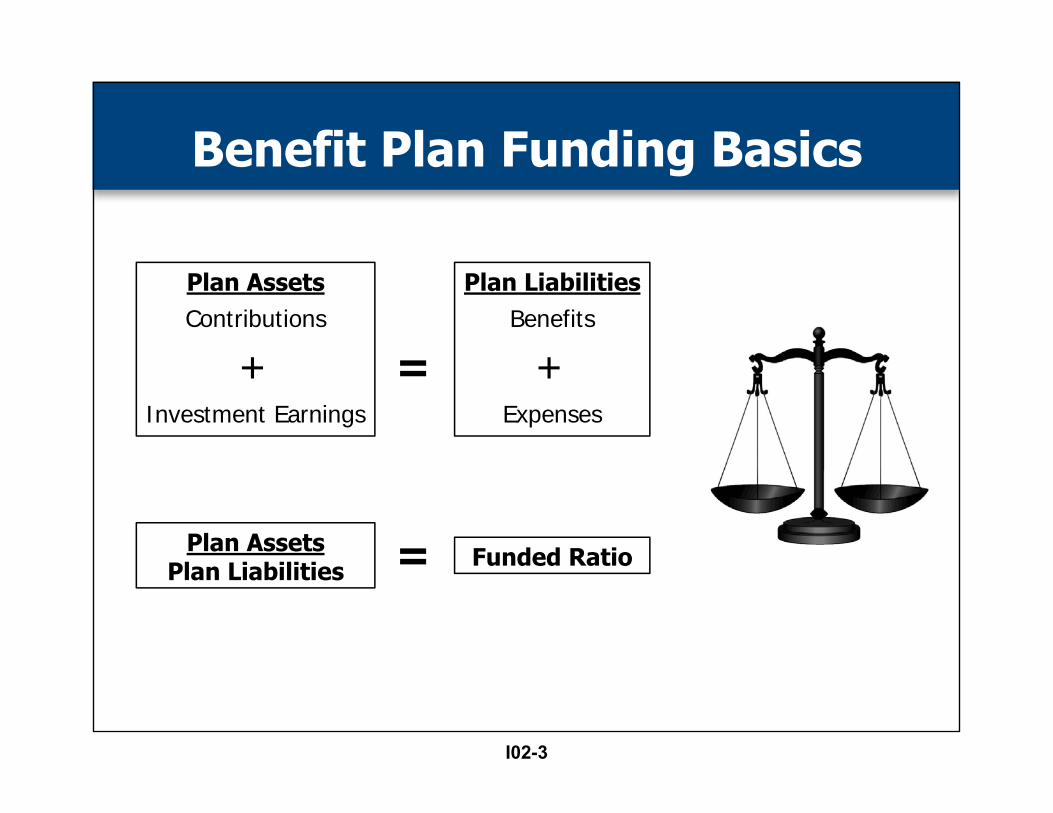

Plan AssetsContributions

+Investment Earnings

Plan LiabilitiesBenefits

+Expenses

=

Plan AssetsPlan Liabilities Funded Ratio=

Benefit Plan Funding Basics

I02-3

Benefit Plan Funding Basics

Plan Funding Level:Actuary assesses plan’s demographics and asset allocation structure to determine current and projected funding levels.Factors considered:• Industry: growing or shrinking

– Manufacturing, building/construction, service, etc.

• Age of participant population and how long they live• Ratio of active vs. inactive participants• Contributions, benefits, expenses• Labor/management negotiations• Rate of return potential

Significant factor that will impact the funding level of a defined benefit pension plan is the assumed and actual

rate of return earned on plans assets.

I02-4

The ASSET ALLOCATION DECISION is the key determinant of a portfolio’s short and long-

term RETURN and RISK

Asset Allocation Decision

Mix of asset classes• Traditional: Equities and bonds• Alternatives: Real estate, private equity, hedge funds, etc.

– Domestic/International– Developed/Emerging markets

Risk management• Understand which strategies will contribute most to total portfolio

risk

I02-5

Building an Investment Program

Three Essential Steps1. Define investor’s

– Goals and objectives– Liquidity needs and investment horizon – Risk tolerance

2. Set asset allocation 3. Set manager structure

I02-6

Building an Investment Program

Define Investor’sa) Goals and objectives

– To be fully funded • What is investor’s current funded status—Green/Yellow/Red?

– Meet/exceed plan’s actuarial interest rate assumption– Achieving the above with acceptable risk (volatility)– Other?

I02-7

Building an Investment Program

Define Investor’sb) Liquidity needs and investment horizon

– Does the plan have net positive or negative cash flow? • If negative, to what extent?

– Will liquidity needs be changing over time?• Industry outlook (growing or shrinking?)• Ratio of active vs. inactive participants• Labor/management negotiations

Liquidity/cash flow needs impact a plan’s time horizonLonger time horizon allows for inclusion of riskier/less liquid

asset classes with higher return potentialTime helps smooth returns

I02-8

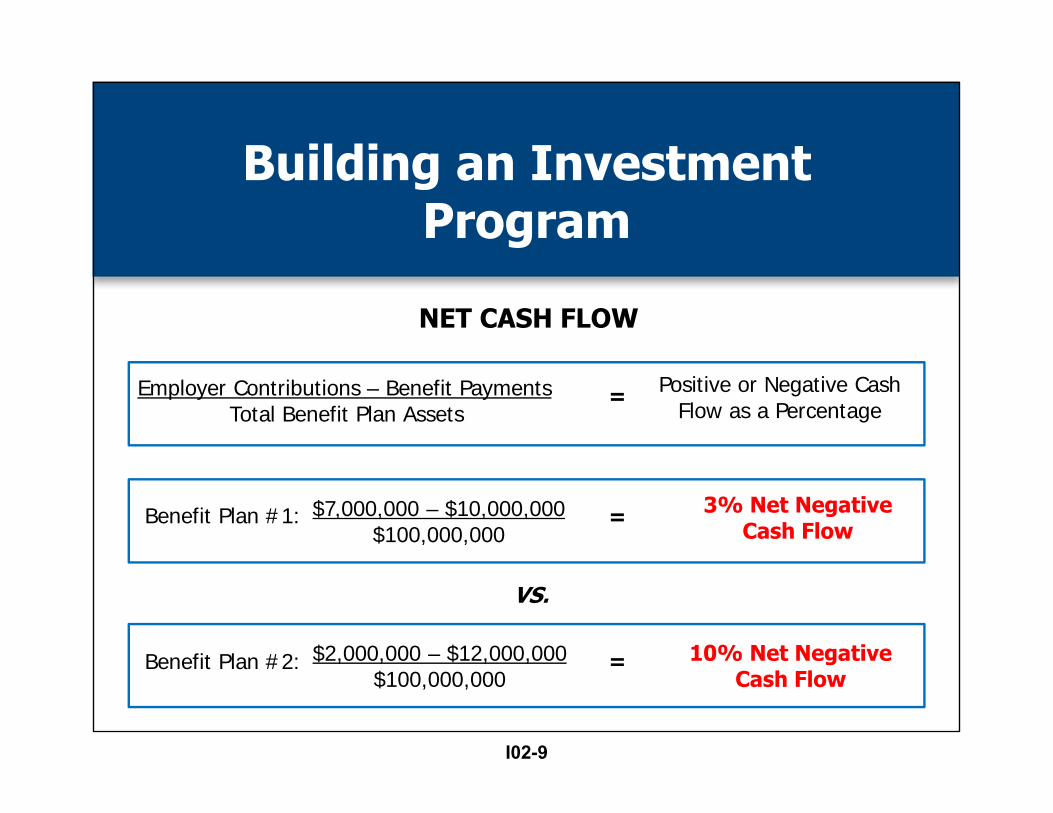

Employer Contributions – Benefit PaymentsTotal Benefit Plan Assets

= Positive or Negative Cash Flow as a Percentage

$7,000,000 – $10,000,000$100,000,000

= 3% Net NegativeCash Flow

$2,000,000 – $12,000,000$100,000,000

10% Net NegativeCash Flow

VS.

NET CASH FLOW

Benefit Plan #1:

Benefit Plan #2: =

Building an Investment Program

I02-9

Building an Investment Program

Define Investor’sc) Risk Tolerance

– Risk/Reward trade off—willingness to take on greater risk in hope of greater return

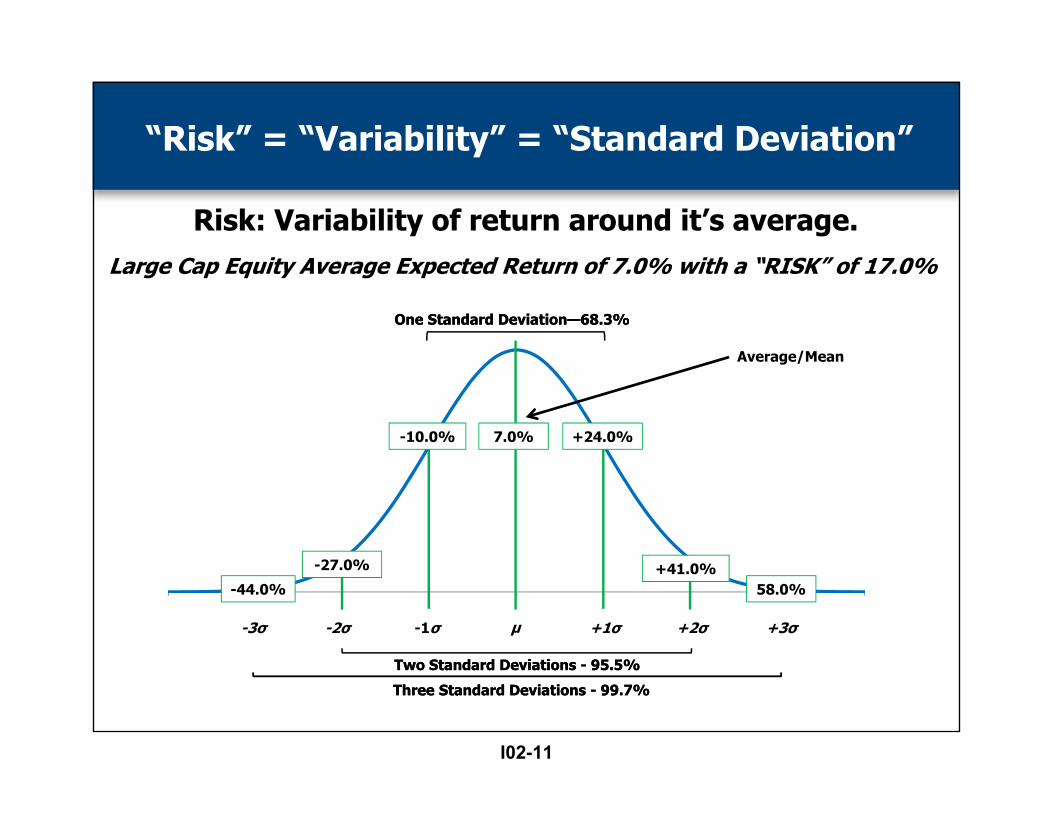

– Most common risk discussed: Variability of Return • Measured by Standard Deviation

I02-10

‐4 ‐3 ‐2 ‐1 0 1 2 3 4

Risk: Variability of return around it’s average.

7.0% +24.0%-10.0%

-27.0% +41.0%

-2σ -1σ +1σ +2σµ-3σ +3σ

Two Standard Deviations - 95.5%

Three Standard Deviations - 99.7%

One Standard Deviation—68.3%

-44.0% 58.0%

Average/Mean

Two Standard Deviations - 95.5%

Three Standard Deviations - 99.7%

One Standard Deviation—68.3%

“Risk” = “Variability” = “Standard Deviation”

Large Cap Equity Average Expected Return of 7.0% with a “RISK” of 17.0%

I02-11

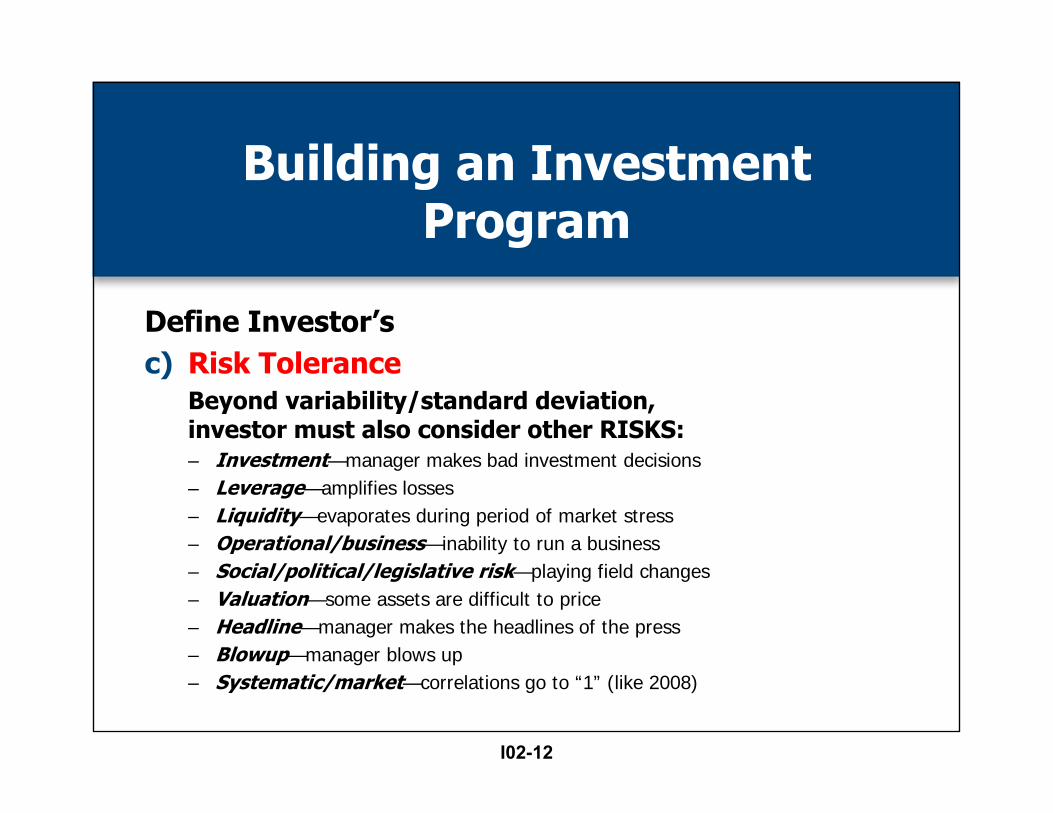

Building an Investment Program

Define Investor’sc) Risk Tolerance

Beyond variability/standard deviation, investor must also consider other RISKS:– Investment—manager makes bad investment decisions– Leverage—amplifies losses– Liquidity—evaporates during period of market stress– Operational/business—inability to run a business– Social/political/legislative risk—playing field changes– Valuation—some assets are difficult to price– Headline—manager makes the headlines of the press– Blowup—manager blows up– Systematic/market—correlations go to “1” (like 2008)

I02-12

Building an Investment Program

1. Define investor’s– Goals and objectives– Liquidity needs and investment horizon – Risk tolerance

2. Set asset allocation 3. Set manager structure

I02-13

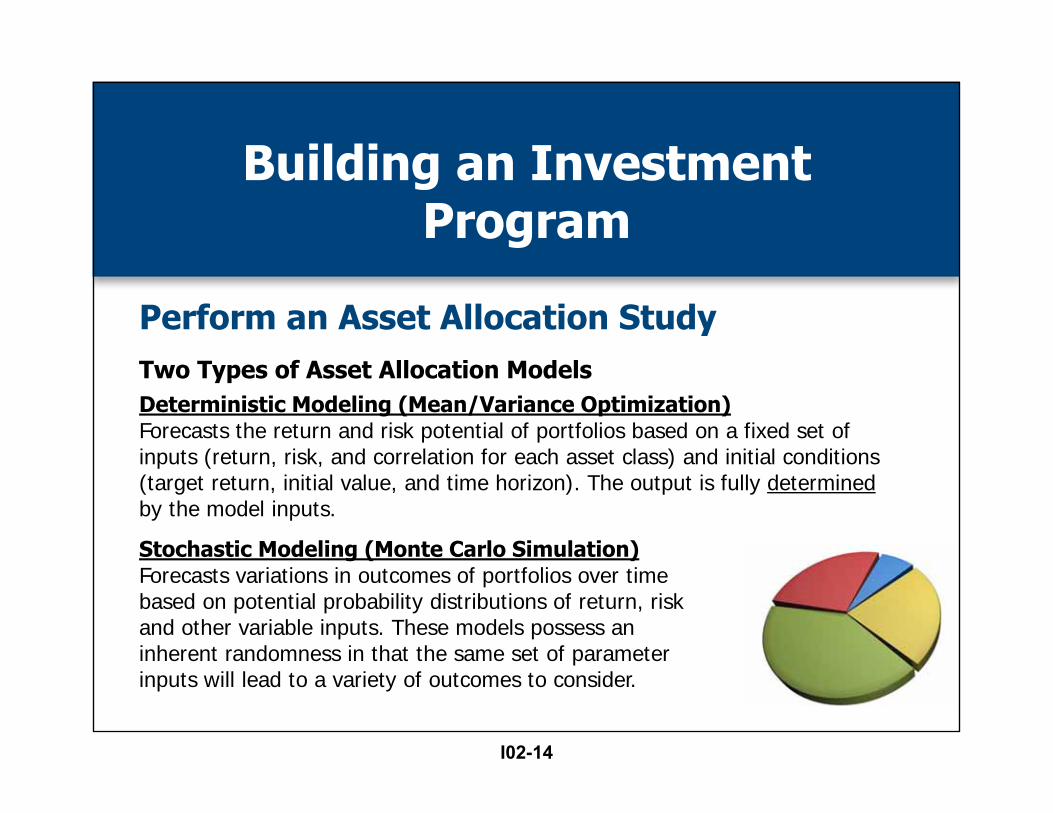

Two Types of Asset Allocation ModelsDeterministic Modeling (Mean/Variance Optimization)Forecasts the return and risk potential of portfolios based on a fixed set of inputs (return, risk, and correlation for each asset class) and initial conditions (target return, initial value, and time horizon). The output is fully determinedby the model inputs.

Stochastic Modeling (Monte Carlo Simulation)Forecasts variations in outcomes of portfolios over time based on potential probability distributions of return, risk and other variable inputs. These models possess an inherent randomness in that the same set of parameter inputs will lead to a variety of outcomes to consider.

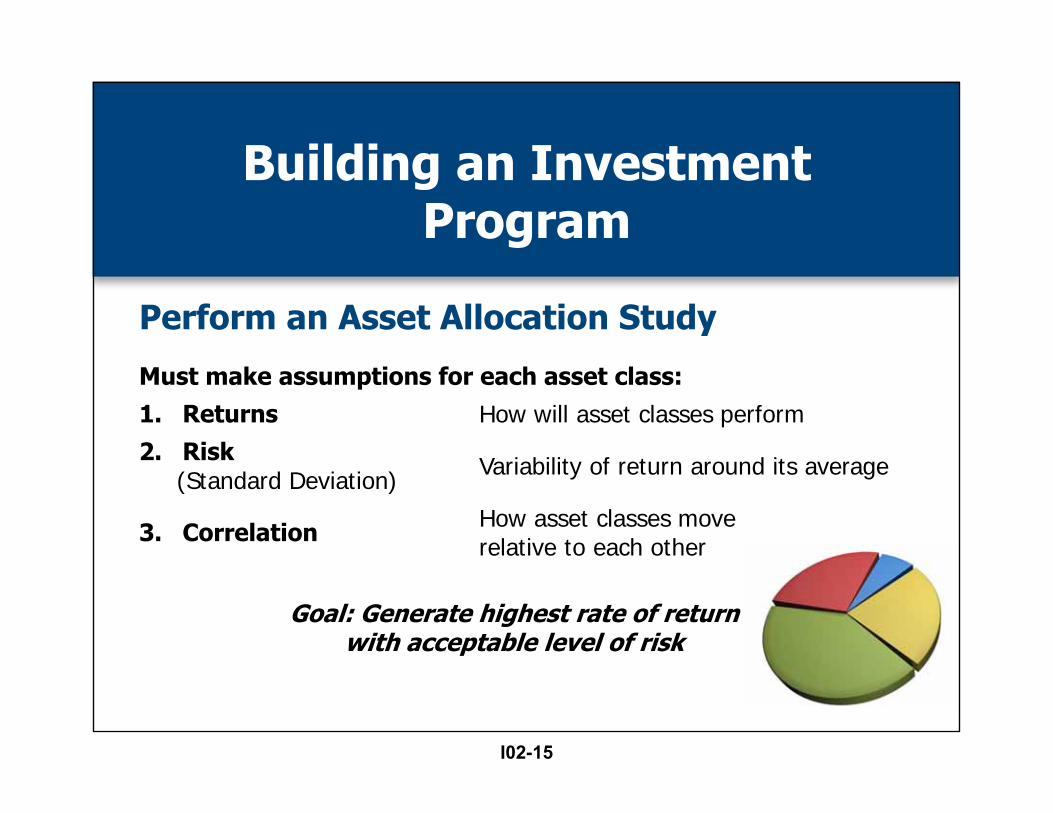

Building an Investment Program

Perform an Asset Allocation Study

I02-14

Must make assumptions for each asset class:1. Returns How will asset classes perform

2. Risk (Standard Deviation) Variability of return around its average

3. Correlation How asset classes move relative to each other

Goal: Generate highest rate of returnwith acceptable level of risk

Building an Investment Program

Perform an Asset Allocation Study

I02-15

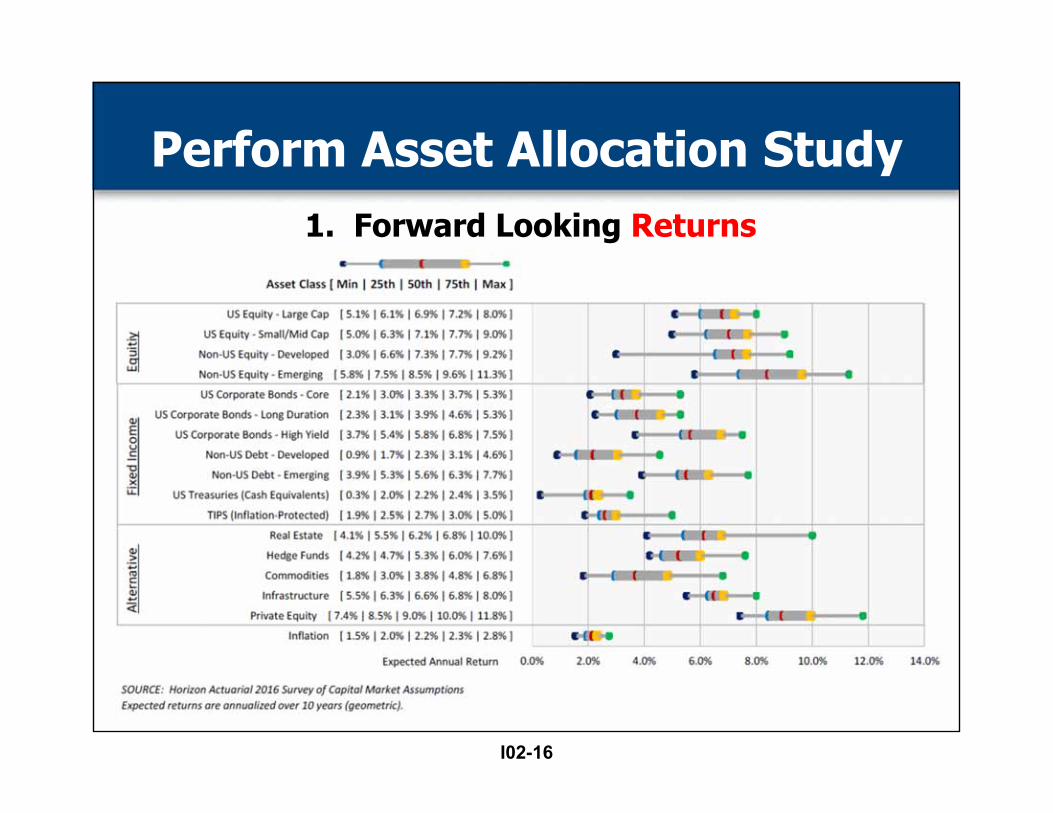

1. Forward Looking Returns

Perform Asset Allocation Study

I02-16

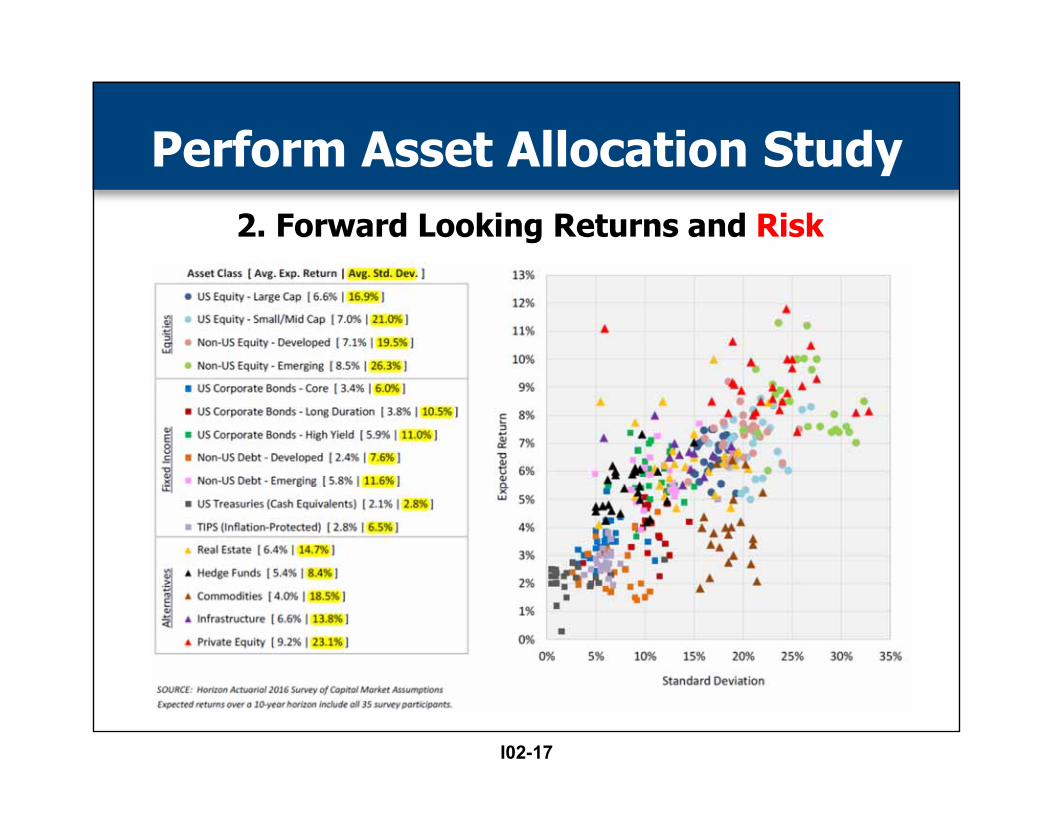

2. Forward Looking Returns and Risk

Perform Asset Allocation Study

I02-17

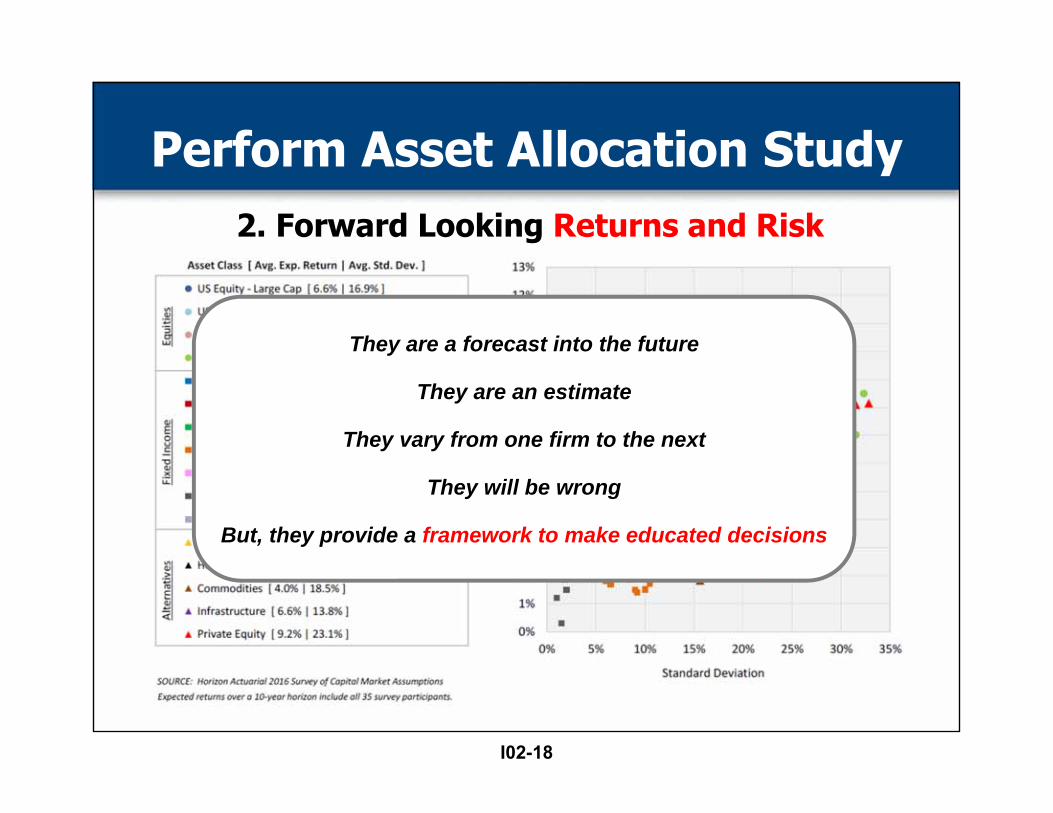

They are a forecast into the future

They are an estimate

They vary from one firm to the next

They will be wrong

But, they provide a framework to make educated decisions

2. Forward Looking Returns and Risk

Perform Asset Allocation Study

I02-18

Perform Asset Allocation Study

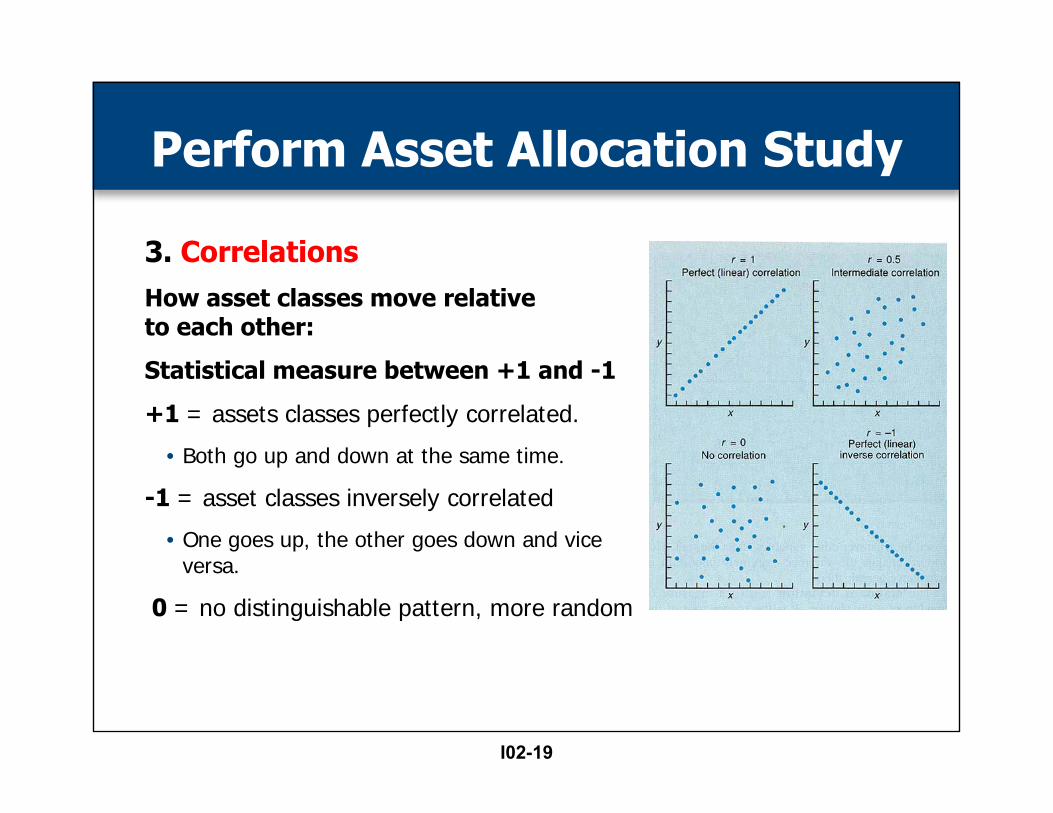

3. CorrelationsHow asset classes move relative to each other:

Statistical measure between +1 and -1

+1 = assets classes perfectly correlated.

• Both go up and down at the same time.

-1 = asset classes inversely correlated

• One goes up, the other goes down and vice versa.

0 = no distinguishable pattern, more random

I02-19

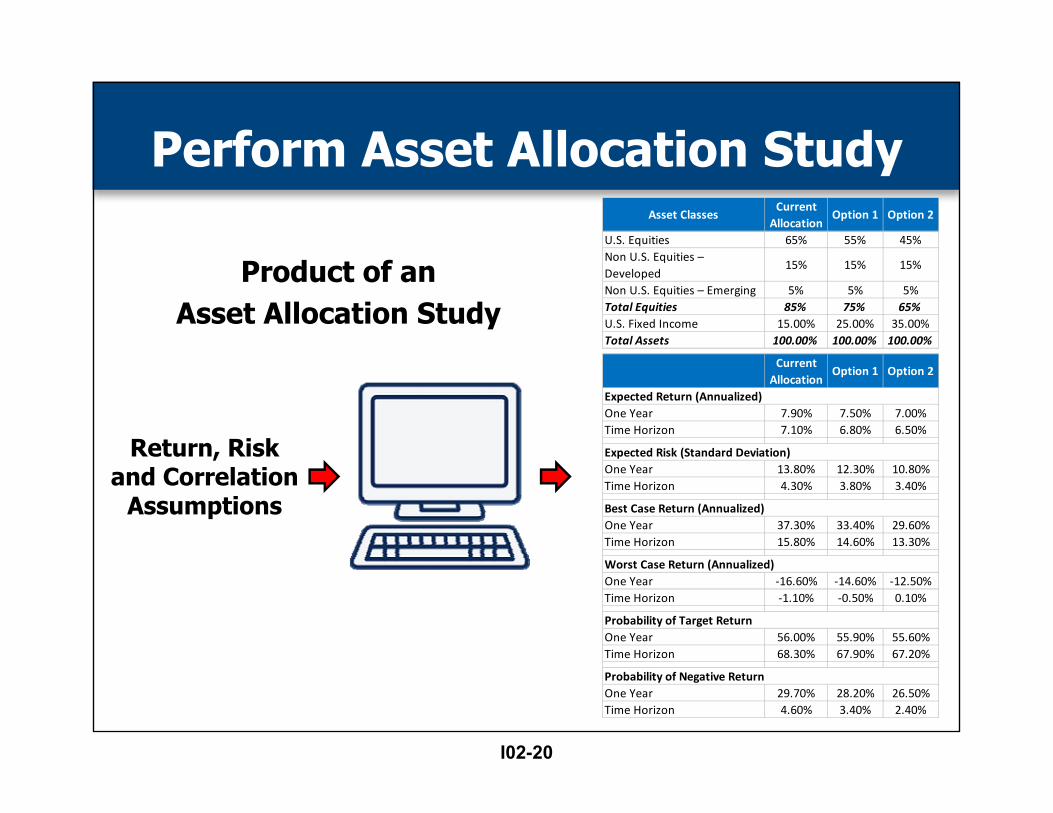

Asset ClassesCurrent Allocation

Option 1 Option 2

U.S. Equities 65% 55% 45%Non U.S. Equities – Developed

15% 15% 15%

Non U.S. Equities – Emerging 5% 5% 5%Total Equities 85% 75% 65%U.S. Fixed Income 15.00% 25.00% 35.00%Total Assets 100.00% 100.00% 100.00%

Current Allocation

Option 1 Option 2

One Year 7.90% 7.50% 7.00%Time Horizon 7.10% 6.80% 6.50%

One Year 13.80% 12.30% 10.80%Time Horizon 4.30% 3.80% 3.40%

One Year 37.30% 33.40% 29.60%Time Horizon 15.80% 14.60% 13.30%

One Year ‐16.60% ‐14.60% ‐12.50%Time Horizon ‐1.10% ‐0.50% 0.10%

One Year 56.00% 55.90% 55.60%Time Horizon 68.30% 67.90% 67.20%

One Year 29.70% 28.20% 26.50%Time Horizon 4.60% 3.40% 2.40%

Probability of Negative Return

Expected Return (Annualized)

Expected Risk (Standard Deviation)

Best Case Return (Annualized)

Worst Case Return (Annualized)

Probability of Target Return

Product of an Asset Allocation Study

Return, Risk and Correlation

Assumptions

Perform Asset Allocation Study

I02-20

Perform Asset Allocation Study

Asset Allocation Studies• Is there an optimal model?• Part science, part art.• Output only as good as the inputs.• Inputs vary from one advisor to the next and will be

wrong.• Still a good tool to help understand inter-relationship

of asset classes and that provides a framework to make educated decisions.

I02-21

Building an Investment Program

1. Define investor’s– Goals and objectives– Liquidity needs and investment horizon – Risk tolerance

2. Set asset allocation 3. Set manager structure

I02-22

Building an Investment Program

Set Manager Structure• Allocation to Core Managers

– Traditional asset classes (equity and fixed income)– Active vs. Passive

• Allocation to Satellite Managers– Both traditional and alternative asset classes– Active, high conviction, opportunistic, value add

• Risk budgeting/risk management– Understanding which strategies will contribute most to total portfolio

risk– Blending non-correlated investment manager strategies to smooth

returns

I02-23

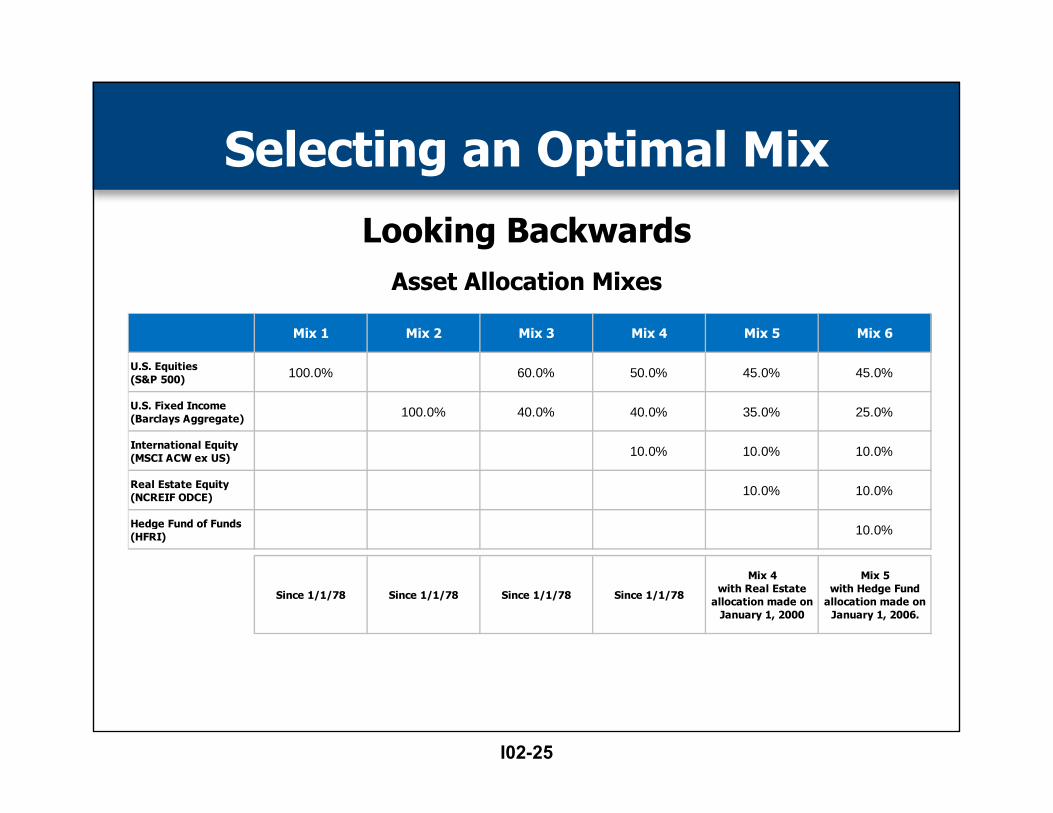

Selecting an Optimal Mix

Looking BackwardsOver the past 30 + years what has been the

optimal asset allocation mix?

Options to consider:• Domestic equity • Domestic fixed income• Domestic equity and fixed income• Domestic + international equity and fixed income• Domestic + international equity, fixed income and real estate• Domestic + international equity, fixed income, real estate and

hedge funds

I02-24

Asset Allocation Mixes

Looking Backwards

Mix 1 Mix 2 Mix 3 Mix 4 Mix 5 Mix 6

U.S. Equities (S&P 500) 100.0% 60.0% 50.0% 45.0% 45.0%

U.S. Fixed Income (Barclays Aggregate) 100.0% 40.0% 40.0% 35.0% 25.0%

International Equity (MSCI ACW ex US) 10.0% 10.0% 10.0%

Real Estate Equity (NCREIF ODCE) 10.0% 10.0%

Hedge Fund of Funds (HFRI) 10.0%

Since 1/1/78 Since 1/1/78 Since 1/1/78 Since 1/1/78

Mix 4 with Real Estate

allocation made on January 1, 2000

Mix 5 with Hedge Fund

allocation made on January 1, 2006.

Selecting an Optimal Mix

I02-25

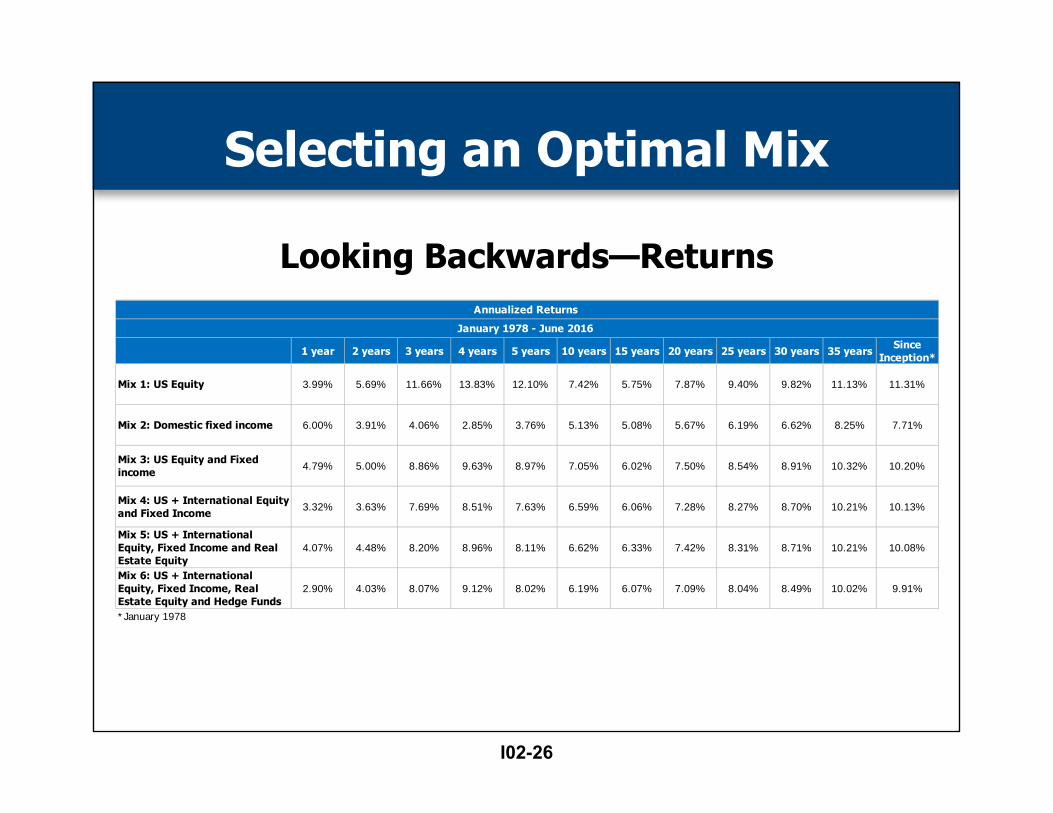

Looking Backwards—Returns

1 year 2 years 3 years 4 years 5 years 10 years 15 years 20 years 25 years 30 years 35 years Since Inception*

Mix 1: US Equity 3.99% 5.69% 11.66% 13.83% 12.10% 7.42% 5.75% 7.87% 9.40% 9.82% 11.13% 11.31%

Mix 2: Domestic fixed income 6.00% 3.91% 4.06% 2.85% 3.76% 5.13% 5.08% 5.67% 6.19% 6.62% 8.25% 7.71%

Mix 3: US Equity and Fixed income 4.79% 5.00% 8.86% 9.63% 8.97% 7.05% 6.02% 7.50% 8.54% 8.91% 10.32% 10.20%

Mix 4: US + International Equity and Fixed Income 3.32% 3.63% 7.69% 8.51% 7.63% 6.59% 6.06% 7.28% 8.27% 8.70% 10.21% 10.13%

Mix 5: US + International Equity, Fixed Income and Real Estate Equity

4.07% 4.48% 8.20% 8.96% 8.11% 6.62% 6.33% 7.42% 8.31% 8.71% 10.21% 10.08%

Mix 6: US + International Equity, Fixed Income, Real Estate Equity and Hedge Funds

2.90% 4.03% 8.07% 9.12% 8.02% 6.19% 6.07% 7.09% 8.04% 8.49% 10.02% 9.91%

*January 1978

Annualized Returns

January 1978 - June 2016

Selecting an Optimal Mix

I02-26

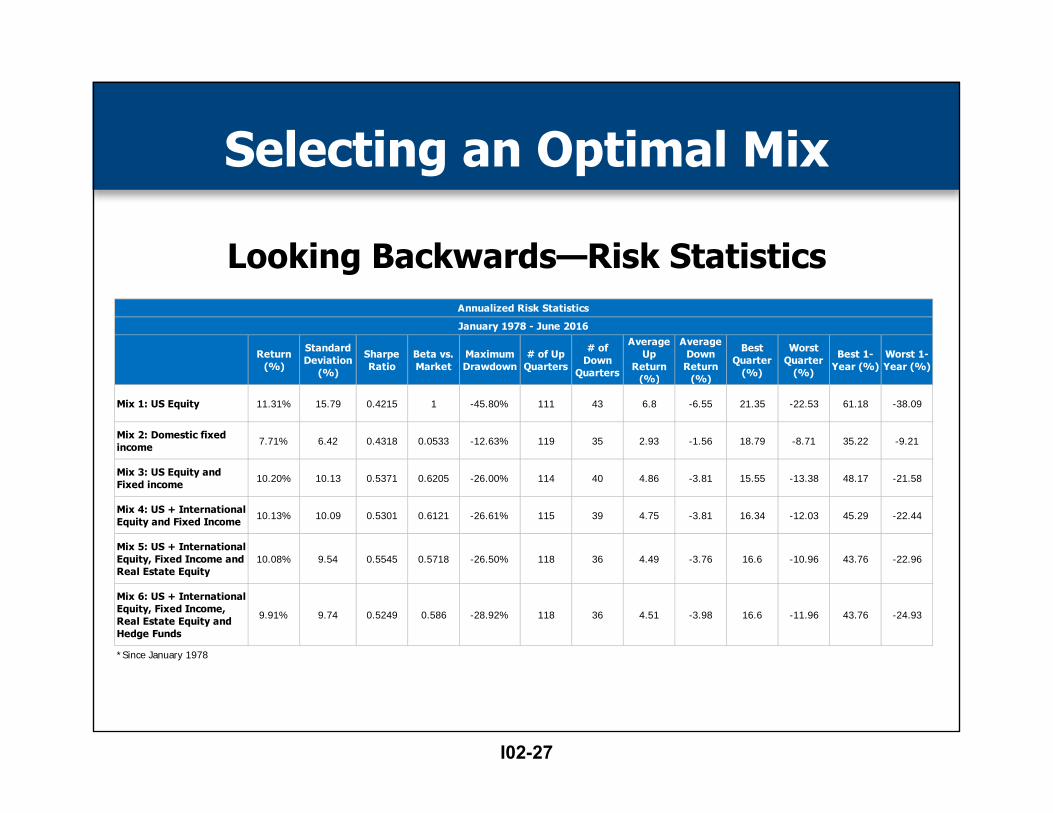

Looking Backwards—Risk Statistics

Return (%)

Standard Deviation

(%)

Sharpe Ratio

Beta vs. Market

Maximum Drawdown

# of Up Quarters

# of Down

Quarters

Average Up

Return (%)

Average Down

Return (%)

Best Quarter

(%)

Worst Quarter

(%)

Best 1-Year (%)

Worst 1-Year (%)

Mix 1: US Equity 11.31% 15.79 0.4215 1 -45.80% 111 43 6.8 -6.55 21.35 -22.53 61.18 -38.09

Mix 2: Domestic fixed income 7.71% 6.42 0.4318 0.0533 -12.63% 119 35 2.93 -1.56 18.79 -8.71 35.22 -9.21

Mix 3: US Equity and Fixed income 10.20% 10.13 0.5371 0.6205 -26.00% 114 40 4.86 -3.81 15.55 -13.38 48.17 -21.58

Mix 4: US + International Equity and Fixed Income 10.13% 10.09 0.5301 0.6121 -26.61% 115 39 4.75 -3.81 16.34 -12.03 45.29 -22.44

Mix 5: US + International Equity, Fixed Income and Real Estate Equity

10.08% 9.54 0.5545 0.5718 -26.50% 118 36 4.49 -3.76 16.6 -10.96 43.76 -22.96

Mix 6: US + International Equity, Fixed Income, Real Estate Equity and Hedge Funds

9.91% 9.74 0.5249 0.586 -28.92% 118 36 4.51 -3.98 16.6 -11.96 43.76 -24.93

*Since January 1978

Annualized Risk Statistics

January 1978 - June 2016

Selecting an Optimal Mix

I02-27

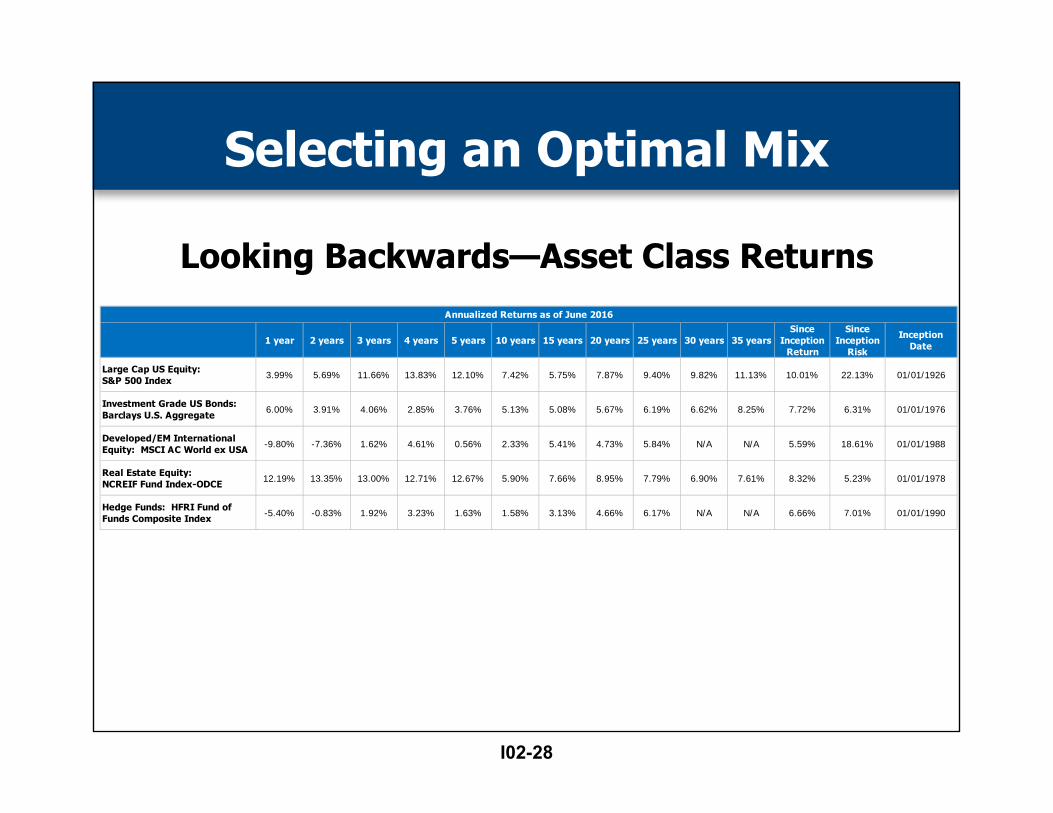

Looking Backwards—Asset Class Returns

1 year 2 years 3 years 4 years 5 years 10 years 15 years 20 years 25 years 30 years 35 yearsSince

Inception Return

Since Inception

Risk

Inception Date

Large Cap US Equity: S&P 500 Index 3.99% 5.69% 11.66% 13.83% 12.10% 7.42% 5.75% 7.87% 9.40% 9.82% 11.13% 10.01% 22.13% 01/01/1926

Investment Grade US Bonds: Barclays U.S. Aggregate 6.00% 3.91% 4.06% 2.85% 3.76% 5.13% 5.08% 5.67% 6.19% 6.62% 8.25% 7.72% 6.31% 01/01/1976

Developed/EM International Equity: MSCI AC World ex USA -9.80% -7.36% 1.62% 4.61% 0.56% 2.33% 5.41% 4.73% 5.84% N/A N/A 5.59% 18.61% 01/01/1988

Real Estate Equity: NCREIF Fund Index-ODCE 12.19% 13.35% 13.00% 12.71% 12.67% 5.90% 7.66% 8.95% 7.79% 6.90% 7.61% 8.32% 5.23% 01/01/1978

Hedge Funds: HFRI Fund of Funds Composite Index -5.40% -0.83% 1.92% 3.23% 1.63% 1.58% 3.13% 4.66% 6.17% N/A N/A 6.66% 7.01% 01/01/1990

Annualized Returns as of June 2016

Selecting an Optimal Mix

I02-28

Selecting an Optimal Mix

Flaws of the analysis• All passive management• Dates on which allocation changes were made are

arbitrary• Target allocations could have been different• Additional asset classes could have been used

Key ConsiderationMust take into consideration the

impact of cash flows

I02-29

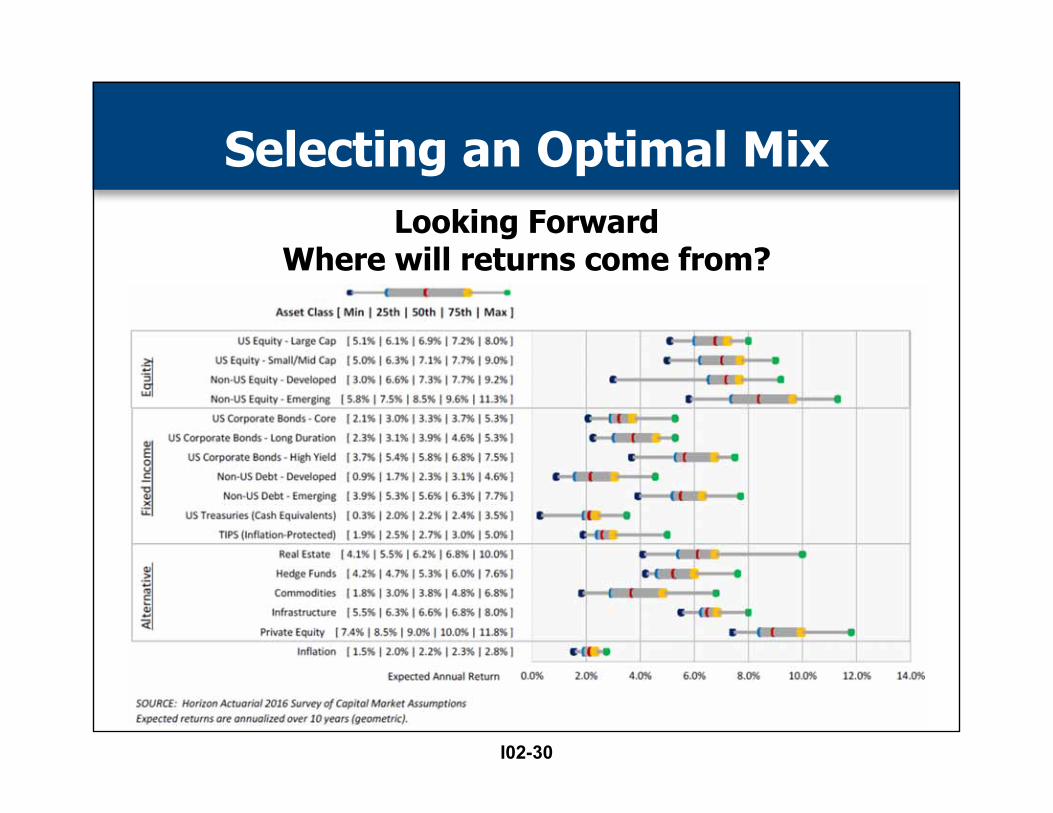

Selecting an Optimal MixLooking Forward

Where will returns come from?

I02-30

‐45

‐35

‐25

‐15

‐5

5

15

25

35

45

55

1926 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s 2010s

Return

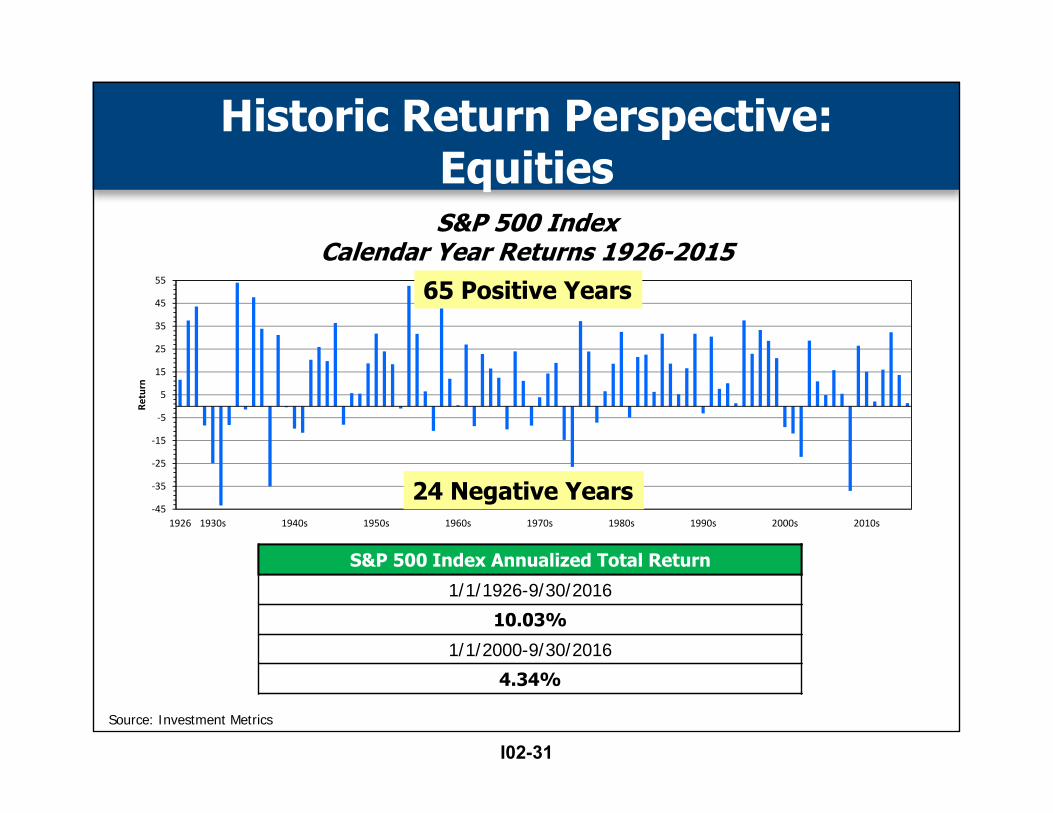

S&P 500 IndexCalendar Year Returns 1926-2015

S&P 500 Index Annualized Total Return

1/1/1926-9/30/2016

10.03%

1/1/2000-9/30/2016

4.34%

Source: Investment Metrics

24 Negative Years

65 Positive Years

Historic Return Perspective: Equities

I02-31

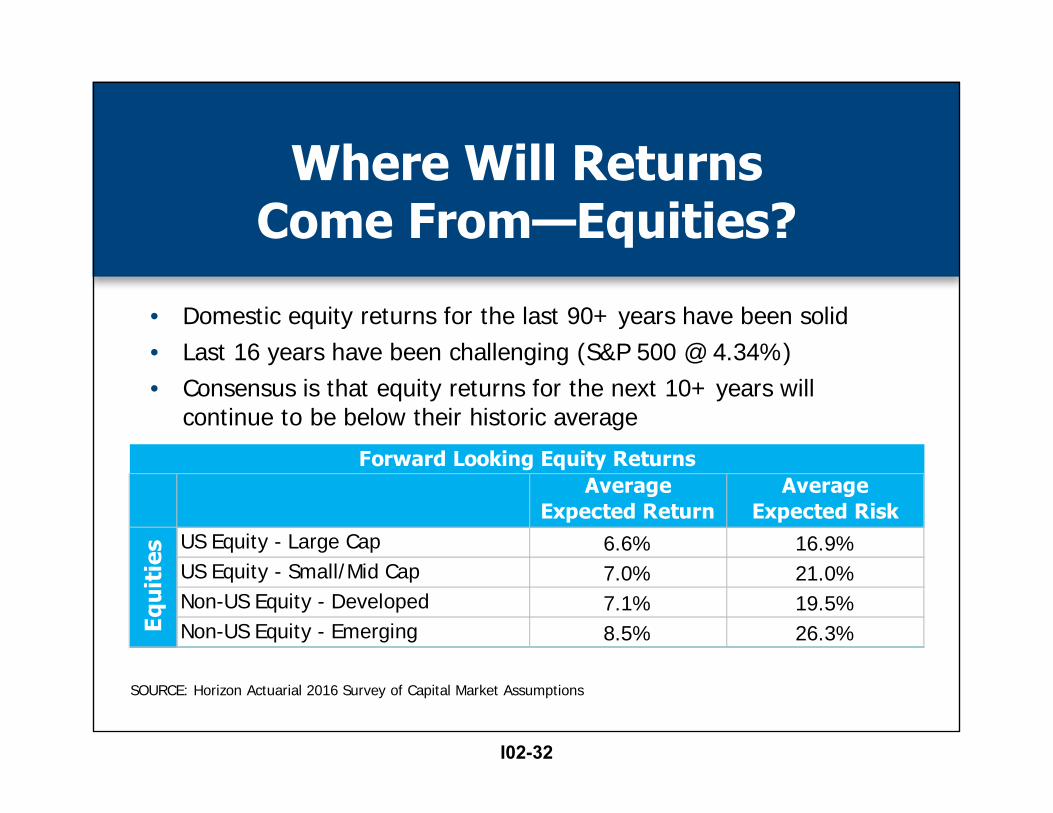

Where Will Returns Come From—Equities?

• Domestic equity returns for the last 90+ years have been solid• Last 16 years have been challenging (S&P 500 @ 4.34%) • Consensus is that equity returns for the next 10+ years will

continue to be below their historic average

SOURCE: Horizon Actuarial 2016 Survey of Capital Market Assumptions

Average Expected Return

Average Expected Risk

US Equity - Large Cap 6.6% 16.9%US Equity - Small/Mid Cap 7.0% 21.0%Non-US Equity - Developed 7.1% 19.5%Non-US Equity - Emerging 8.5% 26.3%

Forward Looking Equity Returns

Equi

ties

I02-32

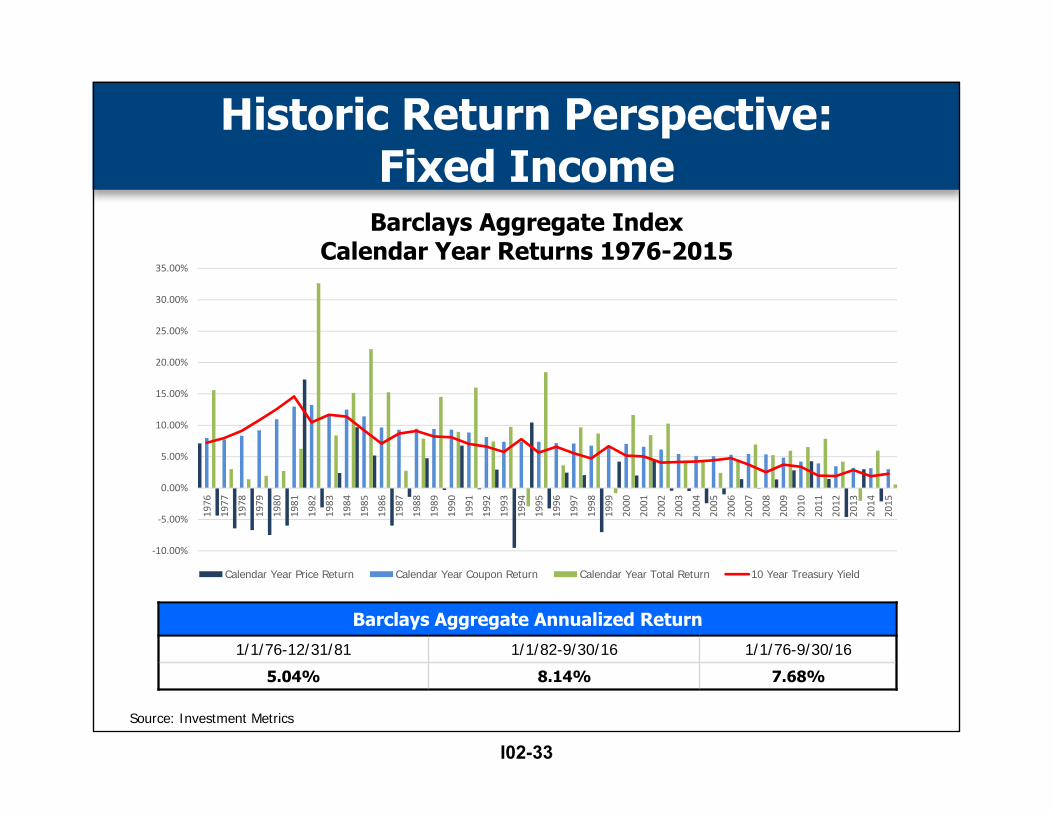

Barclays Aggregate Annualized Return

1/1/76-12/31/81 1/1/82-9/30/16 1/1/76-9/30/16

5.04% 8.14% 7.68%

Source: Investment Metrics

‐10.00%

‐5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Calendar Year Price Return Calendar Year Coupon Return Calendar Year Total Return 10 Year Treasury Yield

Barclays Aggregate IndexCalendar Year Returns 1976-2015

Historic Return Perspective: Fixed Income

I02-33

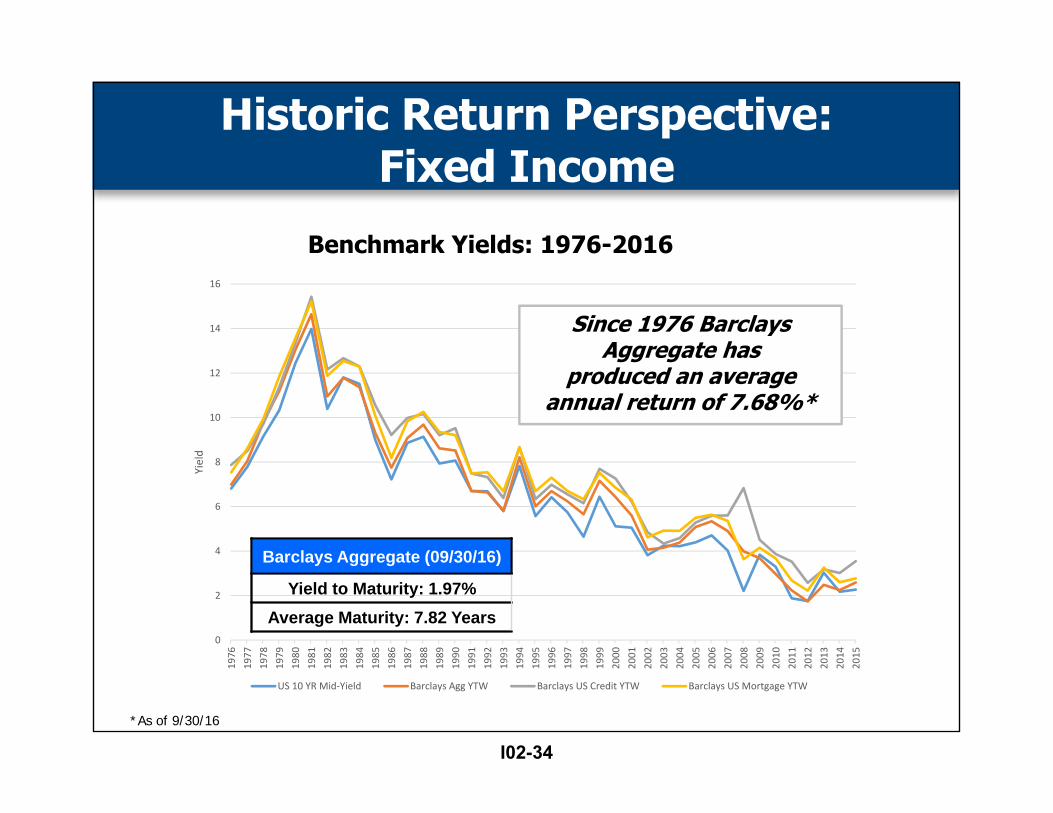

*As of 9/30/16

0

2

4

6

8

10

12

14

16

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Yield

US 10 YR Mid‐Yield Barclays Agg YTW Barclays US Credit YTW Barclays US Mortgage YTW

Since 1976 Barclays Aggregate has

produced an average annual return of 7.68%*

Benchmark Yields: 1976-2016

Barclays Aggregate (09/30/16)

Yield to Maturity: 1.97%Average Maturity: 7.82 Years

Historic Return Perspective: Fixed Income

I02-34

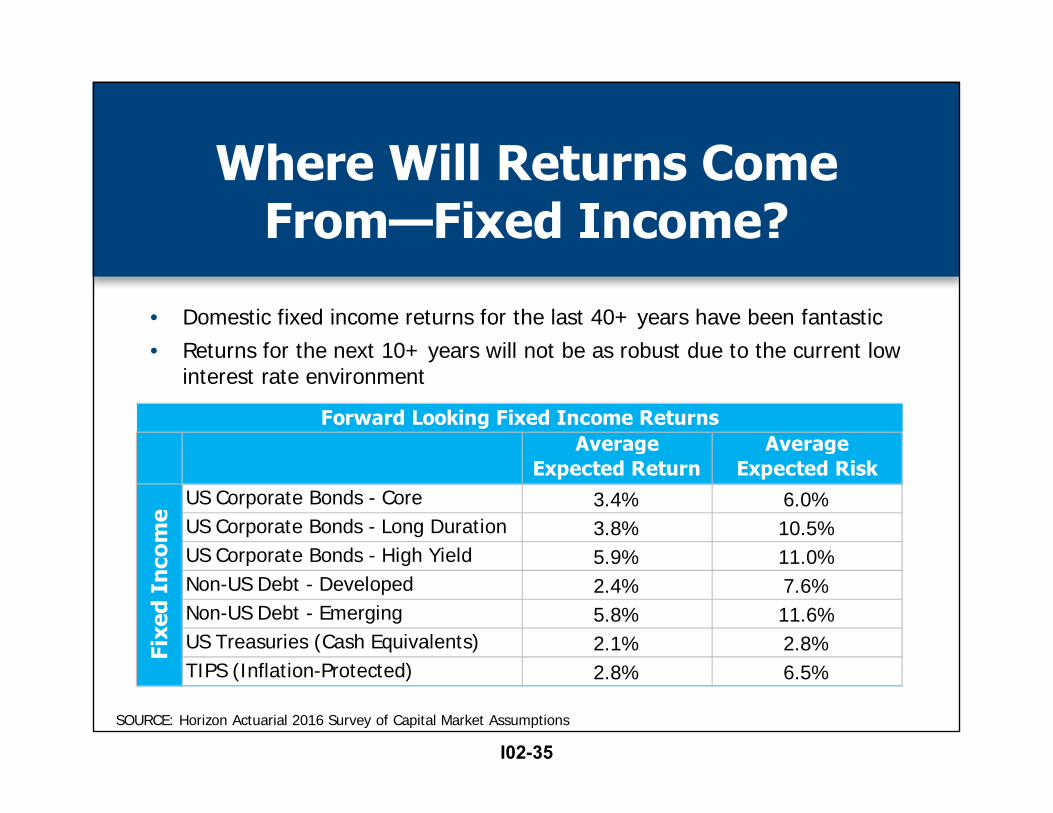

Where Will Returns Come From—Fixed Income?

• Domestic fixed income returns for the last 40+ years have been fantastic• Returns for the next 10+ years will not be as robust due to the current low

interest rate environment

Average Expected Return

Average Expected Risk

US Corporate Bonds - Core 3.4% 6.0%US Corporate Bonds - Long Duration 3.8% 10.5%US Corporate Bonds - High Yield 5.9% 11.0%Non-US Debt - Developed 2.4% 7.6%Non-US Debt - Emerging 5.8% 11.6%US Treasuries (Cash Equivalents) 2.1% 2.8%TIPS (Inflation-Protected) 2.8% 6.5%

Forward Looking Fixed Income Returns

Fixe

d In

com

e

SOURCE: Horizon Actuarial 2016 Survey of Capital Market Assumptions

I02-35

-55.0-35.0-15.0

5.025.045.065.085.0

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ret

urn

(%)

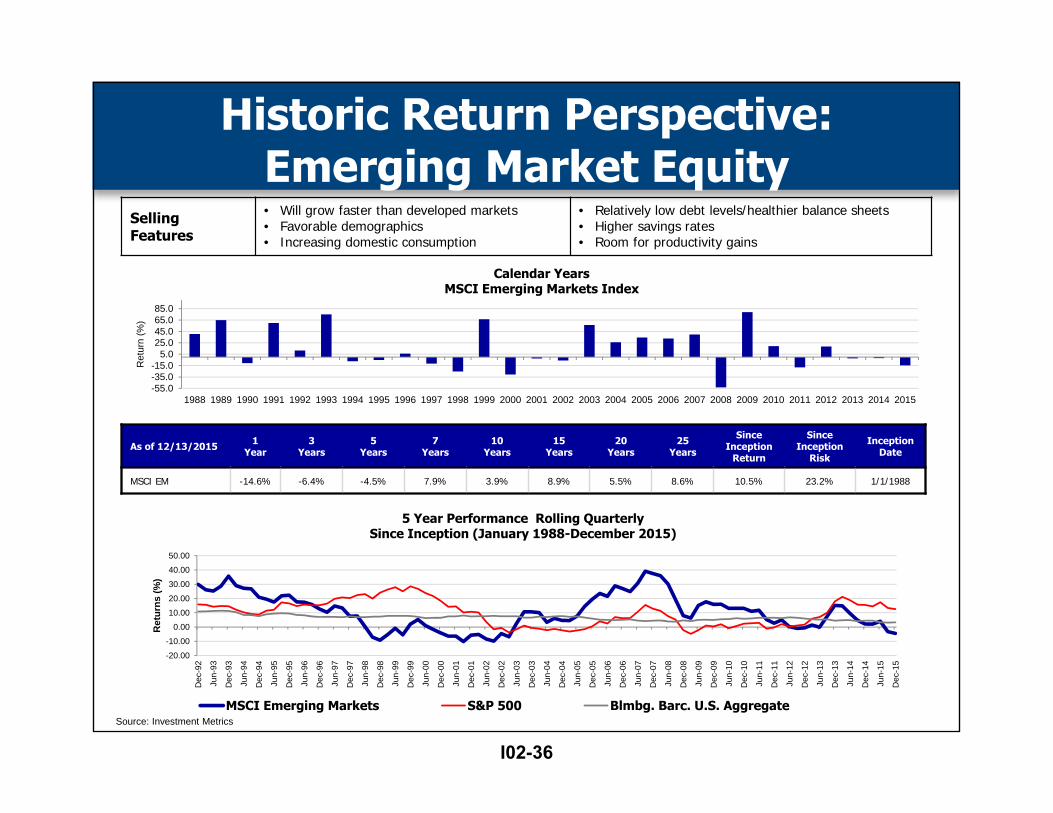

Calendar YearsMSCI Emerging Markets Index

As of 12/13/2015 1Year

3Years

5Years

7Years

10Years

15Years

20Years

25Years

Since Inception

Return

Since Inception

Risk

InceptionDate

MSCI EM -14.6% -6.4% -4.5% 7.9% 3.9% 8.9% 5.5% 8.6% 10.5% 23.2% 1/1/1988

Selling Features

• Will grow faster than developed markets• Favorable demographics• Increasing domestic consumption

• Relatively low debt levels/healthier balance sheets• Higher savings rates • Room for productivity gains

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

Dec

-92

Jun-

93

Dec

-93

Jun-

94

Dec

-94

Jun-

95

Dec

-95

Jun-

96

Dec

-96

Jun-

97

Dec

-97

Jun-

98

Dec

-98

Jun-

99

Dec

-99

Jun-

00

Dec

-00

Jun-

01

Dec

-01

Jun-

02

Dec

-02

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Jun-

14

Dec

-14

Jun-

15

Dec

-15

Ret

urns

(%)

5 Year Performance Rolling QuarterlySince Inception (January 1988-December 2015)

MSCI Emerging Markets S&P 500 Blmbg. Barc. U.S. AggregateSource: Investment Metrics

Historic Return Perspective: Emerging Market Equity

I02-36

-10.00-5.000.005.00

10.0015.0020.0025.0030.0035.00

Dec

-82

Jun-

83D

ec-8

3Ju

n-84

Dec

-84

Jun-

85D

ec-8

5Ju

n-86

Dec

-86

Jun-

87D

ec-8

7Ju

n-88

Dec

-88

Jun-

89D

ec-8

9Ju

n-90

Dec

-90

Jun-

91D

ec-9

1Ju

n-92

Dec

-92

Jun-

93D

ec-9

3Ju

n-94

Dec

-94

Jun-

95D

ec-9

5Ju

n-96

Dec

-96

Jun-

97D

ec-9

7Ju

n-98

Dec

-98

Jun-

99D

ec-9

9Ju

n-00

Dec

-00

Jun-

01D

ec-0

1Ju

n-02

Dec

-02

Jun-

03D

ec-0

3Ju

n-04

Dec

-04

Jun-

05D

ec-0

5Ju

n-06

Dec

-06

Jun-

07D

ec-0

7Ju

n-08

Dec

-08

Jun-

09D

ec-0

9Ju

n-10

Dec

-10

Jun-

11D

ec-1

1Ju

n-12

Dec

-12

Jun-

13D

ec-1

3Ju

n-14

Dec

-14

Jun-

15D

ec-1

5

Ret

urns

(%)

5 Year Performance Rolling QuarterlySince Inception (March 1978-December 2015)

NCREIF ODCE S&P 500 Blmbg. Barc. U.S. Aggregate

As of 12/13/2015 1Year

3Years

5Years

7Years

10Years

15Years

20Years

25Years

Since Inception

Return

Since Inception

Risk

InceptionDate

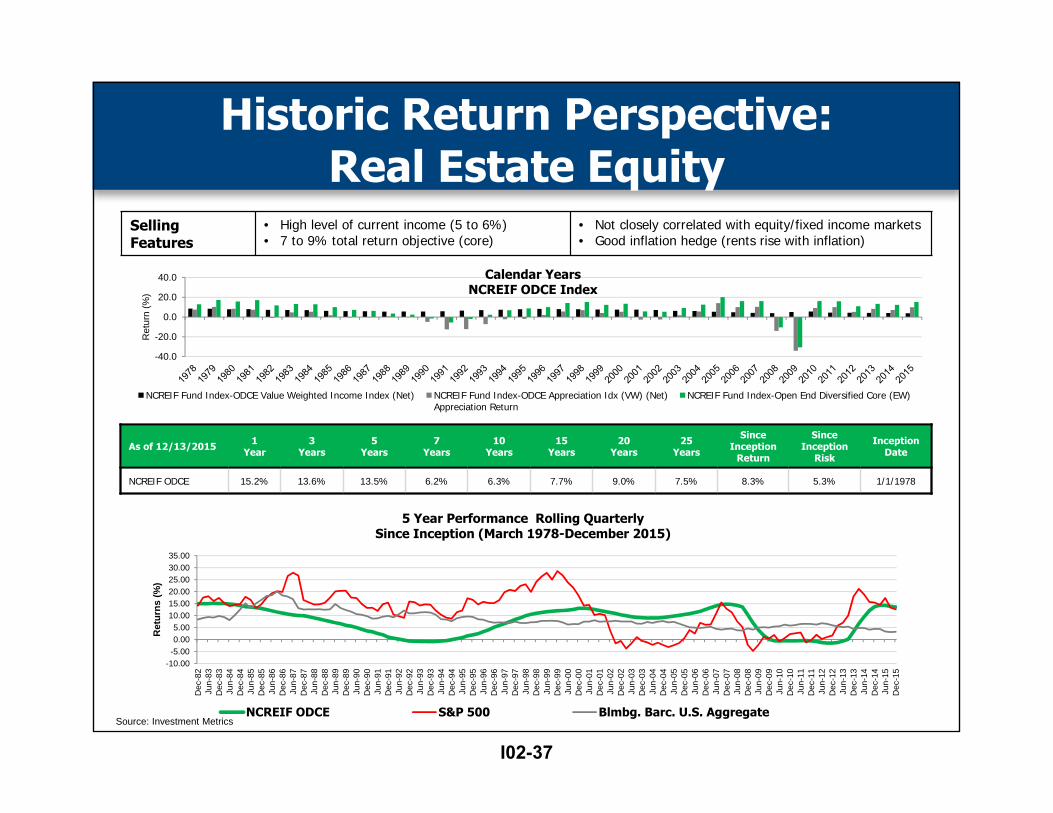

NCREIF ODCE 15.2% 13.6% 13.5% 6.2% 6.3% 7.7% 9.0% 7.5% 8.3% 5.3% 1/1/1978

-40.0

-20.0

0.0

20.0

40.0

Ret

urn

(%)

Calendar YearsNCREIF ODCE Index

NCREIF Fund Index-ODCE Value Weighted Income Index (Net) NCREIF Fund Index-ODCE Appreciation Idx (VW) (Net)Appreciation Return

NCREIF Fund Index-Open End Diversified Core (EW)

Selling Features

• High level of current income (5 to 6%)• 7 to 9% total return objective (core)

• Not closely correlated with equity/fixed income markets• Good inflation hedge (rents rise with inflation)

Source: Investment Metrics

Historic Return Perspective: Real Estate Equity

I02-37

As of 12/13/2015 1Year

3Years

5Years

7Years

10Years

15Years

20Years

Since Inception

Return

Since Inception

Risk

InceptionDate

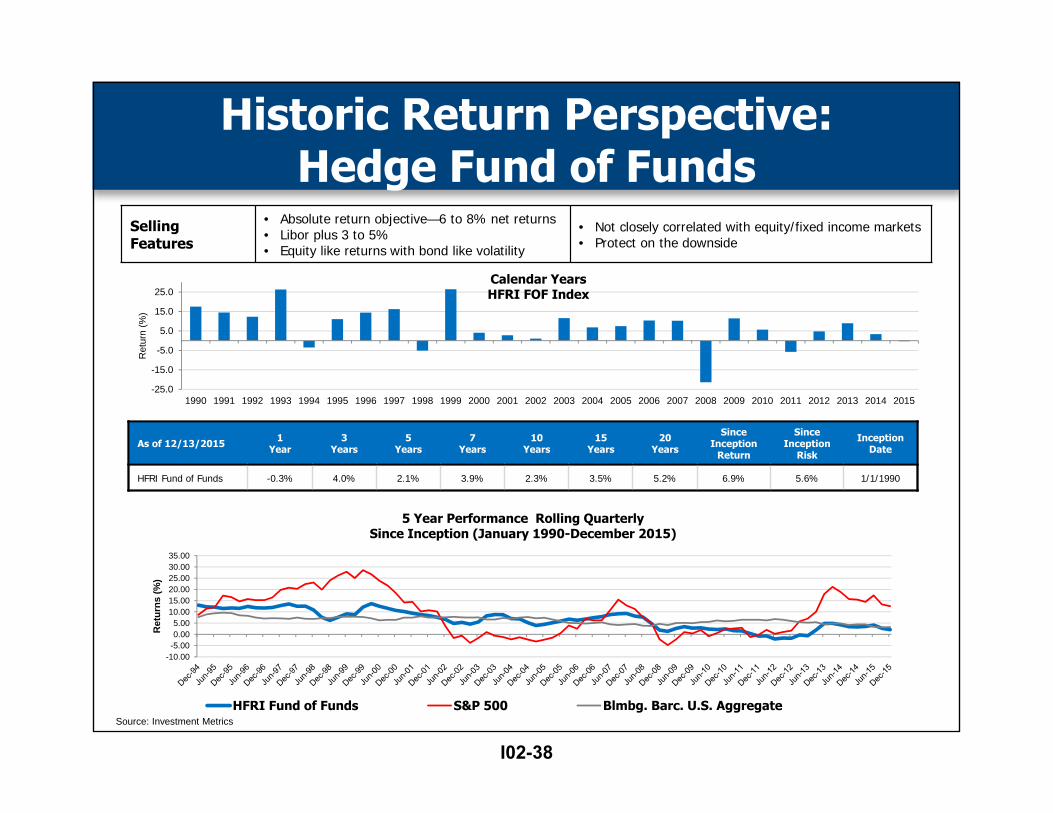

HFRI Fund of Funds -0.3% 4.0% 2.1% 3.9% 2.3% 3.5% 5.2% 6.9% 5.6% 1/1/1990

-25.0

-15.0

-5.0

5.0

15.0

25.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ret

urn

(%)

Calendar YearsHFRI FOF Index

Selling Features

• Absolute return objective—6 to 8% net returns• Libor plus 3 to 5%• Equity like returns with bond like volatility

• Not closely correlated with equity/fixed income markets• Protect on the downside

-10.00-5.000.005.00

10.0015.0020.0025.0030.0035.00

Ret

urns

(%)

5 Year Performance Rolling QuarterlySince Inception (January 1990-December 2015)

HFRI Fund of Funds S&P 500 Blmbg. Barc. U.S. AggregateSource: Investment Metrics

Historic Return Perspective: Hedge Fund of Funds

I02-38

As of 12/13/2015 1Year

3Years

5Years

7Years

10Years

15Years

20Years

Since Inception

Return

Since Inception

Risk

InceptionDate

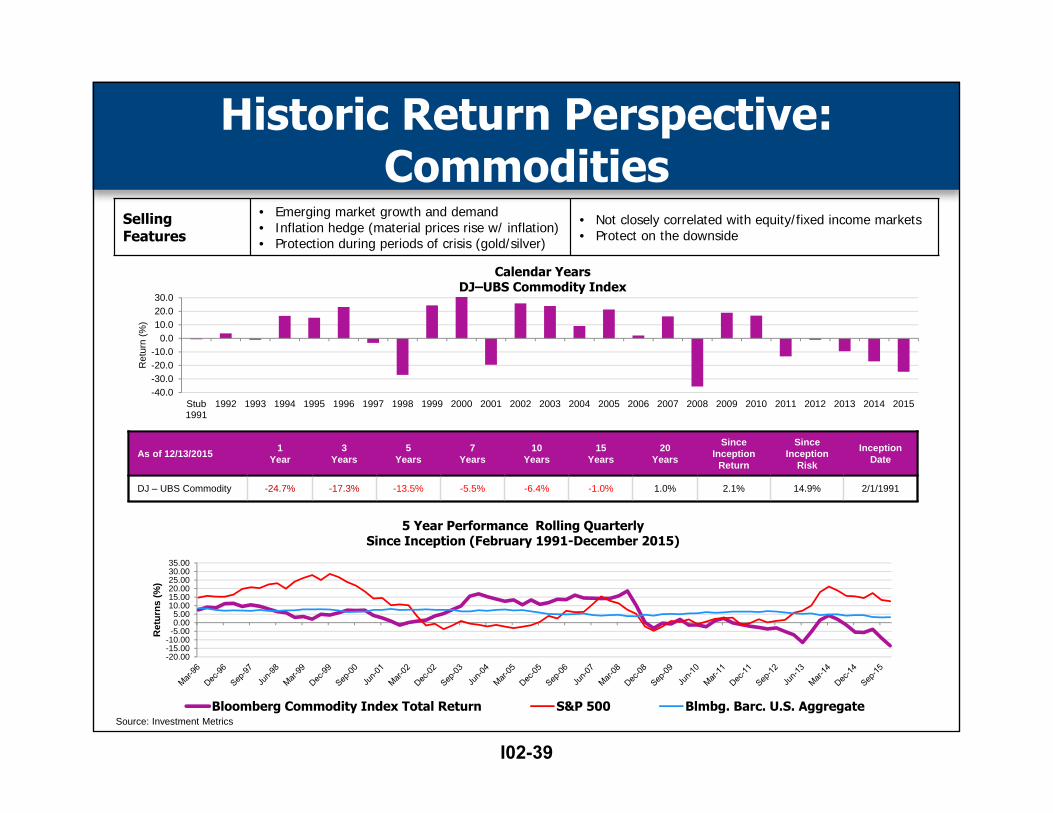

DJ – UBS Commodity -24.7% -17.3% -13.5% -5.5% -6.4% -1.0% 1.0% 2.1% 14.9% 2/1/1991

-40.0-30.0-20.0-10.0

0.010.020.030.0

Stub1991

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ret

urn

(%)

Calendar YearsDJ–UBS Commodity Index

Selling Features

• Emerging market growth and demand• Inflation hedge (material prices rise w/ inflation) • Protection during periods of crisis (gold/silver)

• Not closely correlated with equity/fixed income markets• Protect on the downside

-20.00-15.00-10.00-5.000.005.00

10.0015.0020.0025.0030.0035.00

Ret

urns

(%)

5 Year Performance Rolling QuarterlySince Inception (February 1991-December 2015)

Bloomberg Commodity Index Total Return S&P 500 Blmbg. Barc. U.S. AggregateSource: Investment Metrics

Historic Return Perspective: Commodities

I02-39

-30.0-20.0-10.0

0.010.020.030.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

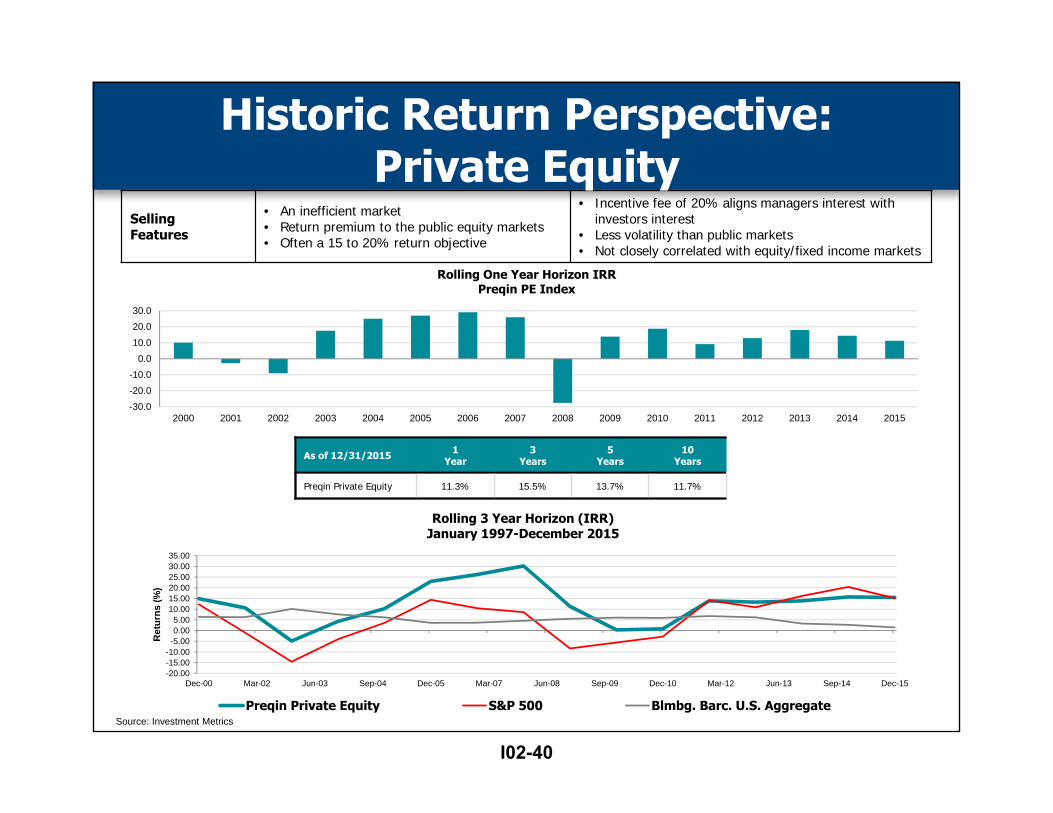

Rolling One Year Horizon IRRPreqin PE Index

As of 12/31/2015 1Year

3Years

5Years

10Years

Preqin Private Equity 11.3% 15.5% 13.7% 11.7%

Selling Features

• An inefficient market• Return premium to the public equity markets• Often a 15 to 20% return objective

• Incentive fee of 20% aligns managers interest with investors interest

• Less volatility than public markets• Not closely correlated with equity/fixed income markets

-20.00-15.00-10.00-5.000.005.00

10.0015.0020.0025.0030.0035.00

Dec-00 Mar-02 Jun-03 Sep-04 Dec-05 Mar-07 Jun-08 Sep-09 Dec-10 Mar-12 Jun-13 Sep-14 Dec-15

Ret

urns

(%)

Rolling 3 Year Horizon (IRR)January 1997-December 2015

Preqin Private Equity S&P 500 Blmbg. Barc. U.S. AggregateSource: Investment Metrics

Historic Return Perspective: Private Equity

I02-40

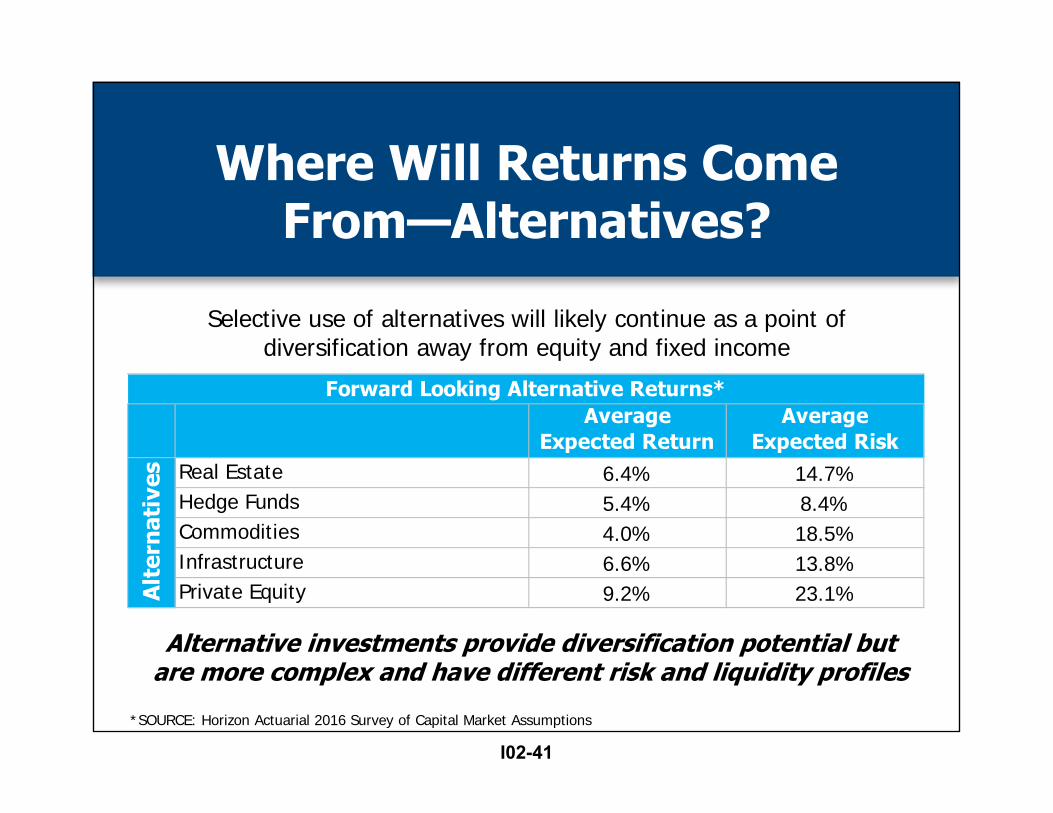

Where Will Returns Come From—Alternatives?

Selective use of alternatives will likely continue as a point of diversification away from equity and fixed income

Average Expected Return

Average Expected Risk

Real Estate 6.4% 14.7%Hedge Funds 5.4% 8.4%Commodities 4.0% 18.5%Infrastructure 6.6% 13.8%Private Equity 9.2% 23.1%A

lter

nati

ves

Forward Looking Alternative Returns*

*SOURCE: Horizon Actuarial 2016 Survey of Capital Market Assumptions

Alternative investments provide diversification potential but are more complex and have different risk and liquidity profiles

I02-41

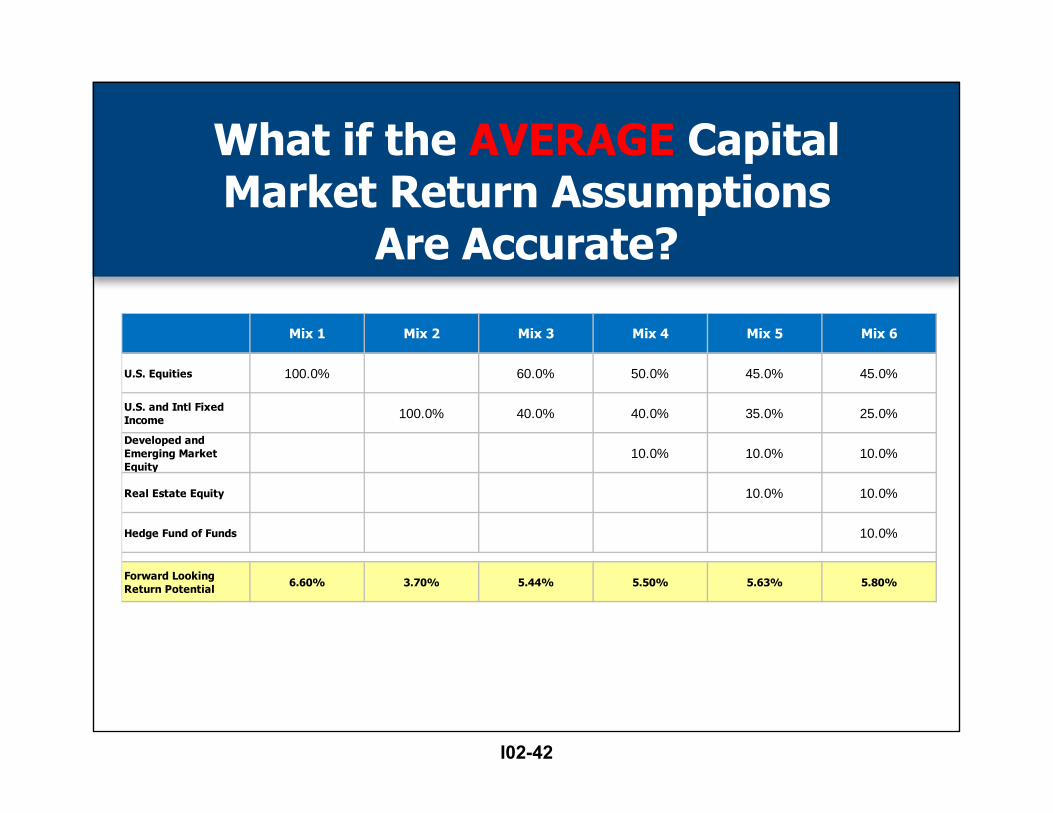

Mix 1 Mix 2 Mix 3 Mix 4 Mix 5 Mix 6

U.S. Equities 100.0% 60.0% 50.0% 45.0% 45.0%

U.S. and Intl Fixed Income 100.0% 40.0% 40.0% 35.0% 25.0%

Developed and Emerging Market Equity

10.0% 10.0% 10.0%

Real Estate Equity 10.0% 10.0%

Hedge Fund of Funds 10.0%

Forward Looking Return Potential 6.60% 3.70% 5.44% 5.50% 5.63% 5.80%

What if the AVERAGE Capital Market Return Assumptions

Are Accurate?

I02-42

Asset Allocation Observations

• Benefit plans have needed and will continue to need equity market returns to achieve their actuarial interest rate assumption.

• Fixed income returns have been fantastic since 1981, but will be challenged in years to come.

• Many points of diversification over the past 16 years have not added value over a 60% equity/40% fixed income portfolio

• Diversification success driven by:– Timing of new allocations.– Performance of managers selected—range of returns in alternative

asset classes is wide.– Degree of diversification—be careful not to diversify too much.

• Must consider risks beyond returns and standard deviation.

I02-43

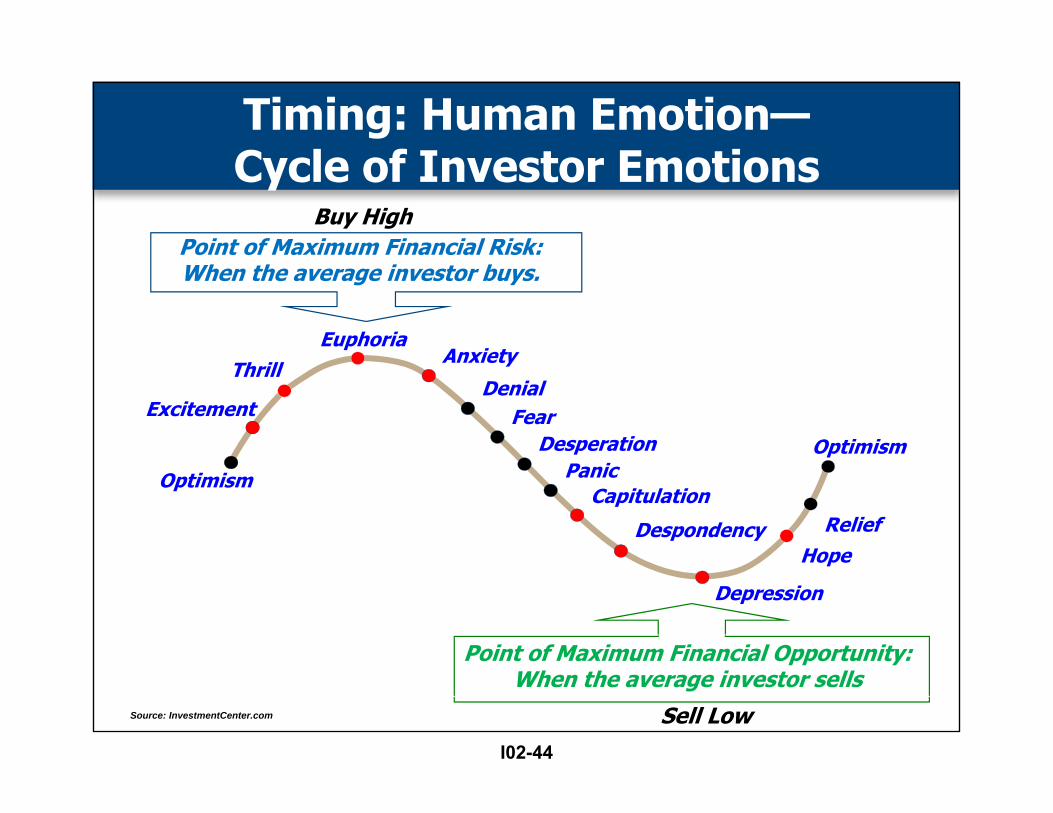

Optimism

Excitement

ThrillEuphoria

AnxietyDenial

FearDesperation

PanicCapitulation

Despondency

Depression

HopeRelief

Optimism

Point of Maximum Financial Risk:When the average investor buys.

Point of Maximum Financial Opportunity:When the average investor sells

Source: InvestmentCenter.com

Buy High

Sell Low

Timing: Human Emotion—Cycle of Investor Emotions

I02-44

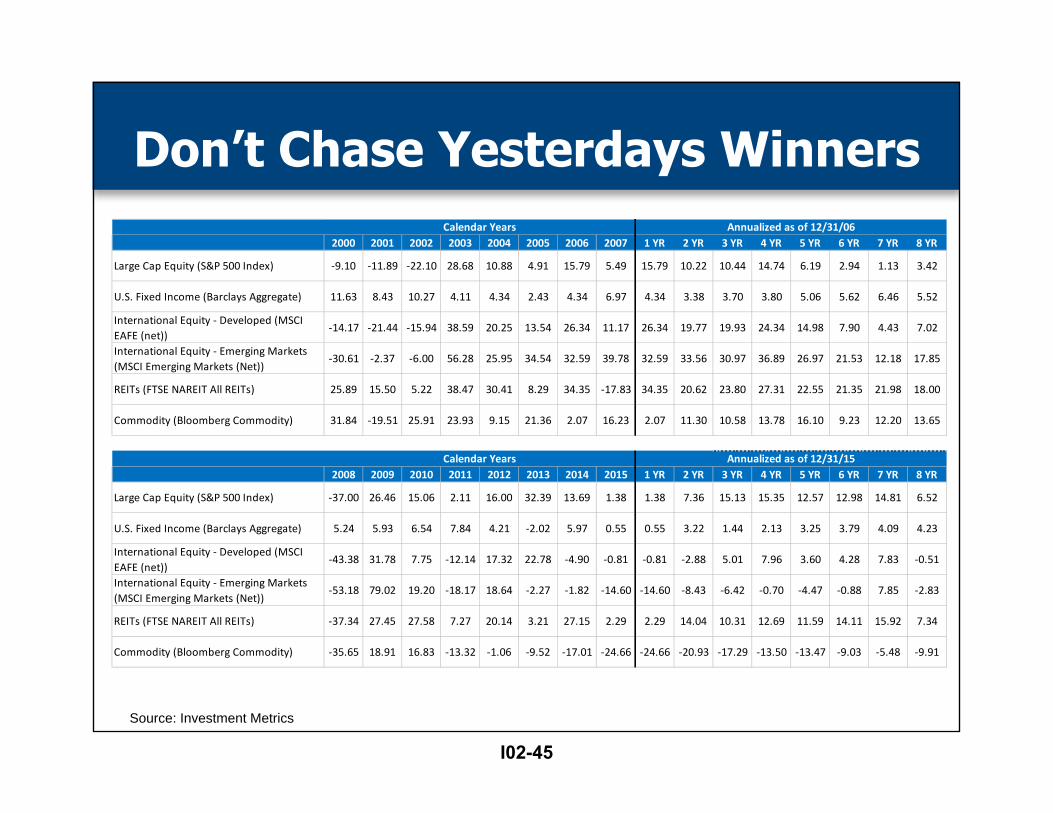

Source: Investment Metrics

2000 2001 2002 2003 2004 2005 2006 2007 1 YR 2 YR 3 YR 4 YR 5 YR 6 YR 7 YR 8 YR

Large Cap Equity (S&P 500 Index) ‐9.10 ‐11.89 ‐22.10 28.68 10.88 4.91 15.79 5.49 15.79 10.22 10.44 14.74 6.19 2.94 1.13 3.42

U.S. Fixed Income (Barclays Aggregate) 11.63 8.43 10.27 4.11 4.34 2.43 4.34 6.97 4.34 3.38 3.70 3.80 5.06 5.62 6.46 5.52

International Equity ‐ Developed (MSCI EAFE (net))

‐14.17 ‐21.44 ‐15.94 38.59 20.25 13.54 26.34 11.17 26.34 19.77 19.93 24.34 14.98 7.90 4.43 7.02

International Equity ‐ Emerging Markets (MSCI Emerging Markets (Net))

‐30.61 ‐2.37 ‐6.00 56.28 25.95 34.54 32.59 39.78 32.59 33.56 30.97 36.89 26.97 21.53 12.18 17.85

REITs (FTSE NAREIT All REITs) 25.89 15.50 5.22 38.47 30.41 8.29 34.35 ‐17.83 34.35 20.62 23.80 27.31 22.55 21.35 21.98 18.00

Commodity (Bloomberg Commodity) 31.84 ‐19.51 25.91 23.93 9.15 21.36 2.07 16.23 2.07 11.30 10.58 13.78 16.10 9.23 12.20 13.65

2008 2009 2010 2011 2012 2013 2014 2015 1 YR 2 YR 3 YR 4 YR 5 YR 6 YR 7 YR 8 YR

Large Cap Equity (S&P 500 Index) ‐37.00 26.46 15.06 2.11 16.00 32.39 13.69 1.38 1.38 7.36 15.13 15.35 12.57 12.98 14.81 6.52

U.S. Fixed Income (Barclays Aggregate) 5.24 5.93 6.54 7.84 4.21 ‐2.02 5.97 0.55 0.55 3.22 1.44 2.13 3.25 3.79 4.09 4.23

International Equity ‐ Developed (MSCI EAFE (net))

‐43.38 31.78 7.75 ‐12.14 17.32 22.78 ‐4.90 ‐0.81 ‐0.81 ‐2.88 5.01 7.96 3.60 4.28 7.83 ‐0.51

International Equity ‐ Emerging Markets (MSCI Emerging Markets (Net))

‐53.18 79.02 19.20 ‐18.17 18.64 ‐2.27 ‐1.82 ‐14.60 ‐14.60 ‐8.43 ‐6.42 ‐0.70 ‐4.47 ‐0.88 7.85 ‐2.83

REITs (FTSE NAREIT All REITs) ‐37.34 27.45 27.58 7.27 20.14 3.21 27.15 2.29 2.29 14.04 10.31 12.69 11.59 14.11 15.92 7.34

Commodity (Bloomberg Commodity) ‐35.65 18.91 16.83 ‐13.32 ‐1.06 ‐9.52 ‐17.01 ‐24.66 ‐24.66 ‐20.93 ‐17.29 ‐13.50 ‐13.47 ‐9.03 ‐5.48 ‐9.91

Annualized as of 12/31/15Calendar Years

Calendar Years Annualized as of 12/31/06

Don’t Chase Yesterdays Winners

I02-45

Session #I02

Asset Allocation in Health and Pension Plans—Your Key Decision

Live by Good Investment Principles:• Allocate sufficient time to focus on the

allocation decision.• Adopt a long-term view. Defined benefit

plan’s have long-term time horizons, but trustees tend to have short-term perspectives.

• Avoid the human emotion related to making investment decisions—don’t chase yesterdays winners.

• Have patience with your asset allocation decisions and active managers.

• Rebalance—trim your winners, add to your out of favor manager.

Website Resourceshttps://www.ifebp.org/inforequest/ifebp/0167444.pdf

62nd Annual Employee Benefits ConferenceNovember 13-16, 2016Orlando, Florida

I02-46

2017 Educational ProgramsInvestments

63rd Annual Employee Benefits Conference October 22-25, 2017 Las Vegas, Nevadawww.ifebp.org/usannual

Investments InstituteMarch 13-15, 2017 Phoenix, Arizonawww.ifebp.org/investments

Portfolio Concepts and ManagementMay 1-4, 2017 Philadelphia, Pennsylvaniawww.ifebp.org/wharton

Related ReadingVisit one of the on-site Bookstore locations or see www.ifebp.org/bookstore for more books.

The Tools & Techniques of Investment Planning, 3rd EditionItem #9029www.ifebp.org/books.asp?9029

816

I02-47