Embed Size (px)

Citation preview

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 139

ASSESMENT OF SERVICE QUALITY IN ETHIOPIAN BANKS (BASED

ONSERVQUAL MODEL): EVIDENCE FROM HAWASSA AND YIRGALEM.

Asegid Getachew (MBA), Lecturer

Hawassa University, College of Business and Economics

Asegid Getachew, Hawassa University

Faculty of Business and Economics, P.O. Box 15, Yirgalem, Ethiopia

ABSTRACT

Service quality measurement has been the main focus of service marketing literature since the development of the famous multiple –

item scale measure of customer perception of service quality in the late 1980’s. A number of researchers have studied the issues in

various organizational setting and have come up with an important finding which have added new theoretical insight .This research in

this regard is was initiated to investigate the issue in the context of the Ethiopian Banking industry.

The research made use of measurement instrument developed by Parasuraman, etal.(1988) to assess the distribution and profile of

service quality dimensions among a selected number of bank customers in Hawassa and Yirgalem. The finding of the research

indicated that there exists a negative gap in customer’s expectation and perception of the quality of service. The findings further

indicated that the negative gap between expectation and perception is quite significant in private banks. The findings of the study will

be informative for bank managers who strive to devise strategies of providing excellent service to their customers by taking in to

account the dynamics of expectation and perception of their customers.

Keywords: Quality, Service Quality, Service Quality Dimensions.

1. INTRODUCTION

In today’s competitive and dynamic business environment the survival and continued growth of organizations is determined by the

level of completive strength that they manage to develop. In this regard as Parasuraman et al., (1988).state intensifying competition

and rapid deregulation have led many service and retail businesses to seek profitable ways to differentiate themselves. And one

strategy as Rudie and Wansley(1985 cited in Bhattacharjee 2010 ) indicate , that has been related to success in these businesses is the

delivery of high service quality. Hence, service quality measurement and improvement is one of the most significant strategic tools for

enhancing efficiency and business growth( Bhattacharjee 2010).

In the service industry, successful companies need more than just a competitive advantage in customer service. They need to have

unwavering loyalty from their customers. The key to providing superior service is to understand and respond to customer expectations.

This is because customers compare perceptions to expectations when judging the quality of a firm’s service offering (Parasuraman et

al., 1988).

Further as Saghier and Nathan (2013) set forth consumers all over the world have become more quality conscious; therefore

customers‟ requirements for higher quality service have been increased. Service sector such as the banks are obliged to provide

excellent services to their customers in order to have sustainable competitive advantage.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 140

Banks play an important and active role in the financial and economic development of a country. An effective banking system greatly

influences the growth of a country in the various sector of the economy. Players in the banking industry face a large number of

complex challenges in the global marketplace. In this regard it is crucial for banks to understand changing customer needs and adopt

the latest information technology system in order to compete more effectively with global organization (Malhorta and Mukherjee,

2004)

As Afrinn (2012) puts it, the banking industry has been increasingly integrated in recent years. Liberalization and deregulation of the

financial sector, coupled with rapid technological advancement and improved communication systems, have contributed to the

integration process. As a result banks now are faced with intense competition. In today’s fast- paced and increasingly competitive

market the bottom line of a firm’s marketing strategy and tactic is to make profit and contribute to the growth of the company.

In the context of Ethiopia the financial sector in general and the banking sector in particular has been showing a remarkable shift.

From 1991 onwards, with the adoption of a new economic system the country has seen the emergence a number of private banks.

These banks, have since then been aggressively expanding throughout the country. Although, banks in Ethiopia, as the findings of

Eshete, etal (2012) suggest are characterized by moderate level of competition, the need to have a competitive edge that will help in

differentiating service delivered to customers is of a paramount importance. Better quality of services provided by banks has a positive

influence on satisfaction of its customers and it directly contributes to profitability of banking industry (Ilyasetal, 2013 ) . And to this

effect, these banks need to understand the dynamics of service quality in the context of the customers they are serving. This paper can,

in this regard, be considered as an initial attempt to investigate the nature of service quality in Ethiopian banks.

1.1 Problem statement

Davi and Ramburuth (2012) , assert that today’s marketing environment is characterized by increased rivalry and changes in many

other macroeconomic variables. One of this is increased competition and it goes without saying that one of the drivers of business

success is having a unique competitive advantage.

As Rahamanetal., ( 2011) assert, quality is the keyword for survival of organizations in the global economy. Organizations are

undergoing a shift from a production-led philosophy to a customer-focused approach. Competitiveness of a firm in the post-liberalized

era is determined by the way it delivers customer service. And in this regard, service quality is an approach to manage business

processes in order to ensure full satisfaction of the customers which will help to increase competitiveness and effectiveness of the

industry. Quality in service is very important especially for the growth and development of service sector business enterprises (Powell,

1995 cited in Rahamanetal., 2011). Therefore, to remain competitive and to excel in the market service delivering firms like banks

need to have a service strategy that takes in to account the expectation and perception of customers.

The concept of service quality ( which is based on the SERVQUAL model developed by Parasuraman, etal 1988) has been studied and

investigated in the banking industry of various countries : The Mauritanian Banking Sector ( Davi and Ramburuth 2012), Hong Kong

Bangink industry (Lau etal.2013), Thecase of commercial Banks in Pengan, Maleysia ( Appananetal., 2013), Banks in Egypt (Saghier

and Nathan 2012), Private commercial banks in Bangladesh ( Rahamanetal., 2011). The case of Commercial banks in Ghana

(Oyetunjietal., 2014)

The service quality model applied in all the above settings measures service quality based the result obtained by analyzing the level of

expectation and perception that customers experience in the service delivery process. And Strauss and Mang( 1999) put, the cultural

interaction between customers and service providers during service encounters might lead to different interpretations, perceptions and

evaluations toward the service performance in the minds of both the customers and the service provider.

Thus as, Winsted (1997a, 1997b cited in Strauss and Mang1999 ), there is hardly any prior discussion about the fact that customers

with different cultural backgrounds may have different expectations toward service encounters and that they may perceive these

situations differently.

The above as a background, the main aim of this paper was to investigate service quality in light of service expectation and perception

of bank customers in Ethiopia. To this effect the research addressed the following questions:

What is the profile of service quality dimensions among bank customers in Ethiopia?

Is there a difference in the distribution of these dimensions between customers of public and private banks?

Is there a variation in service quality dimensions among bank customers due to age differences?

Is there a variation in service quality dimensions among bank customers due to gender differences?

Is there a variation in service quality dimensions among bank customers due to differences in income levels?

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 141

1.2 Theoretical Framework

The conception of Service Quality

The term quality as the originators of the concept (Juran 1974 and Crosby 1979) discuss is quite an elusive concept which describes

conformance to customer requirements. While the substance and determinants of quality may be undefined, its importance to firms

and consumers is unequivocal (Parasuraman ,etal 1985).

Service quality, as opposed to goods quality, is very difficult to operationalize and measure due to the very heterogeneity, perishability

and intangibility of service. There has been a continued research on the definition, modeling, measurement, data collection procedure,

data analysis etc., issues of service quality, leading to development of sound base for the researchers. This documented knowledge

base through several studies on the subject can be of great use to researchers and practitioners in providing a direction on how to

explore/modify the existing service quality concepts with the changing world scenario (shift from conventional personalized services

to web enabled services). (Seth 2004)

Two most popular model of service quality have been considered as seminal and influential in the service quality literature. The fist

model is the one developed by Parasuraman et al. (1985) .the Model goes by the name SERVQUAl ( also termed as Anglo-Saxion

model ). And the one associated with Gronroos (1990) is referred to as NORDIC model of service quality.

The most well-known model is the model of Parasuraman et al. (1985) which is widely utilized in the literature. The model attempts to

show the salient activities of the service organization that influence the perception of quality. Moreover, the model shows the

interaction between these activities and identifies the linkages between the key activities of the service organization or marketer which

are pertinent to the delivery of a satisfactory level of service quality.

Parasuraman et al. (1985) proposed that service quality is a function of the differences between expectation and performance along the

quality dimensions. They developed a service quality model (Figure 1) based on gap analysis. These gaps as Shahin andSamea( 2010)

discuss have the following elements

Gap 1: Customer expectation-management gap. This gap addresses the difference between consumers’ expectations and

management’s perceptions of service quality.

Gap 2: Management perception-service quality specifications gap. This gap addresses the difference between management’s

perceptions of consumer’s expectations and service quality specifications, i.e. improper service-quality standards.

Gap 3: Service quality specification-service delivery gap. This gap addresses the difference between service quality

specifications and service actually delivered, i.e. the service performance gap.

Gap 4: Service delivery-external communication gap. This gap addresses the difference between service delivery and the

communications to consumers about service delivery, i.e. whether promises match delivery.

Gap 5: Expected service-perceived service gap. This gap addresses the difference between consumer’s expectation and

perceived service. This gap depends on size and direction of the four gaps associated with the delivery of service quality on

the marketer’s side.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 142

Figure 1 Service Quality gaps.

In the Nordic model of service quality, popularised by ChristiaanGrönroos(1990) total perceived service quality is the outcome of an

evaluation process where the customer compares context specific expectations of quality with the experienced quality. The

expectations of quality are context specific to the firm under consideration and not based on the total class of service providers, as is

the case in the Anglo-Saxon model. The expected service is influenced by the marketing activities of the service provider and external

influences, such as word-of-mouth, corporate image and customer needs.

In the Nordic model, the outcome of the service and the process of service delivery are both recognized as forming part of the

experienced quality.

Figure 2The Nordic Model

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 143

Measurement of Service quality

Service quality, although very difficult to operationalize, is in most situations measured by the five dimensions and their

corresponding twenty two elements developed by Parasuraman et al. (1985)

1. Tangibles. Physical facilities, equipment’s and appearance of personnel.

2. Reliability. Ability to perform the promised service dependably and accurately.

3. Responsiveness. Willingness to help customers and provide prompt service.

4. Assurance (including competence, courtesy, credibility and security). Knowledge and courtesy of employees and their ability

to inspire trust and confidence.

5. Empathy (including access, communication, understanding the customer). Caring and individualizedattention that the firm

provides to its customers.

2 MATERIALS AND METHODS

2.1 Description of the study area and subjects

Subjects participating in the research were customers of private banks residing in Hawassa and Yirgalem, both of which are fond in

the Southern Nations Nationalities and Peoples Regional State (SNNPRS). The former being capital of the region and the latter a

major town in Dale Wroreda. Currently the branches of at least nine commercial (Private and Public) banks are operating in the

selected study areas.

2.2 Study design

The participant of the study were selected using a non-probability convenience method of sampling. The method is selected because it

gives the researcher the freedom to select respondents who are relevant for the study.

The total number of respondents for the study is determined using a sample size determination formula developed by Krejcie and

Morgan (1970). Since the target population for the research is infinite, a total of 384 ( which is taken from the sample size table

developed by Krejcie and Morgan (1970) ) respondents were planned to be considered sufficient for the study. However only 100

questioners were completed and returned form the respondents ,corresponding to a response rate of 26%

2.3 Study methodology

The instrument used in collecting data for the study was a questionnaire having two parts. The first part of the questionnaire was ued

to collect data related to some, basic background variable like age , gender , income level , etc. The second and major part of the

questionnaire related specifically to the focal concept of the study, Service quality. To measure service quality the study made use of a

multiple-item scale for measuring consumers’ perception of service quality (alias SERVQUAL).

This measurement scale was initially developed by parasuraman, Zeithaml, and Berry (1988) and was latter refined by the same

authors parasuraman, Berry, and Zeithaml (1991) . The scale has been considered as a standard for measuring service quality

throughout the service marketing literature. In its original form, SERVQUAL contains 22 pairs Likert scale statements structured

around five service quality dimensions in order to measure service quality (Cronin and Taylor, 1992 cited in Safakli 2007).

Each statement appears twice. One measures customer expectations of a particular service industry. The other measures the perceived

level of service provided by an individual organization in that industry. The 22 pairs of statements are designed to fit into the five

dimensions of service quality. A seven-point scale ranging from “strongly agree” (7) to “strongly disagree” (1) accompanies each

statement. The “strongly agree” end of scale is designed to correlate with high expectations and high perceptions. Service quality

occurs when expectations are met (or exceeded) and a service gap materializes if expectations are not met. The gap score for each

statement is calculated as the perception score minus the expectation score. A positive gap score implies that expectation have been

met or exceeded and a negative score implies that expectations are not being met. Gap scores can be analyzed for each individual

statement and can be aggregated to give an overall gap score for each dimension (Parasuraman at al., 1988).

2.4 Data management and analysis

The data obtained by distributing questionnaires to the selected professionals was analyzed with the help of SPSS for windows. In this

regard descriptive, correlation and inferential statistics will be used to manipulate the variables of the research. A simple comparison

of the mean results of service quality expectation and perception of customers for each attribute was made to asses’ service quality.

The strength of association between each attribute, the major dimensions of service quality and selected background variables was

measured using correlation analysis.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 144

3 Results and Discussions

The following section presents the results obtained after the analysis of data using different statistical techniques.

Table 1 Background Information

Sex

Frequency Percent

Male 73 73

Female 27 27

Total 100 100

Marital status Frequency Percent

MARRIED 40 40

UNMARRIED 60 60

Total 100 100

Academic level

Frequency Percent

B.A 77 77

MA/MBA/MSC 22 22

Total 99 99

Total 100 100

Salary category

Frequency Percent

Below 2450 25 25

2451-3450 26 26

3450-5500 26 26

5500-8000 22 22

Total 100 100

Client

Frequency Percent

Government 88 88

Private 11 11

Total 100 100

As the data in Table 1. Indicates the respondents of the research are predominantly (73%) male and the remaining 27% female. And of

the total respondents 60% are single and 41 married. With regards to educational level 77 % of the respondents have a BA degree and

22 MSc /MBA. 95.5% of the respondents are within the age of 18-65 and the rest 5% are above the age of 65. 25% of the respondent

earn a monthly income of less than Br. 2500 , 26% of the respondents lie within a monthly income range of 2,451-5,500 Br. And 22%

of the respondents earn a monthly income greater than 8,000 .Majority of the respondent (88% 0 are currently clients of government

banks and the remaining 22% are affiliated with private banks.

3.1 Service quality Gap for each dimension

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 145

Tangibles D

imen

sio

ns

Items

Perception Expectation Difference

Individua

l MEAN

Group

MEAN

Individual

MEAN

Group

MEA

N

Individual

MEAN

Group

MEAN

Ta

ng

ibles

1) Banks should have modern looking

equipment. . 3.86

4.48

-0.62

2) The physical facilities at Banks

should be visually appealing 3.66 4.30 -0.64

3) Employees at Banks should be neat

appearing 3.96 4.05 -0.09

4) Material and information

associated with the service should

be visually appealing. 3.64 3.78 4.28 4.28 -0.64 -0.499

Tangibles basically indicate the appearance of the physical facilities of banks, the physical appearance of employees and the

attractiveness of materials and information to the customer. As the service quality gap analysis in the above table indicates, all items

measuring perception and expectation of customers have a negative gap. The highest gap relates to item “ no 4” and item no”2”

relating to the appalling perception that customers have experienced regarding the physical facilities and materials and information’s

associated with the service they received.

Table 2 Dimension Reliability

Dim

ensio

ns Items

Perception Expectation Difference

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Rel

iab

ilit

y.

1) When the Bank promise to do

something by a certain time, it

does so. 3.50

5.14

-1.64

2) When a customer has a problem,

the Banks’s staff are

sympathetic and reassuring. 3.56 4.27 -0.71

3) The Bank performs the service

right the first time. 3.56 4.25 -0.69

4) The Bank provides the service

at the time it promises to do so. 3.57 3.92 -0.35

5) The Bank keeps its records

accurately 4.00 3.638 4.05 4.33 -0.05 -0.689

The reliability item basically explains the timing with which service is performed ,the level of sympathy and reassurance that staffs of

the bank show to customer , the impression that customers have regarding their first encounter , whether service is done as promised

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 146

and the accuracy of record kept by the bank. As the result summarized in table -2 above indicates the gap between the items measuring

perception and expectation is negative. The highest gap reported relates to item number (1) indicating that most respondents perceive

that banks do not do what they have promised in the time they promised to do it. The lowest gap observed relates to the perception that

customers have regarding records kept by banks.

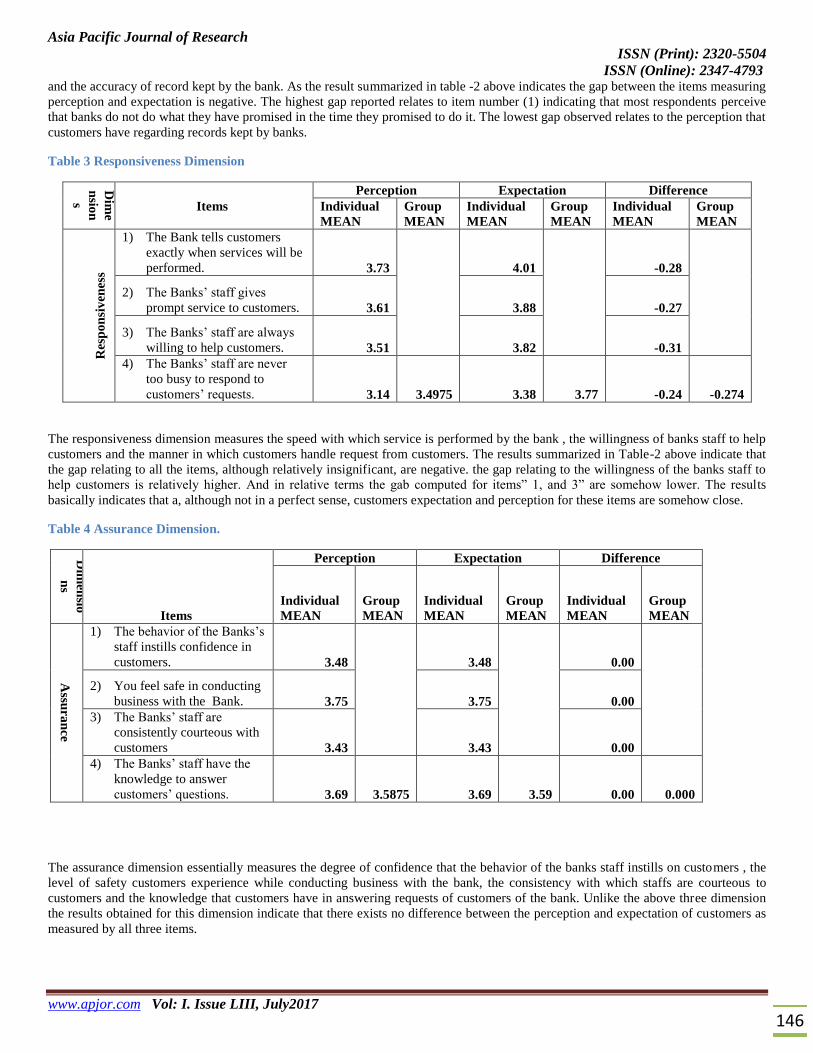

Table 3 Responsiveness Dimension

Dim

e

nsio

n

s Items

Perception Expectation Difference

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Res

po

nsi

ven

ess

1) The Bank tells customers

exactly when services will be

performed. 3.73

4.01

-0.28

2) The Banks’ staff gives

prompt service to customers. 3.61 3.88 -0.27

3) The Banks’ staff are always

willing to help customers. 3.51 3.82 -0.31

4) The Banks’ staff are never

too busy to respond to

customers’ requests. 3.14 3.4975 3.38 3.77 -0.24 -0.274

The responsiveness dimension measures the speed with which service is performed by the bank , the willingness of banks staff to help

customers and the manner in which customers handle request from customers. The results summarized in Table-2 above indicate that

the gap relating to all the items, although relatively insignificant, are negative. the gap relating to the willingness of the banks staff to

help customers is relatively higher. And in relative terms the gab computed for items” 1, and 3” are somehow lower. The results

basically indicates that a, although not in a perfect sense, customers expectation and perception for these items are somehow close.

Table 4 Assurance Dimension.

Dim

ensio

ns

Items

Perception Expectation Difference

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Assu

ran

ce

1) The behavior of the Banks’s

staff instills confidence in

customers. 3.48

3.48

0.00

2) You feel safe in conducting

business with the Bank. 3.75 3.75 0.00

3) The Banks’ staff are

consistently courteous with

customers 3.43 3.43 0.00

4) The Banks’ staff have the

knowledge to answer

customers’ questions. 3.69 3.5875 3.69 3.59 0.00 0.000

The assurance dimension essentially measures the degree of confidence that the behavior of the banks staff instills on customers , the

level of safety customers experience while conducting business with the bank, the consistency with which staffs are courteous to

customers and the knowledge that customers have in answering requests of customers of the bank. Unlike the above three dimension

the results obtained for this dimension indicate that there exists no difference between the perception and expectation of customers as

measured by all three items.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 147

Table 5 Empathy Dimension.

The empathy dimension basically describes whether the banks staff give customers individual attention, the convenience of the banks

operating hours to all customers , the level of personal attention given by the banks staff to customers , the degree of importance

attached to customers bets interest and whether the banks staff understand specific need s of customers. As can be seen in Table two

the results obtained for this dimension, similar to the Assurance dimension tend to indicate that the gap between the expectation and

perception of customers pertaining to all the items is almost zero.

The overall gap computed for each dimension, reported in Table-6 above) indicates that there exists a significant ( relatively speaking)

gap relating to customers expectation and perception for Tangibles , reliability and Responsiveness dimension. The gap reported for

the Assurance and Empathy dimension indicate an insignificant zero difference.

Dim

ensio

ns

Perception Expectation Difference

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Individual

MEAN

Group

MEAN

Em

pa

thy

1) The Banks gives customers

individual attention. 3.55

3.55

0.00

2) The Bank has operating hours

convenient to all their

customers. 3.55 3.55 0.00

3) The Bank has employees who

give customers personal

attention 3.46 3.46 0.00

4) The Bank have their

customer’s best interest at

heart. 3.46 3.46 0.00

5) The Banks’ staff understand

the specific needs of their

customers. 3.44 3.492 3.44 3.49 0.00 0.000

Table 6 Overall Gaps

Dimensions

Gap

Tangibles -0.49863

Reliability -0.68895

Responsiveness -0.27351

Assurance 0

Empathy 0

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 148

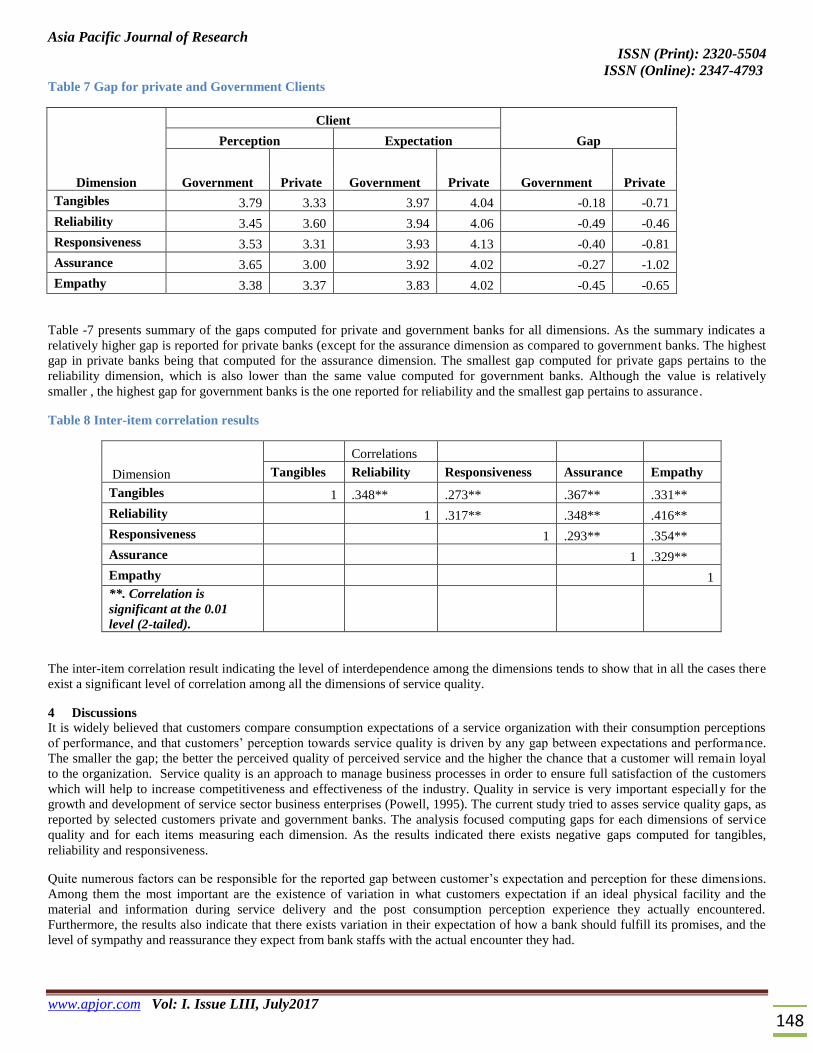

Table 7 Gap for private and Government Clients

Dimension

Client

Gap Perception Expectation

Government Private Government Private Government Private

Tangibles 3.79 3.33 3.97 4.04 -0.18 -0.71

Reliability 3.45 3.60 3.94 4.06 -0.49 -0.46

Responsiveness 3.53 3.31 3.93 4.13 -0.40 -0.81

Assurance 3.65 3.00 3.92 4.02 -0.27 -1.02

Empathy 3.38 3.37 3.83 4.02 -0.45 -0.65

Table -7 presents summary of the gaps computed for private and government banks for all dimensions. As the summary indicates a

relatively higher gap is reported for private banks (except for the assurance dimension as compared to government banks. The highest

gap in private banks being that computed for the assurance dimension. The smallest gap computed for private gaps pertains to the

reliability dimension, which is also lower than the same value computed for government banks. Although the value is relatively

smaller , the highest gap for government banks is the one reported for reliability and the smallest gap pertains to assurance.

Table 8 Inter-item correlation results

Dimension

Correlations

Tangibles Reliability Responsiveness Assurance Empathy

Tangibles 1 .348** .273** .367** .331**

Reliability 1 .317** .348** .416**

Responsiveness 1 .293** .354**

Assurance 1 .329**

Empathy

1

**. Correlation is

significant at the 0.01

level (2-tailed).

The inter-item correlation result indicating the level of interdependence among the dimensions tends to show that in all the cases there

exist a significant level of correlation among all the dimensions of service quality.

4 Discussions

It is widely believed that customers compare consumption expectations of a service organization with their consumption perceptions

of performance, and that customers’ perception towards service quality is driven by any gap between expectations and performance.

The smaller the gap; the better the perceived quality of perceived service and the higher the chance that a customer will remain loyal

to the organization. Service quality is an approach to manage business processes in order to ensure full satisfaction of the customers

which will help to increase competitiveness and effectiveness of the industry. Quality in service is very important especially for the

growth and development of service sector business enterprises (Powell, 1995). The current study tried to asses service quality gaps, as

reported by selected customers private and government banks. The analysis focused computing gaps for each dimensions of service

quality and for each items measuring each dimension. As the results indicated there exists negative gaps computed for tangibles,

reliability and responsiveness.

Quite numerous factors can be responsible for the reported gap between customer’s expectation and perception for these dimensions.

Among them the most important are the existence of variation in what customers expectation if an ideal physical facility and the

material and information during service delivery and the post consumption perception experience they actually encountered.

Furthermore, the results also indicate that there exists variation in their expectation of how a bank should fulfill its promises, and the

level of sympathy and reassurance they expect from bank staffs with the actual encounter they had.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 149

Last but not least results computed indicate the existence of negative deviation with regards to customers expectation of getting prior

information regarding timing of service delivery, the speed with which service is performed and the willingness of banks staff to help

them. However, the results obtained for the assurance and empathy dimensions showed no deviation between expectation and

perception. The result somehow indicates that customers feel confidence and safety transacting with the banks and that they believe

that banks staff have the requisite knowledge to cater to their requests. The other important implication of these result is that there is a

match between customers expectation and perception regarding the individual attention they receive from banks, the convenience of

operating hours and the value given to their special interest.

The study has also tried to assess service quality gaps from the perspective of government and private bank customers. The results

obtained differ from the aggregate result discussed for each dimension. To this effect, the results indicate that government banks are

better in handling expectation of their customers. The results computed for checking inter-item correlation if the individual dimensions

indicated the existence of significant positive interdependence among them, implying that the management of service quality cannot

be effective unless it considers the interplay among the five dimensions.

5 Conclusion and Implication for future Research.

During the past few decades service quality has become a major area of attention topractitioners, managers and researchers owing to

its strong impact on business performance, lower costs, customer satisfaction, customer loyalty and profitability Seth,Netal P (2004).

The current study mainly focused on assessing the service quality gaps observed in selected commercial banks (Government and

Private) in Ethiopia, and as Saghier E,N., Nathan ,D(2013) state SERVQUAL appears to be a reliable scale to measure banking

service quality, and provide a useful diagnostic role to play in assessing and monitoring service quality in banks. To this end, the study

used SERVQUAL to assess existing service quality expectation and perception gaps. the results of the study have tremendous

implications for both organizational practice and future research’s planned to be undertaken in the area.

Banks have to understand the changing needs of customers, their aspirations and expectations to create value. Banks should also have

a strong customer relationship management system that would indicate the worth of the customer and be able to understand his needs

while interacting with him, so as to cross sell their products. The study most of all is very important for management of Banks who

must continuously devise strategies on how to excel by attracting more customers and making these customers more loyal. To

compete in the existing market by providing quality service to customers banks need to primarily understand the dynamics of

customers’ expectations and perception.

SERVQUAL is the most valuable when it is used periodically to track service quality trends , and when it is used in conjunction with

other forms of service quality measurement. Parasuramanetal (1988). To this effect although the results of the current research are an

important input in revealing the reality regarding service quality in banks it cannot by itself be considered as a definitive answer to the

probls of service quality.

The results of the study confirm to the findings of Parasuramanetal( 1991) that indicates SERVQUAL dimension represent five

conceptually distinct facets of service quality which are very interrelated. This has a critical message to practice as it entails the fact

that management of service quality can only be effective if n=managers recognize the interaction among the elemnts defining quality.

The current study only tried to show the existing gap in service quality. So future research is required to relate the issue with important

variables such as overall service quality, customer retention and loyalty and customer satisfaction.

6 References

A. Ananth,A. Ramesh R. and B. Prabahara (2011)” Service quality gap analysis in private sector bank - a customer perspective

“ Indian Journal of Commerce & Management Studies Vol–II , Issue -1 January 2011

B. Afrin, T.(2012), Quality of customer service in the banking sector of Bangladesh: An Explorative study,East West Jouranl of

Business and Social studies, Vol 3.

C. Bhattacharjee, P.K ,2010,Service Quality Measurement with Minimum Attributes (SERVQUAL-MA) Technique Upgrade

by Human Resource Development, International Journal of Innovation, Management and Technology, Vol. 1, No. 3

D. Appanan, S. Doraisamy, B. &Hui, T.X. (2013), Cutomer perception on service quality of Commercial Banks: A case study in

Penang, Malaysia, Academic Research International,4(5),459-468

E. Eshete, Z.S., Teshome, K.W., &Abebe, T.K., (2013), Competition in Ethiopian Banking Industry, African Journal of

Economics, 1(5), 176-190

F. Illyas, A., Nasir, H. Malik, M.R., Mirza U.E., Munir, S.,&Sajid, A., Assessing the service quality of Banks using

SERVQUAL model, Interdisciplinary Journal of contemporary Research in Business, 4(11),390-400.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 150

G. Krejcie, R. V., & Morgan, D. W. 1970. Determining sample size for research activities. Educational andPsychological

Measurement, Vol 30, pp. 607-610.

H. Lau, M. M., Cheung, R., Lam, C. Y. & Chu, T. Y. 2013. Measuring quality in the banking industry: A Hong Kong based

study .Contemporary Management Research, 9(3), 262-282.

I. Devi, R.V, &Ramburuth, K.S. (2012),Assesing Service Quality in the Mauritanian Banking Sector, Prestige International

Journal of Mangemnt,1(1), 115-126.

J. Malhotra, N. & Mukherjee, A. (2004). The relative influence of organizational commitment and job satisfaction on service

quality of customer-contact employees in banking call centres. Journal of Services Marketing, 18 (3), 162-174.

K. Micuda, D. &Cruceru, E.(ND), Testing SERVQUAL dimensions on the Romanian Banking Sector, Proceedings of the

International Conference on RISK MANAGEMENT, ASSESSMENT and MITIGATION, pp329-334

L. Oyetunji, E.O, Baguri, B.B ,& Otis, A.E(2014), Comparison of service quality of two commercial banks in upper east region

of Ghana, Proceedings of the 2014 International Conference on Industrial Engineering and Operations Management Bali,

Indonesia, January 7 – 9, 2014,pp7.782-792

M. Parasuraman, A., Zeithaml, V.A. & Berry, L.L. (1988). SERVQUAL: a multiple-item scale for

N. measuring consumer perceptions of service quality. Journal of Retailing, 64, 12-40

O. Rahaman, M. M, Abdullah, M. &Rahaman, A.(2011), Measuring Service quality using SERVQUAL model: A study on

PCBs( Private commercial Banks in Bangledesh, Business Management Dynamics, 1(1),01-11.

P. Safakli, O.V,(2007), Measuring service quality of commercial banks towards SMEs in Nortern Cyprus, Jouranl of Yasar

University,2(8),827-839

Q. Saghier, N.E, Nathan, D.(2013), Service quality dimensions and customers’ satisfaction of banks in Egypt, Proceedings of

20th International Business Research Conference 4 - 5 April 2013, Dubai, UAE, pp.1-13

R. Seth,N ,. Deshmukh, G. S, and Vrat, P (2004), Service quality models: a review International Journal of Quality & Reliability

Management Vol. 22 No. 9, 2005 pp. 913-949

S. Straus, B. Mang, P.,(1999),”culture shocks” in intercultural service encounters?, Journal of Service Marketing,13(4/5),329-

346.

T. Wayne, S. J., Shore, L. M., &Liden, R. C. (1997). Perceived organizational support and leader-member exchange: A social

exchange perspective. Academy of Management Journal, 40(1), 82–111.

U. Shahin.A and Samea.M (2010)” Developing the Models of Service Quality Gaps: A Critical

V. Discussion “ Journal of Business Management and Strategy Vol. 1, No. 1: E2

W. Yamazakia1. Y, Petchdee ,S ,(2015) , Turnover Intention, Organizational Commitment, and Specific Job Satisfaction among

Production Employees in Thailand, Journal of Business and Management Volume 4, Issue 4

X. Zeithaml VA., Berry, LL., Parasuraman, A., (1993) ,The Nature and Determinants of Consumer

Y. Expectations of Service, Journal of the Academy of Marketing Science, Vol 21

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 151

Annex: Measurement instrument

Variables used in measuring Service Quality.

INSTRUCTIONS

The following statement relate to your opinion about your bank. For each statement indicate the extent you believe your bank

has the feature described by the statement.

Based on the following guideline.

1= Strongly disagree

2= Disagree

3 = Neither disagree nor agree

4= Agree

5= Strongly agree

Put a check mark () in the column corresponding to one of the five points following the particular item to show the degree to

which it relates to your bank.

Perception:

1 =

Strongly

disagree

2 =

Disagree

3 = Neither

disagree

nor agree

4 =

Agree

5 =

Strongly

agree

1. The Bank has modern looking equipment.

2. The physical facilities at the Bank is

visually appealing

3. Employees at the Bank are well dressed and

neat .

4. Material and information associated with

the service are visually appealing.

5. When the Bank promise to do something by

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 152

a certain time, it does so.

6. When a customer has a problem, the

Banks’s staff are sympathetic and

reassuring.

7. The Bank performs the service right the

first time.

8. The Bank provides the service at the time it

promises to do so.

9. The Bank keeps its records accurately

10. The Bank tells customers exactly when

services will be performed.

11. The Banks’ staff gives prompt service to

customers.

12. The Banks’ staff are always willing to help

customers.

13. The Banks’ staff are never too busy to

respond to customers’ requests.

14. The behavior of the Banks’s staff instill

confidence in customers.

15. You feel safe in conducting business with

the Bank.

16. The Banks’ staff are consistently courteous

with customers

17. The Banks’ staff have the knowledge to

answer customers’ questions.

18. The Banks gives customers individual

attention.

19. The Bank has operating hours convenient to

all their customers.

20. The Bank has employees who give

customers personal attention

1 =

Strongly

disagree

2 =

Disagree

3 = Neither

disagree

nor agree

4 =

Agree

5 =

Strongly

agree

21. The Bank have their customer’s best

interest at heart.

22. The Banks’ staff understand the specific

needs of their customers.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 153

INSTRUCTIONS

The following statement relate to your feeling about your bank. For each statement indicate the extent you

believe your bank has the feature described by the statement based on the following guideline.

1= Strongly disagree

2= disagree

3 = Neither disagree nor agree

4= Agree

5= Strongly agree

Put a check mark () in the column corresponding to one of the four points following the particular item to

show the degree to which it relates to your bank.

Expectations:

1 =

Strongly

disagree

2 =

Disagr

ee

3 =

Neither

disagree

nor agree

4 =

Agree

5 =

Strongly

agree

1. Banks should have modern looking

equipment. .

2. The physical facilities at Banks should be

visually appealing

3. Employees at Banks should be neat

appearing

4. Material and information associated with

the service should be visually appealing.

5. When Banks promise to do something by a

certain time, they should do so.

6. When a customer has a problem, Banks’s

staff should be sympathetic and reassuring.

7. Banks should perform the service right the

first time.

1 =

Strongly

disagree

2 =

Disagr

ee

3 =

Neither

disagree

nor agree

4 =

Agree

5 =

Strongly

agree

8. Banks should provide the service at the

time they promise to do so.

9. Banks should insist on error free records

10. Banks should tell customers exactly when

services will be performed.

Asia Pacific Journal of Research

ISSN (Print): 2320-5504

ISSN (Online): 2347-4793

www.apjor.com Vol: I. Issue LIII, July2017 154

11. Banks’ staff should give prompt service to

customers.

12. Banks’ staff should always be willing to

help customers.

13. Banks’ staff should never be too busy to

respond to customers’ requests.

14. The behavior of Banks’s staff should instill

confidence in customers.

15. Customers should feel safe in conducting

business with Banks.

16. Banks’ staff should be consistently

courteous with customers

17. Banks’ staff should have the knowledge to

answer customers’ questions.

18. Banks should will give customers

individual attention.

19. Banks should have operating hours

convenient to all their customers.

20. Banks should have employees who give

customers personal attention

21. Banks should have their customer’s best

interest at heart.

22. Banks’ staff should understand the specific

needs of their customers.