Embed Size (px)

DESCRIPTION

Citation preview

CASE STUDY 1:

Nutrition Labelling &

Packaging Standards

- Dr Roger Bektash

- Ms Cyndy Au

Nutrition Labelling & Packaging

Standards

Dr Roger Bektash

www.foodindustry.asia

VISION FOR ASEAN

Products made for one ASEAN country can be sold in

other ASEAN countries

Efficient Supply Chain

Benefits to local & regional economy

- scale up & efficient manufacture

- increased trade

Benefits for consumers in all countries

4

What’s this got to do with Nutrition Labelling?

www.foodindustry.asia

LABELLING COMPLEXITY -

A MAJOR BARRIER

Common labelling standards are needed for

common information (as in EU)

• Unique Labelling requirements

– goes beyond local language requirements

• There are unique National formats, tolerances or

standards for the same information

• Currently dictating Individual country labels, or

complexity and limiting the information provided

5

www.foodindustry.asia

NUTRITION LABELLING

Nutrition Labelling is either Mandated or the format is

prescribed by most ASEAN countries

- Nutrition Information Facts Panel

Increased Voluntary Information or Claims

- “Good Source of Fibre”

- “Reduced Salt”, and

- Front of Pack “GDA”

6

However there are many challenges ........

www.foodindustry.asia

CHALLENGE 1

Variance in Mandatory & Voluntary requirements

• Malaysia – mandatory nutrition labelling on many

foods

• Indonesia – required on fortified foods

• Singapore – required on foods making nutrient

claims

• Philippines – the nutrition information format

requires specific measurement units

7 Confusing

www.foodindustry.asia

CHALLENGE 2

Differing min & max limits for vitamins & minerals

To meet local standards, one Singaporean

manufacturer needs to:

• Make four different formulations for the same

product to supply 8 ASEAN markets

• And have different analytical testing limits &

requirements for several markets

8

Adding Complexity & Costs

www.foodindustry.asia

CHALLENGE 3

Variance in Tolerance levels for nutrients

• A common recipe across multiple countries faces

differing tolerances for nutrients

• Most ASEAN countries require products to contain at

least 80% of the declared nutrient (as per Codex), but

some impose further restrictions

- more stringent if fortified

- first consignment vs. subsequent shipments

- Nutrients claimed on the front vs. in the NIP on back

Inconsistent

www.foodindustry.asia

CHALLENGE 4

The daily reference values for nutrients vary

• Indonesia, Thailand & the Philippines require the

%RDA to be stated for each nutrient in the NIP;

Malaysia adopts %NRV from Codex

• But these reference values vary between the

countries, making a common NIP label

impossible

10 A disincentive to voluntary nutrition information

www.foodindustry.asia

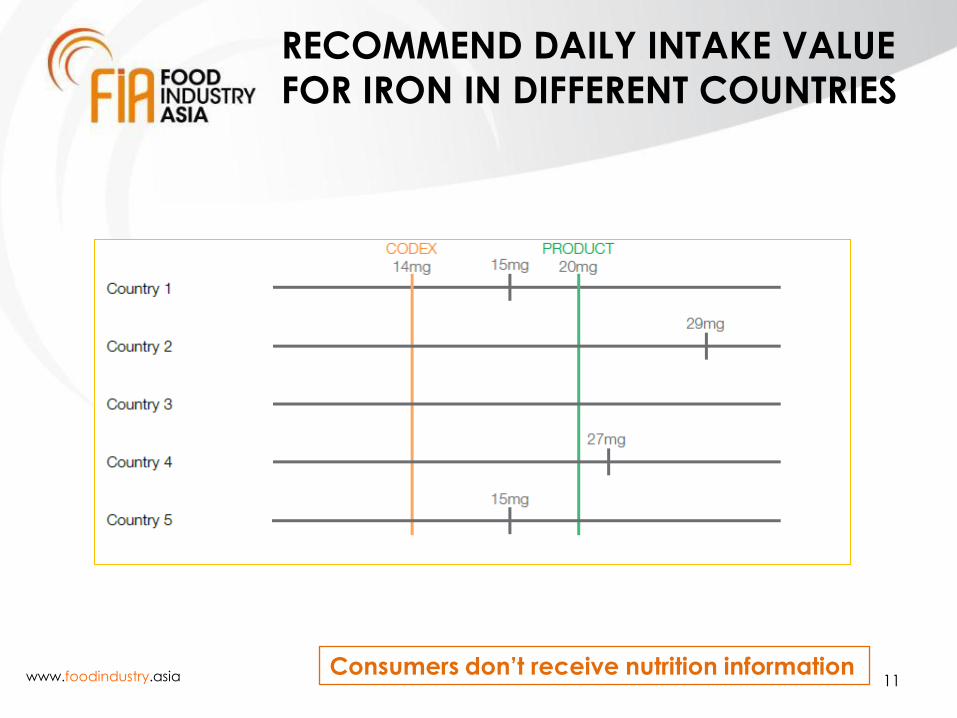

RECOMMEND DAILY INTAKE VALUE

FOR IRON IN DIFFERENT COUNTRIES

11 Consumers don’t receive nutrition information

www.foodindustry.asia

BENEFITS OF HARMONISATION

Nutrient values, tolerances and labelling

• Cost efficiencies for manufacturers, trade,

consumers and governments

• Clarity of information for Consumers

• Increased product availability

12

www.foodindustry.asia

EUROPEAN EXPERIENCE

Reluctance to Invest Capital

Where regulation is fragmented and marketing

opportunities are constrained

13

ASEAN needs: Common labelling

standards for common information

Nutrition Labelling & Packaging

Standards

Ms Cyndy Au

www.foodindustry.asia

CHALLENGES AND OPPORTUNITIES

FOR HARMONIZATION

15

SPECIFIC RECENT EXAMPLES

www.foodindustry.asia

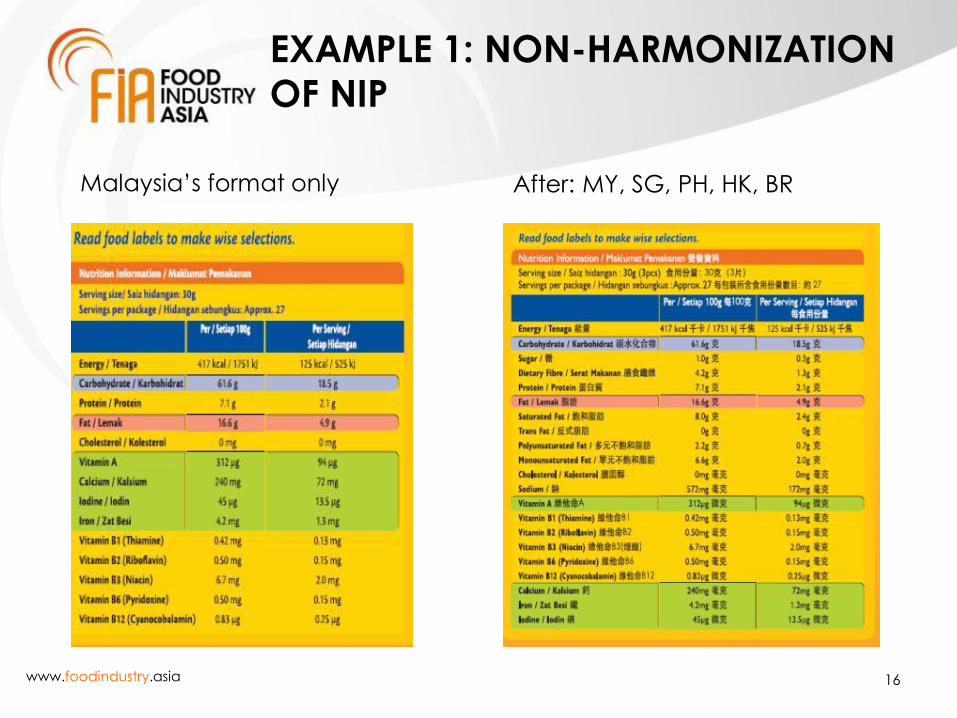

EXAMPLE 1: NON-HARMONIZATION

OF NIP

16

Malaysia’s format only After: MY, SG, PH, HK, BR

www.foodindustry.asia

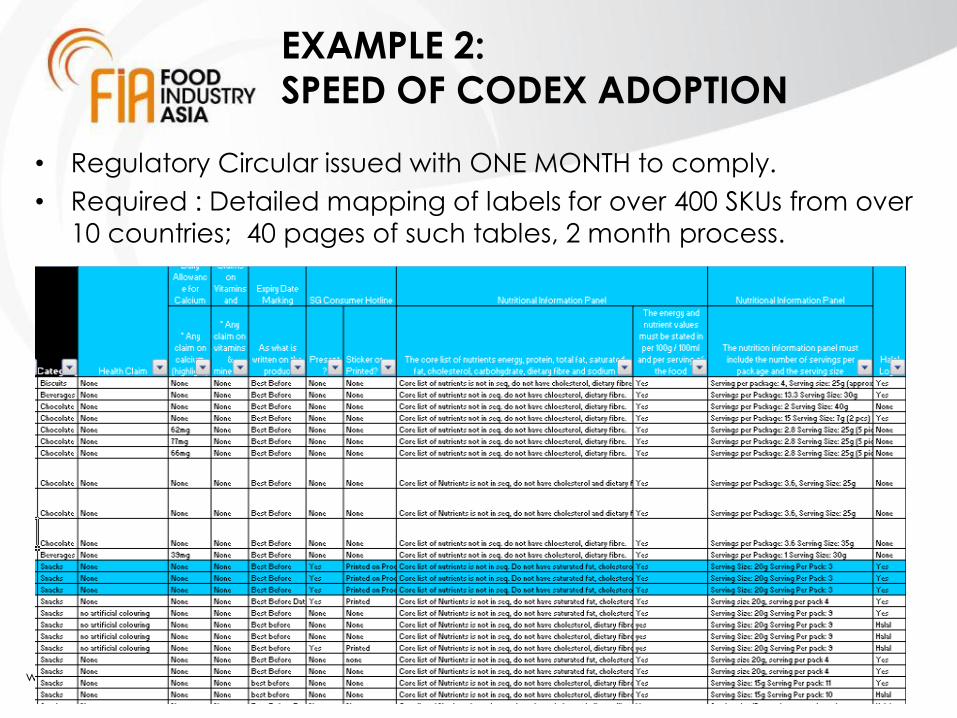

EXAMPLE 2:

SPEED OF CODEX ADOPTION

17

• Regulatory Circular issued with ONE MONTH to comply.

• Required : Detailed mapping of labels for over 400 SKUs from over

10 countries; 40 pages of such tables, 2 month process.

www.foodindustry.asia

EXAMPLE 2:

SPEED OF CODEX ADOPTION

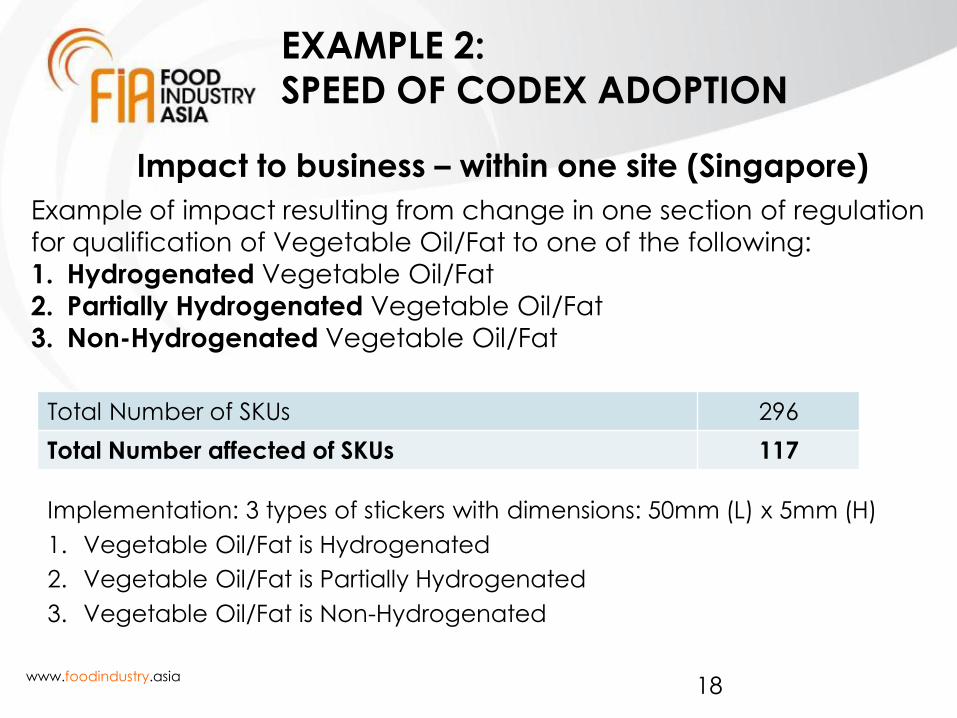

Impact to business – within one site (Singapore)

18

Example of impact resulting from change in one section of regulation

for qualification of Vegetable Oil/Fat to one of the following:

1. Hydrogenated Vegetable Oil/Fat

2. Partially Hydrogenated Vegetable Oil/Fat

3. Non-Hydrogenated Vegetable Oil/Fat

Total Number of SKUs 296

Total Number affected of SKUs 117

Implementation: 3 types of stickers with dimensions: 50mm (L) x 5mm (H)

1. Vegetable Oil/Fat is Hydrogenated

2. Vegetable Oil/Fat is Partially Hydrogenated

3. Vegetable Oil/Fat is Non-Hydrogenated

www.foodindustry.asia

EXAMPLE 2:

SPEED OF CODEX ADOPTION

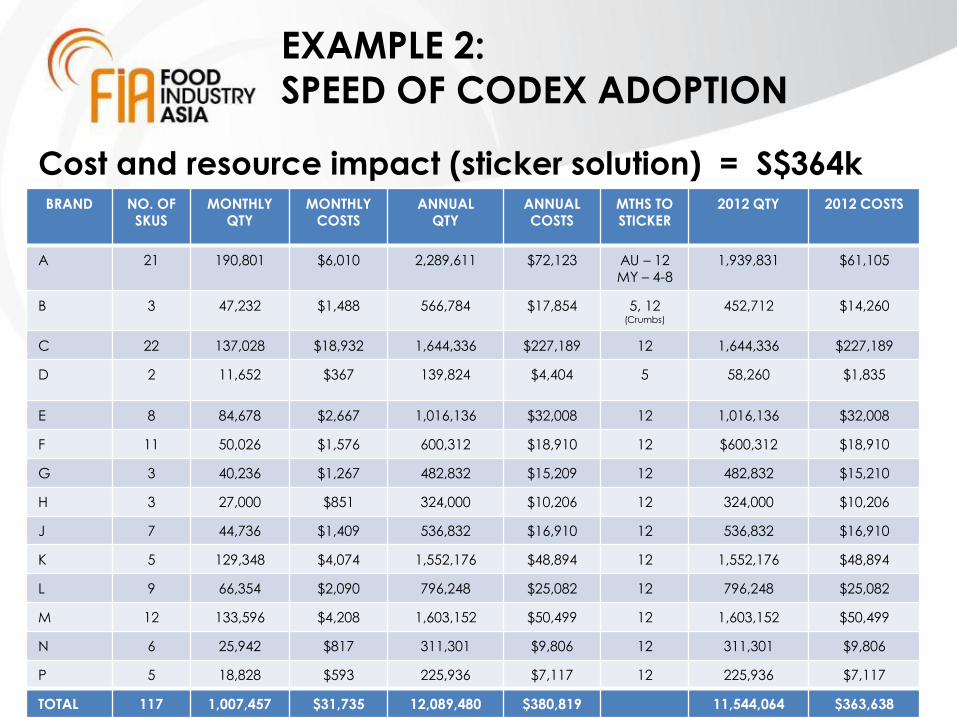

Cost and resource impact (sticker solution) = S$364k

19

BRAND NO. OF SKUS

MONTHLY QTY

MONTHLY COSTS

ANNUAL QTY

ANNUAL COSTS

MTHS TO STICKER

2012 QTY 2012 COSTS

A 21 190,801 $6,010 2,289,611 $72,123 AU – 12 MY – 4-8

1,939,831 $61,105

B 3 47,232 $1,488 566,784 $17,854 5, 12 (Crumbs)

452,712 $14,260

C 22 137,028 $18,932 1,644,336 $227,189 12 1,644,336 $227,189

D 2 11,652 $367 139,824 $4,404 5 58,260 $1,835

E 8 84,678 $2,667 1,016,136 $32,008 12 1,016,136 $32,008

F 11 50,026 $1,576 600,312 $18,910 12 $600,312 $18,910

G 3 40,236 $1,267 482,832 $15,209 12 482,832 $15,210

H 3 27,000 $851 324,000 $10,206 12 324,000 $10,206

J 7 44,736 $1,409 536,832 $16,910 12 536,832 $16,910

K 5 129,348 $4,074 1,552,176 $48,894 12 1,552,176 $48,894

L 9 66,354 $2,090 796,248 $25,082 12 796,248 $25,082

M 12 133,596 $4,208 1,603,152 $50,499 12 1,603,152 $50,499

N 6 25,942 $817 311,301 $9,806 12 311,301 $9,806

P 5 18,828 $593 225,936 $7,117 12 225,936 $7,117

TOTAL 117 1,007,457 $31,735 12,089,480 $380,819 11,544,064 $363,638

www.foodindustry.asia

EXAMPLE 3: NET WEIGHT LABELLING

NEW REQUIREMENT ONE COUNTRY

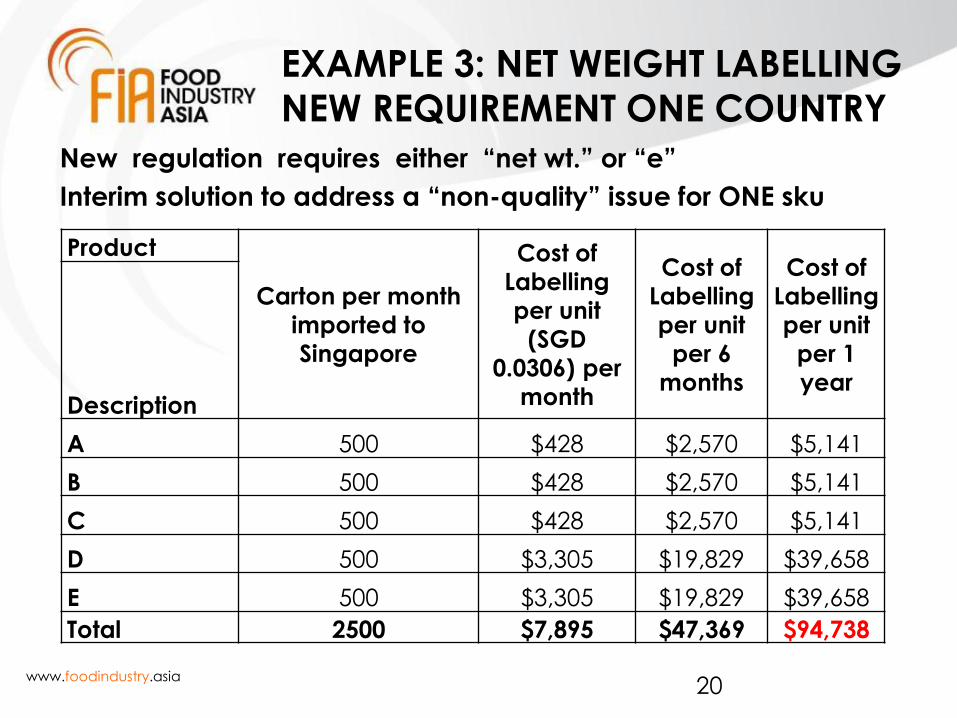

New regulation requires either “net wt.” or “e”

Interim solution to address a “non-quality” issue for ONE sku

20

Product

Carton per month

imported to

Singapore

Cost of

Labelling

per unit

(SGD

0.0306) per

month

Cost of

Labelling

per unit

per 6

months

Cost of

Labelling

per unit

per 1

year Description

A 500 $428 $2,570 $5,141

B 500 $428 $2,570 $5,141

C 500 $428 $2,570 $5,141

D 500 $3,305 $19,829 $39,658

E 500 $3,305 $19,829 $39,658

Total 2500 $7,895 $47,369 $94,738

www.foodindustry.asia

NEGATIVE IMPACTS

21

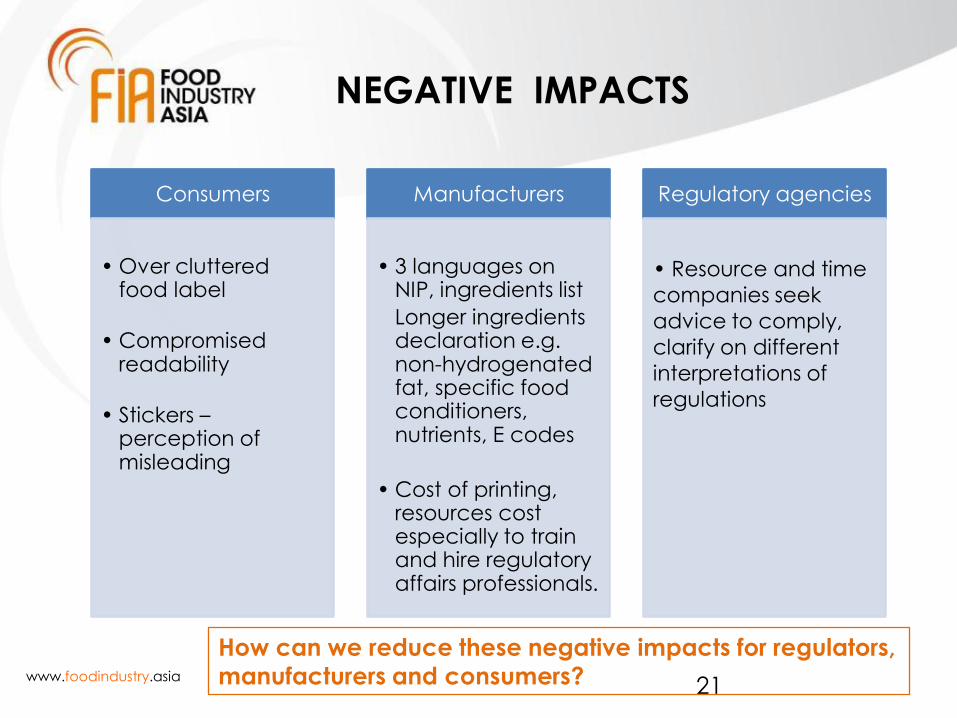

Consumers

• Over cluttered food label

• Compromised readability

• Stickers – perception of misleading

Manufacturers

• 3 languages on NIP, ingredients list

Longer ingredients declaration e.g. non-hydrogenated fat, specific food conditioners, nutrients, E codes

• Cost of printing, resources cost especially to train and hire regulatory affairs professionals.

Regulatory agencies

• Resource and time

companies seek

advice to comply,

clarify on different

interpretations of

regulations

How can we reduce these negative impacts for regulators,

manufacturers and consumers?

www.foodindustry.asia

EUROPEAN EXPERIENCE

Reluctance to Invest Capital

Where regulation is fragmented and marketing

opportunities are constrained

22

ASEAN needs: Common labelling

standards for common information

So what do we want to do about it ?

www.foodindustry.asia

WAY FORWARD

1. How can industry contribute to the development of national regulations in the region harmonized toward Codex standards?

2. How can food industry create a level playing field in implementation of harmonized regulations by MNCs and SMEs?

23

Regulatory agencies and industry both want clear

regulations & standards for labelling and claims.

ASEAN needs: Common labelling standards for

common information