Embed Size (px)

DESCRIPTION

Archer Daniels Midland Company NYSE:ADM Chutinush Taksinapinunt has issued a strong buy on Archer Daniel Midland Company NYSE:ADM with a Price Target of $50 in 2011. Archer Daniels Midland Company is principally engaged in procuring, transporting, storing, processing, and merchandising agricultural commodities and products.

Citation preview

Archer Daniel Midland Company

Archer Daniel Midland Company

ADM : NYSE

Chutinush Taksinapinunt

Archer Daniel Midland Company

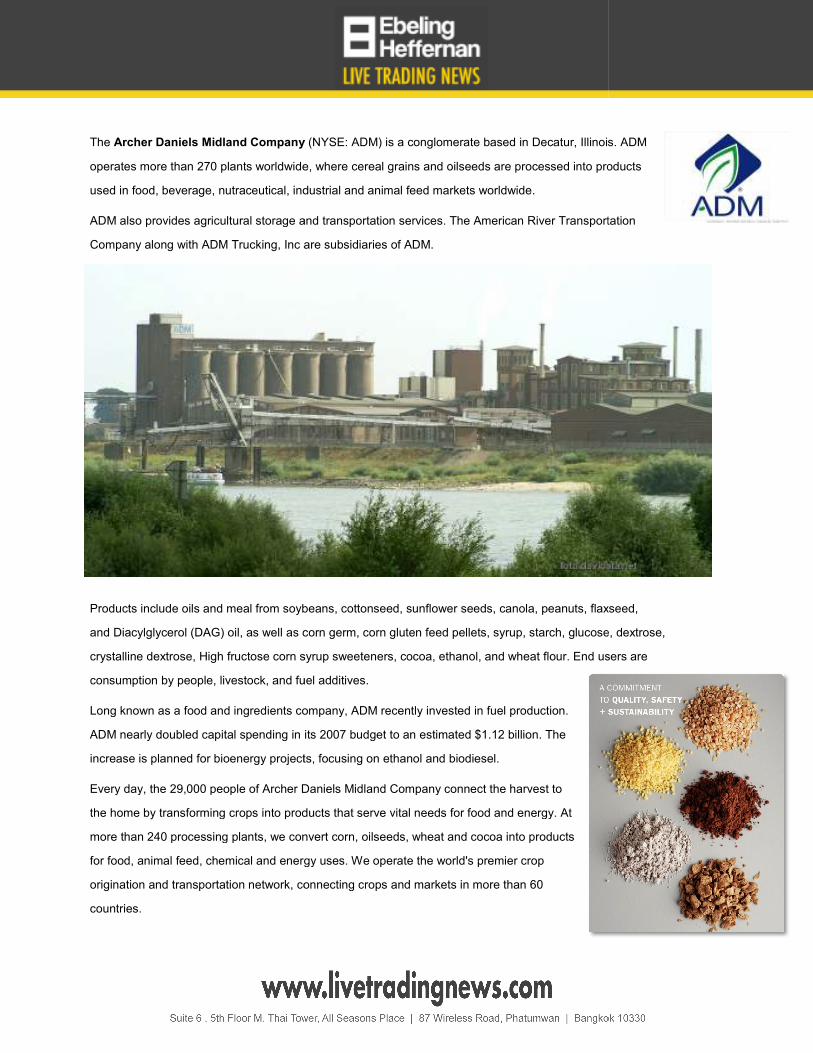

The Archer Daniels Midland Company

operates more than 270 plants worldwide, where

used in food, beverage, nutraceutical, industrial

ADM also provides agricultural storage and

Company along with ADM Trucking, Inc are subsidiaries of ADM.

Products include oils and meal from soybeans

and Diacylglycerol (DAG) oil, as well as c

crystalline dextrose, High fructose corn syrup

consumption by people, livestock, and fuel

Long known as a food and ingredients company, ADM recently invested in fuel production.

ADM nearly doubled capital spending in its 2007 budget to an estimated $1.12 billion. The

increase is planned for bioenergy projects, focusing on

Every day, the 29,000 people of Archer Daniels Midland Company connect the harvest to

the home by transforming crops into products that serve vital needs for food and energy. At

more than 240 processing plants, we convert corn, oilseeds, wheat and cocoa into products

for food, animal feed, chemical and energy uses. We operate the world's premier crop

origination and transportation network, connecting crops and markets in more than 60

countries.

Archer Daniels Midland Company (NYSE: ADM) is a conglomerate based in Decatur, Illinois

wide, where cereal grains and oilseeds are processed into products

industrial and animal feed markets worldwide.

storage and transportation services. The American River Transportation

are subsidiaries of ADM.

soybeans, cottonseed, sunflower seeds, canola, peanuts, flaxseed

corn germ, corn gluten feed pellets, syrup, starch, glucose

High fructose corn syrup sweeteners, cocoa, ethanol, and wheat flour. End users

fuel additives.

Long known as a food and ingredients company, ADM recently invested in fuel production.

ADM nearly doubled capital spending in its 2007 budget to an estimated $1.12 billion. The

increase is planned for bioenergy projects, focusing on ethanol and biodiesel.

Every day, the 29,000 people of Archer Daniels Midland Company connect the harvest to

forming crops into products that serve vital needs for food and energy. At

more than 240 processing plants, we convert corn, oilseeds, wheat and cocoa into products

for food, animal feed, chemical and energy uses. We operate the world's premier crop

ation and transportation network, connecting crops and markets in more than 60

Decatur, Illinois. ADM

are processed into products

iver Transportation

flaxseed,

glucose, dextrose,

users are

Recent News

Burcon NutraScience Corporation And Archer Daniels Midland Company Enter Into CLARISOY Letter Of

Intent

Monday, 15 Nov 2010 09:07am EST

Burcon NutraScience Corporation (Burcon) announced that it has signed a non-binding letter of intent

(Letter of Intent) with Archer Daniels Midland Company (ADM) which details the intention of the two

parties to enter into a license agreement pursuant to which Burcon will license (License) its CLARISOY

technology to ADM on an exclusive basis to produce, market and sell CLARISOY soy protein isolates

(CLARISOY or the Products) world-wide (Definitive Agreement). The Letter of Intent outlines the major

agreed-upon terms for the proposed Definitive Agreement whereby Burcon will grant an exclusive,

world-wide and royalty-bearing license to ADM for Burcon's CLARISOY soy protein isolate technology. The

terms of the proposed License include: License to ADM of all intellectual property, including know-how

and trade secrets, concerning the manufacture and use of CLARISOY Royalty stream payable to Burcon on

a quarterly basis begins upon the signing of the Definitive Agreement Engineering and design of initial

semi-works commercial CLARISOY production plant to be completed by ADM concurrent with the

completion of the Definitive Agreement. Royalty structure incorporates financial incentive for ADM to

expand sales globally Concurrent with and forming part of the Letter of Intent, Burcon has also agreed to

enter into a stand-still/no-shop agreement with ADM while the two parties negotiate and execute the

Definitive Agreement for the CLARISOY License.

Archer Daniels Midland Company To Construct Biodiesel Facility in Joaçaba, Brazil

Tuesday, 2 Nov 2010 02:00pm EDT

Archer Daniels Midland Company announced that it will construct a second biodiesel plant in Brazil. The

facility, to be built in Joaçaba, Santa Catarina, will be adjacent to existing ADM soybean crushing and

refining facilities. With an annual biodiesel production capacity of 164,000 metric tons, the plant will

increase ADM’s biodiesel capacity in Brazil by more than 50%. Construction will begin in March of 2011

and is expected to be completed during the first half of 2012.

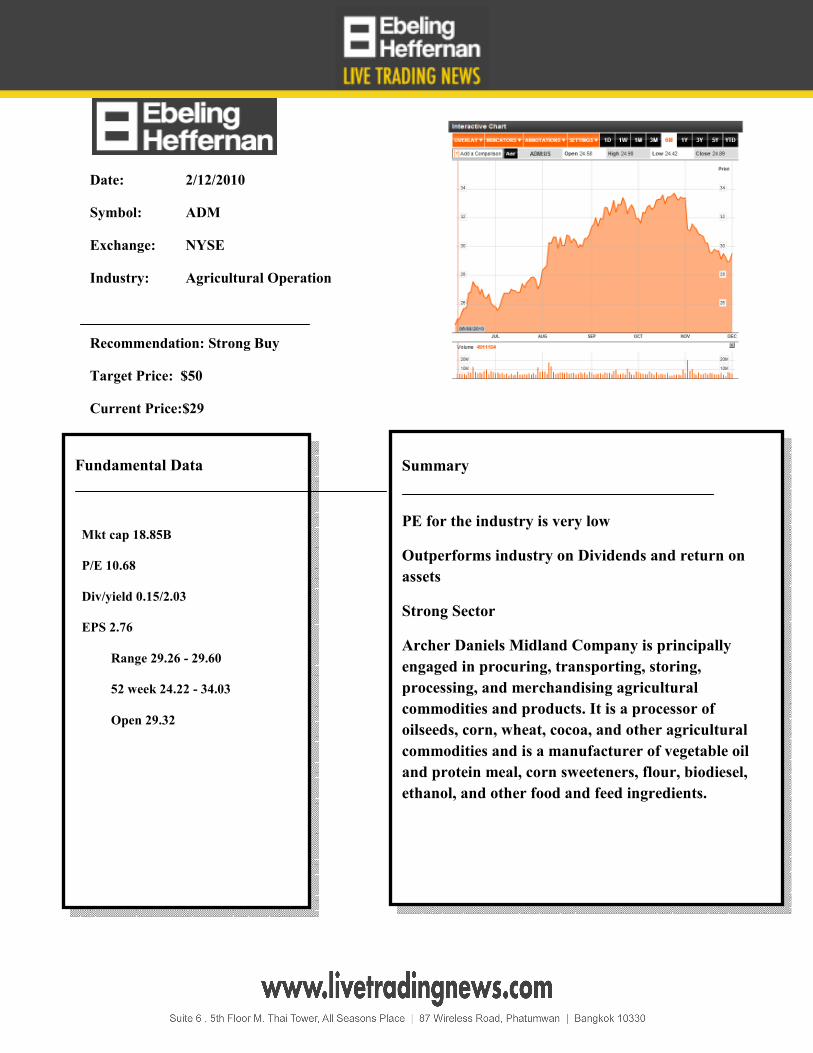

Date: 2/12/2010

Symbol: ADM

Exchange: NYSE

Industry: Agricultural Operation

Recommendation: Strong Buy

Target Price: $50

Current Price:$29

Summary

PE for the industry is very low

Outperforms industry on Dividends and return on

assets

Strong Sector

Archer Daniels Midland Company is principally

engaged in procuring, transporting, storing,

processing, and merchandising agricultural

commodities and products. It is a processor of

oilseeds, corn, wheat, cocoa, and other agricultural

commodities and is a manufacturer of vegetable oil

and protein meal, corn sweeteners, flour, biodiesel,

ethanol, and other food and feed ingredients.

Fundamental Data

Mkt cap 18.85B

P/E 10.68

Div/yield 0.15/2.03

EPS 2.76

Range 29.26 - 29.60

52 week 24.22 - 34.03

Open 29.32

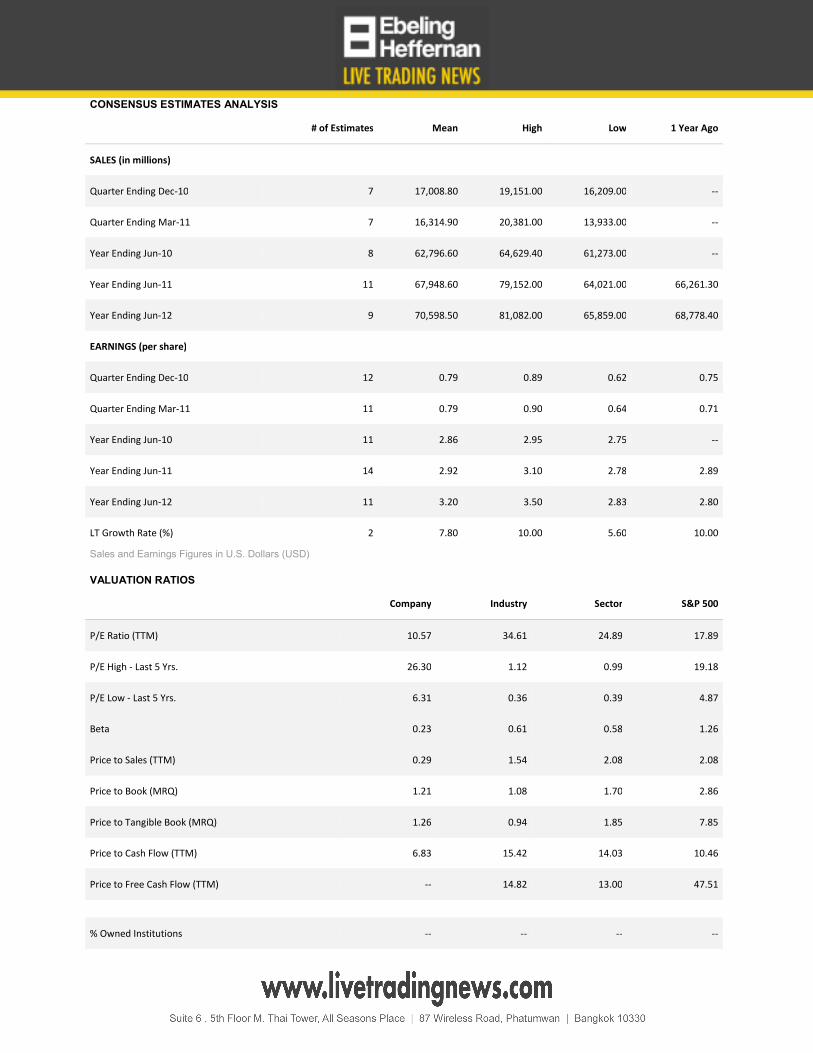

CONSENSUS ESTIMATES ANALYSIS

# of Estimates Mean High Low 1 Year Ago

SALES (in millions)

Quarter Ending Dec-10 7 17,008.80 19,151.00 16,209.00 --

Quarter Ending Mar-11 7 16,314.90 20,381.00 13,933.00 --

Year Ending Jun-10 8 62,796.60 64,629.40 61,273.00 --

Year Ending Jun-11 11 67,948.60 79,152.00 64,021.00 66,261.30

Year Ending Jun-12 9 70,598.50 81,082.00 65,859.00 68,778.40

EARNINGS (per share)

Quarter Ending Dec-10 12 0.79 0.89 0.62 0.75

Quarter Ending Mar-11 11 0.79 0.90 0.64 0.71

Year Ending Jun-10 11 2.86 2.95 2.75 --

Year Ending Jun-11 14 2.92 3.10 2.78 2.89

Year Ending Jun-12 11 3.20 3.50 2.83 2.80

LT Growth Rate (%) 2 7.80 10.00 5.60 10.00

Sales and Earnings Figures in U.S. Dollars (USD)

VALUATION RATIOS

Company Industry Sector S&P 500

P/E Ratio (TTM) 10.57 34.61 24.89 17.89

P/E High - Last 5 Yrs. 26.30 1.12 0.99 19.18

P/E Low - Last 5 Yrs. 6.31 0.36 0.39 4.87

Beta 0.23 0.61 0.58 1.26

Price to Sales (TTM) 0.29 1.54 2.08 2.08

Price to Book (MRQ) 1.21 1.08 1.70 2.86

Price to Tangible Book (MRQ) 1.26 0.94 1.85 7.85

Price to Cash Flow (TTM) 6.83 15.42 14.03 10.46

Price to Free Cash Flow (TTM) -- 14.82 13.00 47.51

% Owned Institutions -- -- -- --

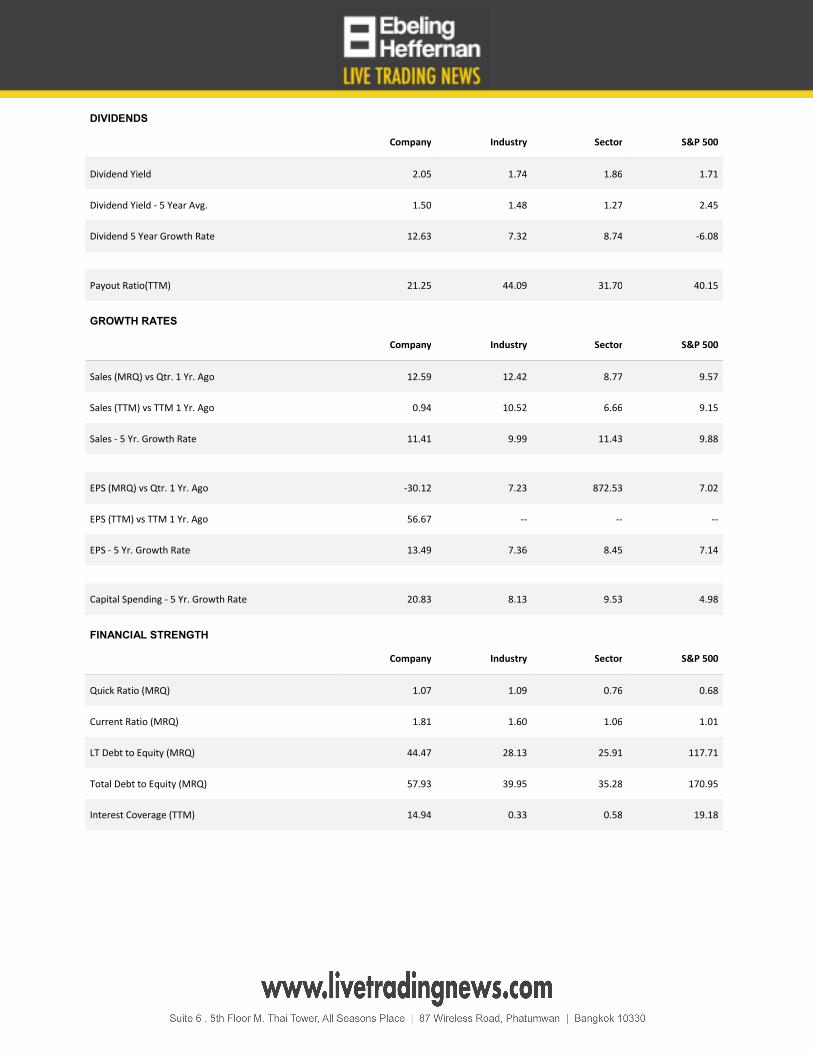

DIVIDENDS

Company Industry Sector S&P 500

Dividend Yield 2.05 1.74 1.86 1.71

Dividend Yield - 5 Year Avg. 1.50 1.48 1.27 2.45

Dividend 5 Year Growth Rate 12.63 7.32 8.74 -6.08

Payout Ratio(TTM) 21.25 44.09 31.70 40.15

GROWTH RATES

Company Industry Sector S&P 500

Sales (MRQ) vs Qtr. 1 Yr. Ago 12.59 12.42 8.77 9.57

Sales (TTM) vs TTM 1 Yr. Ago 0.94 10.52 6.66 9.15

Sales - 5 Yr. Growth Rate 11.41 9.99 11.43 9.88

EPS (MRQ) vs Qtr. 1 Yr. Ago -30.12 7.23 872.53 7.02

EPS (TTM) vs TTM 1 Yr. Ago 56.67 -- -- --

EPS - 5 Yr. Growth Rate 13.49 7.36 8.45 7.14

Capital Spending - 5 Yr. Growth Rate 20.83 8.13 9.53 4.98

FINANCIAL STRENGTH

Company Industry Sector S&P 500

Quick Ratio (MRQ) 1.07 1.09 0.76 0.68

Current Ratio (MRQ) 1.81 1.60 1.06 1.01

LT Debt to Equity (MRQ) 44.47 28.13 25.91 117.71

Total Debt to Equity (MRQ) 57.93 39.95 35.28 170.95

Interest Coverage (TTM) 14.94 0.33 0.58 19.18

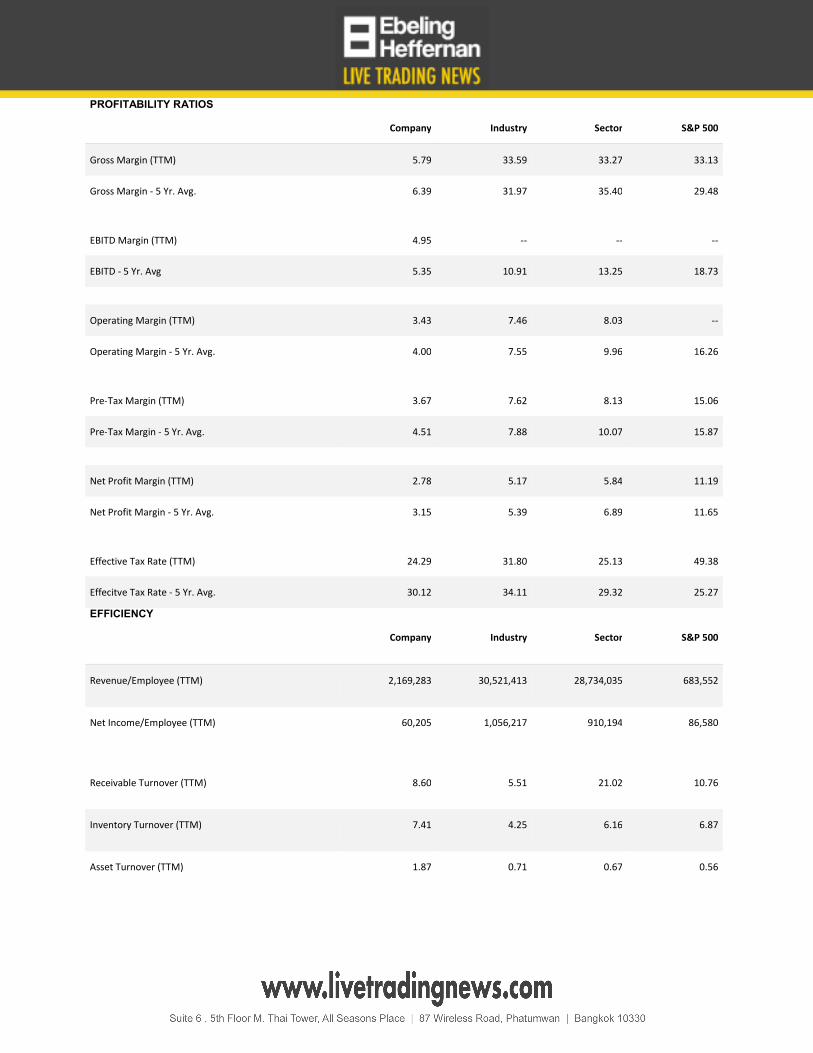

PROFITABILITY RATIOS

Company Industry Sector S&P 500

Gross Margin (TTM) 5.79 33.59 33.27 33.13

Gross Margin - 5 Yr. Avg. 6.39 31.97 35.40 29.48

EBITD Margin (TTM) 4.95 -- -- --

EBITD - 5 Yr. Avg 5.35 10.91 13.25 18.73

Operating Margin (TTM) 3.43 7.46 8.03 --

Operating Margin - 5 Yr. Avg. 4.00 7.55 9.96 16.26

Pre-Tax Margin (TTM) 3.67 7.62 8.13 15.06

Pre-Tax Margin - 5 Yr. Avg. 4.51 7.88 10.07 15.87

Net Profit Margin (TTM) 2.78 5.17 5.84 11.19

Net Profit Margin - 5 Yr. Avg. 3.15 5.39 6.89 11.65

Effective Tax Rate (TTM) 24.29 31.80 25.13 49.38

Effecitve Tax Rate - 5 Yr. Avg. 30.12 34.11 29.32 25.27

EFFICIENCY

Company Industry Sector S&P 500

Revenue/Employee (TTM) 2,169,283 30,521,413 28,734,035 683,552

Net Income/Employee (TTM) 60,205 1,056,217 910,194 86,580

Receivable Turnover (TTM) 8.60 5.51 21.02 10.76

Inventory Turnover (TTM) 7.41 4.25 6.16 6.87

Asset Turnover (TTM) 1.87 0.71 0.67 0.56

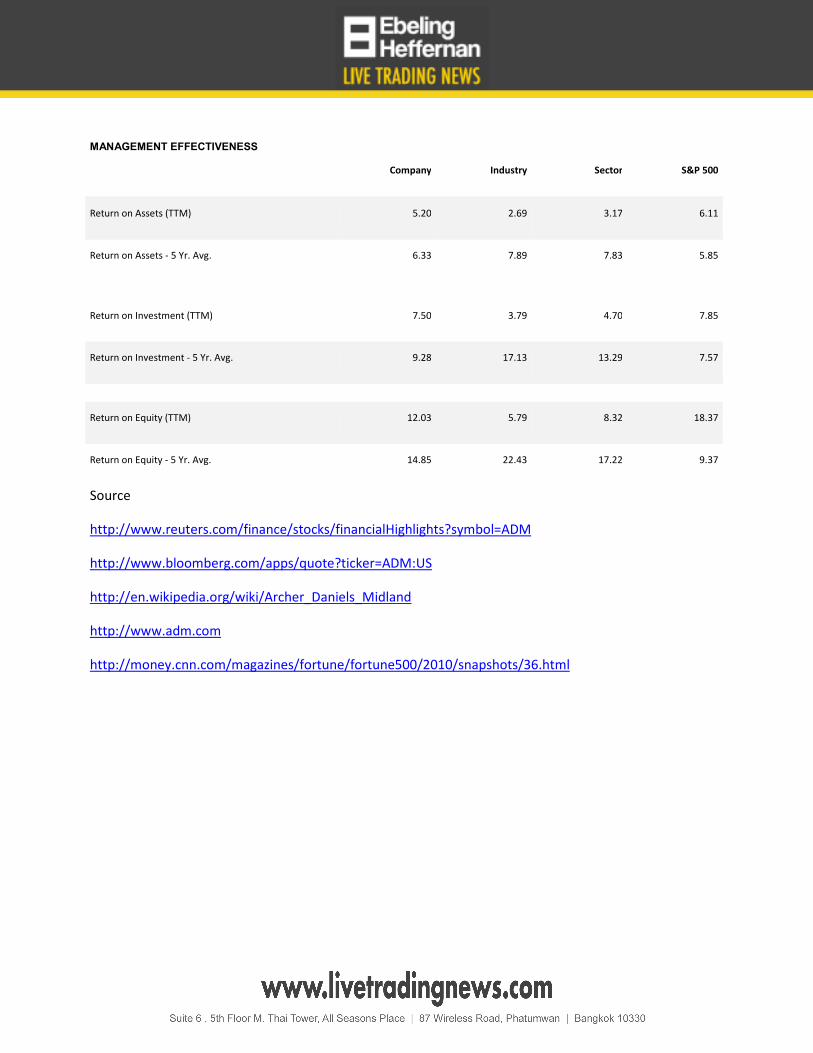

MANAGEMENT EFFECTIVENESS

Company Industry Sector S&P 500

Return on Assets (TTM) 5.20 2.69 3.17 6.11

Return on Assets - 5 Yr. Avg. 6.33 7.89 7.83 5.85

Return on Investment (TTM) 7.50 3.79 4.70 7.85

Return on Investment - 5 Yr. Avg. 9.28 17.13 13.29 7.57

Return on Equity (TTM) 12.03 5.79 8.32 18.37

Return on Equity - 5 Yr. Avg. 14.85 22.43 17.22 9.37

Source

http://www.reuters.com/finance/stocks/financialHighlights?symbol=ADM

http://www.bloomberg.com/apps/quote?ticker=ADM:US

http://en.wikipedia.org/wiki/Archer_Daniels_Midland

http://www.adm.com

http://money.cnn.com/magazines/fortune/fortune500/2010/snapshots/36.html

Contact Detail:

Chutinush Taksinapinunt

Corporate Account Executive

Heffernan Capital Management

Email: [email protected]

Chutinush Taksinapinunt holds a Bachelor of Business Administrators degree Majoring in

Finance and Banking. Chutinush Taksinapinunt is an experienced market maker and Portfolio

Manager, having worked with some of Thailand’s largest Securities Company and Financial

Institutions.

Price Estimate by Shayne Heffernan PhD

Shayne Heffernan of Ebeling Heffernan holds a PhD in Economics serves as CEO of Heffernan

Holdings Inc and Co Founder of Ebeling Heffernan www.ebeling-heffernan.com

Bangkok

Suite 53 Athenee Tower 63 Wireless Road, Lumpini, Pathumwan, Bangkok 10330 THAILAND

Tel: +66 2 126 8000 Fax: +66 2 126 8080

New York

347 5th Avenue, Suite 1402-508 Ny, NY 10016

Tel: +1 646-403-9881 Fax: +1 646-403-8014

Singapore

3 Raffles Place #07-01 Bharat Building Singapore 048617

Tel: +65 6329 6408Fax: +65 6329 9699

Disclaimer

Ebeling Heffernan (EH) distributes research and other information purchased and compiled from outside sources and analysts. This

report/release/advertisement is a commercial advertisement and is for general information purposes only. Do not base any investment decision

on information in this report/release/advertisement. EH is not a registered Investment Advisor or a member of any association for other

research providers. Under no circumstances is this report/release/advertisement to be used or considered as an offer to sell or a solicitation of

any offer to buy any security or other debt instruments, or any options, futures or other derivatives related to such securities herein. All

information herein is not intended to be used for investment advice. Price Targets are academic theory and should not be relied upon. The

majority of these profiled companies are highly risky OTC Bulletin Board or Pink Sheet companies. All readers of this information indemnify EH

from any liability for all accessed information. EH will not be responsible for updating any of its information in its report/release/advertisements.

EH advises recipients of all such data to be validated from the issuing company including all statistical information derived from SEC filings, from

data sources or financial information and data from the issuing company contained herein. The reader should seek professional financial advice,

verify all claims and do his/her own research and due diligence before investing in any securities mentioned. EH will not be liable to any person

or entity for the quality, accuracy, completeness, reliability or timeliness of information in this report/release/advertisement, or for any

direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information, products or services from any

person or entity including but not limited to lost profits, loss of opportunities, trading losses, and damages that may result from any

incompleteness or inaccuracy in any of EH’s profiled companies. When paid in stock, EH its affiliates, directors, officers, outside sources, investor

awareness groups and employees may liquidate shares at any time or hold for investment purposes. Readers are advised to review SEC periodic

reports: Forms 10-Q, 10K, Form 8-K, insider reports, Forms 3, 4, 5 Schedule 13D, www.sec.gov.nasd.com, www.pinksheets.com, www.sec.gov

and www.finra.com. SPC is compliant with the Can Spam Act of 2003. Investing in micro cap and small cap securities is speculative and carries a

high degree of risk. Investors can lose their entire investment. The Private Securities Litigation Reform Act of 1995 provides investors a 'safe

harbor' in regard to forward-looking statements. EH cautions all investors that such forward-looking statements in this

report/release/advertisement are not guarantees of future performance. Investors should understand that statements regarding future

prospects may not be realized. This report/release/advertisement does not have regard to the specific investment objective, financial situation,

suitability, and the particular need of any specific person who may receive this report/release/advertisement. Investors should note that income

from such securities, if any, may fluctuate and that each security's price or value may rise or fall substantially. Accordingly, investors may receive

back less than originally invested, or lose their entire investment. Past performance is not indicative of future performance. The Company has

not paid compensation for this commercial advertisement. HCM. has written this commercial advertisement for EH.

![Theses and Dissertations Thesis Collection · Danielson[Ref.6],inhisworkofdevelopinglong-range planning at Archer-Daniels-Midland Company,reportedonthe model usedinthatcompany.First,theeconomicinfluencesonthe](https://img.pdfslide.us/doc/110x75/600c56fc4c6a2310c1691ccd/theses-and-dissertations-thesis-collection-danielsonref6inhisworkofdevelopinglong-range.jpg)