Embed Size (px)

Citation preview

1

© 2012 Deloitte SA. Private and confidential.

Audit.Tax.Consulting.Corporate Finance.

Appréhender la gestion des risques au sein de différents types d’entreprises

David Stréliski,

Financial Risk Management, 26.04.2012

© 2012 Deloitte SA. Private and confidential.

Contents

Banking sector

• Banks structure and their types of risk

• Risk Management framework

Asset Managers

• Managing systemic and specific risks

• Impact of Solvency II for insurance clients

Risk Management in non-financial corporations

Risk management in Commodity Trading

1

2

3

4

2

2

© 2012 Deloitte SA. Private and confidential.

Banking Sector: 1

• Banks structure and their types of risk

• A Risk Management Framework

© 2012 Deloitte SA. Private and confidential.

Comprendre les domaines d’activités et drivers de

profitabilité d’une banque

4

• LE FINANCEMENT

Prêter à des particuliers et/ou entreprises pour financer un projet donné.

Rentabilité: structure des taux de prêt vs source de fonds, spreads de crédit:

Rdt = Δ [ TauxActifs - TauxPassifs ] = Transformation d‟échéances + Spread de crédit

• LE NEGOCE

Négoce de titres financiers sur les marchés financiers organisés ou de gré à gré:

• Compte propre (marché secondaire): rentabilité des fonds propres de la banque

• Pour tiers et market making (marché primaire): émissions, structurations, etc.

Rentabilité à CT: revente d‟un instrument financier à un prix supérieur au coût brut

Rdt = Δ [ Prixvente – CoûtAchat – Coût Trading – CoûtFinancement ]

• LES DEPOTS ET L‟EPARGNE

• Dépôts des clients de la banque désireux de « sécuriser » leurs liquidités et permettant par ailleurs de financer une partie de ses activités

• Produits d‟épargne pour offrir aux client un rendement sur leurs liquidités et sur lesquels la banque perçoit des commissions. Comprend la banque privée

Rentabilité: Source stable de financement de l‟actif et source de commissions de gestion.

Rdt = Δ [ Commission de gestion – Rémunération des dépôts ]

3

© 2012 Deloitte SA. Private and confidential.

Comprendre les risques essentiels d’une banque

5

• LE FINANCEMENT:

o Risque de taux d‟intérêt

o Risque de crédit

o Risque de contrepartie

o Risque pays

• LE NEGOCE:

o Risque de marché systémique (béta)

o Risque de marché spécifique (alpha)

o Risque de liquidité systémique

(liquidité de marché)

o Risque de liquidité spécifique

(liquidité d‟un titre en particulier)

• LES DEPOTS/L’EPARGNE:

o Risque de liquidité de financement

o Risque de taux d‟intérêt

• AUTRES RISQUES TRANSVERSAUX:

o Risques opérationnels

o Risques de réputation

o Risques stratégiques

o Risques réglementaires

o Risques émergents

© 2012 Deloitte SA. Private and confidential.

Gestion du risque de taux ALM

6

Actifs taux fixe

Actifs taux

variable

Passifs taux

variable

Passifs taux fixe

Risque de sensibilité

des fonds propres

Risque de sensibilité

de la marge

Potentiellement

élevé si différentiel

de duration important

A priori nul car

marge connue à

court terme

A priori nul car

variabilité des taux à

court terme

A priori faible car

marge connue mais

attention au risque

de base

Elevé Elevé

Bilan bancaire

Jambe

receveuse taux

variable

Jambe payeuse

taux fixe

Σ (Cft . e-rt)

De 1 à n années

Δ (Cft) De 1 à 12 mois

Fonds propres

• Effet de valeur = risque de baisse de la valeur économique des fonds propres suite à une variation de la courbe des taux d‟intérêt

• Effet de revenu = risque de baisse des bénéfices suite à une variation similaire.

Hors-Bilan

Profil de risque du portefeuille

en vue dynamique

Après couverture

Avant couverture

σ (R) E(R)

4

© 2012 Deloitte SA. Private and confidential.

Banking Sector: 1

• Banks structure and their types of risk

• A Risk Management Framework

© 2012 Deloitte SA. Private and confidential.

Le cadre de la gestion des risques

La fonction Risque doit conjuguer rôle de surveillance opérationnelle et support du

développement stratégique et du pilotage des activités.

8

5

© 2012 Deloitte SA. Private and confidential.

Les dimensions du Risk Management dans une banque

La réglementation Suisse impose un cadre d‟analyse Risk Management des banques qui

détermine le découpage entre les différentes dimensions.

9

© 2012 Deloitte SA. Private and confidential.

Définitions des classes de risques dans la banque

Source pour A-E: Basel Committee on Banking Supervision; Source pour F-H: Best Practice

10

6

© 2012 Deloitte SA. Private and confidential.

Asset Management: 2

• Managing systemic & specific risks

• Impact of Solvency II for insurance clients

© 2012 Deloitte SA. Private and confidential.

Introduction Un univers instable

• La rémunération de la prime de risque à long terme n‟est plus garantie et le défi essentiel

du gestionnaire d‟actifs se meut peu-à-peu de „gagner de l‟argent‟ à „ne pas en perdre‟

• Les modèles statiques imposés par la théorie financière classique, que cela soit pour la

gestion de portefeuille comme Markowitz, ou bien la gestion des risques comme la Value-

at-Risk, ne sont plus un gage de confiance et de stabilité

• L‟impératif de performance sur le long terme nécessite désormais plus de flexibilité et de

créativité au sein du portefeuille, tout en maintenant un environnement de gestion des

risques de plus en plus pointu, et reposant sur l‟étude systématique de scenarii divergeant

du cas de base

• Le choix des investissements est de plus en plus crucial, et le recours à des gérants de

fonds compétents et intègres doit se reposer sur une méthodologie sans faille

12

7

© 2012 Deloitte SA. Private and confidential.

Contents

13

Gestion du risque systémique et allocation tactique

Gestion du risque spécifique et sélection des investissements

© 2012 Deloitte SA. Private and confidential.

Principes clés

• Les stratégies de placement doivent être dûment documentées au sein d‟une politique

• La stratégie d‟investissement doit être en adéquation en tous temps avec la politique et

l‟appétit au risque fixé par l‟institution

• La gouvernance en matière de décision d‟investissement, de re-balancement et de

désinvestissement doit être clairement définie et documentée, et appliquée

systématiquement de manière cohérente

• L‟institution doit mettre en œuvre des méthodologies adaptées au profil de risque des

portefeuilles gérés et utiliser des outils qui soient en phase avec le degré de complexité

• Les méthodes de calcul de la performance et des indicateurs de risque doivent être

documentées afin d‟offrir le maximum de transparence aux investisseurs

• Un reporting détaillé doit être produit régulièrement afin d‟obtenir une vision optimale

de l‟évolution du profil de risque du portefeuille, y compris dans un contexte de stress

scenario

14

8

© 2012 Deloitte SA. Private and confidential.

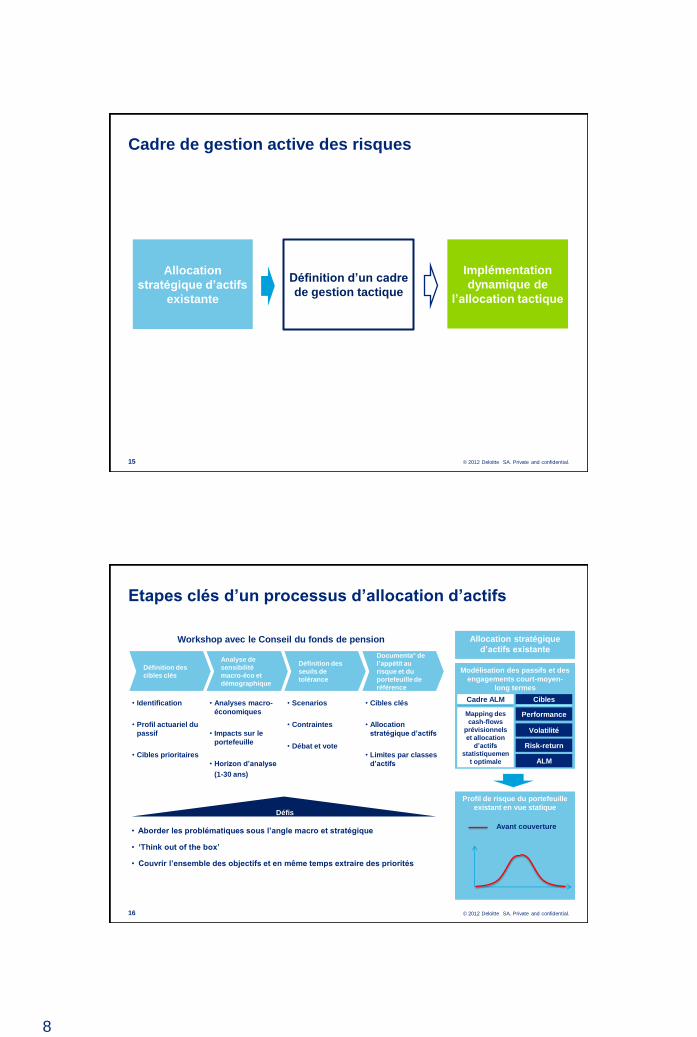

Cadre de gestion active des risques

15

Allocation

stratégique d’actifs

existante

Implémentation

dynamique de

l’allocation tactique

Définition d’un cadre

de gestion tactique

© 2012 Deloitte SA. Private and confidential.

Etapes clés d’un processus d’allocation d’actifs

16

• Aborder les problématiques sous l’angle macro et stratégique

• ‘Think out of the box’

• Couvrir l’ensemble des objectifs et en même temps extraire des priorités

Analyse de

sensibilité

macro-éco et

démographique

Définition des

seuils de

tolérance

Documenta° de

l’appétit au

risque et du

portefeuille de

référence

• Analyses macro-

économiques

• Impacts sur le

portefeuille

• Horizon d’analyse

(1-30 ans)

• Identification

• Profil actuariel du

passif

• Cibles prioritaires

• Scenarios

• Contraintes

• Débat et vote

• Cibles clés

• Allocation

stratégique d’actifs

• Limites par classes

d’actifs

Définition des

cibles clés

Workshop avec le Conseil du fonds de pension

Défis

Modélisation des passifs et des

engagements court-moyen-

long termes

Performance

Volatilité

Allocation stratégique

d’actifs existante

Profil de risque du portefeuille

existant en vue statique

Avant couverture

Risk-return

ALM

Mapping des

cash-flows

prévisionnels

et allocation

d’actifs

statistiquemen

t optimale

Cibles Cadre ALM

9

© 2012 Deloitte SA. Private and confidential.

Définition d’un cadre de gestion tactique

Définition de scenarii de

stress

Fixation de niveaux de

tolérance au risque sous

l’angle de la résilience du

portefeuille aux scenarii de

stress

Impacts sur les sensibilités

Marges d’allocations

tactiques

• Consolider les différents compartiments du portefeuille:

- Méthodologie et outils d‟analyse du risque pour l‟agrégation des différents effets dus

aux facteurs de risques

- Perspective consolidée du risque via un reporting performant

- Système de limites opérationnelles/tactiques en parallèle des limites stratégiques

• Prévoir un budget de risque pour les opérations de couverture du portefeuille:

- Définition et mise en pratique d‟un overlay « risk management » au sein du

portefeuille

- Vision tactique et ajustement à court ou moyen terme du profil d‟investissement

autour du portefeuille cible stratégique

• Effectuer une cartographie détaillée des impacts, en particulier en cas d‟occurrence des

scenarii de stress poussés:

- Mouvements des facteurs de risque et distorsions éventuelles de liquidité générées

par de tels chocs.

- Effets corrélatifs et de propagation des différents facteurs de risque

• Définir un scénario de base + plusieurs scenarii de stress (« stress tests ») en

considérant à la fois:

- Hypothèses systémiques/macro-économiques de grands chocs

- Hypothèses spécifiques

17

© 2012 Deloitte SA. Private and confidential.

Construction de portefeuille et stratégie de couverture

optimale • Définir les types de stratégies de couverture à tester:

- Faisabilité, coûts/bénéfices, besoins opérationnels, scénario „worst

case‟ et stratégies de sortie

- Anticipation des impacts sur les différents horizons de gestion et de

couverture du portefeuille

• Produire des scenarii de couverture versus sans couverture:

distribution + stress scenario et en extraire un programme de

couverture de nature contra-cyclique, avec un budget de risque

(volatilité) strict et optimal

• Eviter les biais directionnels dans les hypothèses des stratégies et

pour le testing

• „Vendre‟ la stratégie au Conseil et aux auditeurs

• Implémenter et piloter la stratégie à long terme avec un focus tactique

à court/moyen terme reposant sur un panel d‟ajustements possibles

en cas de réalisation d‟un scénario de stress donné

• Fixation d‟un système de limites élaboré à plusieurs niveaux:

opérationnel/tactique et stratégique, reposant sur des indicateurs et

de risque et des analyses de natures technique et fondamentale

Implémentation dynamique

de l’allocation tactique

Mise en place d’une allocation

tactique flexible via un budget

de risque prédéfini

Système de limites et de

contraintes stratégiques et

opérationnelles

Analyses des scenarii de

stress et des stratégies de

couverture optimales

Programme de couverture

contra-cyclique

Profil de risque du portefeuille

en vue dynamique

Après couverture

Avant couverture

σ (R) E(R)

18

10

© 2012 Deloitte SA. Private and confidential.

Gestion du risque systémique et allocation tactique Vue d‟ensemble

19

Révision du profil d’investissement

dans une perspective d’allocation

tactique et de gestion dynamique

des risques

Modélisation des passifs et des

engagements court-moyen-

long termes

Performance

Volatilité

Allocation stratégique

d’actifs existante Implémentation

dynamique de l’allocation

tactique

Définition de scenarii de stress

Fixation de niveaux de tolérance

au risque sous l’angle de la

résilience du portefeuille aux

scenarii de stress

Impacts sur les sensibilités

Mise en place d’une allocation

tactique flexible via un budget de

risque prédéfini

Système de limites et de

contraintes stratégiques et

opérationnelles

Analyses des scenarii de

stress et des stratégies de

couverture optimales Marges d’allocations tactiques

Profil de risque du portefeuille

existant en vue statique

Modélisation des facteurs clés de

risques et analyse en cas de base

et en stress scenarii

1y 2y

Avant couverture

Risk-return

Corrélations

Profil de risque du portefeuille

en vue dynamique

Après couverture

Avant couverture

Mapping des

cash-flows

prévisionnels

et allocation

d’actifs

statistiquemen

t optimale

Cibles Cadre ALM

Définition d’un cadre de

gestion tactique

Programme de couverture

contra-cyclique

σ (R) E(R)

© 2012 Deloitte SA. Private and confidential.

Contents

20

Gestion du risque systémique et allocation tactique

Gestion du risque spécifique et sélection des investissements

11

© 2012 Deloitte SA. Private and confidential.

Etapes du processus d’investissements

Stratégie d’investissement

Allocation d’actif

Analyse

Quantitative

Sélection des investissements

Analyse

Qualitative

Due diligence

opérationnelle

Décision

d’investissement

Surveillance / Suivi / Reporting

21

© 2012 Deloitte SA. Private and confidential.

Analyse Qualitative

Les 4 pierres angulaires

22

Consistance de

la performance Capacités de

recherche

démontrées

Processus

d’investissement

Stabilité de la

société de

gestion

• Préparation aux entretiens

• Analyse au niveau du groupe

• Evaluation du manager et de son équipe

• Analyse d‟attribution de la performance

• Entretiens

• Groupe:

• Statut

• Culture

• Discipline

• L‟équipe

• Expérience

• Changements

• Style & créativité

• Autres responsabilités

12

© 2012 Deloitte SA. Private and confidential.

Analyse Quantitative

23

• Mesures de surperformance (Alpha)

• Betas (sensibilités aux facteurs de risque)

• Autres ratios (information, Sharpe, Sortino, Omega)

• Maximum Drawdown

• VaR et scénarii de stress

• Style drift

• Attribution performance

• Passé l‟étape 2:

• Expérience: gestionnaire et équipe

• Analyse de style

• Analyse d‟attribution de performance

1. Screening de

l’univers 2. Analyse quantitative

3. Recherche

préliminaire

• Secteurs/segments appropriés par classe d‟actifs

• Consistance: Track record et performance

• Critères de taille minimale

© 2012 Deloitte SA. Private and confidential.

Analyse Opérationnelle

24

• Préparation du questionnaire

‒ Questions sur les processus opérationnels

‒ Approche audit et gestion des risques

‒ Couverture optimale des risques structurels et opérationnels

• Domaines couverts

‒ Test d‟intégrité des gérants

‒ Performance des avoirs sous gestion: administrateurs, dépositaires indépendants

‒ Risque de contrepartie sur les tiers: brokers, administrateurs, auditeurs, etc.

‒ Structure et gouvernance chez le gestionnaire

‒ Capacités des systèmes vs stratégie d‟investissement (intensité/fréquence des

transactions, liquidité des marchés investis, etc.)

13

© 2012 Deloitte SA. Private and confidential.

Conclusion Les défis de la gestion d‟actif des fonds de pension

25

Gérer les risques systémiques dans l‟allocation d‟actifs

Gérer les risques spécifiques des gestionnaires externes

© 2012 Deloitte SA. Private and confidential.

Asset Management: 2

• Managing systemic & specific risks

• Impact of Solvency II for insurance clients

14

© 2012 Deloitte SA. Private and confidential.

Contents

What is Solvency II for insurers

Implications for Asset Managers

27

© 2012 Deloitte SA. Private and confidential.

How is Solvency II regime structured?

Pillars are used as a way of grouping SII requirements

Solvency II can be thought of as being based on three guiding principles (pillars) which cut

across strategic, market, credit, operational, insurance and liquidity risk.

28

Liquidity Risk

Insurance Risk

Market Risk

Credit Risk

Operational Risk

SOLVENCY II

Quantification Governance Disclosure

Strategic and

Reputational Risk Pillar 1 Quantitative

Requirements

Pillar 2 Qualitative Requirements

& Rules on Supervision

Pillar 3 Supervisory Reporting

and Public Disclosure

Capital Requirements

Valuation of Assets and

Liabilities

Own Funds

System of Governance

Own Risk and Solvency

Assessment (ORSA)

Capabilities and powers

of regulators, areas of

activity

Transparency

Disclosure

requirements

15

© 2012 Deloitte SA. Private and confidential.

Pillar 1 concerns the Solvency II balance sheet. It ‘requires

regulated firms to calculate its capital requirement using either

a standard formula or an internal model’.

Solvency II foresees two levels of capital requirements:

• Solvency Capital Requirements (SCR)

–Level of capital to enable firm to absorb significant unforeseen

losses

–Gives reasonable assurance to policyholders and beneficiaries

–Calibrated at 99.5% confidence over 1 year

–Can use standard formula or own Internal Model

• Minimum Capital Requirements (MCR)

–Threshold that could trigger the ultimate supervisory action if

breached

–Unacceptable risk to policyholder

–Consider expenses in run-off

Pillar I: Quantitative requirements

Pillar 1

Quantitative

Requirements

Minimum capital

Requirement

Solvency Capital

Requirement (SCR)

Technical Provisions

Investment Rules

Own funds

Quantification

29

© 2012 Deloitte SA. Private and confidential.

Risk Types Covered by Pillar I for a life insurance

company

Economic capital

Aggregation

Market

risk

Credit

risk

Underwriting

risk

Operational

risk

• Interest rate

• Equity

• Property

• Spread

• Currency

• Concentratio

n

• Corporate

bonds

• Counterparty

:

reinsurance,

reimburseme

nt

• Mortality

• Longevity

• Disability

• Expense

• Revision

• Lapse

• Catastrophe

• Poor internal

processes,

fraud, errors,

IT problems

…

• External

events,

changing

risk, legal

changes…

Minimum Financial

Requirements

• Appropriate Technical

Provisions

(Economic Value)

• Solvency Capital

Requirement based on

complete risk profile

• Appropriate Assets

supporting the obligations

Pillar I

30

16

© 2012 Deloitte SA. Private and confidential.

‒ The Supervisory Authorities and General Rules:

• supervisors shall be responsible for evaluating how insurance and

reinsurance undertakings are assessing their capital adequacy needs

relative to their risks (i.e. the Supervisory Review Process, or SRP).

• To perform this role, they are empowered to require remedial actions

when capital does not seem to be adequate.

‒ The System of Governance: robust governance requirements being a

pre-requisite for an efficient solvency system, (re)insurance company

are requested to comply with the requirements on fit and proper, risk

management, the own risk and solvency assessment (ORSA), internal

control, internal audit, the actuarial function and outsourcing.

In particular, the underlying objective of the ORSA is to ensure

• they identify and assess all risks they are (or could be) exposed to;

• they maintain sufficient capital to face these risks; and

• they develop and better use risk management techniques in

monitoring and managing these risks.

Pillar II: Qualitative Requirements & Rules on

Supervision

1

2

Pillar 2

Qualitative

Requirements &

Rules

on Supervision

Own Risk and

Solvency

Assessment (ORSA)

Capabilities and

powers of regulators,

areas of activity

Governance

31

© 2012 Deloitte SA. Private and confidential.

Pillar III: Supervisory Reporting and Public Disclosure

Pillar 3

Supervisory

Reporting and Public

Disclosure

Transparency

Disclosure

requirements

Competition related

Elements

ctivity

Disclosure

Pillar III deals with market transparency and discipline in the insurance

industry, ensuring that firms publish key information that is relevant to

the market.

• Market transparency and discipline will be increased in order to provide a

better insight into the actual risk and return profile of an insurance company.

• Disclosure, market transparencies and market disciplines will include:

– Solvency & Financial Condition Report

– Extensive publishing duties

– Risk-Management Processes

– Scenario-Analysis

– Reinsurance Processes

– Push transparency towards corporate governance

– Dialogue with IASB

• Pillar 3 will aim to harmonise reporting to supervisors, including different

types of information a supervisor needs to perform its functions and

information normally not in public domain

• A more consistent and open regulatory framework should make it easier for

companies to sell across different markets, promoting competition

32

17

© 2012 Deloitte SA. Private and confidential.

Contents

What is Solvency II for insurers

Implications for Asset Managers

33

© 2012 Deloitte SA. Private and confidential.

Opportunities and challenges for asset managers Solvency II is presenting opportunities and challenges for asset managers. Asset managers who

recognise the opportunities and address the challenges early will have a competitive advantage

over their peers.

.

Pillar 3 Market Discipline

Opportunities

• Insurers need managers who can provide quality data in a timely fashion

Providing quality data in a timely

fashion is a business imperative for attracting insurance business

Challenges

• Report delivery time and frequency In general, the current report delivery timelines are not satisfactory for public disclosure requirements and the frequency does not allow the management to react quickly to changes in business or environment. Insurers will need quality data within days of quarter end to meet current proposed reporting requirements to regulators of 20 business days.

• On-demand capability

A compliant insurer must be able to answer supervisor’s queries promptly and provide supportive quantitative information.

Pillar 2 Supervisor Review

Opportunities

• Insurers will want to invest with managers that can evidence minimal operational risks

Insurers are required to understand and

manage all risks including outsourced services.

Challenges

• Evidencing risk management to clients

SAS 70s generally cover financial reporting risks, so evidencing risk management over investment risks will be a challenge (regular DD reviews are not likely to fulfil this requirement). Insurers need to quantify the risks embedded in the asset manager.

• On-going risk management Insurers will need to monitor asset

managers and their products on an on-going basis.

Pillar 1 Quantitative Requirements

Opportunities

• Creating bespoke products Insurers will need tailor made products

that reflect their risk tolerances and minimise capital requirements

Challenges

• Availability and quality of input data Updated quantitative methodologies may require more detail on investment strategy and investments data from the investment manager which may require new processes with custodians and administrators.

• Granularity of data and analysis

The regulation requires more detailed analysis of risks and sensitivities, which increases the volume of modelling data that needs to be processed by actuaries.

• Different requirements Different Insurers are likely to have

different information requirements for their models.

34

18

© 2012 Deloitte SA. Private and confidential.

ALM in light of Solvency II Capital charge by asset type and some consequences

35

Some predictions you have certainly already

heard :

• Increasing demand for government bonds

• Reduction of investments in risky assets

• Increasing demand for derivative instruments

and structured products

49%

39%

25%

7.5%3.3% 2.7%

0%

25%

11%9%

0%

10%

20%

30%

40%

50%

Private Equity/ Hedge

Funds

Equities Property Credit BBB Credit AA Credit AAA Government bond

10 year credit

3 year credit

But also increased discussions regarding:

• Risk/return asset profile vs. liability profile

• Initial solvency position and risk appetite

• Business strategy and choice of risks

retained

ALM is a major component of Pillar II and

ORSA (Own Risk and Solvency Assessment)

© 2012 Deloitte SA. Private and confidential.

Tailored asset structures for Solvency II purposes Challenges of transparency on risk reporting

36

•Under the Solvency II Standard Formula, insurers will need to obtain reporting on the

sensitivity of each investment to the following dimensions defined in the market risk

module: Equity, Spread, Interest, Property, Currency, Illiquidity and Concentration

• The capital charge for market risk module (SCRMarket) is calculated at each sub-module

and then a pre-defined correlation matrix is used to determine overall capital requirement

• Treatment of investment funds under (SCRMarket) can follow on of those 3 methods:

• Look-through approach: composition of the fund is known and each sub module

applied to relevant underlying assets of the fund to estimate overall SCRMarket

• ->This is the approach to favor

• Mandate-based approach: assumes the investment fund invests in accordance with

its mandate in a way to produce the maximum overall capital requirement

• -> Need to define the maximum risk under the mandate

• Alternatively, if the investment fund is neither transparent nor its mandate clear

enough, it triggers the highest capital requirement (40%).

• -> The trigger to disinvestment by many insurers from hedge funds real estate

and private equity

19

© 2012 Deloitte SA. Private and confidential.

Risk Management in non-financial

Corporations

3

© 2012 Deloitte SA. Private and confidential.

Contents

Introduction: New Context

Integrated Corporate Financial Risk Management

38

20

© 2012 Deloitte SA. Private and confidential.

More global means more risks Corporations in Switzerland are getting more global...

... and this creates additional risks

39

Interest rates

Good: current cost of financing

Bad:

• Refinancing 2011-13: term & currency

• Value of leveraged/financed projects

• Cost of hedging (upward slope + vol)

• Low return on liquidities and cash

Cash management

• Pooling of cash with multiple

currencies, locations

• Dealing with more banks (credit &

country risk)

• Capital movement restrictions in some

countries

Exchange rates

Good: imports, global acquisitions

Bad:

• Competitiveness of exports (pricing,

margins)

• Consolidated value of net assets

• Transaction risks intercompany

• Cost/benefits of business relocations

Commodity price

• Cost & supply of inputs for food &

beverage, manufacturing, etc.

• Energy: cost of transportation, shipping

and heating/cooling

• Uncertain value of inventories

• New commodities = new risks

• Volatility = cost of hedging (margin)

© 2012 Deloitte SA. Private and confidential.

Hedging challenges Some exposures are naturally hedged but some remain

40

• Identify and measure how

FX, commodity and interest

rates interact and affect

results on a consolidated

basis (eg. oil cost vs USD

revenues)

1. Modify the business model (pricing,

integration, M&A, relocate production in

export markets,...)

but these decisions have strategic

and structural implications (tax,

human capital, infrastructures, inputs

supply, know how, feasibility, timing…)

2. Consider financial hedges: key domain

of the treasurer

Two ways to hedge net exposure

Assess net exposure across

all risks and business

21

© 2012 Deloitte SA. Private and confidential.

Contents

Introduction: New Context

Integrated Corporate Financial Risk Management

41

© 2012 Deloitte SA. Private and confidential.

The risk management framework How to optimize the hedging strategy with corporate objectives

42

Business model

Key Targets

Working Capital

EBIT Net Inc

ROCE ROE

EVA SVA

+ =

Board of Directors Treasurer

Pro-forma financials

Risk factors sensitivity

Forecasted cash flows

EBIT = Earnings Before Interests & Taxes; ROCE = Return On Capital Employed;

ROE = Return On Equity; EVA = Economic Value Added; SVA = Shareholder Value Added;

Hedging strategy

+

Derivatives

Hedge Accounting

Hedge Accounting

Results risk profile

After hedging

Key risk factors

1y 2y

Before hedging

1

2

3

5 4

22

© 2012 Deloitte SA. Private and confidential.

Setting risk appetite and objectives Tone from the top

43

Challenges:

• Keep discussion at macro and strategic level

• Avoid consensus forecast (think out of the box)

• Cover all strategic objectives and prioritize at the same time

Macro

sensitivity

analysis

Define

tolerance

levels

Document risk

appetite

• Economic &

Accounting

• Prices impact

• Horizon (1-3y)

• Identify

• Prioritize

• Debate & vote

• Scenarios

• Constraint

• Debate & vote

• Key targets

• Tolerance levels

• Hedging

approach

Define

key targets

Workshop with the Board of Directors

Key Targets

Working Capital

EBIT Net Inc

ROCE ROE

EVA SVA

1

© 2012 Deloitte SA. Private and confidential.

Identifying business model exposures Key challenges

44

Pro-forma

financials

Risk

factors

sensitivity

Forecasted

cash flows

Hedge

Accounting

• Define clear pro forma financials based on expected results and market prices

• Develop long term forecasts of corporate cash flows

• Identify all relevant market risks impacting financial results (B/S, I/S, CFS, ratios, etc)

• Map material accounts impacted by change in key risk factors:

- Translate risk factor changes into accounting results and cash movements over

the time horizon

- Combine cross effects of risk factors (eg. FX + Interest rates)

• Consolidate all accounts with modeled sensitivities

- Need tool to combine all accounts under specific GAAP with consolidation of risk

factor effects

- Consolidated picture & single entity perspective

- Avoid being lost in details & keep coherence of results

• Add capacity for financial hedges to the business model

- Define types of derivatives and related accounting rules (Fwd, Swap, Futures,

Options)

- Assess financial statements impacts from changes in markets, with hedge

accounting or not

Business model

Pro-forma financials

Risk factors sensitivity

Forecastedcash flows

Hedge Accounting

2

23

© 2012 Deloitte SA. Private and confidential. 45

Modeling market risk factors Key challenges

• Coherent with past data

and current markets

• Steps (month/quarter)

• Horizon (1 – 3 y)

• Use historical data

• Mean reversion

• Regime changes

• Seasonnality

Building scenarii &

models

Testing scenarii &

models

• Coherent co-

dependence &

correlations

• Don‟t miss potential

worst cases

• Back-test results

• Usable in business

model

Forecast key risk

factors

3

© 2012 Deloitte SA. Private and confidential.

• Present key target variables and time horizon

• Illustrate tolerance levels

• Present clear distribution of net risk exposures

• Measure combined effect of different risk factors

• Measure aggregate impact on the whole business model

46

Building corporate risk reporting Key challenges

Results risk profile

Before hedging

4

24

© 2012 Deloitte SA. Private and confidential.

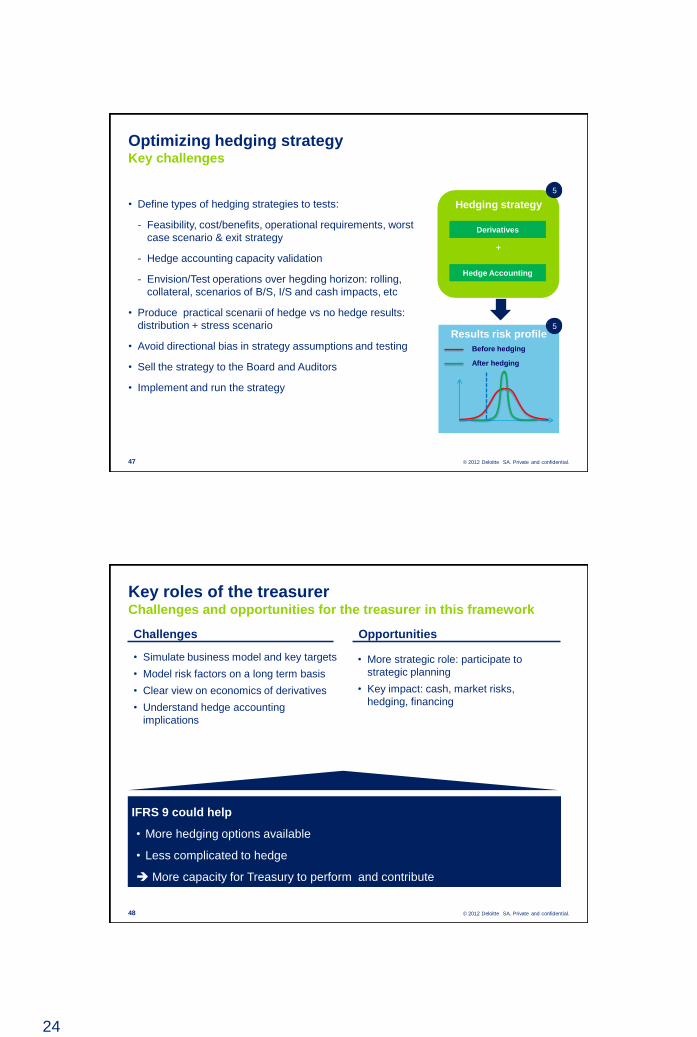

• Define types of hedging strategies to tests:

- Feasibility, cost/benefits, operational requirements, worst

case scenario & exit strategy

- Hedge accounting capacity validation

- Envision/Test operations over hegding horizon: rolling,

collateral, scenarios of B/S, I/S and cash impacts, etc

• Produce practical scenarii of hedge vs no hedge results:

distribution + stress scenario

• Avoid directional bias in strategy assumptions and testing

• Sell the strategy to the Board and Auditors

• Implement and run the strategy

47

Optimizing hedging strategy Key challenges

Results risk profile

After hedging

Hedging strategy

+

Derivatives

Hedge Accounting

Before hedging

5

5

© 2012 Deloitte SA. Private and confidential.

Key roles of the treasurer Challenges and opportunities for the treasurer in this framework

48

Challenges Opportunities

• Simulate business model and key targets

• Model risk factors on a long term basis

• Clear view on economics of derivatives

• Understand hedge accounting

implications

• More strategic role: participate to

strategic planning

• Key impact: cash, market risks,

hedging, financing

IFRS 9 could help

• More hedging options available

• Less complicated to hedge

More capacity for Treasury to perform and contribute

25

© 2012 Deloitte SA. Private and confidential.

Risk Management in Commodity

Trading

4

© 2012 Deloitte SA. Private and confidential.

Business Strategies and Related Risks

An entity may choose to engage in various business strategies, including certain types of financial

activities (thereby incurring risk), because it believes that it is well positioned to profit from such activity.

REWARD

RISKLow High

High

Low

Marketing

Trading

Dealing

Note: marketing and dealing activities may present

greater or lesser risks depending on specific

strategies utilized.

An integrated energy company may engage in

marketing, dealing, or trading.

Each of these activities entails very different

risk profiles with corresponding risk/return

relationships as depicted.

Marketing is the activity of selling available

energy that is backed up by a company‟s

generation assets.

Dealing is the process of entering into

simultaneous transactions for which the risks

offset, locking in a margin in between.

Trading entails consciously taking a market

position based on a proprietary view of market

conditions and prices. In trading, there is a

clear recognition that the proprietary positions

result in market price exposure, but there is an

expectation of additional profit from assuming

this risk.

50

26

© 2012 Deloitte SA. Private and confidential.

The risk of human error or

fraud, or that the system of

control will fail to adequately

record, monitor, and account

for transactions or positions.

The potential financial loss

resulting from a counterparty‟s

failure to honor its obligations.

The potential change in value

of a contract, liability or cash

flow given adverse movements

in market factors.

Policies and

procedures

Controls

Limits

Probability of

counterparty default

Amount of

counterparty

exposure

Volatility of markets

Price Risk

Curve/Model Risk

Liquidity Risk

Spread Risk

Location Risk

Option Risk

Volumetric Risk

Operational

Risk

Credit Risk

Market Risk

Definition Components Risk Type

Difficult to Measure

Measurable

Measurable

Measurability

Energy Trading Related Risks There are 4 categories of risk to measure and manage

The risk to fall short of

liquidities in the overall books

of the companies due to the

structure of cash inflows and

outflows

Contractual inflows

and outflows

Cost of financing

Effects of Market and

Credit Risks on cash

Treasury

Risk

Difficult to Measure

51

© 2012 Deloitte SA. Private and confidential.

Accounting Flow Transaction Order

Economical Flow Product Pricing

Month 2

Brent

Physical Flow Product

Transportation Time

Treasury Flow Definitive Cash Settlement

Transaction Flow View

Transaction Risk View

Market Risk

Operational Risk

Credit Risk

Treasury Risk

Provisional Cash Flow

Inventory Recording

Risks in a transaction lifecycle There are four dimensions of flows that interact to impact the

different types of risk over the lifecycle of commodity trading

52

27

© 2012 Deloitte SA. Private and confidential.

Drivers of Risk Affects Examples

Market Changes Prices Oil Price Increase

Volatilities Spark-Spread

Correlation Trader Confidence

Demand Volatilities

Liquidity

Commodity Physical System Changes Storage Available Capacity

Capacity Forced Outage

Delivery

Transmission

Human Error Trader Administrative Error

Quant Valuation Error

Management Trading Loss

Credit Management Decision

Modeling

Drivers of Risk Amount and change in level of risk can be affected by a number of

drivers

53

© 2012 Deloitte SA. Private and confidential.

Volumetric Risk:

Changes in value of assets and liabilities from the change in customer demand.

Example:

Power demanded varies in response to customer outages, weather, market prices etc. These

changes in demand can affect market prices, net supply positions, and portfolio value.

Credit Risk:

Credit Risk is the potential loss of value from the default of payment or delivery by a

counter-party less recovery.

Examples:

1. Counter-party does not deliver power associated with a physical call option. Power must be

procured at current market prices.

2. Counter-party does not pay for delivered power.

Volumetric and Credit Risks Value of a portfolio can change as a result of volatility in market

price, physical volume demanded and counterparties ability to fulfil

commitments

54

28

© 2012 Deloitte SA. Private and confidential.

Types of Risk Analysis

• Current Risk: Portfolio Mark to

Market

• Probable Risk: Value at Risk (VAR)

• Improbable Risk: Risk Stress and

Scenario Simulation

• Portfolio Sensitivity

–Delta

–Gamma

–Vega

–Theta

–Rho

• Credit Exposure/Credit Value at Risk

Measures

• Portfolio value at a period of time

• Measures potential losses to portfolio value in a given

time period with a confidence interval

• Provides a broader view of potential market scenario

occurrences including unusual events

• Measures the sensitivity of portfolio value changes to

changes in drivers

• Sensitivity to price change

• Sensitivity to volatility change

• Sensitivity to time

• Sensitivity to discount rates

• Sensitivity to changes in delta

• Measures current and potential exposure to risk of default

of payment and delivery as well as potential recovery.

CVAR measures potential exposure.

Type of Risk Analysis Market Risk is measured by analyzing changes in portfolio values

55

© 2012 Deloitte SA. Private and confidential.

Constructing a forward curve that is useful for trading and risk management

purposes often involves an elaborate extrapolation exercise

The resulting curve is typically partly market-based and partly model-based,

and hence may not be entirely transactable.

If a majority of price setters end up using similar econometric models – for

example mean-reverting -- it is possible (but by no means guaranteed) that

model-based forward prices converge to market prices at the longer end of

the curve.

As the markets get deeper and more liquid, longer dated instruments will

begin to appear, and the forward curve will be more market-based and less

model-based in course of time.

While longer dated contracts are presently transacted in OTC markets, the

forward curves underlying these transactions are not publicly available.

Understandably, these curves are viewed as extremely proprietary.

Given liquidity in energy and especially power markets is limited to short maturities (12-

18 months), a forward curve needs to be synthetically constructed from market data.

Type of Risk Analysis – Current Risk Forward curves

56

29

© 2012 Deloitte SA. Private and confidential.

The maximum shortfall of earnings, relative to a specified

target, that could be experienced over a given horizon

period at a given level of confidence.

The maximum shortfall of value, relative to a specified

target, that could be experienced over a given horizon

period at a given level of confidence.

The maximum shortfall of net cash generated, relative to a specified target, that could be experienced over a given horizon period at a given level of confidence.

Earnings at Risk

(EaR)

Value at Risk

(VaR):

Cash Flow at Risk

(CFaR):

Type of Risk Analysis – Probable Risk Probable risk measures take into consideration the stochastic

variation of historical prices to indicate potential exposure

57

© 2012 Deloitte SA. Private and confidential.

Management and Measurement of Risks

58

VIEW

RISK OBJECTIVE

RISK MEASURE

PERFORMANCE MEASURE

TRADING WHOLESALE

MARKETING

RETAIL

MARKETING RESOURCES

Long-Term Long-Term Short-Term Short-Term

Balanced Minimized Minimized Exposed

EaR EaR VaR VaR

CFROI CFROI RAROC RAROC

PORTFOLIOS

An activity based book structure more meaningfully distinguishes between different

risk objectives and capital utilization, and better supports alternative risk and

performance measures.

Cash Flow Return on Investment (CFROI): an approximation of the average real rate of return earned by a

company on all of its operating assets; a discounted cash flow (DCF) metric.

Risk Adjusted Return on Capital (RAROC)): the ratio of return (often adjusted by expected loss) to economic

capital, where economic capital is defined as VaR and GMaR for trading activities plus unexpected loss.

58

30

© 2012 Deloitte SA. Private and confidential.

Tiers of Complexity for Advanced Analytics

Market

Research

Deterministic

Models

Dynamic

Valuation/Risk Measurement

Dynamic

Optimization

• Optimize individual assets (e.g. storage)

• Optimize portfolios using risk and expected return

• Optimize tactical activities (e.g. fuel procurement)

• Incorporate volatility and correlation

• Generate Earnings/Cash Flow @ Risk measures

• Quantify optionality across the value chain

• Forecast flat prices and diffs

• Model arbitrage opportunities

• Generate intrinsic value estimates of options

• Process fundamental and technical market data

• Estimate market trends

59

© 2012 Deloitte SA. Private and confidential.

Example of Advanced Analytics – O&G

60

Market

Research

Price

Forecasting

Arbitrage

Transport

(pipelines/shipping)

Portfolio

Optimization

Crude

Supply

Directional

intuition only

Deterministic

Models

Dynamic

Valuation/Risk

Measurement

Using

fundamental

and/or technical

methods

Dynamic

Optimization

Storage

Using

Fundamental

and/or

technical

methods

Includes

single price

forecasts and

other market

conventions

Generates

“intrinsic value”

estimates

based on

deterministic

forecast

Incorporate

volatility and

correlation

Generate “extrinsic

value” estimates

for location spread.

Real option value of

destination switching

Quantify the option

to wait to purchase

crude supply

Options across time

and crude type

Time spread

options

Optimal injection/

withdrawal

Portfolio of assets,

structured

contracts, hedges

and trades each

with a value and a

risk level

Maximize the

portfolio value

given an specified

level of risk

60

31

© 2012 Deloitte SA. Private and confidential.

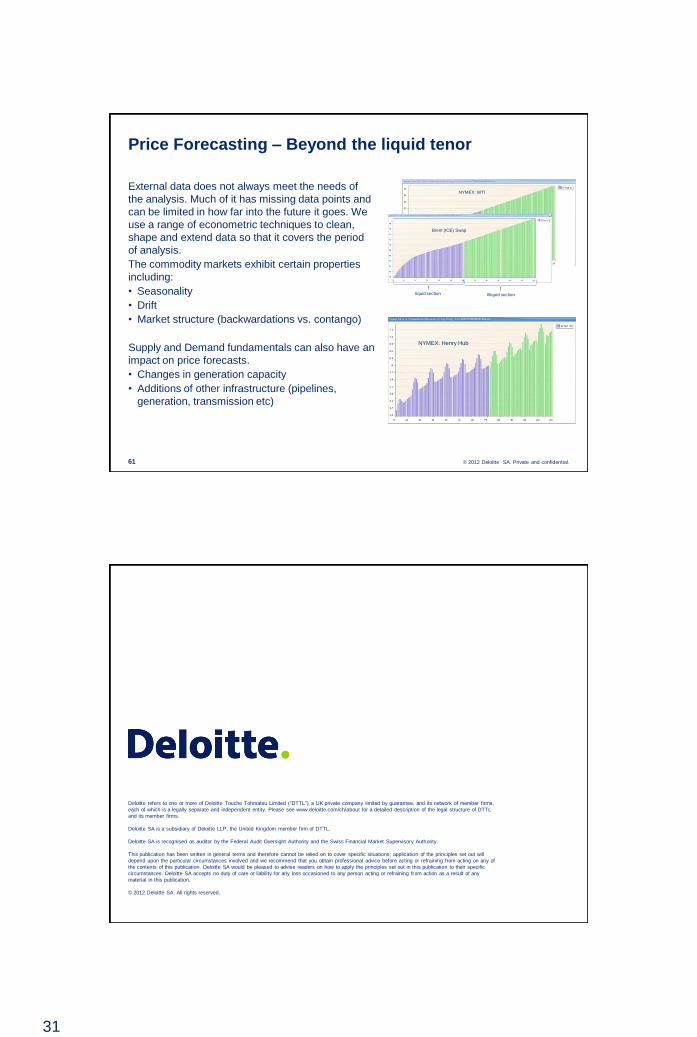

External data does not always meet the needs of

the analysis. Much of it has missing data points and

can be limited in how far into the future it goes. We

use a range of econometric techniques to clean,

shape and extend data so that it covers the period

of analysis.

The commodity markets exhibit certain properties

including:

• Seasonality

• Drift

• Market structure (backwardations vs. contango)

Supply and Demand fundamentals can also have an

impact on price forecasts.

• Changes in generation capacity

• Additions of other infrastructure (pipelines,

generation, transmission etc)

Price Forecasting – Beyond the liquid tenor

NYMEX: WTI

Brent (ICE) Swap

Illiquid sectionliquid section

NYMEX: Henry Hub

61

© 2012 Deloitte SA. Private and confidential.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms,

each of which is a legally separate and independent entity. Please see www.deloitte.com/ch/about for a detailed description of the legal structure of DTTL

and its member firms.

Deloitte SA is a subsidiary of Deloitte LLP, the United Kingdom member firm of DTTL.

Deloitte SA is recognised as auditor by the Federal Audit Oversight Authority and the Swiss Financial Market Supervisory Authority.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will

depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of

the contents of this publication. Deloitte SA would be pleased to advise readers on how to apply the principles set out in this publication to their specific

circumstances. Deloitte SA accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any

material in this publication.

© 2012 Deloitte SA. All rights reserved.

62