Embed Size (px)

Citation preview

APPENDIX 4E – PRELIMINARY FINAL REPORT

Name of Entity: Crowe Horwath Australasia Ltd

(formerly WHK Group Limited)

ABN: 93 006 650 693

Period: Year Ended 30 June 2013

The following documents comprise the information required to be given

to the ASX in accordance with Listing Rule 4.3A.

20 August 2013

For

per

sona

l use

onl

y

Crowe Horwath Australasia Ltd

Appendix 4E

Preliminary Final Report

Appendix 4E

Preliminary Final Report

Name of entity

Crowe Horwath Australasia Ltd (formerly WHK Group Limited) and its Controlled Entities

Reporting Period (year ended) Previous Corresponding Period (year ended)

30 JUNE 2013 30 JUNE 2012

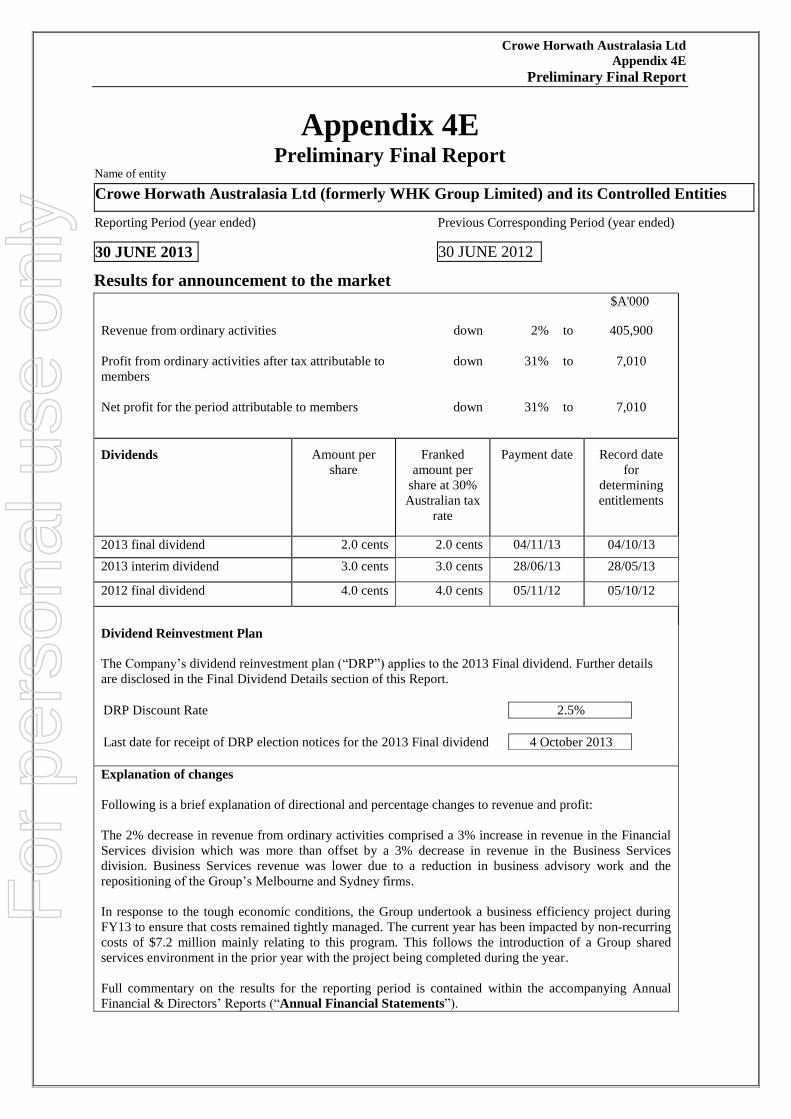

Results for announcement to the market

$A'000

Revenue from ordinary activities

down

2%

to

405,900

Profit from ordinary activities after tax attributable to

members

down

31%

to

7,010

Net profit for the period attributable to members

down

31%

to

7,010

Dividends

Amount per

share

Franked

amount per

share at 30%

Australian tax

rate

Payment date Record date

for

determining

entitlements

2013 final dividend 2.0 cents 2.0 cents 04/11/13 04/10/13

2013 interim dividend 3.0 cents 3.0 cents 28/06/13 28/05/13

2012 final dividend 4.0 cents 4.0 cents 05/11/12 05/10/12

Dividend Reinvestment Plan

The Company’s dividend reinvestment plan (“DRP”) applies to the 2013 Final dividend. Further details

are disclosed in the Final Dividend Details section of this Report.

DRP Discount Rate 2.5%

Last date for receipt of DRP election notices for the 2013 Final dividend 4 October 2013

Explanation of changes

Following is a brief explanation of directional and percentage changes to revenue and profit:

The 2% decrease in revenue from ordinary activities comprised a 3% increase in revenue in the Financial

Services division which was more than offset by a 3% decrease in revenue in the Business Services

division. Business Services revenue was lower due to a reduction in business advisory work and the

repositioning of the Group’s Melbourne and Sydney firms.

In response to the tough economic conditions, the Group undertook a business efficiency project during

FY13 to ensure that costs remained tightly managed. The current year has been impacted by non-recurring

costs of $7.2 million mainly relating to this program. This follows the introduction of a Group shared

services environment in the prior year with the project being completed during the year.

Full commentary on the results for the reporting period is contained within the accompanying Annual

Financial & Directors’ Reports (“Annual Financial Statements”).

For

per

sona

l use

onl

y

Crowe Horwath Australasia Ltd

Appendix 4E

Preliminary Final Report

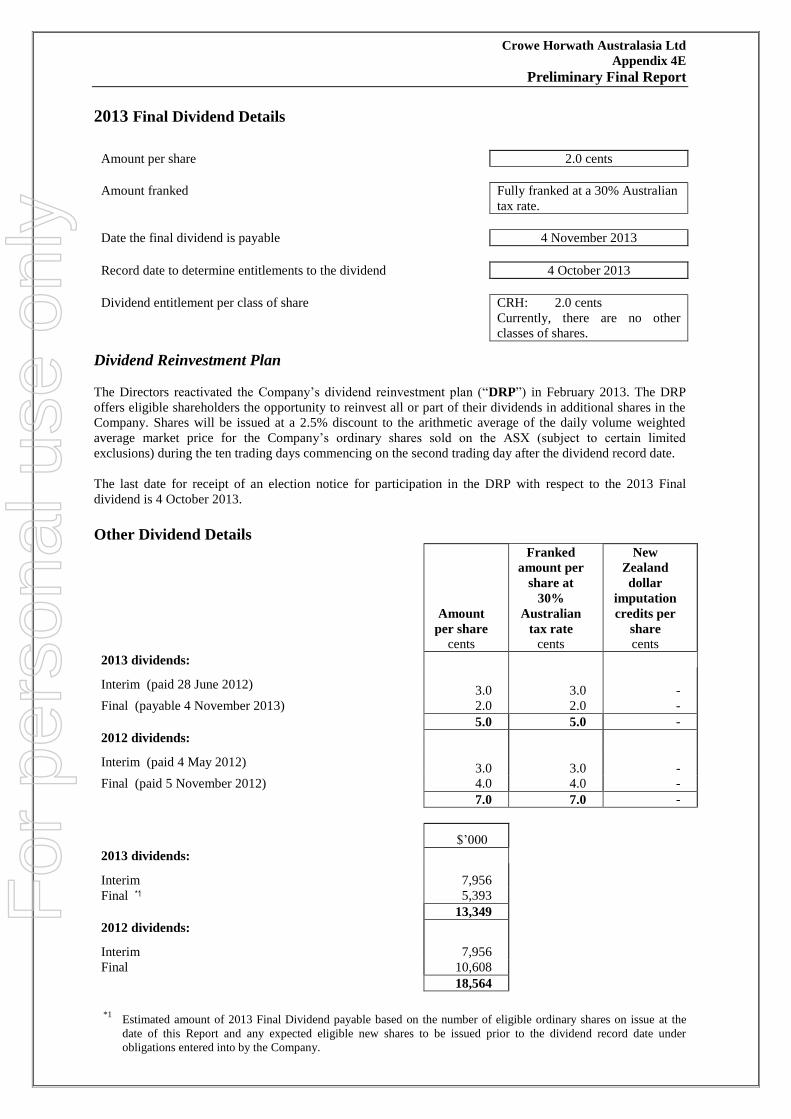

2013 Final Dividend Details

Amount per share 2.0 cents

Amount franked Fully franked at a 30% Australian

tax rate.

Date the final dividend is payable 4 November 2013

Record date to determine entitlements to the dividend 4 October 2013

Dividend entitlement per class of share

CRH: 2.0 cents

Currently, there are no other

classes of shares.

Dividend Reinvestment Plan

The Directors reactivated the Company’s dividend reinvestment plan (“DRP”) in February 2013. The DRP

offers eligible shareholders the opportunity to reinvest all or part of their dividends in additional shares in the

Company. Shares will be issued at a 2.5% discount to the arithmetic average of the daily volume weighted

average market price for the Company’s ordinary shares sold on the ASX (subject to certain limited

exclusions) during the ten trading days commencing on the second trading day after the dividend record date.

The last date for receipt of an election notice for participation in the DRP with respect to the 2013 Final

dividend is 4 October 2013.

Other Dividend Details

Amount

per share

cents

Franked

amount per

share at

30%

Australian

tax rate

cents

New

Zealand

dollar

imputation

credits per

share

cents

2013 dividends:

Interim (paid 28 June 2012)

3.0

3.0

-

Final (payable 4 November 2013) 2.0 2.0 -

5.0 5.0 -

2012 dividends:

Interim (paid 4 May 2012)

3.0

3.0

-

Final (paid 5 November 2012) 4.0 4.0 -

7.0 7.0 -

$’000

2013 dividends:

Interim 7,956

Final *1 5,393

13,349

2012 dividends:

Interim 7,956

Final 10,608

18,564

*1 Estimated amount of 2013 Final Dividend payable based on the number of eligible ordinary shares on issue at the

date of this Report and any expected eligible new shares to be issued prior to the dividend record date under

obligations entered into by the Company.

For

per

sona

l use

onl

y

Crowe Horwath Australasia Ltd

Appendix 4E

Preliminary Final Report

Net Tangible Asset Backing

As at

30 June 2013

cents

As at

30 June 2013

cents

Net tangible assets per share 5.4 8.7

Status of Audit

An unqualified, signed Independent Auditor’s Report is included within the Annual Financial Statements

which accompany this Report.

Control Gained Over Entities During the Year

Name of entity

Date control

was gained

Companies (all 100% owned)

Crowe Horwath NZ Financial Advice Limited 9 May 2013

Businesses

Dudenas Financial Planning 1 August 2012

Coopers Accountants & Advisors 1 October 2012

Bronwyn Monopoli 19 October 2012

Martin Mulcahy Business Solutions 1November 2012

Thompson Croft 1 February 2013

McMasters Accounting Services 15 April 2013

Details of the business combinations completed during the year are shown in Note 22 to the Annual Financial

Statements which accompany this Report where material to the understanding of that Report.

Loss of Control of Entities During the Year

The following wholly owned subsidiary companies where de-registered or liquidated during the year:

Name of entity

Companies (all 100% owned)

Date control

was lost

WHKCP Pty Ltd 13 October 2012

WHK Superannuation Pty Limited

WHK Tax Lawyers Pty Ltd

21 October 2012

31 May 2013

For

per

sona

l use

onl

y

Crowe Horwath Australasia Ltd

Appendix 4E

Preliminary Final Report

Issued Securities at the End of the Current Period – 30 June 2013

Total

number

Number

quoted

Price per

security

Amount

paid up per

security

Ordinary shares

Ordinary classes

269,665,096

269,665,096

Changes during the current year:

Avg Avg

Increases through issues – Dividend

Reinvestment Plan 4,464,444 4,464,444 $0.66 $0.66

Performance Rights

Right to a fully paid ordinary share

1,000,000

nil

Changes during the current year: - -

Schedule of Outstanding Performance Rights at 30 June 2012

Granted No. of Rights Performance Period

November 2011 1,000,000 1 July 2011 to 30 June 2014

Capital Management

The Company has established an on-market share buy-back scheme for capital management purposes

including for use in conjunction with employee share plans and the dividend reinvestment plan. No shares

were acquired on-market during the current period.

Financial Statements and Commentary on the Results for the Year

A statement of comprehensive income, a statement of financial position, a statement of changes in equity and a

statement of cash flows for the year ended 30 June 2013, presented on a consolidated basis with accompanying

notes, are contained in the Annual Financial Statements which accompany this Report.

A commentary on the results for the year ended 30 June 2013 is also contained within the Annual Financial

Statements.

2013 Annual Meeting

The 2013 Annual Meeting of shareholders of the Company will be held as follows:

Time and date:

9.30 am on Monday 21 October 2013

Place:

RACV Club (Bourke Room 1 & 2)

Level 2, 501 Bourke Street, Melbourne, Victoria, Australia

B Paterson

Company Secretary

20 August 2013

For

per

sona

l use

onl

y

ANNUAL FINANCIAL &

DIRECTORS’ REPORTS

2013

CROWE HORWATH AUSTRALASIA LTD

(FORMERLY WHK GROUP LIMITED)

ACN 006 650 693

AND ITS CONTROLLED ENTITIES For

per

sona

l use

onl

y

CONTENTS

1 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Contents 1

Chairman’s Report 2

Directors’ Review 5

Directors’ Report 14

Corporate Governance Statement 31

Financial Report 42

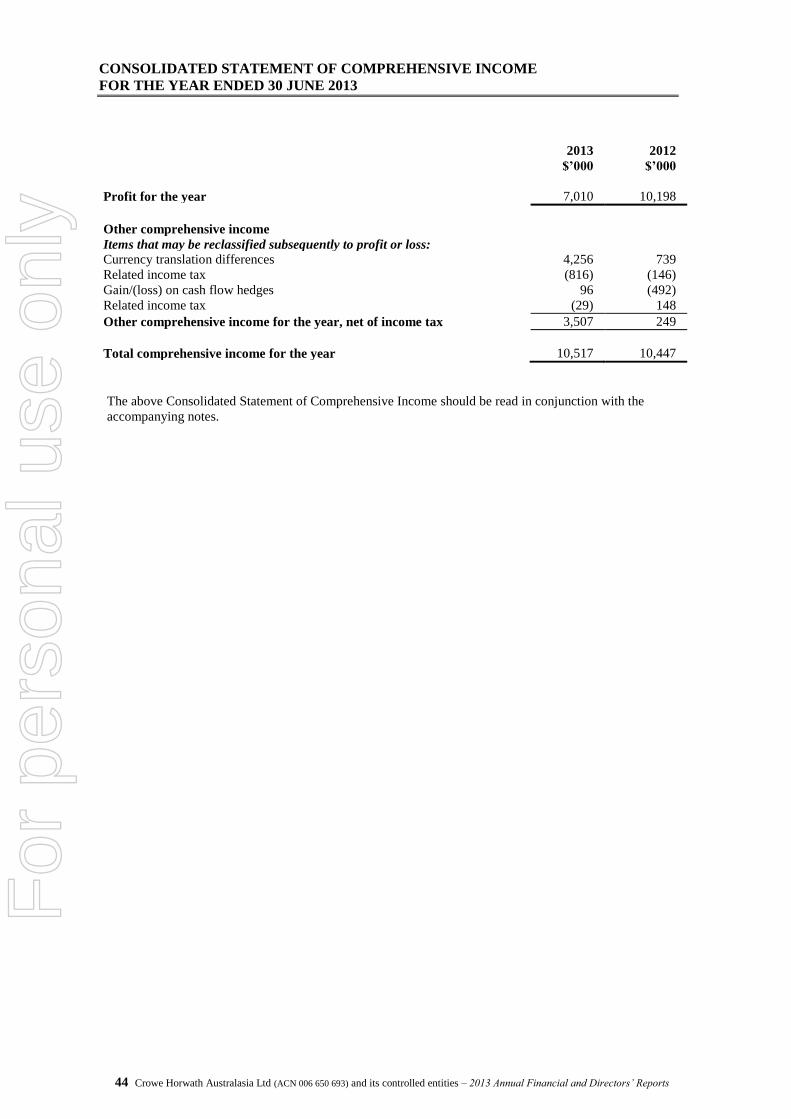

Consolidated Income Statement for the year ended 30 June 2013 43

Consolidated Statement of Comprehensive Income for the year ended 30 June 2013 44

Consolidated Statement of Financial Position as at 30 June 2013 45

Consolidated Statement of Changes in Equity for the year ended 30 June 2013 46

Consolidated Statement of Cash Flows for the year ended 30 June 2013 47

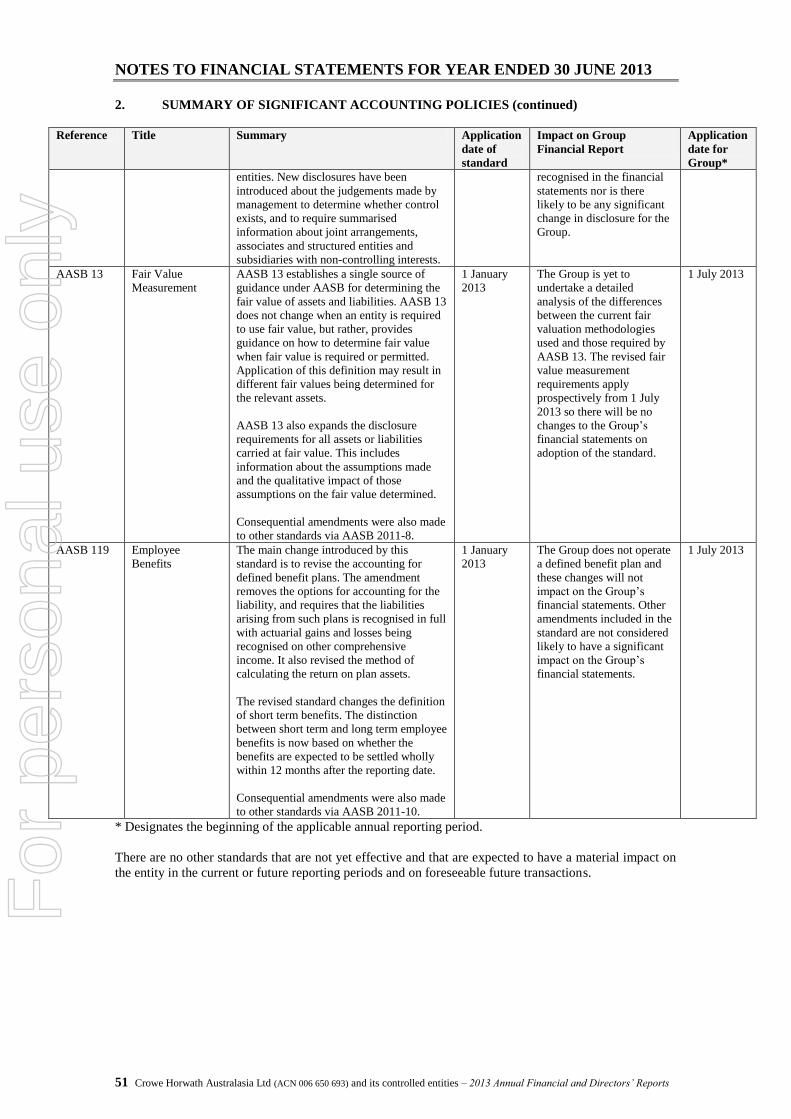

Notes to Financial Statements for the year ended 30 June 2013 48

Directors’ Declaration 108

Auditor’s Independence Declaration 109

Independent Audit Report to Members 110

ASX Shareholder Information 113

Company Particulars 115

For

per

sona

l use

onl

y

CHAIRMAN’S REPORT

2 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Crowe Horwath Australasia Ltd (the Group) has experienced difficult trading conditions during the

year. The Group has found business confidence to be low in its key client demographic, being the SME

sector, which has impacted on the ability or willingness for clients to commit to discretionary

expenditure. The reported profit for the year has decreased reflecting these difficult economic

circumstances. Whilst external conditions have been particularly challenging, the business has completed

many of the transformation projects initiated over the past two years. These include a restructured and

aligned leadership team, new remuneration model for principals, business efficiency program, Group

shared services environment and a successful move to one brand.

Operating Performance

Group revenue decreased by 2% to $405.9 million during the year. Pleasingly revenue from the Financial

Services Division grew by 3% to $94.6 million. It is worth noting this positive result in an environment

where global economic conditions remain uncertain. Revenue was up across the Financial Services

Division but was particularly strong in Risk Insurance, General Insurance and Finance Broking.

Financial Planning revenue growth was modest at 1% but increased activity to drive cross referrals in the

business succeeded in increasing up-front revenue by 11%. This places the Group in a strong position to

build on this performance in future periods. Self Managed Super Administration recorded solid revenue

growth of 3% and remains an important strategic service line as the Group seeks to leverage its market

leadership position.

Business Services revenue decreased by 3% to $311.3 million. The Group continues to benefit from a

client base requiring a high level of non-discretionary compliance work across a large number of

geographical centres, in both regional and capital city locations in Australia and New Zealand. The

overall decline in Business Services revenue is attributable to a decrease in the more profitable business

advisory work. Clients restricted their discretionary expenditure during the year with respect to advisory

services, reflecting the uncertain wider economic and political outlook. This resulted in the Group

announcing a trading update in April 2013 that second half earnings were expected to be down on the

previous year. Business Services revenue was also impacted by the repositioning of the Group’s

Melbourne and Sydney firms following the departure of a number of principals over the past 18 months.

New principals have been appointed to refocus these businesses on end to end business advisory

capability. The Group expects the benefits from these changes to be recognised over time as the new

principals build their revenue capability.

In response to the tough economic conditions the Group undertook a business efficiency project during

the year to ensure that costs remained tightly managed. The Group will continue to recognise the

incremental benefits of this project in the next financial year and beyond.

Net Profit After Tax at $7.0 million compares to the prior year of $10.2 million. The current year

includes significant non-recurring costs associated with, principally, the business efficiency program.

Normalised Earnings Before Interest, Tax and Amortisation (i.e. before project/ non-recurring costs), a

more meaningful indicator of underlying performance was $26.5 million (2012: $36.6 million). The

lower earnings are mainly due to lower business services revenue.

In summary, the difficult business conditions have brought about a result that is reflective of the

conditions and confidence in the Group’s target SME markets. The Group is proud of the trusted

relationships that it holds with its clients and is confident that it is well placed to provide high quality

business advice to its clients when confidence returns to the sector. The Group has achieved solid

earnings growth in Financial Services and is well placed to benefit from rising financial markets in future

periods. The actions taken through the business efficiency program should also lead to improved

profitability in future periods.

Operating Cash Flow & Financial Position

Cash flow from operations was maintained with a surplus of $10.7 million (2012: $20.7 million). The

operating cash flow was impacted primarily by lower business advisory revenue and the costs of

executing the business efficiency program in the current year.

For

per

sona

l use

onl

y

CHAIRMAN’S REPORT

3 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

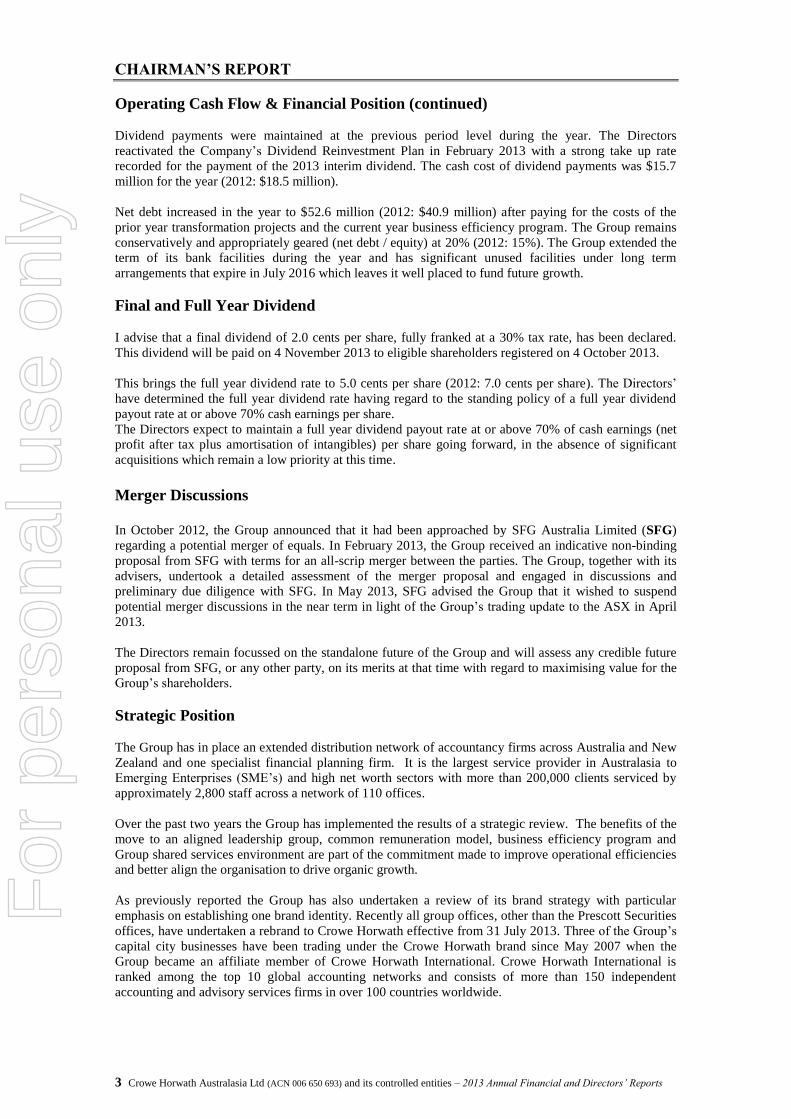

Operating Cash Flow & Financial Position (continued)

Dividend payments were maintained at the previous period level during the year. The Directors

reactivated the Company’s Dividend Reinvestment Plan in February 2013 with a strong take up rate

recorded for the payment of the 2013 interim dividend. The cash cost of dividend payments was $15.7

million for the year (2012: $18.5 million).

Net debt increased in the year to $52.6 million (2012: $40.9 million) after paying for the costs of the

prior year transformation projects and the current year business efficiency program. The Group remains

conservatively and appropriately geared (net debt / equity) at 20% (2012: 15%). The Group extended the

term of its bank facilities during the year and has significant unused facilities under long term

arrangements that expire in July 2016 which leaves it well placed to fund future growth.

Final and Full Year Dividend

I advise that a final dividend of 2.0 cents per share, fully franked at a 30% tax rate, has been declared.

This dividend will be paid on 4 November 2013 to eligible shareholders registered on 4 October 2013.

This brings the full year dividend rate to 5.0 cents per share (2012: 7.0 cents per share). The Directors’

have determined the full year dividend rate having regard to the standing policy of a full year dividend

payout rate at or above 70% cash earnings per share.

The Directors expect to maintain a full year dividend payout rate at or above 70% of cash earnings (net

profit after tax plus amortisation of intangibles) per share going forward, in the absence of significant

acquisitions which remain a low priority at this time.

Merger Discussions

In October 2012, the Group announced that it had been approached by SFG Australia Limited (SFG)

regarding a potential merger of equals. In February 2013, the Group received an indicative non-binding

proposal from SFG with terms for an all-scrip merger between the parties. The Group, together with its

advisers, undertook a detailed assessment of the merger proposal and engaged in discussions and

preliminary due diligence with SFG. In May 2013, SFG advised the Group that it wished to suspend

potential merger discussions in the near term in light of the Group’s trading update to the ASX in April

2013.

The Directors remain focussed on the standalone future of the Group and will assess any credible future

proposal from SFG, or any other party, on its merits at that time with regard to maximising value for the

Group’s shareholders.

Strategic Position

The Group has in place an extended distribution network of accountancy firms across Australia and New

Zealand and one specialist financial planning firm. It is the largest service provider in Australasia to

Emerging Enterprises (SME’s) and high net worth sectors with more than 200,000 clients serviced by

approximately 2,800 staff across a network of 110 offices.

Over the past two years the Group has implemented the results of a strategic review. The benefits of the

move to an aligned leadership group, common remuneration model, business efficiency program and

Group shared services environment are part of the commitment made to improve operational efficiencies

and better align the organisation to drive organic growth.

As previously reported the Group has also undertaken a review of its brand strategy with particular

emphasis on establishing one brand identity. Recently all group offices, other than the Prescott Securities

offices, have undertaken a rebrand to Crowe Horwath effective from 31 July 2013. Three of the Group’s

capital city businesses have been trading under the Crowe Horwath brand since May 2007 when the

Group became an affiliate member of Crowe Horwath International. Crowe Horwath International is

ranked among the top 10 global accounting networks and consists of more than 150 independent

accounting and advisory services firms in over 100 countries worldwide.

For

per

sona

l use

onl

y

CHAIRMAN’S REPORT

4 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Strategic Position (continued)

Consistent with the one brand identity, the Company changed its name to Crowe Horwath Australasia

Ltd on 31 July 2013 following shareholder approval granted at the last Annual General Meeting. The

Company’s new ASX code is CRH.

Outlook

Given the broad outlook for a slow economy in FY14 the Group expects business confidence in the SME

market to remain low and trading conditions challenging. The initiatives completed during the FY13 year

to drive more efficient operations will be essential in a period of continued subdued business activity.

The Group’s sound balance sheet and quality businesses with enduring trusted client relationships will

assist the Group in delivering value to its clients and shareholders in future periods.

The Directors advise that, like FY13, they intend to remain focused on organic revenue growth, cost

control, tightly managing cash flow from operations and margin improvement across both Business

Services and Financial Services operations. In FY14 the Group will focus on leveraging the size of its

network to better generate growth opportunities, expand the use of cloud based technologies to improve

service efficiencies and leverage its common Crowe Horwath brand.

Similarly, there is further scope for improvement in Financial Services as the Federal Government’s

Future of Financial Advice (FoFA) reforms are demanding that the industry move to a “fee for service”

model. The Group has fully adopted a culture of “fee for service” in the Financial Services division and

welcomes the changes to improve the overall professionalism in the industry.

Acknowledgement

I thank all employees and shareholders of the Group for their support during these challenging times and

look forward to pursuing the Group’s strategic objectives over the coming year.

Richard Grellman

Chairman

20 August 2013

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

5 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Performance Overview

The Directors believe the overall performance of Crowe Horwath Australasia Ltd and its controlled

entities (Crowe Horwath or the Group) during the 2012/13 year was reflective of the low growth

business environment being experienced by professional services firms in both Australia and New

Zealand. The challenging trading conditions in both its Australian and New Zealand markets have led to

a decline in profit during the year.

Operating revenue decreased by 2% to $405.9 million primarily due to a 3% decline in Business Services

revenue. The weak conditions and confidence in the Group’s target SME market led to a reduction in

discretionary advisory services to clients and associated Business Services revenue. In addition the

Group is repositioning its businesses in the important Sydney and Melbourne markets. These businesses

have undergone significant change during the year with a number of principals exiting the businesses and

a similar number of high calibre individuals being recruited or promoted. It is anticipated that these new

principals will bring new revenue opportunities to the Group progressively over the coming periods as

they build their relationships and client portfolios.

Pleasingly, Financial Services revenue increased by 3%, partly offsetting the reduction in Business

Services revenue. The growth in Financial Services revenue was achieved across a range of services

including Financial Planning, Risk Insurance, General Insurance and Finance Broking in an environment

where economic conditions remain uncertain.

During the year, the Group undertook a business efficiency project to ensure that costs remained tightly

managed in response to the harsh economic conditions. It also implemented the major change programs

introduced in the previous financial year which included the introduction of a Group shared services

environment. These programs and projects should provide on-going financial benefits for the Group.

Cash flow was reduced due to lower business advisory revenue, the costs of the business efficiency

program undertaken during the year and payments made for the one-off costs of the prior year

transformation projects.

Net debt increased to $52.6 million (2012: $40.9 million) during the year. Gearing (net debt/equity) at

year end increased from 15% to 20%, which is still considered conservative by the Directors. During the

year, the Group extended the term of its bank facilities to 31 July 2016. The Group has maintained a

sound balance sheet position with significant unused banking facilities.

Full Year Profit Summary

Net Profit

Group performance for the financial year ended 30 June 2013 is summarised below:

Operating revenue fell by 2% to $405.9 million (2012: $413.4 million).

Normalised EBITA fell by 28% to $26.5 million (2012: $36.6 million) due primarily to lower

business advisory revenue.

Net Profit After Tax fell 31% to $7.0 million (2012: $10.2 million)

2009 2010 2011 2012 2013

421.2

413.0

406.1

413.4

405.9

$ m

illi

on

Operating Revenue

2009 2010 2011 2012 2013

47.0 46.1 40.9

36.6

26.5

$ m

illi

on

Normalised EBITA

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

6 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Full Year Profit Summary (continued)

2012/13

2011/12

Increase /

(Decrease)

($m) ($m)

Operating Revenue 405.9 413.4 (2)%

Normalised EBITA (a) 26.5 36.6 (28)%

less Non-recurring Costs (net of tax) (5.1) (9.0) (43)%

less Interest Expense (4.8) (5.0) (4)%

less Tax (6.9) (9.8) (30)%

Cash Earnings 9.7 12.8 (24)%

less Amortisation of Intangible Assets (2.7) (2.6) 4%

Net Profit 7.0 10.2 (31)%

Note: (a) Normalised EBITA = Net Profit before interest, tax, amortisation of intangible assets and

non-recurring items.

Final and Full Year Dividend

The Directors have declared a final dividend of 2.0 cents per share, fully franked at a 30% tax rate (2012:

4.0 cents per share). This brings the full year dividend rate to 5.0 cents per share (2012: 7.0 cents per

share).

The Directors have determined the full year dividend rate of 5.0 cents per share having regard to the

standing policy of a full year dividend payout rate at or above 70% of cash earnings per share and their

commitment to shareholders to a higher payout rate as considered appropriate based on the Group’s

financial performance and market and economic conditions.

The final dividend of 2.0 cents per share is payable on 4 November 2013, with the record date for

determining entitlements to the final dividend being 4 October 2013.

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

7 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

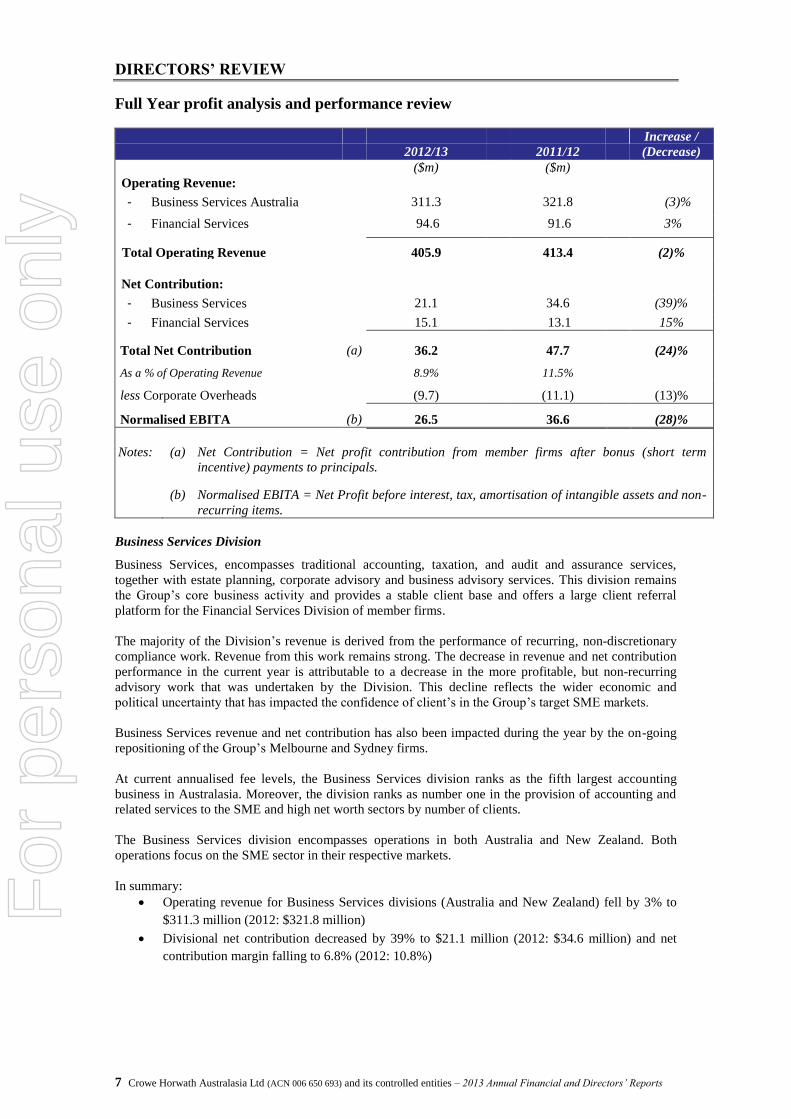

Full Year profit analysis and performance review

2012/13

2011/12

Increase /

(Decrease)

($m) ($m)

Operating Revenue:

- Business Services Australia 311.3 321.8 (3)%

- Financial Services 94.6 91.6 3%

Total Operating Revenue 405.9 413.4 (2)%

Net Contribution:

- Business Services 21.1 34.6 (39)%

- Financial Services 15.1 13.1 15%

Total Net Contribution (a) 36.2 47.7 (24)%

As a % of Operating Revenue 8.9% 11.5%

less Corporate Overheads (9.7) (11.1) (13)%

Normalised EBITA (b) 26.5 36.6 (28)%

Notes: (a) Net Contribution = Net profit contribution from member firms after bonus (short term

incentive) payments to principals.

(b) Normalised EBITA = Net Profit before interest, tax, amortisation of intangible assets and non-

recurring items.

Business Services Division

Business Services, encompasses traditional accounting, taxation, and audit and assurance services,

together with estate planning, corporate advisory and business advisory services. This division remains

the Group’s core business activity and provides a stable client base and offers a large client referral

platform for the Financial Services Division of member firms.

The majority of the Division’s revenue is derived from the performance of recurring, non-discretionary

compliance work. Revenue from this work remains strong. The decrease in revenue and net contribution

performance in the current year is attributable to a decrease in the more profitable, but non-recurring

advisory work that was undertaken by the Division. This decline reflects the wider economic and

political uncertainty that has impacted the confidence of client’s in the Group’s target SME markets.

Business Services revenue and net contribution has also been impacted during the year by the on-going

repositioning of the Group’s Melbourne and Sydney firms.

At current annualised fee levels, the Business Services division ranks as the fifth largest accounting

business in Australasia. Moreover, the division ranks as number one in the provision of accounting and

related services to the SME and high net worth sectors by number of clients.

The Business Services division encompasses operations in both Australia and New Zealand. Both

operations focus on the SME sector in their respective markets.

In summary:

Operating revenue for Business Services divisions (Australia and New Zealand) fell by 3% to

$311.3 million (2012: $321.8 million)

Divisional net contribution decreased by 39% to $21.1 million (2012: $34.6 million) and net

contribution margin falling to 6.8% (2012: 10.8%)

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

8 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Full Year profit analysis and performance review (continued)

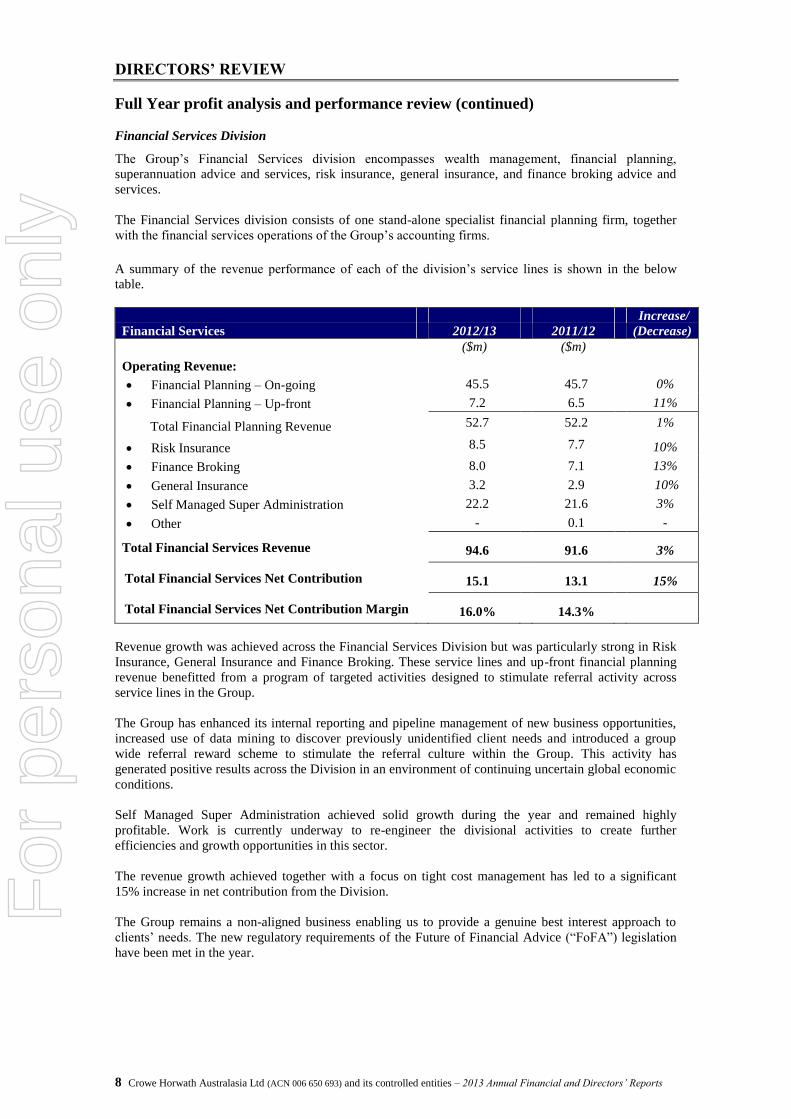

Financial Services Division

The Group’s Financial Services division encompasses wealth management, financial planning,

superannuation advice and services, risk insurance, general insurance, and finance broking advice and

services.

The Financial Services division consists of one stand-alone specialist financial planning firm, together

with the financial services operations of the Group’s accounting firms.

A summary of the revenue performance of each of the division’s service lines is shown in the below

table.

Financial Services

2012/13

2011/12

Increase/

(Decrease)

($m) ($m)

Operating Revenue:

Financial Planning – On-going 45.5 45.7 0%

Financial Planning – Up-front 7.2 6.5 11%

Total Financial Planning Revenue 52.7 52.2 1%

Risk Insurance 8.5 7.7 10%

Finance Broking 8.0 7.1 13%

General Insurance 3.2 2.9 10%

Self Managed Super Administration 22.2 21.6 3%

Other - 0.1 -

Total Financial Services Revenue 94.6 91.6 3%

Total Financial Services Net Contribution 15.1 13.1 15%

Total Financial Services Net Contribution Margin 16.0% 14.3%

Revenue growth was achieved across the Financial Services Division but was particularly strong in Risk

Insurance, General Insurance and Finance Broking. These service lines and up-front financial planning

revenue benefitted from a program of targeted activities designed to stimulate referral activity across

service lines in the Group.

The Group has enhanced its internal reporting and pipeline management of new business opportunities,

increased use of data mining to discover previously unidentified client needs and introduced a group

wide referral reward scheme to stimulate the referral culture within the Group. This activity has

generated positive results across the Division in an environment of continuing uncertain global economic

conditions.

Self Managed Super Administration achieved solid growth during the year and remained highly

profitable. Work is currently underway to re-engineer the divisional activities to create further

efficiencies and growth opportunities in this sector.

The revenue growth achieved together with a focus on tight cost management has led to a significant

15% increase in net contribution from the Division.

The Group remains a non-aligned business enabling us to provide a genuine best interest approach to

clients’ needs. The new regulatory requirements of the Future of Financial Advice (“FoFA”) legislation

have been met in the year.

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

9 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

New business acquisitions

The Group continued to keep acquisition activity subdued during the year with a preference and focus on

organic growth and completing its major change programs and business efficiency project, given its

already well established distribution network across Australia and New Zealand.

Whilst the Group is well placed to pursue high quality, strategic acquisition opportunities, growth by

acquisition remains a low priority at present given the continued focus on organic growth and business

improvement.

Operating cash flow

Operating cash flow at $10.7 million (2012: $20.7 million) was impacted by significant non-recurring

costs in the completion of the business efficiency program completed during the year in addition to the

costs associated with assessing a significant merger opportunity that arose during the year.

Cash Flow from Operations

2012/13

2011/12

Increase/

(Decrease)

($m) ($m) ($m)

Normalised EBITA (a) 26.5 36.6 (10.1)

less Non-recurring/ project Costs (7.2) (12.9) 5.7

add back Depreciation 5.7 8.6 (2.9)

EBITDA 25.0 32.3 (7.3)

Less/ add Working Capital Movement (7.1) 0.2 (7.3)

less Interest (4.2) (4.5) 0.3

less Tax Paid (3.0) (7.3) 4.3

Cash Flow from Operations 10.7 20.7 (10.0)

Note: (a) Normalised EBITA = Net profit before interest, tax, amortisation of intangible assets and

non-recurring items.

Working capital levels continued to be contained during the year by tight management and control of

lock-up (debtors plus work in progress), with average lock-up over the period being maintained at 97

days (2012: 98 days), which was a good result given the tough business conditions. Lock-up closed at 78

days (2012: 78 days).

However, working capital was impacted by the movement of other liabilities including the payment of

employee liabilities to employees as a result of the business efficiency program run in the current year,

the payment of accrued project liabilities from the functional support review project and lower staff

bonuses accrued in the current year.

Dividend payments in the year were maintained at $15.6 million, inclusive of the cash benefit of $2.9

million attributable to the Company’s Dividend Reinvestment Plan (2012: $18.5 million).

Crowe Horwath’s gearing (net debt/equity) rose moderately to 20% (2012: 15%) and remains in the

middle of the Board approved gearing range. This relatively conservative gearing position is considered

appropriate to the current economic climate.

The Group’s balance sheet and financial position is supported by long term funding arrangements

providing available undrawn funds at 30 June 2013 of $43.1 million. During the year the Group extended

its banking facilities held with National Australia Bank. The Group has a non-amortising $75 million

banking facility and a $20 million amortising facility, both expiring on 31 July 2016. Repayments of

$2.5 million are required every 6 months, commencing 1 January 2014, on the amortising facility. The

bank also has a NZ$10 million facility with Bank of New Zealand subject to annual renewal on 31 July

each year.

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

10 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Review of Operations

Over the past two years Crowe Horwath Australasia has embarked on a program to be the number one

advisory business that provides business advice to small and mid size businesses, government and

strategic accounts and financial advice to high net worth individuals. To achieve this vision Crowe

Horwath has also identified the need to be known by its clients, staff, shareholders and competitors as a

values based organisation that not only acts as ONE, but also gains the benefits of operating as ONE.

In order to act as ONE we have identified the need to embed continuous improvement in the way we

operate our business; to foster and encourage a culture of entrepreneurialism and a sense of local

ownership; and to ensure our client relationships are responsive and intimate, with our advice being

provided in real time.

Over the last two years we have also taken the opportunity to clearly state that our primary audience for

business services is small to mid sized business, strategic accounts and government enterprises and for

financial services high net worth individuals who seek to prosper. We remain committed to talking to

these clients in the capital cities of Australia and New Zealand as well as the large regional centres of

both countries. When we talk to them we will continue our focus on maintaining our Number ONE

position in the ‘S’ of SME and expanding our share of the ‘M’ in the SME market. We also remain

steadfast in our commitment to the smaller regional centres of Australia and New Zealand where we

remain the best equipped to deliver services to businesses and individuals of all sizes. Many larger

organisations (strategic accounts) also recognise the value of our extensive geographical coverage and

we see great opportunity emerging with these businesses now and in the future.

Business Strategies

In order for the group to achieve the vision of the number One advisory company in Australia and New

Zealand there are a number of foundations that we have put in place over the past two years.

We are ONEWe value… Ownership Courage Unity

We strengthen these values with behaviour thatillustrates…

Discipline & focus

Excellence in execution

Taking responsibility

Honesty

Acceptance

Trust

Innovation

Relationshipbuilding

Proactivesharing

Leveraging of expertise

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

11 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Business Strategies (continued)

Talented people in the right roles

One of the key measures of a successful business is the ability to attract and retain top talent. Each year

Crowe Horwath measures staff engagement across the company to determine areas of strength and

opportunities for improvement. Internally this survey is called the “A Great Place to Work” survey and

the results are provided by office location with measurable actions put in place for continuous

improvement.

With a large geographic footprint across Australia and New Zealand it is critical that we provide young

people right across both countries the opportunity to commence their working careers with Crowe

Horwath. Over the past year we recruited over 120 graduates into our organisation ensuring that we have

a regular supply of the best and brightest of emerging talent across Australia and New Zealand.

A number of key appointments were made during the year including a new leader (Yvette Pietsch) for

our Central West business, a new Chief Executive of our Melbourne firm (Dave Moores) and a new

leader for our Self Managed Superannuation business (Susie Salmon).

Following the successful implementation of our Group shared services environment and the restructuring

of our leadership team a business efficiency program was implemented to better leverage our

administrative staff across the company.

Client Centric Culture

Our client relationships are at the centre of everything we do at Crowe Horwath. We engage leading

research consultant, Beaton Consulting, with the resulting outcomes providing real insight as to client

and market expectations around service and capabilities which has in turn allowed us to remain focused

on the key elements important to our clients.

We believe it is important to operate in the same geographies of our clients. Our broad geographic

coverage results in trusted client relationships that in many cases are multi-generational. We will

continue to leverage the strength of these trusted relationships to add further value to our clients.

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

12 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Business Strategies (continued)

We are excited by the opportunities to leverage the deep understanding we already have of our clients,

and extend this into providing detailed insights into their financial performance and how they relate to

their industry peers. We plan to use the information and tools at our disposal to develop an intimate

knowledge of our clients, provide perspective and clarity on their performance, and work with them to

ensure they are the leaders in their industries. With the strength of our position in the SME market we

intend on becoming an important source of high quality benchmarking data for our clients, and a

recognised leader in advisory services into their industries.

Operational Excellence

We continued the focus and use of a common Sales Pipeline Management system during the year in

order to track and monitor sales leads and opportunities. This is a key foundation process in the creation

of a business development and sales oriented high performance culture.

Our clients continue to value the responsiveness of our teams and our ability to ensure work is performed

in a timely manner. To ensure we continue to strengthen this area we are introducing the practice across

all offices of daily activity meetings to ensure all staff are responsible for achieving daily activity targets.

The Group shared services environment provides us with the ability to rationalise our cost base providing

a platform for future growth. The essence of this project has been to rationalise the number of non-client

facing staff in our client facing businesses by significantly centralising our HR, finance and IT functions

in to a Group function – therefore giving us scale for the future.

Our risk management program continues to focus on ensuring our strategic goals are met with emphasis

on continuing to encourage our staff and executives to develop new service offerings for our clients

within our risk appetite. To support this, corporate governance is structured to enhance our risk

management program into the business at all levels, with awareness driving education, ongoing training

and cooperation of all staff.

Crowe Horwath remains fully supportive of the FoFA reforms with a focus on providing advice on a fee

for service basis with no product or platform commissions. We also believe we are well placed to

leverage off our business services culture to develop and participate in the emerging scalable advice

market with a focus on tax effective advice. With competitor consolidation occurring in the product

provider space we believe our clear competitive advantage of non-aligned advice will hold us in good

stead under the ‘client best interest’ test.

Future Prospects

With our vision and strategy clear Crowe Horwath is well placed to focus on driving organic growth

though a number of key objectives in the coming years:

Advisory

Crowe Horwath will continue to look at new ways of offering advisory services to our clients.

We want to continue to build on our already strong position as a leading provider of cloud accounting

solutions to our clients. We are a recognised leader in adopting cloud accounting technologies and

incorporating them into a total advisory services offering, and have experienced very positive momentum

over the past twelve months, both with our existing client base as well as attracting new clients. Our

cloud accounting offerings provide us with the opportunity to have more frequent and higher value-

adding interactions with our clients, and extend our advisory capabilities into providing ‘virtual’ services

to them.

A continued emphasis on staff training will occur over the coming year to ensure all staff are aware of

the capability that exists across our Group.

For

per

sona

l use

onl

y

DIRECTORS’ REVIEW

13 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Future Prospects (continued)

Financial Services and SMSF

A key focus area in Financial Services for next year is to improve the consistency of our client offerings

in the Financial Planning and SMSF Administration areas. Presently, there is some variation that exists

across different locations. The migration to a single business model based on consistency, adaptability

and repeatability will ensure improved service and interactions with our clients, better pricing delivery,

greater opportunities for new business and reduced risk.

Improving the referral culture across the Group is another strategic priority within Financial

Services. Over the last twelve months, some important steps have been taken, including the introduction

of a new Group-wide referral incentive scheme and increased focus on data-mining our client base to

identify specific opportunities. Our plan for this year is to build on the improvements made – the

incentive scheme will continue while the emphasis on data mining will increase. Additionally, we will

be making changes to improve the process to record, capture and report the referrals made. Teamwork

and trust are critical elements of a referral culture and the operating framework is in place to ensure these

attributes exist in each location.

One Brand

The move to a common brand across all of our integrated accounting and financial planning offices will

ensure we maximize our marketing spend, ensure better leverage of resources, support stronger inbound

referrals from the global Crowe Horwath network and create stronger opportunities for staff exchange

resulting in an ability to better attract and retain staff. The Group is an affiliate member of Crowe

Horwath International which is the ninth largest international network of independent accounting and

advisory services firms. Crowe Horwath International has a strong and growing presence in Asia which

we expect to benefit the Group in the medium term.

Organic Growth

The key to growing the business organically is ensuring all staff have the skills, service offerings and the

time to engage in meaningful discussions with our clients.

A comprehensive training program is being deployed across all offices to ensure staff have the skills

required to have these meaningful discussions with clients. This is supported by access to the best

capability across the company. All staff now have access to specialist capability across the group to

ensure the right advice is given at the right time. The introduction of a Group shared services

environment and the adoption of cloud accounting for our clients will result in staff spending less time

on administration and more time with clients.

Crowe Horwath will continue to look at additional service offerings that enhance our existing portfolio in

the areas of both business and financial advisory.

Outlook

The Directors reaffirm the outlook for the Group as disclosed in the Chairman’s Report.

Richard Grellman John Lombard

Chairman Managing Director

20 August 2013

For

per

sona

l use

onl

y

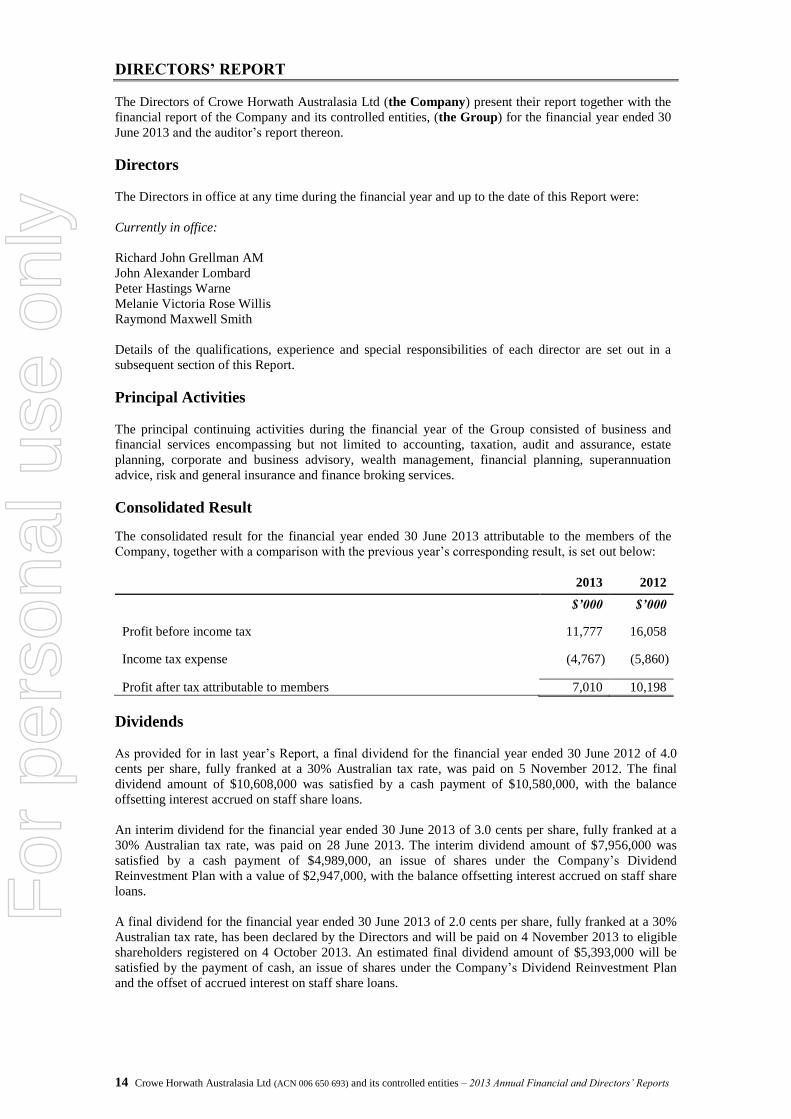

DIRECTORS’ REPORT

14 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

The Directors of Crowe Horwath Australasia Ltd (the Company) present their report together with the

financial report of the Company and its controlled entities, (the Group) for the financial year ended 30

June 2013 and the auditor’s report thereon.

Directors

The Directors in office at any time during the financial year and up to the date of this Report were:

Currently in office:

Richard John Grellman AM

John Alexander Lombard

Peter Hastings Warne

Melanie Victoria Rose Willis

Raymond Maxwell Smith

Details of the qualifications, experience and special responsibilities of each director are set out in a

subsequent section of this Report.

Principal Activities

The principal continuing activities during the financial year of the Group consisted of business and

financial services encompassing but not limited to accounting, taxation, audit and assurance, estate

planning, corporate and business advisory, wealth management, financial planning, superannuation

advice, risk and general insurance and finance broking services.

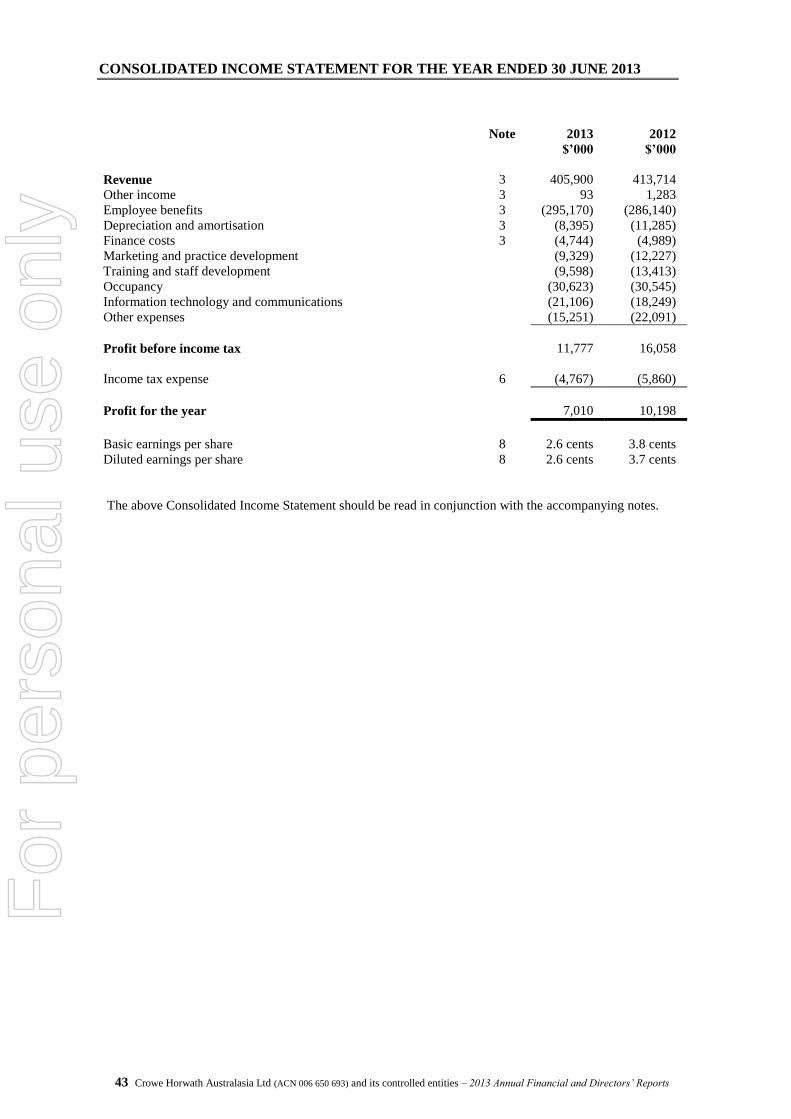

Consolidated Result

The consolidated result for the financial year ended 30 June 2013 attributable to the members of the

Company, together with a comparison with the previous year’s corresponding result, is set out below:

2013 2012

$’000 $’000

Profit before income tax 11,777 16,058

Income tax expense (4,767) (5,860)

Profit after tax attributable to members 7,010 10,198

Dividends

As provided for in last year’s Report, a final dividend for the financial year ended 30 June 2012 of 4.0

cents per share, fully franked at a 30% Australian tax rate, was paid on 5 November 2012. The final

dividend amount of $10,608,000 was satisfied by a cash payment of $10,580,000, with the balance

offsetting interest accrued on staff share loans.

An interim dividend for the financial year ended 30 June 2013 of 3.0 cents per share, fully franked at a

30% Australian tax rate, was paid on 28 June 2013. The interim dividend amount of $7,956,000 was

satisfied by a cash payment of $4,989,000, an issue of shares under the Company’s Dividend

Reinvestment Plan with a value of $2,947,000, with the balance offsetting interest accrued on staff share

loans.

A final dividend for the financial year ended 30 June 2013 of 2.0 cents per share, fully franked at a 30%

Australian tax rate, has been declared by the Directors and will be paid on 4 November 2013 to eligible

shareholders registered on 4 October 2013. An estimated final dividend amount of $5,393,000 will be

satisfied by the payment of cash, an issue of shares under the Company’s Dividend Reinvestment Plan

and the offset of accrued interest on staff share loans.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

15 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

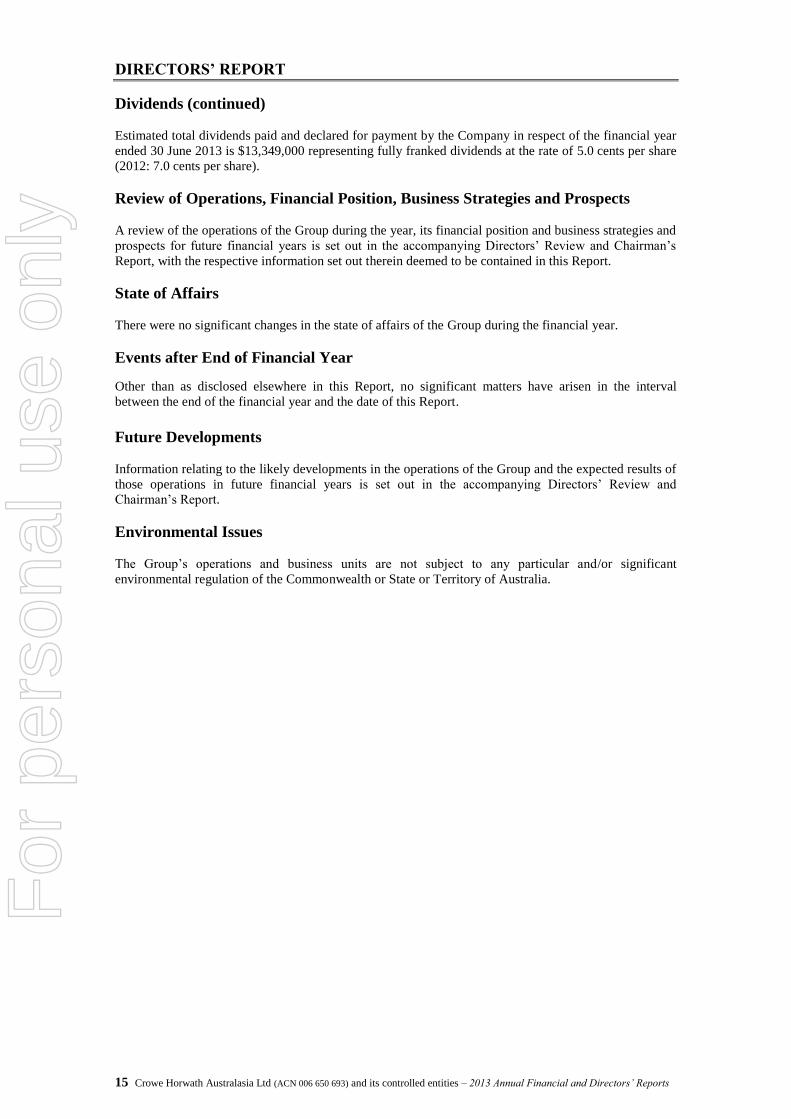

Dividends (continued)

Estimated total dividends paid and declared for payment by the Company in respect of the financial year

ended 30 June 2013 is $13,349,000 representing fully franked dividends at the rate of 5.0 cents per share

(2012: 7.0 cents per share).

Review of Operations, Financial Position, Business Strategies and Prospects

A review of the operations of the Group during the year, its financial position and business strategies and

prospects for future financial years is set out in the accompanying Directors’ Review and Chairman’s

Report, with the respective information set out therein deemed to be contained in this Report.

State of Affairs

There were no significant changes in the state of affairs of the Group during the financial year.

Events after End of Financial Year

Other than as disclosed elsewhere in this Report, no significant matters have arisen in the interval

between the end of the financial year and the date of this Report.

Future Developments

Information relating to the likely developments in the operations of the Group and the expected results of

those operations in future financial years is set out in the accompanying Directors’ Review and

Chairman’s Report.

Environmental Issues

The Group’s operations and business units are not subject to any particular and/or significant

environmental regulation of the Commonwealth or State or Territory of Australia.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

16 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Information on Directors

Particulars concerning the Directors, their qualifications, experience and special responsibilities as at the

date of this Report are set out below:

Directors in office at the date of this Report:

Richard John Grellman AM: FCA

Chairman and Independent, Non-Executive Director

Age 63

Appointed 15 March 2011

Experience: Mr Grellman has a wealth of accounting and finance expertise with over 32 years of

experience in the accounting profession. The majority of this time was spent in the Corporate Recovery

Division of KPMG, with the last 10 years more specifically focussed on the provision of strategic advice

and services to the financial services sector.

He was a partner of KPMG from 1982 to 2000 and a member of KPMG's national board from 1995 to

1997 and its executive from 1997 to 2000.

Mr Grellman was appointed a member of the Order of Australia in 2007 for services to the community,

particularly through leadership roles with Mission Australia and fundraising with Variety, The

Childrens Charity, and to the finance and insurance sectors.

Mr Grellman is Chairman of Genworth Financial Mortgage Insurance Holdings Pty Limited and related

entities and Bible Society Australia, and a director of Bisalloy Steel Group Ltd (since 26 February 2003).

Former listed entity directorships in the last 3 years: Director of AMP Limited (22 March 2000 to 12

May 2011) and of Centennial Coal Company Limited (21 February 2008 to 22 September 2010).

Peter Hastings Warne: BA, FAICD

Deputy Chairman and Independent, Non-Executive Director

Age 57

Director since May 2007

Audit and Risk Committee member

Nominations and Remuneration Committee member (Chairman)

Experience: Mr Warne has a broad range of skills, knowledge and experience following a long and

successful career in the financial services industry. He worked with Bankers Trust Australia Limited for

19 years, holding senior positions in the Fixed Interest and Capital Markets divisions, and was head of

the Financial Markets Group for 11 years. He has also provided product and industry advice on a

consultancy basis to a number of leading companies and government bodies.

Mr Warne is a director of Securities Exchanges Guarantee Corporation Limited, Securities Industry

Research Centre of Asia-Pacific (SIRCA) Limited and New South Wales Treasury Corporation. He is

also on the advisory boards of the Australian Office of Financial Management and Macquarie University

Faculty of Business and Economics.

Other listed entity directorships in the last 3 years: Chairman of ALE Property Management Limited

(since 8 September 2003) and a director of ASX Limited (since 25 July 2006), Macquarie Bank Limited

(since 1 July 2007) and Macquarie Group Limited (since 20 August 2007). He is also a director of former

listed entity, SFE Corporation Limited (since 11 September 2000).

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

17 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Information on Directors (continued)

Raymond Maxwell Smith: Dip Comm., FAICD, FCPA Independent, Non-Executive Director

Age 66

Director since May 2009

Audit and Risk Committee member (Chairman)

Nominations and Remuneration Committee member

Experience: Mr Smith was the Chief Financial Officer of Smorgon Steel Group Limited (SSGL) from

1996 to 2007. During that period he was at the forefront of the rationalisation of the Australian Steel

Industry, culminating in the 2007 merger of SSGL and OneSteel Limited.

Mr Smith has a wealth of corporate and financial experience, including in the areas of strategy,

acquisitions and disposals, and treasury and fund raising. Mr Smith is a Trustee of the Melbourne &

Olympic Parks Trust.

Other listed entity directorships in the last 3 years: K&S Corporation Limited (since 15 February 2008),

Transpacific Industries Group Ltd (since 1 April 2011) and Warrnambool Cheese and Butter Factory

Company Holdings Limited (since 31 May 2013). Former director of Willmott Forests Limited (28

August 2008 to 15 March 2011).

Melanie Victoria Rose Willis: B Ec, MTax, ASIA, FAICD

Independent, Non-Executive Director

Age 48

Director since February 2006

Audit and Risk Committee member

Nominations and Remuneration Committee member

Experience: Ms Willis has a broad range of skills in strategy, finance, turnarounds and operations as

Chief Executive Officer, NRMA Investments with NRMA Motoring & Services responsible for Thrifty

Australia and New Zealand, NRMA Travel, Holiday Parks, Travelodge and the Investment Portfolio.

Prior to NRMA she had a successful 15 year career in investment banking. She was a director at

Deutsche Bank and prior to this worked at Bankers Trust and Westpac. In addition she has provided

strategic and financial advice on a consultancy basis to a number of listed companies.

Ms Willis is a director of numerous NRMA companies in her executive role with that organisation.

Previously she led a financial services start up Smart Rate Money Limited and has held non executive

director positions on Rhodium Asset Management Limited and Hydro Tasmania.

Former listed entity directorships in the last 3 years: Aevum Limited (2 August 2006 to 23 December

2010).

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

18 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Information on Directors (continued)

John Alexander Lombard: B App. Sci., Grad Dip App. Fin. & Invest., GAICD

Managing Director Age 46

Appointed 1 July 2011

Experience: Mr Lombard has over 20 years experience in the professional services industry and

understands the need to constantly transform these businesses to meet changing customer and industry

demands. He has extensive international experience and has lived and worked in Indonesia, Singapore

and Germany.

Mr Lombard joined the Company from SAP where he was a Senior Vice President and member of

SAP’s Global Senior Executive Team. He has held a number of senior roles at SAP including leading

professional services organisations across Australia, New Zealand and then the broader Asia Pacific

Japan region. Most recently, Mr Lombard was the Global Executive responsible for business

transformation, business analytics and IT transformation services at SAP based in Germany.

Prior to joining SAP, Mr Lombard was a Managing Director with KPMG Consulting (BearingPoint)

responsible for consulting services across a number of key accounts and industries including consumer

products, pharmaceuticals, financial services and government. Prior to his time with BearingPoint, he

was part of the Management Consulting practice at PricewaterhouseCoopers.

Company Secretary Information

Details of the qualifications and experience of the Company Secretary of the Company at the financial

year end:

Bruce Craig Paterson: B. Bus (Acc), Grad. Dip. CSP, FCPA, ACIS

Mr Paterson was appointed Company Secretary of the Company in June 2001, previously being Finance

Manager and Company Secretary of other listed and unlisted entities. He has over 25 years experience in

a range of areas including accounting, finance, resources, property and investment banking. Mr Paterson

is an associate member of Chartered Secretaries Australia and the Institute of Chartered Secretaries and

Administrators.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

19 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Remuneration Report (Audited)

This Remuneration Report outlines the director and executive remuneration arrangements of the Company and the

Group in accordance with the requirements of the Corporations Act 2001 and its Regulations. For the purpose of this

Report, key management personnel (KMP) of the Group are defined as those persons having authority and

responsibility for planning, directing and controlling the major activities of the Company and the Group, directly or

indirectly, including any director (whether executive or otherwise) of the Company.

For the purposes of this Report, the term ‘executive’ encompasses the Executive Director and other senior executives

of the Company who are key management personnel.

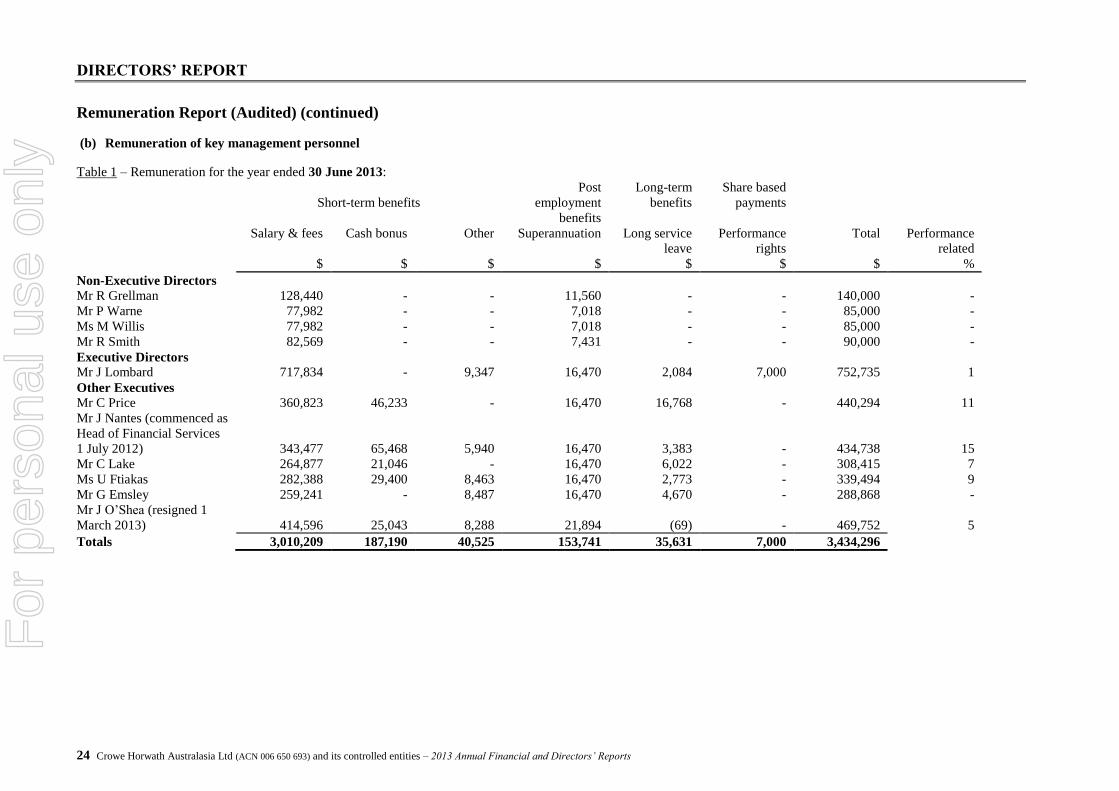

Details of key management personnel

i) Directors

Mr R Grellman AM Chairman – Non-Executive

Mr P Warne Deputy Chairman – Non-Executive

Mr R Smith Non-Executive

Ms M Willis Non-Executive

Mr J Lombard Managing Director – Executive

ii) Executives

Mr C Price Group Chief Financial Officer

Mr J Nantes Head of Financial Services (commenced in the role from 1 July 2012)

Mr C Lake Chief Risk Officer

Ms U Ftiakas Group General Manager, Human Resources

Mr G Emsley Group Chief Information Officer

Mr J O’Shea Group General Manager, Marketing and Communications (resigned 1

March 2013)

(a) Remuneration Policy

The Company’s remuneration policy has been designed to align director and executive objectives with business and

shareholder objectives by providing a fixed remuneration component and, where appropriate, offering specific short

and longer term incentives to executives based on key performance areas linked to performance, growth and financial

results. The Nominations and Remuneration Committee has previously reviewed the remuneration policy against a set

of best practice guiding principles which have been adopted. The Directors believe the remuneration policy to be

appropriate and effective in its ability to attract, retain and properly reward the best executives and directors to run and

manage the Company and the Group, as well as create goal congruence between directors, executives and

shareholders.

The Board’s policy for determining the nature and amount of remuneration for key management personnel is set out

below:

(i) Non-Executive Directors

The Company’s Nominations and Remuneration Committee is responsible for reviewing the adequacy and form of

remuneration of Non-Executive Directors of the Company. Directors’ fees are reviewed and determined annually,

within the aggregate amount approved by shareholders from time to time. Regard is given to the size and complexity

of the Group’s operations, contribution to the achievements of the Group and the responsibilities, risks and workload

requirements of individual Directors, including Board committee service. Appropriate external advice is sought as

required.

Because the focus of the Board is on the long term strategic direction of the Company and the Group, there is no link

between director remuneration and the short term results of the Company or the Group. Directors’ fees therefore

comprise only a fixed remuneration component.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

20 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Remuneration Report (Audited) (continued)

Details of annual fees currently payable to Non-Executive Directors of the Company are:

Board Chairman $140,000

Audit and Risk Committee Chairman $90,000

Other Non-Executive Directors $85,000

The aggregate amount of remuneration available to Non-Executive Directors, as approved by shareholders at the

annual general meeting held in November 2007, is $600,000 per annum.

The Company does not provide retirement payments to Non-Executive Directors other than amounts required in

accordance with its statutory superannuation requirements.

(ii) Executives

The Group aims to reward executives with a level and mix of remuneration commensurate with their position,

experience, responsibilities and performance. The Nominations and Remuneration Committee is responsible for

ensuring that executive remuneration is competitive with market standards and structured so as to align the interests of

executives with those of shareholders. External remuneration consultants are used on an as required basis to provided

assistance and independent advice on structuring and measurement of short term and long term incentive

arrangements. Remuneration consultants were not used in the current year in relation to key management personnel

remuneration arrangements. Executives are rewarded based on Group, business unit and individual performance

against targets referenced to appropriate benchmarks including achievement of budgets and other key performance

indicators (KPIs).

Executive remuneration consists of the following components:

Base remuneration; and

Performance based remuneration – this component comprises 2 elements:

- short term incentives (STI) in the form of cash bonuses; and

- long term incentives (LTI) in the form of performance rights for the Managing Director and up until 30 June

2013, deferred cash bonuses for the Group Chief Financial Officer and other executives as determined by the

Board. The Board is currently considering replacement LTI arrangements for executives.

Base Remuneration

Base remuneration is fixed and takes into account the scope of the role, level of skills and required experience.

Executives have the opportunity to receive this remuneration in a variety of approved forms including cash,

superannuation and fringe benefits such as motor vehicles and parking. It is intended that the manner of payment

chosen is optimal to each executive without creating undue cost for the Group.

Base remuneration is reviewed annually by the Nominations and Remuneration Committee having regard to Group,

business unit and individual performance. The Committee seeks internal and external advice when appropriate,

including recommendations by the Managing Director, other than with respect to his own position.

The base remuneration component of executives for the 2012/13 year is detailed in Table 1.

STI - Cash Bonuses

Cash bonuses are used to link the achievement of short term operational and Group targets, as identified by the

Directors and senior management, with the remuneration of executives charged with delivering or influencing those

targets. They are predetermined annually as a fixed percentage of base salary. In the 2012/13 year, the Managing

Director was entitled to receive up to 100% of base salary as a cash bonus whilst other executives could receive

between 15% - 25% dependent upon position.

Performance criteria and measures are specifically tailored to each executive’s circumstances and reviewed and

approved by the Nominations and Remuneration Committee. Budgets and prior year results are used to measure

financial performance, whilst non-financial KPIs are used to target other key identified areas.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

21 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Remuneration Report (Audited) (continued)

Performance criteria are predominantly weighted towards the financial performance of the Group, relative to other

targets. The range of weightings of performance measures across the major elements which apply to executives are as

follows:

- Financial 10% - 60%

- People 0% - 70%

- Process 0% - 70%

- Customer & market 0% - 50%

A summary of key components of the major elements of the performance criteria follows:

Financial

Revenue growth

Cash earnings per share growth

Net contribution (both dollars and margins)

Return on capital employed

People

Shift to advisory services

Reward and recognition process

Leadership development

A ‘great place to work’ and “One” initiatives

Process

Functional support (including transitional projects)

Capital and treasury management

Financial reporting and benchmarking

Adherence to / development of best Group practices

Continuous improvements including quality control and compliance

Customer & market

Organic growth

Cross selling and ‘Total Financial Solutions’

Client satisfaction and engagement

Marketing and brand development

The above performance criteria were chosen as they represent the key drivers for the short term success of the Group

as they relate to the relevant executives and their ability to influence outcomes. These criteria also provide a

framework for delivering longer term value for the Group as they are aligned with the underlying foundations of the

business being our people, our clients, our market and communities, and our shareholders.

Cash bonuses are determined on an individual basis having regard to achievement of a mix of specifically agreed

performance criteria.

For the Managing Director - cash bonus amounts can range from 0% to 50% of the available STI for achieving agreed

target performance levels, with the potential to receive up to 100% for meeting agreed stretch performance objectives.

As EBITA thresholds were not achieved for the 2012/13 financial year, no bonus was payable with respect to this

period.

For other executives – cash bonus amounts can range from 0% of the available STI when performance does not meet

expected threshold levels, to 100% for meeting target levels and up to 125% for achieving exceptional performance.

The Nominations and Remuneration Committee approves the basis and amount of executive cash bonuses prior to

payment. Externally audited financial information is used to assess financial KPI’s whilst discretionary components

are assessed or reviewed by the Nominations and Remuneration Committee during the approval process. This method

was chosen as it provides independence from management and enables Directors to evaluate executive performance

first hand. Cash bonuses are paid annually normally within three months of year end, once approved.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

22 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Remuneration Report (Audited) (continued)

Cash bonuses earned by executives with respect to the 2012/13 financial year are detailed in Table 1.

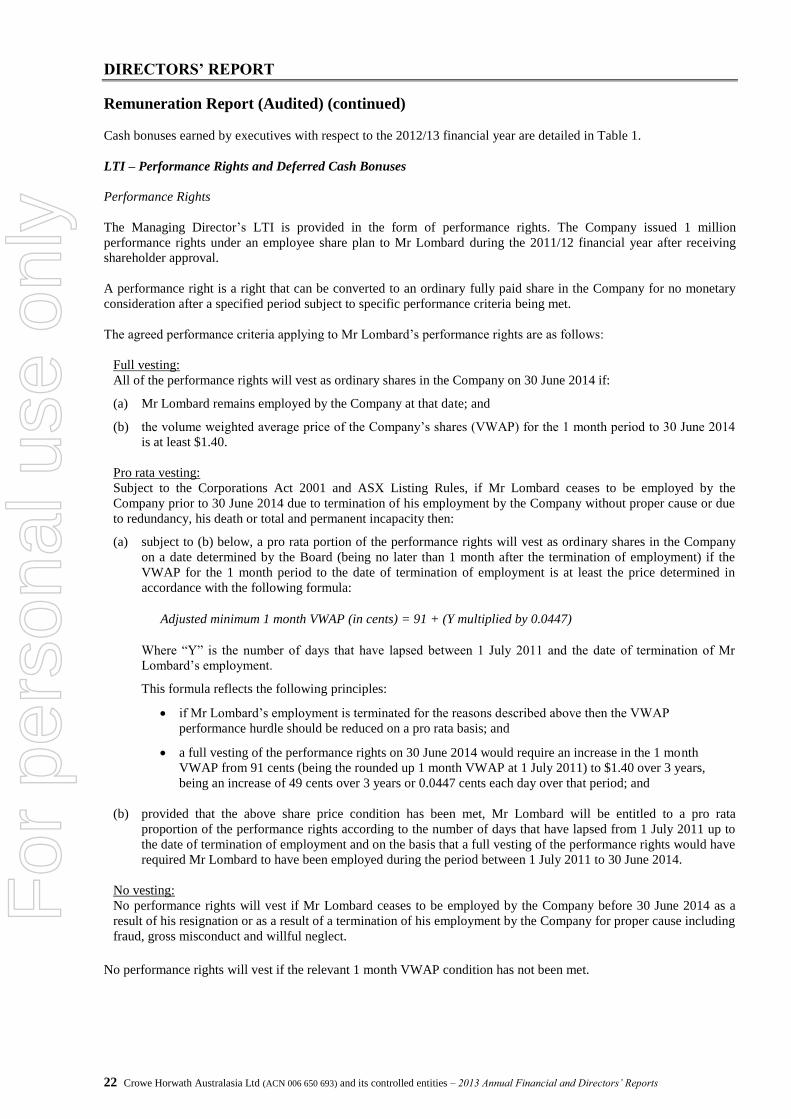

LTI – Performance Rights and Deferred Cash Bonuses

Performance Rights

The Managing Director’s LTI is provided in the form of performance rights. The Company issued 1 million

performance rights under an employee share plan to Mr Lombard during the 2011/12 financial year after receiving

shareholder approval.

A performance right is a right that can be converted to an ordinary fully paid share in the Company for no monetary

consideration after a specified period subject to specific performance criteria being met.

The agreed performance criteria applying to Mr Lombard’s performance rights are as follows:

Full vesting:

All of the performance rights will vest as ordinary shares in the Company on 30 June 2014 if:

(a) Mr Lombard remains employed by the Company at that date; and

(b) the volume weighted average price of the Company’s shares (VWAP) for the 1 month period to 30 June 2014

is at least $1.40.

Pro rata vesting:

Subject to the Corporations Act 2001 and ASX Listing Rules, if Mr Lombard ceases to be employed by the

Company prior to 30 June 2014 due to termination of his employment by the Company without proper cause or due

to redundancy, his death or total and permanent incapacity then:

(a) subject to (b) below, a pro rata portion of the performance rights will vest as ordinary shares in the Company

on a date determined by the Board (being no later than 1 month after the termination of employment) if the

VWAP for the 1 month period to the date of termination of employment is at least the price determined in

accordance with the following formula:

Adjusted minimum 1 month VWAP (in cents) = 91 + (Y multiplied by 0.0447)

Where “Y” is the number of days that have lapsed between 1 July 2011 and the date of termination of Mr

Lombard’s employment.

This formula reflects the following principles:

if Mr Lombard’s employment is terminated for the reasons described above then the VWAP

performance hurdle should be reduced on a pro rata basis; and

a full vesting of the performance rights on 30 June 2014 would require an increase in the 1 month

VWAP from 91 cents (being the rounded up 1 month VWAP at 1 July 2011) to $1.40 over 3 years,

being an increase of 49 cents over 3 years or 0.0447 cents each day over that period; and

(b) provided that the above share price condition has been met, Mr Lombard will be entitled to a pro rata

proportion of the performance rights according to the number of days that have lapsed from 1 July 2011 up to

the date of termination of employment and on the basis that a full vesting of the performance rights would have

required Mr Lombard to have been employed during the period between 1 July 2011 to 30 June 2014.

No vesting:

No performance rights will vest if Mr Lombard ceases to be employed by the Company before 30 June 2014 as a

result of his resignation or as a result of a termination of his employment by the Company for proper cause including

fraud, gross misconduct and willful neglect.

No performance rights will vest if the relevant 1 month VWAP condition has not been met.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

23 Crowe Horwath Australasia Ltd (ACN 006 650 693) and its controlled entities – 2013 Annual Financial and Directors’ Reports

Remuneration Report (Audited) (continued)

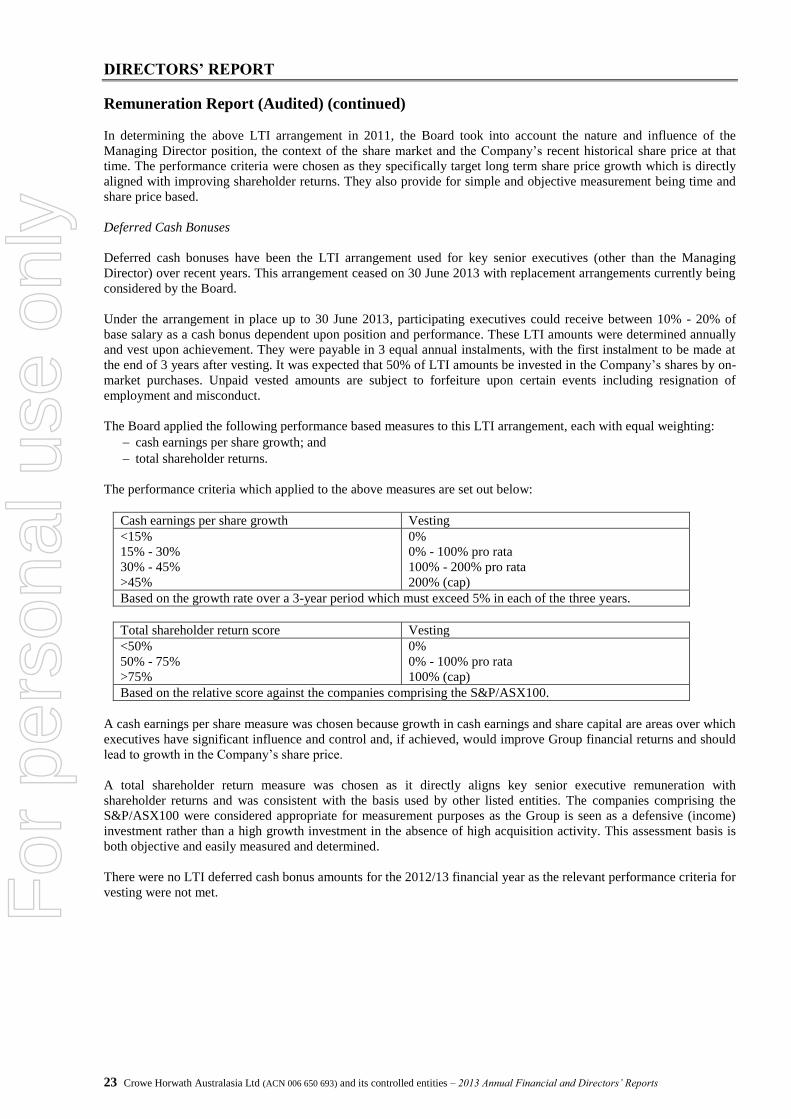

In determining the above LTI arrangement in 2011, the Board took into account the nature and influence of the

Managing Director position, the context of the share market and the Company’s recent historical share price at that

time. The performance criteria were chosen as they specifically target long term share price growth which is directly

aligned with improving shareholder returns. They also provide for simple and objective measurement being time and

share price based.

Deferred Cash Bonuses

Deferred cash bonuses have been the LTI arrangement used for key senior executives (other than the Managing

Director) over recent years. This arrangement ceased on 30 June 2013 with replacement arrangements currently being

considered by the Board.

Under the arrangement in place up to 30 June 2013, participating executives could receive between 10% - 20% of

base salary as a cash bonus dependent upon position and performance. These LTI amounts were determined annually

and vest upon achievement. They were payable in 3 equal annual instalments, with the first instalment to be made at

the end of 3 years after vesting. It was expected that 50% of LTI amounts be invested in the Company’s shares by on-

market purchases. Unpaid vested amounts are subject to forfeiture upon certain events including resignation of

employment and misconduct.

The Board applied the following performance based measures to this LTI arrangement, each with equal weighting:

cash earnings per share growth; and

total shareholder returns.

The performance criteria which applied to the above measures are set out below:

Cash earnings per share growth Vesting

<15%

15% - 30%

30% - 45%

>45%

0%

0% - 100% pro rata

100% - 200% pro rata

200% (cap)

Based on the growth rate over a 3-year period which must exceed 5% in each of the three years.

Total shareholder return score Vesting

<50%

50% - 75%

>75%

0%

0% - 100% pro rata

100% (cap)

Based on the relative score against the companies comprising the S&P/ASX100.