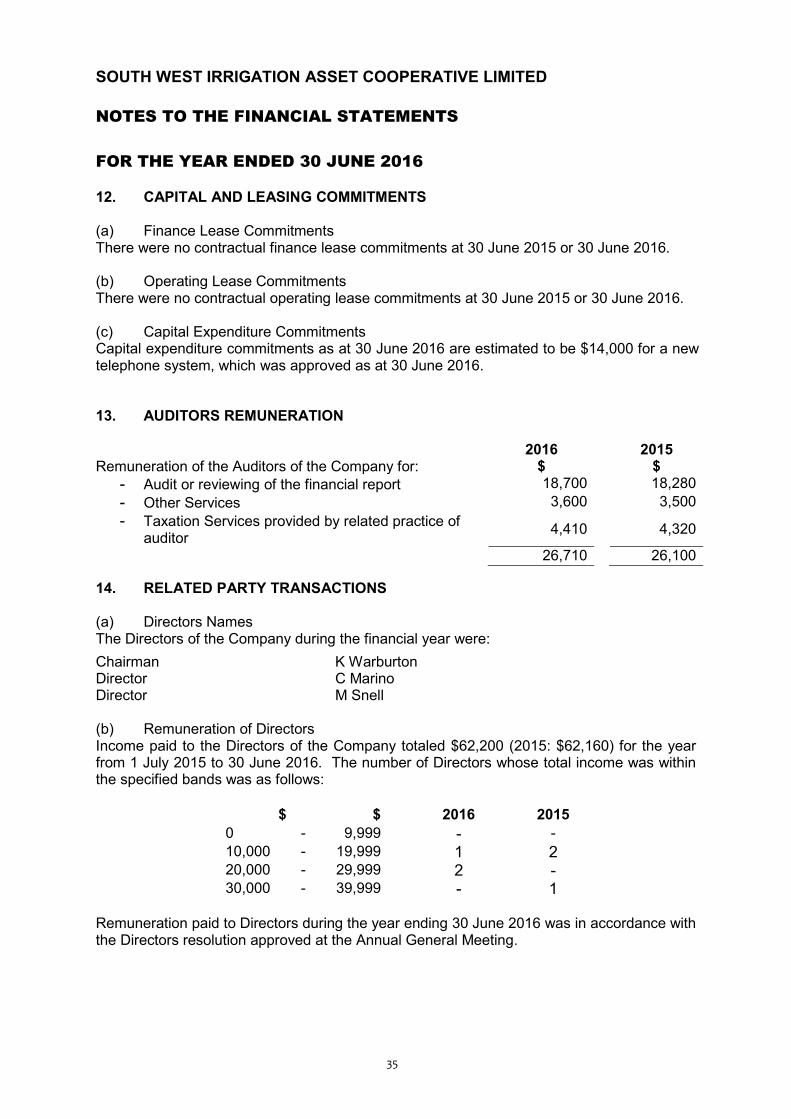

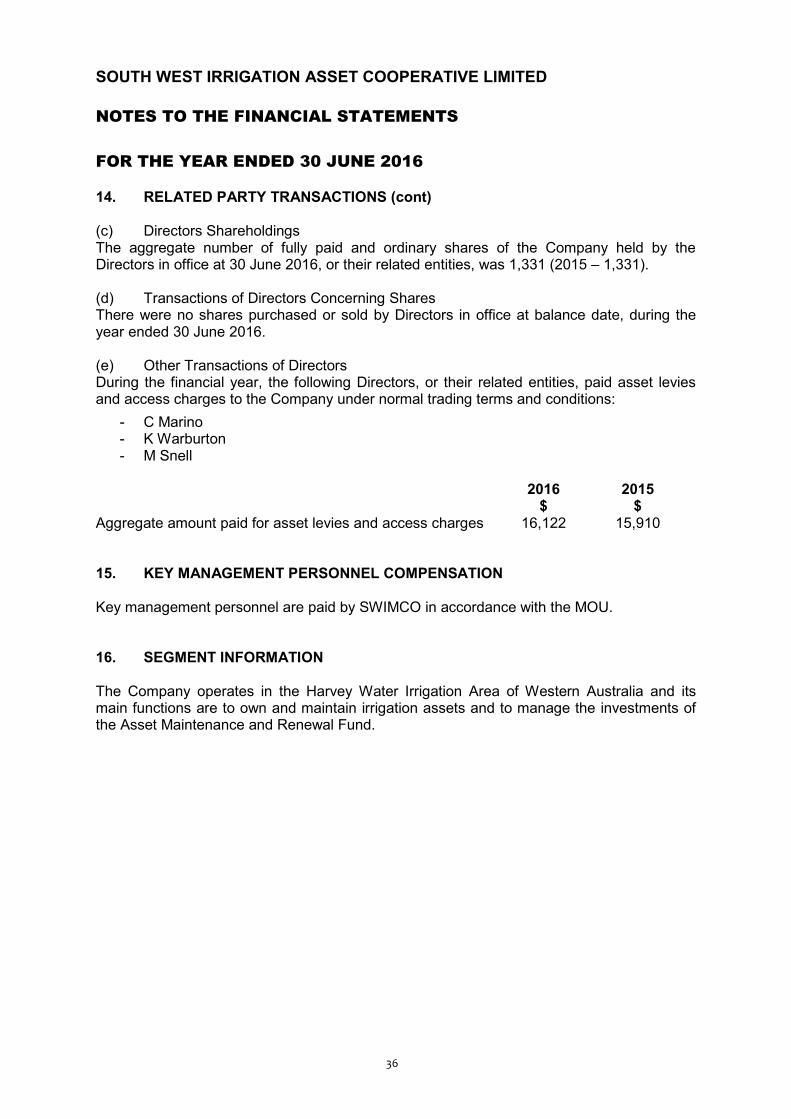

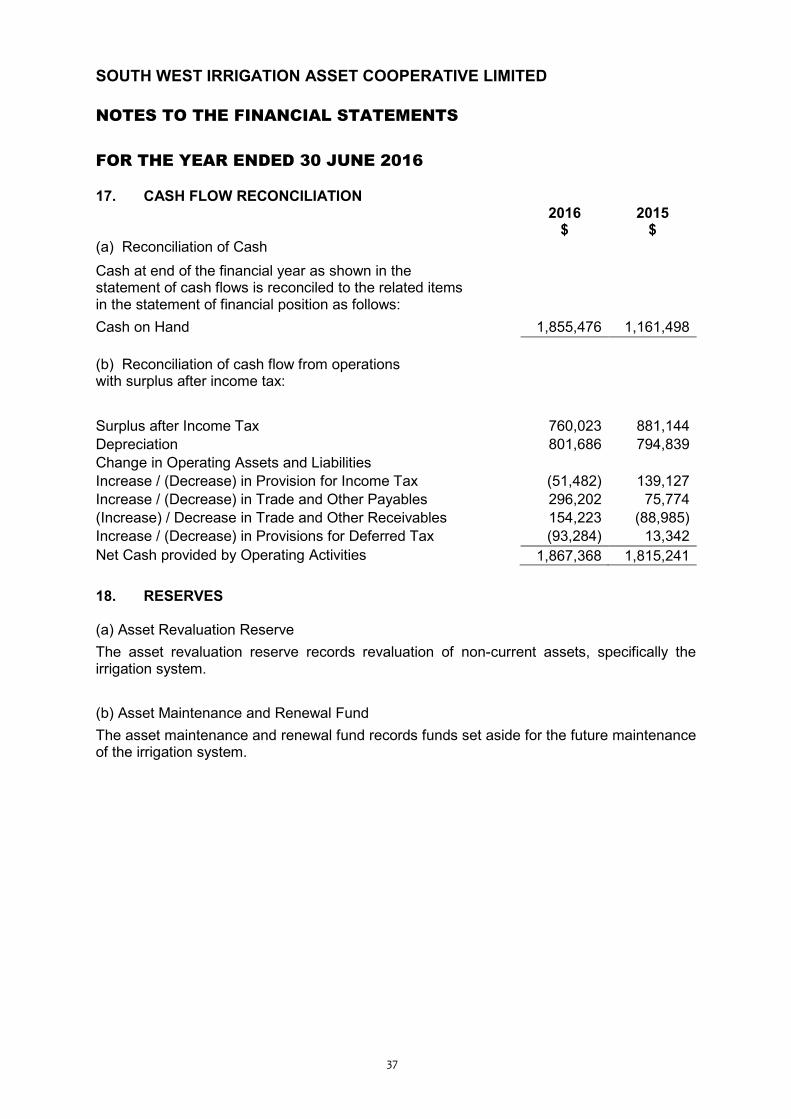

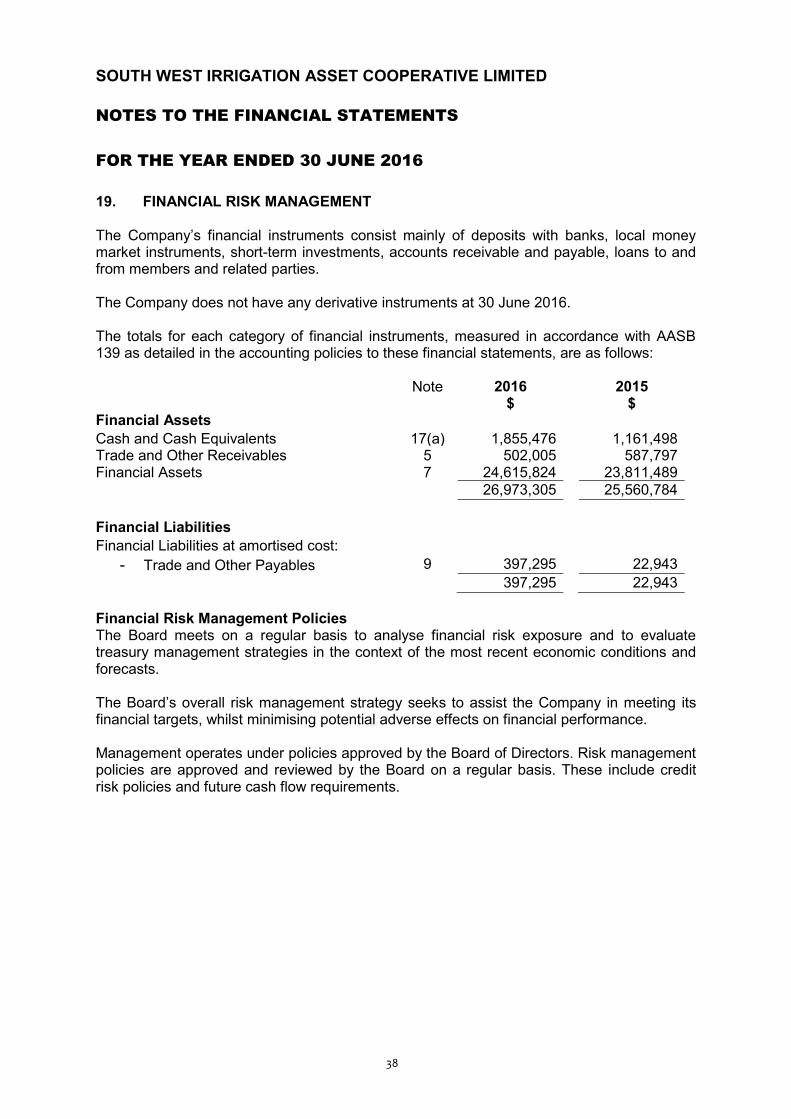

Embed Size (px)

Citation preview

SWIAC

SOUTH WEST IRRIGATION ASSET MANAGEMENT COOPERATIVE LIMITED

Annu

al R

epor

t

2016

This page has been left blank intentionally

Table of Contents

At a Glance ....................................................... 1

Chairman’s Report ........................................... 2

Board of Directors ........................................... 5

Company Secretary ......................................... 5

Corporate Governance .................................... 6

Directors’ Report ............................................. 9

Statutory Report of the Directors ................. 11

Certificate by the Directors ............................ 11

Financial Report .............................................. 12

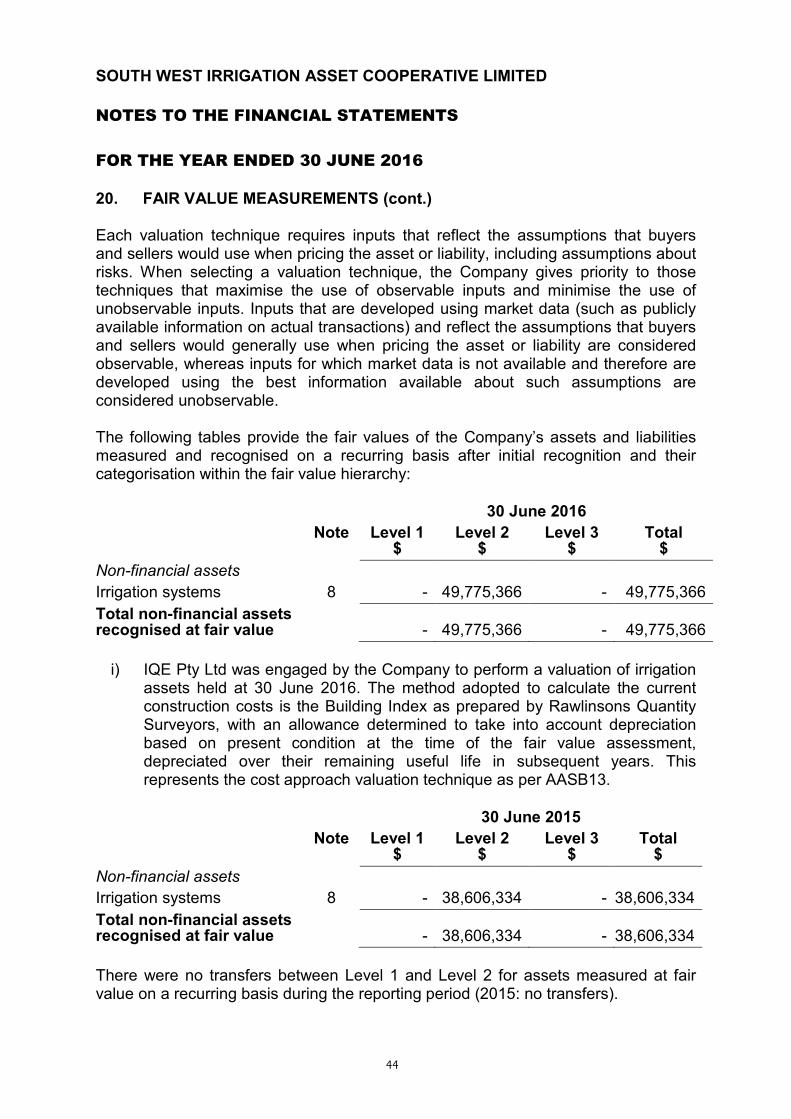

Audit Report .................................................. 46

Auditor’s Independence Declaration ........... 48

Table of Contents

At a Glance ....................................................... 1

Chairman’s Report ........................................... 2

Board of Directors ........................................... 4

Company Secretary ......................................... 4

Corporate Governance .................................... 5

Directors’ Report ............................................. 8

Statutory Report of the Directors ................ 10

Certificate by the Directors ........................... 10

Financial Report .............................................. 11

Audit Report .................................................. 44

Auditor's Independence Declaration ........... 46

SWIAC

1

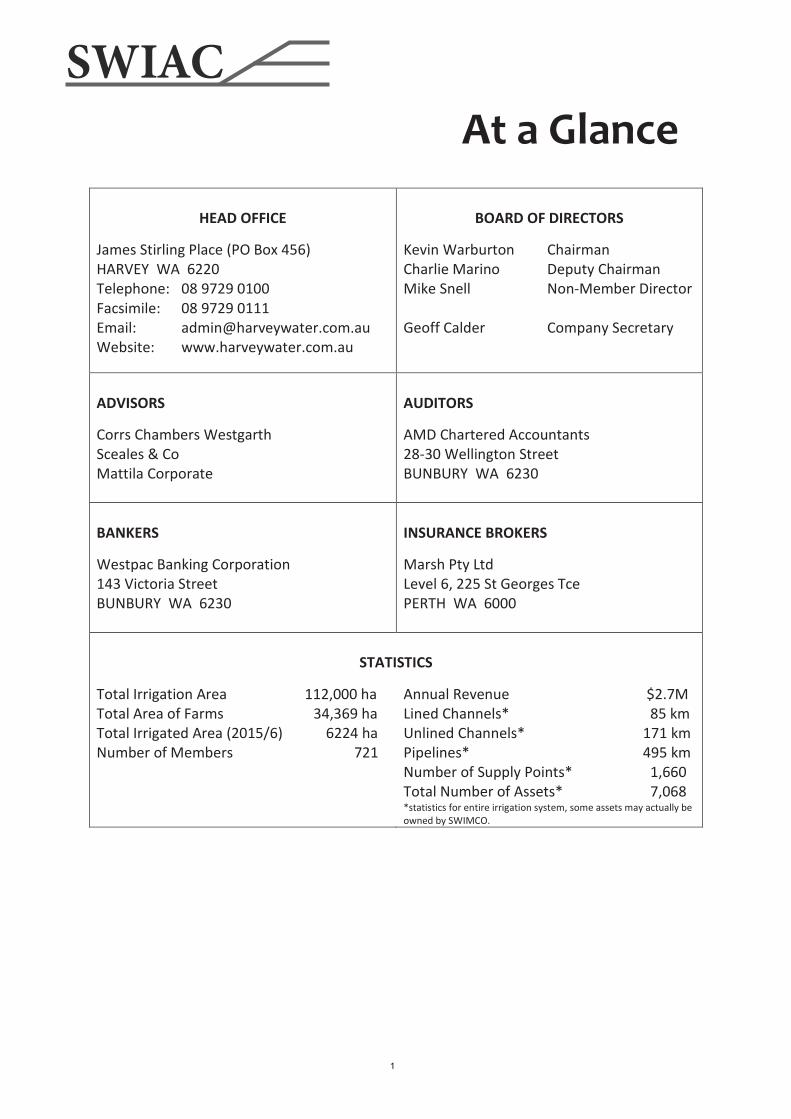

At a Glance

HEAD OFFICE

James Stirling Place (PO Box 456) HARVEY WA 6220 Telephone: 08 9729 0100 Facsimile: 08 9729 0111 Email: [email protected] Website: www.harveywater.com.au

BOARD OF DIRECTORS

Kevin Warburton Chairman Charlie Marino Deputy Chairman Mike Snell Non-Member Director Geoff Calder Company Secretary

ADVISORS

Corrs Chambers Westgarth Sceales & Co Mattila Corporate

AUDITORS

AMD Chartered Accountants 28-30 Wellington Street BUNBURY WA 6230

BANKERS

Westpac Banking Corporation 143 Victoria Street BUNBURY WA 6230

INSURANCE BROKERS

Marsh Pty Ltd Level 6, 225 St Georges Tce PERTH WA 6000

STATISTICS

Total Irrigation Area 112,000 ha Total Area of Farms 34,369 ha Total Irrigated Area (2015/6) 6224 ha Number of Members 721

Annual Revenue $2.7M Lined Channels* 85 km Unlined Channels* 171 km Pipelines* 495 km Number of Supply Points* 1,660 Total Number of Assets* 7,068 *statistics for entire irrigation system, some assets may actually be owned by SWIMCO.

SWIAC

1

At a Glance

HEAD OFFICE

James Stirling Place (PO Box 456) HARVEY WA 6220 Telephone: 08 9729 0100 Facsimile: 08 9729 0111 Email: [email protected] Website: www.harveywater.com.au

BOARD OF DIRECTORS

Kevin Warburton Chairman Charlie Marino Deputy Chairman Mike Snell Non-Member Director Geoff Calder Company Secretary

ADVISORS

Corrs Chambers Westgarth Sceales & Co Mattila Corporate

AUDITORS

AMD Chartered Accountants 28-30 Wellington Street BUNBURY WA 6230

BANKERS

Westpac Banking Corporation 143 Victoria Street BUNBURY WA 6230

INSURANCE BROKERS

Marsh Pty Ltd Level 6, 225 St Georges Tce PERTH WA 6000

STATISTICS

Total Irrigation Area 112,000 ha Total Area of Farms 34,369 ha Total Irrigated Area (2015/6) 6224 ha Number of Members 721

Annual Revenue $2.7M Lined Channels* 85 km Unlined Channels* 171 km Pipelines* 495 km Number of Supply Points* 1,660 Total Number of Assets* 7,068 *statistics for entire irrigation system, some assets may actually be owned by SWIMCO.

1

At a Glance

HEAD OFFICE

James Stirling Place (PO Box 456) HARVEY WA 6220 Telephone: 08 9729 0100 Facsimile: 08 9729 0111 Email: [email protected] Website: www.harveywater.com.au

BOARD OF DIRECTORS

Kevin Warburton Chairman Charlie Marino Deputy Chairman Mike Snell Non-Member Director Geoff Calder Company Secretary

ADVISORS

Corrs Chambers Westgarth Sceales & Co Mattila Corporate

AUDITORS

AMD Chartered Accountants 28-30 Wellington Street BUNBURY WA 6230

BANKERS

Westpac Banking Corporation 143 Victoria Street BUNBURY WA 6230

INSURANCE BROKERS

Marsh Pty Ltd Level 6, 225 St Georges Tce PERTH WA 6000

STATISTICS

Total Irrigation Area 112,000 ha Total Area of Farms 34,369 ha Total Irrigated Area (2015/6) 6224 ha Number of Members 721

Annual Revenue $2.7M Lined Channels* 85 km Unlined Channels* 171 km Pipelines* 495 km Number of Supply Points* 1,660 Total Number of Assets* 7,068 *statistics for entire irrigation system, some assets may actually be owned by SWIMCO.

2

Chairman’s Report

Kevin Warburton – Chairman

It is my pleasure to present the Annual Report for 2015/6, my first as Chairman of the South West Irrigation Asset Cooperative, with a steady as she goes financial performance. FINANCE

The mutual cooperative has a conservative investment policy that focuses on capital security to limit potential negative impacts on our shareholders funds. For the 2015/6 financial year the cooperative recorded an operating surplus of $760,023 with total funds of $24,615,824 invested in capital secure, interest bearing deposits with high rating banks. The growth of the investment fund has been affected by lower interest rates but SWIAC still has the ability and intention of using these funds to help fix the water quality problems from Wellington dam and to convert the open channel water delivery system to a piped gravity one in the Collie River Irrigation District (CRID), if the Collie Water proposal becomes a reality. COLLIE WATER PROPOSAL Last year we reported that Harvey Water and SWIAC would put an Expression of Interest (EoI) into a Water for Food Program that was targeting Myalup & Wellington. The EoI was reviewed by a Technical Advisory Group, in comparison to other EoI, and ours was referred to a Ministerial Advisory Committee which then accepted it for further development and investigation. The Minister for Water, Hon Mia Davies announced the Collie Water proposal in early 2016.

SWIAC

2

Chairman’s Report

Kevin Warburton – Chairman

It is my pleasure to present the Annual Report for 2015/6, my first as Chairman of the South West Irrigation Asset Cooperative, with a steady as she goes financial performance. FINANCE

The mutual cooperative has a conservative investment policy that focuses on capital security to limit potential negative impacts on our shareholders funds. For the 2015/6 financial year the cooperative recorded an operating surplus of $760,023 with total funds of $24,615,824 invested in capital secure, interest bearing deposits with high rating banks. The growth of the investment fund has been affected by lower interest rates but SWIAC still has the ability and intention of using these funds to help fix the water quality problems from Wellington dam and to convert the open channel water delivery system to a piped gravity one in the Collie River Irrigation District (CRID), if the Collie Water proposal becomes a reality. COLLIE WATER PROPOSAL Last year we reported that Harvey Water and SWIAC would put an Expression of Interest (EoI) into a Water for Food Program that was targeting Myalup & Wellington. The EoI was reviewed by a Technical Advisory Group, in comparison to other EoI, and ours was referred to a Ministerial Advisory Committee which then accepted it for further development and investigation. The Minister for Water, Hon Mia Davies announced the Collie Water proposal in early 2016.

3

That EoI was submitted in the name of Collie Water which is a partnership between Harvey Water, SWIAC and Aqua Ferre. Aqua Ferre are investors with interests in agricultural opportunities.

The Collie Water proposal targets three water problems, which are the need for increased reliability of supply of potable quality water for the Great Southern Towns, better quality water for CRID and more and better quality water for the Myalup Irrigated Agricultural Precinct (MIAP). It solves these problems by making better use of water that we already have access to.

The proposal includes above and below the Wellington dam and MIAP components. Of particular relevance to CRID members, is the proposal to construct a gravity driven, piped water supply as has been done for Waroona & Harvey.

There are a lot of studies on Managed Aquifer Recharge, engineering options, environmental assessments, licensing arrangements, water supply agreements and pricing with prospective users, approvals, designs, costing and so forth to complete the full pre-feasibility proposal which will be presented to the State Government for their decision on financial support by the end of 2016. It may then go on to the Commonwealth Government for their consideration. Suffice to say that SWIAC is using its best endeavours and its financial resources to take this opportunity to improve the water quality and delivery service to CRID irrigators.

This is a very large project that will require private and government funding at State and Commonwealth levels backed by a positive economic analysis and the political will to deliver the undoubted benefits.

ASSET MANAGEMENT

Our CRID assets are being kept in care and maintenance mode this year with the usual channel lining repair and refurbishment being carried out until we have more certainty on the Collie Water proposal. SWIAC, in agreement with SWIMCO, has carried out cathodic protection on our Harvey Central Pipe Scheme (HCPS) to protect our steel pipes from corrosion. This cost $308,842 and further investment will be made to complete the full task in the coming year. New meters and data loggers continue to be installed in the HCPS to bring the technology into line with that on the newer piped infrastructure. SWIMCO has carried out a wide range of R&M works under agreement with SWIAC that include maintenance, refurbishment and lining of channels and operating and metering devices amounting to $228,000 in direct cost to SWIAC and $213,000 to SWIMCO, not including overhead expenses.

SWIAC

3

That EoI was submitted in the name of Collie Water which is a partnership between Harvey Water, SWIAC and Aqua Ferre. Aqua Ferre are investors with interests in agricultural opportunities.

The Collie Water proposal targets three water problems, which are the need for increased reliability of supply of potable quality water for the Great Southern Towns, better quality water for CRID and more and better quality water for the Myalup Irrigated Agricultural Precinct (MIAP). It solves these problems by making better use of water that we already have access to.

The proposal includes above and below the Wellington dam and MIAP components. Of particular relevance to CRID members, is the proposal to construct a gravity driven, piped water supply as has been done for Waroona & Harvey.

There are a lot of studies on Managed Aquifer Recharge, engineering options, environmental assessments, licensing arrangements, water supply agreements and pricing with prospective users, approvals, designs, costing and so forth to complete the full pre-feasibility proposal which will be presented to the State Government for their decision on financial support by the end of 2016. It may then go on to the Commonwealth Government for their consideration. Suffice to say that SWIAC is using its best endeavours and its financial resources to take this opportunity to improve the water quality and delivery service to CRID irrigators.

This is a very large project that will require private and government funding at State and Commonwealth levels backed by a positive economic analysis and the political will to deliver the undoubted benefits.

ASSET MANAGEMENT

Our CRID assets are being kept in care and maintenance mode this year with the usual channel lining repair and refurbishment being carried out until we have more certainty on the Collie Water proposal. SWIAC, in agreement with SWIMCO, has carried out cathodic protection on our Harvey Central Pipe Scheme (HCPS) to protect our steel pipes from corrosion. This cost $308,842 and further investment will be made to complete the full task in the coming year. New meters and data loggers continue to be installed in the HCPS to bring the technology into line with that on the newer piped infrastructure. SWIMCO has carried out a wide range of R&M works under agreement with SWIAC that include maintenance, refurbishment and lining of channels and operating and metering devices amounting to $228,000 in direct cost to SWIAC and $213,000 to SWIMCO, not including overhead expenses.

4

Filling of redundant channels in consultation with Water Corporation cost $193,120 this year.

SUPPORT

SWIAC continues to provide strong support to SWIMCO in its endeavors to reduce the salinity in Wellington dam, bring some rationality to the fixed charges levied by Water Corporation and then to pipe the CRID, with the wide ranging and long lasting benefits those changes will bring to the co-operative, its members and the local economy. The majority of the funds provided to this project will be from SWIAC Asset Maintenance & Replacement funds. ACKNOWLEDGEMENTS Our relationship with SWIMCO remains harmonious and is operating smoothly to achieve the best benefits for all shareholders. I sincerely thank the Chairman and Directors of SWIMCO for their assistance to SWIAC. SWIMCO staff led by their untiring and committed General Manager Geoff Calder, Operations Manager Stephen Cook and Corporate Services Manager Alan Thornton, continue to provide dedicated, professional services to the Board and to the members. I thank all the staff and commend them for their efforts. The continuing support of my fellow Directors through the past year is much appreciated and I offer many thanks.

SWIAC

4

Filling of redundant channels in consultation with Water Corporation cost $193,120 this year.

SUPPORT

SWIAC continues to provide strong support to SWIMCO in its endeavors to reduce the salinity in Wellington dam, bring some rationality to the fixed charges levied by Water Corporation and then to pipe the CRID, with the wide ranging and long lasting benefits those changes will bring to the co-operative, its members and the local economy. The majority of the funds provided to this project will be from SWIAC Asset Maintenance & Replacement funds. ACKNOWLEDGEMENTS Our relationship with SWIMCO remains harmonious and is operating smoothly to achieve the best benefits for all shareholders. I sincerely thank the Chairman and Directors of SWIMCO for their assistance to SWIAC. SWIMCO staff led by their untiring and committed General Manager Geoff Calder, Operations Manager Stephen Cook and Corporate Services Manager Alan Thornton, continue to provide dedicated, professional services to the Board and to the members. I thank all the staff and commend them for their efforts. The continuing support of my fellow Directors through the past year is much appreciated and I offer many thanks.

5

Board of Directors Charlie Marino is a dairy and beef farmer from Harvey, after spending some years as a Bank Officer. He was a member of the previous South West Irrigation Management Committee, and served on the SWIMCO Board and the Audit Committee. Charlie was elected to the Board of SWIAC at the 2009 AGM and stepped down as Chairman at the 2015 AGM.

Kevin Warburton is a beef farmer from Brunswick Junction. He is an active and respected local community member, serving 18 years as President of the local kindergarten and primary school and serving on the school council. He has coached basketball and junior football and was previously president of the Brunswick Basketball Club. Kevin also served 15 years with the Kemerton Community Advisory Group and was past Vice-president of the Dairy Section of WAFF. Kevin was elected to the Board of SWIAC at the 2013 AGM and Chairman in 2015.

Mike Snell was elected to the SWIAC Board as a non-member Director at the 2008 AGM. Mike worked for over 30 years with Price Waterhouse Coopers and since retiring has served on the board of a variety of commercial and community organisations. He is also a Director of the South West Irrigation Management Co-operative Ltd. Mike is a Fellow of the Institute of Chartered Accountants in Australia and a Graduate Member of the Australian Institute of Company Directors.

Company Secretary

Geoff Calder has been Company Secretary of SWIAC since its inception in 1996. Geoff holds a Bachelor of Agricultural Science from UWA, a Graduate Diploma in Business from Curtin University and a Graduate Certificate in Asian Business from Edith Cowan University.

SWIAC

5

Board of Directors Charlie Marino is a dairy and beef farmer from Harvey, after spending some years as a Bank Officer. He was a member of the previous South West Irrigation Management Committee, and served on the SWIMCO Board and the Audit Committee. Charlie was elected to the Board of SWIAC at the 2009 AGM and stepped down as Chairman at the 2015 AGM.

Kevin Warburton is a beef farmer from Brunswick Junction. He is an active and respected local community member, serving 18 years as President of the local kindergarten and primary school and serving on the school council. He has coached basketball and junior football and was previously president of the Brunswick Basketball Club. Kevin also served 15 years with the Kemerton Community Advisory Group and was past Vice-president of the Dairy Section of WAFF. Kevin was elected to the Board of SWIAC at the 2013 AGM and Chairman in 2015.

Mike Snell was elected to the SWIAC Board as a non-member Director at the 2008 AGM. Mike worked for over 30 years with Price Waterhouse Coopers and since retiring has served on the board of a variety of commercial and community organisations. He is also a Director of the South West Irrigation Management Co-operative Ltd. Mike is a Fellow of the Institute of Chartered Accountants in Australia and a Graduate Member of the Australian Institute of Company Directors.

Company Secretary

Geoff Calder has been Company Secretary of SWIAC since its inception in 1996. Geoff holds a Bachelor of Agricultural Science from UWA, a Graduate Diploma in Business from Curtin University and a Graduate Certificate in Asian Business from Edith Cowan University.

6

Corporate Governance Board Responsibilities The Board is accountable to members for the performance of the Co-operative. In carrying out its responsibilities, the Board undertakes to serve the interests of members, employees, customers and the broader community, honestly, fairly, diligently and in accordance with the Rules, Company Policy, Directors’ Code of Conduct and with applicable laws.

In particular, the Board:

• Sets and reviews strategic direction • Establishes and reviews policy • Ensures compliance with laws and all appropriate accounting standards • Monitors the operating and financial performance of the Company • Monitors risk management • Ensures adequate and inclusive communication with shareholders.

Board Structure The Rules provide for a maximum of five Directors. This includes no more than two member representatives from any of the Collie River, Harvey or Waroona district with no less than two districts represented. There can also be one non-member Director with skills, experience or knowledge in the engineering, industrial, legal, commercial or financial sectors.

The Board currently comprises two member Directors, sourced from the Harvey and Collie River districts, and one non-member Director. Details of the Directors, as at the date of this report, including their qualifications and experience are set out on page 5.

Meetings Under the Rules the Board is able to schedule and regulate meetings as they see fit. The Board met, for formal Board meetings, on nine occasions during the year. In addition to this, the Board meets whenever necessary to deal with specific matters. Details of Directors’ attendance at meetings are set out on page 9.

The Chairman and the Company Secretary establish meeting agendas to ensure adequate coverage of strategic, financial and risk areas. Directors are encouraged to participate and exercise their independent judgment.

Access to Information and Professional Advice Directors receive regular detailed financial and operational reports and have unrestricted access to Company records and information. The members of the Board have the authority to engage independent experts should it be considered necessary subject to the prior approval of the Chairman.

SWIAC

6

Corporate Governance Board Responsibilities The Board is accountable to members for the performance of the Co-operative. In carrying out its responsibilities, the Board undertakes to serve the interests of members, employees, customers and the broader community, honestly, fairly, diligently and in accordance with the Rules, Company Policy, Directors’ Code of Conduct and with applicable laws.

In particular, the Board:

• Sets and reviews strategic direction • Establishes and reviews policy • Ensures compliance with laws and all appropriate accounting standards • Monitors the operating and financial performance of the Company • Monitors risk management • Ensures adequate and inclusive communication with shareholders.

Board Structure The Rules provide for a maximum of five Directors. This includes no more than two member representatives from any of the Collie River, Harvey or Waroona district with no less than two districts represented. There can also be one non-member Director with skills, experience or knowledge in the engineering, industrial, legal, commercial or financial sectors.

The Board currently comprises two member Directors, sourced from the Harvey and Collie River districts, and one non-member Director. Details of the Directors, as at the date of this report, including their qualifications and experience are set out on page 5.

Meetings Under the Rules the Board is able to schedule and regulate meetings as they see fit. The Board met, for formal Board meetings, on nine occasions during the year. In addition to this, the Board meets whenever necessary to deal with specific matters. Details of Directors’ attendance at meetings are set out on page 9.

The Chairman and the Company Secretary establish meeting agendas to ensure adequate coverage of strategic, financial and risk areas. Directors are encouraged to participate and exercise their independent judgment.

Access to Information and Professional Advice Directors receive regular detailed financial and operational reports and have unrestricted access to Company records and information. The members of the Board have the authority to engage independent experts should it be considered necessary subject to the prior approval of the Chairman.

7

Corporate Governance (cont.) Directors and Officers Insurance and Deeds of Indemnity The Company provides Directors’ and Officers’ Insurance and access to Deeds of Indemnity Insurance to the maximum extent permitted by law.

Director Training All Directors are expected to maintain the skills required to discharge their obligations to the Company. Directors are encouraged to undertake continuing professional education involving industry seminars and approved education courses. All Directors are encouraged to attend industry specific conferences including the annual IAL Conference and the WA Co-operatives Conference.

Review of Board and Director Performance The Remuneration Committee is responsible for overseeing the annual evaluation of Board and Director performance. Evaluations are conducted every year and have produced continuing improvements in Board processes and overall efficiency.

Committees of the Board The Board has established one current standing committee to assist in the discharge of its responsibilities, being the Remuneration Committee, a joint Committee with the South West Irrigation Management Co-operative (SWIMCO). The Remuneration Committee has its own charter which describes its role and duties.

SWIAC has an Asset Committee which is responsible for reviewing the proposed asset management program drawn up in consultation with SWIMCO. The committee meets on an ad hoc basis at the discretion of the Board.

Minutes of standing committees are provided to all Directors and the proceedings of each meeting are reported by the Chairman of the committee at the next Board meeting. The Board reviews the composition of its committees annually at the first Board meeting following the Annual General Meeting.

Remuneration Committee The Remuneration Committee is a joint committee of both SWIAC and SWIMCO. Remuneration issues in respect to Directors are considered as a group rather than individually given the common shareholding. The primary functions of the Remuneration Committee are to:

• Make specific recommendations to the Board of SWIAC on the remuneration of

Directors and the Company Secretary. • Undertake a review of the performance of the Company Secretary at least annually,

setting goals for the coming year and reviewing progress in achieving these goals

SWIAC

7

Corporate Governance (cont.) Directors and Officers Insurance and Deeds of Indemnity The Company provides Directors’ and Officers’ Insurance and access to Deeds of Indemnity Insurance to the maximum extent permitted by law.

Director Training All Directors are expected to maintain the skills required to discharge their obligations to the Company. Directors are encouraged to undertake continuing professional education involving industry seminars and approved education courses. All Directors are encouraged to attend industry specific conferences including the annual IAL Conference and the WA Co-operatives Conference.

Review of Board and Director Performance The Remuneration Committee is responsible for overseeing the annual evaluation of Board and Director performance. Evaluations are conducted every year and have produced continuing improvements in Board processes and overall efficiency.

Committees of the Board The Board has established one current standing committee to assist in the discharge of its responsibilities, being the Remuneration Committee, a joint Committee with the South West Irrigation Management Co-operative (SWIMCO). The Remuneration Committee has its own charter which describes its role and duties.

SWIAC has an Asset Committee which is responsible for reviewing the proposed asset management program drawn up in consultation with SWIMCO. The committee meets on an ad hoc basis at the discretion of the Board.

Minutes of standing committees are provided to all Directors and the proceedings of each meeting are reported by the Chairman of the committee at the next Board meeting. The Board reviews the composition of its committees annually at the first Board meeting following the Annual General Meeting.

Remuneration Committee The Remuneration Committee is a joint committee of both SWIAC and SWIMCO. Remuneration issues in respect to Directors are considered as a group rather than individually given the common shareholding. The primary functions of the Remuneration Committee are to:

• Make specific recommendations to the Board of SWIAC on the remuneration of

Directors and the Company Secretary. • Undertake a review of the performance of the Company Secretary at least annually,

setting goals for the coming year and reviewing progress in achieving these goals

8

Corporate Governance (cont.)

• Oversee the annual evaluation of Board and Director performance • Review Board succession plans including the appointment of non-member Directors. Members of the Remuneration Committee are:

Mike Snell (Chairman) Kevin Warburton (Chair of SWIAC) Ian Eckersley (Chair of SWIMCO)

Disputes Panel In accordance with Rule 88, the Chairman has determined that the Disputes Panel shall comprise all Directors of the Company and three members who are not Directors. For the period ended 30 June 2016, the non-Director members were:

Frank Parravicini Vernon Pitter Terry Treasure

The Disputes Panel was not required to convene during the year.

Communication with Shareholders Directors recognise that shareholders, as the ultimate owners of the Company, are entitled to receive timely and relevant information about the Company. The Board has approved a Communication Policy that aims to promote open and effective communication with shareholders and other stakeholders of the Co-operative. A range of communication means are used including:

• Annual Report • Annual General Meeting • “Under the Trees” meetings with shareholders • Annual Irrigators meeting • website www.harveywater.com.au • Harvey Water Video/CD • Newspaper advertisements • Regular Shareholder mail outs (“The Furphy”) • General media releases and public comment.

SWIAC

8

Corporate Governance (cont.)

• Oversee the annual evaluation of Board and Director performance • Review Board succession plans including the appointment of non-member Directors. Members of the Remuneration Committee are:

Mike Snell (Chairman) Kevin Warburton (Chair of SWIAC) Ian Eckersley (Chair of SWIMCO)

Disputes Panel In accordance with Rule 88, the Chairman has determined that the Disputes Panel shall comprise all Directors of the Company and three members who are not Directors. For the period ended 30 June 2016, the non-Director members were:

Frank Parravicini Vernon Pitter Terry Treasure

The Disputes Panel was not required to convene during the year.

Communication with Shareholders Directors recognise that shareholders, as the ultimate owners of the Company, are entitled to receive timely and relevant information about the Company. The Board has approved a Communication Policy that aims to promote open and effective communication with shareholders and other stakeholders of the Co-operative. A range of communication means are used including:

• Annual Report • Annual General Meeting • “Under the Trees” meetings with shareholders • Annual Irrigators meeting • website www.harveywater.com.au • Harvey Water Video/CD • Newspaper advertisements • Regular Shareholder mail outs (“The Furphy”) • General media releases and public comment.

9

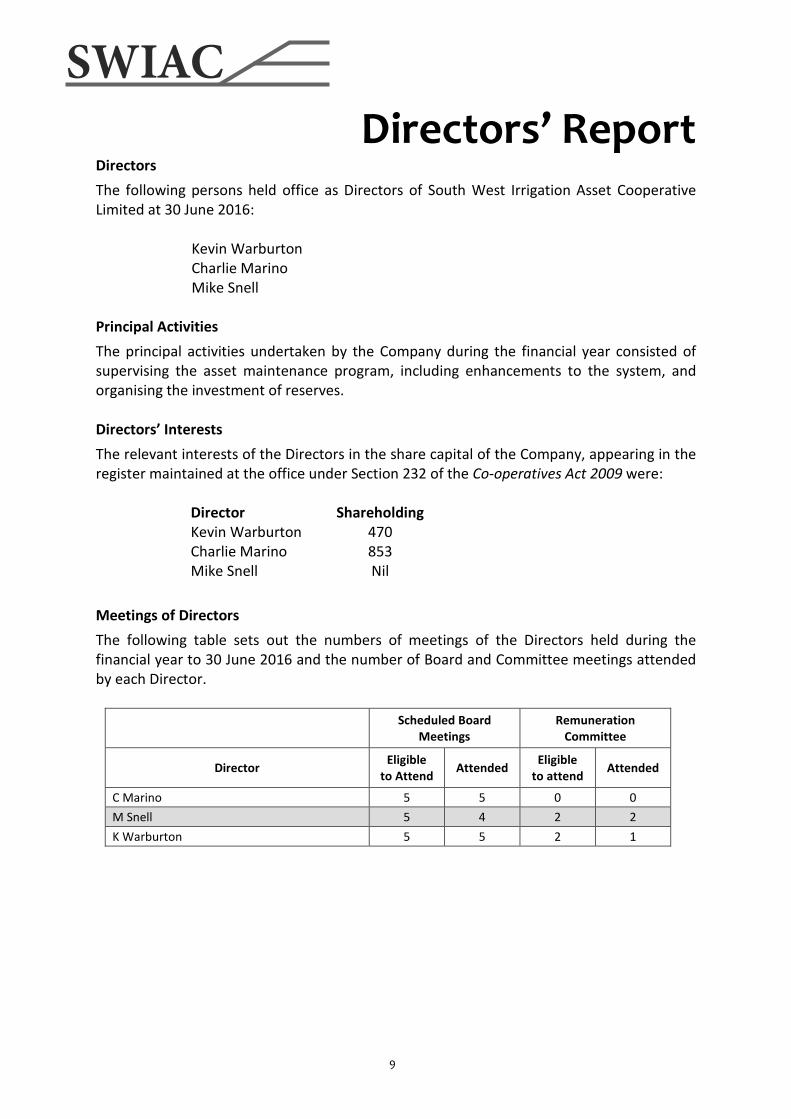

Directors’ Report Directors The following persons held office as Directors of South West Irrigation Asset Cooperative Limited at 30 June 2016:

Kevin Warburton Charlie Marino Mike Snell

Principal Activities The principal activities undertaken by the Company during the financial year consisted of supervising the asset maintenance program, including enhancements to the system, and organising the investment of reserves.

Directors’ Interests The relevant interests of the Directors in the share capital of the Company, appearing in the register maintained at the office under Section 232 of the Co-operatives Act 2009 were:

Director Shareholding Kevin Warburton 470 Charlie Marino 853 Mike Snell Nil

Meetings of Directors The following table sets out the numbers of meetings of the Directors held during the financial year to 30 June 2016 and the number of Board and Committee meetings attended by each Director.

Scheduled Board Meetings

Remuneration Committee

Director Eligible to Attend Attended Eligible

to attend Attended

C Marino 5 5 0 0 M Snell 5 4 2 2 K Warburton 5 5 2 1

SWIAC

9

Directors’ Report Directors The following persons held office as Directors of South West Irrigation Asset Cooperative Limited at 30 June 2016:

Kevin Warburton Charlie Marino Mike Snell

Principal Activities The principal activities undertaken by the Company during the financial year consisted of supervising the asset maintenance program, including enhancements to the system, and organising the investment of reserves.

Directors’ Interests The relevant interests of the Directors in the share capital of the Company, appearing in the register maintained at the office under Section 232 of the Co-operatives Act 2009 were:

Director Shareholding Kevin Warburton 470 Charlie Marino 853 Mike Snell Nil

Meetings of Directors The following table sets out the numbers of meetings of the Directors held during the financial year to 30 June 2016 and the number of Board and Committee meetings attended by each Director.

Scheduled Board Meetings

Remuneration Committee

Director Eligible to Attend Attended Eligible

to attend Attended

C Marino 5 5 0 0 M Snell 5 4 2 2 K Warburton 5 5 2 1

10

Directors’ Report (cont.) Significant Changes There were no significant changes in the state of affairs of the Company that occurred during the year which are not otherwise in this report and the accounts.

Directors’ Benefits No Director of the Company has received, or has become entitled to receive, a benefit (other than a remuneration benefit included in Note 14 to the accounts) because of a contract that the Director, or a firm in which the Director is a member, or an entity in which the Director has a substantial financial interest, has made with the Company.

Auditor AMD Chartered Accountants of Bunbury, were appointed auditors of the Company at the Annual General Meeting held 18 November 2015.

This report is made in accordance with a resolution of the Directors.

Kevin Thomas Warburton Carmelo Marino Chairman Director Harvey, Western Australia 19 October 2016

SWIAC

10

Directors’ Report (cont.) Significant Changes There were no significant changes in the state of affairs of the Company that occurred during the year which are not otherwise in this report and the accounts.

Directors’ Benefits No Director of the Company has received, or has become entitled to receive, a benefit (other than a remuneration benefit included in Note 14 to the accounts) because of a contract that the Director, or a firm in which the Director is a member, or an entity in which the Director has a substantial financial interest, has made with the Company.

Auditor AMD Chartered Accountants of Bunbury, were appointed auditors of the Company at the Annual General Meeting held 18 November 2015.

This report is made in accordance with a resolution of the Directors.

Kevin Thomas Warburton Carmelo Marino Chairman Director Harvey, Western Australia 19 October 2016

11

Statutory Report of the Directors In accordance with the requirements of s.295 (4) of the Corporations Act 2001 and Rule 74, the Directors declare that that: (a) in the directors’ opinion, there are reasonable grounds to believe that the Co-

operative will be able to pay its debts as and when they become due and payable; (b) in the directors’ opinion, the attached financial statements and notes thereto are in

accordance with the Corporations Act 2001, including compliance with accounting standards and giving a true and fair view of the financial position and performance of the Co-operative; and

(c) no dividend is recommended. Signed in accordance with a resolution of the Directors made pursuant to s.295 (5) of the Corporations Act 2001. On behalf of the Directors

Kevin Thomas Warburton Carmelo Marino Chairman Director Harvey, Western Australia 19 October 2016

Certificate by the Directors We, (Kevin Thomas Warburton and Carmelo Marino), being two of the Directors of South West Irrigation Asset Cooperative Limited do hereby certify on behalf of the Board that, in our opinion, the accompanying Statement of Financial Position is drawn up so as to exhibit a true and correct view of the state of the Company’s affairs and that, in our opinion, the Statement of Financial Performance is drawn up so as to exhibit a true and correct view of the results of the business of the Company for the year.

Kevin Thomas Warburton Carmelo Marino Chairman Director Harvey, Western Australia 19 October 2016

SWIAC

11

Statutory Report of the Directors In accordance with the requirements of s.295 (4) of the Corporations Act 2001 and Rule 74, the Directors declare that that: (a) in the directors’ opinion, there are reasonable grounds to believe that the Co-

operative will be able to pay its debts as and when they become due and payable; (b) in the directors’ opinion, the attached financial statements and notes thereto are in

accordance with the Corporations Act 2001, including compliance with accounting standards and giving a true and fair view of the financial position and performance of the Co-operative; and

(c) no dividend is recommended. Signed in accordance with a resolution of the Directors made pursuant to s.295 (5) of the Corporations Act 2001. On behalf of the Directors

Kevin Thomas Warburton Carmelo Marino Chairman Director Harvey, Western Australia 19 October 2016

Certificate by the Directors We, (Kevin Thomas Warburton and Carmelo Marino), being two of the Directors of South West Irrigation Asset Cooperative Limited do hereby certify on behalf of the Board that, in our opinion, the accompanying Statement of Financial Position is drawn up so as to exhibit a true and correct view of the state of the Company’s affairs and that, in our opinion, the Statement of Financial Performance is drawn up so as to exhibit a true and correct view of the results of the business of the Company for the year.

Kevin Thomas Warburton Carmelo Marino Chairman Director Harvey, Western Australia 19 October 2016

12

SOUTH WEST IRRIGATION ASSET CO-OPERATIVE LIMITED

Financial Report

30 June 2016

SWIAC

13

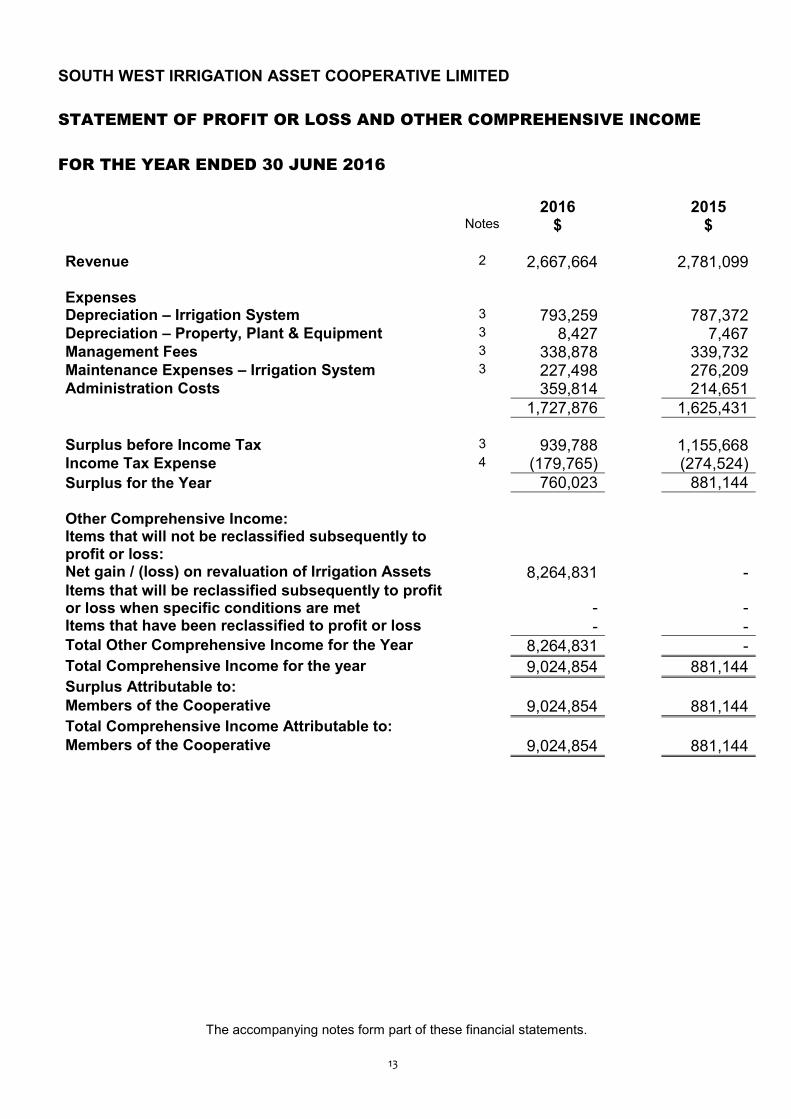

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30 JUNE 2016

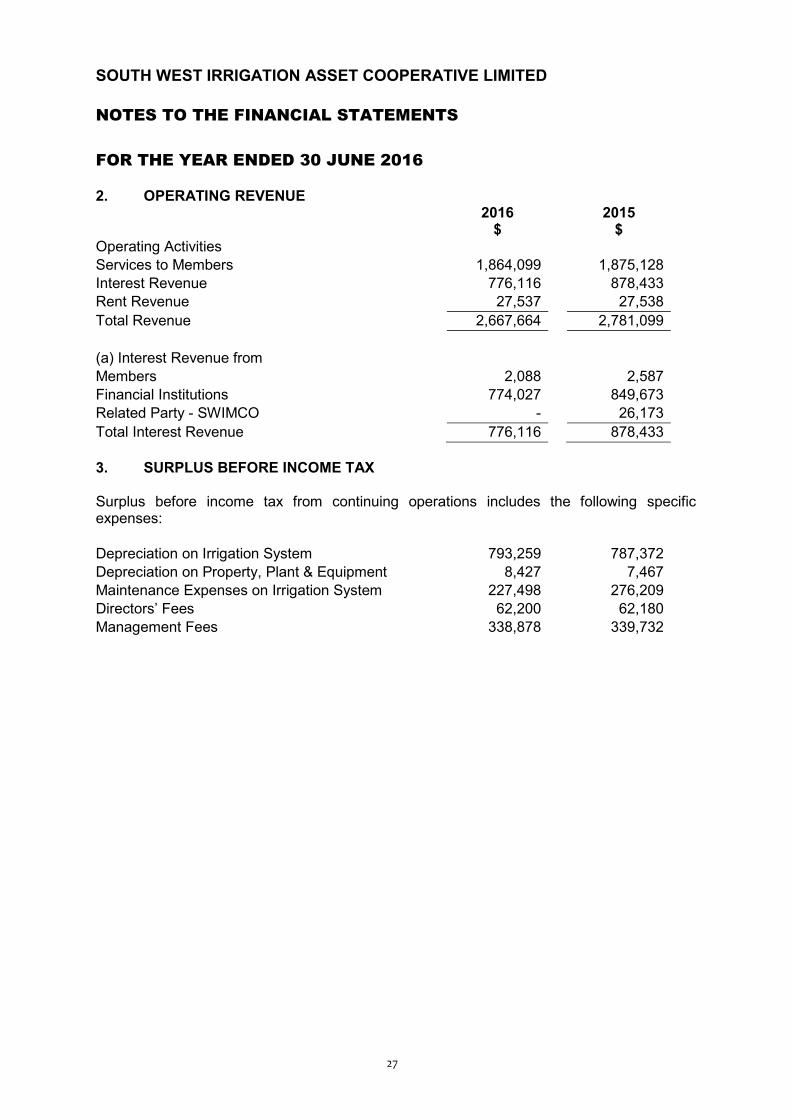

2016 2015Notes $ $

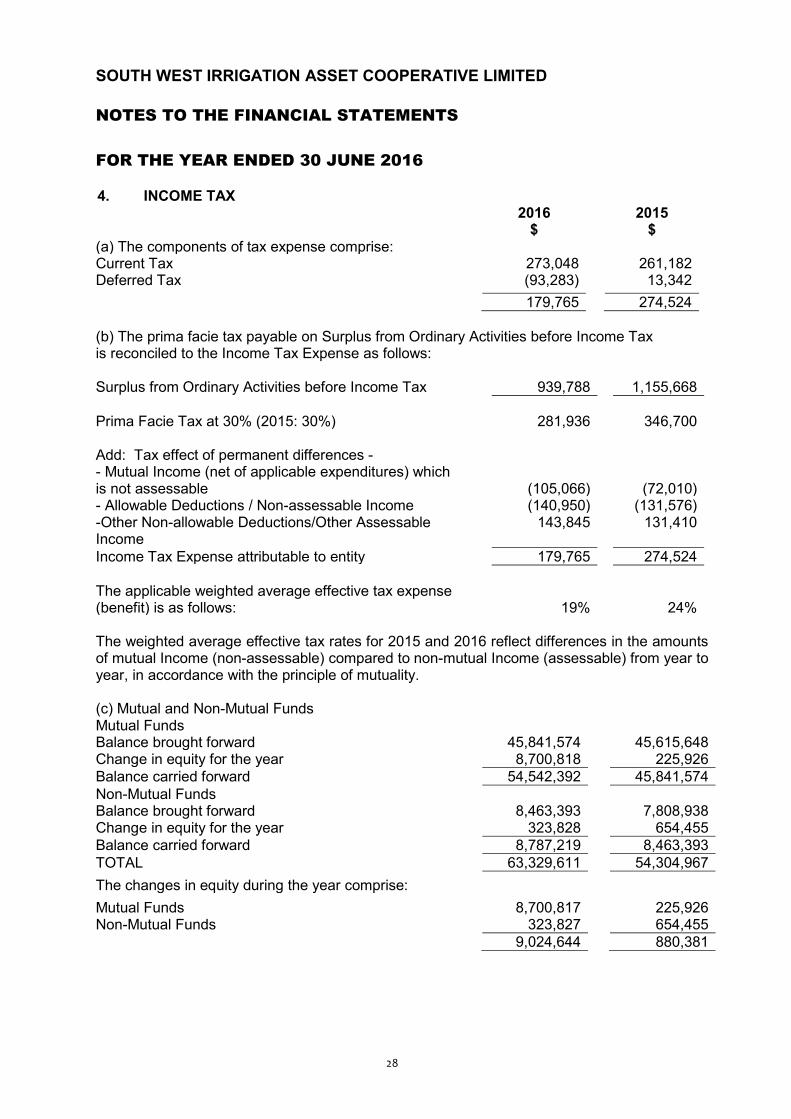

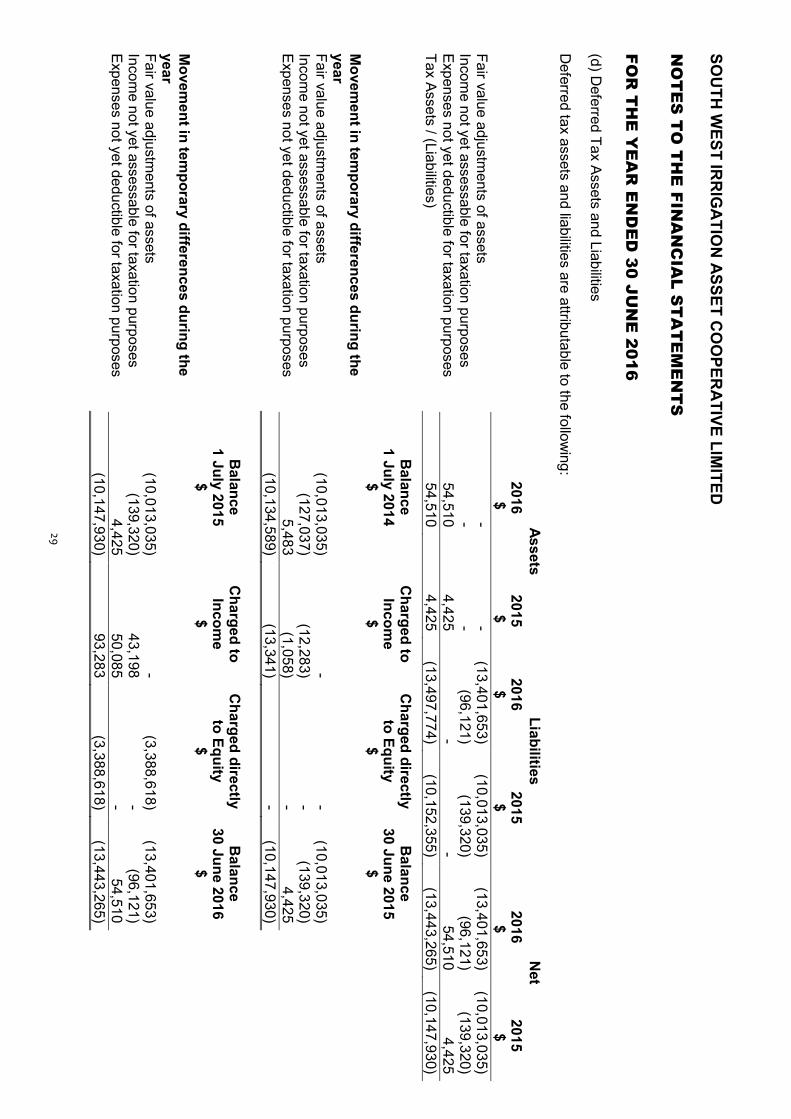

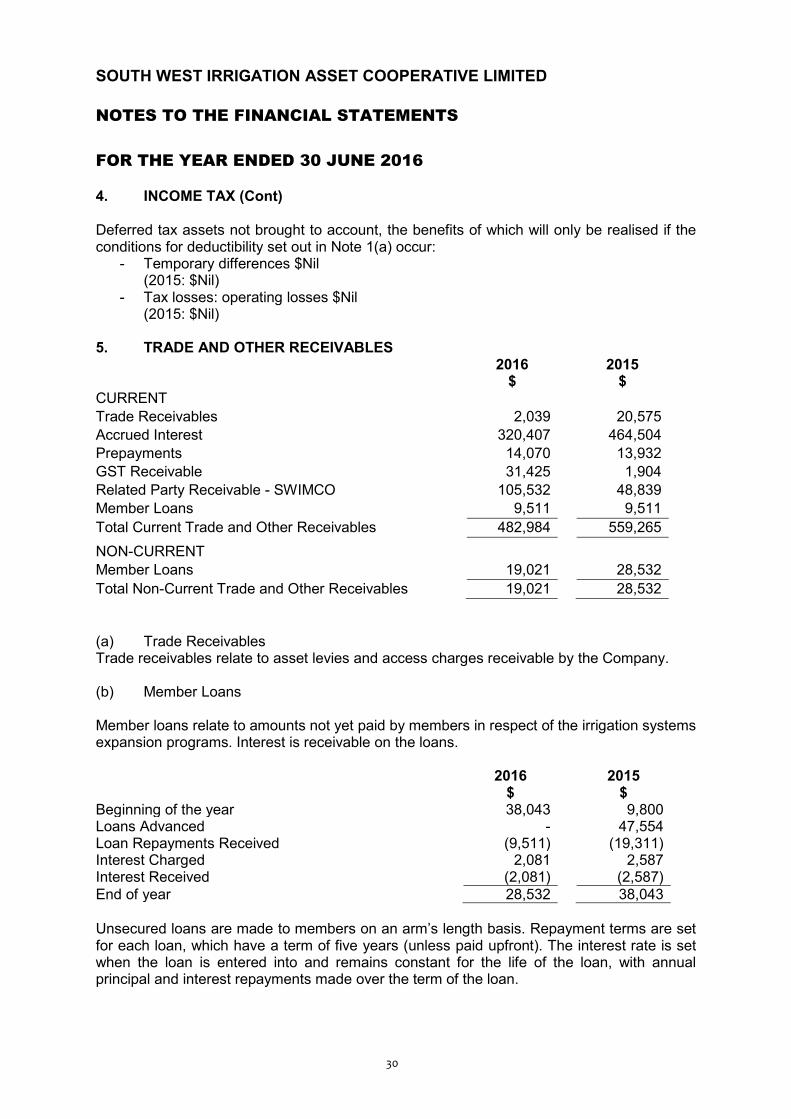

Revenue 2 2,667,664 2,781,099

Expenses Depreciation – Irrigation System 3 793,259 787,372Depreciation – Property, Plant & Equipment 3 8,427 7,467Management Fees 3 338,878 339,732Maintenance Expenses – Irrigation System 3 227,498 276,209Administration Costs 359,814 214,651

1,727,876 1,625,431

Surplus before Income Tax 3 939,788 1,155,668Income Tax Expense 4 (179,765) (274,524)Surplus for the Year 760,023 881,144

Other Comprehensive Income:Items that will not be reclassified subsequently to profit or loss:Net gain / (loss) on revaluation of Irrigation Assets 8,264,831 -Items that will be reclassified subsequently to profit or loss when specific conditions are met - -Items that have been reclassified to profit or loss - -Total Other Comprehensive Income for the Year 8,264,831 -Total Comprehensive Income for the year 9,024,854 881,144Surplus Attributable to:Members of the Cooperative 9,024,854 881,144Total Comprehensive Income Attributable to:Members of the Cooperative 9,024,854 881,144

The accompanying notes form part of these financial statements.

13

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30 JUNE 2016

2016 2015Notes $ $

Revenue 2 2,667,664 2,781,099

Expenses Depreciation – Irrigation System 3 793,259 787,372Depreciation – Property, Plant & Equipment 3 8,427 7,467Management Fees 3 338,878 339,732Maintenance Expenses – Irrigation System 3 227,498 276,209Administration Costs 359,814 214,651

1,727,876 1,625,431

Surplus before Income Tax 3 939,788 1,155,668Income Tax Expense 4 (179,765) (274,524)Surplus for the Year 760,023 881,144

Other Comprehensive Income:Items that will not be reclassified subsequently to profit or loss:Net gain / (loss) on revaluation of Irrigation Assets 8,264,831 -Items that will be reclassified subsequently to profit or loss when specific conditions are met - -Items that have been reclassified to profit or loss - -Total Other Comprehensive Income for the Year 8,264,831 -Total Comprehensive Income for the year 9,024,854 881,144Surplus Attributable to:Members of the Cooperative 9,024,854 881,144Total Comprehensive Income Attributable to:Members of the Cooperative 9,024,854 881,144

The accompanying notes form part of these financial statements.

14

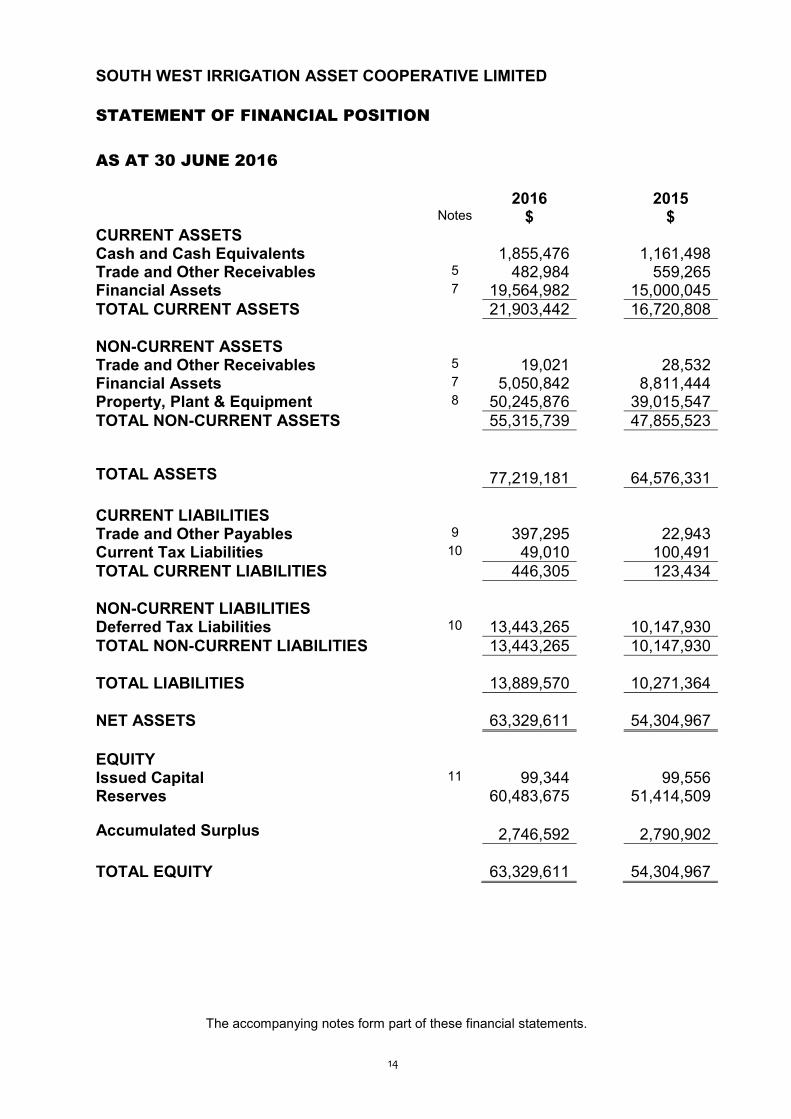

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2016

2016 2015Notes $ $

CURRENT ASSETSCash and Cash Equivalents 1,855,476 1,161,498Trade and Other Receivables 5 482,984 559,265Financial Assets 7 19,564,982 15,000,045TOTAL CURRENT ASSETS 21,903,442 16,720,808

NON-CURRENT ASSETSTrade and Other Receivables 5 19,021 28,532Financial Assets 7 5,050,842 8,811,444Property, Plant & Equipment 8 50,245,876 39,015,547TOTAL NON-CURRENT ASSETS 55,315,739 47,855,523

TOTAL ASSETS 77,219,181 64,576,331

CURRENT LIABILITIESTrade and Other Payables 9 397,295 22,943Current Tax Liabilities 10 49,010 100,491TOTAL CURRENT LIABILITIES 446,305 123,434

NON-CURRENT LIABILITIESDeferred Tax Liabilities 10 13,443,265 10,147,930TOTAL NON-CURRENT LIABILITIES 13,443,265 10,147,930

TOTAL LIABILITIES 13,889,570 10,271,364

NET ASSETS 63,329,611 54,304,967

EQUITYIssued Capital 11 99,344 99,556Reserves 60,483,675 51,414,509

Accumulated Surplus 2,746,592 2,790,902

TOTAL EQUITY 63,329,611 54,304,967

The accompanying notes form part of these financial statements.

14

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2016

2016 2015Notes $ $

CURRENT ASSETSCash and Cash Equivalents 1,855,476 1,161,498Trade and Other Receivables 5 482,984 559,265Financial Assets 7 19,564,982 15,000,045TOTAL CURRENT ASSETS 21,903,442 16,720,808

NON-CURRENT ASSETSTrade and Other Receivables 5 19,021 28,532Financial Assets 7 5,050,842 8,811,444Property, Plant & Equipment 8 50,245,876 39,015,547TOTAL NON-CURRENT ASSETS 55,315,739 47,855,523

TOTAL ASSETS 77,219,181 64,576,331

CURRENT LIABILITIESTrade and Other Payables 9 397,295 22,943Current Tax Liabilities 10 49,010 100,491TOTAL CURRENT LIABILITIES 446,305 123,434

NON-CURRENT LIABILITIESDeferred Tax Liabilities 10 13,443,265 10,147,930TOTAL NON-CURRENT LIABILITIES 13,443,265 10,147,930

TOTAL LIABILITIES 13,889,570 10,271,364

NET ASSETS 63,329,611 54,304,967

EQUITYIssued Capital 11 99,344 99,556Reserves 60,483,675 51,414,509

Accumulated Surplus 2,746,592 2,790,902

TOTAL EQUITY 63,329,611 54,304,967

The accompanying notes form part of these financial statements.

15

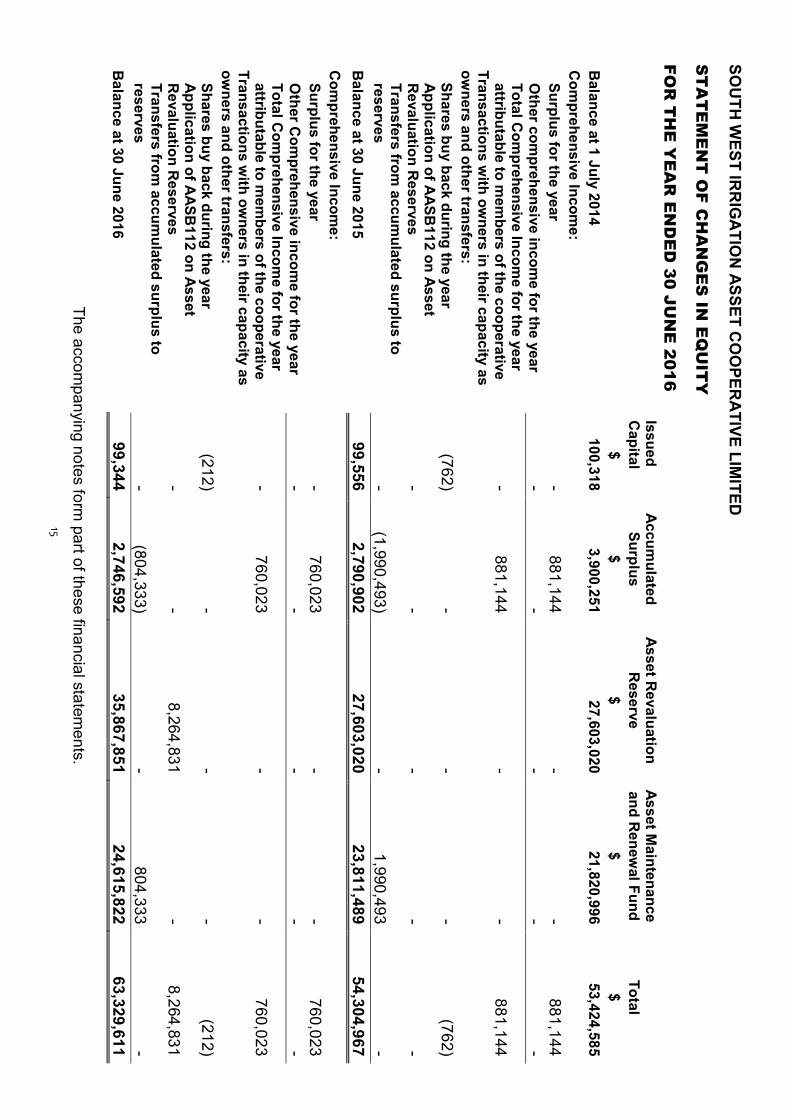

SOU

TH W

EST IRR

IGA

TION

ASSET C

OO

PERA

TIVE LIMITED

ST

AT

EM

EN

T O

F CH

AN

GE

S IN

EQ

UIT

Y

FOR

TH

E Y

EA

R E

ND

ED

30JU

NE

2016Issued C

apitalAccum

ulated Surplus

Asset Revaluation

Reserve

Asset Maintenance

and Renew

al FundTotal

$$

$$

$B

alance at 1 July 2014100,318

3,900,25127,603,020

21,820,99653,424,585

Com

prehensive Income:

Surplus for the year-

881,144-

-881,144

Other com

prehensive income for the year

--

--

-Total C

omprehensive Incom

e for the year attributable to m

embers of the cooperative

-881,144

--

881,144Transactions w

ith owners in their capacity as

owners and other transfers:

Shares buy back during the year(762)

--

-(762)

Application of AASB

112 on Asset R

evaluation Reserves

--

--

-Transfers from

accumulated surplus to

reserves-

(1,990,493)-

1,990,493-

Balance at 30 June 2015

99,5562,790,902

27,603,02023,811,489

54,304,967C

omprehensive Incom

e:Surplus for the year

-760,023

--

760,023O

ther Com

prehensive income for the year

--

--

-Total C

omprehensive Incom

e for the year attributable to m

embers of the cooperative

-760,023

--

760,023Transactions w

ith owners in their capacity as

owners and other transfers:

Shares buy back during the year (212)

--

-(212)

Application of AASB

112 on Asset R

evaluation Reserves

--

8,264,831-

8,264,831Transfers from

accumulated surplus to

reserves-

(804,333)-

804,333-

Balance at 30 June 2016

99,3442,746,592

35,867,85124,615,822

63,329,611

The accompanying notes form

part of these financial statements.

16

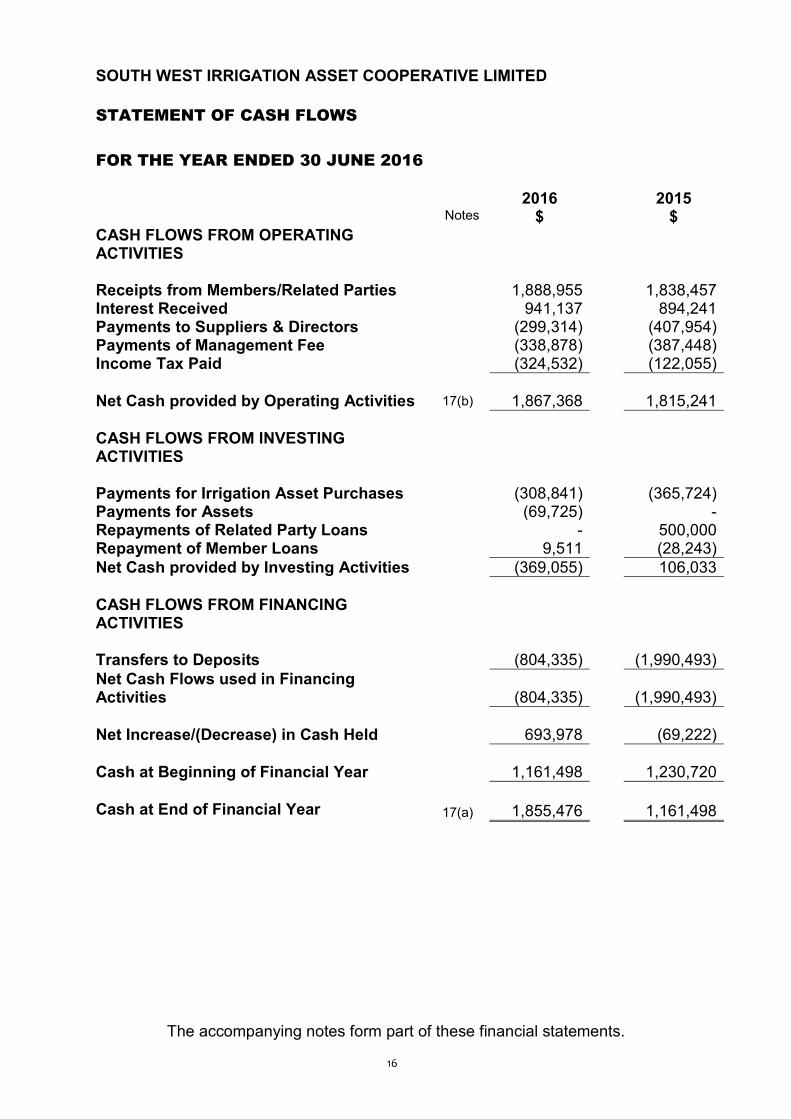

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2016

2016 2015Notes $ $

CASH FLOWS FROM OPERATING ACTIVITIES

Receipts from Members/Related Parties 1,888,955 1,838,457Interest Received 941,137 894,241Payments to Suppliers & Directors (299,314) (407,954)Payments of Management Fee (338,878) (387,448)Income Tax Paid (324,532) (122,055)

Net Cash provided by Operating Activities 17(b) 1,867,368 1,815,241

CASH FLOWS FROM INVESTING ACTIVITIES

Payments for Irrigation Asset Purchases (308,841) (365,724)Payments for Assets (69,725) -Repayments of Related Party Loans - 500,000Repayment of Member Loans 9,511 (28,243)Net Cash provided by Investing Activities (369,055) 106,033

CASH FLOWS FROM FINANCING ACTIVITIES

Transfers to Deposits (804,335) (1,990,493)Net Cash Flows used in Financing Activities (804,335) (1,990,493)

Net Increase/(Decrease) in Cash Held 693,978 (69,222)

Cash at Beginning of Financial Year 1,161,498 1,230,720

Cash at End of Financial Year 17(a) 1,855,476 1,161,498

The accompanying notes form part of these financial statements.

16

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2016

2016 2015Notes $ $

CASH FLOWS FROM OPERATING ACTIVITIES

Receipts from Members/Related Parties 1,888,955 1,838,457Interest Received 941,137 894,241Payments to Suppliers & Directors (299,314) (407,954)Payments of Management Fee (338,878) (387,448)Income Tax Paid (324,532) (122,055)

Net Cash provided by Operating Activities 17(b) 1,867,368 1,815,241

CASH FLOWS FROM INVESTING ACTIVITIES

Payments for Irrigation Asset Purchases (308,841) (365,724)Payments for Assets (69,725) -Repayments of Related Party Loans - 500,000Repayment of Member Loans 9,511 (28,243)Net Cash provided by Investing Activities (369,055) 106,033

CASH FLOWS FROM FINANCING ACTIVITIES

Transfers to Deposits (804,335) (1,990,493)Net Cash Flows used in Financing Activities (804,335) (1,990,493)

Net Increase/(Decrease) in Cash Held 693,978 (69,222)

Cash at Beginning of Financial Year 1,161,498 1,230,720

Cash at End of Financial Year 17(a) 1,855,476 1,161,498

The accompanying notes form part of these financial statements.

17

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES

South West Irrigation Asset Cooperative Limited (‘the Company’) is a co-operative limited by shares, incorporated and domiciled in Australia.

Basis of PreparationThe financial statements are general purpose financial statements that have been prepared in accordance with Australian Accounting Standards of the Australian Accounting Standards Board and the Cooperatives Act 2009.

Australian Accounting Standards set out accounting policies that the AASB has concluded would result in financial statements containing relevant and reliable information about transactions, events and conditions. Material accounting policies adopted in the preparation of the financial statements are presented below and have been consistently applied unless otherwise stated.

The financial statements have been prepared on an accruals basis and are based on historical costs, modified where applicable by the measurement at fair value of selected non-current assets, financial assets and financial liabilities. The amounts presented in the financial statements have been rounded to the nearest dollar.

(a) Income TaxThe income tax expense (revenue) for the year comprises current income tax expense (income) and deferred tax expense (income). Current income tax expense (income) charged (or credited) to the profit or loss is the tax payable (receivable) on taxable income for the year adjusted for any non-assessable or disallowed items, including mutual income as defined below. Current tax liabilities (assets) are therefore measured at the amounts expected to be paid to (recovered from) the relevant taxation authority.

Current and deferred income tax expense (income) is calculated using applicable income tax rates enacted, or substantially enacted, as at reporting date.

In 1996 a tax ruling was received from the Australian Taxation Office defining income that is assessable under the Income Tax Assessment Act:

Mutual IncomeMutual Income relates to monies paid to the Company by its members.

Taxable IncomeTaxable Income relates to monies received from other sources that do not meet the mutuality requirements and are taxable. A major source of this income is interest received.

Deferred TaxDeferred income tax expense reflects movements in deferred tax asset and deferred tax liability balances during the year as well as unused tax losses.

Current and deferred income tax expense (income) is charged (or credited) outside profit or loss when the tax relates to items that are recognised outside profit or loss.

17

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES

South West Irrigation Asset Cooperative Limited (‘the Company’) is a co-operative limited by shares, incorporated and domiciled in Australia.

Basis of PreparationThe financial statements are general purpose financial statements that have been prepared in accordance with Australian Accounting Standards of the Australian Accounting Standards Board and the Cooperatives Act 2009.

Australian Accounting Standards set out accounting policies that the AASB has concluded would result in financial statements containing relevant and reliable information about transactions, events and conditions. Material accounting policies adopted in the preparation of the financial statements are presented below and have been consistently applied unless otherwise stated.

The financial statements have been prepared on an accruals basis and are based on historical costs, modified where applicable by the measurement at fair value of selected non-current assets, financial assets and financial liabilities. The amounts presented in the financial statements have been rounded to the nearest dollar.

(a) Income TaxThe income tax expense (revenue) for the year comprises current income tax expense (income) and deferred tax expense (income). Current income tax expense (income) charged (or credited) to the profit or loss is the tax payable (receivable) on taxable income for the year adjusted for any non-assessable or disallowed items, including mutual income as defined below. Current tax liabilities (assets) are therefore measured at the amounts expected to be paid to (recovered from) the relevant taxation authority.

Current and deferred income tax expense (income) is calculated using applicable income tax rates enacted, or substantially enacted, as at reporting date.

In 1996 a tax ruling was received from the Australian Taxation Office defining income that is assessable under the Income Tax Assessment Act:

Mutual IncomeMutual Income relates to monies paid to the Company by its members.

Taxable IncomeTaxable Income relates to monies received from other sources that do not meet the mutuality requirements and are taxable. A major source of this income is interest received.

Deferred TaxDeferred income tax expense reflects movements in deferred tax asset and deferred tax liability balances during the year as well as unused tax losses.

Current and deferred income tax expense (income) is charged (or credited) outside profit or loss when the tax relates to items that are recognised outside profit or loss.

18

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

Deferred tax assets and liabilities are calculated at the tax rates that are expected to apply to the period when the asset is realised or the liability is settled, based on tax rates enacted or substantively enacted at the end of the reporting date. Their measurement also reflects the manner in which management expects to recover or settle the carrying amount of the related asset or liability.

Deferred tax assets relating to temporary differences and unused tax losses are recognised only to the extent that it is probable that future taxable profit will be available against which the benefits of the deferred tax asset can be utilised.

Where temporary differences exist in relation to investments in subsidiaries, branches, associates, and joint ventures, deferred tax assets and liabilities are not recognised where the timing of the reversal of the temporary difference can be controlled and it is not probable that the reversal will occur in the foreseeable future.

Current tax assets and liabilities are offset where a legally enforceable right of set-off exists and it is intended that net settlement or simultaneous realisation and settlement of the respective asset and liability will occur. Deferred tax assets and liabilities are offset where a legally enforceable right of set-off exists, the deferred tax assets and liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities where it is intended that net settlement or simultaneous realisation and settlement of the respective asset and liability will occur in future periods in which significant amounts of deferred tax assets or liabilities are expected to be recovered or settled.

(b) Fair Value of Assets and Liabilities The Company measures some of its assets and liabilities at fair value on either a recurring or non-recurring basis, depending on the requirements of the applicable Accounting Standard.

Fair value is the price the Company would receive to sell an asset or would have to pay to transfer a liability in an orderly (i.e. unforced) transaction between independent, knowledgeable and willing market participants at the measurement date.

As fair value is a market-based measure, the closest equivalent observable market pricing information is used to determine fair value. Adjustments to market values may be made having regard to the characteristics of the specific asset or liability. The fair values of assets and liabilities that are not traded in an active market are determined using one or more valuation techniques. These valuation techniques maximise, to the extent possible, the use of observable market data.

To the extent possible, market information is extracted from either the principal market for the asset or liability (i.e. the market with the greatest volume and level of activity for the asset or liability) or, in the absence of such a market, the most advantageous market available to the entity at the end of the reporting period (i.e. the market that maximises the receipts from the sale of the asset or minimises the payments made to transfer the liability, after taking into account transaction costs and transport costs).

18

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

Deferred tax assets and liabilities are calculated at the tax rates that are expected to apply to the period when the asset is realised or the liability is settled, based on tax rates enacted or substantively enacted at the end of the reporting date. Their measurement also reflects the manner in which management expects to recover or settle the carrying amount of the related asset or liability.

Deferred tax assets relating to temporary differences and unused tax losses are recognised only to the extent that it is probable that future taxable profit will be available against which the benefits of the deferred tax asset can be utilised.

Where temporary differences exist in relation to investments in subsidiaries, branches, associates, and joint ventures, deferred tax assets and liabilities are not recognised where the timing of the reversal of the temporary difference can be controlled and it is not probable that the reversal will occur in the foreseeable future.

Current tax assets and liabilities are offset where a legally enforceable right of set-off exists and it is intended that net settlement or simultaneous realisation and settlement of the respective asset and liability will occur. Deferred tax assets and liabilities are offset where a legally enforceable right of set-off exists, the deferred tax assets and liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities where it is intended that net settlement or simultaneous realisation and settlement of the respective asset and liability will occur in future periods in which significant amounts of deferred tax assets or liabilities are expected to be recovered or settled.

(b) Fair Value of Assets and Liabilities The Company measures some of its assets and liabilities at fair value on either a recurring or non-recurring basis, depending on the requirements of the applicable Accounting Standard.

Fair value is the price the Company would receive to sell an asset or would have to pay to transfer a liability in an orderly (i.e. unforced) transaction between independent, knowledgeable and willing market participants at the measurement date.

As fair value is a market-based measure, the closest equivalent observable market pricing information is used to determine fair value. Adjustments to market values may be made having regard to the characteristics of the specific asset or liability. The fair values of assets and liabilities that are not traded in an active market are determined using one or more valuation techniques. These valuation techniques maximise, to the extent possible, the use of observable market data.

To the extent possible, market information is extracted from either the principal market for the asset or liability (i.e. the market with the greatest volume and level of activity for the asset or liability) or, in the absence of such a market, the most advantageous market available to the entity at the end of the reporting period (i.e. the market that maximises the receipts from the sale of the asset or minimises the payments made to transfer the liability, after taking into account transaction costs and transport costs).

19

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

For non-financial assets, the fair value measurement also takes into account a market participant’s ability to use the asset in its highest and best use or to sell it to another market participant that would use the asset in its highest and best use.

The fair value of liabilities and the entity’s own equity instruments may be valued, where there is no observable market price in relation to the transfer of such financial instrument, by reference to observable market information where such instruments are held as assets. Where this information is not available, other valuation techniques are adopted and, where significant, are detailed in the respective note to the financial statements.

(c) Property, Plant and EquipmentEach class of property, plant and equipment is carried at cost or fair value as indicated less, where applicable, any accumulated depreciation and impairment losses.

Irrigation SystemsThe irrigation systems comprising channels, water control structures and associated assets are recorded at fair value.

Fair value is determined by an independent valuation estimating the replacement cost of the irrigation systems less, where applicable, subsequent depreciation and impairment losses.

Revaluation adjustments are made against asset revaluation reserves, where appropriate.

PropertyFreehold land and buildings are measured on the cost basis less depreciation and impairment losses for buildings.

Plant and EquipmentPlant and equipment are measured on the cost basis and are therefore carried at cost less accumulated depreciation and any accumulated impairment losses. In the event the carrying amount of plant and equipment is greater than the estimated recoverable amount, the carrying amount is written down immediately to the estimated recoverable amount and impairment losses are recognised either in profit or loss or as a revaluation decrease if the impairment losses relate to a revalued asset. A formal assessment of recoverable amount is made when impairment indicators are present.

Subsequent costs are included in the assets carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Company and the cost of the item can be measured reliably. All other repairs and maintenance are recognised as expenses in the statement of profit or loss and other comprehensive income during the financial period in which they are incurred.

DepreciationThe depreciable amount of all fixed assets including buildings but excluding freehold land is depreciated on a straight line basis over their useful lives to the Company commencing from the time the asset is held ready for use.

19

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

For non-financial assets, the fair value measurement also takes into account a market participant’s ability to use the asset in its highest and best use or to sell it to another market participant that would use the asset in its highest and best use.

The fair value of liabilities and the entity’s own equity instruments may be valued, where there is no observable market price in relation to the transfer of such financial instrument, by reference to observable market information where such instruments are held as assets. Where this information is not available, other valuation techniques are adopted and, where significant, are detailed in the respective note to the financial statements.

(c) Property, Plant and EquipmentEach class of property, plant and equipment is carried at cost or fair value as indicated less, where applicable, any accumulated depreciation and impairment losses.

Irrigation SystemsThe irrigation systems comprising channels, water control structures and associated assets are recorded at fair value.

Fair value is determined by an independent valuation estimating the replacement cost of the irrigation systems less, where applicable, subsequent depreciation and impairment losses.

Revaluation adjustments are made against asset revaluation reserves, where appropriate.

PropertyFreehold land and buildings are measured on the cost basis less depreciation and impairment losses for buildings.

Plant and EquipmentPlant and equipment are measured on the cost basis and are therefore carried at cost less accumulated depreciation and any accumulated impairment losses. In the event the carrying amount of plant and equipment is greater than the estimated recoverable amount, the carrying amount is written down immediately to the estimated recoverable amount and impairment losses are recognised either in profit or loss or as a revaluation decrease if the impairment losses relate to a revalued asset. A formal assessment of recoverable amount is made when impairment indicators are present.

Subsequent costs are included in the assets carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Company and the cost of the item can be measured reliably. All other repairs and maintenance are recognised as expenses in the statement of profit or loss and other comprehensive income during the financial period in which they are incurred.

DepreciationThe depreciable amount of all fixed assets including buildings but excluding freehold land is depreciated on a straight line basis over their useful lives to the Company commencing from the time the asset is held ready for use.

20

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

The depreciation rates used for each class of depreciable assets are:

Class of Fixed Asset Depreciation RateBuildings 2.5%Irrigation Assets

– Piping Assets 1%– Channelled Assets 2.5%

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each reporting period.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.

Gains and losses on disposals are determined by comparing proceeds with the carrying amount. These gains or losses are included in the statement of profit or loss and other comprehensive income. When revalued assets are sold, amounts included in the revaluation surplus relating to that asset are transferred to retained earnings.

(d) Financial InstrumentsInitial Recognition and MeasurementFinancial assets and financial liabilities are recognised when the entity becomes a party to the contractual provisions of the instrument. For financial assets, this is equivalent to the date that the Company commits itself to either purchase or sell the asset (i.e. trade date accounting is adopted).

Financial instruments are initially measured at fair value plus transaction costs, except where the instrument is classified ‘at fair value through profit or loss’ in which case transaction costs are expensed to profit or loss immediately.

Classification and Subsequent MeasurementFinancial instruments are subsequently measured at either fair value, amortised cost using the effective interest rate method or cost. Fair value represents the amount for which an asset could be exchanged or a liability settled, between knowledgeable, willing parties. Where available, quoted prices in an active market are used to determine fair value. In other circumstances valuation techniques are adopted.

Amortised cost is calculated as the amount at which the financial asset or financial liability is measured at initial recognition less principal repayments and any reduction for impairment, and then adjusted for any cumulative amortisation of the difference between the initial amount and the maturity amount calculated using the effective interest rate method.

The effective interest method is used to allocate interest income or interest expense over the relevant period and is equivalent to the rate that exactly discounts estimated future cash payments or receipts (including fees, transaction costs and other premiums or discounts) through the expected life (or when this cannot be reliably predicted, the contractual term) of the financial instrument to the net carrying amount of the financial asset or financial liability. Revisions to expected future net cash flows will necessitate an adjustment to the carrying value with a consequential recognition of an income or expense in profit or loss.

20

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

The depreciation rates used for each class of depreciable assets are:

Class of Fixed Asset Depreciation RateBuildings 2.5%Irrigation Assets

– Piping Assets 1%– Channelled Assets 2.5%

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each reporting period.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.

Gains and losses on disposals are determined by comparing proceeds with the carrying amount. These gains or losses are included in the statement of profit or loss and other comprehensive income. When revalued assets are sold, amounts included in the revaluation surplus relating to that asset are transferred to retained earnings.

(d) Financial InstrumentsInitial Recognition and MeasurementFinancial assets and financial liabilities are recognised when the entity becomes a party to the contractual provisions of the instrument. For financial assets, this is equivalent to the date that the Company commits itself to either purchase or sell the asset (i.e. trade date accounting is adopted).

Financial instruments are initially measured at fair value plus transaction costs, except where the instrument is classified ‘at fair value through profit or loss’ in which case transaction costs are expensed to profit or loss immediately.

Classification and Subsequent MeasurementFinancial instruments are subsequently measured at either fair value, amortised cost using the effective interest rate method or cost. Fair value represents the amount for which an asset could be exchanged or a liability settled, between knowledgeable, willing parties. Where available, quoted prices in an active market are used to determine fair value. In other circumstances valuation techniques are adopted.

Amortised cost is calculated as the amount at which the financial asset or financial liability is measured at initial recognition less principal repayments and any reduction for impairment, and then adjusted for any cumulative amortisation of the difference between the initial amount and the maturity amount calculated using the effective interest rate method.

The effective interest method is used to allocate interest income or interest expense over the relevant period and is equivalent to the rate that exactly discounts estimated future cash payments or receipts (including fees, transaction costs and other premiums or discounts) through the expected life (or when this cannot be reliably predicted, the contractual term) of the financial instrument to the net carrying amount of the financial asset or financial liability. Revisions to expected future net cash flows will necessitate an adjustment to the carrying value with a consequential recognition of an income or expense in profit or loss.

21

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

Fair value is determined based on current bid prices for all quoted investments. Valuationtechniques are applied to determine the fair value for all unlisted securities, including recent arms’ length transactions, reference to similar instruments and option pricing models.

(i) Financial Assets at Fair Value through Profit or LossFinancial assets are classified at ‘fair value through profit or loss’ when they are either held for trading for the purpose of short term profit taking, derivatives not held for hedging purposes, or when they are designated as such to avoid an accounting mismatch or enable performance evaluation where a group of financial assets is managed by key management personnel on a fair value basis in accordance with a documented risk management or investment strategy. Such assets are subsequently measured at fair value with changes in carrying value being included in profit or loss.

(ii) Loans and ReceivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market and are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss through the amortisation process and when the financial asset is derecognised.

(iii) Held-to-maturity InvestmentsHeld-to-maturity investments are non-derivative financial assets that have fixed maturities and fixed or determinable payments, and it is the Company’s intention to hold these investments to maturity. They are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss through the amortisation process and when the financial asset is derecognised.

(iv) Available-for-sale Financial AssetsAvailable-for-sale financial assets are non-derivative financial assets that are either not capable of being classified into other categories of financial assets due to their nature or they are designated as such by management. They comprise investments in the equity of other entities where there is neither a fixed maturity nor fixed or determinable payments.

They are subsequently measured at fair value with any remeasurements other than impairment losses and foreign exchange gains and losses recognised in other comprehensive income. When the financial asset is derecognised, the cumulative gain or loss pertaining to that asset previously recognised in other comprehensive income is reclassified into profit or loss.

Available-for-sale financial assets are included in non-current assets, except for those which are expected to be disposed of within 12 months after the end of the reporting period, which will be classified as current assets.

(v) Financial Liabilities Non-derivative financial liabilities (excluding financial guarantees) are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss through the amortisation process and when the financial asset is derecognised.

21

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

Fair value is determined based on current bid prices for all quoted investments. Valuationtechniques are applied to determine the fair value for all unlisted securities, including recent arms’ length transactions, reference to similar instruments and option pricing models.

(i) Financial Assets at Fair Value through Profit or LossFinancial assets are classified at ‘fair value through profit or loss’ when they are either held for trading for the purpose of short term profit taking, derivatives not held for hedging purposes, or when they are designated as such to avoid an accounting mismatch or enable performance evaluation where a group of financial assets is managed by key management personnel on a fair value basis in accordance with a documented risk management or investment strategy. Such assets are subsequently measured at fair value with changes in carrying value being included in profit or loss.

(ii) Loans and ReceivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market and are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss through the amortisation process and when the financial asset is derecognised.

(iii) Held-to-maturity InvestmentsHeld-to-maturity investments are non-derivative financial assets that have fixed maturities and fixed or determinable payments, and it is the Company’s intention to hold these investments to maturity. They are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss through the amortisation process and when the financial asset is derecognised.

(iv) Available-for-sale Financial AssetsAvailable-for-sale financial assets are non-derivative financial assets that are either not capable of being classified into other categories of financial assets due to their nature or they are designated as such by management. They comprise investments in the equity of other entities where there is neither a fixed maturity nor fixed or determinable payments.

They are subsequently measured at fair value with any remeasurements other than impairment losses and foreign exchange gains and losses recognised in other comprehensive income. When the financial asset is derecognised, the cumulative gain or loss pertaining to that asset previously recognised in other comprehensive income is reclassified into profit or loss.

Available-for-sale financial assets are included in non-current assets, except for those which are expected to be disposed of within 12 months after the end of the reporting period, which will be classified as current assets.

(v) Financial Liabilities Non-derivative financial liabilities (excluding financial guarantees) are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss through the amortisation process and when the financial asset is derecognised.

22

SOUTH WEST IRRIGATION ASSET COOPERATIVE LIMITED

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2016

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES (Cont)

ImpairmentAt the end of each reporting period, the Company assesses whether there is objective evidence that a financial instrument has been impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events (a “loss event”) having occurred, which has an impact on the estimated future cash flows of the financial asset(s).

In the case of available-for-sale financial instruments, a significant or prolonged decline in the market value of the instrument is considered to constitute a loss event. Impairment losses are recognised in profit or loss immediately. Also, any cumulative decline in fair value previously recognised in other comprehensive income is reclassified to profit and loss at this point.