Embed Size (px)

Citation preview

ANNUAL REPORT15 April - 31 December 2017

Strategic report

Overview

Business model 4

Our mission 6

Strategic summary 8

Chief Executive's Review 10

Health and Safety

Safety record 18

Approach 21

Strategy in action

UK and Ireland Fuels 32

International Fuels 42

Global Biofuels 50

Infrastructure 56

Market review

Global markets 24

UK and Irish markets 25

Biofuel markets 26

Brazilian market 28

Canadian market 29

Middle Eastern market 30

1

3

4

5

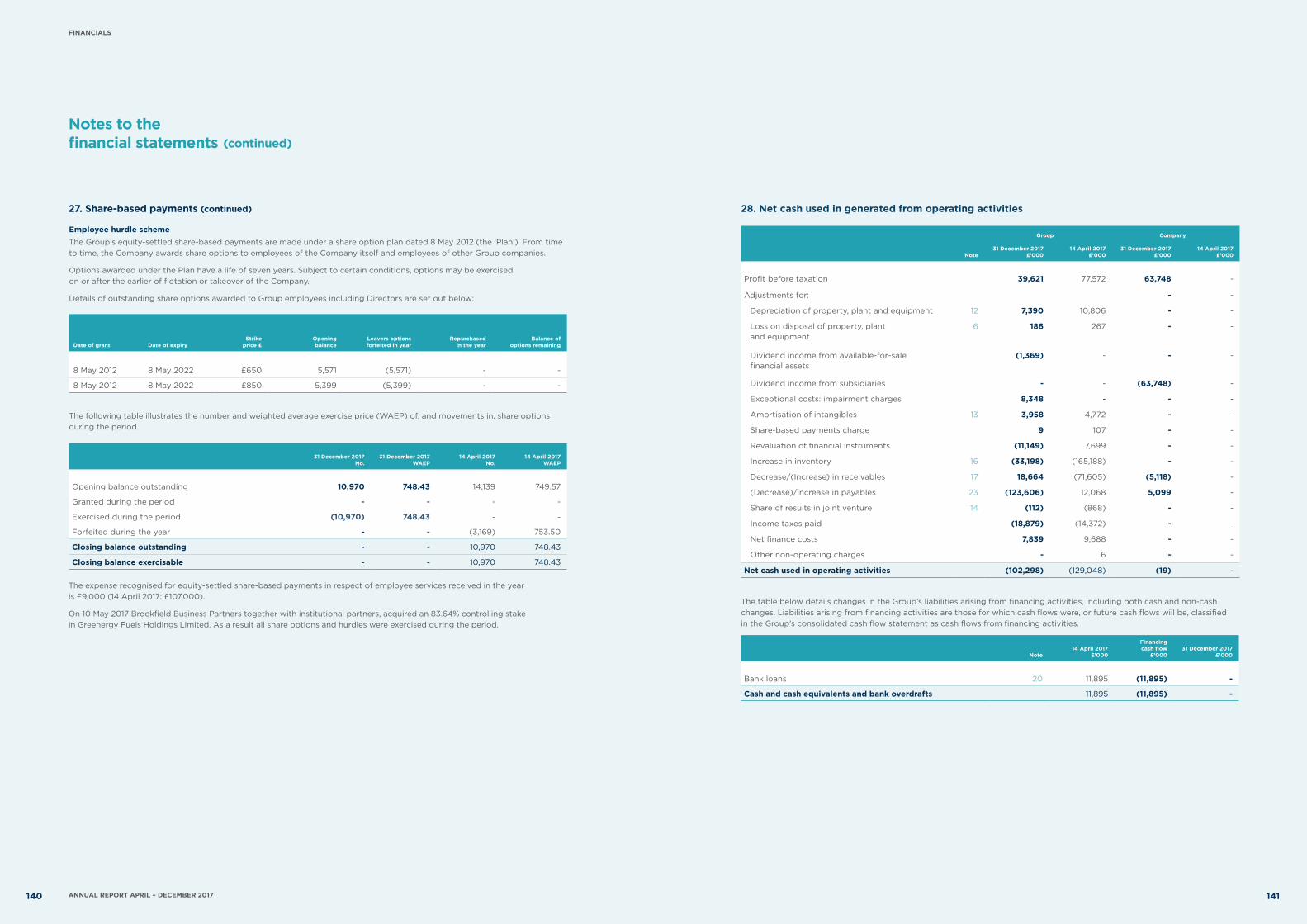

2

2 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGIC REPORT » CONTENTS

Following a change in our financial year, this report relates to the 37 week period from 15 April – 31 December 2017.

Key performance indicators

Financial KPIs 63

Operational KPIs 65

Enviromental KPIs 66

Service quality KPIs 67

Managing our risks

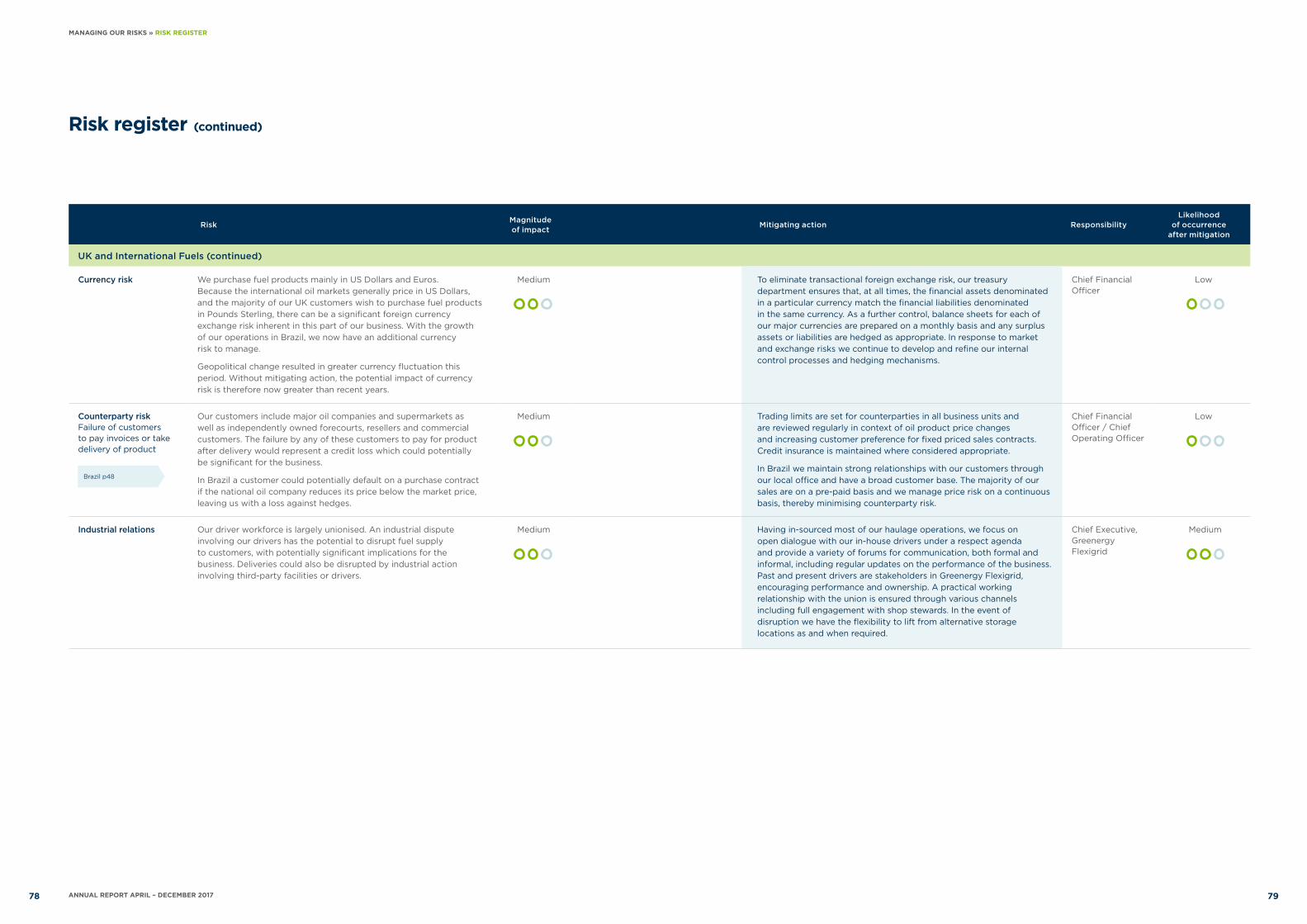

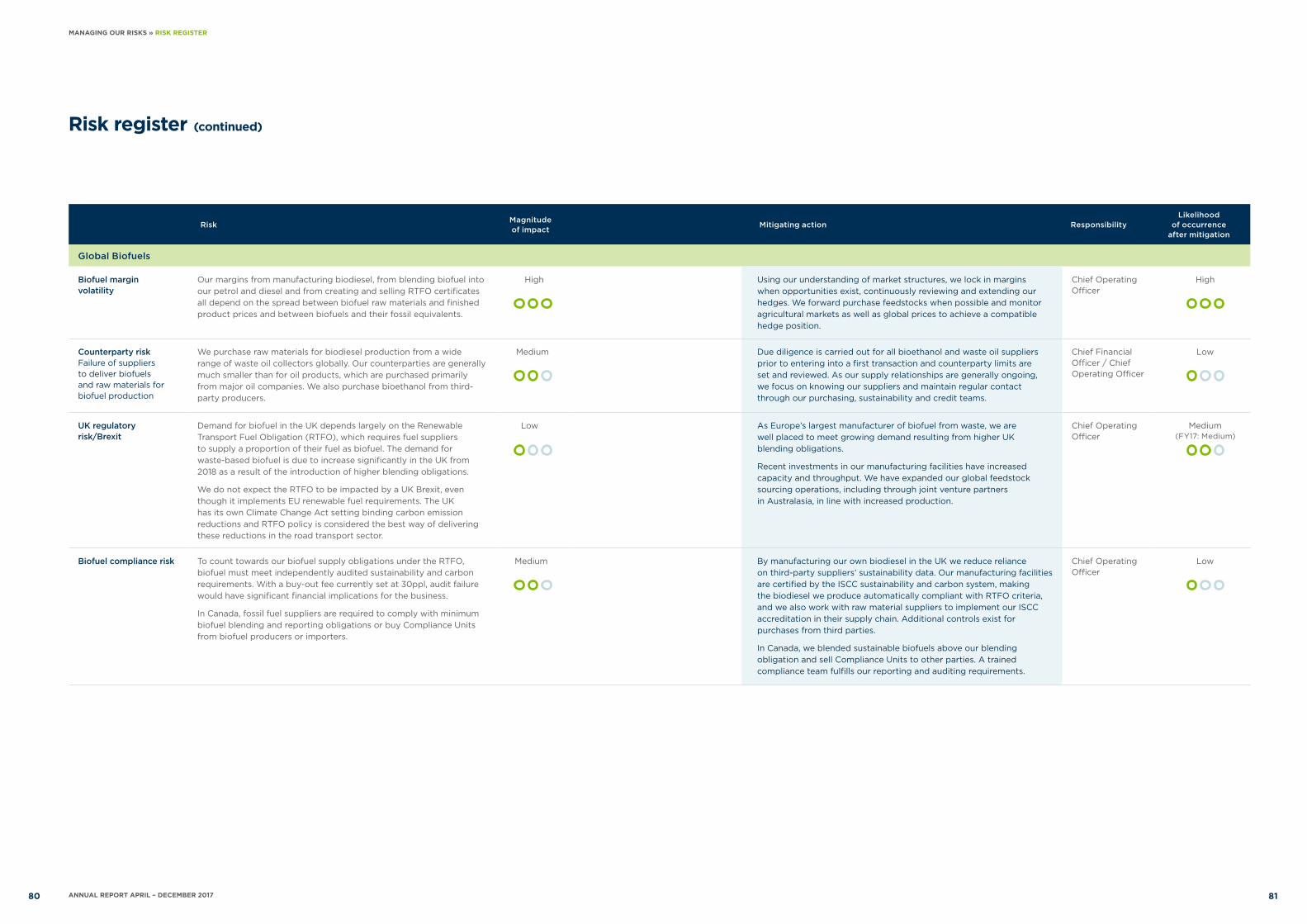

Risk overview 73

Risk register 74

People and environment

Executive Directors 84

Employment 86

Biofuel sustainability 88

Carbon emissions 90

Directors' reports

Strategic report 92

Directors’ report 94

Chief Financial Officer's Review 68

8

10 11

97

6

3

Financials

Independent auditors’ report 98

Consolidated income statement 100

Consolidated statement 101 of comprehensive income

Consolidated and 102 Company balance sheets

Consolidated statement 104 of changes in equity

Company statement 105 of changes in equity

Consolidated and Company 106 statements of cash flows

Notes to the financial 107statements

Officers and 147professional advisors

Registered offices 148

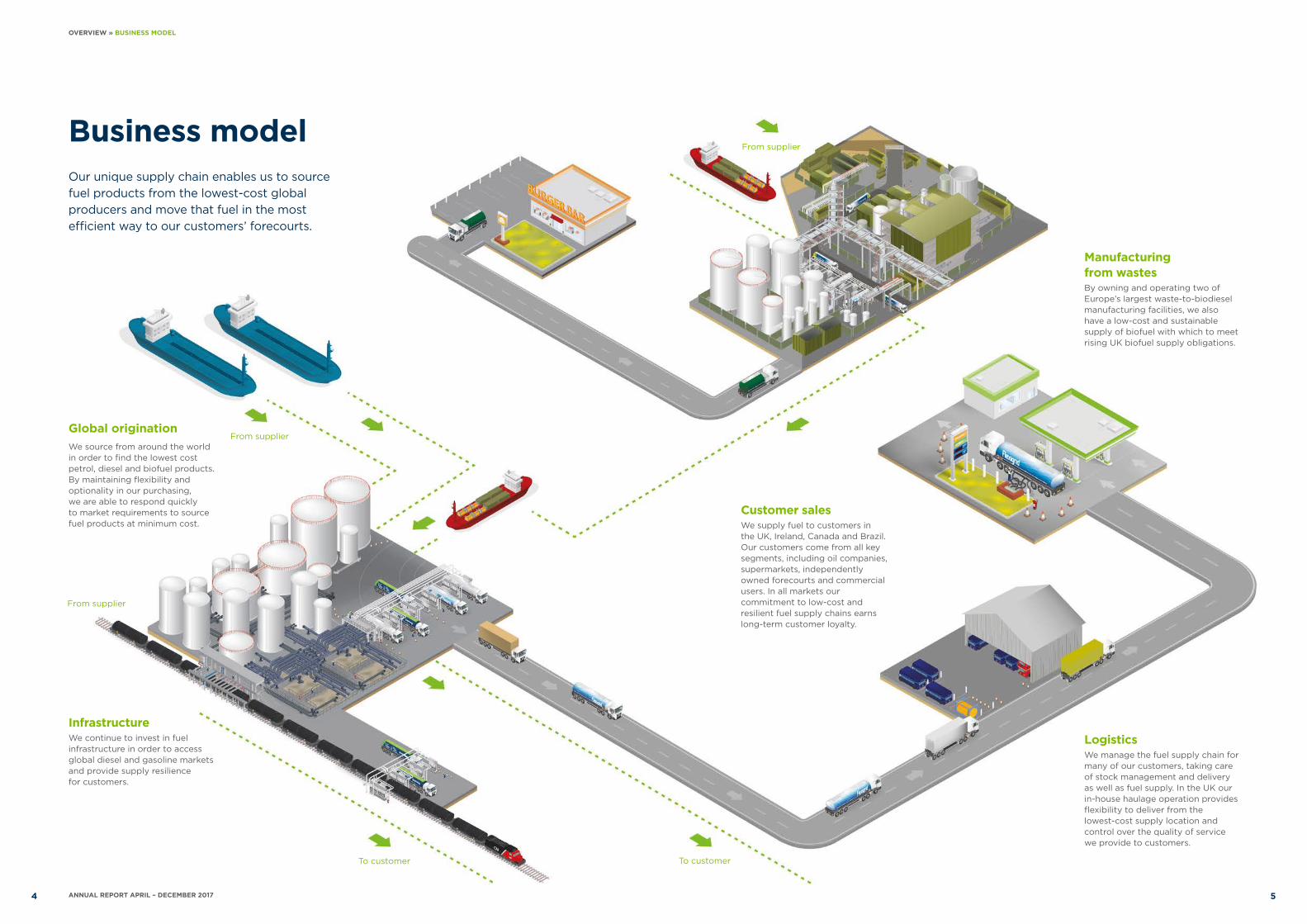

Business modelOur unique supply chain enables us to source fuel products from the lowest-cost global producers and move that fuel in the most efficient way to our customers’ forecourts.

Global originationWe source from around the world in order to find the lowest cost petrol, diesel and biofuel products. By maintaining flexibility and optionality in our purchasing, we are able to respond quickly to market requirements to source fuel products at minimum cost.

Infrastructure We continue to invest in fuel infrastructure in order to access global diesel and gasoline markets and provide supply resilience for customers.

From supplier

To customer

Manufacturing from wastesBy owning and operating two of Europe’s largest waste-to-biodiesel manufacturing facilities, we also have a low-cost and sustainable supply of biofuel with which to meet rising UK biofuel supply obligations.

Customer salesWe supply fuel to customers in the UK, Ireland, Canada and Brazil. Our customers come from all key segments, including oil companies, supermarkets, independently owned forecourts and commercial users. In all markets our commitment to low-cost and resilient fuel supply chains earns long-term customer loyalty.

LogisticsWe manage the fuel supply chain for many of our customers, taking care of stock management and delivery as well as fuel supply. In the UK our in-house haulage operation provides flexibility to deliver from the lowest-cost supply location and control over the quality of service we provide to customers.

To customer

From supplier

From supplier

54 ANNUAL REPORT APRIL – DECEMBER 2017

OVERVIEW » BUSINESS MODEL

Our missionTo deliver long-term customer partnerships by being the fuel provider with the:

» Lowest-cost» Highest reliability» Best systems and control» Easiest people to deal with» Most transparency

Navigator Terminals | Thames, UK

76 ANNUAL REPORT APRIL – DECEMBER 2017

OVERVIEW » OUR MISSION

Strategic summary

International Fuels

UK and Ireland Fuels p32

UK and Ireland Fuels

Our aim

Develop low-cost and resilient fuel supply chains to earn the long-term loyalty of our customers in the UK and Ireland

Highlights:

» Acquisition of Inver Energy, giving us a business in Ireland for the first time and access to the Inver retail brand

» Opening of Thames Oilport for diesel supply, creating capacity and resilience in the busy South East Region

» Further growth in sales to independent forecourt operators, including under our Branded Wholesaler agreement with Esso in the UK, and to other delivered-in customers.

Our aim

Expand by replicating our UK success in other markets

Highlights:

» In Canada, acquisition of the CAN-OP fuel business in Northern Ontario, expanding our existing supply footprint into a new region

» Also in Canada, continued expansion of our supply chain capability to enable sourcing from North America by rail and Europe by sea, giving us supply chain optionality and the ability to ensure year-round product availability for customers

» Further growth in our diesel imports into Brazil

» Successful first period of commercial operations by our petrol blending joint venture in Bahrain.

Global Biofuels Infrastructure

Our aim

Create value from biofuel manufacturing and supply

Highlights:

» Continued growth in our biodiesel manufacturing output as a result of investments in incremental process improvements

» Further extension of our raw material supply chains, particularly outside Europe, to allow for sourcing of waste oils with particular quality characteristics or in smaller containers

» Growth in sales of biofuel and UK Renewable Transport Fuel Certificates to other oil companies.

Our aim

Acquire, regenerate and operate assets that support our supply chain objectives

Highlights:

» Successful start to diesel throughput and supply at Thames Oilport in the UK

» Also in the UK, completion of a diesel pipeline linking our various Teesside facilities and expansion of a jetty pipeline on the Thames, creating cost and operational efficiencies

» Purchase of a 50% share of the AFSC terminal at Foynes, a deep-water multi-product terminal on the west coast of Ireland, as part of our acquisition of Inver Energy

» In Canada, acquisition of the CAN-OP rail-fed facility at Thunder Bay and completion of works to double the size of our first rail-to-road supply location in Toronto.

International Fuels p42

Global Biofuels p50

Infrastructure p56

98 ANNUAL REPORT APRIL – DECEMBER 2017 9

OVERVIEW » STRATEGIC SUMMARY

The increase in biofuel supply obligations in the UK represents a significant development for the business. Our investments in biodiesel manufacturing facilities and raw material supply chains position us well to meet the rapidly growing requirement for waste-based biofuel.

"The business continued to perform to expectation in this 37 week period. We expanded our international businesses both organically and through acquisition and grew delivered-in sales in the UK. Our biodiesel manufacturing operation made a particularly strong contribution following investment in incremental process improvements. "Andrew OwensChief Executive

Chief Executive's Review

Safety, Health, Environment and Quality

Our approach to safety is underpinned by open and honest reporting and sharing of event learnings across the business. With this awareness, we are best placed to take effective action to prevent future events.

A particular priority this period was to address the rate of RIDDOR1 reportable injuries resulting from manual-handling or slips by drivers, which had increased in FY17. We introduced more targeted training, including our own video, which resulted in a significant reduction in this type of injury this period.

As we expand internationally, we are introducing our safety culture to employees who are new to the business and providing training and auditing for our international businesses.

Markets

The most significant market change this period was the introduction of new legislation in the UK to increase biofuel supply obligations, which we expect will support the continued strong performance of our biofuels business. Effective April 2018, the percentage of biofuel that UK fuel suppliers are required to blend into their petrol and diesel increased from 4.75% to 7.25%, with further rises legislated for in subsequent years. With new caps on supply of crop-based biofuel, these higher obligations will be met primarily from waste-based biofuel of the kind we manufacture in the UK. This will create important new supply and margin opportunities.

Global demand for diesel continued to rise as a result of world economic growth. With OPEC maintaining its production restrictions, diesel stocks started to deplete this period, exacerbated by hurricanes in the latter half of 2017.

As a result, diesel markets tightened and returned to backwardated market conditions. Therefore, we sold out the diesel we were holding in long-term storage at Thames Oilport and on Teesside.

In the UK, road fuel demand remained flat and surprisingly dieselisation continued, with diesel demand rising 1.0% in the 2017 calendar year and gasoline demand falling by 1.9%. We expect this trend to reverse as a result of Government plans to improve air quality by curbing the use of diesel vehicles, which in calendar year 2017 resulted in a fall in new diesel car registrations.

Health and Safety p17

Market review p23

Boardroom | London, UK

EBITDA2

£67.2m

KPI

(excluding exceptionals for 37 week period)

1 www.hse.gov.uk/riddor2 Earnings before interest, taxation, depreciation and amortisation

1110 ANNUAL REPORT APRIL – DECEMBER 2017

CHIEF EXECUTIVE'S REVIEW

Chief exec reviewKPI: EBITDA

(excluding exceptionals)

20130

80

60

2014 2015

100

£ (

mill

ion

)

20

40

2016 2017

67.2

30.9

20.5

47.6

17.6 89.2

23.3

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

Chief exec reviewKPI: Global sales volume

pg 12

20130

20

15

10

2014 2015

5

2016 2017

14.4

5.3

17.6 19.1

Bill

ion

litr

es

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

15.1 15.5

Results

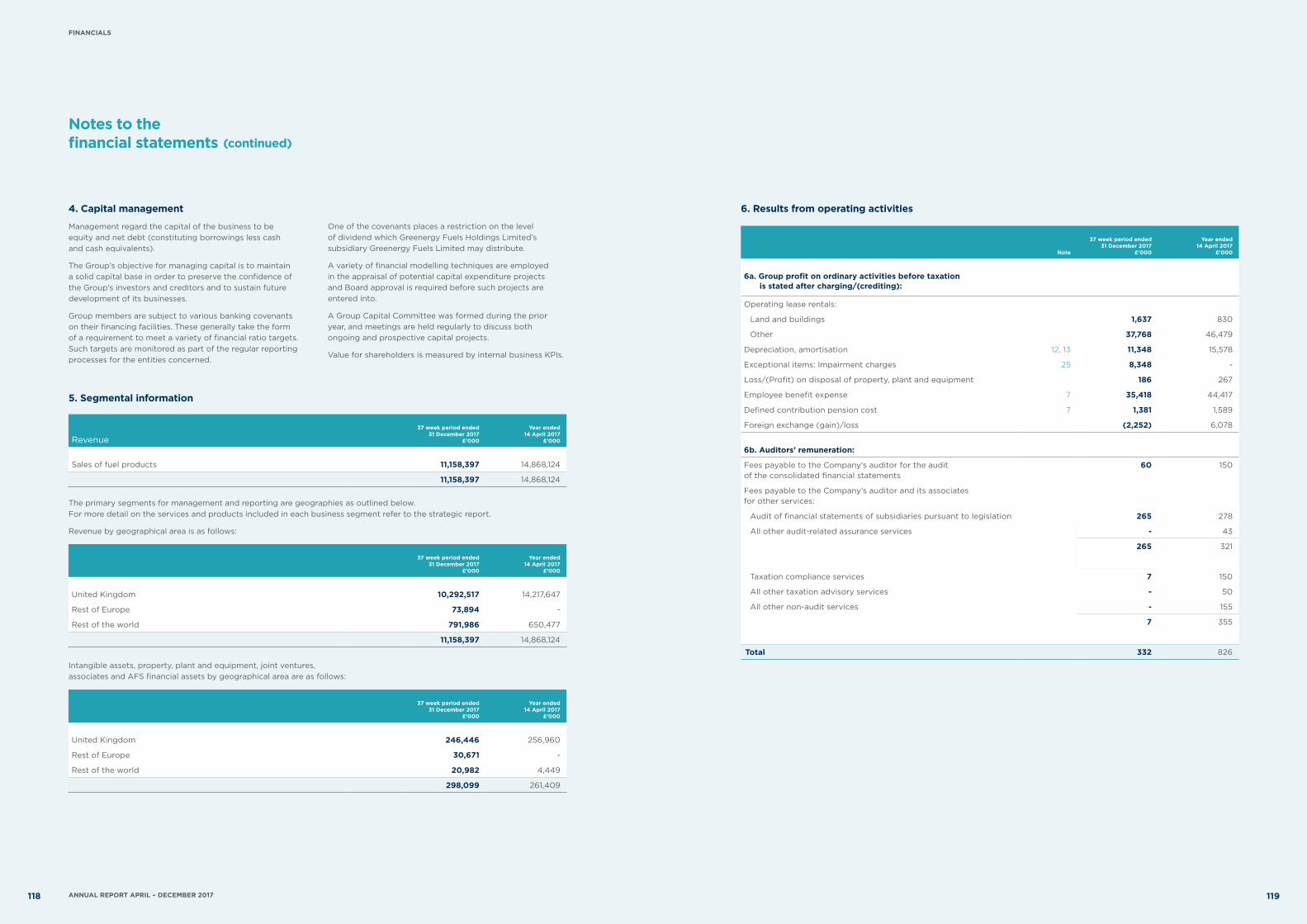

Our results were affected by the change in year-end from 15 April to 31 December resulting in a shorter 37 week trading period.

EBITDA1 amounted to £67.2 million for the 37 week period from 15 April 2017 to 31 December 2017 (equivalent period in 2016: £70.6m). Profit before tax and before exceptionals totalled £48.0m (equivalent period in 2016: £56.4m). The most significant impact on performance was from:

» Volume growth in our biodiesel production, combined with stronger manufacturing margins achieved by supply chain diversification and efficiency and reliability improvements

» Strong but transient margins for imports into Brazil

» Lower UK diesel margins in tighter market conditions following hurricanes in the latter half of 2017.

Chief Financial Officer’s Review p68

Financial KPIs p63

Thames Oilport | UK

KPI: EBITDA (excluding exceptionals)

KPI: Global sales volume

1 Earnings before interest, taxation, depreciation and amortisation

1312 ANNUAL REPORT APRIL – DECEMBER 2017

CHIEF EXECUTIVE'S REVIEW » RESULTS

Chief exec reviewFuel sales by region

15 April -31 December

UK and Ireland

Brazil

Canada

84% 12%4%

Fuel sales by region 15 April 2017 – 31 December 2017

International FuelsWe continue to use our UK experience and capabilities to expand in new markets.

In Canada, we are developing flexible supply chains and investing in infrastructure in order to provide low-cost fuel to our customers, using sea and rail access to deliver supply resilience throughout the year. Our acquisition of CAN-OP, a fuel marketer and terminal operator in Northern Ontario, gives us an additional rail-fed distribution location in the growing Ontario fuels market. We also completed the development of the Breakaway retail brand offer and commenced roll-out of the concept to Canadian dealers. With developments both in our supply chain and our customer offer, we are well positioned for further growth in Canada.

The Brazilian market increased its reliance on fuel imports, creating ongoing, but transient, supply opportunities for us in Brazil. We expanded our diesel supply into Brazil and towards the end of the period made our first gasoline imports, building on our reputation as a trusted trading counterparty.

In the Middle East, we are part of Bahrain Gasoline Blending (BGB), a strategic joint venture between nogaholding, Bapco (the national oil company of Bahrain) and Greenergy. This period, BGB successfully blended gasoline to meet domestic Bahraini demand and made its first export cargo. The joint venture is evaluating engineering works to expand and enhance the gasoline blending facilities in Bahrain to give greater trading capability and flexibility.

International Fuels p42

This period we made three acquisitions, taking over Inver Energy in the UK and Ireland, CAN-OP in Canada and concluding a waste oil origination joint venture in Australia. Each of these transactions was originated through our industry relationships.

Strategy

UK and Ireland FuelsIn the UK, strong refining margins resulted in highly competitive market conditions. However, we continued to grow, delivered-in sales to commercial and retail customers, including as part of our branded wholesaler agreement with Esso. The number of independent forecourt sites we were contracted to supply increased organically to 521 at the end of the period, up 32% from April 2017. As we earn trust and respect in the sector as a flexible and high service fuel supplier, we won new business from all competing brands.

In line with the growth of our delivered-in business, we expanded our in-house haulage capability within Greenergy Flexigrid, recruiting additional drivers and extending our fleet to minimise our reliance on sub-contractors.

We were pleased to acquire Inver Energy’s fuel infrastructure and supply businesses, giving us a supply footprint in Ireland for the first time. Inver’s business model is very similar to Greenergy’s, based on importing lowest-cost products and staying close to customers. Inver has its own retail brand in Ireland and we intend to offer the brand to retail dealers in other markets.

Our UK margins were affected by a tightening of the global diesel market and a return to backwardated market conditions. One-off costs were also created as a result of third-party damage to one of our busiest jetties on the Thames, which severely restricted downwards the size of ships that could use the jetty. As smaller ships cost more to operate, this resulted in higher product and shipping-related costs for the business, but our ability to maintain continuous supply through this period is evidence of the supply resilience we offer to customers.

Partially offsetting the Thames jetty issue, we commissioned two new product pipelines. The first links the deep-water jetty at our North Tees facility with our other terminals on Teesside, allowing large and lower cost diesel ships to supply all terminals. The other, on the Thames, allows gasoline ships to discharge at much higher rates, cutting jetty time and demurrage bills.

UK and Ireland Fuels p32

Chief Executive's Review (continued)

1514 ANNUAL REPORT APRIL – DECEMBER 2017

CHIEF EXECUTIVE'S REVIEW

Health and Safety3

Global BiofuelsDemand for waste-based biofuel increased significantly in the UK from April 2018 as a result of the introduction of higher blending obligations. In anticipation of these higher mandates we have been working to increase our production of biodiesel from waste through a variety of incremental expansion investments at our manufacturing facilities. Our biodiesel output was 26% higher this period compared with the same period in 2016.

We also invested further in upstream raw material supply chains, including through a new joint venture in Australia, in order to access growing volumes of feedstock with quality characteristics best suited to our manufacturing facilities. We have been particularly successful in moving used cooking oil from Asia to the UK and we plan more investments in this area.

InfrastructureWe continue to make strategic infrastructure investments to support our fuel supply objectives.

In the UK, we opened Thames Oilport for diesel supply by truck having regenerated former refinery infrastructure for use as an import terminal. This gives us a second supply location on the Thames and deep-water import capability. Through the acquisition of Inver Energy we also now own a share of the Foynes terminal in Ireland and 100% of the Cardiff terminal in the UK.

We also made strong progress towards realising the value of the substantial surplus land associated with Thames Enterprise Park, which uses land not required for Thames Oilport. Our first land disposals were ahead of expectation and the permitting process for land development gained strong momentum.

In Canada, we completed works to double the size of our first rail-to-road supply location in Toronto, creating additional capacity at a location that is convenient for customers. Following our acquisition of the CAN-OP business in Northern Ontario, we plan to refurbish and expand the Thunder Bay fuel terminal in order to benefit from its position at a key petroleum supply/trading intersection.

OwnershipFollowing the investment by Brookfield Business Partners which completed in May 2017, Greenergy Fuels Holdings is now a Brookfield subsidiary. The Executive Directors of Greenergy Fuels Holdings are unchanged and continue to run the business. The investment by Brookfield Business Partners increases our access to capital and allows us to participate in larger-scale strategic project and acquisition activities.

Outlook

Looking forward we expect to grow our supply to the UK independent forecourt sector and expand our Irish operations. We also see further opportunities within our global biofuels business, in our fuel supply operations in Canada and Brazil and in BGB, our joint venture in Bahrain, and we expect these areas to be the main recipients of our project capital expenditure going forward. We also remain active in seeking further bolt-on acquisition opportunities in both the petroleum and biofuel markets across the world.

Global Biofuels p50

Infrastructure p56

As we expand our biodiesel manufacturing operations in the UK, we are also investing upstream to source waste oils globally. This period we concluded a new joint venture partnership in Australia and expanded our joint venture operations in China.

Andrew OwensChief Executive

1716 ANNUAL REPORT APRIL – DECEMBER 2017

CHIEF EXECUTIVE'S REVIEW

Incident rate per 100,000 hours worked

FY17 (April 2016 to April 2017)

-

0.0 0.7

1.0

3.1

14.8

263.9

Fatalities

RIDDOR dangerous occurrences or injuries

Lost time injuries

Minor injuries

Near misses

Hazard observations

Safety record

Where we have gained important learning from events, that information is communicated across the business as part of our policy of prevention and continual improvement.

In the previous financial year we witnessed a rise in the rate of RIDDOR reportable injuries, primarily as a result of drivers sustaining injuries through manual-handling or slips.

This period, all injury rates have reduced. A contributing factor has been improved sharing of event learnings when significant injuries and events occur, to increase awareness and help prevent further events of the same kind.

There were three separate RIDDOR reportable injuries across the business this period:

» Two slip/trip/fall injuries to drivers

» One other injury to a driver.

There were no RIDDOR dangerous occurrences.

DEFINITIONS RIDDOR dangerous occurrence: an incident with a high potential to cause death or serious injury (as defined by the RIDDOR regulations).

RIDDOR injury: a specified major injury such as a fracture or serious burns, or an injury resulting in an absence from or restricted work for more than seven days.

Lost time injury: an injury resulting in an absence from work beyond the shift in which the injury was sustained.

Minor injury: an injury which is not RIDDOR reportable and does not require time off work or restricted work duties.

Near miss: an unplanned event that did not result in injury, illness, damage or non-compliance but which had the potential to do so.

Hazard observation: an ‘act’ or a ‘condition’ that has the potential to cause injury, loss or damage.

"We focus on continuous improvement in safety across the business, with our key message of Certainty, Curiosity and STOP reiterating personal accountability for safety. "Kolade AfuwapeHead of Process Integrity

Per 100,000 hours worked

15 April 2017 to 31 December 2017

-

- 0.3

0.8

2.5

7.2

243.8

RIDDOR events/injuries

Lost time injury

Minor injuries

Near misses

Hazard observations

Fatalities

1918 ANNUAL REPORT APRIL – DECEMBER 2017

HEALTH AND SAFETY » SAFETY RECORD

Case study

Learning from events

A large proportion of lost-time and RIDDOR reportable injuries in FY17 were related to manual handling issues amongst our drivers. We therefore created a bespoke training programme and video focused specifically on correct manual handling techniques for routine driver tasks such as draining and handling fuel delivery hoses. This has contributed to a marked reduction in lost-time injuries related to manual handling and has been positively received by drivers.

Customer forecourt | Bristol, UK

Approach

This period we made a number of international acquisitions. Our immediate focus has been the integration of our health and safety standards into these businesses.

Open and honest reporting

We maintain a strong reporting culture across all parts of the business, from high hazard operating sites and haulage operations to offices. We encourage observation and reporting of hazards, near misses and unwanted events, however small, without fear of blame.

By capturing information about hazards and incidents that might easily remain unnoticed, we aim to reduce risks and improve safe working practices. We have worked to ensure that new staff, contractors and businesses are rapidly introduced to the Greenergy culture of open and honest reporting.

Investigation and learning

A comprehensive central reporting system supports the detailed reporting and systematic investigation of each reported observation and unwanted event, so we can identify lessons to be learned from individual events and broader trends. We then act to correct issues that have potential to lead to injuries, asset damage, environmental impacts or significant business impact.

Where key lessons have been identified, a ‘Lesson Learned’ brief is produced and shared across the business via noticeboards, the intranet and toolbox talks. A monthly Flexigrid safety bulletin has also been introduced to share key learnings and performance with haulage staff and drivers.

International safety awareness

We recognise the importance of extending our strong SHEQ (Safety, Health, Environment and Quality) culture to all parts of our growing global business. We have developed and started to implement a long- term plan to extend SHEQ support, training and auditing to our international businesses. Gap assessments and audits have been introduced to gain a broad understanding of the existing SHEQ culture in new business areas. Based on this we have started a programme of training on safety awareness, hazard observations and Greenergy expectations for safety walks, event reporting and investigation in our international businesses.

Personal safety

2120 ANNUAL REPORT APRIL – DECEMBER 2017

HEALTH AND SAFETY » CASE STUDY

Safe operating standards

We continue to review, extend and improve our Safe Operating Standards to provide a structured and consistent approach to safety across all our operations.

Continual improvement of the standards is driven by the Process Integrity team. The team shares knowledge and experience from all parts of the business, including joint venture businesses and contract operators working on behalf of Greenergy, formally and informally through team and cross-site meetings, publications, intranet and management leadership.

Auditing

Group Process Integrity audits continued across all our operations, at all our own facilities and also at joint venture facilities. To ensure compliance with Greenergy performance requirements, we also capture third-party terminals and contract haulage operations within our audit programme.

This period, the full auditing plan was extended to include existing international operations and new acquisitions.

Where we have identified opportunities for improvement of facilities or processes, follow up audits take place to ensure recommendations have been implemented.

Emergency planning and exercise

Whilst our SHEQ management systems focus strongly on the prevention of unwanted events, we do recognise the potential for such events to occur and the need to be prepared for such eventualities.

We ensure that all of our facilities and business operations have effective emergency management plans in place and we review and test these plans on a regular basis. At a strategic level, the Group Crisis Management Plan is reviewed regularly. Following a recent review we have provided awareness information to refresh the whole Greenergy workforce on when and how to activate this plan.

Process safety Market review4

2322 ANNUAL REPORT APRIL – DECEMBER 2017

HEALTH AND SAFETY » APPROACH

1000

1500

2000

3000

3500

4000

2500mt

Dec 17Jan 17Jan 16Jan 15Jan 14Jan 13

Bill

ion

to

nn

es

2.25

2.05

1.45

1.25

1.85

1.65

2013 2014 20152011 2012 2016 2017

Diesel

Petrol

Mill

ion

to

nn

es

15

10

5

(5)

(10)

(15)

0

2005 2007 2009 2011 2013 2015 2017

Net imports

Net exports

Global markets

Global diesel demand growth was not offset by increased refinery production, and product stocks fell from their previous levels. Market structures changed as a result and we sold out our contango stocks.

The announcement of UK Government plans to curb the use of diesel vehicles did not immediately affect demand for UK diesel fuel.

Fuel products have been in plentiful supply over recent years, with diesel stocks reaching a peak in Europe at the end of 2015 and declining slowing subsequently. This resulted in contango market conditions from 2015 into early 2017, meaning that prompt prices were lower than forward prices.

In these prior years, when the level of the contango exceeded tankage and working capital costs, we put diesel into storage at Thames Oilport and Navigator North Tees in the UK, where we had available capacity. This represented a new source of margin for the business.

This period, however, the market moved from a contango to a backwardated price structure. Even though refinery margins were strong and refinery utilisation rates high, global diesel demand outstripped production and diesel stocks declined. The market tightness was exacerbated by hurricanes in the latter half of 2017, which temporarily affected refinery production in the US. With these changing market conditions, we released our diesel from contango storage.

UK and Irish markets

Fuel imports into the UK

Net imports of petroleum products were lower than in 2016 due to:

» Continuing strong refiningmargins and high utilisationrates for UK refineries

» The ending of contango marketconditions, which had resultedin stock building and recordlevels of imports in 2016.

As a result, the level of net imports into the UK was 10.1m tonnes, down from 10.5m tonnes in 20162.

Source: Reuters 1 SMMT 2 UK Department for Business, Energy and Industrial Strategy

of Irish fuel demand is met through imports

70%

Ireland relies on fuel imports to meet its growing fuel requirements

Road fuel demand in Ireland continues to rise as a result of population growth. Dieselisation continued this period, with diesel demand rising 3.4% in the calendar year 2017 and gasoline demand falling 1%.

Ireland has one refinery located in the rural south and no pipeline-fed inland terminals, so 70% of Irish fuel demand is met through imports. Our acquisition of 50% of the Foynes import terminal as part of the Inver Energy transaction gives us a strategically important supply location to meet demand in the west of the country.

UK and Ireland Fuels p32

Global markets ARA diesel stocks

Continued growth in UK diesel demand

Road fuel demand in the UK remained flat in the 2017 calendar year (2016: up 2.2%). Once again, there was growth in diesel demand, up 1.0% (2016: up 4.2%), while gasoline demand fell by 1.9% (2016: down 1.3%).

The continued rise in diesel consumption occurred despite the announcement of Government plans to reduce diesel engine emissions, including higher taxes on new diesel vehicles from 2018. This impacted sales of new diesel cars (down 17% in the 2017 calendar year1) but at year- end had not yet affected demand for diesel fuel, which is also used by buses, light and heavy goods vehicles.

Road fuel demand

2.65

2.45

Net fuel import

2524 ANNUAL REPORT APRIL – DECEMBER 2017

MARKET REVIEW » GLOBAL MARKETS / UK AND IRISH MARKETS

UK and Ireland Fuels p32

4

10

12

8

6

Pec

enta

ge

%

Apr2014

Apr2018

Apr2017

Jan2020

Jan2019

Jan2022

Jan2021

Apr2016

Apr2015

Apr2013

4.75%

10.4%10.1%

7.25%

8.50%

9.75%

Post year-end, the UK Government adopted legislation to amend the UK’s Renewable Transport Fuel Obligation.

The new legislation:

» Significantly increases the amount of waste-based biofuel that must be blended into fuel in the UK

» Introduces maximum levels for competing biofuels made from crops.

These changes take effect from April 2018 and create new supply opportunities for us as Europe’s largest producer and supplier of biofuel from waste.

UK biofuel supply obligations

Biodiesel manufacturing facility | Teesside, UK

Percentage biofuel inclusion rates required under the Renewable Transport Fuel Obligation

Global Biofuels p50

Case study

Rising biofuel supply obligations

2726 ANNUAL REPORT APRIL – DECEMBER 2017

MARKET REVIEW » BIOFUEL MARKETS

Market reviewBrazil marketDiesel imports into Brazil

0

8

14

12

10

6

cbm

(m

illio

n)

4

2

2013 20162015 201720142012

Diesel imports into Brazil

Brazilian market

The Brazilian road fuels market continued its rapid transition from a regulated market supplied by the ‘national’ oil company to a growing import market.

Severe hurricanes in autumn 2017 resulted in lost refinery output in the USA Midwest, increasing our products costs into Canada.

Canadian market

We source lowest-cost product from across the world for our Canadian fuel supply business, and the USA Mid-West and Europe are both key sources of product to us. Hurricanes resulted in a sudden fall in refinery output in both the USA Mid-West and mid-continent, and any available product from the Mid-West headed south and east to replace lost production in Texas.

With our unique marine and rail-fed logistics capability and our supply chain flexibility, we were able to switch our sourcing to other markets to ensure continued supply resilience for customers. However, we incurred higher product costs and lower margins in Canada until normal refinery production resumed.

Canada p44

Growing requirement for fuel imports

The Brazilian road fuels market has historically been supplied almost exclusively by the state-regulated ‘national’ oil company but is currently undergoing significant change.

This period, the ‘national’ oil company:

» Reduced its supply into the domestic market, resulting in growing demand for fuel imports by new suppliers such as Greenergy

» Began divesting of infrastructure assets, reducing future domestic supply capacity.

Together, these trends are increasing the country’s requirement for fuel imports. Diesel imports were equivalent to 24% of domestic diesel demand in 2017, up from 15% the previous year. Gasoline imports accounted for 15% of the domestic gasoline market in 2017, up 1.5m cbm on 2016.

The ‘national’ oil company also introduced daily pricing from July 2017, replacing the periodic price reviews which characterised the market in the previous year. The move to a pricing structure more closely aligned to world markets reduced our exposure to counterparty risk.

Brazil p48

Risk register p74

Source: ANP (Brazil national Agency of Petroleum, Natural Gas and Biofuels)

2928 ANNUAL REPORT APRIL – DECEMBER 2017

MARKET REVIEW » BRAZIL MARKET

Strategy in action5capacity by 2022

1.3mb/d

Middle Eastern market

Our gasoline blending joint venture aims to supply its Bahraini home market and meet growing gasoline demand in other GCC countries and in Asia.

The Middle East continues to see a significant expansion in refinery production, with 1.3 million barrels/day of capacity due to come on stream by 2022 and a further 1.1 mb/d by 20254. With these new refineries geared towards diesel exports, there are significant regional imbalances in gasoline components, creating import, blending and supply opportunities for our gasoline joint venture in Bahrain.

Middle East p49

4 Source: OPEC

MARKET REVIEW » MIDDLE EASTERN MARKET

3130 ANNUAL REPORT APRIL – DECEMBER 2017

UK and Ireland Fuels

Customer forecourt | London, UK

"Access to import infrastructure continues to be strategically important, allowing us to minimise product costs and ensure supply resilience for our customers. By acquiring Inver Energy this period, we have extended our infrastructure footprint and fuel supply into the Irish market for the first time."

Caroline LumbardUK Trading Director

Aim: Develop low-cost and resilient fuel supply chains to earn the long-term loyalty of our customers in the UK and Ireland

Supply locations

Areas of population density

3332 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » UK AND IRELAND FUELS

UK and ireland fuelsKPI: average ship size (cbm)

25

20

15

10

Ave

rgae

sh

ip s

ize

(cb

m t

ho

usa

nd

)

2011 2012 20162015 20172013 2014

12,929

21,217

19,676

Creating economies of scale by using larger vessels

KPI

UK and Ireland Fuels

Competition in the UK road fuels market remained intense following a period of strong refining margins. We used our import infrastructure to buy globally and minimise product costs.

(continued)

Strategic capability 1 Source diesel from the lowest-cost global producers

In 2015 and 2016 diesel was in plentiful supply, with high global diesel stocks giving us strong purchase margins. This year saw a decline in global diesel stocks and, following hurricanes in the USA in the second half of 2017, a return to backwardated market conditions. Margins for prompt purchases were therefore lower than in prior years.

We expect the UK road fuels market to continue to be highly competitive in 2018 following a period of strong margins for UK refiners. Our capacity rights at the UK’s only east-coast deep-water road fuel jetties, at Navigator North Tees and Thames Oilport, and our investment in pipeline connections between our Teesside facilities, are all important in this context, giving us the flexibility to source a variety of cargo sizes and specifications at the lowest cost.

Strategic capability 3 Create cost and operational efficiencies

We continue to work to create operational and supply chain efficiencies and reduce unit costs across the business. This period, we:

» Brought into use a diesel pipeline linking Navigator North Tees (a former refinery), Navigator Seal Sands and Inter-Terminals Seal Sands. We are now able to receive diesel on larger ships via the deep-water jetty at Navigator North Tees and move it by pipeline to our neighbouring supply locations, creating cost and operational efficiencies. This period, we received our first LR2 vessel (capacity 110kt) into Navigator North Tees

» Increased the capacity of the pipeline from the jetties at Navigator Thames. By debottlenecking this busy terminal, we have reduced ship discharge times and associated shipping-related costs

» Continued to optimise our haulage operations to lift from the lowest-cost location.

Our aim is to use bigger ships wherever economic to achieve economies of scale and debottleneck busy terminals.

However, this period, the average size of ships used in the UK fell as a result of:

» Jetty damage on the Thames, which severely restricted the size of ships we were able to receive

» The drawing-down of our contango stock at Thames Oilport and Navigator North Tees.

We expect average vessel size to increase in 2018 following jetty repairs at Navigator Thames and completion of the Teesside diesel pipeline.

Strategic capability 2 Blend gasoline from component products

We operate sophisticated gasoline blending systems at three UK locations, Navigator Thames, Navigator Seal Sands and Inter-Terminals Seal Sands. These three facilities in combination continue to offer significant operational flexibility.

Gasoline blend margins remained stable overall. Strong demand from the petrochemical sector increased the price of naphtha, a typical petrol blend component, but this was partially offset by other components in our blending pool. The scale of our petrol blending operations allows us to accommodate a range of minority components we would otherwise be unable to use.

Global markets p24

Global markets p24

Thames case study p36

KPI: average ship size (cbm)

3534 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » UK AND IRELAND FUELS

Case study

Jetty damage on the Thames

Third-party damage to the jetty infrastructure at Navigator Thames, our busiest import terminal, restricted the size of ships we were able to receive at the facility from mid November 2017.

We used our significant supply chain capability and our additional supply location at Thames Oilport to ensure uninterrupted supply for customers following the incident, but incurred increased product and shipping costs as a result.

Navigator Terminals | Thames, UK

3736 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » UK AND IRELAND FUELS

Dec2015

250Dec2016

Dec2017

Apr2017

350

300

277

344

319

301

0

600

500

400

300

200

100

Apr2013

Apr2015

Apr2016

Apr2017

Apr2014

Dec2017

521

396

Nu

mb

er o

f si

tes

sup

plie

d

KPI: Independent forecourts

Our Greenergy Flexigrid logistics operation provides greater control over the quality of service we provide to customers and allows us to adapt continually to deliver from the lowest-cost supply location.

We have established Thames Oilport as a new diesel supply location, providing increased resilience in the busy South East region.

Strategic capability 4 Make safe, reliable and cost-efficient fuel deliveries to customers

We expanded our in-house haulage capability within Greenergy Flexigrid to meet our growing supply requirements in the UK.

We recruited more drivers into Greenergy Flexigrid in order to meet a greater proportion of our deliveries from our own fleet, reducing reliance on subcontractors and improving overall resilience and quality. We also increased the size of our fleet, ordering an additional 26 tankers and 34 trailers to be delivered after the end of the period.

Strategic capability 5 Grow in target markets

Independent forecourts

We significantly expanded sales to the independently owned forecourt sector in the UK, and by the end of 2017 were contracted to supply some 521 independently-owned sites (Esso: 387; other: 134). Some of these contracts are for supply commencing in 2018.

Our ability to offer fuel supply under a choice of brands (Esso, convenience brands or operators’ own brands) continues to be attractive, allowing us to meet the needs of the larger forecourt groups as well as those of single-site dealers.

Thames Oilport

We commenced diesel and gasoil supply from Thames Oilport this period, giving us a second significant import and supply location in the South East of England, an area of population and demand growth. This has provided improved supply security for customers and reduced peak-time queuing at the nearby Navigator Thames terminal.

With expanding sales from Thames Oilport, we extended facilities for drivers, brought into use additional road loading facilities and completed new additive systems, allowing us to meet customer-specific specifications.

Our investment in newer vehicles improved fuel efficiency. Average MPG from our in-house fleet improved to 8.99 miles per gallon, a 5% improvement on the same period in 2016 (industry average: 7.9 miles per gallon1).

Work continued on a new scheduling system designed to improve fleet utilisation and real-time reporting of ETAs. This is part of a major systems upgrade to bring operational efficiencies and add capability and scalability, to support the continued growth of our in-house haulage function.

In FY17 we took over the management of our vehicle maintenance operations from a previously outsourced function. With better resource planning this period, we improved vehicle up-time to 94% (FY17: 92%) and increased fleet utilisation.

Infrastructure p58

UK and Ireland Fuels (continued)

Number of Greenergy Flexigrid drivers

Includes Inver dealers referenced on p40

"Our independent fuel retail offer goes from strength to strength. We continue to work to earn the loyalty of each and every customer by delivering unparalleled supply reliability and customer responsiveness. "Debbie GhigiRetail Territory Manager

1 Department for Transport, updated November 2017

3938 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » UK AND IRELAND FUELS

Our plans in the UK and Ireland

» Maintain sales growth to the independent forecourt sector in the UK and Ireland

» Progress the regeneration in Thames Oilport to add petrol handling capability

» Expand our UK in-house haulage operation to meet growth in our delivered-in fuel supply

» Integrate Inver’s import and storage operations into our global purchasing strategies, to create supply chain efficiencies and economies of scale

» Explore opportunities to expand our supply footprint in Ireland.

We acquired Inver Energy’s fuel infrastructure and supply operations in Ireland and the UK. After a period of familiarisation, we are preparing to integrate our businesses to create supply chain efficiencies and economies of scale.

Strategic capability 6 Grow Inver sales in Ireland

As part of the acquisition of Inver Energy we acquired Inver’s storage facilities and supply operations in Ireland and the UK.

Inver currently imports diesel, gasoline, gasoil, kerosene, marine fuel and jet fuel into Ireland. We will look at opportunities to integrate Inver’s supply chains into our global purchasing and supply strategies, to achieve supply chain efficiencies and economies of scale.

Inver also supplies fuel to independent forecourt operators under its own brand. The Inver brand combines a clean, modern image with support for local community initiatives and offers independent retailers competitive and flexible pricing together with service quality and security of supply. The development of own-branded retail sales has enabled Inver to diversify its sales portfolio and establish longer-term relationships with customers. We will work to expand this part of Inver’s Irish business and consider opportunities to use the Inver brand in other markets.

With Inver’s storage and supply facilities on the west coast of Ireland, we are now ideally placed to supply customers in the south and west of the country. Going forward, we will explore opportunities to commence supply in the more densely populated east coast region.

Infrastructure p60

"We have developed a highly successful retail brand in the Irish market. We are now exploring opportunities to develop the brand outside of Ireland."Chris O’CallaghanHead of Branded Supply at Greenergy and Managing Director of Inver Energy

UK and Ireland Fuels (continued)

Customer forecourt | Limerick, Ireland

4140 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » UK AND IRELAND FUELS

Strategy in actionInternational fuelsNon-UK sales pg 42

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

Lit

res

(bill

ion

)

2013 20152014 20172016

2.5

2.0

1.0

0.5

1.5

3.0

0

KPI: Non-UK sales

International Fuels

We further expanded our international fuel businesses, increasing our fuel imports into Brazil and acquiring the CAN-OP fuel terminal in Canada to give us a new supply location in northern Ontario. In Bahrain our petrol blending joint venture is now supplying gasoline to the local Bahraini market.

Aim: Expand internationally by replicating our UK experience in other markets

Rail-to-road facility | Toronto, Canada

4342 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » INTERNATIONAL FUELS

Marketing terminal

Supply terminal

CANADA

USA

Concord

NEW YORK

ONTARIO

QUEBEC

Quebec City

Chicago

Hamilton

Toledo

Detroit

Concord

Thunder Bay

Toronto

CANADA

USA

Concord

NEW YORK

ONTARIO

QUEBEC

Quebec City

Chicago

Hamilton

Toledo

Detroit

Concord

Thunder Bay

Toronto

Dec2015

Dec2016

Apr2017

Dec2017

0

50

100

150

200

250

109

155

231

177

We extended our supply chains in order to source fuel products from a range of markets, using sea and rail access to deliver supply resilience throughout the year.

Strategic capability 1 Develop low-cost, multi-modal and reliable supply chains

We operate multi-modal supply chains comprising domestic and international rail, international shipping or a break-bulk combination of both. This unique flexibility allows us to source from the prevailing lowest-cost market around the world.

During the period we purchased product from Western Canada, USA Mid-West, Europe and local Canadian refiners.

Our supply chain flexibility was evident during the latter half of the period where the hurricanes in the USA caused significant refinery outages and tightness in product availability. At this time we maintained continuous supply for our customers by shifting our sourcing more towards Canada and Europe.

We intend to expand our supply sourcing options as our supply footprint grows, creating further long-term relationships with domestic and foreign refiners in order to maintain supply resilience for customers.

Canada

Canadian market p29

Case study

Creating resilient fuel supply chains

Historically, growth in fuel demand in Canada has not been matched by investment in fuel supply infrastructure, resulting in supply disruption and product outages in the market.

We are developing flexible supply chains and investing in critical supply assets in order to create year-round product availability for customers.

Number of railcars leased in Canada

4544 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » INTERNATIONAL FUELS

We expanded further in Canada, acquiring a fuel supply business and terminal in northern Ontario and expanding sales from our rail-to-road facility in Toronto.

Strategic capability 2 Invest in infrastructure to expand supply and improve supply resilience

Expanding existing rail-to-road facilities in Toronto

We completed the expansion of our first rail-to-road supply location at Concord, north of Toronto. The facility has added capacity in a convenient location and continues to be extremely popular with customers. We intend to replicate this model in other regions across the country in the years ahead.

Strategic capability 3 Commence branded sales to independent fuel retailers

Breakaway: A new retail proposition

We are developing a unique retail brand that draws on Canadians’ love of ice hockey. After extensive market research, we have selected Breakaway as the brand name for our retail offer. Accompanying our fuel offer, we have partnered with Gateway Newstands who will be able to provide customers with an industry-leading C-store offering.

The Breakaway brand offers an alternative to major oil company brands which are currently concentrated in the market and allows us to target sales to independently owned forecourt groups in Canada.

We expect to have our first Breakaway branded site operational by summer 2018, with a rollout to other sites following shortly thereafter.

A new sourcing and supply terminal in Northern Ontario

During the year we acquired 100% of the shares of Canadian Operators Petroleum (CAN-OP), a fuel marketer and terminal operator in Thunder Bay. CAN-OP’s operations include a gasoline and diesel wholesale business and a wholly owned petroleum storage and supply facility, Wascan Terminals Inc.

Located in Northern Ontario, Thunder Bay expands our supply footprint into a new developing region. The terminal facility is rail-fed, allowing for efficient integration into our existing supply chains.

Over the next twelve months, we plan to upgrade and expand the facility to make fuel supply more reliable and competitive in Thunder Bay and the surrounding region. This significant investment will be positive for the local community.

The acquisition also included a retail site and cardlock/truck stop, which we also plan to upgrade.

"We continue to make significant investments into oil supply chain infrastructure in Canada. We aim to bring low-cost fuel and higher levels of supply reliability to customers in regions that have historically been poorly served. "Adam TraegerDirector of Investments

Canada

Infrastructure p56

Our plans in Canada

» Expand our network of suppliers across Canada, USA and Europe for enhanced supply chain flexibility

» Commence sales under the Breakaway brand, providing a new, flexible branded offer to the independent market

» Expand and modernise our new facility in Thunder Bay, to provide this important region with an industry leading offering

» Develop and invest in additional supply infrastructure, including additional rail-to-road facilities, to create new supply capability.

(continued)

4746 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » INTERNATIONAL FUELS

BRAZIL

Santos

Paranaguá

The Brazilian market is increasingly reliant on fuel imports to meet domestic demand. We increased our diesel imports into Brazil and made our first gasoline sales.

Bahrain Gasoline Blending (BGB), our joint venture in Bahrain, is now blending gasoline for the domestic Bahraini market and for export.

Strategic capability 4 Increase domestic sales into Brazil

Fuel product imports into the Brazilian market continued to increase this period because supply from the ‘national’ oil company was insufficient to meet domestic demand.

As customers looked for alternative sources of supply, we expanded our imports of diesel, supplying from facilities at Santos in the centre south and Paranaguá in the south, both areas of population density.

Strategic capability 5 Develop lasting relationships in the Middle East

We are now blending gasoline within Bahrain Gasoline Blending (BGB), a joint venture between nogaholding, Bapco (the national oil company of the Kingdom of Bahrain) and Greenergy. The joint venture commenced operations in February 2017.

This period, BGB:

» Met its objectives by adding value to Bahrain’s gasoline pool in terms of better blend margins, trading and risk management

» Blended more than 5 million barrels of gasoline

» Supplied gasoline to meet demand within the local market

» Exported the first finished gasoline cargo out of Bahrain for more than five years

» Developed trading relationships with most of the major refineries and traders in the region.

The joint venture is also evaluating engineering works to expand and enhance the gasoline blending facilities in Bahrain. These additional facilities would give greater trading capability and flexibility, allowing BGB to source and trade a wider variety of gasoline products and further improve its blend economics.

Diesel demand in Brazil is significantly linked to agricultural and industrial production and therefore varies by season. When diesel demand dropped at the end of the harvest season and start of the holiday period in November and December, we used available tankage to make our first imports of gasoline into Brazil.

Across all our relationships we continue to work to gain the trust and loyalty of new and existing customers, cementing our reputation as a reliable supplier.

"Across all our relationships we are working to earn the trust and long-term loyalty of new and existing customers, building on our reputation as a trusted trading counterparty in the Brazilian market. "Nelson OstanelloChief Executive, Greenergy Brazil

Brazil Middle East

Market review p23

Market review p30

Our plans in Brazil and the Middle East

» Continue to expand fuel imports into Brazil to meet growing demand

» Increase our storage capacity in Brazil in order to supply other regions

» As a shareholder within BGB, pursue opportunities to become a major gasoline player in the Middle East.

Supplying Brazil

4948 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » INTERNATIONAL FUELS

Strategy in actionGlobal biofuelsbiodiesel manufacturing output

Pro

du

ctio

n (

cbm

)

2013* 2014* 2015 2016 2017

*Flood 15 Apr - 31 Dec

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

Global Biofuels

Aim: Create value from biofuel manufacturing and supply

"We have achieved further significant growth in our biodiesel manufacturing output, benefitting from previous investments and ongoing process and technical improvements. We are ideally placed to meet growing demand for biofuel resulting from rising UK Government mandates effective April 2018."

Paul BatesonChief Operating Officer

Biodiesel manufacturing output

Market review p23

Biodiesel manufacturing facility | Immingham, UK

5150 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » GLOBAL BIOFUELS

USAUK

China

Middle East

Australia

Our global biofuel supply chain

Global sourcing We purchase waste oils as feedstock for our biodiesel manufacturing activities. By diversifying our supply chains globally we are able to source increasing quantities of the most appropriate feedstock, to meet our growing production requirements.

Biodiesel productionWith two manufacturing facilities on the east coast of England, we are Europe’s largest producer of waste-based biodiesel. We continue to expand our production to meet rising demand resulting from additional UK Government incentives.

Location: Immingham and Teesside, UK

Storage and supplyWe blend biodiesel and bioethanol into the petrol and diesel we supply in the UK, Ireland and Canada to meet regulatory requirements.

We also supply biodiesel and bioethanol to other oil companies in the UK, Ireland and in Canada, meeting customer-specific sustainability requirements.

Our storage facilities in the UK, Canada and Rotterdam give us the capacity to meet biofuel demand in different markets.

Imports: Australia, China, Middle East, USA

Supply: UK, Canada and mainland Europe

We continue to scale up our sourcing operations in line with growth in our manufacturing operation, making upstream investments.

Strategic capability 1 Source biofuels and biofuel raw materials globally

Expansion of our biodiesel manufacturing output required a significant increase in the volume of waste oils we source. By diversifying our supply chains beyond the UK and Europe to countries where there are no comparable biofuel supply obligations or incentives, we:

» Reduced raw material costs

» Sourced growing volumes of feedstock with quality characteristics that are best suited to our manufacturing operations.

This period, we expanded our sourcing from Asia, Australia and the Middle East, concluding a new joint venture partnership in Australia and expanding our joint venture operations in China. We also increased the volume of product sourced in smaller containers, including ISO containers, reducing product costs and making new supply chains available to us.

Global Biofuels (continued)

5352 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » GLOBAL BIOFUELS

"This period we achieved a 26% increase in our biodiesel manufacturing operations compared with the same period in 2016, consolidating our position as Europe’s largest manufacturer of waste-based biodiesel. "Paul CurtisChief Executive, Global Biofuels

» Investments to improve raw material flexibility and increase yield

» Ongoing process and technical improvements at both facilities

» Investment in our own facilities for receiving ISO containers, increasing our ability to receive raw materials with specific quality characteristics and reducing third-party handling costs.

Strategic capability 2 Manufacture biodiesel from wastes

Combined production at our manufacturing facilities at Immingham and Teesside increased further this period as a result of ongoing improvements.

We benefitted from:

» A used cooking oil pre-processing facility at Teesside completed in 2016, allowing the plant to process more difficult waste oils into a high quality sustainable fuel

Strategic capability 3 Supply biofuel to third parties

We increased our biofuel sales to other oil companies in Canada, the UK, Ireland and elsewhere in Europe.

Our focus is on meeting customer-specific sustainability requirements, recognising the characteristics of different continents and markets. By applying our unique sustainability IP, we create value for customers and maximise the value of the biofuel we supply.

Strategic capability 4 Generation and sale of UK RTFO certificates

We continue to blend biofuel into the petrol and diesel we supply in the UK in order to:

» Meet our own biofuel supply obligations under the Renewable Transport Fuel Obligation (RTFO)

» Generate certificates for sale to other oil companies by blending more biofuel than our obligated amount.

By increasing the amount of biodiesel blended into our diesel throughout the period, we increased the number of certificates we generated. Market values for third- party certificate sale increased during the latter half of this period in anticipation of the rise in RTFO obligation amounts from April 2018, resulting in higher margins from certificate generation.

We plan to

» Make further investments in our biodiesel manufacturing facilities to increase capacity

» Expand our biodiesel raw material origination with a particular emphasis on the Middle East and Asia

» Maximise biodiesel blending and RFTO certificate generation.

Market review p23

Global Biofuels (continued)

We made further improvements to our biodiesel manufacturing operations to increase the volume of biodiesel we produce and drive down unit costs.

5554 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » GLOBAL BIOFUELS

Infrastructure

Aim: Acquire, regenerate and integrate assets to support our supply chain objectives

"We are using our understanding of fuel markets and our experience as an infrastructure user to develop strategically important assets that support our long-term supply objectives.

This period, we opened Thames Oilport for diesel supply by truck and acquired 100% of the Cardiff terminal, where we already store and supply fuel, as part of the Inver Energy transaction. We also extended our infrastructure footprint internationally, acquiring a 50% share in the Foynes terminal in Ireland and 100% of the rail-fed terminal at Thunder Bay in Northern Ontario. "Chris BrookhouseInfrastructure Director

Thames Oilport | UK

5756 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » INFRASTRUCTURE

Foynes

Navigator Seal Sands

Thunder Bay

Toronto

Navigator North Tees

Thames OilportThames Enterprise Park

Navigator Thames

Cardi�

Plymouth

Foynes

Navigator Seal Sands

Thunder Bay

Toronto

Navigator North Tees

Thames OilportThames Enterprise Park

Navigator Thames

Cardi�

Plymouth

Wholly owned

Part owned

We are regenerating fuel infrastructure in the UK and Canada to add functionality, flexibility and value.

Strategic capability 1 Regenerate legacy infrastructure to increase value

Thames Oilport, UK

We continue to progress the phased development of Thames Oilport with our joint venture partner:

» We commenced road-loading of diesel and heating oil, giving us a new and strategically important supply location in the South East of England. This follows extensive refurbishment works in prior years to tankage, pipes, jetty infrastructure, road-loading facilities and the terminal control system

» The connection to the UK Oil Pipeline (UKOP) was commissioned. This is strategically important for the facility, enabling diesel to be supplied by pipeline to customers in other parts of the UK

» We brought into use additional road loading facilities to meet sales growth

» We began design works for gasoline storage and supply, to be developed as the next phase of regeneration.

Thunder Bay, Canada

Our acquisition of Canadian Operators Petroleum (CAN-OP) included the purchase of 100% of the shares in Wascan Terminals Inc, a storage and supply facility located in Thunder Bay in northern Ontario. We commenced engineering works to upgrade and expand the terminal to:

» Enhance the approach to health and safety for our employees, customers and suppliers

» Expand rail supply and storage infrastructure at the facility to replicate our successful rail-to-road concept already in operation at Toronto

» Modernise and expand road-loading facilities.

Infrastructure Our infrastructure investments

UK and Ireland

UK and Ireland Fuels p39

Toronto, Canada

We completed the expansion of our first rail-to-road supply location at Concord, north of Toronto. The works have doubled the size of the facility, providing increased supply security to the Greater Toronto region, and added full biofuel blending and dye capability to our customer offering.

Teesside, UK

We completed work on a diesel pipeline linking Navigator North Tees (a former refinery), Navigator Seal Sands and Inter-Terminals Seal Sands. By connecting the deep-water jetty at Navigator North Tees with our other supply locations nearby, we aim to create economies of scale, reducing shipping-related costs and improving purchase margins.

International Fuels p46

UK and Ireland Fuels p35

(continued)

Canada

International Fuels p46

Part owned

Wholly owned

Thunder Bay » Acquired this period

» Strategic location at a key petroleum supply/trading intersection

Toronto

Foynes » 50% share acquired this period

» Deep-water multi-product import terminal

» Realising the value of former refinery land not required as fuel infrastructure

Thames Oilport » Opened this period for diesel

supply by truck

Thames Enterprise Park

Cardiff

Teesside

» 100% share acquired this period

» Continues as a Greenergy stock-managed terminal

» New diesel pipeline connections completed this period

» Our first rail-road facility

» Unique concept suitable for other locations

5958 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » INFRASTRUCTURE

Thames Enterprise Park | UK

Strategic capability 2 Operate fuel infrastructure to meet regional demand

Purchase of Inver terminals at Foynes and Cardiff

Our acquisition of Inver Energy included Inver’s 50% share in the AFSC facilities at Foynes and its wholly-owned facility in Cardiff.

The AFSC terminal at Foynes is a multi-product, deep-water facility at a strategic location on the west coast of Ireland, allowing us to import, store and supply a range of fuel products.

We have operated from Inver’s Cardiff terminal since 2012, moving gasoline blended at our Teesside facilities by rail to Cardiff and importing diesel by ship. We will be carrying out a strategic review to ensure we make best use of the facility now that it is under Greenergy ownership.

Navigator Terminals

In 2016 we formed Navigator Terminals with various institutional investors to own and operate fuel storage and blend facilities in the UK. Our participation in Navigator provides:

» Continued access to strategically important fuel storage and blending facilities on the Thames and Teesside

» More integrated supply chain management across Navigator facilities

» Shareholder income.

Plymouth

We continue to operate our Plymouth facility as a key part of our national supply chain. Over our ten years of ownership we have upgraded the facility to comply fully with post-Buncefield safety and environmental requirements.

Infrastructure

UK and Ireland fuels p40

(continued)

We have invested in strategically important infrastructure assets that supply our ongoing fuel supply commitments.

We plan to

» Continue the regeneration of Thames Oilport

» Upgrade and expand the Thunder Bay facility

» Progress the development of Thames Enterprise Park with a view to maximising land value at sale.

Case study

Creating value from former refinery land at Thames Enterprise Park

We are working to realise the value of the substantial area of land at Thames Enterprise Park, using land not required for the Thames Oilport import terminal.

This period, we completed the first phase of demolition of refinery infrastructure and obtained planning permission for land remediation on part of the site. With masterplan planning approval already granted, we expect to submit an outline planning application for the entire land redevelopment in 2018.

6160 ANNUAL REPORT APRIL – DECEMBER 2017

STRATEGY IN ACTION » INFRASTRUCTURE

20150

80

60

2016 2017

100

£ (

mill

ion

)

20

40

Key performance indicatorsEBITDA excluding exceptionals

47.6

89.267.2

30.9

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

20150

80

60

2016 2017

100

£ (

mill

ion

)

20

40

22.1

64.348.0

23.2

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

EBITDA excluding exceptionals

£67.2m

Profit before tax and before exceptionals

£48.0m

Key performance indicators6

EBITDA/Profit before taxEBITDA for the 37 week period to 31 December was £67.1m before exceptional items, compared to £70.6m during the equivalent period in the prior year. Results from the established UK business were affected by lower diesel margins but our UK performance was bolstered by profits in Brazil plus stronger returns from biodiesel production.

Financial KPIs

Chief Executive's Review p10

Chief Financial Officer’s Review p68

EBITDA excluding exceptionals

Profit before tax and before exceptionals

6362 ANNUAL REPORT APRIL – DECEMBER 2017

Operational KPisGroup sales volume

20150

15

2016 2017

20

Lit

res

(bill

ion

)

5

10

17.619.1 14.4

5.3

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

Operational KPisBiodiesel manufacturing

2015 2016 2017

cbm

15 A

pr

- 31

Dec

1 Ja

n -

14 A

pr

Operational KPisInternational sales growth

2015

1.5

2016 20170

2.5

2.0

Lit

res

(bill

ion

)

0.5

1.0

3.0

0.60.6

1.4

2.4

15 A

pr

- 31

Dec

1 Ja

n -

14

Ap

r

Operational KPisShip sizes

10

20

14

18

16

12

22

2013 2015 20162014 2017

Ave

rag

e sh

ip s

ize

cb

m (

00

0)

16,744

19,676

21,217

Operational KPisIndependent forecourts

0

600

500

400

300

200

100

Apr2013

Apr2015

Apr2016

Apr2017

Apr2014

Dec2017

521

Group sales volumeGroup sales volume grew as a result of international expansion.

Biodiesel manufacturing outputProduction volume increased strongly as a result of previous investments to expand manufacturing capacity and create operational efficiencies.

International sales growthOur non-UK sales grew strongly as we expanded our fuel supply operations in Brazil and Canada and acquired the Inver business in Ireland.

Ship sizesOur ability to receive product on larger ships was impacted by third-party damage to one of the jetties at our main supply facility on the Thames.

Sales to UK independent forecourtsSales to the independently owned forecourt sector in the UK continued to expand rapidly as we won business from all competing brands.

Operational KPIs

Chief Executive's Review p10

Global Biofuels p50

Number of independently-owned forecourts contracted to supply

Combined output from Immingham and Teesside facilties (cbm)

Size of ships importing Greenergy fuel into the UK (cbm)

UK and Ireland Fuels p35

UK and Ireland Fuels p39International Fuels p42

UK and Ireland Fuels p40

Customer forecourt | Exeter, UK

6564 ANNUAL REPORT APRIL – DECEMBER 2017

KEY PERFORMANCE INDICATORS

Service quality KPisOn-time deliveries

Per

cen

t

Apr2017

Dec2017

100

90

70

80

60

Environmental KPisbiodiesel from waste

Jan-Apr2017

Apr-Dec2017

20150

2016

100

80

60

40

20

Per

cen

tag

e %

99.95 100 100 100

Environmental KPisfuel e�ciency

in our in-house �eet

20150

8

2016 Jan-Apr2017

Apr-Dec2017

10

MP

G

4

6

2

8.26 8.43 8.71 8.99

Environmental KPisbioethanol from waste

Jan-Apr2017

Apr-Dec2017

2015 2016

Per

cen

tag

e %

0

100

80

60

40

20

39

66

4740

Apr2017

Dec2017

100

90

70

80

60

Per

cen

t

Service quality KPisTruck lwaiting times

0

35

30

20

25

15

10

5

Jan2015

Dec2017

10.10%

31.80%

Per

cen

t

Bioethanol from waste

On-time deliveries (UK) The complexity of our delivery operations increased further as we expanded our delivered-in sales, including to the independent forecourt sector.

To support the continued growth of the business we are undertaking a major systems upgrade to give improved scheduling and in-cab functionality. This will allow us to improve customer service, for example by providing real-time reporting of ETAs.

Biofuel from wasteWe seek to maximise our use of waste-based biofuels in our blending in the UK, using biodiesel produced in our own manufacturing operations and, when available, waste-based bioethanol sourced from third parties.

The amount of waste-based bioethanol that we were able to source in the market in 2017 was limited due to competitive pressures.

Fuel efficiency in our in-house haulage fleet Fuel efficiency in our in-house fleet improved this period as a result of the introduction of new, more fuel-efficient vehicles.

Invoice accuracyOur invoice accuracy is an indicator of the quality of the information flow throughout our business.

In order to improve the efficiency and accuracy of our processes, we continue to automate our invoicing wherever possible. The proportion of invoices that were automatically generated this period was 95% (FY17: 94%).

Truck loading times By minimising delays for trucks collecting fuel from our terminals, we improve our own, and our customers’ operational efficiency.

The opening of Thames Oilport for diesel supply has reduced peak-time congestion at Navigator Thames, our busiest terminal.

Environmental KPIs Service quality KPIs

UK and Ireland Fuels p38

Biofuel sustainability p88

UK and Ireland Fuels p38 UK and Ireland Fuels p39

Percentage of trucks taking more than 30 minutes to load, Navigator Thames terminal.

Biodiesel from waste

6766 ANNUAL REPORT APRIL – DECEMBER 2017

KEY PERFORMANCE INDICATORS

Boardroom | London, UKCHIEF FINANCIAL OFFICER’S REVIEW

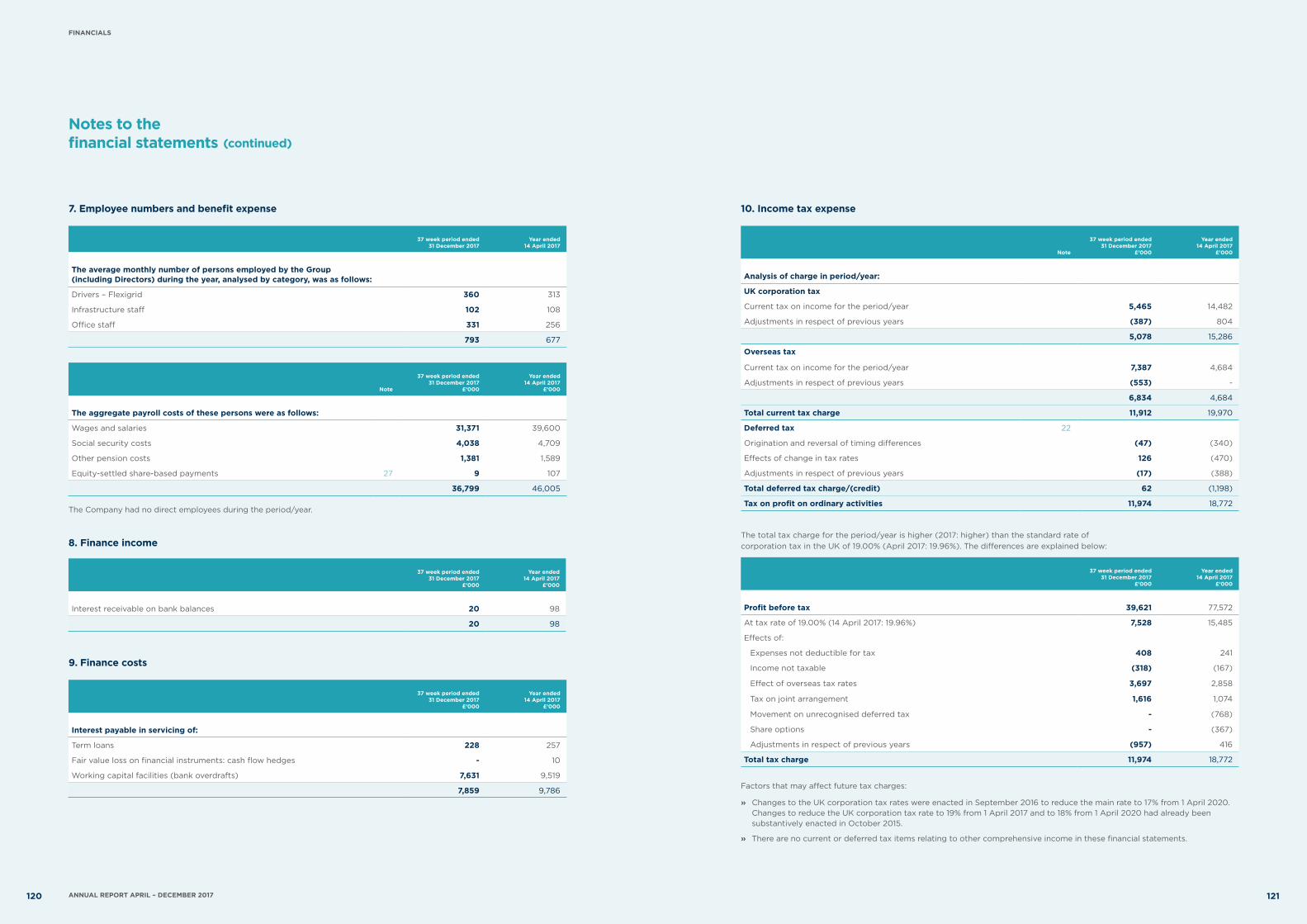

EBITDA for the 37 week period to 31 December was £67.2m before exceptional items, compared to £70.6m during the equivalent period in the prior year. Profit before tax and before exceptional items was £48.0m compared to £56.4m during the equivalent period in the prior year.

"During a shortened reporting period, results were 5% below the equivalent period last year. Our UK and Canadian businesses performed well in testing market conditions. The Group’s results were boosted by a strong contribution from our Brazilian operation as well as improved output from our biodiesel production facilities following a capital expansion programme. Further capital investment and expansion of supply origination will continue in the current year. Our strategic investment programme saw the acquisition of Inver Energy, marking our entry into the Irish fuels market. "Stephen McCaffreyChief Financial Officer

Chief Financial Officer’s Review

Change in reporting period

During this period we moved our financial year-end to the calendar year-end of 31 December; as such, the current period under review represents 37 weeks of trading.

The change in reporting date also drives a change in the allocation of our year-end balance sheet compared to what has been presented in previous years as at 14 April. This is due to the fluctuating nature and relative scale of balances associated with our indirect tax collection and repayment cycle, which runs from 15th to 14th of the month. However the net asset position remains unaffected.

International growth

We continue to achieve stronger margins in Brazil during the period resulting in a higher contribution than forecast. Towards the final quarter of the period and subsequently, the Brazilian market began to show signs of oversupply; as such we do not anticipate as strong a performance in 2018 as the structure of the market continues to change.

We believe there is a long-term future for Greenergy in Brazil as a net importer of fuels, and we continue to assess potential infrastructure opportunities in the region to expand our footprint.

Despite a slow start to the period, the Canadian business recovered in the later months and contributed positively overall. During the period, we acquired an existing business, trading as CAN-OP, which extends our existing customer base and also provides access to additional infrastructure in the form of an operational terminal. We plan to invest in the terminal during 2018 to modernise the facility and expand the customer base.

As part of a wider investment strategy we acquired Inver Energy, an established fuel supply business based in Ireland. This investment will provide access to new markets as well as local infrastructure and has made a positive contribution to Group results since the acquisition was completed in October 2017. This is an initial step in aiming for an Ireland-wide supply operation.

Canada p44

Brazil p48

6968 ANNUAL REPORT APRIL – DECEMBER 2017

The strategic investments made during the period are already making good contributions and this is expected to continue into the next financial year.

UK market