Embed Size (px)

Citation preview

Welltec® AnnuAl RepoRt 2011 1

AnnuAl RepoRt

Welltec International ApS

Central Business Registration No: 30 69 50 03

Welltec® AnnuAl RepoRt 2011 2

focused on estAblishing A succesful tRend

Welltec® AnnuAl RepoRt 2011 3

Contents

company details 4

statement by Management on the Annual Report 5

independent Auditors’ Report 6

group chart 7

consolidated Key figures for the group 8

Management commentary 9

statement of comprehensive income 2011 28

statement of financial position at 31st december 2011 29

statement of changes in equity at 31st december 2011 31

statement of cash flows

for the period 1st January - 31st december 2011 32

notes 33

Welltec® AnnuAl RepoRt 2011 4

CoMpAnY DetAIls

Company Welltec international Aps

gydevang 25

3450 Allerød

denmark

phone: 48 14 35 14

fax: 48 14 35 18

internet: www.welltec.com

e-mail: [email protected]

central business Registration no: 30 69 50 03

Registered in: Allerød

Accounting year: 1/1 - 31/12 2011

Board of Directors søren Jørgensen

Jørgen hallundbæk

han sikkens

scott c. collins

Executive Board Jørgen hallundbæk

Company auditors deloitte statsautoriseret Revisionspartnerselskab

the Annual general Meeting adopted the annual report on March 27, 2012.

Chairman of the General Meeting

Welltec® AnnuAl RepoRt 2011 5

stAteMent BY MAnAGeMent on tHe AnnuAl RepoRt

We have today considered and approved the annual report of

Welltec international Aps for the financial year January 1, 2011

to december 31, 2011.

the consolidated financial statements and parent financial

statements are prepared in accordance with international

financial Reporting standards as adopted by the eu and addi-

tional danish disclosure requirements for annual reports.

in our opinion, the consolidated financial statements and the

parent financial statements give a true and fair view of the

group’s and the parent’s financial position at december 31,

2011 as well as of their financial performance and their cash

flows for the financial year January 1, 2011–december 31,

2011.

We also believe that the management commentary contains a

fair review of the development of the group’s and the parent’s

activities and financial position, together with a description of

the principal risks and uncertainties that the group and the par-

ent face.

We recommend the annual report for adoption at the Annual

general Meeting.

Allerød, March 2, 2012

Executive Board:

Jørgen hallundbæk

chief executive officer

Board of Directors:

søren Jørgensen scott c. collins

chairman

Jørgen hallundbæk Johannes K. J. sikkens

Welltec® AnnuAl RepoRt 2011 6

copenhagen, March 2, 2012

Deloitte

statsautoriseret Revisionspartnerselskab

Anders dons Martin faarborg state Authorised state Authorised public Accountant public Accountant

InDepenDent AuDItoRs’ RepoRt

To the shareholders of Welltec International ApS

Report on the consolidated financial statements and parent

financial statements

We have audited the consolidated financial statements and parent

financial statements of Welltec international Aps for the financial year

January 1 - december 31, 2011, which comprise the statement of

comprehensive income, statement of financial position, statement of

changes in equity, cash flow statement and notes, including the ac-

counting policies, for the group as well as the parent. the consolidated

financial statements and parent financial statements have been pre-

pared in accordance with international financial Reporting standards as

adopted by the eu and disclosure requirements of the danish financial

statements Act.

Management’s responsibility for the consolidated financial

statements and parent financial statements

Management is responsible for the preparation of consolidated finan-

cial statements and parent financial statements that give a true and fair

view in accordance with international financial Reporting standards as

adopted by the eu and disclosure requirements of the danish financial

statements Act and for such internal control as Management deter-

mines is necessary to enable the preparation of consolidated financial

statements and parent financial statements that are free from material

misstatement, whether due to fraud or error.

Auditor’s responsibility

our responsibility is to express an opinion on the consolidated financial

statements and parent financial statements based on our audit. We

conducted our audit in accordance with international standards on

Auditing and additional requirements under danish audit regulation.

this requires that we comply with ethical requirements and plan and

perform the audit to obtain reasonable assurance about whether the

consolidated financial statements and parent financial statements are

free from material misstatement.

An audit involves performing procedures to obtain audit evidence

about the amounts and disclosures in the consolidated financial

statements and parent financial statements. the procedures selected

depend on the auditor’s judgement, including the assessment of the

risks of material misstatements of the consolidated financial state-

ments and parent financial statements, whether due to fraud or error.

in making those risk assessments, the auditor considers internal control

relevant to the entity’s preparation of consolidated financial statements

and parent financial statements that give a true and fair view in order

to design audit procedures that are appropriate in the circumstances,

but not for the purpose of expressing an opinion on the effectiveness

of the entity’s internal control. An audit also includes evaluating the

appropriateness of accounting policies used and the reasonableness

of accounting estimates made by Management, as well as the overall

presentation of the consolidated financial statements and parent finan-

cial statements.

We believe that the audit evidence we have obtained is sufficient and

appropriate to provide a basis for our audit opinion.

our audit has not resulted in any qualification.

Opinion

in our opinion, the consolidated financial statements and parent finan-

cial statements give a true and fair view of the group’s and the parent’s

financial position at december 31, 2011, and of the results of their op-

erations and cash flows for the financial year January 1 - december 31,

2011 in accordance with international financial Reporting standards as

adopted by the eu and disclosure requirements of the danish financial

statements Act.

Statement on the management commentary

pursuant to the danish financial statements Act, we have read the

management commentary. We have not performed any further proce-

dures in addition to the audit of the consolidated financial statements

and parent financial statements.

on this basis, it is our opinion that the information provided in the

management commentary is consistent with the consolidated financial

statements and parent financial statements.

Welltec® AnnuAl RepoRt 2011 7

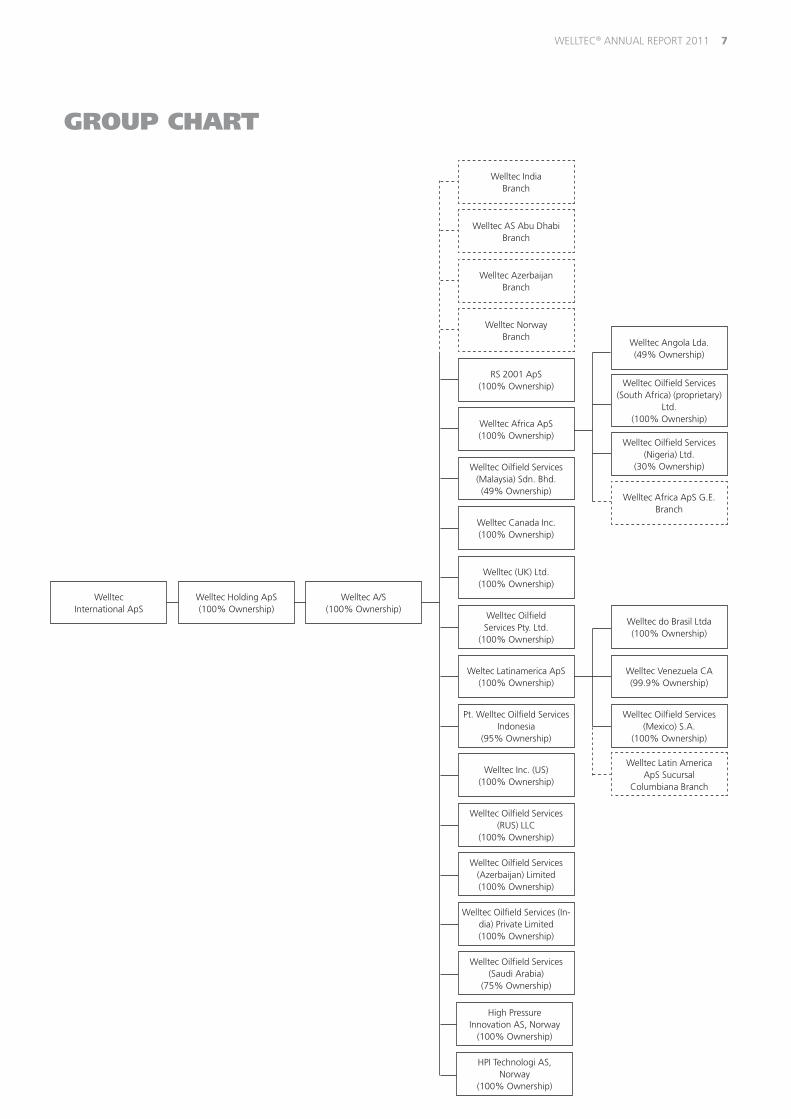

GRoup CHARt

Welltec indiabranch

Welltec As Abu dhabibranch

Welltec Azerbaijanbranch

Welltec norwaybranch

Rs 2001 Aps(100% ownership)

Welltec Africa Aps(100% ownership)

Welltec oilfield services (Malaysia) sdn. bhd.(49% ownership)

Welltec canada inc.(100% ownership)

Welltec (uK) ltd.(100% ownership)

Welltec oilfield services pty. ltd.

(100% ownership)

Weltec latinamerica Aps(100% ownership)

pt. Welltec oilfield services indonesia

(95% ownership)

Welltec inc. (us)(100% ownership)

Welltec oilfield services (Rus) llc

(100% ownership)

Welltec oilfield services (Azerbaijan) limited(100% ownership)

Welltec oilfield services (in-dia) private limited(100% ownership)

Welltec oilfield services (saudi Arabia)

(75% ownership)

Welltec Angola lda.(49% ownership)

Welltec oilfield services (nigeria) ltd.

(30% ownership)

Welltec do brasil ltda(100% ownership)

Welltec Venezuela cA(99.9% ownership)

Welltec oilfield services (Mexico) s.A.

(100% ownership)

Welltec latin America Aps sucursal

columbiana branch

Welltec Africa Aps g.e. branch

Welltecinternational Aps

Welltec holding Aps(100% ownership)

Welltec A/s(100% ownership)

high pressure innovation As, norway

(100% ownership)

hpi technologi As, norway

(100% ownership)

Welltec oilfield services(south Africa) (proprietary)

ltd.(100% ownership)

Welltec® AnnuAl RepoRt 2011 8

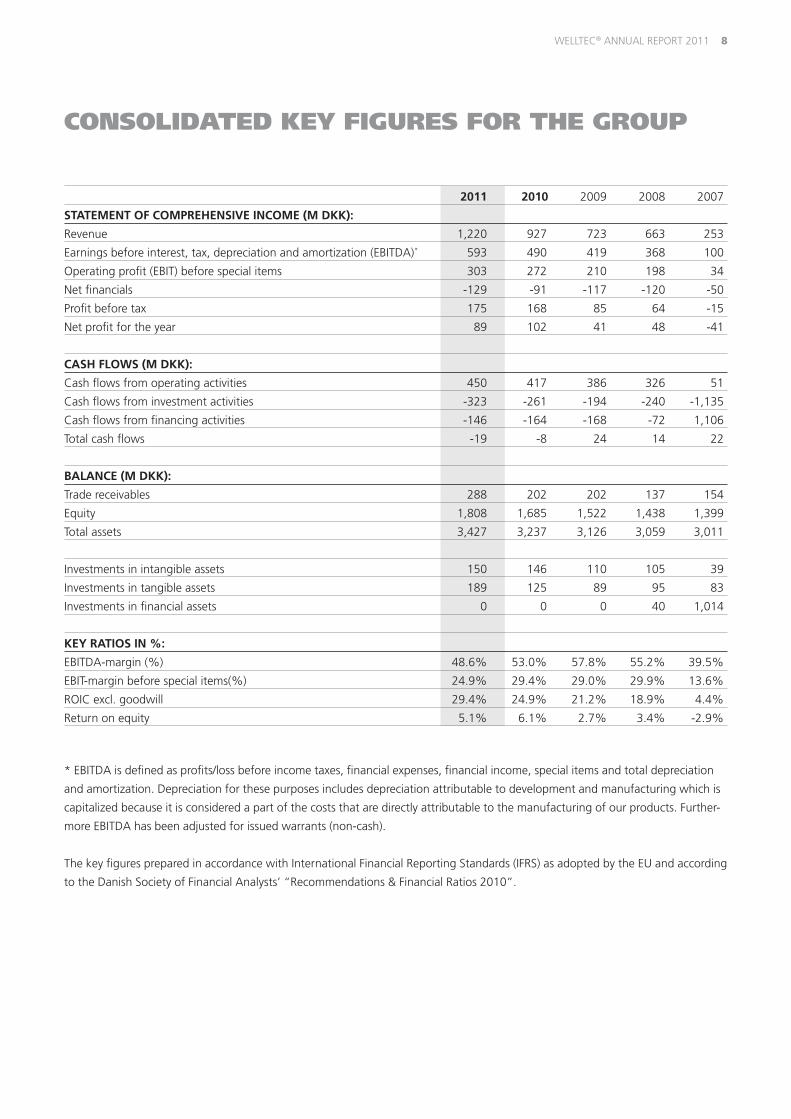

ConsolIDAteD KeY FIGuRes FoR tHe GRoup

2011 2010 2009 2008 2007

STATEMEnT Of COMpREhEnSIvE InCOME (M DKK):

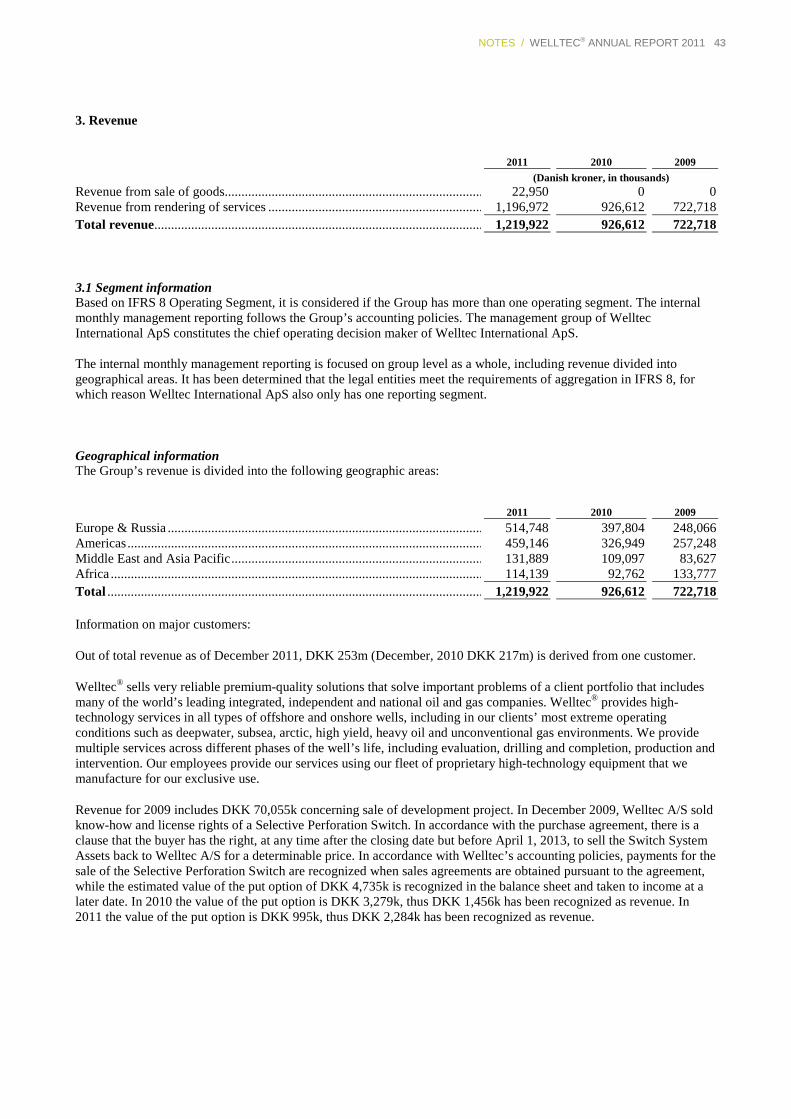

Revenue 1,220 927 723 663 253

earnings before interest, tax, depreciation and amortization (ebitdA)* 593 490 419 368 100

operating profit (ebit) before special items 303 272 210 198 34

net financials -129 -91 -117 -120 -50

profit before tax 175 168 85 64 -15

net profit for the year 89 102 41 48 -41

CASh flOWS (M DKK):

cash flows from operating activities 450 417 386 326 51

cash flows from investment activities -323 -261 -194 -240 -1,135

cash flows from financing activities -146 -164 -168 -72 1,106

total cash flows -19 -8 24 14 22

BAlAnCE (M DKK):

trade receivables 288 202 202 137 154

equity 1,808 1,685 1,522 1,438 1,399

total assets 3,427 3,237 3,126 3,059 3,011

investments in intangible assets 150 146 110 105 39

investments in tangible assets 189 125 89 95 83

investments in financial assets 0 0 0 40 1,014

KEy RATIOS In %:

ebitdA-margin (%) 48.6% 53.0% 57.8% 55.2% 39.5%

ebit-margin before special items(%) 24.9% 29.4% 29.0% 29.9% 13.6%

Roic excl. goodwill 29.4% 24.9% 21.2% 18.9% 4.4%

Return on equity 5.1% 6.1% 2.7% 3.4% -2.9%

* ebitdA is defined as profits/loss before income taxes, financial expenses, financial income, special items and total depreciation

and amortization. depreciation for these purposes includes depreciation attributable to development and manufacturing which is

capitalized because it is considered a part of the costs that are directly attributable to the manufacturing of our products. further-

more ebitdA has been adjusted for issued warrants (non-cash).

the key figures prepared in accordance with international financial Reporting standards (ifRs) as adopted by the eu and according

to the danish society of financial Analysts’ “Recommendations & financial Ratios 2010”.

Welltec® AnnuAl RepoRt 2011 9

MAnAGeMent CoMMentARY

RESulTS AnD OuTlOOK

Development in activities and finances

Welltec® achieved another successful year in 2011, secur-

ing record revenues of dKK 1,220 million in the period ended

december 31, 2011. this represents a growth of 31.7% year

on year in comparison to 2010 and is in line with the outlook

presented in the 2010 Annual Report.

the growth can be attributed to three main areas; an increase

of activity within our existing client base, commercialization of

new products and expansion within some geographical areas

brought about by an increase in tool fleet and client mix.

gross profit margin for the Year ending december 31, 2011

was 57.7% with the costs of service provision increasing rela-

tively to revenue as a result of required investments made in

the operational organization to perpetuate the growth plan.

Adjusted for issuance of non-cash warrants of dKK 33.3 mil-

lion, the administrative costs increased proportional to revenue.

profit from operations before special items (ebit) was dKK

303 million, a 11.5% increase on 2010. the ebit margin was

24.9% against 29.4% in 2010, reflecting the lower gross

profit margin compared to 2010.

profit for the year was dKK 89 million, a 12.2% decrease on

2010, reflecting the issuance of warrants (non-cash) to employ-

ees and increased taxes primarily related to tax provisions.

Welltec® once again recorded a positive cash flow from op-

erations, which in addition to investments in equipment and

development activities were used for installments and interest

payments.

Outlook

the outlook for the future remains positive. As the oil and gas

industry is risk averse due to the substantial economic costs

and business implications of failure or mishaps, many new

technologies fail to gain customer acceptance and therefore

do not succeed commercially. conversely, once a technology is

proven to be reliable, it secures a position of acceptance and

becomes a planned part of the work program. the group’s per-

formance is evidence of broad client acceptance by multiple oil

and gas companies around the world in many different operat-

ing environments.

Welltec® has created a unique position in the robotic well in-

tervention market through technology leadership and has the

highest market share of available robot tractors. growth will

continue in our tractor and intervention capabilities as well as

with new innovations. this is supported in 2012 by the intro-

duction of new products and services such as the Well cutter

tool.

furthermore Welltec® is in the process of increasing the organi-

zational capacity in order to support the future growth. this

process will continue into 2012.

Management expects growth for the group both in revenue as

well as ebitdA in 2012. Revenue is expected to be in the range

of dKK 1,350m to 1,500m and ebitdA margin is expected to

be at or around historic levels.

Events after the balance sheet date

february 1, 2012 we announced the completion of an us$

325 million aggregate principal amount 8 % senior secured

notes due 2019 offering. the 144A/Regs offering drew de-

mand from institutional investors in both europe and the us.

pRofit fRoM opeRAtions befoRe speciAl iteMs (ebit) WAs

dKK 303 Million, A 11.5% incReAse on 2010

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 10

the notes have been assigned a b1 rating by Moody’s (stable

outlook) and a bb- rating by standard & poor’s (stable outlook)

with equivalent corporate ratings. the notes have been listed

on the official list and admitted to trading on the euro Mtf

Market of the luxembourg stock exchange.

the net proceeds of the offering of the notes will be used to

refinance existing credit facilities, pay a special shareholder dis-

tribution and for general corporate purposes. part of the share-

holder distribution will be done through payout of extraordi-

nary divided from Welltec international Aps.

to complete the refinancing of existing facilities, the follow-

ing extraordinary dividends have been distributed in february,

2012. from Welltec Africa Aps dKK 31.4 million was distrib-

uted to Welltec A/s. from Welltec A/s dKK 728.6 million was

distributed to Welltec holding Aps. from Welltec holding Aps

dKK 787.3 million was distributed to Welltec international Aps.

in february 2012 Welltec® announced that the company,

through its wholly owned subsidiary Welltec canada inc. grew

its operations with the acquisition of endeavor e-line services,

the wireline portion of essential energy services, ltd. in calgary,

Alberta. the total cost of the business combination was agreed

to dKK 41.4 million. the transaction is financed through exist-

ing cash resources.

As the final acquisition date is february 2, 2012, it is not pos-

sible to provide details about the pre-acquistion balance sheet

and the total transaction costs.

no further significant events regarding the group’s activities

have occurred since december 31, 2011.

pROfIlE Of WEllTEC®

Who we are

As a leading provider of well intervention services to the oil

and gas industry, our robotic technology enables operators to

conduct interventions safer, faster and with higher accuracy,

thereby enabling the oil and gas industry to optimize the pro-

ductivity from wells draining a reservoir. Welltec® also provides

well completion products that help build flexible wells which

can be intervened through-out the life of the well, allowing

for a continuous adaptation of the well to the conditions in

the reservoir. by providing our services and solutions, we help

secure the most optimal use of the oil and gas resources , and

thereby enable a better supply of energy for people and allow

for improved production of reserves that otherwise couldn’t be

produced optimally.

historically, our founder began drawing up the plans for the

first Well tractor in 1987 and we were formally established

in 1989, changing our name to Welltec® in 1994. We initially

operated primarily in the north sea oil and gas market but have

since grown through new service development and geographi-

cal expansion to provide a wide range of services to our cus-

tomers all over the world.

today Welltec® is headquartered in Allerød, denmark, and

operates in all major hydrocarbon producing areas of the

world, employing more than 790 employees with offices in 22

countries.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 11

What we do

We provide our services and solutions in any environment

where hydrocarbons are produced – onshore or offshore,

in oil or gas wells, in mature oilfields and in fields under

development.

Most of our activities are related to the production phase of oil

and gas wells, but as we grow our business, our services and

solutions portfolio addresses the entire life cycle of a well, from

drilling and evaluation to completion, production and plug and

abandonment.

our well intervention services, from which we currently de-

rive most of our revenue, provides our customers with well

management solutions through a wide range of services, from

conveyance of well logging and surveillance measurements to

complex clean-out and maintenance operations.

in addition, we have in 2011 started the full-scale commerciali-

zation of our well completion products and solutions aimed at

enabling wells to come on stream faster with increased safety,

reduced cost and higher productivity.

We develop, test, manufacture and use proprietary technology

and equipment to provide our services and solutions. our pro-

prietary high-technology equipment is developed, tested and

manufactured in-house for our exclusive use.

our tractor based, light footprint technology (Well tractor®) has

represented a breakthrough in deploying and operating oil and

gas well intervention tools. compared to coiled tubing or simi-

lar heavy-duty equipment, our technology has several benefits,

including an ability to operate at high pressure and tempera-

tures, in large depths, over long distances and at high devia-

tions. our technology is also deployable in a faster and more

flexible manner compared to our competitors (including being

transportable by helicopter or truck) and provides for riserless

well intervention and fast rig up / rig down time.

At Welltec®, we believe that bringing technology to a higher

level will yield benefits for the industry. therefore we con-

stantly work at pushing the boundaries for what we can do to

sweep reservoirs better though using improved technology. our

development and engineering (d&e) department continues to

develop new technology that allows us to both enhance our

existing solutions and provide new ones. We invest heavily in

the development of new technology, and during 2011 we in-

vested more than 11.1% of our total revenues in d&e.

Where we work

We can work in virtually any environments where oil or gas is

being extracted regardless of whether it is a conventional or

unconventional reserve that is being drained and regardless of

whether it is onshore or offshore. Also in more complicated or

hostile environments, such as deepwater, subsea, arctic, or re-

mote areas, or in wells sweeping challenging reserves, such as

heavy oil, sAgd, tight oil, geothermal and unconventional gas,

our technology is delivering tangible benefits for the operator.

our operations are focused in three geographic marketing

areas: (1) europe & Russia, (2) Americas and (3) Middle east,

Africa (MeA) & Asia pacific (ApAc). our customers include key

national and a wide range of the world’s most renown major

stRAtegicAllY, We focus on dRiVing the coMpAnY’s deVelopMent

thRough focus on thRee stRAtegic theMes foR the coMing YeARs: gRoWth, stRength And position.

GRowtH

MAnAgeMent coMMentARY /

Welltec® plAns to stRengthen ouR business And opeRAtionAl Model to pRoVide betteR seRVices

foR ouR custoMeRs in A WAY Which endoRses long teRM RelAtionships.

stRenGtH

Welltec® AnnuAl RepoRt 2011 12

and independent oil companies (such as statoil, saudi Aramco,

petrobras, petronas, sonangol, peMeX, conocophillips, total,

exxonMobil, shell, bp, chevron and canadian natural Resourc-

es limited (cnRl)), from which we derive the majority of our

revenue, as well as other oilfield services providers.

WEllTEC’S STRATEGy

strategically we are focused on driving the company’s devel-

opment through focus on three strategic themes; growth,

strength and position.

We believe that challenging conventional solutions will contin-

ue to allow us to deliver disruptive technology that adds value

for our clients. coupled with improved service delivery and a

responsiveness to our client’s needs, we will deliver growth in

several key regions:

• north America: We aim to leverage our existing operations

in the united states and canada, where we believe our cur-

rent footprint in the conveyance market for unconventional

oil and gas plays will serve as a solid basis for the diversifi-

cation of our offerings to include high-technology services

such as conveyance, milling and cleaning that today are

served primarily by conventional technologies.

• brazil: Recent offshore discoveries and our existing business

with petrobras constitute a potential for significant growth

in activities.

• Russia/cis: in the Russian market, we have been providing

mostly wireline conveyance services to many of our custom-

ers but we believe that there is potential for selling a broad-

er range of services, including more complex and high-value

services and solutions to our large gas producing customers.

• Middle east: We believe that there are also opportunities in

the Middle east, where the national oil companies represent

a large growth potential, in particular in saudi Arabia, uAe,

Qatar and Kuwait.

• southeast Asia: the large offshore activities in Malaysia, bru-

nei, Vietnam and indonesia represent growth opportunities,

where our current track record can help us get even further

work.

Build a stronger and more resilient company

We plan to continue to strengthen our business and opera-

tional models to provide better services in a way that endorses

long term relationships with our customers. Working more

closely with our customers over longer periods of time ensures

not only a more stable revenue stream but also allows Welltec®

to develop faster and more accurately solutions to meet our

customers’ challenges; thereby perpetuating the value cycle.

We have begun several projects which support this initiative,

including:

• expansion of our service offerings and product ranges to

broaden our portfolio and reduce dependency upon a single

offering.

• establishing more direct, contractual ties with our customers

as well as longer duration agreements which secures more

planned, dedicated work.

• streamlining our organizational structure to reflect our value

chain, and thereby matching a global, company-wide inte-

gration of services where roles, responsibilities and interac-

tions between different parts of the organization are being

clarified to improve performance;

• Recruiting and keeping new engineering and management

talent; and

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 13

• introducing scalable structures and procedures across our

organization that support our growth, primarily through lev-

eraging our already established it-driven infrastructure and

ensuring that knowledge is built into the structure of the

organization rather than depending on specific individuals.

Maximize the value we provide to our customers

Welltec® is focused on providing services where we can be

unique and avoiding those markets where services are effec-

tively commoditized. We intend to attract and satisfy more ref-

erence customers like statoil through a focus on global account

management, by maintaining our focus on direct customer re-

lationships and by accelerating the rate of technology replace-

ment to our offerings across all geographies.

We pursue strategic partnerships with other service providers,

such as selected wireline providers, vessel providers and tech-

nology companies, where our combined offerings can be pre-

sented to customers as a complete solution. Welltec® can posi-

tion ourselves as the lead contractor when required, thereby

gaining direct customer access in both tender and transactional

engagements.

furthermore we actively engage in developing new solution

concepts that addresses our customer’s largest challenges, such

as riserless well intervention services for subsea wells, plug and

abandonment of wells and open-hole intervention services in

horizontals that require integrated, specialized solutions and

equipment. in due time, these solutions will provide significant

value to our customers as they will enable them to redefine the

manner in which they operate today. We believe the value crea-

tion this delivers for our customers will be rewarded through

an increase in our own business. overall, Welltec’s goal is to

ensure that we maintain our status quo as a top provider of our

current offerings while simultaneously providing unique, new

solutions in other segments. our pipeline of new service and

product initiatives are aimed at developing a diversified and

growing business in terms of revenues and margins in 2012

and beyond.

WEllTEC®’S COMpETITIvE STREnGThS

position ourselves within important industry growth

areas

over the last decade, operational and capital expenditure by

oil and gas companies has increased. We expect this trend to

continue given the ongoing efforts to improve production from

existing fields and search for new reserves. forecast spend for

the major oil and gas companies is up and we believe this trend

will favor companies such as Welltec® that have advanced and

differentiated technological offerings covering all phases of the

well lifecycle. Moreover, we expect demand for well interven-

tion services to increase relatively unaffected by oil price fluc-

tuations due to capex budgets versus opex budgets, which are

historically less dependent on oil prices.

from a global perspective, oil fields are maturing and new dis-

coveries are not keeping pace with declines or demand consid-

eration. this combination of increasingly mature fields, reduced

quantity and size of new discoveries and increasing global

demand represents a huge challenge for all. Welltec’s expecta-

tions are that our value proposition of developing methods for

increased reservoir optimization will resonate with our custom-

er’s around the world as they seek to increase the life span of

existing fields.

new discoveries are increasingly being made in areas present-

ing significant operational complexity for exploration and

development. Almost half of all newly discovered oil reserves

since 2000 have been made in offshore deepwater or ultra

deepwater. An increasing portion of new supply is also coming

from unconventional reserves (such as shale gas or shale oil)

adding further complexity in the form of more horizontal well

designs. the shift in discoveries and resource types have also

increased the technical risk of projects and the requirements of

the equipment and services necessary to handle these extreme

operating conditions, which have also driven the need to use

ouR goAl is to ensuRe thAt We MAintAin ouR stAtus Quo As A top pRoVideR of ouR

cuRRent offeRings While siMultAneouslY deVeloping otheR uniQue offeRings.

posItIon

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 14

advanced technologies in well intervention. it is our experience

that oil and gas companies are becoming more likely to work

with suppliers of high-quality services as they deliver a higher

long-term value. With the increased complexity and costs of

new discoveries, we believe that well interventions have be-

come an attractive economic proposition compared to explor-

ing for new reserves. Welltec’s technology, which has a proven

record of successful operations in these environments, will

continue to be in demand.

Superior technology offering

the increased focus on enhancing oil and gas recovery rates

and improving well profitability has led to an increasing indus-

try acceptance of the robotic technology we offer.

Well intervention services increases well profitability through

increased recovery rates and cash flow from production. given

the challenges of sustaining oil and gas production to meet de-

mand we expect the well intervention market will grow signifi-

cant in the coming years. due to its superior performance, we

expect robotic technology to grow even faster than the market

for conventional intervention technologies, and gradually even

replacing older methods. Robotic intervention technology is

superior to these conventional methods because:

• it can be safer given its smaller footprint and lower num-

ber of personnel involved, leading to significant health and

safety advantages for our customers;

• it is less intrusive because it requires a smaller set up space

and a more limited amount of equipment to be inserted into

the well, typically resulting in less damage to the well;

• it can be an order of magnitude faster than conventional

methods due to deployment and rig up times; and

• it is more cost efficient, both in terms of lower direct in-

tervention costs and lower future costs for subsequent

interventions

Sustainable, protected market leadership

We were pioneers in the well intervention services market with

our robotic technology and continue to have a leadership posi-

tion. We believe we have one of the largest inventories of op-

erational tractors globally, and in 2011 we believe that we per-

formed more than half of all well interventions using tractors.

our technological leadership has been recognized by both cus-

tomers and industry associations, and we have been awarded

several industry leading recognitions, such as the 2010 spot-

light technology Award. We have also accumulated many

“firsts” for well-intervention tools within our industry, including

what we believe are records with our Well tractor for deepest

well intervention and highest deviation well intervention, as

well as deepest water depth intervention using riserless light

well intervention.

to maintain our leading position and further grow our business

we continue to focus on technological innovation. We often

work in conjunction with our customers on developing new

applications and tools in order to solve specific needs of our

customers. this enables us to develop a deep understanding

of our customers’ business requirements and the challenges

they face while strengthening our relationships with them. We

continue to devote considerable time and resources to develop-

ment and engineering, and are working on several projects to

deliver the next generation of tools and solutions.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 15

hand-in-hand with our dedicated efforts on technology innova-

tions, we vigorously protect our technology and intellectual

property. We have implemented a rigorous intellectual property

rights strategy, including the registration of over 110 patent

families with more than 2.000 individual patents and patent

applications at various stages of registration or application.

We have measures in place to avoid unintended dissemina-

tion of our trade secrets and know-how. this includes in-house

manufacturing of key components, operating our tractors and

tools by our own personnel and restricting access to key manu-

facturing data such as blue-prints.

We believe that our leading position will be maintained and

our business will grow as a consequence of our commitment

to quality in execution and customer service. in the market for

well intervention services, technical reliability and overall service

quality are significant factors (along with price) in our custom-

ers’ purchasing decisions. through continuous evolution and

improvement of our work processes, we believe we offer supe-

rior service quality.

RISKS RElATED TO OuR BuSInESS

Business and industry related risks

our business is affected by the level of expenditures of compa-

nies engaged in the production, exploration and development

of oil and gas.

traditionally, the oil and gas industry is highly cyclical and ex-

penditures can be cancelled or reduced on short notice. While

demand for our services is primarily dependent on operating

expenditures by the oil and gas industry (primarily optimizing

recovery rates for existing wells), demand for our services also

depends on the capital expenditures of this industry (primarily

drilling new wells). A decrease in operating expenditures by the

oil and gas industry may have adverse effects on our revenue

and profits in the shorter term, while a decrease in the capital

expenditures of this industry may have adverse effects on our

revenue and profits in the longer term.

the total level of expenditures by the oil and gas industry for

production, exploration and development of oil and natural

gas reserves is sensitive to a number of factors, primarily oil

and gas prices and the industry’s view of future oil and gas

prices, which historically have been volatile. long-term oil and

gas prices are affected by numerous factors, including (i) the

demand for energy, which is affected by worldwide popula-

tion growth and general economic and business conditions; (ii)

the ability of the organization of petroleum exporting coun-

tries (opec) to set and maintain production levels; (iii) oil and

gas production by non-opec countries; (iv) the cost of explor-

ing for, producing and delivering oil and gas; (v) political and

economic uncertainty and socio-political unrest; (vi) the level of

worldwide oil exploration and production activity; (vii) tech-

nological advances affecting energy consumption; and (viii)

weather conditions.

if oil and gas prices were to increase significantly, companies

engaged in the production, exploration and development of

onshore and offshore oil and gas are more likely to focus on

exploration and development of new reserves rather than

seeking to increase production and recovery rates through well

intervention. further, if oil and gas prices were to decrease sig-

nificantly, well intervention may not be cost-effective for these

companies, although expenditures on well intervention would

likely be reduced less than capital expenditures. since we cur-

rently derive a majority of our revenues from well intervention

services, a significant increase or decrease of oil and gas prices

may have an adverse effect on our revenue and profits.

Skilled technical personnel

highly-skilled personnel are required to develop, manufacture

and operate Welltec®’s sophisticated equipment and support

our business. Management believes it has put in place an entre-

preneurial, international and flexible organization that is attrac-

tive to future and current employees. to date, the group has

successfully recruited, absorbed, trained and retained excellent

people, and expects to continue doing so.

We belieVe thAt ouR leAding position Will be MAintAined And ouR business Will gRoW As A conseQuence of ouR coMMitMent to QuAlitY in eXecution And custoMeR seRVice.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 16

Intellectual property

the group’s business relies upon the proprietary knowledge

and innovation know-how. We have put in place an extensive

series of legal, human, process, physical and it security meas-

ures and controls to protect our intellectual property. Among

others, these measures include legal protection via patents and

patent applications pending on our sophisticated equipment

and contractual agreements.

Environmental performance

Welltec® considers quality, health, safety and respect for the

environment to be an integral part of our business. We build

quality, health, safety and respect for the environment into our

processes starting at the design phase and track performance.

Keeping high environmental standards is critical to ensure both

future and present contracts. there are no environmental inci-

dents to report. We believe our sophisticated clean technology

is part of the solution that helps our clients meet the world’s

need for energy security while at the same time reducing

greenhouse gas emissions and promoting sustainable economic

growth.

financial risks

Financial exposure

due to the group’s foreign activities and credit facilities in

foreign currencies, its profit/loss, cash flows and equity are

affected by changes in exchange rates and interest rates for a

number of currencies, primarily us dollars.

Foreign exchange fluctuations

the reporting currency of the group is the danish Kroner and

the functional currency of each of the groups’ subsidiaries

is that of the country in which the subsidiary is domiciled. A

significant proportion of the group’s revenues, expenses and

other liabilities are denominated in currencies other than the

danish Kroner, in particular us dollars. fluctuations in the value

of other currencies as compared with the danish Kroner could

result in translation losses or gains. the company has to a

significant extent hedged its net position in us dollars through

certain foreign exchange contracts.

Interest rate risk

since our primary financing is senior secured bonds at a

fixed interest rate, the interest rate risk has been substantially

reduced.

Credit risk

the group’s services are provided to a variety of contractual

counterparties and are therefore subject to the risk of non-

payment for services or non-reimbursement of costs. counter-

party credit risk is believed to be low because all of the group’s

customers are large corporations in the oil industry deemed

creditworthy. therefore, Management assesses that there are

no significant risks involved.

Liquidity risk

our ability to make payments on and to refinance our indebt-

edness, and to fund planned capital expenditures and other

strategic investments will depend on our ability to generate

cash in the future. this, to a certain extent, is subject to gen-

eral economic, financial, competitive, legislative, regulatory

and other factors that are beyond our control. We anticipate

that we will continue to make capital investments to develop

and purchase additional equipment to expand our services,

increase our capacity and replace existing equipment. our

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 17

capital investments require cash that we could otherwise ap-

ply to other business needs. however, if we do not incur these

expenditures while our competitors make substantial invest-

ments, our market share may decline and our business may be

adversely affected.

it is the group’s policy that capital raising and distribution of

cash are managed centrally by the group’s finance department

to the extent it is deemed appropriate. the group has the op-

tion of adjusting centrally the cash outflow in investments in in-

tangible assets and property, plant and equipment in denmark.

based on our current level of operations and anticipated cost

management and operating improvements, we believe our

expected cash flow from operations, available cash, proceeds

from bond issuance and other sources of available financing

will be adequate to meet our future liquidity.

uncertainty relating to recognition and measurement

the preparation of financial statements and related disclosures

in conformity with international financial Reporting standards

as adopted by the eu requires the group to make estimates

and assumptions that affect the reported amounts of assets

and liabilities, the disclosure of contingent assets and liabilities

and the reported amounts of revenue and expenses. the ac-

counting policies involved “critical accounting judgments and

key sources of estimation uncertainty” (see note 2), because

they are particularly dependent on estimates and assumptions

made by the group about matters that are inherently uncertain.

A summary of all the group’s significant accounting policies is

included in note 1 to the annual report.

the group bases its estimates on historical experience and on

various other assumptions that are believed to be reasonable

under the circumstances, the results of which form the basis for

making judgments about the carrying values of assets and lia-

bilities that are not readily apparent from other sources. Actual

results may be different from these estimates under different

assumptions or conditions.

unusual circumstances

there were no unusual circumstances in 2011 that affected the

annual report.

CORpORATE SOCIAl RESpOnSIBIlITy

the following statement of corporate social Responsibility

(csR) pursuant to the danish financial statements Act section

99a is part of the Management’s Review in the 2011 Annual

Report.

Corporate Social Responsibility policy

At Welltec®, we believe that we share a responsibility which

not only includes the interests of our stakeholders but also, due

to the nature of the business, extends beyond this in a greater

context.

this responsibility is defined in the various polices which have

been developed and implemented to comply with the objec-

tives of csR. the principles encompassed in the policies have

been developed and continue to be reviewed against and up-

dated by reference to relevant codes of corporate governance

and international standards including the united nations (un)

universal declaration of human Rights, the international labor

organization (ilo) declaration on fundamental principles and

Rights at Work, the guidelines for Multinational enterprises

established by the organization for economic cooperation and

We AnticipAte thAt We Will continue to MAKe cApitAl inVestMents to deVelop And puRchAse AdditionAl eQuipMent to eXpAnd ouR seRVices, incReAse ouR cApAcitY And ReplAce eXisting eQuipMent.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 18

development (oecd), the Rio declaration on environment and

development, the un convention against corruption and ap-

plicable legislation governing the interest of our stakeholders.

the areas currently covered by our csR policies are:

• business ethics

• Anti-corruption

• health, safety and environment

• employment

• customers

the policies are approved by the board of directors; they have

been communicated to all employees and are posted on the

corporate intranet portal accessible to all employees. it is the

responsibility of each and every manager to ensure compliance

with the policies.

the chief executive officer has delegated the responsibility of

monitoring compliance to the following Vice presidents and

chiefs for their respective areas:

• legal

• human Resource

• Qhse (Quality, health, safety, environment)

• commercial

Key indicators and reports are monitored and appropriate au-

dits performed and followed up.

Business Ethics

Policy

Welltec® generally encourages, operates and enforces the fol-

lowing management principle: “At Welltec®, we say what we

do and we do what we say”. this general management princi-

ple facilitates certainty to all our stakeholders that predictability

and reliability are the norm when dealing with a Welltec® repre-

sentative. We consider this predictability and reliability as key

drivers in our approach to business ethics.

Implementation

our code of business ethics is embedded as an integral part of

our overall csR procedures, and is an underlying driver in all we

do.

procedurally, it is an integral part of our top management pro-

cedures on mission, vision and values, as well as the Welltec®

corporate social Responsibility policy – all of which is available

to all employees on the corporate intranet. below the primary

policies are presented

our employees and officers should conduct their business af-

fairs in such a manner that our reputation will not be damaged

if the details of their dealings should become a matter of public

discussion.

our conviction to uphold ethical standards in all our corporate

activities is a common mindset of all our employees. We strive

to do business with customers and suppliers of sound business

character and reputation and we do not knowingly support any

public or private organization, which supports discriminatory

policies or practices.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 19

We expect all our employees to perform their work with hon-

esty, truthfulness and integrity, hereunder to respect and abide

by the guidelines expressed in this policy.

it is our policy to comply with all governmental laws, rules and

regulations applicable to our business.

All employees are responsible for the immediate and accurate

reporting to higher management of work-related information

of importance to this policy.

Key Results in 2011 and Future Plans

Maintaining high business ethical standards is part of the duty

for all employees in the company.

in 2011, there have been no major events caused solemnly by

an employee’s non-compliance with our business ethical code.

going forward in 2012, we will be continuously working on

keeping our high business ethical principles. As we see it busi-

ness of high principle

• generates greater drive and effectiveness because people

know that they can do the right thing decisively and with

confidence

• Attracts high-caliber people more easily, thereby gaining a

basic competitive and thereby profit edge.

• develops better and more profitable relations with cus-

tomers and suppliers, as well as with the general environ-

ment, such as the general society, competitors and other

stakeholders.

Anti-Corruption

Policy

Welltec® maintains a general screening program applicable for

agents, representatives and joint venture partners in territories

where transparency and corruption are imminent issues. this

screening program comprises of a questionnaire combined with

a review process under which a potential agent, representa-

tive and joint venture partner is screened for undue relation-

ships and channels of influence. further during such process,

a search up against applicable european and us lists of special

designated nationals will be done.

further, Welltec® operates a zero-tolerance policy towards cor-

ruptive behavior of employees and representatives. Any indica-

tion implying corruption will immediately trigger an internal

investigation led by the legal department and supplemented

by the hR department.

Implementation

in 2011 the new uK Anti-bribery Act became effective and this

required an examination of existing policies and compliance

with the new legislation in relation with Welltec®’s operations

in the uK.

in addition, Welltec® did in 2011 expand its partner screening

process, by the adaption and application of the methods from

common export control end user processes. to this extent,

Welltec®’s partner screening process now entails screening up

against the current lists of special designated nationals utilized

in export control end user screening.

Key Results in 2011 and Future Plans

As a result of this policy one ‘whistle-blowing’ incident was

recorded and duly acted upon. one incident was discovered

during internal control and acted upon.

two screenings took place. no agents were turned down. the

screening process has resulted in transparency with regard to

relationships as well as interests and hence an increased likeli-

hood of mitigating the risk of corruption.

RespeCtWe eXpect All ouR eMploYees to peRfoRM theiR WoRK With honestY, tRuthfulness And

integRitY, heReundeR to Respect And Abide bY the guidelines eXpRessed in this policY.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 20

Welltec® will continue the improvement of the screening pro-

cedures, review processes and further incorporate additional

fcpA (foreign corrupt practices Act) based initiatives. further,

Welltec will continue to monitor initiatives and guidelines is-

sued by oecd and transparency international to identify poli-

cies and procedures that in the future will improve measures

against corruption.

in 2012 Welltec® will further develop and strengthen its efforts

within the consolidated compliance functions, which covers not

only csR related functions, but also trade and export control

compliance.

health, Safety and Environment

Policy

Welltec® generally promotes actions, attitudes and decisions

that facilitate maximum awareness towards potential health

and safety hazards thereby facilitating maximum alertness with

the objective to reduce and minimize the number of incidents.

Welltec® imposes certain duties upon employees and subcon-

tractors which require them to conform to any local statu-

tory or legal safety regulations in the location where we are

operating.

it is the intention of Welltec®, so far as is reasonably practica-

ble, to ensure that:

• the provision, commissioning and maintenance of plant and

systems of work are safe and without risks to health.

• Arrangements for use, handling, storage and transport of

articles and substances for use at work are safe and without

risks to health.

• Adequate information is available with respect to articles

and substances used at work detailing the conditions and

precautions necessary to ensure that when properly used

they will be safe and without risk to health.

• employees are provided with such information, instruction,

training and supervision as is necessary to secure their health

and safety.

• the maintenance of all plant, machinery and equipment

is safe not only to employees, and subcontractors and but

to any person who may be affected with regards to any by

premises or operations under our control.

• the working environment of all employees is safe and with-

out risks to health and adequate provisions are made with

regard to the facilities and arrangements for their welfare at

work.

• the risk of driving, which is assessed to be a potential safety

risk faced by our employees, is minimized.

it shall be the duty of all employees at work:

• to take reasonable steps for the health and safety of them-

selves and of other persons who may be affected by their

acts or omissions at work.

• to co-operate with the organization in regards to any duty

or requirement imposed on the employer or any other per-

son by or under any of the relevant statutory duties.

based on our mission, vision and values, Welltec® aspires to be

the leading global provider of well services to the oil- and gas

industry with focus on protection of the environment and the

surrounding society.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 21

environmental preservation is regarded as being of paramount

importance. We integrate environmental aspects in all decisions

and actions, and we seek to plan and execute all activities in a

manner that lowers resource consumption and possible envi-

ronmental hazards.

Implementation

hse WAll - central board has been created with the most im-

port information in regards to hse.

hse intRoduction - All new hires attend an hse introduction

program where all hse policies, procedures and practices are a

part of the agenda. upon completion of the hse introduction,

employees read and sign an acknowledgement statement en-

suring that they have read and understand all Welltec govern-

ing procedures.

hse tRAining - health and safety training is an integral part of

all Welltec internal courses.

Qhse Meetings - At the bases – worldwide - health and safety

meetings as well as briefings are held monthly where all base

employees shall attend.

MAnAgeMent Meetings - As a result of the general ap-

proach, the weekly corporate management meetings are

opened with a review on any health and safety issues which

have occurred in the preceding week.

hse sYsteMs And pRogRAMs – for monitoring progress we

use incident Reporting system 3 (iRs3), safety card observa-

tion program (scop), health and safety statistics and Annual

internal Audits.

hse coMMittee - aims to influence Welltec business in a way

that best serves and inspires the working individual to achieve

the highest degree of safety and health practices through con-

tinuous improvement

hse officeRs / hse MAnAgeRs - All Welltec bases / locations

have a hse officer or an hse Manager employed. his/hers

main tasks is to lead the hse work at the base; ensuring that

all Welltec policies and procedures plus the local legislation is

implemented and followed

Key Results and Future plans

HSE Statistics

Welltec® is monitoring the hse performance by tracking the

Medical treatments (Mto), lost time incidents (lti), Restricted

Work cases (RWc), Vehicle accidents and fatalities (ftl). Also

the lost time incidents frequency, the total Recordable case

frequency and the Vehicle Accident frequency is also measured

and monitored. it is the hse officer / hse Manager´s responsi-

bility to ensure that the hse statistics are updated monthly. the

statistics are posted on the hse Wall and are also used during

the regional performance meetings.

We can observe from the graphs below that the total of Mto,

lti, RWc has decreased in 2011 even though the amount of

working hours has increased from 1,010,798 to 1,123,393

hours. the Vehicle accidents / collisions have increased however

the amount of kilometers driven has increased dramatically

(from 2,371,756 to 3,067,145). note that none of the vehicle

accidents / collisions has resulted in personal injury.

With more than 5 years of experience, incident Report-

ing has been developed as a comprehensive and extensive

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 22

non-conformance and hse performance reporting system, pro-

viding data for regular reviews of hse performance which can

be selected from a population of all listed Welltec® bases.

With Welltec’s business growing fast and with our client re-

quirements increase – playing closer scrutiny to the special

points of interest related to resolution of issues documented.

Welltec® therefore introduced a new and improved hse appli-

cation in november 2011. As the system is still new, and due to

the limited data entry, the iRs3 statistics cannot be a contribut-

ing factor in our performance monitoring at this point.

SCOP statistics

scop stands for Welltec´s safety card observation programme,

a programme aimed at preventing incidents and injuries.

the main objective of the program is to train each member

of the line organization to eliminate incidents and injuries by

skilfully observing people as they work, talking with them to

correct their unsafe acts, and encouraging them to follow safe

work practices.

Welltec® Qhse rolled out the scop program globally in

september 2011 and the results of the program are not yet

concluded. the statistics are used for monitoring trends either

within a local base or even globally.

Audits (internal)

our global Qhse continuously performs audits of selected

bases in order to assess the effectiveness of the continuous im-

provement cycle of the internal Quality and hse Management

system of Welltec. the audit tool is the prime instrument for

measuring the business interface between Welltec hQ and

Welltec bases worldwide and between the Welltec bases and

the oil operators.

the real product of the audit process is to create specific action

points for the Welltec base continuous improvement process.

in 2011, global Qhse audited hR, d&e Mechanical, com-

mercial, and sourcing based at headquarters and 9 bases

worldwide.

Environmental report

in 2011 the Welltec® facilities in denmark were audited by the

Municipality, nature and environment Auditor. the scope of

the audit concentrated in the environmental re-certification.

the audit results showed that great improvements were made

and therefore Welltec® was upgraded to category 1; which is

the highest scale achievable. in order to sustain the category 1,

great efforts were made ensuring that the environmental report

also contained a detailed description of the current environ-

mental state including continuous improvements, future plans

and detailed monitoring of the consumption of chemicals,

waste, electricity, heat and water.

Audit results (3rd party)

Welltec® is been also been audited by 3rd party companies as

well such as “det norske Veritas” (dnV) for ensuring compli-

ance with iso9001:2008, oil operators for assessing Welltec´s

ability to effectively manage the hazards associated with the

services provided to the oil operator as well as Authorities.

Welltec WoRldWide heAlth And sAfetY stAtistics

Figure 1: Worldwide HSE Statistics

Welltec WoRldWide Vehicle stAtistics

Figure 2: Worldwide Vehicle accidents and collision statistics

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 23

As Welltec® holds an iso 9001:2008 certificate, surveillance

audits are performed by dnV on a yearly basis as well as re-

certification audits every 3 years.

in 2011; Welltec dK has been audited by dnV, Welltec Angola

has been audited by totAl, Welltec colombia by Ruc, Welltec

brazil by petrobras, Welltec canada by certification of Recong-

nition and Welltec Mexico by peMeX. All audits results showed

increasing improvement.

Safety culture survey

in June 2011, Welltec´s first safety culture survey was born

and launched in denmark, norway, us and canada. the pur-

pose of the audit was to identify trends within the same geog-

raphy (denmark and norway as well as us and canada) and

to get an idea of how the employees perceived safety within

Welltec®.

the results were very positive, for example 70% of the partici-

pants said that the hse incidents/investigations are handled

appropriately in Welltec®, 100% of the participants they have

no problem of stopping an unsafe job/task.

Employment

Policy

the employment policy at Welltec is based on the fundamen-

tal belief that the employee as an individual and as part of a

group constitutes the key asset. hence, and with due consider-

ation to the working field and conditions, measures which go

beyond the norm are practiced to safeguard and maximize the

health and safety aspects of the employees when performing

their duties.

Welltec® recognizes a shared responsibility on behalf of all em-

ployees to exercise the principles of mutual respect and dignity

in all working relationships and consequently enforces a policy

of zero tolerance with regard to harassment or discrimination.

Welltec practices the principle of equal employment opportuni-

ty without regard to race, religion, national origin, gender, age,

physical disability or political affiliation.

Implementation

We apply a principle of duality in recruitment processes and

also use objective profiling tools to assess candidates.

We regularly measure physical and psychological work climate

and we closely follow up on undesired results from the work

place surveys.

for long-term ill employees, we work closely and actively with

local authorities and community centers in order to define indi-

vidual solutions, including definition of flex jobs (permanently

reduced work time), temporarily reduced work time, redefini-

tion of work area, etc.

employees are covered by a collective health insurance as ap-

propriate in country of employment. Where applicable, insur-

ances include psychologist assistance in connection with stress

and accidents/traumas.

Key Results in 2011 and Future Plans

Key results for 2011 include in addition to the above men-

tioned areas:

• At least half a dozen long term ill employees have benefit-

ted from the individual solutions approach to their work

assignment.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 24

• More than 100 employees have followed internal training

in the areas of field engineer courses, special equipment

courses, project Management courses, etc.

• compliance reviews in a number of the countries in which

we operate – this has led to improved compliance.

• Results of the 2011 Work place survey in denmark indicate

no big issues, and subsequent sector action plans primarily

address physical workplace improvements.

• Welltec will continue work to improve employee condi-

tions, and expect during 2012 to launch additional initia-

tives such as a new hR it system to support information

capture, update and reporting thus enabling better focusing

of resources and improved decision making and worldwide

processes for global performance appraisal, employee on-

boarding, etc.

Customers

Policy

Welltec perceives customers as business partners and pursues

an open and transparent partnership characterized by frequent

and relevant dialogue with focus on serving their interests.

it is the policy of Welltec to provide services and products that

excel in quality and at all times conform to best practices as ex-

ercised by industry, herein adherence to responsible standards

of performance with particular consideration to protect the

environment and the health and safety of all people involved.

in situations, where a customer or regulatory body wishes to

investigate a non-successful operation or an issue of regulatory

non-compliance a failure investigation is initiated to ensure:

• that investigations requested by the clients are performed.

• that conformed and controlled methods are followed when

handling misruns; covering from job planning, equipment,

procedures, communication to human factors.

• lessons learned are properly communicated throughout the

organization in order to minimize the risk of re-occurrence.

• A failure report is prepared on a timely manner for the cli-

ent, prior to officially closing the investigation.

All non-optimal or non-compliant findings from the internal

Welltec investigation are openly disclosed to the customer or

regulatory body in order to achieve maximum transparency and

optimal lessons learned, enabling hindrance of repetition of

any such issues.

Implementation

to ensure continuously improvement of service quality on jobs

performed a training program “job editor champions” were

launched, to ensure the data quality remains high during the

high growth we are currently facing.

Key Results in 2011 and Future Plans

As a result of the constant focus on service quality throughout

the organization and the new training program “job editor

champions” Welltec has had an increase in service quality from

2010 to 2011.

the focus to drive dialogue with customers has led to an

increased focus on meeting with our customers regularly. in

2011, we have registered more than 8300 meetings in our

cRM system, versus the 2890 meetings registered in 2010.

it is the policY of Welltec® to pRoVide seRVices And pRoducts thAt eXcel in QuAlitY

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 25

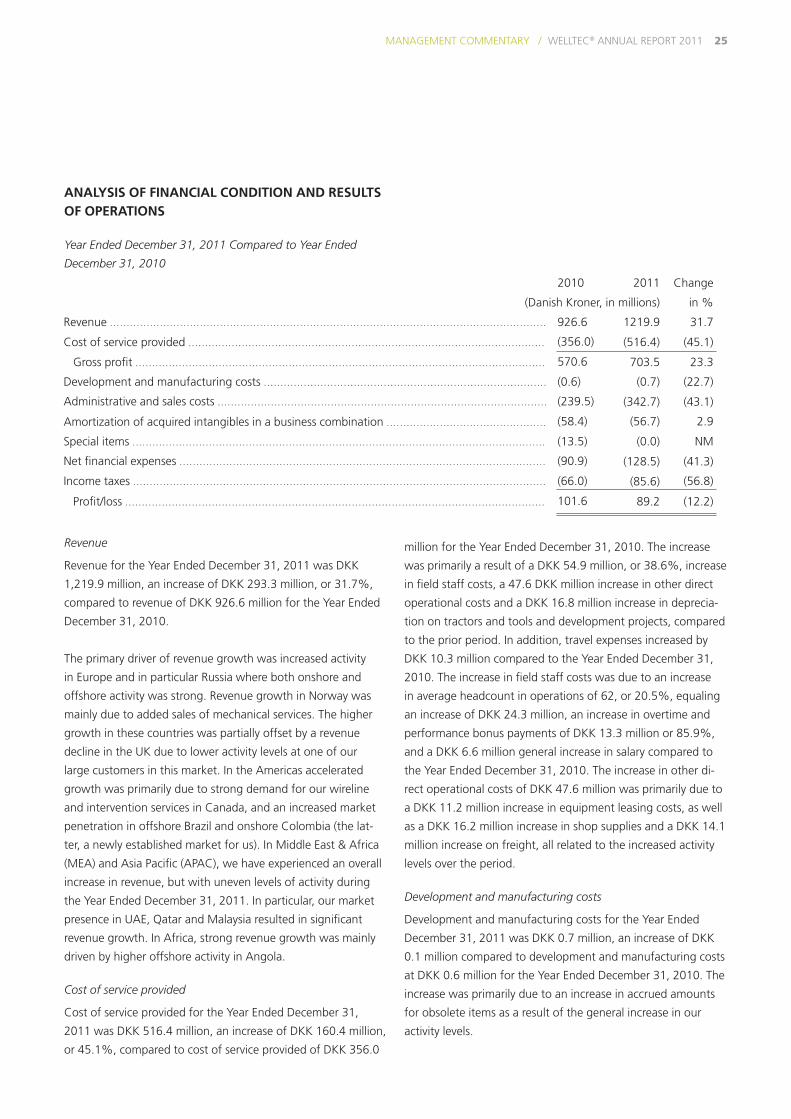

2010 2011 change

(danish Kroner, in millions) in %

Revenue ................................................................................................................................... 926.6 1219.9 31.7

cost of service provided ........................................................................................................... (356.0) (516.4) (45.1)

gross profit ........................................................................................................................... 570.6 703.5 23.3

development and manufacturing costs ..................................................................................... (0.6) (0.7) (22.7)

Administrative and sales costs ................................................................................................... (239.5) (342.7) (43.1)

Amortization of acquired intangibles in a business combination ................................................ (58.4) (56.7) 2.9

special items ............................................................................................................................ (13.5) (0.0) nM

net financial expenses .............................................................................................................. (90.9) (128.5) (41.3)

income taxes ............................................................................................................................ (66.0) (85.6) (56.8)

profit/loss .............................................................................................................................. 101.6 89.2 (12.2)

AnAlySIS Of fInAnCIAl COnDITIOn AnD RESulTS Of OpERATIOnS

Year Ended December 31, 2011 Compared to Year Ended

December 31, 2010

Revenue

Revenue for the Year ended december 31, 2011 was dKK

1,219.9 million, an increase of dKK 293.3 million, or 31.7%,

compared to revenue of dKK 926.6 million for the Year ended

december 31, 2010.

the primary driver of revenue growth was increased activity

in europe and in particular Russia where both onshore and

offshore activity was strong. Revenue growth in norway was

mainly due to added sales of mechanical services. the higher

growth in these countries was partially offset by a revenue

decline in the uK due to lower activity levels at one of our

large customers in this market. in the Americas accelerated

growth was primarily due to strong demand for our wireline

and intervention services in canada, and an increased market

penetration in offshore brazil and onshore colombia (the lat-

ter, a newly established market for us). in Middle east & Africa

(MeA) and Asia pacific (ApAc), we have experienced an overall

increase in revenue, but with uneven levels of activity during

the Year ended december 31, 2011. in particular, our market

presence in uAe, Qatar and Malaysia resulted in significant

revenue growth. in Africa, strong revenue growth was mainly

driven by higher offshore activity in Angola.

Cost of service provided

cost of service provided for the Year ended december 31,

2011 was dKK 516.4 million, an increase of dKK 160.4 million,

or 45.1%, compared to cost of service provided of dKK 356.0

million for the Year ended december 31, 2010. the increase

was primarily a result of a dKK 54.9 million, or 38.6%, increase

in field staff costs, a 47.6 dKK million increase in other direct

operational costs and a dKK 16.8 million increase in deprecia-

tion on tractors and tools and development projects, compared

to the prior period. in addition, travel expenses increased by

dKK 10.3 million compared to the Year ended december 31,

2010. the increase in field staff costs was due to an increase

in average headcount in operations of 62, or 20.5%, equaling

an increase of dKK 24.3 million, an increase in overtime and

performance bonus payments of dKK 13.3 million or 85.9%,

and a dKK 6.6 million general increase in salary compared to

the Year ended december 31, 2010. the increase in other di-

rect operational costs of dKK 47.6 million was primarily due to

a dKK 11.2 million increase in equipment leasing costs, as well

as a dKK 16.2 million increase in shop supplies and a dKK 14.1

million increase on freight, all related to the increased activity

levels over the period.

Development and manufacturing costs

development and manufacturing costs for the Year ended

december 31, 2011 was dKK 0.7 million, an increase of dKK

0.1 million compared to development and manufacturing costs

at dKK 0.6 million for the Year ended december 31, 2010. the

increase was primarily due to an increase in accrued amounts

for obsolete items as a result of the general increase in our

activity levels.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 26

Administrative and sales costs

Administrative and sales costs for the Year ended december

31, 2011 were dKK 342.7 million, an increase of dKK 104.2

million, or 43.1%, compared to administrative and sales cost

of dKK 239.5 million for the Year ended december 31, 2010.

the increase in 2011 was primarily a result of an increase in

staff costs of dKK 70.4 million, or 58.7%, compared to the

prior period. the staff costs include issuance of warrants (non-

cash) to employees at a value of dKK 33.3 million. Adjusted

for issuance of warrants staff cost increased by dKK 37.3 mil-

lion or 31.1%. Average headcount in sales and administration

increased by 61, or 40.1%, in 2011 compared to Year ended

december 31, 2010. other administrative and sales costs in-

creased by dKK 33.8 million, or 38.1%, compared to the prior

period. the increase was primarily due to an increase in lease

costs for premises of dKK 10.4 million, in particular related to

our new facility in norway. travel costs increased by dKK 4.1

million, or 45.8%, primarily due to the overall increased activ-

ity. insurance costs increased by dKK 6.4 million primarily re-

lated to increased activities in Russia. other administrative and

sales costs for the Year ended december 31, 2011 increased by

dKK 12.9 million primarily due to increased activity levels.

Amortization of acquired intangibles in a business combination

there was no change in the amortization of acquired intangi-

bles in a business combination for the Year ended december

31, 2011 compared to the Year ended december 31, 2010.

Special items

special items for the Year ended december 31, 2011 were dKK

0.0 million, a decrease of dKK 13.5 million compared to dKK

13.5 million for the Year ended december 31, 2010. special

items in the year ended december 31, 2010 primarily related to

costs for third party advisors (such as auditors and lawyers) in

connection with a proposed capital markets transaction.

Net financial expenses

net financial expenses for the Year ended december 31, 2011

were dKK 126.8 million, an increase of dKK 35.9 million com-

pared to dKK 90.0 million for the Year ended december 31,

2010. interest expenses were dKK 66.7 million, an increase by

dKK 13.1 million over the prior period. other financial ex-

penses were dKK 21.5 million for the Year ended december

31, 2011, compared to dKK 5.7 million in the same period in

2010. the increase was primarily related to expensed redemp-

tion fees of dKK 13.6 million regarding refinancing of earlier

credit facilities.

Income taxes

income taxes for the Year ended december 31, 2011 were dKK

85.6 million, an increase of dKK 19.6 million, or 29.8%, com-

pared to income taxes of dKK 66.0 million for the Year ended

december 31, 2010. the increase was primarily due to a dKK

18.6 million tax provision.

MAnAgeMent coMMentARY /

Welltec® AnnuAl RepoRt 2011 27

finAnciAl stAteMent

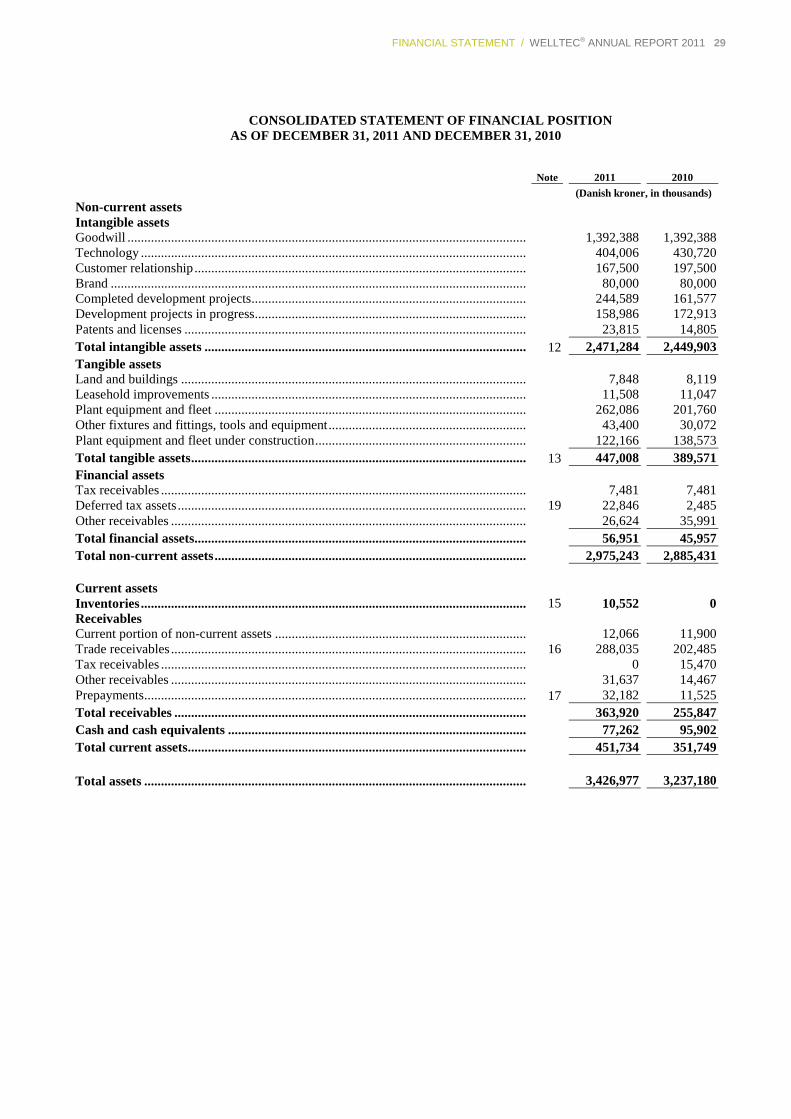

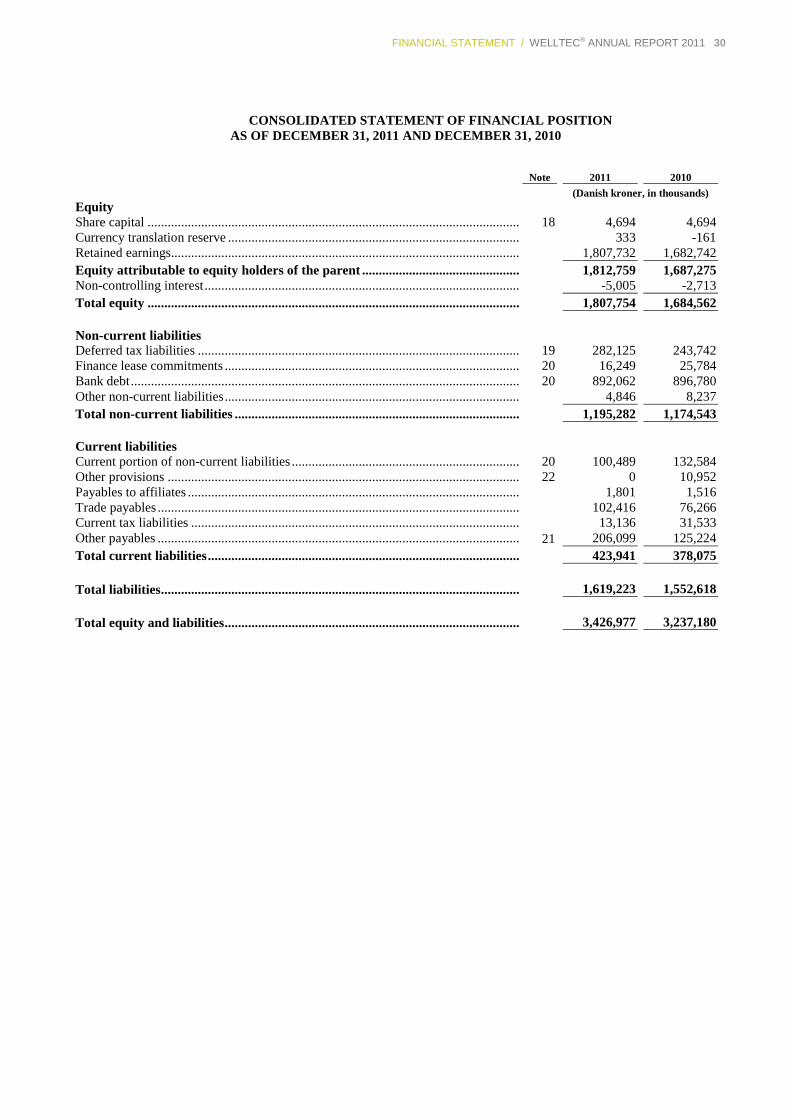

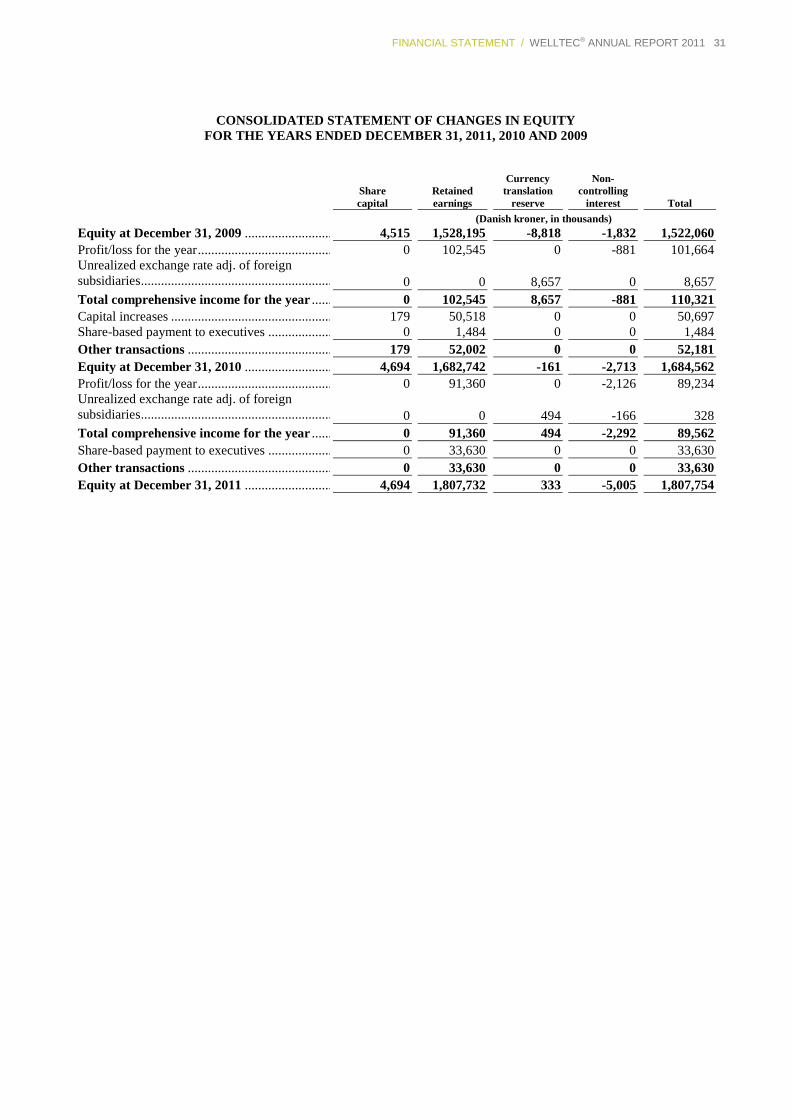

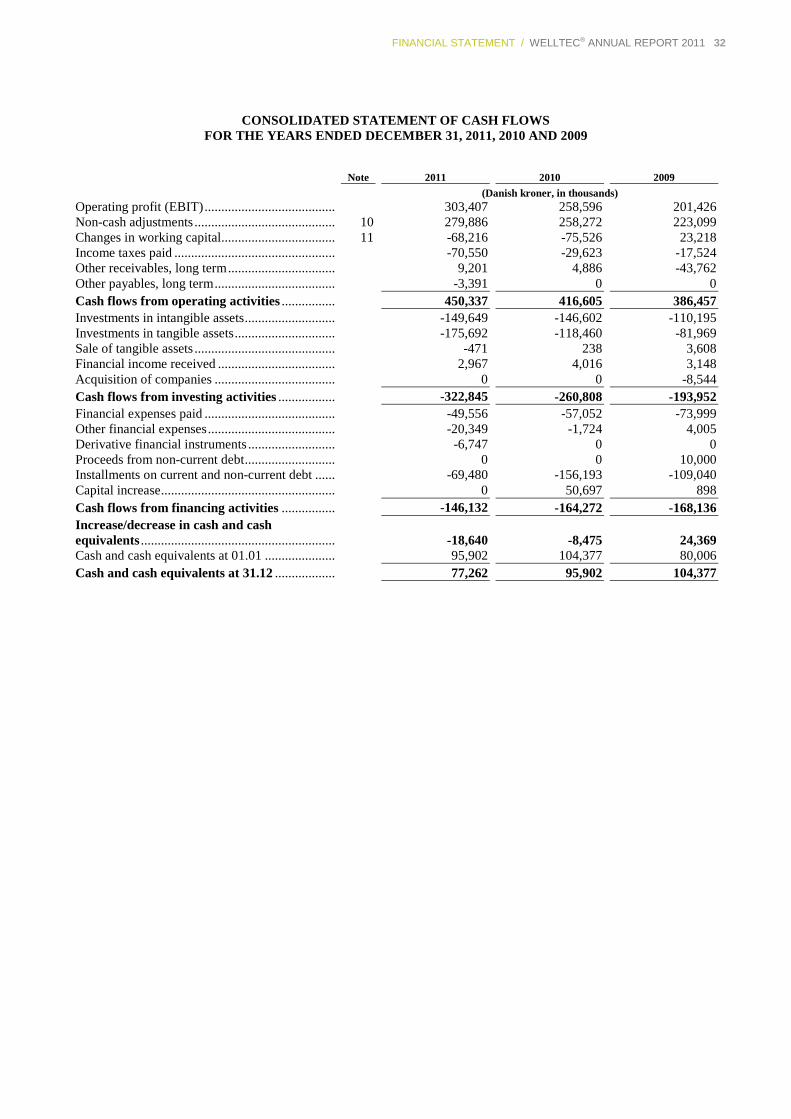

FINANCIAL STATEMENT / WELLTEC® ANNUAL REPORT 2011 28

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE YEARS ENDED DECEMBER 31, 2011, 2010 AND 2009

Note

2011

2010

2009

(Danish kroner, in thousands) Revenue ............................................................... 3 1,219,922 926,612 722,718 Cost of services provided ..................................... 4, 5 -516,403 -356,009 -277,309 Gross profit ........................................................ 703,519 570,603 445,409 Development and manufacturing costs ................ 4, 5 -680 -554 -6,643 Administrative and sales costs ............................4, 5 -342,718 -239,549 -174,146 Amortization of acquired intangibles in a business combination ........................................... 5 -56,714 -58,422 -55,000 Operating profit (EBIT) before special items.. 303,407 272,078 209,620 Special items ........................................................ 6 0 -13,482 -8,193 Operating profit (EBIT) .................................... 303,407 258,596 201,427 Financial income .................................................. 7 24,630 30,138 10,797 Financial expenses ............................................... 8 -153,158 -121,073 -127,496 Profit before tax ................................................. 174,879 167,661 84,728 Income taxes ........................................................ 9 -85,645 -65,997 -43,236 Profit for the year .............................................. 89,234 101,664 41,492 Other comprehensive income for the year Unrealized exchange rate adjustments of foreign subsidiaries and branches ........................ 328 8,657 39,947 Total comprehensive income 89,562 110,321 81,439