Embed Size (px)

Citation preview

ANNUAL REPORT 2018

NITOL INSURANCE COMPANY LIMITEDYour Security is our responsibility

ANNUAL REPORT

2018

Table ofCONTENTS

02 NITOL Insurance Co. Ltd.Annual Report 2018

Le�er of Transmi�al 03No�ce of the 20th Annual General Mee�ng 04Corporate Informa�on 05Company Profile 06About Us 07Products & Services 08Board of Directors 10Le�er from the Chairman to Owners 11Profile of the Directors 14Corporate Management 20Message from Chief Execu�ve Officer 22Execu�ve Management (Head Office) 24Execu�ve Management (Branch Manager) 26Shareholder Informa�on 28Informa�on 29Shareholding Structure 30Access To Reports And Enquiries 31Financial Highlights 32Achievement 2018 33Disclosure on Evalua�on of Quarterly Report 34Financial Highlights (5 Years at a glance) 35Graphical Appearance 36Value Added Statement 38Market Value Added Statement 39Contribu�on to the Na�onal Economy 40Credit Ra�ng Report 41BAPLC Membership Cer�ficate 42Disclosure & Compliance 43Compliance Disclosure 44Disclosure of the No�fica�ons 46

Solvency Margin Posi�on 47Compliance Report on BSEC’s No�fica�on 48Cer�ficate of Compliance 54Statement of Corporate Governance 55Statements 59Statement on Internal Control 60Related Party Transac�ons 61Statement of Risk Management 62Statement of Social Responsibility 65Statement of Human Resources 66Statement on Going Concern and Liquidity Management 67Dividend 68Directors‘ Report 6919th Annual General Mee�ng 2018 84Financial Indica�on 85Accoun�ng Ra�os of 2018 & 2017 86Declara�on of Chief Execu�ve Officer andChief Financial Officer 87Directors Responsibili�es for Financial Statements 88Claims Management 89Clients Complains and Consultancy 90Market Share of Insurance Business of the Company 91Report on Audit Commi�ee 92Auditors’ Report to the shareholders 93Business Conference 2019 134Pictures of Various Program and Ac�vi�es 135Company’s Assets 141Branch Network 142Proxy Form 143

a

a

a

bc

cc

cd

d

d

d

d

e e

e

g gk

kmt

m

m

p s 11

1

122

2 2

3

4

44

Letter of Transmittal

03 NITOL Insurance Co. Ltd.Annual Report 2018

All Shareholders,

Bangladesh Securi�es and Exchange Commission,Insurance Development and Regulatory Authority,Registrar of Joint Stock Companies & Firms,Dhaka Stock Exchange Limited &Chi�agong Stock Exchange Limited.

Subject: Annual Report for the year ended December 31, 2018

Dear Sir(s)/Madam(s):

We are pleased to present before you a copy of the Company’s AnnualReport 2018 along with the Audited Financial Statements for the yearended December 31, 2018 for your kind informa�on.

Yours Sincerely,

Md. Shakhawat HossainCompany Secretary

Notice of the20th Annual General MeetingNo�ce is hereby given that the 20th Annual General Mee�ng of Nitol Insurance Company Limited will be held at “Spectra Conven�on Centre Limited”, House # 19, Road # 7, Gulshan – 1, Dhaka – 1212, on Sunday, May 05, 2019 at 11:00 AM to transact the following businesses:

1. To receive & adopt the Directors’ Report and Audited Financial Statements of the Company for the year ended December 31, 2018 together with the Auditors’ Report thereon;2. To declare Dividend for the year 2018;3. To elect / re-elect Director;4. To appoint/ re-appoint Auditors for the year 2019 and fix their remunera�on;5. To appoint compliance Auditor for the year 2019 and fix their remunera�on;6. Miscellaneous, if any;

By order of the Board of Directors

Dated: April 04, 2019Dhaka Md. Shakhawat Hossain Company Secretary

Notes:

1. February 20, 2019 was scheduled as Record Date. Shareholders, whose name were appeared on the Register of Members on the Record Date, will be eligible to a�end the mee�ng and qualify for dividend.

2. A member en�tled to a�end and vote at general mee�ng is en�tled to appoint a Proxy (as per Ar�cles of Associa�on proxy will be a member/shareholder of the Company) to a�end the mee�ng and vote on his/her behalf. The Proxy Form duly completed, must be affixed with a revenue stamp of BDT. 20/- and deposited at the registered office of the Company not later than 72 hours before the �me of holding the mee�ng.

3. Members are requested to no�fy their change of address, if any.

N.B.: As per Bangladesh Securities and Exchange Commission (BSEC) Notification # SEC/CMRRCD/2009-193/154 dated October 24, 2013 “No benefit in Cash or kind other than in the form of Cash Dividend or Stock Dividend, shall be paid to the holders of the equity security”.

04 NITOL Insurance Co. Ltd.Annual Report 2018

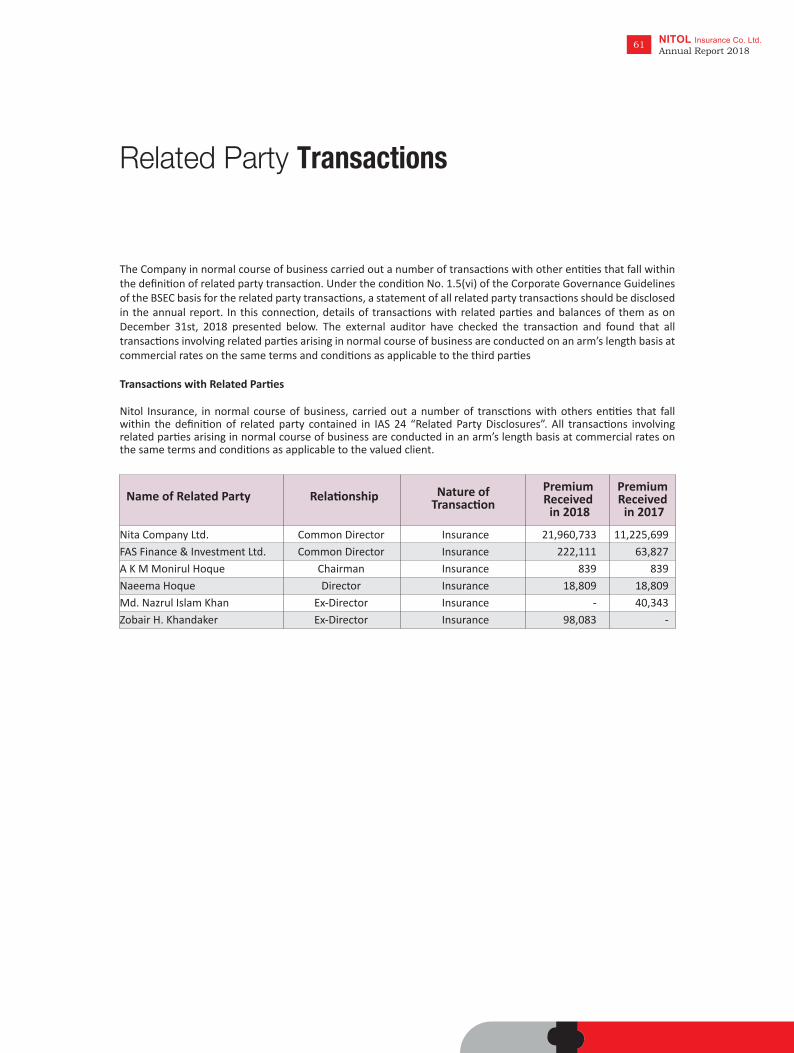

Corporate Information

05 NITOL Insurance Co. Ltd.Annual Report 2018

Cer�ficate of Incorpora�on : October 4, 1999

Cer�ficate of Commencement of Business : October 4, 1999

Cer�ficate No. of Registra�on : C-38743(701)/99

Cer�ficate of Registra�on from CCI : November 18, 1999

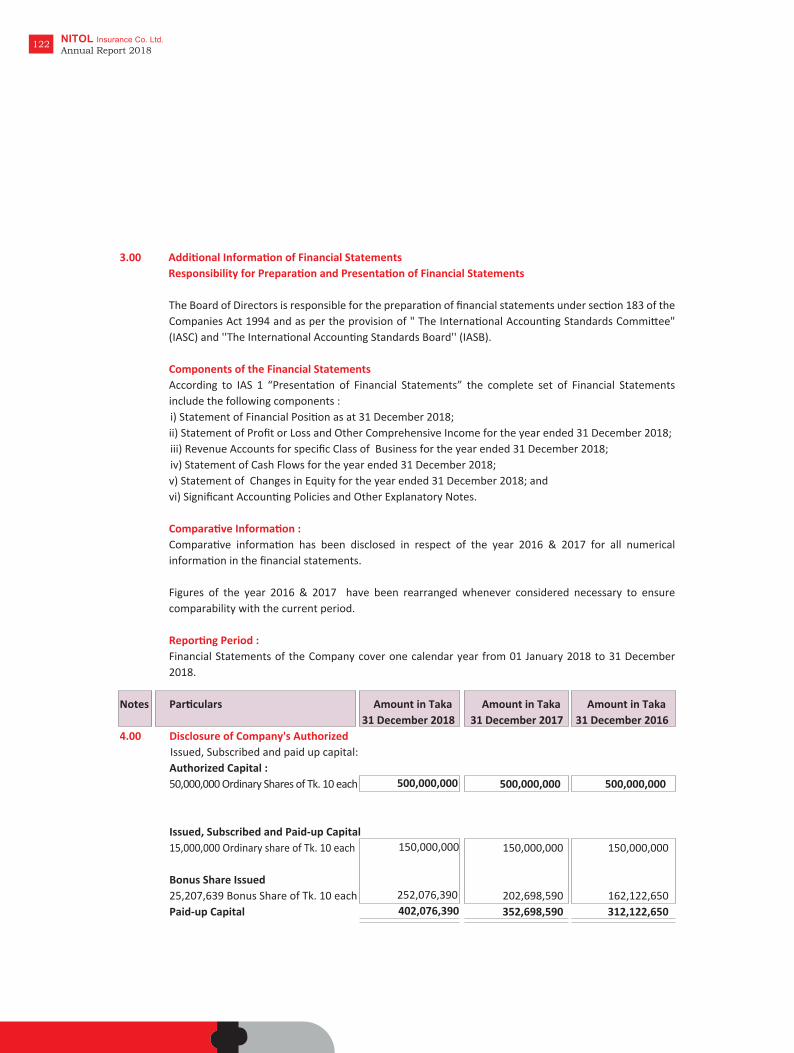

Authorized Capital : Tk. 50 Crore

Total Paid-up Capital : Tk. 402,076,390

Total Paid-up Number of Share : 40,207,639 @ Tk. 10 each

Ini�al Paid-up Capital on October 04, 1999 : Tk. 6 Crore

Paid-up Capital from IPO : Tk. 9 Crore

Date of approval of raising of capital of Tk. 9 Crore from BSEC : June 23, 2005

Date of Lis�ng of Dhaka Stock Exchange Ltd. (DSE) : November 29, 2005

Date of Lis�ng of Chi�agong Stock Exchange Ltd. (CSE) : October 10, 2005

First Trading in DSE & CSE : November 29, 2005

Registered Office and Head OfficeNitol Insurance Company LimitedPolice Plaza Concord, Tower - 2(6th Floor), Plot - 2, Road - 144Gulshan - 1, Dhaka - 1212.Tel: 88-02-55045202-05Fax: 88-02-55045206e-mail: [email protected]

Nature of BusinessAll kinds of Non-Life Insurance

Credit Ra�ngRated ‘AA-’ for the year 2017 by Credit Ra�ngInforma�on and Services Limited (CRISL)

AuditorMahfel Huq & Co.Chartered AccountantsCorporate OfficeBGIC Tower (4th Floor)34, Topkhana Road,Dhaka 1000.

Tax AdvisorMr. Nil Ratan SahaIncome Tax Prac��onerConfidence Tower, Flat # 15-D,5/Kha Satmasjid Road, Dhaka-1207.

Overseas Claim Se�ling AgentW. E. Cox Claims Group (Europe) LimitedGravesend, Kent, United Kingdom

Company Profile

06 NITOL Insurance Co. Ltd.Annual Report 2018

BankerJamuna Bank LimitedDutch-Bangla Bank Limited

Re-InsurerSadharan Bima Corpora�on, BangladeshNa�onal Insurance Company Limited, Kolkata, IndiaAsian Reinsurance Corpora�on, Bangkok, ThailandGIC Re, BhutanKenya Reinsurance Corpora�on, Nairobi, KenyaCICA-Re, AfricaZEP-Re, Kenya

Reinsurance BrokerJ.B. Boda Reinsurance Brokers Pvt. Ltd., IndiaProtec�on Reinsurance Services, W.L.L., BahrainRisk Care Insurance Broking Service Pvt. Ltd., IndiaSalasar Services (Insurance Broker) Pvt. Ltd., IndiaAlliance Insurance Brokers Pvt. Ltd., IndiaUnison Insurance Broking Services Pvt. Ltd., IndiaHeritage Insurance Brokers Pvt. Ltd., IndiaMarsh India Insurance Brokers Pvt. Ltd.

MembershipBangladesh Insurance Associa�on (BIA)Bangladesh Associa�on of Publicly Listed Company (BAPLC)Metropolitan Chamber of Commerce & Industry (MCCI)Dhaka Chamber of Commerce and Industry (DCCI)Bangladesh Malaysia Chamber of Commerce & Industry (BMCCI)India-Bangladesh Chamber of Commerce & Industry (IBCCI)Confedera�on of Asia Pacific Chamber of Commerce and Industry (CACCI)

About Us

Our Mission To provide the financial security to our clients, with

utmost good faith, sincerity and dedica�ons. To provide service to the insuring community,

according to their need and expecta�on. To conduct business fairly, honestly and with

transparency.

Our Objec�ves To follow utmost good faith & other principles of insurance strictly Best services to our clients Protec�on of investment of our Shareholders Welfare of our Employees Due revenue collec�on for the Government Ethical and moral social order Good governance for us and all around us Transparency in disclosures

Our VisionOur vision is the Apex of Success. We have to reach to that goal by our modern thinking, hard labour, �me-worthy decision, sincerity and unparalleled service. We are commi�ed to our slogan “Your Security is our Responsibility”

07 NITOL Insurance Co. Ltd.Annual Report 2018

Products & Services

Property InsuranceFire Insurance Including Allied PerilsHotel Owner’s All Risks InsuranceProperty Damage All Risks (PDAR) InsurancePower Plant Opera�onal Package InsuranceHouseholders Comprehensive InsuranceIndustrial All Risks (IAR) Insurance including Machinery Breakdown & Business Interrup�on

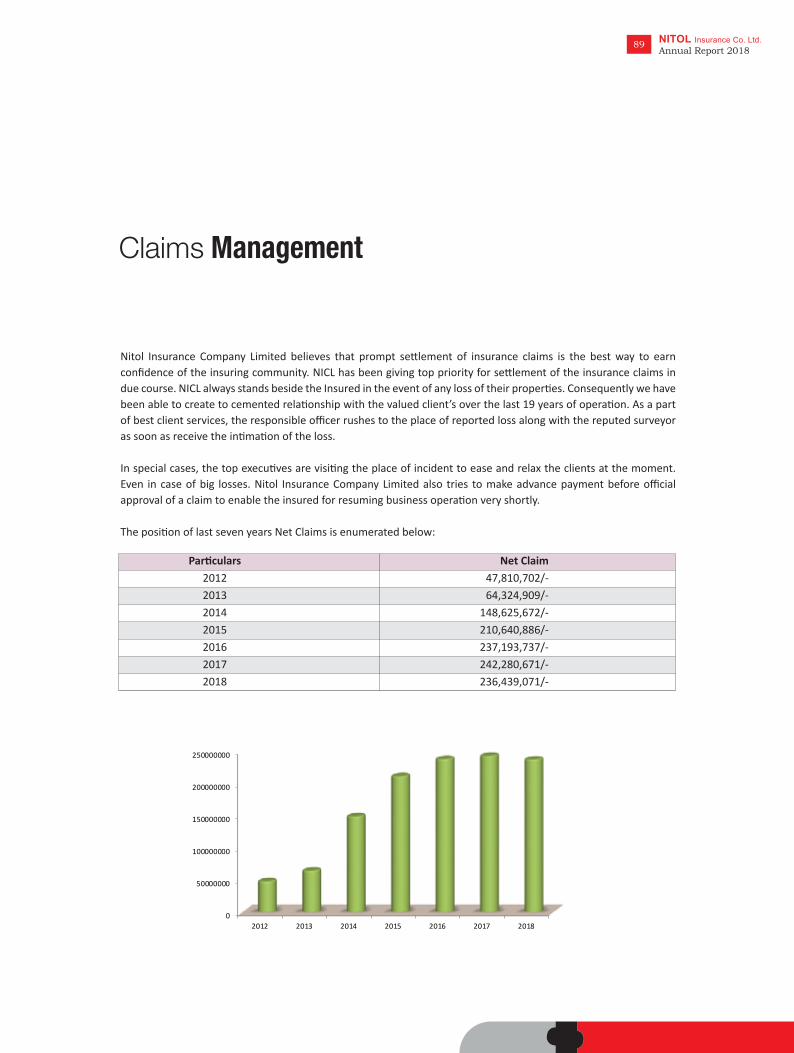

Motor (Comprehensive & Act Liability)InsurancePrivate Vehicle InsuranceCommercial Vehicle InsuranceMotor Cycle InsuranceMotor Trade Insurance

Miscellaneous (Financial) InsuranceCash-in-Safe (CIS) InsuranceCash-on-Counter (COC) InsuranceCash-in-Transit (CIT) InsuranceSafe Deposit Box (Bank Locker’s) InsuranceMoney Insurance (MI) for Bank only

Miscellaneous (Health) InsuranceThe Health Plan Insurance Contract (Hospitaliza�on)Hajj and Umrah Insurance

Miscellaneous (Personal Accident)InsurancePersonal Accident (PA) InsurancePeople’s Personal Accident (PPA) InsurancePersonal Accident (Air) Insurance

Miscellaneous (Liability)InsuranceBurglary and House Breaking (BG) InsuranceWorkmen’s Compensa�on (WC) InsuranceFidelity Guarantee (FG) InsuranceAll Risks (AR) InsurancePublic Liability InsuranceProduct Liability InsuranceCommercial General Liability including Automobile & Employer’s Liability

Marine InsuranceAll types of Marine Cargo Import and Export InsuranceAll types of Marine Hull InsuranceGoods-in-Transit Insurance

Avia�on InsuranceAvia�on Hull Insurance

Engineering InsuranceContractor’s All Risks (CAR) InsuranceErec�on All Risks (EAR) InsuranceBoiler and Pressure Vessel (BPV) InsuranceMachinery Breakdown (MBD) InsuranceDeteriora�on of Stock (DOS) InsuranceLi�, Hoist and Crane InsuranceElectronic Equipment Insurance (EEI)

Overseas Mediclaim Insurance Business and Holiday TourCorporate Frequent TravelEmployment and Studies

08 NITOL Insurance Co. Ltd.Annual Report 2018

09 NITOL Insurance Co. Ltd.Annual Report 2018

BOARD OF

DIRECTORS

ChairmanA K M Monirul Hoque

Vice ChairmanMd. Anowar Husain, FCMA

DirectorsMahmudul Hoque ShamimNaeema HoqueChandra Shekhar Das, FCA[Representa�ve of Praga� Life Insurance]Md. Siddiqur Rahman, FCS[Representa�ve of FAS Finance & Investment Ltd.]

Independent DirectorsMd. Mamunur Rashid, FCMADr. Md. Akram Hossain

Managing Director & Chief Execu�ve OfficerS.M. Mahbubul Karim

Directors Resigned from the Board Zobair Humayun KhandakerMd. Nazrul Islam Khan[Representa�ve of ICB]

Composition ofBoard of Directors & Its CommitteeBoard of Directors

Commi�ee

Audit Commi�eeChairmanMd. Mamunur Rashid, FCMAMembersMd. Anowar Husain, FCMAZobair Humayun Khandaker (Resigned)Mahmudul Hoque Shamim

Execu�ve Commi�eeChairmanNaeema HoqueMembersZobair Humayun Khandaker (Resigned)Mahmudul Hoque Shamim

Claims Commi�eeChairmanA K M Monirul HoqueMembersMd. Anowar Husain, FCMAS.M. Mahbubul Karim

Risk Management Commi�eeChairmanMahmudul Hoque ShamimMembersZobair Humayun Khandaker (Resigned)Md. Siddiqur Rahman, FCSChandra Shekhar Das, FCA

10 NITOL Insurance Co. Ltd.Annual Report 2018

NICL is one of the amazing Insurance Company, which run parallel to the technologies and IT systems. We have the most advance integrated software operational activity, which secured our online services. We have an attention in our future plan to build-up online marketing to reach wider group of people. Our attempt is to cooperate and satisfy the customers.

Letter from the CHAIRMANto Owners

11 NITOL Insurance Co. Ltd.Annual Report 2018

12 NITOL Insurance Co. Ltd.Annual Report 2018

Bismillahi-r-Rahmani-r-Rahim

Assalamu Alaikum Wa Rahmatullahi Wa Barakatuh

Dear Shareholders,

Economy turns into turmoil state during elec�on year. As 2018 was the year of general elec�on; customarily economy should fall down by its natural course. Instead of having disorders in poli�cs, na�onal economy was compara�vely sta�c in last year. Conversely, local insurance companies have disappoin�ng figure and failed to add growth in na�onal economy as well. As a result, large number of industries had to suffer badly.

We have number of companies that are newly growing-up but their contribu�on to GDP is not sa�sfactory. Insurance companies (both life and non-life) contributed to GDP about 0.9%. WTO has collected data from 2012 to 2017 reagrding contribu�on of insurance companies in GDP. They have found the gradual declining phase of premium, which was disappoin�ng to WTO.

In 2012, Life and Non-life insurance companies contributed to GDP about 0.83%, of which ra�o was 62% for life and 21% for non-life. This condi�on became worse in step-wise fashion �ll 2017 and came to 55%, where, life and non-life insurance comprises 0.40% and 0.15% respec�vely.

I personally intended to assure our share holders that we are successful to hold up our success- speed instead of having countrywide adverse situa�on. If we look at our

13 NITOL Insurance Co. Ltd.Annual Report 2018

report, we manage to find out the picture that NICL has earned profits of 7.48% in premium and 14.81% in underwri�ng.

Bangladesh has entered into an island of global digital network. People are taking support of this digital technology. They are adop�ng this networking system and becoming more familiar to this. This scenario helps us to introduce digital networking service. We have started our program with Motor Insurance under this framework. Now, anyone can take the opportunity of our on-line services and facili�es from anywhere to make his/her motor vehicle insured. We have turned the process easy. Anyone can use debit/credit card, online banking, and even mobile banking service like; bkash, ipay or rocket etc. This new path has ensured transparency more successfully. In turn, it is becoming popular to the young people. We are planning to do our all ac�vi�es through online, Inshallah.

Indeed, this is an immense pleasure to speak on behalf of the Board of Directors. As a Chairman of the NICL it is my pleasure to welcome you all to the 20th Annual General Mee�ng of Nitol Insurance Company Limited.

Also, I must ar�culate my gra�tude for the amazing support and faith that you have shown in establishing the company.

Being here as a Chairman of NICL, it has been a thrilling experience and I believe that our best days are yet to come by the grace of Allah (Subhanatayala).

NICL is one of the amazing Insurance Company which runs parallel to the technologies and IT systems. We have the most advance integrated so�ware opera�onal ac�vity, which secured our

online services. We have an a�en�on in our future plan build-up online marke�ng to reach wider group of people. Our a�empt is to cooperate and sa�sfy the customers. I am indeed enthusias�c not only as the Chairman, but also as an investor.

NICL has the efficient and effec�ve opera�onal system, which aligned with the strategy. We have reliable financial repor�ng and management informa�on, completed and �mely made; and the Company is in compliance with applicable laws and regula�ons as well as the Company's internal policies and ethical values including sustainability. The Company has a well defined organiza�onal structure and documented policy guidelines. This is to tell you that our standards are set very high in order to protect our clients.

I am gra�fied to Insurance Development & Regulatory Authority (IDRA) for their guidance and strong regula�on policies to develop the industry. I must appreciate their ac�ve par�cipa�on for promo�ng the benefits of Insurance to the Government. Special thanks to Bangladesh Insurance Associa�on (BIA), Bangladesh Securi�es and Exchange Commission (BSEC), Registrar of Joint Stock Companies & Firms, Dhaka Stock Exchange Limited (DSE) and Chi�agong Stock Exchange Limited (CSE). Furthermore, I want to thank the authori�es of the People's Republic of Bangladesh for their support.

Thank you all.

A K M Monirul HoqueChairman

Profile of the DirectorsA K M Monirul HoqueChairman

Mr. A K M Monirul Hoque started his business career in 1982 when he established a partnership voca�onal training center, Swi� Engineering and Technological Training Center (SETTC), to develop the skills of people in diverse fields such as driving, computer proficiency, tailoring along with shorthand, and so on. He founded this ins�tu�on when he was just 20 years old, while pursuing a Bachelor of Commerce (B.COM) Degree under Dhaka University. Mr. Hoque, addi�onally, has a Masters in Commerce Degree (M.COM) under Dhaka University with a concentra�on in Management.

In 1984, Mr. Hoque joined Nitol Motors Limited (NML)-the sole distributor of the dis�nguished Indian company called TATA Motors LTD (TML); he was the Execu�ve Director there. Mr. Hoque was the Head of the Marke�ng of the NML vehicles and directly involved in the sales and promo�on of products for 21 years i.e. �ll 31st December 2005. Mr. Hoque is also the Founder Chairman of Nitol Insurance Company Limited (NICL), a Non-life Public Limited Insurance Company, established in 1999.

Mrs. Naeema Hoque, wife of Mr. Hoque, completed her BA (Honors) and Masters of Arts (MA) in Philosophy from Dhaka University. Mrs. Hoque is also the Chairman of Execu�ve Commi�ee of NICL and deal with day to day work with management. Mrs. Hoque is the Life Member of Baridhara Cosmopolitan Club Limited (BCCL), Baridhara Society (BS), Gulshan Society (GS) and involved in many social and charitable organiza�ons.

14 NITOL Insurance Co. Ltd.Annual Report 2018

The couple is blessed with two daughters. The elder daughter, Ms. Salwa Hoque completed her undergraduate degree with a double major in Communica�on and English Literature (dis�nc�on) from the University of Washington (UW) in Sea�le, USA. She holds a Master’s degree from the Ivy League ins�tu�on Columbia University in New York, USA. Currently, she is a Ph.D. student and teaching assistant at New York University (NYU), New York, USA. Ms. Salwa is Permanent member of Gulshan Club Limited and Life Member of Baridhara Society. Younger daughter, Ms. Wasfia Hoque is majoring in Chemistry at the University of Washington (UW), Sea�le, USA. She is academically trained in French and ins�tu�onally proficient in playing the piano.

Mr. Hoque loves exploring new countries and has travelled all over the world. He enjoys immersing in diverse cultures, which enable him to understand, appreciate and interact with people of various tradi�ons with different ethnicity and background. His no�on is that exploring and learning about other culture broadens perspec�ve and encourages embracing people of diversity and difference. Apart from that, Mr. Hoque enjoys playing Golf and Snooker regularly. He loves to watch various sports such as Football, Tennis, Formula1 and so on; Cricket is his favorite sport. Mr. Hoque a�ended many seminars and symposiums all over the world. Mr. Hoque is an ac�ve and social person. He is member of various notable clubs and associa�ons in the country. He is a life member of SAARC. Mr. & Mrs. Hoque are also Life member of Gulshan Society.

Bangladesh Insurance Associa�on (BIA):Execu�ve Commi�ee (EC) Member: 2011-16, Vice President: 2017-18

General Body Member:Federa�on of Bangladesh Chamber of Commerce and Industries (FBCCI) India Bangladesh Chamber of Commerce and Industries (IBCCI) Bangladesh Malaysia Chamber of Commerce and Industries (BMCCI)Metropolitan Chamber of Commerce and Industries (MCCI)Dhaka Chamber of Commerce & Industry (DCCI) Bangladesh Associa�on of Publicly Listed Companies (BAPLC) Confedera�on of Asia-Pacific Chambers of Commerce and Industry (CACCI)SAARC Chamber of Commerce and Industries

Club Members:Dhaka Club Limited (DCL)Gulshan Club Limited (GCL)U�ara Club Limited (UCL)Narayanganj Club Limited (NCL)Baridhara Cosmopolitan Club Limited (BCCL)Fu-Wang Bowling Club Ltd. (FWBCL) Lt. Sheikh Jamal Dhanmondi Club Limited (SJDCL)Dhaka Boat Club Limited (DBCL)Kurmitola Golf Club Savar Golf ClubNarayanganj Rifle Club Gulshan Shoo�ng Club Baridhra Society Gulshan Society.

A K M Monirul HoqueChairman

Mr. A K M Monirul Hoque started his business career in 1982 when he established a partnership voca�onal training center, Swi� Engineering and Technological Training Center (SETTC), to develop the skills of people in diverse fields such as driving, computer proficiency, tailoring along with shorthand, and so on. He founded this ins�tu�on when he was just 20 years old, while pursuing a Bachelor of Commerce (B.COM) Degree under Dhaka University. Mr. Hoque, addi�onally, has a Masters in Commerce Degree (M.COM) under Dhaka University with a concentra�on in Management.

In 1984, Mr. Hoque joined Nitol Motors Limited (NML)-the sole distributor of the dis�nguished Indian company called TATA Motors LTD (TML); he was the Execu�ve Director there. Mr. Hoque was the Head of the Marke�ng of the NML vehicles and directly involved in the sales and promo�on of products for 21 years i.e. �ll 31st December 2005. Mr. Hoque is also the Founder Chairman of Nitol Insurance Company Limited (NICL), a Non-life Public Limited Insurance Company, established in 1999.

Mrs. Naeema Hoque, wife of Mr. Hoque, completed her BA (Honors) and Masters of Arts (MA) in Philosophy from Dhaka University. Mrs. Hoque is also the Chairman of Execu�ve Commi�ee of NICL and deal with day to day work with management. Mrs. Hoque is the Life Member of Baridhara Cosmopolitan Club Limited (BCCL), Baridhara Society (BS), Gulshan Society (GS) and involved in many social and charitable organiza�ons.

15 NITOL Insurance Co. Ltd.Annual Report 2018

The couple is blessed with two daughters. The elder daughter, Ms. Salwa Hoque completed her undergraduate degree with a double major in Communica�on and English Literature (dis�nc�on) from the University of Washington (UW) in Sea�le, USA. She holds a Master’s degree from the Ivy League ins�tu�on Columbia University in New York, USA. Currently, she is a Ph.D. student and teaching assistant at New York University (NYU), New York, USA. Ms. Salwa is Permanent member of Gulshan Club Limited and Life Member of Baridhara Society. Younger daughter, Ms. Wasfia Hoque is majoring in Chemistry at the University of Washington (UW), Sea�le, USA. She is academically trained in French and ins�tu�onally proficient in playing the piano.

Mr. Hoque loves exploring new countries and has travelled all over the world. He enjoys immersing in diverse cultures, which enable him to understand, appreciate and interact with people of various tradi�ons with different ethnicity and background. His no�on is that exploring and learning about other culture broadens perspec�ve and encourages embracing people of diversity and difference. Apart from that, Mr. Hoque enjoys playing Golf and Snooker regularly. He loves to watch various sports such as Football, Tennis, Formula1 and so on; Cricket is his favorite sport. Mr. Hoque a�ended many seminars and symposiums all over the world. Mr. Hoque is an ac�ve and social person. He is member of various notable clubs and associa�ons in the country. He is a life member of SAARC. Mr. & Mrs. Hoque are also Life member of Gulshan Society.

Bangladesh Insurance Associa�on (BIA):Execu�ve Commi�ee (EC) Member: 2011-16, Vice President: 2017-18

General Body Member:Federa�on of Bangladesh Chamber of Commerce and Industries (FBCCI) India Bangladesh Chamber of Commerce and Industries (IBCCI) Bangladesh Malaysia Chamber of Commerce and Industries (BMCCI)Metropolitan Chamber of Commerce and Industries (MCCI)Dhaka Chamber of Commerce & Industry (DCCI) Bangladesh Associa�on of Publicly Listed Companies (BAPLC) Confedera�on of Asia-Pacific Chambers of Commerce and Industry (CACCI)SAARC Chamber of Commerce and Industries

Club Members:Dhaka Club Limited (DCL)Gulshan Club Limited (GCL)U�ara Club Limited (UCL)Narayanganj Club Limited (NCL)Baridhara Cosmopolitan Club Limited (BCCL)Fu-Wang Bowling Club Ltd. (FWBCL) Lt. Sheikh Jamal Dhanmondi Club Limited (SJDCL)Dhaka Boat Club Limited (DBCL)Kurmitola Golf Club Savar Golf ClubNarayanganj Rifle Club Gulshan Shoo�ng Club Baridhra Society Gulshan Society.

Profile of the Directors

Md. Anowar Husain, FCMAVice Chairman

16 NITOL Insurance Co. Ltd.Annual Report 2018

Mr. Md. Anowar Husain, a Fellow of Cost and Management Accountants from London, FCMA (London), FCMA (Dhaka) had been in the UK about 25 years and a�er returned from the UK, joined as a Sponsor Director of Nita Co. Ltd. in 1991 a joint Venture with TATA Motors Ltd., India, and also Sponsor Director of Nitol Insurance Co. Ltd. (a Publicly Traded Company). He has nearly 58 years working experience in home and abroad in various type of Organiza�ons and Establishments in the UK & Middle East. Par�cipated in many Interna�onal Business Mee�ngs, Seminars & Fairs in home and abroad, ac�ve number of the high level policy making body in respect of financial investments, and developments and looking a�er the whole financial assets of the Nita Co. Ltd as Finance Director.

Traveled most of the European countries, USA, Middle East and some Southeast Asian countries. Ac�ve member of some non-poli�cal, social, cultural and religious organiza�ons, His wife Nazme Ara Husain M.A (University of Dhaka) is the Director of Nita Co. Ltd. and also Treasurer of Bangladesh Women Chamber of Commerce & Industries. Blessed with two Daughters Natasha Husain Radiologist (USA) & Bipasha Husain, MBA (USA) both are married now are living in USA.

Mahmudul Hoque ShamimDirector

Mr. Mahmudul Hoque Shamim is a renowned businessman. He is a Sponsor Shareholder Director of the Company. He has completed M.Com & C.A. (Course completed) and also Fellow of Ins�tute of Management Consultant Bangladesh (IMCB). He is a Director of Alight Real Estate Ltd. & L-Tech Bd. Ltd. He is a member of Army Golf Club.

The spouse of Mr. Mahmudul Hoque Shamim is Mrs. Amena Hossain Lucky (B.Sc., Hons., M.Sc.). They have two children; they are Mr. Ahnaf Shahriar Hoque (Son) & Arisha Hoque (Daughter).

Profile of the Directors

Chandra Shekhar Das, FCADirector, [Representa�ve of Praga� Life Insurance]

Mr. Chandra Shekhar Das was born in Jhalaka� in 1975. A�er comple�on of Master Degree; he became Chartered Accountant from the Ins�tute of Chartered Accountants of Bangladesh (ICAB) in 2009 and working with Praga� Life Insurance Limited as DMD (F&A). He wrote various ar�cles on economic, insurance etc in na�onal dailies. He par�cipated in many seminars, workshops, training programs.

Naeema HoqueDirector

Ms. Naeema Hoque, wife of Mr. A K M Monirul Hoque, completed her BA (Honors) and Masters of Arts (MA) in Philosophy from Dhaka University. Ms. Hoque doing bou�que business since 1992. Moreover, Ms. Hoque was the Execu�ve Member (EC) of Bangladesh Handicra� Associa�on (Banglacra�) from 1998-2000. She was the key and significant member in organizing the first Banglacra� All Members Showcase, which was inaugurated by the Prime Minister, at the �me, Sheikh Hasina. She was the EC member and Treasurer of Banglacra� for 2013-2015. Mrs. Hoque is, furthermore, the Life member of Baridhara Cosmopolitan Club Limited (BCCL), Baridhara Society, Gulshan Society (GS) and involved in many social and charitable organiza�ons.

17 NITOL Insurance Co. Ltd.Annual Report 2018

Profile of the Directors

Mr. Md. Siddiqur Rahman is one of the Directors of Nitol Insurance Company Limited. Simultaneously, he is the Managing Director of Simtex Industries Limited, a public limited Company listed with Dhaka Stock Exchange Limited and Chi�agong Stock Exchange Limited. Recently he was elected Chairman of FAS Finance and Investment Limited, He is also a Director of FAS Capital Management Limited and Clewiston Foods and Accommoda�on Limited (Owner Company of Radisson Blue, Cox’s Bazar). Mr. Rahman has a brilliant academic career and secured many scholarships in public level examina�ons. Mr. Rahman did his Masters in Business Administra�on and Advance Cer�ficate in Business Administra�on (ACBA) from the Ins�tute of Business Administra�on (IBA) under the University of Dhaka. He is also an FCS (Fellow member of The Ins�tute of Chartered Secretaries of Bangladesh). Besides, Mr. Rahman holds a Postgraduate Diploma in Financial Management from Bangladesh Ins�tute of Management (BIM) and he has wide working experience in different private and public limited companies before star�ng his own business career in the year 2001. Mr. Rahman is a dynamic businessman with more than 15 years of business experience. Mr. Rahman established his first business venture Simtex Bangladesh Limited in a very small scale in the year 2001. Since then by the dint of his dynamic leadership and excellent entrepreneurship, he expanded his business ventures both ver�cally and horizontally. He is a permanent member of Dhaka Club Limited and Dhanmondi Club Limited. He is also a donor Member of U�ara Club Limited and All Community Club Limited. He visited many countries of the world for study and business purpose including UK, USA, Canada, Germany, Australia, Belgium, France, Italy, China, Malaysia, Thailand, UAE and many more. Mr. Rahman is happily married and is blessed with three sons.

Md. Mamunur Rashid, FCMAIndependent Director

Md. Mamunur Rashid FCMA, a Fellow Member of the Ins�tute of Cost & Management Accountants of Bangladesh (ICMAB). He obtained his undergraduate degree in Bachelors of Commerce in the year 1987 and post- gradua�on degree in Masters of Commerce (Management) in the year 1989, securing First Class 2nd Posi�on and First Class 4th Posi�on respec�vely both under the University of Dhaka.

Presently Mr. Rashid is the Deputy Managing Director at Index Group of Companies. He is serving as the Independent Director at Nitol Insurance Co. Ltd- a listed Insurance company in Bangladesh, Independent Director at West Zone Power Distribu�on Company Ltd. an Enterprise of Bangladesh Power Development Board, Vice President, Bangladesh Ceramics Manufacturers and Exporters Associa�on (BCMEA).

Mr. Rashid served as the Chief Financial Officer at Kazi Farms Group, Director of Finance at Sheba Phone, Financial Controller & Company Secretary at Summit Power Limited, Chief Accountant at BRAC-Aarong, and Finance Manager at Desh Group of Companies. He also served in Government organiza�ons namely, Bangladesh Power Development Board (BPDB) and Bangladesh Parjatan Corpora�on (BPC) and Bangladesh Steel & Engineering Corpora�on (BSEC) at various capaci�es. Mr. Rashid is currently serving as the Council member of the Na�onal Council of ICMAB. He also served as the Execu�ve Secretary of South Asian Federa�on of Accountants (SAFA) for the year 2013.

Md. Siddiqur RahmanDirector, (Representa�ve of FAS Finance & Investment Ltd.)

18 NITOL Insurance Co. Ltd.Annual Report 2018

Profile of the Directors

Dr. Md. Akram HossainIndependent Director

Dr. Md. Akram Hossain, Associate Professor of Management Informa�on Systems Department of University of Dhaka, obtained his undergraduate degree in Bachelors of Business Administra�on (BBA) in the year 2000 and his post gradua�on degree in Masters of Business Administra�on (MBA) in the year 2001, securing CGPA – 3.75 (2nd Posi�on) and CGPA – 3.70 (2nd Posi�on) respec�vely both under the University of Dhaka. Dr. Akram completed Doctor of Philosophy (Ph D) degree in the year 2013 under Commonwealth split site study. He is serving as Assistant Proctor and member of Central Admission Commi�ee of the University of Dhaka. Dr. Akram is an Interna�onal researcher and he has 23 na�onal & interna�onal ar�cles which are published in popular journals. As an academician he a�ended and presented his research paper in various countries like USA, UK, Canada, Australia, Singapore, Turkey, Thailand and Malaysia in different interna�onal academic & research based conferences. He also got best paper award in Australia and Malaysia. He served as faculty member of: East West University (EWU), Brac University, ASA University Bangladesh (ASAUB), State University of Bangladesh (SUB) etc. Dr. Akram also working as visi�ng faculty member of BRAC University and East West University in Bangladesh.

S. M. Mahbubul KarimManaging Director &Chief Execu�ve Officer

Mr. Karim did his Masters Degree (MSS) in Public Administra�on from the University of Dhaka in the year 1985. He has started his insurance career with United Insurance Co. Ltd. in 1986. He worked there �ll 2000 and held the responsibility of Re-insurance and Specialized Underwri�ng as the Department Incharge. In July 2000 he joined Nitol Insurance Co. Ltd. and held responsibility of Underwri�ng, Reinsurance & Claims Department as in-charge. In 2006, he took the responsibility of “Company Secretary”. He became the Managing Director & CEO of Nitol Insurance Co. Ltd. on 1st January, 2012. He has long 33 (Thirty Three) years of prac�cal job experience in leading private non-life insurance companies having wide experience in Underwri�ng, Reinsurance, Claims, HRD and Secretarial & Corporate Affairs. He a�ended various training programmes on insurance & re-insurance at home & abroad i.e. Management of Reinsurance Por�olio at Na�onal Insurance Academy (NIA), Pune, India, Risk Underwri�ng & Re-insurance conducted jointly by ACR Retakaful, Malaysia & J.B. Boda Brokerage Agencies, Malaysia, a�ended training programmes organized by Bangladesh Insurance Academy, jointly with Asian Re and Munich Re on Reinsurance and Specialized Underwri�ng, a�ended training programs on Corporate Governance organized by Dhaka Stock Exchange Ltd. and also a�ended various insurance related courses and seminars organized by Bangladesh Insurance Academy and Bangladesh Insurance Associa�on. He has been selected by the Bangladesh Insurance Associa�on (BIA) as a resource person to provide lecture at the training program of Insurance Officials of Private Insurance Companies conducted by Bangladesh Insurance Associa�on (BIA). He is also a member of the Technical Sub-Commi�ee of the Bangladesh Insurance Associa�on (BIA). He is a member of Bangladesh Insurance Forum (BIF).

19 NITOL Insurance Co. Ltd.Annual Report 2018

Corporate

Management

Message from Chief Executive Officer

NICL solidified its posi�on as a leading motor Insurance services provider by providing dedicated services. Besides, NICL depicts its posi�ons fairly at fire, marine and others classes of insurances business. Sophis�cated online pla�orm and digital reach allow it to provide tailored services to thousands of customers on a real-�me basis.

22 NITOL Insurance Co. Ltd.Annual Report 2018

23 NITOL Insurance Co. Ltd.Annual Report 2018

Message from CEOBismillahi-r-Rahmani-r-Rahim

Dear Shareholders, valued clients and well wishers,

Assalamu Alaikum

We are in the ins�ga�on of digitaliza�on which affec�ng every aspect of our business. Digital technology is reshaping the market. We do even the simplest tasks, and technological advances hold poten�al for innova�ve new service offerings. Besides regulatory bodies and Insurance industry’s associa�on trying to develop and well-organized the industry to gain customers confidence. The forces drive opportuni�es to our industry to growth with stakeholders interest. For us, the transparency and prompt service is the power that build customers confidence and that is key of business.

We are fortunate to be in a strong, compe��ve posi�on, as our performance in 2018 demonstrated. Despite country’s poli�cal flux in last quarter our focused business and discipline delivered, improved underwri�ng, reduced costs and an expanded premium base, crea�ng immense opportuni�es for 2018 and beyond. Underlying our confident outlook are our clear strengths: our business mix balanced across products; a talent base with an innova�ve customer focus; a strong balance sheet; and a highly regarded brand. Our focus is now on using all of our skills, knowledge, exper�se and resources to ensure that we con�nue to meet customers’ needs and deliver the best possible experience. In an�cipa�on of this journey, NICL has been proac�vely reposi�oning itself to capture these opportuni�es. We have simplified our structure and unified our business to give us a clearer line of sight to our customers. And we have systema�cally built on our core capabili�es by expanding our service offerings, distribu�on reach and customer engagement pla�orms. We have a team with good knowledge of what customers need and how to bring our business priori�es into line with the changes we face. Clearly we s�ll have work to do. We will con�nue to reduce our cost base and improve our technical underwri�ng performance, and will implement changes that allow us to devote more �me and resources to interac�ng with customers.

In 2018, NICL solidified its posi�on as a leading motor

Insurance services provider by providing dedicated services. Besides, NICL depicts its posi�ons fairly at fire, marine and others classes of insurances business. Sophis�cated online pla�orm and digital reach allow it to provide tailored services to thousands of customers on a real-�me basis. To reduce customers’ hassle we simplified payment method by signing MOU with different banks and e-payments gateways.

An organiza�on can only succeed if it is able to a�ract and retain talented, skilled and mo�vated individuals insuring good governance. Good Governance in Corporate Sector includes transparency, accountability, fairness and responsibility. We believe the true and effec�ve Corporate Governance for the growth and development. So the issues of Corporate Governance are con�nuously receiving priority and keen a�en�on in all aspects of the company's Management. It is our organiza�onal determina�on and wishes to a�end the highest peak in this arena to keep our promising standard in maintaining the Good Governance. I am grateful to all our employees for their contribu�ons, ideas and hard work. To make sure we con�nue to have the right people in the right roles, and to help them to further develop, we are constantly looking at ways to support them.

Our strategy calls for us to focus on customers, simplify our business, and take an innova�ve approach. To make a difference to our customers’ means to completely rethink the way we do business. This will include adop�ng the right mindset to succeed. We must get even be�er at pu�ng customers first. To ensure we are able to do this, we are transforming our culture. By introducing a clearer approach to our purpose and values, we can broaden our understanding of our relevance to customer sand all our stakeholders. Our strategy, culture, and the strengths of our business put us in an enviable posi�on, helping us to generate cash for shareholders, while making us be�er at serving those who depend on us, year for year, to secure their lives, livelihoods and futures. Based on our performance in 2018, we can look ahead with great confidence that we have the right approach, mind set and culture to compete in this exci�ng, customer centric-world. Besides, we manage our opera�on with �mely ini�a�ves and by abiding the rules and regula�on of the Insurance Development and Regulatory Authority (IDRA), Bangladesh Securi�es and Exchange Commission (BSEC), Registrar of Joint Stock Companies & Firms (RJSC), Dhaka Stock Exchange Limited (DSE), Chi�agong Stock Exchange Limited (CSE) as well as other relevant authori�es.

Our credit ra�ng is AA- (pronounced as Double A minus) by Credit Ra�ng Informa�on & Services Ltd. (CRISL) which reflects our financial strength and claim paying ability.

As always, we would like to thank our Board of Directors for their con�nued guidance, the Government and regulators for their co-opera�on and facilita�on, and our shareholders & other stakeholders and media for their con�nuing trust and support. More importantly, a special thanks to all our employees who have worked hard to create more value for our clients every day.

We sincerely look forward to welcoming you at our 20th Annual General Mee�ng (AGM).

S. M. Mahbubul KarimChief Execu�ve Officer

Executive Management(Head Office)

24 NITOL Insurance Co. Ltd.Annual Report 2018

Executive MANAGEMENTHead Office

S.M. Mahbubul KarimManaging Director & CEO

Tapas Kumar PodderAddi�onal Managing Director &

Head of Opera�on Division

Mahbub AlamGeneral Manager &

Head of Admin and HR Dept.

Md. Altaf HossainGeneral Manager &

Chief Financial Officer (CFO)

Md. Shakhawat HossainGeneral Manager &Company Secretary

Md. Liakat Hossen, FCMAGeneral Manager &

Head of Internal Audit and Compliance

Md. Abdul WahabDeputy General Manager &Head of Underwri�ng Dept.

Abdullah Al Mamun TazuDeputy General Manager &

Head of Branch Monitoring andBusiness Development Dept.

Md. Nazrul Islam, ABIAAssistant General Manager &Head of Re-Insurance Dept.

Md. Abu Ahmed SumanManager &

Head of IT and Digital Marke�ng Dept.

25 NITOL Insurance Co. Ltd.Annual Report 2018

Mominul IslamAddi�onal Managing Director & Head of Branch

Bijoy Nagar Branch

Haditul Islam (Hedayet)Deputy Managing Director & Head of Branch

Gulshan Branch

Md. Ashraf UllahDeputy Managing Director & Head of Branch

Cha�ogram Branch

Md. Wahidur RahmanAssistant Managing Director & Head of Branch

Dhanmondi Branch

Saker AhmedAssistant Managing Director & Head of Branch

Karwan Bazar Branch

Tariq MahmudAssistant Managing Director & Head of Branch

Joydevpur Branch

G.M. AlimuddinAssistant Managing Director & Head of Branch

Dilkusha Branch

Executive MANAGEMENTHead of Branch

26 NITOL Insurance Co. Ltd.Annual Report 2018

Md. Altaf HossainGeneral Manager & Head of Branch

Mohakhali Branch

Md. A�qur RahmanGeneral Manager & Head of Branch

Rajshahi Branch

M. Muzammel HoqueGeneral Manager & Head of Branch

Cumilla Branch

Nozmul Hoque ChowdhuryDeputy General Manager & Head of Branch

Sylhet Branch

Kabir Uddin AhmedDeputy General Manager & Head of Branch

U�ara Branch

Prodip Kumar GhoshDeputy General Manager & Head of Branch

Rangpur Branch

Mokarrom Mustafa Khan MilonAssistant General Manager & Head of Branch

Jashore Branch

Md. Nazrul IslamAssistant General Manager & Head of Branch

Kush�a Branch

Md. Abdul MannanAssistant General Manager & Head of Branch

Jamalpur Branch

Md. Borhan Uddin ChowdhuryAssistant General Manager & Head of Branch

Narayangonj Branch

Md. Shamim KabirManager & Head of BranchDinajpur Branch

Dewan Jahid HossainManager & Head of BranchBarishal Branch

27 NITOL Insurance Co. Ltd.Annual Report 2018

SHAREHOLDER

INFORMATION

REGISTERED/HEAD OFFICEPolice Plaza Concord, Tower - 2(6th Floor), Plot - 2, Road - 144Gulshan - 1, Dhaka - 1212.Tel: 88-02-55045202-05Fax: 88-02-55045206e-mail: [email protected]

LISTING ON STOCK EXCHANGESNitol Insurance Company Limited was listed on 29 November 2005 at Dhaka Stock Exchange Ltd. and on 10th October 2005 at Chi�agong Stock Exchange Ltd.

LISTING FEESThe annual lis�ng fee for the year 2019 has been paid to the stock exchanges within the prescribed �me limit.

STOCK CODEThe stock code for trading in equity shares of Dhaka Stock Exchange at NITOLINS and Chi�agong Stock Exchange at NITOLINS.

STATUTORY COMPLIANCEDuring the year the Company has complied with all applicable provisions, filed all returns/forms and furnished all relevant informa�on as required under the Companies Act, 1994 and allied laws and rules, the Bangladesh Securi�es and Exchange Commission (BSEC) Regula�ons and the Stock Exchanges Lis�ng Regula�ons 2015.

RECORD DATEThe register of Member and share transfer books of the Company shall remain closed on February 20, 2019.

20TH ANNUAL GENERAL MEETINGDate: May 05, 2019Time: 11:00 AMVenue: Spectra Conven�on Centre Limited, House # 19, Road # 7, Gulshan – 1, Dhaka – 1212.

WEBSITE OF THE COMPANYA website of the Company has been developed which allows the users to get the Company related informa�on about its financial, history, types of insurance available with the Company and list of reinsures etc. Annual, half yearly and quarterly financial statements of the Company are available at www.nitolinsurance.com

GENERAL MEETINGS AND VOTING RIGHTSPursuant to sec�on 81 of the Companies Act, 1994, NICL holds general mee�ng of shareholders at least once a year. Every shareholder has a right to a�end the general mee�ng; the no�ce of such mee�ng is sent to all the shareholders at least fourteen days before the mee�ng and also adver�sed in English and one Bangla newspaper having circula�on in Bangladesh. All shares issued by the Company carry equal vo�ng rights. Generally, such a right is endowed to them by sec�on 82(1). On a pool votes may be given either personally or by proxy.

PROXIESPursuant to Sec�on 85 of the Companies Act, 1994 and according to the MoA and AoA of the Company, every shareholder who is en�tled to a�end and vote at a general mee�ng, can appoint another person as his/her proxy to a�end and vote instead of himself/herself. Every note calling a general mee�ng contains a statement that shareholder en�tled to a�end and vote is en�tled to appoint a proxy who needs to be a member of the Company. The instrument appoin�ng proxy, duly signed by the shareholder appoin�ng the proxy should be deposited with

Information

29 NITOL Insurance Co. Ltd.Annual Report 2018

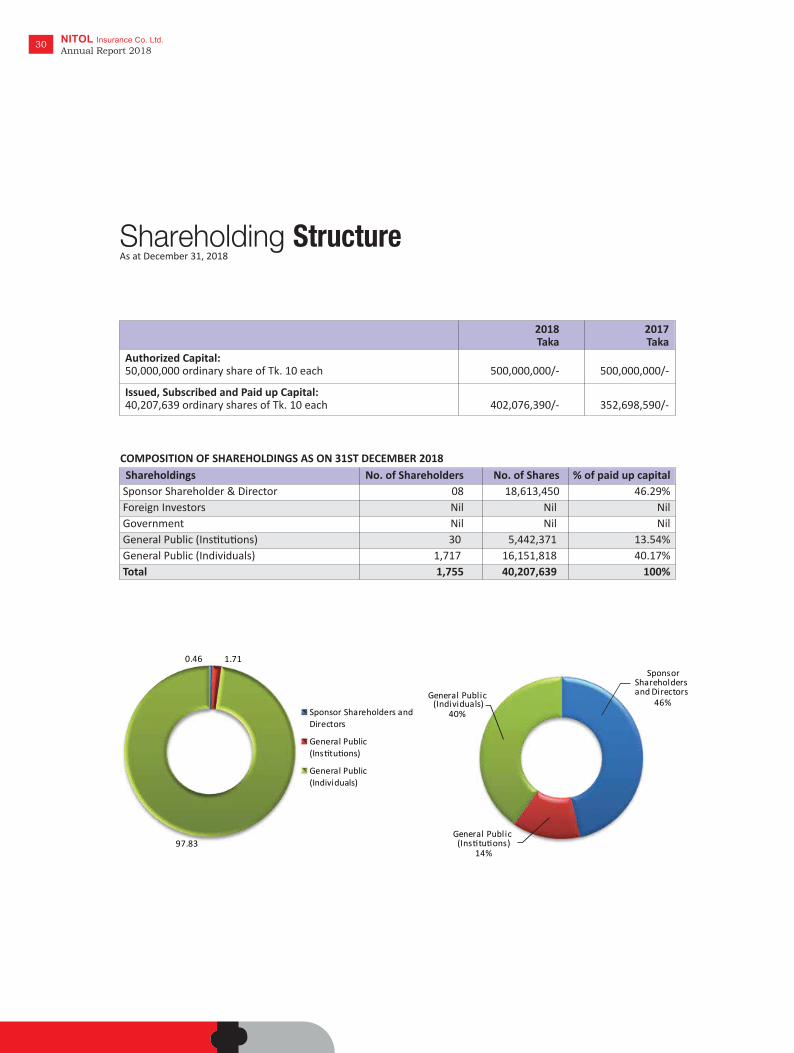

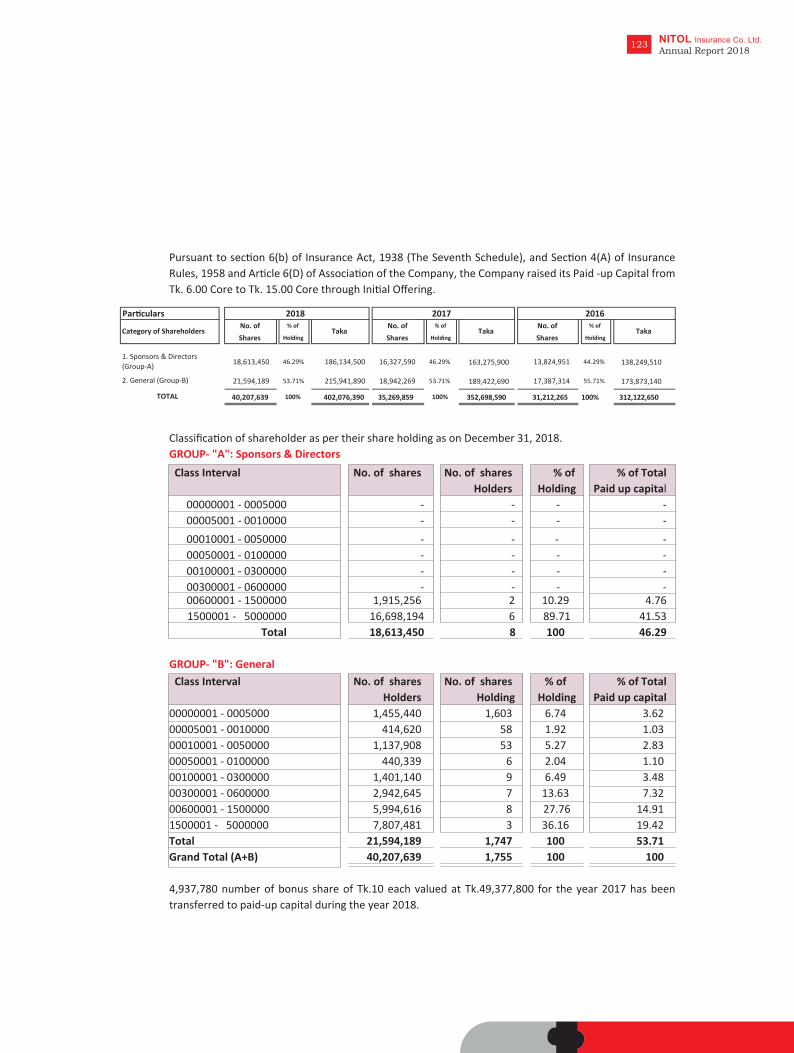

2018 2017 Taka Taka Authorized Capital: 50,000,000 ordinary share of Tk. 10 each 500,000,000/- 500,000,000/-

Issued, Subscribed and Paid up Capital: 40,207,639 ordinary shares of Tk. 10 each 402,076,390/- 352,698,590/-

Shareholding StructureAs at December 31, 2018

30 NITOL Insurance Co. Ltd.Annual Report 2018

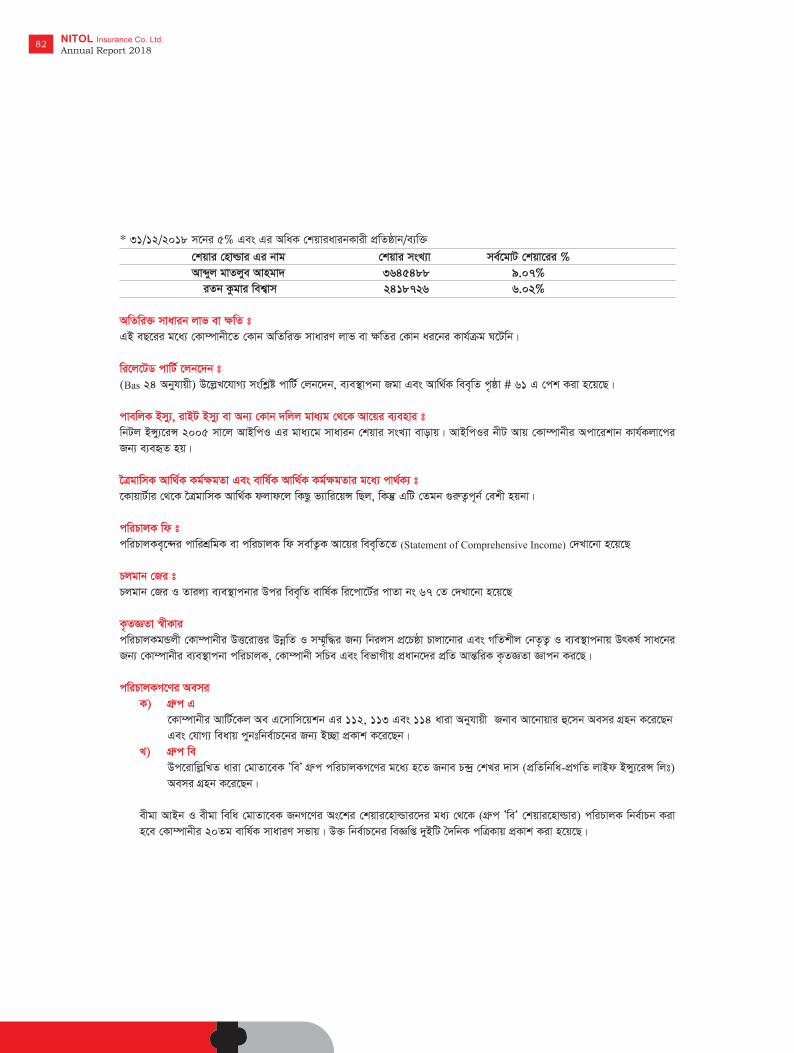

COMPOSITION OF SHAREHOLDINGS AS ON 31ST DECEMBER 2018 Shareholdings No. of Shareholders No. of Shares % of paid up capital Sponsor Shareholder & Director 08 18,613,450 46.29% Foreign Investors Nil Nil Nil Government Nil Nil Nil General Public (Ins�tu�ons) 30 5,442,371 13.54% General Public (Individuals) 1,717 16,151,818 40.17% Total 1,755 40,207,639 100%

0.46 1.71

97.83

Sponsor Shareholders andDirectors

General Public(Ins�tu�ons)

General Public(Individuals)

Sponsor Shareholders and Directors

46%

General Publ ic (Ins�tu�ons)

14%

General Publ ic (Individuals)

40%

Access To Reports And Enquiries

31 NITOL Insurance Co. Ltd.Annual Report 2018

Annual Report - Annual report of the Company is available in the Share Department of the Company and Company’s website www.nitolinsurance.com. Any requirements, Investors or Stakeholders can look a�er the annual report or printed copies obtained by wri�ng to Company Secretary.

Quarterly Reports - The Company publishes interim reports, at end of first, second and third quarters of the financial year. The interim reports can be accessed from the Company’s websitewww.nitolinsurance.com or printed copies obtained by wri�ng to Company Secretary.

Shareholders’ enquiries - Nitol Insurance Company Limited has a separate Share Department to communicate with Shareholders, Stakeholders and Investors may contact at any �me to Share Department for any sort of informa�on and query. To make the Annual General Mee�ng more par�cipatory, arranging AGM in well-known place & convenient �me allowing shareholders to speak in the AGM freely and making their valuable proposals and sugges�ons. Quarries rela�ng to shareholders holdings or interest and payment of dividends or share cer�ficates can be sent or shareholders might be communicated to the following address.

Share Department - Md. Shakhawat Hossain General Manager & Company Secretary

A. A. M. Rajibul Hassan Senior Officer

Police Plaza Concord, Tower - 2 (6th Floor), Plot - 2, Road - 144 Gulshan - 1, Dhaka - 1212. Tel: 88-02-55045202-05 Fax: 88-02-55045206 e-mail: [email protected] www.nitolinsurance.com

FINANCIAL

HIGHLIGHTS

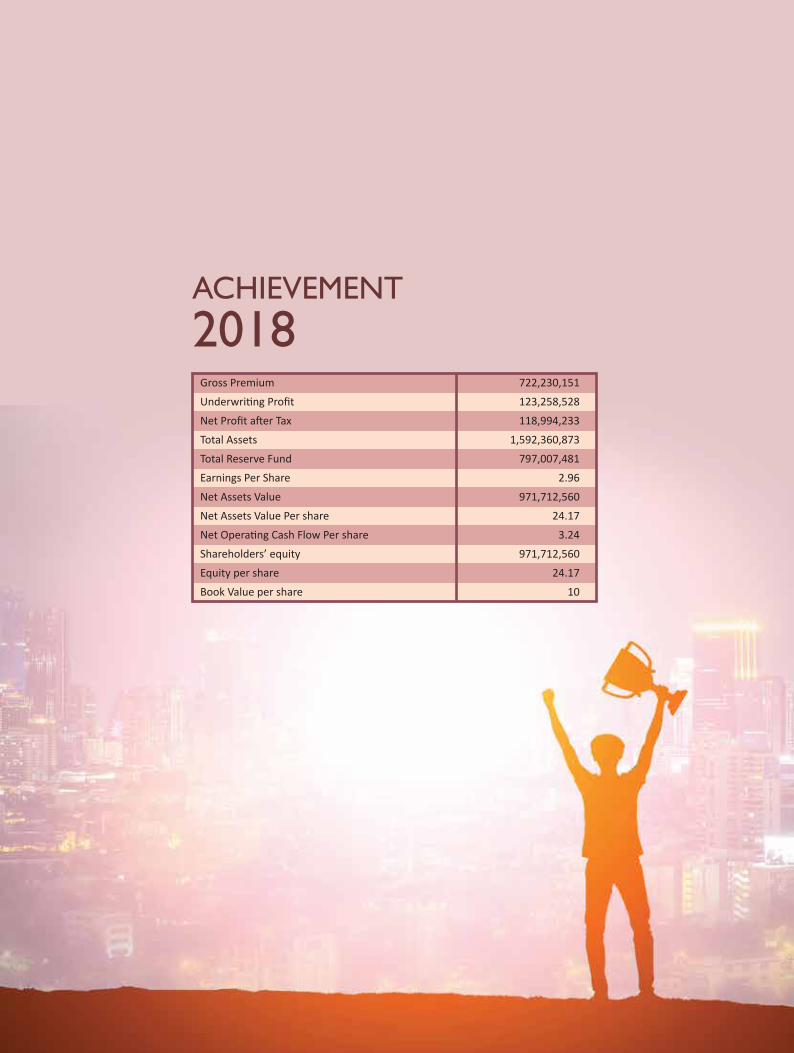

ACHIEVEMENT2018

Gross Premium 722,230,151

Underwri�ng Profit 123,258,528

Net Profit a�er Tax 118,994,233

Total Assets 1,592,360,873

Total Reserve Fund 797,007,481

Earnings Per Share 2.96

Net Assets Value 971,712,560

Net Assets Value Per share 24.17

Net Opera�ng Cash Flow Per share 3.24

Shareholders’ equity 971,712,560

Equity per share 24.17

Book Value per share 10

Figure BDT in Million

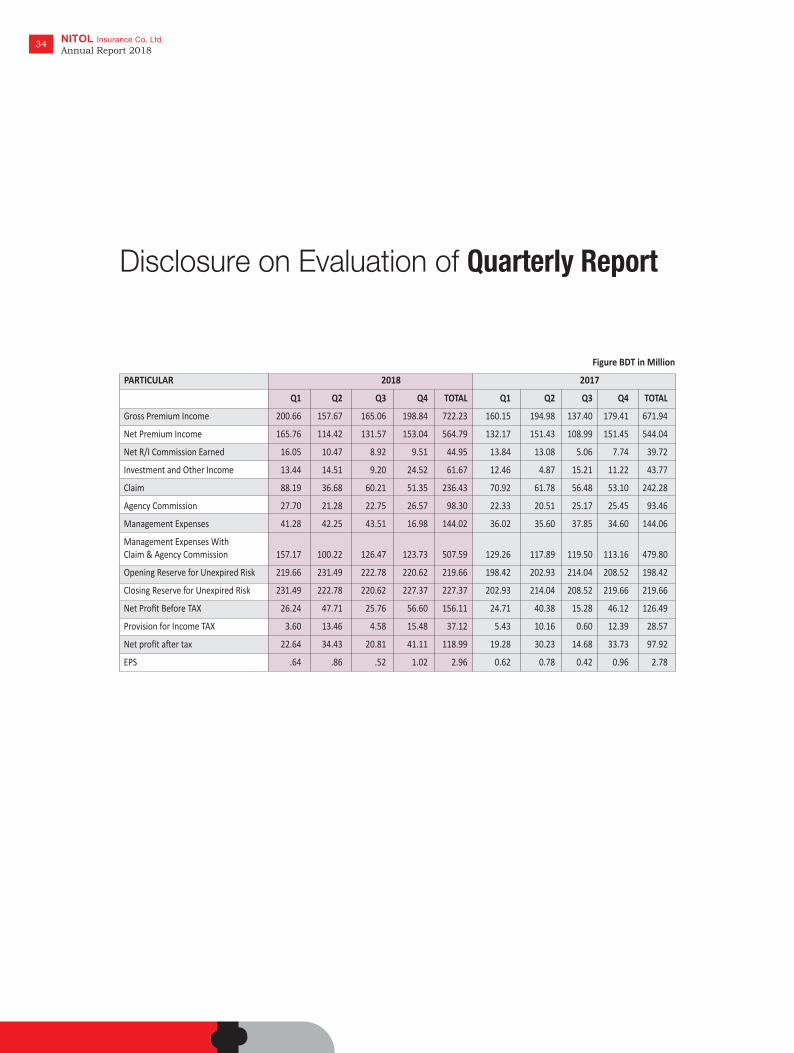

PARTICULAR 2018 2017

Q1 Q2 Q3 Q4 TOTAL Q1 Q2 Q3 Q4 TOTAL

Gross Premium Income 200.66 157.67 165.06 198.84 722.23 160.15 194.98 137.40 179.41 671.94

Net Premium Income 165.76 114.42 131.57 153.04 564.79 132.17 151.43 108.99 151.45 544.04

Net R/I Commission Earned 16.05 10.47 8.92 9.51 44.95 13.84 13.08 5.06 7.74 39.72

Investment and Other Income 13.44 14.51 9.20 24.52 61.67 12.46 4.87 15.21 11.22 43.77

Claim 88.19 36.68 60.21 51.35 236.43 70.92 61.78 56.48 53.10 242.28

Agency Commission 27.70 21.28 22.75 26.57 98.30 22.33 20.51 25.17 25.45 93.46

Management Expenses 41.28 42.25 43.51 16.98 144.02 36.02 35.60 37.85 34.60 144.06

Management Expenses With Claim & Agency Commission 157.17 100.22 126.47 123.73 507.59 129.26 117.89 119.50 113.16 479.80

Opening Reserve for Unexpired Risk 219.66 231.49 222.78 220.62 219.66 198.42 202.93 214.04 208.52 198.42

Closing Reserve for Unexpired Risk 231.49 222.78 220.62 227.37 227.37 202.93 214.04 208.52 219.66 219.66

Net Profit Before TAX 26.24 47.71 25.76 56.60 156.11 24.71 40.38 15.28 46.12 126.49

Provision for Income TAX 3.60 13.46 4.58 15.48 37.12 5.43 10.16 0.60 12.39 28.57

Net profit a�er tax 22.64 34.43 20.81 41.11 118.99 19.28 30.23 14.68 33.73 97.92

EPS .64 .86 .52 1.02 2.96 0.62 0.78 0.42 0.96 2.78

34 NITOL Insurance Co. Ltd.Annual Report 2018

Disclosure on Evaluation of Quarterly Report

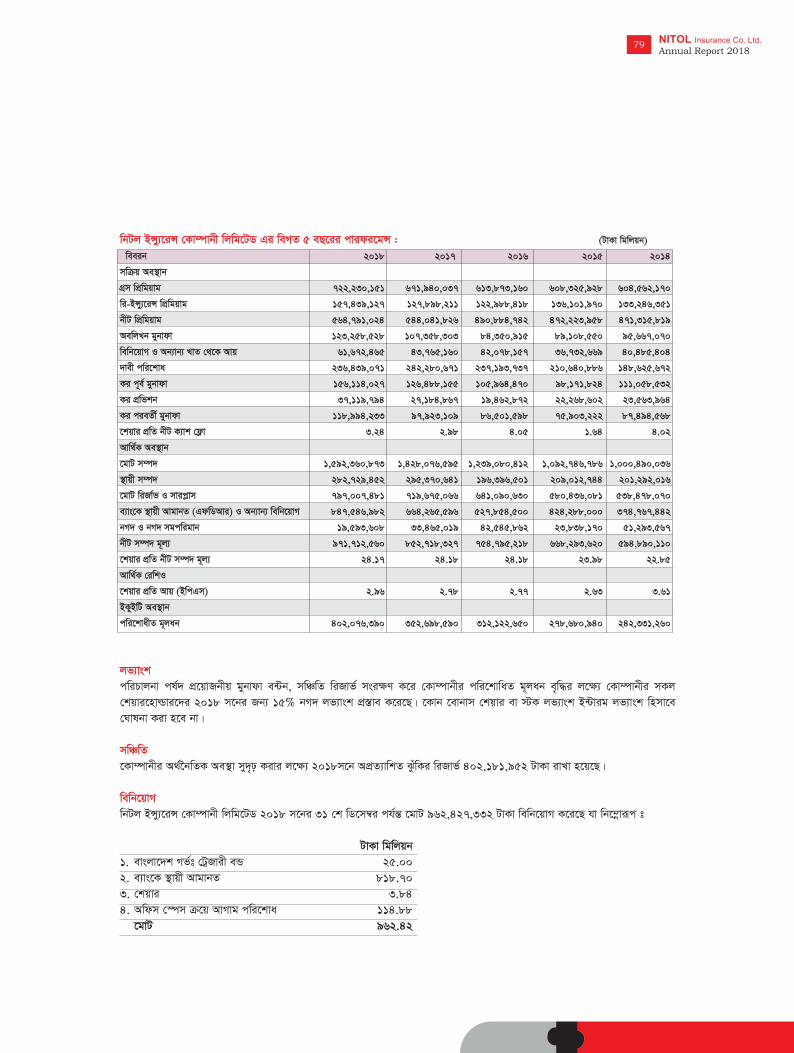

Financial Highlights(5 Years at a glance)

Figure in BDTPARTICULARS 2018 2017 2016 2015 2014

OPERATIONAL POSITIONGross Premium Income 722,230,151 671,940,037 613,873,160 608,325,928 604,562,170Re-Insurance Premium 157,439,127 127,898,211 122,988,418 136,101,970 133,246,351Net Premium Income 564,791,024 544,041,826 490,884,742 472,223,958 471,315,819Underwri�ng Profit 123,258,528 107,358,303 84,350,915 89,108,550 95,667,070Investment & Other Income 61,672,465 43,765,160 42,078,157 36,732,669 40,485,404Claim Paid 236,439,071 242,280,671 237,193,737 210,640,886 148,625,672Net Profit Before Tax 156,114,027 126,488,155 105,964,470 98,171,824 111,058,532Tax Provision 37,119,794 27,184,867 19,462,872 22,268,602 23,563,964Net Profit A�er Tax 118,994,233 97,923,109 86,501,598 75,903,222 87,494,568Net Opera�ng Cash Flow 3.24 2.98 4.05 1.64 4.02 FINANCIAL POSITIONTotal Assets 1,592,360,873 1,428,076,595 1,239,080,412 1,092,746,786 1,000,490,036Fixed Assets 282,729,452 295,370,641 196,396,501 209,012,744 201,292,016Total Reserve & Surplus 797,007,481 719,675,066 641,090,630 580,436,081 538,478,070Advance for Office Space 114,880,350 114,880,350 183,005,350 152,153,850 158,562,350FDR & BGTB 843,700,000 660,000,000 526,600,000 422,600,000 373,006,000Cash & Cash Equivalents 19,593,608 33,465,019 42,545,862 23,838,170 51,293,567Net Asset Value 971,712,560 852,718,327 754,795,218 668,293,620 594,890,110Net Asset Value (PS) 24.17 24.18 24.18 23.98 22.85

FINANCIAL RATIOEarnings Per Share (EPS) 2.96 2.78 2.77 2.63 3.61 EQUITY POSITIONPaid-up Capital 402,076,390 352,698,590 312,122,650 278,680,940 242,331,260

35 NITOL Insurance Co. Ltd.Annual Report 2018

Graphical Appearance

36 NITOL Insurance Co. Ltd.Annual Report 2018

540,000,000

560,000,000

580,000,000

600,000,000

620,000,000

640,000,000

660,000,000

680,000,000

700,000,000

720,000,000

740,000,000

2014 2015 2016 2017 2018

Gross Premium Income

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

2014 2015 2016 2017 2018

Re-Insurance Premium

420,000,000

440,000,000

460,000,000

480,000,000

500,000,000

520,000,000

540,000,000

560,000,000

580,000,000

2014 2015 2016 2017 2018

Net Premium Income

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

2014 2015 2016 2017 2018

Underwri�ng Profit

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

2014 2015 2016 2017 2018

Investment & Other Income

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

2014 2015 2016 2017 2018

Claim Paid

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

2014 2015 2016 2017 2018

Net Profit Before Tax

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2014 2015 2016 2017 2018

Tax Provision

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

2014 2015 2016 2017 2018

Net Profit A�er Tax

Graphical Appearance

37 NITOL Insurance Co. Ltd.Annual Report 2018

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

2014 2015 2016 2017 2018

Advance for Office Space

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

800,000,000

900,000,000

2014 2015 2016 2017 2018

FDR & BGTB

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

2014 2015 2016 2017 2018

Cash & Cash Equivalents

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

2014 2015 2016 2017 2018

Net Asset Value

0

0.5

1

1.5

2

2.5

3

3.5

4

2014 2015 2016 2017 2018

Earnings Per Share (EPS)

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

2014 2015 2016 2017 2018

Total Assets

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

2014 2015 2016 2017 2018

Fixed Assets

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

800,000,000

900,000,000

2014 2015 2016 2017 2018

Total Reserve & Surplus

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

450,000,000

2014 2015 2016 2017 2018

Paid-up Capital

Value Added StatementFor the year ended 31 december, 2018

Value Added Taka in Million

Gross Premium 722.23

Commission on Re-Insurance 44.95

Investment & Others Income 61.67

VAT & Stamp Duty 98.01

Total 926.86

Distribu�on of Value Addi�on Taka in Million

Re-Insurance Premium Ceded 157.43

Management Expenses 172.84

Agency Commission 98.31

Net Claims 236.44

Unexpired Risk Adjustment 7.72

Income Tax to Government 37.11

Dividend to Distribu�on 49.38

VAT & Stamp Duty 98.01

Reserve & Surplus 69.62

Total 926.86

38 NITOL Insurance Co. Ltd.Annual Report 2018

ValueAdded

Distribu�on ofValue Addi�on

Gross Premium

Commission on Re-Insurance

Investment & Others Income

VAT&Stamp Duty Re-Insurance

Premium Ceded

Management Expenses

Agency CommissionNet Claims

Unexpired Risk Adjustment

Income Tax to Governmenmt

Dividend to Distribu�on

VAT & Stamp Duty

Reserve & Surplus

Market Value Added Statement

This statement Shows the difference between the market value of a company and the capital contributed by the investors.

A posi�ve MVA indicates that the company could add the value to the shareholders wealth. The following statement indicates the MVA at the year ended on 31st December 2018.

Market Value Added Statement

Par�culars Number of Share Total Value (in Taka)

Market Value 40,207,639 1,125,813,892.00

Book Value 40,207,639 402,076,390.00

Market Value Added 723,737,502.00

39 NITOL Insurance Co. Ltd.Annual Report 2018

Market ValueAdded Statement

Market Value

Book Value

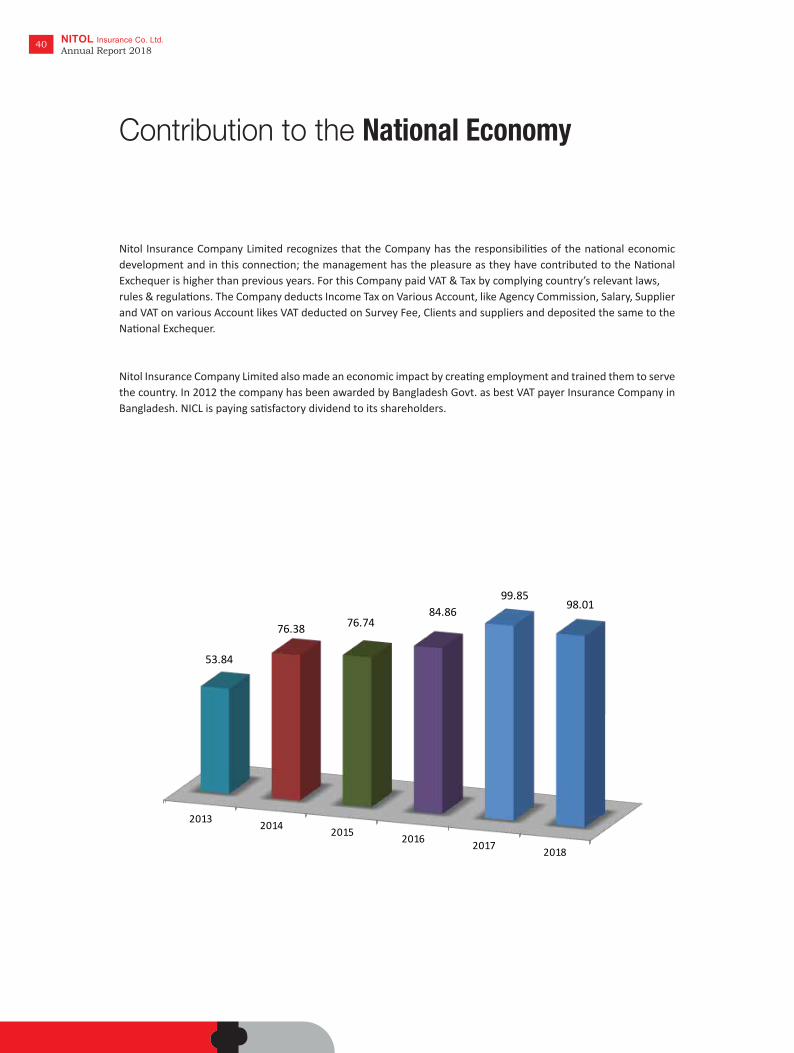

Contribution to the National Economy

Nitol Insurance Company Limited recognizes that the Company has the responsibili�es of the na�onal economic development and in this connec�on; the management has the pleasure as they have contributed to the Na�onal Exchequer is higher than previous years. For this Company paid VAT & Tax by complying country’s relevant laws,rules & regula�ons. The Company deducts Income Tax on Various Account, like Agency Commission, Salary, Supplier and VAT on various Account likes VAT deducted on Survey Fee, Clients and suppliers and deposited the same to theNa�onal Exchequer.

Nitol Insurance Company Limited also made an economic impact by crea�ng employment and trained them to serve the country. In 2012 the company has been awarded by Bangladesh Govt. as best VAT payer Insurance Company in Bangladesh. NICL is paying sa�sfactory dividend to its shareholders.

40 NITOL Insurance Co. Ltd.Annual Report 2018

2013 2014 2015 2016 2017 2018

53.84

76.38 76.7484.86

99.8598.01

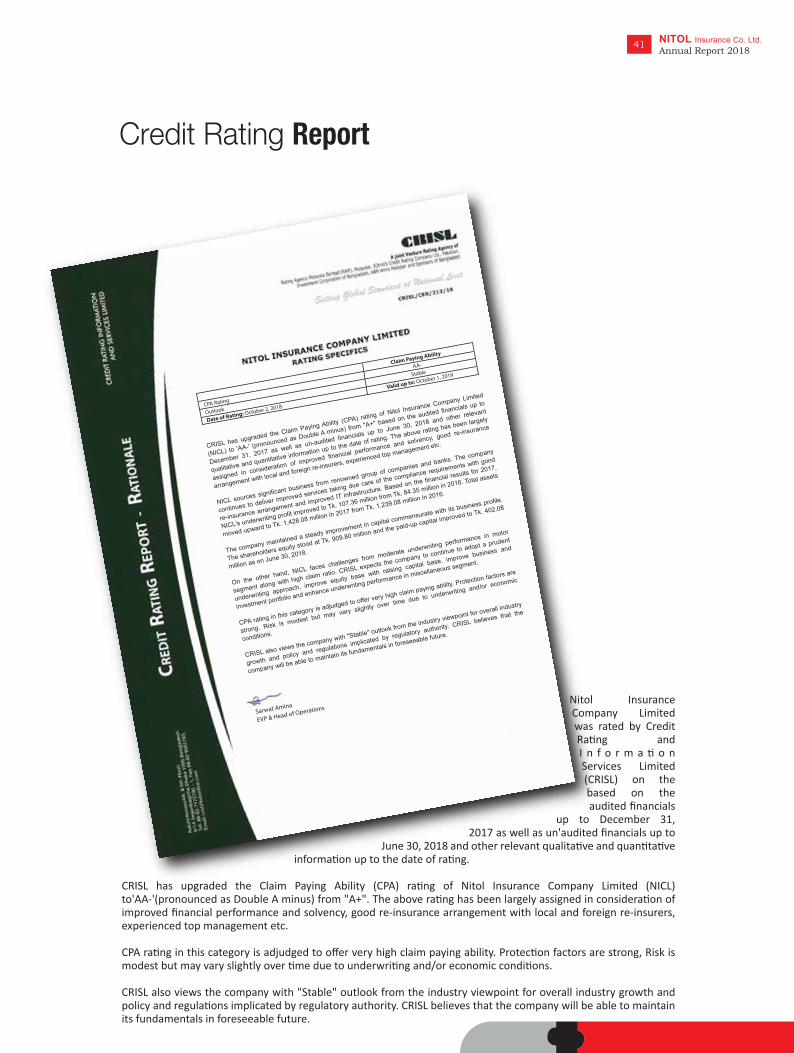

Nitol Insurance Company Limited was rated by Credit Ra�ng and I n f o r m a � o n Services Limited (CRISL) on the based on the audited financials

up to December 31, 2017 as well as un'audited financials up to

June 30, 2018 and other relevant qualita�ve and quan�ta�ve informa�on up to the date of ra�ng.

CRISL has upgraded the Claim Paying Ability (CPA) ra�ng of Nitol Insurance Company Limited (NICL) to'AA-'(pronounced as Double A minus) from "A+". The above ra�ng has been largely assigned in considera�on of improved financial performance and solvency, good re-insurance arrangement with local and foreign re-insurers, experienced top management etc.

CPA ra�ng in this category is adjudged to offer very high claim paying ability. Protec�on factors are strong, Risk is modest but may vary slightly over �me due to underwri�ng and/or economic condi�ons.

CRISL also views the company with "Stable" outlook from the industry viewpoint for overall industry growth and policy and regula�ons implicated by regulatory authority. CRISL believes that the company will be able to maintain its fundamentals in foreseeable future.

Credit Rating Report

41 NITOL Insurance Co. Ltd.Annual Report 2018

BAPLC Membership CertificateAs per SEC No�fica�on # SEC/CMRRCD/2006-161/324 dated April 11, 2010, we present the below Membership Cer�ficate given by Bangladesh Associa�on of Publicly Listed Companies (BAPLC) :

42 NITOL Insurance Co. Ltd.Annual Report 2018

DISCLOSURE &COMPLIANCE

Re-Elec�on of DirectorsCompany’s Ar�cles of Associa�on require that one-third director shall re�re from the office by rota�on each year except Chief Execu�ve Officer (Managing Director) and Independent Director of the Company. If they are eligible for the re-appointment, they could be re-elected by the shareholders in the next Annual General Mee�ng.

Removal and Appointment of the Chief Execu�ve Officer (Managing Director)Insurance Act- 2010 defined the appointment and removal of the Chief Execu�ve Officer (CEO) from his office of the Company with the consent of Insurance Development & Regulatory Authority (IDRA), the Board of Directors may remove the CEO (Managing Director) from his office and accordingly with prior approval of IDRA, the board may appoint any qualified person as a new CEO (Managing Director) instead of the removed CEO (Managing Director). Mr. S.M. Mahbubul Karim, Chief Execu�ve Officer has been reappointed in the Company with the approval of IDRA effec�ve from 1st January 2018 for next 03 (three) years.

Compliance Disclosure

44 NITOL Insurance Co. Ltd.Annual Report 2018

Disclosure of Directors Remunera�onBoard of Directors of the Company is non-execu�ve director except CEO (Managing Director). They don’t get any incen�ve or bonus for the performance of the board. The non-execu�ve directors get only mee�ng fees for a�ending the Board and Commi�ee mee�ngs at Tk. 5,000 / Tk. 8,000 per mee�ng. CEO (Managing Director) remunera�on package determine by the Board, which requires approval from the IDRA. As per corporate governance requirement we publish our non-execu�ve director mee�ng fees in the annual report. During the year, the mee�ng fees of the Director fees were Tk. 365,000/-.

Disclosure of Related Party Transac�onsCompany’s related par�es transac�ons are made for ordinary business purpose. A statement of related party transac�on presented in the notes to the Financial Statements No. # 132 of the report and the transac�ons of related par�es were checked and verified by the external auditor.

Disclosure on The Financial Performance of The CompanyNitol Insurance Company Limited is always aware about the disclosure of the financial performance for the requirement of regulatory authority. In this connec�on, the Company published the quarterly, half yearly and annual reports in the daily newspaper and Company’s website in �me. The Management also informed the Price Sensi�ve Informa�on (PSI) to the regulatory in �me and accordingly published in the daily newspapers and also electronic media. The Company’s Financial Statements have been prepared and published according to the Interna�onal Accoun�ng Standards (IAS) / Bangladesh Accoun�ng Standards (BAS) / Interna�onal Financial Repor�ng Standards (IFRS) / Bangladesh Financial Repor�ng Standards (BFRS) The Companies Act 1994, the Insurance Act 2010, the Insurance Rules, the Securi�es and Exchange Rules 1987 and Ins�tute of Chartered Accountant of Bangladesh (ICAB) guidelines. Other opera�onal informa�on was also published on the basis of the related rules and regula�ons requirements.

Appointment of External AuditorsThe External Auditor completed the annual audit about the accounts a�er appointment by the shareholders in the Annual General Mee�ng. With the recommenda�on of the Board of Directors, the shareholders confirmed the appointment of the external auditor in the annual general mee�ng specify remunera�on of its service. As per Finance Act. 1993 an Auditor cannot be appointed for more than three consecu�ve years. M/s. Mahfel Huq & Co., Chartered Accountants was appointed in the 19th AGM held on May 08, 2018, for the year of 2018.

Disclosure of The External/statutory Auditors EngagementM/s. Mahfel Huq & Co., Chartered Accountants the external auditors of the Company was not engaged with the following services of the Company:

- Appraisal or valua�on services or fairness opinion- Financial Informa�on System design and implementa�on- Book Keeping or other service related to the accoun�ng records or financial statements- Broker-dealer services- Actuarial services- Internal Audit Services- Any other service that the Audit Commi�ee determines- Tax Consultancy- No partner or employees of the external audit firms shall possess share of the Company, they audit at least during the tenure of the audit assignment of the Company.

45 NITOL Insurance Co. Ltd.Annual Report 2018

FULFILL THE MINIMUM SHARE HOLDING:According to the no�fica�on of BSEC, the Directors jointly hold minimum 30% (thirty percent) of share of the paid-up capital of the Company and each Director other than Independent/ Nominated Director(s) of the Company’s minimum holding should be 2% (two percent) shares. Currently, the Directors of the Company have jointly maintained 46.29% and also each Director hold 2% Shares of paid-up capital of the Company.

REPORT ON THE COMPLIANCE OF THE CONDITIONS OF SEC’S NOTIFICATION :In accordance with the Securi�es and Exchange Commission’s No�fica�on No/SEC/CMRRCD/2006-158/137/Admin/44 dated 07 August 2012 to report on the Compliance of certain condi�ons. The no�fica�on was issued to fulfill the good corporate governance prac�ce in the listed Companies for the interest of the investors’ and the capital market. The Company has followed the no�fica�ons in the Company and the implementa�on status of the corporate governance is given in the annual report. And also we have achieved the compliance cer�ficate from M/s. Mumlook Mustaque & Co., Chartered Accountants. The Board of the Nitol Insurance Company Limited has approved the guidance notes of Bangladesh Bank on An� Money Laundering (AML) & Comba�ng Terrorist Financing (CFT) and advised the Management to follow the recommenda�ons of AML & CFT.

NICL has established Central Compliance Unit consis�ng of 18 (eighteen) members headed by Mr. Tapas Kumar Podder, Addi�onal Managing Director of the Company as the Chief An� Money Laundering Compliance Officer (CAMLCO) under advice of the Board of Directors.

FULFILL THE ANTI MONEY LAUNDERING RULES :All the concerned Branches/Departments such as Underwri�ng, Re-Insurance, Accounts and Claims Department have been instructed to remain alert from the mo�ve of Money Launderer’s in connec�on of insurance underwri�ng & claims se�lement. And it was also advised all Branches/Departments to inform immediately the Chief An� Money Laundering Compliance Officer if any suspicious ac�vity of any insured/clients are found in connec�on of insurance documenta�on.

Reinsurance RiskThe Board of Directors annually approves the Reinsurance principles and the Maximum Risk retained for own account. In prac�ce, this Risk is kept lower if this is jus�fiable considering the price of Reinsurance. Reten�on in risk specific Reinsurance is a Maximum of BDT. 10,000,000/- for Fire Risk, BDT. 3,000,000/-for Marine Cargo, BDT. 3,000,000/- for Marine Hull, BDT. 1,000,000/- for Miscellaneous & Engineering, BDT. 300,000/- for Motor Loss. Under Fire Catastrophe Reinsurance Risk is BDT 30 Lac under 1st layer, BDT 1.00 Crore under 2nd layer & BDT 2.50 Crore under 3rd layer, the level of Reinsurance protec�on has an impact on the need of solvency capital. Only Companies with a sufficiently high Insurance financial strength ra�ng are accepted as Reinsurers. Moreover, maximum limits have been confirmed for the amounts of risk that can be ceded to anyone Reinsurer. These limits depend on the nature of the risk involved and on the Company’s solvency. Nitol Insurance Company Limited has mainly placed its Reinsurance agreements with the Companies at least ‘A’ ra�ng affirmed. Companys treaty Reinsunance are (i) Sadharan Bima Corpora�on, Bangladesh, (ii) Na�onal Insurance Company Limited, Kolkota, India (iii) Asian Reinsurance Corpora�on, Bangkok, Thailand, (iv) GIC Re Bhutan, (v) Kenya Reinsurance Corpora�on, Nairobi, Kenya, (vi) CICA-Re, Africa, (vii) ZEP-Re, Kenya.

Disclosure of the Notifications

46 NITOL Insurance Co. Ltd.Annual Report 2018

Solvency margin is the amount by which the assets of an insurer exceeds its liabili�es, and will form part of the insurer’s funds. Under sec�on 43 of Insurance Act 2010 the Insurance Company required to maintain adequate Solvency Margin. The solvency of an insurance Company corresponds to its ability to pay claims. The solvency of insurance company or its financial strength depends chiefly on whether sufficient technical reserves have been set up for the obliga�ons entered into and whether the Company has adequate capital as security.

In Bangladesh regula�ons for Solvency Margin for non-life insurance Company have been prepared by IDRA but not yet been approved by the Finance Ministry thereby not yet promulgated through official gaze�e.

During the year 2018, Nitol Insurance Company Limited has achieved solvency margin 7.79 �mes of required level. The details as follows:

Year 2018SOLVENCY MARGIN BASED ON PREMIUM INCOME: Amount in Million Taka Class of Business Net Gross Factors G.P. a�er 20% of 20% of 20% of Premium Premium applica�on of GPF NP (NP & GPF) Factor which is higher Fire 27.26 87.87 0.50 43.94 8.79 5.45 8.79 Marine Cargo 185.20 224.42 0.70 157.09 31.42 37.04 37.04 Marine Hull 2.42 11.21 0.50 5.61 1.12 0.48 1.12 Motor 344.28 350.67 0.85 298.07 59.61 68.86 68.86 Miscellaneous 5.64 48.06 0.70 33.64 6.73 1.13 6.73 Total 564.80 722.23 122.53

SOLVENCY MARGIN BASED ON ASSETS & LIABILITIES: Amount in Million Taka

Par�culars Amount Par�culars Amount Total Assets as per Balance Sheet 1,592.36 Total Liabili�es 1,592.36 Less: Amount due from Others (20.20) Sundry Creditors (43.96) Outstanding Premium - Amount Due to Others (68.91) Furniture & Fixture (2.39) Provision for Income Tax (212.89) Deposit Premium (22.14) Reserve for Unexpired Risk (227.37) Reserve for excep�on all loss (402.18)(A) TOTAL ASSETS 1,569.77 (B) TOTAL LIABILITIES 614.91

Solvency Margin Available (A-B) 954.86

SOLVENCY RATIO (Times)

Par�culars 2018 Solvency Margin Available (A-B) 954.86 Required Solvency Margin 122.53 Solvency Ra�o (Times) 7.79

Solvency Margin Position

47 NITOL Insurance Co. Ltd.Annual Report 2018

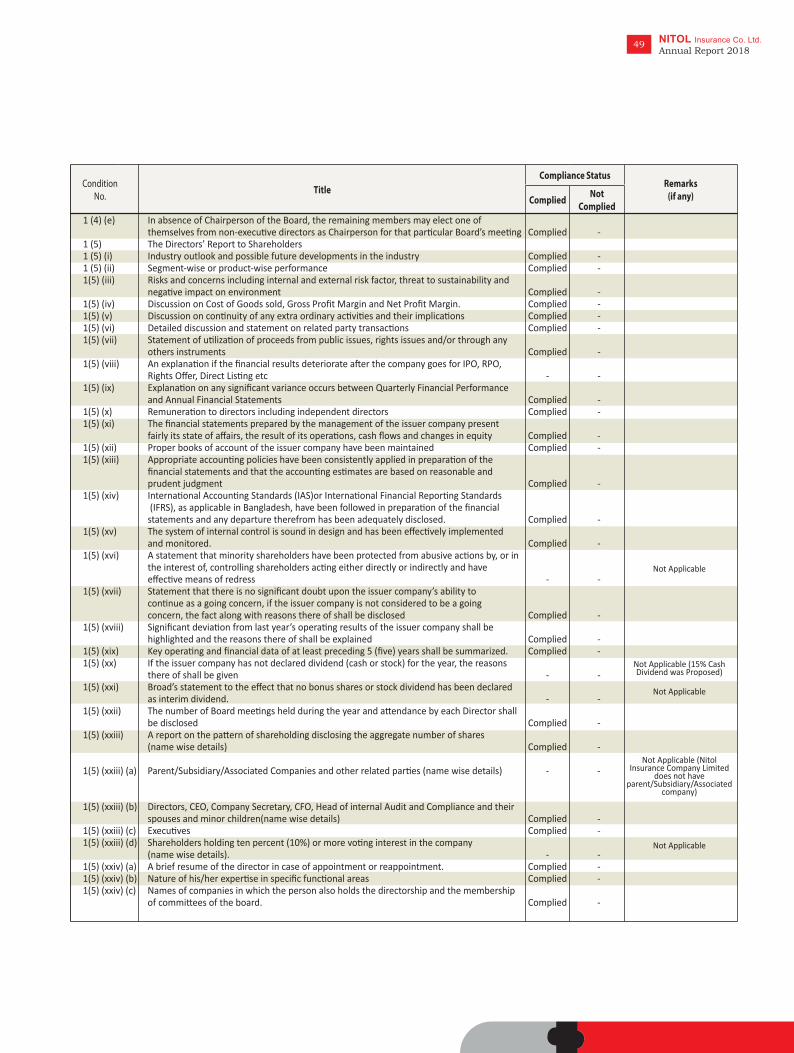

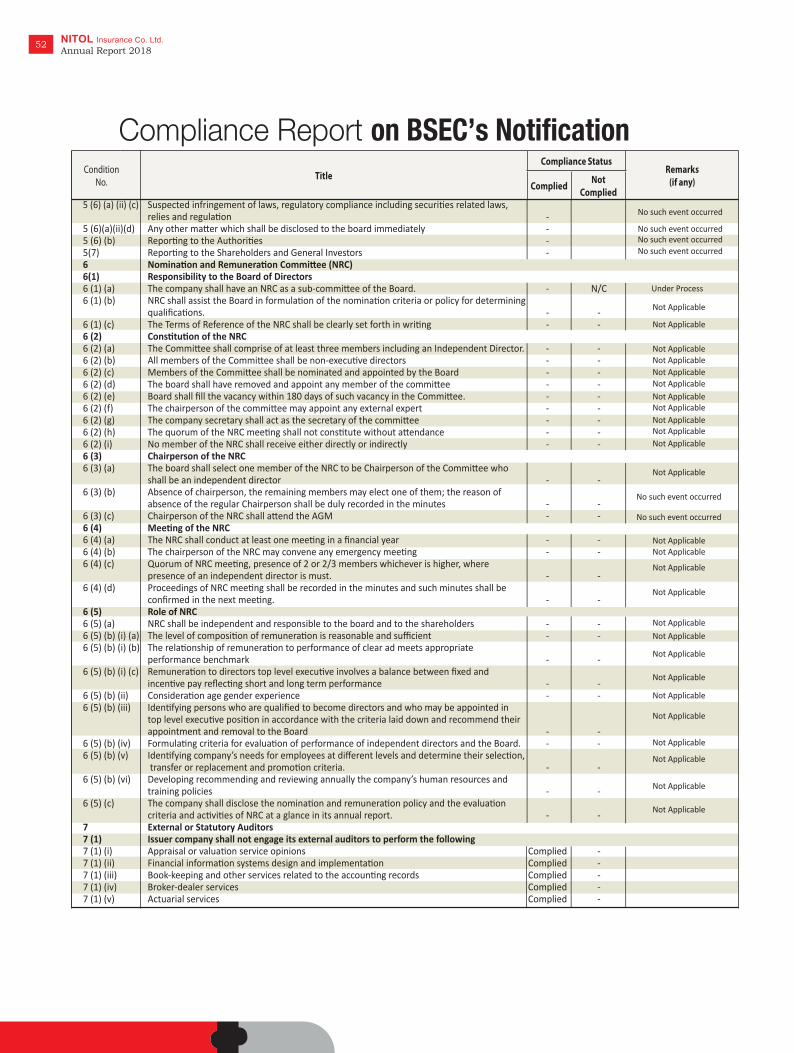

Compliance Report on BSEC’s NotificationReport on Compliance of Corporate Governance Guidelines of Nitol Insurance Co. Ltd. BSEC/CMRRCD/2006-158/207/Admin/80, dated June 03, 2018

48 NITOL Insurance Co. Ltd.Annual Report 2018

1 Board of directors1 (1) Size of the Board of Directors Complied - 1 (2) Independent Directors1 (2) (a) 1/5thof the total number of Board of Directors Complied - 1 (2) (b) (i) Does not hold any share or less than 1% shares of the total paid-up share of the Company Complied -

1 (2) (b) (ii) Not a Sponsor of the Company Complied - 1 (2) (b) (iii) Who has not been an execu�ve of the company in immediately procedure 2 (two) financial years Complied - 1 (2) (b) (iv) Who does not have any other rela�onship, whether pecuniary or otherwise with the company or its subsidiary or associated companies Complied - 1 (2) (b) (v) Who is not a member or TREC (Training Right En�tlement Cer�ficate)holder, director or officer of any stock exchange Complied - 1 (2) (b) (vi) Who is not a shareholder, director excep�ng independent director or officer of any member or TREC holder of stock exchange or an intermediary of the capital market Complied - 1 (2) (b) (vii) Who is not a partner or an execu�ve or was not a partner or execu�ve during the preceding 3 (three) years of the concerned companies statutory audit firm or audit firm engaged in internal audit services or conduc�ng special audit or professional cer�fying compliance of this code Complied - 1 (2) (b) (viii) Who is not independent director in more than 5 (five) listed companies Complied - 1 (2) (b) (ix) Who has not been convicted by a court of competent jurisdic�on as a defaulter in payment of any loan or any advance to a bank or a NBFI (Non-Bank Financial Ins�tu�on) Complied - 1 (2) (b) (x) Who has not been convicted for a criminal offence involving moral turpitude Complied - 1 (2) (c) Shall be appointed by the board and approved by the shareholders in the Annual General Mee�ng (AGM) Complied - 1 (2) (d) Post of independent director(s) cannot remain vacant for more than 90 (ninety)days Complied - 1 (2) (e) Tenure of independent directors’ office shall be for a period of 3 (three) years, which may be extended for 1 (one) tenure only. Complied -1 (3) Qualifica�on of Independent director1(3) (a) Shall be a knowledgeable individual with integrity able to ensure compliance with financial laws, regulatory requirements and corporate laws Complied - 1 (3) (b)(i) Business leader who is or was a promoter or director of an unlisted company having minimum paid capital of Tk100.00 million or any listed company or a member of any na�onal or interna�onal chamber of commerce or business associa�on Complied - 1 (3) (b)(ii) Should be a Corporate Leader Complied - 1 (3) (b) (iii) Formal official of government or statutory or autonomous or regulatory body in the posi�on not below 5th grade of the na�onal pay scale. Complied - 1 (3) (b) (iv) University Teacher who has educa�onal background in Economics or Commerce or Business Studies or Law. Complied - 1 (3) (b) (v) Professional who is or was an advocate prac�cing at least in the High Court Division of Bangladesh Supreme Court or a CA/CMA/CFA/CCA/CPA or Chartered Management Accountant/CS or equivalent qualifica�on Complied - 1(3)(c) The independent director shall have at least 10 (ten) years of experiences in any field men�oned in clause (b) Complied - 1(3)(d) Relaxa�on in special cases subject to prior approval of the commission - -

1 (4) Duality of Chairperson of the Board of Directors and Managing Director or Chief Execu�ve Officer1 (4) (a) The posi�ons of Chairperson of the board and MD and/or CEO of the company shall be filled by different individuals. Complied - 1 (4) (b) MD and/or CEO of a listed Company shall not hold the same posi�on in another listed Company Complied - 1 (4) (c) The chairperson of the Board shall be elected from among the non-execu�ve directors of the company. Complied - 1 (4) (d) The board shall clearly define respec�ve roles and responsibili�es of the chairperson and the managing director or chief execu�ve officer Complied -

Not Applicable (No Special Case arose)

Status of compliance with the condi�ons imposed by the Commission’s No�fica�on No. BSEC/CMRRCD/2006-158/207/Admin/80, dated June 03, 2018 issued under sec�on 2CC of the Securi�es and Exchange Ordinance, 1969 is presented below:

Not holding any share of the company

49 NITOL Insurance Co. Ltd.Annual Report 2018

1 (4) (e) In absence of Chairperson of the Board, the remaining members may elect one of themselves from non-execu�ve directors as Chairperson for that par�cular Board’s mee�ng Complied - 1 (5) The Directors’ Report to Shareholders1 (5) (i) Industry outlook and possible future developments in the industry Complied - 1 (5) (ii) Segment-wise or product-wise performance Complied - 1(5) (iii) Risks and concerns including internal and external risk factor, threat to sustainability and nega�ve impact on environment Complied - 1(5) (iv) Discussion on Cost of Goods sold, Gross Profit Margin and Net Profit Margin. Complied - 1(5) (v) Discussion on con�nuity of any extra ordinary ac�vi�es and their implica�ons Complied - 1(5) (vi) Detailed discussion and statement on related party transac�ons Complied - 1(5) (vii) Statement of u�liza�on of proceeds from public issues, rights issues and/or through any others instruments Complied - 1(5) (viii) An explana�on if the financial results deteriorate a�er the company goes for IPO, RPO, Rights Offer, Direct Lis�ng etc - -1(5) (ix) Explana�on on any significant variance occurs between Quarterly Financial Performance and Annual Financial Statements Complied - 1(5) (x) Remunera�on to directors including independent directors Complied - 1(5) (xi) The financial statements prepared by the management of the issuer company present fairly its state of affairs, the result of its opera�ons, cash flows and changes in equity Complied - 1(5) (xii) Proper books of account of the issuer company have been maintained Complied - 1(5) (xiii) Appropriate accoun�ng policies have been consistently applied in prepara�on of the financial statements and that the accoun�ng es�mates are based on reasonable and prudent judgment Complied - 1(5) (xiv) Interna�onal Accoun�ng Standards (IAS)or Interna�onal Financial Repor�ng Standards (IFRS), as applicable in Bangladesh, have been followed in prepara�on of the financial statements and any departure therefrom has been adequately disclosed. Complied - 1(5) (xv) The system of internal control is sound in design and has been effec�vely implemented and monitored. Complied - 1(5) (xvi) A statement that minority shareholders have been protected from abusive ac�ons by, or in the interest of, controlling shareholders ac�ng either directly or indirectly and have effec�ve means of redress - -1(5) (xvii) Statement that there is no significant doubt upon the issuer company’s ability to con�nue as a going concern, if the issuer company is not considered to be a going concern, the fact along with reasons there of shall be disclosed Complied - 1(5) (xviii) Significant devia�on from last year’s opera�ng results of the issuer company shall be highlighted and the reasons there of shall be explained Complied - 1(5) (xix) Key opera�ng and financial data of at least preceding 5 (five) years shall be summarized. Complied - 1(5) (xx) If the issuer company has not declared dividend (cash or stock) for the year, the reasons there of shall be given - - 1(5) (xxi) Broad’s statement to the effect that no bonus shares or stock dividend has been declared as interim dividend. - -1(5) (xxii) The number of Board mee�ngs held during the year and a�endance by each Director shall be disclosed Complied - 1(5) (xxiii) A report on the pa�ern of shareholding disclosing the aggregate number of shares (name wise details) Complied -

1(5) (xxiii) (a) Parent/Subsidiary/Associated Companies and other related par�es (name wise details) - -

1(5) (xxiii) (b) Directors, CEO, Company Secretary, CFO, Head of internal Audit and Compliance and their spouses and minor children(name wise details) Complied - 1(5) (xxiii) (c) Execu�ves Complied - 1(5) (xxiii) (d) Shareholders holding ten percent (10%) or more vo�ng interest in the company (name wise details). - -1(5) (xxiv) (a) A brief resume of the director in case of appointment or reappointment. Complied - 1(5) (xxiv) (b) Nature of his/her exper�se in specific func�onal areas Complied - 1(5) (xxiv) (c) Names of companies in which the person also holds the directorship and the membership of commi�ees of the board. Complied -

Not Applicable (Nitol Insurance Company Limited

does not have parent/Subsidiary/Associated

company)

Not Applicable (15% Cash Dividend was Proposed)

Not Applicable

Not Applicable

Not Applicable

Compliance Report on BSEC’s Notification

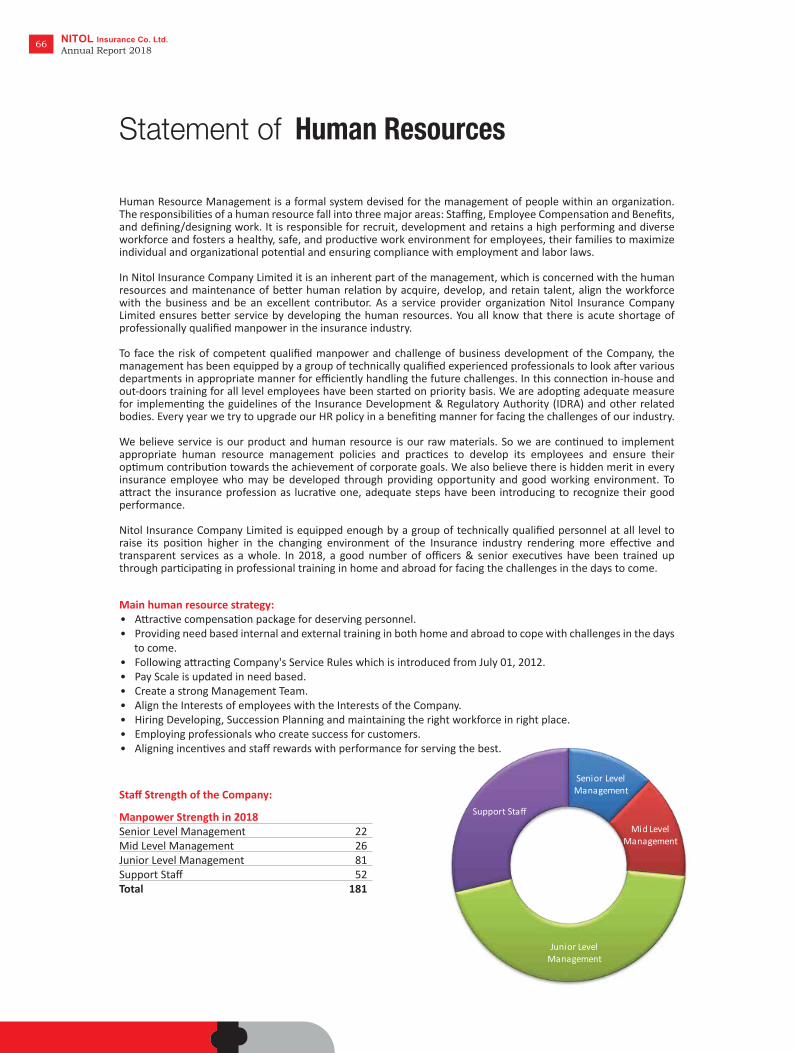

50 NITOL Insurance Co. Ltd.Annual Report 2018