Embed Size (px)

Citation preview

REPORTANNUAL 2015

ANNUAL REPORT MILLENNIUM ANGOLA 2015

CONTENTS

ANNUAL REPORT2015

2015 Contents 5

5 Message of the Chief Executive Officer

6 Main Highlights

7 Key Indicators

8 Executive Committee

9 Shareholder Structure and Governing Bodies

10 Economic Environment

20 Regulatory Changes to the Financial System

24 Business Summary

38 Distribution Network

46 Financial Statements

51 Notes to the Financial Statements

93 Proposed Appropriation of Net Income

94 Independent Auditors' Report

96 Opinion of the Supervisory Board on the Account of 2015

CONTENTS

MESSAGE OF THE CHIEF EXECUTIVE OFFICER

ANNUAL REPORT2015

2015 7

MESSAGE OF THE CHIEF EXECUTIVE OFFICER

Throughout 2015 and in the wake of the constraints of the economic context of 2014, the Angolan economy

was severely affected by the sharply declining price of the barrel of oil in international markets and, consequently,

by the lack of foreign currency to fund imports, on which Angola is heavily dependent. This scenario has made

it very clear that there is an imperative need for economic diversification, in order to facilitate the business

environment and attract direct investment towards other activity sectors, outside the petroleum sector, which

shall boost the Angolan economy in the medium term.

The fall in the price of oil significantly reduced fiscal revenue and the obtaining of foreign currency. This evolution

particularly constrained private consumption and public investment, and contributed to the GDP growth rate

having shifted from 4.8% in 2014, to 3.5% in 2015, according to IMF forecasts. In this environment, the kwanza

devalued sharply and the inflation rate exceeded 14%, imposing the need for a more restrictive monetary policy.

In 2016, the IMF expects that the GDP growth rate should continue at 3.5%, supported by the effects of the

policies which have been progressively adopted with a view to reducing dependence on the petroleum sector

and assuring a greater diversification of economic activity.

In 2015, Banco Millennium Angola opened 2 Branches and 1 Prestige Centre, thus holding a network, as

at 31 December 2015, of 89 Retail Branches, of which 54 are open every Saturday morning, 13 Prestige

Centres and 8 Business Centres, of which 2 are dedicated to the oil industry, amounting to a total of 110

Customer attendance points by the end of 2015.

As a result of the expansion of the network and the increasingly higher penetration rate in the market by the

oldest Branches, the number of Customers grew by 12% in relation to the previous year.

The net income of Banco Millennium Angola stood at 6,760 million kwanzas in 2015, corresponding to 18%

more than the previous year. This figure was influenced by the positive evolution of net operating income, in

spite of the growth of operating costs (derived from inflation, exchange rate devaluation and wage revision) and

provisions.

Net operating income increased by approximately 38% compared to 2014, driven by the performance of net

interest income and the earnings from financial transactions, which recorded growth rates of 28% and 121%,

respectively.

The return on average equity (ROAE) stood at 17.0% in 2015 (16.1% in 2014), and the solvency ratio as at 31

December 2015 was 13.7% (-0.1 p.p. compared to 31 December 2014). The coverage ratio of loans overdue

by more than 90 days by provisions evolved to 267%, as at 31 December 2015, compared to 196%, as at 31

December 2014.

During 2015, BMA's staff grew by 7.2%, shifting from 1,143 Employees in 2014 to 1,225 Employees in 2015,

which implied an increase of 82 new Employees, with the proportion of Angolans in the staff remaining stable,

at around 98%.

The Talent Management and Retention Policy included two new Programmes for Development of Skills –

Millenniuns High Potential, held in collaboration with Universidade Católica de Lisboa, and People Grow (junior

Employees aged below 35 years old with potential and employed for less than 2 years).

Throughout 2015, 161 training actions were carried out, corresponding to 4,017 training hours, with natural

focus on contents directed at duties of the Commercial Area, covering all the essential aspects for a good

performance of daily activities, both from the technical and behavioural point of view.

Finally, and as usual, my sincere gratitude is extended to all the Employees for the effort, dedication and care with

which they dealt with the challenges faced in 2015. A special acknowledgment is also made of our Customers

for the preference and confidence that has been unfailingly demonstrated and for the privilege of serving them,

with the assurance of BMA's commitment to continue to endeavour towards the continuous and sustained

improvement of the quality of the service provided.

My sincere thanks to all.

Chief Executive Officer

8 2015

MAIN HIGHLIGHTS

NET INCOME

6,760million AOA

RETURN ON AVERAGE EQUITY

(ROAE)

17.0%

COST-TO-INCOME

45.8%

SOLVENCY RATIO

13.7%

NUMBER OFCUSTOMERS

597,263

NUMBER OFEMPLOYEES

1,225

NUMBER OF BRANCHES, BUSINESS CENTRES

AND PRESTIGE CENTRES

89+8+13 =110

TOTAL CUSTOMER FUNDS

249,111million AOA

GROSS CREDIT

146,936million AOA

2015 9

KEY INDICATORS

KEY MANAGEMENT INDICATORS2015

(Million 2014

(Million AOA) Change %

2015(Million

2014(Million USD)(*) Change %

BALANCE SHEET

Total net assets 244,669 40% 2,378.6 7%

Loans to Customers (gross values) 125,542 17% 1,220.5 -11%

Loans to Customers, net of provisions 117,748 13% 1,144.7 -14%

Total Customer funds 180,900 38% 1,759.0 5%

Total net loans/Customer resources 65.1% -11.5 p,p, 65.1% -11.5 p,p,

Net worth 38,092 18% 369.9 -10%

Solvency ratio 13.8% -0.1 p,p,

PROFITABILITY

Net operating income 19,354 38% 196.9 13%

Operating costs 9,815 25% 99.9 3%

Provisions 2,705 148% 27.5 103%

Industrial tax 1,018 10% 10.4 -10%

Net income for the year 5,741 18% 58.4 -3%

Net interest income/Net operating income 58.5% -4.3 p,p,

Net fees/Net operating income 22.2% -4.5 p,p,

Financial results/Net operating income 17.4% 10.5 p,p,

Return on Average Assets (ROAA) 2.5% -0.1 p,p,

Return on Average Equity (ROAE) 16.1% 0.9 p,p,

STRUCTURE

Number of Branches, Business Centres and Prestige Centres 110 107 3%

Luanda 76 74 3%

Other provinces 34 33 3%

Number of active ATM (**) 120 119 1%

Number of active POS (**) 1,938 48%

Number of active Cards (**) 148,785 33%

Number of Employees 1,143 7%

Number of Customers 534,101 12%

EFFICIENCY AND PRODUCTIVITY

Cost-to-income 50.9% -5.1 p,p,

Number of Employees/Number of Branches, Business Centres and Prestige Centres

10.7 4.3%

Net income/Average number of Employees 5.2 8.9%

Net operating income/Average number of Employees 17.6 27.4%

Structural costs/Average number of Employees 8.9 15.9%

Number of Customers/Number of Branches, Business Centres and Prestige Centres

4,992 8.8%

CREDIT QUALITY

Loans overdue > 90 days as % of loans to Customers 3.2% 0.2 p,p,

Coverage of loans overdue > 90 days by provisions 196% 71 p,p,

(*) Merely indicative values in USD (conversion of values in national currency at the average exchange rate of USD/AOA for the values of the Income Statement:

98.291 in 2014 and 119.717 in 2015; and at the exchange rate of USD/AOA at the end of the year for the Balance Sheet headings: 102.863 in 2014 and

135.315 in 2015).

(**) Source: EMIS Monthly Statistics Report relative to the months of December 2014 and 2015.

10 2015

Chief Executive Officer Vice-PresidentJoão MatiasMemberMember Member

EXECUTIVE COMMITTEE

2015 11

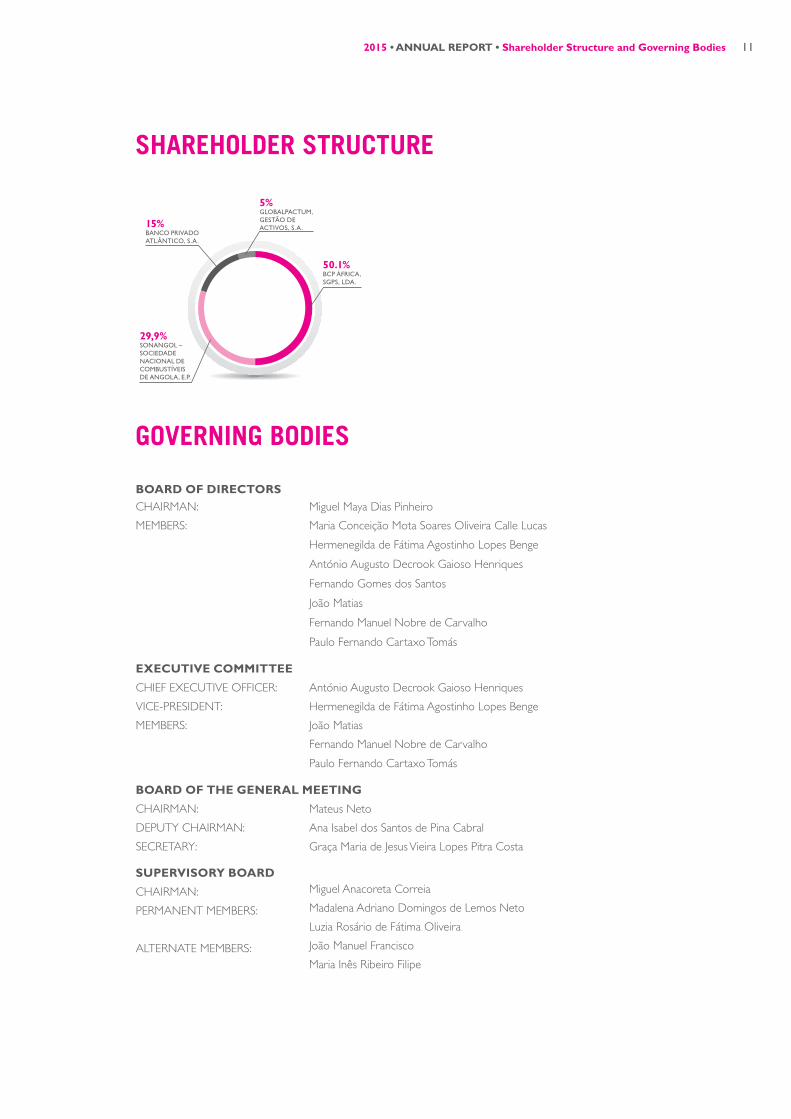

SHAREHOLDER STRUCTURE

GOVERNING BODIES

29,9%SONANGOL –

SOCIEDADE

NACIONAL DE

COMBUSTÍVEIS

DE ANGOLA, E.P.

50.1%BCP ÁFRICA,

SGPS, LDA.

15%BANCO PRIVADO

ATLÂNTICO, S.A.

5%GLOBALPACTUM,GESTÃO DE

ACTIVOS, S.A.

CHAIRMAN: Miguel Maya Dias Pinheiro

MEMBERS: Maria Conceição Mota Soares Oliveira Calle Lucas

Hermenegilda de Fátima Agostinho Lopes Benge

António Augusto Decrook Gaioso Henriques

Fernando Gomes dos Santos

João Matias

Fernando Manuel Nobre de Carvalho

Paulo Fernando Cartaxo Tomás

CHIEF EXECUTIVE OFFICER: António Augusto Decrook Gaioso Henriques

VICE-PRESIDENT: Hermenegilda de Fátima Agostinho Lopes Benge

MEMBERS: João Matias

Fernando Manuel Nobre de Carvalho

Paulo Fernando Cartaxo Tomás

CHAIRMAN: Mateus Neto

DEPUTY CHAIRMAN: Ana Isabel dos Santos de Pina Cabral

SECRETARY: Graça Maria de Jesus Vieira Lopes Pitra Costa

CHAIRMAN: Miguel Anacoreta Correia

PERMANENT MEMBERS: Madalena Adriano Domingos de Lemos Neto

Luzia Rosário de Fátima Oliveira

ALTERNATE MEMBERS: João Manuel Francisco

Maria Inês Ribeiro Filipe

12 2015

ECONOMIC ENVIRONMENT

GLOBAL ECONOMIC ENVIRONMENT

According to the projections of the International Monetary Fund (IMF), the rate of expansion of global economic

activity, in 2015, is estimated to have fallen to the lowest level since 2009, in a context where the strong dynamics of

the developed economies was not sufficient to offset the loss of vibrancy of the emerging markets. The pronounced

decline in the price of raw materials, in addition to having intensified the split between the two groups of economies,

further deepened global deflationary pressures, creating a scenario of greater financial vulnerability, as well as the need

to maintain widespread accommodative monetary conditions.

In the euro zone, the improvement of monetary conditions, derived from the more expansionary position endorsed

by the European Central Bank (ECB), the effective depreciation of the euro, the reduction of the cost of energy and

the greater neutrality of the budgetary policies of the "peripheral" countries have boosted the process of economic

recovery. In fact, after the 0.9% growth in 2014, the European Commission (EC) estimates that GDP should have grown

by 1.6% in 2015 and that in 2016 the rate of expansion should increase to 1.8%. However, the weakness of the emerging

economies, the aggravation of geopolitical tensions and the risks inherent to the need to continue with the structural

reforms in course in various Member States may eventually constrain the rate of recovery of the euro zone.

In the USA, the sustained increase of employment and real disposable income, combined with the low level of interest

rates, have driven consumption and residential investment. Nonetheless, the recession associated to the collapse of

the price of oil which has ravaged the North American energy sector and the appreciation of the dollar have exerted

an adverse effect on business investment and exports, which resulted in a GDP growth rate similar to that observed

in 2014, which stood at 2.4%. In 2016, the evolution of private consumption should be the pendulum determining

the robustness of economic growth, which in turn should imply a good performance of the labour market, under

circumstances hampered by the presumable normalisation of monetary policy and concomitant intensification of the

trend of appreciation of the dollar relative to all the other main international currencies.

GLOBAL ECONOMIC GROWTH REMAINS MODERATE

Annual growth rate of real GDP (in %)

World economy Developed economies Emerging economies

0

-4

-2

2

4

6

8

0

-4

-2

2

4

6

8

Source: IMF WEO (January 2016).

2016(p.)201520142009 2010 2011 2012 2013

2015 13

The Chinese economy continued to show clear signs of loss of vigour throughout 2015, especially in terms of

the demand components which had substantiated its growth model, namely concerning exports and investment.

The principal risk for 2016 resides in the possible further weakening of the renmimbi, which would carry the

associated risk of capital flight and consequent deterioration of financial conditions for Chinese households and

businesses.

In 2016, the global economy shall face complex and varied risks. The negative spiral lodged between the

productive sector of commodities and the emerging economies threatens to continue to restrict the recovery

of global demand and cause a correction in international financial markets. On the other hand, the expected

increase of reference interest rates set by the Federal Reserve and the consequent aggravation of the high level

debt service of the business sector of the USA embody the risk of retraction of investment and, furthermore,

consumption. Finally, the prevalence of various focus points of geopolitical tension and security issues in Europe

constitute barriers whose effects are difficult to quantify, but even so are considered potentially adverse to the

consolidation of the economic upswing of the euro zone.

GLOBAL FINANCIAL MARKETS

The evolution of the financial markets in 2015 was dominated by increased volatility, presumably derived from

the uncertainty relative to the implications for the global economy of the slowdown of the emerging markets

and the beginning of the process of reversal of the expansionary policy of the North American Federal Reserve.

In this context, the geographic areas where monetary policy was more accommodative, as was the case of the

euro zone and Japan, as a rule, recorded levels of appreciation of financial assets above those of the economies

in which monetary conditions had become more restrictive, as occurred in the USA and, with less intensity, in

the emerging markets. The reference stock market indices of the USA closed the year with zero or negative

appreciation, while the equivalent European and Japanese indices recorded gains of around 10%. Concerning

exchange rates, the most notable development was the appreciation of the United States dollar, in particular,

relative to the currency of countries that are most dependent on commodity exports.

In contrast to the previous years, the performance of the international debt market in 2015 was marked by a clear

divergence between the stability of the prices of securities issued by extremely credit-worthy entities on the one

hand, and the devaluation of higher risk bonds on the other hand. In the euro zone, in spite of the ECB having

GLOBAL STOCK MARKET INDEX DEVALUED AND VOLATILITY INCREASED

World equity index (Jan 2014 = 100)

Euro Stoxx 600 bank index (Jan 2014 = 100)

Volatility index (VIX)

Source: Datastream.

May 15 Sep. 15 Nov. 15Jul. 15 Dec. 15Jan. 15 Mar. 1585

90

95

100

105

125

110

115

120

25

45

30

35

40

20

15

10

14

implemented a public debt purchase programme, the risk premiums of the sovereign debt of the "peripheral"

countries showed an erratic performance, but without a defined direction, after the very significant compression

which occurred between 2013 and 2014. Even so, the intensification of the expansionary content of the ECB's

monetary policy, including the setting of the deposit facility interest rate at negative values, produced a shift of the

Euribor rates to levels below zero up to the period of six months and contributed to the depreciation of the euro,

especially relative to the dollar.

OUTLOOK FOR THE PORTUGUESE ECONOMY

The recovery of the Portuguese economy consolidated throughout 2015 benefited from the lower funding costs,

the fall in the price of oil, the acceleration of the European economy, the gains of external competitiveness derived

from the effective depreciation of the euro and, in a more indirect manner, from the structural reforms implemented

during the adjustment programme. According to the European Commission estimate, GDP should have grown by

1.5% in 2015, above the 0.9% recorded in 2014. The greater strength of economic activity was essentially due to the

buoyancy of private consumption and exports, as investment continued at a lower rate than in the preceding year.

In 2016, the trend of recovery of activity should continue supported by domestic demand, which should benefit

from the increased employment and disposable income, the low cost of energy, the low level of interest rates and

also from the implementation of the new European funding framework, namely the Portugal 2020 programme.

However, the risk of slowdown of the international economy combined with the fragility of the emerging markets,

and the possible occurrence of a significant correction in financial markets, constitute the main barriers to the

sustained recovery of the national economy.

The postponement of the process of sale of Novo Banco to 2016 and the application, at the end of the year, of

a measure of resolution to Banco Banif were marking events in the evolution of the Portuguese banking system

in 2015, disturbing the process in course of improved profitability, and consolidation of the liquidity and solvency

position of credit institutions in Portugal, reflected in the progressive attenuation of the trend of reduction of credit

granted to the economy.

The profitability of the financial sector in 2015, excluding the cases mentioned above, tended to improve in relation

to the previous year, based, on the one hand, on the favourable evolution of the core income (i.e. net interest

income and fees) and on the gains in financial transactions associated to the improvement of the country's risk

premium, especially in the first half of the year, and on the other hand, due to the less negative evolution of the cost

of risk and greater contention of operating costs in Portugal.

PORTUGUESE ECONOMY CONTINUES ALONG THE PATH OF RECOVERY

GDP (real year-on-year growth rate in %)

Coincident indicator (Millennium bcp)

Source: Datastream and Millennium bcp.

Mar. 11 Mar. 12 Mar. 13 Mar. 15Mar. 10

-6

-4

-2

0

2

4

-6

-4

-2

0

2

4

2015

15

Sustaining the process of improved profitability remains one of the primary challenges to be faced in 2016, the success

of which shall greatly depend on the risks and uncertainties of the international context, the recovery of the Portuguese

economy and the relative evolution of the cost of risk and net interest income. The repercussions of the resolution

process constitute latent factors of uncertainty in the banking business, both in terms of the confidence shown by

Customers and investors, and regarding the profound alteration of the competitive context of the Portuguese market.

The deepening of the Banking Union and the consequent regulatory framework, the financial integration under the

wings of the Capital Markets Union project and the use of new business concepts derived from the endorsement

and application of new technological potentialities shall continue to be motives for the banks to rethink their business

strategy and positioning.

INTERNATIONAL OPERATIONS

According to IMF estimates, Poland recorded a GDP growth rate of 3.5% in 2015, presenting itself as one of the

most dynamic economies of the European Union. The primary contribution to this performance came from private

consumption, underpinned by the increased disposable income, the easy access to credit and the improvement of the

labour market, further boosted by the favourable evolution of investment. In turn, net external demand should have

contributed nothing to GDP. The scenario of great buoyancy in economic activity was not, however, reflected in a rise

of inflation, due to the persistence of strong external deflationary pressures. In this context of low levels of inflation,

the monetary policy continued accommodative, which contributed to the relative stability of the zloty in relation to the

euro for the year as a whole. For 2016, the IMF forecasts that Poland should maintain robust growth levels, not excluding,

however, the risks for economic activity, sustainability of public finance and compliance with the European commitments

that may arise from the policies announced by the government which took up office following the legislative elections

of October 2015.

After five consecutive years recording growth rates above 7%, the Mozambican economy appears to have slowed down

in 2015, with the IMF projecting an expansion of 6.3%. This evolution was determined by the reduction of commodity

prices, in particular of gas, coal and aluminium, which led to a decline of revenue from export of commodities and

cooling down of direct foreign investment, which resulted in a deterioration of the current account of the balance of

payments and, consequently, the devaluation of the metical. The exchange rate instability, particularly accentuated in

November, led the Mozambican government to request an emergency loan from the IMF and adopt a more restrictive

monetary and budgetary policy aimed at restoring economic stability. In this context, concerns deepened regarding the

sustainability of public debt (primarily denominated in foreign currency), which led to a downward revision of the ratings

attributed by the international agencies. For 2016, in spite of the international scenario being challenging, the IMF foresees

a minor acceleration of the Mozambican economy, underpinned by productivity gains expected in agriculture and by the

expansion of coal production, following the opening of new transport channels, namely by railway.

In 2015, the Angolan economy pursued its trajectory of deceleration. The fall in the price of oil significantly reduced fiscal

revenue and the obtaining of foreign currency inherent to exports of the energy sector, which particularly constrained

private consumption and public investment, having contributed to the GDP growth rate having shifted from 4.8% in

2014, to 3.5% in 2015, according to IMF forecasts. In this environment, the kwanza recorded a sharp devaluation and

the inflation rate stood at close to 10%, imposing the need for more restrictive monetary policy. In 2016, the IMF

expects that the GDP growth rate should continue at 3.5%, supported by the effects of the policies which have been

progressively adopted with a view to reducing dependence of the petroleum sector and assuring a greater diversification

of economic activity, as the external context should remain adverse, especially with respect to the progression of the

Chinese economy and evolution of the price of oil.

GROSS DOMESTIC PRODUCT

Annual growth rate (in %)

2013 2014 2015 2016 2017

EUROPEAN UNION 0.2 1.5 1.5 1.4 1.3

Portugal -1.6 0.9 1.6 1.5 1.4

Poland 1.7 3.4 3.5 3.5 3.6

SUB-SAHARAN AFRICA 5.2 5.0 3.5 4.0 4.7

Angola 6.8 4.8 3.5 3.5 3.8

Mozambique 7.4 7.4 6.3 6.5 7.9

Source: IMF (February 2016).

IMF estimate.

2015

16

ANGOLAN ECONOMY

Throughout 2015 and in the wake of the constraints of the economic context of 2014, the Angolan economy was

severely affected, experiencing situations of evident economic and financial crisis derived from the abrupt, accentuated

and persistent decline of the prices of the barrel of oil in the international market and, consequently, the lack of foreign

currency to fund imports, on which Angola is heavily dependent. These two aspects significantly compromised the

continued growth of the Angolan economy over the entire year in reference. These factors influenced the volume

of revenue obtained to maintain macroeconomic stability, reflected in the reduction of domestic production, in the

aggravation/increase of the exchange rate and inflation rate – which shows a galloping upward trend – and in the

significant decline of purchasing power parity, affecting the disposable income of the population in a widespread manner,

which has felt in the slowdown of demand.

The initial outlook embodied in the Angolan State Budget for 2015 indicated that the country should see its public

accounts shift from a surplus to a deficit position due to the reduction of fiscal revenue derived from the lower

price of oil, implying a reduction in budget results. Public debt should reach a figure of 38.7 million euros, equivalent

to 35.5% of GDP, combining External Debt (24.5%) and Domestic Debt (11%). The State deficit should grow 38

times between 2014 and 2015. The stock of public debt should be exacerbated with an estimated debt of 7.6%

in public accounts, signalling the enormous difficulties expected in 2015, despite the outlook of year-on-year GDP

growth of 9.7%.

The Angolan State Budget for 2015 was drawn up with forecast expenditure of 5,215 trillion AOA and revenue

of 4,184 trillion AOA, the latter corresponding to 11.80% less than in 2014, with fiscal revenue derived from oil

standing at 2.5 trillion AOA, representing a decline of 16% in relation to the estimate for this year and 66% of

current revenue. Production is estimated to increase by 10.7%, from 604.4 million barrels in 2014, to 669.1 million

barrels in 2015. The Budget also forecast an inflation rate of 7%, an exchange rate of 99.10 AOA per dollar, and a

money growth rate based on M2 of 16%, with a stock of net international reserves of 23.5 billion dollars.

Operating in a context of uncertainty and as a precautionary measure, the Angolan State Budget was prepared

based on a fiscal price of 81 dollars per barrel, forecasting a revenue of 2,551 billion AOA (21.2 billion euros).

In view of the persistent slump in the price of the barrel of oil in the international market, it was decided that a

budgetary review was required which established the budgetary average reference price of crude oil at 40 USD,

reflecting a loss of 14 billion USD, to levels above 50%, and a cut in State current expenditure (goods and services)

of 50% and 53% in public investment.

EVOLUTION OF THE AVERAGE PRICE AND MONTHLY CHANGE

IN THE PRICE OF THE BARREL OF OIL

Monthly Average Price of the Barrel of Oil

(USD) Change (%)

Source: World Bank.

Jan. 1

4

Feb. 1

4

Mar

. 14

Apr. 1

4

May

14

Jun. 1

4

Jul.

14

Aug.

14

Sep. 1

4

Oct

. 14

Nov.

14

Dec

. 14

Jan. 1

5

Feb. 1

5

Mar

. 15

Apr. 1

5

May

15

Jun. 1

5

Jul.

15

Aug.

15

Sep. 1

5

Oct

. 15

Nov.

15

Dec

. 15

0

20

40

120

60

80

100

-10%

20%

-5%

0

5%

15%

10%

-15%

-20%

-25%

2015

17

The economy and consequently the Angolan financial system have been visibly shaken by the current situation of

world markets. In order to reduce the identified vulnerabilities and reinforce the measures aimed at containing

the downward spiral of the country's economic and financial circumstances, the government embarked upon

a series of initiatives aimed at maximising the reversal of the scenario of economic deterioration, triggering and

reinforcing actions aimed at (1) diversifying the economy circumscribed in the national objectives of the policy

to promote and diversify economic development, 2013-2017; (2) intensifying the implementation of the tax

reform, so as to widen the tax base and lower the vulnerability of public expenditure to fluctuations in the price

of the barrel of oil; and (3) reverse the course of contractionist fiscal policy, seeking to expand non-oil revenue

and enhance the quality of State expenditure. For this purpose, urgent resources for the funding of the economy

have been mobilised, domestically and externally, namely through the issue of public debt on the domestic and

external market – Angola made its first incursion into the internal capital market, with the issue of eurobonds,

on 5 November, launching a public debt issue of 1.5 billion dollars at ten years, with an annual interest rate of

9.5%, as well as via the attraction of domestic and external loans from China, Brazil and the International Bank

of Reconstruction and Development (IBRD). By mid October, the value of public debt corresponded to 5.8%

of the GDP projected for 2015.

Economic and social development programmes were implemented, aimed at reinforcing and improving the

water supply and sanitation system, expanding the capacity of production and system of transport of electricity,

involving logistics platforms, the recovery and maintenance of roads and hospital and education infrastructures.

The petroleum sector is expected to grow by around 7.8% – as a consequence of increased oil production of

around 1.8 million barrels of crude per day, while the non-oil sector is forecast to grow by 2.4%, which aggregates

growth levels of 2.5% in agriculture, 2.6% in manufacturing industry and 2.2% in trade services. The energy sector

should grow by 12%, the construction sector by 3.5% and the diamond sector by 3.2%.

The government was forced to optimise the burden of subsidies, due to the effect associated to the slump in

oil revenue and adjustment of the exchange rate on the import price of petroleum derivatives. Fuel prices were

increased, significantly reducing the State monetary contribution in this range of products. From 1 January 2016

onwards, diesel was no longer subsidised by the Angolan government with the price becoming subject to the

free market system, and likewise for petrol since April, with new price increases having occurred on that date.

Also in terms of government policy to address the less favourable international and domestic economic and

financial environment, and aimed at optimising the burden of subsidies and lowering them to the levels of

coverage of the fiscal revenue, the government also adjusted electricity and drinking water tariffs for the

provinces of Luanda and Benguela, pursuant to Executive Decree 705/15 and the combined Executive Diploma,

both of 30 December, of the Ministry of Finance and Ministry of Energy and Water.

The adjustments carried out to the fuel, energy and water subsidies enabled the saving of funds aimed at the

rational coverage of public and private expenditure and creation of space to assure the coordinated conduct of

fiscal, monetary and foreign exchange policies as well as the funding of actions relative to the objectives of the

National Development Plan 2013-2017.

The Angolan financial system has recorded a significant liquidity deficit in terms of external currency/USD to

meet market needs, in particular relative to imports, remittances and transfer of foreign currency and payments

abroad, via debit/credit cards, indicating a decline in the country's Net International Reserves – the total value of

the amount auctioned in November represented merely 33.6% of the corresponding amount auctioned in June.

This illustrates the country's difficulty in dealing adequately with the Balance of Payments imbalances, controlling

and influencing the exchange rate, assuring confidence in the national currency and promoting a reference

monetary policy for foreign investors and loans.

The supply of dollars to the market via the banking system has proved to be increasingly more rationed and

restricted, with the evident reduction of the offer of foreign currency in the primary market, giving rise to

galloping speculation around the dollar in the informal market. In view of a context aggravated by the need for

foreign currency and in an attempt to develop mechanisms to adjust/stabilise the foreign exchange market and

money market, Banco Nacional de Angola (BNA) set in motion a series of actions, aimed at maintaining the

control/tight hold of monetary and exchange rate policy, via devaluation of the Angolan currency during the year,

specifically on 4 June and 10 September. The kwanza lost 37% of its value with respect to the American dollar,

in the primary market, the strongest annual devaluation of the dollar since October 2009. As at 31 December

2015, the dollar stood at 400 AOA on the informal market. Nevertheless, on 4 January 2016, BNA once again

increase the dollar exchange rate to 156.386 kwanzas.

2015

18

The deterioration of the USD/AOA exchange rate undermined the confidence of economic agents and significantly

affected the inflation rate, which surpassed two digits. One of the focus points of the government's measures to

control the fiscal and monetary policy should involve the challenge of controlling the rate of inflation, combined

with the protection of net international reserves. The control of this issue shall be one of the arguments to boost

the recovery of the confidence of the domestic and external market.

Another measure taken by BNA, aimed at safeguarding the exercise of transparency in banking activity and

fostering confidence in the Angolan financial system, in line with the foreign pressure derived from the drying up

of dollars in Angola by North American banks, was the publication of Directive 2/DRO/DSI/15, Guidelines on the

Prevention of Money Laundering and Combat of Terrorist Financing in Relations with Correspondent Banks and

Client Banks, and the launch of a media campaign aimed at reiterating the commitment to combat illegal financial

flows. These measures seek to strengthen the regulatory mechanisms and guidelines on this matter, in relations with

correspondent banks and client banks. On this issue, the impact of the EIU (Economist Intelligence Unit) forecast is

that the BNA's commitment to clean up the country's financial system is positive. Albeit addressing illegal financing

flows, this Directive shall also require strong enforcement measures; hence, while not being guaranteed in the

opinion of the EIU, its forecasts continue unchanged.

During 2015, the Angolan economy was subject to an adverse circumstantial context, which shows no prospect

of recovery in the short and medium term. The significant variation of the targets associated to the fundamental

assumptions of the Angolan economic model has compromised the achievement of the State Budget targets, as

well as the goals and objectives of the National Development Plan 2013/2017. The price of its most important

resource, oil, has stood, in some circumstances and in an accentuated form, at levels below USD 40, having reached

the average value of USD 36.5 in the month of December and annual value of USD 53. Consequently, Angolan

fiscal revenue fell by 850 billion kwanzas, with this indicator having plunged by 26.35% over a 12 month period,

from the total of 4,096 billion kwanzas in 2014, to 3,242 billion kwanzas in 2015. The exchange rate on the primary

market stood at 130.68 AOA per dollar and the inflation rate reached 14.27%, greatly above the projected 7.46%.

Net international reserves declined by 11.53%, corresponding to 24.1 billion dollars for around six months of

imports. The expected economic growth of 4.8% was cut to effective growth of merely 2.8%, in spite of the

increased oil production of very close to 1.8 barrels/day.

Monthly inflation

Accumulated inflation

Inflation over the last 12 months

Source: BNA.

EVOLUTION OF THE INFLATION RATE

0%

2%

4%

6%

8%

10%

16%

14%

12%

Jan

uar

y

Febru

ary

Mar

ch

April

May

June

July

Augu

st

Septe

mber

Oct

ober

Nove

mber

Dec

ember

2015

19

OUTLOOK FOR 2016

2016 shall be a difficult year for Angola, as the uncertainty around the evolution of the price of oil presents

considerable risks for budgetary implementation and for the prospects of economic growth, with the forecast

maintenance of the restrictive macroeconomic scenario. The world economic context of the petroleum sector,

concerning the constraints on demand and supply, point to a gloomy outlook for oil producing countries, in view of

the persistent outlook of the descending price of the barrel.

The slump in the price of oil has significantly reduced fiscal revenue and exports. The need to resolve the identified

vulnerabilities, and also to diversify the economy, improve the management of oil revenue volatility and implement

structural reforms to assure macroeconomic stability and the sustainability of national debt shall constitute the

primary challenges of the Angolan government in 2016. Accordingly, there is also a continuous need to search

for solutions for debt problems, relaunch imports, reduce the exchange rate, aimed at restoring the value of the

national currency, and reduce the inflation rate to stimulate demand.

According to the Angolan State Budget for 2016, the economy should grow at a more moderate rate, with a

stagnation of the administrative public sector. The Angolan government estimates real GDP growth of 3.3% – slightly

above the population growth rate of 3%/year –, relative to the estimated growth of the previous year (2.8%),

underpinned by an expected growth of 4.8% forecast for oil production, which should record an acceleration of 1.89

million barrels/day, following the expected increased production in the oil blocks of Cabinda and operationalisation

of the Mafumeira and Satelite Kizomba projects.

Also according to the State Budget, the sectors of the national economy which shall show strongest development

shall be energy, with a forecast growth of 20%, agriculture with expected growth of 4.6%, and the manufacturing

industry and construction sectors with 3.1%. Overall, in 2016, the non-oil sector shall record a moderate

reinforcement, with expected growth of 2.7%, in 2016, when compared with the 2.4% growth projected for 2015.

In terms of participation in GDP, the oil and non-oil sectors should contribute with 1.5% and 1.9%, respectively.

Budgeted in overall terms, with revenue and expenditure of equal value, at 6,429,287,906,777 kwanzas (38.2 billion

euros), the State Budget for 2016, approved at the National Assembly in December, is described by the government

as maintaining the austerity, due to the oil price crisis which, just in 2015, forced the cutting of one third of expenditure

and implies a deficit of 5.5%. According to the State Budget, all the wealth generated in Angola by oil should reach 3,301

billion kwanzas (19.3 billion euros) this year, with a forecast 3% increase in crude oil exports, to 689.4 million barrels. The

budget also forecasts an increased stock of public debt to 49.2 billion dollars, 49.7% of GDP (31.1% external and 18.6%

domestic), equivalent to half the national wealth that shall be generated by the country in 2016.

EVOLUTION AND FORECAST OF GDP AND GDP PER CAPITA

GDP (%)

GDP Per Capita (000)

Source: EIU/MINFIN-OGE/FMI.

2010 2011 2012 2013 2014 2015 2016

1

2

6

5

4

3

7

8

1

2

3

4

5

6

7

00

3.3

5.8

2015

20

The Angolan government projected for 2016 an average price of 45 USD per barrel exported, whereas the price on

the international market fell to values below 28 dollars in January, aggravating fears on the implementation of some

projects, investments and public expenditure of the country. The inflation rate was placed at 11%, corresponding

to the adjustments to be carried out in the economy, in line with the forecast in the National Development Plan

2013-2017, with a forecast deficit of 781.2 billion kwanzas, equivalent to 5.5% of GDP.

The principal potential risks for the national economy in 2016, related to international and national economic

circumstances, according to the State Budget, are: 1) the volatility of the price of oil and 2) exchange rate

depreciation. It is expected that the State Budget will be revised if the price of petrol does not rise, as the capacity

to repay foreign loans is strongly limited by the current capacity to generate foreign currency. In view of the

current scenario of the national economy and in the context of maintenance of the national objectives of the

policy to boost and diversify economic development for 2013-2017, the government has highlighted a series of

priorities that will be enforced under the following fundamental action programmes: Programme of Diversification

of National Production, which shall assure the construction of a solid and diversified economic base, aimed at

reducing the dependence on consumer product imports and the high dependence on oil sector exports, where

this programme shall include a structural reform in agriculture; Programme of Creation of Priority Clusters, directed

at the development of economic sectors which shall enable the constitution of comparative and competitive

advantages capable of relaunching the Angolan economy; and the Angola Invest Programme, which should create

and drive the Angolan business structure, strengthening it to a positioning that is more active, employment creating

and wealth generating for the country.

According to the IMF, public debt should increase significantly, but growth should remain stable, warning that the

economic and financial situation in Angola shall continue to be a challenge in 2016, because an oil price recovery

is not expected. However, the IMF noted that the growth of the Angolan economy in 2016 should continue stable

at around 3.5%.

The Centre for research and Scientific Studies (CEIC) estimates that the Angolan economy lost 555 million dollars

in the first 20 days of the year, due to the fall in the price of the barrel of crude oil in the international market, based

on the figures of the Angolan State Budget for 2016 for the export of the barrel of crude at 45 dollars, when the

price was already below 30 dollars. This aspect constitutes an indicator of the eminent possibility of a State Budget

revision.

The government has recently delineated a crisis mitigation strategy, as a consequence of the decline of the price

of the barrel of oil, assuring that it will focus on increasing non-oil tax revenue, optimising public expenditure and

rationalising the import of goods. On this last issue, the new customs tariff was enforced on 1 January, referring

to duties on imported items, such as mineral water. The measures to be adopted involve fiscal, monetary, external

trade and real economy aspects, aimed at reducing the impact of the scarcity of foreign currency in the national

economy.

Following this, the special contribution was announced applicable to most banking operations, at a rate of 0.1%,

except wages and deposits, which shall be enforced three months after the publication in Diário da República, and

the alterations to the Urban Property Tax, as a condition, among others, to offset the potential restriction in the

maintenance of the social programmes foreseen in the National Development Plan (PND) 2013-2017. Other

measures included the strengthening of action mechanisms of the General Tax Administration (AGT) to ensure

the continued growth rate of non-oil revenues; the stimulation of the tax enforcement mechanisms of taxpayer

debts; the continuation of the process of inspection of taxpayers receiving tax benefits; and the continuation of

the process of taxpayers in breach of labour income tax (IRT) obligations; follow-up of the process of optimisation

of subsidies in the price of fuel, energy and water (already undertaken), and collective urban, railway, sea or land

transport, through revision of the respective tariffs.

2015

21

Despite premature, the revision of the State Budget may be imminent, which is not a good sign for national

and foreign investors, as this scenario places in question the country's macroeconomic stability. This revision shall

naturally depend on the trend followed by the price of oil in the near future. The OPEC estimates that the demand

for oil should reach 31.6 million barrels per day in 2016, i.e. 1.7 million more than that estimated in January of

approximately 1.5 million barrels per day. Goldman Sachs lowered the forecast for Brent prices in 2016, 2017 and

2018 to 45 USD, 62 USD and 63 USD per barrel, respectively. Standard & Poor's reduced its oil price estimates in

2016 to 40 USD per barrel, from previous projections of 55 and 50 USD.

The World Bank issued a downward revision for its forecast oil price for 2016. The projection disclosed in October

2015 pointed to 51 dollars per barrel, while it is currently standing at 37 dollars per barrel. This revision takes into

account the restarting of exports from Iran and the slowdown of growth in the main emerging economies. Oil

prices fell by close to 47% in 2015 and, on average, should descend a further 27% in 2016. However, a gradual

recovery over the year is also expected, with probable cuts in production and strengthening of demand.

The economic context of 2016 faces numerous uncertainties, whose underlying theme gravitates around the

expected evolution of the price of oil. The International Monetary Fund and the World Bank prepared a loan of

4 billion dollars, which may be the first of a series of financial bailouts to oil-producing countries affected by the

decline of oil prices, which have experienced an imbalance in their public finance and entered an exchange rate

crisis following the appreciation of the dollar.

Regarding Angola, the IMF advocates that the priorities should be: making the labour market more flexible;

promoting private investment; improving the business environment, especially reducing bureaucracy, facilitating

the process of incorporation of companies, strengthening the supremacy of the law and improving physical

infrastructures and human capital. The IMF also recommends the continued cutting of fuel subsidies, while at the

same time expanding delineated assistance to the poor.

Recently, Standard & Poor’s downgraded the rating of Angolan sovereign debt from "B+" to "B", but with an

outlook of "stable" evolution. This downward revision of the rating is justified by the decline of the price of oil

and dependence on these exports, leading to the country's increased indebtedness. For this agency, the State's

domestic and external loans, combined with a weak exchange rate, have elevated the weight of public debt,

with it being expected that Angola's gross debt should reach 50% of GDP by this year. Now, the outlook of

"stable" evolution is justified by the forecast of a gradual decrease of the Angolan deficit, thus reducing the risks

of external financing, also taking into account the government's response to the crisis, aimed at preventing the

deterioration of the fiscal and debt situation.

Standard & Poor’s also foresees the need for Angola's gross external financing of approximately 31 billion USD,

this year and the next, of which around half is short term.

EVOLUTION AND FORECAST OF THE PRICE OF THE BARREL OF OIL

Source: EIU/World Bank.

2018201720162009 2010 2011 2012 2013 2014 2015

0

20

40

60

80

100

120

62

80

111 109

96

53

112

37

55

45

2015

22 2015

NOTICES

Notice 08/2014, of 04 December

Establishes the period as of which the "Series 1999" notes and coins shall no longer be in circulation. Pursuant to this

Notice, notes and metal coins of the "Series 1999" shall only remain in circulation, together with notes and metal

coins of the "Series 2012", up to 31 December 2014.

Notice 09/2014, of 05 December

Establishes the rules and principles ruling the advertising of financial products and services marketed by financial

institutions under the supervision of Banco Nacional de Angola.

Notice 10/2014, of 05 December

Regulates the characteristics and requirements of the guarantees which financial institutions receive, as well as the

respective guarantors, in order to be eligible for prudential effects.

Notice 11/2014, of 10 December

Establishes specific requirements for credit operations made by financial institutions authorised by Banco Nacional

de Angola or which, under the terms and conditions stipulated in the Law of Financial Institutions, are under its

supervision.

Notice 12/2014, of 10 December

Regulates the process of constitution of provisions of financial institutions.

Notice 01/2015, of 26 January

Readjusts the regulations on the import, export and re-export of foreign currency by banking financial institutions,

and determines the information that should be provided to Banco Nacional de Angola.

Main alterations:

a) Exempts prior authorisation – Banking institutions are henceforth authorised to import, export and re-export of

foreign currency, as well as travel cheques, without prior authorisation by Banco Nacional de Angola;

b) Duty of disclosure – Banking institutions should inform Banco Nacional de Angola about each foreign currency

import and export operation carried out. The information should be reported through the System of Financial

Institutions (SSIF) by the last day of the week when the operation took place.

Notice 02/2015, of 26 January

Updates the regulations on the limit of exposure to exchange rate risk and gold of financial institutions under

supervision of Banco Nacional de Angola.

Main alterations:

a) Treasury securities indexed to foreign currency are exempt from calculation of foreign exchange exposure.

Notice 03/2015, of 20 April

Establishes the minimum requirements, rules and principles to be observed by financial institutions when advertising

the financial products and services marketed to the public.

Notice 04/2015, of 20 April

Establishes the period as of which the "Series 1999" and "2003" notes and coins shall no longer be in circulation.

Notice 05/2015, of 20 April

Defines the requirements of the cheque forms used in the Payment System of Angola.

REGULATORY CHANGES TO THE FINANCIAL SYSTEM

2015 23

Notice 06/2015, of 20 April

Establishes the rules for identification of Deposit Accounts.

Notice 07/2015, of 20 April

Defines and establishes the dates and requirements for the extinction of the Securities Clearing Service (SCV) and

operationalisation of the Cheque Clearing Subsystem (SCC).

Notice 08/2015, of 20 April

Establishes the conditions of compulsory settlement of inter-bank transfers in the Payment System by Gross in Real

Time (SPTR).

Notice 09/2015, of 20 April

Establishes the execution times for transfers and remittances, as well as the deadline for funds to become available

to the beneficiary, following the deposit of cash and cheques, transfers or remittances.

Notice 10/2015, of 16 June

Establishes the terms and conditions for the inflow and outflow of domestic and foreign currency, held by individuals,

foreign exchange residents or non-foreign exchange residents, whose destination or origin is the Republic of

Namibia, using the land border of Santa Clara (Cunene – Angola) or Oshikango (Namibia).

Notice 11/2015, of 25 December

Regulates the classification of the clearing and settlement subsystems of the Payment System of Angola (SPA), with

a view to the adoption of risk control mechanisms, and stipulates and functioning and operationalisation of these

sub-systems and the responsibilities of the operators.

Notice 12/2015, of 29 December

Monetary Conversion Agreement concluded between Banco Nacional de Angola and the Bank of Namibia. Adopts

a new implementation mechanism and establishes new procedures on the transport of domestic and foreign

currency across the land border of Santa Clara (Angola) and Oshikango (Namibia) and defines the new rules of

the framework of procedures for transactions carried out by financial and banking institutions and foreign exchange

bureaus, under the aforesaid agreement.

INSTRUCTIONS

Instruction 07/2014, of 03 December

Adjusts the rules for calculation and compliance with the required reserves to the current context of macroeconomic

stability.

Main alterations:

a) Increase of the coefficient of required reserves in national currency, from 12.5% to 15%;

b) The requirement in national currency can be deducted by the amount of up to 60% of the assets representing

the value of the credit disbursement granted in domestic current in the sectors of Agriculture, Fisheries and

Production of Food Products, provided that the maturity is more than or equal to 36 months.

Instruction 01/2015, of 26 January

Establishes criteria for classification of countries and identification of multilateral development banks and international

organisations, for prudential effects.

Instruction 02/2015, of 14 January

Establishes the methodologies that can be used to define the minimum amounts of provisions that should be

constituted, in the context of the determinations on the process of constitution of provisions stipulated in Notice

12/2014, of 17 December.

Instruction 04/2015, of 02 March

This instruction adjusts the procedures relative to the holding of sessions to purchase and sell foreign currency

established in Instruction 01/2011, of 12 April, aimed at preserving balance in the foreign exchange market,

instructing additional operating rules relative to the purchase and sale of foreign currency, amending the text

of points 3.1.2, 3.1.5 and 8, adding points 3.1.7, 3.1.8 and 3.1.8.1, defining priorities to the destination of foreign

currency acquired by commercial banks from Banco Nacional de Angola and/or its Clients, namely Transaction of

Goods and Current Invisibles.

24

Instruction 05/2015, of 02 March

Defines the technical specifications of the Standard Cheque, in conformity with article 1 of Notice 05/2012, of 20

April. This "Cheque" is named "Standard Cheque Model 2.1" (two point one).

Instruction 06/2015, of 26 May

Establishes rules for containment of the risk of settlement in the subsystems of the Automatic Clearing Chamber

of Angola (CCAA), considering the negative impact of the impossibility of payments due to insufficient backing

of a participant over the others or users of the Payment Subsystem of Angola (SPS), defining, among others, the

mechanisms for constitution, composition, assessment, operationalisation and default.

Instruction 07/2015, of 25 May

Regulates the terms and conditions under which foreign exchange bureaus can purchase and sell foreign currency.

Instruction 08/2015, of 03 June

Proceeds with the adjustment of the rules for calculation and compliance with the required reserves to the current

context of macroeconomic stability.

This Instruction establishes that the coefficient of reserves applicable to the daily balances of the items comprising

the base of incidence, with the exception of the accounts of the Central Government, Local Government and

Municipal Administrations, is 25% (compared to the previous 20%), where banks may meet up to 10% (compared

to the previous 5%) of the requirement in Treasury Bonds, weighting the respective maturities, provided that they

were issued from January 2015 onwards and belong to the banks' own portfolio.

Instruction 09/2015, of 04 June

Establishes the methodologies that can be used to define the minimum amounts of provisions that should be

constituted, in the context of the determinations on the process of constitution of provisions stipulated in Notice

12/2014, of 17 December.

Instruction 10/2015, of 04 June

With a view to preserving a balance between the operationalisation of the foreign exchange market and the

objectives of exchange rate policy, this instruction establishes requirements, criteria and adjustments to the

procedures of holding of sessions to purchase and sell foreign currency.

Instruction 11/2015, of 18 June

Establishes the operating rules to be observed by banking financial institutions and foreign exchange bureaus,

located along the border zone of Santa Clara, province of Cunene, for foreign exchange transactions involving

Namibian Dollars (NAD) and to monitor the flow of operations carried out under the Monetary Conversion

Agreement concluded between Banco Nacional de Angola and the Bank of Namibia.

Instruction 12/2015, of 24 June

Following Instruction 10/2015, this instruction defines new requirements to be observed by financial institutions

in the process of carrying out foreign exchange operations involving goods, current invisibles, capital and sale to

Foreign Exchange Bureaus.

Instruction 13/2015, of 01 June

Establishes that, under their essential duties, Development Banks may participate in the interbank money market to

assign liquidity, through submission or not of guarantees by the receiving banking institutions.

Instruction 14/2015, of 07 July(1)

Establishes that the effective exchange rate to be applied by Banking Financial Institutions authorised to conduct

the foreign exchange trade, in each sale of foreign currency transaction, intended for the payment of operations

of import of goods, i.e. the effective nominal exchange rate plus all the fees and costs net of taxes, should not

exceed the reference exchange rate for sale published by Banco Nacional de Angola, plus a spread of up to 3%

(three per cent).

In all other foreign exchange operations, including the purchase and sale of foreign notes or travel cheques, the

effective exchange rate to be applied by Banking Financial Institutions authorised to conduct foreign exchange trade,

in each operation of sale of foreign currency, is freely negotiated.

(1) This Instruction was replaced by Instruction 15/2015, of 13 July.

2015

25

The sale of foreign currency by Banking Financial Institutions to foreign exchange bureaus can only involve notes

and travel cheques.

Instruction 15/2015, of 13 July

Suspends the enforcement and consequent applicability of Instruction 14/2015, of 07 July, and re-establishes the

enforcement of Instruction 03/2014, of 04 April, and all the regulations that are not contradictory to it.

Instruction 16/2015, of 22 July

Determines the establishment and maintenance of required reserves in national currency and foreign currency,

pursuant to Instruction 08/2015, of 3 June, which has been revoked, with some amendments concerning the

form of calculation, namely the weekly calculation formula for the arithmetic average of the balances stated in the

respective accounts during business days of the week (numbers 9 and 10) and the contents of numbers 15 and 18.

Instruction 17/2015, of 20 August

Establishes the operating procedures for the holding of auctions for the sale of foreign currency to Foreign

Exchange Bureaus. For example: 1) only foreign exchange bureaus that are authorised by Banco Nacional de

Angola can conduct foreign exchange trade; 2) the sessions are carried out based on the best offer; 3) the sessions

are not attended in person and are operationalised under the terms of number 3 of the present instruction: on

the date and at the time stipulated by the Asset Market department, the foreign exchange bureaus should send

their bids to the electronic address [email protected], indicating: 1) the purchase amount in foreign currency of each bid

and exchange rate; 2) the maximum of three names of banking financial institutions domiciled in the country, for

purposes of settlement of the operation by Banco Nacional de Angola, namely the realisation of the credit of the

foreign currency and debit in national currency; the sum of the bids submitted by each foreign exchange bureau

cannot exceed twice the value of its own funds; the amount of each bid cannot be less than 50,000 USD.

Instruction 18/2015, of 21 August

Establishes the frequency, form and content of the statistical information to be provided to Banco Nacional de

Angola by the issuers and acquirers of payment cards and by the firm operating the Multicaixa subsystem, where

the frequency and period depend on the type of data in question (information of statistical nature should be sent

monthly, up to 10h00 of the day of the month following that to which it refers), highlighting various exceptions

relative, for example, to the context of fraud or attempted fraud or operational problems, whenever it is deemed

that the seriousness of the occurrence requires urgent measures by third parties.

Instruction 20/2015, of 21 August

Establishes rules and procedures inherent to the system for monitoring and treating foreign exchange operations,

aimed at improving the information provided by Banking Financial Institutions, assuring the correct definition and

monitoring of the execution of Banco Nacional de Angola's exchange rate policy.

DIRECTIVES

Directive 02/DRO/DSI/2015, of 10 December

Guidelines on the Prevention of Money Laundering and Combat of Terrorist Financing in Relations with

Correspondent Banks and Client Banks, regulating the conditions of exercise, the duties of disclosure and clarification,

as well as the instruments, mechanisms and formalities necessarily applicable to the effective compliance with the

obligations established in the law.

Directive 03/DRO/DSI/2015, of 23 December

Considering the need to adjust the interest rates for the Permanent Facilities of Assignment and Absorption of

Liquidity, and in conformity with the decision of the fifty-first ordinary meeting of the Monetary Policy Committee

held on 21 December 2015, this directive establishes a 2.5% increase of the Rediscount Interest Rate, shifting it from

12.5% to 15%, which should be reviewed periodically by the Monetary Policy Committee.

Directive 13/DMA/2015, of 28 December

Grants Banking Financial Institutions the prerogative to make liquidity absorption investments at seven days, with the

rate for this maturity being established at 1.75%, and this rate being subject to periodic review by Banco Nacional

de Angola.

2015

26 2015

NET INCOME

The net income of Banco Millennium Angola stood at 6,760 million

kwanzas, in 2015, corresponding to 18% more than the previous year. This

figure was influenced by the positive evolution of net operating income

(in particular net interest income and earnings from financial transactions),

in spite of the growth of operating costs (derived from inflation, exchange

rate devaluation and wage revision) and provisions.

NET OPERATING INCOME

Net operating income increased by approximately 38%, compared to

2014, driven by the performance of net interest income and the earnings

from financial transactions, which recorded growth rates of 28% and

121%, respectively.

2015 2014(Million AOA)

Chan. %

Net interest income 11,320 28%

Net fees 4,300 10%

Earnings from financial transactions

3,365 121%

Other income 56 368 -85%

NET OPERATING INCOME 19,354 38%

Net interest income amounted to 14,446 million kwanzas in 2015. The

growth of this margin was essentially due to the increased average

volume, average rate of loans and average yield of public debt securities,

in spite of the higher average volume of deposits and the higher average

volume and rate of liquidity funding.

Net fees reached 4,724 million kwanzas in 2015, compared to 4,300

million kwanzas in 2014. The increased fees resulted from the favourable

evolution of fees related to credit operations and documentary credit,

notwithstanding the reduction observed in fees related to remittances

and cards.

Earnings from financial transactions amounted to 7,420 million kwanzas,

corresponding to an increase of 121% in relation to the previous

year, where the positive effect of the exchange rate devaluation was

par ticularly influential, despite the reduction of the supply of USD in

the Angolan foreign exchange market.

OPERATING COSTS

Operating costs, which aggregate staff costs, external supplies and services

and the depreciation and amortisation for the year, reached 12,295 million

kwanzas, in 2015 (9,815 million kwanzas in 2014), representing a 25%

increase in comparison to the previous year.

BUSINESS SUMMARY

NET INCOME

Million AOA

2013 2014 2015

4,872

5,741

6,760

NET OPERATING INCOME

Million AOA

2013 2014 2015

17,281

19,354

26,646

2015 27

2015 2014(Million AOA)

Chan. %

Staff costs 4,227 39%

External supplies and services 4,314 8%

Depreciation and amortisation for the year

1,274 40%

OPERATING COSTS 9,815 25%

This evolution was essentially the result of the impact of the exchange rate

devaluation, the effect of inflation, the annual wage update and adjustments

derived from the career progression and increased number of Employees

(to meet the expansion of the commercial network and creation of a new

organic unit of the central services).

The efficiency ratio (cost-to-income) stood at 45.8% in 2015, an improvement

compared to the 50.9% recorded in 2014, due to the operating costs having

grown at a lower rate than that of net operating income.

PROVISIONS

2015 2014(Million AOA)

Chan. %

Provisions for loans 2,524 165%

Other provisions -1 176 -101%

PROVISIONS 2,700 148%

Provisions for loans reached 6,697 million kwanzas in 2015, 165% more than in

the previous year, due to the worsening economic conditions associated to the

context in which the Bank operates.

PROFITABILITY

The return on average equity (ROAE) stood at 17.0% in 2015 (16.1% in 2014).

NET ASSETS

Total assets amounted to 342,914 million kwanzas as at 31 December 2015,

compared to 244,699 million kwanzas as at 31 December 2014, with this

net change corresponding to a 40% increase in the year under review.

FUNDS AND LOANS

Customer funds recorded impressive growth, of approximately 38%

year-on-year, amounting to 249,111 million kwanzas as at 31 December

2015.

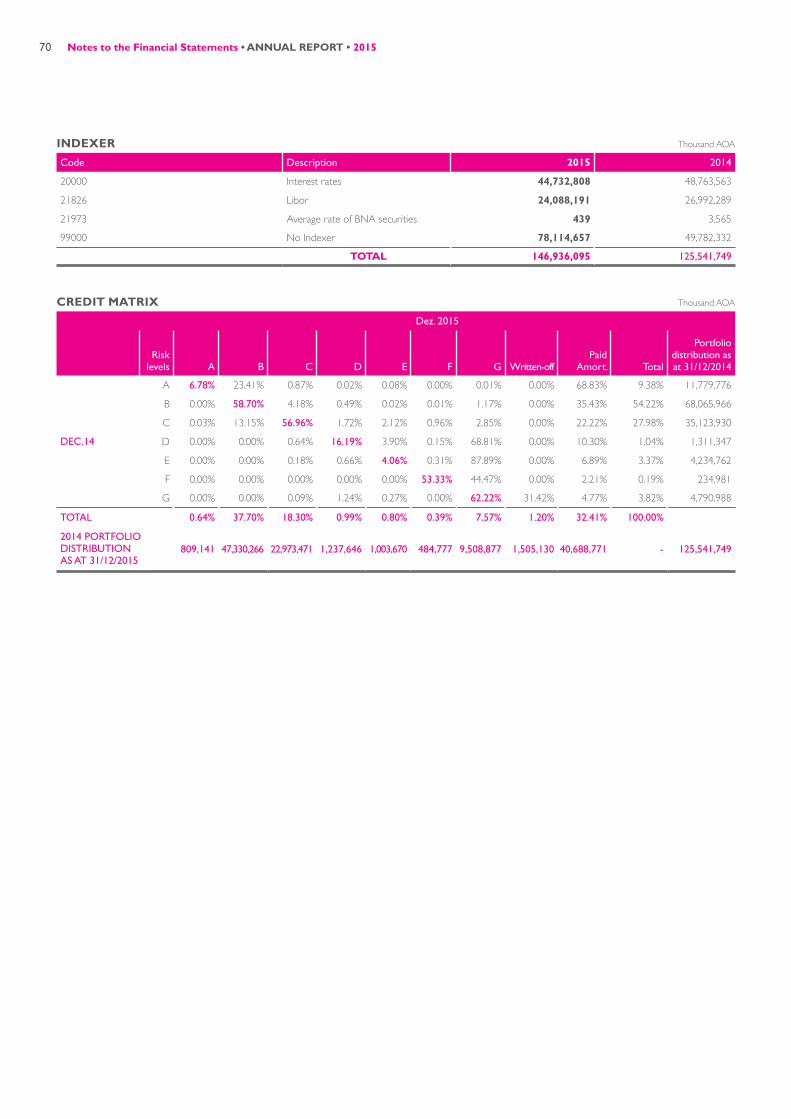

The portfolio of gross loans increased by 17%, to 146,936 million kwanzas.

It should be stressed that BMA maintained its position of leadership in

support to the Angolan productive sector replacing imports through the

Angola Invest Programme (a programme created by the Executive in

partnership with the Commercial Banks).

The loan-to-deposit ratio fell by 11 p.p., from 65% in 2014 to 54% in 2015,

due to stronger growth of funds in relation to loans.

OPERATING COSTS

Million AOA

2013 2014 2015

9,0859,815

12,295

CUSTOMER FUNDS

Million AOA

2013 2014 2015

162,727

180,900

249,111

GROSS LOANS

Million AOA

86,653

125,542

146,936

2013 2014 2015

28

CREDIT QUALITY

The quality of the loan portfolio, assessed by the proportion of loans

overdue by more than 90 days, stood at 3.4% as at 31 December 2015

(3.2% as at 31 December 2014).

The coverage ratio of loans overdue by more than 90 days by provisions

evolved to 267% as at 31 December 2015, compared to 196% as at 31

December 2014.

SOLVENCY

2015 2014(Million AOA)

Chan. %

Risk weighted assets (RWA) 219,547 25%

Qualified own funds 30,217 24%

SOLVENCY RATIO 13.8% -0.1 p.p.

As at 31 December 2015, the solvency ratio corresponded to 13.7% (-0.1

p.p. relative to 31 December 2014), a figure rather above the regulatory

minimum 10%.

DISTRIBUTION NETWORK

In 2015, BMA inaugurated 2 Branches and 1 Prestige Centre. As at 31

December 2015, the Bank had a network of 89 Retail Branches, 54 of which

are open on Saturday morning, 13 Prestige Centres and 8 Business Centres.

CUSTOMERS

As a result of the expansion of the network and the increasingly higher

penetration rate in the market by the oldest Branches, the number of

Customers grew by 12% in relation to the previous year.

REMOTE CHANNELS

As occurred in the previous year, Banco Millennium Angola showed strong

dynamics in the placement of Automatic Payment Terminals (EFTPOS –

electronic funds transfer at point of sale) and cards in 2015.

The total number of EFTPOS grew by 48% compared to the previous year.

The number of active cards stood at approximately 198 thousand by the

end of the year, corresponding to 33% growth over 2015.

A total number of 120 Automatic Teller Machines (ATM) had been installed

by the end of 2015.

MARKETING, COMMUNICATION AND SOCIAL RESPONSIBILITY

In 2015, the expansion of the network included the inauguration of 2

Branches and 1 Prestige Centre, leading to a total of 89 Retail Network

Branches, of which 54 are open on Saturday morning, 13 Prestige Centres

and 8 Business & Corporate Centres, two of which intended for the oil

industry. The number of Customers amounted to 597,263 in December

2015, having grown by 11.8% in relation to the previous year.

BRANCHES, BUSINESS CENTRES

AND PRESTIGE CENTRES

2013 2014 2015

Branches

Business Centres

Prestige Centres

13

8

89

110

12

8

87

76

82

95

107

NUMBER OF CUSTOMERS

2013 2014 2015

437,635

534,101

597,263

2015

29

EFTPOS

2013 2014 2015

1,215

1,938

2,859

ACTIVE CARDS

2013 2014 2015

120,436

148,785

198,186

The Easy Payment service was continued in 2015 for products and

services, with an increasing number of Customers using remote channels

of Millennium Angola, and corresponding reduction in physical visits to

the Branch. This service includes Internet Banking, SMS Banking, App

Millennium AO and the Contact Centre. Follow-up was also given to

the "I am + Millennium" campaign, a Customer loyalty programme which

attribute "Millenniuns" (points worth prizes) to Customers for their

intensive use of the Bank's products and services. The Woman Offer was

also re-launched, which is a series of products and services of exclusive

subscription by women, covering: a specific Woman demand account and

Multicaixa ATM card, a saving plan aimed at family protection, health and

automobile insurance and access to credit, which supports the creation and

development of business by Angolan female entrepreneurs. With respect

to saving, new products were launched with attractive growing rates at 24

months: the Always Rising term Deposit for the Mass Market segment, and

the Growing Rate Deposit for the Prestige segment. The Net Super Deposit

has also been launched, a term deposit at 30, 90, 180 and 360 days, of

exclusive constitution on Millennium Angola's website, with a promotional

differentiating rate (weekly) and subject to limited stock.

Regarding companies, the Bank has maintained its focus on Small and

Medium-Sized Enterprises (SME), through the Excellent SME initiative.

This innovative programme in the market seeks to distinguish, within the

entire group of Customers of Millennium Angola, the Companies which

are outstanding due to their good economic performance, professionalism,

financial solidity, qualified labour and position in the market. In 2015, 575

companies were distinguished in the 2nd Excellent SME Gala, a number

considerably higher than in the previous year (230), confirming the Bank's

affirmation in this segment. As a corollary of this positioning, Millennium

Angola upheld its strong leadership in all the indicators of the Angola Invest

Programme, a programme created by the Executive, in partnership with the

commercial banks, which seeks to boost credit concession to Micro, Small

and Medium-Sized Enterprises (MPME).

Aimed at attracting new talent, the Bank has maintained its participation

in employment fairs (in Luanda and Lisbon) and delivered presentations at

Universidade Agostinho Neto.

The Talent Management and Retention Policy included two new Programmes for Development of Skills –

Millenniuns High Potential, held in collaboration with Universidade Católica de Lisboa, and People Grow

(junior Employees aged below 35 years old with potential and employed for less than two years). A Process of

Certification of Managers of Individual and Company Customers has also been developed in partnership with

the Portuguese Bank Training Institute (IFB). In 2015, a total of 4,017 training hours through personal attendance

were administered and 6,136 training hours via e-learning.

Concerning the attribution of awards, BMA received a new certification of Software Quality based on ISO/IEC

25010, attributed by the prestigious technological institute ISQapave and SQS Portugal, and was distinguished

with the awards of Best Commercial Bank Angola 2015 by Capital Finance International (cfi.co), a highly reputed

British journal specialised in economic and financial affairs, and Best Internet Bank Angola 2015 by Global Banking

& Finance Review.

Recently, the Bank became one of the first members of the Angola Securities and Debt Stock Exchange

(BODIVA), after signing the contract qualifying it to trade securities issued by the State. The agreement allows

Millennium Angola to participate on behalf of its Customers in the Treasury Securities Registration Market

(MRTT), in the Wholesale Trading Market (MTG) and Continuous Trading Market (MTC).

Finally, the Bank has also invested in sponsorships and attendance of events, such as the Offshore World

Championship of Sport Fishing; the Benguela International Fair (FIB); the First Scientific Congress and Third

Symposium of Cardiology and Cardiac Surgery dedicated to the theme "40 Years Health – Conquests and

2015

30

Challenges towards Excellence"; the Angola Observatory – a study which raises a series of questions about how

the phenomenon of social ascension is processed and the models sought by Angolans for their lives and for the

future of their children. In art and music, BMA supported the painting exhibition "The Proverbial Singularity of the

Baobab Tree" by the artist Don Sebas Cassule at the Portuguese Cultural Centre, as well as the tour to Portugal

of the singer Yolanda Semedo (prescriber of the Millennium Angola brand).

Under Social Responsibility, the Bank continued its support to Lar de Nazaré, in Cacuaco, assisting vulnerable children.

HUMAN RESOURCES

In 2015, BMA's Policy on Human Resources continued with its strategy of consolidation, focused on talent

management and strengthening Millennium Culture among our People.

In this context of development which is intended to be sustainable, the assessment of performance, planning of

careers and overall enhancement of skills has acquired new vibrancy, with the implementation of human capital

development projects.

Likewise, and because the motivation, commitment and well-being of all the Employees are fundamental vectors

for success, new plans were also implemented in a structured form for Internal Communication and Internal

Social Responsibility.

Main accomplishments by areas of intervention:

RECRUITMENT AND SELECTION The focus on this activity has been replacement, with priority given to the recruitment and selection of high potential staff. 216 persons have been contracted, representing an increase of 7.2% relative to 2014, thus contributing to enhance the staff, once again, with most incidence in the Commercial Area, with 76% of the recruits.