Embed Size (px)

Citation preview

ANNUAL REPORT 2009

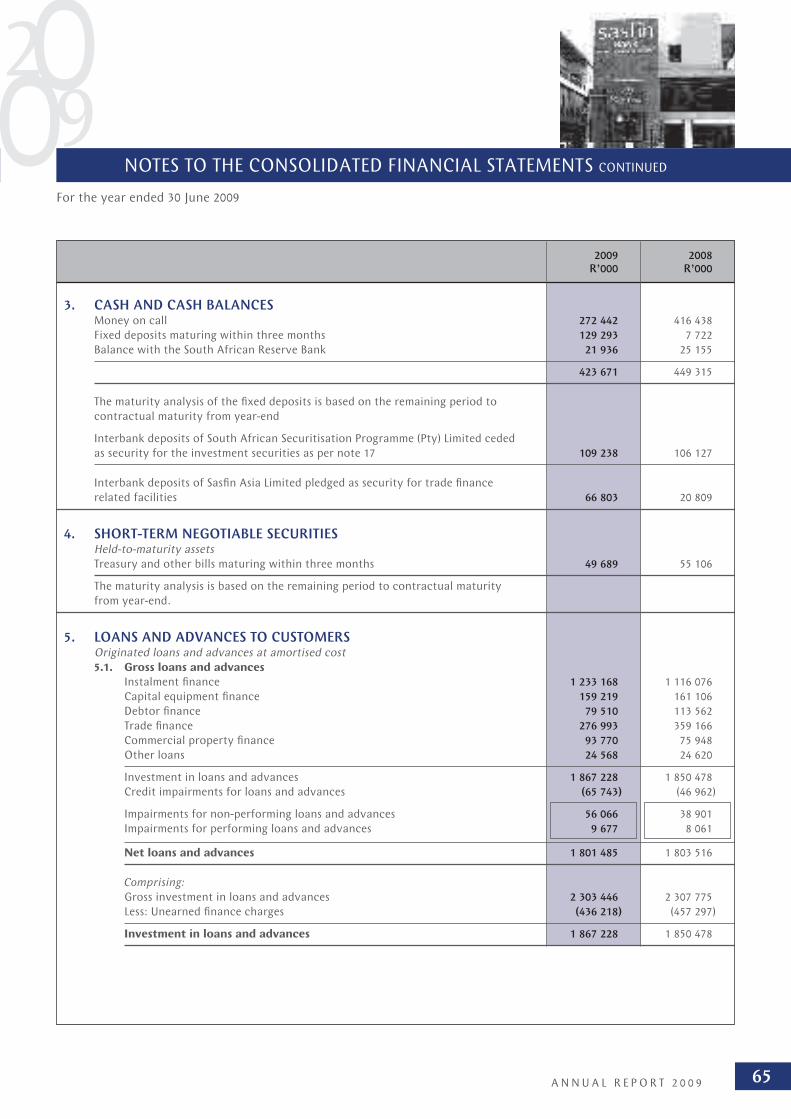

CONTENTS

1

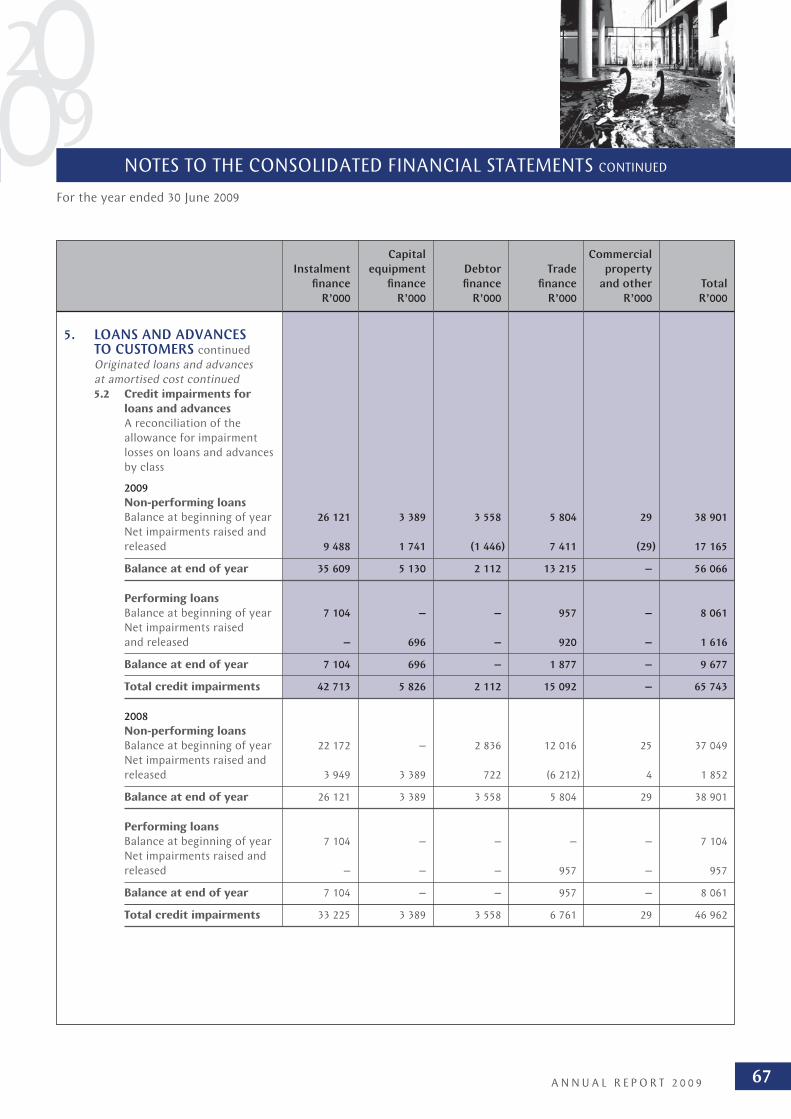

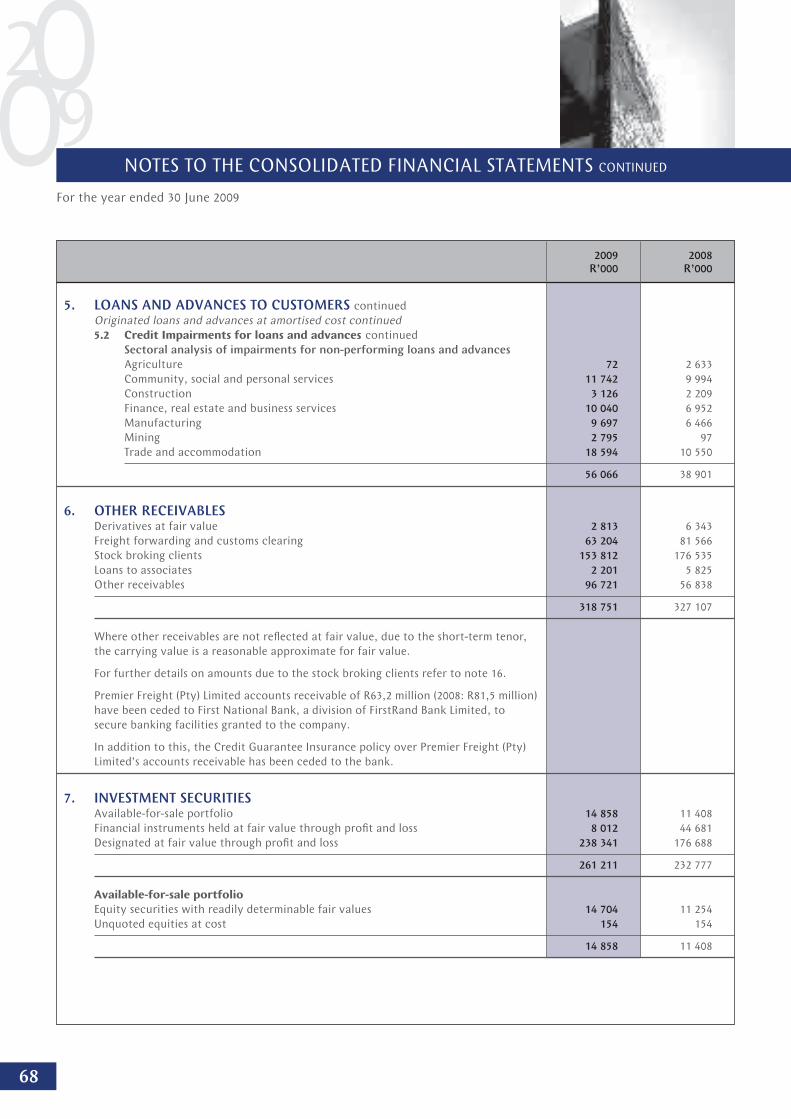

COONNTTEENNTS

1

2 Glossary

3 Sasfi n Group’s Mission, Markets and Values

4 The Sasfi n Group

5 The Board of Directors

6 Executive Committee

7 Business Banking

8 Capital

9 Wealth Management

10 Treasury

11 Logistics and Risk Management

12 Corporate Services

13 Group Salient Features

16 Group Structure

19 Chairman’s Report

23 Chief Executive Offi cer’s Report

28 Risk Management Report

30 Compliance Report

31 Corporate Governance Report

36 Sustainability Report

39 Directors’ Responsibility Statement

39 Company Secretary’s Certifi cate

40 Report of the Independent Auditors

40 Audit Committee Report

41 Directors’ Report

44 Consolidated Statement of Financial Position

45 Consolidated Income Statement

46 Consolidated Statement of Comprehensive Income

47 Statement of Changes in Equity

48 Cash Flow Statements

49 Notes to the Consolidated Financial Statements

110 Company Financial Statements

113 Notes to the Company Financial Statements

120 Shareholder and Administrative Information

122 Notice of Annual General Meeting

Insert Form of Proxy

IBC Sasfi n Group Contact Information

A N N U A L R E P O R T 2 0 0 9

GLOSSARY

ABI Accredited Business Introducer

Basel II Basel II Capital Accord

BEE Black Economic Empowerment

ERM Enterprise Risk Management

FIC Financial Intelligence Centre

FSB Financial Services Board

FSC Financial Sector Charter

HR Human Resources

IFRS International Financial Reporting Standards

InnoVent InnoVent Investment Holdings (Pty) Limited

InnoVent Rentals InnoVent Rental and Asset Management (Pty) Limited

NCA National Credit Act

Premier Premier Freight (Pty) Limited

SAL Sasfi n Asia Limited

SAM Sasfi n Asset Managers (Pty) Limited

SasCred SasCred Financial Services Limited

Sasfi n Sasfi n Holdings Limited

SASP South African Securitisation Programme (Pty) Limited

SasSec Sasfi n Securities (Pty) Limited

SFAS Sasfi n Financial Advisory Services (Pty) Limited

SFS Sasfi n Financial Services (Pty) Limited

SME Small to Medium Enterprises

SREF Sasfi n Real Estate Fund

The Bank Sasfi n Bank Limited

The Company/The Group Sasfi n Holdings Limited

The JSE JSE Limited

The SARB South African Reserve Bank

TOPP Training Outside Public Practice

2

OUR MISSIONTo be the preferred specialist banking and fi nancial services provider

in our chosen markets.

OUR MARKETSEntrepreneurial corporate, commercial and private clients seeking wealth creation,

enhancement and preservation.

OUR VALUESThe Sasfi n Group has identifi ed the following core values as being imperative

to the achievement of its objectives:

satisfy all our stakeholders.

act with integrity, fairness and trust in all matters.

stay transparent and honest while striving for excellence.

focus 100% on our clients’ needs.

instil passion and create a culture of entrepreneurial thinking and innovation.

nurture our personnel and contribute to the development of our country.

3

4 A N N U A L R E P O R T 2 0 0 9

THE SASFIN GROUP

Sasfi n is an independent banking and fi nancial services group,listed on the JSE since 1987.

Having evolved from a family-owned textile company established in 1951, Sasfi n

understands and appreciates what it takes to be a successful entrepreneur and the

perseverance and dedication needed to grow and manage a business. We partner

each and every client with respect and honesty offering tailor-made solutions to

meet business challenges. Each of our fi ve divisions, Business Banking, Capital, Wealth

Management, Treasury and Logistics and Risk Management offer a range of specialised

products and services to assist clients at all stages of their development.

THE BOARD OF DIRECTORS

Seated from left to right: Martin Glatt (Chairman), Dolly Mokgatle,

Roland Sassoon (Chief Executive Offi cer)

Standing from left to right: Eddie Blight, Malcolm Segal (Financial Director),

Norman Axten, Shahied Rylands, Marius Smith

5

6

EXECUTIVE COMMITTEE

Seated from left to right: Malcolm Segal, Louis Dirker, Kurt Diedrick,

Naseema Fakir, Brenton Booth, Dawie Olivier,

Maston Lane, Linda Fröhlich, Enzo Pietropaolo,

Howard Brown, Deon van der Westhuizen,

Nirri Ranchod, Gavin Came, Leonard Eiser,

Roland Sassoon

Standing from left to right: Tyrone Soondarjee, Gary Patterson, Gary Taylor,

DJ Kumbula, Tracey Chinman, Zakhe Khuzwayo

7

BUSINESS BANKING

Business Banking assists entrepreneurs with tailor-made fi nancial and managerial

solutions to assist in business growth. Be it Trade Finance, Debtor Finance, Rental

Finance or Capital Equipment Finance, Sasfi n’s experienced lending arm affords

entrepreneurs the opportunity, insight and expert advice to unlock business

potential by improving access to working capital and assist with cash fl ow challenges.

Seated from left to right: Linda Fröhlich, Nirri Ranchod

Standing from left to right: DJ Kumbula, Deon Kleynhans,

Zakhe Khuzwayo, Brenton Booth

BUSINESS BANKING

8

Sasfi n’s specialised team assists entrepreneurs in optimising their business

potential through opportunities in private equity, property private equity,

corporate fi nance and mergers and acquisitions.

Seated: Malcolm Segal

Standing from left to right: Vernon Leas, Gayle Burbaitzky,

Eton Price, Neil Eppel, Leonard Eiser

CAPITAL

WEALTH MANAGEMENT

With access to leading specialists, Sasfi n is equipped to offer expertise and practical

advice in the creation and enhancement of individual investment portfolios. The

Sasfi n Wealth Management division includes three subsidiary divisions: Sasfi n

Securities, Sasfi n Financial Advisory Services and Sasfi n Asset Managers. Sasfi n Wealth

Management offers a lucrative mix of investment products, advisory services and a

blend of local and international investments. Furthermore, Sasfi n Asset Consulting is

a highly focused, hands-on unit with the capabilities to offer unbiased quantitative

and qualitative assessments on fund assets and liabilities.

From left to right: Gillian Scott, David Shapiro, Dale Franklin,

Gavin Came, Gerhardt van Niekerk 9

10

TREASURY

Treasury offers a comprehensive range of products and services to manage both

personal and company cash investment requirements through products such as

domestic money market portfolios and asset-backed securitisation. In addition,

Sasfi n’s International Treasury provides solutions to all personal or company

foreign exchange requirements.

Seated from left to right: Louis Dirker, Shereen Botha, Anneke van Wyk

Standing from left to right: Lynette van der Westhuizen, Enzo Pietropaolo

11

LOGISTICS AND RISK MANAGEMENT

Logistics and Risk Management provides clients with services not normally considered

within the scope of ordinary banking but which are complementary to their needs.

This division conveniently allows clients full access to a dynamic range of services

from a single supplier. These exclusive services include healthcare consulting, freight

forwarding and clearing and short-term insurance.

From left to right: Steven Romberg, Gary Taylor, Tony Lenhoff

12

CORPORATE SERVICES

R I S K A N D C R E D I T

• Approves and controls credit

• Ensures credit policies are

updated and strictly enforced

• Group risk management

I N F O R M A T I O N T E C H N O L O G Y

• Develops the Group’s

IT strategy

• Enables and facilitates

business through close and

continuous partnerships

• Upgrades and maintains the

Group’s IT infrastructure

M A R K E T I N G

• Strategic communication

• Advertising

• Public relations

• Product launches and

promotional requirements

B U S I N E S S D E V E L O P M E N T

• Accredited Business

Introducer programme

• Customer relationship

management

• Develops new business

channels

FINANCE AND ADMINISTRATION

• Financial and statutory

reporting

• Regulatory reporting

• Group administration and

facilities management

• Group accounting

• Group secretarial

• Group taxation

C O M P L I A N C E

• Group compliance deals with

internal control procedures,

legislation and regulations,

including the Financial Sector

Charter

I N T E R N A L A U D I T

• Carries out the internal audit

functions and provides reasonable

assurance that the Group’s

objectives will be met

H U M A N R E S O U R C E S

• Skills development and

training

• Transformation

• Talent management

13A N N U A L R E P O R T 2 0 0 9

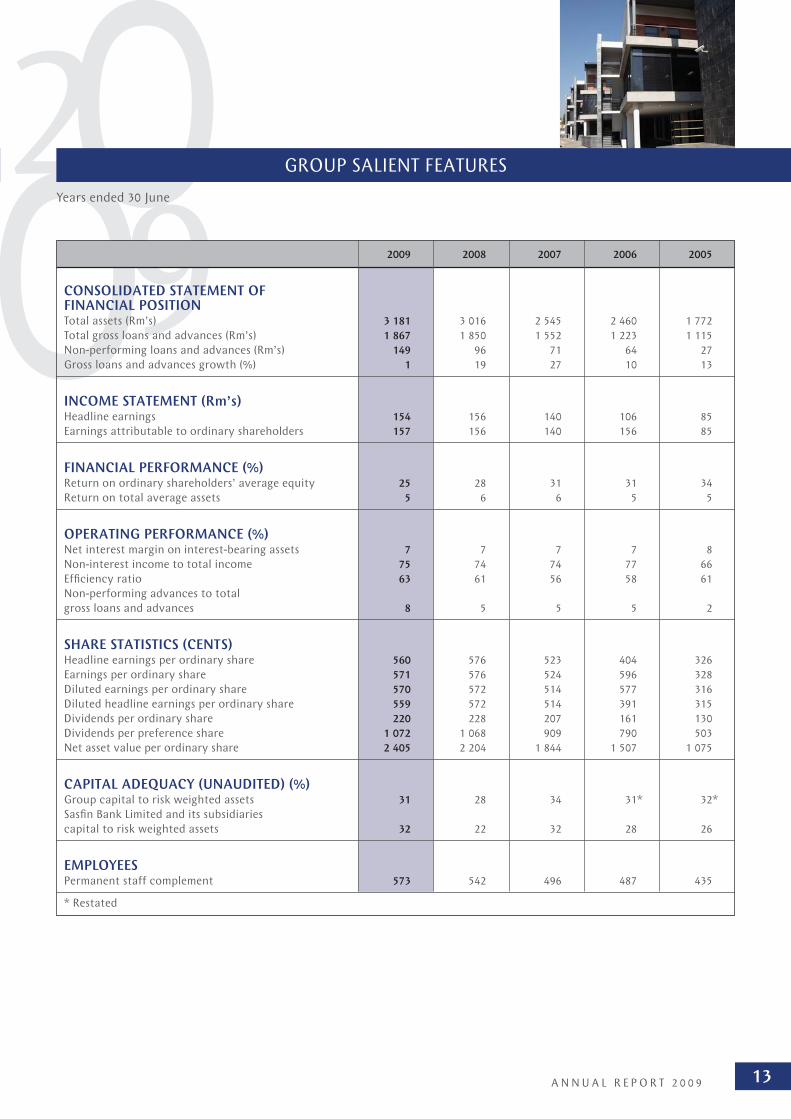

GROUP SALIENT FEATURES

Years ended 30 June

2009 2008 2007 2006 2005

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONTotal assets (Rm’s) 3 181 3 016 2 545 2 460 1 772

Total gross loans and advances (Rm’s) 1 867 1 850 1 552 1 223 1 115

Non-performing loans and advances (Rm’s) 149 96 71 64 27

Gross loans and advances growth (%) 1 19 27 10 13

INCOME STATEMENT (Rm’s)Headline earnings 154 156 140 106 85

Earnings attributable to ordinary shareholders 157 156 140 156 85

FINANCIAL PERFORMANCE (%)Return on ordinary shareholders’ average equity 25 28 31 31 34

Return on total average assets 5 6 6 5 5

OPERATING PERFORMANCE (%)Net interest margin on interest-bearing assets 7 7 7 7 8

Non-interest income to total income 75 74 74 77 66

Effi ciency ratio 63 61 56 58 61

Non-performing advances to total

gross loans and advances 8 5 5 5 2

SHARE STATISTICS (CENTS)Headline earnings per ordinary share 560 576 523 404 326

Earnings per ordinary share 571 576 524 596 328

Diluted earnings per ordinary share 570 572 514 577 316

Diluted headline earnings per ordinary share 559 572 514 391 315

Dividends per ordinary share 220 228 207 161 130

Dividends per preference share 1 072 1 068 909 790 503

Net asset value per ordinary share 2 405 2 204 1 844 1 507 1 075

CAPITAL ADEQUACY (UNAUDITED) (%)Group capital to risk weighted assets 31 28 34 31* 32*

Sasfi n Bank Limited and its subsidiaries

capital to risk weighted assets 32 22 32 28 26

EMPLOYEESPermanent staff complement 573 542 496 487 435

* Restated

14

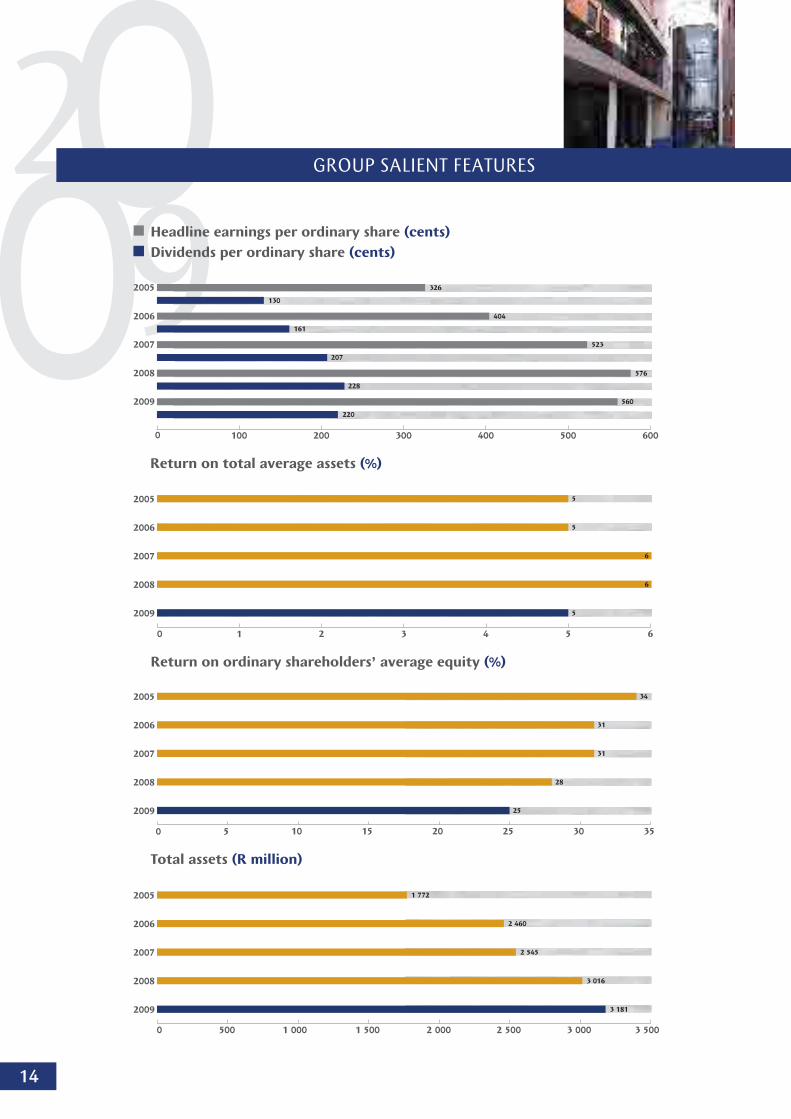

GROUP SALIENT FEATURES

Headline earnings per ordinary share (cents)

Dividends per ordinary share (cents)

100 200 300 400 500 600

2009

2008

2007

2006

2005 326

130

404

161

523

576

228

220

560

207

Return on ordinary shareholders’ average equity (%)

0 5 10 15 20 25 30 35

2009

2008

2007

2006

2005 34

31

31

28

25

2009

2008

2007

2006

2005

Total assets (R million)

1 772

2 460

2 545

3 016

3 181

0 500 1 000 1 500 2 000 2 500 3 000 3 500

0

Return on total average assets (%)

0 1 2 3 4 5 6

2009

2008

2007

2006

2005 5

5

5

6

6

6

15A N N U A L R E P O R T 2 0 0 9

GROUP SALIENT FEATURES

Loans and advances

Gross advances (R million)

Non-performing loans: Advances (%)

Credit impairments: Advances (%)

2005

1 1

15

1 2

23

1 5

52

1 8

50

1 8

67

2006 2007 2008 20090

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

0

1

2

3

4

5

6

7

8

9

2,4

2,3

5,2

2,7

4,6

2,8

5,2

2,5

8,0

3,5

%

R m

illion

2005 2006 2007 2008 2009

Gross advances (R million) 1 115 1 223 1 552 1 850 1 867

Non-performing loans: Advances (%) 2,4 5,2 4,6 5,2 8,0

Credit impairments: Advances (%) 2,3 2,7 2,8 2,5 3,5

Net asset value per ordinary share (cents)

5,4

5,0

0 500

2009

2008

2007

2006

2005 1 075

1 507

1 844

2 204

2 405

1 000 1 500 2 000 2 500 3 000

Group capital adequacy (unaudited) (%)

Bank and its subsidiaries capital adequacy (unaudited) (%)

2005 2006 2007 2008 2009

2632

2831

3234

2228

3231

16

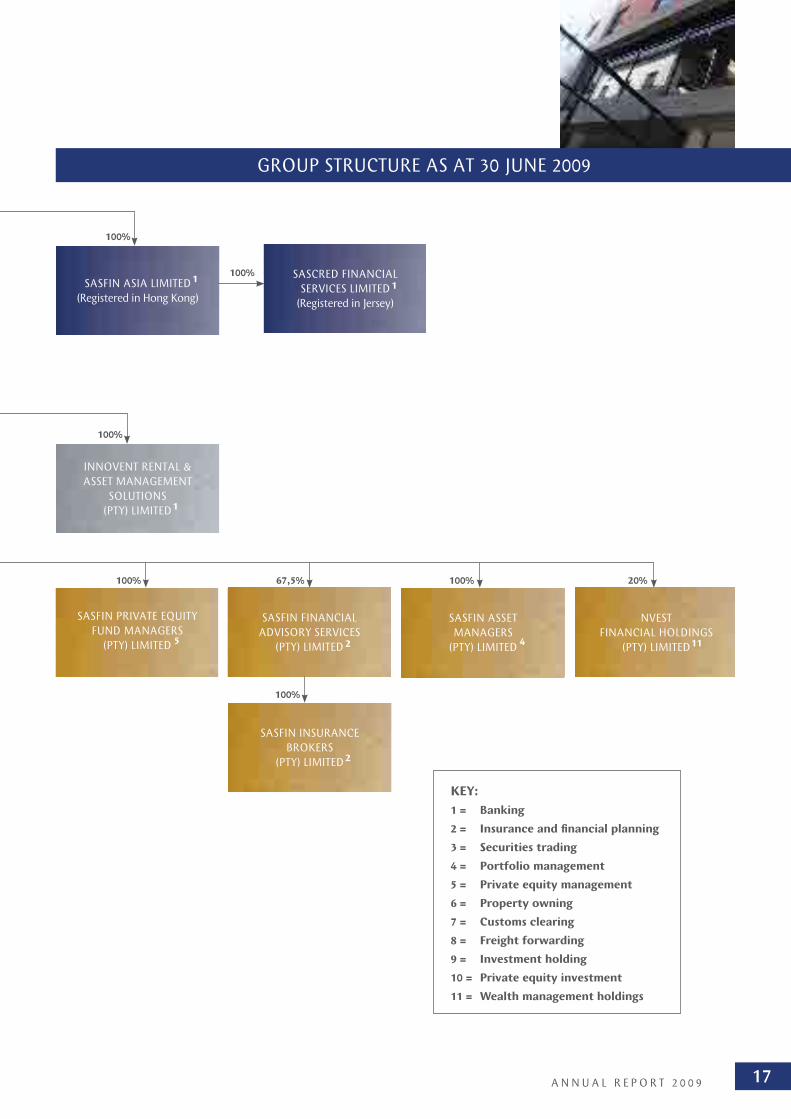

GROUP STRUCTURE AS AT 30 JUNE 2009

SASFIN FINANCIAL SERVICES

(PTY) LIMITED

SASFIN PROPERTIES (PTY) LIMITED,

SASFIN PROPERTIES II (PTY) LIMITED

AND

SASFIN PROPERTIES III (PTY) LIMITED

SASFIN PRIVATE EQUITY

INVESTMENT HOLDINGS

(PTY) LIMITED

SASFIN HOLDINGS

LIMITED

SASFIN BANK LIMITED

SASFIN SECURITIES

(PTY) LIMITED

PREMIER FREIGHT

(PTY) LIMITED

SASFIN - MDM

PRIVATE EQUITY

FUND I

90%

90%

100%

100%

63%

100%

52.4%

1

9

6

10

7

5

3/4

INNOVENT SPV 2

(PTY) LIMITED 9

INNOVENT INVESTMENT

HOLDINGS

(PTY) LIMITED

INNOVENT SPV 1

(PTY) LIMITED

100%

100%

99

SOUTH AFRICAN

SECURITISATION

PROGRAMME (PTY) LIMITED(Residual ownership

held via a trust)

1

33,6%

6%

6%

4%

4%

100%

HECNY

TRANSPORTATION SA

(PTY) LIMITED 8

50%

Sasfi n Holdings

Limited owns

R26m preference

shares in

InnoVent SPV 1

(Pty) Limited

17A N N U A L R E P O R T 2 0 0 9

GROUP STRUCTURE AS AT 30 JUNE 2009

KEY:

1 = Banking

2 = Insurance and fi nancial planning

3 = Securities trading

4 = Portfolio management

5 = Private equity management

6 = Property owning

7 = Customs clearing

8 = Freight forwarding

9 = Investment holding

10 = Private equity investment

11 = Wealth management holdings

SASFIN ASIA LIMITED

(Registered in Hong Kong)

SASCRED FINANCIAL

SERVICES LIMITED

(Registered in Jersey)

SASFIN PRIVATE EQUITY

FUND MANAGERS

(PTY) LIMITED

SASFIN FINANCIAL

ADVISORY SERVICES

(PTY) LIMITED

SASFIN INSURANCE

BROKERS

(PTY) LIMITED

SASFIN ASSET

MANAGERS

(PTY) LIMITED

NVEST

FINANCIAL HOLDINGS

(PTY) LIMITED

100%

100%

100%67,5% 20%

100%

5 2

2

4 11

INNOVENT RENTAL &

ASSET MANAGEMENT

SOLUTIONS

(PTY) LIMITED

100%

1

11

100%

MARTIN GLATT CHAIRMAN

18

19A N N U A L R E P O R T 2 0 0 9

CHAIRMAN’S REPORT

It gives me great pleasure to present Sasfi n’s 2009 Annual Report, the 22nd

since its listing on the JSE in 1987. “

“

RESULTSAgainst the backdrop of the global economic crisis, Sasfi n has

produced satisfactory results for the year under review, with

headline earnings, at R154 million, 2% down on the previous

year, representing an acceptable return of 25% on average

shareholders’ equity.

CAPITAL INJECTIONSAfter protracted negotiations and an extensive due diligence

investigation, the IFC agreed to subscribe for 3,01 million

shares in Sasfi n at R24,81 per share, and to inject a further

R82,45 million into the Bank by way of Tier ll capital. These

agreements are subject to various conditions that are expected

to be fulfi lled by the end of September. The IFC has also provided

a US$10 million guarantee for bank facilities for Sasfi n Asia

Limited. Sasfi n is delighted with its association with the IFC,

which, as part of the World Bank, is very infl uential and has

already added real value to the Company.

CAPITAL ADEQUACYThe Group’s Capital Adequacy Ratio at year end increased

from 28% to 31%, compared with the minimum required

ratio determined in accordance with Basel ll of 9,75%. With

the injection of the Tiers I and ll capital referred to above,

Sasfi n’s Capital Adequacy increases to approximately 36%. This

represents a strong ‘war chest’ for the Company in these times

of interesting opportunities.

LIQUIDITY During November 2008, which coincided with the peak of the

global credit crunch, Sasfi n succeeded in not only rolling its

securitisation notes of R702 million, but in placing an additional

R198 million of notes at attractive rates. This is a show of

confi dence by the debt capital market in the quality of Sasfi n’s

securitised assets, its systems and its vanilla securitisation

structure, which is the oldest such structure in South Africa. This

structure maintained its excellent rating after the credit crunch,

due to the quality and spread of its uncorrelated debtors, and

its high yield, which results in strong embedded value for the

protection of note holders.

Sasfi n’s liquidity, which is based on diverse funding from deposits

(mainly from its private clients), securitisation, interbank

facilities and a strong capital base, has in these volatile times

proved to be robust.

CREDIT LOSSESAs a result of the deterioration in the economic environment,

Sasfi n’s annual credit losses have increased signifi cantly and

now stand at 1% of average loan and advances. Whilst this

compares favourably with most South African banks, the

Company is constantly reviewing its credit granting processes

in an endeavour to maintain an acceptable level of credit losses

going forward.

ECONOMIC ENVIRONMENT For the decade to 2007, the global economy had experienced a

protracted period of benignity, during which there was a major

migration of industry to various under developed economies,

notably China and India. This created huge trade imbalances and

reverse capital fl ows with economies in the western world. Part of

this debt was employed by fi nancial institutions in unsustainable

sub-prime housing loans, credit cards and leverage buy-outs,

using sophisticated fi nancial structures.

As the money supply was tightened in response to increased

infl ation, these loans started to unravel, which in turn decimated

the Tier 1 capital of many of the world’s great fi nancial institutions,

and the resultant credit crunch led to a collapse in the global

economy, the severity of which has not been witnessed in living

memory.

A number of countries in the developed world have resorted

to quantitative monetary stimulation, including bank bailouts,

involving trillions of dollars, the cost of which, in terms of

taxation, infl ation and interest, will be felt for years to come.

Fortunately the main emerging economies are continuing to

grow, albeit at much reduced rates.

Whilst South Africa has also moved into recession, it is

fortunately in relatively good economic shape, with consumer

credit, infl ation and current account and fi scal defi cits expected

to reduce over time. For this we must compliment Government,

20

and in particular, Trevor Manuel, our past Minister of Finance,

Tito Mboweni, the Governor of the Reserve Bank and Errol Kruger,

the Registrar of Banks, who in contrast to their counterparts

in many developed economies, have maintained a disciplined

economy in general and in the banking sector in particular.

However, South Africa’s scourge of unemployment and violent

crime remains endemic, with the labour unions’ recent pyrrhic

victories exacerbating the situation for all South Africans.

As a large exporter of primary products, South Africa has been

badly affected by the sharp fall in commodity prices, which now

appears to be recovering. The fl ight of capital brought about

by the global credit crunch has caused a national liquidity

shortage, which is now starting to ease. However, the recovery

in the global economy remains fragile and another dip cannot

be ruled out.

THE BANKING INDUSTRYThe implosion of some of the world’s most illustrious banks and

fi nancial institutions in the fi nancial services sector is widely

expected to lead to a ‘back-to-basics’ approach. Banks worldwide

are focusing on strong capital ratios, prioritising solvency over

profi tability, cleaning up risky areas on group balance sheets

and installing appropriate buffers that stand up to stress testing.

Increased government intervention is likely to become a way of

life in the fi nancial sector. Regulators have become far more

mindful of the risks banks take and will be tempted to tighten

the screws considerably, particularly for those banks that are

deemed “too-big-to-fail”.

There has been a public outcry at the breaches of trust placed

in many of the world’s leading fi nancial institutions by the

investing public, inter alia for:

• investing client savings in questionable funds, on which

institutions had received generous management and

performance fees, justifi ed by their claims of due diligence

and sanitation, which, in hindsight was clearly lacking, and

• paying extraordinary performance bonuses to senior

executives, which encouraged a cavalier approach to risk

taking.

Swashbuckling fi nancial structuring is a thing of the past.

Banking has reverted to far more conservatism, which is vital for

the health of the entire economic system.

SASFIN’S PROSPECTSThe major banks have come to realise that to appropriately

manage their inherent risks, a management intensive service is

necessary for the small and medium sized commercial market.

For this market to be viable, increased pricing is necessary,

which improves the overall competitive position of Sasfi n’s

Business Banking division. Sasfi n’s Wealth Management division

also benefi ts from the general disillusionment with the larger

fi nancial institutions. The withdrawal from certain specialised

areas by larger banks represents great opportunity for smaller

more personalised fi nanciers, like Sasfi n.

With increased regulation, bank licences are becoming far more

onerous and expensive to maintain. The fl ip side of this is that

a bank licence now represents a huge barrier to entry, which

Sasfi n intends to leverage off more fully in future.

Sasfi n has:

• high capital adequacy and strong liquidity,

• a good reputation,

• a solid base of depositors,

• excellent management, staff and systems

• products that meet the needs of its target market, and

• an excellent client base.

Whilst Sasfi n recognises the need to improve in a number of its

functions, it is well placed to not only continue to weather the

storm, but to achieve strong growth, as and when the economy

turns.

CHAIRMAN’S REPORT CONTINUED

21A N N U A L R E P O R T 2 0 0 9

APPRECIATIONI extend my appreciation to my fellow directors and Sasfi n’s

management and staff, who have excelled themselves in diffi cult

conditions. In particular I would like to thank our executive

directors, Roland Sassoon and Malcolm Segal for their continued

valued contribution. I also thank our professional advisors, and

the SARB for their invaluable guidance, our valued clients for

their support and our shareholders for their faith in Sasfi n. I take

this opportunity of welcoming as the new Governor of the SARB,

Gill Marcus, who is so well qualifi ed to step into the very large

shoes to be left by her esteemed predecessor, Tito Mboweni.

It is my intention to retire as Chairman and director during the

course of the current year. I take this opportunity of thanking

my colleagues for their loyalty and support during the 22 years

of my chairmanship and of expressing my confi dence in their

ability to continue to take the Group to higher levels for the

benefi t of all its stakeholders.

I particularly commend Roland Sassoon on his achievements as

Chief Executive Offi cer during this period and wish him further

success.

Martin Glatt

Chairman

2 September 2009

CHAIRMAN’S REPORT CONTINUED

ROLAND SASSOON CHIEF EXECUTIVE OFFICER

22

23A N N U A L R E P O R T 2 0 0 9

CHIEF EXECUTIVE OFFICER’S REPORT

SASFIN’S TARGET MARKET Entrepreneurs have a pioneering spirit, with a propensity

to sail uncharted waters. This is often accompanied by a

lack of fi nancial sophistication, frustrating their ability to

secure appropriate fi nancial facilities. A proactive and highly

personalised relationship with a banking group that empathises

with their needs and understands their inherent risks is therefore

essential.

Sasfi n not only satisfi es these criteria, but is equipped to service

its growing base of corporate, business and private clients in this

target market, with its:

• entrepreneurial culture, having its origins as a textile merchant,

• dedicated and talented human resources,

• comprehensive range of banking and fi nancial products,

• state-of-the-art information technology,

• considerable fi nancial resources, and

• capable risk and credit management.

RESULTSGiven the sharp economic decline, Sasfi n produced satisfactory

results for the year under review. The Group achieved profi t for

the year of R189 million (2008: R184 million), whilst headline

earnings for the year under review decreased by 2% from

R156 million to R154 million, representing returns on ordinary

shareholders’ average equity of 25% (2008: 28%) and on total

average assets of 5% (2008: 6%).

DEVELOPMENTSDuring the year under review, the Group took the following

signifi cant steps:

• It negotiated, subject to various conditions, for the injection

of US$10 million each of Tier l and Tier ll capital from the

IFC. This follows the US$10 million bank guarantee that was

provided by the IFC last year. Apart from the increase in

capital adequacy and liquidity that this brings, having the

IFC as a partner has strategic signifi cance, in view of the

enormous infl uence in international fi nancial circles that the

IFC, as a member of the World Bank, wields.

• At fi nancial year end Sasfi n moved into its newly developed

premises in Waverley, with excellent modern facilities,

including best of breed infrastructure for banking storage,

security and business continuity. This new facility will enable

the Group to continue to expand strongly.

• Sasfi n has invested considerable human and fi nancial

resources in upgrading its IT systems, which is expected to

result in a signifi cant improvement in effi ciency.

• Sasfi n has refi ned its stress testing models in terms of Basel ll

in respect of capital adequacy as well as liquidity, which are

now continuously applied.

• Subsequent to the departure of the Group Managing Director,

the following signifi cant staff appointments were made:

– Malcolm Segal took on the added role of Group Financial

Director and, together with the Chief Executive Offi cer,

assumed the “four eye” responsibilities in terms of SARB

regulations.

– Maston Lane was promoted to Group Chief Operations

Offi cer

– Gavin Came was promoted to Head of Wealth Management

Division

These developments are all designed to open the way for Sasfi n’s

next expansion phase.

PROSPECTSThe banking industry is feeling the effects of the economic

contraction, in both volumes and credit losses, which are likely

to persist, albeit on a reduced scale, for most of the current

fi nancial year.

As the big banking groups shy away from Sasfi n’s target market

of small to medium sized businesses, Sasfi n expects to attract a

bigger share of this market. However, it should be emphasised

that, although Sasfi n has the capacity for strong growth, it will

remain very conservative in its lending activities during these

diffi cult times.

CAPITAL ADEQUACYOn 30 June 2009, the Group capital adequacy was 31% (2008:

28%), and that of the Bank 32% (2008: 22%), which is well above

the prescribed minimum requirement. With the injection of

capital by the IFC, the Group capital adequacy is expected to

increase to 36%, which will enable continued expansion.

24

OPERATING DIVISIONS:

BUSINESS BANKINGContribution to profi t for the year: 2009: R65,5 million

(2008: R61,4 million).

The Business Banking division houses the lending activities of the

Group.

EQUIPMENT RENTAL FINANCE UNIT

This unit fi nances offi ce automation and allied equipment through

operating rentals. By providing excellent service, this unit has

increased its market share and is benefi ting from improved

margins which have offset the increased costs of funding and

credit losses. This unit is confi dent of continuing to operate at

these enhanced levels.

BUSINESS FINANCE UNIT

This unit houses the Group’s trade, debtor and capital equipment

fi nancing activities. Resulting from the global credit crunch in

late 2008, this unit experienced a contraction in activity and a

rise in credit losses. The void of fi nancing available to SMEs has

opened up opportunities to grow this business at acceptable

margins and the pipeline of new applications for the current

fi nancial year is encouraging.

CAPITAL Contribution to profi t for the year: 2009: R28,1 million

(2008: R43,4 million).

Sasfi n Capital undertakes the Group’s proprietary private equity

and third party fund management activities and also houses the

Corporate Finance unit.

As might be expected in the current economic environment,

results for the year were down by 35% on the prior year.

PRIVATE EQUITY UNIT

Given the economic climate, the Group adopted a conservative

stance to this asset class and the focus of management was on

the performance of the existing portfolio investments as opposed

to originating and executing new investments.

Together with 3rd party funds, the Group has R238 million in

proprietary and managed private equity investments.

The mark to market revaluation surplus of the private equity

portfolios was adversely affected by:

• the general slowdown in economic conditions which

generally impacted on the trading performance of portfolio

companies,

• the downward adjustment of proxy price earnings multiples

of equivalent companies listed on the JSE by reference to

which the portfolios are valued, and

• the softening of the real estate market.

There has recently been evidence of a revival in the demand for

growth and development capital as entrepreneurs start to focus

beyond the immediate diffi cult trading conditions.

CORPORATE FINANCE UNIT

This unit provides merger and acquisition origination and

execution support services as well as the full range of JSE Sponsor

and AltX Designated Advisor services to a sizeable portfolio

of listed companies. It generally focuses on companies with a

market capitalisation of less than R5 billion and also provides

corporate advisory services to the Group.

The unit failed to achieve its budget for the year, mainly as a

result of delays caused by the economic slowdown.

The team has a good blend of youth and experience and is well

positioned in its target market and is thus expected to deliver

improved performance in the year ahead.

TREASURYContribution to profi t for the year: 2009: R60,5 million

(2008: R34,3 million)

This division undertakes the Group’s Domestic and International

treasury services.

DOMESTIC TREASURY

This unit manages the funding of the Group, which is mainly

through equity, including preference shares, securitisation,

deposits and interbank facilities.

Despite the effects of the global credit crisis, Group Treasury not

only refi nanced R702 million of securitisation notes falling due

in November 2008, but also issued an additional R198 million

of notes. This achievement is indicative of the outstanding

performance of the Group’s securitisation vehicle, as well as the

confi dence that the market has in it, which is the oldest active

securitisation vehicle in South Africa, having been incorporated

in 1991.

Whilst deposits declined by 20% during the year under review,

there are clear indications of a rise in deposits in the current

fi nancial year.

In line with developments in the banking industry since the

Global Credit Crunch, margins charged out to divisions on loans

have increased.

Future focus will be to broaden the depositor base by offering a

wider range of products to individuals and SME’s.

INTERNATIONAL TREASURY

The Bank, as an Authorised Foreign Exchange Dealer, provides a

full range of foreign exchange services through this unit.

CHIEF EXECUTIVE OFFICER’S REPORT CONTINUED

25A N N U A L R E P O R T 2 0 0 9

This unit was established to complement the Group’s modular

range of banking products and fi nancial services focused on the

needs of corporate, commercial and individual clients.

In order to facilitate import and export transactions for the

Group’s clients, the Bank offers spot and foreign exchange

contracts and related swaps, as well as Customer Foreign

Currency accounts, and advising of letters of credits anywhere in

the world, while individual clients can avail of the Bank’s ability

to transfer discretionary or foreign investment allowances in all

major currencies across the globe.

This unit went through a period of systems development, having

invested heavily in state of the art Treasury IT systems and is now

poised for solid growth.

WEALTH MANAGEMENTContribution to profi t for the year: 2009: R21,3 million

(2008: R32,9 million).

This division comprises SasSec’s domestic 120 year old stock

broking and portfolio management unit, the newly launched

asset management subsidiary, SAM and the Financial Advisory

and Asset Consulting units.

Apart from offering a full range of independent advisory

services through Sasfi n Financial Planning, SAM and Sasfi n

Asset Consultancy, Sasfi n now offers a range of unit trusts and

multi-managed Retirement Investment Funds, with assets now

comfortably exceeding R5 billion.

STOCK BROKING AND PORTFOLIO MANAGEMENT UNIT

The global credit crunch and consequent market collapse,

initially felt in the latter part of 2008, had an impact on SasSec,

with assets under administration down by 14% to end the year

at R25 billion.

During the year, the East London Branch of SasSec was sold to

a broad-based fi nancial consulting business, NVest Financial

Holdings Limited, in exchange for a 20% interest.

ASSET MANAGEMENT UNIT

The asset-managed products, previously housed elsewhere in this

division, are being transferred to SAM. These include the Sasfi n

Twenty Ten and Sasfi n Equity Funds, the Sasfi n International

Fund and the Group’s Managed Funds, as well as certain bespoke

portfolios managed for third party institutional clients. Two

additional funds, The Sasfi n Wealth Preserver Fund and the Sasfi n

Balanced Fund, were promoted for the fi rst time under the Sasfi n

banner. SAM also houses portfolios constructed specifi cally

for pension and provident fund assets. A focused team is now

dedicated to promote this growing range of retail and wholesale

funds.

FINANCIAL PLANNING UNIT

SFAS has maintained its client-facing focus by continuing to

appoint new planners which now number over 20. This business

grew its top line revenue by about 17% in diffi cult market

conditions. In a new development, planners from this unit are

now physically placed within all the divisions of Sasfi n, allowing

for a deeper focus on the joint promotion of the respective

services of each division. This unit is expected to steadily increase

its support for SAM and SasSec.

ASSET CONSULTING UNIT

Assets under mandate now exceed R4 billion. This unit is

benefi ting from the governance that is emerging from the roll

out of SAM and has in turn commenced placing a proportion of

its funds with SAM.

LOGISTICS AND RISK MANAGEMENTContribution to profi t for the year: 2009: R13,6 million

(2008: R12,4 million).

This division comprises the Group’s Freight Services, Healthcare

Consulting and Short-term Insurance Broking units.

FREIGHT SERVICES UNIT

The restructuring of Premier’s sales and marketing department

has been successfully completed, resulting in good growth

despite the economic slowdown.

Premier produced an excellent result and in fact achieved an

all time record in its 32 year history. Premier traded strongly

in the fi rst six months of its fi nancial year, with a slowdown in

the second six months, but still managed to produce a stellar

performance.

Management continues to focus strongly on cost containment

to ensure that Premier remains profi table during the economic

downturn, whilst being poised to take advantage when the

economy turns.

SHORT-TERM INSURANCE BROKING UNIT

The short-term insurance broking business that was housed in

Sasfi n Insurance Brokers (Pty) Limited is now a division of SFAS.

This operation, which was previously outsourced, is managed in

house and is on target and poised to grow signifi cantly as the

Group’s divisions continue to provide support.

HEALTHCARE CONSULTING UNIT

This unit continued to make a solid contribution especially since

its revenues are only marginally negatively affected by economic

downturns.

CHIEF EXECUTIVE OFFICER’S REPORT CONTINUED

26

CORPORATE SERVICES:

MARKETING AND BUSINESS DEVELOPMENTSasfi n’s marketing department is involved in articulating

the Group’s value offering to its staff, clients, shareholders,

stakeholders and the investment community at large, through

a strategic integrated communications-based programme. A

highlight in the past year’s marketing activities was a full-

scale communications programme for Sasfi n’s move to its new

premises in Johannesburg. The internal programme was aimed

at enthusing staff about the new move to mark a fresh start and

to ensure staff buy-in for a smooth relocation. The external leg

of the programme facilitated the introduction of clients, media

and external stakeholders to the new building and showcasing

its state of the art features.

The Group has strengthened its marketing strategy in line with

its theme of “Growth in Progress”. A new advertising agency

has been appointed to infuse Sasfi n’s corporate advertising

programme with a fresh creative strategy that will reinforce

the Group’s positioning as a growing contender in the fi nancial

services sector.

Sasfi n has also continued with a robust media relations campaign,

maintaining relationships with key journalists by keeping them

informed of major group announcements and newsworthy

activities. The Group continues to follow the strictest protocol

when engaging media, ensuring that information is accurate and

timeous and that media have full access to Sasfi n’s executive

management for direct comment.

Marketing support is also extended to the Group’s various

business units by packaging and promoting new products,

facilitating business development processes and brokering

stakeholder contact.

The marketing department continues to keep abreast of

emerging communication tools and technologies that will hone

the organisation’s ability to engage its internal and external

target audiences effectively.

INFORMATION TECHNOLOGY The past year was one fi lled with excitement and opportunity

in the technology arena. With a move to the new Head Offi ce,

it was opportune to start preparing and streamlining the

infrastructured environment to achieve uninterrupted services

during the move, and improved effi ciencies afterwards. Under

the auspices of the architecture team, the end of July 2009 saw

the IT environment in the Group migrate to the new data centre,

and running at even higher effi ciency and reliability than has

ever been the case.

With the pressures of the contracting economy worldwide

weighing heavily, Sasfi n’s Group IT has also been able to improve

levels of service, whilst spending less in the operations area than

projected. Furthermore, with the improved environment put in

place during the migration process, operating costs are forecast

to reduce in the coming fi nancial year.

FINANCE AND ADMINISTRATION During the year, this department was involved in major upgrades

necessary in terms of the Basel II Capital Accord, including a

working ICAAP model. It is responsible for Group accounting and

reporting, including statutory reporting to the SARB, with whom

it maintains open and constructive communication channels.

It is also responsible for Group administration. It continues to

discharge its responsibilities with integrity and effi ciency.

COMPLIANCEThis independent department, established and operational inter

alia in terms of Section 47 of the Banks Act and Regulation

49 of the Banking Regulations as well as other key regulatory

legislation covering the broader group, including FAIS, the

Securities Services Act and FICA, continues to act as a key

interface with the regulatory authorities and is an essential

component of the Group’s risk management framework. Further

details are provided in the expanded Compliance Report on

page 30.

GROUP INTERNAL AUDITGroup Internal Audit is an independent risk management

function, whose purpose and responsibilities are governed by

standards of the Institute of Internal Auditors. Its independence

is assured through its functional reporting to the Chairman of the

Group Audit and Compliance Committee, who is an independent

non-executive director of Sasfi n. The Head of Group Internal

Audit reports administratively to the Chief Executive Offi cer.

In the year under review, the audit methodology was brought

in line with international best practice, the staff skills capability

was strengthened and a new audit management system was

introduced to ensure consistency of the application of the audit

methodology.

RISK AND CREDIT Sasfi n’s credit and risk policies are well established, with

principles that have been tried and tested over many years within

the Group. Adherence to these policies are monitored by a Credit

Review Committee which meets monthly, and a Risk and Capital

Management Committee which meets quarterly, both of which

report to the Board with recommendations to ensure relevance

in an ever-changing fi nancial and regulatory environment.

Policies include set standards of presentation of credit proposals,

acceptable fi nancial criteria, delegated mandates, security

standards, review frequencies, risk monitoring and recovery of

accounts in default.

CHIEF EXECUTIVE OFFICER’S REPORT CONTINUED

27A N N U A L R E P O R T 2 0 0 9

Given the current tighter economic conditions, clients showing

early signs of fi nancial distress are closely monitored with a

view to taking swift action, by providing the necessary fi nancial

assistance where the risk remains acceptable, failing which, the

most effective exit strategy is planned and executed. Tools such

as asset and fi nancial audits, interim reviews and regular client

visits are used for this purpose.

Credit decisions are made by two or more credit managers

according to a delegated mandate structure, with all new facility

approvals being debated at daily credit meetings, which include

senior executive management.

Where Sasfi n is likely to incur a loss on a specifi c account, an

independent analysis is made of the events and circumstances

that led to this position, in order to gain full value from the

experience and to make any appropriate changes in policy.

HUMAN RESOURCESThe HR department provides comprehensive human resource

management services across the Group and serves as a strategic

partner alongside the various business units and departments,

facilitating employees’ commitment and success through

positive human relationships.

The Group’s transformation objectives are progressing in line

with targets. A mentorship programme has been developed

for talented employees from disadvantaged backgrounds,

in order to retain their talent, and help them achieve greater

levels of success within the organisation. All appointments are

made with due consideration being paid to employment equity

commitments.

Staff development and growth is continually enhanced and

employees are encouraged to pursue further education and

training, ranging from basic adult literacy programmes and

learnerships to post-graduate degrees. Formal learning is

complemented by on-the-job training.

Sasfi n’s study loan scheme enables employees to manage the cost

of higher education. Once more, the Workplace Skills Plans and

Implementation Reports met the requirements of the relevant

authorities, from whom a full rebate of Skills Development Levies

was received.

Performance management initiatives are well received within

the Group, where both management and employees benefi t from

regular feedback and review.

Employee Wellness remains a priority, with on-site consultants

being available to assist employees with their healthcare needs.

HIV training is provided to employees, and annual wellness

days are arranged for staff to avail themselves of free medical

screening.

Among the new initiatives introduced this past year, are the Cell

C Take-a-girl-child-to-work Day, the publication of a quarterly

HR newsletter and an induction video for all new employees.

The HR department remains sensitive to the needs of the Group’s

most important asset: its people, in achieving the Group’s

business objectives and helping them realise their personal

growth and career ambitions.

BLACK ECONOMIC EMPOWERMENTWhilst there is continuing uncertainty about the status of the

FSC, Sasfi n has consistently improved its scorecard and has again

been awarded an “A” rating for BEE by the FSC Council during

the year under review.

In order to maintain the impetus of the broad based BEE

imperative and monitor its compliance in this regard, Sasfi n has

established a Transformation committee.

APPRECIATIONI am grateful to each of Sasfi n’s dedicated and extremely

competent directors, general managers and staff members for

their wonderful service to the Group. In particular, I thank

Malcolm Segal, Maston Lane and Gavin Came for taking on

expanded roles in the Company.

I also thank Sasfi n’s clients for their loyalty and support, and our

professional advisors and the Registrar of Banks and his offi ce,

for their sound guidance.

I would like to pay tribute to Martin Glatt, who after 22 years

as our chairman, will be retiring. It was during the 1987 stock

exchange boom that Martin decided to back Sasfi n for a listing

on the Development Capital Market of its shares at 60 cents a

share. No sooner had the prospectuses been printed, the stock

market collapsed and we were faced with the prospect of an

aborted listing. Fortunately, Martin came to the rescue by taking

up a larger issue of shares. It is that level of commitment that

has characterised Martin’s involvement with the Company, for

which he will be sorely missed.

I look forward in the year ahead to further enhancing the

“win-win” relationships that exist with all Sasfi n’s stakeholders.

Roland Sassoon

Chief Executive Offi cer

2 September 2009

CHIEF EXECUTIVE OFFICER’S REPORT CONTINUED

28

INTRODUCTIONSasfi n’s risk management approach provides effective mechanisms to address the identifi cation, measurement and evaluation of actual and potential risk areas. This, combined with a balanced approach to risk, and keeping in mind our optimum levels of risk appetite, ensures that we retain our entrepreneurial drive and remain able to achieve our core strategic, operational, fi nancial and compliance objectives.

Risks can be described as the possibility that unforeseen future events could occur which could impact on the ability of the Group to achieve its desired objectives.

Failure to manage substantive risk effectively and in a timely manner can have severe consequences on business. Effective risk management therefore remains a key focus of management processes within Sasfi n and our risk management framework addresses such risks as credit, funding, liquidity and interest rate risks, market, business and operational risks which include pricing, market penetration, service levels, the security of our staff, HR risks, assets and information, business disruption, legal documentation or contractual risk, technology risk, settlement, payment and processing risk, reputational risk, fraud risk and compliance with regulatory and statutory requirements risks.

PHILOSOPHYThe business of banking and fi nancial services is conducted within an environment of complex interrelated risks. This has become even more applicable with the advent of the new regulations relating to banks, as amended for the Basel II Capital Accord, which has ushered in a more risk-sensitive approach to banking than any of its predecessors.

At Sasfi n, risk management is regarded as being one of our competitive advantages.

Our risk management programme supports the view that the management of risk is the responsibility of all, and Sasfi n proactively identifi es risk in delivering products and services to the market in an effi cient and cost effective manner. The programme also supports the analysis of problems from various angles, to identify not only the risk mitigation, but also to anticipate and act on potential opportunities – thereby challenging conventional wisdom and creating better solutions.

STRUCTURERisk is managed and monitored in accordance with the risk management framework of the board of directors, board committees, executive and operational management, compliance offi cers and the risk management functions of the operational units.

The risk management framework is designed to ensure:

• the detection and minimisation of signifi cant risks;• the reliability of fi nancial information;• the reliability and integrity of operational processes; and• compliance with statutory and regulatory requirements.

Sasfi n employs three lines of defence. The fi rst line of defence

includes the internal controls management has implemented in

business. The second and third lines of defence are the Group

Risk and Group Internal Audit Departments, respectively.

Sasfi n has also applied an integrated approach to risk

management. Group Internal Audit is able to utilise the risk

assessment performed by Group Risk, in order to risk-rate their

audits. In doing so, the Internal Audit function provides the

board and management with an independent assessment of the

effectiveness of the risk management processes within the Group.

The risk management responsibilities are carried by the following

key committees:

• Boards of directors

• Group executive

• Directors’ Affairs (Corporate Governance)

• Directors’ Strategy and Review

• Asset and Liability

• Risk and Capital Management

• Credit Review

• Group and subsidiaries’ Audit and Compliance

• Information Technology Steering

• Human Resources and Remuneration

• Group Strategy

ENTERPRISE RISK MANAGEMENT (ERM)ERM is a process implemented by an entity’s board of directors,

management and other personnel and is applied in strategy

setting across the enterprise. It is designed to identify potential

events that may affect the entity and to manage risks remaining

within its risk appetite to provide reasonable assurance regarding

the achievement of entity objectives.

Sasfi n’s ERM, which has been rolled out across the organisation,

supports the Basel ll Capital Accord imperatives relative to the

determination and alignment of strategic objectives, capital

requirements and risk management. The requirements of Basel II

have also been incorporated into the Regulations to the Banks

Act 94 of 1990. Sasfi n also subscribes to the COSO Enterprise

Risk Management Framework, which is then integrated with the

requirements of the Basel II Capital Accord and the Regulations

to the Banks Act.

Capital requirements are calculated using a risk-sensitive

approach. The management of capital and capital adequacy is

detailed in note 37 to the Financial Statements.

Sasfi n’s approach to the management of key risk areas is as

follows:

CREDIT RISK

Represents the risk of loss incurred directly by providing credit

or indirectly by assuming a fi nancial obligation or by becoming

exposed to counterparty failure.

RISK MANAGEMENT REPORT

29A N N U A L R E P O R T 2 0 0 9

Credit risk exists in both on- and off-balance sheet exposures and may arise from the non-performance by a borrower, counterparty or an issuer such as a securities fi rm.

Credit risk management processes are governed by the Group’s credit policy guidelines. These guidelines are reviewed regularly and any amendments thereto are subject to the evaluation and approval of the Credit Review committee. Facilities granted to counterparties are governed by internal and prudential limits, which restrict large exposures relative to the Group’s capital.

Credit facilities are approved within the credit mandate structure.

Large facilities are ratifi ed by the Credit Review committee, with facilities above R18 million requiring approval by the Group board of directors.

Counterparty creditworthiness is evaluated in terms of policy guidelines and limits are set before credit is granted.

Risk mitigation includes:

Trade Finance Various types of collateral are obtained to secure the exposure but the primary security is usually Notarial Bonds over movables, and ownership over goods fi nanced.

Debtor Finance Various types of collateral are obtained to secure the exposure but the primary security is usually the receivables purchased.

Equipment Finance The primary security is the asset being fi nanced.

The impairment policy of the Group is conservative and satisfi es regulatory requirements.

LIQUIDITY RISKThe risk arising from the potential inability of the Group to accommodate decreases in liabilities or to fund increases in assets in full, at the right time, place and currency.

This area of risk is closely monitored by the Asset and Liability committee and is managed according to the policies of the committee and in accordance with the following process:

• maintenance of balance sheet liquidity ratios• assessment of depositor concentration in terms of the overall

funding mix• ensuring an adequate portfolio of marketable assets and

short term investments, and• liquidity contingency plans relevant to changing needs.

INTEREST RATE RISKRepresents the risk that fl uctuating interest rates could unfavourably affect the Group’s earnings and the value of its assets, liabilities and/or capital.

This area of risk is closely monitored by the Asset and Liability committee, which approves the policies and limits for the management of interest rate risk and monitors these exposures and the effectiveness of the risk management processes.

Group Treasury’s responsibility is to establish and maintain an interest rate risk management framework and to recommend appropriate risk limits.

MARKET RISKRepresents the risk of loss due to adverse movements in the market, for example, where interest rates rise because of changes in such factors as exchange rates, infl ation and market liquidity. Sasfi n does not enter into Proprietary Trading.

Approach:

• The board of directors grants general authority to undertake market risk. Limits are set for individual business units to contain losses within specifi ed limits in the event of adverse market movements.

• Prospective investments require formal authorisation and have to undergo deal sanctioning. Market risk from investments is managed in accordance with its purpose and strategic benefi t. Periodic reviews and reassessments are undertaken.

• Limited foreign exchange risk arises due to the low value of such transactions. It is Group policy not to have any material uncovered foreign exchange transactions.

OPERATIONAL RISKRepresents the risk of loss resulting from inadequate or failed internal processes, people and systems and/or from external events. Operational risk incorporates legal risk and excludes strategic risk.

Operational risk includes, amongst others, the potential for loss arising from fl aws or malfunctioning in automated systems, business continuity planning, failures in internal fi nancial and administrative controls and non-compliance with Group policies and procedures.

Control mechanisms have been established within the different divisions to manage operational risk. Divisional management apply their specialised knowledge of the markets in which they operate to fi ne-tune their risk control procedures and systems of internal control. Losses arising from Operational risk are tracked on a regular basis.

RISK MANAGEMENT REPORT CONTINUED

30

The Group’s independent compliance function has been established, inter alia, in terms of Section 47 of the Banks Act and Regulation 49 of the Banking Regulations as well as in terms of other key regulatory legislation applicable to the Group as a whole, including FAIS, the Securities Services Act, FICA and the NCA. It thus operates in terms of the overall applicable legislative and regulatory framework. The objective of the function is to ensure that Sasfi n continuously manages its regulatory and supervisory risks and complies with applicable laws, regulations and supervisory requirements. At the strategic level, Sasfi n sees compliance as a tool supporting an effective level of corporate governance within the organisation. Operational policy documents and procedure manuals are regularly reviewed by the compliance department which provides both legal and regulatory support to the Group.

Over the last few years, Sasfi n has been faced with a veritable raft of new regulation and regulatory changes, which has placed considerable additional pressure on banks, and indeed their clients, to ensure that Sasfi n satisfi es the demands of the regulatory environment. Arguably, this increased workload has had a disproportionate impact on smaller banks.

Sasfi n’s compliance function operates independently from the overall risk management function and internal audit function, which have themselves been bolstered to facilitate the additional responsibilities arising from the implementation of Basel ll and the increasingly sophisticated legal environment. This structure supports best practice principles and has strengthened Sasfi n management of Risk, Internal Audit and Compliance.

FICA, in particular, imposes onerous requirements relative to the identifi cation of clients and the reporting of suspicious transactions. As at June 2009, Sasfi n has managed to achieve a compliance level of 99,5%. All remaining accounts have been frozen in accordance with the regulations. During the past year, the Financial Advisory Task Force, an intergovernmental body which sets international anti-money laundering and counter-terrorism policies, conducted its fi ve-yearly country review of South Africa and made a number of recommendations. As a result thereof, substantial changes to FICA are anticipated, which ought to enhance the effectiveness of the anti-money laundering process.

The Compliance division also oversees and monitors the process of transformation within Sasfi n. This process is guided by the provisions of the FSC. The FSC came into being in January 2004, following a Nedlac Financial Sector Summit. The FSC was more recently gazetted as a sector code in terms of section 12 of the Broad Based Black Economic Empowerment Act but as a result of the inability of all stakeholders to agree on the alignment process with the generic codes, has not yet been ratifi ed in terms of section 9 of the Act. This process has been dogged by disagreements between the various stakeholders which have not as yet been resolved. This, however, does not detract from the key objectives of the Charter which commit the fi nancial sector to “actively promoting a transformed, vibrant and globally

competitive fi nancial sector that refl ects the demographics

of South Africa, and contributes to the establishment of an

equitable society by effectively providing accessible fi nancial

services to black people and by directing investment into

targeted sectors of the economy.”

Sasfi n has submitted its report to the FSC Council in the year

under review and is pleased to have retained its “A” rating

with an improved score of 89,36%. It has substantially met the

targets in respect of the key pillars of ownership and control,

procurement, access to fi nancial services, corporate social

investment and enterprise development.

The ongoing expansion of the number of services and products

offered by Sasfi n do increase the burden of compliance, as these

products are almost always subjected to regulation. In particular,

the expansion of Sasfi n’s foreign exchange department and the

increased number and complexity of wealth management related

products pose a continual challenge to the compliance division.

Sasfi n is registered as an authorised credit provider in terms of

the NCA. Whilst the regulatory framework surrounding the NCA

is indeed onerous, it is to be noted that the NCA is primarily

aimed at the protection of the individual consumer, who is not

part of Sasfi n’s target market. Unlike the retail banks, Sasfi n has

not experienced any adverse impact on the demand for credit

placed upon it as a result of the NCA. Likewise the recently

enacted Consumer Protection Bill although likely to create an

additional compliance burden, is not expected to materially

impact on Sasfi n’s target market.

The new Companies Act constitutes a comprehensive overhaul of

the Company Law legislative framework. Sasfi n is actively taking

steps to adjust to the new corporate environment which will

be created once the Act comes into operation. The compliance

division continues to monitor the legislative environment

and ensures that line management complies with all laws and

regulations as part of their normal operational duties.

GENERALIn terms of Regulation 39 of the Banks Act, the Bank’s board

of directors is required to report to the Registrar of Banks on

the effectiveness of the system of internal controls relating to

fi nancial and regulatory reporting and their compliance with the

Banks Act and Regulations.

To the best of their knowledge, the relevant boards of directors

are of the opinion that there are no indications of any material

breakdown in the functioning of these controls, procedures and

systems, during the period under review.

While the cost of compliance is increasing in parallel with

the escalating regulatory load, Sasfi n believes that a rigorous

compliance regime is essential to the future well being and

strategic development of the Group.

COMPLIANCE REPORT

31A N N U A L R E P O R T 2 0 0 9

Sasfi n prides itself on being a good corporate citizen, recognising

that effective corporate governance practices are essential to

achieving and maintaining trust and confi dence in both the

organisation and the banking system as a whole. Sasfi n actively

manages its corporate governance through the relationships

between management, the boards of directors, shareholders and

other stakeholders. To this end, Sasfi n endorses the principles

incorporated in the Code of Corporate Practices and Conduct as

set out in the King II Report which forms the basis upon which the

Group’s commitment to sound corporate governance is pursued.

Sasfi n also endorses the FSC in order to raise the skills and fully

incorporate the enormous talent of the previously disadvantaged

members of the South African society. The various committees

of the boards of directors are charged with monitoring and

evaluating conformity with the provisions of these requirements,

as well as the International Financial Reporting Standards, the JSE

Listings Requirements, the Banks Act and all the other statutes

and regulations to which the Group is bound to ensure integrity,

accountability, transparency and equal opportunity in the

conduct of the Group’s various business enterprises.

REGULATORY ENVIRONMENTGiven the important fi nancial intermediation role of banks

in a sophisticated economy, their high degree of sensitivity

to potential diffi culties arising from ineffective corporate

governance and the need to safeguard depositors’ funds,

corporate governance for banking organisations is of

great importance to both local and international fi nancial

systems and merits targeted supervisory guidance. This is

particularly so in the wake of the international liquidity crisis

which vividly exposed the effects of poor governance in other

jurisdictions.

The SARB, through its Bank Supervision Department, carries

the responsibility for ensuring that a sound and well-regulated

banking system exists in South Africa and that prudent risk

management practices are embedded within the banking

environment. The directors of a bank are required in terms of

the Banks Act to report annually to the Registrar of Banks on

the effi cacy of the systems of internal control and to provide

reasonable assurance as to the integrity and reliability of the

fi nancial statements, as well as on Corporate Governance.

Additionally, the directors are required to safeguard, verify and

maintain accountability for the Bank’s assets.

• Sasfi n is committed to adherence to and application of high

standards of corporate governance. The senior management

and boards of directors of Sasfi n take their responsibilities to

ensuring effective corporate governance seriously.

• Sasfi n, from time to time reviews its corporate governance

to ensure compliance with accepted corporate-governance

principles.

• Sasfi n is mindful that it operates on the basis of continuous

improvement, especially given the ever evolving governance

standards in South Africa and internationally.

Sasfi n has a compliance programme, which is under the control

of a General Manager who reports to the Chief Executive Offi cer

and who has unrestricted access to the Chairman of the Audit

and Compliance committee. The JSE regulates the activities of

SasSec. Sasfi n Bank and SFAS also fall under the regulatory arm

of the Financial Services Board. The Compliance department

allocates full time resources to both SasSec and SFAS who ensure

that appropriate standards are maintained.

The directors bear responsibility for setting and maintaining the

Group’s systems of internal controls and protecting its assets

and earnings against material fi nancial loss. They are committed

to discharging these responsibilities as cost-effectively as

possible. Business risks are assessed on an ongoing basis and

risk management procedures are modifi ed and implemented

as needed. The Group has a comprehensive reporting system,

which is monitored and reviewed monthly by management and

the directors. The system facilitates budgetary control, provides

reasonable assurance as to the accuracy of fi nancial statements

and safeguards the Group’s assets.

THE KING II CODE OF CORPORATE PRACTICES AND CONDUCTThe boards of directors of companies in the Group are committed

to maintaining the standards of integrity and openness detailed

in the Code of Corporate Practices and Conduct recommended in

the King Report on Corporate Governance. Sasfi n adheres both

to the specifi ed provisions of the King Code and to its underlying

principles of fairness, transparency, accountability, social

responsibility and environmental consciousness. The Group is

committed to meeting the exacting governance standards which

are anticipated in the King III report.

THE BOARDS OF DIRECTORSThe responsibilities of the Group’s boards of directors include

reviewing and guiding corporate strategy, risk propensity,

budgets and business plans. These boards meet regularly to

monitor executive management and thereby retain full and

effective control over their operations. The Chairpersons of

the Company, the Bank and its main subsidiaries, are all non-

executive directors. These boards include non-executive directors

of suffi cient calibre, experience and number for their views

to carry signifi cant weight in business decisions. The various

boards are responsible for setting policy, monitoring corporate

performance and overseeing major capital expenditure. Where

necessary, independent professional advice is canvassed. The

company secretary ensures that statutory and other procedures

are followed.

CORPORATE GOVERNANCE REPORT

32

SASFIN HOLDINGS LIMITED AND SASFIN BANK LIMITED BOARD CHARTERThe boards subscribe to good corporate governance and strive to

be effective in lending and controlling the companies. As a bank-

controlling company or bank, the boards recognise that they are

bound by the Banks Act and as such, consist of both executive

and non-executive directors (including independent directors)

to the extent appropriate in terms of that Act. The concept of

a unitary board, consisting of executive directors, with their

intimate knowledge of the business, and non-executive directors

who can bring a broader view to the Company’s activities,

particularly those who have intimate knowledge of banking

and fi nancial service industries, remains the favoured board

structure. Management of business risk and the exercise of

commercial judgement are the essence of this mutual association

and exchange of business experience and knowledge. The boards

accept they have a collective responsibility to provide effective

corporate governance that involves a set of relationships

between management, the boards, shareowners and other

relevant stakeholders, in a manner whereby the boards:

• determine the entity’s purpose and values,

• determine the strategies to achieve the entity’s purpose (that

is, its strategic intent and objectives as a business enterprise)

and to implement its values (that is, its organisational

behaviour and norms to achieve its purpose) in order to

ensure that it survives and thrives,

• exercise leadership, enterprise, integrity and judgement in

directing the entity so as to achieve its continuing prosperity,

• ensure that procedures and practices are in place that

protect the entity’s assets and reputation,

• monitor and evaluate the implementation of strategies,

policies, management performance criteria and business

plans,

• ensure compliance with all relevant laws, regulations and

codes of best business practice,

• ensure that technology and systems used are adequate to

run the business properly and for it to compete through the

effi cient use of its assets, processes and human resources,

• identify key risk areas and key performance indicators

in order to generate economic profi t, so as to enhance

shareowner value in the long term and recognise the wider

interests of society,

• regularly assess performance and effectiveness as a whole,

and that of individual directors, including the Chief Executive

Offi cer, and

• ensure that the entity has developed a succession plan for its

exe cutive directors and senior management.

The boards strive to focus on performance in directing the

commercial and economic fortunes of the entity, and not only

concentrate on issues of conformance. The boards recognise

that enterprise is the disposition to engage in undertakings of

risk and are constituted in a manner that provides a balance

between enterprise and control. All directors recognise that

absolute integrity is necessary to meet their onerous obligations

and responsibilities.

The boards comprise a balance of executive and non-executive

directors, with a majority of non-executive directors, of whom

suffi cient are independent of management for minority interests

to be protected, and conform to the “four-eyes” principle as

required by the South African Reserve Bank. The boards also take

cognisance of gender and racial mix.

The boards are selected from individuals of integrity from a broad

range of backgrounds, who can bring a blend of knowledge,

skills, objectivity, experience and commitment to the board

under the fi rm and objective leadership of a chairperson, who

is an independent non-executive director, and who accept the

responsibilities and duties that the post entails and who provides

the direction necessary for effective boards. Non-executive

directors are appointed for a three-year period and are not

automatically re-appointed.

The boards strive to exercise objective judgement on the

corporate affairs of the business enterprise, independent from

management and insist on suffi cient management information

to enable a proper and objective assessment to be made by

the directors collectively. The boards guide and set the pace

of the entity’s operations and future developments. In so

doing, the boards regularly review and evaluate the present

and future strengths, weaknesses and opportunities of, and

threats to the entity. Comparisons with competitors, locally and

internationally, and best practice are major ingredients in this

process – especially in the era of the global economy and the

rapid transmission of information electronically.

The boards recognise that transactions between the entity and

its managers, directors or large or dominant shareowners are

rife with potential confl icts of interest. The personal interests of

directors or persons closely associated with the director do not

take precedence over those of the entity and its shareowners. All

directors avoid confl icts of interest, even where these can only

be perceived to exist. Full and timely disclosure of any confl ict,

or potential confl ict, is made known to the board. Where

an actual or potential confl ict does arise, on declaring their

interest, a director may participate in the debate and/or vote

on the matter, but must give careful consideration to his/her

integrity in such circumstances and the potential consequences

it may have for the board, the entity and themselves personally,

but in any major issue are expected to recuse themselves.

Any director with a substantial interest in the entity, such as

a major shareowner, is expected to recognise the potential

for a confl ict of interest and accept that his/her primary