Embed Size (px)

Citation preview

The bank for a changing world

BNP PARIBAS LUXEMBOURG 2 0 0 4

ANNUAL REPORT 2004BNP PARIBAS LUXEMBOURG

Contents pages

2

3

4

5

6

12

14

15

48

B N P P A R I B A S L U X E M B O U R G

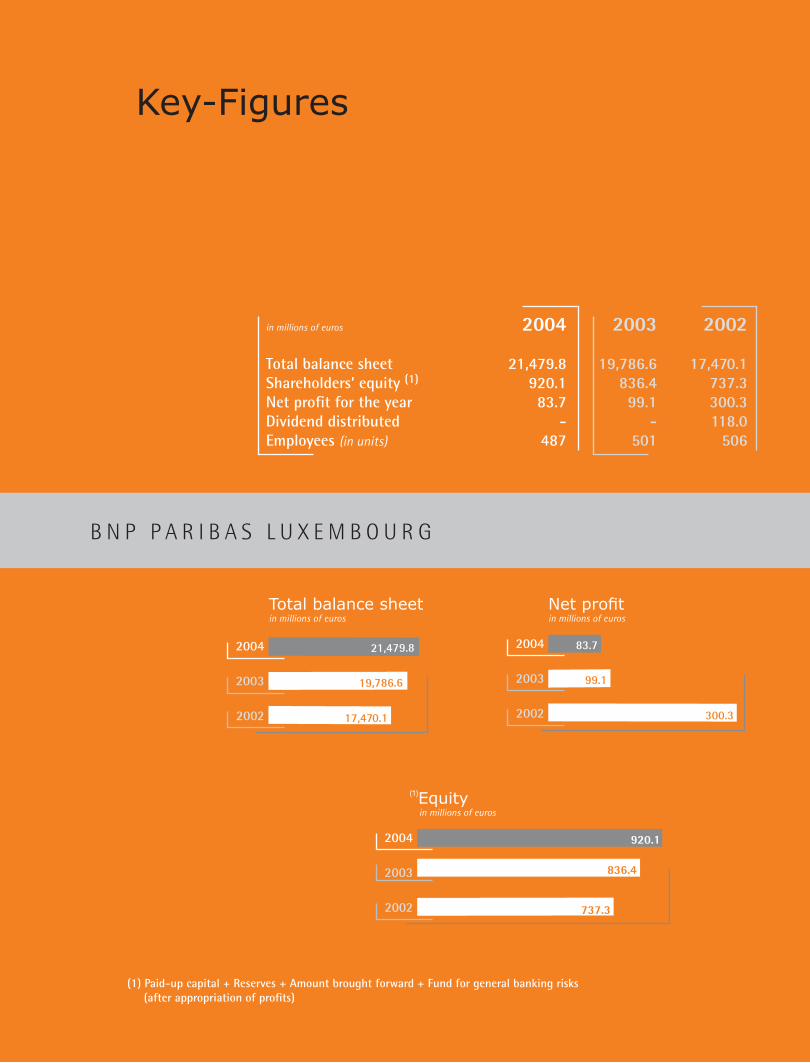

Key-Figures 2002 – 2004

Chairman’s Statement

Board of Directors

Management

Management Report from the Board of Directors to the Ordinary General Meeting of April 6, 2005

Balance Sheet as at December 31, 2004

Profit and Loss Accountas at December 31, 2004

Notes to the Annual Accountsas at December 31, 2004

Auditor’s Report

in millions of euros 2004 2003 2002 Total balance sheet 21,479.8 19,786.6 17,470.1Shareholders’ equity (1) 920.1 836.4 737.3Net profit for the year 83.7 99.1 300.3Dividend distributed - - 118.0Employees (in units) 487 501 506

(1) Paid-up capital + Reserves + Amount brought forward + Fund for general banking risks (after appropriation of profits)

B N P P A R I B A S L U X E M B O U R G

Key-Figures

Total balance sheetin millions of euros

17,470.1

19,786.6

21,479.82004

2003

2002

Net profitin millions of euros

99.1

300.3

83.72004

2003

2002

(1)Equity in millions of euros

836.4

737.3

920.12004

2003

2002

Despite a year marked by major geopolitical tensions and considerable volatility in the price of energy, raw materials and currencies, there was a general strengthening of the world economy, which grew by 5 percent in 2004.

Nonetheless a number of geopolitical or structural imbalances persisted, whether it concerned the difference between a vigorous growth in the US and Asia and a very slow recovery in Europe, or the continuing high budget deficits in most industrialised countries.

In this economic environment, which forced the American Federal Reserve to change its monetary policy by carrying out five successive increases in its intervention rate, the stock markets certainly performed less brilliantly then in 2003. Nevertheless, fuelled by good corporate results, the major indices registered increases : 3.1% for the Dow Jones, 7.6% for the Nikkei, 7.3% for the DAX, 6.9% for the FTSE and 7.4% for the CAC40.

The LuxX, the Luxembourg Stock Exchange index, performed particularly well, with an increase of 26.8%.

On the occasion of its 75th anniversary, the Luxembourg Stock Exchange once again demonstrated its vitality with an exceptional year for the official listings of various types of instruments : debt instruments, undertakings for collective investments, warrants...

The number of instruments quoted, increasing by 13.5% to 33,022 securities, and the volume of trades on the secondary market, progressing by 50.7%, demonstrate the dynamism of the Financial Centre of Luxembourg.

For its part, BNP Paribas Luxembourg has continued its policy of business development which has allowed each one of its business activities to produce good operating results, although the decrease in the net earnings of the Bank, which were affected by the changes in participating interests, do not reflect these results :

• Despite an adverse environment, linked to the impact of the falling dollar on a part of the income and a repatriation of capital out of Luxembourg, the Private Bank has realised results comparable to those of the previous year.

• Largely as a result of the early close-out of non-recurring transactions, market activities have recorded a particularly favourable year.

• Finally, a sustained effort within the Corporate Client domain has led to an increase in market share in this area.

Given the constant evolution of the fiscal and regulatory environment in Europe, the BNP Paribas Group will rely on its creativity, its capacity for financial engineering, its commercial dynamism and its rigorous operational procedures, in the hope of improving the quality of its service, year after year, to the satisfaction of its clients.

This is the aim of the entire staff of BNP Paribas Luxembourg for 2005.

Chairman’s Statement

Vivien Lévy-Garboua

AN

NU

AL

RE

PO

RT

20

04

P A G E S 2 3

Board of Directors

ChairmanVivien LEVY-GARBOUA

Member of the BNP Paribas Executive Committee, Head of Compliance and Internal Control Coordinatoruntil March 4, 2005

DirectorsMarc ASSAChief Executive Officer and Chairman of the Management Board of Tarkett

Alain BAILLYChief Executive Officer, Managing Director of BNP Paribas Luxembourg until December 31, 2004

Philippe BORDENAVEMember of the BNP Paribas Executive Committee,Chief Financial Officer

François DEBIESSEChief Executive Officer of BNP Paribas Private Banking

Dominique HOENNSenior Advisor of BNP Paribas

Edmond ISRAELHonorary Chairman of Clearstream International SA

Vivien LEVY-GARBOUAMember of the BNP Paribas Executive Committee, Head of Compliance and Internal Control Coordinator

Board SecretaryDaniel POSTAL

Alain PAPIASSE

Member of the BNP Paribas Executive Committee, Head of AMS (Asset Management and Services)from March 4, 2005

Jacques LOESCHAvocat à la Cour

Jacques-Philippe MARSONChief Executive Officer of BNP Paribas Securities Services

Eric MARTINChief Executive Officer, Managing Director of BNP Paribas Luxembourgfrom January 1, 2005

Alain PAPIASSEMember of the BNP Paribas Executive Committee, Head of AMS (Asset Management and Services)from February 23, 2005

Jacques POOSCompanies’ Director

Roger SIETZENCompanies’ Director

François TESCHManaging Director of Le Foyer Finance

Gilles de VAUGRIGNEUSEChairman of BNP Paribas Asset Management

Management

General ManagementManaging Director

Alain BAILLY until December 31, 2004

Eric MARTIN from January 1, 2005

Deputy General Manager

Patrice CROCHET

Business LinesALM Treasury

Dominique GOULEM

Private Bank

Patrice CROCHET

Coverage and Territories Europe

Pierre BONIN

Cortal Consors*

Fabrice FLET until January 31, 2005

Stéphane HONIG from February 1, 2005

Fixed Income

Dominique GOULEM

FunctionsLegal Department

Daniel POSTAL

Internal Audit

Jean-François VITTE

External Communication

Liliane PEIFFER

Ethics and Compliance

Anne KAYSER-NEUSS

Finance, Central Organization

Yvan JUCHEM

Risk Management

Dominique MOREL

Operations and Information Technology

Philippe STERNO

Organization

Fabrice CUCCHI

Human Resources

Jean-Claude BAROTTE

AN

NU

AL

RE

PO

RT

20

04

B N P P A R I B A S L U X E M B O U R G

* Cortal Consors, based in Luxembourg since 1993, joined BNP Paribas Luxembourg as a department from January 1, 2005.

P A G E S 4 5

Management Report of the Board of Directors

to the Ordinary General Meeting of April 6, 2005

For BNP Paribas Luxembourg, the year 2004 marked the launching of a major business offensive, which impacted on all the activities of the Bank.

In 2004 the Bank continued to reinforce the security of its data processing and the efficiency of its operating systems through a number of projects supervised by the General Management of the BNP Paribas Group.

We have moreover carried out, within the allocated time limit, the adaptation of our information systems to the new International Financial Reporting Standards (IFRS), which are applicable to the consolidated accounts of our parent company from 2005.

Finally, this year we successfully concluded the merger of the Bank with Cortal Consors Luxembourg, another subsidiary of the BNP Paribas Group, which specialises in brokerage and online investment. The goal of this merger, completed on January 1, 2005, is to develop synergies between these two entities.

Balance sheet and results

As at December 31, 2004 total assets amounted to 21,479.8 million euros compared with 19,786.6 million euros at the 2003 year-end, an increase that can be attributed essentially to a growth in interbank operations.

Own funds (capital, reserves, profit brought forward and fund for general banking risks) after appropriation of profit for the 2004 financial

year, as proposed in this report for approval by the Meeting, will amount to 920.1 million euros compared with 836.4 million euros as at December 31, 2003.

Net profit for the year was 83.7 million euros compared with 99.1 million euros in 2003. This difference, compared with the 2003 financial year, is largely attributable to a decrease in income from participating interests.

Against a backdrop of contrasting economic and financial data, the decrease in net banking income of 35.9 million euros, or 22% compared with the previous year, is principally due to a decrease of 35.3 euros in dividends from participating interests. The interest margin decreased by 9.5 million euros, while the commissions margin increased by 11.4 million euros. Earnings from financial operations decreased moderately by 2.5 million euros compared with 2003.

Other operating income increased by 14.7 million, mainly as a result of a rise in capital gains in 2004 of 17.7 million euros, made on the sale of participating interests.

General administrative expenses are 2.9 million euros or 5% higher, compared with 2003.

With regard to provisioning and value re-adjustments, the Bank has reduced its net charges by 4.2 million euros in comparison with 2003.

The Capital Adequacy Directive ratio (CAD) decreased from 21.4% at year-end 2003 to

the unfavourable conditions, related to the institution of tax amnesties in certain neighbouring countries, private banking acti-vities realised steady growth in 2004.

We have strengthened our global reach by becoming the agent for Investlife, the life insurance subsidiary of the BNP Paribas Group in Luxembourg. We can thus offer our clients additional solutions to problems relating to estate planning or wealth management.

ALM Treasury has achieved excellent results in 2004 thanks to the early liquidation of a certain number of long-term positions. After a slight exchange-related downturn, funding continued to grow in volume as well as in market share.

Fixed Income has continued to expand its range of quality exchange products for institutional customers, banks and corporations in accordance with its forward-looking three-year plan.

The activity of Coverage and Territories Europe (CTE) in Luxembourg was well-placed throughout 2004. Having been designated, along with nine other European countries, as a strategic territory for the development of BNP Paribas Group’s Corporate activity, the Luxembourg Corporate team has worked hard both to win over new clients and also to increase market share with existing clients. The CTE team has also made a substantial effort in promoting the Financial Centre of Luxembourg by underlining the advantages it offers to large corporations.

17.2% as at December 31, 2004. This decline, compared with year-end 2003, is attributed to an increase in balance sheet items as at December 31, 2004, which was partially offset by an increase in eligible capital.

Appropriation of profit

Taking into account the profit brought forward from 2004 of 453 million euros and net profit for 2004 of 83.7 million euros, the total amount for allocation is 536.7 million euros.

We propose that this be allocated as follows :

in euros

Legal reserve 56,000Other reserves * 8,628,387Profit brought forward 528,048,590

Total 536,732,977

(*) of which 6,831,301 euros net to reserve for reduction of tax on net worth and 1,797,086 euros to the free reserves

In accordance with Article 70 of the Law of June 17, 1992, we confirm that no major events have occurred since the end of the financial year 2004 with the exception of the merger-takeover by the Bank of Cortal Consors Luxembourg of which we already held 40%. In payment for the net assets brought by the shareholder Cortal Consors France, the Bank issued 12,000 new shares.

Activities/Business lines

Private Banking finished the year with results comparable to those of 2003. Leaving aside

AN

NU

AL

RE

PO

RT

20

04

P A G E S 6 7

Strategy in using financial instruments

The Bank’s activities with regard to financial instruments mainly concern hedging operations.

The main treasury instruments include fixed or floating-rate loans, repurchase agreements and income transferable securities.

With a view to minimising the interest rate risk inherent in the different balance sheet items, the Bank basically uses interest rate swaps and currency swaps.

Transactions for trading purposes involving interest rate instruments are conducted solely in income transferable securities and interest rate swaps.

The Bank does not take foreign exchange positions for trading purposes.

The Bank’s risk management objectives and strategies

The Bank’s risk management policy is firmly enshrined in the risk policy framework set out by the BNP Paribas Group.

Consequently, the Bank has a dedicated risk department of its own, drawn from the Group Risk Management department of the BNP Paribas Group. This department operates according to the following principles :

• It supervises all risk-taking, the primary responsibility in terms of risk being with the business lines.

• In order to increase its independence, the department manager works directly for the global function and reports to the Managing Director.

• Among the different types of potential risk, this department is in charge of credit, counterparty and market risks.

In practice, the activities of the Risk Management department can be characterised by two main levels of responsibility :

- a decision-making role in co-operation with the individual departments,

- a responsibility for control, raising the alarm and reporting.

Credit and counterparty risk

In terms of credit and counterparty risk, the Bank applies the General Credit Policy of the BNP Paribas Group. As well as defining decision-making procedures with regard to the approval of credit, this policy also sets out the rules governing sector-based and country risks.

Acceptance of a credit risk or counterparty risk linked to a borrower or group of borrowers takes practical effect in the form of an authorisation, subject to the prior agreement of an independent representative of the Group’s Risk Management department.

Market risks

Market risk is the potential loss from an interest rate or foreign exchange position in the event of an unfavourable development in the market parameters (interest rate, exchange rate).

The Bank’s interest rate risk is measured by using an internal model developed by the BNP Paribas Group. This enables cash shortage and surplus to be measured and analysed by currency, parameter (short-term funds, speculative portfolio, long-term positions) and by maturity. The interest rate position per currency and per parameter is controlled by means of limits expressed as a one-year equivalent.

The Bank’s foreign exchange risk, expressed in nominal value, is measured by totalling up the absolute values of open positions in each currency, converted into euros. This foreign exchange position is subject to both an intraday and an overnight limit. The principle of hedging foreign exchange risk prevails with regard to all instruments and all portfolios.

Interest rate positions of a speculative nature and the foreign exchange position are subject to a VaR (Value at Risk) calculation using an internal model developed by the BNP Paribas Group. The VaR measures the potential variation in current value of the portfolio for a given time horizon (10 days) and a given probability level (99%), assuming normal market conditions.

The authorisations are created and updated using the Bank’s various IT tools, and come under the responsibility of the Risk Management department, which must also ensure in advance that the conditions set out in the credit agreement have been met. Adherence to these conditions is monitored initially by the departments as part of their day-to-day work, and then by the Risk Management department at a second level.

The authorisations are subject to periodic review, at least once a year, which involves analysing the ability of the borrowers to meet their obligations and adapting the Bank’s position accordingly. In particular, the Bank’s risk exposure to its different counterparties can be reduced by means of guarantees or compensation agreements.

The above principles are also applied to credit risk emanating from derivatives. The level of risk is calculated either on a lump-sum basis or on a “marked to market plus add-on” basis, taking into account the type of instrument and its maturity date. These lump-sum amounts are expressed as a percentage of the nominal or notional value of the transaction. The “marked to market plus add-on“ approach corresponds to the valuation of the instrument at its market value, which is then increased by a percentage of the notional amount.

AN

NU

AL

RE

PO

RT

20

04

P A G E S 8 9

Each of the limits described above is subject to daily monitoring by the Risk Management department which, furthermore, conducts a monthly calculation of the Bank’s exposure to interest rate risk in exotic currencies on the basis of worst-case scenarios. These scenarios simulate the effects of a monetary crisis, lasting two months, on the Bank’s short-term positions in exotic currencies.

Finally, the Bank has set up an Asset and Liability COmmittee (ALCO) whose task is to examine the following aspects on a quarterly basis : liquidity positions ; adherence to credit limits imposed on the trading room ; the Bank’s liquidity policy ; the worst-case scenarios used to test the Bank’s exposure to interest rate risk in exotic currencies ; balance sheet structure and the investment of capital and reserves.

Liquidity risks

Liquidity risk can be defined as the risk of finding oneself in a position in which it is impossible to relinquish an approved credit (asset) or to find a resource (liability) whilst at the same time being forced to incur a major loss. It can in particular take the form of an increase in financing costs on the interbank market, making it impossible for the bank concerned to meet its obligations to customers or counterparties. It is a question of determining the Bank’s dependence on last-minute financing in the major currencies in the event of a liquidity crisis.

The risk is subject to a limit known as the “overnight guideline” and is subject to daily checks by the Risk Management department.

In terms of the liquidity requirements under the regulations in force in Luxembourg, the Bank has always greatly exceeded the minimum requirement of 30%. This ratio is monitored on a monthly basis by the Finance function together with the ALM Treasury Business Line.

As at December 31, 2004 the liquidity ratio was 91.6% (December 31, 2003 : 84.4%). The average monthly liquidity ratio in 2004 was 91.2% (monthly average in 2003 : 89.5%)

Operational risk

In accordance with the Advanced Measurement Approach (AMA) chosen by the BNP Paribas Group, BNP Paribas Luxembourg has continued the implementation of its operational risk management systems. In this context, the year 2004 was marked in a number of aspects.

The consolidation of the first stage of the approach, namely the setting up of the historical database of incidents (IMS) : the basic parameter has been adapted to take into account more precisely incidents relating to Ethics and Compliance, and Legal and Data Processing matters. These changes reinforce the transparency of the Bank’s operational risks.

With respect to the second stage, namely the implementation of the new operational risk

Eric Martin, took over his responsibilities as Managing Director, Chief Executive Officer on January 1, 2005.

Outlook

In 2005 the accent will continue to be on business development relying on a stronger operation, notably as a result of our merger with Cortal Consors Luxembourg and the subsequent cross selling opportunities.

The Bank has fixed a goal for itself of making the new directive on savings, which will be applicable from July 1, 2005, an opportunity to enlarge our product offerings with innovative formulas, by calling on the expertise of our professionals.

In 2005 we will continue to develop our processing channels in order to offer an even better quality of service to our customers and to improve the efficiency of our operations.

management policy defined by the Group at the end of 2003 : this year the key processes have been identified and documented. More-over, in order to support the implementation of this policy, management systems have been developed and progressively put into operation. Upon completion, they will form the basis of an internal model for the evaluation of operational risks and will be reviewed by the competent surveillance authorities at the end of 2006.

In parallel, the inclusion of an operational risk analysis of current processes (the organisation and structure of budget management) has been put in place.

Finally, in accordance with the guidelines of Basel II and the standards of the Group, the management structure for operational risk has been strengthened. Thus an Operational Risk analyst has been named and an Operational Risk Committee has been set up.

Human resources

As at December 31, 2004 the Bank employed 487 people compared with 501 as at Decem-ber 31, 2003.

The Board of Directors would like to thank the Management and the entire workforce for their continued support in 2004 and especially to thank Alain Bailly who has been assigned to other duties within our Group. His successor,

AN

NU

AL

RE

PO

RT

20

04

P A G E S 10 11

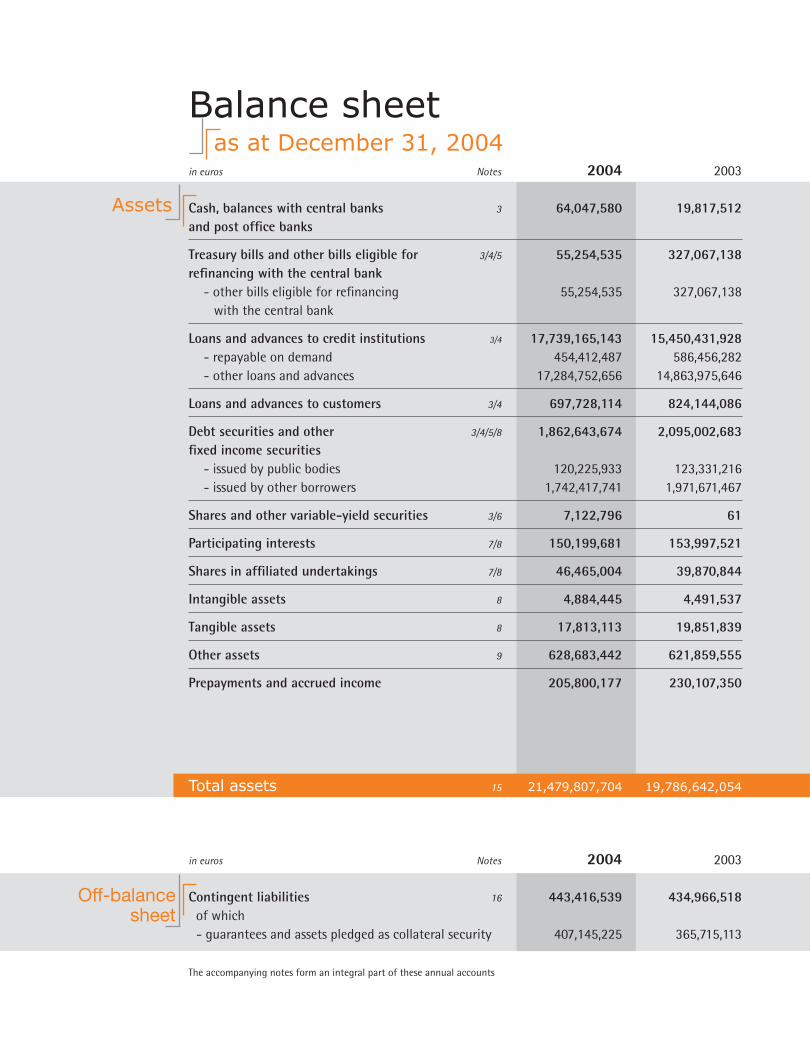

in euros Notes 2004 2003 Cash, balances with central banks 3 64,047,580 19,817,512and post office banks

Treasury bills and other bills eligible for 3/4/5 55,254,535 327,067,138refinancing with the central bank - other bills eligible for refinancing 55,254,535 327,067,138 with the central bank

Loans and advances to credit institutions 3/4 17,739,165,143 15,450,431,928 - repayable on demand 454,412,487 586,456,282 - other loans and advances 17,284,752,656 14,863,975,646

Loans and advances to customers 3/4 697,728,114 824,144,086

Debt securities and other 3/4/5/8 1,862,643,674 2,095,002,683fixed income securities - issued by public bodies 120,225,933 123,331,216 - issued by other borrowers 1,742,417,741 1,971,671,467

Shares and other variable-yield securities 3/6 7,122,796 61

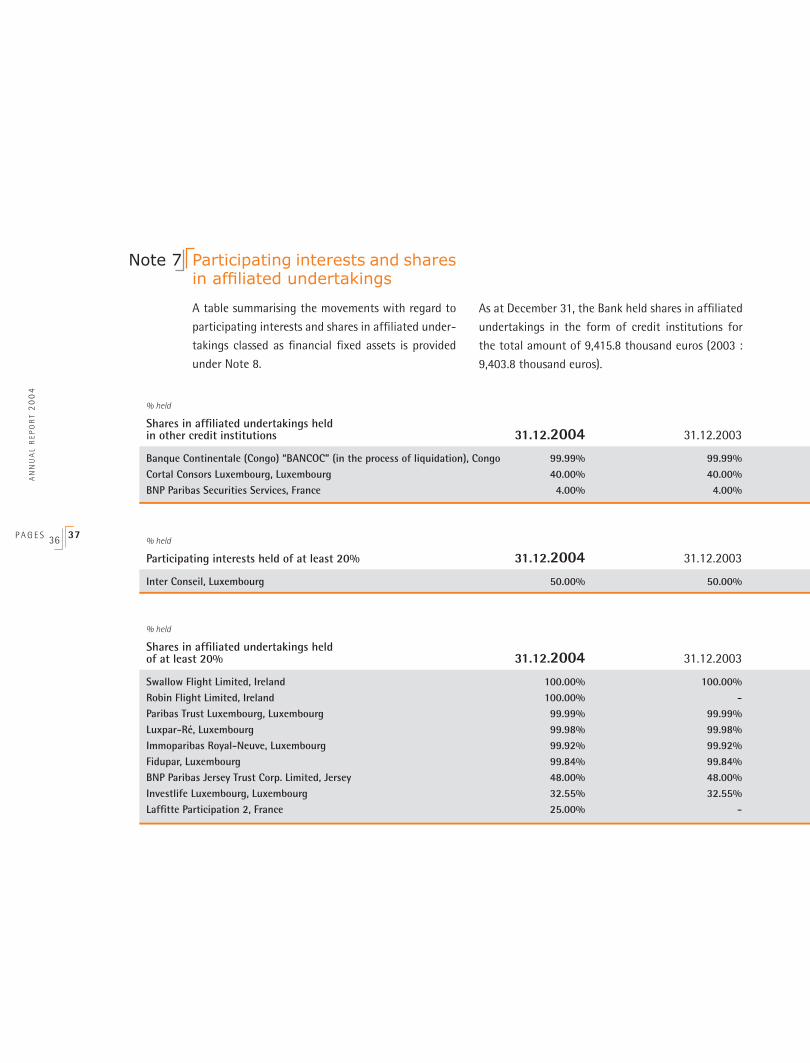

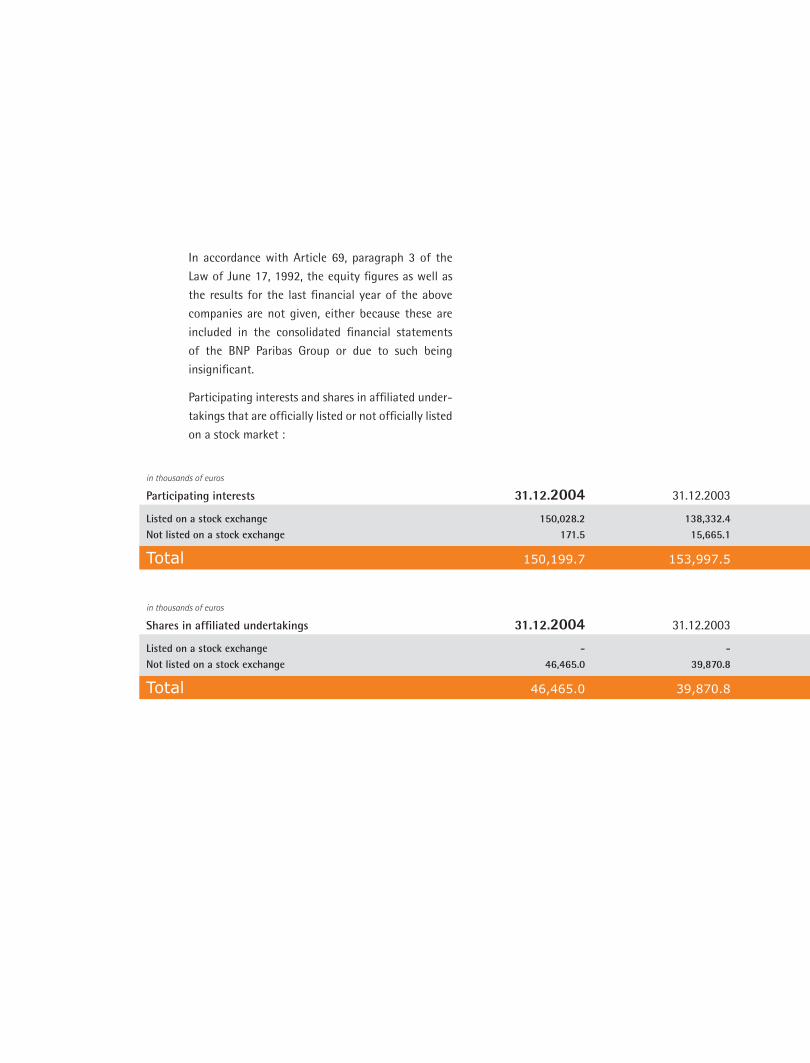

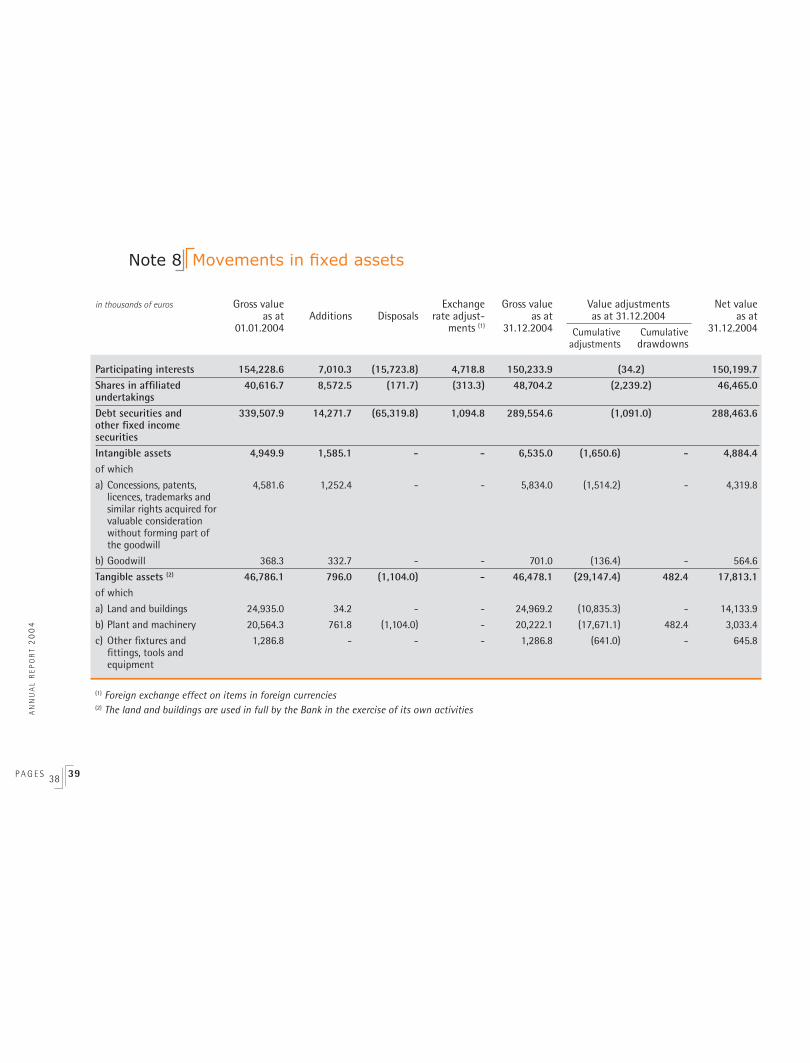

Participating interests 7/8 150,199,681 153,997,521

Shares in affiliated undertakings 7/8 46,465,004 39,870,844

Intangible assets 8 4,884,445 4,491,537

Tangible assets 8 17,813,113 19,851,839

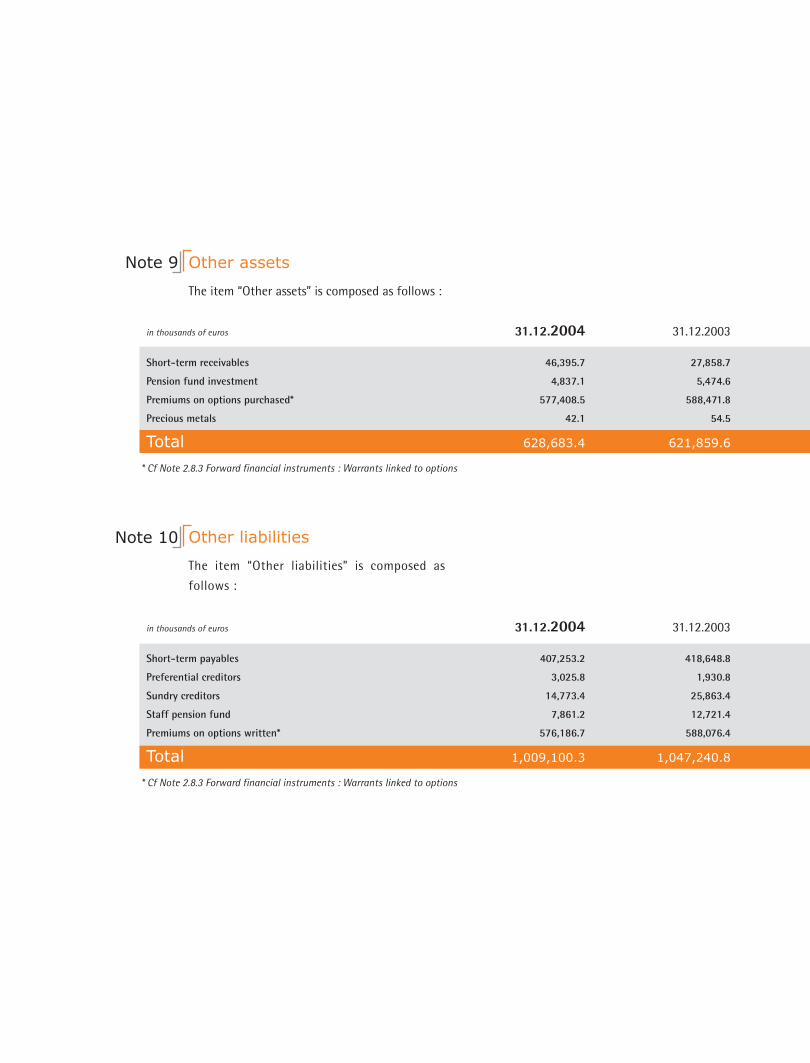

Other assets 9 628,683,442 621,859,555

Prepayments and accrued income 205,800,177 230,107,350

Total assets 15 21,479,807,704 19,786,642,054

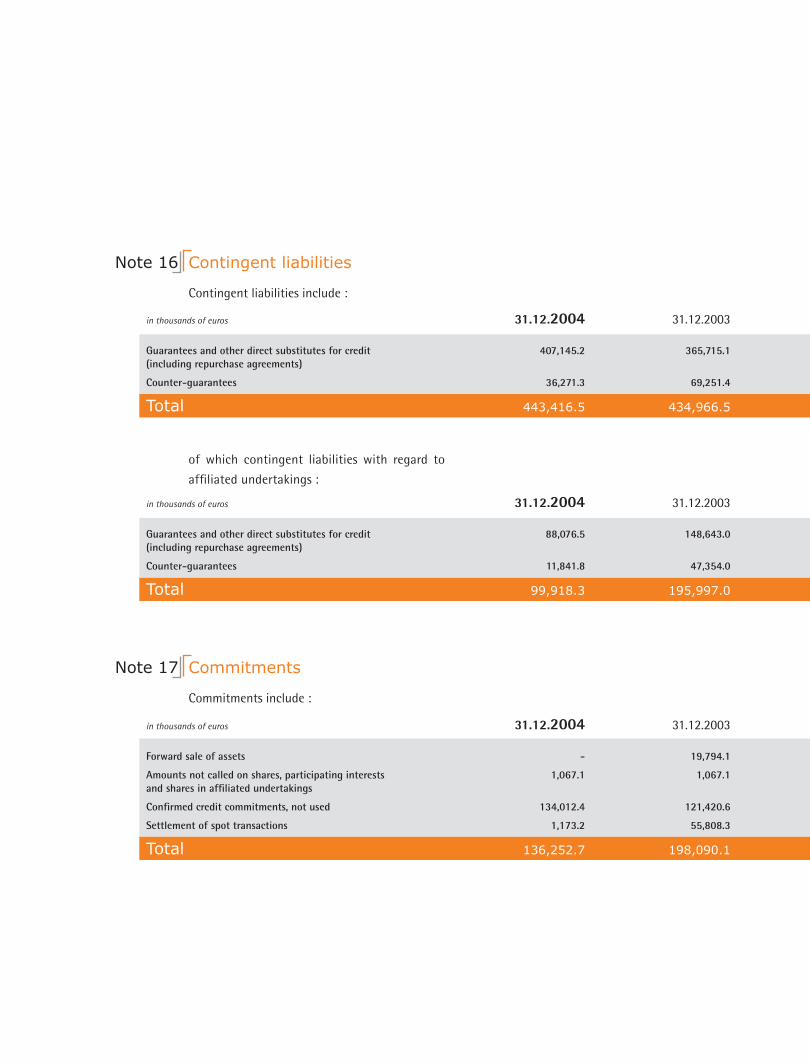

in euros Notes 2004 2003 Contingent liabilities 16 443,416,539 434,966,518 of which - guarantees and assets pledged as collateral security 407,145,225 365,715,113

The accompanying notes form an integral part of these annual accounts

Off-balance sheet

Balance sheet as at December 31, 2004

Assets

Liabilities and Shareholders’

Equity

Off-balance sheet

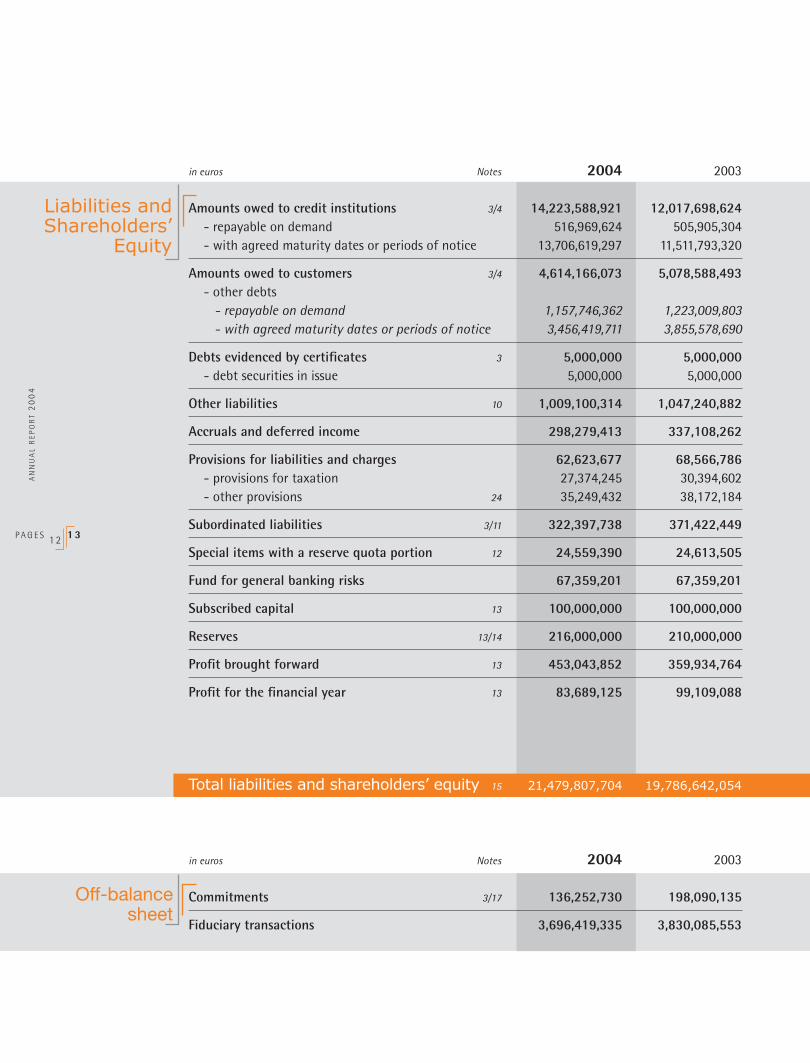

in euros Notes 2004 2003

Amounts owed to credit institutions 3/4 14,223,588,921 12,017,698,624 - repayable on demand 516,969,624 505,905,304 - with agreed maturity dates or periods of notice 13,706,619,297 11,511,793,320

Amounts owed to customers 3/4 4,614,166,073 5,078,588,493 - other debts - repayable on demand 1,157,746,362 1,223,009,803 - with agreed maturity dates or periods of notice 3,456,419,711 3,855,578,690

Debts evidenced by certificates 3 5,000,000 5,000,000 - debt securities in issue 5,000,000 5,000,000

Other liabilities 10 1,009,100,314 1,047,240,882

Accruals and deferred income 298,279,413 337,108,262

Provisions for liabilities and charges 62,623,677 68,566,786 - provisions for taxation 27,374,245 30,394,602 - other provisions 24 35,249,432 38,172,184

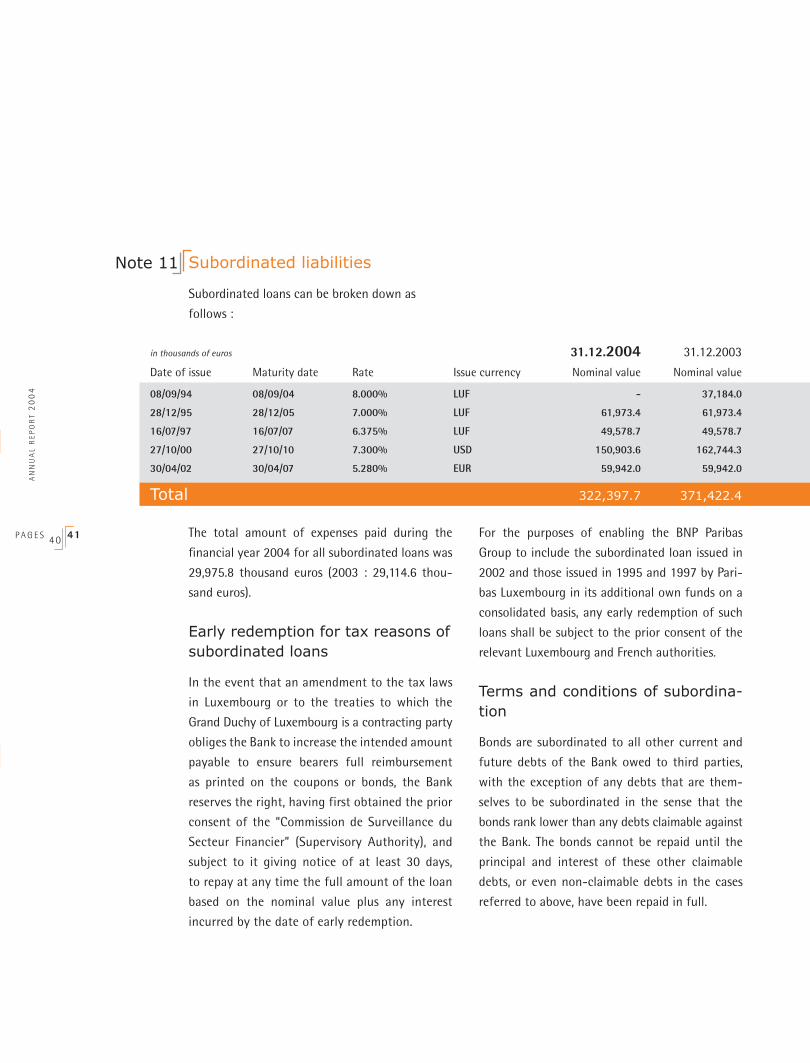

Subordinated liabilities 3/11 322,397,738 371,422,449

Special items with a reserve quota portion 12 24,559,390 24,613,505

Fund for general banking risks 67,359,201 67,359,201

Subscribed capital 13 100,000,000 100,000,000

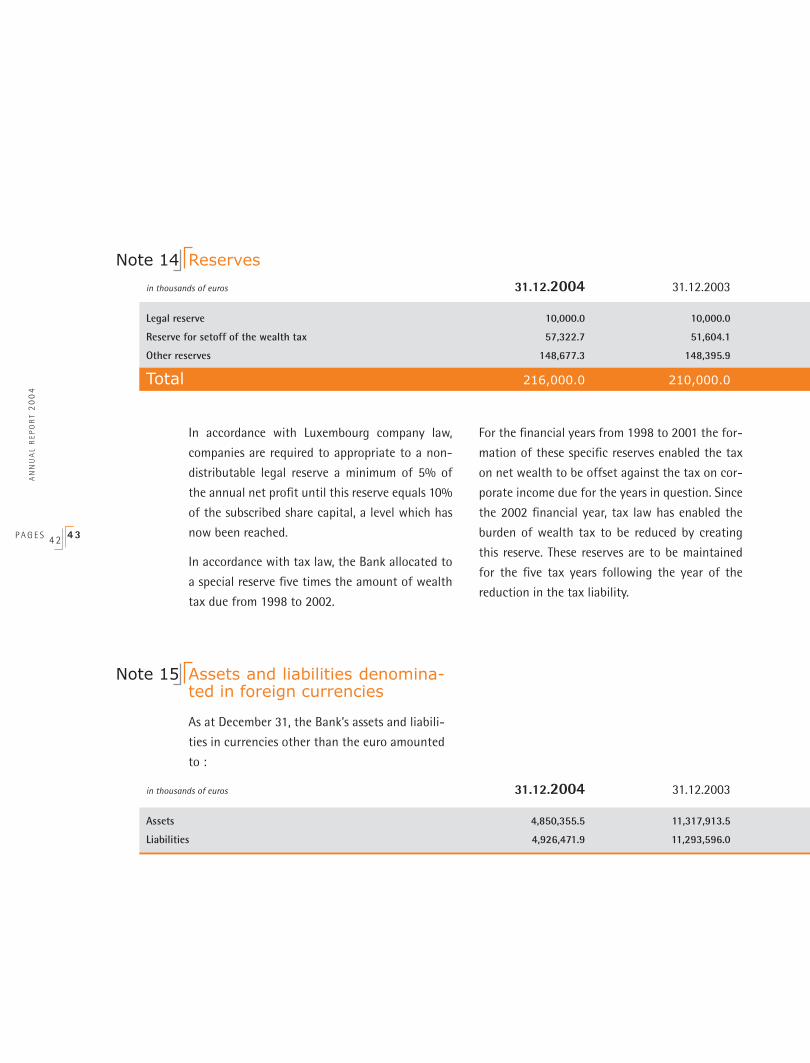

Reserves 13/14 216,000,000 210,000,000

Profit brought forward 13 453,043,852 359,934,764

Profit for the financial year 13 83,689,125 99,109,088

Total liabilities and shareholders’ equity 15 21,479,807,704 19,786,642,054

in euros Notes 2004 2003

Commitments 3/17 136,252,730 198,090,135 Fiduciary transactions 3,696,419,335 3,830,085,553

AN

NU

AL

RE

PO

RT

20

04

P A G E S 1 2 1 3

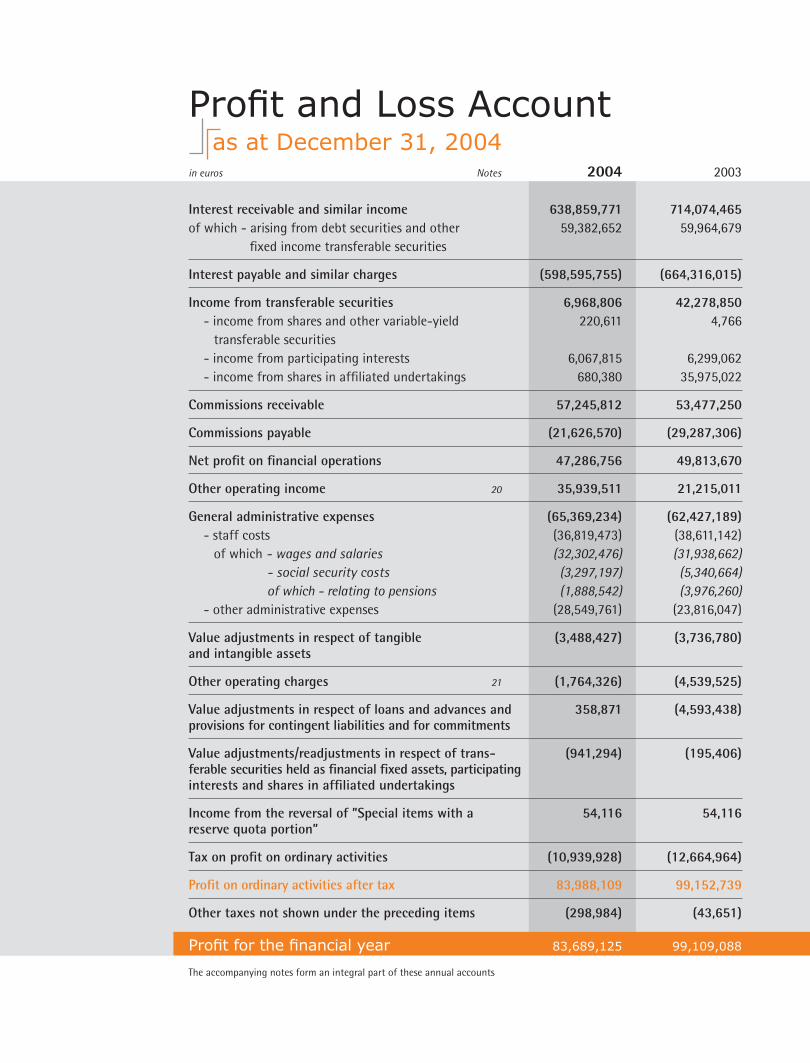

in euros Notes 2004 2003 Interest receivable and similar income 638,859,771 714,074,465of which - arising from debt securities and other 59,382,652 59,964,679 fixed income transferable securities Interest payable and similar charges (598,595,755) (664,316,015) Income from transferable securities 6,968,806 42,278,850 - income from shares and other variable-yield 220,611 4,766 transferable securities - income from participating interests 6,067,815 6,299,062 - income from shares in affiliated undertakings 680,380 35,975,022 Commissions receivable 57,245,812 53,477,250 Commissions payable (21,626,570) (29,287,306) Net profit on financial operations 47,286,756 49,813,670 Other operating income 20 35,939,511 21,215,011 General administrative expenses (65,369,234) (62,427,189) - staff costs (36,819,473) (38,611,142) of which - wages and salaries (32,302,476) (31,938,662) - social security costs (3,297,197) (5,340,664) of which - relating to pensions (1,888,542) (3,976,260) - other administrative expenses (28,549,761) (23,816,047) Value adjustments in respect of tangible (3,488,427) (3,736,780)and intangible assets Other operating charges 21 (1,764,326) (4,539,525) Value adjustments in respect of loans and advances and 358,871 (4,593,438)provisions for contingent liabilities and for commitments Value adjustments/readjustments in respect of trans- (941,294) (195,406)ferable securities held as financial fixed assets, participatinginterests and shares in affiliated undertakings Income from the reversal of ”Special items with a 54,116 54,116reserve quota portion” Tax on profit on ordinary activities (10,939,928) (12,664,964)

Profit on ordinary activities after tax 83,988,109 99,152,739 Other taxes not shown under the preceding items (298,984) (43,651)

Profit for the financial year 83,689,125 99,109,088

The accompanying notes form an integral part of these annual accounts

Profit and Loss Account as at December 31, 2004

Notes to the Annual Accounts as at December 31, 2004

General

BNP Paribas Luxembourg, hereinafter referred to

as “the Bank”, was established on October 23, 1964

in the form of a public limited company subject to

Luxembourg law by the name of “Banque de Paris et

des Pays-Bas pour le Grand-Duché de Luxembourg

SA”.

On July 17, 2000 Paribas Luxembourg and Banque

Nationale de Paris (Luxembourg) SA, a public limited

company under Luxembourg law established on May

28, 1921, merged to form BNP Paribas Luxembourg

with retroactive effect for accounting purposes from

January 1, 2000.

Under Luxembourg law the Bank may engage in

any form of banking transactions. The Bank is a

subsidiary of BNP Paribas, “société anonyme” under

French law with its registered office at 16 boulevard

des Italiens, F-75009 Paris.

The Bank’s annual accounts are included in the con-

solidated annual accounts prepared by BNP Paribas,

which are available from the registered office of

BNP Paribas.

The Bank is exempt from the requirement to publish

consolidated annual accounts and a consolidated

management report.

Significant accounting policies

The Bank’s annual accounts are prepared in accor-

dance with the laws and regulations applicable to the

banking sector in the Grand Duchy of Luxembourg.

The following accounting principles are of particular

significance :

2.1 Currency translation

The annual accounts are expressed in euros.

The Bank uses the multi-currency accounting method

which involves recording assets and liabilities, off-

balance sheet items and income and expenses in their

original currencies.

For the purposes of preparing financial statements

in euros, assets and liabilities as well as suspense

accounts denominated in currencies other than the

euro are translated on the basis of the spot exchange

rates recorded at the balance sheet date.

Income and expenses in currencies other than the

euro are recorded in their respective currencies and

translated on a daily basis at the prevailing exchange

rates at the recording date.

Foreign exchange gains and losses resulting from the

net non-forward-hedged spot currency position are

posted to the profit and loss account.

Exchange differences resulting from the valuation

of spot exchange transactions hedged by forward

exchange transactions (swaps) are set against each

other under prepayments and accrued income,

and accruals and deferred income. Any differences

between the spot and forward exchange rates

(premium or discount) realised in the conclusion of

such transactions are accounted for in the profit and

loss account pro rata temporis.

Forward exchange transactions that are not linked to

balance sheet items are valued at the forward rate

applicable at the balance sheet date.

AN

NU

AL

RE

PO

RT

20

04

P A G E S 1 4 15

Note 1

Note 2

Provision is made for unrealised losses on non-hedged

forward exchange translations whilst any unrealised

gains are not taken into account.

On hedged forward exchange transactions, a provision

is made to cover estimated residual losses, after off

setting those losses against estimated gains on

all transactions maturing the same day or earlier.

Estimated residual gains are not taken into account.

2.2 Demand and fixed-term assets and liabilities

Assets and liabilities that are repayable on demand

include those amounts that could be recovered at

any time without notice, or with a period or notice

period of 24 hours or of one working day, has been

agreed. The expression “with agreed maturity dates”

as used with regard to the various accounting items

refers to a final maturity of more than one working

day, including periods of notice of more than one

working day. Assets and liabilities are classed

according to the remaining maturity, in other words

the remaining term as at the balance sheet date.

2.3 Fixed income securities

All of the securities included in the three portfolio

categories are entered in the balance sheet in their

currency of issue. They are valued at the closing date

according to the methods applicable to each portfolio

category.

2.3.1 Financial fixed assets

Financial fixed assets are fixed income securities

intended for use on a long-term basis in the Bank’s

activities.

Financial fixed assets are entered in the balance sheet

at purchase price.

Within the limit specified by the Luxembourg

Banking Regulations, the Bank distinguishes between

transferable securities that are valued according to

the purchase price method and those securities that

are valued according to the principle of lower of cost

or market.

2.3.1.1 Transferable securities maintained at

purchase price

With regard to securities in this portfolio subcate-

gory, the premium is treated differently according to

whether there exists matched refinancing or interest

rate risk hedging.

With regard to securities for which there exists

matched refinancing or interest rate risk hedging,

the difference between the purchase price and the

redemption price is accrued.

With regard to other securities, the full depreciation

of the premium is applied throughout the year

of acquisition, within the limit specified by the

Luxembourg Banking Regulations.

Value adjustments are only made for permanent

depreciation ; unrealised gains are not taken into

account.

2.3.1.2 Securities valued at the lower of cost

or market

Securities are valued at the lower of cost, minus any

prorated premiums or discounts, or of market. Value

adjustments are made to take account of unrealised

losses. Any unrealised gains are not taken into

account.

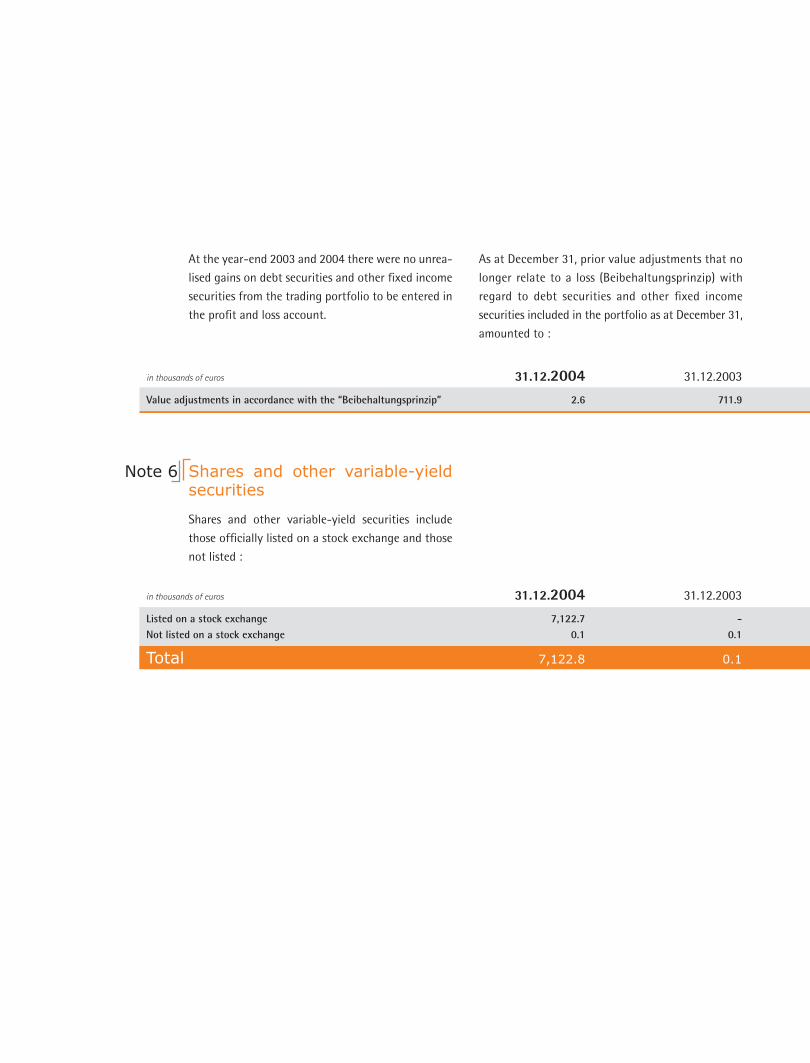

Prior value adjustments that no longer relate to a

loss at the closing date are maintained for the se-

curities included in the portfolio as at 31 December

(Beibehaltungsprinzip).

AN

NU

AL

RE

PO

RT

20

04

P A G E S 16 17

2.3.2 Structural portfolio

The securities included in this portfolio are securities

that were acquired with a view to earning a return.

They are entered in the balance sheet at their pur-

chase price. The premium is depreciated pro rata

temporis for the period for which the security

has already been held. The securities are valued at

the lower of cost, adjusted to take account of the

depreciated premium, or of market. Value adjust-

ments are made to take account of unrealised losses.

Any unrealised gains are not taken into account.

Prior value adjustments that no longer relate to a

loss at the closing date are maintained for the se-

curities included in the portfolio as at 31 December

(Beibehaltungsprinzip).

2.3.3 Trading portfolio

The fixed income securities in the trading portfolio

are held with the purpose of being resold in the

short term.

They are valued and entered in the balance sheet

at their market value. Unrealised valuation gains

and losses are taken to the profit and loss account

at the balance sheet date.

2.4 Variable-yield securities

2.4.1 Structural portfolio

Variable-yield securities are posted to the balance

sheet at their purchase price in the reporting currency

of the issuing company.

The securities are valued at the lower of cost or

market. Value adjustments are made to take account

of unrealised losses. Any unrealised gains are not

taken into account.

2.4.2 Financial fixed assets

Participating interests and shares in affiliated under-

takings considered to be financial fixed assets are

recorded at the acquisition cost and in the reporting

currency of the issuing company. Value adjustments

are made in the event of a permanent depreciation.

2.5 Tangible and intangible assets

Tangible and intangible assets are recorded in the

balance sheet at the acquisition cost less accumula-

ted depreciation. The annual depreciation is carried

out on a straight line basis and the rate fixed

according to the estimated useful life of the goods.

Land is not subject to depreciation.

The depreciation rates used are the following :

Acquisitions in the amount of or less than 870 euros

or the equivalent countervalue are entered under

“Other administrative expenses”.

2.6 Value adjustments and provisions

Specific provisions (value adjustments) established to

cover loans and advances and sovereign risks with

regard to which the Bank regards recoverability as

uncertain are presented as a reduction in the value

of the assets. Value adjustments and provisions for

contingent liabilities and for amounts owed are

made in the same currency as the currency of the risk

being covered.

2004 2003Goodwill 20% 20%

Buildings, installations 2% to 10% 2% to 10%and fixtures

IT equipment and software 20% to 33% 20% to 33%

Other technical installations, 10% to 25% 10% to 25%plant, fixtures and vehicles

Allocations to and withdrawals from value adjust-

ments and provisions for contingent liabilities and

amounts owed are offset in the profit and loss

account.

The lump-sum provision for risk exposures esta-

blished on the basis provided by Luxembourg tax

and banking legislation is recorded in the reporting

currency. The portion of the general provision

calculated on the basis of the credit risk of the

balance sheet items is deducted from the asset items

used in the calculation.

The portion of the general provision calculated on

the basis of other risks is entered on the liabilities

side under the item “Provisions for liabilities and

charges”.

Provisions for liabilities and charges are accounted

for to cover losses or debts that are clearly of a

restricted nature but which, as at the balance sheet

date, are either probable or certain but yet to be

specified in terms of amount or due date.

The Bank has established a fund for general banking

risks on the liabilities side of the balance sheet. This

provision has been made in the currency in which the

capital is expressed from profits after tax but prior to

determination of net profit.

2.7 Debts

Debts are entered on the liabilities side of the balance

sheet at their repayment value.

2.8 Forward financial instruments

2.8.1 Interest rate swaps

Forward interest rate instruments, mainly Interest

Rate Swaps (IRS), traded on the OTC market and not

allocated to specific assets or liabilities, are valued

at market value. Unrealised losses are taken into

account in the result whilst no account is taken of

unrealised gains.

IRS traded on the OTC market and used to hedge

the Bank’s interest rate positions are not valued at

market value.

2.8.2 Options

With regard to options traded on the OTC market

that are not allocated to specific assets or liabilities,

premiums paid or received are recorded in the

balance sheet or until the option is exercised or

until maturity if the option has not been exercised

by then. Commitments relating to issued options are

recorded as off-balance sheet items.

Options held for purposes other than hedging are

valued at their market value. Estimated unrealised

losses are taken into account in the profit and loss

account while no account is taken of unrealised

gains.

Options held for hedging purposes, other than those

purchased to hedge warrant issues, are not valued.

Options traded on the organised market to hedge

transactions in the opposite direction, or options with

identical characteristics, also traded on the organised

market, are treated as follows : the position on these

instruments having been closed, the profit/loss from

the premiums received and paid is entered in the

profit and loss account.

2.8.3 Warrants linked to options

The Bank issues warrants based on stock market

indexes or baskets of shares. These warrant issues

are fully hedged through the purchase of options

with the same characteristics as the warrants, i.e. the

AN

NU

AL

RE

PO

RT

20

04

P A G E S 18 19

same strike price, the same maturity date and the

same underlying instrument.

Premiums paid for the purchase of options are

entered under “Other assets”. Premiums received

for the issues of warrants are entered under “Other

liabilities”.

Option premiums relating to purchased options and

issued warrants are valued at market value.

2.9 Taxes

Taxes are charged to the financial year to which the

earnings are recorded.

Provisions for tax are entered on the liabilities side

under the balance sheet item “Provisions for liabili-

ties and charges” for the financial years for which the

tax authorities have not yet fixed the final amount

of tax due.

Use of financial instruments

3.1 Strategy and policy with regard to use of financial instruments

The market activities of the Bank are fully compliant

with the strategy of the BNP Paribas Group in terms

of objectives, organisational structure and products.

The objectives include participation in the global

financing of the Group, operation financing for

customers and the generating of earnings through

margins and product trading.

The Bank accepts deposits from its clients on a fixed

and variable-rate basis and for different periods. It

then seeks to benefit from higher average interest

rate margins by investing these deposits in high-

quality assets.

The Bank also seeks to increase its margins by

consolidating its short-term cash flow by means of

loans covering longer periods whilst maintaining

sufficient liquidity to honour its commitments.

The organisational structure is based on different

business lines. Responsibility for all of the risks

associated with the Bank’s operations is ultimately

borne by the managers of the different business lines

at head office. The business lines that specialise in

interest rate and foreign exchange take charge of

the related risks in these areas, from which the other

business lines are kept separate. The Bank only makes

use of traditional products, avoiding any high-risk or

complex products.

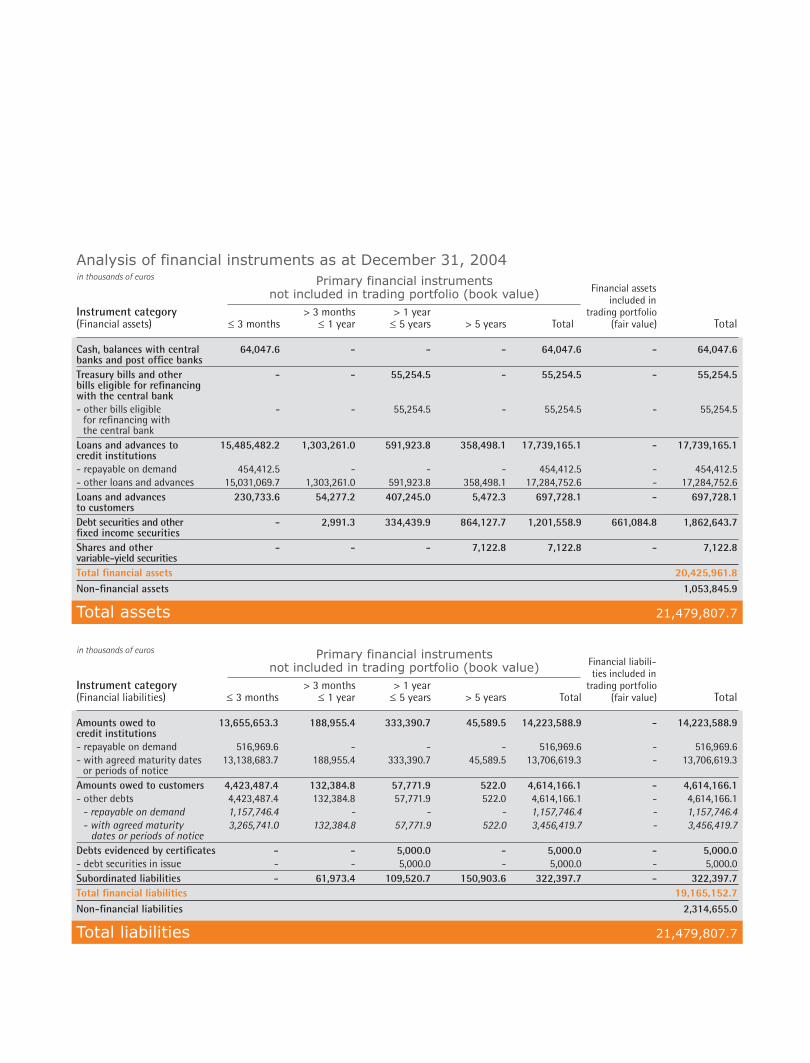

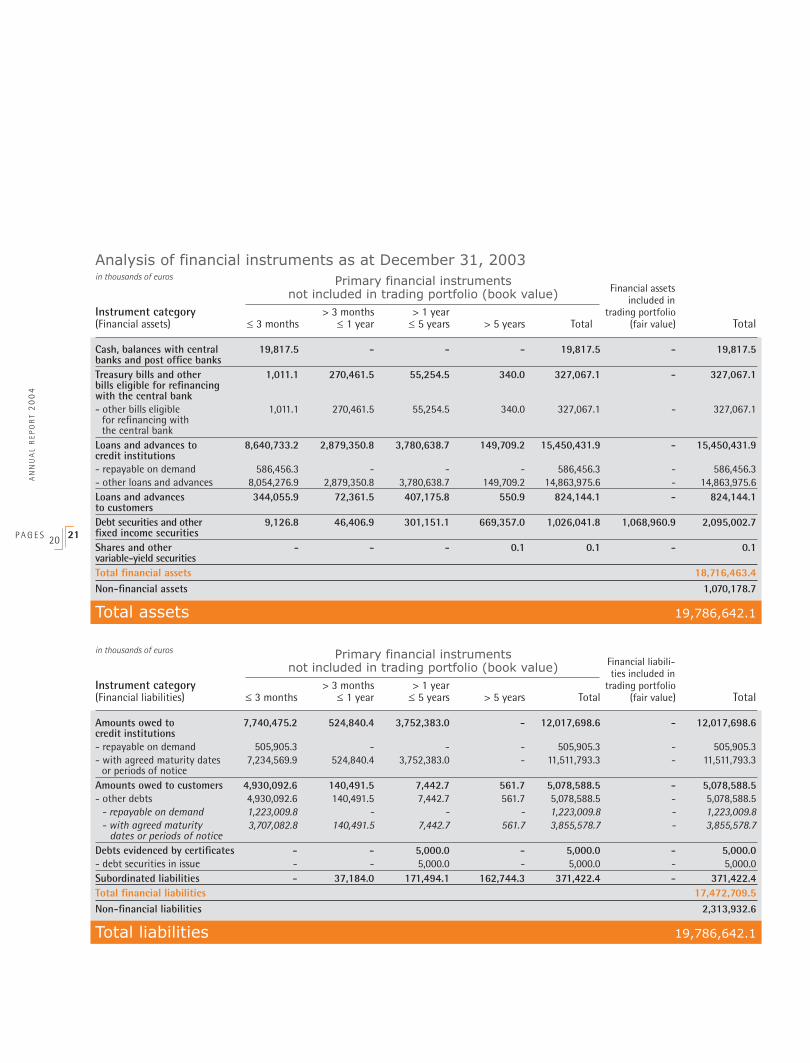

3.2 Analysis of financial instruments

3.2.1 Information on primary financial instruments

The tables below analyse the level of activity in

primary financial instruments (primary financial

instruments held for trading purposes and primary

financial instruments held for hedging or other

purposes) on the part of the Bank, by grouping the

instruments according to remaining maturities. The

financial instruments not included in the trading

portfolio are reported at their book value whilst

trading instruments are recorded at fair value with

their acquisition value given by way of comparison.

“Fair value” is understood to mean the value at which

an asset may be exchanged or a liability settled in

the context of an ordinary transaction entered into

under normal conditions between independent,

informed and willing parties, other than in a forced

or liquidation sale.

Note 3

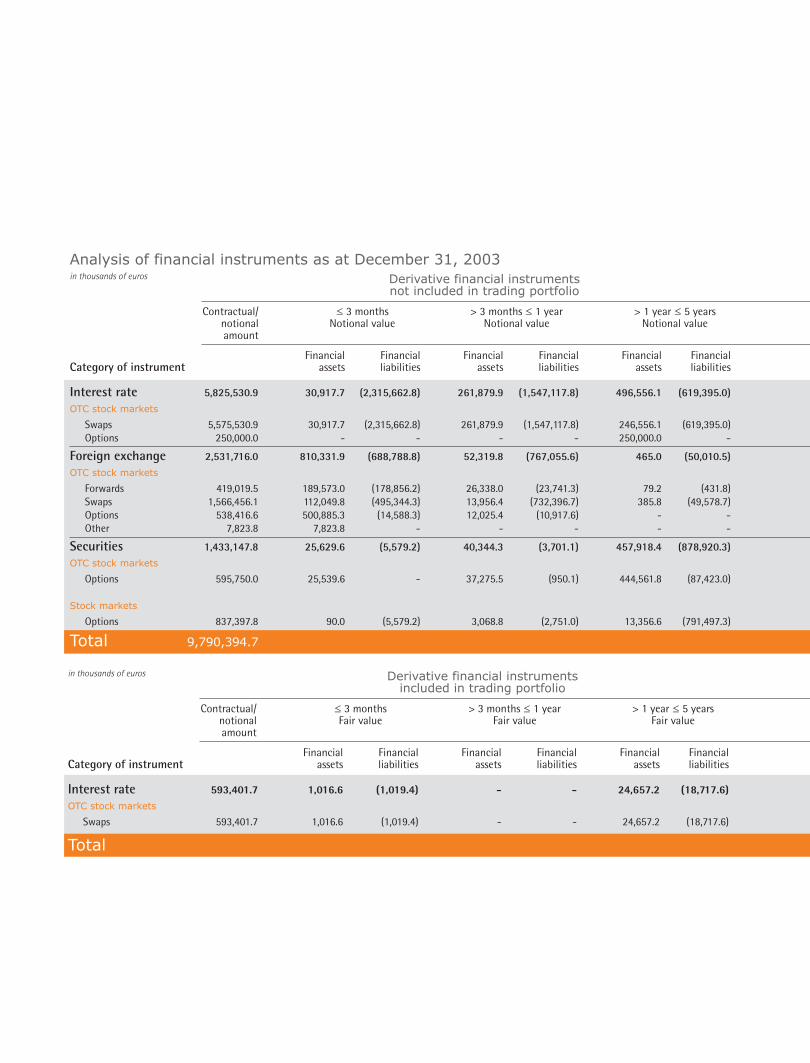

in thousands of euros Primary financial instruments

Financial liabili- not included in trading portfolio (book value) ties included in Instrument category > 3 months > 1 year trading portfolio (Financial liabilities) ≤ 3 months ≤ 1 year ≤ 5 years > 5 years Total (fair value) Total

Amounts owed to 13,655,653.3 188,955.4 333,390.7 45,589.5 14,223,588.9 - 14,223,588.9credit institutions - repayable on demand 516,969.6 - - - 516,969.6 - 516,969.6- with agreed maturity dates 13,138,683.7 188,955.4 333,390.7 45,589.5 13,706,619.3 - 13,706,619.3 or periods of notice Amounts owed to customers 4,423,487.4 132,384.8 57,771.9 522.0 4,614,166.1 - 4,614,166.1- other debts 4,423,487.4 132,384.8 57,771.9 522.0 4,614,166.1 - 4,614,166.1 - repayable on demand 1,157,746.4 - - - 1,157,746.4 - 1,157,746.4 - with agreed maturity 3,265,741.0 132,384.8 57,771.9 522.0 3,456,419.7 - 3,456,419.7 dates or periods of notice Debts evidenced by certificates - - 5,000.0 - 5,000.0 - 5,000.0- debt securities in issue - - 5,000.0 - 5,000.0 - 5,000.0Subordinated liabilities - 61,973.4 109,520.7 150,903.6 322,397.7 - 322,397.7Total financial liabilities 19,165,152.7Non-financial liabilities 2,314,655.0

Total liabilities 21,479,807.7

Analysis of financial instruments as at December 31, 2004 in thousands of euros Primary financial instruments

Financial assets not included in trading portfolio (book value) included in Instrument category > 3 months > 1 year trading portfolio (Financial assets) ≤ 3 months ≤ 1 year ≤ 5 years > 5 years Total (fair value) Total Cash, balances with central 64,047.6 - - - 64,047.6 - 64,047.6banks and post office banks Treasury bills and other - - 55,254.5 - 55,254.5 - 55,254.5bills eligible for refinancing with the central bank - other bills eligible - - 55,254.5 - 55,254.5 - 55,254.5 for refinancing with the central bank Loans and advances to 15,485,482.2 1,303,261.0 591,923.8 358,498.1 17,739,165.1 - 17,739,165.1credit institutions - repayable on demand 454,412.5 - - - 454,412.5 - 454,412.5- other loans and advances 15,031,069.7 1,303,261.0 591,923.8 358,498.1 17,284,752.6 - 17,284,752.6Loans and advances 230,733.6 54,277.2 407,245.0 5,472.3 697,728.1 - 697,728.1to customers Debt securities and other - 2,991.3 334,439.9 864,127.7 1,201,558.9 661,084.8 1,862,643.7fixed income securities Shares and other - - - 7,122.8 7,122.8 - 7,122.8variable-yield securities Total financial assets 20,425,961.8Non-financial assets 1,053,845.9

Total assets 21,479,807.7

in thousands of euros Primary financial instruments

Financial liabili- not included in trading portfolio (book value) ties included in Instrument category > 3 months > 1 year trading portfolio (Financial liabilities) ≤ 3 months ≤ 1 year ≤ 5 years > 5 years Total (fair value) Total

Amounts owed to 7,740,475.2 524,840.4 3,752,383.0 - 12,017,698.6 - 12,017,698.6credit institutions - repayable on demand 505,905.3 - - - 505,905.3 - 505,905.3- with agreed maturity dates 7,234,569.9 524,840.4 3,752,383.0 - 11,511,793.3 - 11,511,793.3 or periods of notice Amounts owed to customers 4,930,092.6 140,491.5 7,442.7 561.7 5,078,588.5 - 5,078,588.5- other debts 4,930,092.6 140,491.5 7,442.7 561.7 5,078,588.5 - 5,078,588.5 - repayable on demand 1,223,009.8 - - - 1,223,009.8 - 1,223,009.8 - with agreed maturity 3,707,082.8 140,491.5 7,442.7 561.7 3,855,578.7 - 3,855,578.7 dates or periods of notice Debts evidenced by certificates - - 5,000.0 - 5,000.0 - 5,000.0- debt securities in issue - - 5,000.0 - 5,000.0 - 5,000.0Subordinated liabilities - 37,184.0 171,494.1 162,744.3 371,422.4 - 371,422.4Total financial liabilities 17,472,709.5Non-financial liabilities 2,313,932.6

Total liabilities 19,786,642.1

AN

NU

AL

RE

PO

RT

20

04

P A G E S 20 21

Analysis of financial instruments as at December 31, 2003 in thousands of euros Primary financial instruments

Financial assets not included in trading portfolio (book value) included in Instrument category > 3 months > 1 year trading portfolio (Financial assets) ≤ 3 months ≤ 1 year ≤ 5 years > 5 years Total (fair value) Total Cash, balances with central 19,817.5 - - - 19,817.5 - 19,817.5banks and post office banks Treasury bills and other 1,011.1 270,461.5 55,254.5 340.0 327,067.1 - 327,067.1bills eligible for refinancing with the central bank - other bills eligible 1,011.1 270,461.5 55,254.5 340.0 327,067.1 - 327,067.1 for refinancing with the central bank Loans and advances to 8,640,733.2 2,879,350.8 3,780,638.7 149,709.2 15,450,431.9 - 15,450,431.9credit institutions - repayable on demand 586,456.3 - - - 586,456.3 - 586,456.3- other loans and advances 8,054,276.9 2,879,350.8 3,780,638.7 149,709.2 14,863,975.6 - 14,863,975.6Loans and advances 344,055.9 72,361.5 407,175.8 550.9 824,144.1 - 824,144.1to customers Debt securities and other 9,126.8 46,406.9 301,151.1 669,357.0 1,026,041.8 1,068,960.9 2,095,002.7fixed income securities Shares and other - - - 0.1 0.1 - 0.1variable-yield securities Total financial assets 18,716,463.4Non-financial assets 1,070,178.7

Total assets 19,786,642.1

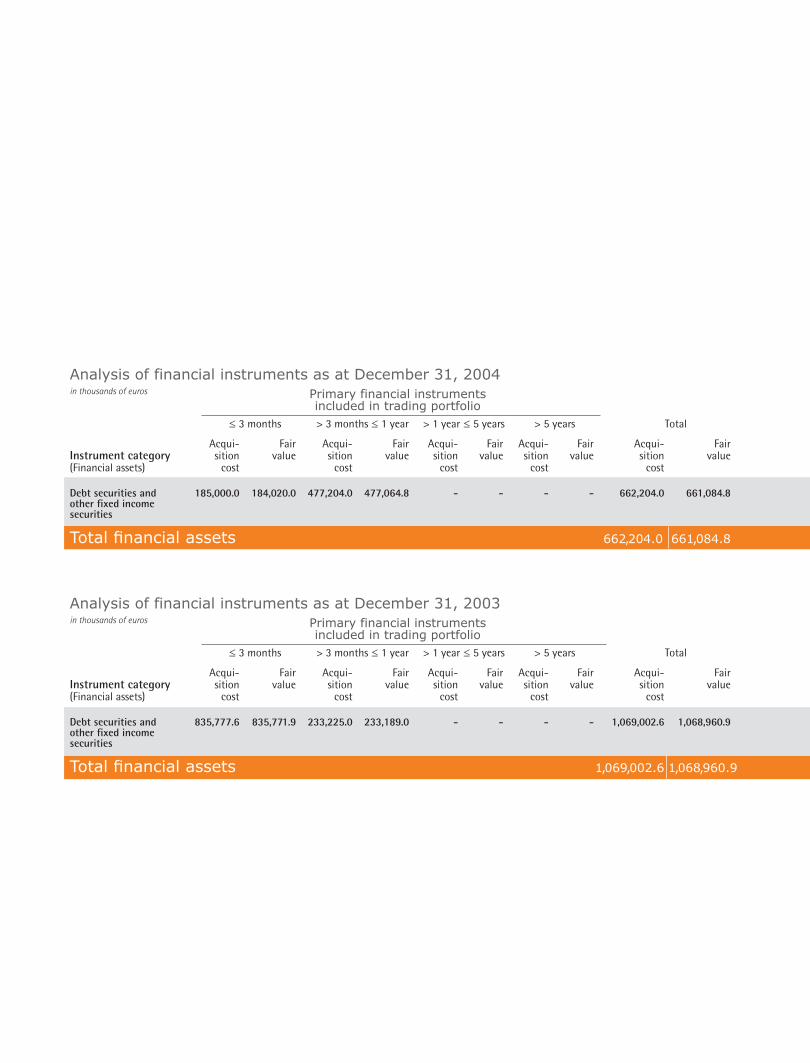

Analysis of financial instruments as at December 31, 2004 in thousands of euros Primary financial instruments included in trading portfolio ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total

Acqui- Fair Acqui- Fair Acqui- Fair Acqui- Fair Acqui- FairInstrument category sition value sition value sition value sition value sition value(Financial assets) cost cost cost cost cost

Debt securities and 185,000.0 184,020.0 477,204.0 477,064.8 - - - - 662,204.0 661,084.8other fixed income securities

Total financial assets 662,204.0 661,084.8

Analysis of financial instruments as at December 31, 2003 in thousands of euros Primary financial instruments included in trading portfolio ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total

Acqui- Fair Acqui- Fair Acqui- Fair Acqui- Fair Acqui- FairInstrument category sition value sition value sition value sition value sition value(Financial assets) cost cost cost cost cost

Debt securities and 835,777.6 835,771.9 233,225.0 233,189.0 - - - - 1,069,002.6 1,068,960.9other fixed income securities

Total financial assets 1,069,002.6 1,068,960.9

AN

NU

AL

RE

PO

RT

20

04

P A G E S 22 23

3.2.2 Information on derivative finan-cial instruments

3.2.2.1 Description of derivative financial

instruments used

The Bank uses the following derivative financial

instruments, basically for hedging purposes but also

with regard to trading. These transactions are either

traded on a stock market or traded on an OTC basis

between the Bank and its counterparties.

Forward exchange transactions represent commit-

ments entered into on an OTC basis to purchase

foreign currency in exchange for delivery of the

equivalent value in another currency at an exchange

rate and on a date specified at the time of the

transaction being concluded.

Currency swaps involve an initial exchange on a spot

basis of amounts in two currencies. This is followed

by a second exchange of these amounts at maturity

in the opposite direction, adjusted to take account

of the difference in interest rates applied to the two

currencies, subject to conditions and dates specified

upon conclusion of the swap.

Interest rate swaps involve the exchange of one

interest rate for another, either on the basis of a fixed

versus a floating rate, or on the basis of two floating

rates, calculated on the basis of the same notional

amount in a currency that is itself not swapped.

Cross currency interest rate swaps are a combination

of a currency swap and an interest rate swap

involving the exchange at the outset and at maturity

of the nominal amount and the exchange of interest

rates at intermediate dates and at maturity.

These three types of swaps are traded on the OTC

market.

Options are contractual agreements whereby the

seller (issuer) gives the buyer (holder) the right, but

not the obligation, either to buy (call option) or

to sell (put option) a predetermined amount of a

foreign currency or of securities at a predetermined

price either on a specified date or during a specified

period. Linked to the risk of the transaction, the seller

receives a premium from the buyer. The options may

be traded on a stock market or be traded directly

between the Bank and its counterparty.

The Bank also issues warrants based on stock market

indexes or baskets of shares. These warrant issues are

fully hedged through the purchase of options with

the same characteristics as the warrants, i.e. the

same strike price, the same maturity date and the

same underlying instrument.

The Bank also engages in forward security selling.

3.2.2.2 Analysis of derivative financial

instruments

The tables below analyse the level of derivative

financial instruments used by the Bank for purposes

other than trading, according to notional amount

and grouped according to the residual period until

the maturity date. Derivative financial instruments

traded outside of stock markets and derivative

financial instruments traded on the stock markets

are presented separately.

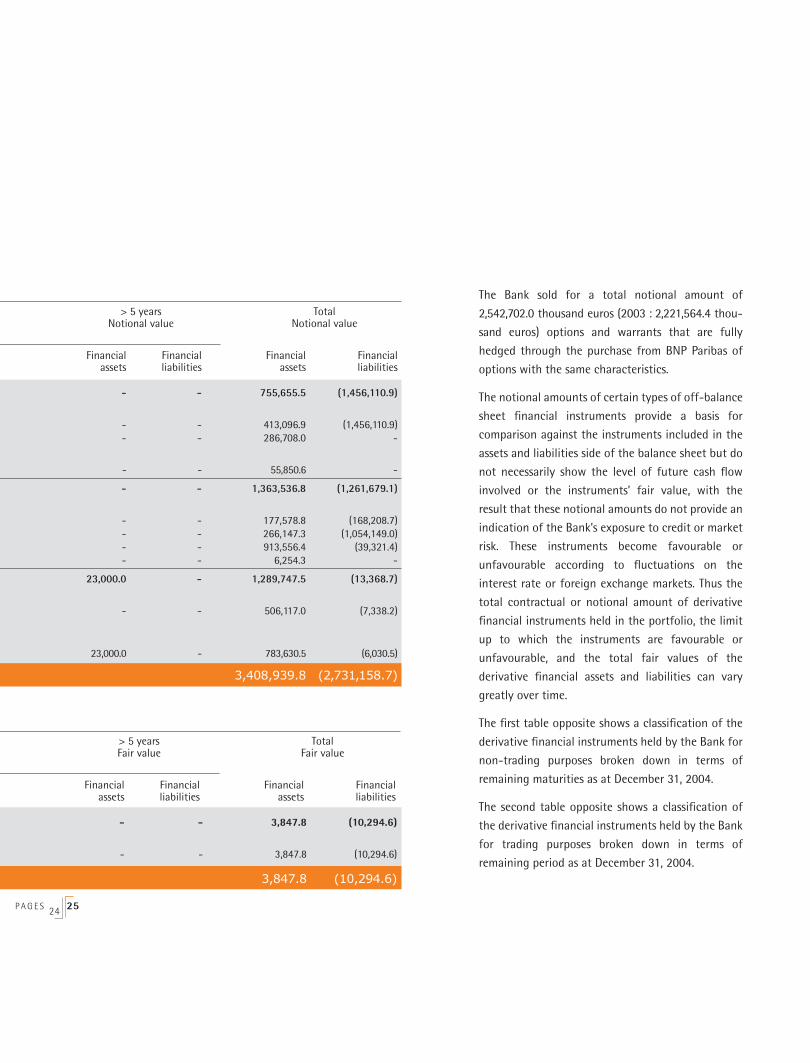

Analysis of financial instruments as at December 31, 2004 in thousands of euros Derivative financial instruments not included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Notional value Notional value Notional value Notional value Notional value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 2,211,766.4 55,850.6 (1,410,878.9) 184,596.9 (45,232.0) 515,208.0 - - - 755,655.5 (1,456,110.9)OTC stock markets Swaps 1,869,207.8 - (1,410,878.9) 184,596.9 (45,232.0) 228,500.0 - - - 413,096.9 (1,456,110.9) Options 286,708.0 - - - - 286,708.0 - - - 286,708.0 -

Stock markets Other 55,850.6 55,850.6 - - - - - - - 55,850.6 -

Foreign exchange 2,625,215.9 790,084.3 (1,028,129.4) 559,571.8 (231,585.8) 13,880.7 (1,963.9) - - 1,363,536.8 (1,261,679.1)OTC stock markets Forwards 345,787.5 119,491.7 (110,385.2) 57,997.9 (57,731.7) 89.2 (91.8) - - 177,578.8 (168,208.7) Swaps 1,320,296.3 262,535.4 (899,852.9) 3,611.9 (154,296.1) - - - - 266,147.3 (1,054,149.0) Options 952,877.8 401,802.9 (17,891.3) 497,962.0 (19,558.0) 13,791.5 (1,872.1) - - 913,556.4 (39,321.4) Other 6,254.3 6,254.3 - - - - - - - 6,254.3 -

Securities 1,303,116.2 45,663.9 (2,121.5) 249,144.4 (1,966.8) 971,939.2 (9,280.4) 23,000.0 - 1,289,747.5 (13,368.7)OTC stock markets Options 513,455.2 45,663.9 - 18,807.1 - 441,646.0 (7,338.2) - - 506,117.0 (7,338.2) Stock markets Options 789,661.0 - (2,121.5) 230,337.3 (1,966.8) 530,293.2 (1,942.2) 23,000.0 - 783,630.5 (6,030.5)

Total 6,140,098.5 3,408,939.8 (2,731,158.7)

in thousands of euros Derivative financial instruments included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Fair value Fair value Fair value Fair value Fair value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 163,665.6 - - 3,847.8 (10,294.6) - - - - 3,847.8 (10,294.6)OTC stock markets

Swaps 163,665.6 - - 3,847.8 (10,294.6) - - - - 3,847.8 (10,294.6)

Total 3,847.8 (10,294.6)

Analysis of financial instruments as at December 31, 2004 in thousands of euros Derivative financial instruments not included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Notional value Notional value Notional value Notional value Notional value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 2,211,766.4 55,850.6 (1,410,878.9) 184,596.9 (45,232.0) 515,208.0 - - - 755,655.5 (1,456,110.9)OTC stock markets Swaps 1,869,207.8 - (1,410,878.9) 184,596.9 (45,232.0) 228,500.0 - - - 413,096.9 (1,456,110.9) Options 286,708.0 - - - - 286,708.0 - - - 286,708.0 -

Stock markets Other 55,850.6 55,850.6 - - - - - - - 55,850.6 -

Foreign exchange 2,625,215.9 790,084.3 (1,028,129.4) 559,571.8 (231,585.8) 13,880.7 (1,963.9) - - 1,363,536.8 (1,261,679.1)OTC stock markets Forwards 345,787.5 119,491.7 (110,385.2) 57,997.9 (57,731.7) 89.2 (91.8) - - 177,578.8 (168,208.7) Swaps 1,320,296.3 262,535.4 (899,852.9) 3,611.9 (154,296.1) - - - - 266,147.3 (1,054,149.0) Options 952,877.8 401,802.9 (17,891.3) 497,962.0 (19,558.0) 13,791.5 (1,872.1) - - 913,556.4 (39,321.4) Other 6,254.3 6,254.3 - - - - - - - 6,254.3 -

Securities 1,303,116.2 45,663.9 (2,121.5) 249,144.4 (1,966.8) 971,939.2 (9,280.4) 23,000.0 - 1,289,747.5 (13,368.7)OTC stock markets Options 513,455.2 45,663.9 - 18,807.1 - 441,646.0 (7,338.2) - - 506,117.0 (7,338.2) Stock markets Options 789,661.0 - (2,121.5) 230,337.3 (1,966.8) 530,293.2 (1,942.2) 23,000.0 - 783,630.5 (6,030.5)

Total 6,140,098.5 3,408,939.8 (2,731,158.7)

in thousands of euros Derivative financial instruments included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Fair value Fair value Fair value Fair value Fair value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 163,665.6 - - 3,847.8 (10,294.6) - - - - 3,847.8 (10,294.6)OTC stock markets

Swaps 163,665.6 - - 3,847.8 (10,294.6) - - - - 3,847.8 (10,294.6)

Total 3,847.8 (10,294.6)

The Bank sold for a total notional amount of

2,542,702.0 thousand euros (2003 : 2,221,564.4 thou-

sand euros) options and warrants that are fully

hedged through the purchase from BNP Paribas of

options with the same characteristics.

The notional amounts of certain types of off-balance

sheet financial instruments provide a basis for

comparison against the instruments included in the

assets and liabilities side of the balance sheet but do

not necessarily show the level of future cash flow

involved or the instruments’ fair value, with the

result that these notional amounts do not provide an

indication of the Bank’s exposure to credit or market

risk. These instruments become favourable or

unfavourable according to fluctuations on the

interest rate or foreign exchange markets. Thus the

total contractual or notional amount of derivative

financial instruments held in the portfolio, the limit

up to which the instruments are favourable or

unfavourable, and the total fair values of the

derivative financial assets and liabilities can vary

greatly over time.

The first table opposite shows a classification of the

derivative financial instruments held by the Bank for

non-trading purposes broken down in terms of

remaining maturities as at December 31, 2004.

The second table opposite shows a classification of

the derivative financial instruments held by the Bank

for trading purposes broken down in terms of

remaining period as at December 31, 2004.

P A G E S 24 25

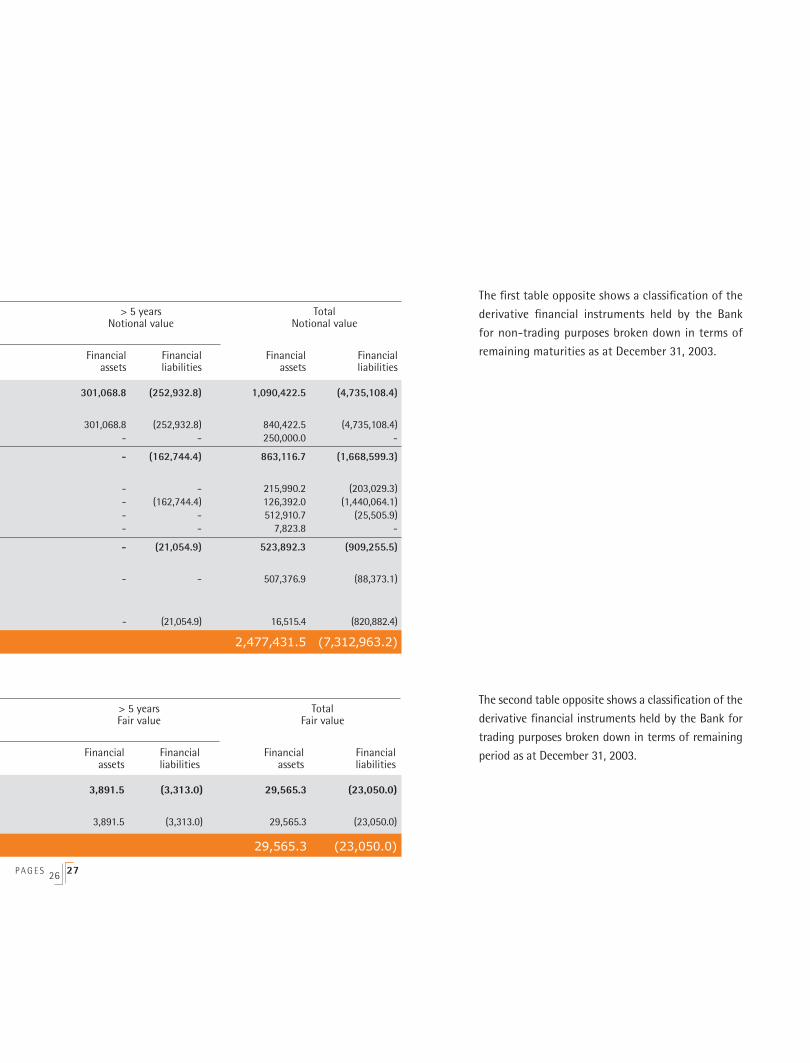

Analysis of financial instruments as at December 31, 2003 in thousands of euros Derivative financial instruments not included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Notional value Notional value Notional value Notional value Notional value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 5,825,530.9 30,917.7 (2,315,662.8) 261,879.9 (1,547,117.8) 496,556.1 (619,395.0) 301,068.8 (252,932.8) 1,090,422.5 (4,735,108.4)OTC stock markets Swaps 5,575,530.9 30,917.7 (2,315,662.8) 261,879.9 (1,547,117.8) 246,556.1 (619,395.0) 301,068.8 (252,932.8) 840,422.5 (4,735,108.4) Options 250,000.0 - - - - 250,000.0 - - - 250,000.0 -

Foreign exchange 2,531,716.0 810,331.9 (688,788.8) 52,319.8 (767,055.6) 465.0 (50,010.5) - (162,744.4) 863,116.7 (1,668,599.3)OTC stock markets Forwards 419,019.5 189,573.0 (178,856.2) 26,338.0 (23,741.3) 79.2 (431.8) - - 215,990.2 (203,029.3) Swaps 1,566,456.1 112,049.8 (495,344.3) 13,956.4 (732,396.7) 385.8 (49,578.7) - (162,744.4) 126,392.0 (1,440,064.1) Options 538,416.6 500,885.3 (14,588.3) 12,025.4 (10,917.6) - - - - 512,910.7 (25,505.9) Other 7,823.8 7,823.8 - - - - - - - 7,823.8 -

Securities 1,433,147.8 25,629.6 (5,579.2) 40,344.3 (3,701.1) 457,918.4 (878,920.3) - (21,054.9) 523,892.3 (909,255.5)OTC stock markets Options 595,750.0 25,539.6 - 37,275.5 (950.1) 444,561.8 (87,423.0) - - 507,376.9 (88,373.1) Stock markets Options 837,397.8 90.0 (5,579.2) 3,068.8 (2,751.0) 13,356.6 (791,497.3) - (21,054.9) 16,515.4 (820,882.4)

Total 9,790,394.7 2,477,431.5 (7,312,963.2)

in thousands of euros Derivative financial instruments included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Fair value Fair value Fair value Fair value Fair value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 593,401.7 1,016.6 (1,019.4) - - 24,657.2 (18,717.6) 3,891.5 (3,313.0) 29,565.3 (23,050.0)OTC stock markets

Swaps 593,401.7 1,016.6 (1,019.4) - - 24,657.2 (18,717.6) 3,891.5 (3,313.0) 29,565.3 (23,050.0)

Total 29,565.3 (23,050.0)

Analysis of financial instruments as at December 31, 2003 in thousands of euros Derivative financial instruments not included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Notional value Notional value Notional value Notional value Notional value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 5,825,530.9 30,917.7 (2,315,662.8) 261,879.9 (1,547,117.8) 496,556.1 (619,395.0) 301,068.8 (252,932.8) 1,090,422.5 (4,735,108.4)OTC stock markets Swaps 5,575,530.9 30,917.7 (2,315,662.8) 261,879.9 (1,547,117.8) 246,556.1 (619,395.0) 301,068.8 (252,932.8) 840,422.5 (4,735,108.4) Options 250,000.0 - - - - 250,000.0 - - - 250,000.0 -

Foreign exchange 2,531,716.0 810,331.9 (688,788.8) 52,319.8 (767,055.6) 465.0 (50,010.5) - (162,744.4) 863,116.7 (1,668,599.3)OTC stock markets Forwards 419,019.5 189,573.0 (178,856.2) 26,338.0 (23,741.3) 79.2 (431.8) - - 215,990.2 (203,029.3) Swaps 1,566,456.1 112,049.8 (495,344.3) 13,956.4 (732,396.7) 385.8 (49,578.7) - (162,744.4) 126,392.0 (1,440,064.1) Options 538,416.6 500,885.3 (14,588.3) 12,025.4 (10,917.6) - - - - 512,910.7 (25,505.9) Other 7,823.8 7,823.8 - - - - - - - 7,823.8 -

Securities 1,433,147.8 25,629.6 (5,579.2) 40,344.3 (3,701.1) 457,918.4 (878,920.3) - (21,054.9) 523,892.3 (909,255.5)OTC stock markets Options 595,750.0 25,539.6 - 37,275.5 (950.1) 444,561.8 (87,423.0) - - 507,376.9 (88,373.1) Stock markets Options 837,397.8 90.0 (5,579.2) 3,068.8 (2,751.0) 13,356.6 (791,497.3) - (21,054.9) 16,515.4 (820,882.4)

Total 9,790,394.7 2,477,431.5 (7,312,963.2)

in thousands of euros Derivative financial instruments included in trading portfolio Contractual/ ≤ 3 months > 3 months ≤ 1 year > 1 year ≤ 5 years > 5 years Total notional Fair value Fair value Fair value Fair value Fair value amount

Financial Financial Financial Financial Financial Financial Financial Financial Financial FinancialCategory of instrument assets liabilities assets liabilities assets liabilities assets liabilities assets liabilities Interest rate 593,401.7 1,016.6 (1,019.4) - - 24,657.2 (18,717.6) 3,891.5 (3,313.0) 29,565.3 (23,050.0)OTC stock markets

Swaps 593,401.7 1,016.6 (1,019.4) - - 24,657.2 (18,717.6) 3,891.5 (3,313.0) 29,565.3 (23,050.0)

Total 29,565.3 (23,050.0)

The first table opposite shows a classification of the

derivative financial instruments held by the Bank

for non-trading purposes broken down in terms of

remaining maturities as at December 31, 2003.

The second table opposite shows a classification of the

derivative financial instruments held by the Bank for

trading purposes broken down in terms of remaining

period as at December 31, 2003.

P A G E S 26 27

3.3 Credit Risk

3.3.1 Description of credit risk

Credit risk is defined as the risk linked to the bor-

rower’s default or changes in solvency, irrespective

of whether such an eventuality is due to a specific

development or wider developments that affect the

country in which the counterparty is based.

Credit risk can be analysed from different perspec-

tives, such as risk concentration, the geographical

distribution of debtors, the quality of any guarantees

received and payment risk.

The Global Credit Policy of the BNP Paribas Group

provides a framework of action relating to the

activities that generate this type of risk :

- loans and other funding instruments,

- holding of securities for own account,

- commitments and contingent liabilities,

- financial contracts.

This policy sets out the rules with regard to sector-

based and country risk and stipulates the decision-

making procedure with regard to the award of credit.

The credit risk linked to balance sheet or off-balance

sheet operations of a borrower or group of borrowers

is subject to limits (or “authorisations”). The decision

on the limit allocated is taken within a system

of delegated authority, with the amount varying

according to the nature of the borrower and activity

concerned. The decision must be made in cooperation

with an independent representative from the Group

Risk Management department, who holds a right of

veto. The different levels of authorisation are ranked

in internal rating categories for the counterparty

and/or the group of economically-linked borrowers

(business groups) to which it belongs.

The authorisations are introduced and updated using

the Bank’s various IT tools, responsibility for which

lies with the Risk Management department, which

must also ensure in advance that the conditions

set out in the credit agreement have been met.

Adherence to the authorisations is monitored by the

business lines as part of their day-to-day work and

by the Risk Management department at a second

level.

The authorisations are subject to periodic review,

at least once per year, which involves analysing the

ability of the borrowers to meet their obligations

and adapting the Bank’s position accordingly. In

particular, the Bank’s risk exposure to different

counterparties can be reduced by means of guarantee

or compensation agreements.

Taking into account the specific characteristics of its

customer portfolio, the Bank basically manages two

types of guarantee :

- bank guarantees with which it is provided,

- financial assets deposited with it and pledged

in its favour. Criteria specific to the BNP Paribas

Group are applied with regard to the eligibility

and diversification of pledged assets. Similarly,

standards are in place stipulating a financing rate

for each type of eligible asset, in other words the

amount of acceptable credit based on the asset’s

market value.

Coverage of credit risk in the form of guarantees

is monitored by the business lines on a day-to-day

basis and by the Risk Management department at a

second level.

AN

NU

AL

RE

PO

RT

20

04

P A G E S 28 29

The above principles are also applied to credit risk

linked to derivatives. This risk is calculated on a lump-

sum determination, taking into account the type of

instrument and its term. These lump-sum amounts

are expressed as a percentage of the nominal or

notional value of the transaction. The “marked to

market plus add-on” approach corresponds to the

valuation of the instrument at the market rate,

which is then increased by a given percentage of the

notional amount.

The Bank may request that collateral be provided,

particularly with regard to transactions initiated by

counterparties other than banks.

3.3.2 Measures of credit risk exposure

The credit risk linked to operations involving primary

financial instruments is measured on the basis of the

book value after deducting any value adjustments.

In the tables below, guarantees received by the bank,

which enable exposure to credit risk to be reduced,

are not taken into account. The system of calculating

counterparty risk with regard to derivative instru-

ments is based on a lump-sum method that takes

into account the type of instrument and its term.

The following lump-sum amounts are applied to the

nominal or notional value to calculate the credit risk

(current risk and potential future risk) on all of the

following transactions :

Currency swaps, forward exchange transactions and CCIRS (Cross Currrency Interest Rate Swap)

- 3% for a remaining maturity of less than 7 days,

- 10% for a remaining maturity of less than 1 year,

- 20% for a maturity of between 1 and 3 years,

- 25% for a maturity of between 3 and 7 years,

- 30% for a maturity of between 7 and 10 years.

Repo transactions- 3% for a remaining maturity of less than 7 days,

- 10% for a remaining maturity of less than 1 year,

- 20% for a maturity of between 1 and 3 years.

Since October 2004 the measure of counterparty risk

on IRS type derivative instruments is calculated by a

method which consists of estimating the fair value of

the outstanding contracts. This form of calculation

replaces the former lump-sum method.

Method1- The fair value of each contract is calculated in

a conservative manner, by taking into account

its most unfavourable value from a set of

simulations. These simulations envisage all the

possible variations of return based on market

movements and volatility.

2- The total fair values of all the contracts with a

given counterparty are aggregated and offset

according to the netting and margin-call con-

tracts signed with the counterparty.

3- The result is then compared to the authorised

limit for the said counterparty.

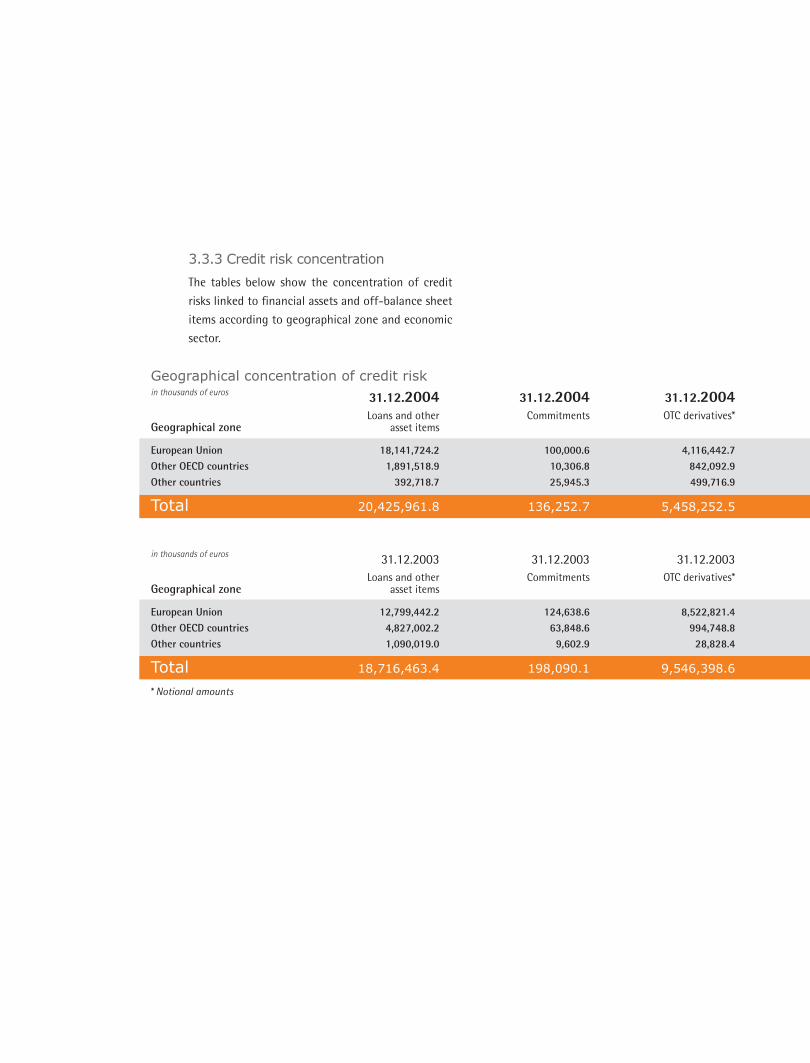

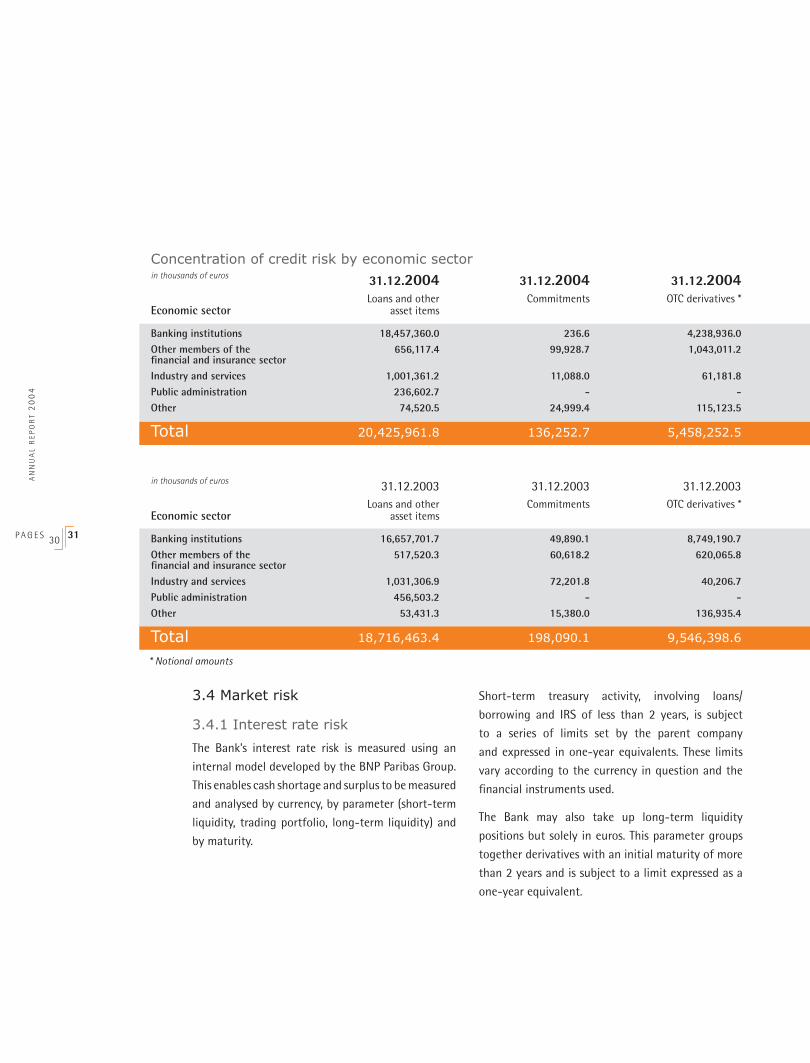

3.3.3 Credit risk concentration

The tables below show the concentration of credit

risks linked to financial assets and off-balance sheet

items according to geographical zone and economic

sector.

Geographical concentration of credit risk in thousands of euros 31.12.2004 31.12.2004 31.12.2004 Loans and other Commitments OTC derivatives* Geographical zone asset items

European Union 18,141,724.2 100,000.6 4,116,442.7Other OECD countries 1,891,518.9 10,306.8 842,092.9Other countries 392,718.7 25,945.3 499,716.9

Total 20,425,961.8 136,252.7 5,458,252.5

in thousands of euros 31.12.2003 31.12.2003 31.12.2003 Loans and other Commitments OTC derivatives* Geographical zone asset items

European Union 12,799,442.2 124,638.6 8,522,821.4Other OECD countries 4,827,002.2 63,848.6 994,748.8Other countries 1,090,019.0 9,602.9 28,828.4

Total 18,716,463.4 198,090.1 9,546,398.6

* Notional amounts

AN

NU

AL

RE

PO

RT

20

04

P A G E S 30 31

3.4 Market risk

3.4.1 Interest rate risk

The Bank’s interest rate risk is measured using an

internal model developed by the BNP Paribas Group.

This enables cash shortage and surplus to be measured

and analysed by currency, by parameter (short-term

liquidity, trading portfolio, long-term liquidity) and

by maturity.

Short-term treasury activity, involving loans/

borrowing and IRS of less than 2 years, is subject

to a series of limits set by the parent company

and expressed in one-year equivalents. These limits

vary according to the currency in question and the

financial instruments used.

The Bank may also take up long-term liquidity

positions but solely in euros. This parameter groups

together derivatives with an initial maturity of more

than 2 years and is subject to a limit expressed as a

one-year equivalent.

Concentration of credit risk by economic sector in thousands of euros 31.12.2004 31.12.2004 31.12.2004 Loans and other Commitments OTC derivatives * Economic sector asset items

Banking institutions 18,457,360.0 236.6 4,238,936.0Other members of the 656,117.4 99,928.7 1,043,011.2financial and insurance sector Industry and services 1,001,361.2 11,088.0 61,181.8Public administration 236,602.7 - -Other 74,520.5 24,999.4 115,123.5

Total 20,425,961.8 136,252.7 5,458,252.5

in thousands of euros 31.12.2003 31.12.2003 31.12.2003 Loans and other Commitments OTC derivatives * Economic sector asset items

Banking institutions 16,657,701.7 49,890.1 8,749,190.7Other members of the 517,520.3 60,618.2 620,065.8financial and insurance sector Industry and services 1,031,306.9 72,201.8 40,206.7Public administration 456,503.2 - -Other 53,431.3 15,380.0 136,935.4

Total 18,716,463.4 198,090.1 9,546,398.6

* Notional amounts

Interest rate positions of a speculative nature and

the foreign exchange position are subject to a VaR

(Value at Risk) calculation using an internal model

developed by the BNP Paribas Group. The VaR

measures the potential variation in current value

of the portfolio for a given time horizon (10 days)

and a given probability level (99%) assuming normal

market conditions.

Each of the limits described above is subject to daily

monitoring by the Risk Management department

which, furthermore, conducts a monthly calculation

of the Bank’s exposure to interest rate risk in exotic

currencies on the basis of worst-case scenarios.

These scenarios simulate the effects of a monetary

crisis lasting two months on the Bank’s short-term

positions in exotic currencies.

Finally, the Bank has set up an Asset and Liability

COmmittee (ALCO) whose task it is to examine the

following aspects on a quarterly basis : liquidity

positions, adherence to credit limits imposed on the

trading room, the Bank’s liquidity policy, the worst-

case scenarios used to test the Bank’s exposure

to interest rate risk in exotic currencies, balance

sheet structure and the investment of capital and

reserves.

3.4.2 Foreign exchange risk

The foreign exchange activity of the Bank involves

the sale of products to customers without the Bank

adopting any positions of its own.

The Bank’s foreign exchange position, expressed

in nominal value, is measured by totalling up the

absolute values of open positions in each currency,

converted into euros. This position is subject to two

limits :

- an intraday limit, defining the maximum foreign

exchange position that may be maintained

throughout the day,

- an overnight limit, of lesser importance, defining

the maximum foreign exchange position that may

be maintained at the end of the day.

The principle of hedging foreign exchange risk pre-

vails with regard to all instruments and portfolios.

The Bank’s foreign exchange position is also subject

to daily calculations of GEaR.

Finally, the Risk Management department is respon-

sible for daily monitoring of foreign exchange risk.

AN

NU

AL

RE

PO

RT

20

04

P A G E S 32 33

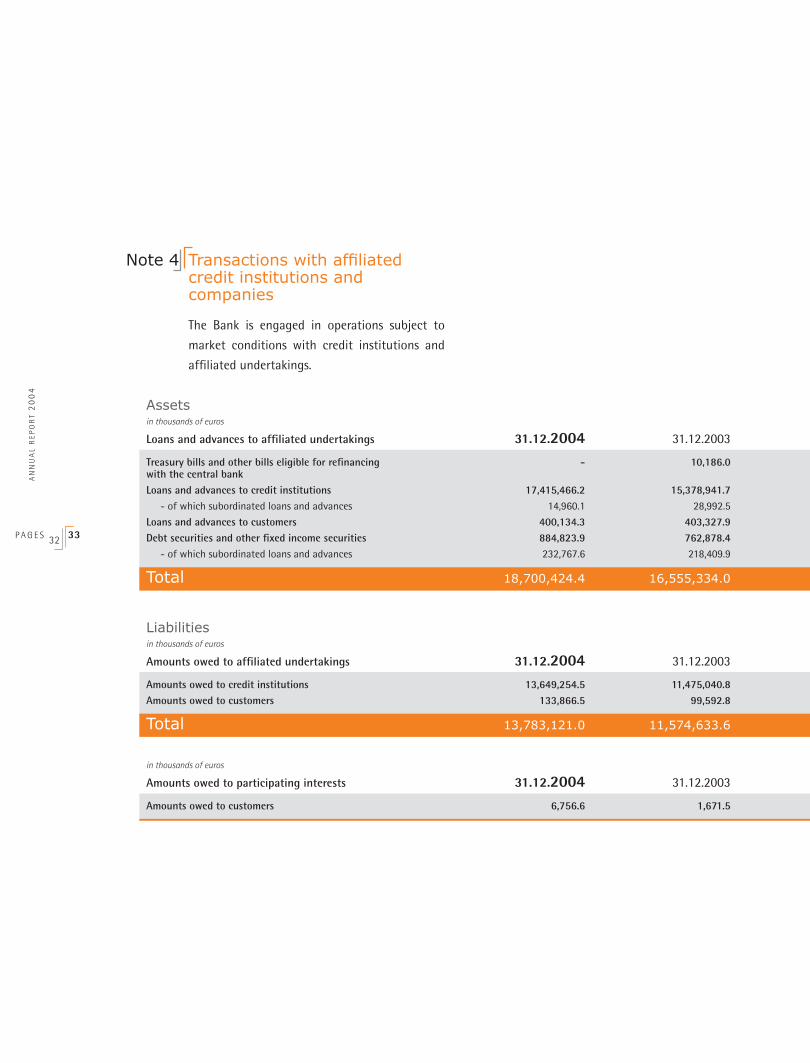

Assets in thousands of euros Loans and advances to affiliated undertakings 31.12.2004 31.12.2003

Treasury bills and other bills eligible for refinancing - 10,186.0with the central bank Loans and advances to credit institutions 17,415,466.2 15,378,941.7 - of which subordinated loans and advances 14,960.1 28,992.5

Loans and advances to customers 400,134.3 403,327.9Debt securities and other fixed income securities 884,823.9 762,878.4 - of which subordinated loans and advances 232,767.6 218,409.9

Total 18,700,424.4 16,555,334.0

Transactions with affiliatedcredit institutions and companies

The Bank is engaged in operations subject to

market conditions with credit institutions and

affiliated undertakings.

Note 4

Liabilities in thousands of euros Amounts owed to affiliated undertakings 31.12.2004 31.12.2003

Amounts owed to credit institutions 13,649,254.5 11,475,040.8Amounts owed to customers 133,866.5 99,592.8

Total 13,783,121.0 11,574,633.6

in thousands of euros Amounts owed to participating interests 31.12.2004 31.12.2003

Amounts owed to customers 6,756.6 1,671.5

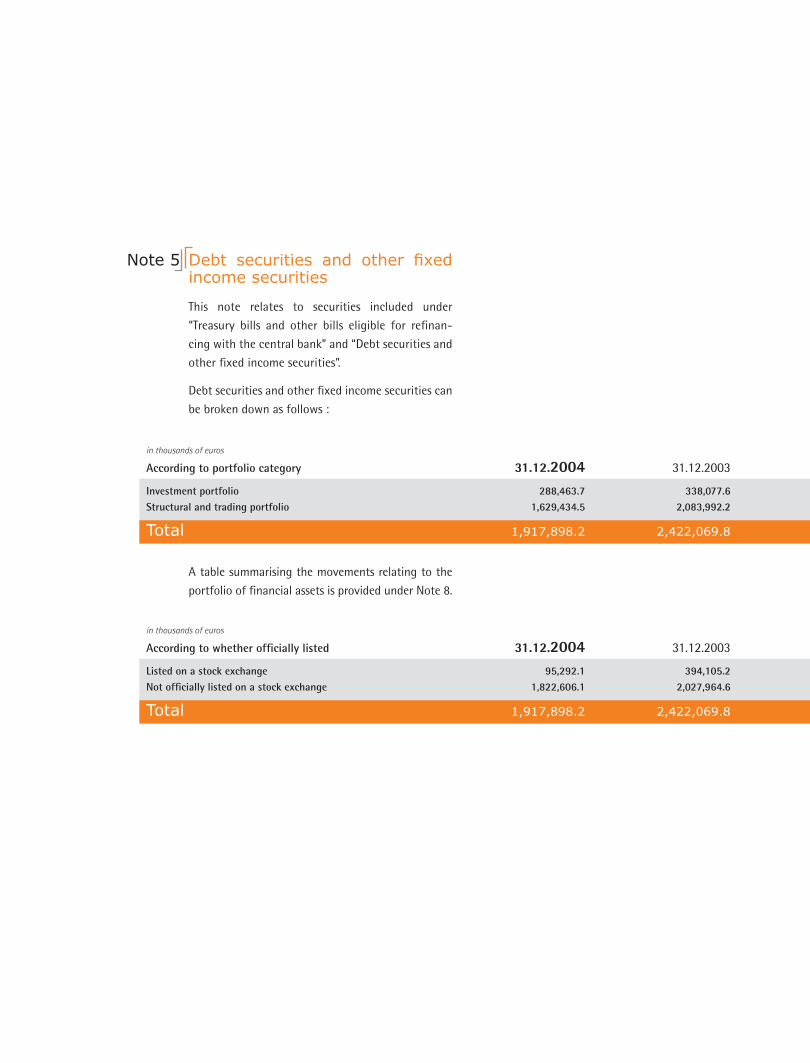

Debt securities and other fixed income securities

This note relates to securities included under

“Treasury bills and other bills eligible for refinan-

cing with the central bank” and “Debt securities and

other fixed income securities”.

Debt securities and other fixed income securities can

be broken down as follows :

Note 5

in thousands of euros According to portfolio category 31.12.2004 31.12.2003

Investment portfolio 288,463.7 338,077.6Structural and trading portfolio 1,629,434.5 2,083,992.2

Total 1,917,898.2 2,422,069.8

A table summarising the movements relating to the

portfolio of financial assets is provided under Note 8.

in thousands of euros According to whether officially listed 31.12.2004 31.12.2003

Listed on a stock exchange 95,292.1 394,105.2Not officially listed on a stock exchange 1,822,606.1 2,027,964.6

Total 1,917,898.2 2,422,069.8

AN

NU

AL

RE

PO

RT

20

04

P A G E S 34 35

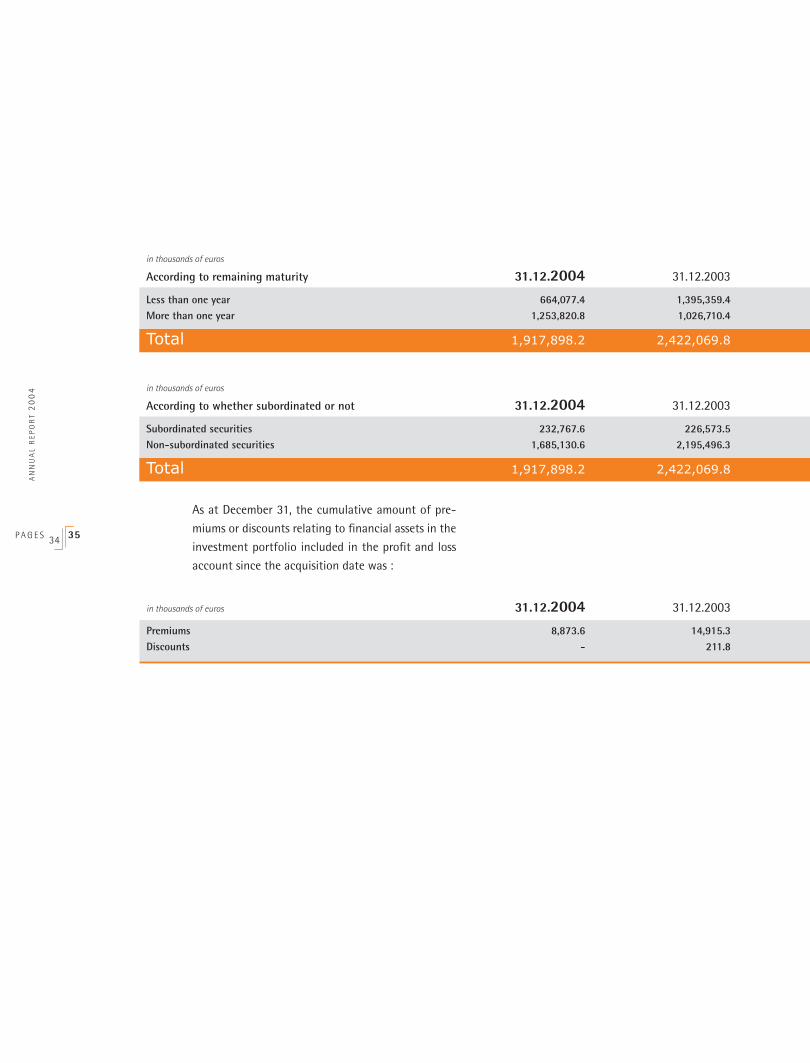

in thousands of euros According to remaining maturity 31.12.2004 31.12.2003