Embed Size (px)

Citation preview

AN

NU

AL

RE

PO

RT

19

99

EU

RO

PE

AN

CE

NT

RA

L B

AN

KE

N

EC

B

EZ

B

EK

T

BC

E

EK

P

A N N U A LR E P O R T

1999

A N N U A LR E P O R T

1999

© European Central Bank, 2000

Address Kaiserstrasse 29

D-60311 Frankfurt am Main

Germany

Postal address Postfach 16 03 19

D-60066 Frankfurt am Main

Germany

Telephone +49 69 1344 0

Internet http://www.ecb.int

Fax +49 69 1344 6000

Telex 411 144 ecb d

All rights reserved.

Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

The cut-off date for the data included in this Report was 7 March 2000.

ISSN 1561-4573

ECB Annua l Repor t • 1999 III

Contents

Foreword 2

Chapter I

Economic development and monetary policy

1 Monetary policy decisions in the context of the Eurosystem’s strategy 8

2 Monetary and financial developments 112.1 Monetary developments 112.2 Financial markets 15

3 Price developments 23

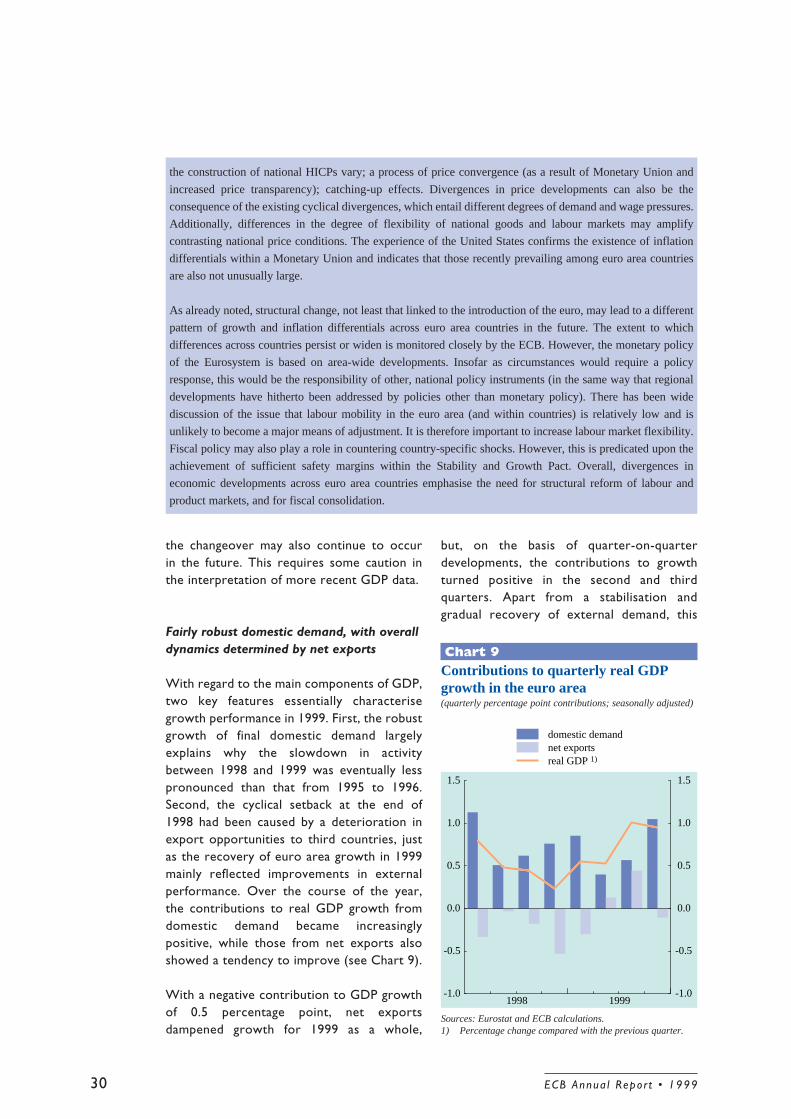

4 Output, demand and labour market developments 28

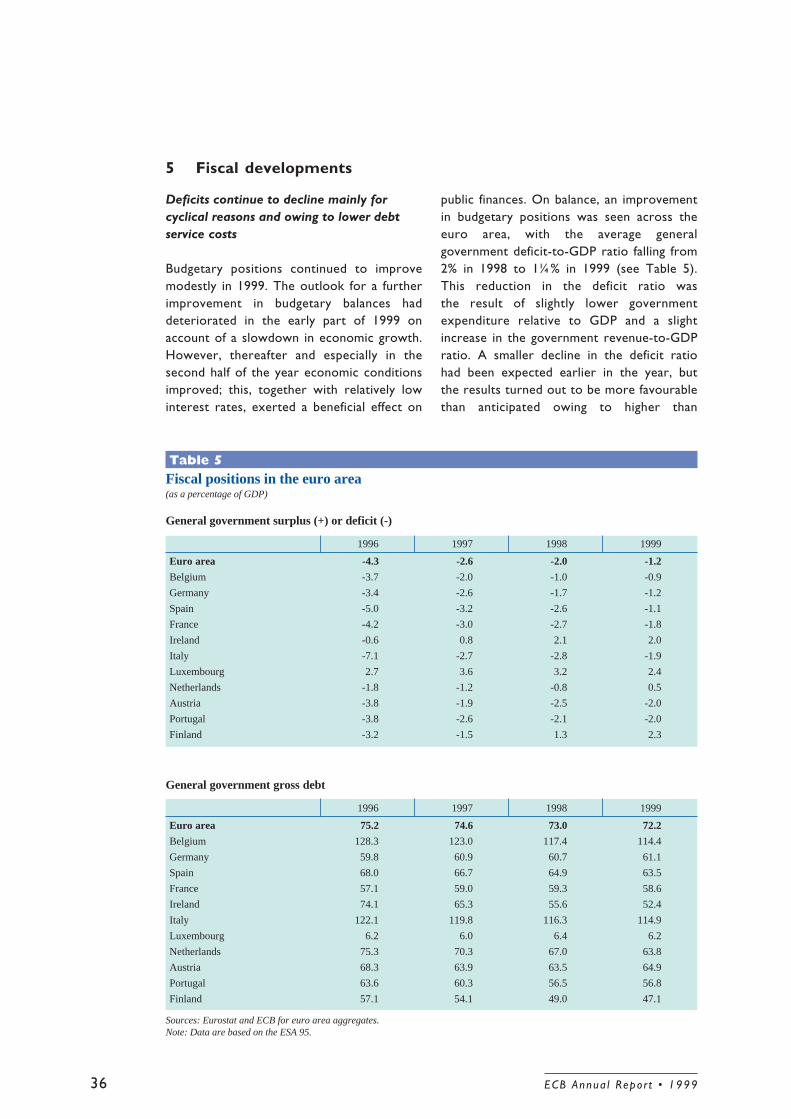

5 Fiscal developments 36

6 The global macroeconomic environment, exchange rates and the balanceof payments 39

Chapter II

Central bank operations

1 Monetary policy implementation 481.1 Liquidity management 481.2 The main refinancing operations 491.3 The longer-term refinancing operations 501.4 Other open market operations 511.5 Standing facilities 511.6 The minimum reserve system 521.7 The Eurosystem’s eligible collateral and its use for credit operations 521.8 Participation of Eurosystem counterparties in monetary policy operations 531.9 Money market developments 54

2 Investment of foreign exchange assets and own funds 542.1 The foreign reserve assets of the Eurosystem 542.2 The Eurosystem’s approach to foreign reserve management 552.3 The ECB’s own funds management 55

3 Payment and settlement systems operations 563.1 The TARGET system 563.2 The correspondent central banking model 58

4 Risk management 59

ECB Annua l Repor t • 1999IV

Chapter III

Economic developments in the other countries of the European Union 64

Chapter IV

European/international co-operation and the Eurosystem

1 European issues 741.1 Bilateral relations 741.2 Co-ordination of national economic policies in the European Union 771.3 Macroeconomic Dialogue 79

2 International issues 802.1 The activities of the ECB in the field of multilateral co-operation 812.2 The development of bilateral relations between the ECB and countries

outside the European Union 842.3 The architecture of the international monetary and financial system 842.4 The international role of the euro 87

Chapter V

Payment and securities settlement systems

1 Oversight of large-value payment systems 92

2 Oversight of retail payment systems 92

3 Other payment systems activities 94

4 Securities settlement systems policy 94

Chapter VI

Financial stability and prudential supervision

1 The institutional framework for financial stability 98

2 Structural changes in the EU banking and financial sector 100

3 Macro-prudential analysis 101

4 Risk assessment systems and credit registers 102

ECB Annua l Repor t • 1999 V

Chapter VII

The production of the euro banknotes and preparationsfor the cash changeover

1 Production of the euro banknotes 106

2 The quality of the euro banknotes and coins 106

3 Protecting the euro banknotes and coins against counterfeiting 107

4 The EURO 2002 campaign 107

5 The changeover to the euro banknotes and coins in 2002 108

6 Cash circulation before 2002 109

Chapter VIII

Development of the statistical framework 114

Chapter IX

Other tasks and activities

1 Advisory functions 120

2 Compliance with the prohibitions on monetary financing and privilegedaccess 121

3 Transition to the year 2000 122

4 The administration of the borrowing and lending operationsby the European Community 125

Chapter X

Public information and accountability

1 The ECB’s information policy and its tools 1281.1 Communication policy objectives 1281.2 Communication tools 128

2 Accountability 1292.1 Central bank independence and accountability in Economic and

Monetary Union 1292.2 The role of the European Parliament in holding the ECB to account 130

ECB Annua l Repor t • 1999VI

Chapter XI

The institutional framework of the Eurosystem andthe European System of Central Banks

1 The Eurosystem and the European System of Central Banks 134

2 The decision-making bodies of the ECB 1352.1 Governing Council 1352.2 The Executive Board 1372.3 The General Council 138

3 The organisation of the ECB 1403.1 Corporate governance 1403.2 Staff developments 1403.3 The organisational chart of the ECB 141

4 ESCB Committees 142

Chapter XII

Annual Accounts of the ECB and Consolidated Balance Sheet of theEurosystem 1999 145

Annexes

Glossary 164Chronology of monetary policy measures of the Eurosystem 176

Documents published by the European Central Bank (ECB) 181

List of Boxes, Tables and Charts

Boxes

1 Structural changes in the banking sector and their relevance for monetary policy 152 Assessing the factors behind the rise in nominal bond yields using index-linked bonds 20

Chart: Break-even inflation rate calculated for the French CPI 203 The effects of market deregulation on consumer prices 25

Chart: Telephone and telefax equipment and services 254 Growth and inflation divergences in the euro area 29

Table: Real GDP growth and HICP inflation in euro area countries 295 The decline in the surplus of trade in goods of the euro area in 1999 44

Chart: Import volumes of major euro area export markets 44

ECB Annua l Repor t • 1999 VII

6 The function and activities of the ECB permanent representation in Washington, D.C. 827 Consultation procedures in 1999 120

Tables

1 Price and cost developments in the euro area 232 Composition of real GDP growth in the euro area 283 Industrial production in the euro area 324 Labour market developments in the euro area 345 Fiscal positions in the euro area 366 Macroeconomic indicators for Denmark 657 Macroeconomic indicators for Greece 678 Macroeconomic indicators for Sweden 699 Macroeconomic indicators for the United Kingdom 7010 Quantity of euro banknotes to be produced by 1 January 2002 110

Charts

1 ECB interest rates and money market rates 92 M3 growth in the euro area 113 Components of M3 in the euro area 124 Loans to the private sector and retail interest rates 145 Short-term interest rates in the euro area 176a Long-term government bond yields in the euro area, the United States and Japan 186b Ten-year interest differential of the United States against the euro area 187 Stock price indices in the euro area, the United States and Japan 228 Breakdown of HICP inflation in the euro area by components 249 Contributions to quarterly real GDP growth in the euro area 3010 Confidence indicators in the euro area 3211 Total employment in the euro area 3312 Unemployment in the euro area 3413 Main developments in major industrialised economies 4114 Nominal effective exchange rate 42

ECB Annua l Repor t • 1999VIII

ECB Annua l Repor t • 1999 IX

Abbreviations

Countries

BE BelgiumDK DenmarkDE GermanyGR GreeceES SpainFR FranceIE IrelandIT ItalyLU LuxembourgNL NetherlandsAT AustriaPT PortugalFI FinlandSE SwedenUK United KingdomJP JapanUS United States

Others

BIS Bank for International SettlementsBPM4 IMF Balance of Payments Manual (4th edition)BPM5 IMF Balance of Payments Manual (5th edition)CDs certificates of depositc.i.f. cost, insurance and freight at the importer’s borderCPI Consumer Price IndexECB European Central BankECU European Currency UnitEMI European Monetary InstituteESA 95 European System of Accounts 1995ESCB European System of Central BanksEU European UnionEUR eurof.o.b. free on board at the exporter’s borderGDP gross domestic productHICP Harmonised Index of Consumer PricesILO International Labour OrganizationIMF International Monetary FundMFIs Monetary Financial InstitutionsNCBs national central banksrepos repurchase agreementsSITC Rev. 3 Standard International Trade Classification (revision 3)

In accordance with Community practice, the EU countries are listed in this Bulletinusing the alphabetical order of the country names in the national languages.

ECB Annua l Repor t • 1999X

Foreword

ECB Annua l Repor t • 19992

This is the first ECB Annual Report coveringa full year of Eurosystem monetary policy. Italso deals with the other activities of theEurosystem and the European System ofCentral Banks.

Looking back on the first year of the euro,there are grounds for experiencing a senseof satisfaction. The single monetary policystarted under reasonably favourableconditions inherited as a result of soundpolicy measures adopted in the run-up tothe introduction of the euro. In addition, theEurosystem’s monetary policy strategyproved to be a valuable tool both for makingmonetary policy decisions and in explainingthese decisions to the general public.Throughout the year, the Eurosystem wastherefore able to focus on maintaining theenvironment of price stability, with inflationrunning on average at just over 1%. The factthat prices could be kept stable in the euroarea is an achievement that should not beunderestimated. An examination of the nottoo distant past should make that clear. Inthe past half century price stability has beenthe exception rather than the rule. TheEurosystem will, therefore, continue toexplain the importance of its primary

objective of maintaining price stability in theeuro area and its monetary policy willcontinue to be conducted with a view toachieving this objective. There are, however,limits to the power of monetary policy. Itcannot, for instance, prevent short-termfluctuations in price developments. Instead,monetary policy must focus on the mediumterm and be assessed from a medium-termperspective. Moreover, monetary policyneeds the support of sound fiscal policies, ofstructural policies that aim to ensure thatmarkets operate efficiently, as well as ofresponsible behaviour on the part of wagenegotiators.

The Eurosystem must act as a single unit andas a truly European body, which means thatdecisions always need to be taken from anarea-wide perspective. Monetary policy is oneand indivisible; it cannot react to situationsin individual countries or regions in the euroarea. In any monetary union of the size of theeuro area it is inevitable that inflation andother economic developments will not becompletely uniform across all the countriesinvolved. The existence of such differences,unless they exceed certain levels, should beseen as normal, as shown by the experiencein other large monetary unions, such as theUnited States. However, should differencesthreaten to become too large, the policyresponse can only be provided nationally, byfiscal policy, structural policies and theadaptability of the markets.

In late 1998 and during the first months of1999 the euro area economy experienced aslowdown in growth at a time when inflationwas already low. The financial crises in Asiaand Russia made themselves felt in Europe. Abroadly based assessment of the outlook forprice developments and the risks to pricestability, the second pillar of our monetarypolicy strategy, on balance pointed to furtherdownward pressure on prices. The first pillarof the strategy, a prominent role for moneywith an analysis of monetary growth relativeto its reference value, showed a rate ofgrowth of M3 of around 5% in early 1999.This was still relatively close to the reference

ECB Annua l Repor t • 1999 3

value of 4½%. It seemed likely that thechangeover to the euro itself had affectedmonetary growth in early 1999. It didnot appear, therefore, that monetarydevelopments in early 1999 implied a risk toprice stability in the medium term. Thus,taking the information of both pillarstogether, the Governing Council of the ECBdecided on 8 April to reduce the ECB’s mainrefinancing rate by 50 basis points, to 2.50%.Following this rate cut, nominal short-terminterest rates in the euro area were athistorically low levels. This contributed to anenvironment in which the growth potentialof the euro area could be exploited withoutendangering price stability.

In the course of 1999 downward risks toprice stability receded and upward risks cameto the fore, with their magnitude graduallyincreasing. The difference between thegrowth of money and its reference valuecontinued to widen, while credit granted tothe private sector grew by an annual rate inexcess of 10%. The liquidity in the euro areawas ample, while ECB interest rates wererelatively low. All these developments wereindicative of upward risks to price stability inthe medium term. At the same time, upwardpressures on prices came from the continuedrise in oil prices and from the depreciation ofthe euro exchange rate in an environmentwhere the economic outlook started tobrighten up. Therefore, both pillars of themonetary policy strategy pointed toincreasing risks to price stability in themedium term. On 4 November 1999 theGoverning Council raised the three mainECB interest rates by 50 basis points.Subsequently, on 3 February and 16 March2000, it was decided to increase theseinterest rates by a further 25 basis points ineach case. The timing of all these movesdemonstrated the forward-looking characterof the Eurosystem’s monetary policy; byacting before risks become reality, latersharper increases in interest rates can beavoided. Rather than nipping economicrecovery in the bud, such policy measurescontribute to creating one of the conditionsfor lasting strong economic growth.

The euro is new and the ECB and theEurosystem are young. Little more than ayear has passed since the euro wasintroduced. The actual introduction of theeuro, including the technical aspects of theprocess, went smoothly. The first few weeksof January 1999 saw the integration of themoney markets in the euro area. Theoperational framework of the Eurosystem,with its use of refinancing operations,standing facilities and a minimum reservesystem with an averaging provision,functioned remarkably well. Overnightinterest rates were generally very stablewithout the need to resort to fine-tuningoperations. The ECB conducted only onefine-tuning operation in early 2000 to mopup some excess liquidity after the successfultransition to the year 2000.

The Eurosystem is naturally taking a keeninterest in developments related to thepossible expansion of the euro area. That iswhy developments in EU Member Stateswhich have not yet adopted the euro areanalysed carefully. The Eurosystem values itswork with these Member States in theGeneral Council of the ECB. The Eurosystemalso closely monitors the process ofaccession of new Member States to theEuropean Union. Ultimately, these countrieshave to fulfil the convergence criteria andcan then adopt the euro. In this context, theEurosystem has established contacts with thecentral banks in all the accession countriesand is ready to contribute to the accessionprocess within its fields of competence.

So far, I have focused mainly on the activitiesof the ECB and the Eurosystem. However,immediately upon its launch the euro startedto have an impact on the financial sector as awhole, the euro area economy in general andthe global monetary system. The euroimmediately became the second mostimportant currency at the global level. Theimpact of the euro is ongoing and willincrease in scope in the years to come. Theeuro will change the euro area economy and,indeed, has already begun to do so. Existingtrends in the financial sector were boosted

ECB Annua l Repor t • 19994

by the launch of the euro. Generally speaking,the role of financial markets in the allocationof financial resources is growing relative tothe role of financial intermediaries. The depthand liquidity of capital markets are increasing.Some segments of the capital market whichhad previously been underdeveloped, such asthe corporate bond market, have grownsignificantly. In general, turnover in thefinancial markets was high, showing that theeuro was well received.

Greater integration of the capital markets isstill possible, and would be helped bymeasures to level the playing-field further.This also applies to the creation of a singlemarket for financial services. The Eurosystemhas, for example, emphasised the fact thatretail payment systems, which reduce thecosts and increase the speed of cross-borderpayments, have to be developed forimplementation no later than the date onwhich the euro banknotes and coins are putinto circulation.

Pressures to restructure mounted in 1999,as also evidenced by high merger andacquisition activity, and not only in thefinancial sector. In the financial sector alltypes of intermediaries and institutions, frombanks to stock exchanges, are affected, asare payment and securities settlementsystems. Although mergers and acquisitionsare often still national in character, this maywell change in the future. The euro stimulatescompetition by enhancing transparency, andcross-border comparisons become simplerwithin the euro area. This has a favourableeffect on the functioning of the Single Marketand thereby ultimately enhances economicwelfare. This process will be given a furtherboost by the introduction of euro banknotesand coins. The introduction of the euro alsoimplies that differences in the quality ofeconomic policies of countries in the euroarea are more easily exposed. This should beseen as an opportunity for governments tolearn from each other and to discover andadopt best practices. Structural changes inthe euro area are carefully monitored andanalysed by the Eurosystem, since they may

have an impact on the way in which and thespeed with which monetary policy measuresaffect the economic process and, in particular,inflation. From a more general perspective,an efficient and sound euro area financialsystem is important, since this also facilitatesthe conduct of monetary policy.

There are also some changes not directlyrelated to the introduction of the euro whichcall for the attention of the Eurosystem. Thedevelopment of electronic money impingeson all major central bank functions: monetarypolicy, the concern to maintain financialstability, banking supervision and theoversight of payment systems. TheEurosystem attaches great importance to theadoption of a sound regulatory frameworkfor issuers of electronic money. As thisAnnual Report goes to press, progress hasbeen made in this area in the European Union,but the current proposals for regulation leaveroom for further improvement. Thisconcerns, in particular, provisions to ensurethat only supervised credit institutions areallowed to issue significant amounts ofelectronic money, that the Eurosystem canextend its monetary policy instruments toissuers of electronic money, and thatelectronic money should always beredeemable at par value.

The transition to the new millennium turnedout to be a non-event, thanks largely to themeticulous preparations in many sectors,including the financial sector and theEurosystem. The euro got off to a good start,but making the euro and Economic andMonetary Union a success is clearly a long-term process. The Eurosystem will play itspart in endeavouring to ensure that success.Work in all the areas mentioned above, andin others, will continue this year and beyond,with a view to further establishing the euroand the Eurosystem, its infrastructure and itspolicy framework.

The economy of the euro area isnow entering a crucial phase. A goldenopportunity to achieve substantial reductionsin the level of unemployment throughout the

ECB Annua l Repor t • 1999 5

euro area and to revitalise the economy isarising, now that economic growth isaccelerating in a climate of price stability.This opportunity can only be seized if policy-makers make the right choices and theprivate sector is confident about the futureand thus dares to take initiatives. Firmlyfocusing on maintaining price stability in themedium term is the best contributionmonetary policy can make to reducingunemployment. At the same time, this wouldfurther enhance the credibility of theEurosystem and boost the confidence ofcitizens that their currency, the euro, willretain its value over time. In line with theStability and Growth Pact, budgetaryauthorities should reduce their budgetdeficits to close to balance, or even create

surpluses. Governments should translatetheir intentions to undertake structuralreforms enabling markets to operate moreflexibly into deeds and build on the measureswhich they have already taken. In wagenegotiations social partners should take intoaccount the importance of maintaining pricestability, the growth of productivity, the needto reduce unemployment and the fact thatdifferent local circumstances requiredifferentiated wage developments; weshould all consider the future as offeringopportunities to bring welfare to Europeancitizens; we should all seize theseopportunities, thereby fostering Europe’sdevelopment into a major dynamic force inthe world economy.

Frankfurt am Main, March 2000

Willem F. Duisenberg

ECB Annua l Repor t • 19996

Chapter I

Economic deve lopmentsand monetary po l i cy

ECB Annua l Repor t • 19998

I Monetary policy decisions in the context of the Eurosystem’sstrategy

In accordance with its statutory obligations,the primary objective of the Eurosystem is tomaintain price stability in the euro area. Inorder to achieve this objective, monetarypolicy decisions are taken in a forward-looking manner based on a stability-orientedstrategy. This strategy was adopted inOctober 1998 (see the article in the January1999 issue of the ECB Monthly Bulletinentitled “The stability-oriented monetarypolicy strategy of the Eurosystem”). Tosummarise, the Governing Council of the ECBannounced a quantitative definition of pricestability, namely an annual increase of below2% in the Harmonised Index of ConsumerPrices (HICP) for the euro area. It was alsostated that price stability is to be maintainedover the medium term. In order to assessthe outlook for price developments and therisks to future price stability, a two-pillarapproach was adopted. The first pillar assignsa prominent role to money, signalled by theannouncement of a reference value for thegrowth rate of a broad monetary aggregate.In December 1998 the reference value wasset at an annual growth rate of 4½% for M3.Monetary developments in relation to thereference value are analysed on an ongoingbasis for the information that they containregarding future price developments over themedium term. In the context of the secondpillar, a broadly based assessment isundertaken of other indicators containinginformation about the outlook for pricedevelopments and the risks to pricestability in the euro area. This assessmentencompasses a wide range of financial marketand other economic indicators, includingforecasts. Against this background, monetarypolicy does not react mechanically todevelopments in a single indicator or forecast.Rather, based on a thorough analysis of theinformation provided by the two pillars of itsstrategy, the Governing Council sets theinterest rates on the monetary policyinstruments of the Eurosystem at the levelwhich will best serve to maintain pricestability in the medium term.

The interest rates on the three mainmonetary policy instruments at the start ofStage Three of Economic and Monetary Union(EMU) were officially announced on22 December 1998. The decision followed aco-ordinated interest rate reduction by thenational central banks, decided upon earlierin December 1998, which had virtuallycompleted the process of convergence of theofficial interest rates in the countries thatnow form the euro area. On 22 December1998 the rate on the first main refinancingoperation to be conducted in 1999 was set at3.0%. In addition, the rate on the marginallending facility was set at 4.5% and that onthe deposit facility at 2.0%, both with effectfrom 1 January 1999. As a temporarymeasure, in order to smooth the transitionto a single money market, the GoverningCouncil of the ECB adopted a “narrowcorridor” for short-term market interestrates from 4 to 21 January 1999 by settingthe interest rates on the marginal lendingfacility and the deposit facility at 3.25% and2.75% respectively (see Chart 1 and thesection entitled “Chronology of monetarypolicy measures of the Eurosystem”).

In the first quarter of 1999 price pressurescontinued to be weak. HICP inflation stoodat 0.8% in December 1998 and remained atthat level in January and February 1999. Inthis environment of low inflation, signsemerged that the extent of the slowdown ofeconomic activity in the euro area – mainlycaused by weaker external demand – mightbe greater than had been anticipated inlate 1998. Figures on real GDP growthpointed to a significant economic slowdown.Furthermore, industrial production growthwas weakening and business confidence wasdeclining continuously. Therefore, it becameincreasingly clear at that time that the risksto price stability in the medium term weremainly on the downside.

However, in assessing the outlook for pricestability, it was also necessary to take into

9ECB Annua l Repor t • 1999

account the fact that some indicatorsappeared to point in the opposite directionin early 1999. In particular, the three-monthaverage of the annual growth rates of M3 forthe period from December 1998 to February1999 was around 5.0%, i.e. somewhat inexcess of the reference value. The Januarymonetary data showed a significant increasein overnight deposits. In addition, credit tothe private sector was growing fast, at a rateof around 10% in early 1999. Furthermore,despite the economic slowdown, consumerconfidence remained comparatively high.Finally, oil prices started to rise as from mid-February 1999 and the euro depreciated ineffective terms in the first few months of1999, two factors which were also able toexert upward pressure on prices.

The Governing Council was therefore facedwith some conflicting signals in early 1999.With regard to monetary developments,however, M3 growth was still close to thereference value of 4½%. In addition, itappeared that the special environmentresulting from the changeover to Stage Threeof EMU had contributed significantly to thesharp increase in overnight deposits inJanuary. The partial reversal in the growthof overnight deposits, which occurred

in February, strengthened this view.Furthermore, it could not be ruled out thatinstitutional factors, such as changes in thestatistical reporting systems and the move tothe new minimum reserve system, had playeda role in the exceptionally strong monetarygrowth in January. Therefore, given theuncertainties surrounding the analysis ofmonetary developments in early 1999 andthe modest deviation from the referencevalue, the Governing Council did not regardmonetary developments as implying upwardrisks to price stability at that time.

All in all, in an environment where currentinflation rates were significantly below the upperlimit of the Eurosystem’s definition of pricestability and in view of downward pressures onfuture price developments associated with aweakening in economic activity, the GoverningCouncil decided on 8 April to reduce the mainrefinancing rate by 50 basis points to 2.5%. Onthe same occasion it lowered the rate on themarginal lending facility by 100 basis pointsto 3.5% and that on the deposit facility by50 basis points to 1.5%, thereby establishing asymmetrical interest rate corridor aroundthe rate on the main refinancing operations.These policy moves were deemed appropriateas a precautionary measure to preserve price

marginal lending ratedeposit ratemain refinancing rate

one-month interest rate (EURIBOR)overnight interest rate (EONIA)

Q1 Q2 Q3 Q4 Q11999 2000

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Chart 1ECB interest rates and money market rates(percentages per annum; daily data)

Sources: ECB and Reuters.

ECB Annua l Repor t • 199910

stability in the medium term and, in doing so,contribute to better exploiting the growthpotential of the euro area economy.

Later on in the year the balance of risksgradually moved from the downside to theupside. The three-month moving average ofthe annual rate of M3 growth followed agradually rising trend, approaching 6.0% overthe summer. Even when excluding theexceptional developments at the verybeginning of 1999, a protracted monetaryexpansion was evident. The annual growthrate of overnight deposits remained high. Inparallel, credit to the private sector continuedto expand rapidly, confirming that liquiditywas ample.

At the same time the external environmentstrengthened as the Asian economiesstabilised and then started to recover, whileconcerns about financial turmoil in otheremerging markets receded. In addition,economic activity in the United States showedcontinuing signs of strength. In thisenvironment, economic activity in the euroarea progressively recovered. The first signsof this process were observed in thesubstantial improvement in businessconfidence over the summer. Industrialproduction stabilised in the second quarterof 1999 and accelerated in the third quarter.The steady increase in bond yields over thesummer also signalled market expectationsof an improvement in long-term economicconditions, as well as some increase ininflation expectations. Overall, it graduallybecame clear that economic activity in theeuro area was set to accelerate significantlyin the course of 1999 and in the year 2000.Moreover, the effective exchange rate of theeuro weakened further and oil pricescontinued to rise, both of which weregradually feeding through to consumer prices.

It was therefore evident that the balance ofrisks to price stability had been progressivelymoving upwards since the beginning of thesummer and that the downside risks whichwere present at the time of the reduction inECB interest rates in April no longer

prevailed. Against this background, theGoverning Council decided on 4 November1999 to raise the rate on the main refinancingoperations by 50 basis points, to 3.0%. Onthe same occasion the rates on the depositfacility and the marginal lending facility werealso raised by 50 basis points, to 2.0% and4.0% respectively.

This change in the stance of monetary policywas expected to prevent the ample liquidityfrom translating into upward pressureson prices over the medium term andto contribute to maintaining inflationexpectations safely below 2%. It was alsoconsidered that such a timely rise in interestrates would contribute to avoiding the needfor stronger measures later on and, hence,would help to sustain non-inflationary growthover an extended period of time. The size ofthe move was also aimed at removinguncertainties about the near-term course ofmonetary policy, thereby contributing toreducing any uncertainty premia potentiallyprevalent in financial markets. In addition, itaimed to help contain a possible increase involatility in money markets in the period oftransition to the year 2000.

At its meeting on 2 December 1999 theGoverning Council reviewed the referencevalue for monetary growth, in accordancewith the announcement it had made inDecember 1998. It was decided to confirmthe reference value for monetary growth,namely an annual growth rate of 4½% for thebroad aggregate M3. This decision was takenon the grounds that the componentsunderlying the derivation of the firstreference value in December 1998, namelythe Eurosystem’s definition of price stability(an annual increase of below 2% in the HICPfor the euro area) and the estimates of trendreal GDP growth (2% to 2½%), as well as thetrend decline in M3 income velocity (½% to1%), had basically remained unchanged.

The Governing Council also decided that, asbefore, monetary developments would beassessed in relation to the reference value onthe basis of a three-month moving average of

11ECB Annua l Repor t • 1999

annual growth rates of M3. Furthermore, itre-emphasised that this assessment would bemade in parallel with the broadly basedassessment of the outlook for pricedevelopments constituting the second pillarof the Eurosystem’s strategy. Monetary policydecisions aimed at the maintenance of pricestability over the medium term would thuscontinue to be based on the informationobtained from both pillars of the strategy.Finally, it was decided henceforth to reviewthe reference value for money on a regularannual basis, with the next review to takeplace in December 2000.

In late 1999 and early 2000 monetary andcredit growth continued to signal ampleliquidity in the euro area. At the same time,

developments in the exchange rate and incommodity prices continued to contribute toincreases in import prices and costs in theeuro area. As such increases were larger andmore protracted than previously foreseen,the risk of second round effects on consumerprices rose significantly, particularly at a timewhen economic activity in the euro area waspicking up strongly. As both of the pillars ofthe monetary policy strategy of theEurosystem were seen to indicate upwardrisks to price stability, the Governing Councilof the ECB decided twice, on 3 February and16 March 2000, to raise the interest rates onthe main refinancing operations, the depositfacility and the marginal lending facility by 25basis points in each case.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 1997 1998 1999

3.0

4.0

5.0

6.0

7.0

3.0

4.0

5.0

6.0

7.0

M3 M3 (three-month centred moving average) reference value (4 1/2%)

Chart 2M3 growth in the euro area(annual percentage changes)

Source: ECB.

2 Monetary and financial developments

2.1 Monetary developments

M3 growth in excess of the reference value

The annual growth rate of the broad monetaryaggregate M3 increased gradually throughout1999. The three-month average of the annual

growth rates of M3, covering the period fromOctober to December, stood at 6.0% (seeChart 2). This compares with 4.8% in the lastquarter of 1998. Accordingly, M3 growthincreasingly deviated from the reference valueof 4½%. On average in 1999 M3 grew by 5.7%,compared with 4.9% in 1998 and 4.1% in 1997.

ECB Annua l Repor t • 199912

The monetary expansion in 1999 was fosteredby the low level of opportunity costs ofholding, in particular, the most liquidcomponents of M3. Moreover, the economicupturn in the euro area is likely to havespurred money demand for transactionpurposes. Furthermore, one-off portfolioreallocations relating to the introduction ofthe euro and the new reserve requirementregime appear to have affected M3 growth atthe beginning of the year. Overall, themonetary expansion reflected ample liquidityfor most of 1999.

Turning to the individual components of M3,the growth of currency in circulationrecovered in 1999, after having been verysubdued in the previous year. In the fourthquarter of 1999 the annual increase ofcurrency in circulation reached 6.4%,compared with only 0.4% in the last quarterof 1998 and 2.7% in the last quarter of 1997(see Chart 3). The economic upswing andthe low opportunity costs of holdingbanknotes may have supported this upwardtrend. In addition, a temporary rise in theprecautionary demand for currency was

recorded shortly before the transition to theyear 2000.

Overnight deposits grew at a very rapid pacein 1999, although the rate of expansionmoderated somewhat in the last part of theyear. In the last quarter of 1999 the annualrate of increase stood at 12.7%, comparedwith 10.6% in the fourth quarter of 1998 and9.3% in the corresponding period of 1997. Asurge in the demand for overnight depositsoccurred in January 1999, reflecting thespecific circumstances prevailing at the startof EMU. In addition, the low levels of inflationand interest rates and the resulting lowopportunity costs of holding overnightdeposits, as well as the economic upswing inthe euro area may explain the relativelystrong demand for overnight deposits in1999.

By contrast, as in previous years, short-termdeposits other than overnight deposits(namely deposits redeemable at a period ofnotice of up to three months and depositswith an agreed maturity of up to two years)showed a rather subdued expansion in 1999.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q41997 1998 1999

-10

-5

0

5

10

15

20

-10

-5

0

5

10

15

20

currency in circulationovernight deposits

other short-term depositsmarketable instruments

Chart 3Components of M3 in the euro area(annual percentage changes)

Source: ECB.

13ECB Annua l Repor t • 1999

In the last quarter of 1999 the annual rate ofincrease was 1.7%, compared with 2.6% inthe fourth quarter of 1998 and 1.1% in thecorresponding period of 1997. The apparentlylow level of attractiveness of these othershort-term deposits for investors may berelated to the fact that the spread betweenthe interest rate on these deposits and thaton overnight deposits narrowed significantlyin the first three quarters of the year andremained comparatively low thereafter.Moreover, the steepening of the yield curvein 1999 may have been accompanied by shiftstowards investments in longer-term financialassets. In addition, in some countries portfolioshifts out of these other short-term depositswere probably related to a significant declinein inflation expectations over recent years.

After having dropped significantly at the endof 1998 and the beginning of 1999, thedemand for the other instruments includedin M3 (negotiable instruments and repurchaseagreements) recovered significantlythroughout 1999. In the last quarter of 1999the annual growth rate stood at 5.2%,compared with 2.5% in the last quarter of1998 and 7.3% in the last quarter of 1997.The recovery in the course of 1999 wasmainly due to a significant increase in thegrowth of both money market fund sharesand debt securities issued with a maturityof up to one year. The demand for thesecomponents may have been temporarilyspurred by uncertainties in financial markets,in particular in late summer and autumn,regarding the future development of bondyields. Under such circumstances short-termmarketable assets, which are relatively liquidand offer a return higher than that ondeposits with an agreed maturity of up totwo years, are often used to park funds forsome time. Moreover the attractiveness ofthese instruments was increased by the risein short-term market rates after the end ofSeptember. Balance of payments statistics forsome euro area countries suggest that thegrowth of money market fund shares andmoney market paper as well as of debtsecurities in 1999 was partly a result ofpurchases of these instruments by non-euro

area residents. Although the concept of M3only refers to monetary holdings of euro arearesidents, statistical limitations do not, at thecurrent stage, permit negotiable securitiesissued by MFIs and held by non-residentsto be identified separately. While thissuggests that some caution should beexercised when interpreting the developmentof these marketable instruments, the overallassessment of monetary growth in 1999 isjudged not to be significantly affected.

In January 2000 the annual rate of M3 growthfell significantly, to 5.0%, from 6.2% inDecember 1999. However, this was mainlythe result of a base effect, i.e. the fact thatowing to the special environment at the startof Stage Three of EMU the monthly increasein M3 in January 1999 was exceptionallystrong.

Strong expansion of credit

Turning to the counterparts of M3 in theconsolidated balance sheet of the MFI sector,the annual rate of expansion of credit tohouseholds and corporations was between10% and 11% for most of the year. Amongthe components of credit to the privatesector, the outstanding amount of loans(which accounts for around 90% of totalcredit to the private sector) grew at an annualaverage rate of 10.0% in 1999 and it continuedto expand strongly in January 2000 (at 8.7%on an annual basis). This compares withannual average growth rates of 8.3% in 1998and 6.6% in 1997. Data on the breakdown ofMFI loans to euro area residents bycounterpart sector, type of loan and originalmaturity indicate that this strong expansionof loans was broadly based across the privatesector.

The dynamic expansion of loans tohouseholds and corporations probably mainlyreflected the low level of bank lending interestrates compared with historical experienceand the pick-up in economic activity in theeuro area. In the first half of the year retaillending interest rates for all types of loans

ECB Annua l Repor t • 199914

continued on the declining trend which hadbeen apparent over previous years (seeChart 4). Subsequently, interest rates onloans for house purchase and longer-termloans to enterprises showed a rising trend,reflecting, with a time-lag, the increase incapital market interest rates which began inMay 1999. Towards the end of 1999 thehigher interest rates in money markets, whichanticipated some tightening in monetarypolicy, led to a moderate increase in banklending rates on consumer loans and short-term loans to enterprises. The fact that thegrowth of loans remained strong despiterising interest rates suggests that the pick-upin economic activity is likely to have playedan important role in sustaining the highgrowth of loans to the private sector in thelatter part of 1999, although there may alsohave been some frontloading of borrowingduring this period owing to expectations onthe part of private agents of further increasesin bank lending rates. Other contributingfactors in 1999 were the intense merger andacquisition activity (see Section 2.2), whichtended to be partly financed by short andmedium-term loans, and the interactionbetween mortgage loans and rapidly rising

real estate prices in some euro areacountries.

The growth of credit to general governmentremained subdued throughout 1999, at anannual average rate of 1.1%. This slow rate ofgrowth occurred both in loans and in MFIholdings of government debt securities andwas in line with the diminished financingneeds of the general government sectorobserved in 1999.

As regards other counterparts of M3, longer-term financial liabilities of the MFI sector grewat a relatively strong pace in 1999 (an annualgrowth rate of 7.3% was recorded in thefourth quarter, compared with 4.7% in thelast quarter of 1998), in line with thesteepening of the yield curve.

Finally, during 1999 the net external assetposition of the MFI sector declinedsignificantly on an annual basis (by€166 billion). The decline mirrored the factthat overall the transactions of euro areanon-MFI residents with non-euro arearesidents resulted in a net outflow of funds.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 1997 1998 1999

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

loans to the private sectorretail rate on loans to enterprises up to one yearretail rate on loans to enterprises over one year

retail rate on consumer creditretail rate on housing loans

Chart 4Loans to the private sector and retail interest rates(loans: annual percentage changes; interest rates in percentages per annum)

Source: ECB.

15ECB Annua l Repor t • 1999

2.2 Financial markets

Rapid growth of corporate financingthrough debt securities issuance

The start of Stage Three of EMU has acted asa catalyst for the development and integrationof the euro area capital markets towards apan-European capital market.

With regard to the euro-denominated bondmarket, the most significant development in1999 was undoubtedly the rapid growth ofthe private or corporate bond market, whichsurpassed the expectations of many observersprior to the launch of the euro. This marketgained momentum with the launch of largedebt securities issues which were related toa number of sizeable mergers and acquisitionsin the first half of 1999. The rather smooth

Box 1Structural changes in the banking sector and their relevance for monetary policy

Developments in the competitive environment of financial services and the related structural developments in

the banking sector are of relevance for the single monetary policy. In the past, banks in the euro area have been

the main providers of financial services in rather fragmented and sheltered domestic markets. However, as

barriers between various domestic or local markets have been reduced, banks are facing more competition

from one another as well as from other providers of financial services. These changes in the competitive

environment have resulted in pressure for banks to become more efficient and have prompted initiatives to

maintain competitive positions, one manifestation of which is the merger and acquisition activity, which has

gathered pace significantly over the past few years. This pattern of restructuring and consolidation continued

in 1999. In particular, the number of large institutions involved in bank mergers was relatively high throughout

1999.

The main driving forces behind this trend towards restructuring and consolidation in the euro area banking

sector are technological developments, globalisation, deregulation and increased demand for sophisticated

financial services, with the introduction of the euro appearing to have acted as a catalyst for these forces.

Indeed, these driving forces are seen to be reshaping the market so that financial services should become more

competitive and also more integrated both within the euro area and at the global level.

However, most of the merger and acquisition activity in the euro area banking sector has not so far taken place

across national borders within the euro area. The focus on national mergers may be explained by an incentive

to improve efficiency by removing overlapping operations as well as by defensive strategies. In addition,

issues related to cultural proximity and expectations that mergers and acquisitions at the national level are

more manageable than cross-border mergers also seem to play an important role. This national orientation

towards mergers and acquisitions has given rise to some concerns about the increased market shares of the

largest domestic institutions. However, while some adverse effects on competition at the local level cannot be

ruled out in the short term, the main picture emerging in respect of the financial services market seems to be

one of increased competition and reduced fragmentation in the long term.

These changes in the competitive conditions in the banking market, as well as the possible effects on the

financial strength of the banking sector, may be of relevance for the transmission mechanism of monetary

policy. First, the speed of monetary policy transmission may be enhanced, as banks in more competitive

markets tend to adjust their retail interest rates more rapidly in response to changes in market rates. Second,

the relative importance of the credit channel of monetary policy may be altered as a result of changes in

relationships between banks and their clients, which are particularly relevant for the financing of small

businesses and households. Finally, increased competition in the euro area would tend to speed up the move

towards a more integrated banking system across participating countries, which could reduce cross-country

asymmetries in the transmission mechanism of monetary policy.

ECB Annua l Repor t • 199916

and rapid way in which the euro-denominatedcorporate bond market proved able toabsorb these issues was widely regarded asan important sign of the increased depth ofthis market. In particular, the issuance ofeuro-denominated debt securities by privatenon-financial corporations and private utilitycompanies increased in 1999 compared with1998. According to commercial data sources,the largest private issuers of debt securitiesin 1999 were banks, which accounted forthe bulk of total private sector issuancevolume, followed respectively by non-financialcorporations, other financing companiesand utility companies. Taking a globalperspective, the growth of net issuance ofeuro-denominated debt securities during1999 was particularly strong when comparedwith US dollar denominated debt securitiesissuance. Yen-denominated issuance alsoexperienced a strong recovery in 1999 whencompared with 1998.

One of the most important factors behindthe growth in the euro-denominatedcorporate bond market has been the ongoingprocess of corporate restructuring in Europe,which has resulted in a strong demand forfunds in the private corporate sector. Ingeneral, merger and acquisition activitiesundertaken by euro area companies grewconsiderably in 1999, for both the bankingand the non-banking industry (see Box 1).Euro area companies involved in merger andacquisition activities and operations such asleveraged buyouts – in which the takeover ofa company is financed through the issuanceof high-yield bonds – financed these deals, toa significant extent, with large euro-denominated debt securities issues, whichoften served to repay bridging facilities(mainly syndicated loans). This led to somevery large issues, unprecedented in thehistory of European capital markets. Thesignificant growth in private euro-denominated debt securities issuance wasaccompanied by a reduction in the relativeimportance of the public sector in the debtsecurities markets in 1999, which alsoreflected the relatively smaller increases inthe financing needs of the public sector in

1999 compared with previous years. Inaddition, a shift in demand towards higherrisk securities in order to obtain higherreturns owing to the historically low levels ofinterest rates also seemed to play asupportive role in the growth of corporatedebt securities issuance.

As discussed in the article in the January 2000issue of the ECB Monthly Bulletin entitled“The euro area one year after theintroduction of the euro: key characteristicsand changes in the financial structure”, therewere a number of notable developments inthe euro area capital markets during 1999.These included closer co-operation betweennational stock exchanges and thedevelopment of electronic trading platformsin both bond and stock markets.

Money market rates mirroring ECB interestrates

In 1999 the ECB managed to steer short-term money market rates by means of theinterest rate which was applied to the mainrefinancing operations. The overnight interestrate, as measured by the EONIA (the “euroovernight index average”), was generally veryclose to the rate applied to the mainrefinancing operations, the average spreadbetween the two rates being equal to 3 basispoints in 1999 (see Chart 1). The volatility ofthe EONIA rate was relatively low. Somewhatlarger fluctuations were normally onlyrecorded towards the end of the reservemaintenance periods, which is when theminimum reserve constraint on the bankingsystem becomes binding. In view of the steadypattern of the EONIA rate, the ECB saw noneed to conduct fine-tuning open marketoperations in the course of 1999.

Other money market rates were equallystable, apart from episodes when marketparticipants anticipated a move in ECBinterest rates or, towards the end of theyear, when short-term interest rates rose onaccount of market concerns related to thetransition to the year 2000.

17ECB Annua l Repor t • 1999

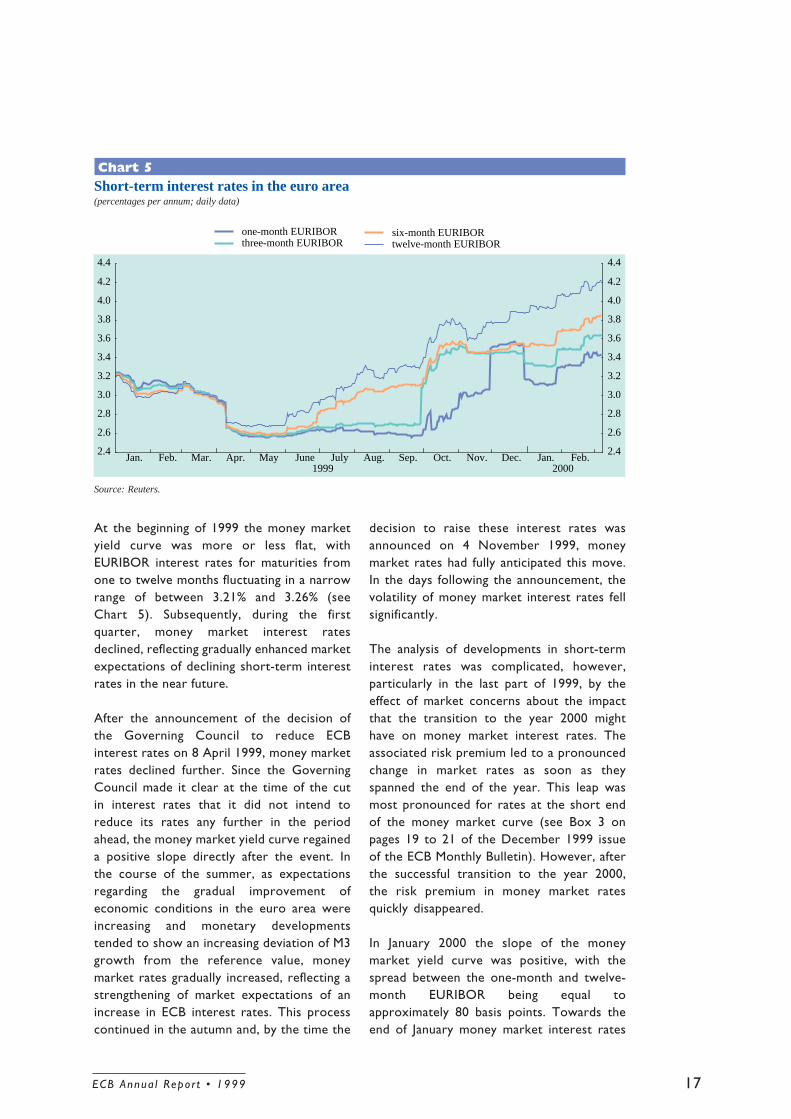

At the beginning of 1999 the money marketyield curve was more or less flat, withEURIBOR interest rates for maturities fromone to twelve months fluctuating in a narrowrange of between 3.21% and 3.26% (seeChart 5). Subsequently, during the firstquarter, money market interest ratesdeclined, reflecting gradually enhanced marketexpectations of declining short-term interestrates in the near future.

After the announcement of the decision ofthe Governing Council to reduce ECBinterest rates on 8 April 1999, money marketrates declined further. Since the GoverningCouncil made it clear at the time of the cutin interest rates that it did not intend toreduce its rates any further in the periodahead, the money market yield curve regaineda positive slope directly after the event. Inthe course of the summer, as expectationsregarding the gradual improvement ofeconomic conditions in the euro area wereincreasing and monetary developmentstended to show an increasing deviation of M3growth from the reference value, moneymarket rates gradually increased, reflecting astrengthening of market expectations of anincrease in ECB interest rates. This processcontinued in the autumn and, by the time the

decision to raise these interest rates wasannounced on 4 November 1999, moneymarket rates had fully anticipated this move.In the days following the announcement, thevolatility of money market interest rates fellsignificantly.

The analysis of developments in short-terminterest rates was complicated, however,particularly in the last part of 1999, by theeffect of market concerns about the impactthat the transition to the year 2000 mighthave on money market interest rates. Theassociated risk premium led to a pronouncedchange in market rates as soon as theyspanned the end of the year. This leap wasmost pronounced for rates at the short endof the money market curve (see Box 3 onpages 19 to 21 of the December 1999 issueof the ECB Monthly Bulletin). However, afterthe successful transition to the year 2000,the risk premium in money market ratesquickly disappeared.

In January 2000 the slope of the moneymarket yield curve was positive, with thespread between the one-month and twelve-month EURIBOR being equal toapproximately 80 basis points. Towards theend of January money market interest rates

Jan. Feb. Mar. Apr. May June July Aug. Sep. Oct. Nov. Dec. Jan. Feb.1999 2000

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

one-month EURIBORthree-month EURIBOR

six-month EURIBORtwelve-month EURIBOR

Chart 5Short-term interest rates in the euro area(percentages per annum; daily data)

Source: Reuters.

ECB Annua l Repor t • 199918

moved upwards, in anticipation of thedecision to raise ECB interest rates whichwas announced on 3 February 2000. In thecourse of February, money market interestrates gradually increased further.

Long-term bond yields increase fromhistorical lows as growth prospects brighten

Following the prolonged decline in long-terminterest rates which was observed inindustrialised countries throughout much ofthe 1990s, long-term government bond yieldsin the euro area reached their lowest levelsfor the past 50 years in early 1999 (seeChart 6(a)). From May 1999 onwards,however, they began to edge upwards, initiallyled by bond yield increases in the UnitedStates and by an increase in inflationexpectations from the very low levelsprevailing in early 1999, but later onincreasingly due to brighter economicprospects for the euro area. Overall, in theeuro area, ten-year bond yields increased bymore than 150 basis points in 1999, reachinga level of around 5.5% by the end of the year.Similarly, in the United States the ten-yearbond yield rose by around 180 basis points,to around 6.5%, in 1999. As a result of thesedevelopments the spread between US andeuro area ten-year bond yields widenedslightly during 1999, reaching 100 basis pointsby the end of the year. In Japan developmentsin long-term bond yields differed somewhatfrom the euro area and the United States.Following initial declines from the relativelyhigh levels reached in the aftermath of thefinancial turbulence in late 1998, Japaneselong-term yields seemed to stabilise at a levelbelow 2% in the second half of 1999. Betweenthe end of 1998 and the final trading day of1999, the ten-year bond yield in Japandeclined by approximately 40 basis points, toaround 1.6%.

The main factor underlying developments inglobal bond markets in 1999 was a pick-up inworldwide growth expectations as concernsof a prolonged global growth downturn,which had existed in the financial markets as

Source: Reuters.Note: Long-term government bond yields refer to ten-year bondsor to the closest available bond maturity.

Chart 6

(a) Long-term government bond yields in theeuro area, the United States and Japan(percentages per annum; daily data)

(b) Ten-year interest rate differential of the UnitedStates against the euro area(percentages per annum; daily data)

1995 1996 1997 1998 19990.0

2.0

4.0

6.0

8.0

10.0

0.0

2.0

4.0

6.0

8.0

10.0

euro area United States Japan

1995 1996 1997 1998 1999-3.0

-2.0

-1.0

0.0

1.0

2.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

a result of the financial turbulence of 1998,began to recede. The US economy continuedto grow at a remarkable pace throughout1999 and, although there were few visiblesigns of rising inflation, the increasingtightness in the labour market resulted ingrowing concerns in financial markets thatthe US economy was growing at a rate thatmight lead to inflationary pressures in the

19ECB Annua l Repor t • 1999

economy. To a large extent, thesedevelopments contributed to the substantialincrease in US long-term bond yieldswitnessed throughout 1999. In addition,although a further improvement in the fiscalsituation in the United States may havereduced the pressures on capital marketsfrom the public sector, a sizeable increase incorporate bond issuance in the United Statesduring the year may have placed upwardpressure on US bond yields.

By contrast with developments in the UnitedStates, long-term bond yields in the euro arearemained broadly stable in the first fourmonths of 1999, reflecting the more sluggishpace of economic recovery and the subduedinflationary pressures in the euro area whichwere reflected in the decision of theGoverning Council of the ECB to lowerinterest rates in April. Apart from theaforementioned spillover effect of thecontinued rise in US bond yields, it seemslikely that part of the gradual increase inbond yields as from May resulted from theunwinding of the safe-haven portfoliopositions that had been built up during 1998,as well as an increase in inflation expectationsfrom the very low levels prevailing in early1999 in the wake of the financial turbulenceof the previous year. Developments in thepricing of French index-linked bonds at thistime appeared to be consistent with thosefactors behind the increase in nominal bondyields (see Box 2). In addition, as was thecase in the United States, a significant increasein the level of corporate bond issuanceactivity in the euro area may have put upwardpressure on long-term bond yields. However,the increase in euro area bond yields in Mayand the first half of June 1999 was much lesspronounced than in the United States,reflecting differences in cyclical positions,leading to a substantial widening of the long-term interest rate differential vis-à-vis theUnited States up to a maximum level ofalmost 160 basis points in mid-June. Later on,as increasing signs of an economic recoveryin the euro area appeared, the spreadbetween US and euro area long-term bondyields narrowed rapidly (see Chart 6(b)).

Until the end of October 1999 long-termbond yields in the euro area continued tofollow an upward trend. As from the end ofOctober, growing expectations in capitalmarkets that ECB interest rates were to beraised in a context of increasing evidence ofupward price pressures, and the subsequentdecision on 4 November, temporarily led tosignificant declines in long-term bond yields.This seemed to suggest that, as a result ofthe decision to raise interest rates, marketparticipants had revised their long-terminflation expectations downwards andlowered the magnitude of the inflation riskpremium required for holding euro-denominated bonds. However, during theremainder of 1999 euro area bond yieldsedged up again, partly following upwardmovements in long-term yields in the UnitedStates and partly in response to furtherpositive news regarding the outlook for theeuro area economy. As a result of the morepronounced increases in US bond yields, theyield differential vis-à-vis the United Statesbegan to increase again in November andDecember.

The developments described above were alsoreflected in movements in the euro area yieldcurve throughout 1999. Between the firstand the last trading day of 1999 the slope ofthe yield curve, as measured by the differencebetween ten-year euro area bond yields andthe three-month EURIBOR interest rate,increased by around 140 basis points to 215basis points. The main part of this increasetook place during the first nine months of1999. Since the yield curve typically becomessteeper in advance of a pick-up in the pace ofeconomic activity, the observed steepeningof the euro area yield curve in 1999 seemedmainly to reflect increasing optimism on thepart of market participants about futureeconomic prospects and an increase ininflation expectations from the very low levelsprevailing in early 1999. However, cautionshould be exercised when interpreting overallyield curve movements, as other factors, suchas the unwinding of safe-haven portfoliopositions and spillovers from US bondmarkets may also have influenced long-term

ECB Annua l Repor t • 199920

Box 2Assessing the factors behind the rise in nominal bond yields using index-linkedbonds

In order to assess how various underlying factors may have influenced nominal long-term bond yields in the

euro area in 1999, it is useful to remember that, broadly speaking, the nominal yield on a government bond

with a specified time to maturity can be broken down into three elements. These are the real interest rate

required by investors for holding the bond until it matures, compensation for the average expected inflation

rate during the life of the bond, and a component associated with term or risk premia linked to, inter alia,

uncertainty about future rates of inflation. The yield on index-linked bonds can assist in producing this

breakdown. The differential between a long-term bond yield and the real yield available on an index-linked

bond of the same maturity is generally known as the “break-even” inflation rate. This is because with this rate

of inflation, the expected return to an investor will be the same regardless of whether the investment is made in

a fixed nominal income or an index-linked bond.

However, the break-even inflation rate is not a direct measure of inflation expectations because it does not take

into account the role of various risk premia. On the one hand, the break-even rate tends to over-estimate

expected inflation since the yield on the nominal bond usually contains an inflation risk premium. On the other

hand, the lower level of liquidity that usually characterises index-linked bond markets implies that the real

yield on index-linked bonds may incorporate a liquidity premium. The only index-linked bonds that exist in

the euro area were issued by the French Treasury with 10-year and 30-year maturities. The break-even

inflation rate of these bonds refers to a specific measure of the French Consumer Price Index (CPI), namely

the CPI excluding tobacco, and does not refer to the euro area HICP. These properties illustrate the limitations

of this indicator for evaluating developments in the euro area.

Nevertheless, bearing these caveats in mind, developments in 1999 in the pricing of ten-year index-linked

bonds issued by the French Treasury provided some indications that both improved growth expectations and

changes in inflation expectations may have played important roles in determining movements in nominal

long-term interest rates during the year. Between the end of 1998 and the end of 1999 the real interest rate

available on the ten-year French index-linked bond increased by around 50 basis points. At the same time, the

Break-even inflation rate calculated for the French CPI(in percentages; daily data)

Sources: French Treasury, ISMA and Reuters.Note: The real bond yields are derived from the market prices of French bonds which are indexed to the French CPI (excludingtobacco) and mature in 2009. The nominal bond yields are derived from the market prices of French fixed income bonds whichalso mature in 2009.

Q4 Q1 Q2 Q3 Q4 Q11999 20001998

0

1

2

3

4

5

6

0

1

2

3

4

5

6

break-even inflation rate nominal bond yield real bond yield

21ECB Annua l Repor t • 1999

ten-year break-even inflation rate increased by approximately 110 basis points from the extraordinarily low

levels observed in early 1999, at a time when risks to price stability were perceived to be mainly on the

downside (see the chart above).

It is worth noting that the rise in the real yield and the increase in the break-even inflation rate occurred during

different periods of 1999. While the break-even inflation rate increased steadily in the second quarter and

levelled off after June, the real interest rate increased mainly in the second half of the year. This suggests that

the increases in nominal euro area bond yields were initially attributable more to inflation expectations

increasing from very low levels than to increasing real rates. However, the unwinding of the safe-haven

portfolio positions from emerging markets that had been built up during 1998 might also help to explain part

of the increase in long-term interest rates in the first half of 1999, since they may have artificially compressed

the break-even inflation rates prevailing in the early months of 1999. Spillovers from rising bond yields in the

United States may, at times, also have played a role in this rise in break-even inflation rates in the first half of

1999. Later on, as more and more signs of an economic recovery appeared, the rise in nominal bond yields

related more to increasing long-term real interest rates, while the break-even inflation rate remained stable.

interest rate developments in the euro areain 1999.

In the first half of January 2000 euro areabond yields showed some limited increases,mainly as a result of spillovers coming fromUS bond markets, where yields rosesignificantly. Subsequent to this, bond yieldsin the euro area remained broadly stable forthe rest of January and throughout thefollowing month. At the same time, thedifferential between euro area and US long-term interest rates was somewhat volatileand did not exhibit any discernible trend inearly 2000.

Global stock prices increase significantly

In 1999 stock prices in industrialisedeconomies showed large increases, continuingthe upward trend observed over previousyears (see Chart 7). A very large increasewas seen in the euro area, where by the endof December 1999 the Dow Jones EUROSTOXX index stood 40% above end-1998levels. In the United States, by the end ofDecember 1999 the Standard and Poor’s 500index was 19% above end-1998 levels, whilein Japan a significant increase of 37% was alsoobserved for the Nikkei 225 index. The mainfactor underlying developments in globalstock markets during 1999 seemed to have

been improving market assessments of futureglobal growth prospects.

Throughout most of 1999 the evolution ofglobal stock market developments provideda supportive environment for stock pricedevelopments in the euro area. The principalsource of the increase in US stock pricesseemed to be favourable expectations offuture corporate earnings growth, linked tothe robust pace of activity in the US economy.In particular, optimism about the long-termearnings growth prospects for high-technology firms played an important role.Against this background, the NasdaqComposite index (which contains a highproportion of technology stocks) increasedby 86% in 1999.

Japanese stock prices appeared to benefitfrom increasing optimism about the prospectsfor future corporate earnings growth linkedto a recovery in the Japanese economyparticularly during the first half of 1999,before stabilising in the second half of 1999.At the same time the decline in long-termgovernment bond yields in Japan seemed tohave played a supportive role in the increasein Japanese stock prices, as did thedepreciation of the Japanese yen vis-à-vis theUS dollar during the first half of 1999,particularly with regard to the stock pricesof export-oriented companies.

ECB Annua l Repor t • 199922

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q11997 1998 1999

40

60

80

100

120

140

160

40

60

80

100

120

140

160

euro area United States Japan

Stock prices in the euro area remained relativelysubdued in the first few months of 1999,reflecting the sluggish pace of economicrecovery in the euro area. Later on, asexpectations regarding the pace of future activitybegan to improve, stock prices in the euro areastarted to edge upwards. The resilience of thisincrease to the parallel increases in long-termbond yields in the euro area was notable andappeared to indicate strong underlyingexpectations for corporate profitability anddividend growth in the euro area. Theimprovement in stock prices was initially moreapparent for those firms with a higher degreeof exposure to the external economicenvironment than in the stock prices of firmswith a more domestic orientation. To the extentthat larger firms tend to have a higher degreeof exposure to the external economicenvironment, this was indicated by the strongerperformance of the Dow Jones EURO STOXX50 index, which is composed of largecorporations, compared with that of the broadDow Jones EURO STOXX index.

In the second half of 1999, as marketparticipants became more optimistic with

regard to the prospects for domestic demandgrowth in parallel with improvements inbusiness and consumer confidence, stockprice increases became more broadly basedacross the different sectors of the economy.Towards the end of the year, particularlyafter mid-October, relatively sharp stockprice increases were seen in the technologyand telecommunications sectors. In thesesectors, by the end of 1999, stock prices hadincreased by 134% and 105% respectivelycompared with the end of 1998, whichcontributed significantly to aggregate euroarea stock price increases. Increases in thetechnology and telecommunications sectorsseemed to be partly linked to favourableprofit growth expectations followingcorporate restructuring and mergers andacquisitions activity in these sectors andsignificant expansion of the internet business.

In the period from end-1999 to 7 March 2000contrasting developments were seen ininternational stock markets. While stockprices in the United States, as measured bythe Standard and Poor’s 500 index, declinedby 8%, in Japan the Nikkei 225 index rose by

Chart 7Stock price indices in the euro area, the United States and Japan(1 January 1999 = 100; daily data)

Source: Reuters.Note: Dow Jones EURO STOXX broad (stock price) index for the euro area, Standard and Poor’s 500 for the United States andNikkei 225 for Japan.

23ECB Annua l Repor t • 1999

5%, while in the euro area the Dow JonesEURO STOXX index rose by 11%. Continuingthe trend that became evident in the lattermonths of 1999, stock prices in thetechnology sector of the euro area rose by36% during this period and made a significant

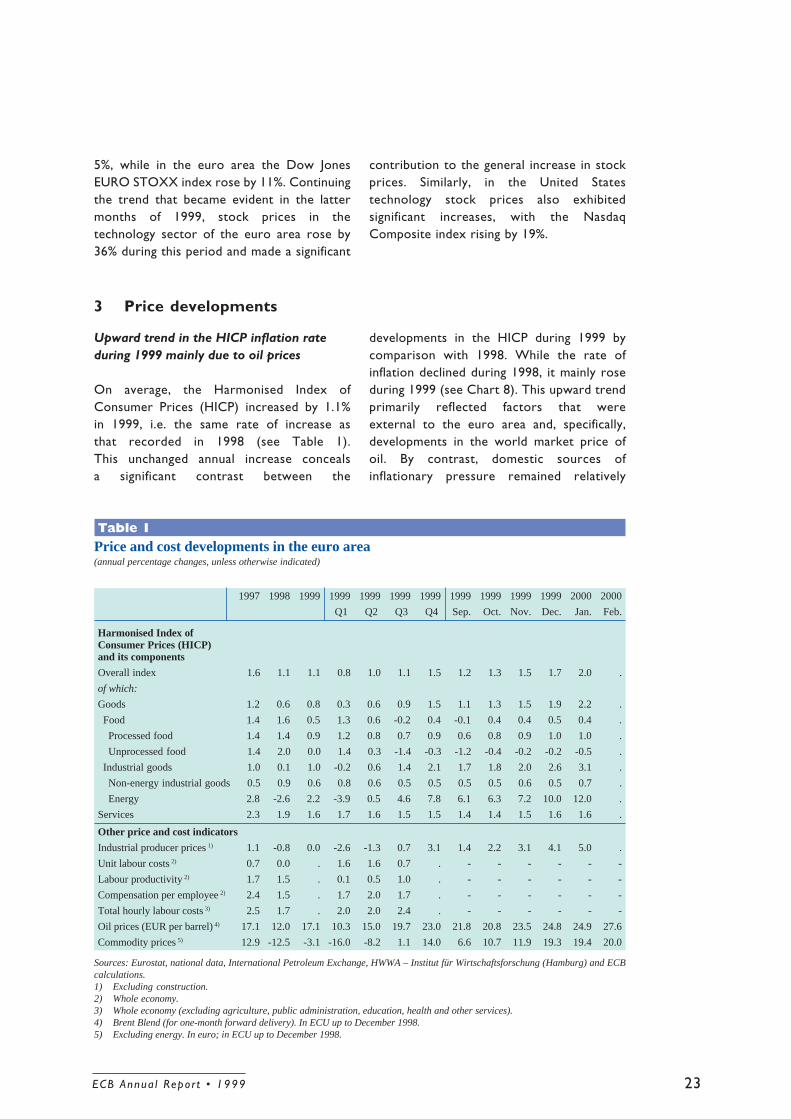

3 Price developments

Upward trend in the HICP inflation rateduring 1999 mainly due to oil prices

On average, the Harmonised Index ofConsumer Prices (HICP) increased by 1.1%in 1999, i.e. the same rate of increase asthat recorded in 1998 (see Table 1).This unchanged annual increase concealsa significant contrast between the

developments in the HICP during 1999 bycomparison with 1998. While the rate ofinflation declined during 1998, it mainly roseduring 1999 (see Chart 8). This upward trendprimarily reflected factors that wereexternal to the euro area and, specifically,developments in the world market price ofoil. By contrast, domestic sources ofinflationary pressure remained relatively

contribution to the general increase in stockprices. Similarly, in the United Statestechnology stock prices also exhibitedsignificant increases, with the NasdaqComposite index rising by 19%.

1997 1998 1999 1999 1999 1999 1999 1999 1999 1999 1999 2000 2000

Q1 Q2 Q3 Q4 Sep. Oct. Nov. Dec. Jan. Feb.

Harmonised Index ofConsumer Prices (HICP)and its components

Overall index 1.6 1.1 1.1 0.8 1.0 1.1 1.5 1.2 1.3 1.5 1.7 2.0 .

of which:

Goods 1.2 0.6 0.8 0.3 0.6 0.9 1.5 1.1 1.3 1.5 1.9 2.2 .

Food 1.4 1.6 0.5 1.3 0.6 -0.2 0.4 -0.1 0.4 0.4 0.5 0.4 .

Processed food 1.4 1.4 0.9 1.2 0.8 0.7 0.9 0.6 0.8 0.9 1.0 1.0 .

Unprocessed food 1.4 2.0 0.0 1.4 0.3 -1.4 -0.3 -1.2 -0.4 -0.2 -0.2 -0.5 .

Industrial goods 1.0 0.1 1.0 -0.2 0.6 1.4 2.1 1.7 1.8 2.0 2.6 3.1 .

Non-energy industrial goods 0.5 0.9 0.6 0.8 0.6 0.5 0.5 0.5 0.5 0.6 0.5 0.7 .

Energy 2.8 -2.6 2.2 -3.9 0.5 4.6 7.8 6.1 6.3 7.2 10.0 12.0 .

Services 2.3 1.9 1.6 1.7 1.6 1.5 1.5 1.4 1.4 1.5 1.6 1.6 .

Other price and cost indicators

Industrial producer prices 1) 1.1 -0.8 0.0 -2.6 -1.3 0.7 3.1 1.4 2.2 3.1 4.1 5.0 .

Unit labour costs 2) 0.7 0.0 . 1.6 1.6 0.7 . - - - - - -

Labour productivity 2) 1.7 1.5 . 0.1 0.5 1.0 . - - - - - -

Compensation per employee 2) 2.4 1.5 . 1.7 2.0 1.7 . - - - - - -

Total hourly labour costs 3) 2.5 1.7 . 2.0 2.0 2.4 . - - - - - -

Oil prices (EUR per barrel) 4) 17.1 12.0 17.1 10.3 15.0 19.7 23.0 21.8 20.8 23.5 24.8 24.9 27.6

Commodity prices 5) 12.9 -12.5 -3.1 -16.0 -8.2 1.1 14.0 6.6 10.7 11.9 19.3 19.4 20.0

Table 1Price and cost developments in the euro area(annual percentage changes, unless otherwise indicated)

Sources: Eurostat, national data, International Petroleum Exchange, HWWA – Institut für Wirtschaftsforschung (Hamburg) and ECBcalculations.1) Excluding construction.2) Whole economy.3) Whole economy (excluding agriculture, public administration, education, health and other services).4) Brent Blend (for one-month forward delivery). In ECU up to December 1998.5) Excluding energy. In euro; in ECU up to December 1998.

ECB Annua l Repor t • 199924

subdued in 1999. By December 1999, overallHICP inflation stood at 1.7% year-on-year,compared with 0.8% in December 1998.Inflation increased further to 2.0% year-on-yearin January 2000, mainly reflecting the persistenceof the increase in oil prices.

Over the course of 1999 oil prices increasedfrom €10.3 per barrel in the first quarter toan average of €23.0 per barrel in the fourthquarter, reflecting a gradual but significantrecovery in the world market price of oil andalso a depreciation in the euro’s exchangerate vis-à-vis the US dollar. This rise, whichreversed a steady decline observed in 1998,was swiftly reflected in the energy componentof the HICP; by December 1999 energyprices, which include a large excise component,had increased by 10% year-on-year, withmost of the increase concentrated inliquid fuel prices. Other energy componentsexhibited a more stable pattern of increaseor were, as in the case of electricity pricesin some euro area countries, subjectto downward pressure associated with

deregulation. In addition, increasing oil priceswere to some extent offset by downwardpressure from other prices. In particular,unprocessed food prices made a significantnegative contribution to the rate of increasein consumer prices.

Underlying price increases were moresubdued

Apart from the relatively volatile componentsdescribed above, consumer price increases werefar more subdued in 1999, with the rate ofincrease in the HICP excluding energy pricesand seasonal food declining to 1.0%, comparedwith an average of 1.4% in 1998. This reflectedsignificant declines in the rate of increase in theprice of non-energy industrial goods, servicesand processed food. In the case of the non-energy industrial goods component of the HICP,the pass-through from rising producer priceswas relatively limited in 1999. Developments inproducer prices, in turn, mainly reflectedincreases in oil and non-oil commodity prices,

Chart 8Breakdown of HICP inflation in the euro area by components(annual percentage changes; monthly data)

Source: Eurostat.

1996 1997 1998 1999-6

-4

-2

0

2

4

6

8

10

12

-6

-4

-2

0

2

4

6

8

10

12

total HICPservices

unprocessed foodprocessed food

non-energy industrial goodsenergy

25ECB Annua l Repor t • 1999

Box 3The effects of market deregulation on consumer prices

In a number of sectors of the euro area economy there have been ongoing efforts to liberalise markets in order

to ensure that firms are operating on a commercial basis and in a competitive environment. This process,

which increases the overall efficiency with which resources are used, is viewed as making a positive

contribution to overall economic welfare. In many cases, the liberalisation process can give rise to downward

pressure on prices and profit margins. Market liberalisation continued in 1999 and, while it is difficult to

separate clearly the price effects of liberalisation from the impact of other factors such as technological

change, it was associated with a further decline in the prices of a number of goods and, in particular, services.

The telecommunications market provides the most striking example of the extent of the impact of increased

competition on consumer prices. While liberalisation of EU telecommunications markets began in some

countries in the 1980s, it accelerated over the course of the 1990s, in parallel with rapid technological

innovation. In principle, most telecommunications markets in the EU have been completely opened up to